Take-Two Interactive: The Grand Theft Empire

I. Introduction & Episode Roadmap

Picture the scene on the morning of June 25, 2026. Across PlayStation and Xbox storefronts, a single button is about to go live, and somewhere in Rockstar's Edinburgh and New York studios, server engineers are bracing the way a coastal town braces for a hurricane that the forecasters insist is coming. The button says "Pre-order." The product is Grand Theft Auto VI, locked for release on Thursday, November 19, 2026, after a delay from its original 2025 window.1 When the second trailer dropped, it pulled in hundreds of millions of views in a single day — not for a film, not for a music video, but for a video game that wouldn't be playable for months. Wall Street has already done the arithmetic. Analysts are projecting the single largest commercial entertainment launch in human history, a debut that could outsell any movie opening weekend, any album drop, any console launch that came before it.

Here's the part that makes this a business story and not just a gaming story. The company that owns Grand Theft Auto — Take-Two Interactive Software, ticker TTWO on the NASDAQ — was, two decades ago, a corporate punchline. It was a publisher that lost money, restated its financials, got raided by the SEC, was hauled in front of the FTC, became the favorite target of American politicians looking for someone to blame for youth violence, and watched its own founder become the first chief executive in U.S. history convicted of a felony for backdating stock options.4 This was not a blue-chip media asset. This was a distressed, scandal-soaked, governance-disaster of a company that most institutional investors wouldn't touch without gloves.

And yet, by mid-2026, Take-Two has become a roughly $25 billion enterprise generating $6.72 billion in annual Net Bookings, sitting on the most valuable single piece of intellectual property in interactive entertainment, and operating as one of only a handful of companies on Earth capable of financing a single video game that reportedly costs north of a billion dollars to make.2 How did the ugly duckling become the swan? That is the question this episode answers.

Three big themes run underneath everything we'll cover today.

The first is creative autonomy versus operational discipline — the central management paradox of the modern entertainment business. Rockstar Games is run by genuine artists who treat deadlines as suggestions and perfectionism as a religion. 2K is a content factory that has to ship NBA 2K every single autumn like clockwork. Holding both inside one corporate shell, without strangling the creativity or losing financial control, is the core organizational achievement of Take-Two. We'll spend real time on how they built the walls that let geniuses be eccentric while the holding company stays solvent.

The second theme is what we'll call the externalized C-suite. Take-Two does not actually employ its chief executive in the conventional sense. Strauss Zelnick, the chairman and CEO, runs the company through his private firm, ZelnickMedia, under a management contract — an arrangement that is unusual, occasionally controversial, and extraordinarily lucrative. We'll dissect exactly how the money flows and why it's structured the way it is.

The third theme is the mobile pivot. In 2022, Take-Two paid $12.7 billion for Zynga, the most consequential capital-allocation decision in its history.3 We'll benchmark that deal against every comparable transaction in the sector and ask the question every investor should ask: did they overpay, or did they buy the future at a fair price?

So here's the roadmap. We'll start with the 2007 boardroom coup that created the modern company. We'll watch Zelnick fend off a hostile takeover from Electronic Arts in 2008 using nothing but conviction and a release date. We'll go deep on the economics of Grand Theft Auto and NBA 2K — the two engines that pay for everything. We'll benchmark the Zynga megadeal against the Gearbox bargain. We'll map the compensation machine. We'll run the whole thing through Porter and Hamilton Helmer's strategy frameworks. And we'll close with the bull case, the bear case, and the three numbers that actually matter. Let's get into it.

II. The Catalyst: The 2007 Boardroom Coup

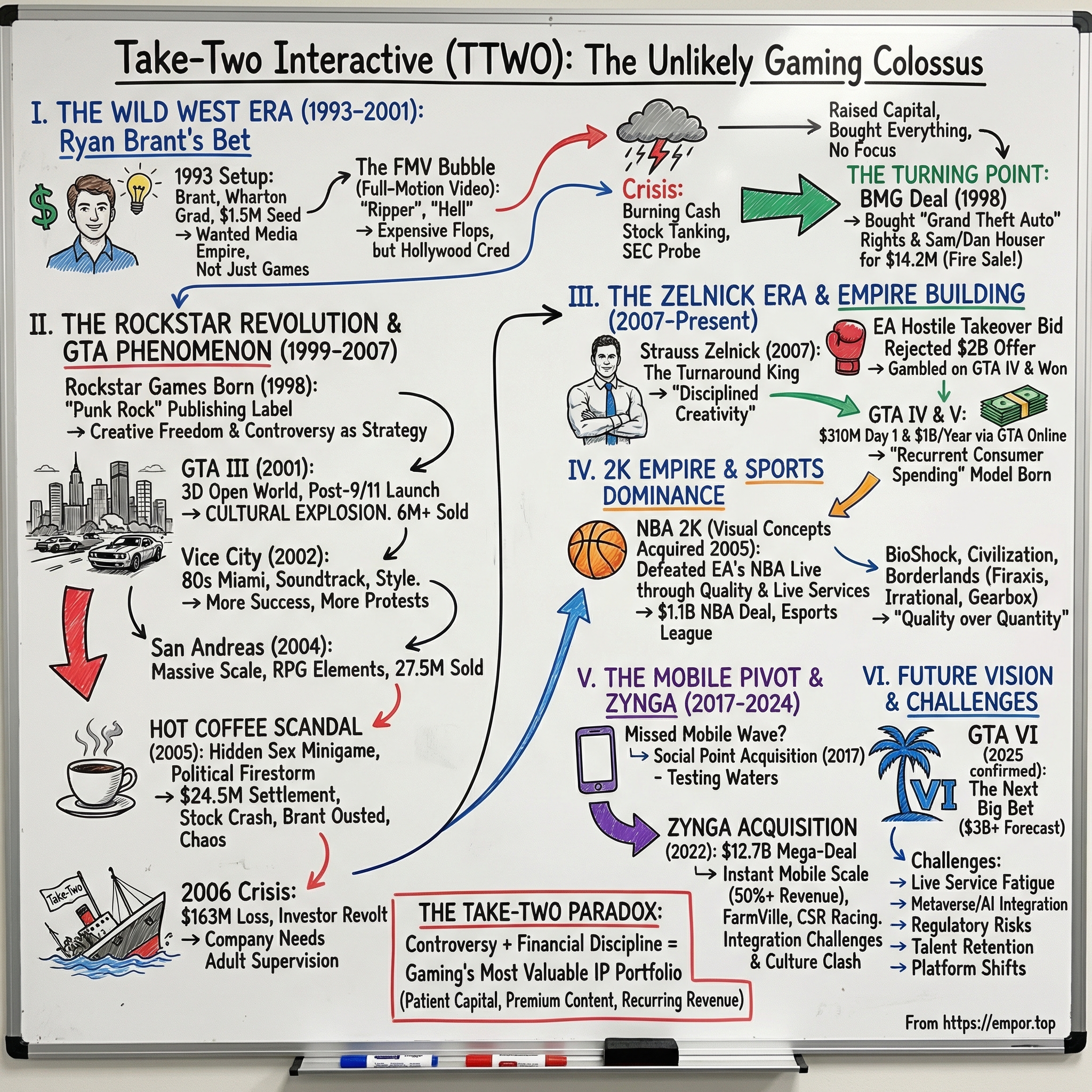

To understand how good things got, you have to sit for a moment in how bad they were. By 2006, Take-Two Interactive was, in the polite language of the financial press, "troubled," and in the impolite language of its own shareholders, a dumpster fire. The company had been founded in 1993 by Ryan Brant, a young, ambitious entrepreneur with a knack for acquiring studios and a much weaker knack for the unglamorous discipline of corporate governance. Under Brant, Take-Two assembled a genuinely brilliant creative portfolio — it had acquired the studio that would become Rockstar, and it had the Grand Theft Auto franchise, which by the mid-2000s was a cultural phenomenon. But it papered over the brilliance with an accounting scandal that would have made Enron's auditors wince.

In February 2007, Ryan Brant pleaded guilty to falsifying business records, admitting that he had backdated stock option grants — repeatedly timing the paper grant dates to moments when Take-Two's stock had bottomed out, manufacturing instant paper gains for himself and other executives. He agreed to pay back more than $7 million and became, in the unflattering historical footnote that follows him to this day, the first chief executive in America to be criminally convicted in the options-backdating wave that swept corporate America in the 2000s.4 The founder of the company was a felon. That was the starting position.

The accounting fraud was only one of the fires. The other was cultural and political. In 2005, modders discovered that Grand Theft Auto: San Andreas contained hidden, sexually explicit minigame content that could be unlocked with a third-party patch — the infamous "Hot Coffee" content. The fallout was brutal: the game was re-rated, retailers pulled it from shelves, the company faced an FTC investigation and class-action lawsuits, and Take-Two became Exhibit A in every congressional hearing about video games and morality. The recalls and legal costs were real money, and they landed on a company that was already bleeding. Take-Two posted a net loss in the neighborhood of $185 million in fiscal 2006.5 A scandal-ridden balance sheet, a criminally-convicted founder, a politically toxic flagship product, and an operating business that was hemorrhaging cash — this was a company begging to be taken over or torn apart.

Enter the activists. This is where the story turns, and it turns on a clever piece of corporate-law engineering. A coalition of large institutional shareholders — led by OppenheimerFunds, which held roughly a quarter of the stock, alongside D.E. Shaw, Tudor Investment Corporation, and Steven Cohen's SAC Capital — had collectively accumulated something like 46% of Take-Two's shares.5 They were furious, they were organized, and they wanted the board gone. The problem with throwing out a board is that it usually requires a full, expensive, drawn-out proxy fight. The activists found a shortcut. Under Delaware corporate law, a group of ten or fewer shareholders of record can act by written consent and call for change without running the full proxy gauntlet. Holding nearly half the company between a tiny handful of sophisticated funds, they qualified.

And they had a frontman: Strauss Zelnick. Zelnick was not a games guy in the Silicon Valley sense — he was a media operator with a résumé that read like a tour of the entertainment industry's executive suites. A Harvard-trained lawyer and Harvard MBA, he had run 20th Century Fox's home entertainment business, served as president of Columbia Pictures, and most relevantly had been CEO of BMG Entertainment, where he'd managed exactly the kind of temperamental creative talent that a record label and a game studio have in common. After leaving the corporate world, he co-founded a private equity and advisory firm, ZelnickMedia, built specifically to take operating control of media and entertainment companies. Take-Two was precisely the kind of broken-but-valuable asset he was hunting for.

The execution was swift and, for the people on the receiving end, merciless. At the annual shareholder meeting on March 29, 2007, the dissident coalition's slate won. Shareholders voted to replace five of the six sitting board members in a single stroke.[^6] Zelnick was installed as executive chairman, and his firm, ZelnickMedia, was handed a management contract to run the company. The symbolism of the moment was captured by what happened to the incumbent CEO, Paul Eibeler: the new regime didn't wait for a graceful transition. Eibeler was reportedly let go over the phone, immediately, the formalities of a multi-decade career compressed into a single call.5

The pitch Zelnick made to shareholders was deceptively simple and would become the company's operating philosophy for the next two decades: be creative-first and disciplined-second. Don't strangle the studios — they are the entire reason the asset is worth anything. But wrap them in real financial controls, real governance, and a holding company that knows how to manage cash, defend itself, and allocate capital. The old, scandal-stained history of Take-Two effectively ends here. Everything that matters about the modern company begins with that March 2007 vote. And the new regime barely had time to unpack its boxes before the entire strategy was put to the ultimate test — because within a year, one of the largest companies in the industry decided to simply buy the whole thing out from under them.

III. Fending Off the Giant: The 2008 EA Hostile Takeover Defense

In February 2008, Strauss Zelnick had been running Take-Two for less than a year when Electronic Arts walked up to the table, put down a stack of cash, and tried to take the company off the board entirely. On February 24, EA went public with an unsolicited, all-cash proposal to acquire Take-Two for $26.00 per share — valuing the company at roughly $2 billion and representing a premium of about 64% over where the stock had been trading before the approach.[^7] This was not a polite merger conversation. EA had taken its offer over the heads of the board and straight to the shareholders, the classic structure of a hostile tender. It was a bear hug, and it was designed to be very hard to refuse.

The strategic logic on EA's side was sound, and it's worth understanding because it explains the timing. The video game industry was consolidating. Activision and Vivendi Games were in the middle of merging to form Activision Blizzard, a giant that would tower over the publishing landscape. EA, the reigning heavyweight, wanted a counterweight, and the most valuable independent asset on the board was Take-Two's Grand Theft Auto. Buy Take-Two, and EA would own the one franchise that could go toe-to-toe with anything Activision Blizzard could field. The premium was generous, the cash was certain, and EA had every reason to believe a recently-rescued, scandal-scarred company would jump at a clean exit at a fat price.

Here's where Zelnick's read of the situation diverged from the market's, and where this becomes a master class in negotiating leverage. The board's response was that the offer was "opportunistic" and "inadequate" — and they meant something specific by it.7 The timing was the tell. EA had made its move in February. Grand Theft Auto IV — the first new mainline GTA in years, the most anticipated game on the planet — was scheduled to launch on April 29, 2008. EA was, in essence, trying to buy the company in the narrow window before the market could see what GTA IV was actually worth. Zelnick understood that the entire value of the negotiation hinged on that release. So he did something that takes nerve when there's $2 billion in certain cash on the table: he refused to engage in substantive talks until after the game shipped.

It was a high-stakes game of chicken, and the stakes were Zelnick's credibility and the shareholders' money. If GTA IV underwhelmed, he'd look like a fool who turned down a 64% premium out of vanity. If it delivered, he'd have proof that the market — and EA — were dramatically underpricing the asset.

GTA IV delivered. The game launched and generated approximately $500 million in worldwide revenue in its first week alone, moving something like six million copies, with the first day pulling in over $300 million.6 To put that in the language of the time: it wasn't just the biggest game launch ever — it was, by the company's own framing and by most contemporary accounts, the largest launch in the history of any entertainment medium, outpacing the opening of any film or album. The number Zelnick had been betting on wasn't a projection anymore. It was a receipt.

What happened next was the slow, undignified retreat of a frustrated acquirer. EA formally commenced its tender offer in March, then extended the deadline, then extended it again. At one point EA actually reduced its price slightly, to $25.74 per share, to account for stock that Take-Two had granted to executives in the interim — a small, telling move that signaled EA was nickel-and-diming rather than negotiating from strength.7 Shareholders, watching GTA IV print money, declined to tender in any meaningful numbers; only a small single-digit percentage of shares were ever offered up to EA. By September 2008, with the financial crisis beginning to swallow the entire economy and Take-Two's intrinsic value now obvious to everyone, EA walked away. No deal. The company stayed independent.

The lesson cemented Zelnick's reputation and shaped the company's identity. The market — and a far larger, more sophisticated rival — had fundamentally underestimated the long-tail cash flows buried inside Take-Two's intellectual property. A blockbuster game wasn't a one-time event; it was an annuity. EA saw a $2 billion company. Zelnick saw a franchise that would generate multiples of that over the following decade. He was right, and the proof would arrive five years later in the form of a game that didn't just beat GTA IV's records but rendered them quaint. To understand why, we need to open up the engine room.

IV. The Core Engine: Rockstar, 2K, and the Economics of AAA Gaming

There's a building in downtown Manhattan where, for years, some of the most valuable creative work in the entertainment industry happened behind doors that almost no outsider ever walked through. Rockstar Games is famously, almost pathologically private. It does not do the trade-show circuit the way its rivals do. It does not flood the calendar with releases. It disappears for years at a time and then resurfaces with something that reorders the entire industry. This is not an accident of personality; it is a business model. And it is the single most important thing to understand about Take-Two.

Let's meet the two pillars.

The first pillar is Rockstar Games, led by Sam Houser — the soft-spoken, obsessive British co-founder whose brother and longtime creative partner Dan Houser left the company in 2020, ending one of the great creative partnerships in gaming. Think of Rockstar as the prestige-cinema wing of the business: enormous budgets, multi-year timelines, total creative control, and a brand that means "event." When Rockstar ships a game, it is not competing with other games that week — it is competing with whatever else humanity might do with its leisure time. The economics here are difficult to overstate. Grand Theft Auto V, released in 2013, has sold more than 215 million copies across its various platform re-releases, making it one of the best-selling entertainment products ever created in any medium, and it has generated something on the order of $8 billion in lifetime bookings.8 One game. Thirteen years. Still, in fiscal 2026, one of the company's single largest revenue contributors.2

How does a 2013 game stay near the top of the charts in 2026? The answer is Grand Theft Auto Online, and it's the most important strategic innovation in the company's history. Rockstar took the single-player blockbuster and bolted on a persistent online world where players spend real money on virtual currency, vehicles, properties, and cosmetics. That turned a one-time $60 purchase into a decade-long subscription-like cash machine that requires no sequel to keep printing money. The cinematic blockbuster gets you in the door; the online world keeps your wallet open for ten years.

The second pillar is 2K Games, and specifically the studio Visual Concepts and its flagship, NBA 2K. If Rockstar is prestige cinema, 2K is network television — reliable, annualized, and metronomic. Every autumn, a new NBA 2K ships. It is one of the most dependable revenue generators in the entire industry, and in fiscal 2026 the latest editions, NBA 2K26 and NBA 2K25, were the company's single largest contributors to Net Bookings.2 Where Rockstar's genius is unpredictable and lumpy, 2K's genius is consistency. The basketball sim has its own recurring-revenue engine — virtual currency that players spend to build and upgrade their teams and avatars — that turns each annual release into a year-round monetization platform. Together, the lumpy giant and the steady metronome give Take-Two something rare: blockbuster upside with a baseline of predictable cash flow underneath it.

Now, let's place this in the competitive landscape, because scale is everything in this industry. In fiscal 2026, Take-Two generated $6.72 billion in Net Bookings.2 Its closest traditional Western peer, Electronic Arts, did roughly $8.0 billion — bigger, broader, anchored by sports franchises like EA Sports FC and Madden.9 Ubisoft, the French publisher behind Assassin's Creed, has fallen to roughly $2.3 billion and has spent years struggling with an over-saturated release slate and creative misfires — a useful reminder that scale and pedigree don't guarantee survival in this business. Microsoft, having swallowed Activision Blizzard in a $68.7 billion deal that closed in late 2023, now commands a gaming-bookings footprint well north of $8 billion and sits on Call of Duty, World of Warcraft, and Candy Crush simultaneously.

And then there are the truly enormous international players that dwarf everyone on a corporate-revenue basis. 腾讯 Tencent, through its games division, runs a global games operation comfortably above $25 billion, owning stakes in seemingly half the industry. ソニーグループ Sony's PlayStation games-and-network business is similarly in the $25 billion-plus range. 网易 NetEase clears $11 billion in games; 任天堂 Nintendo, on the strength of its first-party franchises and the Switch ecosystem, is likewise an $11 billion-class games business. Below them sit the specialists — ネクソン Nexon at roughly $3 billion, built on Asian live-service titles, and 크래프톤 Krafton, the PUBG maker, at around $1.5 billion. The point of this tour is not the precise figures; it's the shape of the market. Take-Two is a focused, premium-IP boutique sitting in a field of conglomerates many times its size.

So how does a comparatively small company win against giants? Not by out-producing them. Take-Two's entire playbook is extreme concentration — a deliberate refusal to spread itself thin. Instead of shipping dozens of mediocre titles a year, it pours its resources into a tiny number of "forever franchises" and then milks them through what the company calls Recurrent Consumer Spending: the virtual currency, downloadable content, in-game purchases, and online memberships that keep flowing in long after the initial sale. In fiscal 2026, recurrent consumer spending accounted for roughly 78% of total Net Bookings — the steady, annuity-like river of cash that turns hit games into durable financial assets.2 That is the magic trick. A blockbuster is an event; recurrent spending is a business. The question, by the early 2020s, was whether that business could survive a structural shift in where the world plays games. The answer required the biggest check the company had ever written.

V. The Zynga Merger & Benchmarking Capital Allocation

For most of its life, Take-Two had a blind spot the size of a smartphone. The company that owned the most valuable franchises in console gaming was almost entirely absent from the platform where, by the late 2010s, the majority of the world's gamers and a huge share of the industry's profits actually lived: mobile. Before 2022, mobile was only about 12% of Take-Two's Net Bookings. The company that dominated the living room had barely shown up in your pocket. In an industry where mobile had become the single largest segment, that was not a gap — it was an existential risk hiding in plain sight.

Strauss Zelnick's answer, announced in January 2022 and closed that May, was to buy the gap closed in a single transaction. Take-Two acquired Zynga — the FarmVille-and-Words-With-Friends company that had reinvented itself into a serious mobile publishing platform — for an enterprise value of $12.7 billion.3 The structure was a mix of cash and stock, valuing Zynga at $9.86 per share, a 64% premium to where Zynga had been trading before the deal leaked, and it instantly made Take-Two one of the largest mobile game publishers on the planet.313 It was, by a wide margin, the biggest bet the company had ever placed.

The natural question — the one every value-conscious investor asked at the time — is: did they overpay? You can't answer that in a vacuum. You have to benchmark it against how the market priced comparable mobile assets, and here the comparison gets genuinely interesting.

Take-Two paid for Zynga at roughly 16 times forward EBITDA and close to 5 times trailing revenue. Now hold that next to the two most relevant comparables. When Activision Blizzard bought King — the Candy Crush maker — back in 2016 for about $5 billion, it paid roughly 6.4 times forward EBITDA and 2.4 times revenue, at a premium of around 20%. When EA bought Glu Mobile in 2021 for about $2.1 billion, it paid roughly 15 times EBITDA and 3.1 times revenue. So on an earnings-multiple basis, Take-Two paid materially more than Activision did for King and roughly in line with what EA paid for Glu — but on a revenue multiple, it paid the steepest price of the three.

What explains the gap? Two things. First, timing. Activision bought King at a trough — King was a single-franchise company that the market feared had peaked with Candy Crush, so it traded cheap. Zynga, by contrast, was a diversified, growing, scaled platform, and Take-Two was paying a premium that reflected genuine scarcity value. There are only so many mobile publishers of real scale on the open market, and a company that needs to fix a strategic hole now doesn't get to wait for a trough. The premium was the price of urgency plus scarcity. Second, this wasn't just a purchase of games — it was a purchase of capability.

Because the deeper logic of the Zynga deal was never really about Toon Blast or Match Factory! or Empires & Puzzles, valuable as those franchises are. It was about two things Take-Two couldn't build itself fast enough. The first was Zynga's mobile publishing machine — the user-acquisition expertise, the live-operations muscle, the monetization know-how that turns a free download into a paying habit. The second was Chartboost, Zynga's proprietary mobile advertising and monetization platform — an ad-tech engine that lets the combined company acquire users and monetize them without handing as much margin to third parties. The thesis was that Take-Two could pour its dormant, world-famous console IP — Rockstar's and 2K's franchises — into Zynga's mobile distribution engine and reach a billion phones it had never touched. Management targeted roughly $100 million in annual cost synergies and more than $500 million in incremental net-bookings opportunities over time.3

Did the bet pay off? The numbers in mid-2026 are striking. Mobile, which was 12% of the business before the deal, now represents 49% of Take-Two's Net Bookings — roughly $3.3 billion of the $6.72 billion total.2 The company that couldn't find its way onto a smartphone in 2021 now derives nearly half its revenue from one. Whatever you think of the multiple paid, the strategic objective — transforming a console-centric publisher into a mobile-first one — was achieved with unusual speed and decisiveness.

Now, for contrast — and to prove that Zelnick's firm isn't simply in love with writing big checks — look at the other end of the capital-allocation spectrum. In March 2024, Take-Two agreed to acquire Gearbox Software, the studio behind the Borderlands franchise, for $460 million in stock.11 What makes this deal a thing of beauty for a disciplined buyer is the price history. Embracer Group, the acquisitive Swedish conglomerate, had bought Gearbox in 2021 in a deal valued at up to $1.3 billion. Three years later, with Embracer in financial distress and forced to dismantle its empire after a $2 billion Saudi-backed funding deal collapsed, Take-Two scooped up the same studio for roughly a third of that headline price.11 Same asset, a fraction of the cost, bought from a motivated seller at exactly the wrong moment for them and the right moment for Take-Two.

Put the two deals side by side and you see the real ZelnickMedia capital-allocation philosophy. When a strategic asset is scarce and the window is closing — mobile scale, in 2022 — pay the premium and move fast, because the cost of not having it is existential. When an asset comes available because a distressed seller needs cash — Gearbox, in 2024 — pay nothing close to the premium and let someone else's panic become your bargain. Same firm, opposite tactics, one consistent logic: pay up only when scarcity demands it. Which brings us to the firm itself, and to the most unusual feature of this entire company — the fact that the people making these billion-dollar decisions don't technically work here.

VI. Modern Management: The ZelnickMedia Playbook & Incentive Structure

Here's a corporate-governance riddle. The chief executive officer and chairman of a $25 billion publicly-traded company walks into the office every day, makes the biggest decisions, signs off on billion-dollar acquisitions, and represents the company to Wall Street. And yet he is not, in the conventional sense, an employee of that company. There's no employment contract, no W-2 in the usual way. He works for a different firm entirely — his own — which has signed a contract to run the public company on behalf of its shareholders. If that sounds strange, it should. Almost no large public company is structured this way. Take-Two is.

The modern leadership is a tight, two-man partnership at the top. Strauss Zelnick, whom we've already met, serves as chairman and CEO. His longtime partner Karl Slatoff serves as president and runs much of the day-to-day operating machinery. Slatoff has been at Zelnick's side for the entire post-2007 era, a steady operational counterweight to Zelnick's deal-making and external-facing role. But neither man is paid by Take-Two as a salaried executive. Instead, Take-Two has a management agreement with ZelnickMedia Corporation — the private firm — and ZMC, in turn, provides the executive talent.

Let's follow the money, because it's the most distinctive feature of the whole arrangement. Under the management agreement signed in 2022 and running through March 31, 2029, Take-Two pays ZelnickMedia a monthly management fee of $275,000 — about $3.3 million a year — plus an annual cash bonus opportunity with a target of roughly $6.6 million and a maximum that runs to roughly $13.2 million.12 That pool of cash is then split internally between the partners, with Zelnick and Slatoff dividing it on roughly a 60/40 basis. So the headline cash compensation flows to a firm, not a person, and the firm allocates it among its principals. It is, in effect, an outsourced C-suite — the management equivalent of hiring a private-equity operating team to run your company permanently rather than employing executives directly.

The cash, though, is the small part of the story. The real compensation — and the part that has periodically drawn fire from institutional shareholders and proxy advisors — is paid in equity, in restricted stock units, and the structure of that equity is where this gets genuinely interesting from an investor's perspective. Historically, large RSU grants to an external management firm are exactly the kind of thing that makes governance watchdogs nervous, because they can dilute common shareholders and reward executives regardless of performance. So the 2022 agreement was deliberately engineered to tie the bulk of the equity to outcomes shareholders actually care about.

Two performance metrics govern the equity awards, and the weighting tells you everything about what management is being paid to prioritize. Seventy-five percent of the performance equity is tied to relative total shareholder return — specifically, whether Take-Two's stock outperforms the NASDAQ-100 Index over a multi-year measurement period.12 This is the cleanest possible alignment: the managers get paid the big money only if the stock beats a broad benchmark, not merely if it rises with the market tide. The remaining twenty-five percent is tied to Recurrent Consumer Spending — the live-services, virtual-currency, microtransaction revenue stream we discussed earlier.12 That second metric is a quiet but powerful signal. By putting a quarter of the top team's incentive equity on recurrent spending, the board is explicitly paying management to keep building and milking the GTA Online and NBA 2K monetization engines — the battle passes, the virtual currencies, the in-game stores. When you wonder why Take-Two leans so hard into recurrent monetization, the answer is partly that its leaders are paid, in writing, to do exactly that.

There's a real "skin in the game" dimension here too, which blunts some of the criticism. The ZMC partners are restricted from selling their shares until March 31, 2029, except to cover taxes — a multi-year lock-up that ties their wealth to the company's medium-term trajectory rather than letting them cash out on a single good quarter. Zelnick personally holds roughly 1.4 million shares, a stake worth well over $240 million at recent prices, and Slatoff holds roughly 1.37 million. Ownership guidelines require the CEO to hold stock worth at least six times his base compensation. Whatever you make of the externalized structure, the people running Take-Two have an enormous fraction of their personal net worth riding on the same stock that retail and institutional shareholders own.

So how should an investor think about this? On one hand, the structure is unusual and the optics of paying a private firm to run a public company will never sit perfectly with every governance purist; dilution from the equity awards is a real, recurring drag on per-share economics. On the other hand, the performance alignment is, by the standards of public-company pay, genuinely tight — beat the index and grow recurrent spending, or the big money doesn't vest. It's a trade-off, not a free lunch, and reasonable people weigh it differently. To judge whether the moat that all this is designed to protect is actually durable, we need to step back from the org chart and run the business through the two frameworks every serious investor should keep in their toolkit.

VII. Strategic Frameworks: Porter's 5 Forces & Hamilton's 7 Powers

Strip away the personalities and the deal history, and you're left with a more fundamental question: what, exactly, protects this business from being competed away? Anyone can make a video game. Talented people make brilliant ones every year and go broke doing it. So why does Take-Two get to earn extraordinary, durable returns on a tiny handful of franchises while better-funded giants like Ubisoft stumble? Let's run it through Hamilton Helmer's 7 Powers and Michael Porter's Five Forces and find the actual sources of advantage.

Start with what Helmer would call a Cornerstone Resource — a uniquely valuable asset that a company controls and competitors cannot replicate. For Take-Two, the cornerstone is Rockstar itself: the specific accumulation of talent, institutional knowledge, and brand equity that lets one studio spend the better part of a decade and well over a billion dollars on a single title and be all but guaranteed a multiple of that back. This is not a resource you can hire your way into. You cannot post a job listing for "the team that made GTA V." It is a cultural institution that took twenty-five years to compound, and its scarcity is the whole point. There are perhaps a half-dozen development teams on Earth that can execute open-world games at that tier, and Take-Two owns the most valuable one outright. When the market doubts whether GTA VI can possibly justify its budget, the historical answer is that this particular cornerstone resource has never failed to deliver a 10x outcome — a track record no competitor can claim.

Next, Network Effects, the power Helmer considers among the most durable of all. Take-Two's live-service worlds — GTA Online and NBA 2K — are not just games; they're social graphs. People play where their friends play. A teenager doesn't pick NBA 2K over a rival basketball game on the merits of the dribbling physics; he picks it because his entire friend group is already there, with their teams and their progress and their shared sessions. Every additional player makes the world more valuable to every existing player, and that social gravity creates switching costs that have nothing to do with the quality of any individual feature. It's the same dynamic that protects a messaging app or a social network, quietly operating inside a basketball simulator. This is why a 2013 game's online mode can still be a top revenue contributor in 2026 — the network, not the graphics, is the moat.

Third, Scale Economies, which in modern AAA gaming have become almost absurd. The cost of producing a frontier open-world title — reportedly upwards of $1.5 billion for GTA VI once you fold in marketing — has risen to a level that only a tiny oligopoly of publishers can finance at all. This cuts two ways as a power. It's a barrier that keeps new entrants out, and it's an advantage that accrues to the few who can spread that fixed cost across hundreds of millions of units and a decade of recurrent spending. A studio that sells five million copies and a studio that sells two hundred million copies face the same billion-dollar development bill; only one of them turns it into a fortune. Scale doesn't just help here — it's the difference between a viable business and a bankruptcy.

Now flip to Porter, and the picture sharpens further.

Threat of new entrants: very low. This is about as fortified as an industry gets. To threaten Take-Two at the top tier, a new entrant would need world-class technical talent, a billion-plus dollars of patient capital willing to wait five years for a return, and — the part you can't buy — brand equity and a fanbase that takes decades to build. The combination is effectively insurmountable. New studios are born constantly; new top-tier open-world console studios essentially are not.

Supplier power: moderate to high, but managed. The "suppliers" here are the platform owners — Sony and Microsoft — who control the storefronts and historically take a roughly 30% cut of digital sales. That's a meaningful tax, and on paper it gives the platforms real power. But Take-Two holds an unusual amount of counter-leverage, because its biggest games are system-sellers. People buy a PlayStation in order to play Grand Theft Auto; the hardware needs the software as much as the software needs the hardware. A console without GTA is a harder console to sell. That mutual dependence keeps the relationship balanced and gives Take-Two more negotiating room than a small publisher would ever have.

Buyer power: moderate. Individual gamers are price-sensitive, vocal, and quick to revolt — gaming communities can organize a backlash against a publisher overnight, and Take-Two has felt that heat over monetization more than once. But for genuine "must-play" cultural events like a new Grand Theft Auto, demand is strikingly inelastic. Players who grumble about a $70 or $80 price tag buy the game anyway, because not playing it means being left out of a cultural moment their entire social circle is participating in. The buyer has power over a mediocre title and almost none over a phenomenon.

Add it up, and you get a business with multiple reinforcing moats: an irreplaceable cornerstone resource, genuine network effects, brutal scale economies, near-total protection from new entrants, and inelastic demand for its flagship product. That's a formidable structure. But a strong moat and a good investment are not the same thing — price, concentration, and execution risk all sit on top of the structure. So let's weigh both sides honestly.

VIII. The Bull vs. Bear Case & Key KPIs

Every investment thesis eventually has to leave the realm of frameworks and confront the numbers that will actually prove or disprove it. For Take-Two in mid-2026, the entire debate hangs on a single, looming event and a handful of metrics that will tell you, quarter by quarter, whether the story is working. Let's start with what to watch, then argue both sides.

The three KPIs that matter most. You don't need to track forty metrics to follow this company; you need three.

The first is Net Bookings guidance versus realization — specifically, whether Take-Two actually delivers the leap it has promised. The company posted $6.72 billion in Net Bookings in fiscal 2026 and has guided to $8.0–$8.2 billion for fiscal 2027, an implied jump of roughly 20% driven almost entirely by the GTA VI launch.2 The single most important thing an investor can do is watch whether reported bookings track that guided ramp. A miss would signal that either the launch slipped or the monetization disappointed; a beat would confirm the thesis in the most direct way possible.

The second is Recurrent Consumer Spending growth. Because roughly 78% of bookings now come from recurrent spending, the durability of the whole business depends on those live-service rivers continuing to flow.2 The number to watch is whether recurrent spending keeps growing or starts to flatten — flattening would be the early warning sign of player fatigue, the quiet killer of live-service economics.

The third is Zynga's mobile margins, or more precisely, user-acquisition cost. Mobile is now half the company, but mobile profitability lives and dies on what you pay to acquire each player versus what you earn from them. If user-acquisition costs climb faster than monetization, the mobile segment can grow its top line while quietly eroding its contribution to profit. Watch the segment margins, not just the segment revenue.

The bull case is, in a word, GTA VI. The November 19, 2026 launch is positioned to shatter every entertainment sales record in existence, and the bull thesis is that it does three things at once. It drives an enormous launch-quarter spike in console-software sales. It catalyzes a multi-year hardware and engagement cycle as players upgrade consoles to play it. And — most importantly for the long-term holder — it seeds GTA Online 2.0, a next-generation persistent world that could, if it matches or exceeds the original's trajectory, generate a decade-plus tail of recurrent cash flow. Remember that the first GTA Online was still a top revenue contributor thirteen years after the base game launched. If the sequel's online mode does the same, the cash flows extend well into the 2030s. The second leg of the bull case is mobile integration: that Zynga's monetization engine successfully ports Rockstar's and 2K's dormant IP onto phones, turning franchises that currently monetize tens of millions of console players into ones that reach hundreds of millions of mobile players. Stack the GTA VI supercycle on top of a working mobile flywheel, and you have a company whose earnings power steps up to a structurally higher level.

The bear case is the mirror image, and it's serious. The first and largest risk is single-asset concentration. Strip away the diversification talk and Take-Two's valuation rests, to an uncomfortable degree, on one studio and increasingly on one game. Any stumble with GTA VI — a botched technical launch, server meltdowns on day one, a multiplayer monetization model that the community rejects, or simply an online mode that fails to replicate GTA V's extraordinary run — would be financially disastrous relative to expectations, because so much is priced in. The company has been here before in spirit: its near-death experiences have always traced back to over-dependence on the Rockstar franchise. The structure that makes the bull case so explosive — concentration on forever-franchises — is exactly what makes the bear case so sharp. Concentration cuts both ways.

The second bear risk is margin dilution. The ZelnickMedia equity compensation, the ongoing RSU grants, and the stock issued to fund acquisitions like Zynga and Gearbox all chip away at per-share economics. A company can grow bookings impressively while growing share count alongside it, leaving common shareholders with less of each incremental dollar than the headline numbers suggest. Watch the diluted share count as carefully as the bookings line.

There's also a useful piece of second-layer context worth flagging: the competitive set is consolidating around Take-Two in real time. Microsoft now owns Activision Blizzard. And Electronic Arts — the same EA that tried to buy Take-Two in 2008 — agreed in 2026 to be taken private in a roughly $55 billion deal led by a consortium including Saudi Arabia's Public Investment Fund.10 EA posted record net bookings of roughly $8 billion in fiscal 2026 even as it prepared to leave the public markets.9 What that means for Take-Two is a landscape in which its two largest Western competitors are now owned by entities with effectively bottomless balance sheets — a sovereign wealth fund and the most valuable company in the world. Take-Two, by contrast, remains an independent public company that lives or dies on the quality of its own slate. That independence is part of the appeal and part of the risk: there's no deep-pocketed parent to absorb a bad year.

Weighing it honestly: this is a company with a genuine, multi-layered moat, an extraordinary near-term catalyst, a proven management team with deep skin in the game — and a valuation that leans heavily on a single November release going right. The bull and bear cases aren't really in conflict; they're two readings of the same concentrated bet. Which brings us, finally, to the lessons.

IX. Epilogue & Business Lessons

Step all the way back from the deal tables and the KPIs, and Take-Two's two-decade arc resolves into three lessons that travel well beyond gaming.

The first is IP curation as a moat — or, as Zelnick himself has often put it, the idea that quality is the ultimate business plan. The most counterintuitive thing about Rockstar's economics is that the discipline of delay is itself a source of value. GTA VI was originally targeted for a fall 2025 window and was pushed to November 19, 2026, explicitly to allow more polish.1 In most businesses, slipping a product launch by a year is a confession of failure. In this one, it's a deliberate act of value creation, because the difference between a very good GTA and a generational one is measured in billions of dollars and a decade of recurrent cash flow. Take-Two has internalized that a forever-franchise is too valuable to rush. The willingness to leave near-term revenue on the table in service of long-term franchise health is the single hardest discipline in entertainment, and it's the one Take-Two has institutionalized.

The second lesson is about corporate restructuring — the proof that aligning the right institutional capital with the right operating expertise can rescue an asset everyone else has written off as toxic. In 2007, Take-Two was a felon-founded, SEC-investigated, politically-radioactive mess. The activists who took it over didn't fix it by gutting the creative talent that made it valuable; they fixed it by wrapping that talent in governance, discipline, and a management structure built to defend and allocate capital intelligently. The cornerstone resource was always there. What was missing was the operating system around it. Sometimes the most valuable thing a turnaround can do is leave the crown jewels alone and rebuild everything else.

The third lesson is about bold capital allocation — the discipline of knowing when to swing hard. The Zynga acquisition was a $12.7 billion bet placed at a premium multiple, made not because the core business was failing but because the company saw a structural shift it could not afford to miss. Paired with the bargain-bin discipline of the Gearbox deal, it reveals a management philosophy that is neither reflexively cheap nor reflexively aggressive, but situational: pay up when scarcity and timing demand it, and pay nothing close when a distressed seller hands you the chance. The willingness to make a transformative, balance-sheet-bending bet when the strategic logic is clear — and the patience to wait for bargains the rest of the time — is the kind of capital-allocation temperament that compounds value over decades.

On November 19, 2026, the entire two-decade thesis will be put to its largest single test. A once-bankrupt, scandal-scarred publisher that politicians loved to hate and a far larger rival once tried to swallow whole now stands on the edge of what is projected to be the biggest entertainment launch ever recorded. Whether GTA VI vindicates the concentration bet or exposes its fragility, the story of how Take-Two got here — from a felony conviction to the verge of redefining the economics of media — is already one of the most remarkable corporate transformations in the modern entertainment business.

References

-

Grand Theft Auto VI is Now Set to Launch November 19, 2026 — Rockstar Games Newswire, 2026 ↩↩

-

Take-Two Interactive Software Inc — Form 8-K, Q4 and FY2026 Earnings Release, SEC EDGAR, 2026-05-21 ↩↩↩↩↩↩↩↩

-

Take-Two and Zynga to Combine — Business Wire / Take-Two Interactive, 2022-01-10 ↩↩↩↩

-

Ex-CEO of Take Two Pleads Guilty in Options Backdating Case — CNBC, 2007-02-14 ↩↩

-

Shareholders Force Board Change at Take-Two — GamesIndustry.biz, 2007-03-30 ↩↩↩

-

GTA IV Sets Sales Records with 6 Million Unit / $500 Million First Week — Engadget, 2008-05-07 ↩

-

Take-Two Interactive Software Inc — Schedule 14D-9, Board Recommendation Against EA Offer, SEC EDGAR, 2008 ↩↩

-

Take-Two Reveals Its Latest Figures, Including 215 Million GTA V Units Sold — IG News / Instant Gaming, 2026 ↩

-

Electronic Arts Reports Record Net Bookings and Revenue for FY2026 — EA Investor Relations, 2026-05-20 ↩↩

-

Electronic Arts to Be Taken Private by Investor Consortium for $55 Billion — Game Developer, 2026-05-05 ↩

-

Take-Two Interactive to Acquire 'Borderlands' Developer Gearbox From Embracer Group for $460 Million — Variety, 2024-03-28 ↩↩

-

Take-Two Interactive Software Inc — Form 8-K, 2022 Management Agreement with ZelnickMedia, SEC EDGAR, 2022 ↩↩↩

-

Take-Two Completes Zynga Acquisition — GamesIndustry.biz, 2022-05-23 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube