Trane Technologies: The Cold Chain and the Megawatt Thermal Loop

I. Introduction: The $115B Climate Pure-Play Hiding in Plain Sight

Start with a number that should not make sense. In the summer of 2026, a company whose corporate DNA traces back to casting iron radiators in a Wisconsin river town commands a stock-market value of roughly $108 to $110 billion — bigger than Ford, bigger than most household-name banks, bigger than the entire domestic airline industry combined.6 It sells air conditioners and refrigerated truck units. And it trades at around 30 times forward earnings, a multiple the market usually reserves for software companies, not for machines that get lowered into building basements by crane.5

That is the puzzle worth two hours of your attention. Trane Technologies plc, ticker TT on the New York Stock Exchange, is one of the most valuable industrial companies on Earth, yet almost nobody outside the heating, ventilation and air-conditioning trade could tell you what it does. It is a pure-play climate technology company — meaning it makes the machines that move heat around, in buildings and in transport — and it is priced as if it has cracked something its multi-industrial peers have not. Standard diversified industrials like Emerson or Honeywell trade in the high-teens to low-twenties on forward earnings. Trane sits a full multiple-tier above them.5

The core paradox is this: how does a business rooted in nineteenth-century mechanical engineering earn a twenty-first-century growth premium? The short answer, which the rest of this story will test rather than assume, has three parts. The first is a double transition the physical economy is living through right now — the decarbonization of buildings, which pushes the world from gas furnaces toward electric heat pumps, and the AI-driven explosion of data center construction, which is generating heat loads that traditional cooling simply cannot handle. Trane sells into both. The second is structure: a decade of corporate surgery that stripped a sprawling conglomerate down to a single, high-return business. The third is moat — a distribution model and a service annuity that competitors have spent years trying to copy.

We will walk the arc chronologically. It begins with two separate origin stories, a plumber's son in La Crosse, Wisconsin, and a golf-course bet in Minneapolis. It runs through the leveraged-buyout era and a $10.1 billion acquisition timed almost perfectly to detonate at the bottom of a financial crisis. It turns on a piece of financial engineering executed in 2020 — a Reverse Morris Trust spin-off — that unlocked the premium the stock enjoys today. And it ends in the engine room and on the battlefield: the segment economics, the seven sources of competitive power, the AI cooling surge, the CEO who spent forty years inside the company, and the bull-versus-bear stress test that any sober investor has to run before paying 30 times earnings for anything.

It is worth puncturing one myth up front, because it distorts how many people approach the stock. The myth is that Trane's premium is a bet on air conditioners — that this is, at heart, an HVAC company that has gotten expensive. The reality is more specific and more interesting: the market is not paying up for the metal boxes at all. It is paying up for the service annuity attached to a vast installed base, for a distribution model that specifies competitors out of buildings before they can bid, and, most recently, for a claim on the thermal side of the AI build-out. Get that distinction wrong — treat Trane as "an AC company at 30 times earnings" rather than as an installed-base services franchise with an equipment business attached — and you will misjudge both the bull case and the risks. The equipment is the hook. The economics live downstream of it.

A word on posture before we start. This is not a Trane investor-relations document. The company tells a very good story about itself, and much of it is true. But "management says it will win" is a claim, not evidence, and the interesting work is separating the two. Let's begin where the machines were born.

II. The Dual Roots: Reuben Trane and the Cold Chain

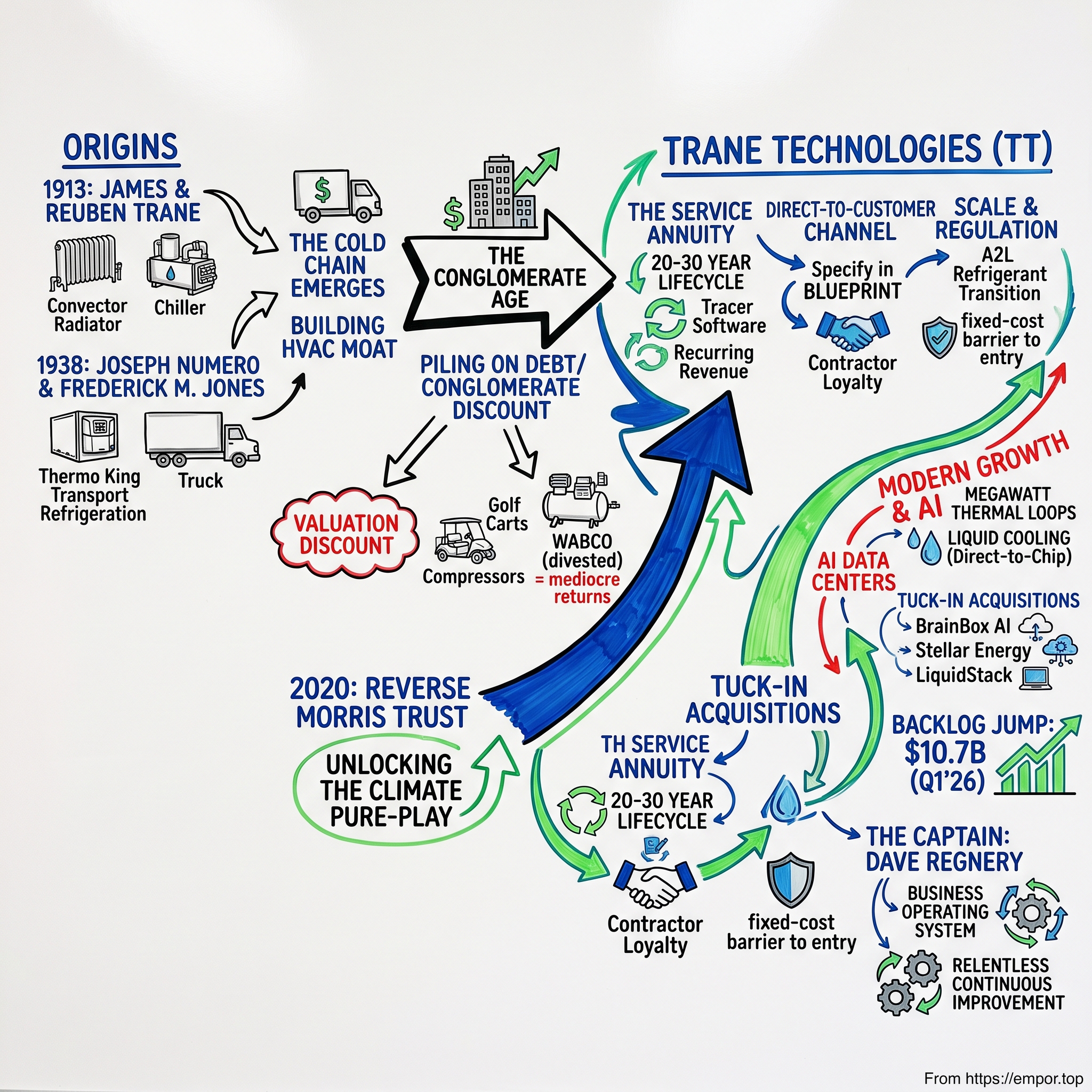

Picture La Crosse, Wisconsin, in the first decade of the twentieth century — a Mississippi River town of lumber mills and brutal winters, where the difference between a warm building and a cold one was a matter of survival, not comfort. Into this world came James Trane, a Norwegian immigrant who worked as a plumber and heating man, and who had an inventor's irritation with the tools of his trade. Cast-iron radiators were heavy, ugly, slow to warm, and murder to install. James tinkered. But it was his son, Reuben Trane, a mechanical engineer, who turned tinkering into an industry. In 1913, father and son incorporated The Trane Company, and a family plumbing shop became a manufacturer.

Reuben's breakthrough arrived in 1925 with the convector radiator — a heat exchanger built from copper and steel fins rather than heavy cast iron.7 The physics were elegant: more surface area, less mass, faster and more even heat transfer, at a fraction of the weight. If you have ever felt warm air rise off a modern baseboard heater, you have felt Reuben Trane's idea. It made Trane a serious company. But the invention that changed the shape of cities came in 1938, when Trane introduced the Turbovac, the first hermetic centrifugal water chiller.7 Here is why that mattered, translated out of engineer-speak: a centrifugal chiller uses a spinning impeller — think of a jet engine's compressor — to move enormous quantities of heat out of a large building efficiently. "Hermetic" meant the motor and compressor were sealed together, reducing leaks and maintenance.

Before reliable large-scale chilling, the skyscraper was a fair-weather machine. You could build tall, but the upper floors baked in summer and the sealed glass towers of modern architecture were physically unlivable. Trane's chillers — and those of a handful of competitors racing alongside — are part of the hidden infrastructure that made the air-conditioned high-rise, the modern hospital, and the industrial clean room possible. Out of this reliability grew the tagline that still hangs over the brand: "It's Hard to Stop a Trane." A pun, yes, but also a genuine marketing asset — three generations of contractors learned to associate the name with equipment that simply kept running. And in a business where the buyer is often not the end user but a contractor staking his own reputation on the equipment he installs, that reputation for reliability is worth real money. A contractor who has never had a Trane callback will specify Trane again; the brand is, in effect, a promise made from one tradesman to another. That dynamic — the professional buyer, not the consumer, as the true customer — is a thread that runs through the whole company and helps explain the moat we'll dissect later.

Through the mid-twentieth century, Trane grew into a pillar of the American mechanical-engineering establishment, its chillers and air handlers embedded in the postwar building boom, its name a fixture in the mechanical rooms of hospitals, universities, and office towers. But being an excellent, focused engineering company was, by the standards of the era, almost a liability. The prevailing wisdom held that scale and diversification meant safety, that a good business was better inside a big one. It was a wisdom that would cost Trane its independence — and eventually, decades later, prove exactly backwards.

Now shift two hundred miles north, to Minneapolis, and to a completely different founding myth. The story, told and retold, is that in 1938 an entrepreneur named Joseph Numero and a self-taught inventor named Frederick McKinley Jones were standing near a golf course when the conversation turned to a problem: a truckload of chickens had spoiled in transit because ice-cooling didn't work once a truck started moving. Numero, half in jest, bet that Jones could build something better. Jones — one of the most prolific African-American inventors in American history, a man with more than sixty patents and no formal engineering degree — went and did it. He designed the first practical, self-contained, shock-resistant refrigeration unit that could be bolted to a moving truck. He patented the Model C transport refrigeration unit in 1940.8

It is difficult to overstate what Jones actually invented. He did not just build a better cooler; he created the cold chain — the unbroken run of refrigeration that lets a strawberry picked in California arrive fresh in Chicago, that lets insulin and, decades later, vaccines cross continents without spoiling. Supermarkets as we know them, global produce trade, modern pharmaceutical distribution: all of it rides on the descendants of Jones's Model C. And the wartime timing gave the invention an immediate, deadly-serious application: during the Second World War, portable refrigeration units built on Jones's designs kept blood, medicine, and food fresh for field hospitals and troops in theaters where none of it could otherwise survive the heat. A technology born to stop chickens from spoiling on a Minnesota highway ended up preserving battlefield plasma. Jones did all of this, it bears repeating, as a Black self-taught engineer in a rigidly segregated America — a man who could patent a revolution in food logistics but could not, in much of the country he was feeding, eat at the same lunch counter as the executives selling his machines.

The company he and Numero built became Thermo King, and it is worth pausing on the strategic shape of that business, because it is a very different animal from the building-HVAC franchise it now sits beside. Transport refrigeration is a replacement-and-fleet business: trucking companies, food distributors, and increasingly pharmaceutical logistics operators run large fleets of refrigerated trailers, and those units wear out on a predictable cycle, get serviced through a dealer network, and get replaced. It is more cyclical than building HVAC — when freight volumes slump, fleet owners defer purchases — but it carries the same essential DNA: sell a durable machine, then earn on parts and service across its life. Two inventions, two cities, two problems — heating a building and cooling a truck — that would eventually converge under one corporate roof. But the path they took to get there did not run through any grand thermal strategy. It ran, as most twentieth-century industrial history did, straight through the age of the conglomerate and the leveraged buyout.

III. The Conglomerate Era: Leveraged Buyouts and the $10B Peak-Market Bet

For most of the twentieth century, the logic of American business ran in one direction: get bigger, get more diversified, bolt unrelated cash flows together and call it stability. Trane and Thermo King spent four decades being passed between owners who believed exactly that — and it is a decade-by-decade lesson in why the strategy so often destroyed the value it promised to create.

The first buyer was American Standard, the plumbing-fixtures giant, which acquired Trane in 1984 for roughly half a billion dollars in cash — contemporaneous reporting put the tender near $34 a share.9 American Standard's ambition was to build a diversified building-products empire spanning bathrooms, air conditioning, and vehicle brakes. It is a perfectly reasonable-sounding logic — these are all things that go into buildings and machines — and it is the exact logic that would later be judged a value-destroying mistake. The businesses shared a customer set in the loosest sense and almost no real operating synergy. A toilet and a centrifugal chiller are not, it turns out, meaningfully cheaper to make or sell under one roof.

That empire, in turn, made American Standard itself a target — because a collection of decent businesses trading at a conglomerate discount is precisely what a corporate raider hunts for. In 1988, the takeover specialist Black & Decker launched a hostile bid, and American Standard's management fought it off the only way the 1980s knew how: by taking the company private in a leveraged buyout, piling on debt to buy out shareholders and slam the door on the raider. It worked, in the narrow sense that management kept control. But debt became the company's permanent weather. For years afterward, cash that might have gone into R&D or new capacity went instead to servicing borrowings incurred to survive a takeover fight. This is the hidden tax of the LBO era on operating businesses: the financial maneuver that saves the company's independence often starves the very operations it was meant to protect. Trane spent much of the 1990s as a strong business inside a financially constrained parent.

By 2007, a different kind of pressure — activist investors demanding that conglomerates justify their own existence — forced American Standard to do the math on its own parts. The conclusion was that the whole was worth less than the pieces. So the company dismembered itself into three: it spun off its vehicle-controls business as WABCO, sold its Bath & Kitchen division to the private-equity firm Bain Capital, and renamed the surviving, pure-play air-conditioning business Trane Inc.10 For the first time in decades, Trane stood alone as a focused HVAC company — briefly.

Because the very next year, the consolidation machine came around again. Ingersoll Rand — a heavy-industrial group whose roots ran back to 1871, and which had already bought Thermo King in 1997 — announced it would acquire Trane Inc. for approximately $10.1 billion in cash and stock.11 The deal, struck in late 2007 and completed in June 2008, reunited the building-cooling business and the truck-cooling business under one owner. It was also a masterclass in catastrophic timing. The ink was barely dry when the Global Financial Crisis arrived. Commercial construction froze. Residential housing, the other leg of HVAC demand, collapsed outright. Ingersoll Rand had paid a peak-cycle price for a cyclical asset and then watched the cycle fall off a cliff.

To understand how bad the timing was, hold the two halves of the cycle side by side. Commercial HVAC demand is tied to non-residential construction — offices, hospitals, hotels, factories — which is one of the most interest-rate-sensitive and confidence-sensitive things in the entire economy. When credit froze in 2008 and 2009, construction projects were cancelled or mothballed by the thousand, and the equipment orders that would have flowed from them simply evaporated. Residential HVAC, meanwhile, is tied to housing starts and home sales, and American housing did not merely slow — it experienced its worst collapse since the Depression. Ingersoll Rand had bought a business whose two demand engines were both wired directly into the parts of the economy that broke first and hardest. A peak-cycle price met a trough-cycle reality within months.

What followed was more than a decade of what investors call the conglomerate discount, and it is the crucial setup for everything that comes next. Inside Ingersoll Rand, the Trane and Thermo King businesses were genuinely excellent — high-margin, growing, and generating strong returns on the capital they consumed. But they were bolted to an Industrial segment: air compressors, assembly tools, material-handling equipment, fluid-management products, and, improbably, Club Car golf carts. That segment was capital-hungry, deeply cyclical, and structurally lower-return — the kind of business that eats reinvestment and hands back a mediocre return on it. The market, unable or unwilling to value the good business separately from the mediocre one, applied a blended, mediocre multiple to the whole.

The mechanism of the discount is worth making concrete, because it is the entire pivot of this story. Imagine you are an investor who loves the economics of commercial chillers — the recurring service, the switching costs, the pricing power — and would happily pay a rich multiple for a pure version of it. You cannot buy that inside Ingersoll Rand, because your dollar also buys a slice of golf carts and industrial compressors that you would pay a much lower multiple for. So you either pass, or you pay a weighted-average price that under-rewards the crown jewel and over-rewards the laggard. Multiply that across the whole investor base and you get a stock that structurally cannot earn what its best business deserves. Two great climate franchises spent years trapped inside a valuation that reflected their least attractive sibling. The obvious question — why are these things in the same company? — hung over Ingersoll Rand for a decade before anyone finally answered it. The answer, when it arrived, was not a better product. It was a better structure.

IV. The Masterstroke: The 2020 Reverse Morris Trust

The answer, when it came, was a piece of financial engineering elegant enough to belong in a textbook — and, in fact, it now does. The architect was Michael Lamach, Ingersoll Rand's long-serving chief executive, who had concluded that the only way to let the climate business earn the multiple it deserved was to physically separate it from the industrial business. The elegant part was how he did it, because a naïve spin-off would have triggered an enormous tax bill.

The instrument was a Reverse Morris Trust, or RMT — a structure that lets a company divest a division tax-free by spinning it off and immediately merging it with an outside partner, provided the original shareholders end up owning more than half of the combined entity. Ingersoll Rand took its Industrial segment, spun it out, and merged it with Gardner Denver, a publicly traded maker of flow-control and compression equipment. Legacy Ingersoll Rand shareholders received 50.1% of the newly combined industrial company — just over the line that kept the whole thing tax-free.1213 In a final twist of corporate identity, the combined industrial company kept the storied Ingersoll Rand name and its ticker, IR. The industrial brand went with the compressors; the climate business had to become something new.

That new thing was Trane Technologies plc, which began trading on the NYSE under TT on March 2, 2020, days after the legal separation completed at the end of February.12 It was incorporated in Ireland — headquartered in Swords, in County Dublin, a domicile chosen years earlier for tax efficiency — while its operational heart stayed in Davidson, North Carolina. And then, with almost comic timing, the world locked down. Trane Technologies was born as a public company into the opening days of a global pandemic, which is worth remembering when assessing what came next: this was not a spin-off that sailed out onto calm seas.

Yet the market's verdict was swift and, over the following years, emphatic. As a captive division inside Ingersoll Rand, the climate assets had been valued at something like 12 to 15 times EV/EBITDA — a respectable but unremarkable industrial multiple. Freed to trade on their own merits, they re-rated. The multiple pushed past 20 times, and eventually well beyond, as investors did the arithmetic the conglomerate structure had obscured: this was a business with structurally higher margins, structurally higher returns on invested capital, and a services annuity that most industrials could only envy.5

The return-on-invested-capital point deserves a beat, because it is the deepest reason the two businesses belonged apart. Return on invested capital measures how much profit a company squeezes from every dollar tied up in factories, inventory, and working capital — it is the truest single gauge of business quality. The old Industrial segment was capital-heavy: compressors and material-handling equipment demand large plants and lots of tooling, and they earn a modest return on all of it. Climate is comparatively capital-light for an industrial, because so much of its profit comes from the service annuity, which requires technicians and software rather than blast furnaces. Bolt a high-ROIC business to a low-ROIC one and the blended number lands in the mediocre middle — which is exactly the number the market had been valuing. Separate them, and capital that used to be trapped funding low-return compressor plants could be redirected entirely to high-return climate reinvestment. The spin-off didn't just change the story investors told; it changed where the company's next dollar of capital could go.

There is a subtlety in the RMT structure worth dwelling on, because it explains why so many industrial conglomerates use it. A plain spin-off of an appreciated business can trigger corporate-level tax, and an outright sale would trigger it too — the government treats it as if you sold the asset at a gain. The Reverse Morris Trust threads the needle: by spinning the division to your own shareholders and then merging it with a partner in a deal where those shareholders retain more than 50% control, the transaction qualifies as a tax-free reorganization rather than a taxable sale. The 50.1% figure was not a rounding artifact; it was the load-bearing number that kept the entire structure out of the taxman's hands. Get it wrong by a fraction and the tax shield collapses. This is the kind of detail that separates financial engineering from financial accident, and Lamach's team executed it precisely.

Consider, too, what the transaction said about management's read of its own portfolio. Ingersoll Rand did not sell the climate business and keep the industrial one; it did the reverse in spirit — it kept the industrial legacy name on the divested piece and reinvented the retained climate business as something new. The tell is in where the continuing leadership went. Lamach and the core team stayed with the climate company, Trane Technologies. That is management voting with its feet about which business had the better future, and it is a signal an investor should weight more heavily than any slide deck.

Here is the analytical point, and it is the first of several worth extracting cleanly. The spin-off did not make the underlying machines better. The chillers were the same chillers on March 2 as on February 28. What changed was capital allocation and disclosure. Freed from the industrial segment, management could pour every dollar of reinvestment into HVAC and transport refrigeration, where returns were highest, and investors could finally see the economics without a lower-return business muddying the picture. The re-rating was not the market being fooled by a cosmetic change; it was the market correctly repricing a business whose true quality had been genuinely obscured. The value was always there; the structure had been hiding it. That is the entire case for focus in a single episode — and it sets up the question the next section has to answer. Is the business underneath actually as good as the re-rated multiple now implies?

V. Inside the Engine Room: Segment Economics & The Direct-to-Customer Moat

To answer that, you have to open the hood — and the first thing you notice is how lopsided the machine is. Trane reports in three geographic segments, and one of them does almost all the work.

The Americas segment generated $17.17 billion of net revenue in 2025, roughly 80.5% of the company's $21.32 billion total, and it drives the overwhelming majority of consolidated operating profit.21 This is the beating heart: North American commercial HVAC — the big applied chillers and building systems sold into offices, hospitals, schools, and data centers — plus residential heating and cooling and the Thermo King transport business. EMEA, at $2.80 billion (about 13.1% of revenue), is a distant second, centered on the European push toward building electrification, commercial heat pumps, and regional cold chain.2 Asia Pacific, at $1.35 billion (about 6.3%), is the smallest and the most volatile, historically dragged around by the fortunes of Chinese commercial real estate.2 The concentration is the point: Trane is, to a first approximation, a North American company with two international options attached — but the options are not equal. EMEA carries a genuine secular story: Europe's push to electrify heating, replacing gas boilers with electric heat pumps, is a policy-driven tailwind for exactly the equipment Trane makes, and it is why the company positions its European business around commercial heat pumps and building electrification rather than legacy systems. A heat pump, for the uninitiated, is simply an air conditioner that can run in reverse — moving heat into a building in winter as easily as it removes it in summer — and it is several times more energy-efficient than burning gas, which is what makes it central to any building-decarbonization plan. Asia Pacific, by contrast, is less an option than a persistent drag, its fortunes chained to Chinese commercial construction, which has been mired in a property downturn that shows no clean sign of resolving. The honest framing is that Trane's international segments are a growth call on Europe and a show-me story in Asia, and neither moves the consolidated needle the way the Americas engine does.

It is worth understanding why the Americas mix is so profitable, because it is not just about size. Within the Americas, the most valuable slice is commercial "applied" HVAC — the large, custom-engineered systems for big buildings — as opposed to "unitary" equipment, the more standardized boxes that cool a small store or a home. Applied systems are designed, not just bought: they require engineering, integration, controls, and commissioning, and each one is effectively a bespoke project. That complexity is a feature, not a bug, from Trane's standpoint. It is precisely what a distributor-and-catalog competitor struggles to replicate, and it is what pulls the high-margin service work along behind it. The residential and light-commercial business, by contrast, is a tougher, more commoditized, more cyclical arena — and, as the bear case will show, it was the source of most of the pain in 2025.

So why does the applied-heavy Americas engine earn a premium multiple rather than a plumbing-supply multiple? The most useful lens is Hamilton Helmer's 7 Powers framework, which asks what specific, durable mechanism keeps competitors from simply competing away your profits. Trane exhibits at least three, and they compound.

The first is what looks like a cornered resource: the direct-to-customer sales channel. Most HVAC manufacturers sell through independent, third-party distributors who then sell to contractors — an arm's-length model where the manufacturer's brand is one option on a shelf. In North American commercial HVAC, Trane does something different and expensive: it employs thousands of its own sales engineers who work directly with building developers, architects, and consulting mechanical engineers at the blueprint stage. Think about what that means. When a hospital or a data center is still a drawing, a Trane engineer is in the room helping specify the equipment — which means the building's mechanical design gets written around Trane's systems before the project ever goes out to bid. By the time competitors get a look, the specification is already tilted. On the Q1 2026 earnings call, management returned repeatedly to this channel as the reason bookings could surge without a fight on price.4 It is not a moat that shows up on a balance sheet, but it is real, and it is decades in the building.

The second power is high switching costs, and this is where the economics get genuinely attractive. When a multi-million-dollar Trane centrifugal chiller is lowered by crane into the basement of a hospital, the building is then plumbed, ducted, wired, and controlled around that machine. Ripping it out to switch brands is not a purchase decision; it is a construction project — one that means shutting down critical building systems, re-engineering the mechanical room, and re-commissioning the whole plant. For a hospital or a data center, where downtime is measured in millions of dollars an hour, that is close to unthinkable outside of a scheduled end-of-life replacement. So the customer stays, not out of loyalty, but out of the sheer sunk cost of the surrounding infrastructure.

That physical lock-in feeds the part of the business investors care about most: the service annuity. Over a chiller's twenty-to-thirty-year life, the parts, the proprietary digital controls — Trane's Tracer building-automation and connected-building software — and the maintenance contracts generate several multiples of the original equipment sale. The mechanism is worth spelling out, because it is the crux of the investment case. The building owner needs the chiller to keep running; Trane holds the proprietary parts, the controls software, and the trained technicians who know the machine; and the cost of a failure to the owner dwarfs the cost of a service contract. That asymmetry is what lets the service business earn high margins year after year without a price war. Management frames the initial hardware as the entrance fee and the lifecycle as the real prize, and on the Q1 2026 call it reiterated that services run at roughly one-third of total enterprise revenue and grow at a high-single-digit clip through cycles.4 The strategic significance is that a third of the company behaves less like a machinery business and more like an installed-base subscription — recurring, sticky, and largely insulated from the construction cycle that whipsaws the equipment side.

A company that is one-third recurring, high-margin, counter-cyclical service revenue simply is not valued like a pure equipment maker. That is the single most important sentence in the valuation case, and it is worth being precise about what it does and does not prove. It explains why Trane deserves a premium to a commodity industrial. It does not, by itself, justify any particular premium — 30 times forward earnings is a market judgment about growth and durability layered on top of the service annuity, and that judgment is exactly what the bear case will contest.

The third power is scale economies, sharpened by regulation — a mechanism we'll see turned into a weapon in a later section. Here the layman's translation matters, because "refrigerant transition" sounds like a footnote and is actually a portfolio-wide re-engineering event. The fluids that carry heat inside every air conditioner and chiller — refrigerants — are potent greenhouse gases when they leak, some thousands of times more warming than carbon dioxide. Regulators on both sides of the Atlantic have mandated a phase-down: the U.S. under the AIM Act administered by the EPA, Europe under its F-Gas rules. The industry's answer is a new generation of low-global-warming-potential refrigerants such as R-454B, which are mildly flammable — classified "A2L" — and therefore require redesigned equipment, new safety systems, new certifications, and retrained installers across the entire product line.

That re-engineering costs hundreds of millions of dollars, and here is the competitive twist: it is a fixed cost. Whether you sell a million units or fifty thousand, you pay roughly the same to redesign the platform and clear the regulations. Trane can spread that cost across a $21 billion revenue base; a small regional competitor spreads it across a fraction of that and faces margin compression or an existential squeeze. The bigger you are, the cheaper compliance is per unit sold — which means a rule written to protect the climate quietly functions as a barrier to entry that protects the incumbent. We will see the same transition, in the next breath, cutting the other way as a near-term risk, because a change this sweeping is disruptive even for the company best positioned to absorb it.

The honest caveat: none of these powers is unique to Trane. Carrier and Johnson Controls run their own applied businesses and service annuities. What Trane has is not a category of one but a degree advantage — a more developed direct channel, a larger installed base, a longer head start on the service loop. That is a real edge, but it is a lead, not a fortress, and the competitors are now sharpening. Hold that thought; first, the reason the whole industry is suddenly on fire.

VI. Modern Playbook: The AI Data Center Cooling Surge & Advanced Electrification

For most of its life, Trane's demand curve was a function of two boring things: the weather and the construction cycle. Then artificial intelligence rewrote the physics of the building.

Here is the mechanism, in plain terms. Training and running large AI models requires racks of specialized chips — graphics processors, mostly — packed together at densities that would have been unthinkable a few years ago. Those chips turn electricity into computation and, as an unavoidable byproduct, into heat — enormous, concentrated heat. A traditional server rack might dissipate a few kilowatts, comfortably handled by blowing cold air across it, the way a household fan cools a room. An AI rack can exceed 30 to 50 kilowatts and climb toward 100 and beyond, at which point air-cooling hits a wall of physics: air simply cannot absorb and carry away heat fast enough, no matter how hard you blow it, to keep the silicon from throttling or frying.

The industry's answer is to switch cooling fluids. Water and specialized dielectric liquids can carry roughly a thousand times more heat per unit volume than air, so the frontier of data-center design is about bringing liquid ever closer to the chip. There is a ladder of techniques, and it helps to picture it: at the base, big chilled-water plants cool the air in the room; one rung up, "direct-to-chip" cooling runs liquid through cold plates bolted onto the processors themselves; at the top, "immersion" cooling submerges entire servers in tanks of non-conductive fluid that boils gently as it carries heat away. Each rung requires more specialized engineering — and each rung is a place Trane now intends to sell. The whole facility still needs industrial-scale chilling to reject all that captured heat to the outside world, and that base layer has been Trane's home turf for eighty years. What changed is that the turf got suddenly, violently rezoned as the hottest real estate in technology, and the customer set narrowed to a handful of hyperscalers spending tens of billions of dollars a year.

The financial fingerprint of this shift is startling. Trane's enterprise backlog — the dollar value of orders booked but not yet delivered, and the single best leading indicator of near-term demand — stood at a record $7.8 billion at the end of 2025.1 One quarter later, at the end of the first quarter of 2026, it had jumped to $10.7 billion, an increase of more than 30% in three months, a move almost unheard of for a company this size.3 The driver was explicit: Americas Applied Solutions bookings — the big, engineered, data-center-scale systems — rose more than 160% year over year, the third straight quarter of Applied bookings growth above 100%, producing a book-to-bill ratio around 150%.34 In plain English, Trane booked one and a half dollars of new orders for every dollar it shipped. That is a business being handed more demand than it can currently convert. The rest of the quarter's numbers pointed the same way: revenue of roughly $4.97 billion beat expectations, adjusted earnings came in at $2.63 a share, and management nudged up full-year 2026 guidance, raising organic revenue growth toward 7% and lifting the adjusted-EPS range.3 A guidance raise this early in the year, off a backlog that had just jumped 30%, is management signaling confidence — and confidence, in a company that has historically guided conservatively, is itself information.

There is a discipline worth applying to that confidence, though. A guidance raise is a promise, and the right way to hold a management team accountable is to compare what it says now against what it said before and will say later. Trane has, to its credit, a multi-year record of setting achievable targets and then clearing them — the narrative across its recent calls has been consistent, and the misses it has had, chiefly in residential, it has explained in specific operational terms rather than macro hand-waving. That track record is why the market extends it the benefit of the doubt. It is also exactly what an investor should watch for cracks in: the first time the story shifts, the targets quietly move, or a miss gets blamed on the weather, the premium's foundation starts to erode.

Rather than chase this with a single massive, dilutive acquisition, Trane's playbook has been a series of targeted, technology-forward tuck-ins — and the pattern reveals the strategy. In December 2025 it agreed to buy Stellar Energy, a maker of modular, factory-built data-center cooling plants; the deal closed in February 2026, added roughly $1 billion to backlog, and management guided to about $500 million of revenue from it in 2026 alone.15144 Weeks later, in early 2026, it acquired LiquidStack, a specialist in direct-to-chip and immersion liquid cooling — buying the exact technology the highest-density AI racks require.16 Those two deals, back to back, are a clear statement: Trane intends to own the cooling stack from the building plant all the way down to the chip. The ambition got an external validation in October 2025, when Trane unveiled a thermal-management reference design purpose-built for gigawatt-scale NVIDIA AI factories — a blueprint developed with the dominant maker of AI chips for how to cool the facilities those chips will live in.19 Being designed-in at the reference-architecture stage of the AI build-out is the data-center-era echo of the blueprint-stage specification advantage described earlier.

The digital and life-science tuck-ins fill out the picture, and they reveal a deliberate layering of the moat. In January 2025 Trane completed its acquisition of BrainBox AI, whose software autonomously optimizes a building's HVAC in real time, using machine learning to predict thermal loads and adjust the system minute by minute, with claimed energy reductions of up to 25%.17 In late 2023 it completed the purchase of Nuvolo, a cloud platform for managing building assets and workplaces, deepening the software layer that binds a customer's facilities data to Trane's ecosystem.18 And in May 2023 it bought Helmer Scientific for roughly $263 million, extending Thermo King's cold-chain expertise into precision refrigeration for clinical and life-science applications — vaccines, blood, laboratory samples — a niche with regulatory tailwinds and premium margins.[^19]

The through-line is a benchmarking exercise every investor should run on serial acquirers: are the deals cheap financial arbitrage or expensive strategic reinforcement? Trane's are clearly the latter. It has paid up — an estimated high-teens-to-low-twenties EBITDA multiple for the software-native firms, richer than the multiple its own hardware earns — and the justification is not that the targets are undervalued but that they are complementary. Each software layer makes the installed base a little harder to leave and the pricing a little easier to defend against Carrier and Johnson Controls. That is a coherent strategy, but it carries its own risk worth naming: paying premium multiples for small, unproven software assets is exactly the kind of "strategic" acquisition that can quietly destroy value if the integration disappoints or the technology is leapfrogged. Serial tuck-in acquirers earn trust deal by deal, and the honest verdict on BrainBox AI and Nuvolo is that it is still too early to know whether they compound or merely cost.

A note of skepticism is warranted here, because backlog is a promise, not a delivery. A book-to-bill of 150% is thrilling on the way up and punishing on the way down; the same leading indicator that surged in early 2026 will fall fastest if hyperscale capital-expenditure plans get trimmed. The bookings are real. Whether they convert to profit at the margins management implies, and whether the AI build-out proves to be a durable plateau or a spike, is the central open question — and it runs straight into the bear case. First, the person responsible for delivering on all of it.

VII. The Captain of the Ship: Dave Regnery and the Business Operating System

In 1985, a newly minted graduate named Dave Regnery took a job at Trane as a sales engineer — one of those field-level roles walking construction sites and sitting with mechanical contractors, learning the business from the blueprint up.20 He never left. Over the next thirty-five years he moved through division after division, absorbing the tribal knowledge of a company whose product cycles run in decades and whose customer relationships outlast most careers. He became president and chief operating officer as the spin-off took shape in early 2020, chief executive in July 2021, and chairman in January 2022.20

That biography is not incidental color; it is a governance fact with two edges. On the positive side, a CEO who spent nearly four decades inside the direct sales force carries enormous credibility with the engineers and contractors who actually specify the equipment — he speaks their language because it was once his job. In an industry built on multi-decade trust, that continuity is a genuine asset. The skeptical read is the mirror image: a lifer at the top is, almost by definition, unlikely to challenge the company's foundational assumptions, and deep insider tenure can shade into insularity. Both things are true. The evidence for which one dominates is in the operating results.

The operating discipline runs on what Trane calls its business operating system — a rigorous, continuous-improvement management framework that outside observers frequently compare to the legendary Danaher Business System, the lean playbook that turned Danaher into one of the great industrial compounders. (Trane's own materials describe the system in its own terms; the Danaher parallel is an analyst framing, not a company claim, and worth flagging as such.) Stripped of the jargon, what a system like this actually does is unglamorous and powerful: it makes continuous improvement a habit rather than a project. Small teams relentlessly attack waste in the factory and the office — shaving minutes off a process, dollars off a bill of materials, defects off a production line — and the gains compound quarter after quarter. The genius of the approach is not any single tool; it is the culture of never declaring the work finished, and the discipline of measuring everything so that improvement is provable rather than asserted.

Whatever the pedigree, the outputs are measurable, and measurable outputs are the only honest way to judge a management framework. Management has repeatedly targeted and delivered roughly 100-plus basis points of adjusted operating-margin expansion a year, alongside strong pricing that has offset inflation and tariffs.4 On the January 2026 call closing out the year, management framed that pricing-plus-productivity combination as the durable core of the model even as volumes wobbled.[^27] The analytical read: consistent margin expansion delivered through a cyclical downturn in residential is the strongest available evidence that the operating system is real and not a slide. Anyone can expand margins in a boom; doing it while a major end-market is shrinking is the tell that separates a genuine productivity engine from a rising tide. The company's ability to raise price without losing volume is the clearest evidence that the pricing power described earlier is real rather than rhetorical.

One number deserves a skeptic's asterisk. Trane markets its free-cash-flow discipline hard, targeting conversion of roughly 100% of adjusted net earnings into cash — an important claim, because cash conversion is where accounting profits either prove real or evaporate. In 2025 the actual figure came in at about 98%, just shy of the target.1 That is a fine result and a rounding error in the scheme of things, but it is worth noting precisely because management talks about 100% as a floor; the honest characterization is "aims for 100%, delivered 98%," not "consistently exceeds 100%." Holding a company to its own framing is the whole job.

Capital allocation is the other place where a management team's real priorities show, and Trane's pattern is telling. The company has leaned on a balanced framework: reinvest in the business first, fund the technology tuck-ins described earlier, pay and grow a dividend, and return the balance through buybacks. What it has conspicuously not done is chase a transformational, balance-sheet-straining acquisition — no answer to Carrier's €12 billion Viessmann deal, no bet-the-company move. For a company generating strong free cash flow at a cyclical high, that restraint is itself a decision, and a defensible one; the risk with serial acquirers is usually that they can't stop, and so far Trane has kept its deals small enough to absorb. The counter-argument a skeptic would raise is that buying back stock at 30 times earnings is a rich use of cash, and that the tuck-in strategy, however disciplined, is still an admission that the company must keep buying growth rather than generating all of it organically.

On incentives, the alignment looks strong on paper. Trane's proxy sets a stock-ownership guideline requiring the CEO to hold shares worth a multiple of base salary, and Regnery's actual holdings run far in excess of that floor — genuine skin in the game rather than the token stake some boards accept.21 Variable pay is tied to total shareholder return and capital efficiency, with a modifier linked to the company's 2030 sustainability commitments, including the "Gigaton Challenge," an ambition to help customers cut their carbon footprints by one billion metric tons of CO2-equivalent by 2030.22 A cynic will note that ESG-linked pay modifiers are easy to design generously, and that "help customers reduce emissions" is a softer, less falsifiable target than a hard financial metric. A fairer read is that for a company whose entire growth thesis is the electrification of buildings and the efficiency of cooling, tying a slice of compensation to customer emissions reductions is at least strategically coherent — the sustainability story and the sales story are, for once, genuinely the same story. Coherent, however, is not the same as insulated from competition — and the competition has spent the last two years getting dangerous.

VIII. The Skeptical Investor Stress Test: Bull vs. Bear

Every premium multiple is an argument, and every argument invites a rebuttal. So let's war-game the stock the way a thoughtful long-short investor would — starting with the battlefield, because Trane's competitive set has been reshaped almost beyond recognition in the last three years.

For most of its life, Trane's edge over its two closest American rivals was partly self-inflicted on their side: both were distracted by conglomerate sprawl. That excuse is gone. Carrier Global (CARR), the business Willis Carrier's air-conditioning empire became, executed its own radical simplification — divesting its fire & security and commercial-refrigeration divisions and paying roughly €12 billion for Viessmann Climate Solutions to plant a flag in European heat pumps.24[^26] Carrier is now, like Trane, a focused climate pure-play. Johnson Controls (JCI) went the other way down the same road, selling its residential and light-commercial HVAC business to Robert Bosch for about $8 billion, announced in July 2024, to concentrate on commercial building automation and controls.23 The strategic point is uncomfortable for Trane bulls: the two rivals who used to fight with one hand tied behind their backs have both untied the hand.

Apply Porter's five forces and the picture sharpens. Rivalry is intensifying precisely because the majors have sharpened. Buyer power is muted in commercial applied — the specification lock-in and switching costs blunt it — but real in residential, where a homeowner shopping a furnace replacement has genuine choice and price sensitivity, and where the contractor, not the brand, often drives the decision. Supplier power is modest but not trivial: the refrigerant transition has, at moments, made low-GWP refrigerant supply itself a bottleneck. Threat of new entrants into commercial applied is low — the channel and installed base are decades in the making — but the threat of substitutes and adjacent attackers is the live one, and it wears several faces.

The most formidable competitor isn't American at all: ダイキン工業 Daikin Industries (6367) of Japan is the global revenue leader in HVAC, with unmatched compressor technology and dominance in the variable-refrigerant-flow systems — modular, ductless setups that let each zone of a building run at its own temperature — that are the global standard across Asia and Europe and are gaining share in North America. Daikin is the one rival with the scale to match Trane's regulatory-cost advantage worldwide. In premium North American residential, Lennox International (LII) is a focused specialist running 20%-plus operating margins, proof that a disciplined single-market player can out-earn the giants on its home turf. And at the value end, China's 美的集团 Midea Group (000333) and 格力电器 Gree Electric (000651) are vast, low-cost manufacturers that dominate Asian and emerging markets and increasingly export components and finished units globally — the threat of lower-cost substitutes made corporate, and the reason Trane's Asia Pacific segment is its weakest.

Trane's answer to all of them is the same: it doesn't try to win on price, it wins on the engineered, serviced, specified commercial systems where its channel and installed base matter most. Run the 7 Powers scorecard honestly and the verdict is that Trane holds degree advantages, not kind advantages — its channel, switching costs, and scale are better developed than most rivals', but every one of those powers exists, in some measure, at Carrier, Johnson Controls, and Daikin too. That is a defensible position, and a genuinely good business, but it is not an unassailable one, and it concedes large swaths of the global market — the price-sensitive residential mass market, most of Asia — by design.

Now the bear case, stated as strongly as it deserves. The first charge is the valuation air pocket. At around 30 times forward earnings, Trane trades at a large premium to Carrier and JCI, both closer to the mid-twenties.5 A premium can be justified by superior growth and returns — but it also means the stock is priced for continued execution, with little margin for error. If AI data-center capital spending decelerates, or if elevated interest rates keep suppressing housing, the same multiple that expanded on the way up can compress violently. Much of the recent backlog surge is tied to a single, capital-intensive, cyclical end market controlled by a handful of hyperscale buyers; concentration cuts both ways.

The second charge is the residential drag and the refrigerant transition, and this is where the near-term risk is most concrete. Residential HVAC saw material volume declines in 2025, squeezed by high interest rates that froze home sales and remodeling, and compounded by the very refrigerant switch that functions as a moat over the long run. In the short run, that transition is friction: contractors must retrain on mildly flammable A2L gases, retool their trucks and shops, and navigate new supply chains and pricing, and there was a well-documented period of pre-buying older equipment ahead of the cutover followed by a demand air-pocket after it. Management told investors to expect a residential recovery in the second half of 2026. But "recovery in the second half" is one of the most-repeated and least-reliable phrases in cyclical investing, and a skeptic is right to withhold credit until the volumes actually turn. The credibility test here is specific and checkable: does residential inflect in the back half of 2026 as promised, or does the excuse migrate to 2027?

The third charge is the sharpened competitors above: the intensity of competition in commercial and data-center cooling is structurally rising, not falling, at exactly the moment Trane is valued as if its lead were permanent. And there is a fourth, subtler charge that ties the others together — concentration and cyclicality masquerading as secular growth. The backlog surge that so excites the market is disproportionately data-center demand, which is disproportionately a handful of hyperscale buyers, whose capital-spending plans can be revised faster than a chiller can be built. A record book-to-bill is the mathematical signature of a boom; it is also, mechanically, what you see at the top. None of this makes the bull case wrong. It makes it conditional — on AI capex holding, on residential turning, and on the moat widening faster than three focused rivals can close it.

An activist would push on one more thing: whether a 40-year insider chairman-and-CEO with a supportive board is the right governance structure to stay paranoid in a market this suddenly crowded. There is no scandal here, no related-party mess, no leverage problem — Trane's balance sheet and disclosure are clean, which is itself worth stating. The stress test is not about malfeasance; it is about whether excellence, richly priced, can persist against rivals who have finally focused. The bull says the moat and the service annuity win. The bear says you are paying a software multiple for a machinery company at a cyclical peak. Both are serious. What lessons does the whole arc leave behind?

IX. Playbook: Business & Investing Lessons

Strip the story to its transferable ideas and four stand out — each earned by the narrative rather than asserted over it.

Focus wins; conglomerates lose. The single most value-creating act in this entire history was not an invention or an acquisition but a subtraction — the 2020 Reverse Morris Trust that separated the industrial business from the climate business. Neither company's machines improved that day, yet both re-rated, because capital could finally flow to its highest-return use and investors could finally see clean economics. The lesson for anyone analyzing a diversified industrial is to ask what the sum-of-the-parts looks like and why the parts are still married. Sometimes the biggest lever is the org chart.

Distribution is the ultimate moat. In heavy industry, having the best machine is table stakes; controlling how it gets specified is the edge. Trane's army of sales engineers, embedded at the blueprint stage, writes the company into building designs before a competitor gets a bid. This is a reminder that moats often live in commercial architecture, not in the product spec sheet — and that they take decades and real payroll to build, which is exactly why they are hard to copy.

Turn regulatory headwinds into moats. The refrigerant phase-down is a cost imposed on the whole industry, and Trane's instinct was not to lobby against it but to absorb the R&D cost across its scale and let smaller rivals struggle with compliance. Regulation that raises the fixed cost of staying in business is, for the largest player, a competitive gift disguised as a burden. The general principle: watch which competitor a new rule actually hurts.

Promote from within for complex, long-cycle systems. Dave Regnery's four decades inside the company are a double-edged asset, but in a business where customer relationships and product cycles both run twenty-plus years, deep institutional knowledge is a genuine form of capital. The caution attached to the lesson is equally important: insider continuity buys credibility and coherence, but investors should keep asking whether it also buys complacency, especially now that the competitive set has been redrawn.

Underneath all four sits a fifth, unstated lesson that is really a warning about the reader's own psychology: a great business and a great investment are not the same thing, and the gap between them is price. Everything in this story argues that Trane is a genuinely excellent operation — focused, moated, well-run, riding real secular tailwinds. None of it settles whether the stock, at a software-like multiple, has already priced that excellence in full. The discipline the whole arc teaches is to separate the quality of the business (high, and well-evidenced) from the attractiveness of the entry point (a function of a multiple that assumes the good times continue). Confusing the two is how investors overpay for wonderful companies.

X. Epilogue & Outro

So, what should a long-term investor actually watch from here, once the narrative is set aside and only the instruments remain? Three gauges matter more than the rest.

The first is Applied Solutions bookings growth in the Americas — the most direct read on whether the AI data-center cooling surge is a durable wave or a spike. Bookings are a leading indicator; they turn before revenue does, in both directions, which makes them the earliest place any deceleration will show. The second is the enterprise backlog, sitting at a record $10.7 billion as of the first quarter of 2026 — the stock of future revenue, and the number to track for whether that book-to-bill can hold above one or begins to normalize.3 The third is the pairing of services revenue contribution and organic margin expansion — whether services stays around a third of the enterprise, and whether management keeps delivering its roughly 100-basis-point annual margin improvement.4 Those two together are the proof, quarter by quarter, of whether the moat is compounding or merely holding.

A fourth gauge belongs on the watch-list as a falsification test rather than a growth signal: residential volumes and the free-cash-flow conversion rate. Residential is where management has made a specific, dated promise — a second-half-2026 recovery — and it is the cleanest place to check whether the company still does what it says it will do. Cash conversion, which slipped just below its 100% target in 2025, is where accounting profit gets validated as real money; a persistent gap between reported earnings and cash would be the first quiet sign that the quality of the business is eroding beneath a still-rising stock. None of these numbers requires calculation — they are all disclosed each quarter — and together they let an investor mark the thesis to reality instead of to narrative.

There is a version of this story that ends in vindication: a focused climate pure-play, riding the twin tailwinds of electrification and AI, converting a decades-old distribution advantage and service annuity into durable, above-industry returns that justify every turn of its premium multiple. And there is a version that ends in disappointment: a cyclical machinery business caught at a peak, priced for perfection, meeting freshly focused rivals and a data-center cycle that turns. The evidence today leans toward the first story, but the price already assumes it, which is precisely why the bear case deserves respect rather than dismissal.

Whatever the market decides, it is worth ending where the story began — with the engineers. A plumber's son in La Crosse who thought radiators were too heavy. A self-taught inventor near a Minneapolis golf course who refused to let a truckload of chickens spoil. Reuben Trane and Frederick Jones never met, never imagined a $110 billion company, and never used the phrase "book-to-bill." They just solved the unglamorous physical problems of moving heat from where it wasn't wanted to where it was. More than a century later, that quiet work — cooling the buildings, chilling the trucks, and now taming the furnace-heat of the machines that run artificial intelligence — is still the whole business. The financial engineering came and went and came again. The thermal engineering never stopped.

References

-

Trane Technologies Reports Fourth Quarter and Full Year 2025 Results — SEC Form 8-K Exhibit 99.1, 2026-01-29 ↩↩↩

-

Trane Technologies plc 2025 Form 10-K Annual Report — SEC, 2026-02-13 ↩↩↩

-

Trane Technologies First-Quarter 2026 Results — SEC Form 8-K Exhibit 99.1, 2026-04-30 ↩↩↩↩

-

Trane Technologies Q1 2026 Earnings Call Transcript — Trane Technologies, 2026-04-30 ↩↩↩↩↩↩

-

Why Trane Technologies Commands a Structural Premium Over Peers — Bloomberg, 2025-11-20 ↩↩↩↩

-

Trane Technologies Market Capitalization — CompaniesMarketCap, 2026 ↩

-

Frederick McKinley Jones — National Inventors Hall of Fame ↩

-

The purchase of Trane Co. by American Standard Inc. — UPI Archives, 1983-12-06 ↩

-

American Standard Companies — Encyclopædia Britannica / corporate history record ↩

-

Ingersoll Rand to Acquire Trane Inc. for Approximately $10.1 Billion — Trane Technologies IR, 2007-12-17 ↩

-

Ingersoll Rand and Gardner Denver Complete Reverse Morris Trust Transaction — Business Wire, 2020-03-02 ↩↩

-

Gardner Denver and Ingersoll Rand Industrial Segment Merger SEC Filing — SEC, 2020-03-02 ↩

-

Trane Technologies Completes Acquisition of Stellar Energy — Trane Technologies IR, 2026-02-18 ↩

-

Trane Technologies to Acquire Stellar Energy Digital Business — Trane Technologies IR, 2025-12-02 ↩

-

Trane Technologies Completes Acquisition of LiquidStack — Trane Technologies IR, 2026-03-03 ↩

-

Trane Technologies Completes Acquisition of BrainBox AI — Business Wire, 2025-01-03 ↩

-

Trane Technologies Completes Acquisition of Nuvolo — Business Wire, 2023-11-03 ↩

-

Trane Technologies Unveils Thermal Management Reference Design for Gigawatt-Scale NVIDIA AI Factories — Trane Technologies IR, 2025-10-28 ↩

-

Dave Regnery, Chair and CEO — Trane Technologies Leadership ↩↩

-

Johnson Controls to Sell Residential and Light Commercial HVAC Business to Bosch — Johnson Controls IR, 2024-07-23 ↩

-

Carrier Announces Portfolio Transformation to Create Global Leader in Intelligent Climate and Energy Solutions — Carrier, 2023-04 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube