Tyson Foods: From Chicken Trucks to Protein Empire

I. Introduction & Episode Setup

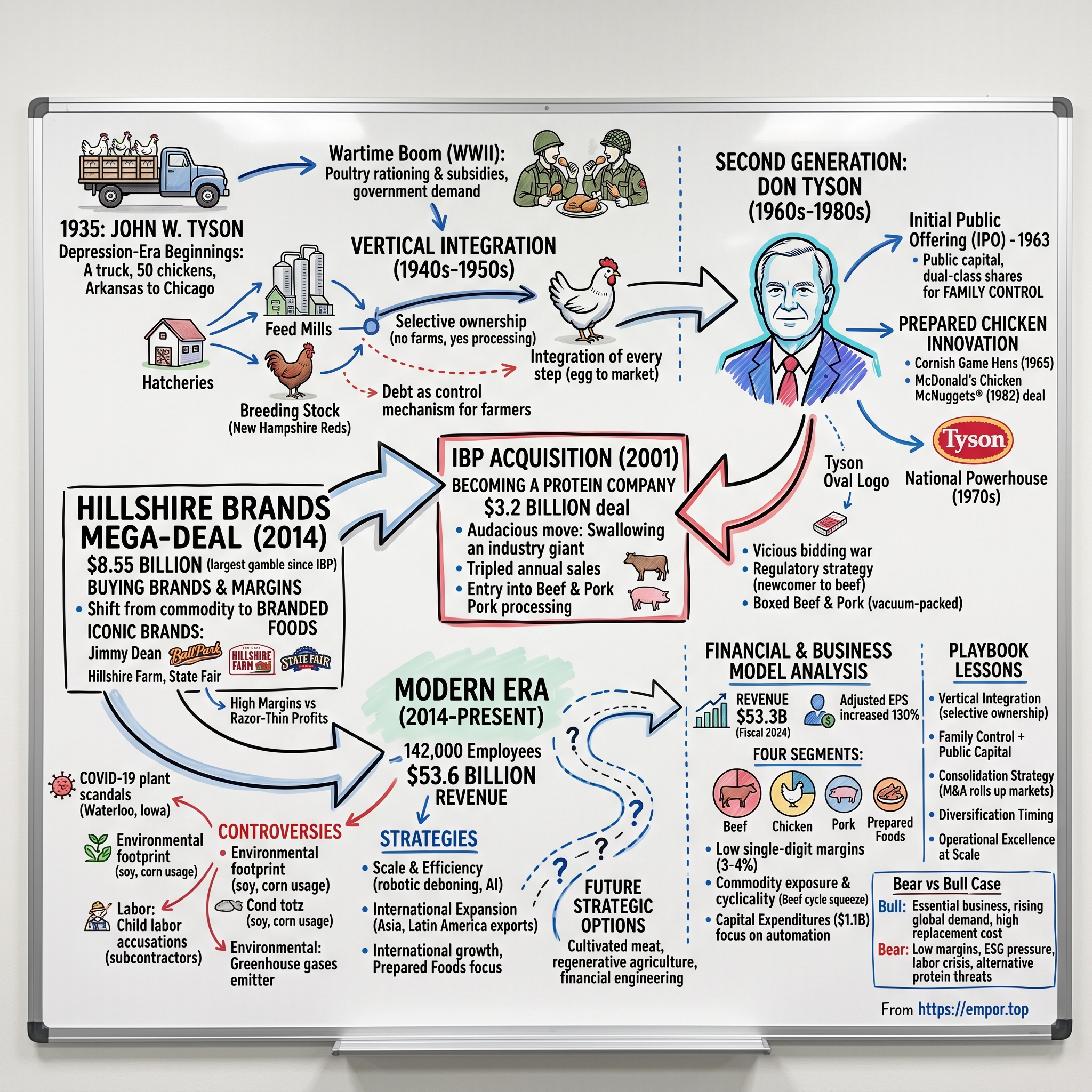

Picture this: A single truck loaded with 50 chickens, rattling through Depression-era Arkansas toward Chicago in 1935. The driver, John W. Tyson, had borrowed against everything he owned to make this run. He'd return with $235 in profit—enough to convince him that hauling chickens beat farming cotton in the midst of America's worst economic crisis. That modest truck would become the foundation of what is today a $53.6 billion revenue colossus that processes one out of every five pounds of meat consumed in America.

Tyson Foods stands as the world's second-largest processor of chicken, beef, and pork—surpassed globally only by Brazilian giant JBS. Walk into any American grocery store, restaurant, or school cafeteria, and you're almost certainly consuming Tyson protein, whether you know it or not. The company supplies McDonald's, KFC, Taco Bell, Burger King, Wendy's, Walmart, and Kroger. Its brands—from Jimmy Dean to Hillshire Farm to Ball Park—dominate refrigerated aisles. With 142,000 employees operating across four continents, Tyson has become synonymous with American meat production itself.

But here's the central question that drives our story: How did a Depression-era chicken trucker with a borrowed stake truck build what would become America's protein empire? The answer isn't just about chickens or even meat—it's about timing, vertical integration, family control, ruthless consolidation, and a willingness to embrace controversy in pursuit of scale. It's about three generations of Tysons who transformed American agriculture from fragmented family farms into an industrialized machine that feeds millions daily.

Our journey will take us from that first truck to the revolutionary concept of vertical integration in poultry, through the acquisition sprees that consolidated a fragmented industry, to the transformative $3.2 billion IBP acquisition that redefined Tyson as a multi-protein powerhouse. We'll explore how the company pioneered everything from chicken nuggets for McDonald's to boxed beef that revolutionized distribution. And we'll confront the darker side of this empire—the environmental impacts, labor controversies, and ethical questions that shadow every efficiency gain.

This is fundamentally a story about American capitalism in its purest form: the relentless pursuit of efficiency and scale in turning living animals into affordable protein. It's about how a family maintained iron-grip control while accessing public capital markets through clever share structures. And it's about what happens when feeding a nation becomes big business—really big business.

What makes Tyson particularly fascinating for students of business history is how it mirrors and shapes the evolution of American food itself. When John W. Tyson started hauling chickens, Americans ate about 10 pounds of chicken per year. Today? Over 90 pounds. That's not just a business growing with demand—that's a business creating and capturing an entire market transformation.

II. The Depression Era Origins & John W. Tyson

The Arkansas summer of 1931 offered little promise. John W. Tyson arrived in Springdale with his wife Mildred and one-year-old son Don, carrying the weight of Depression-era desperation. He had eleven cents in his pocket—not enough for a meal, barely enough for hope. The family had fled the failing farms of Missouri, joining the great migration of desperate Americans seeking any opportunity to survive. John bought a cup of coffee with a nickel and started looking for work hauling whatever needed moving—hay, fruit, chickens, anything.

For four years, John scraped by as a hauler for local farmers, learning the rhythms of northwest Arkansas agriculture. Following the collapse of the fruit industry in northwest Arkansas in the late 1920s, many farmers turned to raising poultry as a source of income. The connection of Highway 71 to Midwest markets opened a corridor of possibility. Chickens, unlike cattle or hogs, could be transported live in large numbers. They ate less, weighed less, and multiplied faster. John noticed something else: chickens were bringing in higher prices in the northern parts of the United States than in his home of Arkansas.

The gamble that changed everything came in 1935. John generated a $235 profit from his initial capital of $1,000 loan and $800 of his own money—he had borrowed against everything, risking complete ruin. He hauled approximately 50 chickens to sell in Chicago in 1935. That first Chicago run netted him more money than he'd seen in years. On his first journey there, he turned a profit of $235, encouraging him to start shipping poultry to Midwest markets on a full-time basis.

But this wasn't just about loading chickens on a truck. John Tyson became an innovator out of necessity. He stacked and nailed chicken coops onto a trailer and devised an in-transit feeding system to allow longer hauls. Without refrigeration or federal highways, keeping chickens alive for a thousand-mile journey required ingenuity. The feeding system meant birds could survive trips to Detroit, Cincinnati, Cleveland—markets that paid premium prices for fresh poultry.

World War II proved to be a boon for Tyson, as wartime rationing of beef and government subsidization of poultry made many northwest Arkansas chicken producers—particularly John Tyson—enormous profits. Chicken wasn't rationed like beef and pork. Suddenly, Americans who couldn't get their usual proteins turned to poultry. Demand exploded. The government actively subsidized production to feed troops and civilians alike. John Tyson found himself at the center of a boom he couldn't have imagined when he'd scraped together that first loan.

The wartime surge created new problems that demanded vertical integration—though John didn't call it that yet. When a supplier could not keep up with his need for baby chicks, Tyson bought an incubator, hatched them himself and began selling chicks to growers. When feed became scarce and expensive, he became a commercial feed dealer for Ralston Purina. Each bottleneck in the supply chain became an opportunity to expand control.

The logistical challenges of wartime shaped Tyson's business model in unexpected ways. He could not send drivers out on Thursdays and Fridays, when they would arrive at closed terminals on weekends. To avoid having stalled drivers on the payroll, he began buying and mixing wheat bran, corn and soybean meal and built a commercial mill, entering the feed business. What started as a scheduling problem became a profit center.

In 1943, Tyson bought 40 acres next to U.S. 71 in Springdale and purchased a few small broiler houses. This wasn't just expansion—it was the beginning of controlling production from egg to market. In 1943, he invested in a poultry-growing operation, and accordingly, the process of vertical integration—in which a poultry firm owns virtually every step of the production process from feed to distribution.

The formal incorporation came in 1947. John incorporates his growing business as Tyson Feed and Hatchery, Inc., in 1947. The company now provides three essential services: the sale of baby chicks, the sale of feed, and the transportation of chickens to market. By 1950, the numbers told the story of transformation: Tyson Feed and Hatchery processed 12,000 chickens a week, employed 52 people and grossed $1 million.

John Tyson understood breeding mattered as much as feeding. On April 10, 1946, John has a load of Andy Christy's New Hampshire Reds delivered by airplane to Fayetteville, a first for Northwest Arkansas. John says later, "I decided early that, if you had the best chicks in the area, you'd have the best customers and get the best results". These New Hampshire Reds, bred specifically for meat yield rather than egg production, represented the future of industrial poultry. John then did something radical: he threw the industry a curveball when he began cross-breeding his birds, resulting in poultry that performed better than pedigrees.

The transformation from hauler to integrated producer happened gradually, then suddenly. By 1957, the company produced 10 million broilers—nearly a thousand-fold increase from those first 50 chickens in 1935. But success brought new challenges. The postwar adjustment of the economy caused drastic price fluctuations, which forced many poultry growers into bankruptcy. Diseases ravaged farms. Competition intensified as other operators copied Tyson's methods.

This volatility would set the stage for the next chapter—when John's son Don would push for even greater integration, building the processing plant that would complete their control of the supply chain. The foundation was set: a Depression-era trucker had become a poultry baron, controlling chickens from egg to market. But the empire was just beginning.

III. Don Tyson Takes the Wheel: The Second Generation (1960s-1980s)

January 15, 1967. A railroad crossing near Springdale. The screech of brakes, the blast of a horn, then silence. In 1967, Don Tyson suddenly took the helm of the company after John Tyson and his wife were killed when their car was struck by a train. In an instant, the thirty-seven-year-old Don Tyson went from heir apparent to CEO of a company processing 48 million chickens a year. He hadn't planned for this moment to come so soon, but he'd been preparing for it his entire life.

In 1944, at age 14, Tyson was first introduced into the poultry industry as a chicken catcher and truck driver at Tyson's Feed and Hatchery, the family's poultry feed and live production business. In 1952, he left the University of Arkansas to join his father in expanding the business. Don's decision to leave college wasn't impulsive—he saw opportunity slipping away while he sat in classrooms. As he later recalled, "I left the [University of Arkansas] in 1952, and from that day until 1963, the year I took the company public, I worked in the business six days a week and on Dad's farm on the seventh day".

The son had different ideas than the father. Where John W. Tyson built relationships one handshake at a time, Don thought in systems and scale. The company opened its first poultry processing plant in 1958 on Randall Road in Springdale, with Donald Tyson as the first plant manager. Don had pushed his father hard for this plant, seeing that controlling processing was the missing link in their vertical integration. Originally budgeted at $75,000, John was not happy when his son's new processing plant went over budget. Don gets a bank loan to finish construction. At a final cost of $90,000, the Randall Road plant opens in 1958.

That processing plant changed everything. At that time, Tyson Foods controlled less than two percent of the U.S. chicken market. Don saw a fragmented industry ripe for consolidation. His strategy was brutally simple: acquire struggling competitors during downturns, integrate their operations, cut costs through scale. The 1960s poultry market gave him plenty of opportunities—wild price swings, disease outbreaks, and undercapitalized family operations going under.

The company went public with its initial public offering of stock in 1963 under the name Tyson's Foods, Inc. This gave Don access to capital markets while maintaining family control through a dual-class share structure—a move that would define Tyson's governance for generations. Don becomes president of the company in 1966. Following his father's death, Don Tyson took his place as chairman and CEO.

The transformation under Don's leadership was immediate and dramatic. He introduced what would become Tyson's signature innovation: prepared chicken products. Tyson joined the company in 1952 and made his mark on the family business in 1965 when he persuaded his father to introduce the Rock Cornish game hen as a specialty item at a flat rate of 50 cents per bird. These weren't actually Cornish or game hens—just five-week-old chickens marketed brilliantly. But they commanded premium prices and opened Don's eyes to value-added products.

The 1970s marked Tyson's emergence as a national powerhouse. In 1972, the company name changes to Tyson Foods, Inc., as we know it today. Along with the name change, we introduced a new look, the Tyson® oval. This wasn't just rebranding—it signaled Don's ambition to move beyond commodity chicken. The company made Fortune 1000 in 1970, a remarkable achievement for an Arkansas poultry processor.

Then came the pivot that would define modern Tyson: diversification beyond chicken. In 1977, Tyson became the nation's largest hog producer through strategic acquisitions in North Carolina. This was controversial within the company—many executives saw it as losing focus. Don saw it as risk mitigation. Different proteins had different cycles. When chicken prices crashed, pork might boom.

But the real breakthrough came in 1982. In 1982, the firm made the Fortune 500 list as one of America's largest companies, and it also secured lucrative contracts to supply chicken nuggets to restaurants such as fast-food giant McDonald's. The McDonald's deal wasn't just another contract—it fundamentally changed how Americans ate chicken. Back in 1982, McDonald's, in partnership with Keystone, Chicken McNuggets® were developed, which revolutionized the way Americans ate chicken and Tyson was asked to commercialize.

In the early 1980s when McDonald's launched McNuggets, Tyson was tasked with actually producing the pressed-together little chunks of chicken. The company developed a new chicken breed -- dubbed "Mr. McDonald" -- that it used in the morsels. This wasn't just about making nuggets—it was about engineering chickens specifically for processed food, creating supply chains that could deliver identical products to thousands of locations, and doing it all at a scale and price point that made chicken accessible to everyone.

The decade culminated with Don's boldest move yet. Seven years later, the company purchased Holly Farms. Tyson battled for six months with the Nebraska firm ConAgra for control of Holly Farms and in 1989 Don Tyson finally agreed to pay $1.29 billion for Holly Farms. This wasn't just an acquisition—it was a hostile takeover battle that captivated Wall Street. In 1990 Tyson's sales increased 50.7 percent as a result of the Holly Farms acquisition. The deal nearly doubled Tyson's market share overnight.

By the time Don stepped back from day-to-day operations in 1991, remaining chairman until 1995, he had transformed his father's trucking operation into something unrecognizable. During his tenure, the company's revenue increased from $51 million to more than $10 billion. In 1998, as the nation's leading poultry supplier, Tyson Foods, Inc., controlled 28 percent of the market with $7.4 billion in sales. Then the Tyson team numbered 70,000 worldwide, operating 70 food-processing plants in 17 states.

Don Tyson's legacy went beyond numbers. He pioneered the contract farming system that would become standard across American agriculture—nominally independent farmers raising Tyson's chickens with Tyson's feed under Tyson's specifications. Critics called it feudalism. Don called it efficiency. He created the template for turning a commodity into branded consumer products. And he established the acquisition playbook that would guide Tyson through its next transformation. But perhaps most importantly, he proved that with enough scale, vertical integration, and ruthless efficiency, you could dominate an entire protein category. The question for his successors would be: why stop at chicken?

IV. The Vertical Integration Playbook

The genius of Tyson's vertical integration model lies not in what the company owns, but in what it doesn't. In the early days of vertical integration, Tyson Foods, the pioneer of the model, realized that farming was the least profitable and most risky side of the business. This insight would reshape American agriculture forever.

Consider the elegant brutality of the system: Tyson Foods has been working with poultry farmers on a contract basis since the late 1940s. We supply the birds and feed, as well as technical expertise, while the poultry farmer provides the labor, housing and utilities to support the birds. On paper, it sounds like partnership. In practice, it's something else entirely.

The company's control begins before a single egg hatches. Tyson's poultry production process is fully vertically integrated. It begins with poultry breeding stock that are raised on a pullet farm for 20 weeks. After this, the chickens are sent to the breeder house where they lay eggs at around 26 weeks. Tyson owns the breeding stock, selects the genetics, controls the feed formulation, and determines every aspect of how the birds will be raised. The farmers? They own the debt.

The numbers tell the story of this asymmetry. Today, we pay nearly $820 million annually to the more than 3,600 poultry farmers who contract with us. That sounds generous until you realize these farmers collectively hold billions in debt for chicken houses built to Tyson's specifications. Former Tyson contract growers who spoke to Investigate Midwest said they have had to take out upwards of $2 million loans to become Tyson contract growers.

The control mechanism is debt, not ownership. Journalist Christopher Leonard, who has written extensively about the poultry industry, says, in the film, that the contract farming system "allows [the companies] to control the farm without actually owning it." Control is largely exercised through debt: in 2011, contract growers' total debt amounted to $5.2 billion. Two-thirds of contract growers have significant debt.

Here's how the trap works: A farmer borrows millions to build chicken houses to Tyson's exact specifications—the ventilation systems, the feeding equipment, the dimensions of the buildings themselves. To be considered a Tyson Foods contract poultry farmer, you must have existing chicken housing or property that could be used to build housing, within an approximate 30-to-50-mile radius of the feed mills that serve our poultry processing complexes. This is because of the efficiencies needed for delivering feed, chicks and providing service. These houses can't easily be repurposed for other companies or uses. The farmer is locked in.

The economic logic for Tyson is unassailable. This benefits the farmers because it insulates the farmer from the risk of changing market prices for chicken and feed ingredients such as corn and soybean meal, which represents most of the cost of raising a chicken. So, farmers' compensation is not dependent on what the feed costs or prices at the grocery store. But this "protection" comes at a price: total dependence.

What Tyson created wasn't just a business model—it was an entire ecosystem of control. The company operates feed mills that convert corn and soybeans into precisely formulated rations. It runs hatcheries that produce millions of chicks weekly, each one genetically selected for maximum meat yield and minimum grow-out time. It employs armies of technicians who visit farms, monitoring everything from mortality rates to feed conversion ratios.

The processing plants represent the apex of this integration. When Don Tyson built that first plant in 1958, he understood that controlling processing meant controlling pricing, quality, and market access. Today's plants are marvels of industrial efficiency, processing 45 million chickens weekly across Tyson's network. Every step is choreographed: birds arrive at predetermined weights, are processed through automated systems, and emerge as hundreds of different products—from whole chickens to nuggets to pet food ingredients.

The innovation extends beyond mere ownership of assets. Tyson pioneered the concept of coordinated production scheduling. Eggs are hatched, chicks are delivered to farms, feed is distributed, and birds are collected for processing—all on a schedule calculated to maximize plant utilization and minimize costs. A delay anywhere in the chain cascades through the entire system.

The average farmer has been raising chickens for Tyson Foods for 17 years. Some farm families have been raising chickens for us for three generations. This longevity masks a darker reality. Farmers who try to leave find their chicken houses are worthless to anyone but Tyson. Growers will build or purchase barns with company-specific parameters. In instances where a contract is cut short or growers want to move to a different poultry company, they often are unable to use or sell the equipment and barns they already own.

The tournament system adds another layer of control. Traditionally, companies like Tyson provide incentives to farmers to deliver safer, healthier and better quality chickens: while every farmer gets paid a base rate, farmers who deliver birds above the average standard can receive a bonus that's based off a points system. Farmers compete against their neighbors, with winners receiving bonuses and losers facing potential contract termination. It keeps farmers isolated, suspicious of each other, unable to organize collectively.

The power of this model became clear during expansion phases. When Tyson wanted to increase production, it didn't need to buy land or build farms. It simply offered contracts to new growers, who would borrow money to build houses, assuming the risk while Tyson reaped the rewards. When demand softened, Tyson could reduce bird placements, leaving farmers with empty houses and mounting debts.

Critics call it exploitation. Calling the poultry industry "extremely unfair" and "exploitative" of farmers, Kelloway added that Tyson's size and political power make it difficult to hold them accountable. Tyson calls it efficiency. The truth is, it's both. The system produces remarkably cheap protein—American consumers pay less for chicken, adjusted for inflation, than almost any time in history. But that efficiency is built on a foundation of farmer debt and corporate control that would have seemed dystopian to John W. Tyson in 1935.

The vertical integration model Tyson pioneered has been copied across agriculture—in pork, in beef, even in vegetables. It represents a fundamental shift in how food is produced: from independent farmers selling to markets, to contractors serving industrial systems. Owning the whole supply chain has allowed integrators to control price and quality, while the economies of scale they have achieved have made chicken the most consumed protein in the US. It has also reaped massive profits for the companies — in 2014, Tyson, the top poultry integrator, had earnings from its chicken business of $11 billion.

This is the machine Don Tyson built and refined—a system so comprehensive that a chicken's life is predetermined from conception to consumption. Every input measured, every process optimized, every inefficiency eliminated. It's capitalism perfected, if your definition of perfection doesn't include the farmers holding the debt, the workers processing the birds, or the communities dealing with the waste. But for delivering protein to American plates? The machine works exactly as designed.

V. The IBP Acquisition: Becoming a Protein Company (2001)

The phone rang at John H. Tyson's office on a cold January morning in 2001. On the line was Robert Peterson, IBP's CEO, with news that would trigger the most dramatic transformation in American meat production history. Smithfield Foods had just bid $32 per share for IBP. If John wanted to create the world's first true protein empire, he had 48 hours to make his move.

In 2001, Tyson Foods acquired IBP, Inc., the largest beef packer and number two pork processor in the United States, for US$3.2 billion in cash and stock. But this simple statement masks one of the most audacious corporate maneuvers in food industry history—a deal that would transform Tyson from a chicken company that happened to process some pork into the undisputed protein king of America.

IBP is the world's largest manufacturer of fresh meats and frozen and refrigerated food products, with 2000 annual sales of approximately $17 billion. To understand the magnitude of this acquisition, consider that Tyson's annual sales would triple to an estimated $24 billion a year after IBP comes on board. This wasn't just buying a competitor—it was swallowing an industry giant whole.

The strategic logic was compelling. Chicken had made Tyson rich, but it was also a commodity trap. Margins were thin, cycles brutal, and growth increasingly difficult as the company already controlled nearly 30% of the U.S. chicken market. John H. Tyson, who had taken over as CEO in 2000 after his father Don stepped back, saw what his grandfather and father had built and asked a different question: Why should protein be segregated? Why shouldn't one company provide all the animal protein America consumed?

IBP itself was no ordinary target. Founded as Iowa Beef Packers, Inc. on March 17, 1960 by Currier J. Holman and A.D. Anderson, it opened its first slaughterhouse in Denison, Iowa, and eliminated the need for skilled workers. The company had revolutionized beef processing much as Tyson had transformed chicken. In 1967, IBP introduced boxed beef and pork, which were vacuum packed and in smaller portions. It was a new option then, when the traditional method of shipping product was in whole carcass form. The boxed meat also saved energy and transportation costs by eliminating the shipment of fat, bones and trimmings.

The bidding war that erupted was vicious. Smithfield, the world's largest hog producer and processor, made an offer Nov. 12 to purchase IBP for $25 a share in stock. They bumped it to $32 this weekend to no avail. Tyson had started at $26, moved to $27, and finally sealed the deal at $30 per share. But why did IBP choose the lower offer?

The answer lay in regulatory strategy. Nicholson said since Tyson doesn't own pork processing plants and is a relatively small pork producer with 100,000 sows, unlike Smithfield, government regulators should look more favorably on this deal. He said Tyson doesn't have any plans to vertically integrate the pork industry. Smithfield's dominance in pork would have created antitrust nightmares. Tyson, despite being the chicken king, was a newcomer to beef and a minor player in pork—making the deal paradoxically easier to approve.

But the deal almost died before it closed. After signing in January, Tyson got cold feet. IBP's financials looked worse than expected. A subsidiary was under SEC investigation. The company tried to walk away, triggering one of the most dramatic legal battles in M&A history. Tyson Foods Inc. must go through with its $3.2 billion cash and stock acquisition of meatpacker IBP Inc., a Delaware Chancery Court ruled Friday. The judge's decision was scathing—Tyson had signed a deal and would be forced to honor it.

The integration challenge was staggering. The Company has approximately 120,000 team members in more than 300 facilities and offices in 32 states and 22 countries worldwide. Tyson was absorbing 52,000 IBP employees, dozens of processing plants, and entirely different corporate cultures. The chicken people from Arkansas suddenly had to manage beef operations in Nebraska and pork facilities in Iowa.

The Company operates in five business segments: Beef, Chicken, Pork, Prepared Foods and Other. This new structure reflected a fundamental shift in how Tyson saw itself. No longer organized around a dominant protein with side businesses, the company now positioned itself as a balanced protein portfolio. Each segment would operate semi-independently while sharing distribution, customer relationships, and back-office functions.

The immediate results were mixed but promising. Beef segment sales, which include only the nine weeks of IBP results, were $2 billion, including case-ready sales of $116 million. Beef segment operating income totaled $32 million. The beef business was profitable from day one, validating the strategic thesis.

What Tyson gained went beyond just beef and pork processing capacity. IBP brought relationships with every major retailer in America, expertise in case-ready meat products, and crucially, geographic diversification. While Tyson's chicken operations were concentrated in the South, IBP's facilities dotted the Midwest, closer to both cattle country and major population centers.

The cultural clash was real. IBP was famously tough—a company that had broken the unions, pioneered the use of immigrant labor, and operated with a ruthlessness that made even Tyson look gentle. The original IBP features prominently in Eric Schlosser's Fast Food Nation as the company that closed down the Chicago meatpacking district as a result of its industrial practices. Integrating these operations required delicate balancing.

But John H. Tyson understood something his critics missed: American protein consumption was converging. Consumers didn't shop for "chicken companies" or "beef companies"—they bought protein. Retailers didn't want to deal with separate suppliers for each meat. Restaurants needed partners who could provide everything from chicken nuggets to beef patties to bacon. The IBP acquisition positioned Tyson to be that single source.

Andrew P. Wolf of BB&T Capital Markets said last month that a Tyson-IBP merger would create a company with 30 percent of the beef market, 33 percent of the chicken market and 18 percent of the pork market. These market shares gave Tyson unprecedented pricing power and negotiating leverage. When Walmart wanted to discuss meat procurement, they now essentially had to talk to Tyson.

The financing structure revealed Tyson's confidence. Tyson will also assume $1.5 billion in IBP debt. Total consideration approached $5 billion—a massive bet for a company that had grown primarily through smaller, strategic acquisitions. But the Tyson family's control through dual-class shares meant they could make this generational bet without activist interference.

Looking back, the IBP acquisition marked the moment Tyson stopped being a poultry company that processed other proteins and became America's protein company. The new Tyson Foods, Inc. is the world's largest processor and marketer of beef, chicken and pork products and produces a wide variety of brand name, processed food products. The transformation was complete—from John W. Tyson's truck hauling 50 chickens to a corporation controlling one-fifth of all meat consumed in America.

The deal also set a template for industry consolidation that continues today. Competitors scrambled to match Tyson's scale, triggering waves of mergers. The era of regional meat packers was ending. Scale, integration, and multi-protein capabilities became table stakes. In forcing through the IBP acquisition, John H. Tyson didn't just transform his company—he reshaped an entire industry's structure.

VI. The Third Generation & Hillshire Brands Mega-Deal (2000s-2014)

The boardroom at Tyson headquarters buzzed with tension on June 8, 2014. John H. Tyson, now chairman, watched as CEO Donnie Smith laid out the numbers one more time. Pilgrim's Pride had just bid $55 per share for Hillshire Brands. If Tyson wanted to transform from a commodity meat processor into a branded foods powerhouse, they had 24 hours to make their move. The all-cash transaction is valued at approximately $8.55 billion, including Hillshire Brands' outstanding net debt. It would be the company's biggest gamble since IBP.

Tyson Foods will acquire all outstanding shares of Hillshire Brands for $63 per share. The all-cash transaction is valued at approximately $8.55 billion, including Hillshire Brands' outstanding net debt. The price tag was staggering—nearly triple what they'd paid for IBP thirteen years earlier. But this wasn't about buying processing capacity. This was about buying brands, margins, and a ticket out of the commodity trap.

John H. Tyson had assumed the CEO role in 2000, taking over from Leland Tollett after his father Don's retirement. The third generation faced a different challenge than his predecessors. John W. had built the foundation, Don had scaled it to dominance, but John H. inherited a mature business in an increasingly consolidated industry. Growth through traditional means was hitting natural limits.

The family control structure remained iron-clad. Through the dual-class share system Don had engineered during the 1963 IPO, the Tyson family maintained voting control despite owning a minority of total equity. This gave John H. the freedom to make bold moves without worrying about activist investors or hostile takeovers. "Tyson Foods has a history of growing through strategic acquisition," said John Tyson, chairman of the board, "It is the view of the board of directors that this is truly a transformational opportunity and one that best fits with our strategic plan while enhancing our margins and creating long-term shareholder value."

Prior to its acquisition by Tyson Foods, the company employed over 9,000 people and generated nearly $4 billion in annual sales. Hillshire wasn't just another meat company—it was a collection of America's most beloved food brands. Jimmy Dean sausages, Ball Park hot dogs, Hillshire Farm deli meats, State Fair corn dogs. These weren't commodities; they were brands with pricing power, customer loyalty, and crucially, higher margins.

The strategic rationale was compelling. "In fiscal 2013, Hillshire had a net margin of 4.7 % versus 2.3% for Tyson. On an operating basis, Hillshire's retail business had an 11.4% operating margin and its foodservice business a 7.3% margin," Kay said. Compare that Tyson's overall operating margin of 4% in 2013 and Kay said it's easy to see the attraction. Tyson was generating massive revenues but razor-thin profits. Hillshire generated a quarter of Tyson's sales but nearly half the margin.

The bidding war that erupted was fierce. Hillshire had originally agreed to buy Pinnacle Foods for $6.6 billion, trying to create its own food conglomerate. Then Pilgrim's Pride, backed by Brazilian giant JBS, crashed the party with an unsolicited $55 per share bid. Tyson, the largest U.S. meat processor, on Monday announced an agreement to buy Hillshire for $63 per share. That topped last week's $55 bid from Pilgrim's Pride, which is majority owned by Brazilian meatpacking giant JBS.

But Tyson's offer came with conditions. In addition, Tyson Foods will be making, on behalf of Hillshire Brands, a payment of the $163 million termination fee associated with the termination of Hillshire Brands' merger agreement with Pinnacle Foods Inc. Tyson was essentially paying Hillshire's breakup fee to walk away from the Pinnacle deal—a bold move that showed how desperately they wanted this acquisition.

The financing was audacious. Unlike the IBP deal, which used a mix of cash and stock, this was all cash—$8.55 billion in cold, hard currency. The transaction would be funded by cash on hand and a fully committed bridge facility from Morgan Stanley Senior Funding, Inc. and JP Morgan Securities LLC. The Tyson family agreed to dilute their holdings if necessary to maintain the company's investment grade rating.

"We want to buy this business for what it can become, not just for what it is now. Great brands like Hillshire, Jimmy Dean and Ball Park just don't come available very often,'' Tyson Chief Executive Donnie Smith said on a conference call with reporters. Smith, who had worked his way up from the processing plants, understood something fundamental: Tyson could produce all the chicken in the world, but without brands, they were always one cent away from losing a customer.

The regulatory hurdles were surprisingly manageable. The Department of Justice announced today that it will require Tyson Foods Inc. to divest Heinold Hog Markets, its sow purchasing business, in order to proceed with its $8.5 billion acquisition of The Hillshire Brands Company. The department said that, without the required divestiture, the transaction would have combined companies that account for more than a third of sow purchases from U.S. farmers, thereby likely reducing competition for purchases of sows from farmers. A relatively minor divestiture cleared the path.

The all-cash transaction is valued at approximately $8.55 billion, including Hillshire Brands' outstanding net debt, and represents a multiple of 16.7x trailing 12 months adjusted EBITDA or 10.5x including $300 million in synergies. The expected synergies were massive—$300 million annually through operational efficiencies, shared distribution, and eliminated redundancies. Tyson reported that the combination of assets will accelerate its growth in the coveted $1 billion breakfast-food category, the fastest growing segment in the food sector. Tyson CEO Donnie Smith said combining the brand strengths of Wright Brand bacon and Jimmy Dean sausage make for a blissful marriage and growing market share.

The transformation was immediate and profound. The combination of Tyson Foods and Hillshire Brands creates a single company with more than $40 billion in annual sales and a portfolio that includes recognized brands such as Tyson®, Wright®, Jimmy Dean®, Ball Park®, State Fair® and Hillshire Farm®. Overnight, Tyson went from being primarily a supplier to retailers and restaurants to being a major player in the branded consumer goods space.

The cultural integration proved smoother than IBP. Hillshire's Chicago sophistication meshed better with the evolving Tyson culture than IBP's rough-edged Midwest pragmatism had. The companies shared a focus on innovation, brand building, and premium positioning. Where IBP brought scale and efficiency, Hillshire brought marketing expertise and consumer insight.

Smith said the combined brands include four that are worth $1 billion or more. He said the combined companies will be the No. 2 player in the frozen retail category with $3.7 billion in annual sales, leap frogging over ConAgra Foods at $3.3 billion. This wasn't just adding brands—it was achieving critical mass in retail, gaining shelf space, and negotiating power with increasingly consolidated grocery chains.

For John H. Tyson, the Hillshire acquisition represented the fulfillment of a vision that had been building since IBP. His grandfather had created a chicken company. His father had scaled it to dominance. John H. was creating something entirely new—a protein-based consumer goods company that happened to own the supply chain all the way back to the farm.

The deal also marked a generational shift in strategy. Where previous acquisitions focused on production assets and market share, Hillshire was about intangible assets—brands, recipes, consumer relationships. "The Hillshire Brands acquisition would represent a defining moment for Tyson Foods," said Donnie Smith, Tyson's president and chief executive officer. It was defining indeed—the moment Tyson stopped being just a meat company and became a food company.

By the time the deal closed in August 2014, Tyson had transformed itself more radically than at any point since going public in 1963. The company that John W. Tyson started with a borrowed truck and 50 chickens now owned some of America's most iconic food brands, employed over 115,000 people, and generated over $40 billion in annual sales. The question now wasn't whether Tyson could compete—it was whether anyone could compete with Tyson.

VII. Modern Era: Scale, Efficiency & Controversies (2014-Present)

The meat packing plant in Waterloo, Iowa, became ground zero for everything wrong with modern industrial meat production. In April 2020, as COVID-19 swept through the facility, more than 1,000 of the plant's 2,800 workers would test positive. Five would die. During the COVID-19 pandemic, Tyson Foods was accused by some employees of failing to implement certain recommended protections, including physical distancing measures, plexiglass barriers and wearing of face masks. But the real scandal came later: plant managers had allegedly placed bets on how many workers would get sick.

This is the paradox of modern Tyson: a company that feeds America, employs 142,000 people, and generates over $53 billion in annual revenue, yet operates under a constant cloud of controversy. The business today: 142,000 team members, sells to national restaurant chains, schools, military bases, hospitals, and through all major retail channels including club stores, grocery stores, and discount stores. Produces about one-fifth of beef, chicken, and pork sold in the US, supplies major chains including KFC, Taco Bell, McDonald's, Burger King, Wendy's, Walmart, Kroger.

The leadership carousel that followed the pandemic reflected deeper instability. Dean Banks, former Alphabet executive (October 2020-June 2021). He received a $1.2 million salary and received a $5 million bonus to move to northwest Arkansas by December 2020. However, his ambitious plans were quickly overwhelmed by surging infections at Tyson plants along with allegations senior managers bet on worker COVID-19 cases. In the wake of multiple scandals after just 8 months as CEO, Banks abruptly resigned in June 2021 for undisclosed reasons before substantially impacting company strategy or culture.

Enter Donnie King. Long-time Tyson executive Donnie D King returned to the helm in mid-2021, resuming leadership amidst lingering pandemic impacts and inflationary pressures on the meat industry. An alumnus of the University of Arkansas at Little Rock, he had worked at Tyson for 36 years, beginning in 1982. King represented continuity—a company lifer who understood the business from the processing floor up.

King inherited a company facing existential questions. Tyson has been involved in numerous controversies related to environment, animal welfare, and employee welfare. The environmental footprint alone is staggering: In 2020, it was reported that Tyson Foods uses 4.89 million acres of land for soybeans and 5.2 billion acres of corn for providing feed for their 6 million cows, 22 million hogs, and 2 billion chickens. Tyson is the second-largest emitter of greenhouse gases in the global food industry.

The labor controversies run deeper than COVID. I am alarmed by new reports that Tyson Foods has actively participated in dangerous and illegal child labor practices. The report opens with the story of a teenager whose arm was ripped down to the tendons after it got caught in a factory machine. The Times suggests Tyson evades accountability for illegal child labor by relying on subcontractors. "Even when inspectors do catch child-labor violations," the Times reported, "they usually fine only the subcontracted companies, not the brands themselves."

Yet King has pushed forward with expansion and modernization. Notably, during the pandemic, Tyson began operations at its new $425 million, 370,000 square foot poultry complex in Humboldt, Tennessee. In August 2021, we announced a $300 million investment to build a new 325,000 square foot fully-cooked chicken plant in Danville, Virginia. The investments continue despite controversies—or perhaps because of them, as automation reduces reliance on human labor.

The operational excellence initiatives reflect a company trying to square an impossible circle. On one hand, Tyson pursues cutting-edge efficiency: robotic deboning systems, AI-powered quality control, predictive analytics for supply chain optimization. Its plants slaughter approximately 155,000 cattle, 461,000 pigs, and 45,000,000 chickens every week with industrial precision that would astound John W. Tyson.

On the other hand, each efficiency gain seems to generate new controversies. Faster line speeds lead to more worker injuries. Concentrated animal feeding operations create environmental disasters. Contract farming systems trap farmers in debt. The very scale that makes chicken affordable makes reform nearly impossible.

The company has attempted to navigate changing consumer preferences with mixed results. In 2016, Tyson Foods bought a 5% stake in the meat alternative company Beyond Meat, becoming the first major meat producer to invest in a meat alternative company. But by 2019, Tyson sold its stake in advance of Beyond Meat's initial public offering, with CEO Noel White saying Tyson intended to develop its own meat alternatives. The Raised & Rooted brand launched but struggled—consumers who want plant-based proteins don't trust Tyson, and Tyson's core customers don't want plant-based proteins.

The international expansion efforts have proven more successful. With facilities in 30 states, Tyson produces quality food in places like San Lorenzo, California; Joslin, Illinois; Storm Lake, Iowa. But the real growth comes from exports—Tyson annually exports the largest percentage of beef out of the United States, capitalizing on growing protein demand in Asia and Latin America.

The family dynamics add another layer of complexity. On June 13, 2024, Tyson Foods heir John R. Tyson, who has served as the company's chief financial officer (CFO), would be suspended from the company following his second alcohol related arrest. The fourth generation seems less interested in—or capable of—maintaining the dynasty their great-grandfather started with a borrowed truck.

King's strategy has been pragmatic: focus on what Tyson does best while making incremental improvements where possible. "I believe we need to be sharply focused on operating with excellence, executing our strategies, and continuing to innovate across our businesses throughout the world." The company anticipates total adjusted operating income of $1.9-2.3 billion for fiscal 2025—solid if unspectacular returns.

The prepared foods strategy continues to evolve. The Hillshire Brands acquisition has paid dividends, with Jimmy Dean and Ball Park maintaining strong market positions. But the commodity meat business remains the core, subject to all its traditional volatilities: grain prices, disease outbreaks, trade wars, consumer trends.

Perhaps most tellingly, King's response to political change reveals a company that has learned to survive regardless of external pressures. "There's a lot we don't know at this point, but I would remind you that we've successfully operated this business for … 90 years, no matter the party in control, the environment." Since 1935, the United States has had 14 presidents. Tyson has outlasted them all.

The modern Tyson is a study in contradictions: a family company run by professional managers, a commodity processor selling branded goods, an industrial giant pursuing sustainability, an American company dependent on immigrant labor, a feeding operation criticized for how it feeds. It's too big to fail, too controversial to love, too essential to ignore. The machine John W. Tyson started in 1935 has become something he couldn't have imagined—and might not recognize.

VIII. Financial Performance & Business Model Analysis

The numbers tell a story of scale that defies comprehension. Revenue was $53.309 billion, up 0.8% for fiscal 2024, representing a company that processes enough meat to feed entire nations. Yet beneath this massive top line lies a business model of surprising fragility—margins measured in single digits, fortunes swinging on penny movements in grain prices, entire segments oscillating between profit and loss based on disease outbreaks or weather patterns thousands of miles away.

The company achieved significant improvement in full-year profitability for 2024, with adjusted EPS increasing by over 130% year-over-year. This dramatic improvement masks the volatility inherent in Tyson's four-segment structure. The Company operates in five business segments: Beef, Chicken, Pork, Prepared Foods and Other. Each segment operates as its own mini-empire, with distinct economics, cycles, and challenges.

The Chicken segment represents the historical heart and current star performer. The Chicken segment showed a significant turnaround, achieving its best full-year operating income performance in the past seven years. Chicken AOI: Improved by nearly $1.1 billion for the year, strongest performance since fiscal 2017. Overall, the chicken segment is performing well and Tyson expects its branded retail business with higher margins to lead to solid operating income between $1 billion to $1.2 billion in fiscal 2025.

The chicken business exemplifies Tyson's vertical integration advantage. From breeding to processing, the company controls every step, allowing it to optimize for specific end products. When McDonald's needs a specific size and shape for nuggets, Tyson can breed chickens to match. When retail demands antibiotic-free options, Tyson can adjust its entire supply chain. This flexibility commands premium pricing.

Beef tells a different story—one of commodity exposure and brutal cyclicality. The beef segment had an adjusted operating loss of $71 million in the quarter, down from a $17 million gain reported a year ago. The segment reported a negative operating margin of 1.3% with no indication when it might turn positive. Unlike chicken, where Tyson controls the entire supply chain, beef depends on independent cattle ranchers subject to drought, feed costs, and their own economic pressures.

The cattle cycle—the multi-year process by which herd sizes expand and contract—creates feast-or-famine dynamics. When cattle supplies are tight, as they are now with historically low herd numbers, packers like Tyson get squeezed between high cattle prices and what consumers will pay for beef. We anticipate adjusted operating income (loss) between ($400) million and breakeven in fiscal 2024 for the beef segment, reflecting these challenging dynamics.

Pork occupies a middle ground. Pork AOI Increase: $270 million year-over-year for fiscal 2024. The company benefits from both contract production and spot market purchases, providing some flexibility. But pork remains vulnerable to trade disputes—particularly with China, the world's largest pork consumer—and disease outbreaks like African Swine Fever that can devastate global supply chains overnight.

The Prepared Foods segment represents Tyson's highest-margin future. Prepared Foods AOI Growth: 2% year-over-year, best performance since fiscal year 2018. This is where the Hillshire Brands acquisition pays dividends—branded products like Jimmy Dean sausages and Ball Park hot dogs command premium prices and consumer loyalty. These products transform commodity meat into value-added offerings with 10%+ operating margins versus the low single digits of fresh meat.

The capital allocation strategy reflects both confidence and caution. Tyson expects revenue to be flat or down 1% on the low end, with capital expenditures reduced to $1.1 billion. The company is investing in automation and efficiency rather than capacity expansion, recognizing that in mature markets, operational excellence matters more than scale.

Free cash flow increased by more than $1.6 billion compared to the previous year, driven by improved operating income and prudent capital expenditure management. This cash generation enables consistent dividends—This results in an annual dividend rate in fiscal 2025 of $2.00 for Class A shares and $1.80 for Class B shares, or a 2% increase compared to the fiscal 2024 annual dividend rate—while maintaining financial flexibility.

The margin dynamics reveal the fundamental challenge. Even in a good year, Tyson's overall operating margins hover around 3-4%. Compare this to software companies with 30% margins or pharmaceutical companies with 20%+ margins, and you understand why Tyson trades at modest multiples despite its massive scale. The company processes commodities with enormous capital requirements, regulatory burdens, and social responsibilities, yet captures only a sliver of value.

Risk management becomes existential at this scale. Commodity price hedging, foreign exchange exposure, trade policy shifts—any miscalculation can wipe out quarters of profits. There is also a growing demand for higher-valued products across the world, including specialty products which are in far less demand in the United States, like organ meats. Such demand raises the value of the whole animal, which benefits ranchers, feeders, and producers. Export markets provide crucial margin enhancement by monetizing parts Americans won't eat.

The operational metrics are staggering. Its plants slaughter approximately 155,000 cattle, 461,000 pigs, and 45,000,000 chickens every week. Each plant operates on razor-thin tolerances—a few hours of downtime can destroy profitability for an entire quarter. Labor shortages, equipment failures, or food safety incidents represent constant threats.

For fiscal 2025, the United States Department of Agriculture (USDA) indicates domestic protein production (beef, pork, chicken and turkey) will increase approximately 1% compared to fiscal 2024 levels. This modest growth reflects a mature market where population growth and export demand drive incremental volume rather than transformational expansion.

The financial model ultimately rests on three pillars: scale that creates cost advantages, vertical integration that captures supply chain value, and brands that command premium pricing. Remove any pillar and the edifice crumbles. Tyson must be simultaneously the lowest-cost commodity processor and a premium brand owner—a balancing act that grows more difficult as consumers demand transparency, sustainability, and ethical production while expecting ever-lower prices.

Looking forward, "Looking ahead, we are optimistic about our outlook and our ability to deliver long-term value to our shareholders. Our multi-protein, multi-channel portfolio, combined with our best-in-class team, iconic brands and focus on operational excellence positions us well for Fiscal 2025 and beyond". The optimism is warranted but qualified—Tyson has proven it can generate cash and returns even in challenging environments. But the business model remains fundamentally unchanged since John W. Tyson's day: turning animals into food as efficiently as possible, capturing whatever margin the market allows, and hoping the cycles turn in your favor.

IX. Playbook: Lessons in Building a Food Empire

The Tyson Foods playbook reads like a masterclass in industrial capitalism, each lesson written in the blood, sweat, and debt of three generations building an empire from nothing. These aren't theoretical business school concepts—they're battle-tested strategies that transformed American agriculture and created one of the world's largest food companies.

Lesson 1: Vertical Integration as Competitive Moat

The decision to vertically integrate in the 1940s was foundational. But Tyson's genius wasn't just owning the supply chain—it was selective ownership. The company owns breeding stock, hatcheries, feed mills, and processing plants. But crucially, it doesn't own the farms. In the early days of vertical integration, Tyson Foods, the pioneer of the model, realized that farming was the least profitable and most risky side of the business.

This selective integration creates powerful advantages. Tyson controls quality from genetics to grocery shelf. It captures margin at every step except the riskiest one. Contract farmers bear the capital costs of land and buildings, the operational risks of raising birds, and the financial risks of debt. Tyson bears only the market risk—which it can hedge—and the processing risk—which it can control through operational excellence.

The model scales beautifully. Adding capacity means finding farmers willing to borrow money to build chicken houses, not deploying billions in capital. Exiting a market means ending contracts, not writing off massive fixed assets. It's capitalism's perfect machine: privatized profits, socialized risks.

Lesson 2: Family Control with Public Capital

The dual-class share structure engineered during the 1963 IPO remains Tyson's governance masterstroke. The family maintains voting control through Class B shares while accessing unlimited public capital through Class A shares. This structure enabled massive acquisitions—IBP for $3.2 billion, Hillshire for $8.55 billion—without diluting family control.

This isn't about dynasty building—it's about strategic patience. Public companies face quarterly earnings pressure. Family-controlled companies can think in decades. When John H. Tyson pushed through the IBP acquisition despite legal challenges, he wasn't worried about activist investors or hostile takeovers. The family's voting control meant they could pursue transformational deals that might take years to pay off.

The structure also enables contrarian moves. Investing in plant-based proteins, building excess capacity ahead of demand, maintaining employment during downturns—these decisions might hurt short-term earnings but position the company for long-term dominance. Try explaining that to Carl Icahn without control.

Lesson 3: Consolidation as Strategy

Tyson's growth story is really an acquisition story. From Don Tyson's hostile takeover of Holly Farms to John H.'s transformation via IBP to the Hillshire brands play, each generation has used M&A to redefine the company. But this isn't empire building—it's strategic consolidation with clear industrial logic.

The playbook is consistent: identify fragmented markets, acquire struggling competitors during downturns, integrate operations ruthlessly, and emerge with dominant market share. In chicken, Tyson rolled up regional processors into national scale. With IBP, it replicated the model in beef and pork. Hillshire brought brands and margins.

Each acquisition follows a pattern. First, achieve operational synergies through plant rationalization and procurement scale. Second, leverage distribution relationships—when Walmart negotiates with Tyson, they're negotiating for chicken, beef, pork, and prepared foods in one conversation. Third, apply best practices across the acquired operations, typically improving margins by 200-300 basis points within two years.

Lesson 4: Diversification Timing

The progression from chicken to multi-protein wasn't random—it was carefully sequenced. Tyson first dominated chicken, achieving 25%+ market share and generating consistent cash flow. Only then did it diversify into beef and pork through IBP. Once the protein portfolio was complete, it moved up the value chain into prepared foods with Hillshire.

This sequencing matters. Each stage provided the financial foundation for the next. Chicken profits funded beef and pork expansion. Combined protein scale justified prepared foods premiums. You can't build a branded foods business without reliable protein supply. You can't achieve protein scale without operational excellence in at least one category.

The timing also reflects market maturity. Tyson diversified out of chicken just as growth slowed and margins compressed. It bought into beef and pork when those industries needed consolidation. It acquired brands when consumers shifted toward convenience. Reading market cycles and moving proactively—not reactively—defines the Tyson playbook.

Lesson 5: Operational Excellence at Scale

At Tyson's scale, tiny improvements yield massive returns. Reducing processing cost by one cent per pound across 45 million chickens weekly equals $23 million annually. Improving feed conversion ratios by 1% saves hundreds of millions. This obsession with operational metrics drives everything.

The company pioneered statistical process control in meat processing, treating biological systems like manufacturing lines. Every input is measured, every output tracked, every variance investigated. Tyson's returns are also strengthened by our efforts to become a more agile and efficient company through innovation. This isn't just about cost cutting—it's about predictability in an inherently unpredictable business.

Technology amplifies these advantages. Computer vision systems grade meat quality more consistently than human inspectors. Predictive analytics optimize feed formulations in real-time based on ingredient costs. Automation reduces labor dependency while improving safety. Each innovation might save pennies per pound, but at Tyson's scale, pennies become millions.

Lesson 6: Managing Commodity Cycles

Tyson doesn't fight commodity cycles—it surfs them. The multi-protein portfolio provides natural hedges. When beef margins compress due to high cattle costs, chicken margins often expand as consumers trade down. When grain prices spike, hurting chicken margins, beef margins might improve as producers liquidate herds.

The company also uses financial hedging aggressively, locking in grain costs and foreign exchange rates months in advance. But the real hedge is operational flexibility. Plants designed to process multiple species. Product mix that can shift between fresh and frozen, retail and foodservice, domestic and export. Distribution networks that can redirect product to wherever margins are highest.

This flexibility requires massive investment in systems and processes. But it enables Tyson to capture value regardless of market conditions. In good times, the company expands margins through operational leverage. In bad times, it gains market share as weaker competitors fail.

Lesson 7: Brand Building vs. Commodity Processing

The tension between efficiency and differentiation defines modern Tyson. Commodity processing demands ruthless cost focus—every penny matters when you're competing on price alone. Brand building requires investment in quality, marketing, and innovation that commodity economics won't support.

Tyson's solution is portfolio segmentation. The fresh meat operations run as cost-focused commodity businesses, generating cash and scale. The prepared foods division operates as a branded consumer goods company, investing in innovation and marketing. The segments share infrastructure and purchasing power but maintain distinct operating models.

This dual model is difficult to execute. It requires different metrics, incentives, and cultures within one company. But when it works, it's powerful. Tyson can offer Walmart both the cheapest commodity chicken and the most premium branded products, capturing value across the entire price spectrum.

Lesson 8: Managing Controversy

Perhaps the most uncomfortable lesson from Tyson's playbook is that controversy doesn't kill companies—inefficiency does. Tyson has weathered environmental disasters, labor scandals, animal welfare exposés, and regulatory sanctions. The stock price dips, executives apologize, minor reforms are implemented, and business continues.

This isn't endorsement—it's observation. Tyson's response to controversy follows a pattern: acknowledge concerns, implement visible but limited changes, emphasize economic contributions (jobs, affordable food), and wait for attention to shift. The company bets—correctly so far—that consumers' desire for cheap protein outweighs their ethical concerns.

The playbook includes proactive relationship building with regulators, politicians, and communities. Tyson's economic impact in the communities we operate is more than $27 billion annually, including $638 million in Georgia, $455 million in North Carolina, and $167 million in Virginia. And every year, we invest more than $15 billion with more than 11,000 independent producers who supply us with live cattle, pigs, chickens, and turkeys—many of whom have supplied Tyson for multiple generations. Economic impact buys political protection.

The Meta-Lesson

The ultimate lesson from Tyson's playbook isn't about any single strategy—it's about compound advantages. Vertical integration enables operational excellence which generates cash for acquisitions which create scale advantages which fund brand building which improves margins which attract capital for more acquisitions. Each advantage reinforces the others, creating a flywheel that's nearly impossible to stop.

But flywheels can spin both ways. If operational excellence slips, margins compress, limiting acquisition capacity, reducing scale advantages, constraining brand investment, further pressuring margins. Tyson's playbook works only when executed relentlessly, consistently, and at scale. There's no room for complacency in commodity processing.

The playbook also reveals an uncomfortable truth: in commodity businesses, nice guys finish last. Tyson succeeded by being tougher than competitors, more willing to embrace controversy, more aggressive in pursuit of scale. Whether that's admirable or deplorable depends on your perspective. What's undeniable is that it worked.

X. Bear vs. Bull Case & Future Outlook

The Bull Case: An Essential Business at Replacement Cost

The bullish thesis on Tyson starts with a simple observation: People need protein, Tyson provides protein at scale no competitor can match, and building a comparable operation from scratch would cost tens of billions and take decades. Our multi-protein, multi-channel portfolio, combined with our best-in-class team, iconic brands and focus on operational excellence positions us well for Fiscal 2025 and beyond.

Start with the demand side. Global protein consumption continues rising, driven by population growth and rising incomes in developing markets. The UN projects global meat demand will increase 70% by 2050. American protein consumption, already among the world's highest, shows no signs of declining despite health concerns and alternative protein hype. Today, Americans are demanding higher-quality, convenience and variety—all of which customers are willing to pay for across the food chain, benefiting both cattle producers and beef processors. For example, choice and prime beef grades have increased from 60 percent in 2000 to 85 percent in 2020.

The scale advantages are insurmountable. Tyson produces about one-fifth of the beef, chicken, and pork sold in the United States. This scale creates procurement advantages—when Tyson negotiates grain prices, it's buying for 45 million chickens weekly. It creates distribution efficiency—one truck stop at Walmart can deliver chicken, beef, pork, and prepared foods. It creates operational leverage—fixed costs spread across massive volumes.

The replacement cost argument is compelling. Tyson operates 123 food processing plants. Building a single modern poultry complex costs $400-500 million. A beef plant runs $300-400 million. Add in feed mills, distribution centers, and the thousands of contracted farms, and you're looking at $30-40 billion just to replicate the physical infrastructure. Then consider the intangibles: customer relationships, supply chain expertise, brand value, operational knowledge. No rational competitor would attempt to build this from scratch.

The multi-protein diversification provides resilience. When beef struggles, chicken compensates. When foodservice declines, retail grows. When domestic demand softens, exports increase. For 2025, we expect Prepared Foods and Chicken to deliver approximately 50% of our AOI, with a 10% growth at midpoint. We anticipate growth in Prepared Foods and Chicken, with stable performance in Pork and Beef. This portfolio balance reduces volatility and ensures cash generation across cycles.

The operational improvement story has legs. The company achieved significant improvement in full-year profitability for 2024, with adjusted EPS increasing by over 130% year-over-year. This isn't financial engineering—it's blocking and tackling. Plant automation reduces labor costs 2-3% annually. Data analytics improve yield 1-2% yearly. Supply chain optimization saves hundreds of millions. These improvements compound over time.

The free cash flow generation is robust. We expect free cash flow to be between $1.0 billion and $1.6 billion for fiscal 2025. At current valuations, Tyson trades at less than 10x free cash flow—a bargain for a business with dominant market position and consistent cash generation. The dividend provides downside support while you wait for multiple expansion.

International expansion offers untapped potential. Tyson generates most revenue domestically despite global operations. China alone consumes half the world's pork. Rising Asian middle classes demand higher-quality protein. Tyson's expertise in large-scale production and food safety could command premium valuations in markets desperate for reliable protein supply.

The Bear Case: A Structurally Challenged Business in Secular Decline

The bearish view sees Tyson as a Victorian-era business model struggling against 21st-century headwinds. Start with the brutal economics: commodity processing with single-digit margins, massive capital requirements, and no real pricing power. When your best margin business (Prepared Foods) generates 11% operating margins and your largest business (Beef) loses money, financial engineering can't save you.

The labor crisis is existential. His ambitious plans were quickly overwhelmed by surging infections at Tyson plants along with allegations senior managers bet on worker COVID-19 cases. Meat processing remains one of America's most dangerous, lowest-paid jobs. The workforce depends heavily on immigrants, both documented and undocumented. Rising wages, worker shortages, and automation limits mean structurally higher costs ahead.

Environmental and social governance (ESG) pressures intensify yearly. Tyson is the second-largest emitter of greenhouse gases in the global food industry. According to the Institute for Agriculture and Trade Policy, Tyson is among the largest single sources of greenhouse gases in the world, when the whole process of rearing animals for slaughter (such as producing feed for the animals and using agriculture chemicals) is considered. Carbon taxes, water restrictions, and waste regulations could destroy already-thin margins.

The alternative protein threat is real and accelerating. Beyond Meat and Impossible Foods are today's disruptors, but tomorrow's threats include cultivated meat, precision fermentation, and plant-based alternatives that actually taste good. Tyson's investments in alternative proteins have failed—In 2019, Tyson sold its stake in advance of Beyond Meat's initial public offering, with CEO Noel White saying Tyson intended to develop its own meat alternatives. The company is structurally unable to disrupt itself.

Consumer preferences are shifting faster than Tyson can adapt. Millennials and Gen Z consumers prioritize sustainability, animal welfare, and transparency—none of which align with industrial meat production. They're comfortable with plant-based alternatives and willing to pay premiums for perceived ethical production. Tyson's brand associations—factory farming, environmental damage, labor exploitation—are toxic to these consumers.

The commodity cycle risk remains severe. The beef segment had an adjusted operating loss of $71 million in the quarter, down from a $17 million gain reported a year ago. The segment reported a negative operating margin of 1.3% with no indication when it might turn positive. Beef represents nearly 40% of revenue but generates losses. The cattle cycle won't turn favorable for years. Meanwhile, African Swine Fever, avian flu, or another pandemic could devastate supply chains overnight.

The regulatory and legal risks multiply. "Even when inspectors do catch child-labor violations," the Times reported, "they usually fine only the subcontracted companies, not the brands themselves." In short, "the brands that [have] benefitted from the children's labor [have] faced no consequences". Price-fixing lawsuits, labor violations, environmental sanctions—the legal costs never end. One major food safety incident could trigger billions in liability.

Market structure changes threaten the model. Retail consolidation means fewer, more powerful customers. Walmart and Amazon can demand ever-lower prices. Restaurant chains like McDonald's increasingly bypass processors, dealing directly with farms. The middleman role Tyson occupies becomes less valuable as technology enables direct connections.

Future Strategic Options

The strategic paths forward reflect these competing realities:

Further Consolidation: Tyson could acquire remaining independent processors, particularly in beef where fragmentation remains. JBS's regulatory troubles might create opportunities. But antitrust scrutiny intensifies, and the returns on consolidation diminish as the industry matures.

International Expansion: Building or acquiring processing capacity in growth markets offers higher returns than domestic optimization. But international operations bring political risk, currency exposure, and different competitive dynamics. Tyson's Arkansas culture might not translate to Shanghai or São Paulo.

Alternative Proteins: Tyson could make a massive bet on alternative proteins, acquiring or building next-generation capabilities. But this requires capabilities Tyson doesn't possess—food science, consumer marketing, venture mindset. The company's DNA is industrial efficiency, not innovation.

Value Chain Extension: Moving further downstream into prepared foods, meal kits, or restaurant chains could capture more margin. But this requires different skills and competes with current customers. Moving upstream into farming seems logical but destroys the capital-light contract model.

Financial Engineering: Tyson could leverage its cash flow for massive buybacks, special dividends, or go-private transactions. The family's voting control makes this feasible. But this assumes the business model remains viable long-term—a questionable assumption.

The Fourth Generation Question

Perhaps the biggest uncertainty is leadership. On June 13, 2024, Tyson Foods heir John R. Tyson, who has served as the company's chief financial officer (CFO), would be suspended from the company following his second alcohol related arrest. The fourth generation shows little interest in or aptitude for running an industrial meat company. Professional management under Donnie King provides stability, but family companies without family leadership often lose their way.

The next decade will determine whether Tyson Foods represents the perfection of 20th-century industrial agriculture or its last gasp. Bulls see essential infrastructure trading at distressed valuations. Bears see structural decline masked by financial engineering. Both might be right—Tyson could generate cash for years while its business model slowly erodes.

The truth likely lies between extremes. Tyson will probably survive and even thrive for years, adapting incrementally to new realities. But the days of transformational growth are over. The company that John W. Tyson started with entrepreneurial energy has become what all successful revolutionaries eventually become: the establishment, defending its position against the next wave of disruption.

XI. Epilogue & Reflections

The conference room at Tyson headquarters sits empty now, the late afternoon sun streaming through windows overlooking the Arkansas hills. On the wall hangs a black-and-white photograph: John W. Tyson standing beside his truck in 1935, smiling with the confidence of a man who has no idea he's about to build an empire. If he could see what his company has become—$53 billion in revenue, 142,000 employees, feeding millions daily—would he recognize it as his dream fulfilled or his nightmare realized?

The transformation from Depression-era trucker to protein empire represents more than corporate growth—it's the industrialization of life itself. Where once farmers raised chickens that pecked in yards, Tyson engineered birds that grow so fast they can barely walk. Where once cattle roamed ranches for years, Tyson processes them in minutes with algorithmic precision. Where once food meant connection to land and season, Tyson delivers identical products year-round to identical stores serving increasingly identical meals.

This isn't judgment—it's observation. Tyson feeds America affordably and efficiently. Without industrial agriculture, billions would starve. The average American spends less than 10% of income on food, down from 30% in 1950. That liberation from food insecurity enabled everything else—education, innovation, leisure. Tyson and companies like it deserve credit for that transformation.

Yet the costs are undeniable. Tyson is the second-largest emitter of greenhouse gases in the global food industry. According to the Institute for Agriculture and Trade Policy, Tyson is among the largest single sources of greenhouse gases in the world. Communities near Tyson facilities deal with water pollution, air quality issues, and the social challenges of a low-wage workforce. Contract farmers carry crushing debt while Tyson captures the profits. Workers face dangerous conditions for minimal pay. Animals live brief, confined lives optimized for efficiency rather than welfare.

The biggest surprise in researching Tyson's history is how inevitable it all seems in retrospect. Each decision followed logically from the last. John W. Tyson integrated vertically because it made sense. Don Tyson consolidated the industry because he could. John H. Tyson diversified into beef and pork because growth demanded it. The family didn't set out to industrialize American agriculture—they just kept making rational business decisions that compounded into transformation.

The key takeaways read like lessons from another era:

Scale is everything. In commodity businesses, the largest player wins. Tyson understood this before anyone else and pursued scale relentlessly.

Control the choke points. Tyson doesn't need to own everything—just the critical nodes where value is created or captured.

Embrace controversy. Every efficiency improvement in meat processing generates opposition. Tyson learned to power through rather than apologize.

Family control matters. The ability to think in decades rather than quarters enabled transformational moves impossible for public companies.

Vertical integration works. Despite what business schools teach about focus, owning the supply chain creates advantages competitors can't match.

If we were running Tyson today? The temptation would be to radically restructure—spin off the commodity businesses, double down on brands, invest heavily in alternatives. But that misunderstands what Tyson is. This is an industrial machine optimized for current reality. Dramatic change would destroy more value than it creates.