Tower Semiconductor: The King of Specialty Foundries

I. Introduction & Episode Roadmap

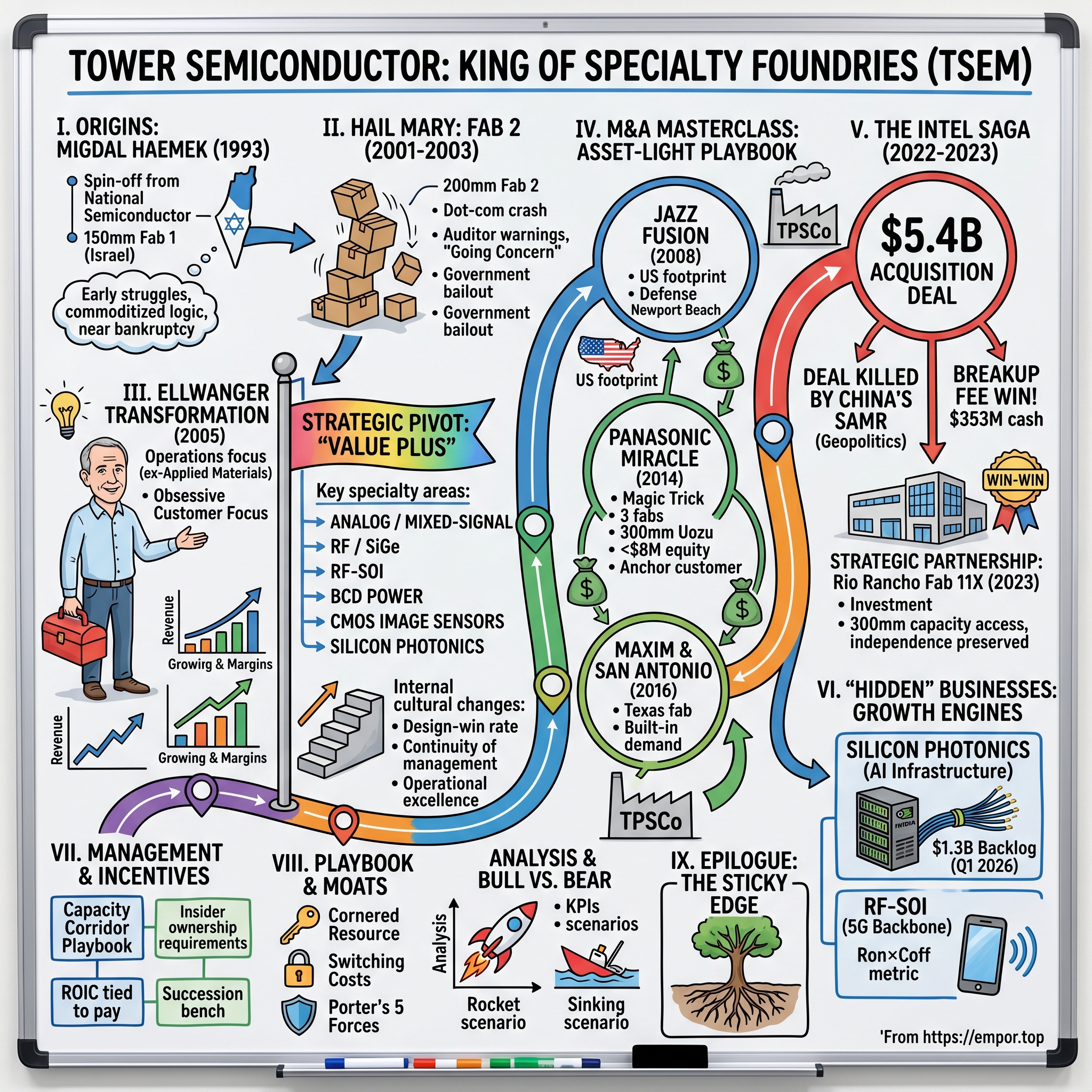

Picture a quiet industrial park on the edge of a small Israeli town called מגדל העמק Migdal HaEmek — population around 25,000, tucked into the Lower Galilee hills about an hour east of Haifa. Olive trees line the access roads. The traffic light at the entrance to the science park blinks yellow at night. And inside a windowless concrete building, in a cleanroom whose air is a thousand times purer than a hospital operating theater, a 200mm silicon wafer is being patterned with structures so small you could fit two thousand of them across the width of a human hair.

Now imagine that on a Sunday morning in February 2022, the CEO of Intel — Pat Gelsinger, the most senior figure in the American semiconductor establishment — picked up the phone and offered to buy this place for $5.4 billion in cash1. Not for the brand, not for the bleeding-edge process technology, but for what was happening inside those cleanrooms. Eighteen months later, China's antitrust regulator effectively killed the deal by simply refusing to rule on it, and Tower Semiconductor walked away — but it walked away with a $353 million breakup fee in its pocket, roughly an entire quarter of free profit deposited by Intel2.

This is the story of how a struggling 1993 spin-off from National Semiconductor, perennially on the verge of bankruptcy through the 1990s and early 2000s, transformed itself into the indispensable backbone of the analog, RF, and silicon-photonics layer of the modern chip stack — and how its CEO Russell Ellwanger turned the foundry industry's most boring "leftover" assets into one of the great asset-light capital-allocation stories of the last twenty years.

To understand Tower, you have to first understand the bifurcation of the foundry business. On one side sits 台積電 TSMC, the giant of Hsinchu, chasing Moore's Law at 3 nanometers and below, spending $40 billion a year on capex, making the GPUs that train large language models. That's the "bleeding edge." On the other side sits a quieter universe of chips that don't need to shrink — the analog amplifier in your AirPods, the power management chip in your laptop, the radio-frequency switch that lets your phone hop between 5G bands, the silicon-photonics transceiver that moves bits inside an Nvidia rack at the speed of light. None of these chips care about 3nm. Many of them are built on geometries that haven't moved in fifteen years. But they are sticky, high-margin, and impossible to substitute. This is the "specialty edge," and Tower is its king.

Three themes run through this episode. First, the asset-light M&A masterclass — how Tower acquired billions of dollars of fab capacity from National Semiconductor, Jazz, パナソニック Panasonic, and Maxim Integrated for what amounted to pocket change, by structuring every deal around a built-in customer commitment. Second, the silicon-photonics revolution — the hidden crown jewel inside Tower that few generalist investors have recognised, now sitting on $1.3 billion of contracted backlog feeding AI infrastructure[^6]. And third, the human story of Russell Ellwanger, an Applied Materials lifer who showed up in Migdal HaEmek in 2005, picked up a company that was burning cash and trading near a dollar, and turned it into a $7 billion enterprise that Intel was willing to pay a 60% premium to own1.

Our roadmap takes us from the dusty origins of Fab 1 in the Galilee, through the Jazz fusion of 2008 and the Panasonic miracle of 2014, into the Intel saga and the regulatory wall in Beijing, and finally into the AI and 5G growth engines that make Tower a 2026 story worth understanding on its own terms.

II. Origins: The Migdal HaEmek Roots

To understand why Tower exists at all, you have to rewind to the semiconductor landscape of the late 1980s. The industry was still vertically integrated. Intel, Motorola, Texas Instruments, and National Semiconductor all designed and manufactured their own chips, in their own fabs, on their own roadmaps. The "foundry" idea — that a chip company could outsource fabrication to a third party — was a radical proposition that 張忠謀 Morris Chang had just begun to commercialise in Taiwan with TSMC, founded in 1987. Nobody in 1990 was sure it would work.

In the middle of this transition sat National Semiconductor, the Santa Clara analog giant. National had set up an Israeli design and manufacturing operation in the 1980s — part of a broader wave of American semiconductor companies that came to Israel for the engineering talent left over from the country's defense industry. The crown jewel of National's Israeli footprint was a 150mm (6-inch) wafer fab nestled in מגדל העמק Migdal HaEmek, a development town that had been settled by Moroccan, Romanian, and Tunisian Jewish immigrants in the 1950s. By the early 1990s, National decided it no longer wanted to operate a foundry in Israel, and a group of local executives and Israeli investors — backed by the U.S. firm Robert Fleming — spun it out as an independent company in 1993. They called it מגדל סמיקונדקטור Tower Semiconductor, after the town's name (Migdal literally means "tower" in Hebrew).

The company went public on NASDAQ in November 1994 under the ticker TSEM. Read the prospectus today and it reads like a relic from another era: Tower was offering 0.6-micron and 1-micron CMOS processes — geometries that even by 1994 standards were already a generation behind the leading edge. The original strategy was to be a small, profitable manufacturer of commodity logic for memory companies and graphics chipmakers. Within a few years, that strategy ran into the brick wall of foundry economics: TSMC and 聯華電子 UMC in Taiwan were investing tens of billions of dollars into next-generation 200mm fabs, and Tower's single 150mm Fab 1 simply could not keep up on cost-per-wafer. By the late 1990s, Tower was losing money in nearly every quarter.

The company's response was the Hail Mary that almost killed it: in 2001, Tower broke ground on Fab 2, a 200mm facility in the same Migdal HaEmek industrial park, financed with a complicated cocktail of Israeli government grants, customer prepayments from Saifun, Macronix, and Alliance Semiconductor, and roughly $1.5 billion of bank debt. The build-out happened directly into the teeth of the dot-com semiconductor crash. By 2003, Fab 2 was operational but desperately underutilised. The company's auditors flagged going-concern doubts. The share price collapsed below a dollar. Israeli newspapers periodically wrote Tower's obituary; one headline in the Hebrew business press called it "the never-ending bailout."

What kept the company alive through this dark decade was, paradoxically, the same thing that had nearly killed it: the Israeli government's strategic interest in preserving an indigenous semiconductor manufacturing capability. Israel viewed its chip ecosystem as a national-security asset, and successive governments were willing to extend grant after grant, loan rescheduling after loan rescheduling, to keep Tower alive. The lesson of Tower's first twelve years is not one of growth — it's one of survival. By 2005, the company was still alive, but barely. The board knew it needed something more than another financing round. It needed a new operating philosophy. And so, in May 2005, they hired a soft-spoken American operations executive from Applied Materials who had never run a public company before. His name was Russell Ellwanger, and he would spend the next two decades quietly reinventing what it means to be a foundry.

III. The Ellwanger Transformation

Russell Ellwanger does not look like a typical semiconductor CEO. He doesn't have a celebrity Twitter feed. He doesn't show up at the World Economic Forum. He flies coach. Colleagues describe him as preternaturally calm — the kind of executive who, when a fab equipment alarm goes off at 2 a.m., is more likely to ask three diagnostic questions than to raise his voice. His background is in operations and process engineering, not finance. Before Tower, he spent fifteen years at Applied Materials, the equipment supplier to virtually every fab in the world, where he ran the company's CMP (chemical-mechanical planarization) division. That experience gave him something most foundry CEOs lack: a deep, hands-on understanding of how every piece of equipment in a fab actually behaves on the production floor.

When Ellwanger arrived in Migdal HaEmek in May 2005, Tower had revenue of roughly $100 million and was burning cash. Within his first hundred days, he made a decision that defined the next twenty years of the company's strategy. He looked at Fab 2 — the 200mm facility that had bankrupted the previous management — and concluded that competing with TSMC and UMC on commodity digital logic was suicide. The Taiwanese had scale Tower could never match. But there was a category of chip that the Taiwanese giants treated as an afterthought: analog and mixed-signal. These were the chips that didn't shrink with Moore's Law — power management ICs, image sensors, RF transceivers, automotive controllers. They were built on mature 180nm, 130nm, and 65nm geometries. They didn't need EUV lithography or 3nm gate-all-around transistors. What they needed was something far harder to manufacture: highly customised "process recipes" — specific combinations of materials, doping concentrations, thermal cycles, and layer stacks tuned for analog performance rather than digital density.

This was the pivot. Ellwanger rebranded the company internally around what he called the "Value Plus" strategy: don't compete with TSMC on what TSMC wants; compete in the niches TSMC ignores5. The corollary was that Tower would need to develop a portfolio of specialty process technologies — SiGe (silicon-germanium) BiCMOS for high-frequency RF, RF-SOI (RF silicon-on-insulator) for switches, BCD (bipolar-CMOS-DMOS) for power management, CMOS image sensors, and eventually silicon photonics — and license them across multiple fabs to maximise utilisation.

What made Ellwanger's transformation different from a typical strategic pivot was the cultural rewiring underneath it. He installed a metric across the company called "customer-design-win rate" and another called "utilisation by process node," and he tied compensation across the engineering and sales organisations to both. He insisted on monthly customer business reviews where every key account had a named executive sponsor. He hired a senior VP layer that, by 2026, is mostly composed of people who have been at Tower for fifteen years or more — an extraordinary continuity in an industry where talent rotates every three years. Among them are Oren Shirazi (CFO since 2005, a veteran of the company's near-death financing rounds), Marco Racanelli (running the Jazz/Newport Beach operations and the RF/SiGe franchise), and Dr. Avi Strum (the head of the Sensors and Displays Business Unit who, before joining Tower, ran imaging at STMicroelectronics).

The result of this rewiring was not visible in the income statement for years. Tower's revenue in 2005 was around $103 million; by 2010 it had crossed $500 million; by 2014 it broke $800 million; by 2019 it was at $1.3 billion, with gross margins climbing from negative territory in the mid-2000s into the high 20s and then the 30s. The line was not always smooth — the 2009 financial crisis hurt, and so did the 2019 inventory correction — but the trajectory was unmistakable. A company that had been trading for change in the mid-2000s was, by the late 2010s, worth $2 billion in market capitalisation. And it had built that value not by inventing a new technology, but by doing the operational equivalent of weightlifting in the basement every day for ten years. Which set the stage for the second part of Ellwanger's playbook: buying other people's fabs.

IV. The M&A Masterclass: Benchmarking the Assets

Here's the central insight that defines Tower's M&A philosophy: a modern 300mm fab built from scratch costs somewhere between $5 billion and $15 billion, takes 3-4 years to construct, and another 18 months to ramp to mature yields. But the world is full of perfectly good existing fabs that their owners no longer want to operate — typically because the parent company has decided to go "fab-lite," or because the fab is too small to justify continued investment by an IDM. Ellwanger looked at this landscape and asked a simple question: what if we could acquire those fabs for the cost of the working capital alone, by guaranteeing the previous owner long-term supply? This is the asset-light M&A playbook, and Tower has run it five times.

The Jazz Fusion (2008)

The first major application of the playbook was Jazz Semiconductor, a 200mm fab in Newport Beach, California, that had been spun out of Conexant (itself spun from Rockwell). Jazz was publicly traded but unloved — it had the most sophisticated SiGe BiCMOS process technology in North America (used for high-end RF and millimeter-wave applications) but lacked scale and was bleeding cash. In May 2008, Tower announced an all-stock acquisition valuing Jazz at approximately $169 million in enterprise value[^8].

The strategic logic was elegant. Jazz brought three things Tower didn't have: a US footprint (critical for defense and aerospace customers under ITAR restrictions), the SiGe process platform, and a customer book that included Skyworks, RFMD (now Qorvo), and a roster of analog incumbents. The combined entity rebranded as TowerJazz and immediately became the dominant non-IDM supplier of SiGe and RF-SOI in the world — a position that would be worth billions of dollars a decade later when 5G phones started shipping in volume. Tower didn't pay $169 million in cash; it paid in its own stock, which at the time was depressed. In effect, it bought a US fab for diluted equity that, by 2020, had recovered tenfold in value.

The Panasonic Miracle (2014)

If Jazz was a clever deal, the パナソニック Panasonic transaction was a magic trick. In December 2013, Tower announced that it had reached an agreement with Panasonic to form a joint venture called Tower Partners Semiconductor Co. (TPSCo). Tower would take 51% of the new entity. In exchange for that controlling stake, it would contribute approximately $7.6 million in equity4. In return, TPSCo received the operating control of three Japanese fabs — in 砺波 Tonami, 北陸 Hokuriku (Arai), and 魚津 Uozu — including a 300mm (12-inch) facility at Uozu. Three fabs. One of them 300mm. For roughly $8 million in cash equity.

To benchmark this: at the time, building a single 300mm fab from greenfield would have cost between $5 billion and $10 billion. Tower acquired controlling operational rights to three existing, fully-staffed, fully-equipped facilities — with hundreds of millions of dollars of annual capacity already qualified — for less than the cost of a Manhattan apartment building. The economics work because Panasonic, the seller, was simultaneously contracted to be the anchor customer. Panasonic committed to a five-year, take-or-pay supply agreement that guaranteed TPSCo a baseline of wafer purchases, ensuring immediate fab utilisation. Panasonic got its captive supply and was relieved of the operational and capital burden of running fabs that were strategic but no longer core. Tower got the 300mm capacity it needed to scale into AI and high-performance analog. Both sides won — but Tower won asymmetrically.

The TPSCo deal is, in this author's view, one of the greatest single capital-allocation moves in modern semiconductor history. It is to fab M&A what Buffett's 1972 See's Candies deal was to consumer M&A: a small dollar amount that unlocked a multi-decade compounding asset.

Even better, the deal contained an option for Tower to eventually buy out Panasonic's stake — an option that Tower exercised more than a decade later. In February 2026, Tower announced it had agreed to acquire 100% of the Uozu 300mm fab from Panasonic, taking full ownership of the crown jewel of the original JV[^5]. The path from a $7.6 million minority option in 2014 to full ownership of a 300mm fab in 2026 traces the entire arc of Tower's playbook.

The Maxim and San Antonio Add-Ons

In subsequent years, Tower deployed the same template at a smaller scale. It acquired Maxim Integrated's San Antonio, Texas, 200mm fab in 2016 for a similar structure: nominal consideration, long-term supply contract back to Maxim. Every acquisition came with a "built-in customer" anchor that guaranteed the new fab would not sit idle. This is the operational genius of Tower's M&A — they don't acquire fabs to find customers. They acquire customers, and the fabs come bundled in.

The cumulative effect was that by 2022, Tower operated fabs in Israel (Migdal HaEmek), California (Newport Beach), Texas (San Antonio), and Japan (Tonami, Hokuriku, Uozu), spanning 150mm, 200mm, and 300mm wafer sizes, with combined annual revenue capacity of over $2 billion. This footprint is what attracted Intel.

V. The Intel Saga: $5.4B and the Breakup Fee

On Tuesday, February 15, 2022, Tower Semiconductor's board approved a deal that, had it closed, would have been the largest M&A transaction in the history of Israel's semiconductor industry. Intel, under newly-returned CEO Pat Gelsinger, announced that it would acquire Tower for $53 per share in cash, valuing the company at approximately $5.4 billion1. Gelsinger's "IDM 2.0" strategy required Intel to build a credible third-party foundry business — the Intel Foundry Services division — and Tower offered exactly what Intel lacked: a customer book of hundreds of analog and specialty fabless companies, a portfolio of mature-node specialty processes, and an executive bench that knew how to run a foundry for external customers (something Intel, after thirty years of serving only itself, had no muscle memory for).

The deal premium was striking. Tower's stock had closed at $33.13 the previous Friday; the $53 offer represented a 60% premium. Tower's shareholders approved the transaction in June 2022 by an overwhelming margin. The deal then needed regulatory clearance in a half-dozen jurisdictions: the United States, the European Union, Japan, South Korea, Taiwan, and crucially, China. Most of those approvals came through within months. China did not.

China's antitrust regulator is called 国家市场监督管理总局 SAMR — the State Administration for Market Regulation. SAMR has the authority to approve, conditionally approve, or reject mergers that involve revenue thresholds in China. In the Tower-Intel case, SAMR did something far more elegant than rejection: it simply did nothing. Month after month, the deal sat in SAMR's review queue with no formal communication. The geopolitical context made the silence deafening. Through 2022 and 2023, US-China relations on semiconductors deteriorated dramatically: the Biden administration's October 2022 export controls, the CHIPS Act, the curtailing of US tool sales to SMIC and YMTC. SAMR's pattern of slow-walking US-acquirer deals (it had previously stalled the Qualcomm-NXP merger to death in 2018) suggested that Tower-Intel was the next chip-industry M&A casualty of the geopolitical standoff7.

The Tower-Intel merger agreement contained an outside date — a deadline by which the deal had to close, or either party could walk. That deadline was August 15, 2023, with a one-time extension option. As August 2023 approached, it became clear that SAMR was not going to act. On August 16, 2023, Intel announced the termination of the agreement2. Per the terms of the merger contract, Intel paid Tower a $353 million termination fee in cash, deposited within days. For Tower shareholders, the deal failure was a bitter pill — eighteen months of management distraction, customers wondering whether their supplier would soon belong to a competitor, and the $53 share price evaporating overnight (the stock closed at $33.78 the day of termination, down nearly 11%).

But Ellwanger refused to let the failed deal be a pure loss. Within weeks, he was on the phone with Intel negotiating what he called the "consolation prize." On September 5, 2023, Tower and Intel announced a strategic partnership in which Tower would invest up to $300 million to install its own equipment inside Intel's Fab 11X in Rio Rancho, New Mexico, gaining access to 300mm fab capacity for Tower's 65nm Power Management process[^3]. In effect, Tower acquired the right to use part of Intel's New Mexico facility — getting the 300mm capacity it would have gotten from the merger, but without buying the company and without diluting its capital structure.

Think about the genius of this outcome for a moment. Tower: 1. Received $353 million in cash from Intel for the failed deal (effectively a free quarter of operating profit). 2. Got 300mm fab capacity in the US through an asset-light arrangement. 3. Retained its independence and full ownership of its franchise. 4. Spent eighteen months in due diligence with the best customer audit imaginable — a $5.4 billion acquirer kicking every tire — and emerged with its specialty thesis intact.

When historians of capital allocation look back at 2023, the Intel-Tower outcome will read as one of the most asymmetric "loss" outcomes in M&A history. Tower's customers, who had quietly worried about Intel ownership for eighteen months, came back to the table immediately with expanded orders. Within a year, Tower's order book was the strongest it had ever been — driven by a quiet revolution in AI infrastructure that the public market still did not fully appreciate.

VI. 'Hidden' Businesses: The AI & 5G Growth Engines

If you talk to a generalist tech investor about "AI infrastructure" in 2026, the names that come up first are Nvidia, Broadcom, AMD, TSMC, and possibly Marvell. Almost nobody mentions Tower. And yet, when you crack open the spec sheet of a modern AI rack — say, the optical interconnects shuttling data between accelerator cards at speeds that would make a 2018 datacenter engineer weep — you find Tower's fingerprints in places you didn't expect.

Silicon Photonics: The Hidden Crown Jewel

The fundamental problem of modern AI compute is not the compute itself. It's moving data between compute elements. A GPU rack can do trillions of math operations per second, but if it can't shuttle the resulting numbers to the next GPU fast enough, all that compute capacity sits idle. Copper wire, the workhorse of electronic interconnect for half a century, hits a hard physical wall above a few tens of gigabits per second over more than a meter or so. Beyond that, you have to switch to light — optical interconnect, where the data is encoded as photons traveling through glass fibers.

Historically, the optical transceivers that performed this electrical-to-optical conversion were built from compound semiconductors like indium phosphide (InP) — exotic, expensive, and hard to manufacture at the volumes required for hyperscaler data centers. Silicon photonics is the technological insight that you can build the same optical functions — modulators, photodetectors, waveguides — using standard silicon CMOS processes, modified with a few extra steps. Once you can build photonics on silicon, you can leverage the entire $500 billion silicon manufacturing ecosystem to drive cost down at volume.

Tower has been quietly building silicon-photonics process platforms for over a decade. The company offers a PH18 silicon-photonics process — a 180nm-based platform — used by major optical transceiver vendors to fabricate the photonic ICs inside 800G, 1.6T, and now 3.2T transceivers. In the past three years, the silicon photonics business has moved from "interesting niche" to "indispensable AI infrastructure layer." On its Q1 2026 earnings call, Tower disclosed that its silicon photonics order book had reached $1.3 billion in contracted future revenue, with customer prepayments funding significant capacity expansion ahead of demand[^6]. That backlog represented more than a full year of incremental revenue stacked on top of the existing $1.5 billion-plus annual run rate. Customers were essentially saying: take our money now, and lock in the capacity, because we cannot afford to miss it.

In layman's terms: every Nvidia GB200 rack shipped, every hyperscaler datacenter buildout, every next-generation AI training cluster has, somewhere inside it, a silicon-photonics transceiver. And a meaningful share of those transceivers contains silicon dies fabricated by Tower. The investor question is not whether the SiPho revenue ramp will continue — the prepayment-backed backlog answers that. The question is whether Tower's specialty process moat in this segment is durable against the inevitable competitive response from TSMC, GlobalFoundries, and STMicroelectronics. So far, the answer appears to be yes, because the recipe — the precise combination of photonics-specific layers, modulator structures, and germanium photodetectors integrated into a 200mm SiGe BiCMOS platform — is not something that can be cloned by reading a paper.

RF-SOI and the 5G Backbone

The other "hidden" business is RF-SOI — radio-frequency silicon-on-insulator. Every modern smartphone contains an RF front-end module that switches the device's antennas between dozens of different cellular bands (LTE bands, 5G sub-6, 5G mmWave, Wi-Fi, Bluetooth, GPS, UWB). The "switch" at the heart of this front-end is built on RF-SOI silicon. Tower is the dominant non-captive supplier of RF-SOI to the major RF front-end vendors — Qorvo, Skyworks, and Broadcom — and has been since the Jazz acquisition brought the SiGe and RF franchise into the fold. A 2021 Bloomberg feature on the 5G supply chain called Tower "the unsung hero of the 5G rollout"6.

The technical metric that matters here is called Ron×Coff (on-resistance times off-capacitance), a figure of merit for RF switch quality. Lower Ron×Coff means lower insertion loss and better antenna selectivity. Tower's process technology has consistently led the industry on this metric, which is why even when Chinese RF-SOI fabs come online with lower prices, the high-end design wins continue to flow to Tower's Newport Beach and Migdal HaEmek lines.

Segment Breakdown

For investors trying to model Tower, it helps to think of the business in two roughly equal halves. The first is the high-margin specialty layer — silicon photonics, RF-SOI, SiGe, BCD power management — disproportionately running on 200mm specialty lines and increasingly on 300mm at Uozu and Intel Rio Rancho. This is the growth engine. The second is the legacy industrial and automotive layer — discrete power devices, CMOS image sensors for industrial cameras, and mature analog — running on the older 150mm and 200mm lines. This part of the business is cyclical, lower-margin, and growing slowly, but it provides the cash flow that funds capacity expansion in the high-growth segments.

The bridge from a $1.5 billion run-rate revenue business to whatever Tower becomes in five years runs through silicon photonics and 300mm capacity. The bridge runs through people who decided, a decade ago, that the future of AI infrastructure was going to need light, and that light was going to need silicon. Which brings us to the management bench that decided that.

VII. Management, Incentives, & Shareholding

In a typical foundry, the CEO is a process engineer who graduated through the technical ranks. In Tower's case, Russell Ellwanger fits that mold — but with the unusual twist that his core formative experience was outside any single fab. At Applied Materials, his job was to make the equipment that the world's fabs depended on work better, faster, and at higher yields. He has, in some sense, seen the inside of every major fab in the world. When he negotiates with customers, he understands their cost structure in granular detail. When he visits a TPSCo fab in Japan, he can debate tool engineers on the optimal CMP slurry chemistry. This operational fluency, combined with what colleagues describe as obsessive customer focus, is the closest thing Tower has to a single point of competitive advantage at the leadership layer.

The Capacity Corridor Playbook

Ellwanger has articulated his strategy in shareholder letters and earnings calls under the rubric of "Capacity Corridors"5. The idea is that Tower commits to a multi-year capacity expansion in a specific specialty process — say, silicon photonics on 300mm — only when it has secured multi-year customer commitments (often with prepayments) covering the bulk of that incremental capacity. This avoids the boom-bust capex cycle that has destroyed value at less disciplined foundries. When you read Tower's annual capex disclosure, you should not think of it as speculative investment. You should think of it as a hedged contract: the dollars are committed only after customer dollars are committed first. The Intel Rio Rancho $300 million investment, the Uozu 300mm buyout, and the silicon-photonics capacity additions all follow this template.

Incentive Architecture

Tower's 2025 proxy statement, filed with the SEC, lays out a compensation philosophy that aligns management with long-term shareholder outcomes in a way that is unusual for an Israeli-incorporated company3. CEO Ellwanger is required to maintain a stock ownership position of at least 3x his base salary. Other named executive officers face proportional requirements. Long-term equity incentives are tied to multi-year performance metrics including Return on Invested Capital (ROIC) and capacity utilisation milestones — not just stock price appreciation. The result is that when you look at insider holdings, the senior team owns meaningful equity, accumulated through years of grants and open-market purchases, and they hold it.

Just as important as what's incentivised is what's not incentivised. There are no rich severance "golden parachutes" tied to a change of control. There is no perk culture — no corporate jet, no executive dining room, no extravagant relocation packages. The proxy reads like a document written by people who genuinely think of themselves as stewards of shareholder capital, not as plenipotentiaries. In an industry where it is depressingly common to see CEOs of $5 billion enterprises rewarded with $30 million annual pay packages, Ellwanger's total compensation has historically tracked a fraction of his US peers.

The Shadow Bench

If Tower has a hidden risk, it is succession. Ellwanger has been CEO for over two decades, and while his energy remains undiminished, no public company can rely indefinitely on a single individual. The reassurance comes from the depth of the senior VP layer. CFO Oren Shirazi has been with the company since 2005. The Newport Beach franchise has been run by Marco Racanelli for over a decade. Avi Strum runs Sensors and Displays. Rafi Mor leads R&D. The average tenure of the senior leadership team is well over fifteen years — meaning the institutional memory of every key customer relationship, every process recipe, every capacity expansion decision is held by a group of people who have been at the company long enough to have internalised the Ellwanger operating philosophy. When the succession event eventually comes, it should be an internal handoff rather than an outside hire, and the playbook is well-documented enough to survive a single retirement.

The board itself has been quietly upgraded over the past five years, adding directors with deep semiconductor and capital-markets experience. The corporate governance is not flashy, but it is solid — which is exactly the profile that an investor should want from a $7 billion specialty foundry. With management aligned, the question becomes: how durable is the underlying business model?

VIII. Playbook: Porter's 5 Forces & 7 Powers

Strategy frameworks are usually applied to businesses retrospectively, as marketing tools by consulting firms. In Tower's case, the frameworks are unusually illuminating, because Tower has structured itself almost mechanically around the concept of durable competitive advantage in specialty foundry.

Hamilton Helmer's 7 Powers Lens

Cornered Resource — Process Recipes: Tower's proprietary process technologies in SiGe BiCMOS, RF-SOI, BCD power management, and silicon photonics constitute a cornered resource in the strictest sense. A "process recipe" is the documented sequence of hundreds of unit-process steps — implant doses, thermal cycles, deposition layer thicknesses, lithography reticles, etch chemistries — that produces a specific chip behavior on a specific platform. These recipes are developed over years of iteration, embedded in proprietary documentation, tied to specific tool configurations, and qualified by individual customers across hundreds of products. A competitor could in theory replicate them, but the time and capital cost is so high that nobody bothers — they instead try to build different recipes from scratch, which means they cannot serve the existing customer designs that have been qualified on Tower's recipes. The moat is real.

Switching Costs — Qualification Cycles: In automotive and aerospace customer programs, a single chip qualification can take 24-36 months. The customer's engineering team must run electrical characterisation, reliability burn-in, automotive-grade temperature cycling, ESD testing, and PPAP (Production Part Approval Process) documentation, all tied to a specific foundry process. Once qualified, that part is locked to that fab for the entire product lifecycle, which in automotive can be 10-15 years. The cost of resourcing — taking the design to a different fab — is so prohibitive that customers do it only under extreme duress. This is why Tower's automotive and industrial revenue base is so sticky.

Process Power — Operational Excellence: This is the muscle that Ellwanger has built over twenty years. Running a high-mix, low-volume specialty fab at high utilisation requires operational sophistication that exceeds what is needed at a high-volume commodity fab. Tower's fabs typically run hundreds of distinct process flows across thousands of distinct product codes simultaneously. The scheduling, planning, and equipment-time-allocation problem is mathematically harder than what TSMC faces in its high-volume 7nm and 5nm fabs. Tower has built proprietary scheduling systems and quality management processes that have, over time, allowed it to operate these complex fabs at utilisation rates and yields that match its IDM peers — a feat that less disciplined specialty foundries have not achieved.

Scale Economies — Limited but Real: Tower's scale advantages are not absolute (TSMC dwarfs Tower in total wafer output) but are real within the specialty foundry universe. Tower's R&D spending, spread across its multi-process portfolio, is funded by a $1.5 billion-plus revenue base. A smaller specialty foundry simply cannot afford to maintain the same R&D investment, which means its process recipes fall behind on each generation. The result is a slow consolidation of specialty foundry volume toward Tower (and a handful of peers like GlobalFoundries and Vanguard).

Porter's 5 Forces

Threat of New Entrants — Low. Building a new specialty fab from greenfield requires $5-15 billion of capital, 3-4 years of construction, and a decade of customer-qualification cycles. Nobody has done it from scratch in twenty years. The only "new" specialty foundries are those carved out of existing IDMs (Tower's playbook).

Bargaining Power of Suppliers — Moderate. Tool suppliers (Applied Materials, Lam Research, ASML, Tokyo Electron) have leverage on equipment pricing, but the absence of EUV requirements means Tower is not held hostage by ASML's monopoly the way leading-edge fabs are.

Bargaining Power of Customers — Moderate but offset by switching costs. Large customers like Skyworks or Qorvo represent meaningful revenue concentration, but the qualification lock-in means they cannot easily resource.

Threat of Substitutes — Low to Moderate. The technical substitutes for specialty silicon (e.g., GaN, SiC, InP for specific applications) are growing in some niches but cannot displace silicon photonics or RF-SOI in their core domains.

Industry Rivalry — Moderate. GlobalFoundries (GFS), 聯華電子 UMC, 世界先進 Vanguard International Semiconductor (VIS), and SMIC all compete in specialty foundry, but each has different sub-segment strengths. Direct head-to-head competition is rare.

Taken together, the strategic position is robust. Tower is not a winner-take-all monopolist; it's a sustainable oligopolist in a structurally attractive niche of the broader foundry industry. Which leads us to the question every investor must ultimately ask: what's it worth, and what could go wrong?

IX. Analysis & Bull vs. Bear Case

Before walking through the bull and bear, it's worth puncturing a common myth about Tower. The myth — repeated in dozens of sell-side notes and casual investor conversations — is that Tower is "a TSMC for analog" and should therefore trade at TSMC-like multiples. The reality is more nuanced. Tower is a specialty foundry, not a general-purpose foundry. Its growth profile is more idiosyncratic — driven by specific platform ramps (silicon photonics today, perhaps GaN-on-silicon tomorrow) rather than by Moore's Law tailwinds. Its margins are structurally lower than TSMC's leading-edge margins (because it doesn't have node-leadership pricing power) but structurally higher than commodity 200mm foundries. The right peer set is GlobalFoundries, Vanguard, and the specialty divisions inside UMC — not TSMC.

Bull Case

The bull case rests on three pillars.

First, the AI infrastructure tailwind via silicon photonics. The $1.3 billion SiPho backlog announced in Q1 2026[^6] reflects a multi-year demand profile that the company can fulfill only by adding meaningful 300mm capacity. As that capacity comes online — through Uozu, through Intel Rio Rancho, and through future expansions — Tower's revenue mix shifts toward higher-margin 300mm specialty product, which should expand gross margins from the low-30s into the mid-30s and potentially the high-30s. If this thesis plays out, Tower transitions from being valued as a cyclical specialty foundry to being valued as an AI-adjacent infrastructure name. Within the AI infrastructure complex, Tower currently trades at a fraction of the EV/sales multiples of Nvidia, Broadcom, or even TSMC.

Second, the 5G/RF-SOI demand resilience. Smartphone unit growth is slow, but the RF content per phone keeps rising as more bands and more carrier-aggregation combinations come online. Tower's dominant share in RF-SOI means that, even in a flat smartphone unit environment, its RF revenue should grow modestly. And the next big content-per-device step — RF for satellite-to-cellular (NTN) and direct-to-device satellite communications — represents incremental demand that is just starting to flow to Tower's customers.

Third, management discipline. Twenty years of disciplined capital allocation, two decades of M&A executed at favorable prices, a leadership team that owns meaningful equity, and a balance sheet strengthened by the $353 million Intel breakup fee mean the optionality for shareholders is asymmetric. Even if growth slows, the downside is cushioned by ROIC discipline.

Bear Case

The bear case is equally coherent.

First, geopolitical concentration. Tower's headquarters and primary R&D base are in Israel, with significant operations in Migdal HaEmek. The Israeli geopolitical environment has been volatile since October 2023, and while Tower's fabs have continued to operate uninterrupted, the perceived risk premium attached to Israel-based industrial assets has risen. A material escalation of regional conflict — or a disruption to Israeli labour availability — would directly affect operations.

Second, smartphone cyclicality. The RF-SOI business is exposed to smartphone unit volumes, which are mature in the West and increasingly competitive in China. A multi-year downturn in smartphone shipments would hit a meaningful slice of Tower's revenue.

Third, competitive response in silicon photonics. The $1.3 billion backlog has put a target on Tower's back. TSMC, GlobalFoundries, and STMicroelectronics are all investing in their own silicon-photonics platforms. The question is whether Tower's first-mover advantage, customer-qualification lock-in, and process moat are enough to defend its share as the SiPho market scales from $2 billion of TAM today to perhaps $10 billion+ later this decade.

Fourth, customer concentration. While Tower has hundreds of customers, the top ten account for a substantial share of revenue, and a single major customer redirecting volume to an internal fab or alternative supplier would meaningfully impact financials.

Competitive Benchmarking

Among public-market peers, GlobalFoundries is the closest comparator — a former IDM (AMD's manufacturing arm, plus IBM's old fab assets) now repositioned as a specialty foundry, with strong RF-SOI franchise and a US/Singapore/Germany footprint. GFS is larger but less focused on the cutting-edge specialty applications (silicon photonics in particular). 聯華電子 UMC competes in mature-node specialty but is more diversified into commodity logic. 世界先進 Vanguard (VIS), the Taiwanese specialty foundry partially owned by TSMC, competes in power management and display drivers but lacks the SiGe and SiPho franchise. In overall positioning, Tower has the most concentrated exposure to the AI-adjacent specialty layer.

The KPIs That Matter

For investors tracking Tower over the coming years, three KPIs are worth watching closely:

- Silicon-photonics revenue and backlog progression — the single largest growth driver, and the variable most likely to surprise (in either direction). Track the contracted backlog figure quarter-over-quarter, the pace of customer prepayments, and management commentary on capacity ramp timing.

- 300mm revenue mix as a percentage of total revenue — the cleanest indicator of structural margin expansion. As 300mm specialty revenue rises through the Uozu and Intel Rio Rancho ramps, gross margin should follow.

- Return on Invested Capital (ROIC) — the discipline metric. Specialty foundry success is ultimately measured not by revenue growth but by capital efficiency. ROIC trending up signals that capex is being deployed against properly-contracted demand; ROIC trending down would signal a Capacity-Corridor breakdown.

The case for Tower in 2026 is fundamentally a case about discipline meeting opportunity. The opportunity — AI-driven optical interconnect demand — is undeniably here. The question is whether Tower's management can continue to convert it into shareholder value with the same patience and rigor that they have demonstrated for the past two decades.

X. Epilogue & Final Reflections

There's a phrase that comes up repeatedly in Russell Ellwanger's letters to shareholders: "the sticky edge." It's his shorthand for the part of the semiconductor universe that Tower lives in — not the bleeding edge of 3nm and 2nm, where TSMC and Samsung battle for trillion-dollar revenue pools, but the sticky edge of analog, RF, and photonics where the customer relationships compound over decades and the moats are built one process recipe at a time.

In a way, Tower is the anti-TSMC. TSMC wins by being ahead — by shipping the next node six months before anyone else, by having more EUV machines than anyone else can afford, by being the only place on earth where the most advanced GPU in the world can be built. Tower wins by being patient — by having the same engineers working on the same customer accounts for fifteen years, by spending less money on capex than competitors do but spending it more wisely, by acquiring fabs nobody else wanted at prices nobody else would believe.

The story of Tower, told over two hours, is fundamentally a story about how patient capital allocation, an unromantic focus on operational excellence, and the unsexy art of finding niches that giants ignore can compound into a $7 billion enterprise. From a 1993 spin-off that nobody outside Migdal HaEmek had heard of, to a 2022 acquisition target for the United States' most strategically important semiconductor company, to a 2026 backbone of the AI infrastructure supply chain — the arc is a quiet one. There are no founder mythologies, no garage origin stories, no Steve Jobs-style charisma. There is just a CEO who flies coach, a senior team that has worked together for two decades, and a portfolio of process recipes that, taken together, constitute one of the more durable moats in modern semiconductors.

For long-term investors, the question Tower presents is one that recurs throughout the history of capital allocation: do you back the bleeding edge, with its winner-take-all dynamics and astronomical capex, or do you back the sticky edge, with its compounding customer relationships and asymmetric M&A optionality? Acquired.fm doesn't make recommendations. But the existence of Tower — and its twenty-year track record — is evidence that the sticky edge can be a remarkably good place to deploy capital, if you know how to find the recipes and the people who guard them. The next chapter is being written right now, in cleanrooms in Migdal HaEmek, Newport Beach, San Antonio, and 魚津 Uozu, where the photons that move tomorrow's AI training data are being patterned onto silicon, one wafer at a time8.

References

-

Tower Semiconductor Investor Relations — 20-F and Annual Reports ↩↩↩

-

Intel Announces Termination of Tower Semiconductor Acquisition — Intel Newsroom, 2023-08-16 ↩↩

-

Tower Semiconductor's TPSCo JV with Panasonic — Reuters, 2013-12-20 ↩

-

Russell Ellwanger on the "Value Plus" Strategy — Seeking Alpha Transcripts, Q1 2026 ↩↩

-

Tower Semiconductor: The Unsung Hero of the 5G Rollout — Bloomberg News, 2021-11-10 ↩

-

China's SAMR and the Blocked Intel-Tower Deal — Financial Times, 2023-08-17 ↩

-

Tower Semiconductor Quarterly Results — Calcalist, 2026-05-15 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube