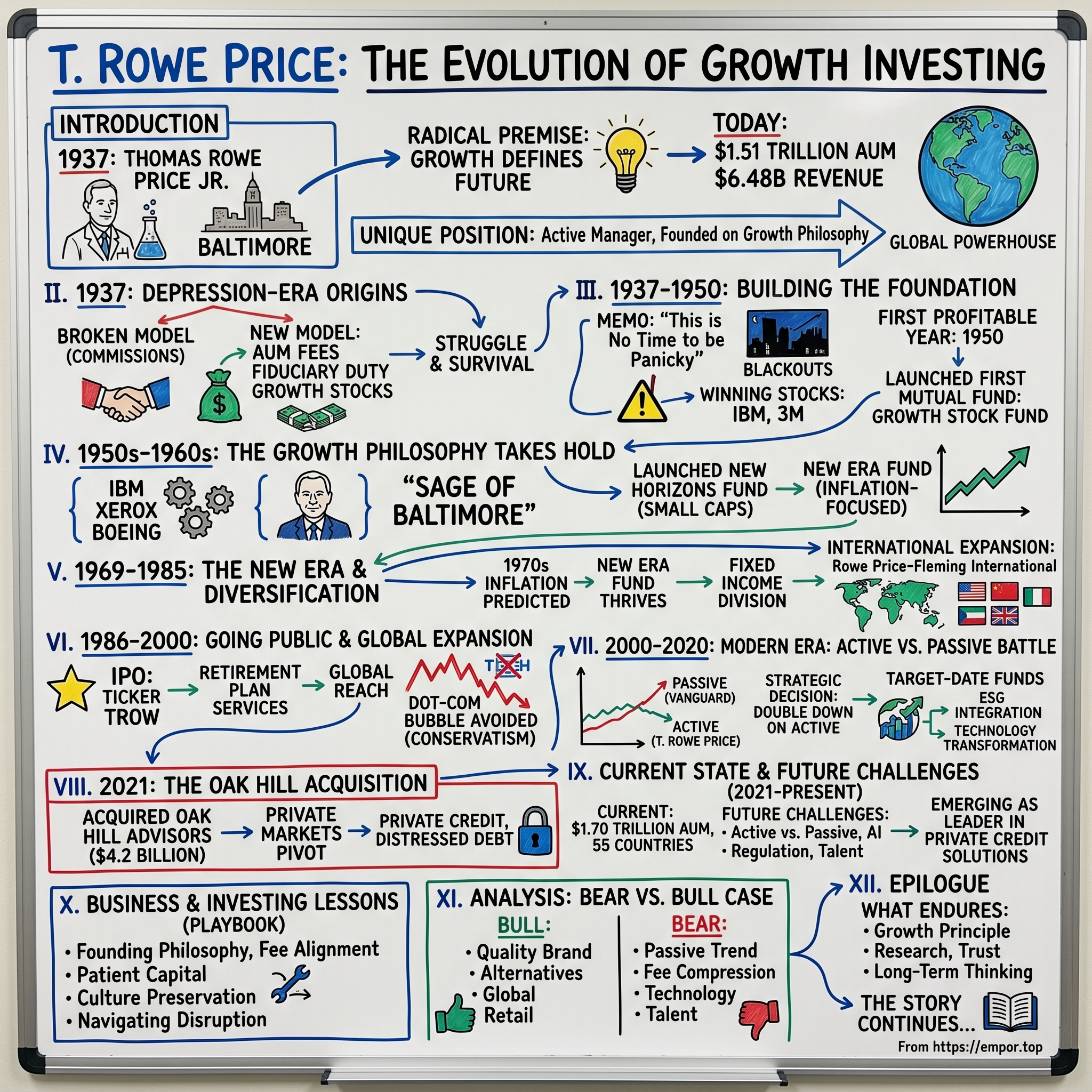

T. Rowe Price: The Evolution of Growth Investing

I. Introduction & Episode Roadmap

Picture Baltimore in 1937: breadlines stretch around corners, banks shutter their doors, and the Dow Jones has lost 89% of its value from its 1929 peak. In a modest office at 10 Light Street, a 38-year-old chemist-turned-financier named Thomas Rowe Price Jr. is doing something that seems utterly insane—he's starting an investment firm. Not just any investment firm, but one built on a radical premise: that growth, not value, would define the future of investing.

Fast forward to today: T. Rowe Price manages $1.51 trillion in assets, generates $6.48 billion in annual revenues, and serves millions of clients across 55 countries. The company that started with a handful of Baltimore families as clients now runs retirement plans for Fortune 500 companies and manages sovereign wealth. It's a transformation that spans nearly nine decades, multiple financial crises, and the complete reimagining of what asset management means.

But here's what makes this story particularly fascinating: T. Rowe Price isn't BlackRock or Vanguard. It didn't win by being first to indexing or by rolling up competitors through mega-acquisitions. Instead, it carved out a unique position as the thinking person's active manager—a firm that somehow maintained its founding philosophy of growth investing while scaling to compete with trillion-dollar giants.

The journey from that Depression-era startup to today's global powerhouse reveals fundamental truths about building enduring financial institutions. It's a story of prescient bets (like calling the 1970s inflation a decade early), painful miscalculations (missing the early indexing wave), and strategic pivots (the recent $4.2 billion Oak Hill acquisition marking its entry into private markets).

Most importantly, it's a story about timing and philosophy. Thomas Rowe Price Jr. didn't just pick stocks differently—he reimagined the entire relationship between money managers and their clients. No commissions. No loads. Just aligned incentives through assets under management fees. In 1937, this was heretical. Today, it's the industry standard.

As we trace this evolution, we'll explore how a Baltimore boutique became "the father of growth investing," why it chose to double down on active management when the world was going passive, and whether its recent push into alternatives represents visionary strategy or desperate adaptation. The central question threading through this narrative: In an age of algorithms and index funds, can a firm built on human judgment and long-term thinking not just survive, but thrive?

The answer, as we'll see, lies not in T. Rowe Price's size or performance metrics, but in understanding how founding principles can both constrain and liberate a company across generations. From Thomas Rowe Price Jr.'s first client meeting in 1937 to today's AI-powered investment platforms, this is the story of how patient capital and contrarian thinking built one of America's last independent asset management giants.

II. The Depression-Era Origin Story (1937)

The mahogany-paneled offices of MacKubin, Legg and Company hummed with nervous energy in early 1937. Baltimore's financial district—such as it was—occupied a handful of buildings near the Inner Harbor, where the smell of coal smoke mixed with salt air from the Chesapeake. Inside the brokerage that would later become Legg Mason, partners huddled over ticker tape while clients called in panicked orders. The market had recovered somewhat from its 1932 lows, but nobody trusted it. Nobody, that is, except Thomas Rowe Price Jr., who at 38 years old was about to walk away from it all.

Price had spent the 1920s as an entry-level researcher and account manager at various Baltimore brokerages, watching the market's spectacular rise and catastrophic fall from a front-row seat. Born in 1898 in rural Maryland, he'd studied chemistry at Swarthmore before discovering his true passion lay in dissecting balance sheets, not chemical compounds. His analytical mind, trained in scientific method, saw patterns others missed. While his colleagues chased yesterday's winners, Price noticed something profound: companies that consistently grew their earnings eventually saw their stock prices follow, regardless of market cycles. But by the mid-1930s, Price had risen to the head of investment for MacKubin, Legg and Co., yet found himself continually clashing with his colleagues who focused on commission-based value investing. The tension wasn't just philosophical—it was ethical. Price watched brokers churn accounts to generate commissions, pushing clients into trades that enriched the firm but impoverished the investor. He'd seen it destroy families during the crash. The model was broken, and everyone knew it, but nobody wanted to fix it because broken was profitable.

Price's path to finance had been circuitous: he started as a chemist at Fort Pitt Enamel, lost that job when the factory went on strike and the bank ceased financing. He joined DuPont as an industrial chemist, where he began reading business publications and developed a love for stocks—only to be laid off again when DuPont's profits nosedived. Two jobs, two layoffs, all before age 25. It was this experience of economic volatility that would shape his investment philosophy: find companies that could grow through any cycle.

The breaking point at MacKubin came in early 1937. While heading the Investment Counseling Department, Price's principles clashed decisively with the firm's commission-based approach. He believed in the client's best interests, advocating for annual fees instead of commissions. His partners thought he was insane. Why give up guaranteed transaction fees for the uncertainty of management fees? In the depths of the Depression, with trading volumes at historic lows, Price was proposing to tie their fortunes directly to their clients' success.

With three other colleagues from MacKubin in tow, Price set out to form his own firm, which he established in 1937 and named T. Rowe Price and Associates. The firm was originally headquartered at 10 Light Street and staffed by this small pool of associates who had left MacKubin, Legg and Co. along with Price.

The timing seemed catastrophic. The market had just suffered another sharp correction in March 1937. Banks were still failing. Unemployment hovered near 15%. Yet Price saw opportunity where others saw disaster. He recognized that the largest fortunes in the country had been created by owning growing businesses. Not trading them, not timing them, but owning them through their growth cycles.

When he founded T. Rowe Price & Associates in 1937, his firm diverged from the norm in three major ways: charging fees based on assets under management rather than sales volume, maintaining a fiduciary duty to clients, and focusing on growth stocks rather than the value investing that dominated Depression-era thinking. This wasn't just a new firm—it was a new model for the entire industry.

Price's vision was deceptively simple yet revolutionary: focusing on investing during a company's early growth phase and emphasizing fundamental research. He believed that identifying companies with sustainable earnings growth—even if they traded at higher multiples than traditional value stocks—would generate superior long-term returns. In 1937, with the Dow still 60% below its 1929 peak, this was borderline heretical.

Price's ethos was straightforward: "If you treat the customer right, he will reward you in the long term". No loads, no commissions, no conflicts. Just aligned incentives through a simple fee on assets managed. If clients prospered, the firm prospered. If they suffered losses, the firm suffered too. It was capitalism at its most elegant.

The early days were brutal. Initially a very small firm focused on wealth management and private investment accounts for Baltimore-area families, the company struggled during the Great Depression and World War II. But Price had something his competitors lacked: conviction born from scientific training and personal experience. He'd survived two layoffs, witnessed the market's greatest crash, and emerged with a theory about how wealth was actually created.

As 1937 turned to 1938, with war clouds gathering in Europe and the American economy sliding back into recession, Thomas Rowe Price Jr. was building something that would outlast them all. He didn't know it yet, but he was laying the foundation for what would become a trillion-dollar enterprise—all from a modest office overlooking Baltimore's Inner Harbor, with a handful of clients and a revolutionary idea about how investing should work.

III. Building the Foundation: Struggle & Survival (1937–1950)

The letter arrived on a humid Baltimore morning in September 1939, just as German tanks rolled into Poland. Thomas Rowe Price Jr. sat at his desk at 10 Light Street, watching the harbor through windows streaked with salt spray, and composed what might have been his firm's epitaph. Two weeks after Germany kicked off WWII by invading Poland, and just two years after founding T. Rowe Price, Thomas wrote a memo to clients titled "This is No Time to be Panicky".

The timing was almost poetic in its difficulty. T. Rowe Price was less than two years old, and clients would not be unreasonable to want to pull their investments from this fledgling firm. Here was Price, having convinced a handful of Baltimore families to trust him with their wealth based on an untested philosophy, now facing the ultimate test: another world war layered atop an incomplete economic recovery. But in that 1939 letter, Price revealed the steel beneath his genteel Baltimore manner. "This is No Time to be Panicky," he titled the memo, cautioning his clients from getting too worked up over forecasts. He laid out what they didn't know, what they did know, and what they believed, before ending with ideas on how to manage investments through uncertain times and prepare for future opportunities. It was masterful client communication—acknowledging fear while projecting confidence, admitting uncertainty while maintaining conviction.

The war years tested every aspect of Price's philosophy. Initially a very small firm focused on wealth management and private investment accounts for Baltimore-area families, the company struggled during the Great Depression and World War II before gaining solid footing at the end of the 1940s. But struggle conceals the daily reality: Price and his small team working 14-hour days, analyzing companies by candlelight during blackouts, writing research reports while Baltimore's shipyards worked round-the-clock building Liberty ships.

Baltimore itself transformed during these years. The advent of WWII changed Baltimore drastically and caused a commercial boom that increased housing and labor demand in all sectors of the city. After Pearl Harbor, Baltimore became a twenty-four-hour city, living according to the peculiar rhythms of shift work. For T. Rowe Price & Associates, this meant opportunity—defense contractors needed capital, workers needed investment options, and a new middle class was emerging from the war economy.

For several years, T. Rowe Price & Associates boasted few individual and no institutional clients. The partners accepted irregular salaries and exchanged actual pay for shares in the new enterprise. Fortunately, Price's wife had the financial resources to bankroll many of the firm's early losses. Even though Price's initial objective—that of building a company with 25 employees and $60 million in assets under management—was reasonable, it remained dubious for nearly the first decade in operation.

Yet even in these lean years, Price's analytical rigor began producing results. The firm would only invest in stock of a company whose president had been carefully interviewed by a T. Rowe Price analyst. The result was several winning stock picks between 1938 and 1949: Sharp & Dohme jumped 468 percent; Abbott Laboratories 334 percent; USF & G Corporation 198 percent; Addressograph-Multigraph 140 percent. In the late 1930s and early 1940s, investments in Minnesota Mining and Manufacturing (later 3M) and IBM also proved invaluable.

These weren't lucky guesses—they were the product of a systematic approach that would become the firm's hallmark. Price insisted on meeting management face-to-face, studying competitive dynamics, and understanding long-term earnings potential. While other investors focused on asset values and dividends, Price looked for what he called "fertile fields"—industries with long runways for growth.

Despite the tremendous odds facing T. Rowe Price before the end of World War II, the company managed to expand at a reasonable rate. According to records kept by Walter Kidd, director of research, total assets under management increased from $2.3 million in 1938 to $28 million in 1945 and $42 million in 1949. These numbers seem quaint by today's standards, but they represented exponential growth during one of history's most challenging periods.

The post-war period brought new challenges and opportunities. Veterans returned home, the GI Bill created a new educated middle class, and suburban expansion began reshaping America. Price sensed the shift before most. He saw that the economy was transitioning from wartime production to peacetime consumption, from heavy industry to consumer goods, from survival to prosperity.

The company faced many challenges during the Great Depression and World War II, but managed to persevere and recorded its first profitable year in 1950. That first profitable year wasn't just a financial milestone—it was validation of a philosophy. Growth investing, fee-based advisory services, and fiduciary responsibility weren't just theoretical concepts anymore. They were a proven business model.

By 1949, Price faced a different problem: success. By 1950, its clientele grew too large for the staff to manage accounts individually, so the firm incorporated and launched its first mutual fund, the T. Rowe Price Growth Stock Fund. This transition from managing separate accounts to pooled investments would transform not just T. Rowe Price, but the entire investment industry.

The decision to launch a mutual fund wasn't taken lightly. Price had built his reputation on personalized service, on knowing each client's situation intimately. But he recognized that democratizing access to professional management—making it available to smaller investors, not just wealthy families—aligned perfectly with his ethical framework. If growth investing could build wealth, why shouldn't everyone have access to it?

As the 1940s drew to a close, T. Rowe Price & Associates had survived its trial by fire. The firm that started with a handful of Baltimore families now managed tens of millions in assets. The investment philosophy dismissed as naive optimism during the Depression had produced spectacular returns. Most importantly, the ethical framework that Price established—putting clients first, charging fair fees, investing for long-term growth—had proven not just morally sound but commercially viable.

The stage was set for expansion. America was entering its greatest period of economic growth, and T. Rowe Price had positioned itself perfectly to capture it. The struggling startup of 1937 was about to become a force that would reshape American investing.

IV. The Growth Philosophy Takes Hold (1950s–1960s)

The photograph from 1955 shows Thomas Rowe Price Jr. at his desk, surrounded by towering stacks of annual reports, his signature bow tie slightly askew, magnifying glass in hand as he scrutinizes a balance sheet. By this point, Forbes had crowned him the "Sage of Baltimore," but Price seemed more interested in earnings growth rates than accolades. The decade that followed would prove his obsession justified.

The 1950s opened with America in the grip of transformation. The Korean War sparked inflation fears, suburbanization was reshaping the economy, and a new generation of companies—IBM, Xerox, Polaroid—were pioneering technologies that seemed straight out of science fiction. While most investors clung to the blue-chip dividend payers that had survived the Depression, Price was studying patent filings and interviewing engineers at companies most people couldn't pronounce. The T. Rowe Price Growth Stock Fund launched in April 1950, marking the firm's transition from managing individual accounts to pooled investments. In its first decade, it produced the best performance record of any U.S. equity mutual fund with the objective of growth. This wasn't luck—it was the vindication of a philosophy that had been mocked during the Depression.

The fund's early holdings read like a who's who of American innovation. Under Price's leadership, the fund invested in companies like IBM, along with Minnesota Mining and Manufacturing (3M), Merck, and Dow Chemical. Price didn't just buy these stocks; he practically lived with them. He'd visit factories, interview middle managers, study competitive dynamics. One famous story has him spending three days at a Xerox facility in Rochester, New York, watching technicians service the early 914 copier, timing how long repairs took, calculating the lifetime value of service contracts.

Gaining traction in Baltimore and along the U.S. eastern seaboard, the firm continued a steady expansion of clientele, staff, and geographic reach. But expansion meant more than just adding clients—it meant codifying the growth philosophy into something teachable, repeatable, scalable. Price began writing what would become legendary research notes, dense with data but animated by narrative. He'd describe a company's "life cycle" like a biologist discussing an organism: youth, growth, maturity, decline.

The philosophy was deceptively simple but revolutionary in practice. While traditional value investors looked for companies trading below their asset values, Price sought companies whose earnings were growing faster than the market average. He believed that sustained earnings growth would eventually be reflected in stock prices, regardless of short-term market fluctuations. The key was identifying companies early in their growth phase—what he called the "fertile fields" of the economy.

By 1960, the success of the Growth Stock Fund prompted the launch of a second fund, the New Horizons Fund, focused specifically on smaller growth companies and technology firms. Price opened a second fund, named the New Horizons Fund, focused on growth investment opportunities, and especially technology firms like Xerox, IBM, and Boeing. This was prescient timing—the 1960s would see the emergence of the "Nifty Fifty," growth stocks that seemed to defy gravity.

The New Horizons Fund represented an evolution in Price's thinking. If the Growth Stock Fund was about finding established companies with strong growth prospects, New Horizons was about identifying tomorrow's giants while they were still small. It was riskier, more volatile, but potentially more rewarding. Price personally interviewed the CEOs of every company the fund invested in, sometimes flying across the country for a two-hour meeting.

In need of more room, the headquarters were moved in 1962 to the new One Charles Center building designed by Ludwig Mies van der Rohe nearby in downtown Baltimore. At the same time, Price began to prepare for retirement, resigning as president of the firm in 1963, delegating some responsibilities, and selling his shares in the company.

The move to One Charles Center was more than geographic—it was symbolic. The modernist tower, with its clean lines and floor-to-ceiling windows, represented the firm's evolution from a Depression-era startup to a modern financial institution. Price's corner office on the 22nd floor overlooked the Inner Harbor, but he spent less time there as the decade progressed. He was transitioning from operator to philosopher, from manager to mentor.

He became well known as the "father of growth investing" and was nicknamed the "Sage of Baltimore" by Forbes. The nickname captured something essential about Price: he wasn't just picking stocks, he was articulating a worldview. Growth investing, in his formulation, was optimistic without being naive, disciplined without being rigid. It assumed that human ingenuity would continue to create value, that well-managed companies would find ways to expand, that the future would be better than the past.

Price's investment philosophy extended beyond stock selection to corporate governance. He insisted that T. Rowe Price analysts serve on portfolio company boards when invited, not to interfere but to understand. He pioneered the practice of proxy voting as a fiduciary responsibility, long before it became standard. He believed that ownership meant responsibility, not just returns.

The 1960s also saw Price develop his theory of "change as the investor's only certainty"—the idea that economic cycles, technological disruption, and social transformation were not aberrations but the normal state of affairs. Successful investing meant not predicting change but adapting to it. This philosophy would prove prescient as the stable prosperity of the 1950s gave way to the turbulence of the late 1960s.

By 1963, when Price resigned as president, the firm managed over $350 million in assets, employed dozens of analysts, and had established itself as one of America's premier growth investment firms. But Price wasn't done. He sensed something others didn't: that the era of stable growth and moderate inflation was ending. The coming decade would require a different approach, and at age 65, when most men were planning retirement, Thomas Rowe Price Jr. was planning one more revolution.

V. The New Era & Diversification (1969–1985)

The scene at T. Rowe Price's Baltimore headquarters in early 1969 was tense. Thomas Rowe Price Jr., now 71 and officially retired as president for six years, stormed into a partners' meeting with a stack of Federal Reserve data and a dire warning: inflation was coming, and it would devastate traditional growth stocks. His younger colleagues, riding high on the go-go years of the 1960s, thought the old man had lost his touch. They were about to learn otherwise.

Despite this, Price maintained an active presence in the firm for several years and urged the opening of the New Era Fund in 1969 as a response to the rapid inflation he predicted would dominate the 1970s. The New Era Fund was Price's last great intellectual contribution—a fund designed specifically to thrive in an inflationary environment by investing in natural resources, commodities, and companies with pricing power.

Price's inflation thesis was contrarian in the extreme. The late 1960s saw modest inflation around 3-4%, and most economists expected it to remain contained. But Price had studied the massive fiscal deficits from Vietnam War spending, the expansion of Great Society programs, and the demographic bubble of baby boomers entering their consumption years. He saw an inflation storm brewing that others missed. By 1974, inflation would hit 11%. By 1980, it would reach 13.5%.

The generational transition at the firm reflected a broader changing of the guard in American finance. In 1971, the year Price completely retired, T. Rowe Price opened its Fixed Income Division, and began to modernize and diversify its operations. This wasn't just adding a new product line—it was recognizing that the firm needed capabilities beyond equity investing to serve increasingly sophisticated institutional clients.

The Fixed Income Division's launch coincided perfectly with the bond market turmoil of the 1970s. As interest rates soared from 6% to eventually over 15% by decade's end, bond prices collapsed, creating both chaos and opportunity. T. Rowe Price's new bond team, applying the same rigorous research approach to credit analysis that the firm had pioneered in equities, found value where others saw only wreckage.

In the 1970s and early 1980s, T. Rowe Price kicked off more assertive growth than before, moving to its current location at 100 East Pratt Street and opening its first international office. The move to 100 East Pratt Street in 1975 consolidated operations that had spread across multiple Baltimore buildings. The new headquarters, a modernist tower overlooking the Inner Harbor, could house 500 employees—a number that seemed impossibly large at the time. The international expansion began modestly but strategically. In 1979, T. Rowe Price launched a joint venture with British asset manager Robert Fleming & Co. named Rowe Price-Fleming International. The venture, which managed $39 billion at its height in 2000, allowed T. Rowe Price to offer a broader range of services and expertise internationally.

The Fleming partnership was crucial for several reasons. T.Rowe Price Associates, Inc., the big Baltimore-based investment adviser, and Robert Fleming Holdings Ltd., of London, announced plans for a joint venture to manage international investments for American institutional investors such as pension funds. The joint venture would combine Price's understanding of the needs of U.S. investors with the London firm's broad international research capability. Each company managed about $6 billion in client assets at the time, making them equals in scale if not geography.

The timing was perfect. A combination of sociopolitical and technological advances in the late 1970s and early 1980s greatly facilitated international trade and investing, virtually turning the financial world into a global marketplace. In 1979, T. Rowe Price's joint venture with Robert Fleming Holdings Ltd., a London-based merchant bank, rode the wave. Meanwhile, the growing popularity of mutual funds throughout the 1980s gave individual investors the resources to invest globally—through fund managers with the ability to conduct international research, probe credit and currency risk, and employ sophisticated hedging techniques.

The 1970s inflation that Thomas Rowe Price Jr. had predicted proved both vindication and challenge. His New Era Fund, focused on natural resources and inflation beneficiaries, performed spectacularly. But traditional growth stocks, the firm's bread and butter, struggled as price-earnings multiples compressed and investors fled to hard assets. The firm had to evolve or risk irrelevance.

This evolution took multiple forms. The Fixed Income Division expanded rapidly, launching municipal bond funds to capitalize on the tax revolt of the late 1970s. By 1978, that fund boasted $215 million in assets and ranked third among more than 40 rivals. By the early 1990s, T. Rowe Price's lineup of tax-free mutual funds offered nearly every maturity category, as well as an insured fund for investors seeking extra credit protection and a high-yield fund for the more risk-tolerant.

The firm also began serving institutional clients more systematically. Pension funds, endowments, and foundations needed sophisticated asset allocation, not just stock picking. T. Rowe Price developed capabilities in balanced fund management, tactical asset allocation, and quantitative strategies—all while maintaining its fundamental research core.

Thomas Rowe Price Jr. died on October 20, 1983, at age 85. He'd lived to see his firm evolve from a five-person startup to a global institution managing billions. More importantly, he'd seen his philosophy validated through multiple market cycles. Growth investing wasn't just a bull market phenomenon—properly executed, it could generate returns through inflation, recession, and recovery.

The firm's culture in this period reflected both continuity and change. The research process Price pioneered—company visits, management interviews, competitive analysis—remained sacrosanct. But new tools emerged: computers for portfolio modeling, derivatives for risk management, global communications for real-time trading. The firm that had started with ledger books and adding machines was becoming a technology-driven enterprise.

By 1985, T. Rowe Price managed over $20 billion in assets, operated offices in multiple countries, and served thousands of institutional and retail clients. The foundation was set for the next transformation: going public. The partnership structure that had served the firm for nearly 50 years would give way to public ownership, bringing new opportunities and new challenges.

VI. Going Public & Global Expansion (1986–2000)

The morning of April 2, 1986, marked a watershed moment. As the opening bell rang at the NASDAQ, T. Rowe Price Group began trading under the ticker symbol TROW. The IPO, priced at $15.50 per share, valued the firm at nearly $200 million—a figure that would have seemed fantastical to Thomas Rowe Price Jr. when he started with $5,000 in working capital in 1937. But for the firm's 300 employees who had received stock grants over the years, it was tangible validation of patient wealth creation.

T. Rowe Price held its initial public offering, valued at nearly $200 million, in 1986. The decision to go public hadn't been taken lightly. For decades, the firm had prided itself on independence, on making decisions based on client needs rather than quarterly earnings. But the capital markets offered something crucial: permanent capital for expansion and liquidity for employee-owners who had built the firm.

Shortly thereafter, the firm began establishing larger office complexes in the U.S. and research offices around the world, beginning with a Hong Kong office in 1987. The Hong Kong office opening in 1987 was perfectly timed—just months before the colony would experience explosive growth as the gateway to China's economic opening. T. Rowe Price's analysts were among the first Western investors to visit Shenzhen's special economic zones, to meet with Chinese entrepreneurs who would build the next generation of Asian conglomerates.

The 1990s brought acceleration on all fronts. Retirement Plan Services were launched in the 1990s alongside additional new services and funds, including mutual funds acquired from other companies such as USF&G. The Retirement Plan Services division represented a strategic bet on defined contribution plans replacing traditional pensions. T. Rowe Price wasn't just managing money anymore—it was providing recordkeeping, participant education, and plan design consulting. The firm was becoming a full-service financial partner.

The international expansion accelerated dramatically as the decade progressed. This momentum, and the firm reaching $100 billion assets under management, pushed T. Rowe Price to create an asset management partnership with Sumitomo Bank and Daiwa Securities in Tokyo in 1999, and to purchase 100% interest of the London-based Rowe Price-Fleming International, which was renamed T. Rowe Price International.

The Fleming acquisition was particularly significant. After 20 years of successful partnership, T. Rowe Price bought out its British partner for an undisclosed sum, gaining complete control of what had become a $39 billion international investment platform. The renamed T. Rowe Price International gave the firm direct ownership of relationships with sovereign wealth funds, European pension schemes, and Asian institutions.

Also in 1999, T. Rowe Price was added to the S&P 500 Index. Inclusion in the S&P 500 meant more than prestige—it meant automatic buying from index funds, greater liquidity, and validation as one of America's most important companies. The stock price jumped 12.8% on the announcement, adding hundreds of millions to the firm's market capitalization in a single day.

But the late 1990s also brought challenges that tested the firm's philosophy. The dot-com bubble was inflating to unprecedented levels. Companies with no earnings—sometimes no revenue—traded at astronomical valuations. T. Rowe Price's growth philosophy had always emphasized earnings growth, not speculative fever. The firm's funds began underperforming as money poured into anything with ".com" in its name.

T. Rowe Price largely avoided the dot-com bubble of 2000. The Wall Street Journal expressed surprise at the firm's moderation with avoiding concentrated holdings in trendy internet technology stocks, in an article published a week before the markets began to crash in March 2000. The discipline to avoid the bubble wasn't easy. Portfolio managers faced daily questions from clients about why they weren't buying Yahoo or Pets.com. Young analysts argued for "new economy" valuation metrics. The firm's stock price lagged peers who were riding the tech wave.

Internal debates raged. Should T. Rowe Price launch an internet fund to capture flows? Should it relax its valuation discipline to remain competitive? The answer, ultimately, was no. The firm launched some technology-focused funds but maintained its insistence on profitable companies with sustainable business models. It was a lonely position in 1999.

The firm's global footprint by 2000 was remarkable. From a single Baltimore office, T. Rowe Price had expanded to locations in London, Hong Kong, Tokyo, Buenos Aires, Copenhagen, and Singapore. Each office wasn't just a sales outpost but a research hub, with local analysts covering regional companies. The sun never set on T. Rowe Price's investment operations.

In 2001, the company launched T. Rowe Price Funds SICAV, domiciled in Luxembourg, for non-U.S. institutional investors and financial intermediaries. Two years later it created target-date retirement funds. The SICAV structure allowed European investors to access T. Rowe Price strategies in a tax-efficient vehicle, while target-date funds would become one of the firm's greatest successes, eventually managing hundreds of billions in retirement assets.

The establishment of T. Rowe Price Group as a holding company in 2000 created the corporate structure for a truly global enterprise. No longer just an investment advisor, the firm now encompassed multiple regulated entities across dozens of jurisdictions. It was a far cry from the partnership Thomas Rowe Price Jr. had founded, yet the core mission remained unchanged: helping clients achieve their financial goals through disciplined, research-driven investing.

By the end of 2000, as the NASDAQ crashed and the dot-com bubble burst, T. Rowe Price's conservatism looked prescient. The firm that had been mocked for missing the internet boom was now flooded with assets from investors seeking quality and stability. Assets under management approached $200 billion. The firm employed over 3,000 people globally. Most importantly, it had maintained its culture and investment discipline through one of history's greatest speculative manias.

The new millennium would bring new challenges—the rise of passive investing, fee compression, regulatory complexity. But T. Rowe Price entered it from a position of strength, having proven that disciplined growth investing could survive and thrive through any market environment.

VII. The Modern Era: Active vs. Passive Battle (2000–2020)

The conference room at 100 East Pratt Street was silent as the PowerPoint slide appeared: "Vanguard's index funds now manage more assets than all of T. Rowe Price combined." It was 2010, and CEO James Kennedy was addressing a harsh reality. The firm that had pioneered professional investment management was watching clients flee to index funds that charged a tenth of its fees. The existential question hung in the air: In a world where computers could replicate the S&P 500 for three basis points, what was the value of human judgment?

The 2000s had started promisingly enough. The dot-com crash vindicated T. Rowe Price's disciplined approach, and assets flowed in from investors burned by speculative excess. But beneath the surface, tectonic shifts were reshaping asset management. Exchange-traded funds (ETFs) were democratizing index investing. Robo-advisors were automating asset allocation. Fee compression was relentless.

The 2008 financial crisis accelerated these trends. Even though T. Rowe Price navigated the crisis relatively well—its conservative underwriting and lack of exposure to exotic derivatives protected client assets—the broader active management industry faced a reckoning. Why pay 75 basis points for active management when markets could collapse 40% regardless? The decade following 2008 saw over $2 trillion flow from active to passive funds.

As of 2019, the company is focused on active management after strategically deciding against a major initiative in passive investment. This decision, made in 2019 after years of internal debate, was perhaps the most important strategic choice in the firm's modern history. While competitors like Fidelity and Charles Schwab rushed to offer zero-fee index funds, T. Rowe Price doubled down on active management.

The rationale was both philosophical and practical. Philosophically, indexing was antithetical to everything Thomas Rowe Price Jr. had stood for—the belief that research, judgment, and active selection could generate superior returns. Practically, T. Rowe Price lacked the scale to compete with Vanguard and BlackRock in the commoditized index fund business. Better to be excellent at active management than mediocre at passive.

But staying active required evolution. T. Rowe Price invested heavily in quantitative capabilities, building teams of Ph.D.s who could parse satellite data to estimate retail traffic or scrape social media to gauge consumer sentiment. The firm's traditionally fundamental analysts now worked alongside data scientists, combining human insight with machine processing power.

Target-date funds became an unexpected bright spot. Two years later it created target-date retirement funds. These funds, which automatically adjust asset allocation as investors approach retirement, played to T. Rowe Price's strengths: multi-asset expertise, risk management, and fiduciary mindset. By 2020, the firm managed over $300 billion in target-date strategies, making it one of the "Big Three" alongside Vanguard and Fidelity.

The international expansion continued, but with a twist. Rather than just exporting U.S. strategies abroad, T. Rowe Price began developing local capabilities. In 2010, T. Rowe Price bought a significant interest in Unit Trust of India, India's oldest mutual fund company and one of its five largest. The UTI investment gave T. Rowe Price access to India's burgeoning middle class and its savings boom.

Technology transformation was another imperative. The firm that had started with paper ledgers now processed millions of transactions daily through sophisticated systems. Client portals provided real-time access to account information. Artificial intelligence helped detect fraud and optimize trade execution. Yet the human element remained central—every portfolio still had a named manager accountable for results.

The regulatory environment grew increasingly complex. Dodd-Frank, MiFID II, and countless other regulations required armies of compliance professionals. T. Rowe Price's legal and compliance staff grew from dozens to hundreds. The cost of being a global asset manager skyrocketed, creating barriers to entry but also protecting established players.

Fee pressure was relentless but manageable. Average fees declined from about 80 basis points in 2000 to 45 basis points by 2020, but assets under management grew from $200 billion to over $1.4 trillion. The math worked: lower margins on much larger scale still produced record revenues. The key was maintaining premium pricing for differentiated strategies while accepting commodity pricing for vanilla products.

In the decade from 2010 to 2020, T. Rowe Price increased its assets under management from $400 billion to $1.6 trillion and annual revenues increased 10.2 percent to $6.2 billion over 2019, placing it 447 on the Fortune 500 list of the largest U.S. companies.

The active versus passive debate raged throughout the decade, but T. Rowe Price found a middle ground. Its actively managed funds didn't try to beat the index every quarter—they aimed to outperform over full market cycles with lower volatility. This approach resonated with retirement savers and institutional investors who valued downside protection as much as upside participation.

Environmental, Social, and Governance (ESG) investing emerged as both opportunity and challenge. Clients increasingly demanded that their investments reflect their values. T. Rowe Price integrated ESG factors into its research process, but resisted the urge to launch dozens of specialized ESG funds. The firm believed that considering environmental and social factors was simply good investing, not a separate category.

By 2020, T. Rowe Price had survived the active-passive wars not by winning decisively but by refusing to fight on unfavorable terrain. While pure-play active managers struggled and pure-play passive managers commoditized, T. Rowe Price occupied a profitable middle ground: sophisticated active strategies for those willing to pay, efficient implementations for those who weren't, and solutions-based approaches for those who wanted both.

The firm that entered 2020 managed $1.4 trillion in assets, employed over 7,000 people globally, and served millions of clients. It remained independent in an industry increasingly dominated by banks and conglomerates. Most remarkably, it maintained the research-driven, client-first culture that Thomas Rowe Price Jr. had established eight decades earlier.

But the biggest transformation was yet to come. The firm built on growth stocks was about to make its boldest bet yet: a multi-billion dollar push into private markets.

VIII. The Oak Hill Acquisition: Private Markets Pivot (2021)

Rob Sharps, T. Rowe Price's CEO since 2017, stood before employees on a crisp October morning in 2021 with an announcement that would have seemed unthinkable just years earlier: T. Rowe Price was acquiring Oak Hill Advisors for up to $4.2 billion, marking its first major foray into alternative investments. The firm that had built its reputation on transparent, liquid, public market investing was diving into the opaque world of private credit, distressed debt, and special situations.T. Rowe Price Group, Inc. announced a definitive agreement to purchase Oak Hill Advisors, L.P. (OHA), a leading alternative credit manager on October 28, 2021. Under the terms of the transaction, T. Rowe Price would acquire 100% of the equity of OHA for a purchase price of up to approximately $4.2 billion, with $3.3 billion payable at closing, approximately 74% in cash and 26% in T. Rowe Price common stock, and up to an additional $900 million in cash upon the achievement of certain business milestones beginning in 2025.

The strategic rationale was compelling. Alternative credit strategies continue to be in demand from institutional and retail investors across the globe seeking attractive yields and risk-adjusted returns. With interest rates near zero and traditional bonds yielding almost nothing, investors were desperate for income. Private credit offered yields of 8-12%, but accessing these markets required specialized expertise that T. Rowe Price lacked.

OHA managed $53 billion of capital (as of July 31, 2021) across its private, distressed, special situations, liquid, structured credit, and real asset strategies. Founded in 1991 by Glenn August, a former Goldman Sachs partner, OHA had built one of the most respected franchises in alternative credit. OHA has generated attractive risk-adjusted returns over its more than 30-year history by specializing in performing and distressed credit related investments in North America, Europe, and other geographies.

The cultural fit was surprisingly strong despite the surface differences. Both firms emphasized fundamental research, long-term relationships, and aligned incentives. OHA's 300 professionals operated with the same analytical rigor that T. Rowe Price applied to public markets, just in the more complex world of private lending, restructurings, and special situations.

The acquisition was completed on December 29, 2021. With the closing of the transaction, OHA would operate as a standalone business within T. Rowe Price, have autonomy over its investment process, and maintain its team and culture. Glenn August continued in his current role and joined T. Rowe Price's Board of Directors and Management Committee.

The deal structure revealed sophisticated thinking about incentive alignment. The $900 million earnout tied to business milestones ensured OHA's partners remained motivated post-acquisition. The 26% stock component aligned OHA with T. Rowe Price's long-term success. Operating as a standalone entity preserved OHA's entrepreneurial culture while providing access to T. Rowe Price's distribution network.

OHA's performance, its global institutional client base, and the positive industry backdrop had positioned it to raise $19.4 billion of capital since January 2020. This fundraising momentum was crucial—in private markets, the ability to raise and deploy capital at scale creates a virtuous cycle of better deal flow, superior terms, and stronger returns.

The integration challenges were substantial. Private credit operates differently from public markets—longer investment horizons, illiquid positions, complex structuring. T. Rowe Price's traditional retail clients weren't equipped to invest directly in private credit funds with high minimums and long lock-ups. The firm needed to create new vehicles to democratize access.

T. Rowe Price and Oak Hill Advisors announced the launch of their joint investment offering, the T. Rowe Price OHA Select Private Credit Fund (OCREDIT), which provides an OHA-managed private credit investment solution for income-oriented individual investors with the convenience of a non-traded, perpetual-life business development company (BDC) structure.

The timing of the acquisition proved fortuitous. As the Federal Reserve raised rates in 2022-2023 to combat inflation, floating-rate private credit outperformed fixed-rate public bonds dramatically. OHA's expertise in navigating credit cycles—honed through multiple downturns—helped T. Rowe Price clients access attractive yields while managing downside risk.

But the acquisition also raised existential questions. Was T. Rowe Price abandoning its transparent, liquid heritage for the opacity of private markets? Could a firm built on daily pricing and redemptions manage assets that traded by appointment? Would the complexity of alternatives dilute the firm's straightforward value proposition?

The answer lay in viewing alternatives not as a departure but as an evolution. Just as Thomas Rowe Price Jr. had expanded from individual stocks to mutual funds, from domestic to international, from equities to fixed income, the move into alternatives represented adaptation to changing client needs. In a world of compressed public market returns, private markets offered the growth and income that traditional assets once provided.

Scale is increasingly important as a competitive advantage in sourcing financing opportunities and driving differentiated returns across alternative credit markets. The combined entity could compete for larger deals, negotiate better terms, and provide complete solutions across public and private markets. It was vertical integration for the modern age.

By 2023, the Oak Hill acquisition was already bearing fruit. The alternatives platform was raising capital at record pace, institutional clients were consolidating relationships, and retail investors were accessing private credit through innovative structures. T. Rowe Price had successfully added a new growth engine while maintaining its traditional strengths.

The acquisition marked more than a strategic pivot—it represented a generational transition. The firm that had mastered public markets over eight decades was positioning itself for a future where the lines between public and private, liquid and illiquid, traditional and alternative would increasingly blur.

IX. Current State & Future Challenges (2021–Present)

The summer heat in Baltimore was oppressive as employees filed into T. Rowe Price's headquarters in August 2025, but the atmosphere inside was electric. The firm had just announced assets under management of $1.70 trillion as of July 31, 2025, a figure that would have seemed impossible just a decade earlier. Yet beneath the surface metrics, fundamental questions about the firm's future remained unanswered.

The numbers told a story of scale and resilience. T. Rowe Price Group, Inc. is a global investment management organization with $1.70 trillion in assets under management, serving millions of clients across 55 countries through 7,868 employees across 17 international offices. About two-thirds of the assets under management are retirement-related, reflecting the firm's dominance in defined contribution plans and target-date funds.

But the headline figures masked underlying tensions. Active management continued to face relentless pressure from passive alternatives. Fee compression showed no signs of abating. New competitors—from Silicon Valley tech giants to Chinese asset managers—were entering the market with different economics and ambitions. The firm that had thrived by zigging when others zagged now faced challenges from every direction.

The Oak Hill integration was proceeding better than expected. The alternatives platform had grown to over $60 billion in assets, attracting institutional investors seeking yield in a volatile rate environment. The launch of retail-oriented private credit funds was democratizing access to alternatives, though operational complexity remained a challenge. Managing illiquid assets required different systems, different risk management, different client communication.

Technology transformation accelerated. Artificial intelligence wasn't just a research tool anymore—it was embedded throughout the organization. Machine learning models helped predict client behavior, optimize portfolio construction, and detect anomalies in trading patterns. Yet the firm maintained its belief that human judgment, particularly in complex situations requiring nuance and context, remained irreplaceable.

The regulatory landscape grew ever more complex. New ESG disclosure requirements, privacy regulations, and cross-border compliance created constant challenges. The cost of being a global asset manager continued to rise, creating barriers for new entrants but also pressuring margins for incumbents. T. Rowe Price's compliance and legal teams now numbered in the hundreds, a far cry from the handful of professionals just two decades earlier.

Geographic expansion continued, but with a focus on depth rather than breadth. Rather than opening offices in every major city, T. Rowe Price concentrated on building scale in key markets. The Asia-Pacific region, particularly China and India, represented enormous growth potential, though navigating regulatory requirements and cultural differences required patience and local expertise.

The leadership transition loomed large. Rob Sharps, CEO since 2017, had successfully navigated the Oak Hill acquisition and maintained the firm's independence, but succession planning was critical. The next generation of leaders would need to balance tradition with innovation, maintain culture while embracing change, and compete globally while staying true to Baltimore roots.

Competition intensified from unexpected quarters. Private equity firms were building asset management capabilities. Insurance companies were expanding beyond traditional fixed income. Sovereign wealth funds were insourcing investment management. The neat categories that once defined the industry—active vs. passive, retail vs. institutional, public vs. private—were breaking down.

Client expectations evolved dramatically. They wanted personalized solutions, not off-the-shelf products. They demanded transparency on fees, performance, and ESG impact. They expected digital interfaces as sophisticated as consumer technology platforms. Meeting these expectations required constant investment in technology and talent.

The war for talent was fierce. T. Rowe Price competed not just with other asset managers but with hedge funds, private equity firms, and technology companies for the best minds. Maintaining the collaborative, research-driven culture while offering competitive compensation was an ongoing challenge. The firm that once recruited primarily from Baltimore-area universities now searched globally for expertise.

Fee pressure remained relentless but manageable. While headline fees continued to decline, T. Rowe Price maintained premium pricing for differentiated capabilities—alternatives, multi-asset solutions, specialized strategies. The key was demonstrating value beyond simple market returns: risk management, tax efficiency, behavioral coaching, retirement planning.

The retirement business remained a crown jewel. With baby boomers retiring at 10,000 per day and defined contribution plans becoming the primary retirement vehicle globally, T. Rowe Price's expertise in target-date funds and retirement income solutions positioned it well. The challenge was maintaining market share as every competitor recognized the same opportunity.

ESG integration evolved from nice-to-have to must-have. Clients, particularly younger ones, expected their investments to reflect their values. T. Rowe Price integrated ESG factors into its research process while resisting the temptation to launch dozens of specialized ESG products. The firm believed that considering environmental and social factors was simply good investing, not a marketing gimmick.

Looking ahead, the path was neither clear nor easy. The firm faced existential questions: Could active management justify its fees in an age of near-perfect information? Would alternatives become commoditized like traditional assets? How would artificial intelligence reshape investment management? Could a firm rooted in 20th-century principles thrive in the 21st-century economy?

Yet T. Rowe Price entered this uncertain future from a position of strength. Independent in an industry increasingly dominated by giants. Profitable in an environment of margin compression. Growing while many peers contracted. Most importantly, it maintained the research-driven, client-first culture that Thomas Rowe Price Jr. had established nearly 90 years earlier.

The firm stood at an inflection point, much as it had in 1937, 1950, 1986, and 2021. Each time, it had adapted while maintaining its core identity. The challenge now was to do so again, in a world changing faster than ever before.

X. Playbook: Business & Investing Lessons

Standing in the archive room at 100 East Pratt Street, surrounded by decades of research reports, memos, and annual letters, one can trace the DNA of investment thinking from Thomas Rowe Price Jr.'s handwritten notes to today's AI-powered analytics. The principles that built a trillion-dollar enterprise weren't revolutionary in isolation—their power lay in consistent application across generations. Here are the enduring lessons from T. Rowe Price's 88-year journey.

The Power of Founding Philosophy

Growth investing's 85+ year run at T. Rowe Price demonstrates that a coherent, well-articulated investment philosophy can survive multiple market cycles, technological disruptions, and generational transitions. Price didn't just pick growth stocks—he created an intellectual framework for identifying and valuing growth that could be taught, refined, and scaled.

The key insight wasn't that growth was better than value, but that sustainable earnings growth, properly identified and patiently held, would eventually be reflected in stock prices. This seems obvious now, but in 1937, when most investors focused on asset values and dividends, it was revolutionary. The philosophy's durability came from its flexibility—it could adapt to new industries, new geographies, new market structures while maintaining its core logic.

The lesson: A founding philosophy must be specific enough to provide guidance but flexible enough to evolve. It should be teachable but not dogmatic, principled but not rigid.

Fee Alignment as Competitive Advantage

T. Rowe Price's decision to charge fees based on assets under management rather than commissions wasn't just ethical—it was strategically brilliant. By aligning the firm's economics with client outcomes, it created a sustainable competitive advantage that transaction-based competitors couldn't match.

This alignment went beyond fee structure. The firm's employee ownership model meant that those making investment decisions had skin in the game. The emphasis on long-term performance over short-term asset gathering meant that bad performance hurt the firm as much as clients. This created a culture of accountability rare in financial services.

The lesson: True alignment goes beyond fee structure to encompass incentives, time horizons, and risk sharing. When provider and client interests align, trust becomes a competitive moat.

Patient Capital Through Market Cycles

T. Rowe Price survived and thrived through the Great Depression, World War II, 1970s stagflation, 1987's Black Monday, the dot-com bubble, 2008's financial crisis, and COVID-19. Each crisis tested the firm differently, but the response was consistent: maintain discipline, don't chase trends, and think long-term.

The firm's patience extended beyond market cycles to business building. It took 13 years to become profitable, 50 years to go public, and 84 years to reach $1 trillion in assets. This patience allowed for organic growth, cultural continuity, and the compound benefits of reputation.

The lesson: In investment management, as in investing itself, time arbitrage is the most sustainable edge. Being able to think in decades when competitors think in quarters creates opportunities.

Build vs. Buy Decisions

T. Rowe Price's growth strategy balanced organic expansion with strategic acquisitions. The firm built most capabilities internally—international investing, fixed income, quantitative strategies—allowing for cultural integration and quality control. But for transformative capabilities like alternatives, it bought, recognizing that some expertise can't be built from scratch.

The Oak Hill acquisition exemplified thoughtful M&A: buying a cultural fit with complementary capabilities, maintaining operational independence, and aligning incentives through earnouts and equity. This contrasted with competitors' serial acquisitions that often destroyed value through cultural clashes and integration failures.

The lesson: Build what's core to your culture and strategy; buy what would take too long to build or require fundamentally different DNA. Always prioritize cultural fit over financial metrics.

Culture Preservation Through Scale

Growing from 5 to 7,868 employees while maintaining a coherent culture required deliberate effort. T. Rowe Price achieved this through several mechanisms: promoting from within, maintaining Baltimore headquarters despite globalization, emphasizing research and intellectual rigor across all roles, and creating formal and informal networks that connected employees across geographies and functions.

The firm's culture wasn't preserved in amber—it evolved with each generation while maintaining core elements. The research process became more quantitative but remained fundamental. The client base became global but the service ethic remained personal. Technology transformed operations but human judgment remained central.

The lesson: Culture scales through systems, not slogans. Embed cultural values in hiring, promotion, compensation, and daily decision-making. Allow for evolution while protecting core principles.

Navigating Industry Disruption

T. Rowe Price faced existential disruption multiple times: index funds in the 1970s, online brokers in the 1990s, ETFs in the 2000s, robo-advisors in the 2010s, and now AI and blockchain. Each time, the firm's response was measured: understand the disruption, adopt what improves client outcomes, but don't abandon core strengths.

The decision to remain focused on active management while competitors rushed to passive was controversial but ultimately successful. By accepting that some assets would go to indexing while focusing on areas where active management added value—alternatives, multi-asset, retirement solutions—T. Rowe Price found profitable niches in a disrupted industry.

The lesson: Disruption rarely destroys entire industries overnight. There's usually time to adapt if you're willing to cannibalize some existing business while doubling down on differentiated capabilities.

The Compound Effect of Reputation

T. Rowe Price's reputation for integrity, built over decades, became its most valuable asset. In an industry plagued by conflicts of interest and short-term thinking, the firm's reputation for putting clients first attracted assets even during periods of underperformance.

This reputation was built through thousands of small decisions: returning fees after poor performance, closing funds to new investors to protect existing clients, providing honest advice even when it meant losing assets. These decisions seemed costly in the short term but created immense long-term value.

The lesson: Reputation compounds like investment returns—slowly at first, then dramatically. Every decision either adds to or subtracts from reputational capital.

Generational Transition Planning

The firm successfully navigated multiple leadership transitions: Thomas Rowe Price Jr. to his successors, family ownership to public ownership, founder-led to professionally managed. Each transition was planned years in advance, with careful attention to cultural continuity and strategic alignment.

The decision to go public in 1986, rather than selling to a bank or insurance company, preserved independence while providing liquidity. The establishment of strong governance structures and independent boards protected against the founder's curse that destroyed many investment firms.

The lesson: Plan succession before it's needed. Build institutions, not personalities. Create governance structures that can survive any individual's departure.

Global Expansion with Local Adaptation

T. Rowe Price's international expansion balanced global consistency with local adaptation. Investment philosophy and research processes were standardized globally, but product offerings, distribution strategies, and client service were localized. This allowed for economies of scale while respecting regional differences.

The firm also recognized that international expansion wasn't just about gathering assets—it was about accessing investment opportunities. Local offices provided insights into regional companies and markets that enhanced global portfolios.

The lesson: Think globally but act locally. Maintain core principles while adapting execution to local contexts.

The Innovation Imperative

Despite its traditional image, T. Rowe Price consistently innovated: first no-load funds, first target-date funds, early adoption of quantitative methods, pioneering ESG integration, and now alternatives and AI. Innovation wasn't pursued for its own sake but to solve client problems or improve investment outcomes.

The firm's innovation model balanced internal R&D with external partnerships and acquisitions. It was fast follower more often than first mover, learning from others' mistakes while applying superior execution.

The lesson: Innovation in financial services is about thoughtful application more than invention. Focus on solving real problems rather than chasing buzzwords.

These lessons, distilled from nearly nine decades of experience, offer a masterclass in building enduring financial institutions. They demonstrate that success in investment management comes not from any single insight or strategy, but from the patient, disciplined application of sound principles across market cycles and generations.

XI. Analysis & Bear vs. Bull Case

The investment committee conference room on the 27th floor offers a panoramic view of Baltimore's Inner Harbor, but on this gray December morning in 2024, the senior partners of a major hedge fund are focused on the screens displaying T. Rowe Price's financials. They're debating whether TROW represents a value trap in a dying industry or a coiled spring ready to benefit from the next phase of wealth creation. The same debate is happening in investment committees worldwide.

The Bull Case: Strength Through Transition

The optimists see T. Rowe Price as a rare combination of quality and value in asset management. Start with the brand strength: 88 years of reputation in an industry where trust is everything. While fintech startups burn through capital trying to acquire customers, T. Rowe Price has multi-generational client relationships and institutional partnerships that would take decades to replicate.

The distribution network is unmatched. Through retirement plan recordkeeping, T. Rowe Price touches millions of Americans' first investment dollar. This creates a customer acquisition funnel that competitors envy—participants in T. Rowe Price-administered 401(k) plans are natural customers for IRAs, 529 plans, and taxable accounts. With 10,000 baby boomers retiring daily and rolling over $2 trillion from 401(k)s to IRAs over the next decade, T. Rowe Price sits at the nexus of the greatest wealth transfer in history.

The alternatives capability via Oak Hill provides a new growth vector just as traditional active management faces headwinds. Private markets are expected to grow from $10 trillion today to $25 trillion by 2030. T. Rowe Price now has institutional-quality capabilities to capture this growth while using its retail distribution to democratize access—a combination few competitors can match.

Global reach provides diversification and growth optionality. While U.S. markets are mature, Asia's wealth management industry is exploding. China's asset management industry is expected to triple by 2030. India's mutual fund penetration is still under 15%. T. Rowe Price's established presence in these markets positions it to capture disproportionate growth.

The financial model remains robust despite fee pressure. Operating margins above 30% are among the industry's best. Zero debt provides flexibility for acquisitions or buybacks. The variable cost structure means the firm can weather downturns better than competitors with high fixed costs. Free cash flow generation is prodigious, funding both growth investments and generous shareholder returns.

Bulls also point to hidden assets: the data accumulated from 88 years of investment research, the intellectual property in proprietary models and processes, the human capital of thousands of experienced professionals. These intangible assets don't appear on the balance sheet but represent enormous value in an industry where information and judgment drive returns.

The Bear Case: Structural Decline

The pessimists see T. Rowe Price as a melting ice cube in the heat of passive indexing. Active management's share of U.S. equity assets has declined from 80% to 40% over two decades and shows no signs of stabilizing. Every basis point of fee compression destroys millions in revenue. The firm's average fee has declined from 80 basis points to 45 basis points since 2000, and the pressure is accelerating.

Passive competition from Vanguard and BlackRock is existential. These giants have scale advantages that allow them to offer index funds at near-zero fees while making money on securities lending and other ancillary services. They're using passive as a loss leader to capture assets, then cross-selling higher-margin products. T. Rowe Price can't compete on price and increasingly struggles to compete on performance.

The bear case sees succession risk as acute. The firm has successfully navigated leadership transitions before, but never in such a challenging environment. The next CEO will need to manage declining traditional business while building new capabilities, maintain culture while transforming operations, and compete globally while remaining anchored in Baltimore. It's a nearly impossible job.

Technology disruption accelerates. Robo-advisors have commoditized asset allocation. AI is replacing human analysts. Blockchain could eliminate traditional intermediaries. Young investors prefer Bitcoin to balanced funds. T. Rowe Price's technology investments, while substantial, may be too little, too late against digital-native competitors.

The cost structure is increasingly uncompetitive. Maintaining 7,868 employees and 17 offices is expensive. Regulatory compliance costs continue to rise. Technology investments are necessary but don't generate revenue. Meanwhile, digital competitors operate with fraction of the headcount and infrastructure.

Client concentration risk is real. The top 10 clients represent a significant portion of assets. If one large institutional client or retirement plan platform switches providers, it could trigger billions in outflows. The retail brand, while strong among older investors, has limited resonance with millennials and Gen Z.

Valuation and Financial Metrics

The financial metrics tell a mixed story. Return on equity above 20% indicates a quality business. But organic growth has turned negative, with outflows exceeding inflows in recent quarters. The dividend yield around 5% attracts income investors but might signal limited growth expectations.

The price-to-earnings ratio in the mid-teens seems reasonable for a financial services firm but expensive for one facing structural headwinds. The price-to-book around 2x is below historical averages but above pure-play passive managers. Enterprise value to AUM of roughly 2% is middle-of-the-pack, neither obviously cheap nor expensive.

Relative valuation versus peers is complicated by different business mixes. BlackRock trades at a premium due to its technology platform and passive dominance. Franklin Resources trades at a discount due to its value orientation and outflows. Invesco and AllianceBernstein face similar active management challenges. T. Rowe Price's valuation seems fair relative to peers but the entire traditional asset management sector trades at depressed multiples.

Competitive Positioning

T. Rowe Price occupies an increasingly narrow competitive niche: too small to compete with the giants on scale, too traditional to compete with disruptors on innovation, too expensive to compete with passive on price. Yet this niche—sophisticated active management for retirement savers and institutions—remains large and profitable.

Versus BlackRock's $10 trillion AUM, T. Rowe Price looks subscale. But BlackRock's size brings its own challenges: regulatory scrutiny, market impact, bureaucracy. T. Rowe Price's relative nimbleness allows for faster decision-making and more personalized service.

Against Vanguard's mutual ownership structure, T. Rowe Price seems disadvantaged. Vanguard can operate at cost, returning all profits to fund shareholders. But public ownership provides T. Rowe Price with acquisition currency and incentive alignment that Vanguard lacks.

Compared to boutique managers, T. Rowe Price has scale advantages in distribution, technology, and compliance. But boutiques have focus, agility, and often superior investment performance in narrow strategies. T. Rowe Price must balance the benefits of scale with the need for investment excellence.

The Role of Alternatives

The Oak Hill acquisition's success is crucial to the investment thesis. If T. Rowe Price can successfully build a multi-hundred-billion-dollar alternatives platform, it could offset traditional active management declines. The early signs are positive: successful fundraising, strong performance, operational integration proceeding smoothly.

But alternatives bring new risks: illiquidity, leverage, complexity. A major credit event or fraud could damage the firm's reputation built over 88 years. Regulatory scrutiny of private markets is increasing. Fee pressure is coming to alternatives just as it came to traditional assets.

The alternatives build-out also raises strategic questions. Should T. Rowe Price expand into private equity, real estate, infrastructure? Each requires different expertise and raises different risks. How much of the firm's capital and management attention should alternatives consume?

The Verdict

The bear-bull debate on T. Rowe Price ultimately comes down to timeframe and belief about active management's future. Bears see inevitable decline as passive indexing and technology eliminate traditional asset managers. Bulls see a quality franchise adapting to new realities while maintaining competitive advantages in distribution, brand, and expertise.

The truth likely lies between extremes. T. Rowe Price faces real challenges that will pressure growth and margins. But the firm has survived and thrived through multiple periods of disruption. Its retirement franchise, global platform, and alternatives capability provide growth options. The question isn't whether T. Rowe Price will survive—it's whether it can generate attractive returns for shareholders while navigating industry transformation.

For long-term investors, T. Rowe Price offers exposure to the secular growth in global wealth management with downside protection from its quality franchise. For traders, it's a battleground stock whose price will fluctuate with flows, market conditions, and sentiment about active management.

The firm that Thomas Rowe Price Jr. founded in 1937 has proven remarkably adaptable. Whether that adaptability can overcome the current industry challenges remains the key question for investors evaluating TROW. The answer will emerge not from spreadsheets or algorithms, but from the thousands of daily decisions made by T. Rowe Price employees serving millions of clients—just as it has for 88 years.

XII. Epilogue & Final Reflections

The morning sun streams through the windows of Thomas Rowe Price Jr.'s preserved office on the executive floor of 100 East Pratt Street. The space remains much as he left it: the worn leather chair, the adding machine he insisted on using even after computers arrived, the framed photo of his first client. Rob Sharps, the current CEO, sometimes comes here to think, surrounded by the tangible reminders of how far the firm has traveled from that first office at 10 Light Street.

What would Thomas Rowe Price Jr. think of today's firm? The chemist-turned-investor who started with $5,000 in working capital would surely marvel at the $1.70 trillion under management. The man who personally interviewed every CEO before investing would be astounded by algorithms parsing satellite data and social media sentiment. The founder who knew every client by name might struggle with serving millions of anonymous 401(k) participants.

Yet in fundamental ways, he would recognize his creation. The investment philosophy remains growth-oriented, seeking companies with sustainable earnings expansion. The fee structure still aligns firm and client interests. The culture still emphasizes research, integrity, and long-term thinking. The headquarters still overlooks Baltimore's Inner Harbor, just a few blocks from where it all began.

The Evolution from Boutique to Behemoth

The transformation from boutique to behemoth wasn't just about scale—it was about institutionalizing genius. Thomas Rowe Price Jr.'s insights about growth investing were brilliant but personal. The firm's great achievement was transforming individual brilliance into organizational capability, making the implicit explicit, the art into science.

This institutionalization came with trade-offs. The firm lost some entrepreneurial spirit with each layer of management added. Compliance requirements constrained creativity. Scale advantages came with bureaucratic disadvantages. The intimate client relationships of the early days gave way to digital interfaces and call centers.

Yet the benefits outweighed the costs. Millions of Americans retire more securely because T. Rowe Price democratized professional investment management. Thousands of employees built careers and wealth through the firm's growth. Baltimore retained a major corporate headquarters when many cities lost theirs to consolidation.

Key Surprises for Founders

The biggest surprise for any founder might be what didn't change. Despite technological revolution, human judgment still matters. Despite globalization, local relationships still count. Despite market evolution, patience still pays. The fundamentals that Thomas Rowe Price Jr. identified—growth, research, alignment—remain as relevant today as in 1937.

But the speed of change would shock any time traveler from the past. Trades that took days now execute in microseconds. Research that required library visits now happens instantly online. Communications that took weeks by mail now occur immediately via video. The firm operates at a pace and scale unimaginable to its founders.

The regulatory burden would also surprise. The firm that started with a handshake and a ledger book now employs hundreds of compliance professionals. Every email is archived, every trade is surveilled, every decision is documented. The cost of being a fiduciary has multiplied exponentially.

Lessons for Modern Founders

T. Rowe Price's journey offers timeless lessons for today's entrepreneurs, particularly in financial services. First, philosophy matters more than products. Products can be copied; philosophy creates sustainable differentiation. Second, culture compounds like returns—small daily decisions aggregate into organizational character. Third, patient capital enables long-term thinking in a short-term world.

The importance of timing emerges clearly. Thomas Rowe Price Jr. didn't invent growth investing in a vacuum—he recognized a shift from an industrial to a consumer economy and positioned accordingly. Similarly, today's founders must identify secular shifts and position for the future, not the present.

The value of independence stands out. By maintaining independence through multiple opportunities to sell, T. Rowe Price preserved its culture and flexibility. Many competitors who sold to banks or insurance companies lost their identity and eventually their relevance.

The Future of Active Management