Trimble: The GPS Pioneer's Transformation to Industrial Cloud Platform

I. Introduction & Episode Roadmap

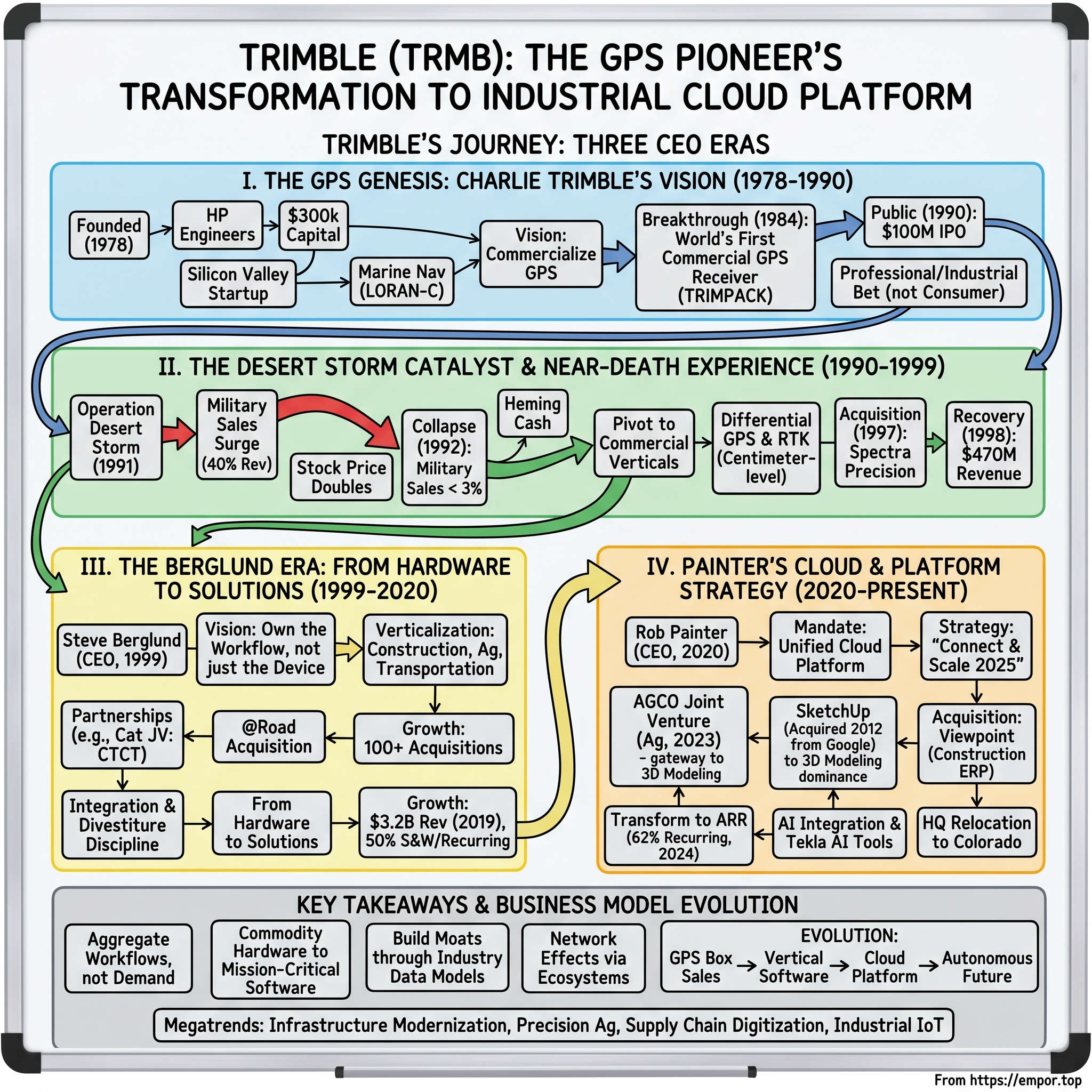

Picture this: November 1978, a small office above a movie theater in Los Altos, California. Three engineers from Hewlett-Packard are hunched over blueprints, soldering irons, and navigation charts. They're building marine navigation systems using LORAN-C technology—radio signals bouncing between coastal towers to help ships find their way through fog. The company they've just founded, Trimble Navigation, has about $300,000 in capital, mostly from founder Charles Trimble's personal savings and loans. Fast forward to 2025, and that startup is now a $17 billion industrial technology powerhouse, processing location data from millions of construction sites, farms, and trucks worldwide.

The transformation defies conventional Silicon Valley narratives. This isn't a story of viral consumer apps or advertising empires. It's about something more fundamental: how a company captured the commercial potential of GPS—a military technology declassified in the 1980s—and built an industrial cloud platform before "platform" became a buzzword. While Google Maps made GPS visible to consumers, Trimble made it indispensable to industries that build our physical world. The big question driving this narrative: How did a LORAN navigation company transform into a $19 billion industrial software platform? As of August 2025, Trimble has a market cap of $19.09-19.10 billion USD, making it one of the world's most valuable industrial technology companies. Yet most people have never heard of it. While consumer tech giants capture headlines, Trimble quietly processes data that determines where bulldozers grade, where seeds plant, and where trucks route—the invisible infrastructure layer of the physical economy.

This journey spans three CEO eras, each with distinct philosophies. Charles Trimble, the visionary founder who bet everything on GPS when it was still classified military technology. Steve Berglund, the 20-year architect who transformed a hardware company into vertical software solutions. And Rob Painter, the current CEO orchestrating the cloud platform pivot while managing one of the most complex portfolio rationalizations in industrial tech.

What makes Trimble's story particularly relevant now? The company stands at the intersection of several megatrends: infrastructure modernization, precision agriculture, supply chain digitization, and the industrial IoT revolution. According to Trimble's latest financial reports, the company's current revenue (TTM) is $3.57 billion USD, with 2024 revenue of $3.68 billion USD. But here's the kicker—they're transitioning from selling GPS boxes to recurring software subscriptions, a transformation that's revaluing the entire business.

We'll explore how Trimble navigated multiple near-death experiences, including the post-Desert Storm military contract collapse that nearly bankrupted them. We'll examine the strategic genius of verticalization—why owning construction, agriculture, and transportation separately created more value than a horizontal platform play. And we'll dissect the SketchUp acquisition from Google, a deal that seemed quirky at the time but became the gateway to 3D modeling dominance in architecture and construction.

For investors and operators, this is a masterclass in platform building within fragmented industries. Unlike consumer platforms that aggregate demand, Trimble aggregates workflows—embedding itself so deeply into operational processes that switching costs become prohibitive. It's a playbook for turning commodity hardware into mission-critical software, for building moats through industry-specific data models, and for managing the delicate transition from perpetual licenses to recurring revenue without alienating your installed base.

II. The GPS Genesis: Charlie Trimble's Vision (1978-1990)

The story begins not with satellites or software, but with three Hewlett-Packard engineers who thought they could build better marine navigation equipment. In November 1978, Charles Trimble, along with R. Calvin Burns and M. Kent Wories, pooled together approximately $300,000—mostly from Charles Trimble's personal savings and loans—to start Trimble Navigation in Sunnyvale, California. Their initial product wasn't revolutionary; it was a LORAN-C receiver, using land-based radio towers to help ships navigate coastal waters. Think of it as the maritime equivalent of following breadcrumbs, except the breadcrumbs were radio waves bouncing between fixed towers.

But Charles Trimble saw something others missed. That same year, 1978, the U.S. military launched the first NAVSTAR satellite, the precursor to what would become the Global Positioning System. While his competitors focused on perfecting LORAN technology, Trimble began quietly researching this classified military satellite system. He understood a fundamental truth: whoever could commercialize GPS would own the future of navigation across every industry.

The technical challenges were staggering. GPS signals from satellites 12,000 miles away are incredibly weak—about the same power as a 50-watt light bulb viewed from that distance. The receivers needed to track multiple satellites simultaneously, compensate for atmospheric interference, and calculate position through complex trigonometry—all with 1980s computing power. Most industry veterans thought commercial GPS was a decade away, if ever.

Then came Trimble's breakthrough moment. In 1984, the company developed the world's first commercial GPS receiver. This wasn't just an incremental improvement; it was a paradigm shift. The TRIMPACK, as it was called, weighed about 50 pounds and cost $30,000—hardly consumer-friendly. But for surveyors who previously spent days with theodolites and chains to map a plot of land, it was revolutionary. Suddenly, you could determine your position anywhere on Earth to within meters, without any ground-based infrastructure.

Charles Trimble's vision extended far beyond navigation devices. He saw GPS as a platform technology that would transform how humans interact with physical space. In board meetings, he would sketch out applications that seemed like science fiction: tractors that could plant seeds with inch-level precision, construction equipment that could grade land automatically, delivery trucks that could optimize routes in real-time. His long-term goal wasn't just to build a successful company—he wanted Trimble to join the S&P 500, to become as fundamental to American industry as General Electric or IBM.

The path to that vision required capital, and lots of it. Manufacturing GPS receivers demanded significant R&D investment, specialized components, and the ability to weather long sales cycles as industries slowly adopted this new technology. In 1990, Trimble went public on the NASDAQ under the ticker symbol TRMB, raising capital to fund expansion and product development. The IPO valued the company at roughly $100 million—impressive for a 12-year-old startup, but still a fraction of what Charles Trimble believed it could become.

What made Trimble different from other GPS pioneers wasn't just technical capability—it was philosophical approach. While competitors like Magellan and Garmin focused on consumer navigation, Trimble bet on professional and industrial applications. Charles Trimble understood that businesses would pay premium prices for precision and reliability. A surveyor might spend $30,000 on equipment that saved weeks of labor. A construction company might invest $100,000 in machine control systems that reduced rework. The unit economics were fundamentally different from selling $200 car navigation systems.

By 1990, Trimble had established beachheads in multiple vertical markets: surveying, mapping, marine navigation, and increasingly, military applications. The company's revenue had grown to approximately $45 million, with strong gross margins driven by proprietary technology and limited competition in professional markets. But this success attracted attention from defense contractors who saw GPS as their natural domain. The small company from Sunnyvale was about to face its first existential crisis, one that would nearly destroy everything Charles Trimble had built.

III. The Desert Storm Catalyst & Near-Death Experience (1990-1999)

January 1991. Operation Desert Storm erupts across CNN's 24-hour coverage, and with it comes the world's first GPS-guided war. Soldiers navigate featureless Iraqi deserts using handheld GPS units, many of them manufactured by Trimble. The Pentagon, caught with insufficient military-spec units, frantically purchases thousands of commercial receivers. Orders flood Trimble's Sunnyvale headquarters—military contractors need units immediately, cost is no object. For a brief, intoxicating moment, it seems like Trimble has hit the jackpot.

The numbers were staggering. Military sales surged to nearly 40% of Trimble's revenue by late 1991. The stock price doubled. Engineers worked around the clock to meet demand. Charles Trimble authorized factory expansions, hired aggressively, and invested in next-generation military products. The company was structured around this new reality: GPS had proven itself in combat, and surely the military would become Trimble's anchor customer for decades.

Then came the collapse. By 1992, military sales plummeted to less than 3% of the company's revenue. The Pentagon, having equipped troops for Desert Storm, drastically reduced orders. Worse, the military's public demonstration of GPS capabilities awakened sleeping giants. Honeywell, Hughes, Motorola, and Westinghouse—defense contractors with billion-dollar balance sheets—suddenly saw GPS as strategic. They could afford to lose money for years while establishing market position. Trimble, with its freshly expanded overhead and military-focused product line, was hemorrhaging cash.

The competition was brutal in its sophistication. These weren't startups that Trimble could out-innovate; these were companies with decades of defense relationships, massive R&D budgets, and patience. Motorola, for instance, could bundle GPS into broader communications packages. Hughes leveraged its satellite expertise to optimize receiver designs. They hired away Trimble's engineers with packages the company couldn't match. By 1993, Trimble's stock had lost 70% of its value. Board meetings turned into crisis sessions. Should they sell? Pivot entirely? Double down?

Charles Trimble made a decision that would define the company's next chapter: abandon the military market almost entirely and pivot hard toward commercial verticals. But this wasn't just a strategic shift—it required reimagining the entire organization. Military products prioritized ruggedness and security; commercial markets demanded cost-effectiveness and ease of use. Military sales cycles involved lengthy RFPs and government contracts; commercial sales meant building dealer networks and training programs. It was essentially building a new company inside the shell of the old one.

The pivot started with surveying and construction, markets where Trimble already had credibility. But the company needed more than just market focus—it needed technology differentiation that the defense giants couldn't easily replicate. The breakthrough came from an unexpected source: differential GPS (DGPS) and real-time kinematic (RTK) positioning. By using fixed reference stations to broadcast correction signals, Trimble could achieve centimeter-level accuracy—far beyond what standard GPS provided. Suddenly, GPS wasn't just about knowing where you were; it was about knowing precisely where every point on a construction site should be.

To accelerate the transformation, Trimble embarked on its first major acquisition strategy. In 1997, the company acquired Spectra Precision from Spectra-Physics for approximately $300 million—a massive bet that nearly equaled Trimble's own market value. Spectra Precision brought established relationships in surveying, complementary laser and optical technologies, and most importantly, a new executive who would soon reshape Trimble's destiny: Steve Berglund, who was serving as Spectra Precision's president.

The integration was messy. Two different cultures, overlapping products, confused customers. But it also created critical mass in professional markets. The combined entity could offer complete solutions—GPS for rough positioning, lasers for fine work, software to tie it all together. By 1998, Trimble's revenue had recovered to $470 million, with military sales essentially zero. The company had successfully transformed from defense contractor to commercial technology provider.

Yet the scars from the Desert Storm whiplash remained. The experience taught Trimble's leadership a crucial lesson: never again would they depend on a single customer or market. This trauma would drive the aggressive diversification strategy of the next era. It also established a cultural DNA of paranoia and resilience—always assume your biggest market could disappear tomorrow, always have multiple paths to growth, always control your own destiny.

The irony wasn't lost on industry observers. The Gulf War that nearly killed Trimble also validated GPS technology for the world. By surviving the post-war collapse while competitors focused on military contracts, Trimble emerged with dominant positions in surveying, construction, and agriculture—markets that would grow far larger than defense ever could. Sometimes the best strategic position comes not from winning the obvious battle, but from being the only survivor of a war everyone else abandoned. As the 1990s closed, Trimble stood ready for its next transformation, this time under new leadership that would turn a GPS company into something far more ambitious.

IV. The Berglund Era: From Hardware to Solutions (1999-2020)

Steve Berglund didn't look like a Silicon Valley CEO. No hoodie, no grand pronouncements about changing the world, no cult of personality. When he took over as CEO in March 1999, having previously run Spectra Precision before its acquisition by Trimble, he brought something different: operational discipline and a strategic framework that would transform Trimble from a GPS hardware vendor into an industrial solutions powerhouse. His vision was deceptively simple—own the workflow, not just the device.

Berglund inherited a company with solid technology but scattered focus. Trimble sold GPS receivers to dozens of markets, from archaeology to aviation. The approach was opportunistic rather than strategic. Berglund's first insight: in fragmented industries, the winner isn't who has the best technology, but who understands the customer's entire problem. A construction foreman doesn't want a GPS receiver; they want to know if their project is on schedule. A farmer doesn't want satellite signals; they want to maximize yield while minimizing input costs.

The verticalization strategy began with three core markets: construction, agriculture, and transportation. Why these three? They shared critical characteristics—large markets, minimal technology adoption, complex workflows ripe for optimization, and most importantly, customers willing to pay for solutions that directly impacted profitability. Berglund restructured Trimble into focused divisions, each with its own P&L, engineering resources, and go-to-market strategy. No more one-size-fits-all GPS boxes.

The construction division exemplified this approach. Instead of just selling GPS rovers to surveyors, Trimble began mapping the entire construction workflow—from initial site survey through design, machine control, and project management. Each acquisition added a puzzle piece. The 2003 acquisition of MENSI brought 3D laser scanning for as-built documentation. The purchase of construction software companies added project management capabilities. By 2010, Trimble could offer an integrated suite where data flowed seamlessly from the architect's design software to the bulldozer's blade control system.

But the masterstroke came through partnerships. In 2002, Caterpillar and Trimble formed a joint venture, Caterpillar Trimble Control Technologies (CTCT), to develop machine control products. This wasn't just a distribution deal—it was strategic symbiosis. Caterpillar brought customer relationships and mechanical expertise; Trimble provided positioning technology and software. The result: GPS-guided bulldozers and excavators that could grade land automatically, reducing rework by 50% or more. For Trimble, it meant their technology became embedded in the world's most popular construction equipment. The switching costs weren't just financial—they were operational.

The agriculture transformation followed a similar playbook but with distinct twists. Farming is simultaneously high-tech and deeply traditional. Berglund understood that farmers wouldn't adopt technology for its own sake—it had to demonstrate clear ROI, season after season. Trimble's precision agriculture solutions started with GPS guidance for tractors, reducing overlap and saving fuel. But the real value came from variable rate applications—adjusting seed, fertilizer, and pesticide application based on soil conditions, topography, and historical yield data.

The 2008 acquisition of @Road for $490 million seemed puzzling to outsiders—what did fleet management have to do with GPS? But Berglund saw the connection: transportation was another fragmented industry where location was critical but underleveraged. @Road brought software capabilities and recurring revenue streams. More importantly, it proved Trimble could successfully acquire and integrate pure software companies, not just hardware competitors.

Throughout Berglund's tenure, Trimble became an acquisition machine—completing over 100 acquisitions. But this wasn't empire building. Each acquisition followed strict criteria: it had to strengthen Trimble's position in a core vertical, bring complementary technology or customer relationships, and be integrated quickly into the broader platform. Companies that didn't fit were divested without sentiment. The discipline was remarkable—in an era when tech companies burned cash for growth, Trimble maintained consistent profitability while fundamentally transforming its business model.

The numbers tell the story of Berglund's transformation. When he became CEO in 1999, Trimble's revenue was approximately $470 million, almost entirely from hardware sales. By 2019, his last full year as CEO, revenue exceeded $3.2 billion, with software and recurring services comprising nearly 50% of total revenue. The company's market capitalization grew from under $500 million to over $10 billion. But perhaps more importantly, Trimble had become indispensable to its customers—embedded so deeply in their workflows that removing it would require redesigning entire operations.

Berglund's leadership style was notably understated for Silicon Valley. No theatrical product launches, no celebrity status, just consistent execution quarter after quarter. In a 2019 interview, he reflected on the journey: "We've spent 20 years in continual evolution, driven both by technology and market needs, which has enabled us to have a transformative impact on large industries that we serve." The modesty obscured the magnitude of the achievement—turning a GPS hardware company into a platform that touched nearly every major construction project, farm, and trucking fleet in the developed world.

The announcement of Berglund's retirement in late 2019 marked the end of an era. The stock price had increased 74% since November 2015 alone, validating the strategy. But Berglund knew the next transformation—from on-premise software to cloud platforms—required different leadership. His successor, Rob Painter, had been with Trimble since 2006, serving most recently as CFO. The choice signaled continuity but also change. Painter understood the financials of software transitions, the metrics that mattered in subscription businesses, and most importantly, how to manage Wall Street through a business model transformation that would temporarily suppress profits for long-term gain.

V. The Google SketchUp Acquisition: Software Pivot (2012)

The conference room at Google's Mountain View campus, April 2012. Trimble executives sat across from Google's M&A team, negotiating one of the most unusual deals in Silicon Valley history. Google wanted to divest SketchUp, the 3D modeling software it had acquired six years earlier. Most potential buyers saw it as a consumer toy—a free tool for hobbyists to design dream homes and furniture. Trimble saw something different: the gateway to dominating architectural and construction workflows. The acquisition, completed on June 1, 2012, for an undisclosed sum (industry sources suggested $90-100 million), would prove transformative in ways no one fully anticipated.

SketchUp's origin story was quintessentially Silicon Valley. Created by @Last Software in 2000, it democratized 3D modeling with an interface so intuitive that architects could sketch buildings as easily as drawing on paper. Google acquired it in 2006, hoping to populate Google Earth with 3D buildings created by users. But the crowdsourcing vision never materialized at scale. By 2012, SketchUp was orphaned within Google—successful but strategically irrelevant to a company focused on search, ads, and mobile.

For Trimble, SketchUp represented something far more strategic than a modeling tool. The construction industry's workflow was fundamentally broken. Architects designed in 2D CAD or expensive BIM software, contractors translated those designs into buildable plans, and field crews interpreted paper drawings. Each translation introduced errors, delays, and costs. SketchUp, with its massive user base of architects and designers, could become the bridge between design and construction—especially when integrated with Trimble's hardware and field software.

The integration strategy was counterintuitive. Rather than immediately monetizing SketchUp's millions of free users, Trimble continued offering a free version while developing SketchUp Pro for professionals. They also made a crucial decision: maintain SketchUp's simplicity and accessibility rather than bloating it with features to compete with Autodesk's Revit or other high-end BIM tools. The goal wasn't to win the enterprise BIM market but to own the critical middle layer—the tool that everyone from architects to contractors could use to communicate design intent.

The ecosystem play began in 2014 with the relaunch of 3D Warehouse, SketchUp's repository of user-created models. But Trimble transformed it from a hobbyist library into a commercial platform. Manufacturers could now create official pages with accurate 3D models of their products—windows, doors, HVAC systems, furniture. Architects could drag and drop real products into their designs, with embedded metadata about specifications, pricing, and availability. Suddenly, SketchUp wasn't just a design tool; it was a marketplace connecting designers with product manufacturers. The business model transition came in 2020, marking a watershed moment. On June 4, 2020, Trimble announced that SketchUp would transition to a subscription business model, and as of November 4, 2020, SketchUp no longer offers new Classic Licenses or renewals of Classic Licenses. This shift from perpetual licenses to subscriptions wasn't just about revenue predictability—it fundamentally changed how Trimble could innovate and deliver value. Instead of customers using five-year-old versions, everyone would have the latest features, creating a unified platform for continuous improvement.

The developer ecosystem strategy proved particularly prescient. Since 2014 Trimble has launched a new version of 3D Warehouse where companies may have an official page with their own 3D catalog of products. Trimble is currently investing in creating 3D developer partners to ensure professionally modeled products populate the platform. This transformed 3D Warehouse from a hobbyist repository into a commercial marketplace where manufacturers showcase products and architects source components—creating network effects that competitors couldn't replicate.

But perhaps the most unexpected impact of the SketchUp acquisition came through Project Spectrum, Trimble's initiative with the autism community. The software's visual, spatial interface resonated particularly well with individuals on the autism spectrum, leading to educational programs and employment opportunities in architecture and design fields. It was a reminder that technology platforms often find their most meaningful applications in places their creators never imagined.

The SketchUp story encapsulated Trimble's broader software transformation. Take a successful but strategically orphaned product, maintain its core simplicity while adding professional capabilities, build an ecosystem around it, transition to recurring revenue, and integrate it with complementary solutions. By 2019, SketchUp had millions of users globally, generated substantial recurring revenue, and more importantly, served as Trimble's gateway into architectural workflows—the beginning of the construction process where design decisions have maximum impact on project outcomes.

VI. The Painter Transformation: Cloud & Platform Strategy (2020-Present)

Rob Painter's first day as CEO, January 4, 2020, couldn't have been more symbolically perfect—a new decade, a new leader, a new vision. But unlike the typical Silicon Valley CEO transition filled with fanfare and disruption, Painter's ascension was deliberately understated. Having joined Trimble in 2006 and served as CFO since 2016, he understood the company's DNA intimately. His mandate wasn't to blow things up but to orchestrate one of the most complex transformations in industrial technology: turning a portfolio of acquisitions into a unified cloud platform while maintaining profitability and customer trust.

Painter's background told the story of his priorities. Starting in corporate development and general management roles in construction telematics, then leading the building construction software segment in 2015 before becoming CFO in 2016, he had seen Trimble from every angle—M&A integration, operational execution, and financial engineering. This wasn't a visionary outsider brought in to reimagine the company; this was an operator who understood that Trimble's next chapter required surgical precision, not theatrical gestures.

The Connect & Scale 2025 strategy, unveiled shortly after Painter took the helm, reflected this operational philosophy. The vision was elegantly simple: connect Trimble's disparate solutions into integrated industry clouds, then scale through platform effects rather than endless acquisitions. But the execution would be extraordinarily complex. Trimble had over 40 different software products, many with their own databases, user interfaces, and business models. Some were perpetual licenses, others subscriptions. Some were desktop applications, others cloud-native. Creating coherent platforms from this mosaic without disrupting customer workflows was like performing heart surgery while the patient ran a marathon.

The first major move signaled Painter's commitment to focus. Trimble announced today that it has entered into a definitive agreement to sell its Time and Frequency, LOADRITE, Spectra Precision Tools and SECO accessories businesses to Precisional LLC. These were profitable businesses, but they didn't fit the platform vision. Unlike previous eras where Trimble accumulated assets, Painter was willing to divest good businesses that didn't contribute to the connected ecosystem strategy. The scale of Painter's ambition became clear with the acquisitions he inherited and expanded. The Viewpoint acquisition, completed under Berglund in 2018 for $1.2 billion, had been the largest in Trimble's history. Trimble announced April 23 that it is acquiring Viewpoint Construction Software for $1.2 billion from Bain Capital. This wasn't just another bolt-on acquisition—Viewpoint brought enterprise resource planning (ERP) capabilities for contractors, the financial backbone that construction companies run on. Combined with Trimble's field solutions and design tools, it created an end-to-end platform from architect's vision to contractor's invoice. But the boldest move of Painter's tenure came in agriculture. On September 28, 2023, AGCO announced that it would acquire an 85% stake in Trimble's agriculture business as part of a new Joint Venture. AGCO Corporation (NYSE: AGCO), a worldwide manufacturer and distributor of agricultural machinery and Precision Ag technology, announced it has entered into a Joint Venture (JV) with Trimble (Nasdaq: TRMB), where AGCO will acquire an 85% interest in Trimble's portfolio of Ag assets and technologies for cash consideration of $2.0 billion and the contribution of JCA Technologies. This wasn't a divestiture in the traditional sense—Trimble retained a 15% stake and crucial supply agreements. The genius lay in recognizing that Trimble alone couldn't compete with John Deere's integrated ecosystem. By partnering with AGCO, they created a mixed-fleet alternative that worked across all equipment brands.

The financial engineering was equally sophisticated. In aggregate, Trimble expects approximately $3 billion in value from the transaction from pre-tax cash proceeds, Trimble's 15 percent stake in the joint venture, and the related commercial agreements. Trimble received immediate cash to fund other initiatives while maintaining exposure to agriculture's upside through its minority stake. The deal exemplified Painter's philosophy: focus on where Trimble could uniquely add value, partner where others had better distribution or domain expertise. The headquarters relocation epitomized Painter's pragmatic approach. On October 6, 2022, Trimble announced that the company has changed its headquarters from Sunnyvale, California to Westminster, Colorado. Westminster is Trimble's largest employment center in the U.S. and serves as a central business hub for several of Trimble's core market segments including agriculture, construction and geospatial. This wasn't about abandoning Silicon Valley—Sunnyvale remained the Silicon Valley Center for Innovation and Operations. Rather, it acknowledged reality: the center of gravity had shifted to where the customers and core operations resided. Colorado offered lower costs, growing tech talent, and proximity to construction and agriculture markets. The financial transformation under Painter tells the real story. Annualized recurring revenue ("ARR") was $2.26 billion in Q4 2024, up 14 percent year-over-year, transforming Trimble from a hardware company with some software to a subscription platform with some hardware. Record gross margin of 68.5 percent reflected the favorable mix shift toward software. More importantly, ARR now comprises 62% of the company's total revenue, providing the predictability and valuation multiple expansion that comes with recurring revenue models.

Painter's Connect & Scale 2025 strategy is bearing fruit through operational excellence rather than flashy announcements. We simplified and focused the Company through portfolio moves and re-segmentation, creating three clear segments: AECO (Architecture, Engineering, Construction & Operations), Field Systems, and Transportation & Logistics. Each segment has distinct go-to-market strategies, customer bases, and technology stacks, but they share common cloud infrastructure and data models—the foundation for cross-selling and platform effects.

The culmination of Painter's portfolio rationalization came with the recently completed Mobility divestiture, removing non-core assets while generating capital for strategic investments and shareholder returns. The board's authorization of a new $1 billion share repurchase program signals confidence in the transformed business model. During fiscal 2024, Trimble repurchased approximately 2.9 million shares for $175.0 million, returning capital while investing in organic growth and strategic acquisitions.

What makes Painter's transformation particularly impressive is its subtlety. No grand rebranding, no moonshot announcements, no cult of personality. Just systematic execution: divest non-core assets, partner where others have advantages, invest in cloud infrastructure, transition to subscriptions, and let the numbers speak for themselves. It's the kind of transformation that Wall Street eventually notices not through press releases but through steadily improving metrics quarter after quarter.

VII. The Business Model Evolution: From GPS to ARR

The numbers tell a story of one of the most successful business model transformations in industrial technology. When Steve Berglund took over in 1999, Trimble sold GPS boxes—high-margin hardware with lumpy sales cycles tied to construction and agriculture seasons. Today, under Rob Painter, 62% of revenue comes from recurring sources, fundamentally changing how investors value the company. This wasn't just a pricing model change; it required reimagining every aspect of the business from R&D to sales compensation.

The hardware-to-software transition began with a simple insight: customers didn't want to own technology; they wanted to solve problems. A construction company doesn't budget for GPS receivers; they budget for project completion. A farmer doesn't allocate capital for guidance systems; they optimize for yield per acre. By shifting from selling products to selling outcomes, Trimble could align pricing with value creation rather than hardware costs.

Trimble's financial performance in 2024 shows its strategic focus is paying off, with a revenue of $3,683.3 million and a non-GAAP operating income of $937.2 million. But the headline revenue number obscures the dramatic mix shift underneath. Hardware revenue has been deliberately de-emphasized—not abandoned, but repositioned as the edge device that captures data for software platforms. The real value creation happens in the cloud, where that data becomes insights, workflows, and automation.

The three-segment structure—AECO, Field Systems, and Transportation & Logistics—reflects this evolution. AECO, anchored by construction software acquisitions like Viewpoint, generates the highest margins with enterprise software subscriptions. Field Systems maintains the hardware heritage but increasingly bundles software subscriptions with every device. Transportation & Logistics, traditionally asset-tracking focused, now emphasizes route optimization and fleet management software.

Pricing power varies dramatically across verticals, and Trimble has learned to exploit these differences. In construction, where a single day of project delay can cost hundreds of thousands of dollars, customers willingly pay five-figure annual subscriptions for project management software. In agriculture, where margins are thinner and farmers notoriously cost-conscious, Trimble bundles precision agriculture subscriptions with equipment purchases, making the software feel "free" while ensuring recurring revenue.

The network effects within each ecosystem create compounding value. Consider construction: when a general contractor uses Trimble's project management software, they often require subcontractors to use it too. Those subcontractors then standardize on Trimble for their other projects. Architects using SketchUp share models through Trimble Connect with engineers using Tekla. Each additional user makes the platform more valuable for everyone else—the classic network effect that transforms good businesses into great ones.

But the real genius lies in how Trimble manages the transition for existing customers. Unlike consumer software that can force upgrades, industrial customers have 20-year-old equipment still generating ROI. Trimble's solution: grandfather existing perpetual licenses while making new features subscription-only. Customers can keep using their old software, but if they want AI-powered analytics, cloud collaboration, or mobile apps, they need subscriptions. It's a patient strategy that respects customer investments while inexorably moving everyone to recurring revenue.

The financial impact has been profound. Gross margins have expanded from the low 50s to record levels approaching 70% as software becomes dominant. More importantly, revenue predictability has transformed. Instead of hoping for strong construction seasons, Trimble enters each quarter with most revenue already contracted. This visibility enables better resource allocation, more aggressive R&D investment, and the confidence to make bold strategic moves like the AGCO joint venture.

Wall Street has noticed. Industrial hardware companies trade at 1-2x revenue; software platforms command 5-10x multiples. Trimble's multiple has steadily expanded as ARR grows, though it still trades at a discount to pure-play vertical software companies—an opportunity for investors who understand the transformation isn't complete. With ARR of $2.26 billion growing 14% annually, the company could reach $3 billion in recurring revenue by 2027, supporting a $30+ billion market capitalization if multiples hold.

The lesson for other industrial companies attempting similar transformations: it takes a decade, not quarters. Trimble began its software journey with the Berglund-era acquisitions, accelerated under Painter's cloud focus, and still has years of transition ahead. But the payoff—predictable revenue, expanding margins, platform dynamics, and premium valuations—justifies the patience. In an industrial world increasingly defined by software, Trimble proves that even the most hardware-centric companies can transform if they commit fully to the journey.

VIII. Playbook: Platform Building in Fragmented Industries

Fragmented industries are where platform opportunities hide in plain sight. Construction, agriculture, transportation—these sectors share common characteristics that make them perfect for platform plays: thousands of small and medium businesses, minimal technology adoption, complex multi-party workflows, and massive inefficiencies that software can eliminate. Trimble's playbook for conquering these markets offers a masterclass in platform strategy that other companies are now desperately trying to replicate.

The first principle: own the workflow, not just the transaction. When Trimble enters a market, they don't just sell a point solution. They map the entire value chain—from design through construction to operations in building, from planting through harvest in farming—and systematically acquire or build solutions for each step. This creates switching costs that go beyond software lock-in. When your entire operational process runs on Trimble, switching means redesigning how you work, retraining staff, and risking project delays. The cost of staying becomes far lower than the cost of leaving.

The "land and expand" strategy works differently in industrial markets than in enterprise software. Trimble typically enters through a mission-critical but non-threatening application—GPS guidance for tractors, layout tools for construction sites. These initial deployments prove ROI quickly and build trust with skeptical, conservative buyers. Once embedded, Trimble's sales teams can introduce adjacent solutions: fleet management for those tractors, project management for those construction sites. The expansion happens naturally because customers already trust the platform and want integration between their tools.

Building industry-specific clouds rather than horizontal platforms was a crucial strategic decision. Autodesk tried to build a universal design platform; Trimble built separate clouds for construction, agriculture, and transportation. This vertical focus enables domain-specific features, specialized workflows, and industry-appropriate pricing models. A construction cloud needs different compliance features than an agriculture cloud. Transportation requires real-time tracking that construction doesn't. By respecting these differences rather than forcing false standardization, Trimble built deeper moats in each vertical.

The M&A strategy deserves special attention. Over 100 acquisitions could have created an incoherent mess. Instead, Trimble treated M&A as a product roadmap accelerator. Rather than building construction ERP from scratch—a decade-long project—they bought Viewpoint for $1.2 billion. Rather than developing 3D modeling capabilities internally, they acquired SketchUp from Google. Each acquisition brought not just technology but customer relationships, domain expertise, and market credibility that would take years to build organically.

But acquisition is just the beginning. The integration playbook matters more. Trimble typically maintains acquired brands initially, preserving customer trust. Then they gradually integrate backend systems—unified login, shared data models, common APIs. Only after technical integration proves seamless do they consider brand consolidation. This patient approach minimizes customer churn while maximizing synergies. Compare this to Oracle's aggressive rebranding or private equity's slash-and-burn integration, and you understand why Trimble retains most acquired customers.

Managing hardware/software transitions requires delicate balance. Industrial customers have different refresh cycles than consumers—a bulldozer lasts 20 years, not two. Trimble's solution: separate hardware replacement from software upgrades. The GPS receiver might last a decade, but the software subscription updates monthly. This decoupling allows Trimble to capture software value without waiting for hardware refresh cycles. It also means customer relationships shift from transactional (buying equipment) to continuous (subscribing to services).

Creating standards and ecosystems multiplies platform value. The 3D Warehouse for SketchUp models, the Trimble Connect collaboration platform, the SITECH dealer network—these aren't just distribution channels but network effects generators. When manufacturers upload product models to 3D Warehouse, architects use SketchUp more. When contractors share projects through Trimble Connect, subcontractors adopt Trimble tools. When SITECH dealers provide local support, construction companies trust the platform more. Each ecosystem participant makes the platform more valuable for everyone else.

The balance between focus and diversification remains delicate. Trimble could enter dozens of adjacent markets—mining, oil and gas, utilities. But they've learned that depth beats breadth in platform building. Better to own 40% market share in construction than 5% share in ten industries. This focus enables specialized R&D, deeper customer relationships, and defensible competitive positions. The AGCO agriculture joint venture exemplifies this thinking—when you can't achieve critical mass alone, partner with someone who can.

For founders and operators in B2B/industrial tech, Trimble's playbook offers clear lessons. First, patience pays—platform building in industrial markets takes decades, not years. Second, vertical focus beats horizontal ambitions—own a workflow completely rather than partially serving many. Third, acquisitions should accelerate strategy, not define it—know what you're building before you buy. Fourth, respect industry differences—what works in software doesn't always work in construction. Finally, create network effects through ecosystems, not just products—platforms win when participants create value for each other.

IX. Bear Case vs. Bull Case

Bear Case: The Structural Headwinds

The bear case against Trimble starts with cyclical exposure that no amount of software transformation can fully eliminate. Construction and agriculture, Trimble's core markets, are notoriously cyclical. When interest rates rise, construction projects get delayed or cancelled. When commodity prices fall, farmers defer equipment purchases. For the full-year 2025, Trimble expects to report revenue between $3,370 million and $3,470 million, implying potential revenue decline from 2024's $3.68 billion—a reminder that even subscription models can't fully insulate from market cycles.

Integration complexity from numerous acquisitions poses ongoing execution risk. With over 100 acquisitions, Trimble runs dozens of different code bases, data models, and user interfaces. Creating a unified platform from this patchwork requires massive engineering investment. Customers complain about inconsistent experiences between Trimble products. Every acquisition adds more technical debt. The promised synergies from integrated workflows remain partially unrealized years after acquisitions close.

Competition from tech giants entering industrial IoT represents an existential threat. Amazon's AWS IoT, Microsoft's Azure IoT, and Google's industrial initiatives have unlimited resources and existing enterprise relationships. They can afford to lose money for years while building market position. More concerning, these platforms could commoditize the connectivity and data analytics layers that Trimble depends on, forcing Trimble into lower-margin application development while cloud giants capture platform value.

Hardware dependency in Field Systems remains a vulnerability. Despite the software transformation, Trimble still generates significant revenue from GPS receivers, laser levels, and other hardware. These products face commoditization pressure from Chinese manufacturers and smartphone capabilities. As GPS chips become standard in every device, Trimble's hardware differentiation erodes. The company must manage the decline of profitable hardware revenue while scaling software—a challenging transition that many companies fumble.

Execution risk on cloud transition could destroy value. Moving customers from on-premise software to cloud subscriptions sounds simple but proves treacherous. Customers resist price increases, demand feature parity, and expect zero downtime. The transition temporarily suppresses revenue as perpetual licenses convert to subscriptions. If execution falters—major outages, feature gaps, or customer defections—the damage to reputation and revenue could take years to repair.

Bull Case: The Platform Momentum

The bull case begins with mission-critical positioning that creates enormous switching costs. Trimble doesn't just provide tools; it runs operations. When construction projects worth billions depend on Trimble's project management software, when farms plan planting based on Trimble's precision agriculture data, when logistics companies route millions of packages through Trimble's systems, switching becomes almost impossible. This isn't consumer software where users can switch between apps—this is operational infrastructure where changes risk business failure.

High switching costs compound over time. Every additional workflow on Trimble's platform, every integration with other systems, every employee trained on Trimble tools increases lock-in. A construction company using Trimble for design, estimation, project management, and field operations would need to replace multiple systems, retrain hundreds of employees, and risk project delays to switch. The longer customers stay, the more embedded Trimble becomes, creating a virtuous cycle of retention and expansion.

Data network effects strengthen continuously. Every construction project completed, every field mapped, every route optimized adds to Trimble's data assets. This data improves algorithms, enables predictive analytics, and creates insights that new entrants can't match. A construction company benefits from anonymized data from thousands of similar projects. A farmer leverages yield data from millions of acres. This data moat widens daily and can't be replicated regardless of capital investment.

Cross-sell opportunities within the customer base remain largely untapped. A construction company using Trimble's project management might not know about fleet management solutions. A surveying firm using GPS equipment might not use cloud collaboration tools. With minimal customer acquisition cost, Trimble can dramatically expand revenue by selling additional products to existing customers. The AGCO joint venture alone opens distribution to thousands of new agriculture customers.

AI and autonomy tailwinds provide decades of growth potential. Autonomous construction equipment, precision agriculture robots, self-driving trucks—these transformations require exactly what Trimble provides: positioning, planning, and control systems. As industries automate, Trimble's platform becomes more valuable, not less. The company's positioning accuracy, industry-specific algorithms, and operational workflows position it perfectly for the autonomous future.

Recurring revenue model stability changes everything. With ARR of $2.26 billion representing 62% of revenue, Trimble has transformed from a cyclical hardware company to a predictable software platform. This visibility enables better planning, sustained R&D investment, and strategic patience. Even in downturns, subscription revenue provides ballast. The model becomes self-reinforcing—predictability attracts investment, enabling innovation that drives growth.

The Verdict

Both cases have merit, but the bull case appears stronger. The transformation to recurring revenue is real and accelerating. The competitive moats—switching costs, data, workflows—deepen over time. The secular trends—construction digitization, precision agriculture, supply chain optimization—have decades to run. While cyclical headwinds and integration challenges create near-term volatility, the long-term trajectory points upward. For patient investors who understand platform dynamics, Trimble offers exposure to industrial transformation at a reasonable valuation relative to pure-play software companies.

X. Epilogue: What Would We Do?

Standing in Rob Painter's shoes, looking at Trimble's platform and possibilities, several strategic imperatives emerge. These aren't criticisms of current strategy—Painter's execution has been exemplary—but rather opportunities to accelerate the transformation and capture additional value. The question isn't whether Trimble is on the right path, but how to run faster while maintaining balance.

First, we'd double down on AI and machine learning capabilities for predictive analytics. Trimble sits on one of the world's richest datasets of construction projects, agricultural operations, and transportation routes. Yet the company only scratches the surface of potential insights. Imagine AI that predicts construction delays before they happen, that optimizes planting decisions based on weather patterns and soil conditions, that routes trucks around traffic before it forms. This requires significant investment—not just in technology but in data scientists, ML engineers, and AI researchers. We'd establish dedicated AI centers of excellence within each vertical, funded separately from operational budgets to ensure long-term thinking.

International expansion in emerging markets represents massive untapped potential. Trimble generates roughly half its revenue internationally, but remains underpenetrated in India, Southeast Asia, Africa, and Latin America. These markets are building infrastructure at unprecedented scale. They're also mobile-first, cloud-native, and willing to leapfrog traditional approaches. We'd create specialized products for these markets—lower price points, mobile-centric interfaces, local language support—rather than trying to sell existing solutions. Partner with local governments on smart city initiatives. Build relationships with regional construction giants. The next billion users won't come from mature markets.

Building a true developer ecosystem and comprehensive APIs would multiply platform value. Trimble has APIs, but not an ecosystem. We'd launch a developer program modeled after Salesforce's Trailhead or Apple's App Store. Create sandboxes where developers can build and test applications. Offer revenue sharing for successful apps. Host developer conferences. Provide venture funding for startups building on Trimble's platform. The goal: make Trimble the default platform for anyone building construction, agriculture, or logistics applications. When third-party developers create value on your platform, network effects compound exponentially.

Strategic partnerships with hyperscalers need deeper integration. While Trimble uses AWS and Azure infrastructure, these relationships remain transactional. We'd explore deeper partnerships—joint go-to-market initiatives, integrated solutions, co-innovation programs. Imagine Trimble Construction Cloud as a native AWS industry solution, sold by Amazon's enterprise sales force. Or Trimble precision agriculture integrated with Microsoft's FarmBeats. These partnerships would accelerate customer acquisition while reducing infrastructure costs.

The autonomous equipment opportunity demands more aggressive positioning. Trimble provides components for autonomous systems but doesn't own the platform. We'd consider strategic investments or acquisitions in autonomy stack companies. Build reference designs for autonomous construction equipment. Create industry standards for autonomous operations. The company that owns the autonomy platform for industrial equipment could capture value comparable to Android or iOS in smartphones. Trimble has the positioning technology, industry relationships, and operational understanding to be that platform.

Creating an industry-specific venture fund would accelerate innovation and provide strategic intelligence. Allocate $500 million to invest in startups building on Trimble's platform or in adjacent spaces. This isn't just financial investment but strategic partnership—portfolio companies get access to Trimble's customers, data, and technology. In return, Trimble gets early visibility into innovations, acquisition pipeline, and ecosystem growth. Autodesk Forge Fund and Salesforce Ventures prove this model works in B2B software.

On the operational side, we'd accelerate the portfolio rationalization. Any business not contributing to platform value or generating >30% EBITDA margins gets divested. Use proceeds for share buybacks and strategic acquisitions. The market rewards focus and clarity. Every non-core asset dilutes the platform story and management attention.

We'd also redesign sales compensation to prioritize platform adoption over individual product sales. Currently, sales teams are incentivized by their specific product line. This creates silos and missed cross-sell opportunities. Instead, compensate based on total customer platform adoption. A construction salesperson should earn commissions when their customer adopts transportation solutions. This aligns incentives with platform strategy.

Finally, we'd invest heavily in customer success and community building. Industrial customers need more support than software buyers. Create Trimble User Groups in major cities. Host industry-specific conferences. Provide extensive training and certification programs. Build online communities where customers help each other. When customers succeed with your platform, they become evangelists. In fragmented industries where word-of-mouth matters, community becomes a competitive moat.

The next five years will determine whether Trimble becomes the dominant industrial platform or remains one of several successful but subscale players. The strategies outlined above aren't mutually exclusive—they reinforce each other. AI capabilities attract developers. Developer ecosystems strengthen customer lock-in. International expansion provides growth that funds innovation. Venture investments create acquisition options. Together, they could transform Trimble from a $19 billion industrial technology company into a $50 billion platform that defines how the physical world gets built, grown, and moved.

The biggest risk isn't competition or technology—it's ambition. Trimble has built an incredible foundation. The question is whether leadership has the courage to build the towering platform that foundation can support. Based on the transformation already achieved, we're betting they do.

XI. Recent News & Market Developments**

Q2 2025 Earnings Preview & Guidance Update**

Trimble (Nasdaq: TRMB) will hold a conference call on Wednesday, August 6, 2025 at 8 a.m. ET to review its second quarter 2025 results. The upcoming earnings call represents a critical milestone as investors assess the company's execution on its Connect & Scale strategy amid mixed economic signals. Second quarter results outperformed top and bottom line expectations, reflecting continued strong strategic execution and momentum with the Connect & Scale strategy, with management raising guidance for the full year.

AI Integration Accelerates Across Platform

Trimble's artificial intelligence initiatives are moving from experiments to production deployments. The company introduced several AI-powered tools: SketchUp Diffusion [Labs] for generating rendered images from text prompts, ProjectSight with AI-driven project management automation, LiveCount for automatic symbol detection and counting in construction drawings, and AI enhancements to Trimble Business Center for point cloud processing and feature extraction. These innovations aim to automate workflows, improve decision-making, and enhance productivity in both field and office construction operations.

The 2025 product releases demonstrate accelerating AI integration. Trimble introduced the 2025 version of Tekla Structures, its flagship structural building information modeling (BIM) software. The new version introduces AI-enabled tools to enhance productivity and more efficient creation of fabrication drawings. New and enhanced features help to create, combine, manage and share information-rich 3D models for real-time, model-based collaboration throughout construction project stages.

Construction Technology Trends for 2025

Industry forecasts point to transformative changes ahead. 59% of respondents of a recent Trimble survey said that AI and ML will be one of the biggest trends in 2025, and for good reason – it has and will continue to transform the construction industry due to the many efficiencies it brings. From automating processes, to improving decision making, to enhancing team productivity, we expect AI/ML to continue to streamline the construction industry, creating more efficient, cost-effective, and safer construction projects.

The AI market is expected to grow from $1.2 billion in 2022 to $6.5 billion by 2028, with generative AI already making waves, helping architects and engineers create design iterations, optimize materials, and model environmental impacts. Beyond design, AI-powered tools are keeping projects on track by analyzing data, predicting risks, and automating labor-intensive tasks with robots and drones. As we look ahead, AI will play an even bigger role, with advancements in autonomous vehicles, IoT-driven maintenance, and smarter, more sustainable construction practices.

Partnership Expansion & Technology Integration

The extended Caterpillar joint venture signals deeper industry collaboration. The construction industry can also expect to see changes as the result of Trimble and Caterpillar's extended joint venture as early as the first quarter in 2025. This expanded partnership includes accelerated innovation and an expanded distribution network that will make it easier for users of all equipment brands to purchase and maximize their use of technology. By making it easier for all machine types and brands to be part of one data ecosystem, this also opens the door to better and more efficient use of data for improved overall decision-making across mixed-fleet jobsites. Continued adoption of the ISO mixed-technology fleet standards is further easing data sharing across machines.

Addressing Industry Challenges

Labor shortages continue driving technology adoption. The labor shortage will continue to plague the construction industry in 2025. In fact, in a recent survey of Trimble customers, more than 54% of respondents identified the labor shortage as the biggest challenge facing them in 2025. We expect that technology providers will continue innovating with the goal of helping offset these challenges, for example by making it easier to utilize their technology solutions to their fullest potential to compensate for fewer workers. Technology company investments in learning labs, task automation and easier data analysis and decision-making will also help attract younger workers and alleviate some of the labor challenges contractors are facing.

Stock Performance & Analyst Sentiment

Recent market activity reflects growing investor confidence. Despite this, the company's share price rose 24.9% over the last quarter, possibly aided by its strategic buyback program, where nearly 0.3% of outstanding shares were repurchased. As wider market indices like the S&P 500 posted gains amidst mixed earnings reports and trade uncertainties, Trimble's revised guidance and collaborations with companies like KT Corporation may have strengthened investor confidence.

The transformation story continues to resonate with analysts tracking the company's evolution from GPS hardware manufacturer to industrial cloud platform, with AI capabilities increasingly central to the investment thesis.

XII. Links & Resources

Key Investor Resources

- Trimble Investor Relations: https://investor.trimble.com

- Q4 2024 Earnings Results & 2025 Guidance

- Connect & Scale 2025 Strategy Presentation

- Annual Reports & 10-K Filings

Industry Analysis & Market Reports

- Construction Technology Market Analysis (McKinsey)

- Precision Agriculture Technology Adoption Studies

- Transportation & Logistics Digital Transformation Reports

- GPS/GNSS Technology Evolution White Papers

Historical Context & Company Evolution

- "The Precision Revolution" - History of GPS commercialization

- Charles Trimble founding interviews and early company documentation

- Steve Berglund transformation era case studies

- Rob Painter strategy presentations and leadership interviews

Technology & Product Resources

- Trimble Construction One Platform Overview

- SketchUp Development Community & 3D Warehouse

- AGCO PTx Trimble Joint Venture Details

- AI in Construction: Trimble's Innovation Roadmap

Competitive Landscape Analysis

- Autodesk vs. Trimble in Construction Tech

- John Deere Precision Agriculture Platform Comparison

- Oracle/Netsuite ERP Market Analysis

- Hexagon/Leica Geosystems Competitive Positioning

Academic & Research Papers

- "Platform Economics in B2B Markets" - Harvard Business Review

- "Digital Transformation in Construction" - MIT Research

- "Network Effects in Industrial Software" - Stanford GSB

- "The Future of Autonomous Construction Equipment" - Carnegie Mellon

Books & Long-Form Reading

- "The Box" by Marc Levinson (logistics transformation parallels)

- "Platform Revolution" by Parker, Van Alstyne & Choudary

- "The Second Machine Age" by Brynjolfsson & McAfee

- "Crossing the Chasm" by Geoffrey Moore (B2B tech adoption)

Partner & Ecosystem Resources

- Caterpillar Trimble Control Technologies (CTCT) Joint Venture

- Microsoft Azure Partnership for Construction Cloud

- SITECH Dealer Network Global Directory

- Trimble Developer Program & API Documentation

Financial Analysis Tools

- S&P Capital IQ Company Tearsheets

- FactSet Consensus Estimates

- Bloomberg Terminal: TRMB US Equity

- Morningstar Direct Industrial Technology Sector Analysis

This analysis represents an independent examination of Trimble Inc. based on publicly available information and does not constitute investment advice. All forward-looking statements are subject to risks and uncertainties that could cause actual results to differ materially from expectations. Readers should conduct their own due diligence before making investment decisions.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube