Tripadvisor, Inc. (TRIP): From the Blue Owl to the Experiences-Led Pivot

I. Introduction & The June 2026 Showdown

On the morning of June 15, 2026, the press releases hit the wires in two languages and from two very different worlds. One came from a 175-year-old American financial institution that prints platinum cards and underwrites the spending of the global affluent. The other came from a Massachusetts internet company whose corporate avatar is a wide-eyed, multi-colored owl. The news: American Express had agreed to buy TheFork — the European restaurant-reservation platform — from Tripadvisor in an all-cash deal worth roughly $700 million.1

Sit with that number for a second. Seven hundred million dollars. On the day the deal was announced, that figure represented something close to 46% of Tripadvisor's entire market capitalization.2 In other words, a company was selling one of its three operating businesses — and the check it received back was nearly half of what the public markets thought the whole enterprise was worth. When a single non-core asset fetches that large a slice of your total value, the market is telling you something uncomfortable: that it has stopped believing in the sum of your parts.

How did we get here? How does a company that was, only a decade earlier, the undisputed king of organic travel search — a business worth more than $12 billion at its 2014 peak, the literal front door of the internet's travel funnel — end up being carved apart, piece by piece, under the watchful eye of activist investors?3

This is the thesis of today's episode, and it's one of the richest corporate transition stories in modern tech. Tripadvisor was a world-class lead-generation machine — arguably one of the most beautiful arbitrage businesses ever built on the open web. It harvested free traffic from Google and sold that traffic, at fat margins, to the online travel agencies who were desperate for high-intent customers. And then, over the course of roughly eight years, that machine was systematically dismantled — partly by forces beyond its control (Google decided it wanted the tollbooth for itself), and partly by one of the most expensive self-inflicted wounds in the history of consumer internet: a product called Instant Booking.

But here's the twist that makes this story worth three and a half hours of your life. While the core business was quietly bleeding out, the same management team — in a single remarkable summer — made two of the most disciplined, asymmetric capital-allocation bets of the entire 2010s. They bought a sleepy tours-and-activities marketplace called Viator and a French restaurant-booking app called LaFourchette, the company that would become TheFork. Together they cost about $340 million. Together they would go on to define what Tripadvisor is in 2026.

So the roadmap for today: we start in a Needham pizza shop in 2000. We move through the SEO glory years and the metasearch gold rush. We dissect the Instant Booking disaster and Google's slow strangulation of organic search. We get into the genuinely thrilling corporate-governance cage match involving John Malone's Liberty empire, Greg Maffei, and a Delaware courtroom that ended up rewriting where American companies choose to incorporate. And we land in the present: a leaner, activist-pressured, experiences-led Tripadvisor under CEO Matt Goldberg, betting its future on a marketplace most travelers have used without ever knowing its name.

Let's go back to the beginning.

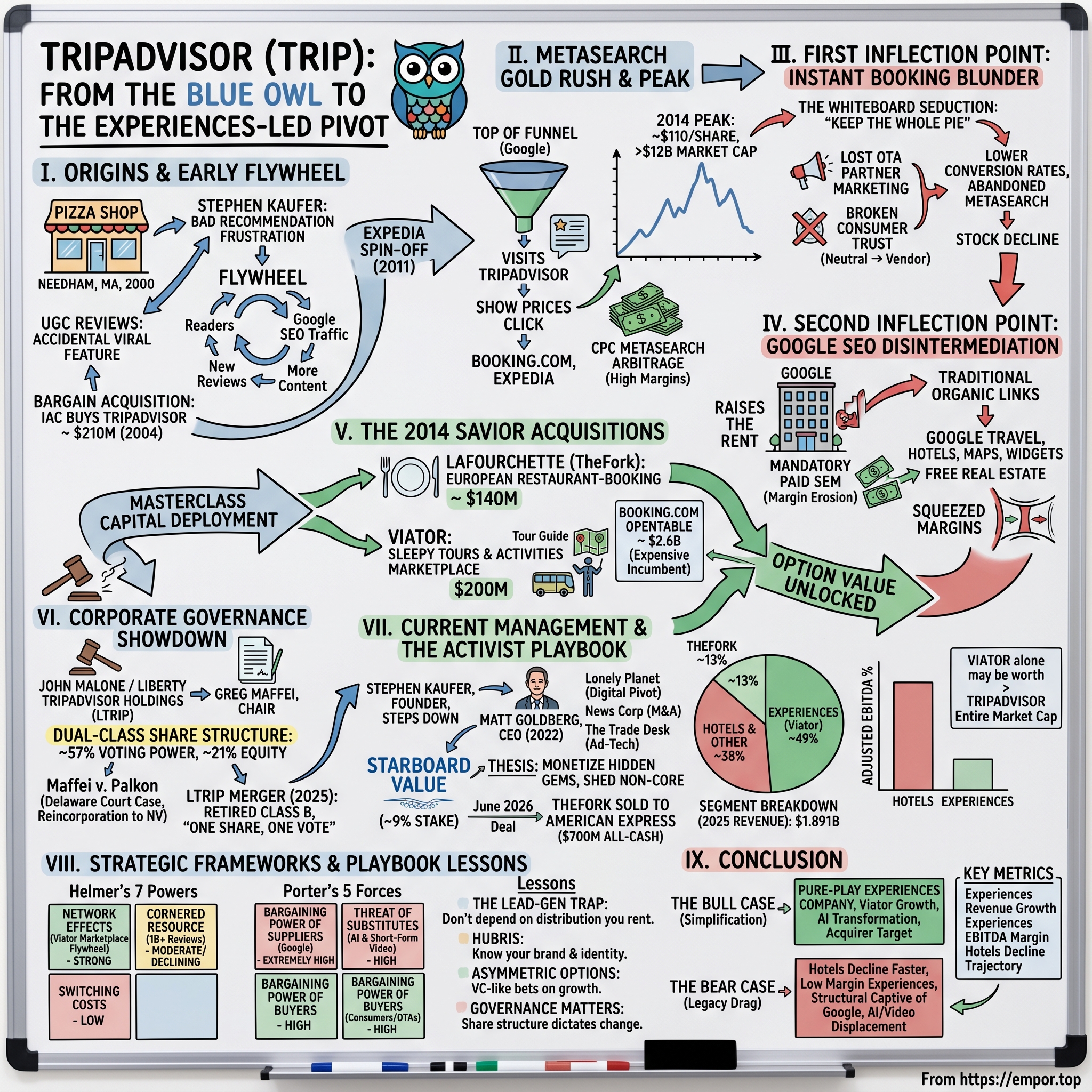

II. Succinct Origins: From a Needham Pizza Shop to the Expedia Spin-Off

The founding myth of Tripadvisor is, fittingly for a reviews company, a story about a bad recommendation. In 2000, a software engineer named Stephen Kaufer was trying to plan a vacation. He went online, found a tour operator, booked it based on the glossy marketing copy — and the trip was a disappointment. Kaufer walked away from the experience with a simple, frustrated question: why was it so hard to find an honest opinion about a place before you spent your money on it?

That frustration became a company. Kaufer co-founded Tripadvisor in 2000, working out of office space in Needham, Massachusetts — famously, above a pizza shop. But here's the detail most people get wrong about the origin story: the original business was not user-generated reviews. Kaufer's first idea was a B2B play — an official, machine-readable search engine that would aggregate content from professional travel guides and editorial sources, and then license that index to other travel websites. It was meant to be the plumbing behind the scenes, not a consumer destination.

That business did not work. The licensing model was slow, the professional content was thin, and traffic was anemic. So the team did what desperate early-stage founders do: they threw a Hail Mary feature onto the site. They added a simple box that let ordinary travelers post their own candid reviews and upload their own photos of hotels and restaurants. No gatekeepers, no editors, no marketing department deciding what you should think.

It went viral. The "wisdom of crowds" — the aggregated, unvarnished verdict of thousands of real travelers — turned out to be far more valuable than any professional guidebook. People trusted the messy honesty of a fellow tourist who'd actually slept in the lumpy bed more than they trusted a brochure. The accidental feature became the entire company. This is the first great lesson of the Tripadvisor story, and we'll return to it: the most valuable asset they ever built was the one they almost didn't build at all.

The flywheel was elegant. Reviews attracted readers; readers searching for travel information attracted Google's algorithm; Google sent enormous volumes of free traffic; some of that traffic stayed to write new reviews; the new reviews attracted more readers. The content compounded, and the search rankings compounded with it.

It didn't take long for the industry's power players to notice. In 2004, Barry Diller's IAC (InterActiveCorp) acquired Tripadvisor for a price that, in hindsight, looks like one of the great bargains in internet history: roughly $210 million.4 A year later, in 2005, IAC spun its travel assets — including Tripadvisor — into a new publicly traded entity called Expedia Group. For the next six years, Tripadvisor sat inside Expedia, quietly becoming the most profitable, highest-margin jewel in the portfolio.

By 2011, that jewel had grown too big and too distinct to stay hidden. In December 2011, Expedia spun off Tripadvisor as a standalone public company on the Nasdaq under the ticker TRIP. The newly independent company arrived on the market with three things: a commanding lead in global travel reviews, an instantly recognizable mascot — the multi-colored owl the world would come to know as "Ollie" — and a business model so profitable it almost seemed unfair. To understand just how good that model was, we need to look under the hood.

III. The Metasearch Gold Rush & Peak Tripadvisor

Here's a question that confuses a lot of people about Tripadvisor's golden years: if the company didn't sell hotel rooms, didn't sell flights, and didn't take a cut of your vacation — how on earth did it make so much money?

The answer is one of the most beautiful business models the open internet ever produced, and it's worth slowing down to explain it in plain terms, because everything that comes later — the blunders, the activists, the breakup — only makes sense once you understand how good this thing was.

Picture the travel-shopping journey as a funnel. At the very top, a traveler types "best hotels in Rome" into Google. They don't know where they want to stay yet; they're just dreaming and comparing. Tripadvisor positioned itself precisely at this top-of-funnel moment — the instant of consideration, before any decision has been made. A traveler would land on a Tripadvisor page packed with reviews, photos, and rankings, scroll through the candid verdicts of people who'd been there, and eventually narrow down to a hotel they liked.

And then came the magic moment. Next to that hotel sat a button: "Show Prices." The traveler clicks. Up pop the rates from a row of online travel agencies — Booking.com, Expedia, Hotels.com, and others — each competing for the booking. And every single time a user clicked through to one of those agencies, the agency paid Tripadvisor a fee. This is the cost-per-click, or CPC, metasearch model.

Think about what's happening economically. Tripadvisor was running a pure arbitrage. On one side, it acquired its inventory — high-intent travelers — essentially for free, harvested from Google's organic search results. On the other side, it sold those travelers to the OTAs, who were locked in a brutal, expensive war to acquire customers and would happily pay a premium for someone already standing at the bottom of the funnel with a credit card warming up. Tripadvisor was the matchmaker who charged both the demand and the supply side, carried no inventory, took no booking risk, and paid almost nothing for its raw material. The gross margins were extraordinary.

And the customers on the buy side were enormous. The two dominant OTAs — Expedia and the company then known as Priceline (later Booking Holdings), the parent of Booking.com — were among the largest digital advertisers on the planet. For years, a meaningful share of Tripadvisor's revenue flowed from just these two customers. That concentration was a strength in the boom and, as we'll see, a loaded gun in the bust.

The numbers tell the story of the peak. Revenue scaled past $1.2 billion, carried on the kind of EBITDA margins that software investors dream about.3 The market fell in love. In 2014, the stock rocketed to an all-time high of around $110 a share, valuing the company at more than $12 billion.3 Tripadvisor wasn't just a travel website; it was, in the most literal sense, the starting point of the internet's entire travel economy — the front door through which hundreds of millions of trips began.

It was, by any measure, a perfect business. Which, of course, is exactly when the people running a perfect business start to get nervous. Because if you're only the matchmaker — if you're only renting out the click — then someone else is keeping the truly enormous prize: the transaction itself. And in 2014, at the very summit of the mountain, Tripadvisor's management looked down at all that economics flowing past them to the OTAs and decided they wanted it. That decision nearly broke the company.

IV. The First Inflection Point: The "Instant Booking" Blunder

There's a particular kind of trap that snares successful companies, and it almost always wears the costume of ambition. You've built a wonderful business doing one thing. You look downstream and see another company doing a related thing and capturing more dollars per customer. And you think: why should they get that? We sent them the customer. We should keep the whole pie.

That is the psychology that produced Instant Booking, and it is the most expensive strategic error in Tripadvisor's history.

The logic, on a whiteboard, was seductive. Tripadvisor sat at the top of the funnel, generating intent. The OTAs sat at the bottom, capturing the booking and the booking economics. Management's reasoning went: why hand the traveler off to Booking.com at the final step and collect a modest click fee, when we could let the traveler complete the entire reservation inside Tripadvisor and keep far more of the value? So in 2014, the company rolled out Instant Booking — a feature that let a user book a hotel room directly on Tripadvisor, without ever leaving the blue owl's nest.

The problem is that a whiteboard doesn't capture relationships, and it doesn't capture trust. Both of those things shattered.

Start with the relationships. The instant Tripadvisor launched Instant Booking, it stopped being the OTAs' single most valuable customer-acquisition partner and became their direct competitor. Booking.com and Expedia were not amused. For years they had paid Tripadvisor handsomely for clicks; now Tripadvisor was trying to keep the customer for itself. The retaliation was rational and swift: the big OTAs pulled back their marketing bids on the platform. And remember the concentration we flagged earlier — when a giant slice of your revenue comes from two customers, and those two customers decide to spend less because you just declared war on them, the hole in your income statement is immediate and deep. Tripadvisor had picked a fight with the very partners who funded its profitability.

Now the trust problem, which was subtler and in some ways worse. For more than a decade, consumers had built a precise mental association with the blue owl: this is the neutral place I go for honest, crowdsourced opinions. Tripadvisor was Switzerland — the disinterested referee you consulted before you went off to transact somewhere else. The brand's entire authority rested on the perception that it wasn't trying to sell you anything. Instant Booking violated that contract. Suddenly the referee was also a vendor. Consumers were confused; the booking flow felt unfamiliar and bolted-on; and conversion rates — the percentage of shoppers who actually completed a purchase — cratered. People simply did not want to buy from the place they went to research.

So Tripadvisor ended up with the worst of both worlds. It alienated the high-margin CPC customers who had paid the bills, and it failed to build a transactional business strong enough to replace them, because its own brand fought the effort at every step. Instead of expanding its share of the travel economics, it cannibalized the most profitable revenue it already had. The much-anticipated transaction windfall never materialized at scale; the click revenue it sacrificed was very real.

The stock told the story without mercy. From that 2014 peak above $110, the shares began a long, grinding, multi-year decline. Management would spend years walking Instant Booking back, eventually de-emphasizing it and returning to a more open, metasearch-style model. But the core hotel business never recovered its former glory. And the cruel part is that even if Instant Booking had been executed flawlessly, a second, larger force was already gathering on the horizon — one that no amount of strategic course-correction could stop. The landlord of the entire internet had decided to raise the rent.

V. The Second Inflection Point: Google's SEO Disintermediation

To understand the existential threat that arrived next, you have to remember where every Tripadvisor visit actually began. It began on Google. The whole magnificent arbitrage machine — the free traffic, the high margins, the perch at the top of the funnel — rested on a single, unspoken assumption: that when someone searched "best hotels in Rome," Google would reward Tripadvisor's deep well of reviews with the top organic results. For years, that assumption held. Tripadvisor owned those blue links. It was, for a long stretch, one of the most SEO-dominant websites in the entire travel category — the textbook example of how to win the organic search game.

But there is a fundamental, structural vulnerability buried in that success, and it's the second great lesson of this episode: if your entire customer-acquisition engine depends on a platform you don't own, then you are a tenant. And the landlord can change the terms whenever it likes.

Google changed the terms. Over a period of years, the search giant rolled out its own travel products — Google Travel, Google Hotels, Google Maps reviews, the interactive local "map pack." And it began doing something that quietly reshaped the economics of the entire web: it pushed the traditional organic links — the free ones that Tripadvisor depended on — further and further down the page. Above them, increasingly, Google placed its own content: its own interactive maps, its own hotel-price comparison widgets, its own booking modules, its own review snippets. The free real estate at the top of the results page, the prime beachfront property that Tripadvisor had occupied for free, was steadily annexed by the landlord for its own use.

The analogy that captures it best: imagine you run a wildly successful shop, and your shop's secret is that it sits at the exit of the world's busiest train station, so foot traffic costs you nothing. Then the railway company that owns the station decides to open its own competing shop — and to build it right at the platform exit, in front of yours, so that every passenger sees the railway's shop first. You haven't moved. Your shop is just as good as it ever was. But the river of free customers has been diverted, and now the only way to get them is to pay the railway for advertising placement.

That's precisely what happened. To keep the traffic flowing, Tripadvisor was increasingly forced to shift from free organic SEO to paid search marketing — buying Google ads (SEM) for the very visitors it used to receive for nothing. This is the death-spiral mechanic. Every dollar paid to Google to recover lost traffic was a dollar of pure margin erosion. The business hadn't gotten worse at what it did; the cost of its core input — customer attention — had simply gone from roughly zero to a large and growing line item. The historical operating margins that had made Tripadvisor a market darling were squeezed from both ends: Instant Booking had damaged the revenue side, and Google's encroachment was now inflating the cost side.

This is the recurring tragedy of businesses built on someone else's distribution. They look like technology companies, but their economics are those of a tenant farmer working land they'll never own. For Tripadvisor's legacy hotel business, the Google squeeze wasn't a storm to be weathered — it was a permanent change in climate.

And yet. While the front door of the house was being slowly bricked up, two rooms in the back were quietly being built out — rooms that almost nobody on Wall Street was paying attention to in 2014. Those two rooms would end up being worth more than the rest of the house combined.

VI. Masterclass Capital Deployment: The 2014 Savior Acquisitions

Let's rewind to the summer of 2014 — the same year as the stock peak, the same year Instant Booking launched, the same year the Google clouds were gathering. It's a strange thing about this period in Tripadvisor's history: while one part of the company was busy making its single worst strategic decision, another part was quietly making two of its best. Both sets of choices flowed from co-founder Stephen Kaufer, still CEO, and history has judged them very differently.

The two acquisitions were small enough that they barely registered as headlines at the time. In May 2014, Tripadvisor bought a French restaurant-reservation company called LaFourchette — literally "the fork" — for a price reported around $140 million.[^5] LaFourchette was the dominant table-booking platform in France and was expanding across Spain and other European markets. Two months later, in July 2014, Tripadvisor acquired Viator, a San Francisco-based booking platform for tours and activities, for $200 million in cash.[^6] At the time of purchase, Viator was a relatively modest operation — a marketplace with roughly 20,000 bookable tours and experiences, connecting travelers with the people who run walking tours, cooking classes, snorkeling trips, and skip-the-line museum tickets around the world.[^6]

Now, to appreciate why these two deals were a masterclass, you have to look at what one of Tripadvisor's much larger rivals did in the very same window — because it provides the perfect natural experiment in capital discipline.

In June 2014, sandwiched right between the LaFourchette and Viator deals, Priceline — soon to rebrand as Booking Holdings — announced it was buying OpenTable, the American restaurant-reservation incumbent, for $2.6 billion in cash.[^7] Read those numbers side by side and let the contrast land. For the restaurant-booking opportunity alone, Booking paid $2.6 billion for the U.S. leader. Tripadvisor paid roughly $140 million for the European leader in the same category — less than one-eighteenth the price.[^5][^7] And the OpenTable deal did not age gracefully: Booking struggled to scale OpenTable's reservation model internationally, and the asset's value would later be written down by a substantial amount as the synergies failed to materialize at the price paid. Booking bought the expensive incumbent at the top; Tripadvisor bought the disciplined regional challenger at a fraction of the cost.

That's the strategic frame: don't overpay for the famous American brand when you can buy the dominant European franchise for pennies on the dollar. But the truly important part isn't the cleverness of the entry price. It's what these two seeds grew into.

Consider where they landed by the mid-2020s. Viator — that 20,000-listing afterthought — grew into the crown jewel of the entire company, a tours-and-activities marketplace generating revenue approaching $1 billion a year and routinely discussed by analysts as a standalone asset worth $2 billion or more.5 And LaFourchette, rebranded as TheFork, scaled across roughly a dozen European countries to become the continent's leading dining-reservation network — the asset American Express agreed to buy in June 2026 for $700 million.1

Do the arithmetic on the whole campaign. Tripadvisor deployed somewhere around $340 million of 2014 capital across these two bets. More than a decade later, that capital had been transformed into well over $3 billion of enterprise value — a Viator worth multiples of its purchase price, plus a $700 million cash exit on TheFork.15 This is the third great lesson of the episode, and it's one every operator with a cash-generating core should tattoo somewhere visible: when your legacy business is a cash cow in slow decline, the smartest thing you can do is use that cash to buy fast-growing adjacent networks. You are buying options. Most options expire worthless. But you only need one Viator to offset the terminal decline of the thing that funded it.

The dying hotel business, in a very real sense, paid for its own replacement. The problem was that for years, the market refused to give Tripadvisor any credit for it — the shiny new growth engines were buried inside a holding company whose stock was being dragged down by the legacy decline and, as we're about to see, controlled by a man whose interests didn't always point in the same direction as ordinary shareholders'. To understand why those buried treasures stayed buried for so long, we have to talk about the most fascinating character in this entire story — and he wasn't even a Tripadvisor employee.

VII. The Corporate Governance Showdown: Greg Maffei & Maffei v. Palkon

Every great business saga has an architect of financial structure lurking in the wings — someone who thinks not in products but in share classes, voting power, and tax-efficient spin-offs. In the Tripadvisor story, that role belongs to the orbit of John Malone, the legendary cable magnate, and his longtime lieutenant Greg Maffei. To understand the modern Tripadvisor, you have to understand that for more than a decade, ordinary shareholders didn't actually control the company. The Liberty empire did.

Here's the mechanism, and it's a classic of the Malone playbook. Tripadvisor was a "controlled company," held under a vehicle called Liberty TripAdvisor Holdings, or LTRIP, chaired by Maffei. The genius — or, depending on your seat, the trap — was in the share structure. Through Class B super-voting shares, Liberty TripAdvisor commanded roughly 57% of Tripadvisor's voting power while owning only about 21% of its actual equity.[^9] Read that again. A bit more than a fifth of the economic ownership translated into outright voting control. This is the dual-class structure in its purest form: a small slice of the money buys the entire steering wheel.

For a while, there's a defensible case for this kind of arrangement. Dual-class structures can shield a company from short-term market panic and let management invest through rough patches without fear of being tossed out. But the same structure that protects can also trap. When the controlling shareholder's incentives diverge from everyone else's — when the person holding the steering wheel owns only a fifth of the car — capital can get locked in place, and necessary, value-unlocking decisions (like, say, selling off hidden gems to the highest bidder) simply don't happen, because they don't suit the controller.

The drama crystallized around an arcane-sounding but genuinely consequential question: which U.S. state's laws should govern the company? In 2023, Maffei and the board moved to reincorporate Tripadvisor out of Delaware — the default home of corporate America — and into Nevada. Why Nevada? Because Nevada's statutes are famously protective of directors and officers, offering far stronger shields against fiduciary-duty lawsuits than Delaware's more shareholder-friendly courts. Minority shareholders cried foul. They sued, in a case that became known as Maffei v. Palkon, arguing that Maffei and the board were using the machinery of reincorporation to insulate themselves from liability — effectively rewriting the rulebook mid-game to protect the people holding the controlling votes.6

This became a landmark fight, because it touched a question with implications far beyond one travel company: can a controlling shareholder move a company to a friendlier legal jurisdiction, capturing a personal benefit (reduced litigation exposure) in the process, without compensating the minority for what they're giving up? In February 2024, a Delaware court declined to block the move, ruling against the shareholders who had tried to stop the Nevada migration.6 The matter ultimately reached the Delaware Supreme Court, which allowed the reincorporation to proceed — a decision watched closely across corporate America as part of a broader wave of companies reconsidering their Delaware allegiance.

And then came the resolution that actually mattered for investors. With the legal path cleared, the stage was set for a historic restructuring. In April 2025, Tripadvisor completed a merger with Liberty TripAdvisor Holdings, in a transaction valued at roughly $435 million, that retired all of the Class B super-voting shares and dissolved the Liberty control structure entirely.[^11] In one stroke, Greg Maffei's grip was gone, and Tripadvisor became a clean, "one share, one vote" company for the first time in its independent life.[^11]

This is the hinge on which the entire modern story turns. As long as the Class B block existed, no outside investor could force a strategic rethink, because the votes simply weren't there to be won. The moment that block was retired, Tripadvisor transformed from an impregnable fortress into something every undervalued, sum-of-the-parts company eventually attracts when its defenses fall: a target. The governance change didn't just tidy up the cap table — it fired the starting gun. And the runners were already at the blocks.

VIII. Current Management & The Activist Playbook

Before we get to the activists, we need to meet the man tasked with steering through the storm — because in July 2022, Tripadvisor did something it had never done before. It replaced its founder.

Stephen Kaufer, who had run the company since that pizza-shop beginning in 2000, stepped down as CEO, and in came Matt Goldberg. If you were designing a résumé for someone meant to drag a Web 1.0 reviews company into the experiences-and-AI era, you might design Goldberg's. He had served as CEO of Lonely Planet, where he orchestrated the storied travel-guide brand's wrenching transition from print to digital — exactly the kind of legacy-to-modern pivot Tripadvisor needed. Before that, he'd been head of M&A at News Corp, giving him a dealmaker's instincts, and he'd run North America as an executive vice president at The Trade Desk, the programmatic ad-tech giant — meaning he understood, intimately, the digital advertising and data ecosystems that both fund and threaten a business like Tripadvisor.7 In other words: a digital-transition operator, a deal guy, and an ad-tech native, all in one hire.

Goldberg's compensation structure tells you what the board actually wanted from him, and it's worth reading like a strategy document. His total package has averaged in the neighborhood of $10 million a year, but the base salary is only $900,000 — a small fraction of the whole.7 The rest is engineered for alignment. His annual cash bonus is split 50/50: half tied to consolidated revenue, half to adjusted EBITDA — twin gauges that force him to balance growth against profitability rather than chasing one at the expense of the other.7 On top of that sits an annual equity grant targeted around $6.35 million, divided evenly between time-vesting restricted stock units (which reward him for staying) and performance-vesting stock units, or PSUs (which reward him only if the company actually hits its targets).7 And critically, Goldberg has real skin in the game: he directly owns roughly 0.22% of the common stock — on the order of 315,000 shares — so his personal wealth rises and falls with the turnaround he was hired to execute.7

Now, back to that starting gun. The instant the Liberty Class B control structure was eliminated in April 2025, Tripadvisor became exactly the kind of company activist investors dream about: undervalued, controlled by no one, sitting on hidden assets, and run by a management team that — conveniently — was already trying to do roughly what an activist would demand. Into that opening stepped Starboard Value, one of the most respected and disciplined activist hedge funds on Wall Street, which built a stake of around 9% in Tripadvisor.8

Starboard's thesis was the same one we've been building toward all episode: the market was valuing Tripadvisor as a melting ice cube of a hotel-metasearch business, while essentially ignoring the multi-billion-dollar growth engine of Viator buried inside it, and giving little credit for the cash value of TheFork. The activist playbook practically wrote itself — monetize the crown jewels that the market won't price, shed the non-core assets, and force the whole enterprise to be valued for what it actually contains.

What's notable — and what makes this less a hostile war than a strategic alignment — is that Goldberg and Starboard largely agreed. The result was the sequence of moves that frames this entire episode: the June 2026 decision to sell TheFork to American Express for $700 million in cash, paired with an aggressive cost-cutting and restructuring program designed to redirect the company's people, capital, and attention almost entirely toward Viator and the experiences business.1 In effect, management and activist locked arms to simplify a sprawling, misunderstood conglomerate into something the market could finally price: a pure-play experiences company with a cash cushion and a declining legacy tail.

To see why everyone — activist, CEO, and acquirer alike — was so focused on this restructuring, you have to look at the actual segment math. Because once you do, the "hidden gem" stops looking hidden and starts looking obvious.

IX. Segment Breakdown: The "Hidden" Multi-Billion Dollar Engine

Numbers can hide a company's true shape, and for years Tripadvisor's reported financials did exactly that — blending a fast-growing star and a slow-declining legacy into a single muddy aggregate that satisfied no one. So in late 2025, management realigned the way it reports the business, and the new structure is essentially a confession of where the future lies. Effective the fourth quarter of 2025, Tripadvisor began reporting in three segments.9

The first is Experiences — which consolidates the Viator brand together with the experiences-related operations of the core Tripadvisor brand. This is the growth engine, the thing the entire strategy now orbits. The second is Hotels and Other — the legacy hotel-metasearch business plus display advertising, the cash-generating but structurally challenged operation we spent two whole sections watching get squeezed by Instant Booking and Google. The third is TheFork — the European dining-reservation engine, now reported separately and slated to come off the books entirely once the American Express transaction closes, expected in late 2026.19

Now the figures that explain everything. For full-year 2025, Tripadvisor reported consolidated revenue of $1.891 billion.9 Of that, the Experiences segment — Viator and friends — generated $924 million, up roughly 10% year over year, which works out to nearly half of the entire group's revenue.9 Sit with that. The business unit that Wall Street couldn't be bothered to value in 2014 is now, a decade later, just about half the company by revenue, and still growing at a healthy double-digit clip while the legacy segment stagnates.9

There is, of course, a catch — and it's an important one for understanding the bull-bear tension. Experiences punches well below its revenue weight on profitability. The segment contributes only around 30% of consolidated adjusted EBITDA, even though it represents close to 50% of revenue.9 In plain terms: Viator is a lower-margin business than the legacy hotel cash cow. Tours-and-activities is a real marketplace with real costs — heavy marketing spend to acquire travelers, payments to operators, the unglamorous work of onboarding hundreds of thousands of local tour providers. It's growing fast, but it's not yet throwing off the kind of fat, lazy margins the old metasearch business once did. The strategic bet is that Experiences can keep growing into its profitability while the high-margin legacy business shrinks — a race between Viator's expansion and Hotels-and-Other's decline.

This brings us to the valuation puzzle that made Starboard salivate and that frames the whole 2026 situation. On a standalone basis, Viator's closest comparable peer — the German tours-and-activities marketplace GetYourGuide — was valued in the private markets at roughly $2 billion.10 Apply anything like that yardstick to Viator, and you reach a conclusion that sounds absurd until you check it twice: Viator alone may be worth more than Tripadvisor's entire consolidated market capitalization, which hovered around $1.5 billion.210 Which means that at prevailing prices, an investor buying the whole of Tripadvisor was arguably paying for Viator and getting the legacy hotel business — and the incoming $700 million of fresh American Express cash — thrown in for free.12

That is the "sum-of-the-parts" disconnect in its starkest form, and it is the entire reason this company became a battleground. But a cheap-looking valuation is only an opportunity if the underlying business can actually defend itself. So let's war-game it properly.

X. Strategic Frameworks: Hamilton's 7 Powers & Porter's 5 Forces

A low valuation tells you what the market feels. Strategic frameworks tell you whether those feelings are justified. So let's run Tripadvisor's two halves — the fading legacy and the ascendant Viator — through Hamilton Helmer's 7 Powers and Michael Porter's 5 Forces, and see what kind of moat actually exists.

Start with Helmer's 7 Powers, the framework for durable competitive advantage.

The strongest power in the portfolio is Scale Economies / Network Effects, and it lives in Viator. Viator is a two-sided marketplace: on one side, hundreds of thousands of local tour and activity operators listing their offerings; on the other, the travelers who book them. The dynamic is self-reinforcing — the more operators list on Viator, the more comprehensive its inventory, which attracts more travelers, which makes the platform more attractive to new operators, who add more inventory. This is the classic marketplace liquidity flywheel, and it is genuinely powerful, especially in North America, where Viator's density of supply has been hard for rivals to replicate. European giant GetYourGuide and the Asia-Pacific powerhouse 客路 Klook both run formidable marketplaces, but breaking Viator's North American liquidity loop has proven stubbornly difficult — once a marketplace reaches critical mass in a geography, dislodging it requires not a better product but a better network, which is far harder to build.10

The second power is a Cornered Resource, and here the verdict is moderate and declining. Tripadvisor's legacy database of over a billion traveler reviews is a genuinely unique asset — a moat of accumulated content no competitor can simply buy. But its potency is eroding. Google's own reviews ecosystem, and the explosion of travel discovery on social platforms, mean that this once-untouchable resource is steadily losing its grip on the traveler's attention. It's still valuable; it's just no longer the kingmaker it was in 2012.

The third power worth flagging is Switching Costs, and the honest assessment is that they are very low. This is the uncomfortable truth at the heart of the experiences business. A traveler planning a trip to Lisbon can open Viator, GetYourGuide, Klook, and Airbnb Experiences in four browser tabs and price-compare a walking tour in ninety seconds. There is nothing locking them in — no data, no subscription, no accumulated history that makes leaving painful. Low switching costs mean the marketplace must win on selection and price every single time, which is precisely why marketing spend is so heavy and margins are thinner than the old metasearch business.

Now Porter's 5 Forces, which maps the structural attractiveness of the industry itself.

Threat of New Entrants: Low. This is Tripadvisor's friend. Replicating a billion reviews and, more importantly, onboarding 300,000-plus localized tour operators across thousands of destinations is brutally capital- and time-intensive. You cannot conjure marketplace liquidity overnight; it takes years of unglamorous supply-side hustle. That barrier protects the incumbents.

Bargaining Power of Suppliers — specifically Google: Extremely High. We've already lived through this one. Google controls the organic search funnel, which means it controls the faucet of customer traffic, which means it can choke Tripadvisor's economics and push it into ever-more-expensive paid acquisition at will. As a supplier of demand, Google holds devastating leverage, and that is the single most important structural weakness in the entire business.

Bargaining Power of Buyers — OTAs and consumers: High. The legacy business depended on a tiny handful of enormous OTA customers — Booking Holdings and Expedia — who can dictate margins and redirect their marketing budgets elsewhere whenever it suits them, as they vividly demonstrated during the Instant Booking war.

Threat of Substitutes: High. This is the modern, generational threat. Younger travelers increasingly bypass traditional review portals entirely, discovering destinations through short-form video on TikTok and Instagram, and increasingly through AI chat assistants that synthesize recommendations directly. When the discovery layer moves to video and AI, a text-and-reviews portal risks becoming the travel equivalent of the printed phone book.

Industry Rivalry: Intense. In experiences, the competition is fierce and well-funded — GetYourGuide pressing hard in Europe, and 携程集团 Trip.com Group dominating in Asia, alongside Klook and Airbnb Experiences. There is no quiet corner of this market.

Put it together and you get a company with one genuinely strong, defensible power — Viator's marketplace network — wrapped inside an industry structure where the most important supplier (Google) and the most disruptive substitute (video and AI discovery) both point in a worrying direction. That tension is the whole investment debate, and it's where we'll land.

XI. Playbook: Key Lessons for Founders & Investors

Before we render the bull and bear cases, let's extract the durable, transferable lessons — the reasons this story will be taught in business schools long after the ticker stops trading.

The Lead-Gen Trap. The first and most important lesson is structural: never build a business whose entire customer-acquisition engine depends on a single third-party platform you do not own. Tripadvisor's golden years rested completely on free Google traffic, and the day Google decided it wanted that traffic for itself, there was nothing Tripadvisor could do but pay up. If you live by SEO, you can die by SEO. The same logic now applies to anyone building on top of a social feed, an app store, or an AI assistant's recommendation engine. Distribution you rent is distribution that can be repriced or repossessed.

The Danger of "Instant Booking" Hubris. The second lesson is about brand and identity. Do not try to convert a high-margin, asset-light, neutral referral business into a transactional one unless your brand natively supports the transaction. Tripadvisor's authority came from being the trusted, disinterested referee — and the moment it tried to also be the vendor, it confused its customers and declared war on the partners who funded it. The economics looked irresistible on a whiteboard; in the real world, they detonated both the brand and the partnerships simultaneously. Know what business your customers think you're in.

The Power of Venture Capital Inside a Public Company. The third lesson is the redemptive one. The $200 million Viator acquisition is a textbook example of buying an asymmetric option — a small, bounded bet with potentially enormous, unbounded upside. When your core business is a cash cow, the highest-return use of that cash may not be buybacks or dividends but a portfolio of small acquisitions of fast-growing adjacent networks. You will be wrong most of the time. That's fine. The math of asymmetric bets means a single Viator — which grew to nearly half the company — can rescue the entire enterprise from the obsolescence of its original business. Cash cows should fund their own successors.

Governance Matters — Enormously. The final lesson ties the whole saga together. Dual-class share structures are a double-edged sword. They can protect a company through volatile patches and let founders invest for the long term. But they can also trap capital and block the very turnarounds shareholders desperately need, when the controller's incentives drift from everyone else's. The elimination of the Liberty TripAdvisor Class B voting block in April 2025 was not a footnote — it was the catalyst. Without it, Starboard could not have built leverage, the board could not have been forced to prioritize shareholder value, and the $700 million TheFork sale almost certainly does not happen on this timeline. Sometimes the most important thing about a company isn't its product or its market — it's who actually holds the votes.

With the lessons banked, let's close by weighing the two futures now in front of this company.

XII. Conclusion

So where does that leave Tripadvisor in the middle of 2026 — a company simultaneously being celebrated for a brilliant decade-old acquisition and dismantled because of a decade of decline?

The bull case is genuinely compelling, and it rests on simplification. Once the American Express transaction closes, Tripadvisor will be a cleaner, sharper enterprise: a pure-play experiences business built around Viator — fast-growing, network-defended, and operating in one of travel's most attractive structural categories — sitting on a pristine balance sheet freshly topped up with $700 million in cash.1 If Matt Goldberg can successfully execute the AI-led transformation of the platform and convert Viator's revenue growth into the margin expansion it currently lacks, the sum-of-the-parts discount that defined the 2020s could finally collapse. A streamlined, debt-light, growing experiences pure-play is exactly the kind of asset that strategic acquirers — an Airbnb, a major OTA — or a financial buyer might pursue at a meaningful premium. In this telling, the breakup isn't a defeat; it's the deliberate clarification of a business the market could never previously see clearly.

The bear case is equally coherent, and it's the one the low valuation has been whispering all along. The legacy hotel-metasearch business may continue declining faster than Viator can grow, leaving the consolidated company stuck on a downward escalator. The experiences segment, for all its growth, carries lower margins and faces ferocious, well-capitalized rivalry from GetYourGuide and 携程集团 Trip.com Group, with low switching costs that prevent it from ever locking customers in. And looming over everything is the same landlord that has haunted this company for a decade: Tripadvisor remains a structural captive of Google's search monopoly, now compounded by the existential question of whether AI chat assistants and short-form video simply route around travel-review portals altogether. In this telling, the company is a collection of decent assets perpetually taxed by the platforms that control its distribution.

For the long-term investor trying to cut through the noise, the metrics that matter most are few and clear. Watch Experiences (Viator) revenue growth — it is the single most important number, the engine on which the entire pure-play thesis depends; a deceleration there would undercut the whole bull case. Watch the Experiences segment's adjusted EBITDA margin — the bet is that profitability climbs as the business scales, and the trajectory of that margin is the truest test of whether Viator is a great business or merely a fast-growing one. And keep an eye on the trajectory of the Hotels and Other segment — not because anyone expects it to grow, but because how gracefully it declines determines how much oxygen the company has to fund Viator's expansion.

The story of Tripadvisor is, in the end, the ultimate case study in digital real estate — what it means to build an empire on land you don't own. It is a chronicle of the transition from Web 1.0 reviews to a modern experiences economy, of a perfect business model undone by a single act of ambition and a landlord's change of heart, and of the sheer, decisive power of corporate governance to either trap value or finally set it free. From a Needham pizza shop to a Delaware courtroom to an all-cash deal with American Express, the blue owl has seen the entire arc of the consumer internet — and its next chapter is only just beginning.

References

-

American Express to Buy TheFork from Tripadvisor for $700 Million — Reuters, 2026-06-15 ↩↩↩↩↩↩↩

-

Tripadvisor Inc (TRIP) Market Data and Stock Quote — Wall Street Journal ↩↩↩

-

Tripadvisor Inc (TRIP.O) Stock Profile and Key Events — Reuters ↩↩↩

-

Tripadvisor Company Financials and Segment Performance — Bloomberg ↩

-

Tripadvisor Earnings Release: Focus Transitions to Experiences and Viator Growth — Phocuswire, 2026-02-12 ↩↩

-

Delaware Court Clears Tripadvisor Shareholder Dispute Over Nevada Reincorporation — Reuters, 2024-02-20 ↩↩

-

Tripadvisor's Matt Goldberg: Corporate Governance and Board of Directors — Tripadvisor IR ↩↩↩↩↩

-

Tripadvisor Earnings Release: Focus Transitions to Experiences and Viator Growth — Phocuswire, 2026-02-12 ↩↩↩↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube