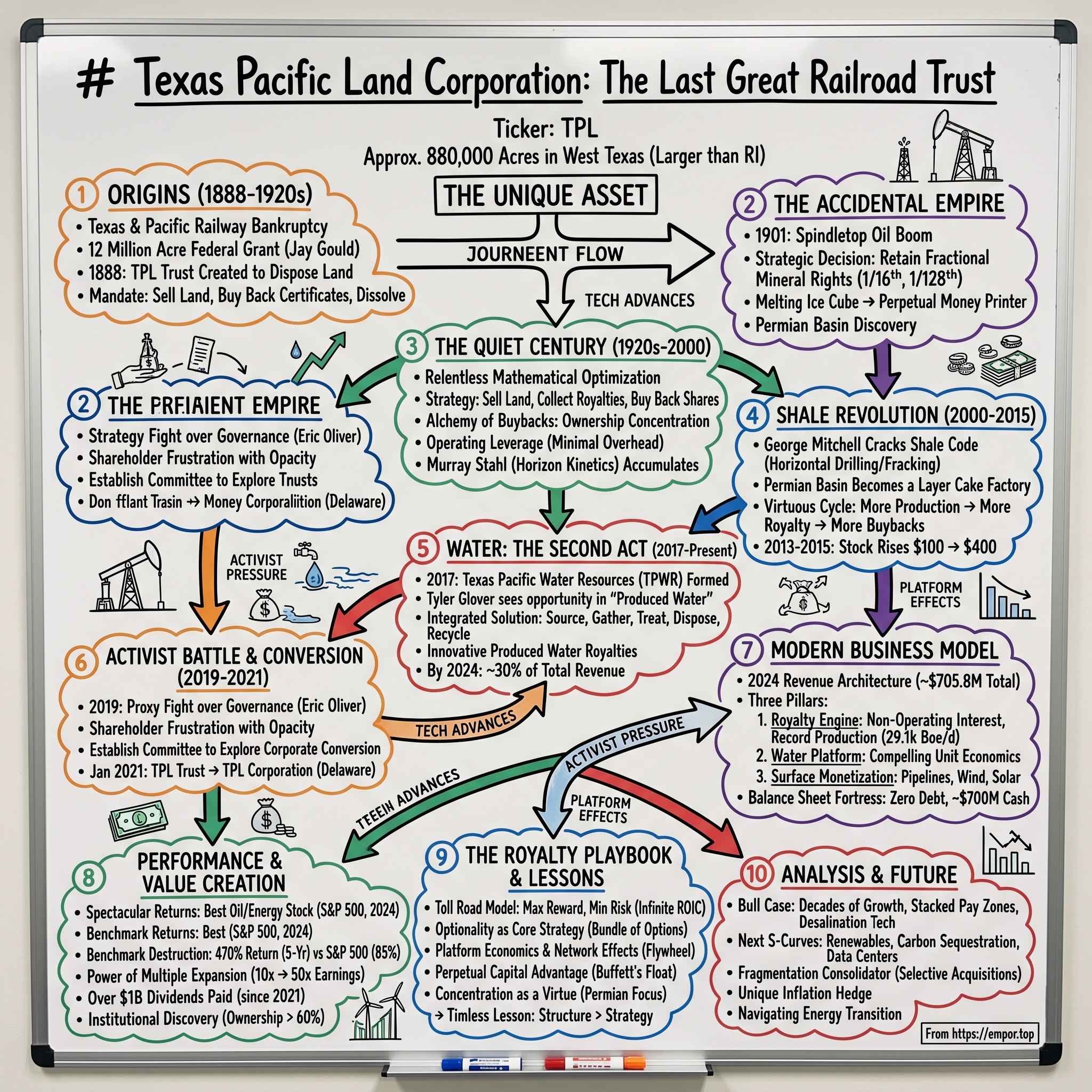

Texas Pacific Land Corporation: The Last Great Railroad Trust

I. Introduction & The Unique Asset

Picture this: In the scorching West Texas desert, where tumbleweeds roll across endless horizons and oil derricks punctuate the landscape like modern monuments, sits one of America's most unusual corporate success stories. A company that was never meant to exist past 1900. A liquidation trust that forgot to liquidate. A railroad failure that became an energy empire.

Texas Pacific Land Corporation controls approximately 880,000 acres across 20 West Texas counties—a land mass larger than Rhode Island. But here's what makes it extraordinary: TPL doesn't drill a single well, doesn't operate a single pump jack, doesn't employ armies of roughnecks. Yet approximately two-thirds of its income flows from oil and gas royalties, generated by others who pay for the privilege of extracting resources from beneath its ancient lands.

The corporate structure itself reads like financial fiction. What began in 1888 as a trust created to dispose of a bankrupt railroad's land holdings survived 133 years as a peculiar legal entity—neither quite a corporation nor a traditional trust—before finally converting to a C-corporation in 2021. During that century-plus journey, it systematically bought back its own shares, shrinking the share count while the land generated ever-increasing cash flows. The result? One of the most spectacular wealth-creation machines in American business history. This is the story of how the broken dreams of 19th-century railroad bondholders accidentally created one of the 21st century's most remarkable wealth-creation machines. How a liquidation trust that should have disappeared by 1900 became a perpetual money printer. How desert land once deemed worthless now generates hundreds of millions in annual cash flow without drilling a single well.

II. Origins: The Railroad That Failed & The Trust That Endured (1888–1920s)

The year was 1881, and Jay Gould—the most feared and reviled financier of the Gilded Age—had just pulled off another coup. Through a byzantine series of stock manipulations and backroom deals, he had wrested control of the Texas and Pacific Railway from its previous owners. The railroad, chartered in 1871 with grand ambitions to connect the American South to the Pacific Ocean, held a federal land grant of epic proportions: over 12 million acres stretching across Texas, a swath of territory larger than the states of Massachusetts and Connecticut combined.

But Gould's magic couldn't save the Texas and Pacific from the brutal economics of railroading in the American Southwest. By 1885, the company was hemorrhaging cash. The vast distances between settlements, the harsh desert climate, and competition from better-positioned rivals had turned the dream of a transcontinental southern route into a financial nightmare. When the railroad finally collapsed into receivership in March 1885, bondholders faced a stark reality: their bonds, once backed by the promise of a thriving railroad, were now worth pennies on the dollar.

Enter the lawyers and financial engineers. In February 1888, after three years of legal wrangling, they devised an unusual solution. Texas Pacific Land Holdings was created in 1888 in the wake of the Texas and Pacific Railway bankruptcy, as a means to dispose of the T&P's vast land holdings. The trust would take possession of approximately 3.5 million acres of the railroad's Texas land grants—land that stretched across 20 counties in West Texas, much of it considered worthless desert at the time.

The mechanism was elegantly simple: bondholders would exchange their defaulted railroad bonds for certificates of proprietary interest in the new trust. These weren't quite shares in the modern sense—they were fractional ownership stakes in a liquidating trust. The trust had one mandate: sell the land, use the proceeds to buy back certificates from holders who wanted out, and eventually dissolve when all the land was sold or all the certificates were retired.

Three men were appointed as trustees to oversee this liquidation: General Grenville Dodge, a Civil War hero and railroad builder; Judge John C. Brown, former governor of Tennessee; and Simmons Hardware Company president George Washington Simmons. They were practical men who understood that selling 3.5 million acres of West Texas scrubland wouldn't happen overnight. Initial land sales were painfully slow—$1 to $3 per acre when they could find buyers at all.

But then something unexpected happened. In 1901, oil exploded from Spindletop near Beaumont, Texas, ushering in the modern petroleum age. Suddenly, mineral rights weren't an afterthought—they were potentially valuable. The trustees made a decision that would echo through the next century: when selling surface land, they would retain a portion of the mineral rights. Not all of them—that would have made the land impossible to sell—but a "non-participating royalty interest," typically 1/16th or 1/128th of any oil produced.

This seemingly minor decision—retaining fractional mineral interests while selling surface rights—transformed the trust from a melting ice cube into something far more interesting. By the 1920s, oil discoveries were spreading across Texas. The trust's retained mineral interests, scattered across millions of acres like seeds in the desert, began generating royalty income. Small amounts at first—a few thousand dollars here and there—but it was pure profit, requiring no capital investment, no operations, no risk.

The trustees, meanwhile, continued their dual mandate: selling land when prices were attractive and using excess cash to buy back certificates. Between 1888 and 1925, they reduced the certificate count from 1.5 million to under 900,000, concentrating ownership among the patient holders who didn't sell. The trust that was supposed to liquidate and disappear had instead discovered a perpetual motion machine: sell surface, keep minerals, buy back shares, repeat.

What the trustees couldn't have known was that beneath their "worthless" West Texas land lay one of the greatest oil reserves on Earth—the Permian Basin. Named after the Permian geological period when these rocks were formed 250 million years ago, the basin would eventually produce more oil than Saudi Arabia's Ghawar field. But that discovery was still decades away. For now, the trust simply persisted, slowly selling land, collecting modest royalties, and buying back certificates from impatient holders who saw little value in waiting.

III. The Quiet Century: Land Sales & Share Buybacks (1920s–2000)

For most of the 20th century, Texas Pacific Land Trust operated in obscurity, a financial oddity known only to a small circle of value investors and trust law enthusiasts. While America experienced the Roaring Twenties, the Great Depression, World War II, and the Space Age, the trust methodically executed the same playbook year after year: sell land, collect royalties, buy back shares.

The numbers tell a story of relentless mathematical optimization. By 1940, the trust had reduced its land holdings to approximately 2 million acres while the certificate count had shrunk to 650,000. By 1960, the land was down to 1.5 million acres and certificates to 400,000. The beauty of this model was its simplicity: as the share count decreased faster than the asset base, each remaining certificate represented an ever-larger slice of the pie.

Consider the experience of a hypothetical long-term holder. In 1930, one certificate represented ownership of approximately 2.5 acres of land plus associated mineral rights. By 1970, through the alchemy of share buybacks, that same certificate represented ownership of nearly 4 acres. The holder hadn't bought more land—the trust's systematic repurchases had simply concentrated ownership among the remaining certificate holders.

The trust's annual reports from this era read like agricultural bulletins. Grazing leases to cattle ranchers generated steady if unspectacular income—$50,000 here, $75,000 there. The occasional oil discovery would spike revenues temporarily before settling back to baseline. In 1952, the trust reported total revenues of $431,000. By 1975, revenues had grown to $2.1 million, driven primarily by increased oil activity and higher commodity prices during the Arab oil embargo.

But the real story was happening below the surface—literally. Each decade brought improvements in drilling technology that made previously uneconomic deposits viable. The trust's policy of retaining mineral rights when selling surface land was creating an increasingly valuable portfolio of royalty interests scattered across the Permian Basin. These interests required zero capital investment and zero operational expertise. When Texaco or Mobil drilled a successful well on land where the trust held royalties, checks simply appeared.

In 1995, the Trust owned 1 million acres of land in west Texas and used the proceeds from periodic land sales, along with modest revenues from grazing fees and oil royalties, to repurchase shares. The trust was trading at just $4.00 per share, valuing the entire enterprise at less than $20 million despite owning a million acres of Texas land. Only a handful of investors recognized the asymmetric opportunity.

Among them was a contrarian value investor named Murray Stahl, who would later play a pivotal role in the trust's history. Stahl, through his firm Horizon Kinetics, began accumulating certificates in the 1990s when the trust was essentially forgotten by the market. His investment thesis was simple but powerful: the land wasn't getting worse, the mineral rights were perpetual, and the share count kept shrinking. It was a coiled spring waiting for a catalyst.

The trust's governance structure during this period was remarkably static. Three trustees, typically Texas businessmen or lawyers, met quarterly to approve land sales and buybacks. They collected modest fees—$75,000 per year in the 1990s—and operated with minimal overhead. The trust didn't even have employees in the traditional sense; it contracted out administrative functions and land management duties.

This bare-bones structure created incredible operating leverage. In 1995, total expenses were less than $500,000 against revenues of $3.2 million. The trust didn't need teams of geologists, drilling crews, or marketing departments. It simply collected checks from oil companies and ranchers, paid minimal expenses, and used the excess cash to buy back more certificates.

At that time, in early 1995, it traded at $4.00 per share. At yearend 2013, the shares closed at $99.99, which works out to about a 19% annualized return. This spectacular performance occurred with virtually no fanfare, no analyst coverage, and no institutional attention. The trust didn't hold earnings calls, didn't provide guidance, and rarely communicated with shareholders beyond required SEC filings.

What changed between 1995 and 2013 wasn't the trust's strategy—it remained exactly the same. What changed was the Permian Basin itself. Advances in horizontal drilling and hydraulic fracturing were about to unlock oil reserves that had been trapped in shale rock for millions of years. The "worthless" desert land that railroad bondholders had reluctantly accepted in 1888 was about to become some of the most valuable real estate on Earth.

By 2000, the trust owned approximately 970,000 acres and had reduced the certificate count to under 50,000. Each certificate now represented ownership of nearly 20 acres of land plus associated mineral rights. Patient holders who had accumulated certificates when the trust traded for single digits were sitting on 10x or 20x returns. But the real explosion in value was yet to come.

IV. The Shale Revolution Changes Everything (2000–2015)

George Mitchell, the son of a Greek goatherder, spent 17 years and nearly bankrupted his company trying to extract natural gas from the Barnett Shale in North Texas. When Mitchell Energy finally cracked the code in 1998—combining horizontal drilling with hydraulic fracturing—it didn't just unlock the Barnett Shale. It revolutionized global energy markets and transformed every oil-bearing shale formation in America into a potential goldmine.

For Texas Pacific Land Trust, sitting atop vast stretches of the Permian Basin, the timing couldn't have been better. The Permian wasn't just any shale play—it was a layer cake of multiple oil-bearing formations stacked on top of each other: the Wolfcamp, the Spraberry, the Bone Spring, the Delaware. Each formation could be drilled and fracked independently, meaning a single surface location could support dozens of wells targeting different depths.

The first horizontal wells in the Permian began appearing on trust land around 2005. Unlike conventional vertical wells that might drain 40 acres, these horizontal wells sent drill bits sideways for miles, exposing thousands of feet of oil-bearing rock. The production profiles were staggering. A single horizontal well could produce 1,000 barrels of oil per day in its first month, generating immediate royalty income for the trust.

Pioneer Natural Resources, one of the first companies to aggressively pursue horizontal drilling in the Permian, began leasing mineral rights from private landowners at unprecedented prices. But the trust didn't need to lease its minerals—it had retained non-participating royalty interests that required no negotiation, no bonus payments, no decision-making. When Pioneer or EOG Resources or Occidental Petroleum drilled a well, the trust automatically received its percentage of production.

The numbers tell the story of transformation. In 2005, the trust reported oil and gas royalty income of $8.7 million. By 2010, as horizontal drilling accelerated, royalty income had grown to $44.9 million. By 2014, it reached $133.8 million. The trust hadn't drilled a single well, hadn't invested a dollar in exploration, hadn't taken any operational risk. It simply collected larger and larger checks as technology unlocked the value beneath its land.

But the real genius of the trust's position became clear when you understood the economics of shale drilling. Unlike conventional oil fields where production might remain stable for decades, shale wells experienced rapid decline rates—often losing 70% of their production in the first year. This meant operators had to constantly drill new wells just to maintain production levels. And every new well meant new royalty income for the trust.

The Permian Basin became a massive factory, with drilling rigs operating 24/7, each well costing $7-10 million to drill and complete. By 2015, over 400 rigs were operating in the Permian, up from fewer than 100 a decade earlier. The basin was producing 2 million barrels per day and climbing rapidly. Industry executives spoke of the Permian as "the gift that keeps on giving" and "Saudi America."

For Texas Pacific Land Trust, the shale revolution created a virtuous cycle. Higher oil production meant more royalty income. More royalty income meant more cash for share buybacks. Share buybacks at reasonable prices were massively accretive because each retired certificate increased the remaining certificates' claim on future royalty streams. Between 2005 and 2015, the trust reduced its certificate count from approximately 47,000 to 33,000, a 30% reduction that increased each remaining certificate's ownership stake by 43%.

The trust also benefited from a hidden advantage: operator competition. As the Permian Basin heated up, oil companies competed fiercely for the best acreage. This competition drove technological innovation as companies sought to extract more oil from each well. Lateral lengths increased from 4,000 feet to 7,500 feet to 10,000 feet and beyond. Fracking techniques improved, using more sand and higher pressures to create more fractures in the rock. Each innovation meant more oil production and more royalty income for the trust.

Meanwhile, surface uses of the land were generating additional revenue streams. Pipeline companies needed easements to transport oil and gas. Wind farms sought leases for turbines. Cell towers, electrical transmission lines, and roads all required surface access. The trust collected fees for all of it, often retaining the ability to grant multiple non-conflicting uses on the same land.

The market was beginning to notice. The trust's certificates, which had traded for $100 in 2013, reached $400 by early 2015. Financial bloggers and value investors were spreading the word about this obscure Texas trust that was printing money from the shale revolution. Yet it remained underfollowed by Wall Street, with no sell-side analyst coverage and minimal institutional ownership.

What most investors missed was that the shale revolution was still in its early innings. The Permian Basin contained an estimated 75 billion barrels of technically recoverable oil, of which less than 10% had been produced. The trust's million acres of land and millions of acres of mineral interests were perfectly positioned for decades of future development.

V. Water: The Second Act Nobody Saw Coming (2017–Present)

In the summer of 2016, Tyler Glover, a petroleum engineer who had joined Texas Pacific as a consultant, noticed something odd in the Permian Basin's production data. For every barrel of oil coming out of the ground, operators were also producing three, five, sometimes ten barrels of ancient saltwater—brine trapped in the rock formations for millions of years. This "produced water" was the industry's dirty secret: it cost money to dispose of, created environmental liabilities, and was becoming a bottleneck for production growth.

Glover saw opportunity where others saw waste. Texas Pacific Land Trust owned not just mineral rights but surface rights across vast swaths of the Permian. What if, instead of merely collecting royalties from oil production, the trust could build a water business that served the entire lifecycle of a well—from the freshwater needed for fracking to the disposal of produced water?

In June 2017, TPL announces the formation of Texas Pacific Water Resources, a wholly-owned subsidiary of TPL focused on providing holistic water services to oil and gas operators in the Permian Basin. The announcement was met with skepticism. The trust had operated for 129 years without employees, without operations, without capital projects. Now it was proposing to build water infrastructure?

But the logic was compelling. A typical horizontal well in the Permian required 10-15 million gallons of water for hydraulic fracturing. In a basin producing millions of barrels of oil per day, that meant billions of gallons of water demand annually. And because water is heavy and expensive to transport, proximity to drilling sites was crucial. The trust's scattered land ownership across the Permian gave it strategic locations that competitors couldn't replicate.

The trust started modestly, drilling water wells and selling freshwater to operators. But the real opportunity emerged in produced water. As Permian production grew, the volume of produced water exploded—from 5 billion barrels in 2017 to over 8 billion barrels by 2020. Most of this water was simply injected into disposal wells, but the disposal capacity was becoming constrained. Some areas were experiencing induced seismicity—earthquakes caused by water injection—leading to regulatory restrictions.

Texas Pacific Water Resources developed an integrated solution. It would gather produced water from operators via pipeline networks, treat it to remove oil and suspended solids, and either dispose of it safely or recycle it for reuse in fracking. The capital investment was significant—tens of millions of dollars for pipelines, treatment facilities, and disposal wells—but the returns were extraordinary.

The economics of water were even better than oil royalties. While oil prices fluctuated wildly—from $70 per barrel to negative $37 during COVID—water volumes were steady and growing. Operators had to deal with produced water regardless of oil prices. And unlike oil royalties where the trust only received 1/16th or 1/128th of revenues, water services captured a much larger share of the value chain.

By 2020, the water segment was generating $70 million in annual revenue. By 2023, it exceeded $100 million. TPL's water-related operations are another growth driver, with produced water royalties increasing 46% year over year in the third quarter. This segment, which is expected to generate $100 million in revenues in 2024, benefits from strategic agreements that require minimal capital expenditure.

The trust pioneered innovative commercial structures. Instead of just charging fees for water disposal, it negotiated "produced water royalties"—agreements where operators paid based on their total water production, similar to oil royalties. These agreements required minimal capital investment from the trust while providing steady, growing income streams.

The strategic positioning was brilliant. The trust's land ownership gave it advantages in permitting and right-of-way acquisition that new entrants couldn't match. Its multi-decade relationships with operators provided trusted partner status. And its patient capital structure—no debt, no private equity pressure for quick exits—allowed it to invest for the long term.

But perhaps the most important insight was recognizing water as a platform for multiple revenue streams. Treated produced water could be sold for reuse in fracking, reducing freshwater demand. The infrastructure built for water could also transport oil and gas. Water disposal sites could be optimized for carbon sequestration as climate regulations evolved.

The Company announces today the development of a new energy-efficient method of produced water desalination and treatment. The Company has successfully conducted a technology pilot and is progressing towards the construction of a larger test facility with an initial capacity of 10,000 barrels of produced water per day. This desalination technology, if successful at scale, could transform produced water from waste into a valuable resource for agriculture or industrial use.

The water business also demonstrated the trust's ability to evolve. After 129 years as a passive royalty collector, it had successfully built an operational business with employees, infrastructure, and customer relationships. The transformation wasn't without challenges—operating expenses increased, capital allocation became more complex—but the value creation was undeniable.

By 2024, water services and related royalties represented nearly 30% of the trust's total revenues. What started as an experiment had become a core pillar of the business model. And with Permian oil production expected to grow for decades and produced water volumes growing even faster, the water business was positioned for continued expansion.

VI. The Activist Battle & Corporate Conversion (2019–2021)

The conference room at the Adolphus Hotel in Dallas was packed on May 22, 2019. Shareholders of Texas Pacific Land Trust had gathered for what promised to be the most contentious meeting in the trust's 131-year history. On one side sat the two aging trustees who had overseen the trust for decades. On the other, Eric Oliver, a former trustee turned activist investor who was waging a proxy battle that would fundamentally reshape the company.

The roots of the conflict traced back to 2016 when Oliver, then a trustee himself, began questioning the trust's governance structure. How could two men—or even three—effectively oversee an entity worth billions of dollars? Why did the trust have no independent directors, no formal committees, no modern governance practices? And most provocatively, why were the trustees so resistant to converting the trust into a regular corporation?

Oliver's campaign resonated with shareholders who had grown frustrated with the trust's opacity. The trust didn't hold earnings calls. It provided minimal disclosure about its water business investments. The trustees seemed to view shareholders as nuisances rather than owners. When Oliver was effectively pushed out as a trustee in 2019, he launched a full-scale proxy fight to return to the board and force change.

In 2019, TPL settled a months-long proxy fight over the election of trustee Eric Oliver. As part of the settlement, the company established a committee to explore whether Texas Pacific should be converted to a Delaware corporation. The settlement was a watershed moment. Not only did Oliver return as a trustee, but the trust agreed to explore the corporate conversion that had been debated for years.

The conversion question was more than administrative minutiae. As a trust, Texas Pacific had operated under an 1888 declaration that limited its activities and created uncertainty about its ability to pursue new business opportunities. Could a trust acquire other companies? Could it issue stock for acquisitions? Could it properly compensate employees with equity? The archaic structure was becoming a competitive disadvantage as the trust sought to build operational businesses like water services.

Enter Murray Stahl, the contrarian investor who had been accumulating shares since the 1990s. Through his firm Horizon Kinetics, Stahl had become one of the trust's largest shareholders, owning approximately 20% of certificates. Stahl brought intellectual firepower and capital markets credibility to the conversion debate. He argued that the trust structure, while historically beneficial, was now constraining value creation.

The conversion process was complex, requiring approval from holders of at least two-thirds of outstanding certificates. Management had to navigate Texas trust law, federal tax implications, and the competing interests of various shareholder constituencies. Some long-term holders worried that conversion would trigger tax consequences or reduce the pressure for share buybacks that had driven returns for decades.

Throughout 2020, as COVID-19 roiled markets and oil prices went negative, the trust methodically worked toward conversion. It hired advisors, drafted proxy statements, and engaged with shareholders. The pandemic actually strengthened the conversion argument—a modern corporate structure would provide more flexibility to navigate unprecedented market conditions.

In 2021, the company reorganized from a trust to a corporation, was subsequently renamed Texas Pacific Land Corporation, and appointed a board of directors to govern. On January 11, 2021, the conversion was completed. Texas Pacific Land Trust ceased to exist after 133 years. In its place stood Texas Pacific Land Corporation, a Delaware corporation with a modern governance structure.

The immediate changes were significant. Instead of three trustees operating with minimal oversight, the new corporation had a seven-member board of directors including independent directors with relevant expertise. It established audit, compensation, and nominating committees. It hired a CEO—Tyler Glover, the engineer who had spearheaded the water business. It implemented equity compensation plans to attract and retain talent.

But some things remained sacred. The corporation maintained the trust's historic commitment to share repurchases, authorizing a new $100 million buyback program immediately after conversion. It preserved the conservative balance sheet, continuing to operate without debt. And it retained the core strategy of generating royalty income while opportunistically developing new revenue streams.

The market's reaction was positive but measured. The stock, which had traded around $600 before the conversion announcement, rose to over $800 by mid-2021. Institutional investors who had been prohibited from owning trust certificates could now buy corporate shares. Index funds that excluded trusts could include TPL. Sell-side analysts finally initiated coverage.

The Company will nominate two new independent directors, Marguerite Woung-Chapman and Robert Roosa, in addition to current director, Murray Stahl. The board composition reflected a balance between continuity and change. Stahl provided deep knowledge of the company's history and value drivers. New independent directors brought expertise in energy, finance, and corporate governance.

The conversion also enabled strategic initiatives that would have been difficult under the trust structure. The corporation could now issue stock for acquisitions, though it remained disciplined about dilution. It could provide equity incentives to employees building the water business. It could engage with investors through earnings calls and investor days.

Yet the activist battle and conversion also revealed tensions that persist today. Some shareholders worry that operational expansion into water and other businesses distracts from the simple, beautiful model of collecting royalties and buying back stock. Others argue that active business development is necessary to maximize the value of TPL's unique asset base.

The governance improvements were undeniable. The new board brought professional oversight, strategic planning, and risk management processes that had been absent under the trust structure. Regular board meetings replaced the informal decision-making of the trustee era. Executive compensation was aligned with shareholder returns rather than fixed fees.

VII. The Modern Business Model & Economics

Step into Texas Pacific Land Corporation's Dallas headquarters today, and you'll find something that would have been unimaginable just a decade ago: actual employees. Over 100 of them, including engineers, geologists, water specialists, and financial analysts. The company that operated for 129 years without a payroll now runs a sophisticated, multi-faceted business that generates nearly three-quarters of a billion dollars in annual revenue.

Total revenues for the year ended December 31, 2024 were $705.8 million compared to $631.6 million for the prior year. All revenue streams except land sales, increased for the year ended December 31, 2024 compared to the prior year, with a $38.5 million increase in water sales being the biggest contributor. The growth in water sales was principally due to an increase of 31.0% in water sales volumes for the year ended December 31, 2024 compared to the prior year.

The revenue architecture reveals a carefully orchestrated symphony of income streams. Oil and gas royalties remain the largest contributor at approximately $390 million annually, but the composition has evolved dramatically. The company now operates across three primary business segments, each with distinct economics and growth trajectories.

The Royalty Engine

At the core remains the perpetual royalty machine. Royalty production of 29.1 thousand barrels of oil equivalent ("Boe") per day, a company record demonstrates the continued vitality of this segment. But understanding the economics requires appreciating the stunning operating leverage. The company incurs essentially zero cost to generate this production. No drilling costs, no completion expenses, no workovers, no plugging liabilities. When Chevron or ConocoPhillips drills a $10 million well on TPL's acreage, TPL receives its fractional share of production in perpetuity.

The royalty portfolio spans different vintages and terms. The oldest positions, retained from land sales in the early 1900s, carry 1/128th non-participating perpetual royalty interests (NPRI) covering approximately 85,000 acres. More recent retentions secured 1/16th NPRI on 371,000 acres. The company also owns approximately 207,000 net royalty acres outright—mineral interests where it owns a larger working interest percentage.

Each percentage point matters enormously at scale. A 1/16th royalty on a well producing 1,000 barrels per day at $75 oil generates $4,687 daily. Multiply that across hundreds of producing wells, and the cash generation becomes staggering. The company's average realized price in 2024 was approximately $41 per BOE, reflecting the mix of oil, gas, and natural gas liquids in its production stream.

The Water Platform

The water business has evolved from experiment to essential pillar, contributing over $150 million in annual revenues through multiple mechanisms. Sourced water sales involve drilling freshwater wells and delivering water for fracking operations. Produced water services encompass gathering, treatment, and disposal of wastewater from oil production. But the masterstroke has been produced water royalties—contractual arrangements where operators pay TPL based on water production volumes, similar to oil royalties.

The unit economics are compelling. Sourced water sells for $0.30 to $0.50 per barrel depending on location and delivery method. Produced water disposal commands $0.50 to $1.00 per barrel. With billions of barrels of water moving through the Permian annually, even small market share translates to significant revenue. The company handled over 100 million barrels of water in 2024, and volumes continue growing faster than oil production as legacy wells produce increasing water cuts.

Surface Monetization

The third leg of the stool—surface rights and easements—generated approximately $50 million in 2024. This includes pipeline easements ($15,000 to $25,000 per mile), wind turbine leases ($5,000 to $10,000 per turbine annually), temporary use permits for drilling pads, and material sales of caliche for road construction. Each use is carefully structured to avoid conflicting with other revenue streams. A single section of land might host oil wells, water pipelines, wind turbines, and grazing cattle simultaneously.

Operating Leverage and Margins

The financial model's beauty lies in its operating leverage. Total revenues for the quarter reached $185.8 million in Q4 2024, while operating expenses were just $41 million, yielding operating margins approaching 78%. This isn't the result of cost-cutting or operational efficiency—it's structural. Royalty income requires no operating expenses. Water infrastructure, once built, has minimal variable costs. Surface easements are pure margin.

Compare this to traditional E&P companies that might spend $30-40 to extract a barrel of oil selling for $75. TPL receives $5-10 per barrel with zero extraction cost. This operating leverage means that commodity price increases flow almost directly to the bottom line. When oil rises from $70 to $80, a traditional producer might see profits increase 50%. TPL's profits might double.

Capital Allocation Framework

Announced a target cash and cash equivalents balance of approximately $700 million. Above this targeted level, TPL will seek to deploy the majority of its free cash flow towards share repurchases and dividends. This framework provides clarity on capital priorities while maintaining flexibility for strategic opportunities.

The company's capital allocation has become increasingly sophisticated. Share repurchases remain a priority, with over $400 million deployed in recent years. Regular dividends have grown to $1.60 per quarter, supplemented by special dividends when cash accumulates. The company paid a $10 special dividend in July 2024, returning $230 million to shareholders.

But the company now also deploys capital for strategic acquisitions. Acquired mineral interests across 7,490 net royalty acres located primarily in the Midland Basin for a purchase price of $275.2 million, net of post-close adjustments, in an all-cash transaction in October 2024. These acquisitions are highly selective, focusing on acreage with multiple producing horizons and strong operator activity.

The Balance Sheet Fortress

Perhaps most remarkably, TPL maintains this entire operation with zero debt. The balance sheet shows over $700 million in cash and equivalents against no financial obligations. This isn't financial conservatism—it's strategic positioning. In commodity markets, leverage amplifies both gains and losses. TPL's debt-free structure means it can survive any commodity price environment and capitalize on distressed opportunities when others are forced sellers.

The company generates free cash flow of approximately $400-500 million annually at current commodity prices. This cash generation is remarkably stable despite commodity volatility because multiple revenue streams provide natural hedges. When oil prices fall, drilling activity might slow, reducing water demand. But existing wells continue producing, generating steady royalty income.

VIII. Performance & Creating Shareholder Value

The numbers are so extraordinary they seem like misprints. With a staggering 127.3% year-to-date gain, it has outperformed even high-flying names like Netflix NFLX and Tesla TSLA. Texas Pacific Land Corporation TPL has been a standout performer in 2024, not only as the best Oil/Energy stock in the S&P 500 but also as the 7th best overall.

But 2024's spectacular return is just the latest chapter in one of the greatest wealth-creation stories in modern markets. A patient investor who bought shares at $100 in 2010 would be sitting on a 17-fold return today, not including dividends. That same $100,000 investment would now be worth $1.7 million—a compound annual return exceeding 22%.

The long-term performance becomes even more remarkable when you extend the timeline. That 1995 investor who bought at $4 per share when the trust owned a million acres of "worthless" West Texas land? Their shares, adjusted for subsequent stock splits, have appreciated approximately 400-fold. A mere $10,000 investment would have grown to $4 million—enough to fund a comfortable retirement from what many considered a speculative bet on desert land.

The Power of Multiple Expansion

The stock's appreciation reflects both fundamental improvement and multiple expansion. In 2010, the trust traded at approximately 10x earnings, befitting its perception as a declining land trust slowly liquidating assets. Today, the corporation trades at over 50x earnings, reflecting its transformation into a growth platform with multiple expansion opportunities.

This rerating wasn't irrational exuberance—it reflected genuine business transformation. The trust of 2010 generated $45 million in revenue entirely from passive sources. The corporation of 2024 generates $700 million across multiple business lines with significant growth visibility. The trust had no employees and no growth strategy. The corporation has over 100 employees executing expansion plans across water, renewables, and strategic acquisitions.

Volatility as Opportunity

The path to these returns wasn't smooth. The stock fell 44% in March 2020 as COVID crashed oil prices. It dropped 32% in 2023 as interest rates rose and recession fears mounted. Each decline created opportunities for the company to repurchase shares at attractive prices and for shrewd investors to accumulate positions.

This volatility reflects TPL's sensitivity to commodity prices and broader energy sentiment. When oil trades at $80, the market extrapolates perpetual prosperity. When oil falls to $40, investors price in permanent decline. The company's long-term shareholders have learned to embrace this volatility, using weakness to accumulate and strength to trim positions.

Shareholder Rewards Beyond Price Appreciation

The total return story extends beyond stock price gains. Since 2021, the company has paid over $1 billion in dividends, including regular quarterly payments and special distributions. The July 2024 special dividend of $10 per share alone returned $230 million to shareholders. For long-term holders, these dividends provide cash returns while maintaining equity exposure to the company's growth.

Share repurchases have been equally rewarding. By reducing share count from 1.5 million certificates in 1888 to approximately 23 million shares today (after adjusting for splits), the company has concentrated ownership dramatically. Each remaining share represents claim to assets and cash flows that would have been spread across 65 times as many shares without the buyback program.

Benchmark Destruction

TPL's performance embarrasses relevant benchmarks. Over the past five years, TPL generated returns of approximately 470% versus 85% for the S&P 500. Against the Energy Select Sector SPDR (XLE), the outperformance is even more dramatic—470% versus 60%. The company has demonstrated that the right assets with the right structure can generate equity-like returns with bond-like predictability.

Even comparing TPL to the best-performing energy stocks reveals exceptional outperformance. ExxonMobil, considered an energy blue-chip, returned approximately 150% over five years. Chevron delivered 120%. ConocoPhillips, one of the better-performing E&P companies, managed 180%. TPL tripled the returns of these industry leaders while taking no operational risk.

The Institutional Discovery

The stock's recent performance partly reflects institutional discovery of the TPL story. Following corporate conversion in 2021, institutional ownership has grown from under 30% to over 60%. Index inclusion, sellside coverage initiation, and improved disclosure have brought new buyers who were previously prohibited from owning trust certificates.

This institutional adoption created a virtuous cycle. Higher institutional ownership led to better liquidity, tighter spreads, and reduced volatility. Better market mechanics attracted more institutions. The stock's addition to the S&P MidCap 400 index in 2022 alone drove millions in forced buying from passive funds.

Creating Per-Share Value

The company's value creation extends beyond absolute metrics to per-share growth. Revenue per share has grown from approximately $20 in 2015 to over $30 in 2024. Free cash flow per share expanded from $5 to over $20. Book value per share increased from $40 to over $100. Each metric shows consistent per-share growth despite significant absolute growth—the hallmark of excellent capital allocation.

This per-share focus permeates management thinking. When evaluating acquisitions, the question isn't whether it increases total production or revenue, but whether it's accretive to per-share value. When considering growth investments, the hurdle isn't just positive returns but returns exceeding what buybacks would deliver.

IX. Playbook: The Royalty Model & Strategic Lessons

Study enough business history, and you'll notice that the greatest fortunes often emerge from owning toll roads, not operating vehicles. John D. Rockefeller didn't pump oil—he controlled refining and distribution. Bill Gates didn't manufacture computers—he licensed operating systems. And Texas Pacific Land doesn't drill wells—it collects royalties from those who do.

The royalty model represents business strategy distilled to its essence: maximum reward with minimum risk. While Occidental Petroleum spends billions drilling wells that might produce nothing, TPL collects checks when those wells hit. While Pioneer Natural Resources manages thousands of employees and complex operations, TPL generates similar margins with a hundred people. While the entire energy sector struggles with capital intensity, TPL prints cash with virtually no capital requirements.

The Beautiful Simplicity of Non-Operating Interest

Consider the elegant economics of a non-participating royalty interest. TPL owns 1/16th of production from a theoretical well. The operator spends $10 million drilling and completing the well. If successful, it produces 500,000 barrels over its lifetime at an average price of $70. The operator must recoup drilling costs, pay operating expenses, manage water disposal, and eventually plug the well. After all expenses, they might net $15 million on their $35 million in gross revenue.

TPL? It receives 1/16th of that $35 million—roughly $2.2 million—with zero investment, zero risk, zero operating cost. The operator bore geological risk, execution risk, commodity price risk during development. TPL bore none of it. Yet TPL's return on invested capital is infinite because the invested capital is zero.

This asymmetry becomes more powerful at scale. Across thousands of wells, operators will experience dry holes, mechanical failures, cost overruns. TPL only participates in successful wells—failures cost nothing. It's like owning a casino where you only collect winnings, never pay losses.

Optionality as Core Strategy

TPL's million acres represent a massive bundle of options on future development. Each acre could host traditional vertical wells, horizontal wells targeting multiple formations, water infrastructure, wind turbines, solar panels, carbon sequestration projects, or uses not yet imagined. The company doesn't have to predict which option will prove most valuable—it retains exposure to all of them.

This optionality framework explains seemingly conservative decisions. Why hasn't TPL sold more land when prices are high? Because land sold today can't benefit from tomorrow's innovations. The trust sold significant acreage in the 1920s for $3 per acre. That same land, if retained, would be generating millions in annual royalties today.

The water business exemplifies optionality in action. Nobody in 2010 predicted water would become a profit center. But because TPL owned surface rights and maintained strategic flexibility, it could capitalize when the opportunity emerged. Future options might include renewable energy, carbon credits, data centers, or technologies not yet invented.

Platform Economics and Network Effects

TPL's land ownership creates platform dynamics rarely seen in commodity businesses. Each new well drilled makes existing water infrastructure more valuable by increasing volumes. Each pipeline easement granted makes the land more attractive for additional pipelines seeking parallel routes. Each wind turbine installed provides infrastructure that makes additional turbines economic.

These network effects compound over time. TPL's water system now serves dozens of operators who share infrastructure costs. This shared infrastructure makes TPL's acreage more attractive for drilling, which generates more royalties, which funds more infrastructure, which attracts more operators. It's a flywheel that accelerates with scale.

The platform extends beyond physical infrastructure to relationships and knowledge. TPL's century-long presence in West Texas provides unmatched understanding of land titles, mineral ownership, and operational history. This institutional knowledge becomes a competitive moat that new entrants can't replicate regardless of capital.

The Perpetual Capital Advantage

Warren Buffett loves insurance float because it provides permanent capital to invest. TPL has something better: perpetual, non-callable, cost-free capital in the form of land and mineral rights. Unlike insurance float which must eventually pay claims, TPL's asset base never demands repayment. It just generates cash forever.

This perpetual capital structure enables truly long-term thinking. While private equity funds face 5-7 year exit pressures and public E&P companies manage quarterly earnings, TPL can make decisions with 50-year payoffs. The water infrastructure investments that seemed expensive in 2017 now generate 20%+ returns. The mineral acquisitions that appeared pricey in 2020 look prescient today.

Perpetual capital also provides staying power through cycles. During the 2014-2016 oil crash, leveraged E&P companies sold prime acreage at distressed prices to survive. TPL, debt-free with steady royalty income, was a buyer. During COVID, when oil went negative, TPL continued collecting water revenues and positioning for recovery.

Concentration as a Virtue

Modern portfolio theory preaches diversification, but TPL demonstrates the power of concentration done right. By focusing exclusively on the Permian Basin—the world's most economic oil resource—TPL avoids the complexity of managing global assets. Every employee understands Permian geology, regulations, and operators. Every investment dollar benefits from accumulated expertise.

This concentration extends to capital allocation. Rather than pursuing unrelated diversification, TPL doubles down on what works: buying more Permian minerals, expanding water infrastructure in the Permian, facilitating renewable development in the Permian. It's the corporate equivalent of Warren Buffett's "circle of competence" philosophy.

Lessons for Building Enduring Businesses

TPL's playbook offers timeless lessons. First, structure matters more than strategy. The decision to retain minerals when selling land, made in 1900, generated more value than any strategic plan. Second, simplicity scales better than complexity. TPL's model—own land, collect royalties—works at $1 million or $1 billion in revenue. Third, patience pays. The land that seemed worthless for decades became priceless when technology evolved.

Most importantly, TPL demonstrates that the best businesses often do less, not more. While competitors frantically drill wells, TPL waits for royalty checks. While others leverage up to boost returns, TPL maintains balance sheet strength. While the industry pursues the latest fad, TPL executes the same playbook it's run for 136 years.

X. Analysis & Future Opportunities

Walk the floor of any energy conference today, and you'll hear two competing narratives about Texas Pacific Land. The bears paint a picture of peak Permian, stranded assets in a decarbonizing world, and a stock priced for perfection. The bulls see decades of drilling inventory, emerging revenue streams, and a unique asset that only becomes more valuable with time. As with most investment debates, the truth lies in the nuanced middle—though perhaps tilted toward the optimistic side.

The Bear Case: What Could Go Wrong

The pessimistic thesis starts with geology. The Permian Basin, however vast, is finite. The best rock has been drilled first—the core of the core where wells generate 30%+ returns at $50 oil. What remains is increasingly marginal: thinner pay zones, higher water cuts, inferior rock quality. The bears argue we've seen peak productivity per well, and future drilling will generate lower returns for operators and lower royalties for TPL.

Depletion math is sobering. At current drilling rates, the Permian produces approximately 6 million barrels per day. TPL's share is roughly 29,000 barrels daily. But shale wells decline rapidly—that 1,000 barrel per day well becomes 300 barrels after one year, 150 after two years. To maintain production, operators must drill continuously. If drilling slows, production collapses, and TPL's royalty income evaporates.

ESG pressures pose existential questions. Major investors increasingly exclude fossil fuel companies from portfolios. European pension funds divest from oil and gas. Even Texas teachers' retirement funds face pressure to avoid energy investments. Can a company deriving 60%+ of revenue from oil and gas royalties survive in an ESG-conscious world?

Concentration risk looms large. TPL has all its eggs in one geographic basket—the Permian Basin of West Texas. A regional issue—water scarcity, regulatory changes, pipeline constraints—could disproportionately impact TPL. Unlike diversified energy companies with global assets, TPL can't offset Permian weakness with strength elsewhere.

Valuation concerns are legitimate. At 50x earnings, TPL trades at twice the S&P 500 multiple and five times traditional energy companies. This premium assumes continued growth, successful execution, and favorable commodity prices. Any disappointment could trigger multiple compression that overwhelms operational progress.

The Bull Case: Decades of Growth Ahead

The optimistic thesis begins with drilling inventory. Industry estimates suggest 50,000+ remaining drilling locations in the Permian at current spacing assumptions. At 2024's pace of 4,000 wells annually, that's more than a decade of drilling. But technology continues improving—longer laterals, better completion techniques, tighter spacing—potentially doubling the recoverable resource.

The Permian's stacked pay zones create multiple development waves. Operators have primarily targeted the Wolfcamp and Spraberry formations. The Bone Spring, Avalon, and other zones remain largely untapped. Each formation represents a new inventory of drilling locations on the same surface acreage—like finding additional gold mines beneath existing ones.

Water growth appears unstoppable. Produced water volumes grow faster than oil production as wells age and water cuts increase. TPL's water handling capacity of 500,000+ barrels per day could double in five years. At $0.50 per barrel margins, that's $100+ million in additional high-margin revenue. The desalination technology, if successful, could transform produced water from waste to resource, opening massive new markets.

Produced water royalties increased $19.9 million, principally due to increased produced water volumes. This growth in water-related revenues provides a natural hedge against declining oil activity—even if drilling slows, existing wells produce increasing amounts of water that must be handled.

Beyond Oil: The Next S-Curves

The renewable opportunity is real and imminent. Texas leads the nation in wind power generation, and West Texas offers ideal conditions—steady winds, sparse population, available land. TPL's million acres could host thousands of wind turbines generating $5,000-10,000 per turbine annually. At scale, wind leases could generate $50-100 million in annual revenue with zero capital investment.

Solar development is accelerating. The same abundant land and sunshine that made West Texas inhospitable to farming makes it perfect for utility-scale solar. Recent projects in the Permian have leased land at $100-200 per acre annually. If TPL leased just 10% of its acreage for solar, that's $10-20 million in pure-margin revenue.

Carbon sequestration represents a massive option value. The Permian's geology—impermeable cap rock, extensive saline aquifers, existing infrastructure—makes it ideal for CO2 storage. The Inflation Reduction Act's 45Q tax credits ($85 per ton for direct air capture) make sequestration economically viable. TPL's land could host projects storing millions of tons of CO2 annually.

Data centers are exploring West Texas. Abundant land, renewable power potential, and fiber optic cables following pipeline routes create interesting possibilities. A single hyperscale data center can lease 100+ acres at premium rates. While speculative today, data center development could emerge as cryptocurrency mining and AI computing demand explosion continues.

The Acquisition Pipeline

Acquired mineral interests across 7,490 net royalty acres located primarily in the Midland Basin for a purchase price of $275.2 million. This recent acquisition demonstrates TPL's ability to deploy capital at attractive returns. The private mineral market remains highly fragmented with thousands of small owners. TPL's permanent capital, operational expertise, and scale advantages position it as a natural consolidator.

The acquisition math is compelling. Private mineral packages typically trade at 5-8x cash flow versus TPL's 20x+ multiple. Even paying premium prices, TPL can acquire minerals accretively. Each acquisition increases scale, diversifies the royalty base, and provides new water and surface development opportunities.

Strategic M&A could accelerate growth. While TPL has focused on asset acquisitions, corporate combinations could provide step-function growth. Acquiring a water midstream company, a renewable developer, or another land/mineral owner could dramatically expand TPL's platform. The debt-free balance sheet provides flexibility for transformational deals.

The Inflation Hedge Argument

TPL offers unique inflation protection. Royalties automatically adjust with commodity prices. Water rates escalate with service costs. Land values appreciate with inflation. Unlike fixed-income investments that lose purchasing power, TPL's revenue streams provide natural inflation adjustment.

Historical evidence supports this thesis. During the 1970s inflation, oil prices rose from $3 to $35. Land values in Texas increased 10-fold. Investors who owned real assets dramatically outperformed those holding financial assets. TPL offers similar exposure today—real assets with pricing power in an potentially inflationary environment.

Navigating the Energy Transition

The energy transition presents both risks and opportunities. While oil demand may eventually peak, the decline will likely be gradual—decades, not years. Meanwhile, transition creates new revenue streams: renewable development, critical mineral extraction, carbon management. TPL's land platform can monetize whatever energy system emerges.

The company's response has been pragmatic. It continues maximizing oil and gas royalties while building options for the future. Water infrastructure serves any industrial development. Land can host any energy technology. The business model—collecting payments for use of essential resources—transcends specific commodities.

XI. Epilogue & What We've Learned

There's a plaque in the Texas Pacific Land Corporation headquarters that nobody talks about much. It lists the names of the original trustees from 1888—men who took on the thankless task of liquidating a failed railroad's land holdings. They couldn't have imagined that their mundane liquidation trust would outlive them by centuries, generate billions in wealth, and become one of the most successful investments in American history.

The story of TPL is, at its core, a story about time. Not market timing or cycle timing, but deep time—the kind measured in decades and centuries rather than quarters and years. It's about an organization that survived long enough for the world to discover value in what it owned all along.

The Power of Accidents

The greatest business models are often discovered, not designed. Nobody in 1888 said, "Let's create a perpetual royalty machine that will compound wealth for 150 years." The trustees simply tried to salvage value from a failed railroad. Each decision—retaining minerals, buying back shares, staying patient—was tactical, not strategic. Yet these tactical decisions, compounded over decades, created strategic brilliance.

This accidental genius permeates TPL's history. The trust structure that seemed archaic enabled tax-efficient share buybacks for a century. The scattered land ownership that complicated management created diversification across the entire Permian Basin. The inability to leverage prevented destruction during downturns. Even the corporate conversion, forced by activist pressure, unlocked institutional ownership and strategic flexibility.

Time Horizons: Playing the 100+ Year Game

While most companies optimize for the next quarter, TPL operates on geological timescales. Oil formed over millions of years. The land isn't going anywhere. Mineral rights are perpetual. This temporal advantage enables decisions that seem irrational short-term but brilliant long-term.

Consider the water infrastructure investments. Building pipelines and treatment facilities required tens of millions in capital with uncertain returns. Most companies wouldn't make that bet. But TPL could afford to be patient, knowing that Permian development would continue for decades. Five years later, water generates $150+ million in annual revenue.

Or examine the mineral acquisition strategy. Paying $275 million for 7,490 net royalty acres seems expensive at $36,000 per acre. But those acres will generate royalties for decades, potentially centuries. The acquisition math works not because year-one yields are attractive but because year-fifty cash flows are valuable.

The Beauty of Simple Business Models

In an era of complex financial engineering, TPL demonstrates the enduring power of simplicity. Own land. Collect payments from those who use it. Buy back stock with excess cash. Repeat. A child could understand the model. Warren Buffett would love it.

This simplicity creates resilience. Complex businesses fail in complex ways—derivatives blow up, technology becomes obsolete, consumer preferences shift. Simple businesses fail simply, and TPL's model has few failure points. As long as land has value and companies need resources, TPL will generate cash.

Simplicity also enables focus. Management doesn't waste time on marginal activities or empire building. Every decision filters through a simple framework: Does this increase per-share value? The answer guides capital allocation, operational investments, and strategic initiatives.

Why TPL Might Be the Perfect Inflation Hedge

As governments worldwide print money to fund deficits, inflation concerns grow. Financial assets—bonds, savings accounts, even some stocks—lose purchasing power as currencies debase. Real assets with pricing power offer protection, and TPL represents a unique collection of such assets.

Oil and gas royalties adjust automatically with commodity prices, which typically rise with inflation. Water rates escalate with operating costs. Land values appreciate over time. The combination provides multiple hedges against currency debasement. Unlike gold, which produces no cash flow, TPL's inflation hedges generate substantial current income.

Historical precedent is compelling. During the 1970s stagflation, energy and land dramatically outperformed financial assets. Investors who owned Texas ranch land or oil royalties preserved and grew wealth while bondholders got destroyed. TPL offers similar exposure with better business characteristics—perpetual royalties versus depleting wells, professional management versus direct ownership hassles.

Final Reflections on Creating Value Through Patience

The greatest fortunes in history—whether Rockefeller's oil empire, Walton's retail dynasty, or Buffett's investment conglomerate—share a common trait: they compound over decades. TPL demonstrates this principle in pure form. No pivots, no disruption, no innovation breakthroughs. Just patient execution of a simple model while value compounds quietly.

For investors, TPL offers profound lessons. First, sometimes the best investments are hiding in plain sight, obscured by complexity or unconventional structures. Second, time is the ultimate competitive advantage—businesses that can think in decades while competitors think in quarters will win. Third, simplicity and focus beat complexity and diversification when executed well.

For business builders, TPL provides a different template. Not every company needs to disrupt industries or revolutionize technology. Some of the greatest businesses simply own valuable assets, operate them intelligently, and distribute cash to owners. It's not exciting, but it works.

The railroad bondholders who reluctantly accepted land trust certificates in 1888 thought they were receiving consolation prizes for their failed investment. They couldn't have imagined their worthless desert land would one day generate hundreds of millions in annual cash flow. They didn't know the Permian Basin existed, much less that it contained 75 billion barrels of oil. They simply owned land and waited.

One hundred thirty-six years later, that patience has been rewarded beyond imagination. Texas Pacific Land Corporation stands as testament to the power of patient capital, simple business models, and very long time horizons. In a world obsessed with disruption and innovation, TPL reminds us that sometimes the oldest strategies—own valuable assets, collect recurring revenue, return cash to shareholders—remain the best.

The trust that refused to die has become a corporation built to last centuries more. As long as energy is needed, water is scarce, and land has value, Texas Pacific will be there—collecting royalties, generating cash, and creating wealth for those patient enough to participate in its journey.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube