TPG Capital: The Art of Contrarian Private Equity

I. Introduction & Cold Open

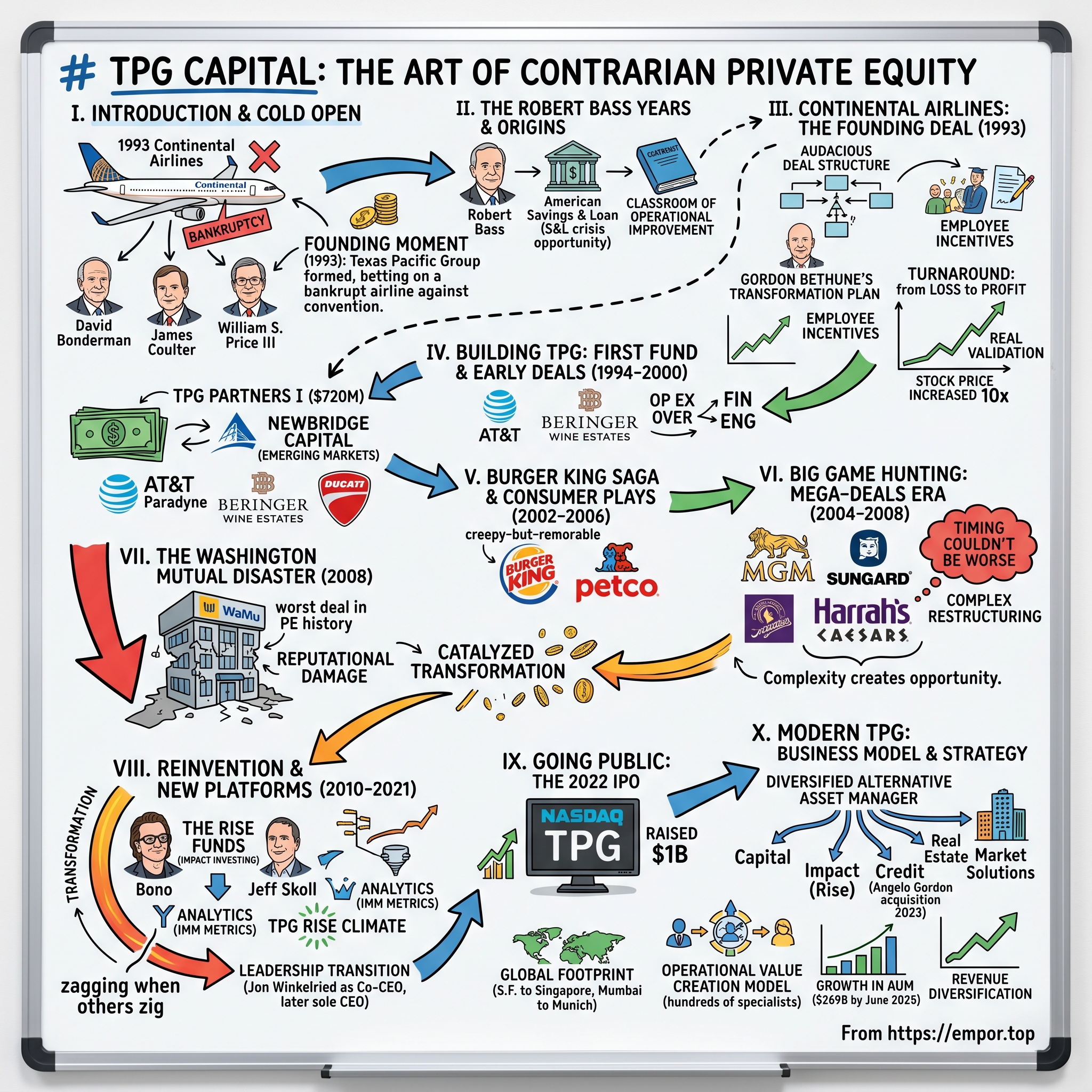

The year is 1993. Continental Airlines sits in bankruptcy court, its fourth CEO in six years having just resigned. The carrier bleeds cash—$108 million in operating losses that year alone. Labor unions seethe with resentment after years of broken promises. Industry analysts write it off as another casualty of the airline shakeout following the Gulf War recession. Most Wall Street firms won't touch it.

But in a Fort Worth office, David Bonderman sees something different. The former bass guitarist turned lawyer turned dealmaker studies the numbers with an intensity that unnerves even his partners. Continental had made $900 million just a few years earlier. The routes are valuable. The brand, despite everything, still carries weight. If you could fix the labor relations, install competent management, and execute a disciplined turnaround—the upside could be extraordinary.

Bonderman picks up the phone to call James Coulter, his protégé from their days at Robert Bass's family office. "I think we should buy an airline," he says. Coulter, ever the numbers man, starts running scenarios. They both know their mentor Bass won't back this play—he's already passed on it once. So they make a decision that will reshape private equity: they'll go it alone.

This is the founding moment of Texas Pacific Group, later known simply as TPG. Three men—Bonderman, Coulter, and William S. Price III—walking away from the safety of a billionaire's backing to bet everything on a bankrupt airline that nobody else wanted. It's a move so audacious that when they show up in bankruptcy court, the judge assumes they're still representing the Bass fortune. They don't correct him.

What unfolds over the next three decades is one of private equity's most remarkable stories. From that single contrarian bet on Continental, TPG would grow into a $239 billion alternative asset management colossus, pioneering everything from impact investing with Bono to complex carve-outs that other firms deemed too difficult. They would suffer spectacular failures—losing $1.35 billion on Washington Mutual in what some called the worst private equity deal ever—yet emerge stronger, eventually taking the firm public in 2022 at a $9 billion valuation.

This is the story of how TPG mastered the art of contrarian investing, building a globally diversified platform across private equity, credit, real estate, and impact strategies. It's about seeing value where others see only risk, about operational excellence over financial engineering, and about maintaining a "nice guy" reputation in an industry often characterized by ruthless cost-cutting. Most importantly, it's about how three partners turned the philosophy of "buying businesses no one else wants" into one of the world's premier investment franchises.

The journey from that bankruptcy courtroom to the NASDAQ opening bell contains lessons not just about private equity, but about patience, partnership, and the power of betting against conventional wisdom when the fundamentals tell a different story.

II. The Robert Bass Years & Origins

Before there was TPG, there was the classroom of Robert Bass—and what a classroom it was. The youngest of four billionaire Bass brothers from Fort Worth, Robert had taken his inheritance from oil wildcatter Sid Richardson and built something different from his siblings' more famous investment vehicles. While brother Sid made headlines with corporate raids and greenmail, Robert quietly assembled a team that would revolutionize leveraged buyouts through operational improvement rather than financial engineering alone.

David Bonderman arrived at Bass's offices in 1983 as an unlikely private equity player. A Harvard Law graduate who'd spent years as a civil rights lawyer and law professor, Bonderman had an intellectual intensity that set him apart from the typical Wall Street dealmaker. He'd represented unions, argued constitutional cases, and could quote obscure legal precedents from memory. But it was his ability to see patterns others missed—to find opportunity in complexity—that caught Robert Bass's attention.

James Coulter joined soon after, a Harvard MBA who became Bonderman's analytical counterpart. Where Bonderman was mercurial and instinctive, Coulter was methodical and precise. Together at Bass Enterprises, they developed what would become TPG's signature approach: finding deeply troubled assets with hidden value, then applying intensive operational expertise to unlock it.

The education came fast and hard. In 1988, Bonderman pushed Bass to acquire American Savings and Loan, a California thrift that had been seized by federal regulators. The entire S&L industry was melting down—the government would eventually spend $124 billion bailing out failed thrifts. Most investors ran from anything touching the sector. But Bonderman saw an arbitrage opportunity: the government was so desperate to offload these assets that it would provide attractive financing and guarantees to buyers.

Bass invested $400 million. The deal required navigating byzantine federal regulations, negotiating with multiple government agencies, and restructuring an institution that had lost $468 million the previous year. Bonderman and Coulter worked eighteen-hour days, sleeping in the office, learning how to transform broken businesses from the inside out. By 1995, when Bass sold to Washington Mutual, that $400 million investment was worth $2 billion—a return that would define their careers. The classroom had more teachers. Bill Price III joined the Bass team after stints at Bain & Company and GE Capital, bringing operational expertise that complemented Bonderman's dealmaking and Coulter's analytics. Together, they formed what one colleague called "the most intellectually formidable investment team in Texas."

But the real test came in 1992. Bonderman had been tracking Continental Airlines through its second bankruptcy. The carrier was toxic—labor relations destroyed, management in chaos, bleeding cash. Yet Bonderman saw the same pattern he'd identified at American Savings: a fundamentally sound business buried under terrible execution. He pitched it hard to Robert Bass.

Bass declined. The airline industry was too volatile, too unionized, too far from his comfort zone. For Bonderman, this was the moment of truth. At age 50, after nearly a decade building Bass's empire, he faced a choice: remain a brilliant lieutenant or strike out on his own.

The decision came during a tense meeting in Bass's Fort Worth office. "Robert, I believe in this deal," Bonderman said. "If you won't do it, I will." Bass, to his credit, understood. Not only did he accept Bonderman's resignation gracefully, he would later invest in the Continental deal as a limited partner—betting on the student rather than the investment.

Coulter faced his own decision. At 33, he was being groomed as Bass's successor. The safe play was to stay. Instead, he chose to follow Bonderman into the unknown. "David taught me to see opportunity where others see disaster," Coulter would later explain. "But more importantly, he taught me that the biggest risk is not taking the right risk when you see it."

Price completed the triumvirate, bringing his GE Capital relationships and operational playbook. The Robert M. Bass Group, Inc. acquired American Savings in December 1988, and the lessons from that deal—navigating government bureaucracy, restructuring distressed operations, managing complex stakeholder relationships—would prove invaluable for what came next.

The three men set up shop with a simple philosophy distilled from their Bass years: buy complexity that others won't touch, apply operational excellence rather than financial engineering, and maintain the patience to see transformations through. They called it "contrarian investing," but it was really about seeing clearly when others were blinded by fear.

As 1992 ended, they had no fund, no institutional backing, and no track record as an independent firm. What they did have was conviction about Continental Airlines and hard-won expertise in turning disasters into fortunes. The education was complete. Now came the test.

III. Continental Airlines: The Founding Deal (1993)

The bankruptcy courtroom in Delaware was nearly empty when David Bonderman stood to address the judge in early 1993. Continental Airlines was on life support—its fourth CEO in six years had just resigned, unions were in open revolt, and the carrier was hemorrhaging $300,000 every single day. The few investment banks that had looked at the deal had walked away. Even the court-appointed advisors seemed resigned to liquidation.

But Bonderman saw what they missed. Yes, Continental had filed for bankruptcy twice. Yes, it had the worst labor relations in the industry. Yes, its customer service rankings were abysmal. But it also had valuable gates at Newark and Houston, a decent route network to Latin America, and—this was crucial—it had made $900 million in operating profit just five years earlier. The airline wasn't fundamentally broken; it was catastrophically mismanaged.

The courtroom drama had an unexpected twist. When Bonderman introduced himself and James Coulter, the judge assumed they were still representing the Bass family fortune. Neither man corrected this misconception. It was a useful fiction—the Bass name carried weight, opened doors, kept conversations going that might otherwise have ended. Only later, after negotiations were well advanced, did stakeholders realize these three men were operating independently.

The deal structure was audacious in its simplicity. Bonderman and Coulter, along with Bill Price, raised $66 million in equity—a combination of their own money, funds from a handful of believers including Robert Bass himself, and a crucial partnership with Air Canada. For this, they acquired 27% of the equity with warrants to increase to 42%—a controlling stake in a $2.5 billion airline. The leverage was extraordinary, but so was the opportunity.

The moment the deal closed in April 1993, Bonderman became chairman and executed a plan they'd been refining for months. Out went the existing management. In came Gordon Bethune, a former Boeing executive who understood both operations and people. Bethune would later describe his first meeting with Bonderman: "He asked me one question: 'Can you make the employees stop hating management?' I said yes. He said, 'You're hired.'"

The transformation was immediate and comprehensive. Within weeks, Bethune was meeting with union leaders, not in corporate boardrooms but in break rooms and hangars. He wore a Continental uniform, flew coach, ate in employee cafeterias. When flight attendants complained about the food service, he changed it. When pilots raised safety concerns, he addressed them immediately. When gate agents said the computer system was garbage, he allocated funds to replace it.

But the real genius was in the incentive alignment. Bonderman and Price structured a profit-sharing plan that gave employees a direct stake in Continental's recovery. Every month the airline made money, every employee got a check. The first profit-sharing payment was just $65 per person. Bethune hand-delivered some of them. The symbolism mattered more than the amount—for the first time in years, management and labor were on the same side.

The numbers tell the story. In 1993, Continental lost $108 million on operations. By 1994, it was profitable. By 1997, operating income hit $716 million. The stock price increased ten-fold. TPG's $66 million investment was worth over $650 million. Air Partners, the vehicle Bonderman created for the deal, delivered returns exceeding 1,000%.

But the real validation came from an unexpected source. The National Franchisee Association, which had observed TPG's approach during due diligence, issued a statement that would define the firm's reputation: "We liked what they had to say about the human component of the businesses they buy. Many other owners are dismissive of labor. These guys understood that you can't transform a service business without transforming the culture."

The Continental deal established three principles that would define TPG for decades. First, operational improvement beats financial engineering. Second, labor relations and culture are often the hidden key to value creation. Third, the best opportunities exist where no one else is willing to look.

As 1993 ended, word of the Continental turnaround spread through investment circles. Three unknowns from Texas had pulled off one of the most audacious buyouts in private equity history. They had no office, no fund, barely any infrastructure. But they had something more valuable: proof that their contrarian approach worked.

Bonderman, ever the showman, marked the moment in characteristic fashion. He threw a party at his Fort Worth home featuring the Rolling Stones—the actual Rolling Stones—performing for a few hundred guests. The message was clear: Texas Pacific Group had arrived, and they were playing a different game than everyone else.

IV. Building TPG: The First Fund & Early Deals (1994-2000)

Fresh off the Continental triumph, Bonderman and Coulter faced a classic Silicon Valley-style problem: they had a hit product but no company. They were operating out of borrowed offices, managing Continental's turnaround while simultaneously trying to raise their first institutional fund. Bonderman worked from Fort Worth, Coulter from San Francisco, conducting partner meetings by phone at 6 AM and 10 PM to bridge the time zones.

The fundraising pitch was unconventional. While other private equity firms led with their pedigrees and financial models, TPG led with a philosophy: "We buy complexity." Their first fund presentation featured case studies of disasters—companies in bankruptcy, industries in upheaval, situations where conventional wisdom said to run away. The Continental story was their calling card, but smart LPs saw something deeper: a reproducible process for finding value in chaos.

They targeted $500 million for TPG Partners I. Skeptics said three guys with one deal couldn't raise institutional money. By late 1994, they closed on $720 million, oversubscribed by 44%. The LP base was telling: university endowments who valued intellectual rigor, pension funds seeking differentiated returns, and importantly, several executives from companies TPG would later target. These weren't just investors; they were a network.

The early deals revealed TPG's emerging playbook. In June 1996, they acquired AT&T Paradyne from Lucent Technologies for $175 million. Paradyne made data communications equipment—unsexy, deteriorating margins, a classic "carve-out" that Lucent wanted gone. TPG saw a technology company trapped inside a bureaucracy. They hired new management, accelerated R&D, and refocused on emerging markets. Three years later, they sold it for $700 million.

But it was the Beringer Wine acquisition that showed TPG's range. In 1996, Nestlé decided wine didn't fit their portfolio—a strategic orphan with great assets but no corporate love. TPG paid $395 million for Wine World Estates, immediately renamed it Beringer Wine Estates, and brought in wine industry veterans who understood premium branding. They consolidated distribution, upgraded vineyards, and pushed into higher-margin segments. When they took it public in 1997, the valuation had nearly tripled.

The Ducati motorcycle purchase that same year seemed to violate every private equity principle. An Italian company, powerful unions, niche market, and a brand that was more myth than business. The Bologna-based manufacturer was hemorrhaging cash, building too many models, and losing to Japanese competitors. TPG's approach was counterintuitive: instead of cost-cutting, they invested heavily in new designs and racing programs. They understood that Ducati wasn't selling motorcycles; it was selling Italian passion on two wheels. By focusing the product line and rebuilding the dealer network, they turned a €90 million loss into €20 million in profit within two years. The geographic expansion came through an innovative structure. In 1994, TPG, Blum Capital and ACON Investments created Newbridge Capital, a joint-venture to invest in emerging markets, particularly in Asia and, later, in Latin America. While competitors focused on developed markets, TPG saw opportunity in Asia's chaos—currencies in flux, regulations changing daily, family-owned conglomerates ripe for modernization. TPG was one of the first alternative asset management firms to establish a dedicated Asia franchise, opening an office in Shanghai in 1994.

In 1997, TPG raised over $2.5 billion for its second private equity fund. The size shocked the industry—from $720 million to $2.5 billion in three years. But LPs weren't buying past performance; they were buying a differentiated strategy. Where KKR and Blackstone competed for mega-buyouts, TPG carved out a niche in complexity.

The J. Crew acquisition in 1997 nearly broke the streak. TPG's most notable investment that year was its takeover of the retailer J. Crew, acquiring an 88% stake for approximately $500 million; the investment struggled due to the high purchase price paid relative to the company's earnings. The retailers was facing competition from Gap and Old Navy, fashion trends were shifting, and TPG paid what many considered a full price. For years, it looked like their first real mistake.

But TPG's response revealed their character. Instead of financial engineering or quick flips, they brought in Mickey Drexler, the retail genius who'd built Gap. They invested in design, upgraded stores, and repositioned J. Crew as "affordable luxury." The company was able to complete a turnaround, beginning in 2002, and to complete an IPO in 2006. The lesson: patience and operational excellence could salvage even problematic deals.

By 2000, TPG had evolved from three guys with a single airline investment to a fully-fledged private equity platform. They had offices in Fort Worth, San Francisco, London, Hong Kong, and Tokyo. They'd completed over 30 deals across industries from technology to wine to motorcycles. Most importantly, they'd proven that their contrarian approach was more than a one-time success—it was a repeatable strategy.

The firm's culture reflected its founders' personalities. Bonderman collected art and threw legendary parties—Bob Dylan at his 60th birthday, the Eagles for a partners' meeting. Coulter was the strategist, building institutional processes while maintaining entrepreneurial flexibility. Price was the operator, developing a bench of executives who could parachute into portfolio companies.

V. The Burger King Saga & Consumer Plays (2002-2006)

The Burger King boardroom in Miami was tense in November 2002. TPG's deal team sat across from Diageo executives, both sides staring at financial projections that had gone from bad to catastrophic. The $2.3 billion buyout announced just four months earlier—TPG's largest deal to date—was falling apart. Same-store sales had collapsed, integration costs had exploded, and Burger King was missing every performance target in the purchase agreement.

Most firms would have walked away or demanded a dramatic price cut that would poison the relationship. TPG did something different. They asked for time to talk to franchisees.

The franchise meetings revealed what Diageo had missed. The 8,000 franchisees who controlled 92% of Burger King restaurants weren't just angry about declining sales—they felt abandoned by years of corporate neglect. Marketing was inconsistent, menu innovation had stalled, and the stores looked tired compared to McDonald's recent renovations. But underneath the frustration, TPG heard something else: these small business owners desperately wanted to succeed.

In July 2002, TPG, together with Bain Capital and Goldman Sachs Capital Partners, announced the $2.3 billion leveraged buyout of Burger King from Diageo. However, in November the original transaction collapsed, when Burger King failed to meet certain performance targets. In December 2002, TPG and its co-investors agreed on a reduced $1.5 billion purchase price for the investment.

The renegotiation was brutal but fair. TPG cut the price to $1.5 billion but committed to a transformation that went beyond cost-cutting. They'd spent two years before the bid cultivating relationships with the National Franchisee Association. As the association's chairman later said: "We liked what they had to say about the human component of the businesses they buy. Many other owners are dismissive of labor."

The TPG consortium had support from Burger King's franchisees, which controlled approximately 92% of Burger King restaurants at the time of the transaction. This wasn't just diplomatic nice-to-have—it was essential. Unlike company-owned chains, Burger King's model meant franchisees controlled everything from store renovations to menu compliance. Without their buy-in, no turnaround was possible.

TPG's playbook was methodical. They brought in Brad Blum, a former CEO of Olive Garden who understood franchisee relations. They invested $750 million in store renovations, creating a "20/20" program that helped franchisees redesign restaurants. Most boldly, under its new owners, Burger King underwent a brand overhaul including the use of The Burger King character in advertising. The creepy-but-memorable King became a cultural phenomenon, driving younger customers back to stores.

The parallel Petco investment showed TPG's range in retail. They'd taken the pet supplies chain private in 2000 for $600 million, then drove a massive expansion—from 530 stores to over 800, while launching an e-commerce platform that competed with early online rivals. When they took it public again in 2002, the valuation had doubled. Then, remarkably, they took it private again in 2006 for $1.8 billion when public markets undervalued the growth potential. It was financial engineering, but with operational substance underneath.

In February 2006, Burger King announced plans for an initial public offering. The IPO in May 2006 valued the company at $2.4 billion, netting TPG and partners a $900 million profit on their $425 million equity investment. More importantly, the deal cemented TPG's reputation as the private equity firm that could handle complex franchisee relationships—a skill that would prove invaluable in future restaurant and retail deals.

The consumer plays of this era revealed TPG's evolution. They weren't just financial engineers or operational experts—they were business anthropologists, understanding the human dynamics that drove value. Whether dealing with Burger King franchisees, Petco customers, or Ducati enthusiasts, they recognized that emotion, culture, and relationships often mattered more than spreadsheets.

This human-centric approach differentiated TPG in an industry increasingly dominated by financial modeling. While competitors focused on leverage ratios and exit multiples, TPG asked different questions: Who are the stakeholders beyond shareholders? What emotional connections drive purchasing decisions? How do you align incentives across complex ecosystems?

The answers to these questions would guide TPG into its next phase: the mega-deals era, where the stakes—and the complexity—would reach unprecedented levels.

VI. Big Game Hunting: Mega-Deals Era (2004-2008)

The phone call came at midnight Fort Worth time in September 2004. David Bonderman was in his home office when the Sony executives rang: "We need a partner for MGM. Are you interested?" Metro-Goldwyn-Mayer, the legendary studio behind James Bond and Rocky, was finally for sale after years of Kirk Kerkorian shopping it around. The price tag: nearly $5 billion. It would be TPG's largest deal ever, and one of the most complex given the studio's tangled rights structure and massive film library.

After a bidding war which included Time Warner and General Electric, MGM was acquired on September 23, 2004, by a partnership consisting of Sony Corporation of America, Comcast, Texas Pacific Group, Providence Equity Partners, and other investors. The consortium structure was unprecedented—Sony wanted the content for its Blu-ray format, Comcast wanted cable programming, and the private equity firms wanted the cash flows from the 4,000-film library. Sony's primary goal was to ensure Blu-ray Disc support at MGM; cost synergies with Sony Pictures Entertainment were secondary.

TPG's role was crucial but specific: they would handle the operational turnaround while Sony managed distribution. The deal valued MGM at $4.8 billion including debt, with TPG and Providence each investing approximately $450 million. It was a classic TPG play—a storied but struggling asset, multiple stakeholders with different agendas, and value hidden in complexity that others couldn't untangle.

But 2005 brought an even bigger opportunity. In 2005, TPG was involved in the buyout of SunGard in a transaction valued at $11.3 billion. TPG's partners in the acquisition were Silver Lake Partners, Bain Capital, Goldman Sachs Capital Partners, Kohlberg Kravis Roberts, Providence Equity Partners, and Blackstone Group. This represented the largest leveraged buyout completed since the takeover of RJR Nabisco at the end of the 1980s leveraged buyout boom.

The SunGard deal was remarkable not just for its size but for its structure. Seven private equity firms coming together was almost unheard of—the egos, the economics, the governance challenges seemed insurmountable. The involvement of seven firms in the consortium was criticized by investors in private equity who considered cross-holdings among firms to be generally unattractive. Yet TPG's Coulter helped architect a structure where each firm took specific responsibilities: Silver Lake handled technology strategy, Blackstone managed financing, TPG drove operational improvements.

At the time of its announcement, SunGard would be the largest buyout of a technology company in history, a distinction later ceded to the buyout of Freescale Semiconductor. The $11.3 billion price tag sent shockwaves through Wall Street. This wasn't just private equity buying companies anymore—this was private equity reshaping entire industries. The Harrah's/Caesars deal would define TPG's reputation for a decade. In December 2006, affiliates of Texas Pacific Group and Apollo Management agreed to acquire Harrah's in an all-cash transaction valued at approximately $27.8 billion, including the assumption of approximately $10.7 billion of debt. It was one of the largest leveraged buyouts in history, dwarfing even the SunGard transaction.

The structure showcased TPG's analytical sophistication. David Bonderman had identified a crucial arbitrage: casino companies traded at lower multiples than hotel REITs despite owning similar real estate. The plan was elegant—split Harrah's into an operating company and a property company, unlock the real estate value, and ride the continuing boom in Las Vegas tourism. TPG would focus on what Bonderman called "the left side of the balance sheet"—operations, customer experience, technology upgrades. Apollo, led by Marc Rowan, would handle the right side—financial structuring, debt markets, capital allocation.

David Bonderman, TPG founding partner, said at the announcement: "We are delighted to be joining with the excellent management team at Harrah's and our private equity partners to continue to build on the Company's strong foundation." CEO Gary Loveman, who rolled over $95 million of his own money into the deal, proclaimed: "This will be a change in ownership, not a change in direction."

The timing couldn't have been worse. The deal was announced in December 2006 but didn't close until January 2008—just months before the financial crisis. TPG and Apollo completed their nearly $30 billion acquisition of Caesars, then called Harrah's, in January 2008 as the Strip thrived amid an economic boom. However, the party would end just a few months later when Lehman Brothers filed for bankruptcy, unleashing the worst U.S. economic downturn since the 1930s.

The private equity firms had loaded Caesars with debt to make their purchase—$25.1 billion in total—leaving the casino operator vulnerable when the economy crashed. Las Vegas tourism collapsed, gaming revenues plummeted, and the highly leveraged structure that looked brilliant in 2006 became a millstone by 2009.

What followed was one of the most complex restructurings in corporate history. Caesars filed for bankruptcy in 2015 and emerged two years later when the private equity firms agreed to spin off some of the company's properties into a real estate investment trust. The saga included over 50 financial transactions, lawsuits accusing the firms of "corporate looting," and negotiations that would stretch for nearly a decade. TPG and Apollo held about 16 percent of Caesars when the company exited bankruptcy in October 2017, down from their original 100% ownership.

The Caesars debacle would haunt TPG for years, becoming a cautionary tale about leverage, timing, and hubris. Yet even as that deal unraveled, TPG was already pivoting, learning from the crisis, and preparing for what would become its most audacious bet yet: Washington Mutual.

VII. The Washington Mutual Disaster (2008)

The conference call on Sunday, April 6, 2008, started at 7 AM Pacific time. David Bonderman was in his Fort Worth office, surrounded by stacks of Washington Mutual financials. On the line were dozens of TPG partners, analysts, and advisors scattered across the globe. The question before them was stark: should TPG lead a $7 billion rescue of the nation's largest savings and loan, a institution with $307 billion in assets that was hemorrhaging deposits and facing a tsunami of mortgage defaults?

The numbers were terrifying. WaMu had lost $1.1 billion in the fourth quarter of 2007. Its stock had fallen from $45 to $13 in less than a year. The bank's aggressive push into option-ARM mortgages—loans that allowed borrowers to choose their monthly payment, often less than the interest owed—had created a ticking time bomb. Yet Bonderman saw opportunity in the carnage. WaMu had 2,200 branches, 43,000 employees, and deep relationships in attractive markets like California and Florida. If TPG could stabilize the bank, the upside was enormous.

On April 7, 2008, TPG led a $7 billion investment in Washington Mutual. The deal structure seemed to protect TPG: they bought newly issued shares at $8.75 each, receiving warrants to purchase additional shares and, crucially, a "price reset" feature. If WaMu raised capital at a lower price, TPG would receive additional shares to maintain their ownership percentage. It was supposed to be downside protection. It became meaningless when the bank failed entirely.

The speed of WaMu's collapse stunned even seasoned financiers. In July, IndyMac Bank failed, triggering panic among depositors at other troubled institutions. By September, after Lehman Brothers collapsed on September 15th, the run on WaMu became unstoppable. Depositors pulled $17 billion in just ten days—nearly 10% of the bank's deposits. Lines formed outside branches. The FDIC later revealed they were tracking WaMu hourly, watching a 150-year-old institution die in real-time.

The end came with brutal swiftness. On September 25, 2008, while WaMu CEO Alan Fishman was literally in the air flying to Seattle, regulators seized the bank. The Office of Thrift Supervision declared WaMu insolvent and appointed the FDIC as receiver. Within hours, JPMorgan Chase acquired WaMu's banking operations for $1.9 billion. TPG's investment—just 140 days old—was worthless.

The numbers were staggering: TPG lost $1.35 billion, making it what some analysts called "the worst deal in private equity history." The fund that invested in WaMu, TPG Partners VI, would ultimately return just 0.9x to investors—the only TPG fund to ever lose money. Limited partners were furious. Several sued, claiming TPG had been reckless in its due diligence.

But the real damage was reputational. TPG had built its brand on operational excellence and contrarian wisdom. WaMu suggested they'd confused contrarianism with recklessness. Critics pointed out warning signs TPG had missed or ignored: the bank's exposure to California real estate, its weak underwriting standards, its aggressive accounting. One competitor privately called it "catching a falling knife with your face."

David Bonderman's response was characteristically defiant and introspective. At a partner meeting in October 2008, he reportedly said: "We got this completely wrong. We misread the speed of the crisis, the psychology of bank runs, and the government's willingness to let institutions fail. But if we stop taking risks because of one disaster, even one this big, then we're not TPG anymore."

The firm's recovery strategy was methodical. First, they stopped trying to defend the investment publicly, acknowledging the failure openly. Second, they doubled down on operational improvements in existing portfolio companies, showing LPs they could still create value. Third, and most importantly, they began developing new investment platforms that would diversify beyond traditional buyouts.

Years later, James Coulter would reflect on WaMu as TPG's "near-death experience." It forced the firm to evolve from a pure-play private equity shop into a multi-platform alternative asset manager. The lessons were expensive but transformative: diversification matters, timing is everything, and sometimes the contrarian bet is wrong.

The WaMu disaster could have destroyed TPG. Instead, it catalyzed a transformation that would, improbably, make them stronger. As 2008 ended with markets in freefall and critics writing TPG's obituary, Bonderman and Coulter were already planning their next act.

VIII. Reinvention & New Platforms (2010-2021)

The meeting took place in an unlikely venue: Bono's Dublin home in early 2016. James Coulter sat across from the U2 frontman, with Jeff Skoll, eBay's first president, joining by video from California. The topic seemed almost absurd for a private equity firm still recovering from WaMu and Caesars: could TPG build a fund that generated both market-rate returns and measurable social impact?

"Capitalism is going up on trial," Bono told them, in what would become a defining phrase for the venture. "Putting profit before people is an unsustainable business model." For most PE firms, this would have been heresy. For TPG, emerging from its darkest period, it was revelation.

The Rise Funds were created in 2016 with the fundamental belief that private enterprise can contribute significantly to addressing various societal challenges globally while delivering strong financial returns. TPG pioneered institutional scale impact investing with the creation of The Rise Fund in 2016. The partnership was unconventional—Founded in 2016 by TPG in partnership with Bono and Jeff Skoll, The Rise Funds invest behind impact entrepreneurs and growth-stage, high potential, mission-driven companies that are focused on achieving the United Nations' Sustainable Development Goals.

The skepticism was immediate and fierce. "There is a lazy mindedness that we afford the do-gooders," Bono himself acknowledged, slamming the rigor of most impact investing to date as "a lot of bad deals done by good people." Critics questioned whether a firm known for leveraged buyouts could genuinely deliver social impact without sacrificing returns.

But TPG's approach was rigorously analytical. They created Y Analytics, a public benefit entity dedicated to developing an "Impact Multiple of Money" (IMM) methodology that would quantify social and environmental outcomes alongside financial returns. From the start, they dedicated significant resources to developing impact underwriting tools and rigorous impact assessment. As a result, they created Y Analytics, a public benefit entity dedicated to helping their impact team better understand, value, and manage social and environmental impact.

The fundraising exceeded all expectations. Private equity firm TPG collected $2 billion for The Rise Fund, tapping growing demand for impact investing to create the largest pool of its kind. The fund, which TPG raised in about seven months, surpassed its $1.5 billion target and hit its $2 billion hard cap, or the maximum amount of outside capital allowed by its agreement with investors. This wasn't charity—major pension funds and sovereign wealth funds committed nine-figure sums.

The Rise Fund's early investments proved the model could work. The Rise Fund was born out of TPG Growth's outstandingly successful investment in Apollo Towers, Indian mobile phone tower company which helped the country progress from zero cell phone penetration to roughly 70 percent, which has subsequently increased GDP by 5 percent whilst simultaneously doubling the value of TPG's initial investment. By 2018, they made their first African investment—a purchase of a stake in digital payments provider Cellulant worth $47.5 million, making it the largest recorded deal involving a FinTech company which trades exclusively in Africa.

The platform expansion accelerated. In 2021, with the launch of TPG Rise Climate in 2021, TPG created the TPG Rise Climate Coalition to bring together nearly 30 of the world's largest multinational companies to facilitate the exchange of expertise, insight, investment ideas and opportunities amongst the coalition. By 2024, with approximately $14 billion in assets across The Rise Funds, TPG Rise Climate, and the Evercare Health Fund, the TPG Rise platform became the world's largest private markets impact investing platform committed to achieving measurable, positive social and environmental outcomes alongside competitive financial returns. The leadership transition marked TPG's full transformation from founder-led buyout shop to institutional alternative asset manager. In 2015, Jon Winkelried joined as Co-CEO alongside Jim Coulter. Winkelried, who previously served as President and Co-Chief Operating Officer of Goldman Sachs, brought institutional credibility and operational discipline. During his 27-year tenure at Goldman Sachs, Winkelried held various senior roles including co-head of the firm's Investment Banking division, co-head of Fixed Income, Currency and Commodities division, and head of the firm's Leveraged Finance business.

The appointment was strategic. "Jon brings experience, insights and creativity to TPG as we continue our evolution as a firm," said Coulter at the time. The partnership brought together complementary skillsets—Coulter's entrepreneurial vision and Winkelried's institutional expertise. The appointment brought together complementary skillsets, and with TPG's global team of senior leaders, Coulter and Winkelried led the firm through a period of significant growth and expansion, nearly doubling the firm's assets under management over the past five years.

By May 2021, the transition was complete. TPG announced that Co-Founder Jim Coulter became Executive Chairman of the firm and Jon Winkelried, who had served as Co-Chief Executive Officer with Coulter, was named sole Chief Executive Officer. As Executive Chairman, Coulter would increase his focus on investing activities, becoming the Managing Partner for TPG Rise Climate, the firm's newly formed climate initiative.

"TPG has continued to succeed because of the trust we put behind leadership; the firm's future under Jon's direction will be no different," said Bonderman about the transition. The symbolism was clear: TPG was no longer the scrappy contrarian firm of three partners betting on distressed airlines. It had become a global platform managing multiple strategies across markets.

The platform expansion was remarkable. Beyond traditional buyouts and the Rise impact funds, TPG built capabilities in growth equity, real estate, credit, and special situations. Each platform operated semi-autonomously but benefited from TPG's accumulated expertise in operational transformation. The firm that once focused solely on "buying businesses no one else wants" now competed across the full spectrum of alternative investments.

The cultural evolution was equally significant. While maintaining its contrarian DNA and operational focus, TPG adopted the infrastructure and governance of a major financial institution. Risk committees, compliance systems, institutional reporting—all the architecture that Winkelried had mastered at Goldman Sachs. Yet somehow, TPG retained its entrepreneurial spirit, continuing to make bold bets while managing downside risk more carefully than in the WaMu era.

As 2021 ended, TPG managed over $100 billion in assets across its platforms. The firm employed over 800 professionals across 18 offices globally. From three partners and a single investment in Continental Airlines, TPG had built one of the world's premier alternative asset managers. The only question remaining was whether the public markets would value this transformation. That answer would come in 2022.

IX. Going Public: The 2022 IPO

The morning of January 13, 2022, marked a historic moment at the NASDAQ MarketSite in Times Square. Jon Winkelried stood at the podium, flanked by partners from around the world, as TPG's ticker symbol appeared on screens for the first time. After three decades as a private partnership, TPG was now a public company.

The numbers told the story of both ambition and market reality. TPG announced the pricing of its initial public offering of 33,900,000 shares of its Class A common stock at a price of $29.50 per share. Of the offered shares, 28,310,194 shares were being offered by the Company and 5,589,806 shares were being offered by an existing strategic investor. The pricing at the midpoint of the $28-$31 range suggested measured investor enthusiasm rather than exuberance.

Private equity firm TPG raised $1 billion in its U.S. initial public offering on Wednesday, at a valuation of $9.1 billion. For context, Compared to the AUM of other public PE firms—Blackstone ($731 billion), Apollo Global Management ($481 billion), KKR ($459 billion) and The Carlyle Group ($293 billion)—TPG entered the public markets as a smaller firm. Yet TPG managed $109 billion of assets under management, making it a formidable player despite its relative size.

The timing was both strategic and challenging. Public PE firms had considerably outperformed the S&P 500 in recent years. While the S&P grew about 115% over the past five years, Blackstone's stock climbed 445% during the same period. KKR rose 409%, Apollo 290% and Carlyle 268%. The public markets had developed an appetite for alternative asset managers, recognizing their ability to generate consistent fee income and occasional spectacular carried interest windfalls.

But the market environment was turning hostile. After coming off a strong 2021—fueled in part by pandemic-winning tech stocks—the Nasdaq Composite was down by about 4% since the start of the year. The day before TPG's debut, JustWorks, the HR software company with an estimated valuation of $2 billion, said it had decided to delay its IPO "due to market conditions at this time".

The IPO structure revealed TPG's evolution into an institutional firm. TPG's IPO documents contained a detailed succession plan that would eventually lead to oversight by a majority independent board of directors, which would be elected by shareholders. This was a far cry from the partnership structure where Bonderman and Coulter made decisions over dinner.

TPG was founded in 1992 by David Bonderman and James Coulter, who remain active at the firm, as well as Bill Price III, who retired in 2006. Now, thirty years later, the founders were ceding control to public shareholders, albeit gradually. The dual-class structure would maintain founder influence initially, but the trajectory toward full institutional governance was clear.

TPG invests across five multi-product platforms: Capital, Growth, Impact, Real Estate, and Market Solutions and the unique strategy is driven by collaboration, innovation. This diversification was key to the IPO pitch—TPG wasn't just a buyout shop anymore, but a diversified alternative asset manager with multiple revenue streams.

The first day of trading on January 13, 2022, saw shares open at $33.25, above the IPO price, before settling near $31. Not spectacular, but solid. The market was signaling qualified approval—TPG had successfully transformed from a scrappy partnership to a public institution, but questions remained about growth prospects and competitive positioning.

For Bonderman and Coulter, watching from their respective offices in Fort Worth and San Francisco, it was a bittersweet moment. They'd built something far greater than they'd imagined when walking away from Robert Bass in 1992. But going public meant the end of an era—no more decisions based purely on conviction, no more patient capital without quarterly scrutiny, no more keeping score by their own metrics alone.

As 2022 unfolded, TPG stock would face the same volatility affecting all growth stocks as interest rates rose and recession fears mounted. But the die was cast. TPG was now playing a different game, one where success would be measured not just in IRRs and multiples, but in quarterly earnings calls and stock price movements. The transformation from contrarian cowboys to public company was complete.

X. The Modern TPG: Business Model & Strategy

The modern TPG operates at a scale unimaginable to its founders in 1992. A leader in the alternative asset space, TPG manages $269 billion in assets through a principled focus on innovation as of June 2025. This represents explosive growth from the $109 billion at the time of the IPO just three years earlier, driven both by organic expansion and strategic acquisitions.

The transformation is most evident in TPG's platform architecture. TPG puts capital to work through six platforms, each operating as a semi-autonomous business unit with dedicated teams, strategies, and investor bases. The Capital platform remains the flagship, housing traditional buyout funds that execute the complex, contrarian deals that built TPG's reputation. But it's now just one piece of a diversified machine.

The Impact platform, anchored by the Rise Funds, manages over $14 billion focused on delivering both financial returns and measurable social outcomes. This isn't greenwashing—TPG developed proprietary metrics through Y Analytics to quantify impact alongside IRR. Portfolio companies range from education technology in India to sustainable agriculture in Africa, proving that doing good and doing well aren't mutually exclusive.

The Credit platform exploded following TPG's acquisition of Angelo Gordon in November 2023, adding more than $220 billion of assets across a broadly diversified set of strategies. This wasn't just bolt-on growth—it fundamentally changed TPG's business mix, adding predictable fee streams from credit strategies that balance the volatility of private equity carried interest.

Real Estate emerged as a distinct platform, moving beyond opportunistic deals to systematic strategies across property types and geographies. From logistics warehouses capitalizing on e-commerce growth to workforce housing addressing affordability crises, TPG applies its operational lens to physical assets.

Market Solutions represents TPG's answer to the liquidity demands of modern investors. These strategies provide more frequent realizations than traditional private equity, using publicly traded securities, secondaries, and co-investments to generate returns with different risk-return profiles.

The geographic footprint reflects global ambitions. TPG's investment and operational teams around the world combine deep product and sector experience with broad capabilities and expertise to develop differentiated insights and add value for fund investors, portfolio companies, management teams, and communities. Offices span from San Francisco to Singapore, Mumbai to Munich, each staffed with local professionals who understand regional dynamics while tapping into TPG's global resources.

The talent strategy has evolved dramatically. While Bonderman and Coulter built TPG with a small team of generalists, today's firm employs specialists across every conceivable discipline. Former CEOs run portfolio operations teams. Industry veterans lead sector-focused investment groups. Data scientists build proprietary analytics platforms. The firm that once relied on three partners' instincts now deploys institutional-grade capabilities.

TPG manages investment funds in growth capital, venture capital, public equity, and debt investments. The firm invests in industries including consumer/retail, media and telecommunications, industrials, technology, travel, leisure, and health care. This sector diversification reduces concentration risk while allowing TPG to capitalize on cross-industry trends like digital transformation and sustainability.

The operational value creation model remains central but has sophisticated beyond recognition. TPG's portfolio operations team numbers in the hundreds, providing expertise in digital transformation, procurement optimization, talent management, and dozens of other disciplines. They don't just advise—they embed with portfolio companies, becoming temporary executives who execute transformations alongside management.

Fee structures have diversified alongside strategies. Traditional private equity funds still charge "2 and 20"—2% management fees and 20% carried interest. But credit funds, real estate vehicles, and perpetual capital strategies generate different economics. This diversification smooths earnings, making TPG more predictable for public market investors who dislike volatility.

The competitive positioning is nuanced. TPG isn't the largest—Blackstone manages nearly three times the assets. It isn't the oldest—KKR predates it by decades. But TPG carved out a distinct identity: the operationally-focused, innovation-driven firm that thrives on complexity. While competitors chase scale through mega-funds, TPG builds new platforms. While others focus on financial engineering, TPG emphasizes operational transformation.

Technology integration accelerated post-IPO. Machine learning models screen thousands of potential investments. Proprietary databases track operational metrics across portfolio companies in real-time. Digital platforms connect TPG's experts with portfolio company executives globally. The firm that started with spreadsheets and instinct now runs on data and algorithms—though human judgment remains paramount.

The LP base evolved from university endowments and family offices to include sovereign wealth funds, insurance companies, and increasingly, retail investors through various fund structures. Rooted in a family office heritage, TPG brings institutional-quality private equity, real estate, and credit opportunities to eligible individual investors. Their innovative approach and close collaboration with financial advisors make it easy for individual investors to access the same exclusive investment opportunities once only reserved for institutions.

As 2024 progresses, TPG stands as validation of its founders' vision—but also transcends it. The scrappy contrarians who bought a bankrupt airline built a global institution managing more capital than many countries' GDP. Yet underneath the institutional polish, the contrarian DNA persists. TPG still seeks complexity others avoid, still believes in operational excellence over financial engineering, still maintains that patience and conviction beat momentum and consensus.

The question facing modern TPG isn't whether it can compete—it clearly can. The question is whether it can maintain its differentiated culture and investment edge while operating at institutional scale with public market scrutiny. History suggests few firms successfully navigate this transition. But then again, TPG has always thrived by defying conventional wisdom.

XI. Playbook: Investment Philosophy & Lessons

The conference room walls at TPG's San Francisco headquarters display a simple phrase that has guided the firm for three decades: "Complexity creates opportunity." It's more than a slogan—it's the distillation of an investment philosophy that turned three partners with no fund into a $269 billion global platform.

The contrarian foundation runs deeper than simply buying unpopular assets. TPG "thrives by buying businesses no one else wants"—but the key word is "thrives." This isn't bottom-fishing or distressed investing in the traditional sense. TPG seeks situations where complexity obscures value, where multiple stakeholders create gridlock, where operational challenges mask strategic potential. Continental Airlines had four CEOs in six years and hostile unions—complexity. MGM had tangled rights structures and multiple corporate owners with different agendas—complexity. Washington Mutual had... well, that was complexity that even TPG couldn't untangle.

The operational excellence imperative distinguishes TPG from financial engineers. When TPG bought Burger King, they didn't just restructure debt and cut costs. They invested $750 million in store renovations, revolutionized marketing with the creepy King character, and most importantly, aligned franchisee incentives with corporate success. The National Franchisee Association's endorsement—"We liked what they had to say about the human component of the businesses they buy"—became TPG's calling card. This focus on operations over engineering means longer hold periods but often spectacular returns when transformations succeed.

Pattern recognition across cycles provided TPG's edge. Bonderman and Coulter witnessed the S&L crisis at Bass, applied those lessons to the airline shakeout, then the dot-com bust, the financial crisis, and the pandemic. Each crisis created similar patterns: forced sellers, frozen credit markets, operational paralysis. TPG learned to move when others couldn't, having pre-positioned capital and relationships to strike quickly. The Rise Fund itself emerged from recognizing a pattern—institutional capital seeking impact investments but finding few scaled platforms.

The stakeholder alignment philosophy emerged from painful experience. Continental succeeded because TPG aligned with unions and franchisees. Caesars failed partly because TPG and Apollo couldn't align creditor interests. The lesson: financial engineering means nothing if human incentives aren't aligned. Today, TPG spends as much time on stakeholder mapping as financial modeling, understanding who wins, who loses, and how to create structures where everyone benefits from success.

Patience as competitive advantage seems paradoxical in an industry obsessed with IRRs and quick flips. But TPG's greatest successes came from patience. They held Continental for years while fixing operations. They spent two years cultivating Burger King franchisees before bidding. They developed Rise for impact over several years before raising a fund. In a world of quarterly earnings and annual fund-raising cycles, the ability to think in decades becomes increasingly rare—and valuable.

The portfolio construction discipline evolved through expensive mistakes. Early TPG funds concentrated bets—Continental was essentially the entire first portfolio. But WaMu taught them about correlation risk—when financial markets seize, everything financial struggles simultaneously. Modern TPG portfolios balance sectors, geographies, and strategies. No single investment can break a fund. No single theme dominates. It's less exciting but more sustainable.

Risk management transformed from gut instinct to institutional process. Early TPG relied on Bonderman's genius and Coulter's analysis. Modern TPG employs chief risk officers, runs Monte Carlo simulations, and maintains strict investment committees. But they learned not to let process kill judgment. The best investments—Continental, Rise, even attempting WaMu—required conviction beyond what models could capture. The trick is knowing when to trust the model and when to trust experience.

The talent leverage model scaled beyond the founders. TPG learned that operational excellence requires operators, not just advisors. So they hired former CEOs as partners, not consultants. They gave carry to operating executives, not just deal partners. They created apprenticeship programs where young professionals work directly with portfolio companies, not just on deal models. The firm's human capital became as important as its financial capital.

Geographic expansion followed opportunity, not fashion. While competitors rushed to China for growth, TPG created Newbridge Capital, a joint-venture to invest in emerging markets, particularly in Asia and, later, in Latin America as early as 1994. They understood that complexity in emerging markets created even more opportunity—if you had local knowledge and global resources. Each geography required different approaches: consensus-building in Japan, government relations in India, family partnerships in Latin America.

The platform evolution strategy emerged from client demands and market gaps. LPs wanted impact investing, so TPG created Rise. Markets needed credit solutions, so TPG acquired Angelo Gordon. Each platform started with a specific opportunity but expanded based on capabilities. The lesson: don't force diversification, let it emerge from expertise.

Value creation evolved from cost-cutting to growth acceleration. Early LBOs focused on efficiency—cut costs, improve margins, exit. But TPG learned that sustainable value comes from growth. Invest in technology, expand markets, improve products. It requires more capital and longer horizons, but creates more value and better outcomes for all stakeholders.

The cultural preservation challenge intensified with scale. How do you maintain entrepreneurial culture in a 1,000-person organization? TPG's answer: radical decentralization with strong values. Each platform operates independently but shares TPG's core principles. Investment committees include founders to preserve institutional memory. Compensation rewards long-term value creation over short-term fees.

The public market navigation required new muscles. Quarterly earnings calls, proxy advisors, regulatory scrutiny—none of this existed in the partnership days. TPG learned to communicate financial complexity to public investors while maintaining strategic flexibility. They balance transparency with competitive sensitivity, disclosure with discretion.

The technology integration accelerated everything. Data analytics identify patterns humans miss. Machine learning models process thousands of investment opportunities. Digital platforms connect global teams instantly. But TPG learned technology amplifies judgment, doesn't replace it. The best investors still rely on pattern recognition, relationship building, and conviction—technology just makes them faster and more informed.

Looking forward, TPG's playbook continues evolving. Climate change creates complexity—and opportunity. Demographic shifts restructure entire industries. Technology disrupts business models daily. Each change creates situations where operational excellence, stakeholder alignment, and patient capital can generate extraordinary returns.

The lessons from TPG's journey distill to timeless principles: Complexity creates opportunity for those who can navigate it. Operational excellence beats financial engineering over time. Stakeholder alignment enables sustainable value creation. Patience provides competitive advantage in impatient markets. Culture scales through values, not rules.

These aren't revolutionary insights. But executing them consistently, at scale, through multiple cycles, across diverse strategies—that's the art of private equity. TPG didn't invent these principles, but they've mastered their application. And in an industry where everyone has capital, that mastery remains their edge.

XII. Analysis & Future Outlook

The bear case for TPG writes itself in the headlines of 2024-2025. Interest rates remain elevated, making leverage expensive and exits challenging. The denominator effect—where institutional investors become overallocated to alternatives as public markets struggle—constrains new fund-raising. Competition intensifies as everyone from sovereign wealth funds to family offices launches direct investment programs, compressing returns. Management fees face pressure as LPs demand better terms. The glory days of private equity, critics argue, are over.

The numbers support some skepticism. TPG trades at a significant discount to net asset value, suggesting public markets doubt the sustainability of current valuations. The stock volatility—swinging 40% in twelve months—reflects uncertainty about future performance. With $246 billion of assets under management, TPG faces the law of large numbers: generating 20% returns on $250 billion is exponentially harder than on $25 billion.

The competitive landscape grows more challenging daily. Blackstone's scale provides unmatched resources. Apollo's credit expertise runs deeper. KKR's technology investments position them for the digital economy. Newer entrants like Thoma Bravo dominate software buyouts. Everyone claims operational expertise now—TPG's historical differentiator has been commoditized.

Yet the bull case remains compelling. TPG invests across a broadly diversified set of strategies, including private equity, impact, credit, real estate, and market solutions—diversification that provides multiple growth vectors regardless of market conditions. When buyout markets slow, credit strategies generate returns. When traditional strategies struggle, impact investing attracts capital. This isn't a one-trick pony dependent on leverage and multiple expansion.

The secular tailwinds for alternative assets remain powerful. Pension funds need returns that public markets can't deliver. Insurance companies seek yield in a low-rate world. Sovereign wealth funds deploy oil revenues into diversifying economies. The institutional shift from 5% alternatives allocation to 15-20% continues inexorably. TPG's $246 billion of assets under management could double without taking market share—just by capturing natural market growth.

TPG's positioning for future megatrends looks prescient. The Rise Climate fund capitalizes on trillions in energy transition investment. Healthcare platforms benefit from aging demographics. Asian strategies tap into the world's growth engine. Technology expertise positions them for AI and digital transformation. While competitors fight over traditional buyouts, TPG builds platforms for tomorrow's opportunities.

The operational DNA provides enduring advantage in a world where financial engineering no longer suffices. As credit markets normalize and multiples compress, returns will come from operational improvement. TPG's decades of operational experience, hundreds of operating partners, and proven transformation playbooks become more valuable, not less. When everyone has capital, execution determines winners.

The talent pipeline suggests continued innovation. TPG attracts former CEOs who want to build rather than retire. Young professionals join for the operational experience, not just financial modeling. The culture rewards long-term value creation over short-term fee generation. This human capital compounds over time, creating institutional knowledge that money can't buy.

Comparing TPG to peers reveals distinct positioning. Blackstone dominates through scale—but scale creates bureaucracy. Apollo excels at credit—but credit faces compression as markets normalize. KKR spans everything—but breadth can dilute focus. Carlyle struggles with succession—a challenge TPG navigated successfully. TPG's sweet spot—large enough for resources, small enough for agility, diversified enough for resilience, focused enough for expertise—may prove optimal.

The technology transformation accelerates TPG's advantages. Data analytics identify opportunities faster. Digital platforms enable remote due diligence. AI enhances pattern recognition. Portfolio companies benefit from TPG's tech expertise and vendor relationships. Technology doesn't replace judgment but amplifies it—and TPG has both.

ESG evolution from compliance to value creation favors TPG's approach. The Rise Funds proved impact investing can generate returns. Climate strategies capitalize on the energy transition. Governance improvements reduce portfolio company risks. What started as LP demands became competitive advantages. TPG leads where others follow.

The geographic diversification provides optionality as growth shifts globally. When China slows, India accelerates. When Europe struggles, Southeast Asia thrives. When developed markets stagnate, emerging markets offer growth. TPG's global platform captures opportunities wherever they emerge, rather than depending on single markets.

Success in five years looks like $500 billion in AUM, driven by organic growth and strategic acquisitions. Multiple strategies generating predictable fees reduce dependence on carried interest volatility. Technology platforms that democratize access to alternatives while maintaining return profiles. Market leadership in impact and climate investing as these sectors mainstream. Stock prices that reflect the value of permanent capital and fee streams, not just current fund performance.

In ten years, TPG could be unrecognizable—a financial services platform beyond traditional private equity. Wealth management channels bringing alternatives to individual investors. Technology ventures disrupting financial services. Operating companies spun out from portfolio transformations. The firm that started buying distressed airlines could become a diversified financial institution rivaling traditional banks in influence if not structure.

The risks are real. A severe recession could trigger massive portfolio write-downs. Rising populism might restrict private equity through taxation or regulation. Competition could compress returns below acceptable levels. Key talent might leave for their own ventures. Cultural dilution could erode TPG's edge.

But TPG has survived and thrived through the S&L crisis, dot-com bust, financial crisis, and pandemic. Each crisis strengthened rather than weakened them. The firm's adaptability—from buyouts to impact, from three partners to global platform, from private partnership to public company—suggests resilience that transcends any single strategy or market environment.

The verdict on TPG's future depends on your timeframe. Short-term traders focusing on quarterly earnings might find better opportunities elsewhere. But long-term investors betting on alternative assets' continued growth, operational excellence's enduring value, and TPG's proven ability to evolve—they might see opportunity where others see only complexity.

Which brings us full circle to TPG's founding philosophy: complexity creates opportunity. The private equity industry faces enormous complexity—regulatory scrutiny, market volatility, competitive intensity, technological disruption. For most firms, this complexity threatens returns. For TPG, it might just be the next great opportunity. The contrarians from Texas have built their entire success on zagging when others zig. No reason to think they'll stop now.

XIII. Recent News

The drumbeat of TPG's recent activity reveals a firm in perpetual motion, executing across all platforms while navigating volatile markets. In October 2024, TPG made headlines with its strategic exit from Creative Artists Agency (CAA), selling its majority stake back to the talent agency in a management buyout that valued CAA at $7 billion. The deal, just two years after TPG's initial investment, demonstrated the firm's ability to create value quickly in creative industries—a sector many PE firms avoid due to its relationship-driven nature. The Angelo Gordon acquisition marked TPG's boldest strategic move since going public. On November 2, 2023, TPG announced the successful completion of its acquisition of Angelo Gordon in a cash and equity transaction valued at approximately $2.7 billion. The transaction also included an earnout based on Angelo Gordon's future financial performance, valued at up to $400 million. The deal instantly transformed TPG's scale—Angelo Gordon would operate as TPG Angelo Gordon, a $74 billion diversified credit and real estate investing platform within TPG, bringing TPG's total AUM across all platforms to $213 billion.

The strategic rationale was compelling. Founded in 1988, Angelo Gordon is a fully integrated and scaled multi-strategy platform with more than 650 employees across 12 offices in the U.S., Europe, and Asia. The acquisition addressed TPG's relative weakness in credit strategies while adding deep real estate expertise. Jon Winkelried called it "a milestone transaction for TPG, representing an important step in our continued evolution as a diversified global alternative asset manager"

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube