Toast: From Restaurant Crisis to Cloud Kitchen Conquest

I. Introduction & The Restaurant Technology Paradox

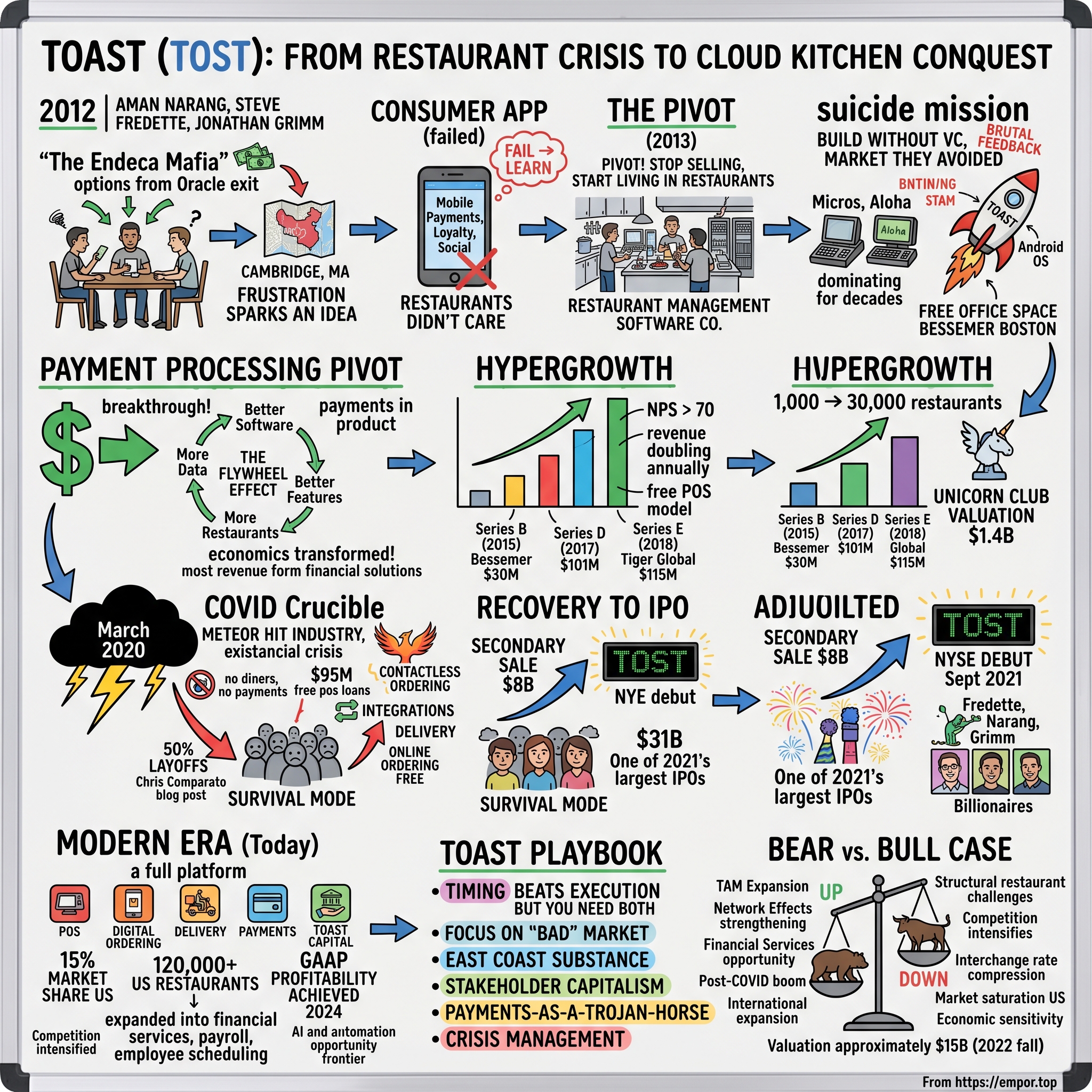

Picture this: It's 2012 in Cambridge, Massachusetts. Three engineers sit in a restaurant, waiting—and waiting—for their check. They've been tapping their fingers for fifteen minutes, watching their server juggle six other tables. One pulls out his iPhone, waves it mockingly at the others. "We can summon a car, trade stocks, and video-call Tokyo from this thing, but we can't pay for a burger?" That frustration would spark a company worth over $30 billion today.

The engineers—Aman Narang, Steve Fredette, and Jonathan Grimm—had just watched their previous employer, Endeca, sell to Oracle for over a billion dollars. They had options money burning holes in their pockets and the itch that afflicts every engineer after a big exit: the need to build something new. What they didn't have was any experience in restaurants. They'd never worked a shift, never calculated food costs, never dealt with the Sunday brunch rush.

Yet today, Toast, Inc. is an American cloud-based restaurant management software company based in Boston, Massachusetts. As of June 2024, Toast is used in approximately 120,000 US restaurants. The company's journey from a failed consumer app to a dominant force in restaurant technology poses a fascinating paradox: How did three engineers with zero restaurant experience build a company that today processes 0.5% of US GDP through their platform?

The answer lies not in Silicon Valley's typical playbook of blitzscaling and venture capital excess, but in something more fundamental: the willingness to embrace an industry everyone else avoided, the patience to understand problems before solving them, and the fortuitous timing that can turn near-death experiences into rocket fuel.

This is the story of Toast—a company that faced 50% layoffs during COVID, was rejected by nearly every West Coast VC, and still emerged as one of the most valuable restaurant technology companies in history. It's a tale of East Coast substance over West Coast hype, of turning payment processing into a Trojan horse for software domination, and of building stakeholder capitalism that actually works when tested by crisis.

Our journey spans from the Endeca mafia's formation in Cambridge to Toast's triumphant NYSE debut at a $31 billion valuation. We'll explore how they discovered that restaurants didn't need another app—they needed a complete reimagining of their operating system. We'll examine the economics that make "free" POS systems profitable, dissect their survival through the restaurant apocalypse of 2020, and analyze whether their dominance can continue against Square, Stripe, and a host of hungry competitors.

The roadmap ahead: We'll start with the origin story and the consumer app that failed spectacularly. Then we'll dive into the "suicide mission" years when they built without venture capital in a market VCs wouldn't touch. We'll unpack the payment processing pivot that changed everything, trace their hypergrowth from 1,000 to 100,000+ restaurants, and relive the COVID crucible that nearly killed them. Finally, we'll assess their current position, decode their playbook, and evaluate the investment case for what's next.

II. Origins: The Endeca Mafia & Finding Product-Market Fit

The story begins not in a garage or a dorm room, but in the gleaming offices of Endeca, a Boston-based enterprise search company that had just sold to Oracle for $1.1 billion in late 2011. Among the celebrating employees were three engineers who'd become close friends: Steve Fredette, Aman Narang, and Jonathan Grimm. They'd helped build Endeca's core technology, and now, with vested options turning into real money, they faced that peculiar post-exit question: What next? Steve Papa, Endeca's charismatic founder who'd built the company from startup to billion-dollar exit, wasn't ready to let his best people drift away. When the three engineers told him they were leaving to start something new—though they weren't quite sure what—Papa did something that would define Toast's trajectory. He called Kent Bennett, a junior associate at Bessemer Venture Partners who'd worked on the Endeca deal, and offered the trio free office space at Bessemer's Boston location until they figured out their next move.

"Steve Papa was so impressed by the trio when they worked for him that he invested $500,000"—and eventually a total of $10 million over time. "When you talk to Steve, he can sound a little crazy. He'll say things with such conviction like 'we're going to take this really really big hill'. And you'd be like 'does he really think we can take that hill? That seems really hard and really big'. He's serious and he's usually right. He taught me to set a high bar and think really big. Sometimes startups think too small and go after some small, niche thing that is just not a big enough idea. But it seems more doable. The big ideas seem the least doable and the most crazy. Toast was a big idea. We were going to go disrupt Micros, this $5B company".

The founders initially created exactly what you'd expect from three engineers in 2012: a consumer mobile app. The idea came during one of their many dinners together around Boston, waiting an annoyingly long time for their check. They wished they could just pay with their smartphones—there was their big idea. Toast's founders initially created a consumer app centered for mobile payments, customer loyalty, promotions, and social aspects that integrated with restaurants' existing POS systems.

They found their first guinea pig at Firebrand Saints, a Cambridge restaurant known for its burgers and large patio. The consumer app worked—technically. Customers could pay with their phones, earn loyalty points, share their experiences. But something was fundamentally broken. Restaurant owners didn't care about another app. They had bigger problems. The pivot moment came when the founders made a radical decision: stop selling to restaurants and start living in them. "In the early days, the reason we were able to build a platform that was differentiated for restaurants was because we lived and breathed restaurants," Aman said. They literally embedded themselves in restaurant operations, shadowing servers during the dinner rush, watching managers struggle with end-of-day reports at 2 AM, understanding why a kitchen display system failure could cost thousands in lost orders.

What they discovered was devastating for their consumer app dreams but enlightening for their future. The founders of Toast realized accepting mobile payments was a much smaller issue for restaurant owners. Also, it was tough for the developers to build an app on top of non-modular on-premise systems. Thus, they pivoted Toast to a restaurant management software company in 2013, starting with POS, payment processing, gift cards, loyalty, and kitchen display system bundled as one solution. This must be one of the most value-creating pivots in the history of the SaaS market!

The decision to build their own POS system seemed insane. Kent Bennett at Bessemer remembers the conversation: "We're gonna build our own POS," Steve said with a smile, like it was obvious. I felt like screaming. "The three of you are going to build a system to replace a forty-year old software stack with thousands of required features? A system that needs to work every minute of every day or else risk putting a restaurant out of business???" ... No. No I didn't. I gave them a 10% shot at a viable product and no chance at a go to market.

But the founders had an ace up their sleeve: Android. While competitors were building on Apple's closed iOS system or outdated Windows terminals, Toast chose Google's open-source Android technology. Leveraging Android, hidden in Apple's shadow at that time, was a stroke of genius that opened up a variety of cheaper hardware options and gave Toast control over the operating system. I thought it would take them years to build a working POS. They did it in months.

The founders' Endeca background proved crucial. This early focus on building feature sets can also be attributed to the background of its founders. All three of them came from Endeca that made enterprise-grade database management systems. Steve led Endeca's mobile web commerce platform, Aman was a product manager working at the intersection of the web and mobile commerce and Jonathan was a software solutions engineer.

By late 2013, they had their first pilot customer. By 2014, they were in dozens of restaurants. And here's where the story takes its most interesting turn: they still hadn't raised institutional venture capital. They raised a $500,000 seed round from their previous boss at Endeca, Steve Papa. Today, Steve's investment is worth billions. Papa's faith went beyond money—he became their coach, their connector, their champion when everyone else thought they were crazy.

III. The "Suicide Mission": Building in a Market VCs Wouldn't Touch

The venture capital community's response to Toast was unanimous: absolutely not. Venture capitalists wanted nothing to do with the restaurant industry, where margins are low and budgets notoriously tight. The feedback was brutal. Restaurants fail at astronomical rates. They operate on 3-5% margins. They're technologically backward. The incumbents—Oracle's Micros and NCR's Aloha—had dominated for decades. Why would anyone fund three engineers with no restaurant experience to compete in this graveyard of failed startups? The rejection stories became legendary. Papa said one Bay Area VC indicated interest in the pitch for Toast, but said he didn't want to get on a plane. Others were more direct: restaurants are a terrible market, you'll never make money, this is a suicide mission. The founders sprinkled in a healthy dose of naivete. Fredette said they were so inexperienced with fundraising and business in general that he and Narang, the chief operating officer, would often debate each other during investor meetings.

But Steve Papa wasn't deterred. "I said, 'guys it's not my space, but you helped me be successful, and I owe it to you,'" Papa, who was on the Toast board until recently, said in an interview after the IPO. "I was going to help them no matter what. In this case it meant capital to get them going." Beyond his initial $500,000, Papa would eventually invest $10 million of his own money, becoming Toast's sole institutional backer for years.

The East Coast location, initially seen as a liability, became a strategic advantage. "We used to talk about West Coast offense, which was hype over substance," Fredette said in an interview from the NYSE on Wednesday. "East Coast would be substance first and not enough hype." They could build without the pressure of Silicon Valley's growth-at-all-costs mentality. "We focused on the middle of the country, which was mostly overlooked," Papa said. "We intentionally chose not to put reps in Silicon Valley."

This geographic focus shaped their go-to-market strategy. Instead of chasing flashy partnerships or enterprise deals, Toast went restaurant by restaurant through flyover country. They'd show up in person, install the system themselves, and sit with staff through dinner rushes to ensure everything worked. No remote demos, no slick sales decks—just proof that the product worked when it mattered.

The bootstrapping years were brutal but formative. The founders set up operations in Narang's basement, where for nine months, his wife—a teacher—would wake up at 6 AM to the sound of engineers arguing about database architecture below. The company culture that emerged was scrappy, obsessive, and deeply technical. They hired other Endeca alumni who understood enterprise-grade systems and could build software that never went down.

By late 2014, the metrics were undeniable. Toast had deployed to thousands of restaurants. They had millions in recurring revenue. They'd grown to 170 employees—all without a dollar of venture capital beyond Papa's angel investments. The product was winning head-to-head against Square and even pulling customers away from Micros and Aloha.

Kent Bennett at Bessemer had been watching from the sidelines for 18 months, hosting monthly dinners with the founders, trying to convince them to take institutional money. In December 2015, he wrote in an internal memo: "We're very excited about this investment – for the past 18 months we've stood by anxiously as the team hit obvious product market fit but punted on raising more equity."

When Toast finally opened up for funding, the terms reflected their leverage: Bessemer recommended a $17.5M investment in the $24M first institutional round, with Google Ventures taking $5 million. The memo noted there were approximately 1 million addressable restaurants in the US, and with current ARR per location around $5,000 and upside with additional product features potentially approaching $10,000, they estimated the market size at $5 – 10 billion. This is large, but maybe not surprising relative to the $600B Americans spend at restaurants every year.

IV. The Payment Processing Pivot: Finding the Business Model

The breakthrough that changed everything happened over breakfast. Months after Bessemer's initial rejection, Aman Narang met Kent Bennett at a local diner. He was excited—unusually so. Toast had just done something that would have horrified any VC if they'd asked permission first: they'd become a payments company. In response to restaurant frustration that POS systems were often out of sync with payment systems (a longstanding issue, not a Toast-specific problem), the team had built payments into their product. If they had bothered to ask a VC first, they would have been told that this wasn't done—given the risk and complexity involved with payments and that they should just stick to software.

Thankfully they ignored conventional wisdom, and thankfully Bennett had the presence of mind to do the math. They were making real money on payments and the product experience was significantly improved. Toast had gone from being a great product with a mediocre business model, to an amazing product with an incredible business model.

The economics were transformative. Most of the revenue (~80%) Toast generates is from financial technology solutions, including customer transaction-based fees to facilitate their payment transactions. Instead of charging restaurants $500-1000 per month for software—a hard sell in an industry with razor-thin margins—they could offer the software at a much lower price and make money on every transaction that flowed through the system.

By 2012 when Toast launched, the payment facilitator (Payfac) model was flourishing and this allowed Toast to redefine the POS business model and literally alter the competitive playing field. By embedding payments into their software stack, they were given two levers for charging customers—SaaS licenses and payments interchange. Restaurants were going to pay someone interchange, but now Toast could give them their core software platform for running the restaurant while also monetizing the payments.

The "free POS" model emerged as their masterstroke. Toast would provide hardware worth thousands of dollars to restaurants at no upfront cost, then recoup the investment through payment processing fees over time. It's fair to assume half of those were "free POS" systems, whereby Toast wrote an estimated $10,000 per merchant on its own balance sheet. The economics worked because restaurants process enormous volumes—a busy restaurant might process $2-3 million annually, generating $60,000-90,000 in processing fees at typical rates.

But here's where Toast got clever: they didn't just become another payment processor. They used the payment data to build better software features. They could show restaurants their busiest hours, most profitable items, server performance metrics—all derived from transaction data that competitors couldn't access. The flywheel effect was powerful: better software drove more payment volume, which generated more data, which enabled better features, which attracted more restaurants.

The competitive moat this created was nearly insurmountable. Legacy POS providers like Micros and NCR couldn't easily become payment processors—it would cannibalize their software revenues. Pure payment companies like Square lacked the deep restaurant-specific features. And new software entrants couldn't match Toast's economics because they didn't have the payment revenue to subsidize hardware and customer acquisition costs.

A bonus of vertical payments in the restaurant industry is the low-risk profile. Compared to a marketplace like Etsy or Stripe's broad customer base, restaurants are relatively easy to KYC, chargeback risk is low and transaction monitoring is more predictable. This meant Toast could capture most of the payment margin without taking on excessive risk.

V. Hypergrowth & The Race to IPO (2015-2021)

When Bessemer finally wrote their $30 million Series B check in 2015—leading with $17.5 million alongside Google Ventures' $5 million—they weren't buying into a startup anymore. By the time Bessemer Venture Partners led the first institutional round in 2015, the company had millions in revenue, 170 employees and was deployed in thousands of restaurants. The investment memo captured the moment perfectly: "We're very excited about this investment – for the past 18 months we've stood by anxiously as the team hit obvious product market fit but punted on raising more equity"

The valuation—about $100 million—would look quaint within months. Toast was about to enter a phase of hypergrowth that would make even West Coast VCs take notice.

The scaling from 1,000 to 30,000 restaurants between 2015 and 2019 wasn't just growth—it was a land grab. Toast had discovered something crucial: restaurants talk to each other. Get one popular spot in a neighborhood, and three more would call within weeks. Win over a respected chef, and their entire network would follow. The company's net promoter score consistently exceeded 70, astronomical for enterprise software.

The funding rounds came fast and furious. Series C in July 2016: $30 million from Bessemer and Google. Series D in May 2017: $101 million led by Generation Investment Management. Each round brought new believers who'd finally done the math—Toast wasn't selling software to restaurants; they were becoming the financial rails of a $900 billion industry.

The Series E in July 2018 marked a turning point: $115 million led by T. Rowe Price and Tiger Global at a $1.4 billion valuation. Toast had officially joined the unicorn club. But more importantly, they'd proven the model could scale. Revenue was doubling annually. The take rate on payments was holding steady despite competition. And the "free POS" model was working—restaurants that started with free hardware were generating positive unit economics within 18-24 months.

During the course of 2019, revenue increased 109 percent as tens of thousands of new restaurants joined the Toast community. The company was burning cash to fuel growth, but the metrics justified it. Gross payment volume was approaching $20 billion annually. The platform was processing millions of orders per day. And they were still only in 2% of US restaurants.

The Series F in February 2020 would go down as one of the most fortuitously timed rounds in startup history. Toast announced a $400M Series F funding round led by Bessemer Venture Partners, TPG, Greenoaks Capital, and Tiger Global Management with participation from Durable Capital Partners LP, TCV, funds and accounts advised by T. Rowe Price Associates, G Squared, Light Street Capital, Alta Park Capital, and others. The valuation: $4.9 billion.

The timing was everything. Think about it: not only was the "free POS" business model impossible at any other time in American history, but Toast closed a $400M round of funding right before it would have been impossible to raise capital. In fact if Toast hadn't closed that $400M in all likelihood they would be declaring bankruptcy in 2020 from the bad debt on their "free POS" loans.

Two weeks later, the world shut down.

VI. The COVID Crucible: 50% Layoffs to Survival

March 2020 hit the restaurant industry like a meteor. "During the month of March, as a result of necessary social distancing and government-mandated closures, restaurant sales declined by 80 percent in most cities," CEO Chris Comparato wrote in a blog post. "This is a massive disruption that hit the industry virtually overnight. Many restaurants that have temporarily closed may never reopen."

For Toast, the crisis was existential. Their entire business model depended on transaction volume. No diners meant no payments meant no revenue. Worse, they had $95 million in "free POS" loans on their balance sheet—hardware they'd given to restaurants that might never reopen to pay them back.

The leadership team faced an impossible decision. They could ride it out, burn through their fresh $400 million, and hope restaurants recovered before the money ran out. Or they could cut deep, preserve capital, and position for survival. On April 8, 2020, they chose survival. Toast reduced the size of its staff by 50% through layoffs and furloughs, according to a blog post from Toast's CEO, Chris Comparato.

When it was clear Covid represented a massive risk to the business, Chris and the team did a tough thing; they reduced the size of the company by 50%. Professionally this was tough because it required scuttling promising projects and doing more with less. Personally, it was devastating. Toast had always been a tightly knit organization. Toast's deep reduction in force meant asking incredible, valued colleagues and friends to leave in the face of a pandemic.

But Toast didn't just cut and hide. They pivoted with remarkable speed to help their customers survive. Within weeks, they'd launched contactless ordering and payment features. They integrated with every major delivery platform. They built curbside pickup workflows. They made their online ordering system free for restaurants struggling to stay alive.

The company also became an unexpected advocate for the industry. Toast stepped it up even further by taking a leadership role in advocating for the restaurant industry by writing letters to Congress, actively lobbying to help secure this funding for the restaurant industry, and partnering with groups like the Independent Restaurant Coalition to support restaurateurs and their employees. Toast backed its action by donating capital to fund restaurant recovery efforts. More recently, Toast partnered with the U.S. Small Business Administration to support its customers with a simplified application process to access restaurant revitalization funds.

During the tumult of the pandemic and shifting operational requirements, Toast's suite of products and services proved vital. The e-commerce tools allowed Toast restaurants to diversify quickly into curbside pick up and delivery, order and pay at the table allowed restaurants to serve customers in a no-contact manner that was safer for customers and servers.

The recovery, when it came, was swift and shocking. By late summer 2020, restaurants that survived were seeing unprecedented demand. Suburban locations were packed. Delivery and takeout had gone from 10% of sales to 30%+. And every restaurant that reopened needed technology more than ever. Toast's payment volume began recovering, then surging past pre-pandemic levels.

VII. The Phoenix Rises: Recovery to IPO

The secondary market told the story before anyone else. In November 2020, Toast had a secondary sale that valued the company at around $8 billion, despite laying off half of its employees in April. Investors who'd watched Toast cut to the bone, then rapidly rebuild as restaurants recovered, saw something remarkable: a company that could manage through crisis while maintaining customer loyalty.

The restaurant industry's recovery was uneven but undeniable. Those that survived emerged different—more digital, more efficient, more dependent on technology. Toast's platform had evolved from nice-to-have to mission-critical. Restaurants that had resisted digital ordering for years were now doing 40% of sales through Toast's online channels. QR code menus, once a novelty, became standard. The pandemic had accelerated restaurant digitization by a decade.

Inside Toast, the mood had shifted from survival to opportunity. They'd rehired many of the laid-off employees and were adding hundreds more. The product roadmap, paused during the crisis, roared back to life. They launched Toast Capital to provide loans to cash-strapped restaurants. They built labor management tools as restaurants struggled with staffing. They deepened integrations with DoorDash, Uber Eats, and the delivery ecosystem that now dominated the industry.

The IPO decision came down to timing and necessity. The public markets were hot, valuations were soaring, and Toast needed capital to fund its aggressive growth plans. But more importantly, going public would give them currency for acquisitions and credibility with enterprise customers who still questioned whether a Boston startup could compete with Oracle and NCR long-term.

On September 22, 2021, Toast went public with an initial public offering under the stock symbol TOST. The company offered shares at $40 initially, with a market capitalization of roughly $20 billion, making it one of 2021's largest American IPOs. The first day's trading was electric. The three guys and some office space eventually became Toast, a provider of software and hardware to restaurants that held its New York Stock Exchange debut on Wednesday, closing the day with a market cap of over $31 billion.

The three co-founders — Steve Fredette, Aman Narang and Jonathan Grimm — are billionaires, and remain top executives at the company. Steve Papa, who'd invested $10 million when everyone else passed, saw his stake worth over $2 billion. Kent Bennett at Bessemer, who'd waited 18 months to invest, had delivered one of the firm's best returns ever.

But the public market debut was just the beginning of a new chapter. Within months, the stock would face the reality of rising interest rates, questions about profitability, and the challenge of maintaining hypergrowth at scale. The honeymoon was short-lived—by 2022, the stock had fallen 80% from its highs as investors rotated out of unprofitable tech companies.

VIII. Modern Era: Platform Expansion & Market Dominance

Today's Toast is a dramatically different company than the one that went public in 2021. With a 15% market share in the U.S. restaurant market and a record 28,000 net locations added in 2024, Toast achieved its first full year of GAAP profitability with a 34% increase in recurring gross profit streams. The transformation from growth-at-all-costs to profitable growth required painful adjustments but validated the underlying business model.

Toast's product suite includes integrated POS systems, digital ordering and delivery solutions, kitchen display systems, contactless payments, and comprehensive restaurant management software. The company serves restaurants of all sizes, from small independent establishments to large enterprise chains across the United States. The platform processes over $100 billion in gross payment volume annually, making it one of the largest payment processors in the restaurant vertical.

The expansion into financial services has been particularly successful. Toast Capital, launched during the pandemic, now originates hundreds of millions in loans annually. The company can underwrite based on real transaction data, offering better rates than traditional lenders while maintaining lower default rates. They've added payroll processing, employee scheduling, and benefits management—each deepening the platform's stickiness while adding high-margin revenue streams.

Competition has intensified from every direction. Square, bolstered by Block's resources, continues to attack from below with simpler, cheaper solutions for small restaurants. Clover, backed by Fiserv, leverages banking relationships to bundle services. New entrants like SpotOn and Lightspeed compete aggressively on price. And the legacy players—Oracle's Micros and NCR's Aloha—still dominate enterprise chains that Toast struggles to crack.

The international opportunity remains largely untapped. Toast has made tentative moves into Canada and the UK, but the complexities of local payment systems, regulations, and restaurant operations have slowed expansion. The company faces a classic dilemma: chase growth internationally while still having runway in the US, or dominate domestically before expanding abroad.

The AI and automation frontier represents both opportunity and threat. Toast has integrated AI for demand forecasting, inventory management, and dynamic pricing. But the real revolution—autonomous ordering, robotic food preparation, fully automated restaurants—could disrupt Toast's human-centered model. The company must balance supporting today's restaurants while preparing for tomorrow's.

IX. Playbook: Lessons from Toast's Journey

The Toast playbook offers contrarian lessons for building in overlooked markets. First, timing beats execution, but you need both. Toast succeeded not just because they built great software, but because they arrived at the exact moment when cloud computing, mobile devices, and payment facilitation converged to make their model possible. A decade earlier, the technology didn't exist. A decade later, the market would be too crowded.

The power of focusing on a "bad" market everyone else ignores cannot be overstated. VCs avoided restaurants for good reasons—low margins, high failure rates, technological resistance. But these same factors created a moat once Toast figured out the model. Competitors couldn't easily enter because the market was genuinely difficult. Customers, once won, rarely switched because changing restaurant systems is painful.

Building in Boston provided unexpected advantages. The East Coast location meant less venture capital pressure, lower burn rates, and access to enterprise software talent from companies like Endeca, HubSpot, and Wayfair. The distance from Silicon Valley forced discipline—they couldn't raise money on hype alone, so they built a real business. Fredette's comment about "East Coast substance" wasn't just regional pride; it was a strategic advantage.

The stakeholder capitalism model, led by CEO Chris Comparato and Co-Founders Aman Narang and Steve Fredette, proved its worth during crisis. It's easy to espouse feel-good ideas in good times, but to stand by your principles during times of strife shows true conviction. The 50% workforce reduction was brutal, but the transparency, severance packages, and commitment to rehiring showed genuine care for employees. The advocacy for restaurant relief and free software during COVID built customer loyalty that pure capitalism couldn't buy.

The payments-as-a-Trojan-horse strategy revolutionized software economics. By monetizing transactions rather than subscriptions, Toast aligned their success with their customers' success. Restaurants didn't feel like they were paying for software—they were sharing revenue with a partner. This psychological shift from cost center to revenue share transformed how restaurants viewed technology investment.

Crisis management at Toast offers a masterclass in cutting deep while preserving optionality. The 50% reduction seemed draconian, but it ensured survival. More importantly, they cut in a way that allowed rapid rebuilding—furloughs rather than just layoffs, maintaining core engineering talent, keeping customer success teams intact. When recovery came, they could scale back up quickly.

Finally, Toast proved that restaurants are actually a great market if you solve the right problem. The issue wasn't that restaurants don't spend on technology—they spend billions on POS systems, payment processing, marketing, and operations. The problem was that previous solutions treated restaurants as generic retail. Toast's obsessive focus on restaurant-specific workflows, from table management to kitchen display systems, created products that felt built by restaurant people for restaurant people.

X. Bear vs. Bull Case & Investment Analysis

Bull Case: The optimistic view starts with TAM expansion. Despite Toast's growth, they're still only in 15% of US restaurants. The digital transformation of restaurants remains early—most still operate on legacy systems or basic Square readers. As minimum wage increases and labor shortages persist, restaurants must adopt technology to survive. Toast's comprehensive platform becomes not optional but essential.

Network effects are strengthening. Every restaurant added makes the platform more valuable for suppliers, delivery services, and financial providers. The data advantage compounds—Toast now has visibility into dining trends, menu performance, and operational metrics that no competitor can match. This data moat enables better products, smarter underwriting, and predictive features that lock in customers.

The financial services opportunity could dwarf the current business. Restaurants need working capital, equipment financing, and employee financial services. Toast Capital is nascent—they could build a full-stack financial services business worth tens of billions alone. Add insurance, benefits management, and supplier financing, and the TAM expands dramatically.

Post-COVID restaurant formation has boomed. New restaurant applications are up 40% from pre-pandemic levels. These digital-native operators choose Toast from day one, avoiding legacy systems entirely. The installed base of old technology is finally aging out, creating a replacement cycle that could drive growth for years.

International expansion remains untapped. The US represents less than 20% of global restaurant spending. Toast's proven model could work in any developed market. Success in the UK or Canada could validate the platform for global expansion, multiplying the addressable market.

Bear Case: The skeptical view starts with structural restaurant industry challenges. Restaurants fail at extraordinary rates—60% close within three years. Rising labor costs, food inflation, and delivery platform fees squeeze already thin margins. If restaurants can't survive, neither can Toast's model. The next recession could trigger a wave of closures that would devastate Toast's economics.

Competition from well-funded players intensifies daily. Square has Block's balance sheet and consumer ecosystem. Stripe's platform approach could extend into vertical solutions. Amazon has explored restaurant technology. These tech giants have resources Toast can't match and could subsidize losses to gain share.

Dependence on payment processing economics creates vulnerability. Interchange rates could compress through regulation or competition. Restaurant payments are increasingly digital, where margins are lower than card-present transactions. If payment economics deteriorate, the entire business model unravels.

Market saturation in the core US market looms. Toast has picked the low-hanging fruit—tech-forward independent restaurants in major markets. The remaining targets are harder to win: enterprise chains require customization, rural restaurants lack volume, and ethnic restaurants often prefer specialized solutions. Growth becomes increasingly expensive as the easy wins disappear.

Economic sensitivity makes Toast a dangerous recession play. Restaurant spending is highly cyclical. In downturns, consumers eat out less, restaurants fail more, and survivors cut costs aggressively. Toast's high operational leverage means revenue declines flow directly to the bottom line. The COVID recovery masked this cyclicality, but the next recession will test the model's durability.

Valuation & Metrics: Current trading multiples reflect these tensions. At today's market cap of approximately $15 billion (down from the $31 billion IPO peak), Toast trades at roughly 3x forward revenues—expensive for a payment processor but cheap for a vertical SaaS company. The company's take rate has remained stable at roughly 3% of gross payment volume, impressive given competitive pressure.

Customer acquisition costs and payback periods have improved with scale. The "free POS" model requires roughly $10,000 upfront investment per location, recovered through payment processing within 24 months. With 120,000 locations and growing, the unit economics clearly work. But the capital intensity limits how fast Toast can grow without dilution or debt.

The competitive moats—switching costs, data advantages, and ecosystem lock-in—appear durable but not impregnable. Restaurants hate changing POS systems, but they will for significant savings. The question becomes whether Toast can maintain premium pricing as the market matures.

XI. Recent News**

Latest quarterly earnings and guidance:** Toast reports strong Q3 results with $56M net income, 28% location growth to 127,000, and $1.6B ARR. Adjusted EBITDA triples YoY to $113M as fintech solutions expand. The third quarter 2024 results demonstrated Toast's continued momentum. CEO and Co-Founder Aman Narang noted, "this fall we launched new products like Branded Mobile App and SMS Marketing alongside over a dozen feature updates. Today we proudly serve nearly 127,000 locations, and we're just getting started."

Key financial metrics reveal a 24% year-over-year increase in Gross Payment Volume (GPV) to $41.7 billion. The company added approximately 7,000 net locations in Q3, increasing total locations to nearly 127,000, up 28% year over year. SaaS ARR grew 33% year over year, driven by strong location growth and a 4% increase in SaaS ARPU on an ARR basis.

Product launches and partnerships: Toast's innovation engine has accelerated significantly in 2024. In May 2025, Toast introduced ToastIQ, an intelligence engine delivering timely prompts, personalized recommendations, and automated workflows designed to transform daily restaurant operations. Built natively into Toast's end-to-end platform, ToastIQ draws on insights from millions of transactions and interactions across 130,000+ locations.

Toast announced its Fall Product Release with new mobile features designed to help restaurants unlock new revenue streams, boost their brand presence, and deepen the connection to their guests. Highlights include a Branded Mobile App and SMS Marketing to drive diner engagement on mobile devices.

Another highlight for Toast is Sous Chef, launched in 2024. This AI-driven tool provides restaurant managers actionable insights to boost sales. Inspired by the kitchen's second-in-command, it streamlines communication, staff coordination and menu management while delivering data-driven recommendations and automation.

M&A activity: In February 2023, it was announced that Toast had acquired Delphi Display Systems, a Costa Mesa-headquartered producer of digital display solutions and drive-thru technology for quick-service restaurants (QSRs). This acquisition strengthened Toast's position in the quick-service segment and added critical drive-thru capabilities.

Executive changes: Toast announced the appointment of Aman Narang as CEO, effective January 1, 2024. Narang has served as Toast's Co-President since December 2012 and Chief Operating Officer since June 2021. He will take over as CEO from Chris Comparato, who has served as the company's CEO since February 2015, leading Toast through a remarkable period of growth with a focus on profitability and operational excellence. Both Comparato and Narang will remain on the Board.

Effective January 1, 2024, Mark Hawkins became Chair of the Toast Board of Directors. This leadership transition marked a return to founder-led management, with Narang bringing deep operational knowledge and continuity to the role.

Market share updates: According to Toast's third Voice of the Restaurant Industry Survey, 28% of restaurant owners surveyed hope to open a new location over the next 12 months. This expansion mindset among restaurant operators bodes well for Toast's continued growth trajectory. The company continues to gain share in both SMB and enterprise segments, with recent wins including major chains transitioning from legacy systems.

XII. Conclusion: The Toast Paradox Resolved

Toast's journey from three engineers frustrated by a slow check to a $15 billion public company processing over $100 billion in payments annually represents more than a business success story—it's a masterclass in contrarian thinking, perfect timing, and stakeholder capitalism that actually works.

The central paradox we posed at the beginning—how did engineers with no restaurant experience build one of the most valuable restaurant technology companies in history—resolves into several key insights. First, their outsider perspective allowed them to see problems insiders had accepted as immutable. Second, their engineering background from Endeca gave them the technical sophistication to build enterprise-grade systems that never fail. Third, and perhaps most importantly, they had the humility to live in restaurants, learn from operators, and build what the industry actually needed rather than what they initially imagined.

The East Coast advantage proved real. By building outside Silicon Valley's hype machine, Toast could focus on substance over story, unit economics over user growth, and profitability over publicity. The company's ability to bootstrap to millions in revenue before taking institutional capital created a discipline that persisted even through hypergrowth. When COVID threatened to destroy everything, that discipline—combined with genuine care for stakeholders—enabled them to cut deep enough to survive while maintaining the capability to roar back.

The payment processing pivot transformed everything. What started as a software company became a fintech company disguised as a software company. This wasn't just about revenue diversification—it fundamentally aligned Toast's incentives with their customers' success. When restaurants process more payments, Toast makes more money. This symbiotic relationship created a moat that pure software or pure payment companies struggle to replicate.

Looking forward, Toast faces both enormous opportunity and significant challenges. The company has proven it can dominate the SMB and mid-market segments, but enterprise chains remain elusive. International expansion offers massive TAM expansion but requires localization that goes beyond language to fundamental differences in how restaurants operate globally. The rise of AI and automation could either strengthen Toast's position as the operating system for restaurants or disrupt the human-centered model they've perfected.

The competitive landscape continues to intensify. Square's simplicity appeals to smaller operators, while Oracle and NCR's entrenchment in enterprises creates switching barriers Toast hasn't fully overcome. New entrants backed by venture capital attack niche segments with focused solutions. Yet Toast's integrated platform, with its flywheel of software driving payments driving more software, creates compounding advantages that are difficult to replicate.

The investment case ultimately comes down to a bet on restaurants themselves. If you believe restaurants will continue to digitize, that independent operators will professionalize, and that the dining experience will evolve but endure, then Toast's position as the operating system for this transformation makes it compelling. If you fear that economic headwinds, changing consumer behavior, or new dining models will fundamentally disrupt the restaurant industry, then Toast's concentration in this vertical represents existential risk.

What Toast has definitively proven is that "bad" markets can be great businesses if you solve real problems with excellent execution. They've shown that stakeholder capitalism isn't just rhetoric—it's a competitive advantage when crisis tests your values. They've demonstrated that the best pivots come not from brainstorming sessions but from listening to customers. And they've validated that sometimes, the best place to build a technology company isn't in technology's epicenter but where your customers actually are.

The three engineers who couldn't get their check fast enough didn't just build a payment system or a POS platform. They built the technology infrastructure for an industry that feeds America, employs millions, and creates the gathering places where life's moments happen. In solving their small frustration, they addressed a massive market failure. In focusing on substance over hype, they created lasting value over fleeting valuations. And in choosing the hardest market that everyone else avoided, they found the opportunity of a lifetime.

Toast's story isn't finished. With Aman Narang now at the helm, the company enters its next chapter with founder-led focus, proven resilience, and the ambition to serve not just 127,000 locations but multiples of that number globally. Whether they achieve that vision will depend on their ability to maintain the discipline that got them here while embracing the innovation required to get there. But if their history is any guide, betting against the company everyone said couldn't succeed has rarely been profitable.

The restaurant industry will continue to evolve, technology will continue to advance, and competition will continue to intensify. But Toast has proven something fundamental: when you truly understand your customers, build products they actually need, and align your success with theirs, you don't just capture value—you create it. That's the real lesson of Toast, and it's one that transcends restaurants, technology, or any single industry. It's a reminder that the best businesses aren't built on clever financial engineering or aggressive growth hacking, but on solving real problems for real people in ways that make everyone better off.

XII. Links & Resources

SEC Filings and Investor Presentations: - Toast Investor Relations: investors.toasttab.com - Latest 10-K Annual Report (2023) - Quarterly 10-Q Filings - S-1 IPO Registration Statement (2021) - Investor Day Presentations (2024) - Proxy Statements (DEF 14A)

Industry Research Reports: - National Restaurant Association Industry Reports - Restaurant Industry Navigator (Credit Suisse) - William Blair Restaurant Technology Reports - Bessemer Venture Partners SaaS Reports - McKinsey on Restaurant Digital Transformation

Founder Interviews and Podcasts: - How I Built This with Guy Raz featuring Toast founders - SaaStr Podcast with Aman Narang - Boston Business Journal interviews - TechCrunch Disrupt presentations - Fortune Brainstorm Tech appearances

Restaurant Industry Analysis: - QSR Magazine Technology Reports - Nation's Restaurant News coverage - Restaurant Business Magazine profiles - FSR Magazine industry analysis - Modern Restaurant Management insights

Technology Deep Dives: - Toast Engineering Blog - Android POS Implementation Case Studies - Payment Processing Technical Documentation - API Documentation and Developer Resources - Toast Product Release Notes

Historical Funding Documents: - Crunchbase Funding History - PitchBook Toast Profile - Bessemer Investment Memos (when available) - SEC Form D Filings - Secondary Market Transaction Reports

Customer Case Studies: - Toast Customer Success Stories - Restaurant Recovery Case Studies (COVID-19) - Enterprise Implementation Studies - ROI Analyses and White Papers - Toast Community Forum Discussions

Competitive Analysis Resources: - Square Seller Community comparisons - G2 Crowd POS Software Reviews - Capterra Restaurant POS Rankings - Software Advice Buyer's Guides - Industry Analyst Reports (Gartner, Forrester)

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube