Topicus.com Inc. (TOI.V): The European Maverick of Vertical Software

I. Introduction & Episode Roadmap

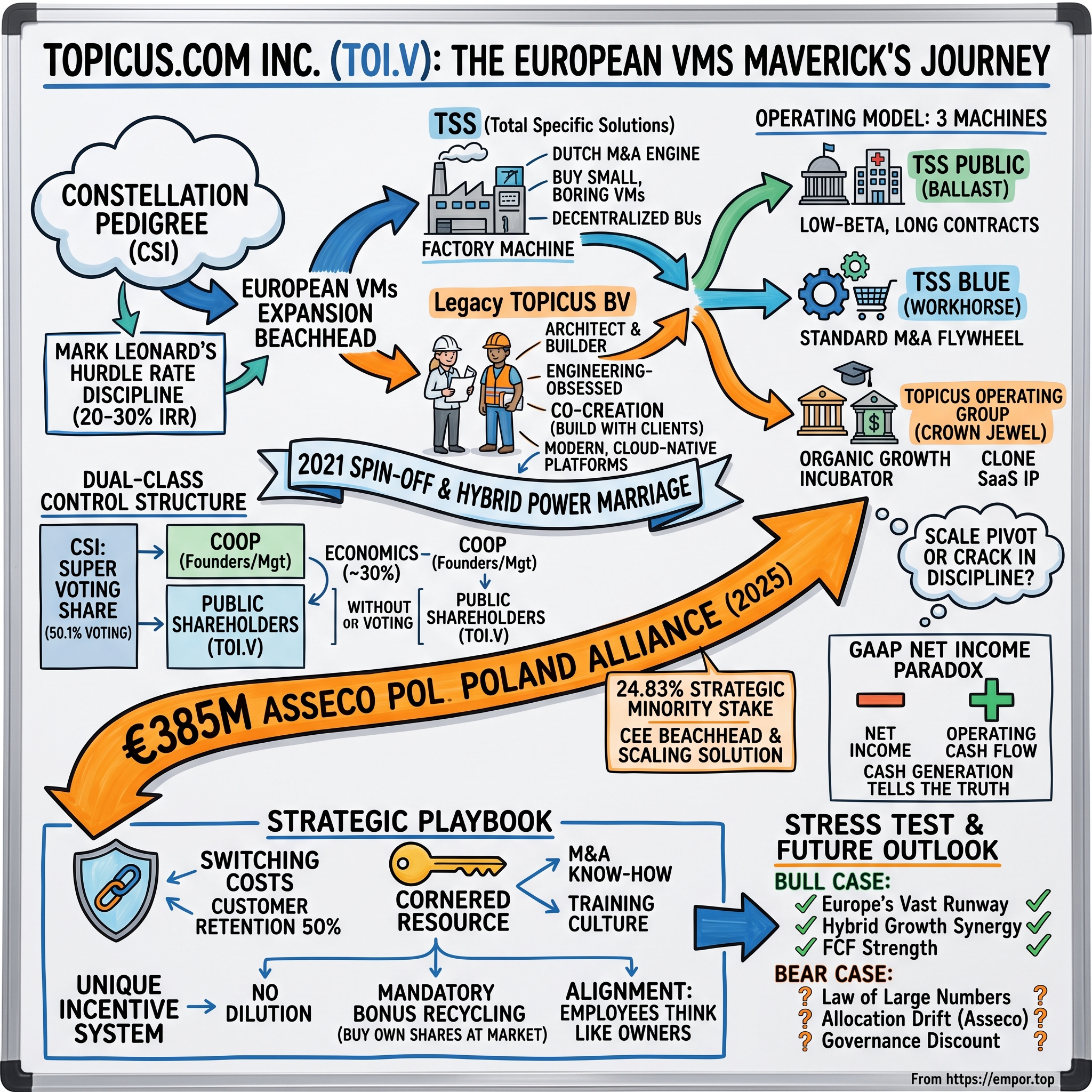

Picture a boardroom in Toronto in late 2020. Mark Leonard, the famously reclusive founder of Constellation Software, is not a man who gives things away. For two decades he had compounded shareholder capital at a rate that turned a modest Canadian software roll-up into one of the best-performing stocks on the planet, and he had done it by hoarding cash-generating businesses the way a dragon hoards gold. And yet here he was, engineering a maneuver to hand one of Constellation's most promising assets — its entire European platform — over to shareholders as a dividend, wrapped inside a newly minted public company listed not on the senior Toronto exchange, but on the junior TSX Venture Exchange.

Why would the most disciplined capital allocator in software voluntarily spin off a crown jewel? That question sits at the heart of the Topicus.com story.

The answer, it turned out, was a bet on hybridization. Topicus.com Inc. — ticker TOI.V, traded on the TSX Venture Exchange (TSXV) — was assembled from two organizations with almost opposite personalities. On one side was Total Specific Solutions (TSS), a Dutch acquisition machine that had absorbed the Constellation playbook and learned to buy small, boring, mission-critical software companies across Europe at disciplined prices. On the other was the legacy Topicus.com BV, an engineering-obsessed Deventer software house that built complex platforms from scratch alongside its customers and actually grew them organically — the one thing traditional software roll-ups almost never do. Bolt the M&A engine to the organic-growth incubator, keep Constellation's iron capital discipline bolted on top, and you get something genuinely unusual: a compounder that can both buy cheaply and build well.

This is the story of how that experiment has played out. Over the next sections we will trace the Constellation pedigree and why Europe became such fertile ground for vertical market software; the twin origin myths of TSS and legacy Topicus; the financial engineering of the January 2021 spin-off with its baroque dual-class control structure; and the €384.9 million Asseco Poland alliance of 2025 — a move so far outside the company's usual playbook that it forces a hard question about whether size is starting to bend the discipline that made the machine work.1 We will dissect the operating model, the legendary "buy shares with your own bonus" incentive system, and then subject the whole thing to a skeptic's stress test using Porter's Five Forces and Hamilton Helmer's 7 Powers.

Throughout, the posture here is that of an independent analyst, not a cheerleader. Management's claims are treated as claims until the evidence — organic growth rates, cash conversion, capital deployment, retention — backs them up. Let's begin where every Topicus conversation eventually must: with the parent.

II. The Constellation Pedigree: The Genesis of European Expansion

To understand Topicus, you first have to understand the strange gravitational body it orbits. Mark Leonard founded Constellation Software in 1995 with roughly $25 million of venture capital and a thesis that almost nobody in technology found interesting: that the least glamorous corner of the software world — small companies making specialized software for narrow industries — was actually the best business model ever invented, if you bought it at the right price and never sold.

Leonard's genius was less technological than organizational and financial. Rather than build a monolith, he built a federation. Constellation acquired vertical market software (VMS) companies and left them almost entirely alone, organizing them into decentralized operating groups run by managers treated as entrepreneurs rather than cogs. The corporate center did two things obsessively well: it allocated capital, and it taught its managers how to allocate capital. Everything else was pushed down to the business-unit level, where the people closest to the customer made the decisions.

The Hurdle Rate as Religion

The mechanism that made this work was the hurdle rate. Constellation historically demanded internal rates of return in the range of roughly 20% to 30% on acquisitions, with larger deals requiring more conviction than smaller ones. What made the discipline remarkable was not the number itself but the refusal to lower it, even when cash piled up and there was pressure to deploy. Leonard argued in his famous shareholder letters that a high hurdle rate has a "magnetic" quality: hold it firm, and over time you attract a pipeline of thousands of small deals that clear it, rather than talking yourself into a handful of large ones that don't. The moment you lower the bar to spend money, you begin destroying the very thing that made you great.

That discipline generated a problem most companies would kill for: too much cash. By the early 2010s Constellation was generating free cash faster than it could deploy at its hurdle rate inside North America, where competition for VMS assets from private equity was intensifying. The company needed a bigger sandbox.

Why Europe

Europe was that sandbox, and it was almost tailor-made for the Constellation model. The reason comes down to fragmentation — the kind Silicon Valley cannot easily steamroll. A medical scheduling suite used by German clinics has to comply with the health regulations of individual German states and operate in German; it cannot be swapped out for a generic American cloud product. Municipal waste-management software in the Netherlands, maritime logistics systems in Scandinavia, pharmacy dispensing platforms, mortgage-advisory tools tuned to Dutch cooperative banking law — each of these is a tiny local monopoly, defended by language, regulation, and the sheer unattractiveness of the niche to a venture capitalist chasing the next horizontal SaaS unicorn.

In other words, Europe offered hundreds of small, defensible, cash-generative software businesses that no one else particularly wanted to buy. For a disciplined acquirer with patient capital, this was paradise.

The Beachhead

Constellation planted its flag in December 2013, agreeing to acquire Total Specific Solutions (TSS) B.V. of the Netherlands — its first major platform acquisition outside North America. The deal closed at year-end 2013 for aggregate cash consideration of roughly €240 million (about US$342 million), a price that worked out to around 2.65 times TSS's forecast net maintenance revenues.3 At the time TSS employed about 1,400 people and had generated roughly €174 million of revenue in 2012, serving general-practitioner, pharmacy, long-term-care, mental-care, property-tax, and civil-affairs markets — a portfolio of exactly the boring, embedded niches Leonard loved.3

The price signalled the discipline. Constellation was not paying frothy growth-software multiples; it was buying durable maintenance revenue at a modest multiple and betting it could compound the platform for decades. What Constellation acquired that day was not just a company but a beachhead — and, crucially, a management team that had independently discovered a version of the same playbook. To understand why that mattered, we have to rewind to how TSS was built.

III. Total Specific Solutions (TSS): Building the European M&A Flywheel

The TSS story does not begin in a garage or a dorm room. It begins in a Frisian family office trying to figure out what to do with a fortune.

Rinse Strikwerda was a Dutch IT entrepreneur who had founded a staffing business, Detach, back in 1984 and floated its successor on the Amsterdam exchange in 1998.7 Cash in hand and looking for the next act, he asked his daughter Tjitske and her husband, a sharp operator named Robin van Poelje, to build a family office that could put the capital to work with structure and patience. Starting around 2006, they zeroed in on a specific idea: acquire and nurture small software companies serving specific end markets, share best practices among them, and reinvest their cash flows to buy more. The vehicle that grew out of this effort became Total Specific Solutions.7

If that description sounds familiar, it should — it is essentially the Constellation model, arrived at independently on the other side of the Atlantic. Which is precisely why the 2013 acquisition was less a takeover than a meeting of minds.

The Operational Transformation

The man who carried the model forward was Robin van Poelje, who had run TSS as CEO from 2010 and stayed on after the Constellation acquisition, eventually becoming Chairman and CEO of Topicus.com Inc. in 2021.8 Under his leadership, TSS absorbed what insiders call "the Constellation Way" and industrialized it across Europe.

In practice that meant taking large, sluggish corporate divisions and breaking them into tiny, autonomous business units, each small enough that a manager could run it like an owner-entrepreneur and be held accountable for its returns. It meant embedding a rigorous capital-allocation vocabulary in which the single source of truth was cash available to shareholders, not accounting earnings. And it meant relentless, high-volume, small-ticket dealmaking: dozens of acquisitions of €1 million–€20 million software businesses, each too small to attract private-equity attention, each accretive if bought below the hurdle.

The analytical point worth pausing on is that this is a fundamentally different skill from building software. It is a repeatable process — sourcing, valuing, negotiating, and integrating small VMS companies — and processes, unlike products, scale with people and training rather than with code. That is what made TSS an engine.

The Limitation Nobody Could Engineer Away

But the engine had a flaw, and it is the flaw that haunts every pure roll-up. The businesses TSS bought were mature, often decades-old software suites with sticky customers but almost no organic growth. Left alone, this kind of legacy VMS typically grows revenue somewhere between flat and low-single-digits, as annual price increases and a trickle of new customers barely offset the slow decay of clients who churn or get acquired. TSS was superb at buying cash flows cheaply; it was not, by itself, a machine for making those cash flows grow.

Over 2013 to 2020, TSS proved the acquisition model could scale across Europe's fragmented map without breaking capital discipline — a genuinely valuable proof of concept. But it also revealed the ceiling. You can compound a roll-up through reinvestment for a long time, but if the underlying assets never grow, the whole edifice depends on an endless supply of cheap deals. Constellation and van Poelje both understood that the truly rare combination — the thing that would let this platform compound for decades rather than years — was to fuse the acquisition engine with a business that actually knew how to grow software organically. And such a business existed, ninety minutes down the road in Deventer.

IV. Legacy Topicus BV: The Maverick of Organic Growth and Dutch Co-Creation

Two men in an attic room in the eastern Dutch city of Deventer, 1998. Harry Romkema and Leo Essink started what would become Topicus not as a software company at all, but as a participation company — a small investment shop.7 The pivot came in 2001, when they reorganized around a conviction that would define the culture for the next two decades: that genuinely innovative business models could only be built by putting IT professionals — not salespeople, not consultants — at the center of the enterprise.7

This was the anti-TSS. Where TSS bought mature companies and optimized them, Topicus built platforms from a blank page, in deep collaboration with anchor customers, in a model the Dutch call "co-creation." A pension fund, a bank, a school board, a regional health network would sit down with Topicus engineers and design the software backbone for an entire sector, together. The result was slower and riskier to create than an acquisition — but when it worked, it produced something a roll-up almost never owns: a modern, cloud-native platform embedded in the daily plumbing of Dutch society, with real organic growth.

Three Verticals, One Country's Infrastructure

Topicus concentrated on three markets, and in each it burrowed into the operational core:

Healthcare. Topicus launched one of the first software-as-a-service general-practitioner information systems in 2005, and over time built regional networks connecting GPs, pharmacies, and patients into unified digital infrastructure.7 When a doctor's daily patient record, prescription, and referral flow runs through your system, you are not a vendor — you are the road the traffic drives on.

Education. In 2003 Topicus launched ParnasSys, described as the first SaaS solution for Dutch primary education, and expanded into student enrollment, tracking, and school administration across primary, secondary, and vocational systems.7 Generations of Dutch schoolchildren have had their academic lives recorded in Topicus software.

Finance. In 2010 Topicus went live with a mortgage-processing platform that optimized the mid- and back-office of one of the largest banks in the Netherlands, and grew from there into mortgage advisory, pension administration, and the systems powering local cooperative banks.7

Why It Grew

The reason legacy Topicus achieved high-single-digit and double-digit organic growth — where TSS's acquisitions crawled — comes down to what it was selling. These were not aging on-premise suites in slow decline; they were highly integrated cloud platforms that became the transactional backbone of whole sectors, expanding as they added modules, transactions, and connected participants. Growth was built into the architecture.

The culture that produced this was intense and famously flat: engineering-led, hierarchy-averse, obsessed with continuous product innovation and impatient with corporate process. It is a culture that produces great software and, its critics would note, does not naturally produce financial discipline or a repeatable acquisition machine.

The Growth Ceiling

By 2020, legacy Topicus BV had a problem that was the mirror image of TSS's. It had conquered its core Dutch verticals and built genuinely excellent, growing platforms — but it was boxed into one small country, and it lacked the cross-border M&A muscle to replicate the feat across the rest of Europe. TSS could buy anything but grow little; Topicus could grow beautifully but only at home. Each was, in effect, the missing half of the other. Constellation looked at the two and saw a flywheel waiting to be assembled.

V. The Power Marriage: The 2021 Spin-Off, Dual-Class Control, and Public Listing

The logic of the 2020 combination was almost mechanical once you saw it. TSS would keep doing what it did best — buying mature but stagnant European software companies at disciplined prices. Legacy Topicus would then bring its scarce skill to bear on those acquisitions: modernizing the products, migrating them to cloud SaaS, and reigniting organic growth. Buy stagnant, make it grow, reinvest the swelling cash flow into more stagnant assets, repeat. The M&A engine feeds the incubator; the incubator raises the returns on everything the engine buys.

Constellation structured the union as a spin-off. On January 4, 2021, it completed the purchase of 100% of Topicus.com BV — acquired from the Topicus founders' holding vehicle, IJssel BV — and combined it with its TSS operating group inside a new public company, Topicus.com Inc.2 Constellation shareholders received the new entity as a dividend-in-kind, at a ratio of 1.859817814 subordinate voting shares of Topicus.com for every Constellation common share held.2 The subordinate voting shares began trading on the TSX Venture Exchange on February 1, 2021.9

At spin-off, the market's implied valuation of the legacy Topicus BV portion of the combination was modest by the standards of the era — on the order of €200 million and change, priced at conservative multiples of recurring revenue at a moment when loss-making American SaaS companies were commanding double-digit revenue multiples. The contrast is the whole point: this was a business being valued on cash it actually produced, not on a growth narrative it promised to deliver someday.

The Control Machinery

Here the structure gets deliberately intricate, and investors should understand exactly what they own. Constellation did not keep a majority of the economics, but it kept ironclad control. It holds a single super voting share that by itself carries 50.1% of the total voting power — a one-share veto over the company.2 It also acquired 39,412,385 preferred shares, convertible one-for-one into subordinate voting shares, and a token 18 ordinary shares; on a fully diluted basis this gave Constellation roughly a 30.35% economic interest at the outset.2 Constellation also held the right to nominate six of the company's ten directors.2

The founders and management aligned themselves through a Dutch cooperative, Topicus.com Coöperatief U.A. — "the Coop." The Joday vehicle associated with the TSS founders (Joday Investments) held exchangeable units representing roughly 28.5% economic interest, while the legacy Topicus side retained a substantial stake as well, both convertible into public shares over time.2 Public shareholders, holding subordinate voting shares, ended up with the balance of the economics and — critically — almost none of the votes.

In May 2021, a preset threshold was reached and Constellation's preferred shares and the corresponding Coop preference units were mandatorily converted into ordinary/subordinate voting shares, simplifying the capital structure while leaving the super voting share — and thus the 50.1% voting lock — firmly in Constellation's hands.10

What the Structure Really Means

Strip away the diagram and the investor takeaway is blunt. A public TOI.V holder is a minority economic participant in a company permanently controlled by another public company, with no ability to influence the board, block a transaction, or force a change of strategy. The bull framing is that this is a feature: it lets management ignore short-term market pressure and compound for decades under the guidance of the best capital allocator in the business, with founders' skin genuinely in the game through the Coop. The bear framing is that public shareholders are passengers whose interests are protected only so long as they happen to align with Constellation's. Both framings are correct simultaneously, and which one dominates depends entirely on whether Constellation continues to behave the way it has. That question became a great deal more pointed in 2025.

Here is the ownership architecture in schematic form:

┌──────────────────────────────────────────────┐

│ Constellation Software (CSI) │

│ - 100% Super Voting Share (50.1% Voting) │

│ - Preferred Shares (converted 2021) │

│ - ~30% Economic Interest │

└──────┬────────────────────────────────┬──────┘

│ │

▼ (Public Listing: TOI.V) ▼

┌──────────────────────────────┐ ┌──────────────────────────────┐

│ Public Shareholders │ │ Joday & IJssel (founders) │

│ - Subordinate Voting Shares │ │ - Exchangeable Coop Units │

└──────────────┬───────────────┘ └──────────────┬───────────────┘

└──────────────────────┬──────────────────────┘

▼

┌──────────────────────────────────────────────┐

│ Topicus.com Inc. │

│ → Topicus.com Coöperatief UA │

└──────┬──────────────┬──────────────┬─────────┘

▼ ▼ ▼

┌────────────┐ ┌────────────┐ ┌────────────┐

│ TSS Public │ │ TSS Blue │ │ Topicus │

│ (Gov / HC) │ │ (Private) │ │ (SaaS/Org) │

└────────────┘ └────────────┘ └────────────┘

VI. The Mega-Pivot: The €385M Asseco Poland Alliance and Central-Eastern Europe Beachhead

For four years, Topicus behaved exactly as advertised: a high-cadence buyer of small European software companies, deploying cash in bite-sized pieces below its hurdle rate. Then, on the last day of January 2025, it did something that made analysts sit up and read the press release twice.

The Anatomy of the Deal

On January 31, 2025, Topicus.com announced that its subsidiary Yukon Niebieski Kapital B.V. had purchased 8,300,029 shares of Asseco Poland S.A. from the media conglomerate Cyfrowy Polsat S.A. — a stake of approximately 9.99% — at 85 Polish złoty per share.4 This was not a small carve-out of a €5 million business unit. It was a minority position in a publicly listed software giant, bought on the open market from another listed company.

Days later the picture widened. On February 3, 2025, Topicus disclosed that Yukon and its affiliate TSS Europe B.V. had signed a shareholders' agreement with the Adam Góral Family Foundation — the vehicle of Asseco's founder — governing their cooperation as fellow shareholders, contingent on Topicus acquiring a further block of treasury shares.5 That second tranche — 12,318,863 treasury shares, another 14.84% of the company, again at 85 PLN — required regulatory clearances and did not close until October 1, 2025, when subsidiary TSS Europe B.V. completed the purchase and the shareholders' agreement took effect.6 The two tranches together left Topicus holding roughly 24.83% of Asseco Poland,6 with a total net investment reported at €384.9 million for 2025.1

Who Is Asseco?

Asseco Poland is one of the largest software and IT-services groups in Central and Eastern Europe, listed on the Warsaw Stock Exchange, and itself the head of a sprawling federation operating in dozens of countries with subsidiaries listed as far afield as Tel Aviv and NASDAQ.4 The strategic logic of the pairing is that Asseco is, structurally, a kindred spirit: a decentralized federation of autonomous IT businesses — a mirror of the Constellation-Topicus model, only rooted in the CEE market rather than the Benelux.

Did They Overpay?

The valuation question is where an independent analyst has to be careful, because the company's framing and the reality both deserve airtime. Western European VMS assets of the kind Topicus usually buys frequently change hands at four to six times revenue. Asseco, by contrast, was acquired at a small multiple of sales and a low-double-digit earnings multiple — a deep discount that reflects genuine drivers: Poland and the broader CEE region carry country and currency risk, and Asseco has historically grown more slowly and at lower margins than a pure high-growth SaaS name. On paper, this looks like a classic value purchase with a margin of safety, exactly the kind of price discipline the company preaches.

The skeptic's counter is equally worth stating: a cheap price is not the same as a good business, a 24.83% minority stake is not control, and buying public equity in another federated conglomerate is a very different exercise from buying and integrating a small VMS company you can actually run. The discount may be cheap for good reason. The honest verdict as of mid-2026 is that the jury is out; the price looks defensible, but the strategic wisdom will only be provable in the returns Asseco delivers over years.

Why This Is a Genuine Pivot

The deeper significance is what the deal says about scale. Topicus did not do this because a €385 million minority stake in a listed company is its favorite kind of investment. It did it, in large part, because the firm now generates so much cash that deploying it all through €10 million micro-acquisitions has become a Sisyphean task. A large public-equity partnership is a way to move a lot of money at once. That is either shrewd adaptation or the first crack in the discipline, depending on your priors — a tension we will return to in the bear case.

The GAAP Paradox

The Asseco deal also produced one of the more instructive accounting episodes in the company's short public life. For the full year 2025, Topicus reported revenue up 20% to €1,552.3 million — yet GAAP net income fell 53%, from €149.5 million to €70.1 million.1 A casual reader might conclude the business had cratered. It had not.

The culprit was a non-cash charge of €221.7 million tied to electing to record the Asseco investment at cost under the equity method of accounting — an accounting adjustment, not a cash outflow or an operating loss.1 The proof that the underlying engine was untouched is in the cash statements: operating cash flow rose 19% to €412.7 million, and free cash flow available to shareholders — the company's north-star metric — climbed 23% to €218.7 million.1 Notably, the fourth quarter alone showed net income up 41% to €79.4 million once the first-quarter Asseco charge was behind it.1

The lesson for investors is a durable one that extends well beyond this single event: for a business like Topicus, reported net income is a noisy, often misleading signal, distorted by acquisition amortization and one-time adjustments. Cash generation is the number that tells the truth. That is not a company excuse; it is simply how the accounting works for a serial acquirer, and it is why the cash metrics deserve the analytical weight.

VII. The Segment Economics & Operating System: TSS Public, TSS Blue, and Topicus Operating Group

If you opened the hood of Topicus.com, you would not find one company. You would find three loosely coupled machines, each with a different temperament, deliberately kept apart so that no central bureaucracy could smother the entrepreneurial units inside them.

TSS Public is the ballast. It aims at governments, public healthcare systems, municipal utilities, and state-backed entities — customers with long procurement cycles, multi-year contracts, and an institutional aversion to ever ripping out a working system. Organic growth here is slow, but the revenue is about as low-beta as software gets. When a national tax authority or a regional hospital network runs on your platform, you are effectively part of the public infrastructure.

TSS Blue is the commercial workhorse. It consolidates private-sector vertical software — real estate, automotive dealerships, retail inventory, and similar niches — through standard, high-cadence M&A. It throws off strong cash and behaves like the classic Constellation roll-up: buy cheap, hold forever, reinvest.

The Topicus Operating Group is the crown jewel, the legacy Deventer engine of organic growth: Dutch education, financial advisory, and clinical-network platforms, still generating the product innovation and cloud IP that the rest of the portfolio can borrow.

The Proportionality Reality

Here is the point that gets lost in the excitement about the high-growth Topicus platforms: they are not where most of the money comes from. The bulk of consolidated revenue and cash flow is generated by the two TSS operating groups — the public and private roll-up businesses — not by the glamorous organic-growth incubator. Roughly speaking, the TSS side carries the majority of the load, and it is that cash that funds the entire capital-deployment engine, including the Asseco stake.

This matters for how you value the company. Topicus is often marketed on the strength of its organic growth, and 4% consolidated organic growth in 2025 is genuinely good for a VMS aggregator.1 But the engine is still, in revenue terms, predominantly a roll-up with a smaller high-growth jewel attached. The bull thesis rests on the synergy: the idea that Topicus can take the cloud-migration and product-led-growth skills honed in Deventer and apply them to slow-growing TSS acquisitions, converting flat legacy suites into defensible, growing SaaS. That is a real and differentiated capability — very few roll-ups have an organic-growth incubator on staff. Whether it moves the needle across a €1.5 billion revenue base fast enough to matter, rather than at the margin, is one of the genuinely open questions about the business, and one worth watching in the organic-growth line each year.

VIII. Playbook: Strategic Moats, Hamilton Helmer's 7 Powers, and the "Mandatory Bonus Recycling" Incentive System

Every durable business has a source of power — some structural reason competitors cannot simply copy it away. For Topicus, the power is unusually easy to name and unusually hard to attack.

Helmer's 7 Powers Applied

Switching Costs (the primary power). This is the load-bearing wall of the entire thesis. When a hospital embeds Topicus software into its patient tracking and billing, when a municipality runs its tax and civil-affairs processes on a TSS platform, when a school records every student's record in ParnasSys — ripping that system out is not a software decision, it is an organizational trauma. It means retraining staff, migrating years of data, revalidating regulatory compliance, and risking operational failure in a mission-critical process, all to save a software bill that is usually a rounding error in the customer's budget. The result is retention that consistently runs very high across VMS portfolios of this type, and the ability to push through modest annual price increases without losing customers. Switching costs are why these tiny companies are so profitable, and why they are so boring that no one tries to disrupt them.

Cornered Resource (the secondary power). The rarer asset is the Constellation operating system itself: decades of accumulated data on thousands of software acquisitions, a proprietary framework for valuing and integrating VMS assets, and — most importantly — a training culture that manufactures disciplined capital allocators. Private equity can outbid Topicus on any single deal; what it cannot easily replicate is an institution that has done the small-VMS deal thousands of times and teaches every business-unit manager to think like a capital allocator. That know-how is the cornered resource, and it is why Topicus can buy, price, and integrate faster and more accurately than most rivals.

Porter's Five Forces

The Five Forces reading is almost monotonously favorable, which is itself the point. Threat of new entrants is very low: the niches are too small to justify the capital and regulatory effort required to build a compliant competitor from scratch. Buyer power is low: customers are fragmented, localized, and captive, and they generally accept inflation-linked price increases rather than endure a migration. Competitive rivalry is low: the operating companies typically sit as local monopolies or duopolies in markets too narrow to attract a serious challenger. The forces that are not fully benign are supplier power — specifically the labor market, since European developer wages have risen and squeeze software margins — and the threat of substitutes, where over a long horizon, generative AI could in principle lower the cost of rebuilding niche software and erode the "too small to bother disrupting" defense. Neither is acute today, but both belong on the risk radar rather than in the "ignore" pile.

The Incentive System That Makes It Work

Now the part of the Topicus machine that most fascinates other companies — and that separates it from virtually every technology firm you can name. Topicus does not pay its people with stock options or restricted share units. It has, essentially, no stock-based compensation. Instead, it uses cash bonuses tied to two things the company can actually control: net revenue growth and return on invested capital, measured excluding cash and debt so managers are judged on the operating economics, not the balance sheet.

The twist is what happens to the bonus. A significant portion of any bonus above a threshold must be used to buy Topicus.com subordinate voting shares — on the open market, at the prevailing price, like any other investor — and hold them for a period of years.9 The prospectus made the philosophy explicit: managers are encouraged to invest a large share of their after-tax bonus in shares bought from the market, an approach the company frames as more shareholder-friendly than dilutive equity grants.

The implications are worth spelling out, because they are the mechanism behind a lot of the discipline the company preaches. First, there is no option-driven dilution silently transferring value from public shareholders to employees — the share count does not balloon. Second, managers hold the same shares as retail investors, bought at market prices, so when they destroy capital, they lose their own money alongside everyone else's. It converts employees from grantees hoping the stock goes up into owners who bleed when it goes down. It is not a panacea — a determined manager can still make bad decisions — but as an alignment device it is among the cleanest structures in public markets, and it is a genuine, if often overlooked, part of why the capital discipline has held.

IX. Valuation, Skeptic Stress-Test, and the Bull vs. Bear Case

A business this admired deserves an adversarial reading, so let's run one properly — the way a skeptical long/short investor or an activist would — before weighing the bull case.

The Bear Case

1. The law of large numbers. This is the most serious structural challenge, and it is arithmetic, not opinion. At more than €1.5 billion of revenue and with the engine reinvesting on the order of €300–400 million of cash per year, Topicus has to find, buy, and integrate an enormous quantity of business annually just to stand still on its growth rate.1 Doing that through €5–20 million micro-acquisitions implies dozens upon dozens of deals every year — a punishing sourcing burden that only intensifies as the company grows. Compounding at 25%+ is far easier on a €200 million base than a €1.5 billion one, and every serial acquirer eventually meets this wall.

2. Asseco as a symptom. The 24.83% Asseco stake can be read charitably as opportunistic value investing — or uncharitably as evidence that the micro-deal model can no longer absorb the cash, forcing the company toward large, low-control public-equity positions.6 A minority stake in another federated conglomerate is harder to underwrite, harder to influence, and further from the "buy small, control fully, integrate tightly" discipline that built the record. If Asseco is the first of many such deals, the risk is a slow drift from operator to holding company — precisely the "capital allocation drift" that has undone other compounders.

3. Governance and the CSI discount. As established, public holders own economics without meaningful votes; Constellation's single super voting share controls the company. That is fine as long as Constellation's interests and strategy align with minority holders'. But there is no recourse if they ever diverge — no ability to replace the board, block a related-party transaction, or force a strategic change. Markets often apply a discount to exactly this kind of controlled, dual-class structure, and that discount is a rational response to a real absence of shareholder power, not merely sentiment.

4. Wage inflation. European developer compensation has risen materially in recent years, and for a business whose cost base is overwhelmingly skilled labor, that is a persistent squeeze on the very margins that make the VMS model attractive.

The Bull Case

1. Europe remains vast and under-consolidated. The runway argument is the strongest bull point, and it is grounded in structure rather than hope. Europe's software landscape is far more fragmented than North America's, insulated into thousands of small, defensible niches by language and national regulation, and largely ignored by venture capital. That is a decades-long supply of exactly the assets Topicus buys — the law of large numbers bites, but the pond is genuinely enormous.

2. The hybrid financial profile is real. The differentiator versus a plain-vanilla aggregator is the organic-growth DNA. Consolidated organic growth of around 4% in 2025, layered on top of 20% total revenue growth, is a materially better profile than the flat-to-low-single-digit organic growth typical of legacy VMS roll-ups.1 If the Deventer incubator can keep lifting the organic rate of acquired businesses even modestly, it changes the compounding math meaningfully.

3. Capital allocation and the alignment record. Led by Robin van Poelje and CFO Jamal Baksh, the team has grown free cash flow available to shareholders to €218.7 million in 2025 — up 23% — while funding acquisitions and the Asseco stake without issuing equity to do it.1 The no-dilution, buy-your-own-shares incentive structure means the people running the machine are aligned with the outcome. On the behavioral test of management credibility — does the narrative stay consistent across filings, is capital discipline maintained, is cash converted as promised — the record so far is strong, with Asseco standing as the single most important thing to watch for evidence of drift.

The Three KPIs That Actually Matter

Cut through everything and there are three numbers to track over time. Organic revenue growth — the proof the core is not quietly decaying and that the incubator synergy is real rather than rhetorical. Free cash flow available to shareholders growth — the true measure of the compounding engine, which rose 23% in 2025.1 And the reinvestment rate combined with return on invested capital — the share of cash successfully redeployed into new deals, and at what returns, which together determine whether the flywheel keeps spinning or stalls against the law of large numbers. Everything else is commentary.

X. Epilogue & Outro

The enduring lesson of Topicus.com is a quiet rebuke to a decade of Silicon Valley orthodoxy. You do not need to build a horizontal, globally dominant platform like Salesforce to win in software. You can instead dominate dozens of small, boring, mission-critical local niches — municipal tax software, GP information systems, mortgage back-offices — treat capital allocation as a scientific discipline rather than a growth-at-all-costs sport, and assemble a defensive compounder out of businesses no one else wanted. It is the opposite of a moonshot: a thousand small, dull, defensible bets, patiently reinvested.

There is a final irony worth sitting with. This globally active, hyper-decentralized, multi-billion-euro operator across two dozen European countries is domiciled on the TSX Venture Exchange — a junior Canadian market designed for early-stage explorers and small-cap hopefuls. It is an odd home for one of the most sophisticated capital-compounding machines in the world, and yet it fits the character of the whole enterprise: understated, indifferent to prestige, and focused on the only thing that has ever mattered to it — the disciplined reinvestment of cash at high rates of return, for as long as the runway allows.

Whether that runway is as long as the bulls believe, and whether the Asseco pivot proves shrewd adaptation or the first bend in a straight discipline, are the questions the next several years will answer. The story so far suggests a machine still running to spec. The independent investor's job is to keep watching the three gauges — organic growth, free cash flow, and the returns on redeployed capital — and to notice the moment, if it ever comes, when the numbers stop telling the story management does.

References

-

Constellation Software Inc. and Topicus.com Inc. Announce Results for Topicus.com Inc. for the Fourth Quarter and Year Ended December 31, 2025 — GlobeNewswire, 2026-02-25 ↩↩↩↩↩↩↩↩↩↩↩

-

Constellation Software Inc. Completes Spin-Out of Topicus.com Inc. — Topicus.com / GlobeNewswire, 2021-01-05 ↩↩↩↩↩↩

-

Constellation Software Inc. Finalizes Acquisition of Total Specific Solutions (TSS) B.V. — Constellation Software Inc., 2013 ↩↩

-

Topicus.com Inc. acquires 9.99% Stake in Asseco Poland S.A. in Poland — GlobeNewswire, 2025-01-31 ↩↩

-

Topicus.com Inc. announces Shareholders' Agreement — Topicus.com, 2025-02-03 ↩

-

Joint Press Release of Constellation Software Inc. and Topicus.com Inc. — Topicus.com Inc. completes Agreement to acquire 14.84% of Treasury Shares in the capital of Asseco Poland S.A. — Topicus.com, 2025-10-01 ↩↩↩

-

Robin van Poelje named as Chief Executive Officer of Topicus.com — Topicus.com, 2021 ↩

-

Subordinate Voting Shares of Topicus.com Inc. to begin trading on the TSX Venture Exchange on February 1, 2021 — GlobeNewswire, 2021-01-28 ↩↩

-

All Preferred Shares of Topicus.com Inc. and Preference Units of Topicus.com Coöperatief U.A. to be Converted — GlobeNewswire, 2021-05-27 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube