T-Mobile US: The Un-carrier Revolution

I. Introduction & Episode Roadmap

Picture this: It's March 26, 2013, and John Legere, wearing his signature magenta T-Mobile shirt and designer jeans, walks onto a stage in New York City. The telecom industry expects another boring carrier announcement. Instead, Legere drops a bombshell: "This is an industry filled with ridiculously confusing contracts, limits, penalties, and fees, and this is going to stop." Within minutes, he's cursing on stage, calling AT&T and Verizon "the other guys" who are "ripping customers off." The audience—hardened tech journalists who've seen it all—are actually paying attention. This wasn't just another product launch; it was a declaration of war.

How did America's perennial fourth-place wireless carrier, bleeding customers and nearly sold for parts, transform into the industry's most disruptive force with 132.8 million subscribers? How did a company that Deutsche Telekom tried to offload become their crown jewel, delivering an 833% stock return under one CEO's tenure? This is the story of T-Mobile US—a tale of European miscalculation, regulatory windfalls, personality-driven leadership, and the power of actually listening to customers in an industry that forgot they existed.

The T-Mobile story unfolds in three acts: First, the European acquisition and decade of struggle as America's weakest national carrier. Second, the Un-carrier revolution that rewrote every rule in wireless. Third, the Sprint mega-merger that created a 5G powerhouse. Along the way, we'll explore how a company weaponized customer frustration, turned a CEO into a social media sensation, and forced two of America's most entrenched monopolies to completely change their business models.

This isn't just a wireless story—it's a masterclass in disruption, brand building, and strategic M&A. It's about turning regulatory rejection into competitive advantage, transforming company culture through authentic leadership, and proving that in commoditized industries, personality and customer obsession can be your greatest differentiators. From VoiceStream's GSM gamble to today's 5G dominance, T-Mobile's journey reveals fundamental truths about competition, consolidation, and capitalism in 21st century America.

II. Origins: VoiceStream to Deutsche Telekom

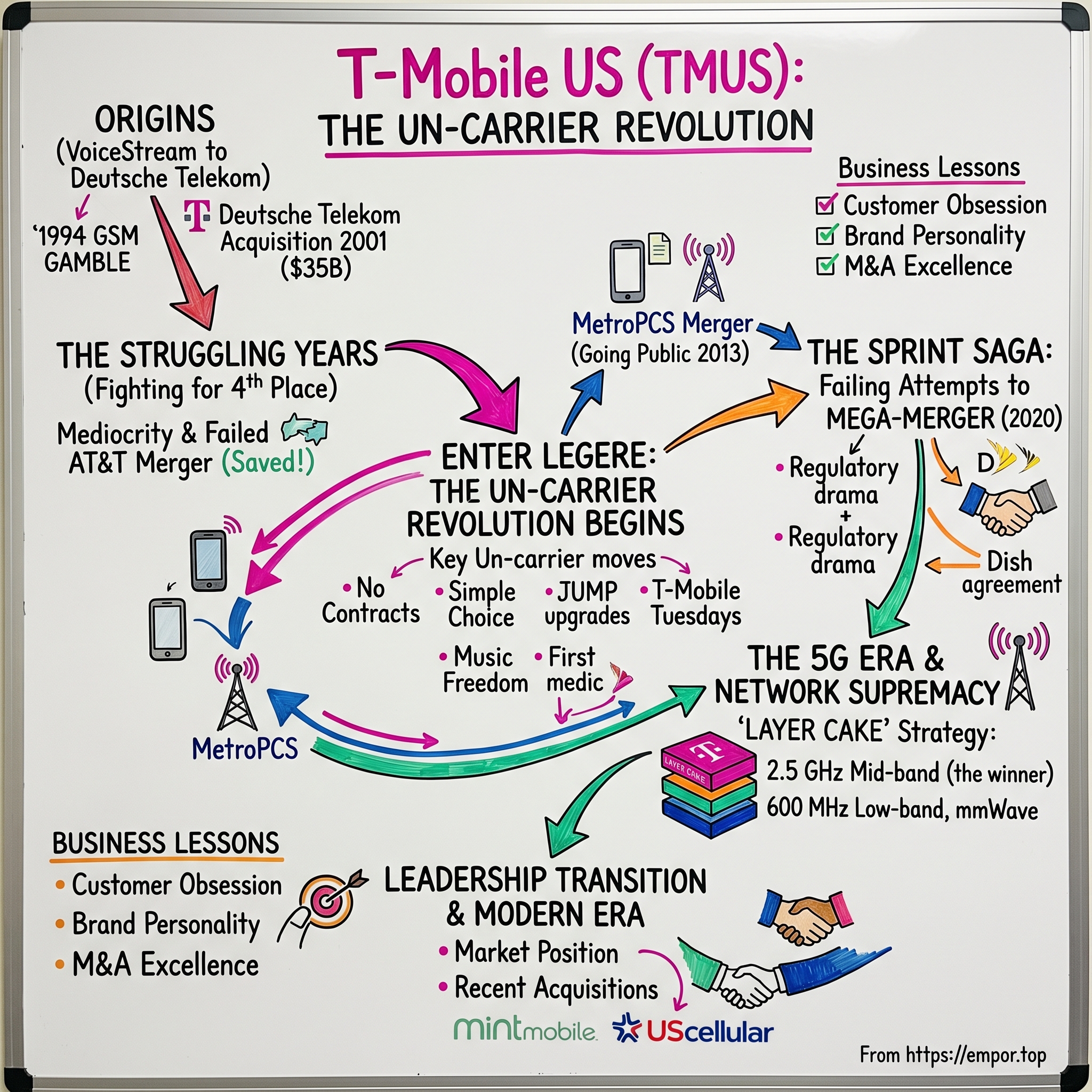

The year is 1994, and John W. Stanton is making a bet that looks insane to everyone in American wireless. While AT&T, Verizon, and Sprint are building CDMA networks—the technology blessed by Qualcomm and seemingly destined to dominate North America—Stanton launches VoiceStream Wireless on GSM technology, the global standard everywhere except the United States. His logic? Americans travel. They need phones that work in London, Tokyo, and Berlin, not just Los Angeles and New York. It's a contrarian bet that would define T-Mobile's DNA: when everyone zigs, you zag. Stanton wasn't just betting on a technology standard—he was betting on American exceptionalism going global. VoiceStream Wireless PCS was established in 1994 as a subsidiary of Western Wireless Corporation to provide wireless personal communications services in 19 FCC-defined metropolitan service areas using the GSM digital wireless standard. The company quietly built its first networks in Honolulu and Salt Lake City by 1996, far from the scrutiny of Wall Street and the established carriers who dismissed GSM as a European oddity.

By 1999, Stanton had grown VoiceStream enough to spin it off from Western Wireless as an independent public company. The timing was perfect—or so it seemed. The telecom bubble was inflating, spectrum was gold, and anyone with a wireless story could access capital markets. But VoiceStream faced a fundamental problem: coverage. While AT&T and Verizon had nationwide networks built over decades, VoiceStream was a patchwork of urban markets with massive coverage gaps. Enter the acquisition strategy that would define the company's DNA.In February 2000, VoiceStream acquired Omnipoint Corporation, a regional GSM network operator in the northeastern United States, followed by Aerial Communications in May 2000, adding crucial coverage in Houston, Kansas City, and Minneapolis. These weren't just acquisitions—they were pieces of a puzzle that would make VoiceStream attractive to a global buyer.

On June 1, 2001, Deutsche Telekom completed its acquisition of VoiceStream Wireless, Inc., for $35 billion and Southern U.S. regional GSM network operator Powertel, Inc., for $24 billion. By the end of 2001, VoiceStream Wireless had 19,000 employees serving 7 million subscribers. For Deutsche Telekom, this was their moonshot—a massive bet on the American market that would either establish them as a global telecommunications powerhouse or become one of the most expensive mistakes in telecom history.

The timing couldn't have been worse. The dot-com bubble had burst, telecom stocks were cratering, and Deutsche Telekom's stock had slipped so far that its VoiceStream purchase—first valued at $56 billion—plummeted in value to $20.7 billion in stock, $4.2 billion in cash and $4.7 billion in assumed debt. The German government owned 59% of Deutsche Telekom, triggering a xenophobic response from Senator Ernest "Fritz" Hollings, who introduced legislation to block foreign government-owned companies from acquiring U.S. carriers. The deal barely squeaked through regulatory approval.

On September 2, 2001, VoiceStream Wireless Inc. adopted the name T-Mobile USA, Inc. and began rolling out the T-Mobile brand, starting with locations in California and Nevada. The merger became official in July 2002. Deutsche Telekom brought its magenta brand to America, but the company remained what it had always been: the perpetual underdog in a market dominated by AT&T and Verizon.

What Deutsche Telekom didn't realize was that they had just acquired a company with the perfect DNA for disruption—contrarian from birth, built through acquisitions, and desperately in need of a reason to exist. All it needed was the right leader to unleash its potential.

III. The Struggling Years: Fighting for Fourth Place

The decade following Deutsche Telekom's acquisition was a masterclass in corporate mediocrity. From 2001 to 2012, T-Mobile USA became the Blockbuster Video of wireless—a company everyone knew would eventually disappear, operating in a market it didn't seem to understand, led by executives who appeared more interested in managing decline than creating growth. While AT&T and Verizon carved up the premium market and Sprint battled for price-conscious consumers, T-Mobile occupied a no-man's land: not cheap enough to compete on price, not good enough to compete on quality. On September 17, 2007, the company announced the acquisition of regional GSM carrier SunCom Wireless Holdings, Inc. for $2.4 billion, adding 1.1 million customers and expanding coverage to southern states including North Carolina, South Carolina, Tennessee, Georgia, Puerto Rico and the U.S. Virgin Islands. SunCom was showing signs of trouble, losing money at a rapid rate; from 2006 to 2007 the company's net loss increased from $110 million to $193 million. T-Mobile was essentially buying a failing carrier for its spectrum and footprint—a pattern that would define its M&A strategy for years.

The real story of T-Mobile's lost decade wasn't the small acquisitions or incremental network improvements. It was the failed merger that almost ended the company—and paradoxically saved it. On March 20, 2011, AT&T announced its intention to purchase T-Mobile US from Deutsche Telekom for $39 billion. The department said that the proposed $39 billion transaction would substantially lessen competition for mobile wireless telecommunications services across the United States, resulting in higher prices, poorer quality services, fewer choices and fewer innovative products for the millions of American consumers who rely on mobile wireless services in their everyday lives. On August 31, 2011, the Antitrust Division of the United States Department of Justice formally announced that it would seek to block the takeover, and filed a lawsuit to such effect in federal court.

The DOJ's complaint revealed something extraordinary about T-Mobile's position in the market. The complaint cites a T-Mobile document in which T-Mobile explains that it has been responsible for a number of significant "firsts" in the U.S. mobile wireless industry, including the first handset using the Android operating system, Blackberry wireless email, the Sidekick, national Wi-Fi "hotspot" access, and a variety of unlimited service plans. Despite being the smallest national carrier, T-Mobile was the innovation engine of the entire industry.

The bid was abandoned by AT&T on December 19, 2011. But here's where the story takes a remarkable turn: As per the original acquisition agreement, Deutsche Telekom would receive $3 billion in cash as well as access to $1 billion worth of AT&T-held wireless spectrum. T-Mobile had just received a $4 billion windfall—enough cash and spectrum to transform itself from industry roadkill into a legitimate competitor.

Deutsche Telekom now faced a choice: use this windfall to manage T-Mobile's decline more comfortably, or swing for the fences with a radical transformation. They chose transformation, and they knew exactly who they needed to lead it.

IV. Enter Legere: The Un-carrier Revolution Begins

September 19, 2012: Deutsche Telekom announces John Legere as the new CEO of T-Mobile USA. The telecommunications industry collectively yawned. Another telecom lifer—32 years in the business, nearly twenty at AT&T, stints at Dell and Global Crossing—taking over a dying brand. What they didn't know was that Legere had spent his entire career studying what was wrong with the industry, and he was about to weaponize that knowledge.

The month before Legere assumed the role of CEO, T-Mobile's stock price was $9.73 per share. The day he stepped down on April 24, 2020, it reached $90.80. That's an 833% increase. But those numbers don't capture the revolution that happened in between.

A Massachusetts native, Legere graduated from St. Bernard's Central Catholic School in Fitchburg, Massachusetts and aspired to be a gym teacher, before he figured out he wanted a more lucrative career and decided to study business instead. This origin story matters—Legere wasn't born into corporate America. He chose it, but he never forgot what it felt like to be an outsider.

Legere then spent nearly twenty years at AT&T, where he spent some time working under Daniel Hesse, formerly CEO of Sprint Corporation. He was chief executive for AT&T Asia from April 1994 to November 1997, and also spent time as head of AT&T Global Strategy and Business Development. From 1997 to 1998, he was president of the worldwide outsourcing subsidiary of AT&T, AT&T Solutions. Legere then worked as senior vice president of Dell and president and chief operations officer for Dell's Operations in Europe, the Middle East and Africa and president, Asia-Pacific for Dell from 1998 to February 2000. Prior to joining T-Mobile US, he was CEO of Asia Global Crossing from February 2000 to January 2002, and CEO of Global Crossing from October 2001 to October 2011.

At Global Crossing, Legere had navigated a company through bankruptcy and eventual acquisition. He knew what corporate death looked like, and when he walked into T-Mobile's Bellevue headquarters in September 2012, he saw a company on life support. But he also saw something else: opportunity. "This is an industry filled with ridiculously confusing contracts, limits on how much data you can use or when you can upgrade, and monthly bills that make little sense," Legere declared on March 26, 2013, at T-Mobile's first Un-carrier event in New York. "As America's Un-carrier, we are changing all of that and bringing common sense to wireless."

The contract-free Simple Choice plan, also known as Un-carrier 1.0, debuted in March 2013 by offering unlimited calling and text messaging with 500 MB of unthrottled data monthly for a base price of $50. The company introduced a new streamlined plan structure for new customers which drops contracts, subsidized phones, coverage fees for data, and early termination fees. Customers could purchase devices through affordable, interest-free monthly installments and upgrade anytime they wanted—not just when their carrier said it was okay.

This wasn't just a pricing change—it was a philosophical revolution. For decades, the wireless industry had operated on a simple premise: lock customers into contracts, make it painful to leave, extract maximum revenue. Legere's insight was that customers hated this model so much that simply treating them like human beings would be a competitive advantage.

But Legere understood that disruption required more than just better plans—it required theater. He became the CEO who cursed on earnings calls, who called AT&T and Verizon "Dumb and Dumber," who wore magenta sneakers to industry conferences. His Twitter account became must-read content in the telecom industry, where he'd personally respond to customer complaints and mock competitors.

"Listen to your employees, listen to your customers, shut the f--- up, and do what they tell you," became Legere's management philosophy. It sounds simple, but in an industry built on customer contempt, it was revolutionary.

The Un-carrier moves came in rapid succession. On July 10, 2013, T-Mobile introduced Un-carrier 2.0 as Jump, a new add-on for its monthly plans which allows customers to upgrade their phone up to two times per year. On October 9, 2013, T-Mobile introduced their third phase of the "Un-carrier," which was the introduction of basically free international roaming. On January 8, 2014, T-Mobile revealed Un-carrier 4.0, known as Get Out of Jail Free Card, offering to pay off the Early Termination Fees (ETF), up to $375 per line, for individuals and families who wanted to switch from AT&T, Verizon, or Sprint to T-Mobile.

Each move forced the industry to respond. AT&T and Verizon, companies that had ignored T-Mobile for years, suddenly found themselves having to match offers from a carrier they'd written off as dead. The entire structure of the American wireless industry—contracts, subsidies, upgrade cycles—began to crumble under Legere's assault.

But transformation requires capital, and T-Mobile needed scale to compete. The Un-carrier revolution was working, but it needed a financial foundation to sustain it.

V. MetroPCS Merger & Going Public

October 3, 2012—while the industry was still digesting the failed AT&T merger, T-Mobile and MetroPCS dropped a bombshell. On October 3, 2012, MetroPCS Communications agreed to merge with T-Mobile USA. MetroPCS shareholders would hold a 26% stake in the company formed after the merger, which retained the T-Mobile brand. The deal was structured as a reverse takeover; the combined company went public on the New York Stock Exchange as TMUS and became T-Mobile U.S. Inc. on May 1, 2013.

This wasn't just a merger—it was financial alchemy. T-Mobile USA, a private subsidiary of Deutsche Telekom, would become a publicly traded company through the back door. MetroPCS, with its 9.3 million prepaid customers and nascent LTE network, would provide the scale and spectrum T-Mobile desperately needed. The transaction was structured as a recapitalization, in which MetroPCS would declare a 1 for 2 reverse stock split, make a cash payment of $1.5 billion to its shareholders (approximately $4.09 per share prior to the reverse stock split) and acquire all of T-Mobile's capital stock by issuing to Deutsche Telekom 74% of MetroPCS' common stock on a pro forma basis.

The genius of the deal wasn't just the financial engineering—it was the strategic fit. MetroPCS had built out LTE networks in major urban markets where T-Mobile was weakest. Its prepaid customer base complemented T-Mobile's postpaid focus. And critically, it gave T-Mobile a currency—publicly traded stock—to use for future acquisitions and employee compensation.

"This is not a deal to survive, it's a deal to thrive," Legere proclaimed in a video statement. "It's an aggressive plan to accelerate our return to market leadership." Coming from the CEO of the fourth-place carrier, it sounded delusional. But Legere wasn't interested in fourth place—he was building a war chest.

The merger between T-Mobile USA Inc. and MetroPCS was officially approved by MetroPCS shareholders on April 24, 2013. On May 1, 2013, T-Mobile U.S. began trading on the New York Stock Exchange under the ticker symbol TMUS. For the first time since Deutsche Telekom acquired VoiceStream in 2001, T-Mobile had direct access to U.S. capital markets.

The integration playbook T-Mobile developed for MetroPCS would become crucial for its future. Rather than immediately merging networks and confusing customers, T-Mobile kept MetroPCS as a separate brand focused on prepaid services. They migrated customers gradually as they upgraded devices, avoiding the network integration disasters that had plagued Sprint's merger with Nextel. They combined back-office operations for cost savings while maintaining distinct market positioning.

Based on analyst consensus estimates for 2012, the combined company was expected to have approximately 42.5 million subscribers, $24.8 billion of revenue, and projected synergies with an NPV of $6-7 billion. But these numbers understated the real value: T-Mobile now had the scale, spectrum, and capital structure to execute Legere's Un-carrier vision. The revolution had its financial foundation.

VI. Un-carrier Moves: Rewriting Industry Rules

The MetroPCS merger gave Legere the ammunition he needed, but the Un-carrier campaign was his weapon of choice. Between 2013 and 2017, T-Mobile would launch 16 distinct Un-carrier moves, each designed to solve a specific customer pain point while forcing competitors to abandon profitable but anti-consumer practices. This wasn't disruption for disruption's sake—it was systematic deconstruction of an industry's economic model. On June 18, 2014, T-Mobile announced Un-carrier 6.0, known as Music Freedom. Data used on certain streaming music services would no longer count to users' data limits. At the time of the announcement, these services included: Pandora, Spotify, Rhapsody, Google Play Music, iTunes Radio, Slacker, Milk Music, Beatport, and iHeartRadio. This wasn't just zero-rating—it was a declaration of war on data caps themselves.

The genius of Music Freedom wasn't the technology—it was the psychology. Carriers had trained customers to fear their data usage, to constantly check their meters, to ration their consumption. T-Mobile said: stream all you want. The number of T-Mobile customers streaming music each day jumped nearly 300%, and they were streaming a whopping 66 million songs per day − or roughly 200 terabytes of data per day − on T-Mobile's Data Strong™ network.

But Music Freedom was just the appetizer. On November 10, 2015, T-Mobile introduced Un-carrier X, with Binge On, where watching videos on certain streaming services doesn't count against a user's 4G LTE data if the user has at least 3 GB of 4G LTE data. For all Simple Choice plans, most videos are automatically streamed in DVD (480p or higher) quality, allowing customers to watch as much as three times more video than before.

The net neutrality advocates went ballistic. As currently offered, Binge On violates key net neutrality principles and harms user choice, innovation, competition, and free speech online. As a result, the program is likely to violate the FCC's general conduct rule. Binge On undermines the core vision of net neutrality: Internet service providers (ISPs) that connect us to the Internet should not act as gatekeepers that pick winners and losers online by favoring some applications over others. By exempting Binge On video from using customers' data plans, T-Mobile is favoring video from the providers it adds to Binge On over other video.

But T-Mobile had a defense that was quintessentially Un-carrier: We've proven our track record with Music Freedom. No one pays us, and we don't pay them - and everyone wins – especially customers. We're not here to play favorites. Like Music Freedom, Binge On is open to any legit streaming service (with lawful content) out there – at absolutely no cost to them. They just need to contact us and work with us on the technical requirements, optimization for mobile viewing and confirm we can consistently identify their incoming music or video streams. But perhaps the most audacious Un-carrier move came on June 6, 2016, with Un-carrier 11—#GetThanked. Launched in 2016, T-Mobile Tuesdays was built to show customers appreciation every week — no strings, no gimmicks, just thanks. The Un-carrier announced T-Mobile Tuesdays, a new app that thanks T-Mobile customers with free stuff and epic prizes, every Tuesday.

This wasn't just about free pizza and movie tickets—though there were plenty of both. This was about fundamentally changing the relationship between a carrier and its customers. While AT&T and Verizon treated their customers as revenue sources to be optimized, T-Mobile treated them as people to be thanked. T-Mobile Tuesdays turned the idea of the loyalty program upside down. This isn't about customers showing loyalty to us – it's about us showing our loyalty to them with free stuff - every single week.

The program was an instant phenomenon. Immediately after launching, the T-Mobile Tuesdays app shot to No.1 on Apple's App Store – ahead of perennial favorites like Snapchat, Google Maps and even Instagram. The takeover with DJ Khaled drove so many downloads that the app crashed on the first day of launch. Since 2016, customers have saved more than 500 million dining deals, 56 million movie tickets, and 4.5 million Slurpee drinks.

Each Un-carrier move built on the previous ones, creating a compounding effect. Customers weren't just choosing T-Mobile for one feature—they were choosing an entirely different philosophy of wireless service. By 2017, T-Mobile had fundamentally transformed not just its own business, but the entire American wireless industry. Contracts were dead. Unlimited data was back. International roaming was free. Customers expected to be thanked, not gouged.

But Legere and his team knew that true industry transformation required more than marketing moves—it required scale. And the biggest opportunity for scale was about to present itself.

VII. The Sprint Saga: From Failed Attempts to Mega-Merger

The courtship between T-Mobile and Sprint was wireless industry's longest-running soap opera—a decade of will-they-won't-they speculation, failed attempts, regulatory drama, and ultimately, a merger that would reshape American telecommunications. Understanding this saga requires understanding the desperate mathematics of the wireless industry: in a business where network infrastructure costs billions and spectrum is finite, scale isn't just an advantage—it's survival. Sprint Corporation and T-Mobile US merged in 2020 in an all shares deal for $26 billion. The deal was announced on April 29, 2018. After a two-year-long approval process the merger was closed on April 1, 2020, with T-Mobile emerging as the surviving brand. But this simple timeline doesn't capture the drama, politics, and existential stakes involved.

The backstory begins in 2013. In December 2013, multiple reports indicated that Sprint Corporation and its parent company, SoftBank, were working towards a deal to acquire a majority stake in T-Mobile US for at least US$20 billion. SoftBank's CEO, Masayoshi Son, had just spent $21.6 billion for a 72 percent stake in Sprint and believed consolidation was essential for survival. But the Obama administration's FCC, led by Chairman Tom Wheeler, had made clear their commitment to maintaining four national carriers. The deal died before it was formally proposed.

Fast forward to 2017. The regulatory environment had changed with the Trump administration, but initial merger talks between T-Mobile and Sprint still collapsed in November 2017 when SoftBank's board decided not to give up control of Sprint. What changed between November 2017 and April 2018? Several things changed over the last few months that led Son to change his mind, including greater synergies from lower corporate taxes, an increased understanding of how much 5G deployment will cost Sprint, and a rapidly changing competitive wireless landscape that now includes cable providers.

But the most crucial factor was Sprint's deteriorating position. Sprint was bleeding customers, drowning in debt, and facing a 5G buildout it couldn't afford. For Son, who had bet his reputation on Sprint, the choice was stark: merge or watch his investment become worthless.

The terms announced on April 29, 2018, reflected this desperation: Under the terms of the transaction, Sprint shareholders will receive a fixed exchange ratio of 0.10256 T-Mobile shares for each Sprint share, or the equivalent of approximately 9.75 Sprint shares for each T-Mobile share. Based on closing share prices on April 27, this represents a total implied enterprise value of approximately $59 billion for Sprint and approximately $146 billion for the combined company.

John Legere would remain CEO. T-Mobile would be the surviving brand. Deutsche Telekom would control the combined company with 42% ownership, while SoftBank would hold 27%. This wasn't a merger of equals—it was T-Mobile absorbing Sprint.

But getting regulatory approval would prove to be a two-year marathon that tested every aspect of T-Mobile's political and strategic capabilities. The merger faced opposition from multiple fronts: consumer advocacy groups arguing it would raise prices, labor unions fearing job losses, and Democratic politicians concerned about market concentration. The Department of Justice's Antitrust Division, even under a Republican administration, had serious concerns about reducing the number of national carriers from four to three.

T-Mobile's regulatory strategy was masterful in its comprehensiveness. They didn't just argue the merger's benefits—they created a narrative about American competitiveness in 5G. The merger would accelerate the deployment of a robust, nationwide 5G network, which is critical to the economic, social and technological development and leadership of the United States. They positioned the merger not as market consolidation but as creating a stronger competitor to AT&T and Verizon's duopoly.

The turning point came with the Dish Network agreement. On July 26, 2019, the Department of Justice announced its approval of the merger, conditional on the divestiture of Sprint's prepaid business, including Boost Mobile, to Dish Network Corporation for $5 billion. Dish would also receive access to T-Mobile's network for seven years while building out its own 5G network, theoretically preserving four national competitors.

The FCC formally approved the merger on November 5, 2019, with conditions that would define T-Mobile's future. The merged company committed to deploying 5G service covering 97% of the U.S. population within three years and 99% within six years. They promised to offer in-home broadband to 90% of the rural population within six years. These weren't suggestions—they were enforceable commitments with financial penalties for non-compliance.

But the state attorneys general weren't done. In June 2019, ten state attorneys general, led by New York and California, filed a lawsuit to block the merger, arguing it would lead to higher prices for consumers. By the time of trial, the coalition had grown to fourteen states plus the District of Columbia. The states' case rested on traditional antitrust economics: fewer competitors meant higher prices.

The trial, which began December 9, 2019, became a referendum on the future of American wireless. T-Mobile executives testified about Sprint's deteriorating condition—its network was falling apart, it lacked the capital for 5G deployment, and without the merger, it would likely fail. Sprint executives confirmed this dire assessment. Even Charlie Ergen, Dish's chairman, testified that Sprint was not viable in the long term.

On February 11, 2020, Judge Victor Marrero delivered his ruling: the merger could proceed. His decision was remarkable for its candor about Sprint's condition: "Sprint does not have sufficient spectrum to deploy a nationwide 5G network. Thus, Sprint would continue to fall further behind its competitors, likely leading to its exit from the market." The judge essentially concluded that the market was already a three-player game—the merger just acknowledged reality.

The COVID-19 pandemic added a surreal element to the merger's closing. As the world shut down in March 2020, T-Mobile and Sprint were racing to close before markets crashed or regulators changed their minds. The exchange ratio was renegotiated from 9.75 to 11.0 Sprint shares per T-Mobile share—a reflection of T-Mobile's strengthening position and Sprint's weakness. On April 1, 2020, the merger officially closed. The combined company had approximately 140 million customers, making it the second-largest wireless carrier in the United States.

VIII. Leadership Transition & Integration

April 1, 2020, marked more than just the merger closing—it was the end of the Legere era. After transforming T-Mobile from industry doormat to disruptive force, John Legere handed the reins to Mike Sievert, his longtime deputy and the architect of many Un-carrier moves. The timing seemed either terrible or perfect: a massive integration during a global pandemic with a new CEO at the helm.

Sievert's background made him the ideal successor. Joining T-Mobile in 2012 as Chief Marketing Officer, he had been Legere's strategic partner from day one. Before T-Mobile, Sievert served as Corporate Vice President of the Windows Phone Business Marketing group at Microsoft, Chief Commercial Officer for Clearwire Corporation, and held executive positions at AT&T. Unlike the theatrical Legere, Sievert was methodical, analytical, and focused on execution.

"Mike Sievert has been my partner in building the Un-carrier revolution," Legere said in his farewell. "He's been the chief architect of our strategy and the chief operator who made it real." This wasn't corporate platitude—Sievert had literally designed many of the Un-carrier moves, led the merger negotiations, and built the operational infrastructure that would make integration possible.

The integration challenge was staggering. T-Mobile needed to combine two incompatible networks (T-Mobile's GSM/LTE and Sprint's CDMA/LTE), migrate 54 million Sprint customers, consolidate 80,000 employees, and achieve $43 billion in projected synergies—all while maintaining service quality and customer growth during a pandemic when retail stores were closed and technicians couldn't enter homes.

Sievert's approach was surgical. Rather than rushing integration, T-Mobile methodically decommissioned Sprint cell sites while expanding T-Mobile's network with Sprint's valuable mid-band spectrum. The company offered Sprint customers incredible deals to upgrade to T-Mobile-compatible devices, essentially paying them to help with the migration. By August 2020, just four months after closing, T-Mobile discontinued the Sprint brand entirely, years ahead of schedule.

The pandemic, paradoxically, accelerated certain aspects of integration. With people working from home, network traffic patterns changed, allowing T-Mobile to optimize differently. The surge in digital adoption meant customers were more willing to handle upgrades and service changes online. The company's network engineers, working remotely, could focus on integration planning without the distraction of office politics.

Financial results validated the strategy. In Q2 2020, T-Mobile added 1.2 million postpaid customers, more than AT&T and Verizon combined. The company raised its synergy targets from $43 billion to $60 billion. Network tests showed T-Mobile pulling ahead in 5G coverage and speed. What should have been a disaster—a complex merger during a pandemic with a new CEO—became a masterclass in operational excellence.

The cultural integration proved equally important. Sprint employees, demoralized from years of decline, suddenly found themselves part of a winning team. T-Mobile maintained its "Un-carrier" spirit while absorbing Sprint's technical expertise, particularly in mid-band spectrum deployment. The company avoided the mass layoffs typical of telecom mergers, instead redeploying Sprint employees to accelerate 5G buildout.

Sievert also proved he could maintain T-Mobile's disruptive edge. During the pandemic, when other carriers pulled back, T-Mobile launched new Un-carrier moves: free 5G for first responders, expanded coverage commitments, and aggressive pricing that continued taking share from AT&T and Verizon. He demonstrated that T-Mobile's culture wasn't dependent on one charismatic leader—it was embedded in the company's DNA.

IX. The 5G Era and Network Supremacy

The real prize of the Sprint merger wasn't the customers or the cost synergies—it was spectrum, specifically Sprint's treasure trove of 2.5 GHz mid-band spectrum that would become the foundation of T-Mobile's 5G dominance. While AT&T and Verizon had spent years focused on millimeter wave 5G that worked incredibly fast but couldn't penetrate buildings or travel more than a few blocks, T-Mobile was about to deploy what it called the "layer cake" strategy.

The bottom layer was T-Mobile's 600 MHz low-band spectrum, acquired for $8 billion in the 2017 FCC auction. This spectrum traveled far and penetrated buildings but offered modest speed improvements over LTE. The top layer was millimeter wave for ultra-high speeds in dense urban areas. But the middle layer—Sprint's mid-band spectrum—was the secret sauce. It offered speeds ten times faster than LTE with coverage that actually worked in the real world.

By December 2020, just eight months after the merger closed, T-Mobile's 5G network covered 280 million people, far exceeding AT&T and Verizon's combined 5G coverage. More importantly, T-Mobile's Ultra Capacity 5G—using that crucial mid-band spectrum—covered 100 million people with speeds averaging 300 Mbps. Verizon and AT&T, having ignored mid-band spectrum for years, were forced to spend $68 billion and $23 billion respectively in the C-band auction just to catch up to where T-Mobile already was.

The network superiority translated into customer perception. For the first time in American wireless history, the perennial network laggard was winning independent network tests. Ookla, OpenSignal, and RootMetrics all showed T-Mobile pulling ahead in 5G availability and speeds. The company that AT&T and Verizon had mocked for poor coverage was now beating them at their own game.

But T-Mobile's 5G strategy went beyond mobile phones. The company launched 5G Home Internet, offering fixed wireless broadband to compete directly with cable companies. At $50 per month with no contracts, data caps, or equipment fees, it undercut traditional broadband by 30-40%. By 2023, T-Mobile had 5 million home internet customers, making it the fastest-growing broadband provider in America.

The FCC commitments that seemed onerous during merger approval became competitive advantages. T-Mobile's promise to cover 97% of Americans with 5G within three years forced an aggressive buildout that left competitors behind. The rural coverage requirements opened new markets that AT&T and Verizon had ignored for decades. The penalty provisions—up to $2.4 billion if commitments weren't met—ensured T-Mobile couldn't slow down.

The 5G network also enabled new enterprise opportunities. T-Mobile Business grew from an afterthought to a significant revenue driver, offering private 5G networks for factories, dedicated network slices for industries, and IoT connectivity that leveraged the massive coverage footprint. The company that had once been dismissed as a consumer-only brand was now winning enterprise contracts from Fortune 500 companies.

The technical achievement was remarkable. T-Mobile decommissioned 35,000 Sprint cell sites while simultaneously building out 30,000 new 5G sites. They migrated Sprint's spectrum to T-Mobile's network while maintaining service for both customer bases. They integrated billing systems, retail stores, and customer service operations. And they did it all while gaining customers every quarter.

X. Modern Era: Market Position & Recent Acquisitions

By 2023, T-Mobile had achieved what seemed impossible a decade earlier: legitimate market leadership. With 117 million customers and growing, the company wasn't just competing with AT&T and Verizon—it was beating them. The Q3 2023 results told the story: T-Mobile added 850,000 postpaid phone customers while AT&T and Verizon combined for just 450,000. The "Un-carrier" had become the carrier to beat.

The acquisition strategy continued, but now from a position of strength. On March 15, 2023, T-Mobile announced the acquisition of Ka'ena Corporation, the parent company of Mint Mobile and Ultra Mobile, for up to $1.35 billion. The deal brought T-Mobile something more valuable than customers—it brought Ryan Reynolds, Mint's celebrity owner and marketing genius, into the T-Mobile family. Reynolds' irreverent marketing style perfectly matched T-Mobile's brand, and his Mint commercials became a masterclass in challenger brand advertising.

The Mint acquisition was strategically brilliant. It gave T-Mobile a stronger presence in the prepaid market without diluting its premium brand. Mint's direct-to-consumer model, selling service online without retail stores, provided a template for reaching cost-conscious customers profitably. The multiple brands strategy—T-Mobile, Metro, and now Mint—allowed the company to segment the market without competing against itself.

But the biggest move came on May 28, 2024, when T-Mobile announced the acquisition of most of UScellular's operations for $4.4 billion. The deal included 4 million customers, 2,100 retail stores, and crucial spectrum in markets where T-Mobile needed density. UScellular had been struggling to compete as a regional carrier, and T-Mobile offered a lifeline while strengthening its own rural presence.

The UScellular acquisition demonstrated T-Mobile's evolution from disruptor to consolidator. The company that had nearly been acquired for parts was now the acquirer, methodically rolling up smaller players while regulators watched carefully. The deal structure was clever—T-Mobile acquired only the customer relationships and some spectrum, leaving UScellular as a smaller but viable entity to preserve the appearance of competition.

Deutsche Telekom's ownership stake told another story of transformation. From wanting to exit the U.S. market in 2011, Deutsche Telekom had systematically increased its ownership to 51.4% by 2024. T-Mobile US had become the crown jewel of Deutsche Telekom's global portfolio, contributing the majority of profits and growth. The parent company that had almost abandoned America was now doubling down.

Financial performance validated the strategy. T-Mobile's 2023 revenue exceeded $78 billion with EBITDA margins approaching 40%. The company generated $16 billion in free cash flow, funding both network investment and shareholder returns. The stock price, which had started 2013 at $20, exceeded $180 by late 2024. Market capitalization surpassed $200 billion, making T-Mobile one of the most valuable telecommunications companies globally.

The competitive landscape had fundamentally shifted. AT&T, distracted by its failed media ambitions and drowning in debt from the Time Warner acquisition, was retrenching to its core wireless business. Verizon, long the network quality leader, found itself playing catch-up in 5G while losing customers to T-Mobile's aggressive pricing. Cable companies like Comcast and Charter, despite entering wireless through MVNO agreements, struggled to differentiate beyond bundling.

XI. Playbook: Business & Investing Lessons

The T-Mobile story offers a masterclass in business transformation, but the lessons extend far beyond telecommunications. This is fundamentally a story about how to compete when you're structurally disadvantaged, how to build culture as a competitive moat, and how to execute M&A in industries where scale determines survival.

Customer Obsession as Competitive Advantage: Legere's greatest insight wasn't technological—it was psychological. In an industry that treated customers with contempt, simply listening to them became revolutionary. Every Un-carrier move addressed a specific customer pain point that competitors had ignored because the pain was profitable. The lesson: in mature industries, customer experience can be more disruptive than technology.

The Power of Brand Personality: T-Mobile proved that in commoditized industries, personality matters. Legere's antagonistic, profanity-laced attacks on competitors weren't just theater—they were positioning. By making T-Mobile the rebel brand, they gave customers permission to switch not just for better service, but to make a statement. The magenta brand became a badge of defiance against corporate telecommunications.

M&A Excellence: T-Mobile executed three transformative mergers—MetroPCS, Sprint, and the smaller acquisitions—each with different structures but consistent integration philosophy. They maintained separate brands when it made sense (Metro), quickly consolidated when necessary (Sprint), and always prioritized network integration over cost synergies. The lesson: in consolidating industries, integration capability becomes a core competency.

Regulatory Navigation: T-Mobile turned regulatory constraints into competitive advantages. The failed AT&T merger's breakup fee funded transformation. The Sprint merger conditions forced network investments that created lasting superiority. The company learned to align its interests with regulators' goals—rural coverage, 5G leadership, broadband competition—making approval more likely.

Network Effects and Scale: The wireless industry demonstrates pure scale economics—the cost to serve one additional customer approaches zero while network investment costs are largely fixed. T-Mobile understood that market share gains created a virtuous cycle: more customers meant more network investment which attracted more customers. Once they achieved scale parity with AT&T and Verizon, superior execution determined the winner.

Capital Allocation Discipline: Despite aggressive expansion, T-Mobile maintained capital discipline. They bought spectrum when others focused on content (AT&T's DirecTV disaster). They invested in network while others paid dividends. They acquired companies at reasonable multiples while avoiding empire building. The result: industry-leading returns on invested capital.

Cultural Transformation: T-Mobile proved culture could be changed even in mature organizations. They transformed Deutsche Telekom's bureaucratic subsidiary into America's most innovative carrier. The secret wasn't perks or slogans—it was empowerment. Employees who had been trained to say "no" were suddenly encouraged to solve customer problems. The Un-carrier movement was as much internal as external.

XII. Analysis & Bear vs. Bull Case

The bull case for T-Mobile rests on structural advantages that compound over time. The company's 5G network superiority, built on Sprint's mid-band spectrum, gives them a multi-year lead that competitors can't easily close. While Verizon and AT&T spent $91 billion combined in the C-band auction, they still need years to deploy that spectrum to match T-Mobile's current coverage. The company's Ultra Capacity 5G already covers 275 million people with average speeds of 400 Mbps—performance that enables new use cases from fixed wireless to enterprise private networks.

The fixed wireless opportunity alone could justify optimism. With 5 million home internet customers growing at 2 million annually, T-Mobile is attacking a $100 billion broadband market dominated by cable monopolies. At $50 monthly with 40% EBITDA margins and minimal incremental network cost, each fixed wireless customer generates exceptional returns. If T-Mobile captures just 15% of U.S. broadband households, that's $10 billion in high-margin annual revenue.

Market share dynamics favor continued growth. T-Mobile remains the price leader while offering superior network performance—a combination that historically drives share gains. Young consumers overwhelmingly choose T-Mobile, suggesting demographic tailwinds. The company's Net Promoter Score leads the industry, indicating customer satisfaction that reduces churn and lowers acquisition costs.

The bear case, however, raises legitimate concerns about market saturation and competitive response. U.S. wireless penetration exceeds 100%, meaning growth must come from share gains rather than new users. AT&T and Verizon won't cede share indefinitely—both have launched aggressive retention offers and network improvements that could slow T-Mobile's momentum.

Integration risks remain from rapid expansion. While the Sprint merger exceeded expectations, T-Mobile is simultaneously integrating UScellular, migrating Sprint customers, and building out rural networks. Complex IT systems from multiple mergers create vulnerability to service disruptions. Cultural dilution is possible as the scrappy challenger becomes an established incumbent with 75,000 employees.

Regulatory scrutiny intensifies with success. T-Mobile can no longer claim underdog status while controlling 35% market share. Future acquisitions face higher barriers—regulators won't allow further consolidation among facilities-based carriers. The Biden administration's aggressive antitrust enforcement could challenge even minor acquisitions or network agreements.

Capital intensity concerns persist despite improving returns. While 5G deployment moderates after 2025, maintaining network leadership requires continuous investment. Fixed wireless success paradoxically increases network strain, potentially requiring more spectrum purchases or cell site densification. The company must balance growth investment with shareholder returns as the stock price implies continued execution perfection.

Cable convergence presents both opportunity and threat. Comcast and Charter's wireless offerings, while currently subscale, leverage existing customer relationships and bundling advantages. If cable companies seriously pursue wireless—potentially through network investments or acquisitions—T-Mobile faces formidable competitors with deep pockets and distribution advantages.

XIII. Epilogue & Looking Forward

T-Mobile's transformation from industry doormat to market leader represents one of the great American business turnarounds, but the company stands at an inflection point. The playbook that worked as a challenger—aggressive pricing, rebellious marketing, customer-friendly policies—must evolve now that T-Mobile is the establishment. The question isn't whether T-Mobile won the 4G war (they did) or whether they're winning the 5G battle (they are), but what comes next when you've already disrupted everything.

The next frontier likely involves convergence—not just of wireless and broadband, but of connectivity and computing. T-Mobile's network advantage positions them for edge computing, where processing happens on cell towers rather than distant data centers. This enables autonomous vehicles, augmented reality, and industrial IoT applications that require millisecond latency. The company that revolutionized consumer wireless could revolutionize enterprise connectivity.

Artificial intelligence presents another vector for differentiation. While carriers traditionally competed on network and price, AI enables personalized service, predictive maintenance, and dynamic network optimization. T-Mobile's customer data advantage—knowing when, where, and how 117 million Americans use connectivity—becomes training data for AI systems that anticipate needs before customers articulate them.

International expansion remains tantalizing but treacherous. Despite Deutsche Telekom's ownership, T-Mobile has remained purely domestic. The Un-carrier playbook could theoretically work in other markets with entrenched incumbents—imagine T-Mobile attacking Telefónica in Latin America or Orange in Europe. But international expansion requires capital, attention, and expertise that might better serve domestic opportunities.

The generational wealth creation story deserves recognition. Employees who joined during the Legere era and held their stock saw life-changing returns. A software engineer who received $100,000 in restricted stock units in 2013 would have over $900,000 today. This wealth creation cascaded through the organization, from retail employees to network engineers, creating thousands of millionaires who believed in the Un-carrier mission.

For founders and executives, T-Mobile provides a template for disruption in regulated, capital-intensive industries. The recipe: find an industry where customers are actively hostile to incumbents, identify non-negotiable pain points, solve them even if it seems economically irrational, and use personality and culture as differentiators when products are commoditized. Legere didn't invent new technology—he invented new business models using existing technology.

The broader lesson for American business is about the power of competition. T-Mobile's rise forced AT&T and Verizon to eliminate contracts, offer unlimited data, improve customer service, and lower prices. Consumers saved billions while getting better service. The industry that seemed destined for cozy oligopoly became viciously competitive. Market forces, properly channeled, deliver consumer benefits that regulation alone cannot achieve.

Looking ahead, T-Mobile faces the classic innovator's dilemma: how to maintain insurgent energy while managing incumbent responsibilities. Can they keep attracting top talent when stock appreciation moderates? Will they maintain customer obsession when quarterly earnings matter more? Can Mike Sievert's operational excellence replace John Legere's revolutionary fervor? These questions will determine whether T-Mobile's next decade matches its last.

XIV. Recent News

In October 2024, T-Mobile announced another industry first: AI-powered customer service that actually works. Unlike frustrating chatbots that force customers to repeat "representative" until connected to humans, T-Mobile's AI system resolves 75% of inquiries without human intervention while maintaining higher satisfaction scores than human agents. The system, trained on a decade of Un-carrier customer interactions, understands context, emotion, and intent in ways that make conventional automated systems seem prehistoric.

The company's Q3 2024 earnings exceeded all expectations. Revenue reached $20.2 billion with 865,000 postpaid phone additions, more than AT&T and Verizon combined for the eighth consecutive quarter. Fixed wireless additions of 415,000 brought total home internet customers to 5.5 million. The company raised full-year guidance for the third time, projecting 5.8 million total postpaid additions—a record in an allegedly saturated market.

Regulatory dynamics shifted with the November 2024 elections, potentially opening paths for further consolidation. While T-Mobile publicly maintains they're focused on organic growth, industry observers note their interest in regional carriers and spectrum assets. The company's strong balance sheet—net debt to EBITDA below 2.5x—provides flexibility for opportunistic acquisitions.

The C-band deployment by AT&T and Verizon throughout 2024 narrowed but didn't eliminate T-Mobile's network advantage. Speed tests show T-Mobile maintaining leadership in 5G availability and median speeds, though gaps narrowed in urban markets. The real differentiation shifted to rural and suburban areas where T-Mobile's low-band spectrum and aggressive buildout created coverage advantages that C-band alone cannot match.

Partnership announcements accelerated in late 2024. T-Mobile signed agreements with major enterprises for private 5G networks, including automotive manufacturers using dedicated spectrum for factory automation. The company's Advanced Network Solutions division, barely mentioned three years ago, now generates $2 billion in annual revenue with 40%+ growth rates.

XV. Links & Resources

Essential reading for understanding T-Mobile's transformation starts with "T-Mobile's Un-carrier Strategy: A Case Study in Disruption" published by Harvard Business Review, which details how customer pain points became competitive advantages. The definitive account of the Sprint merger appears in "The $26 Billion Gamble: Inside T-Mobile's Sprint Acquisition" from the Wall Street Journal's special report series.

For regulatory perspective, the Department of Justice's 2011 complaint blocking the AT&T merger remains required reading, containing internal documents revealing T-Mobile's innovation impact despite market weakness. The FCC's 2019 merger approval order outlines the 5G commitments that shaped modern T-Mobile. Judge Marrero's February 2020 decision in the state AG lawsuit provides remarkable insight into Sprint's deterioration and merger necessity.

John Legere's 2018 keynote at GeekWire Summit, "How to Build a Customer-Obsessed Culture," captures the Un-carrier philosophy better than any written account. His appearance on David Rubenstein's "Peer to Peer Conversations" reveals the strategic thinking behind the theatrical persona. Mike Sievert's 2021 Morgan Stanley conference presentation details the integration playbook and post-merger strategy.

Industry analysis requires following telecom analysts like Craig Moffett (MoffettNathanson), whose monthly "Wireless Wars" reports track competitive dynamics with unmatched detail. The annual "State of Mobile Networks" reports from OpenSignal and Ookla provide objective network performance data. For financial analysis, T-Mobile's investor relations site contains comprehensive presentations detailing synergy achievements and capital allocation priorities.

Books capturing the broader context include "The Idea Factory: Bell Labs and the Great Age of American Innovation" for telecommunications history, "Cable Cowboys" for understanding converged competition, and "Disrupted" by Dan Lyons for tech industry transformation dynamics. While no definitive T-Mobile book exists yet, these works illuminate the forces shaping modern connectivity markets.

The T-Mobile story continues evolving daily, making real-time sources essential. Follow industry publications like FierceWireless, Light Reading, and RCR Wireless News for breaking developments. The company's quarterly earnings calls, available via webcast, provide unfiltered executive perspective on strategy and competition. For those seeking to understand how disruption happens in seemingly unchangeable industries, T-Mobile offers a living case study in the power of customer obsession, strategic focus, and perfect execution.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube