Taylor Morrison Home Corporation: Building the American Dream

I. Introduction & Episode Roadmap

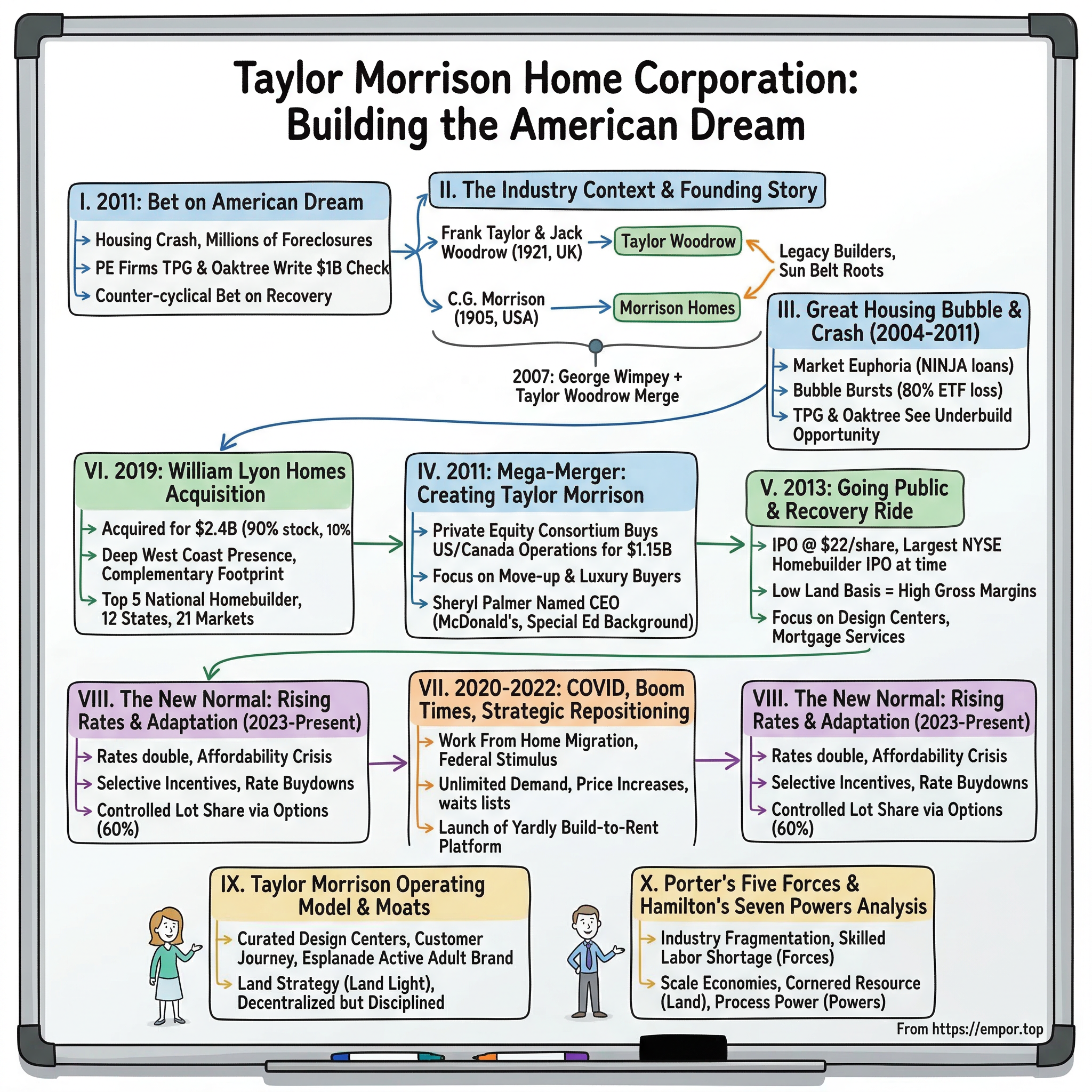

Picture this: it is 2011, and the American housing market is still a smoldering wreck. Millions of foreclosures have gutted neighborhoods from Phoenix to Orlando. Homebuilder stocks have cratered ninety percent from their peaks. Entire subdivisions sit half-finished, their model homes locked and their sales offices dark. And in the middle of this carnage, two private equity firms walk into a room and write a check for over a billion dollars to buy a pair of struggling homebuilders, merge them together, and bet that the American Dream of homeownership is not, in fact, dead.

That bet became Taylor Morrison Home Corporation.

Today, Taylor Morrison ranks among the top eight homebuilders in the United States, generating more than eight billion dollars in annual revenue, closing nearly thirteen thousand homes a year, and operating across twelve states and twenty-one markets. The company has been named America's Most Trusted Home Builder for an unprecedented ten consecutive years. Its chairman and CEO, Sheryl Palmer, is the first and only woman to lead a publicly traded homebuilder in the country. And the stock, which debuted at twenty-two dollars per share in 2013, has delivered returns that would make most growth investors jealous.

But this is not just a story about stock returns. This is a story about timing, courage, and the art of building a national company from the rubble of the worst housing crisis in American history. It is a story about two legacy builders with roots stretching back to 1905 and 1921, a transformative merger executed when nobody wanted to touch housing, a perfectly timed IPO, a bold acquisition completed literally weeks before a global pandemic, and an operating model that has proven remarkably resilient through wild cyclical swings.

The central question is deceptively simple: How did a pair of struggling regional homebuilders become a national powerhouse through what may be the boldest merger in homebuilding history? The answer involves British construction empires, Arizona desert booms, Korean War fighter pilots, a woman who started her career at McDonald's, and the most counter-cyclical private equity bet of the post-crisis era.

The thesis here is not complicated, but it is powerful: in a deeply cyclical, capital-intensive, fragmented industry, the winners are the ones who buy when others are selling, integrate what others cannot, and operate with discipline when the temptation is to swing for the fences. Taylor Morrison did all three. Whether they can keep doing it is the question that matters now.

II. The Homebuilding Industry Context & Founding Story

Before diving into Taylor Morrison's specific journey, it is worth understanding the industry they operate in, because homebuilding is unlike almost any other business in America.

Think of it this way: a homebuilder is simultaneously a real estate developer, a manufacturer, a retailer, a financial services company, and a construction firm. They buy raw land years before a single customer walks through a door. They navigate byzantine local zoning and permitting processes that can take years. They manage hundreds of subcontractor relationships for everything from concrete foundations to kitchen cabinets. They sell a product that costs six hundred thousand dollars on average, where the customer's ability to buy depends entirely on interest rates set by the Federal Reserve.

And they do all of this in an industry that is so cyclical it makes semiconductor companies look stable. When times are good, homebuilders print money. When times are bad, they can lose everything. The reason is that the industry requires enormous upfront capital commitments, buying land, developing infrastructure, building model homes, all before a single revenue dollar is collected. If demand disappears, as it did in 2008, builders are left holding depreciating assets financed with debt that does not depreciate.

The fragmentation of the industry is equally important context. Even today, the top ten homebuilders in America account for less than forty percent of total new home sales. The rest is split among thousands of regional and local builders, many of whom operate in just one or two markets. This fragmentation creates both opportunity and challenge for scale players like Taylor Morrison: opportunity because there is plenty of room to grow share through organic expansion and acquisitions, but challenge because local competitors often have deeper community relationships and lower overhead.

The American homebuilding industry as we know it was born from the post-World War II suburban explosion. When sixteen million veterans returned home and the GI Bill made mortgages accessible, developers like William Levitt pioneered the concept of mass-produced, affordable suburban housing. Levittown on Long Island became the template: buy farmland cheap, standardize designs, build at scale, and sell the American Dream for less than eight thousand dollars a house. By the 1960s and 1970s, production homebuilding had become a real industry, with regional players dominating local markets and a handful of ambitious firms beginning to think nationally.

This is where Taylor Morrison's origin story splits into two threads that would not converge for decades.

The first thread begins in Blackpool, England, in 1921, when Frank Taylor and Jack Woodrow built their first pair of semi-detached houses at 347 and 349 Central Drive. Taylor Woodrow, as the company became known, went public by 1935 and grew into one of Britain's largest construction and development firms. By the 1960s, Taylor Woodrow was looking overseas, entering the Canadian market through the acquisition of Monarch Development Corporation and pushing into the United States. During the 1970s and 1980s, the company found particular success building housing developments in Florida and California, including the award-winning 3,500-home Meadows development in Florida. By the late 1970s, overseas profits accounted for two-thirds of group earnings.

The second thread starts even earlier, in 1905, when C.G. Morrison founded Morrison Homes in Seattle. The company relocated to Northern California in 1946 and grew into a major regional builder, eventually extending operations across Phoenix, Sacramento, Denver, multiple Florida markets, Reno, and several Texas cities. In 1984, George Wimpey Plc, another major British homebuilder, acquired Morrison Homes. So by the mid-1980s, both of the companies that would eventually form Taylor Morrison were owned by competing British construction conglomerates, building homes across the American Sun Belt without any idea their fates were intertwined.

The convergence began on July 6, 2007, when George Wimpey and Taylor Woodrow completed a nil-premium merger valued at approximately six billion pounds, forming Taylor Wimpey Plc. The timing could hardly have been worse. The merger created one of the world's largest homebuilding companies just as the American housing market was about to experience its most devastating collapse since the Great Depression. The US subsidiaries, Morrison Homes Inc. and Taylor Woodrow Inc., initially continued operating under their existing brands before being consolidated under a new name in 2008: Taylor Morrison.

A British empire merger, executed at the absolute peak of the housing bubble, combining two American builders that had been rivals for decades. What could possibly go wrong? As it turned out, almost everything.

What makes this founding history so instructive for investors is that Taylor Morrison did not spring from a single visionary founder with a grand plan. It was assembled from the wreckage of two corporate genealogies, each stretching back over a century, each shaped by the particular rhythms of British construction capital seeking returns in the American Sun Belt. The brands, the land, the teams, the customer relationships, all of that institutional knowledge accumulated over decades would prove to be the raw material from which something genuinely new would eventually be forged. But first, the industry had to go through the most painful reckoning in its history.

III. The Great Housing Bubble & Crash (2004-2011)

To understand what happened next, rewind to 2005. The American housing market was in full euphoria. Home prices had doubled in many markets over just five years. Mortgage lenders were handing out loans to anyone with a pulse, and sometimes to people without one. The now-infamous "NINJA" loans, requiring no income, no job, and no assets, had become commonplace. Homebuilder stocks were trading at valuations that assumed housing prices would rise forever. And builders were acquiring land at frantic prices, leveraging their balance sheets to secure lot positions that would take years to develop.

The logic seemed bulletproof: land is finite, population is growing, and Americans will always want bigger houses in sunnier places. But the problem, as Michael Lewis documented brilliantly in "The Big Short," was that the entire edifice rested on a foundation of fraudulent lending, mis-rated securities, and the collective delusion that national home prices could never decline simultaneously.

The mechanics of how homebuilders got caught are worth understanding because they explain the industry dynamics that still shape Taylor Morrison today. During the boom, builders competed furiously for land, often bidding up prices for raw parcels that would take three to five years to develop into finished lots ready for construction. They financed these land purchases with debt, creating a leverage cycle where rising home prices justified higher land prices, which justified more borrowing. The assumption embedded in every land deal was that home prices would continue rising, or at least remain stable, long enough for the builder to develop and sell the lots at a profit.

When prices reversed, the math collapsed. Land purchased at peak prices was suddenly worth a fraction of what the builder had paid. The debt used to acquire it did not shrink. And the buyers who were supposed to purchase the homes being built on that land were evaporating as the mortgage market froze. Builders found themselves in a death spiral: they had to sell homes at discounted prices to generate cash to service debt on land that was no longer worth what they owed on it.

When the bubble burst in 2007 and 2008, it hit homebuilders harder than almost any other industry in America. Consider the scale of destruction: from peak to trough, the S&P Homebuilders ETF lost roughly eighty percent of its value. Housing starts, which had peaked at over 2.2 million annually in 2005, plummeted to under 500,000 by 2009, the lowest level since records began in the 1950s. Major builders wrote off billions in land values. Some, like Tousa and Levitt and Sons, went bankrupt. Others survived only by slashing workforces, walking away from land contracts, and raising desperate rounds of capital.

The newly formed Taylor Wimpey was not immune. Its American operations, now branded Taylor Morrison, were hemorrhaging cash. The parent company's stock cratered. The beautiful land positions acquired during the boom years were now worth fractions of their purchase prices. Master-planned communities that were supposed to sell out over five years suddenly had no buyers. The company had to write down hundreds of millions in land values and dramatically shrink its operations.

But here is where the story gets interesting. While most of the market was running away from housing, a handful of sophisticated investors were doing the opposite. They were studying the demographics, the supply destruction, and the mathematical inevitability that America would eventually need to build houses again. And they were doing the hardest thing in investing: buying when there was blood in the streets.

The two firms that saw the opportunity most clearly were TPG Capital and Oaktree Capital Management. TPG, founded by David Bonderman and Jim Coulter, was one of the world's largest private equity firms with a reputation for bold, contrarian bets. Oaktree, founded by Howard Marks, was the premier distressed-debt investor in the world, famous for Marks's memos about market cycles and the importance of buying when others are fearful. Together, they formed a thesis that was elegant in its simplicity: American housing had overbuilt during the bubble, but the subsequent crash had created an even more severe underbuild. Population growth had not stopped. Household formation had not stopped. The country was going to need millions of new homes, and the builders who survived with clean balance sheets and good land positions would be extraordinarily well-positioned when demand recovered.

The question was not whether housing would recover. The question was when, and who would be in the best position to benefit. TPG and Oaktree believed they had found the answer in Taylor Wimpey's struggling North American operations. A distressed British parent company needed to sell. The American assets included established brands, experienced teams, and land positions acquired over decades in some of the fastest-growing markets in the country. And the price? In a word: cheap.

Howard Marks himself had written extensively about this kind of opportunity. In his famous memo "The Most Important Thing," he argued that the best investments are found in assets that everyone else has abandoned, where the price has fallen so far that even a modest recovery produces outsized returns. The Taylor Wimpey North American operations fit this framework perfectly: a motivated seller, a deeply depressed asset class, experienced management teams still in place, and a demographic inevitability that would eventually drive recovery.

The thesis was not just about buying cheap, though. It was about creating something that had not existed before: a professionally managed, well-capitalized national homebuilding platform that could grow through the recovery while competitors were still licking their wounds. TPG brought expertise in operational improvement and scaling businesses. Oaktree brought discipline around downside protection and the patience to hold through a multi-year recovery. Together, they saw an opportunity to not just buy a distressed asset but to build a genuine franchise.

By early 2011, with housing starts still near historic lows and most investors still treating homebuilders like radioactive waste, the deal began to take shape. It would prove to be one of the most well-timed private equity investments of the decade.

IV. The Mega-Merger: Creating Taylor Morrison (2011)

On March 31, 2011, Taylor Wimpey announced it was selling its entire North American homebuilding operation. The buyer was a consortium led by TPG Capital, Oaktree Capital Management, and JH Investments, a Canadian investment vehicle.

The purchase price was approximately $1.15 billion for the combined US and Canadian operations, with roughly $955 million attributed to the US business alone. The acquisition vehicle was TMM Holdings Limited Partnership, formed specifically for the transaction. The deal closed on July 13, 2011.

To appreciate how bold this was, consider the context. In the first quarter of 2011, US housing starts were running at an annualized pace of roughly 550,000, barely a quarter of the peak level. Home prices in markets like Phoenix and Las Vegas were still falling. The National Association of Home Builders' confidence index was mired in the twenties, deep in pessimistic territory. Unemployment was still above nine percent nationally and much higher in construction-heavy markets. Buying a homebuilder at this moment was roughly as popular as buying airline stocks on September 12, 2001.

But the consortium saw what others missed.

The assets they were acquiring included operations in Arizona, California, Colorado, Florida, and Texas, which collectively represented the highest-growth demographic corridors in the country. These were not random markets. They were the destinations of the Great American Migration, the long-term population shift from the industrial Midwest and expensive Northeast toward the Sun Belt and Mountain West, driven by lower taxes, warmer weather, cheaper housing, and expanding job markets. This migration had been underway for decades and would only accelerate in the years ahead.

The teams were experienced. Many of the division presidents and operational leaders had been building homes in their markets for decades and had relationships with land sellers, subcontractors, and municipal officials that simply could not be replicated by a new entrant. The land positions, while impaired on a mark-to-market basis, had been acquired over decades and included some of the most desirable locations in their respective markets. And the purchase price, barely above the liquidation value of the land alone, meant the downside was limited while the upside, if housing recovered, was enormous.

The acquisition vehicle was TMM Holdings Limited Partnership, which became the indirect parent of Taylor Morrison Communities, Inc.

The structure gave TPG and Oaktree significant governance rights while preserving the operational independence that homebuilding requires. This is an important nuance that many private equity investors get wrong in the homebuilding industry. Homebuilding is fundamentally a local business. The division president in Orlando knows which land sellers are trustworthy, which subcontractors deliver quality work on time, and which municipal officials can expedite permitting. These relationships take years to build and cannot be imposed from a private equity firm's headquarters in San Francisco or New York. The best PE-backed homebuilders succeed because the financial sponsors provide capital, strategic guidance, and performance accountability while allowing local operators to run their businesses with significant autonomy.

Now here is the part of the story that does not get enough attention: the leadership decision. When the private equity consortium took over, they needed someone to run the combined operation. They found their answer in Sheryl Palmer, who had already been leading the Morrison side of the business since 2007.

Palmer's background is one of the more unconventional paths to a homebuilder CEO suite. She studied special education in college, a discipline that taught her patience, empathy, and the ability to communicate complex ideas simply, skills that would prove surprisingly relevant in leading a customer-facing homebuilding operation. She started her professional career in sales and marketing at McDonald's, hardly the typical resume for someone who would eventually run a company generating eight billion dollars in annual revenue.

But Palmer pivoted into real estate and spent decades building expertise across every function in homebuilding: land acquisition, sales, marketing, development, and operations. She served as division president at Blackhawk Corporation for ten years, building active adult communities in Northern California. This experience with the fifty-five-plus buyer segment would later inform Taylor Morrison's Esplanade brand strategy. She then became Nevada Area President for Pulte and Del Webb, two of the largest national homebuilders, where she gained experience managing operations at scale in one of the most volatile housing markets in the country.

Palmer joined Morrison Homes in 2006, just as the housing market was peaking. The timing was terrible in one sense: she walked into a buzzsaw. But it also meant she was battle-tested. She arrived during the Taylor Woodrow-George Wimpey merger discussions, and approximately thirty days after that merger completed in July 2007, she was asked to become CEO. Her first years leading the company were spent navigating the worst housing downturn in modern history, cutting costs, preserving land positions, and keeping the team together through layoffs and uncertainty.

When TPG and Oaktree acquired the business in 2011, they recognized what they had in Palmer: a leader who had already proven she could operate through a crisis, who understood the customer (particularly the move-up and luxury segments where margins were richest), and who had the operational chops to integrate two distinct organizations. Palmer would go on to become chairman, president, and CEO of the public company, and today remains one of the longest-tenured CEOs in the homebuilding industry.

The naming choice itself tells a story. The new entity kept the Taylor Morrison brand that had been created in 2008 when the US operations were consolidated. It honored both heritage companies, Taylor Woodrow and Morrison Homes, while signaling a fresh start. The Canadian operations under the Monarch brand were eventually separated, keeping the focus squarely on the US market.

The early post-merger execution focused on three priorities: rationalizing the footprint to concentrate on the highest-return markets, extracting cost synergies from combining back-office functions and purchasing, and selectively acquiring land at what were still deeply distressed prices. The company also made a critical strategic choice that would define its identity for years to come: it would focus on move-up and luxury buyers rather than competing in the entry-level segment where margins were thinnest and competition was fiercest.

This was the inflection point. Before July 2011, there were two struggling regional builders owned by a distressed British parent. After July 2011, there was Taylor Morrison: a privately held, well-capitalized national platform backed by two of the smartest money managers in the world, led by a CEO who had already proven she could navigate a crisis, and positioned in the fastest-growing markets in America at the bottom of the cycle. The only question was how long it would take for the market to recognize what they had built.

What is particularly striking about the 2011 deal in retrospect is how few people were willing to make this bet. The private equity world was largely focused on technology, healthcare, and energy. Housing was considered untouchable. The media narrative was dominated by foreclosure horror stories and predictions that the American homeownership model was permanently broken. Millennials, the generation that would eventually become the largest group of homebuyers in history, were being written off as a generation of permanent renters. None of these narratives proved correct, but they created the fear that made the acquisition possible at the price the consortium paid.

For investors, the Taylor Morrison creation story illustrates a principle that sounds simple but is extraordinarily difficult to execute: the best time to buy cyclical assets is when the cycle is at its worst, and the best assets to buy are those with irreplaceable local advantages that will compound in value as the market recovers. The consortium bought land positions, brands, teams, and customer relationships that had taken decades to build, at a fraction of replacement cost. Everything that followed was built on that foundation.

The answer: less than two years.

V. Going Public & The Housing Recovery Ride (2013-2016)

On April 10, 2013, Taylor Morrison Home Corporation priced its initial public offering at twenty-two dollars per share, the high end of the expected range. The offering was upsized due to overwhelming demand, with approximately 32.8 million shares of Class A common stock sold. Credit Suisse and Citi served as lead managers on the deal.

The IPO generated roughly $680 million in net proceeds, making it the largest homebuilding IPO in the history of the New York Stock Exchange at the time. The stock closed up about six percent on its first day of trading under the ticker symbol TMHC.

The timing was exquisite, and not by accident. TPG and Oaktree had spent two years building the business, stabilizing operations, and positioning the company for exactly this moment.

By early 2013, the housing recovery was just beginning to gain traction. Housing starts had climbed back above 900,000 annually, still far below the long-term equilibrium of about 1.5 million, but the trajectory was unmistakably upward. Home prices were rising again in most major markets. And critically, the inventory of existing homes for sale had tightened dramatically, creating a window for new construction that had not existed in years.

Taylor Morrison entered the public markets with several advantages that were direct consequences of the 2011 acquisition. First, the land. Because TPG and Oaktree had bought at the bottom, Taylor Morrison's land basis was extraordinarily low. Lots that might have been worth $100,000 at the 2006 peak and $30,000 at the 2010 trough were now appreciating rapidly as the recovery took hold. This meant the company could sell homes at market prices while enjoying gross margins that reflected land costs from the crisis era, a formula that produced exceptional profitability.

Second, the balance sheet. Unlike many competitors that had emerged from the crisis burdened with debt, Taylor Morrison had been recapitalized by its private equity sponsors. The company had what the industry calls a "fortress balance sheet," with manageable leverage, ample liquidity, and the financial flexibility to acquire land and grow communities without stretching.

Third, the geographic footprint. The company's operations were concentrated in precisely the markets that were recovering fastest: Arizona, Florida, Texas, Colorado, and California. These Sun Belt and growth markets benefited disproportionately from domestic migration patterns, favorable demographics, and job growth that outpaced the national average.

The post-IPO years from 2013 through 2016 were a period of steady, disciplined growth. Taylor Morrison expanded its community count, pushed into new submarkets within its existing geographies, and began establishing a presence in the Carolinas. Revenue grew meaningfully each year as the company delivered more homes at higher average selling prices.

The move-up and luxury positioning proved to be a significant competitive advantage during this period. While entry-level builders competed fiercely on price and struggled with thin margins, Taylor Morrison was selling to buyers who were less rate-sensitive, had more equity from their existing homes, and were willing to pay premiums for design, location, and personalization. The company invested heavily in design centers, those elaborate showrooms where buyers choose their finishes, fixtures, and upgrades. Option and upgrade revenue became a meaningful profit center, effectively allowing the company to earn additional margin on top of the base home price.

Operationally, the company focused on the blocking and tackling that separates good homebuilders from great ones: reducing cycle times from contract to close, standardizing specifications to reduce construction costs, negotiating national purchasing agreements for materials and appliances, and building a culture of accountability at the division level while maintaining centralized financial discipline. These are not glamorous initiatives, but in an industry where the difference between a twenty percent gross margin and a twenty-four percent gross margin can mean hundreds of millions of dollars in annual profit, they are the difference between being a mediocre builder and a market leader.

The financial services segment, which provides mortgage financing, title insurance, and closing services through Taylor Morrison's captive operations, also became an increasingly important contributor during this period. Controlling the mortgage process allowed the company to offer buyers a streamlined experience, reduce fall-through rates from third-party lending delays, and capture additional revenue from each transaction. This vertical integration into financial services is common among the largest builders, including competitors like PulteGroup and Lennar, and represents a meaningful competitive advantage over smaller builders who must rely entirely on third-party lenders.

By 2016, Taylor Morrison had firmly established itself as a top-ten national homebuilder. The private equity sponsors had begun selling down their positions through secondary offerings, realizing substantial returns on their 2011 investment. The company had proven that the counter-cyclical thesis was correct: buying at the bottom, executing through the recovery, and going public at the right moment had created billions of dollars in value. But Palmer and her team were not content to simply ride the recovery wave. They were already thinking about the next move that would transform the company's scale and competitive position.

VI. The William Lyon Homes Acquisition: Going Bigger (2019)

In a conference room somewhere in Scottsdale, Arizona, in the fall of 2019, Sheryl Palmer and her team were studying a target that would represent the company's most ambitious move since its own creation. William Lyon Homes was a West Coast-focused homebuilder with a remarkable history of its own and a geographic footprint that complemented Taylor Morrison's almost perfectly.

William Lyon founded his residential construction firm in 1956 after serving as a US Air Force pilot in the Korean War. Lyon grew up in Los Angeles, attended USC (which he left at age twenty-three), and built his namesake company into one of the largest homebuilders in the Western United States. He was not just a builder; Lyon also served as Chief of the Air Force Reserve from 1975 under both the Ford and Carter administrations. By the time Taylor Morrison came calling, William Lyon Homes and its joint ventures had sold over 73,000 homes, operating primarily in California, Arizona, Nevada, Colorado, Oregon, and Washington.

On November 6, 2019, Taylor Morrison announced it would acquire William Lyon Homes in a deal valued at approximately $2.4 billion, including the assumption of debt. The transaction was structured as roughly ninety percent stock and ten percent cash, with William Lyon shareholders receiving $2.50 in cash plus 0.800 shares of Taylor Morrison common stock per share.

The deal valued William Lyon at approximately 1.1 times book value, a reasonable price that reflected the premium the market placed on West Coast land positions. In homebuilding, book value is an especially meaningful metric because the balance sheet is dominated by tangible assets: land, homes under construction, and finished inventory. A price-to-book of 1.1 times suggested the market was assigning modest value to the franchise beyond its hard assets, leaving upside for the acquirer if integration went well.

The strategic logic was compelling on multiple dimensions. California was the largest housing market in the country by dollar volume, and William Lyon had deep relationships, entitled land positions, and decades of operational expertise across the state. The acquisition would give Taylor Morrison immediate scale in California, Oregon, Washington, and Nevada while strengthening its existing presence in Arizona and Colorado. The combined entity would have approximately 430 active selling communities and a pipeline of roughly 80,000 owned and controlled lots. Management projected about $80 million in annualized cost synergies from eliminating duplicate overhead, leveraging national purchasing, and optimizing back-office functions.

On January 30, 2020, shareholders of both companies approved the merger. The deal closed on February 6, 2020. Taylor Morrison was now solidly positioned as one of the top five homebuilders nationally, with a presence in twelve states and the most diversified geographic footprint of any builder in its size range.

But the timing introduced a wild complication that nobody saw coming. Less than six weeks after the acquisition closed, the World Health Organization declared COVID-19 a global pandemic. By mid-March 2020, construction sites across the country were shutting down, model homes were closing their doors, and the economy was entering what felt like freefall. Taylor Morrison had just completed its largest-ever acquisition and now had to integrate two organizations while simultaneously navigating an unprecedented public health crisis.

The integration challenge was formidable even without a pandemic. Merging homebuilders is notoriously difficult because the business is so local. Each division has its own land pipeline, subcontractor relationships, design standards, and sales processes. Cultures can clash. Key people can leave. And the distraction of integration can cause operational execution to slip at precisely the moment when the market demands focused attention.

Palmer and her team executed the integration largely by keeping what worked and changing only what was necessary. Division presidents in legacy William Lyon markets retained significant autonomy. National purchasing agreements were consolidated to capture synergies. Back-office functions were centralized. But the local teams, the people who knew the land sellers, the subcontractors, and the permitting officials, were largely preserved. This approach reflected a core philosophy: homebuilding is a local business that benefits from national scale, not a national business that happens to have local operations.

The cultural fit between the two companies helped enormously. Both Taylor Morrison and William Lyon positioned themselves in the move-up and luxury segments. Both valued design and customer experience. Both had long histories and professional management cultures. This was not a case of a volume builder swallowing a custom builder, or an entry-level player trying to move upmarket. It was two like-minded organizations combining to create something larger than either could have been alone.

Within twelve months of closing, the company had captured most of the projected synergies, retained the vast majority of key employees, and maintained operational momentum despite the pandemic.

The financial impact was transformative. The combined entity now had the scale to negotiate better terms with national suppliers, the geographic diversification to smooth out regional market volatility, and the community count to attract more attention from equity analysts and institutional investors. The workforce grew to more than three thousand team members. The lot pipeline expanded to give the company years of development runway across its expanded footprint.

For investors evaluating the William Lyon deal, the key lesson is about strategic fit versus financial engineering. Many homebuilder acquisitions fail because the buyer is primarily seeking financial synergies, cost cuts that look good in a spreadsheet but do not translate to the field. Taylor Morrison's approach was different: the deal was driven by geographic and customer segment complementarity, with cost synergies as a secondary benefit. William Lyon's West Coast expertise and land positions were genuinely additive to Taylor Morrison's existing capabilities, not redundant. This distinction between value creation through strategic combination and value extraction through cost-cutting is what separated this deal from the many homebuilder mergers that have destroyed value over the years.

The acquisition would prove to be yet another example of Taylor Morrison's ability to time major moves well and execute them competently, a capability that has become one of the company's defining characteristics.

VII. COVID, Boom Times, and Strategic Repositioning (2020-2022)

The scene in March 2020 was surreal for anyone in the homebuilding industry. One week, sales offices were buzzing with traffic from the spring selling season. The next week, they were locked, their parking lots empty, construction sites idle. Palmer convened daily crisis calls with division presidents across the country. The company had just absorbed thousands of new employees from the William Lyon acquisition. Nobody knew if buyers would cancel contracts en masse, whether construction could continue, or how long the shutdown would last.

Then something remarkable happened. After a brief period of panic, the American housing market did not collapse. It exploded.

The combination of factors that drove the 2020-2022 housing boom was unlike anything the industry had ever seen.

First, the Federal Reserve slashed interest rates to near zero, pushing thirty-year mortgage rates below three percent for the first time in history. To put that in perspective, a buyer purchasing a $500,000 home at a three percent rate pays roughly $2,100 per month in principal and interest. At seven percent, that same home costs $3,300 per month, a fifty percent increase in monthly payment for the identical house. Rates at three percent made homes that had been unaffordable suddenly accessible to millions of buyers.

Second, the federal government pumped trillions in stimulus into the economy, including direct payments to households, enhanced unemployment benefits, and small business support that collectively boosted personal savings rates to historic highs. Suddenly, millions of Americans had the down payment they had been struggling to accumulate.

Third, and perhaps most importantly, the sudden shift to remote work triggered a massive migration from expensive urban apartments to suburban and exurban homes, with millions of Americans simultaneously deciding they needed more space, a home office, and a backyard. The pandemic did not create new housing demand so much as it pulled forward years of demand into a compressed window.

For homebuilders, it was like someone turned on a fire hose of demand. Taylor Morrison, newly enlarged by the William Lyon acquisition and sitting on a massive lot pipeline, was positioned to capture an outsized share of this demand. The company accelerated community openings, ramped up starts, and watched as absorption rates, the number of homes sold per community per month, soared to levels that veterans of the industry had never seen.

The gross margin story during this period was extraordinary.

When demand dramatically outstrips supply, builders gain pricing power. In a normal market, a builder might raise base prices by one or two percent per quarter and offer incentives like closing cost assistance or design center credits to keep traffic flowing. During 2021, Taylor Morrison, like its peers, was raising prices multiple times per month in many communities. The company would increase a home's base price by five, ten, or even fifteen thousand dollars between one buyer's contract and the next. Waiting lists formed. Lotteries were used to allocate limited inventory. Incentives disappeared entirely, an almost unheard-of situation in an industry where some form of buyer incentive is nearly always part of the transaction.

The result was a gross margin expansion that flowed directly to the bottom line, transforming the company's profitability from solid to spectacular.

But here is where Palmer's discipline and experience showed. While some competitors were buying land at frenzied prices, rushing to lock up every available lot to feed the demand machine, Taylor Morrison maintained its underwriting standards. The company continued to evaluate land deals using return thresholds that assumed normalized pricing and absorption, not the fever-dream metrics that the boom market was producing. This discipline would prove critical when the market eventually turned.

The company also began an important strategic shift in how it built homes. Historically, Taylor Morrison had been heavily weighted toward built-to-order construction, where a buyer selects a lot, chooses a floor plan, picks options, and waits several months for the home to be completed. During the boom, the company shifted more aggressively toward speculative, or "spec," construction, where homes are started before a buyer is identified. This was partly a response to market conditions, as demand was so strong that spec homes were selling before the drywall was finished, but it also reflected a longer-term strategic evolution toward faster inventory turns and more efficient capital deployment.

The digital transformation that COVID forced upon the industry also became a lasting competitive advantage. Virtual tours, online sales appointments, digital mortgage applications, and remote closings went from emergency measures to standard operating procedures. Taylor Morrison invested in its digital sales platform, recognizing that today's buyer, particularly the millennial move-up buyer who was becoming an increasingly important customer, expected a seamless digital experience.

By mid-2022, the company had delivered revenue of approximately $8.2 billion, with gross margins that were among the highest in its history. But the leadership team was already preparing for the next phase. The Federal Reserve had begun raising interest rates aggressively to combat inflation, and mortgage rates were climbing rapidly from their historic lows. The question was no longer how to handle unlimited demand. The question was how to prepare for a market that was about to get much more challenging.

The company also invested in its financial services arm during this period, expanding mortgage origination capacity and title services to handle the increased volume. Having a captive mortgage operation proved particularly valuable during the boom, as it allowed Taylor Morrison to control the lending process at a time when third-party lenders were overwhelmed with refinancing activity and struggling to process new purchase loans in a timely manner. Buyers who used the in-house lender had faster, more predictable closings, which reduced the cycle time from contract to close and improved customer satisfaction scores.

Revenue for fiscal 2022 reached approximately $8.2 billion, with gross margins near the highest levels in the company's history as a public entity. The combination of pricing power, low land costs on older vintage lots, and operational leverage from the enlarged platform produced earnings that demonstrated what Taylor Morrison could achieve in a favorable market. But Palmer, who had lived through the 2007-2011 crash as a homebuilder CEO, understood that boom markets do not last. The discipline she and her team maintained during the euphoria, continuing to underwrite land deals at normalized return assumptions rather than peak-market projections, would prove to be one of the most important decisions of her tenure.

In November 2022, the company unveiled a new brand: Yardly, a build-to-rent platform specializing in cottage-style, single-story rental homes with private backyards. This was not a reactive move but a strategic bet on a secular trend. As homeownership affordability deteriorated, the rental market for single-family-quality living was growing rapidly. Yardly represented Taylor Morrison's effort to capture demand that was being priced out of the for-sale market while deploying capital into a complementary business line with different risk characteristics.

VIII. The New Normal: Rising Rates & Adaptation (2023-Present)

The speed of the rate shock was stunning. In January 2022, the average thirty-year fixed mortgage rate was roughly three percent. By October 2022, it had more than doubled to over seven percent. This was the fastest increase in mortgage rates in over four decades, and its impact on housing affordability was devastating.

For a buyer purchasing a $600,000 home with twenty percent down, a three percent rate meant monthly principal and interest payments of about $2,023. At seven percent, that same loan payment jumped to roughly $3,194, an increase of nearly $1,200 per month, or over $14,000 per year. Put differently, a buyer who qualified for a $600,000 home at three percent could only afford roughly $430,000 at seven percent with the same monthly payment. Millions of potential buyers were effectively priced out of the market overnight, not because homes had become more expensive in nominal terms, but because the cost of financing them had exploded.

The impact on homebuilder operations was immediate and dramatic. Net new orders dropped sharply. Cancellation rates spiked as buyers who had locked in contracts at lower rates either could not qualify for new financing or simply got cold feet. Traffic through model homes thinned. The euphoria of 2021 gave way to the hard reality of affordability math that no longer worked for many buyers.

Taylor Morrison's response revealed the operational flexibility that comes from nearly two decades of experience navigating cycles. The company deployed a toolkit that included mortgage rate buydowns, where the builder effectively pays to reduce the buyer's interest rate for the first few years of the loan, closing cost assistance, design center credits, and selective price adjustments. The key word is "selective." Rather than slashing prices across the board, which would have destroyed margins and undermined the value of homes already sold, the company targeted incentives at specific communities and buyer segments where the math needed a nudge to work.

The land strategy advantage that had been built through years of disciplined underwriting now paid dividends. Because Taylor Morrison had not overpaid for land during the boom, the company's cost basis remained manageable even as selling prices moderated. Competitors who had chased land at peak prices found themselves squeezed between declining revenue and elevated costs, a painful combination that forced some to take impairments.

The company also made strategic choices about where to invest. Rather than maintaining exposure across every submarket equally, Taylor Morrison leaned into its strongest geographies, markets where job growth, population inflows, and supply-demand dynamics were most favorable. The company pulled back from fringe or tertiary locations where affordability pressures were most acute and competition from entry-level builders was fiercest.

By 2023, the company delivered revenue of $7.4 billion, down roughly ten percent from the prior year's peak, with adjusted home closings gross margins of twenty-four percent. That margin figure is worth pausing on. In a year when mortgage rates more than doubled and the industry was in the grips of the sharpest affordability crisis in a generation, Taylor Morrison maintained gross margins that would have been considered excellent in any normal year. This is the benefit of the move-up and luxury positioning: buyers in these segments tend to have more equity, higher incomes, and greater financial flexibility than entry-level purchasers.

The recovery in 2024 was meaningful. Revenue climbed back to $8.2 billion, with nearly 12,900 homes closed at an average price of roughly $600,000. Adjusted gross margins ticked up to 24.5 percent. The company repurchased 5.6 million shares, returning capital to shareholders while maintaining balance sheet strength. Community count expanded to 339 outlets.

The 2025 fiscal year, which recently concluded, told a more nuanced story. Revenue came in at $8.1 billion, essentially flat with the prior year, on approximately 13,000 closings. But gross margins compressed to roughly twenty-three percent, reflecting a heavier speculative home mix, rising input costs, and localized market softness. Average selling prices edged down to $597,000. The company guided for community count expansion to 365-370 outlets by year-end 2026, signaling confidence in the medium-term demand trajectory even as near-term conditions remain challenging.

The regional breakdown of the business tells an important story about diversification. In fiscal 2025, the West segment, which includes California, Arizona, Nevada, Colorado, Oregon, and Washington, contributed thirty-two percent of closings and thirty-nine percent of revenue, reflecting higher average selling prices on the West Coast. The Central segment, covering Texas, contributed twenty-six percent of closings and twenty-two percent of revenue. The East segment, encompassing Florida, Georgia, North Carolina, Illinois, and Indiana, delivered forty-two percent of closings and thirty-nine percent of revenue. This three-segment balance means that weakness in any single market or region is unlikely to derail the company's overall performance, a significant improvement from the pre-acquisition days when geographic concentration was a material risk.

A transformative move in the capital-light strategy came through in 2025. The company's controlled lot share through options reached sixty percent of total lots, up from just twenty-three percent in 2019. This shift, which mirrors the approach pioneered by NVR, means Taylor Morrison is tying up far less capital in raw land and instead paying for options that give it the right, but not the obligation, to purchase finished lots. If the market turns down sharply, the company can walk away from option deposits rather than being stuck holding land that is declining in value. This is a fundamental de-risking of the business model, though it comes at the cost of somewhat lower margins on individual homes since the lot developer needs their profit too.

The Yardly build-to-rent platform has also scaled meaningfully. By 2025, the platform had expanded to over thirty-five communities across nine markets, with fifteen actively leasing and over twenty under development. In July 2025, Taylor Morrison secured a three-billion-dollar off-balance-sheet financing facility with Kennedy Lewis Investment Management to fund Yardly's growth. The company sold its first two stabilized Yardly communities in the fourth quarter of 2025, releasing $140 million in capital. This is a significant strategic hedge: if for-sale housing demand weakens, the build-to-rent channel provides an alternative outlet for the company's construction capacity.

IX. The Taylor Morrison Operating Model & Competitive Moats

Walk into a Taylor Morrison design center in Scottsdale or Orlando, and you will understand something about the company's operating model that does not show up in the financials. These are not the sterile, fluorescent-lit showrooms of a volume builder. They are curated experiences, more like high-end retail than construction.

Buyers sit with designers, browse material samples arranged by palette and lifestyle theme, visualize their kitchen in three dimensions on large-screen displays, and select from dozens of options and upgrades, everything from quartz countertop patterns to smart home packages to expanded outdoor living spaces. Each upgrade generates incremental revenue at margins that are typically higher than the base home itself. A buyer who walks in planning to spend $550,000 on a base home might walk out having committed to $620,000 after selecting premium flooring, upgraded appliances, an extended covered patio, and a whole-home water filtration system. That seventy-thousand-dollar spread is overwhelmingly margin-accretive for the builder.

This design center experience is a microcosm of the broader operating philosophy. Taylor Morrison does not try to be the cheapest builder. It tries to be the builder that creates the most value for buyers who can afford to be selective. This shows up in every aspect of the business model.

The build-to-order versus spec balance is one of the most important operational levers in homebuilding, and understanding it is essential for evaluating any homebuilder.

A built-to-order, or BTO, home is one where the builder has a signed contract with a buyer before starting construction. The buyer selects their lot, floor plan, and options, and the builder constructs the home to those specifications. The advantage is low inventory risk: every home under construction has a committed buyer. The disadvantage is longer cycle times, typically six to nine months from contract to close, and the operational complexity of managing customized construction across hundreds of homes simultaneously.

A speculative, or spec, home is the opposite: the builder starts construction before identifying a buyer, typically choosing popular floor plans with broadly appealing specifications. The advantage is speed; a buyer can purchase a home that is nearly complete and move in within weeks rather than months. This turns the builder's capital faster and appeals to buyers who need housing quickly. The risk is that if the market softens, the builder may be stuck with finished inventory that it must discount to sell.

Taylor Morrison has historically tilted toward built-to-order, reflecting its move-up and luxury customer base that values personalization. However, the mix has shifted more toward spec in recent years to improve capital efficiency and meet buyer preferences for faster closings, particularly among younger move-up buyers who want the new-home experience without the six-month wait.

The land strategy deserves special attention because it is arguably the single most important determinant of long-term homebuilder profitability.

Think of a homebuilder's land pipeline as the fuel that powers the entire business. Without lots to build on, the company cannot generate revenue, no matter how efficient its operations or strong its brand. But owning too much land ties up enormous amounts of capital and exposes the company to devastating losses if prices decline. The 2008 crisis destroyed many builders precisely because they had too much land purchased at peak prices, and the industry has been grappling with how to manage this risk ever since.

There are essentially two models for land strategy in homebuilding. The traditional approach, which most builders used through the 2000s, is to buy raw land, develop it into finished lots (installing roads, utilities, and infrastructure), and then build homes on those lots. This approach ties up capital for years but maximizes the builder's profit per lot since it captures both the development margin and the construction margin.

The alternative, pioneered by NVR and increasingly adopted by others including Taylor Morrison, is to use options. Under this model, the builder pays a deposit, typically ten to fifteen percent of the lot price, for the right to purchase finished lots from a third-party land developer at a predetermined price over a specified period. If the market turns down, the builder can walk away from the option, forfeiting only the deposit rather than being stuck with depreciating land. The trade-off is that the lot developer earns a profit, so the builder's margin per home is somewhat lower, but the capital efficiency and risk reduction are substantial.

Taylor Morrison's evolution on this front has been dramatic. In 2019, the company owned outright about seventy-seven percent of its total lot supply. Today, roughly sixty percent of lots are controlled through options rather than owned. The company has a target of sixty-five percent. This transformation, supported by the land banking partnership with Varde Partners established in late 2021, has fundamentally changed the risk profile of the business. The total lot supply of approximately 6.4 years provides visibility well into the future, while the owned supply of about 2.6 years keeps balance sheet risk manageable.

Customer segmentation is another area where the company's positioning creates strategic advantage. Taylor Morrison operates across three primary buyer segments: move-up buyers who are selling a starter home and trading up, luxury buyers at the highest price points, and active adult buyers typically aged fifty-five and older through its Esplanade brand. Each segment has distinct characteristics that favor the company.

Move-up buyers tend to have substantial equity from their existing homes, higher household incomes, and greater financial stability. They are less sensitive to interest rate changes because they are often applying proceeds from a home sale to a large down payment. Luxury buyers are even less rate-sensitive and tend to value design, location, and brand above price. Active adult buyers are frequently purchasing with cash from the sale of a long-term home and represent a growing demographic as the baby boom generation ages into its sixties and seventies.

The Esplanade brand specifically targets this active adult opportunity. These resort-lifestyle communities typically feature clubhouses, pools, fitness centers, and social programming alongside homes designed for single-level living. The economics are attractive: active adult communities tend to have higher absorption rates because the buyer demographic is highly motivated, concentrated geographically in Sun Belt markets where Taylor Morrison already operates, and less affected by mortgage rate volatility since many purchases are cash.

The company operates with a decentralized model where division presidents run their local businesses with significant autonomy over land acquisition, design, pricing, and sales, while corporate headquarters in Scottsdale maintains centralized control over capital allocation, financial reporting, brand standards, and strategic planning. This structure mirrors how most successful homebuilders operate: the best land deals are found by people who know their local markets intimately, but capital discipline requires a central authority that can say no to deals that do not meet return thresholds.

The Darling Homes Collection by Taylor Morrison provides additional brand differentiation in Texas, while the Yardly build-to-rent brand opens an entirely new channel. This multi-brand architecture allows the company to target different buyer segments and price points without diluting the core Taylor Morrison brand promise.

The company's financial services segment, which includes mortgage origination, title insurance, and closing services, adds another dimension to the operating model. By controlling the mortgage process, Taylor Morrison can offer buyers a coordinated experience that reduces closing timelines, minimizes fall-through risk, and captures incremental revenue. The captive lender also gives the company a real-time window into buyer qualification and affordability dynamics, information that feeds back into pricing and incentive decisions at the community level. This is similar to how NVR has long used its integrated mortgage operation as both a profit center and an information advantage.

One strategic choice that has proven prescient is the decision to avoid the entry-level segment where competitors like D.R. Horton and Lennar compete most aggressively. Entry-level homebuilding is a fundamentally different business: margins are thinner, buyers are more rate-sensitive, land can be in less desirable locations, and the competition is primarily on price. By staying focused on move-up and above, Taylor Morrison has maintained pricing power and margin stability through cycles, even if it means forgoing some volume growth that entry-level exposure would provide.

X. Porter's Five Forces & Hamilton's Seven Powers Analysis

To assess whether Taylor Morrison's competitive position is durable, it helps to apply rigorous strategic frameworks to the homebuilding industry.

For context on these frameworks: Porter's Five Forces, developed by Harvard Business School professor Michael Porter, assesses the competitive dynamics of an industry by examining five key pressures that determine profitability. Hamilton Helmer's Seven Powers framework, from his book "7 Powers: The Foundations of Business Strategy," identifies the sources of durable competitive advantage that enable a company to earn persistent differential returns. Applying both to Taylor Morrison reveals where the company's positioning is strongest and where it faces the greatest challenges.

Starting with Porter's Five Forces: the threat of new entrants into homebuilding is moderate. The barriers to entry are substantial. A new builder needs access to capital, land positions that take years to develop, relationships with subcontractors and municipal authorities, and the expertise to navigate complex zoning, permitting, and environmental regulations. That said, homebuilding remains one of the most fragmented industries in America. The top ten builders collectively account for less than forty percent of total new home sales. Private builders, many operating in just one or two markets, start up and shut down with the cycle. So while it is hard to build a national platform, there is always competitive pressure from small local operators.

Supplier power is moderate to high and represents one of the industry's persistent challenges.

On the labor side, homebuilding is almost entirely subcontracted. Unlike a manufacturer that employs its production workers directly, a homebuilder contracts with independent framing crews, electrical contractors, plumbing firms, and dozens of other specialty trades for each home. The skilled trades shortage has been chronic since the financial crisis permanently drove hundreds of thousands of workers out of the construction industry, many of whom never returned. The subcontractor base is fragmented, which in theory should give builders leverage, but the scarcity of skilled framers, electricians, and plumbers gives those who remain significant pricing power. Builders cannot simply fire an underperforming subcontractor if there is no one else available to do the work.

On the materials side, lumber prices have been notoriously volatile, swinging by two to three times in a matter of months during the pandemic-era supply chain disruptions. Major appliance and fixtures suppliers like Masco and Fortune Brands have meaningful pricing leverage given consolidation in those industries. National builders like Taylor Morrison can negotiate volume discounts, but they cannot escape the underlying cost trends that affect the entire industry.

Buyer power is moderate. Each home purchase is a one-at-a-time, deeply emotional transaction. Buyers typically cannot aggregate demand or credibly threaten to switch builders once they have fallen in love with a community or floor plan. However, in softer markets, buyers have more choices and can demand incentives, upgrades, and price concessions. Taylor Morrison's positioning in the move-up and luxury segments somewhat insulates it here, since these buyers are choosing based on location, design, and lifestyle rather than purely on price.

The threat of substitutes is moderate. The most obvious substitute for a new home is an existing home, which represents the vast majority of housing transactions in any given year. Rental housing, whether apartments or single-family rentals, is another substitute for homeownership. However, new homes offer advantages that existing homes and rentals cannot match: modern energy efficiency, current building code compliance, warranty protection, and the ability to personalize. These advantages tend to be most valued by exactly the move-up and luxury buyers Taylor Morrison targets.

Industry rivalry is intense but increasingly rational. After the financial crisis decimated the industry, the surviving public builders have generally maintained disciplined pricing and land acquisition strategies, having learned the painful lesson that aggressive land speculation and price cutting during downturns can be existential threats.

Market share gains tend to come through organic community count growth and acquisitions rather than through destructive price wars. The fragmented nature of the market means that even the largest builders have ample room to grow share without engaging in head-to-head competition in most communities. In a typical metro area, a buyer might have a dozen builders to choose from, but in any given price range and submarket, the competitive set is usually three to five builders. This localized competition structure means that national scale helps with costs but does not directly reduce competitive intensity at the community level.

Turning to Hamilton Helmer's Seven Powers framework, which identifies the sources of durable competitive advantage, the analysis for Taylor Morrison reveals a mixed but interesting picture.

Scale economies represent a meaningful power for Taylor Morrison. National builders benefit from purchasing leverage on materials and appliances, overhead absorption across a larger revenue base, lower cost of capital from public market access, and marketing efficiencies. Taylor Morrison's eight-billion-dollar revenue base gives it significant advantages over the thousands of small private builders that compete in its markets, though it remains smaller than giants like D.R. Horton and Lennar that generate revenue three to four times as large.

Network effects do not apply to homebuilding in any meaningful way. A Taylor Morrison community does not become more valuable because more people buy Taylor Morrison homes in other states. This is a fundamental difference from technology businesses where network effects can create winner-take-all dynamics.

Counter-positioning is partially present. Taylor Morrison's focus on move-up, luxury, and active adult segments represents a strategic choice that would be difficult for entry-level-focused competitors to replicate without cannibalizing their existing business models. A builder like D.R. Horton, which has optimized its entire operation around high-volume, affordable homes, cannot easily pivot to competing in design-center-intensive, lifestyle-oriented communities without fundamentally changing its operating model.

Switching costs are weak in the traditional sense but nuanced in practice. During the shopping phase, buyers can easily visit multiple builder communities and compare offerings. However, once a buyer is under contract, has made design selections, and has an emotional attachment to a specific home and community, the switching costs become substantial, both financially and psychologically.

Branding power is moderate. Taylor Morrison's ten consecutive years as America's Most Trusted Home Builder is a meaningful differentiator, particularly for the move-up buyer who may have had a negative experience with a previous builder. However, homebuilding brands lack the consumer recognition and emotional resonance of consumer packaged goods or technology brands. Most buyers choose a community and location first, then learn about the builder, rather than seeking out a specific builder brand.

Cornered resource is where Taylor Morrison's competitive position is perhaps most defensible. In homebuilding, the cornered resource is land, specifically entitled, permitted land in desirable locations. Taylor Morrison's pipeline of 6.4 years of lot supply, accumulated over decades through multiple market cycles, includes positions in some of the highest-growth corridors in the country. These positions cannot be easily replicated by competitors because the land entitlement and permitting process takes years and requires deep relationships with local governments, land sellers, and developers. The company's long-tenured division presidents, many of whom have spent decades in their local markets, represent an additional cornered resource in the form of institutional knowledge and relationships.

Process power is the third significant source of competitive advantage. Taylor Morrison has demonstrated a repeatable capability in acquiring, integrating, and operating homebuilding businesses through multiple cycles. The 2011 merger that created the company, the 2020 William Lyon acquisition executed during a pandemic, and the ongoing transformation to a capital-light land model all reflect an operational sophistication that competitors have struggled to match. Palmer's team has built institutional knowledge about how to manage a homebuilding business through both booms and busts, and this cycle management expertise is a genuine process power that would take competitors years to develop.

The primary moats for Taylor Morrison, then, are scale economies, cornered resource in the form of land positions and local relationships, and process power through operational and integration excellence.

Comparing Taylor Morrison against its most direct competitors through these frameworks is illuminating. NVR, which pioneered the land-light option model, arguably has the strongest process power in the industry but operates in fewer, less-dynamic markets. Toll Brothers competes most directly in the luxury segment but has historically been more concentrated in the Northeast and Mid-Atlantic. Meritage Homes overlaps significantly in Sun Belt markets but is positioned more toward the entry-level and first-move-up segments. PulteGroup, where Palmer cut her teeth, is the closest competitor in terms of segment mix and geographic breadth but operates at roughly twice the scale.

What sets Taylor Morrison apart in this competitive landscape is the combination of move-up and luxury positioning with active adult exposure, geographic diversity concentrated in the highest-growth markets, a demonstrated ability to execute transformative acquisitions, and an increasingly capital-light land model. No other builder in the top ten combines all four of these characteristics. Whether this combination constitutes a durable competitive advantage or merely a favorable positioning that could be replicated depends largely on execution, which brings the analysis back to management quality and process power as the ultimate differentiators.

XI. Bull vs. Bear Case & What to Watch

The bull case for Taylor Morrison rests on a foundational premise that has only grown stronger since the financial crisis: America has a structural housing shortage that years of underbuilding have made acute.

According to estimates from the National Association of Realtors and various housing research organizations, the United States is short somewhere between three and seven million housing units depending on the methodology used. To put that number in context, the entire US homebuilding industry, public and private builders combined, delivered approximately 1.4 million housing starts in 2024. Even at that pace, closing a four-million-unit deficit while keeping up with new household formation would take a decade or more of sustained above-average construction. This is not a gap that closes quickly, which means the demand backdrop for homebuilders remains structurally favorable for the foreseeable future.

This deficit accumulated because housing starts remained below demographic demand for over a decade following the 2008 crisis. Even with recent construction activity, the gap has not meaningfully closed.

For Taylor Morrison specifically, the bull case adds several company-specific advantages. The fortress balance sheet enables counter-cyclical land acquisition, meaning the company can buy land at discounted prices during downturns when competitors are retrenching. The geographic diversification across twelve states, concentrated in the highest-growth Sun Belt and Mountain West markets, provides multiple engines of growth. The active adult and fifty-five-plus demographic represents a secular tailwind as approximately seventy million baby boomers age into the sweet spot for downsizer and lifestyle community demand. Management's track record of successful mergers and acquisitions, rare in an industry where most deals destroy value, suggests that additional strategic moves could further enhance the platform.

The company's ongoing shift to a capital-light land model also strengthens the bull thesis. By controlling sixty percent of lots through options rather than ownership, Taylor Morrison is reducing the cyclical risk that has historically made homebuilder equity one of the most volatile investments in the market. If this strategy works as intended, it should produce higher returns on equity through cycles while reducing the magnitude of downturns.

The bear case is equally compelling and centers on the inescapable reality that homebuilding is deeply cyclical.

Mortgage rates remain the single most important external variable for any homebuilder, and they are largely outside the company's control. As of early 2026, rates hover near seven percent, levels that have meaningfully impaired affordability even for move-up buyers who represent Taylor Morrison's core customer. The Federal Reserve's monetary policy, inflation trajectory, and the supply-demand dynamics of the mortgage-backed securities market all influence rates in ways that no homebuilder can predict or control.

If rates remain elevated or rise further, or if a recession develops that combines job losses with already-stretched affordability, demand could contract significantly regardless of the structural housing shortage.

Affordability is the bear's sharpest weapon. The math is simple: the median US household income has not kept pace with the combined effect of higher home prices and higher mortgage rates. A generation ago, a typical American household spent roughly twenty-five percent of its income on housing. Today, in many of the Sun Belt markets where Taylor Morrison operates, that figure exceeds thirty-five percent, a level that historically signals a market that is stretched beyond sustainable levels.

Even Taylor Morrison's move-up buyers, who are generally wealthier than the average homebuyer, are facing affordability constraints that affect their willingness to transact. A move-up buyer who needs to sell their existing home before purchasing a new one faces the "lock-in effect," where their current mortgage rate of three or four percent makes them reluctant to sell and take on a new mortgage at seven percent. This dynamic has frozen existing home inventory and reduced the pool of move-up buyers, which is directly relevant to Taylor Morrison's core customer segment.

The 2025 results, which showed margin compression and flat revenue despite community count growth, may be an early signal of these pressures.

Input cost inflation represents another risk. Labor costs have risen significantly since the pandemic, and the construction labor shortage shows no signs of abating. Material costs, while more stable than the extreme volatility of 2021-2022, remain elevated. These cost pressures squeeze margins from the cost side even as affordability limits pricing power on the revenue side.

Climate risk deserves specific mention because Taylor Morrison's geographic footprint is heavily weighted toward markets that face significant climate exposure. Florida, which represents a major portion of the East segment, faces hurricane risk and a rapidly hardening insurance market that has seen some insurers exit the state entirely. In some Florida markets, annual homeowner insurance premiums have tripled or quadrupled in recent years, adding thousands of dollars to the effective cost of homeownership.

Western markets face wildfire risk, particularly in California, Colorado, and parts of Arizona and Nevada. Building code changes, brush clearance requirements, and insurance challenges in wildfire-prone areas add cost and complexity to development. While these risks are not unique to Taylor Morrison, they represent a potential structural headwind for housing demand and construction costs in the company's most important markets.

The concern about private equity overhang has largely dissipated, as TPG and Oaktree exited their positions years ago through secondary offerings following the IPO. This is worth noting as a positive development: many PE-backed companies suffer from persistent share price pressure as their sponsors sell down large positions over multiple years. Taylor Morrison's sponsors executed their exit cleanly, and the shareholder base has transitioned to a mix of long-only institutional investors and index funds.

However, the broader question of institutional ownership dynamics and potential share price volatility remains relevant for a mid-cap homebuilder that does not attract the same analyst coverage or investor attention as mega-cap peers like D.R. Horton or Lennar.

For investors tracking this story, the KPIs that matter most cut through all the complexity of the homebuilding business. Two metrics capture nearly everything an investor needs to monitor.

The first is monthly absorption rate per community, which is the number of net new home orders per community per month. This single metric captures demand conditions, pricing effectiveness, community quality, and competitive positioning in a single number. Taylor Morrison's historical absorption rate has typically run between two and three homes per community per month, with higher rates during boom periods and lower rates during downturns. A sustained decline below two would signal meaningful demand deterioration; a sustained rate above three would indicate strong market conditions.

Think of absorption rate as the heartbeat of the business. When it is strong and steady, the company is healthy. When it weakens, it is an early warning sign that requires attention, whether through pricing adjustments, incentive changes, or community mix shifts.

The second critical metric is adjusted home closings gross margin. This captures the spread between what the company receives for its homes and what it costs to build them, adjusted for one-time items. This metric reflects land cost basis, construction efficiency, pricing power, and incentive levels all rolled into one. Taylor Morrison has generally targeted gross margins in the twenty-two to twenty-five percent range, with the recent compression to twenty-three percent in fiscal 2025 reflecting the challenging current environment. Investors should watch whether this stabilizes, improves, or deteriorates further, as the direction of this metric will determine the trajectory of earnings more than almost any other factor.

A useful myth-versus-reality check on the consensus narrative is warranted here. The myth is that homebuilders are simple commodity businesses where one builder's product is interchangeable with another's. The reality is that meaningful differentiation exists in customer segment focus, geographic positioning, land strategy, and operational execution. Taylor Morrison's move-up and luxury positioning generates structurally different economics than the entry-level segment, just as Toll Brothers' luxury focus generates different economics than D.R. Horton's volume approach. Understanding this segmentation is essential for comparing builders accurately.