TransMedics Group: The Story of Organ Transplantation's Most Audacious Bet

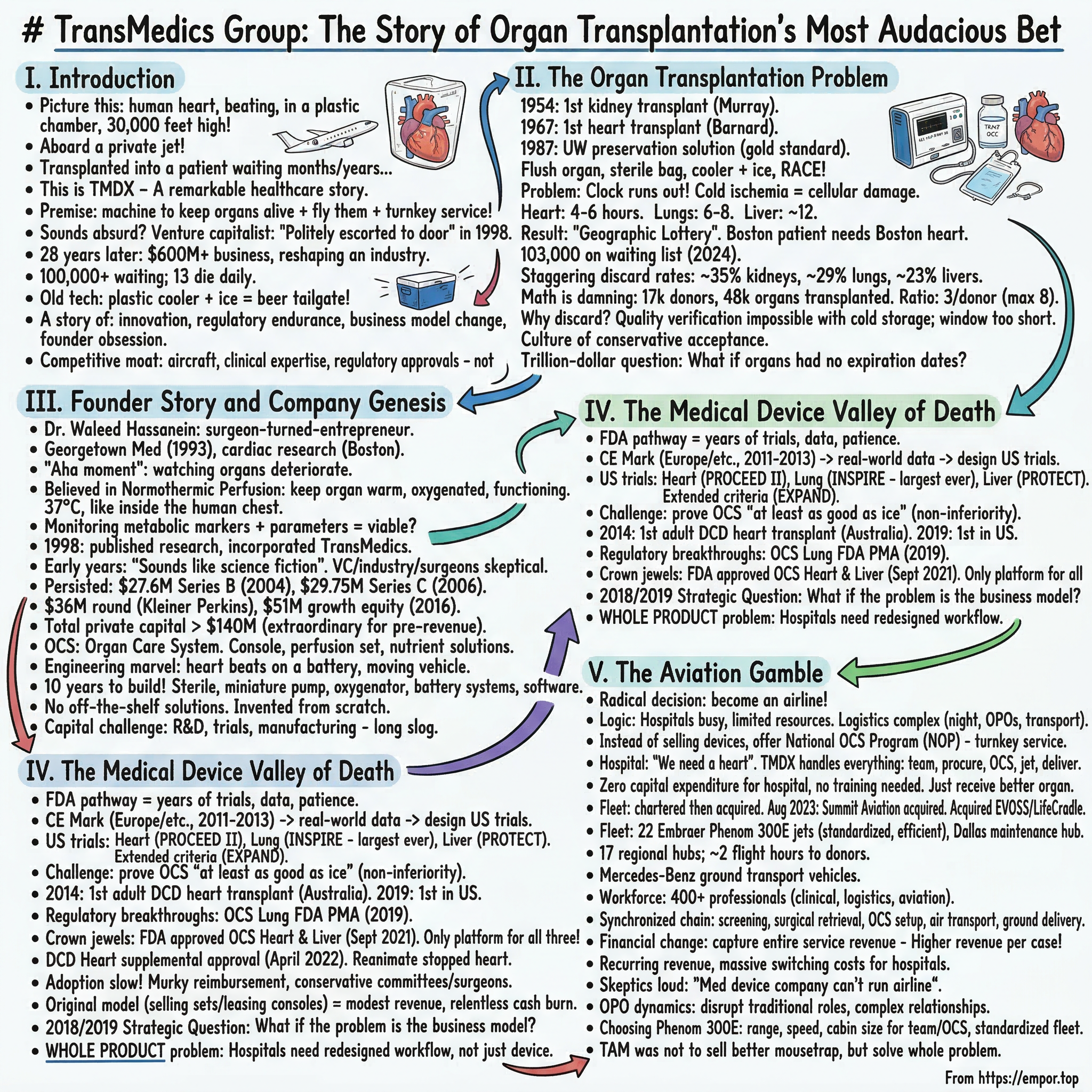

I. Introduction

Picture this: a human heart, still beating, cradled inside a transparent plastic chamber, pulsing rhythmically as warm, oxygenated blood courses through its coronary arteries. It is thirty thousand feet in the air, aboard a private jet streaking across the continental United States at five hundred miles per hour. In a few hours, that heart will be transplanted into a patient who has spent months—maybe years—on a waiting list, tethered to a hospital bed, hoping a phone call comes before their body gives out. This is not science fiction. This is TransMedics Group, ticker TMDX, and it is one of the most remarkable business stories in modern healthcare.

The premise behind TransMedics sounds almost absurdly ambitious: build a machine that keeps human organs alive and functioning outside the body, then build an airline to fly those organs across the country, and wrap the whole thing in a turnkey clinical service that transforms how organ transplantation works in America. If you pitched this to a venture capitalist in 1998—a cardiac surgeon walks in and says he wants to build a portable life-support system for human organs, and oh, by the way, eventually he is going to start an aviation company too—you would get politely escorted to the door.

But that is exactly what Dr. Waleed Hassanein did. And twenty-eight years later, TransMedics has grown from a laboratory concept into a six-hundred-million-dollar-a-year business that is fundamentally reshaping an industry where the stakes could not be higher. More than one hundred thousand Americans sit on organ transplant waiting lists. Thirteen people die every single day because an organ does not arrive in time. And until TransMedics came along, the state-of-the-art technology for transporting a human heart was essentially the same thing you would use to keep beer cold at a tailgate: a plastic cooler packed with ice.

This is a story about medical device innovation, regulatory endurance, business model transformation, and the kind of founder conviction that borders on obsession. It is a story about a company that spent two decades burning cash, fighting through the FDA gauntlet, and nearly running out of money—only to emerge on the other side with a business model so differentiated that no competitor can replicate it. And it is a story with enormous implications for investors trying to understand whether TransMedics is a five-billion-dollar company or a fifty-billion-dollar company, and what the next decade holds for the only firm in the world that operates a private airline dedicated entirely to keeping human organs alive.

The themes we will explore run deep: How does a surgeon-turned-entrepreneur navigate a twenty-year FDA journey without losing faith? When is the right time to abandon your original business model and build something completely different? What does vertical integration look like when it means buying a fleet of jets? How does a company create a market that did not previously exist? And perhaps most importantly: in an era of software-first, asset-light business models, what does it mean to build a company whose competitive moat is made of aircraft, clinical expertise, and regulatory approvals rather than algorithms and network effects?

II. The Organ Transplantation Problem

On December 23, 1954, Dr. Joseph Murray performed the first successful organ transplant at Peter Bent Brigham Hospital in Boston—a kidney transferred between identical twins, Ronald and Richard Herrick. The operation lasted five and a half hours. Richard survived eight more years, long enough to marry and have two children. Murray eventually received the Nobel Prize for his work. Thirteen years later, in December 1967, South African surgeon Christiaan Barnard performed the first human heart transplant at Groote Schuur Hospital in Cape Town. The recipient, Louis Washkansky, survived eighteen days before succumbing to a lung infection. These were the founding miracles of modern transplant medicine—proof that the human body could accept a foreign organ and, with the right conditions, thrive.

But the field's next great breakthrough came not from a surgeon's hands but from a laboratory in Wisconsin. In 1987, Folkert Belzer and James Southard at the University of Wisconsin developed the UW preservation solution, a carefully formulated cocktail of chemicals that could keep harvested organs viable in cold storage for dramatically longer periods than anything that existed before. The UW solution became the gold standard. It allowed livers to survive on ice for up to twenty-four hours and kidneys for even longer. The protocol was elegant in its simplicity: flush the organ with cold preservation solution, place it in a sterile bag, pack it in a cooler with ice, and race it to the transplant center before the clock runs out.

The problem is that the clock always runs out. Cold ischemia—the technical term for storing an organ without blood flow at near-freezing temperatures—triggers a cascade of cellular damage that begins the moment the organ leaves the donor's body. Deprived of oxygen, cells exhaust their energy reserves. Ion pumps that regulate sodium and calcium stop working. Cells swell. Toxic metabolites accumulate. And when the organ is finally rewarmed and reconnected to a blood supply during transplantation, the flood of oxygen triggers an even more destructive wave of damage called reperfusion injury, as reactive oxygen species tear through mitochondria and trigger inflammatory cascades. The heart, composed of dense contractile muscle that demands enormous amounts of energy, is the most vulnerable organ of all. On ice, a heart has four to six hours. A lung gets six to eight. A liver, perhaps twelve.

These time windows create what transplant surgeons call the geographic lottery. If you need a heart transplant and you live in Boston, you can only receive hearts from donors within a few hundred miles—whatever distance a heart can travel and still arrive within that four-to-six-hour cold ischemia window. If you happen to live in a region with few donors but many recipients, your odds plummet. Your zip code, as much as your medical condition, determines whether you live or die.

The geographic inequity is not abstract. Until recently, organ allocation in the United States was divided into fifty-eight donation service areas, each controlled by a local organ procurement organization. Organs were offered first to patients within the local service area, then regionally, then nationally. A patient in New York might die waiting while a compatible organ was discarded in Texas because the logistics of getting it there within the cold ischemia window were impractical. The system was designed around the limitations of ice, not the needs of patients. Reform efforts—particularly the shift to continuous distribution allocation, which eliminates geographic boundaries and uses a composite score to match donors and recipients nationally—have begun to address this, but they also mean organs must travel farther, which makes the limitations of cold storage even more acute.

The consequences of this system are staggering. More than one hundred and three thousand Americans are on the transplant waiting list. In 2024, roughly forty-eight thousand transplants were performed—a record, but less than half the number of people waiting.

The discard rates tell the rest of the story. Nearly thirty-five percent of donated kidneys are discarded. Almost twenty-nine percent of lungs never make it to a recipient. Twenty-three percent of livers are thrown away. These are not damaged organs. Many of them are perfectly viable, but cold storage makes it impossible to verify their quality, the preservation window is too short to transport them far enough, and surgeons—rationally—would rather decline a questionable organ than risk a transplant failure that could kill their patient. The system is designed around the limitations of ice, and ice is a terrible technology for keeping human tissue alive.

The math is damning. Every year in the United States, roughly seventeen thousand deceased donors provide organs. From those donors, roughly forty-eight thousand organs are transplanted. But the gap between supply and demand is not just about the number of donors—it is about the number of usable organs per donor. The theoretical maximum is eight organs per donor. The actual average is closer to three. Cold storage is one of the primary reasons. A heart that might be perfectly viable cannot be used if it takes too long to reach a recipient. A liver from a DCD donor—someone who died from cardiac arrest rather than brain death—suffers warm ischemia that cold storage cannot reverse, so it is often discarded. Lungs, exquisitely sensitive to cold injury, are the most frequently declined organ offered to transplant centers.

Transplant surgeons describe a culture of conservative organ acceptance that cold storage reinforces. One surgeon recounted hearing organ offers she would have accepted but could not because the heart already had twenty or more hours of cold time—and estimated that "hundreds of organs a year" represent lost opportunities. The incentive structure makes this rational: a surgeon who accepts a questionable organ and the patient dies faces severe professional consequences. A surgeon who declines the same organ faces none. The system penalizes risk-taking, and cold storage maximizes the uncertainty that drives risk aversion.

The trillion-dollar question that haunted a generation of transplant researchers was deceptively simple: what if organs did not have expiration dates?

III. Founder Story and Company Genesis

Waleed Hassanein was not a typical medical device entrepreneur. He earned his medical degree from Georgetown University in 1993, having initially studied at Cairo University School of Medicine. He then completed two years of general surgery training at Georgetown University Medical Center before pivoting to a three-year cardiac surgery research fellowship at the West Roxbury VA Medical Center and Brigham and Women's Hospital in Boston—two institutions embedded in the beating heart of American academic medicine. Hassanein was that rare individual who combined deep surgical training with an engineer's instinct for systems design. He did not just want to understand why hearts failed after transplantation. He wanted to build something that would prevent it.

The "aha moment," as Hassanein has described it in interviews, came from watching organs deteriorate. As a cardiac surgery researcher in the late 1990s, he saw firsthand the damage that cold storage inflicted on donor hearts. He understood the biology: the ATP depletion, the ion pump failure, the reperfusion injury. And he understood something that the transplant establishment had not yet fully grasped—that cold storage was not merely imperfect, it was fundamentally wrong. Cooling an organ does not preserve it. It slowly kills it. The right approach, Hassanein believed, was the opposite: keep the organ warm, keep it oxygenated, keep it functioning. Do not put it to sleep. Keep it alive.

The concept was called normothermic perfusion. Instead of flushing a heart with cold solution and packing it on ice, you would connect it to a miniaturized life-support system that circulated warm, oxygenated, nutrient-rich blood through the organ at body temperature—thirty-seven degrees Celsius, the same temperature as inside the human chest. The heart would continue beating. The lungs would continue exchanging gas. The liver would continue producing bile. And crucially, the clinical team could monitor the organ in real time, measuring metabolic markers and hemodynamic parameters to determine whether it was viable for transplant—something utterly impossible with a cooler of ice.

Hassanein published his early research on ex-vivo heart perfusion in the Journal of Thoracic and Cardiovascular Surgery in 1998, earning recognition from the American Association for Thoracic Surgery. That same year, he incorporated TransMedics in Delaware. The company was born from a simple but radical premise: build a portable organ perfusion machine that could keep donor organs alive during transport.

The early years were defined by the phrase "this sounds like science fiction." Venture capitalists were skeptical. The medical device industry was skeptical. Even transplant surgeons—the very people who would use the technology—were skeptical. Normothermic perfusion was an elegant idea, but building a machine that could reliably keep a human heart beating inside a plastic chamber, on a battery, aboard a moving vehicle, at thirty-seven degrees, with real-time monitoring, in a regulatory environment that required years of clinical trials to prove it worked—that was something else entirely.

Hassanein persisted. In January 2004, TransMedics closed a twenty-seven-point-six-million-dollar Series B round co-led by Flagship Ventures, 3i US, and CB Health Ventures. Two years later, a twenty-nine-point-seven-five-million-dollar Series C followed, led by 3i Group.

A subsequent round brought thirty-six million dollars from Foundation Capital and Kleiner Perkins—names that validated the scientific credibility of the vision even as the company remained years away from generating meaningful revenue. A 2016 growth equity round added fifty-one million more, co-led by Fayerweather Fund, Pharmstandard International, and others. Each of these raises diluted earlier investors, but they also kept the dream alive. The total private capital raised before the IPO exceeded one hundred forty million dollars—an extraordinary sum for a medical device company that had yet to generate significant commercial revenue.

The machine itself—which TransMedics branded the Organ Care System, or OCS—was an engineering marvel in miniature. The system consists of three components: a reusable console housing the circulatory pump, batteries, gas delivery subsystem, and monitoring probes; a single-use perfusion set specific to each organ type; and proprietary nutrient and preservation solutions. For a heart, the process works like this: donor blood is placed in a reservoir and supplemented with TransMedics' proprietary solutions. A pump draws the blood through an oxygenator and blood warmer, then directs the warm, oxygenated blood into the aorta, which perfuses the coronary arteries and keeps the heart beating. Blood drains back into the reservoir, completing a continuous circuit. The result is a portable intensive care unit for a single organ—a self-contained ecosystem that maintains near-physiologic conditions indefinitely.

Building this machine took a decade. The engineering challenges were immense: maintaining precise temperature control, ensuring sterility, miniaturizing pump and oxygenator technology, creating robust battery systems, developing monitoring software that could track dozens of parameters in real time. And all of it had to be compact enough to transport, rugged enough to survive air travel, and reliable enough that a cardiac surgeon on the other end would trust it with a patient's life.

Consider the sheer difficulty of what TransMedics was attempting. In a hospital, a heart-lung bypass machine occupies an entire room, requires a dedicated perfusionist, connects to wall-mounted gas supplies, and draws power from the building's electrical grid. Hassanein was trying to shrink all of that into a portable unit that could run on batteries, withstand the vibrations of air travel, maintain sterility for hours, and keep a human heart beating at precisely the right temperature, pressure, and flow rate—while being operated by a small team in the cramped cabin of a jet. Every component had to be rethought from first principles. The oxygenator had to be miniaturized without sacrificing gas exchange efficiency. The pump had to deliver consistent flow without damaging red blood cells. The monitoring system had to be intuitive enough that a perfusionist could manage it during a turbulent flight. There were no off-the-shelf solutions. TransMedics had to invent most of this from scratch.

The human capital challenge was equally daunting. Building a medical device company requires not just engineers but regulatory specialists, clinical researchers, quality assurance experts, and manufacturing technicians—all working toward a product that might not reach market for a decade or more. Hassanein had to recruit and retain talent through years of pre-revenue operation, competing for engineers with established Boston-area medtech firms that could offer stock options with near-term liquidity. The company's location in the greater Boston medical ecosystem—surrounded by Harvard, MIT, Brigham and Women's, and Massachusetts General Hospital—provided access to world-class talent, but keeping that talent motivated through the long slog of R&D required a founder whose personal conviction was contagious.

By the mid-2000s, TransMedics had accumulated more than one hundred forty million dollars in venture capital across multiple rounds—a staggering sum for a pre-revenue medical device company. The investors who backed those rounds were making a bet not just on the technology but on the regulatory strategy, the clinical trial design, the manufacturing scalability, and ultimately on Hassanein himself. It was the kind of deep-tech venture bet that most firms avoid—too capital-intensive, too long a timeline, too many regulatory unknowns. But the payoff, if it worked, would be transformational.

IV. The Medical Device Valley of Death

If founding TransMedics required conviction, navigating the FDA required something closer to religious faith. The regulatory pathway for a novel organ perfusion device—a category that essentially did not exist—demanded years of clinical trials, mountains of data, and the patience to watch competitors with simpler products race ahead while TransMedics methodically built its evidence base.

TransMedics adopted a strategy common among innovative medical device companies: start in Europe, where CE Mark approval was faster and less expensive, then use that clinical experience to design pivotal U.S. trials. The OCS received CE Mark approval in the 2011-2013 timeframe, enabling clinical use in Europe, Australia, and eventually Canada. The early European cases were crucial—they generated real-world data on organ perfusion outcomes that informed the design of U.S. registration trials and gave transplant surgeons their first direct experience with the technology. The PROTECT I trial, conducted at leading centers in England and Germany as early as 2006-2007, represented some of the earliest clinical evidence that the OCS concept could work in real patients. These European pioneers provided the bridge between laboratory proof-of-concept and the large-scale U.S. registration trials that would follow.

The U.S. clinical program was organized around three pivotal trials, each targeting a different organ. PROCEED II tested OCS Heart against standard cold storage for hearts from brain-dead donors. INSPIRE was the first and largest controlled clinical trial ever conducted in lung preservation, spanning twenty-one academic institutions. PROTECT evaluated OCS Liver for both DBD and DCD livers. A supplementary trial, EXPAND, focused specifically on hearts from extended-criteria donors—organs that transplant centers would normally reject because cold storage could not guarantee their viability.

The challenge facing TransMedics in these trials was one of the great ironies of medical device innovation: to win FDA approval, they had to prove that their revolutionary technology was at least as good as ice. This is called a non-inferiority trial design, and it is the standard the FDA requires for most new medical devices. TransMedics could not simply demonstrate that the OCS was technologically superior—they had to conduct large, randomized, controlled trials showing that patient outcomes were at least equivalent to the decades-old standard of care. The clinical and financial burden was enormous. Each trial required hundreds of patients, years of follow-up, and tens of millions of dollars.

Meanwhile, the earliest clinical milestones were being achieved overseas. In 2014, St. Vincent's Hospital in Sydney, Australia performed the world's first series of adult DCD heart transplants using OCS Heart—a landmark that proved the fundamental concept of resuscitating a stopped heart outside the body. In the United States, the first adult DCD heart transplants using OCS occurred in December 2019 at Duke University Hospital and Massachusetts General Hospital, making international headlines and demonstrating the technology's potential to create an entirely new category of donor organs.

The first major U.S. regulatory breakthrough came when OCS Lung received FDA pre-market approval in March 2019, with an expanded indication for both standard and extended-criteria donors following in June of that year. This was significant not just as a regulatory milestone but as proof of concept: the FDA had examined the clinical data and agreed that normothermic perfusion was a viable alternative to cold storage for human lungs. The INSPIRE trial, which supported this approval, was the first and largest controlled preservation study ever in lung transplantation, spanning twenty-one institutions across multiple countries.

Then came the crown jewels. In September 2021, within weeks of each other, the FDA approved both OCS Heart for brain-dead donor hearts and OCS Liver for both DBD and DCD livers. These approvals transformed TransMedics from a one-organ company into the only platform in the world with FDA-cleared normothermic perfusion technology for all three critical transplant organs—hearts, lungs, and livers. Seven months later, in April 2022, the FDA granted a supplemental approval for OCS Heart in DCD hearts—donation after circulatory death—making TransMedics the only technology in the world that could reanimate a heart that had stopped beating and assess it for transplant viability.

But FDA approval was only half the battle. Adoption was painfully slow. Hospital procurement committees were conservative. Transplant surgeons, trained for decades on cold storage protocols, were reluctant to change. The reimbursement landscape was murky—would Medicare and private insurers pay the thirty-eight to eighty thousand dollars per organ that a single-use OCS perfusion set cost? TransMedics' original business model—selling disposable perfusion sets and leasing consoles to transplant centers—generated modest revenue but could not cover the company's R&D and regulatory costs. Cash burn was relentless. Multiple capital raises diluted existing shareholders. The company hovered in the medical device valley of death: approved but not yet adopted, innovative but not yet profitable.

By 2018 and 2019, Hassanein and his team confronted a strategic question that would define the company's future: what if the problem was not the technology, but the business model? What if, instead of selling devices to hospitals and hoping surgeons adopted them, TransMedics took control of the entire value chain—organ procurement, perfusion management, transportation, and delivery? What if TransMedics did not just make the machine, but operated the machine, flew the organ, and managed the entire clinical workflow from donor to recipient?

It was, by any measure, a crazy idea. And it was exactly the right one.

The strategic logic behind this pivot deserves careful examination because it illustrates a broader principle in business strategy. TransMedics was experiencing what Clayton Christensen called the "whole product" problem: the OCS was a brilliant component, but it was not a complete solution. Hospitals needed more than a device—they needed a redesigned workflow. The analogy is to the early days of personal computing: manufacturers sold hardware, but what businesses actually needed was hardware plus software plus support plus integration plus training. Companies that sold the whole solution—like IBM in the mainframe era—captured far more value than those that sold components. Hassanein recognized that organ transplantation had the same dynamics. The device was necessary but not sufficient. The whole product was a service that handled everything from donor evaluation to organ delivery.

V. The Aviation Gamble

The moment TransMedics decided to become an airline was the inflection point that transformed the company from a struggling medical device maker into a vertically integrated healthcare platform with no direct competitor. It is difficult to overstate how radical this decision was. Medical device companies sell devices. They do not buy jets, hire pilots, obtain FAA certification, build regional logistics hubs, and deploy clinical teams on twenty-four-seven rotations across the continental United States. And yet that is precisely what TransMedics did.

The logic, once you understand it, is compelling. TransMedics' original business model assumed that transplant centers would buy OCS perfusion sets, train their staff, and manage the organ procurement process themselves. But transplant centers are busy places with limited resources. Organ procurement is logistically complex—it requires coordinating with organ procurement organizations, arranging transportation, managing the perfusion technology, and deploying surgical teams, often in the middle of the night. Asking a hospital to adopt a new, expensive, unfamiliar technology and simultaneously redesign its procurement workflow was asking too much. The adoption bottleneck was not the OCS itself. It was everything around it.

The National OCS Program, as TransMedics branded its integrated service, flipped the model entirely. Instead of selling devices, TransMedics would provide a complete, turnkey organ procurement and delivery service. A transplant center would simply place a call: "We need a heart for our patient." TransMedics would handle everything else—dispatching a clinical team to the donor hospital, evaluating and procuring the organ, placing it on the OCS, monitoring it during transport, flying it aboard a TransMedics jet to the recipient hospital, and delivering a living, beating, fully assessed organ directly to the operating room.

The transplant center bore no capital expenditure, required no specialized staff training, and assumed no logistical complexity. They just received a better organ. The simplicity of this value proposition cannot be overstated. In a healthcare system notorious for its complexity, TransMedics offered something almost unheard of: a superior clinical outcome with less operational burden on the hospital.

Building this capability during 2020 and 2021—in the depths of a global pandemic—required extraordinary operational ambition. TransMedics began assembling an aviation fleet, initially through charter arrangements and then through direct acquisition.

In August 2023, the company completed its acquisition of Summit Aviation, a premier U.S. charter flight operator, bringing aircraft maintenance and operations expertise in-house. Around the same time, TransMedics acquired EVOSS warm perfusion and LifeCradle cold perfusion technologies from Bridge to Life, consolidating its technological capabilities.

The fleet grew to twenty-two Embraer Phenom 300E jets—all 2021 model year or newer—supported by a dedicated maintenance hub in Dallas and a command center coordinating operations nationwide. Seventeen regional hubs were established across the United States, enabling TransMedics teams to reach donors anywhere in the country within two flight hours or less. The company even partnered with Mercedes-Benz for a fleet of ground transport vehicles.

The workforce grew to more than four hundred clinical, logistics, and aviation professionals—an extraordinary headcount for what was, just a few years earlier, a medical device company with a few dozen employees. Every NOP mission involves a synchronized chain: donor screening, surgical retrieval by a TransMedics-affiliated procurement team, OCS setup and perfusion management by trained perfusionists, air transport aboard a TransMedics jet, and ground delivery to the transplant center. The company built a twenty-four-seven operations command that coordinates all of this in real time.

The financial implications of this transformation were profound. Under the old model, TransMedics earned revenue from a single transaction: selling a perfusion set. Under the National OCS Program, the company earns revenue from the entire service—clinical staffing, technology management, air transport, ground logistics, and organ delivery. Revenue per case is dramatically higher. Margins improve with scale as fixed costs (aircraft, hubs, staff) are spread across more missions.

And critically, the service model creates recurring, predictable revenue: once a transplant center is integrated into the NOP network, the switching costs are massive. There is no easy way to replicate what TransMedics has built, and going back to the old model of ad hoc charter flights and ice coolers means accepting worse organs and worse outcomes.

Skeptics were loud. "A medical device company cannot run an airline," was the consensus view on Wall Street. Aviation is complex, capital-intensive, and heavily regulated. FAA compliance is its own regulatory universe, layered on top of FDA requirements. Managing a fleet of jets, training pilots, maintaining aircraft, and coordinating hundreds of time-critical missions per month—any one of these could go wrong in ways that had nothing to do with TransMedics' core medical technology expertise.

The OPO dynamics added another layer of complexity. The United States has fifty-five to fifty-seven federally designated organ procurement organizations, each holding a geographic monopoly over organ procurement in its region. These nonprofits had managed organ logistics for decades—coordinating with donor hospitals, arranging commercial or charter flights, dispatching surgical teams. TransMedics' NOP was not merely offering them a better tool; it was, in many cases, offering transplant centers an alternative procurement pathway that bypassed the OPO's traditional role. Some OPOs embraced the partnership—TransMedics could handle cases they lacked the resources for, or preserve organs they would otherwise discard. Others viewed TransMedics as a competitor encroaching on their territory. Navigating this ecosystem required diplomatic skill as much as operational capability, and TransMedics' ability to frame the NOP as complementary rather than competitive was a critical factor in its adoption.

The choice of the Embraer Phenom 300E as the fleet workhorse was itself a strategic decision. The Phenom 300 is the most-delivered light jet in the world, known for its range, speed, reliability, and low operating costs. Its cabin is large enough to accommodate the OCS equipment and a clinical team of two to three perfusionists, while its range of roughly two thousand nautical miles covers most donor-to-recipient routes within the continental United States without refueling stops. Using a standardized fleet—all the same aircraft type, all the same model year—simplifies maintenance, pilot training, and parts inventory. It is the same fleet standardization strategy that Southwest Airlines used with the Boeing 737, applied to organ transplant logistics.

But Hassanein had done the math. The organ transplant market was not going to be won by selling a better mousetrap. It was going to be won by solving the whole problem—technology, logistics, clinical expertise, and transportation—in a single integrated offering. TransMedics was not just selling a device anymore. It was selling a service that saved lives.

VI. Proof of Concept and Hockey Stick Growth

The numbers tell the story of what happened next. In 2019, the year TransMedics went public at sixteen dollars per share on the Nasdaq, the company generated twenty-three-point-six million dollars in revenue. In 2020, during the pandemic, revenue inched up to twenty-five-point-six million. In 2021, the year OCS Heart and OCS Liver received FDA approval, revenue grew modestly to thirty-point-three million—the National OCS Program was still in its early stages, and most revenue still came from traditional device sales. Then the hockey stick arrived.

In 2022, with the NOP scaling rapidly and all three organ systems now FDA-approved, revenue tripled to ninety-three-point-five million dollars. In 2023, it nearly tripled again to two hundred forty-one-point-six million. In 2024, it nearly doubled to four hundred forty-one-point-five million. And in 2025, it reached six hundred five-point-five million dollars—a twenty-five-fold increase from the IPO year in just six years.

Read that again: a twenty-five-fold increase in revenue in six years. This is not a SaaS company with zero marginal cost. This is a company that flies jets, employs hundreds of clinical professionals, and manages complex logistics—and it still grew revenue at triple-digit rates for three consecutive years. The company guided 2026 revenue of seven hundred twenty-seven to seven hundred fifty-seven million dollars, implying continued growth of twenty to twenty-five percent.

TransMedics went public on May 2, 2019, pricing its IPO at sixteen dollars per share and raising approximately one hundred five million dollars in gross proceeds with Morgan Stanley and J.P. Morgan as lead underwriters. The timing was fortuitous—just weeks after the first OCS Lung FDA approval—but the stock languished for years as the market waited for commercial traction. The shares actually hit an all-time low of roughly ten dollars in February 2022, just before the revenue explosion began. From that nadir, the stock surged to an all-time high of one hundred seventy-seven dollars in August 2024—an eighteen-fold gain in roughly two and a half years.

The stock's journey from ten dollars to one hundred seventy-seven dollars is worth dwelling on because it illustrates a recurring pattern in medical technology investing. For years, TransMedics was a "show me" story—the technology was approved, but the revenue was not materializing, and the company was burning cash. Institutional investors who analyzed the company saw a medical device maker with limited commercial traction and a history of missed expectations. The NOP transformation was underway but not yet visible in quarterly results. Then, in 2022, when revenue tripled and the growth trajectory became unmistakable, the market re-rated the stock rapidly and violently upward. The lesson is that transformational business model shifts in healthcare often take years to appear in financial statements, and by the time they do, the stock has already moved.

The operational metrics were equally striking. TransMedics facilitated 2,347 OCS cases in 2023, then 3,715 in 2024—a fifty-eight percent increase—and 5,139 in 2025, another thirty-eight percent jump. By 2025, OCS liver cases alone totaled 4,197, capturing roughly thirty-six percent of all U.S. liver transplants, up from twenty-six percent the prior year. OCS heart cases reached 854, representing approximately eighteen percent of U.S. heart transplant volume. The company has set a target of ten thousand annual U.S. NOP transplants by 2028—a number that would represent a transformational share of the overall transplant market.

To put these adoption numbers in context, consider how unprecedented this growth rate is for a medical device platform. Most novel surgical technologies take a decade or more to move from single-digit to double-digit market penetration. TransMedics went from negligible market share to more than a third of all U.S. liver transplants in roughly three years. The NOP model was the accelerant—by removing every adoption barrier except the transplant surgeon's willingness to accept the organ, TransMedics compressed a typical decade-long adoption curve into a fraction of the time. The company was not asking surgeons to learn a new technology. It was asking them to accept a better organ that arrived at their door.

Profitability followed the revenue curve. TransMedics reported its first full year of positive net income in 2024—thirty-five-point-five million dollars on four hundred forty-one million in revenue, an eight percent net margin. In 2025, net income surged to one hundred ninety million dollars, though this figure included an eighty-three-million-dollar one-time tax benefit from releasing deferred tax asset valuation allowances. Stripping out the tax benefit, the underlying profitability still showed dramatic improvement. Gross margins stabilized around sixty percent—a level that reflects the high value-add of the NOP service model and the pricing power that comes from being the only integrated provider. Operating margins expanded by roughly seven hundred fifty basis points year over year, and management has publicly targeted thirty percent operating margins by 2028—a level that would place TransMedics among the most profitable companies in medtech. The company ended the third quarter of 2025 with over four hundred sixty-six million dollars in cash on the balance sheet, having generated positive operating cash flow in 2024 for the first time.

The path from cash-burning startup to cash-generating platform took twenty-six years. But the financial profile that emerged was extraordinary: sixty percent gross margins, rapidly expanding operating margins, strong cash generation, and a capital-light incremental model where each new NOP mission leverages existing infrastructure. For a company that once teetered on the edge of insolvency, the transformation was complete.

But the path was not smooth. In October 2024, TransMedics reported a third-quarter revenue miss, reduced its full-year guidance, and simultaneously announced a CFO transition—Stephen Gordon, who had served since 2015, departed and was replaced by Gerardo Hernandez from Alnylam Pharmaceuticals. The stock cratered more than thirty percent overnight, falling from roughly one hundred twenty-six dollars to ninety. Then, in January 2025, short-seller Scorpion Capital published a three-hundred-forty-two-page report alleging kickbacks, billing fraud, and off-label misuse, with a target price of zero. Shares dropped another thirteen percent. Combined with the October earnings miss, the stock had fallen as much as sixty percent from its August all-time high.

TransMedics' response was methodical. In February 2025, the company announced that an independent review conducted by Kirkland and Ellis, one of the most prestigious law firms in the country, with forensic accounting support, had identified no evidence of misconduct. Hassanein pointed to the company's track record of more than seven thousand successful organ transplants.

The stock began recovering, and by early March 2026, shares were trading in the one hundred twenty to one hundred forty-eight dollar range—up more than one hundred percent from the post-short-report lows. However, a securities fraud class action lawsuit filed by Hagens Berman remained pending with an April 2025 lead plaintiff deadline. Investors should note this legal overhang: while the independent review found no evidence of misconduct, the litigation is unresolved, and its outcome could affect the stock.

The episode is instructive about the risks of investing in high-growth, high-profile healthcare companies. Short sellers target companies where rapid revenue growth, novel business models, and complex reimbursement dynamics create the appearance of potential irregularity—even when none exists. The volatility that followed Scorpion Capital's report illustrates how quickly sentiment can shift and how important it is for management to have independent verification of its practices. TransMedics navigated the crisis, but the stock's sixty-percent drawdown from peak to trough was a reminder that narrative risk is as real as operational risk in small-cap healthcare.

VII. The Business Model Revolution

To understand why TransMedics is so difficult to compete with, you have to understand the economics of the National OCS Program, which are unlike anything else in medical devices.

In the traditional medtech model, a company sells a device to a hospital. The hospital buys it, trains its staff, and uses it. The manufacturer earns revenue from the initial sale and from recurring consumables. This is the razor-and-blade model that has driven companies like Intuitive Surgical, Medtronic, and Abbott for decades. TransMedics started here—selling single-use perfusion sets at thirty-eight to eighty thousand dollars each—but the NOP moved the company far beyond it.

Under the National OCS Program, TransMedics does not sell devices to hospitals. It sells outcomes. A transplant center pays for a complete service: organ evaluation, procurement, perfusion management, air transport, and delivery. The center receives a living, beating, fully assessed organ at its loading dock.

The revenue TransMedics captures per case is significantly higher than a standalone device sale because it includes clinical staffing, aviation, and logistics. And the margin profile improves with scale: every additional mission leverages the same fleet of jets, the same network of hubs, the same trained clinical teams. The fixed-cost infrastructure was expensive to build, but the incremental cost of each additional mission is relatively low.

Customer stickiness is extraordinary. Once a transplant center integrates into the NOP workflow—adjusting its procurement protocols, training its teams to receive NOP-delivered organs, building its transplant program around the expanded donor pool that OCS enables—the switching costs are enormous.

Going back to the old model means fewer organs, shorter preservation windows, no real-time viability assessment, and inferior outcomes. No transplant program director wants to explain to their hospital board why they stopped using a technology that gave them access to more and better organs. And the stickiness compounds over time: as a transplant center performs more OCS-supported transplants, its outcomes data improves, its surgeons become more experienced with OCS-preserved organs, and its reputation as a leading transplant center grows. Walking away from the NOP means walking away from all of that accumulated capability.

TransMedics is also building a data moat. Every OCS case generates a rich dataset: perfusion parameters, organ metabolic markers, hemodynamic measurements, transport conditions, and transplant outcomes. Over time, this becomes a proprietary repository of normothermic perfusion data that no competitor can replicate. The company has hinted at machine learning applications—using its data to develop predictive algorithms that could assess organ viability with increasing precision. This is still early-stage, but the data advantage compounds with every case.

The regulatory moat is equally formidable. FDA pre-market approval for an organ perfusion device requires years of clinical trials, hundreds of patients, and hundreds of millions of dollars. TransMedics has FDA PMA approvals for three organs. Any competitor starting from scratch faces a five-to-ten-year timeline and enormous capital requirements just to reach the starting line. And even if a competitor builds a comparable device, they would still need to replicate the aviation fleet, the logistics network, the clinical teams, and the transplant center relationships that make the NOP work. The technology is necessary but not sufficient. The integrated service model is the moat.

On the reimbursement front, TransMedics benefits from a favorable CMS structure. Organ acquisition costs—including transportation, preservation, and perfusion—are reimbursed as a pass-through, separate from the DRG payment for the transplant procedure itself. This means hospitals do not absorb OCS costs into their operating budgets; the costs are passed directly to Medicare. For hospitals, the NOP is essentially free from a budget perspective, while delivering better outcomes. This reimbursement architecture removes the single biggest barrier to adoption in hospital-based healthcare.

To appreciate how unusual this is, consider the typical adoption barrier for medical devices. When a hospital considers a new surgical robot or imaging system, the CFO must justify the capital expenditure against competing priorities. Department heads fight over budget allocations. Procurement committees demand ROI calculations. The process can take years. TransMedics sidesteps all of this. The transplant center does not buy the OCS. It does not lease a console. It does not hire a perfusionist. It simply receives organs through the NOP, and Medicare reimburses the organ acquisition costs as a pass-through. From the hospital's perspective, the NOP is not a capital purchase—it is a clinical service that arrives with its own funding mechanism built in. This is why adoption has been so rapid once transplant centers understood the model.

International expansion represents the next leg of growth. TransMedics plans to replicate the NOP model in Europe, starting with Italy as the first fully operational international market by the end of 2026. The company has appointed Tamer Khayal, M.D. as SVP of International and is in engagement discussions with the Netherlands, Belgium, France, the UK, and Switzerland. European transplant systems face the same cold storage limitations and organ shortage dynamics as the U.S., and the NOP's value proposition translates directly. However, international expansion is far from guaranteed. European nations have nationalized healthcare systems with distinct regulatory frameworks, procurement structures, and reimbursement models. The NOP cannot simply be copy-pasted from the United States—each market will require localized regulatory clearances, partnerships with national transplant authorities, and potentially different pricing structures. The OCS devices already carry CE Mark certification, which simplifies the technology side, but building the aviation and logistics infrastructure across fragmented European airspace, with its own safety regulations and operational constraints, will require significant investment and patience.

VIII. The Science and Technology Deep Dive

For readers who are not biomedical engineers, the Organ Care System deserves a closer look, because understanding the technology is essential to understanding why TransMedics' competitive position is so durable.

Think of the OCS as a portable intensive care unit for a single organ. In a hospital ICU, a patient receives warm blood, oxygen, nutrients, and continuous monitoring. The OCS does the same thing for a heart, lung, or liver—except the patient is the organ itself, and the ICU fits inside a container that can travel in a van or on a jet. If that sounds simple, consider this analogy: taking a fish out of an aquarium, putting it in a bag of water, and carrying it to another aquarium is cold storage. Building a miniature aquarium with its own filtration, oxygenation, temperature control, and water quality monitoring system, and then carrying that entire ecosystem across the country on a jet—that is the OCS.

For a heart, the system works by connecting the excised organ to a closed-loop perfusion circuit. Donor blood—drawn from the donor before procurement—is placed in a reservoir and supplemented with TransMedics' proprietary solutions containing electrolytes, nutrients, and stabilizing agents. A pump draws the blood through an oxygenator, which infuses it with oxygen and removes carbon dioxide, just like the lungs do in a living body. A warming element brings the blood to thirty-seven degrees Celsius. The warm, oxygenated blood then flows into the aorta—the main artery leaving the heart—where it perfuses the coronary arteries that supply the heart muscle. The heart beats. Blood drains back into the reservoir, and the cycle repeats. Sensors continuously measure oxygen saturation, hematocrit, flow rates, and other parameters, displaying them on a monitor that the perfusionist watches throughout the mission.

The biological difference between normothermic and hypothermic preservation is stark. Cold storage suppresses metabolism—it is the biological equivalent of putting a computer in sleep mode. But "sleep mode" is not benign. Without oxygen and nutrients, cells exhaust their ATP reserves, ion pumps fail, calcium accumulates, and cellular damage begins immediately. The heart is particularly vulnerable because its contractile muscle tissue has enormous energy demands. By contrast, normothermic perfusion maintains active metabolism—the organ is "awake," consuming oxygen, producing energy, and maintaining cellular integrity. There is no ischemia, no energy depletion, and critically, no reperfusion injury when the organ is transplanted.

Perhaps the most transformative capability of the OCS is its ability to assess organ viability in real time. With cold storage, a surgeon must make an accept-or-reject decision based on limited donor information—age, cause of death, cold ischemia time—without any direct measurement of organ function. It is a gamble. With the OCS, the clinical team can observe the heart beating, measure its metabolic output, assess its contractile function, and make a data-driven decision about whether the organ is suitable for transplant. This capability is especially powerful for DCD organs—hearts from donors who have died from circulatory arrest rather than brain death.

DCD hearts were historically considered unusable. When a donor's heart stops beating, the organ suffers a period of "warm ischemia"—oxygen deprivation at body temperature—that was thought to cause irreversible damage. Cold storage could not reverse this damage, and there was no way to assess whether a DCD heart could be resuscitated.

The OCS changed this equation entirely. After procurement, a DCD heart is placed on the OCS, perfused with warm oxygenated blood, and literally brought back to life. The clinical team watches it resume beating and assesses its function before deciding whether to proceed with transplantation.

The clinical results were remarkable. In the pivotal trial, ninety of one hundred one DCD hearts placed on OCS were successfully transplanted—an eighty-nine percent utilization rate—with six-month patient survival of ninety-five percent, compared to eighty-nine percent for standard DBD hearts preserved on ice. Let that sink in: hearts from donors who had already died, hearts that would have been discarded under the old paradigm, were resuscitated, assessed, and transplanted with outcomes that were actually better than conventionally preserved hearts from brain-dead donors. TransMedics effectively created a new category of donor hearts that did not exist before. This single capability—DCD heart transplantation—could increase the U.S. heart donor pool by as much as thirty percent, potentially saving thousands of additional lives each year.

Looking ahead, TransMedics has received full and unconditional FDA IDE approval for two next-generation clinical trials: the ENHANCE Heart trial, granted in February 2026 and expected to enroll more than six hundred fifty patients in the largest heart preservation trial ever conducted worldwide; and the DENOVO Lung trial, approved in January 2026. The company is also preparing a clinical program for OCS Kidney, which would extend the platform into the largest transplant organ category by volume—nearly ninety thousand Americans are waiting for kidneys.

The kidney opportunity deserves particular attention because it is the largest single organ market by volume. Approximately thirty-five percent of donated kidneys are discarded, the highest discard rate of any major transplant organ. Kidneys tolerate cold ischemia longer than hearts or lungs, but extended cold storage times are associated with delayed graft function—meaning the transplanted kidney does not work immediately and the patient requires dialysis while the organ "wakes up." Normothermic perfusion could reduce delayed graft function rates, enable better assessment of marginal kidneys, and ultimately reduce the discard rate. If TransMedics can bring an OCS Kidney to market, the addressable case volume would dwarf the company's current heart, lung, and liver businesses combined.

Beyond organ-specific applications, the normothermic perfusion platform has implications that extend well past transplantation as it is practiced today. Researchers are exploring the possibility of using perfusion time to condition or repair organs—administering drugs, gene therapies, or cellular treatments to an organ while it circulates on the OCS, before transplantation. Imagine a liver that arrives with early signs of fatty disease being treated with defatting agents during the flight, arriving at the transplant center in better condition than when it left the donor. This concept—using the transport window as a treatment window—could transform organs that are currently discarded into viable transplants, dramatically expanding the donor pool. The data that TransMedics accumulates from thousands of perfusion cases will be essential to developing these applications, creating a compounding advantage over time.

IX. The Competitive Landscape and Market Dynamics

TransMedics does not operate in a vacuum, but the competitive landscape reveals just how far ahead it has moved. The three most relevant competitors—Paragonix Technologies, OrganOx, and XVIVO Perfusion—each occupy a different niche, and none approaches TransMedics' breadth.

Paragonix Technologies, recently acquired by Swedish medical device company Getinge for four hundred seventy-seven million dollars, makes the SherpaPak Cardiac Transport System. The SherpaPak is not a perfusion device—it is a sophisticated cooler. It maintains hearts at controlled hypothermic temperatures with precise monitoring, and clinical data has shown meaningful improvements over traditional ice: a fifty percent reduction in severe primary graft dysfunction and fifty-four percent reduction in four-year mortality compared to standard ice storage. It is significantly cheaper and simpler than the OCS. Paragonix claims roughly fifty-four percent market share in static cold storage for hearts. But the SherpaPak cannot resuscitate DCD hearts, cannot assess organ viability in real time, and cannot extend preservation times beyond cold ischemia limits. It is a better cooler, not a new paradigm.

OrganOx, based in the UK, makes the metra—a normothermic machine perfusion device for livers. The metra is the closest technological competitor to TransMedics' OCS Liver: it keeps livers warm, oxygenated, and functioning for up to twenty-four hours. OrganOx has reported more than six thousand clinical uses globally and received FDA clearance for air transport operations in 2025. In February 2025, the company raised one hundred forty-two million dollars in funding. But OrganOx is a liver-only specialist. It does not address hearts or lungs, does not operate an aviation fleet, and does not offer an integrated procurement service.

XVIVO Perfusion, a publicly traded Swedish company, offers the STEEN Solution and XPS system for ex-vivo lung perfusion—a technology used primarily in transplant centers to assess and recondition initially unacceptable donor lungs before transplantation. XVIVO also has a cold perfusion device for hearts under development. The key difference is that XVIVO's system is typically center-based—it assesses organs at the transplant hospital rather than preserving them during transport. XVIVO has strong international presence, particularly in Europe, but lacks TransMedics' integrated logistics model.

It is worth noting what each competitor does not do, because the gaps define TransMedics' strategic position. Paragonix does not perfuse—it cools better. OrganOx does not transport—it perfuses at the hospital or during transport, but only livers. XVIVO does not offer logistics—it sells technology. None of them operates an aviation fleet. None offers a turnkey procurement service. None addresses all three major organs on a single platform. TransMedics is the only company that combines warm perfusion technology for hearts, lungs, and livers with an integrated aviation and clinical logistics network. This is not a marginal advantage. It is a categorical difference—like comparing a taxi dispatcher to Uber's full platform in the early days of ride-sharing.

The broader ecosystem includes fifty-five to fifty-seven federally designated organ procurement organizations—nonprofit monopolies, each controlling organ procurement in a specific geographic region. These OPOs have historically managed the logistics of organ recovery and transport, often using commercial flights or ad-hoc charter services.

TransMedics' NOP effectively competes with and complements the OPO system: it offers transplant centers an alternative procurement pathway that delivers better-preserved organs more reliably. The relationship between TransMedics and OPOs is complex—the company works with some OPOs as partners while its integrated model inherently disrupts others. This dynamic bears watching, because OPOs wield significant influence over organ allocation in their regions, and their cooperation or resistance can meaningfully affect TransMedics' ability to access donors.

The question of whether a large medtech company—Medtronic, Abbott, Johnson and Johnson, or Boston Scientific—might acquire TransMedics is a perennial topic in investor discussions. The company's market capitalization of roughly four to four-and-a-half billion dollars is within acquisition range for any of these players. TransMedics' technology, regulatory approvals, and operational infrastructure would be extraordinarily difficult to replicate organically. But the aviation and logistics components make TransMedics unusual—it is not a clean fit for a traditional device company's operating model. A potential acquirer would need to be comfortable operating an airline, which may limit the pool of interested buyers. There is also the Hassanein factor—the company has been founder-led for twenty-eight years, and it is unclear whether it would function the same way under corporate ownership. History suggests that founder-led platform companies with deep operational complexity—think FedEx under Fred Smith or DaVita under Kent Thiry—lose something essential when the founder departs.

The OPO reform movement adds another dynamic to the competitive landscape. The fifty-five to fifty-seven federally designated organ procurement organizations that control organ procurement in the United States have historically operated as local monopolies with minimal accountability. A bipartisan push for reform—culminating in the Securing the U.S. Organ Procurement and Transplantation Network Act signed by President Biden—has begun dismantling the UNOS monopoly on OPTN management and introducing performance-based metrics for OPOs. This reform is broadly positive for TransMedics: it increases transparency around organ discard rates, creates pressure on underperforming OPOs to improve recovery, and aligns incentives toward the kind of organ utilization maximization that normothermic perfusion enables. But it also introduces uncertainty about how the procurement ecosystem will evolve and whether OPOs will become more collaborative with or more resistant to TransMedics' NOP model.

Policy tailwinds are accelerating. The shift to continuous distribution allocation—already implemented for lungs in March 2023 and under development for hearts and livers—eliminates geographic boundaries in organ allocation and uses a composite score to match donors and recipients nationally. This means organs travel farther: UNOS data showed an additional 1.5 million miles of lung transport and 3.1 million miles of heart transport under the new policy. Longer distances amplify the limitations of cold storage and strengthen the case for normothermic perfusion with dedicated air transport—precisely what TransMedics provides. Additionally, the CMS IOTA model, which took effect in July 2025, creates direct financial incentives for kidney transplant hospitals to increase transplant volumes, rewarding them with performance-based payments of up to fifteen thousand dollars per Medicare transplant. Technologies that enable hospitals to accept more organs become more valuable under this framework.

X. Strategy and Playbook: Business Lessons

TransMedics offers a masterclass in several strategic principles that are worth examining closely.

The most important lesson is knowing when to transform your business model. For nearly two decades, TransMedics operated as a conventional medical device company: build the device, win FDA approval, sell it to hospitals. This model was not working. Adoption was slow, revenue was anemic, and the company was burning cash.

Many companies in this position would have doubled down—hired more salespeople, offered more training, reduced prices. Hassanein did something far more radical: he reimagined the entire value chain. Instead of selling a device and hoping hospitals would figure out how to use it, he built a full-stack service that solved the complete problem. The lesson for founders and investors is that sometimes the technology is right but the business model is wrong, and fixing the business model can unlock value that the technology alone cannot.

Vertical integration—the decision to control procurement, perfusion, transportation, and delivery—contradicts the prevailing wisdom in modern business, which favors asset-light models and outsourcing. TransMedics went the opposite direction, buying jets and hiring pilots. The logic was specific to the company's situation: the organ transplant logistics chain was fragmented, unreliable, and not optimized for the OCS's requirements. Commercial flights introduce unpredictable delays. Charter operators lack transplant-specific expertise. By controlling its own fleet, TransMedics ensures that every mission is optimized for organ preservation, with dedicated aircraft, trained crews, and predictable scheduling. The comparison to FedEx is instructive—Fred Smith made the same bet in the 1970s when he decided that reliable overnight delivery required controlling the entire logistics chain rather than relying on commercial airlines. TransMedics has made an analogous bet in healthcare.

Hassanein's role as a founder-CEO with deep medical credibility has been a significant competitive advantage. Unlike a professional manager parachuted into a medical device company, Hassanein published the original research, designed the clinical trials, and understood the biology of organ preservation at a level that earned the trust of transplant surgeons. His clinical authority gave TransMedics credibility in a field where surgeon adoption requires peer-to-peer validation. This "founder-led advantage" is a pattern seen in other transformative healthcare companies—the combination of scientific expertise and entrepreneurial drive creates a conviction that hired management rarely matches.

The "whole product" strategy—solving the entire problem rather than just selling a component—is a framework from Geoffrey Moore's Crossing the Chasm. The OCS device alone was a component. The National OCS Program is the whole product: technology, clinical expertise, logistics, and transportation bundled into a service that delivers measurable value. Transplant centers do not buy the OCS; they buy more transplants, better outcomes, and expanded donor access. This reframing—from device to outcome—was the key insight that unlocked commercial adoption.

Capital allocation during TransMedics' journey offers its own set of lessons. During the long pre-revenue years, the company raised capital conservatively enough to survive but aggressively enough to fund the clinical trials that would ultimately win FDA approval. The 2019 IPO came at precisely the right moment—just after the first lung approval, when the company could demonstrate regulatory progress to public market investors, but before the NOP transformation had begun. The public market capital gave TransMedics the resources to build its aviation fleet and logistics infrastructure. Had the company gone public too early (when it had no FDA approvals) or too late (after the NOP was already scaling), the capital structure might have looked very different. The timing was impeccable, whether by design or fortune.

The concept of creating new reimbursement categories deserves particular attention. TransMedics did not simply slot into an existing payment framework. It worked within the CMS organ acquisition cost reimbursement structure—a pass-through mechanism that separates procurement costs from the hospital's DRG payment for the transplant itself—to ensure that the NOP's fees would be covered by Medicare without coming out of the hospital's operating budget. This structural feature eliminates the single biggest barrier to healthcare technology adoption: hospital budget constraints. When a transplant center uses the NOP, the cost is borne by the payer system, not by the hospital's P&L. This reimbursement architecture, combined with the CMS IOTA model that directly rewards hospitals for increasing transplant volumes, creates a uniquely favorable economic environment for TransMedics' service.

For deep tech founders, TransMedics offers both inspiration and a cautionary timeline. From founding in 1998 to commercial proof in 2022—when revenue first inflected—was twenty-four years. Two full decades of R&D, clinical trials, regulatory battles, and capital raises before the business model worked. This is not unusual for platform medical technologies—Intuitive Surgical spent a decade developing the da Vinci surgical robot before reaching commercial scale—but it demands a level of patience, persistence, and access to capital that few founders and investors can sustain. TransMedics raised hundreds of millions in private capital before its IPO and continued burning cash for years afterward. The lesson is not that deep tech is easy. The lesson is that when the technology finally works and the business model clicks, the resulting competitive position can be nearly unassailable.

XI. Porter's Five Forces and Hamilton's Seven Powers

TransMedics operates in a market structure that is unusually favorable for the incumbent, and a rigorous strategic analysis reveals why.

Barriers to entry are among the highest in medical technology. A new entrant seeking to replicate TransMedics' position would need to simultaneously achieve FDA pre-market approval for organ perfusion devices—a process requiring years of clinical trials and hundreds of millions in investment—obtain FAA certification for an aviation fleet, build a network of regional logistics hubs, recruit and train hundreds of clinical and aviation professionals, and establish relationships with transplant centers nationwide. Each of these barriers is substantial on its own. Together, they create a wall that no potential competitor can realistically scale in less than a decade. The capital intensity alone—TransMedics has invested hundreds of millions in its fleet, hubs, and clinical infrastructure—makes this a market where deep pockets are necessary but not sufficient.

Supplier power is moderate. TransMedics sources aircraft from Embraer, medical consumables from multiple vendors, and employs clinical and aviation staff in competitive labor markets. None of these inputs are monopoly-controlled, and alternatives exist for most supply categories. Aircraft leasing markets are deep and liquid. However, the specialized clinical staff—perfusionists and organ procurement surgeons—are in limited supply, and labor constraints could emerge as the NOP scales.

Buyer power is moderate to low. Transplant centers are the primary customers, and their alternatives are limited: cold storage (inferior outcomes), building in-house procurement capabilities (expensive and complex), or simply performing fewer transplants (unacceptable). Once a center integrates into the NOP, the value proposition—more organs, better quality, zero capital expenditure—is compelling. Buyer power is further constrained by the CMS reimbursement structure, which passes organ acquisition costs through to Medicare rather than requiring the hospital to absorb them.

The threat of substitutes is low in the near term. Cold storage is the primary substitute, and it is demonstrably inferior for hearts and increasingly viewed as suboptimal for lungs and livers. Organ bioprinting and xenotransplantation—growing organs from scratch or transplanting animal organs into humans—are theoretical substitutes, but they remain ten to twenty years from clinical reality at scale. In the meantime, normothermic perfusion with integrated logistics is the best available solution for the organ shortage.

Competitive rivalry is low. TransMedics is the only company in the world that offers a vertically integrated, multi-organ normothermic perfusion platform with dedicated aviation and logistics. Paragonix competes in cold storage, OrganOx in liver perfusion, and XVIVO in lung perfusion, but none offers the full-stack NOP service. The market is functionally a monopoly for the integrated model, though competition at the individual organ level is more meaningful.

Through Hamilton Helmer's Seven Powers framework, TransMedics' durability becomes even clearer. Scale economies are present and growing: aircraft utilization, route density, and clinical team productivity all improve with volume, creating cost advantages that new entrants cannot match at small scale. Network effects operate in a distinctive way: as more transplant centers join the NOP, the network covers more geographic territory, enabling access to more donors, which produces more organs, which improves outcomes, which attracts more centers. This is a classic two-sided network effect between donor coverage and transplant center adoption.

Counter-positioning may be TransMedics' most powerful strategic advantage. Traditional medical device companies—Medtronic, Abbott, Stryker—could theoretically build an organ perfusion device. But they cannot build the NOP. Their business models are designed around selling devices to hospitals, not operating aviation fleets and clinical procurement teams. Replicating TransMedics' model would require a device company to enter entirely unfamiliar industries—aviation, logistics, organ procurement—and accept the margin dilution and operational complexity that comes with them. Rational incumbents will not do this. They will focus on their core business, and TransMedics' model will continue to diverge from anything they can offer.

This is the essence of counter-positioning as Hamilton Helmer defines it: a new entrant adopts a superior business model that the incumbent cannot replicate without cannibalizing or fundamentally restructuring its existing operations. Medtronic earns forty percent operating margins selling devices. Why would it voluntarily enter a business that requires buying jets, hiring pilots, managing twenty-four-seven operations, and navigating FAA regulations—all to serve a market that is a rounding error on its income statement? The rational answer is that it would not, and that is precisely why TransMedics' position is defensible. The bigger the incumbent, the less sense it makes for them to replicate the NOP.

Switching costs are high. Once a transplant center has built its program around NOP-delivered organs, reverting to the old model means fewer transplants, worse outcomes, and operational disruption.

Cornered resources include FDA approvals (five-to-ten-year advantage over competitors), a proprietary perfusion data repository growing with every case, and deep operational expertise in organ procurement logistics.

Process power—the institutional knowledge embedded in twenty-four-seven operations, cross-functional coordination between clinical and aviation teams, and regulatory compliance across FDA, FAA, and state-level requirements—is difficult to articulate but even more difficult to replicate. How do you hire, train, and coordinate a team that can dispatch a surgical crew to a donor hospital at three in the morning, manage a complex perfusion operation, fly the organ across two time zones, and deliver it to a transplant surgeon who is scrubbing in at that very moment? That capability is not built overnight. It is accumulated through thousands of missions, refined through operational learning, and embedded in institutional processes that take years to develop.

The primary powers driving long-term durability are network effects, switching costs, and cornered resources (regulatory approvals). The moat deepens with every organ transported, every transplant center added to the network, and every year that competitors spend in the clinical trial process. This is a winner-take-most market, and TransMedics holds the winning position.

XII. Bull Case, Bear Case, and Key Risks

The bull case for TransMedics begins with total addressable market expansion. Today, roughly forty-eight thousand organ transplants are performed annually in the United States. But the organ shortage is a supply problem, not a demand problem—more than one hundred thousand people are waiting.

If normothermic perfusion can reduce discard rates, enable DCD organ utilization, and extend preservation times enough to make national organ sharing practical, the total number of transplants could grow dramatically. Some bull-case analysts envision a doubling of annual U.S. transplants within a decade, with TransMedics capturing a dominant share. At roughly one hundred thousand dollars in revenue per NOP case, even modest market expansion implies a multi-billion-dollar domestic revenue opportunity.

International expansion adds another dimension. Europe performs comparable volumes of organ transplants to the United States but faces the same cold storage limitations and organ shortage dynamics. TransMedics plans to launch the NOP model in Italy by the end of 2026, with the Netherlands, Belgium, France, the UK, and Switzerland in the pipeline. If the company can replicate even a fraction of its U.S. success internationally, the revenue opportunity roughly doubles.

Technology evolution strengthens the bull case. The ENHANCE Heart trial, with full FDA IDE approval as of February 2026, aims to demonstrate superiority—not just non-inferiority—of OCS Heart perfusion over cold storage. If successful, this could accelerate adoption from the current eighteen percent of U.S. heart transplants toward majority market share. OCS Kidney, currently in preparation for clinical launch, would extend the platform into the largest transplant organ category by volume. And future applications—AI-driven viability assessment, drug delivery during perfusion, extended preservation times—could further expand the addressable market.

Operating leverage is the financial bull case. Gross margins are already at sixty percent. Operating margins expanded roughly seven hundred fifty basis points in 2025 and management targets thirty percent by 2028. The fixed-cost infrastructure—jets, hubs, command center—is largely built. Each incremental NOP case leverages that infrastructure at high marginal contribution. If revenue reaches the seven-hundred-fifty-million-dollar guided range in 2026 and continues growing twenty-plus percent annually, operating profit could scale rapidly. The parallel to Intuitive Surgical's margin expansion is instructive—Intuitive went from low-teens operating margins in its early commercial years to mid-thirties as its installed base grew and procedure volumes ramped. TransMedics, with its similarly high fixed-cost, high-margin-per-case model, could follow a comparable trajectory if case volumes continue growing.

Additionally, the acquisition premium scenario remains alive. A strategic buyer—whether a large medtech company looking to enter transplant logistics, a private equity firm attracted by the recurring revenue model, or even a healthcare services company seeking to expand into organ transplantation—could see TransMedics' regulatory moat, clinical data, and operational infrastructure as worth a significant premium to the current market capitalization. The company's unique position as the only vertically integrated organ transplant platform in the world makes it a one-of-a-kind asset.

The bear case centers on execution risk and competitive threats.

Aviation is operationally complex, and TransMedics must maintain FAA compliance, manage pilot and clinical staff scheduling, and ensure aircraft reliability across thousands of time-critical missions annually. Any high-profile operational failure—a missed organ delivery, an aircraft incident, a perfusion system malfunction—could damage the company's reputation with transplant centers and invite regulatory scrutiny. The company operates under dual regulatory oversight from both the FDA and the FAA—a combination that no other medical device company faces—and a compliance failure in either domain could have cascading consequences.

Competition is intensifying, and this is the risk that deserves the most careful attention. Paragonix, now backed by Getinge's global resources and distribution network, has a lower-cost cold storage product that may be adequate for many standard-criteria organs. OrganOx, with one hundred forty-two million in fresh capital raised in February 2025, is advancing its liver perfusion technology and recently received FDA clearance for air transport operations. XVIVO is developing heart and kidney perfusion devices that could offer simpler, less capital-intensive alternatives to the OCS.

While none of these competitors matches TransMedics' integrated model, they could erode market share in specific organ categories, particularly if their technologies prove to be "good enough" for routine transplants at a fraction of the cost. The competitive threat is not that someone builds a better OCS—it is that someone builds a simpler, cheaper preservation technology and argues that the full NOP infrastructure is overkill for standard-criteria organs.

Reimbursement risk cannot be ignored. TransMedics' revenue depends on Medicare and private insurers continuing to reimburse organ acquisition costs—including NOP service fees—as a pass-through.

Any CMS policy change that caps or reduces organ acquisition cost reimbursement would directly impact TransMedics' pricing power and margins. Given the current political environment and ongoing debates about healthcare spending, this is not a theoretical risk.