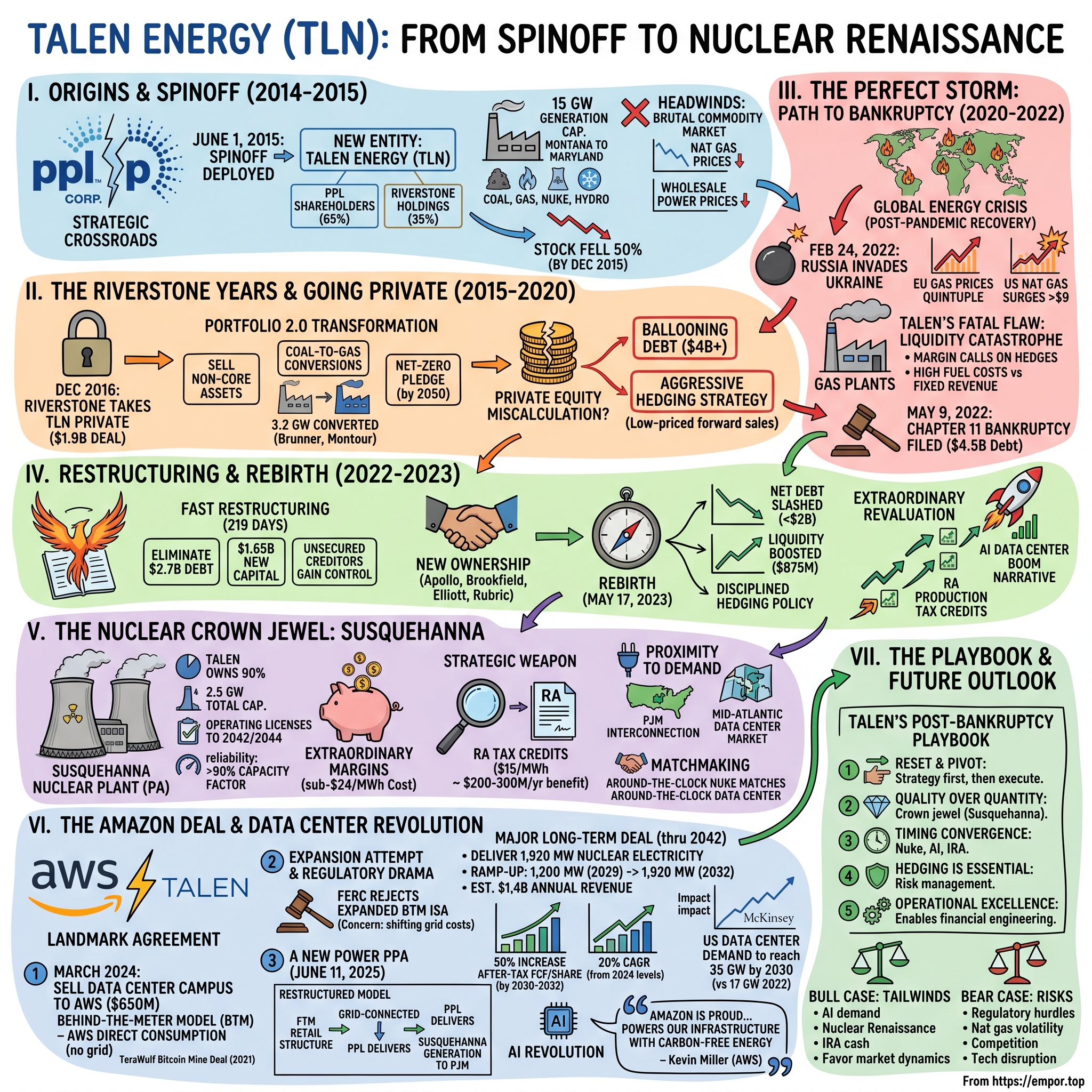

Talen Energy: From Spinoff to Nuclear Renaissance

I. Introduction & Episode Setup

Picture this: May 2022. Natural gas prices are soaring, energy markets are in chaos, and a power company named Talen Energy files for Chapter 11 bankruptcy with $4.5 billion in debt. Fast forward just two years—June 2024—and that same company is signing a landmark deal with Amazon Web Services for up to 1,920 megawatts of nuclear power, enough to power a small city or, more relevantly, the AI revolution's insatiable appetite for electrons.

This is not your typical turnaround story. This is the tale of how a utility spinoff went from Wall Street darling to private equity portfolio company to bankruptcy court to becoming the poster child for America's nuclear renaissance—all in less than a decade.

Today, Talen Energy stands as an independent power producer with 10.7 gigawatts of generation capacity spread across the competitive power markets of the United States. But the crown jewel? Their 90% ownership stake in the Susquehanna nuclear plant in Pennsylvania—2.2 gigawatts of carbon-free baseload power that's become the foundation for what might be the most important infrastructure story of the AI age.

The core question we're exploring: How did a twice-private, once-bankrupt utility spinoff transform into the company best positioned to power the data center boom? The answer involves private equity miscalculations, commodity market chaos, brilliant financial engineering, and perhaps most importantly, being in exactly the right place at exactly the right time with exactly the right assets.

What unfolds is a masterclass in crisis management, strategic positioning, and the value of nuclear baseload in an increasingly electrified world. It's also a cautionary tale about leverage, hedging, and what happens when financial engineering meets the brutal realities of commodity markets.

II. The PPL Origins & Spinoff Era (2014-2015)

The story begins not with Talen, but with PPL Corporation, a Pennsylvania utility that in 2014 faced a strategic crossroads. For decades, PPL had operated as a traditional integrated utility—owning both regulated distribution networks and unregulated power generation assets. But CEO Bill Spence saw the writing on the wall: the competitive generation business was becoming increasingly volatile, capital-intensive, and divorced from the steady, predictable returns that utility investors craved.

"We need to pick a lane," Spence reportedly told his board in late 2013. The lane PPL chose was pure-play regulated utilities, setting in motion one of the most significant utility spinoffs of the decade.

The mechanics were elegant in their simplicity. On June 1, 2015, PPL shareholders received 0.125 shares of a new entity—Talen Energy Corporation—for each share of PPL they owned. This gave PPL shareholders 65% of the new company. The remaining 35%? That went to Riverstone Holdings, a private equity firm specializing in energy investments, which contributed its own portfolio of power plants to create what would become one of America's largest independent power producers.

Paul Farr, a PPL veteran with three decades of experience in competitive markets, was tapped to lead the new entity. His vision was ambitious: combine PPL's 9,000 megawatts of generation with Riverstone's 6,000 megawatts to create a 15,000-megawatt colossus that could compete with the likes of NRG and Calpine. The portfolio was geographically diverse—spanning from Montana to Maryland—and fuel-diverse, with coal, natural gas, nuclear, and even some hydro assets.

But from day one, Talen faced headwinds that would define its trajectory. The Federal Energy Regulatory Commission (FERC) imposed strict market mitigation requirements, forcing Talen to divest certain assets to prevent market concentration. More problematically, the company emerged into a power market experiencing a historic collapse in prices. Natural gas was plummeting toward $2 per million BTU, renewable energy was flooding the grid with subsidized capacity, and wholesale power prices were hitting multi-decade lows.

The spinoff structure itself created complications. PPL shareholders, accustomed to steady utility dividends, suddenly owned shares in a volatile merchant power company. Riverstone, meanwhile, had different incentives—they wanted to optimize the portfolio, potentially take the company private, and generate private equity-style returns. This misalignment would soon become apparent.

By December 2015, just six months after the spinoff, Talen's stock had fallen 50%. The company that was supposed to be a "best-in-class" independent power producer was instead struggling to find its footing in a brutal commodity environment. The stage was set for Riverstone to make its move.

III. The Riverstone Years & Going Private (2015-2020)

Riverstone didn't wait long. By December 2016, barely 18 months after the spinoff, the private equity firm completed its acquisition of the remaining 65% of Talen it didn't already own, taking the company private in a $1.9 billion deal that valued the equity at just $14 per share—a far cry from the mid-$20s where it had briefly traded post-spinoff.

Under private equity ownership, Talen underwent what Riverstone partners called "Portfolio 2.0"—a strategic transformation aimed at modernizing the generation fleet and improving cash flow stability. The playbook was classic private equity: sell non-core assets, convert coal plants to cleaner-burning natural gas, optimize operations, and prepare for an eventual exit.

The coal-to-gas conversions were particularly ambitious. Talen committed to converting 3.2 gigawatts of coal capacity to natural gas, recognizing that coal's economics were becoming increasingly untenable. The Brunner Island facility in Pennsylvania, the Montour plant, and several others underwent multi-hundred-million-dollar transformations. The engineering was complex—retrofitting decades-old boilers to burn a completely different fuel—but the economics seemed compelling with natural gas prices remaining stubbornly low.

Mac McFarland, who would later become CEO, joined during this period as Chief Commercial Officer. A Duke Energy veteran with deep trading and risk management experience, McFarland brought a sophisticated understanding of power markets that would prove crucial in the tumultuous years ahead. "We're not just plant operators," he would tell his team. "We're essentially running a massive commodity hedge fund with physical assets."

By November 2020, Riverstone announced Talen's commitment to a "clean energy future," pledging to achieve net-zero carbon emissions by 2050. The announcement felt both prescient and reactive—prescient because it positioned Talen ahead of the energy transition curve, reactive because institutional investors were increasingly shunning fossil fuel investments.

But here's where the private equity playbook collided with market realities. Power generation is not a software company or a consumer brand that can be quickly optimized and flipped. It's a capital-intensive, highly regulated business subject to commodity price swings, regulatory changes, and multi-year investment cycles. Riverstone's typical 5-7 year hold period was running up against these structural realities.

The company's debt load, meanwhile, had ballooned to over $4 billion as Riverstone used leverage to juice returns—standard private equity practice, but dangerous in a volatile commodity business. More critically, Talen's hedging strategy became increasingly aggressive, or perhaps more accurately, increasingly sparse. As natural gas prices remained low through 2020 and early 2021, the company reduced its forward hedges, essentially making a massive bet that energy prices would remain subdued.

By late 2021, that bet was starting to look catastrophically wrong. Natural gas prices began climbing from historic lows, power prices followed, and Talen found itself dangerously exposed. The company that had gone private to escape public market volatility was about to face something far worse.

IV. The Perfect Storm: Path to Bankruptcy (2020-2022)

The first warning signs appeared in European energy markets. By September 2021, natural gas prices in Europe had quintupled from their 2020 lows as post-pandemic demand recovery collided with supply constraints. U.S. markets, long insulated by domestic shale production, initially shrugged off the European crisis. Talen's management, like many in the industry, believed American gas prices would remain range-bound between $2-4 per million BTU.

Then came February 24, 2022: Russia invaded Ukraine.

Within weeks, the global energy complex went haywire. European gas prices hit the equivalent of $70 per million BTU. U.S. prices, pulled higher by LNG exports, surged past $9—levels not seen since the 2008 financial crisis. For Talen, with its under-hedged position and significant gas-fired generation, this was a liquidity catastrophe in real-time.

Here's the cruel irony: Talen's power plants were printing money. Wholesale electricity prices in PJM, Talen's primary market, were soaring as natural gas set the marginal price. The Susquehanna nuclear plant, with its low variable costs, was generating extraordinary margins. But Talen had a fatal flaw—it had sold forward power at fixed prices without adequately hedging its input costs. As gas prices rose, so did the cost of generating power from its gas plants, but the revenue from those forward sales remained fixed.

The math was brutal. Every dollar increase in natural gas prices meant roughly $200 million in additional annual fuel costs for Talen's gas fleet. By March 2022, the company was burning through cash at an unsustainable rate, facing margin calls on its hedging positions, and struggling to meet debt service obligations.

On May 9, 2022, Talen Energy filed for Chapter 11 bankruptcy protection in the Southern District of Texas, listing $4.5 billion in funded debt obligations. The filing was, in many ways, a formality—the company had been negotiating with creditors for months, and a pre-packaged restructuring plan was already taking shape.

The bankruptcy filing revealed the extent of the damage. Talen had negative working capital of nearly $500 million, its liquidity had evaporated, and its capital structure was simply incompatible with the volatile commodity environment it faced. But buried in the filing was an interesting detail: the company's nuclear assets, particularly Susquehanna, remained highly profitable and strategically valuable.

The restructuring strategy was swift and surgical. Rather than a drawn-out bankruptcy that would destroy value, Talen and its creditors agreed to a pre-negotiated plan that would eliminate $2.7 billion in debt, raise $1.65 billion in new capital, and give control to the unsecured creditors. The speed was essential—every day in bankruptcy meant lost commercial opportunities and potential regulatory complications.

By December 2022, just 219 days after filing, Talen's restructuring plan was confirmed by the bankruptcy court. It was one of the fastest large-scale energy bankruptcies in recent history, a testament to both the clarity of the problem (too much debt, not enough hedging) and the underlying value of the assets.

V. Restructuring & Rebirth (2022-2023)

The financial engineering that brought Talen out of bankruptcy was a masterclass in restructuring. The plan's centerpiece was a $1.4 billion rights offering backstopped by the unsecured creditors, combined with $1.2 billion in new senior secured notes. The existing equity was wiped out—Riverstone's investment went to zero—while unsecured creditors received 97.5% of the reorganized company's equity.

But the real story was who emerged in control. The new shareholder base read like a who's who of distressed debt investing: Apollo, Brookfield, Elliott Management, and Rubric Capital. These weren't passive investors; they were sophisticated operators who understood both the immediate challenges and long-term opportunities in power markets.

Mac McFarland's elevation to CEO in early 2023 signaled a new direction. Unlike his predecessors who came from traditional utility backgrounds, McFarland was a markets guy—someone who understood trading, risk management, and the importance of matching assets with liabilities. His first priority was crystal clear: "We will never again be in a position where commodity price movements can threaten our solvency."

Talen emerged from bankruptcy on May 17, 2023, with a transformed balance sheet. Net debt had been slashed from $4.5 billion to under $2 billion. The company had $875 million in liquidity. Most importantly, it had a disciplined hedging policy that required minimum hedge ratios for forward power sales.

The equity began trading over-the-counter in June 2023 at around $65 per share, implying an enterprise value of roughly $6 billion. Within six months, the stock had more than doubled. By early 2024, it had quadrupled. The creditors who had taken control in the bankruptcy had generated 400% returns in less than a year—one of the most successful bankruptcy recoveries in energy sector history.

What drove this extraordinary revaluation? Part of it was simply the removal of bankruptcy overhang and the cleaned-up balance sheet. But the bigger story was a fundamental shift in how markets were valuing certain power assets, particularly nuclear plants. The Inflation Reduction Act, passed in August 2022 while Talen was in bankruptcy, included production tax credits for existing nuclear plants—a game-changer for Susquehanna's economics.

More subtly but perhaps more importantly, a new narrative was emerging around data centers, artificial intelligence, and the massive electricity demand they would create. Talen, with its nuclear baseload and strategic locations near major data center markets, was suddenly positioned at the intersection of two of the market's most powerful themes: the AI boom and the nuclear renaissance.

VI. The Nuclear Crown Jewel: Susquehanna

To understand Susquehanna's significance to Talen, you need to grasp a fundamental truth about nuclear economics: these plants are money-printing machines when operated well, but financial sinkholes when operated poorly. Susquehanna, with Talen owning 90% and Allegheny Electric Cooperative owning the remaining 10%, represents 2.5 gigawatts of carbon-free baseload capacity—making it the sixth largest nuclear-powered generation facility in the United States.

The plant's economics are staggering. In 2023, Talen's 90% stake produced more than 18 gigawatt-hours at an all-in cost of less than $24 per megawatt-hour. In a world where wholesale power prices regularly exceed $50-100/MWh, those margins are extraordinary. Susquehanna's generation typically accounts for approximately half of Talen's total annual megawatts generated, making it not just an asset but the foundation of the entire enterprise.

Built in the early 1980s with Bechtel as the prime contractor, Susquehanna consists of two General Electric boiling water reactors that have operated with remarkable consistency for four decades. The Nuclear Regulatory Commission extended the operating licenses through 2042 for Unit 1 and 2044 for Unit 2, providing decades of remaining operational life—crucial for long-term power purchase agreements.

But what transformed Susquehanna from a steady cash generator into a strategic weapon was the Inflation Reduction Act's nuclear production tax credit. Starting in 2024, existing nuclear plants can receive up to $15 per megawatt-hour in tax credits, depending on prevailing power prices. For Susquehanna, generating roughly 20 million MWh annually from Talen's share, this translates to potential tax benefits of $200-300 million per year—pure margin improvement that drops straight to the bottom line.

The plant's location, seven miles northeast of Berwick, Pennsylvania, places it perfectly within PJM Interconnection, the world's largest competitive wholesale electricity market. This isn't just about geography; it's about proximity to demand centers. The mid-Atlantic region hosts the highest concentration of data centers in the United States, with Northern Virginia alone accounting for over 35% of global hyperscale capacity.

What makes Susquehanna particularly valuable in the modern context is its ability to provide "behind-the-meter" power—electricity that doesn't need to traverse the increasingly congested transmission grid. Talen's subsidiary Cumulus Data developed a data center campus directly connected to the plant, completing phase 1 construction in January 2023 and selling it to Amazon Web Services for $650 million in March 2024.

The operational excellence story is equally important. Unlike many nuclear plants that struggled with capacity factors in the 70-80% range, Susquehanna has consistently operated above 90%, meaning it produces power more than 90% of the time. This reliability is gold for data center customers who need 24/7/365 uptime.

Mac McFarland understood this dynamic perfectly: "Around-the-clock nuclear power matches very well with around-the-clock data center power needs". In a world where a single hour of downtime at a hyperscale data center can cost millions, the reliability of nuclear baseload becomes a competitive advantage that's nearly impossible to replicate with intermittent renewables or even natural gas plants that require fuel deliveries and maintenance windows.

The strategic importance extends beyond current operations. Susquehanna's site has space for potential small modular reactors (SMRs) and the existing infrastructure—cooling systems, transmission connections, security protocols—that make additional nuclear development far more economical than greenfield sites. With the plant's existing licenses and community acceptance, Susquehanna represents optionality for the next generation of nuclear technology.

VII. The Amazon Deal & Data Center Revolution

The story of how Talen transformed from a distressed power producer into the preferred partner for the world's largest data center operator began with a simple realization: nuclear plants and data centers are perfect complements. One provides 24/7 carbon-free power; the other needs 24/7 carbon-free power. The execution of this match, however, would prove far more complex than anyone anticipated.

Talen Energy announced its sale of a 960-megawatt data center campus to cloud service provider Amazon Web Services (AWS), a subsidiary of Amazon, for $650 million in March 2024. But this was just the opening move in what would become a multi-billion-dollar chess game between technology giants, power producers, and federal regulators.

The initial transaction was structured as a "behind-the-meter" arrangement—AWS would directly consume power from Susquehanna without that electricity ever touching the broader grid. According to the investor presentation, Talen sold the site and assets of Cumulus Data for $650 million. The deal comprises $350 million at close and $300m escrowed, released upon development milestones anticipated in 2024.

This wasn't Talen's first foray into co-located power consumption. TeraWulf and Talen Energy had reached a deal to build the bitcoin mine next to the Susquehanna twin reactors in 2021, using 50 MW of capacity for cryptocurrency mining. But the Amazon deal represented a quantum leap in scale and strategic importance.

The regulatory drama began when Talen and Amazon sought to expand their arrangement. AWS has agreed to buy power from Talen in 120-MW increments for the data center, which could grow to 960 MW, according to Talen. To facilitate the sale of power to the co-located data center, PJM in June asked FERC to approve an amended ISA among the grid operator, Susquehanna Nuclear and PPL Electric Utilities. The amended ISA would have increased the behind-the-meter connection between the power plant and the co-located data center to 480 MW from 300 MW in the existing ISA.

Then came the bombshell. In November 2024, The Federal Energy Regulatory Commission on Friday rejected an amended interconnection service agreement, or ISA, that would have facilitated expanded power sales to a co-located Amazon data center from a nuclear power plant in Pennsylvania that is majority owned by Talen Energy. On a 2-1 vote, with FERC commissioners Mark Christie and Lindsay See in the majority, the agency found that the PJM Interconnection, which filed the amended ISA, failed to show that provisions in the agreement that contravene the grid operator's existing, or pro forma, ISA were needed.

The rejection sent shockwaves through the industry. American Electric Power and Exelon had challenged the arrangement, arguing it could shift up to $140 million in annual transmission costs onto other ratepayers. FERC agreed, essentially ruling that large customers couldn't bypass grid costs while still maintaining grid connectivity as backup.

But Talen and Amazon didn't give up. Instead, they engineered an even more ambitious solution. U.S.-based Talen Energy has signed a major long-term agreement with Amazon to deliver 1,920 megawatts of carbon-free nuclear electricity to support Amazon Web Services (AWS) operations across Pennsylvania. The press release announced a new power purchase agreement (PPA) on June 11, 2025. It is one of the largest clean energy contracts, providing Amazon with zero-emission electricity through 2042, with an option to extend.

The restructured deal was brilliant in its simplicity. The deal, announced on June 11, restructures a previously approved co-located behind-the-meter (BTM) model into a grid-connected, front-of-the-meter (FTM) retail structure. Under the new arrangement, Talen, an independent power producer (IPP), will serve as AWS's licensed retail electricity provider in Pennsylvania, enabling it to source power from the grid and contract directly with AWS. PPL Electric Utilities will deliver the power across the grid, while generation from the two-unit, 2.5-GW Susquehanna nuclear plant will be injected into PJM Interconnection.

The financial implications are staggering. According to Talen, the PPA is expected to generate up to $1.4 billion in annual revenue once the full contract quantity of 1,920 MW is reached—an estimate that reflects the fully ramped contract volume and incorporates annual price escalators of 2% beginning in 2028. The company projects the contract will drive a 50% increase in after-tax cash flow per share compared to 2026 guidance—reaching more than $8 per share by 2030–2032—and deliver a 20% compound annual growth rate from 2024 levels.

The broader context makes this deal even more significant. In the U.S. alone, data center demand is expected to reach 35 GW by 2030, up from 17 GW in 2022, McKinsey & Company projects. The AI revolution, particularly large language models and generative AI, requires computational power at scales previously unimaginable. A single ChatGPT query consumes 10 times the electricity of a Google search. Training GPT-4 required an estimated 50 GWh of electricity—enough to power 5,000 homes for a year.

Kevin Miller, AWS Vice President of Global Data Centers, highlighted Amazon's broader commitment to Pennsylvania, stating: "Amazon is proud to help Pennsylvania advance AI innovation through investments in the Commonwealth's economic and energy future. That's why we're making the largest private sector investment in state history – $20B – to bring 1,250 high-skilled jobs and economic benefits to the state, while also collaborating with Talen Energy to help power our infrastructure with carbon-free energy".

The deal structure also includes sophisticated optionality. The contract, which runs through 2042, calls for delivering 840 MW to 1,200 MW in 2029 and 1,680 MW to 1,920 MW in 2032. This phased approach allows AWS to scale its infrastructure while providing Talen with predictable, long-term contracted revenues.

What makes this particularly clever is how it positions Talen for future opportunities. The company isn't just selling electrons; it's becoming an integrated energy solutions provider for the digital economy. The Amazon relationship provides a template that can be replicated with Microsoft, Google, Meta, and other hyperscalers desperately seeking reliable, carbon-free power for their AI ambitions.

VIII. Modern Portfolio & Market Position

The transformation of Talen's portfolio from a carbon-heavy legacy fleet to a modern, flexible generation platform represents one of the most ambitious fleet transitions in the independent power sector. Talen owns and operates approximately 10.7 gigawatts of power infrastructure in the United States, including 2.2 gigawatts of carbon-free nuclear power and a significant dispatchable natural gas fleet.

The crown achievement of this transformation was the conversion of 3.2 gigawatts of coal capacity to cleaner-burning fuels. The company has already completed the conversion of approximately 3.2 gigawatts of its legacy coal fleet to lower-carbon fuels, including the Brunner Island (dual fuel) and Montour facilities, which together represent over 25% of its total generation capacity, and Unit 3 of the H.A. Wagner facility which was converted from coal.

These weren't simple fuel switches but complex engineering projects requiring hundreds of millions in capital investment. The Brunner Island facility in Pennsylvania, converted to dual-fuel capability, can now burn either natural gas or coal, providing operational flexibility to respond to market conditions. The conversion was completed in 2016, with coal-firing restricted during EPA Ozone Season and scheduled to cease entirely by year-end 2028.

The Montour plant conversion, completed in 2023, transformed a 1960s-era coal facility into a modern gas-fired operation. The engineering challenges were immense—retrofitting boilers designed for pulverized coal to efficiently burn natural gas while maintaining structural integrity and operational reliability. The Wagner Unit 3 conversion to oil, also completed in late 2023, added another dimension of fuel flexibility to the portfolio.

Talen's 6.3 GW natural gas and oil fleet (of which 3.2 gigawatts is from Brunner Island, Montour, and H.A Wagner Unit 3 after conversion) includes seven technologically diverse natural gas and oil generation facilities across the generation stack (including intermediate and peaking dispatch). This diversity isn't just about fuel mix—it's about operational flexibility. Some units are simple-cycle peakers that can start in minutes to capture price spikes. Others are combined-cycle units that operate as baseload or intermediate dispatch, providing the backbone of non-nuclear generation.

The geographic concentration in PJM Interconnection—the world's largest competitive wholesale electricity market—provides significant advantages. PJM's capacity market, which pays generators to be available during peak demand periods, generated billions in revenue for generators in recent auctions. Talen's strategically located assets, particularly those near load centers in Pennsylvania and Maryland, command premium capacity prices.

But the portfolio isn't without challenges. The Brandon Shores facility in Maryland, scheduled for retirement on June 1, 2025, received a reprieve when PJM determined it was needed for reliability. While scheduled to retire on June 1, 2025, Brandon Shores Units 1 and 2 will continue to operate until May 31, 2029 under a "reliability-must-run" (RMR) agreement to provide power necessary to maintain grid and transmission reliability in and around the City of Baltimore until transmission upgrades to provide reliable power to the area from other sources are complete.

This RMR designation is both blessing and curse—it provides guaranteed cost-of-service revenues through 2028 but also locks Talen into operating an aging coal plant that doesn't fit its clean energy narrative. The situation illustrates the complex reality of energy transition: even as companies race toward cleaner portfolios, grid reliability requirements can force continued operation of legacy assets.

The Montana operations add another dimension to the portfolio. Includes the Colstrip Steam Electric Station, a 2-unit coal-fired generation plant located in Colstrip, Montana, with an owned generating capacity of approximately 222 Megawatts. Talen Montana serves as the plant operator and is a subsidiary of Talen Energy. These assets operate in a different market—the Western Electricity Coordinating Council—providing geographic and market diversification.

In March 2024, Talen made a strategic decision to exit the Texas market entirely, selling its 1.7-gigawatt ERCOT portfolio to CPS Energy for $785 million. The sale reflected a strategic focus on PJM markets where Talen has deeper operational expertise and better positioning for data center opportunities.

The environmental performance tells the transformation story in numbers. The overall carbon intensity of our generation was 0.29 metric tons per MWh in 2023, which is over approximately 50% lower than our carbon intensity in 2010. This dramatic reduction positions Talen as one of the cleaner independent power producers, crucial for attracting ESG-conscious customers and investors.

Looking forward, Talen's July 2025 announcement of acquiring the Moxie Freedom and Bayonne facilities for $3.5 billion net represents a doubling down on the PJM market strategy. The net purchase price reflects an attractive acquisition multiple of 6.7x 2026 EV/EBITDA for two of the most efficient natural gas plants in PJM, at a material discount to current new-build CCGT costs. The transaction is expected to be immediately accretive to free cash flow per share by over 40% in 2026, and over 50% through 2029.

These H-class combined cycle plants, with heat rates of 6,550 Btu/kWh, are among the most efficient gas-fired generators in the country. Their addition increases Talen's annual generation from 40 TWh to 60 TWh, effectively adding "another Susquehanna" worth of generation capacity to serve growing data center demand.

IX. Capital Allocation & Financial Engineering

The capital allocation story at Talen Energy post-bankruptcy represents one of the most aggressive shareholder return programs in the utility sector—a stark contrast to the typical utility playbook of steady dividends and conservative balance sheets.

On December 13, 2024, Talen Energy Corporation announced that the Company has closed on its previously announced $850 million incremental Term Loan B credit facility and the repurchase of an equivalent value of shares of Talen's outstanding common stock from affiliates of Rubric Capital Management LP. But the real kicker? Upon the successful upsizing of the Financing from $600 million to $850 million, the Company determined it would use cash on hand to further increase the value of the Repurchase from $850 million to $1 billion in aggregate purchase price.

The mathematics of this buyback are extraordinary. The company expanded the repurchase from $850 million to $1 billion by using additional cash on hand, buying back 4,893,507 shares at $204.35 per share from Rubric Capital Management LP at a 4% discount to the 15-day VWAP. This single transaction retired nearly 10% of the company's outstanding shares.

Mac McFarland's statement captured the aggressive nature of the program: "Demonstrating our commitment to shareholder returns, we have now repurchased more than 20% of our outstanding Common Stock in the past year and, through these repurchases, have bought back nearly 75% of our market capitalization as of our emergence from bankruptcy in May 2023".

Think about that for a moment. A company that emerged from bankruptcy in May 2023 has, within 18 months, repurchased shares equivalent to 75% of its emergence market capitalization. This isn't just returning capital to shareholders; it's a wholesale transformation of the ownership structure.

The Rubric relationship deserves special attention. Rubric Capital Management, one of the major creditors who took control during the bankruptcy, has been systematically monetizing its position—but at negotiated prices that benefit both parties. The 4% discount to VWAP provides Rubric with liquidity for large blocks while giving Talen accretive buybacks without the market impact of open-market purchases.

The financing strategy is equally sophisticated. Rather than using precious cash or issuing equity, Talen tapped the leveraged loan market with Term Loan B financing—typically the cheapest form of institutional debt for companies with stable cash flows. The timing was impeccable, coming just as the Amazon deal was demonstrating the value of Talen's nuclear assets and before potential Federal Reserve rate cuts in 2025.

For full year 2024, Talen reported GAAP Net Income of $998 million, Adjusted EBITDA of $770 million, and Adjusted Free Cash Flow of $283 million, exceeding 2024 guidance midpoints. The company demonstrated robust operational performance with a Fleet EFOF of 2.2% and total generation of 36.3 TWh, with 50% from carbon-free nuclear generation.

The nuclear production tax credit plays a crucial role in this cash generation. Starting in 2024, Susquehanna's ~20 million MWh of annual generation from Talen's 90% stake potentially qualifies for up to $15/MWh in tax credits, depending on power prices. At full value, that's $300 million annually in tax benefits—essentially free cash flow that drops straight to the bottom line through 2032.

But here's where it gets interesting: Talen isn't choosing between growth and returns. The Moxie and Bayonne acquisition is expected to be immediately accretive to free cash flow per share by over 40% in 2026, and over 50% through 2029. "This acquisition enhances Talen's fleet by selectively adding modern, highly efficient baseload H-class CCGTs in Talen's key markets, where we are an innovator in data center contracting," said Mac McFarland.

The company is threading the needle—using leverage strategically to fund both accretive acquisitions and aggressive buybacks, while maintaining investment-grade metrics. Talen expects robust pro forma cash flows to drive rapid deleveraging and is committed to maintaining a leverage target of 3.5x or lower, anticipated by year-end 2026.

The capital allocation framework going forward is clear: The acquisition supports a target of approximately $500 million of annual share repurchases through the 2026 deleveraging period with an aimed return to capital allocation of 70% of adjusted free cash flow thereafter. This isn't the steady 3% dividend yield of a traditional utility; it's private equity-style capital management in a public company wrapper.

The hedging strategy has also evolved dramatically post-bankruptcy. The company has hedged 89% of expected generation volumes for 2025 and 33% for 2026. This disciplined approach to commodity risk management—a direct response to the under-hedged position that triggered the bankruptcy—provides earnings visibility while maintaining upside exposure to power price strength.

What's remarkable is how this aggressive financial engineering hasn't compromised operational performance. The fleet equivalent forced outage factor (EFOF) of 2.2% represents top-quartile operational excellence. Susquehanna's consistent 90%+ capacity factor continues to generate predictable cash flows. The balance sheet, once crushed under $4.5 billion of debt, now supports both growth investments and shareholder returns.

X. Playbook: Lessons from the Journey

The Talen Energy story offers a masterclass in crisis management, strategic positioning, and value creation that transcends the power generation sector. These lessons apply to any capital-intensive business navigating technological disruption, commodity volatility, and changing market dynamics.

Lesson 1: Sometimes bankruptcy is the best strategic option Talen's Chapter 11 filing wasn't a failure—it was a strategic reset. The company entered bankruptcy with a clear plan, negotiated with creditors in advance, and emerged in just 219 days with a cleaned-up balance sheet and new ownership aligned with long-term value creation. The speed of execution preserved commercial relationships, maintained operational continuity, and positioned the company for the AI boom that was just beginning.

Lesson 2: Asset quality matters more than asset quantity While competitors chased scale through acquisitions of marginal assets, Talen focused on its crown jewel—Susquehanna. A single high-quality nuclear plant with 90%+ capacity factor and sub-$25/MWh operating costs proved more valuable than a sprawling portfolio of average assets. When the market turned toward valuing carbon-free, reliable baseload, Talen was perfectly positioned.

Lesson 3: Timing isn't everything, but it's close Talen emerged from bankruptcy just as three massive trends converged: the AI data center boom, the nuclear renaissance driven by climate concerns, and the Inflation Reduction Act's nuclear production tax credits. Lucky? Perhaps. But as Mac McFarland noted, "You make your own luck by being prepared when opportunity knocks."

Lesson 4: Private equity playbooks don't always work in regulated industries Riverstone's leveraged buyout strategy—load up on debt, optimize operations, flip for profit—collided with the realities of commodity markets and regulatory complexity. Power generation isn't software or consumer goods; it requires patient capital, deep operational expertise, and the ability to weather commodity cycles. The bankruptcy wiped out Riverstone's investment entirely.

Lesson 5: First-mover advantage in emerging markets can be decisive Talen's early recognition of the data center opportunity—building Cumulus while still in bankruptcy proceedings—positioned it as the go-to partner when hyperscalers started scrambling for power. The Amazon deal became a template that competitors are still trying to replicate, but Talen had already locked up the best counterparty with the best terms.

Lesson 6: Hedging isn't optional in commodity businesses The under-hedged position that triggered Talen's bankruptcy serves as a cautionary tale. Post-bankruptcy, the company maintains minimum hedge ratios and has built a sophisticated risk management function. As one board member reportedly said, "We'd rather leave money on the table than bet the company on commodity prices."

Lesson 7: Operational excellence enables financial engineering Talen's ability to execute aggressive share buybacks while funding growth investments stems from operational excellence. The 2.2% fleet forced outage rate, Susquehanna's consistent performance, and successful coal-to-gas conversions generate the stable cash flows that support financial flexibility. You can't financially engineer your way out of operational problems.

Lesson 8: The value of strategic assets increases over time Nuclear plants, transmission interconnections, and land suitable for data centers—these assets become more valuable as they become scarcer. Talen's patient ownership of Susquehanna, even through bankruptcy, exemplifies the value of holding strategic assets through cycles rather than selling at the bottom.

Lesson 9: Distressed investors can be excellent owners The creditors who took control—Apollo, Brookfield, Elliott—brought sophisticated capital markets expertise and a long-term value creation mindset. Unlike strategic buyers who might have broken up the company, these investors saw the potential for transformation and provided the patient capital to achieve it.

Lesson 10: Energy transition creates opportunity for those who adapt Rather than fighting the energy transition, Talen embraced it. Coal-to-gas conversions, nuclear life extensions, and data center partnerships all align with a lower-carbon future while generating superior returns. The companies that thrive will be those that see transition as opportunity, not threat.

XI. Bull vs. Bear Case & Future Outlook

Bull Case: The Perfect Storm of Tailwinds

The bullish thesis for Talen rests on multiple converging megatrends that could drive extraordinary value creation over the next decade.

First, the AI and data center explosion is just beginning. McKinsey projects U.S. data center demand will reach 35 GW by 2030, implying a near-doubling from current levels. But that might be conservative—a single large language model training cluster can consume 100+ MW, and we're still in the GPT-4 era. As models grow toward artificial general intelligence, power demands could increase exponentially. Talen's 1.9 GW Amazon contract positions it to capture a meaningful share of this growth.

The nuclear renaissance adds another dimension. After decades of stagnation, nuclear is experiencing renewed interest from policymakers, environmentalists, and technology companies. Microsoft's deal to restart Three Mile Island, Google's SMR partnerships, and Amazon's nuclear investments signal a fundamental shift in how markets value carbon-free baseload. Susquehanna, as one of the best-operated nuclear plants in America, could see its valuation multiple expand dramatically.

The Inflation Reduction Act's nuclear production tax credits provide a decade of enhanced cash flows. At $15/MWh for Susquehanna's 20 million MWh annual production, that's $300 million in annual tax benefits through 2032—enough to fund significant shareholder returns or growth investments. Few other companies have such a clear line of sight to government-supported cash flows.

The supply-demand dynamics in PJM are increasingly favorable. Coal plant retirements are accelerating, renewable intermittency is stressing grid reliability, and new gas plant construction faces permitting challenges. Talen's existing fleet becomes more valuable simply by surviving while competitors shut down. Capacity prices in recent PJM auctions have soared, and this trend could continue.

The optionality around SMRs and uprates could surprise to the upside. If Talen successfully develops SMRs at Susquehanna or other sites, it could add gigawatts of carbon-free capacity at attractive economics. Even modest uprates of existing units could add hundreds of megawatts of high-margin generation.

Finally, M&A potential looms large. With a clean balance sheet, proven management team, and strategic assets, Talen could be an attractive acquisition target for oil majors pivoting to power, technology companies seeking energy security, or international utilities entering U.S. markets. At the right price, a takeout isn't impossible.

Bear Case: Multiple Risks Converging

The bearish perspective sees several significant risks that could derail the Talen story.

Regulatory challenges pose the most immediate threat. FERC's rejection of the initial Amazon behind-the-meter arrangement signals regulatory skepticism about large customers bypassing grid costs. Future data center deals could face similar challenges, limiting Talen's ability to monetize its strategic position. State-level interventions, transmission constraints, or changing market rules could all impact profitability.

Natural gas price volatility remains a constant risk. Despite improved hedging, Talen still has significant gas-fired generation exposed to commodity prices. A sustained spike in gas prices—whether from LNG exports, pipeline constraints, or geopolitical events—could compress margins and stress liquidity. The 2022 bankruptcy serves as a reminder of how quickly commodity markets can turn.

Competition for data center contracts is intensifying. Every independent power producer, utility, and even some industrials are now chasing data center deals. Constellation Energy's nuclear fleet, Vistra's massive battery investments, and new entrants with renewable-plus-storage solutions all compete for hyperscaler contracts. Talen's first-mover advantage could erode quickly.

Technology disruption could undermine the investment thesis. Fusion energy, though perpetually "20 years away," could eventually provide unlimited clean power. More immediately, improvements in renewable energy storage, demand response, or energy efficiency could reduce data centers' willingness to pay premium prices for nuclear baseload. Even advances in AI chip efficiency could reduce power demands.

Grid reliability obligations could become increasingly burdensome. As more coal plants retire and renewable penetration increases, remaining thermal generators face pressure to provide reliability services, often at regulated rates. Talen's plants could become conscripted assets, forced to run uneconomically to maintain grid stability.

Execution risk on growth initiatives shouldn't be ignored. The Moxie and Bayonne acquisitions add complexity and leverage. Integration challenges, unexpected maintenance needs, or operational problems could impact returns. Similarly, the Amazon contract ramp-up requires flawless execution on transmission upgrades and regulatory approvals.

Environmental and social opposition could intensify. Despite nuclear's climate benefits, public opposition to nuclear power remains significant in some communities. Any safety incident—even minor—could trigger regulatory scrutiny and public backlash. Climate activists might also target gas-fired generation, potentially accelerating stranded asset risk.

The Balanced View

The reality likely falls between these extremes. Talen will probably capture meaningful value from the data center boom, but not without regulatory friction and competitive pressure. The nuclear assets will remain valuable, but perhaps not at the astronomical multiples some bulls project. Natural gas volatility will create earnings volatility, but improved hedging should prevent existential threats.

The key variables to watch are: PJM capacity prices (higher is better), the pace of data center development (faster is better), natural gas prices (lower is better), and regulatory decisions on grid cost allocation (favorable rulings unlock value). The company's ability to execute on its contracted backlogs while maintaining operational excellence will ultimately determine success.

XII. Epilogue: What's Next?

The Talen Energy story is far from over. In many ways, the most interesting chapters are just beginning to be written.

The broader independent power producer consolidation thesis suggests Talen could be either acquirer or acquired. The sector's fragmentation, combined with the capital intensity of new development and the scarcity of development sites, points toward inevitable consolidation. Talen's clean balance sheet and proven management team position it well for either scenario.

The grid modernization imperative will reshape power markets over the next decade. As electrification accelerates—electric vehicles, heat pumps, industrial processes—electricity demand could double by 2050. But the grid built for one-way power flow from large central stations must evolve into a complex network managing distributed resources, storage, and bidirectional flows. Companies that can provide reliable, dispatchable power will command premium values.

The question of independence looms large. Will Talen remain a standalone company, or will it become part of something bigger? Technology companies seeking energy security, oil majors pivoting toward electrons, or international utilities seeking U.S. exposure could all be potential acquirers. At a sufficient premium, the board would have to consider offers seriously.

The nuclear-powered computing infrastructure vision is perhaps most intriguing. As AI models grow toward artificial general intelligence, the computational requirements could exceed anything we can currently imagine. The companies that control the power to run these systems will hold enormous strategic value. Talen's combination of nuclear baseload and data center expertise positions it uniquely for this future.

The energy transition will continue creating both opportunities and challenges. Carbon pricing, renewable portfolio standards, and electrification mandates will reshape competitive dynamics. But Talen's low-carbon generation mix and operational flexibility suggest it can adapt to multiple scenarios. The companies that survived the last energy transition—from regulated to competitive markets—were those that combined operational excellence with financial discipline. Talen has demonstrated both.

What's certain is that the next decade in power markets will look nothing like the last. The convergence of technological advancement, climate imperatives, and infrastructure needs creates a generational opportunity for companies positioned correctly. Talen Energy—once left for dead, now powering the future—embodies this transformation.

The final lesson from Talen's journey might be the most important: in commodity markets, survival is victory. The company that emerges from crisis with the right assets, right strategy, and right partners can capture extraordinary value when cycles turn. For Talen Energy, that turn has already begun. The question now is not whether the company will succeed, but how much value it can create along the way.

From a spinoff valued at $3 billion to a bankruptcy filing to a market capitalization exceeding $10 billion—Talen Energy's path demonstrates that in the intersection of old economy assets and new economy demand, extraordinary transformations are possible. The nuclear plants built in the 1980s are powering the AI revolution of the 2020s. The company left for dead in bankruptcy court is now at the forefront of American energy infrastructure.

As Mac McFarland likes to say, "We're not just generating power; we're powering the future." For Talen Energy, that future has never looked brighter.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube