TJX Companies: The Treasure Hunt Empire

I. Introduction & Cold Open

Picture this: It's a Tuesday morning in Framingham, Massachusetts, and before the sun rises, a buyer for TJ Maxx is already on a conference call with a luxury brand in Milan. The fashion house has 50,000 units of last season's collection sitting in a warehouse—beautiful merchandise that didn't sell at full price. Within hours, a deal is struck at 70% below retail, and by next week, those Italian-made handbags will be hanging in a strip mall in suburban Ohio, priced at $39.99 instead of $150.

This scene plays out thousands of times each day across TJX Companies' global empire—a $130+ billion retail colossus built on the simple premise that one retailer's excess inventory is another's treasure. With a market capitalization of $132.27 billion as of August 2024, TJX has quietly become one of the most valuable retailers on Earth, operating over 5,000 stores across nine countries. Yet unlike Amazon, Walmart, or Target, TJX deliberately keeps a low digital profile, generating less than 3% of sales online.

How did a discount retailer's struggling spin-off transform into the undisputed king of off-price retail? The answer lies not in algorithms or e-commerce innovation, but in mastering the ancient art of the deal—scaled to proportions that would make any bazaar merchant weep with envy. This is the story of how TJX turned the treasure hunt into a science, opportunistic buying into an art form, and the clearance rack into a $50 billion annual revenue machine.

The journey from a single discount store in Hyannis to a global retail phenomenon spans nearly seven decades, multiple recessions, a corporate near-death experience, the largest data breach in retail history, and a pandemic that shuttered stores worldwide. Through it all, TJX not only survived but thrived by zigging when others zagged, building a business model so distinctive that even Jeff Bezos couldn't replicate it. As we'll discover, the secret sauce isn't technology—it's something far more human: the thrill of the hunt.

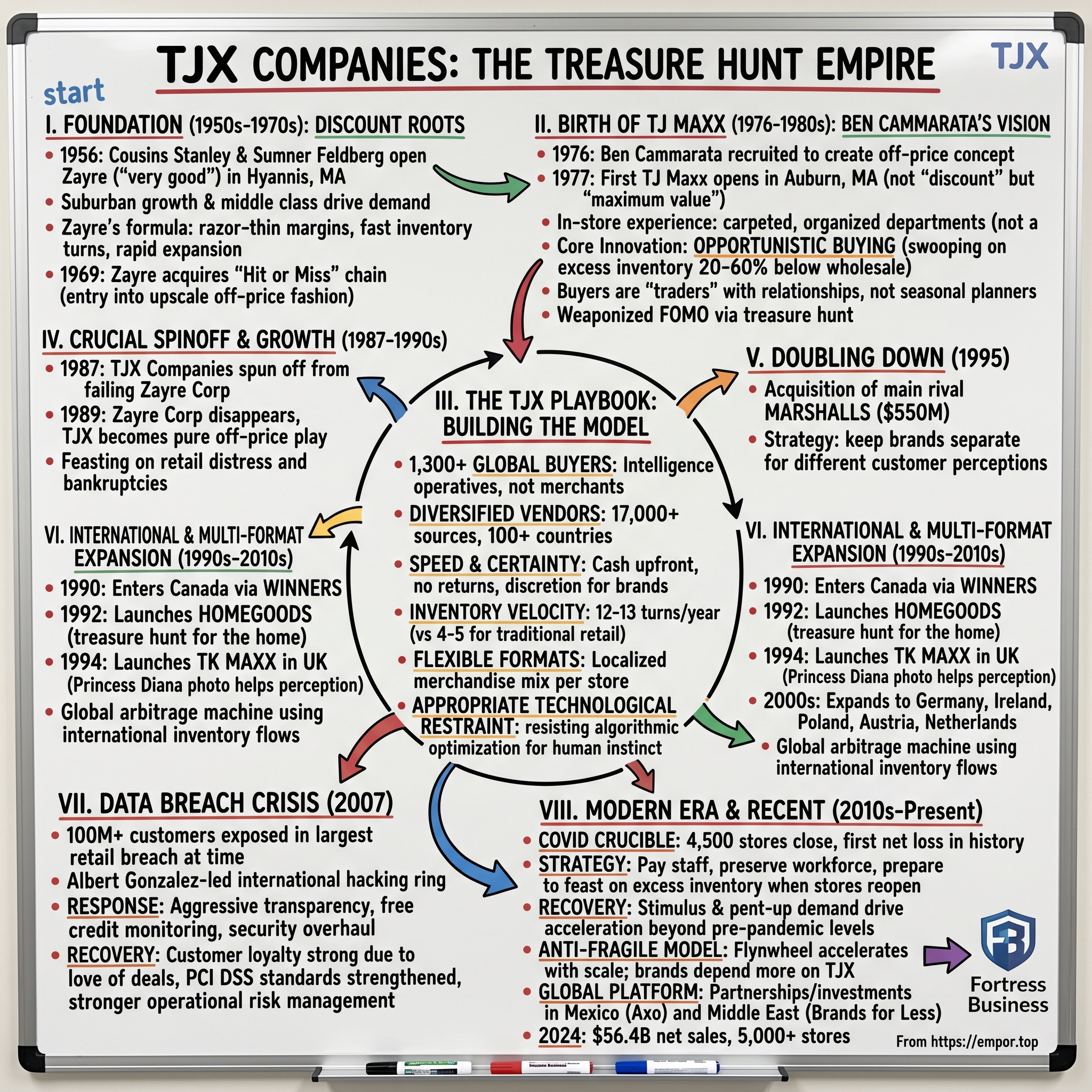

II. The Zayre Foundation: Discount Retail Roots (1956-1976)

The year was 1956, and American retail was experiencing a seismic shift. In the coastal town of Hyannis, Massachusetts—better known as the Kennedy family's summer playground—two cousins named Stanley and Sumner Feldberg opened a store with a peculiar name: Zayre, Yiddish for "very good." While the Kennedys sailed their yachts in nearby waters, the Feldbergs were launching what would become one of the most influential retail experiments in American history.

The Feldbergs weren't retail novices. They'd grown up in their family's business, but they sensed something changing in post-war America. The suburbs were exploding, families had cars, and a new middle class wanted quality goods at prices that didn't require a second mortgage. Traditional department stores, with their marble floors and white-gloved salesladies, were leaving money on the table. The Feldbergs saw opportunity where others saw only downmarket degradation.

Zayre wasn't just another discount store—it was a carefully orchestrated assault on retail orthodoxy. While department stores marked up merchandise 40-50%, Zayre operated on razor-thin margins, turning inventory faster than a short-order cook flips pancakes. The formula was intoxicating: sales doubled every second or third year throughout the 1960s. By the early 1970s, the single Hyannis store had multiplied into more than 200 locations, spreading across the Eastern seaboard like suburban kudzu.

But here's where the story takes its first unexpected turn. In 1965, while Zayre was conquering the discount department store landscape, the Feldbergs noticed something interesting happening in Natick, Massachusetts. A small chain called Hit or Miss was doing something nobody had quite seen before—selling upscale women's clothing at deep discounts, but not damaged goods or last year's styles. This was current-season, designer-label merchandise at prices that made no sense. The store's founder had discovered a secret: high-end retailers and manufacturers always produced too much, and they needed someone to quietly make their mistakes disappear.

Hit or Miss grew so rapidly that within four years, it caught Zayre's attention like a flare in the night. In 1969, Zayre acquired the chain, and with it, gained entry into a new universe—the upscale off-price fashion market. The Feldbergs didn't know it yet, but they had just acquired the DNA strand that would eventually evolve into their entire future.

The early 1970s saw Zayre at its zenith, but success bred complacency. The stores grew larger, the merchandise mix became unfocused, and operational discipline—the very thing that made discount retail work—began to slip. Meanwhile, that little Hit or Miss acquisition kept humming along, generating outsized profits relative to its footprint. Someone at corporate began asking the obvious question: if off-price worked so well for women's fashion, why not try it with everything else?

Enter Bernard "Ben" Cammarata, a merchandising wizard who'd been making waves at Marshalls, then an independent off-price chain. In 1976, Zayre recruited Cammarata with a specific mission: create an off-price concept that could scale beyond Hit or Miss's narrow focus. Cammarata didn't just bring merchandising expertise; he brought a philosophy that would reshape American retail. "Customers don't need everything," he would say. "They need great things at great prices, and they need them to be different every time they visit."

The Zayre leadership gave Cammarata remarkable freedom—a blank canvas to paint his vision of what off-price could become. They had no idea they were essentially funding their own disruption, creating the very entity that would eventually swallow its parent whole.

III. Birth of TJ Maxx: Ben Cammarata's Vision (1976-1987)

Ben Cammarata stood in an empty warehouse in Auburn, Massachusetts, in late 1976, visualizing something that didn't yet exist in American retail. The space would become the first TJ Maxx, but at that moment, it was just concrete floors and fluorescent possibility. Cammarata had spent months studying Hit or Miss, talking to buyers, visiting vendors, and most importantly, watching customers. What he saw convinced him that Americans were ready for a retail revolution—they just didn't know it yet.

The name TJ Maxx was itself a carefully crafted fiction. The "TJ" stood for nothing in particular—Cammarata wanted something that sounded established, perhaps vaguely European, definitely not discount. "Maxx" suggested maximum value without screaming "cheap." This was psychological warfare fought with typography and suggestion. When the first stores opened in 1977, they looked nothing like traditional discount retailers. No warehouse aesthetic, no concrete floors, no harsh lighting. Instead, Cammarata insisted on carpeting, organized departments, and fitting rooms that didn't feel like prison cells.

But the real innovation wasn't in the stores—it was in the buying operation Cammarata constructed. Traditional retailers planned their purchases seasons in advance, committing to specific quantities, colors, and sizes based on forecasts that were wrong as often as they were right. Cammarata flipped this model entirely. His buyers would swoop in after those forecasts failed, purchasing excess inventory at 20-60% below wholesale. It was opportunistic, required massive amounts of cash on hand, and demanded a completely different skill set than traditional retail buying.

"We're not merchants, we're traders," Cammarata would tell his team. He recruited buyers not from retail but from commodities trading floors, people who understood that timing was everything and that the best deal was often the one you walked away from. These buyers didn't attend fashion shows or browse catalogs; they haunted the back offices of Seventh Avenue, building relationships with production managers who knew exactly when a big order would fall through or when a manufacturer had produced an extra 10,000 units "just in case."

The early years were controlled chaos. Merchandise arrived in unpredictable waves—one week might bring a thousand Italian leather jackets, the next, designer towels from a canceled hotel order. Store managers never knew what would show up on the loading dock. This unpredictability, which would have been death for a traditional retailer, became TJ Maxx's greatest asset. Customers learned to visit frequently because that incredible find might not be there tomorrow. Cammarata had weaponized FOMO before Silicon Valley invented the acronym.

By 1980, TJ Maxx had expanded to 31 stores, but more importantly, it had proven the model worked at scale. Vendors who initially viewed TJ Maxx with suspicion—why would luxury brands want their products in a discount chain?—began to see it differently. TJ Maxx offered something invaluable: discretion. Unlike traditional liquidators who might damage a brand's reputation, TJ Maxx mixed merchandise so thoroughly that customers rarely knew whose overproduction they were buying. A Ralph Lauren shirt might sit next to an unknown Italian brand, all at similarly attractive prices.

The numbers told a compelling story. While parent company Zayre's traditional discount stores struggled with 2-3% operating margins, TJ Maxx consistently delivered 5-7%. Same-store sales grew double digits year after year. By 1986, when Zayre's main chain started hemorrhaging money—profits dropped catastrophically as the company lost ground to Walmart and Target—TJ Maxx, Hit or Miss, and a new catalog operation called Chadwick's of Boston continued their relentless growth. That year alone, Zayre opened 35 new TJ Maxx stores and 31 Hit or Miss locations.

Cammarata's vision had created more than a successful retail concept; he'd built an entirely new ecosystem. The company developed TJX University, an internal training program that taught buyers not just how to negotiate but how to think like treasure hunters. They learned to read bankruptcy filings, track fashion weeks not for trends but for overproduction patterns, and build networks of informants across the global supply chain. It was corporate espionage meets garage sale, elevated to a multi-billion dollar art form.

The contrast between Zayre's struggling core business and TJ Maxx's success became impossible to ignore. Board meetings grew tense as directors questioned why the company's future seemed to lie not in its namesake stores but in what had started as a small experiment. Cammarata, ever the diplomat, avoided corporate politics, focusing instead on expansion. But everyone could see where this was heading. The child was about to consume the parent.

IV. The Spinoff: Creating TJX Companies (1987-1989)

The Zayre boardroom in Framingham had the atmosphere of a medical consultation where everyone knew the diagnosis but no one wanted to say it aloud. It was early 1987, and the numbers sprawled across the conference table told a story of two companies trapped in one corporate body. The Zayre discount chain—the founding business, the nameplate on the building—was dying. Meanwhile, the off-price operations led by TJ Maxx were generating profits that looked almost indecent by comparison.

The board made a decision that would have seemed unthinkable just five years earlier: create a new entity called The TJX Companies, Inc., spinning off TJ Maxx, Hit or Miss, and Chadwick's of Boston as a separate public company. On paper, it was a reorganization. In reality, it was an admission that the future lay not in traditional discount retail but in the treasure hunt model Cammarata had perfected.

The spin-off structure was byzantine in its complexity, designed to maintain tax efficiency while giving both entities the freedom to pursue their divergent destinies. TJX Companies would be a separate public entity, but Zayre Corp would retain 83% ownership. Minority shareholders could buy into the pure-play off-price story while Zayre tried to fix its troubled flagship chain. Wall Street loved it—TJX shares surged on their first day of trading.

But the separation only accelerated Zayre's decline. The first half of 1988 brought catastrophic news: operating losses of $69 million on sales of $1.4 billion. Industry observers performed autopsies on a still-breathing patient, citing technological inferiority, deferred maintenance, inventory pileups that looked like retail archaeology sites. Walmart and Target had modernized their supply chains with sophisticated computer systems while Zayre still relied on paper and intuition. The stores themselves had become depressing—dim lighting, scuffed floors, merchandise scattered like aftermath of a particularly aggressive Black Friday.

Then came the decision that would define TJX's future: Zayre's board voted to sell the entire chain of over 400 Zayre stores to Ames Department Stores. The deal was structured as only a desperate seller could accept—$431.4 million in cash, a receivable note that everyone knew might never be collected, and $140 million in Ames preferred stock that was about as stable as nitroglycerin.

Ames, for its part, thought it was getting a bargain, rolling up a weakened competitor to achieve scale. Within two years, the company would file for bankruptcy, taking the Zayre nameplate with it into retail oblivion. But that was still in the future. In the moment, Zayre Corp had essentially sold its own name, keeping only the thriving off-price operations.

June 1989 marked the final transformation. Zayre Corp acquired the outstanding minority interest in TJX, paying shareholders a premium to consolidate control. Then, in a corporate metamorphosis worthy of Kafka, Zayre Corp ceased to exist. The company changed its name to The TJX Companies, Inc., and began trading on the New York Stock Exchange under a new ticker. The discount retailer that started in Hyannis had officially died, and from its ashes rose something entirely different.

Ben Cammarata, who had joined Zayre to run an experiment, now found himself CEO of a public company valued at over $1 billion. In his first letter to shareholders as head of the newly independent TJX, he wrote with characteristic understatement: "Our business model is simple—we buy opportunistically and pass the savings to our customers. But simple doesn't mean easy. It requires discipline, relationships, and a willingness to move fast when opportunity presents itself."

The timing of the transformation proved fortuitous. The late 1980s and early 1990s saw a surge in retail bankruptcies and restructurings as leveraged buyouts went bad and department stores struggled with debt. For TJX, this chaos was Christmas morning. Every bankruptcy created inventory that needed to disappear quickly and quietly. Every failed product launch meant beautiful merchandise available at crushing discounts. The company that had emerged from Zayre's ashes was perfectly positioned to feast on the retail industry's distress.

V. The Off-Price Playbook: Building the Business Model

Inside TJX headquarters, there's a room that buyers call "The Morgue"—shelves lined with products that seemed like great deals but died on the sales floor. A $2,000 designer dress bought for $50 that no one wanted at $199. Artisanal olive oil that was too artisanal. The Morgue serves as a humbling reminder that in the off-price game, the difference between treasure and trash often comes down to instinct, timing, and a mystical understanding of what makes customers reach for their wallets.

The treasure hunt concept that defines TJX wasn't invented so much as discovered through thousands of small experiments. Early buyers noticed that when merchandise was organized too neatly, sales actually dropped. Customers wanted to feel like they were discovering something, not being presented with options. So TJX stores deliberately create what executives call "organized chaos"—just messy enough to feel like a hunt, just organized enough to not frustrate shoppers into leaving.

This psychological manipulation extends to every aspect of the operation. Price tags show "Compare At" prices that may or may not reflect reality but create an anchor in customers' minds. Merchandise is mixed deliberately—a $300 designer bag might sit next to a $30 alternative, making both seem like better deals through proximity. The lighting is bright enough to see merchandise but not so bright that flaws become obvious. It's retail theater, and every element has been tested and refined over decades.

But the real magic happens in the buying operation, which by 2024 has grown to 1,300 buyers—more than most retailers have total corporate employees. These aren't traditional merchants who visit showrooms and select from catalogs. TJX buyers are more like intelligence operatives, maintaining networks of contacts across the global supply chain. They know which Italian manufacturer always overproduces by 20% "for safety." They track which department stores are struggling with cash flow and might need to quietly liquidate inventory. They monitor fashion weeks not for trends but for ambitious production runs that might not sell through.

The numbers behind this operation stagger the mind. TJX sources from more than 17,000 vendors across 100+ countries, with the top 25 vendors comprising only 25% of purchases. This diversification isn't accidental—it ensures no single supplier can hold the company hostage and creates endless opportunities for opportunistic buying. Compare this to traditional retailers who might work with a few hundred vendors and depend heavily on their top 10.

The financial model these buyers operate under would terrify most retail executives. TJX maintains massive amounts of cash and credit facilities—essentially a war chest ready to deploy at a moment's notice. When a European fashion house suddenly needs to clear 100,000 units, TJX can wire payment within hours. This speed and certainty make TJX the buyer of first resort for distressed inventory. Vendors know that dealing with TJX means no negotiations dragging on for weeks, no payment terms stretching to 120 days, no returns or chargebacks. Cash on delivery, merchandise disappears, everyone moves on.

Unlike traditional retailers that buy seasonally—planning fall merchandise in spring, committing to Christmas inventory in July—TJX buys continuously. New merchandise arrives in stores several times a week, with each delivery containing thousands of items. This creates a logistical nightmare that TJX has turned into a competitive advantage. Distribution centers operate like commodity trading floors, with merchandise flowing in and out so quickly that some items spend less than 24 hours in the warehouse.

Store operations reflect this velocity. Traditional retailers might turn inventory 4-5 times per year; TJX targets 12-13 turns. Merchandise that doesn't sell quickly gets marked down aggressively—not because TJX needs the cash, but because floor space is too valuable to waste on slow movers. Store managers have unusual autonomy to adjust prices, move merchandise, and even refuse shipments that don't fit their local market. A TJ Maxx in Scottsdale operates very differently from one in Detroit, and the company encourages this localization.

The training infrastructure supporting this model rivals business schools. TJX University doesn't just teach buying tactics; it imparts a philosophy. New buyers spend months shadowing veterans, learning to read vendor body language, understanding global manufacturing cycles, developing the intuition that separates a great deal from a costly mistake. They study failed retailers like archaeologists examining ruins, understanding why Circuit City's inventory was gold while Borders' was poison.

Perhaps most remarkably, TJX has made this model work at massive scale without the technology infrastructure that defines modern retail. While Amazon uses artificial intelligence to predict demand and Walmart tracks every item with RFID tags, TJX deliberately maintains what one executive called "appropriate technological restraint." The company uses technology for logistics and finance but resists the temptation to algorithmically optimize what is fundamentally a human business—understanding desire, value, and the thrill of discovery.

VI. The Marshalls Acquisition: Doubling Down (1995)

Frank Arnone, CEO of Marshalls, sat across from Ben Cammarata in a Boston law office in November 1995, both men knowing they were about to sign documents that would reshape American retail. Marshalls wasn't just any acquisition target—it was TJX's mirror image, a parallel universe where similar strategies had evolved independently. The irony wasn't lost on either executive: Cammarata had started his career at Marshalls before Zayre poached him to create TJ Maxx, and now he was buying his former employer.

The deal—$550 million in cash and preferred stock paid to Melville Corporation—made headlines for its size, but insiders understood the real story was about market power. Marshalls operated 496 stores generating $2.8 billion in annual sales. Combined with TJ Maxx's 503 stores, TJX would overnight become a colossus in off-price retail, with nearly 1,000 locations and enough buying power to make any vendor take their call.

Melville Corporation, Marshalls' parent, was a bloated conglomerate struggling with everything from CVS pharmacies to Kay-Bee Toys. They needed cash and focus, making Marshalls expendable despite its profitability. For TJX, the timing was perfect—retail consolidation was accelerating, and whoever achieved scale first would have permanent advantages in the off-price game.

But the integration challenged every assumption about retail mergers. Convention said you'd consolidate the brands, eliminate redundancy, achieve "synergies"—that bloodless corporate term for firing people. Cammarata did the opposite. He kept both brands separate, maintaining distinct buying teams, different merchandise mixes, even competing for the same real estate. When asked why, he responded with characteristic insight: "Customers think they're different, so they are different."

This decision seemed insane to Wall Street analysts who'd built models assuming massive cost savings. But Cammarata understood something they didn't: in off-price retail, perception is reality. TJ Maxx had cultivated a slightly more upscale image, focusing on fashion and home goods. Marshalls skewed more toward family basics and footwear. The overlap was substantial, but the differences—however subtle—mattered to customers who would drive past one to shop at the other.

The real synergies came in places customers never saw. Combined buying power meant better deals from vendors who now viewed TJX as their most important outlet for excess inventory. The company could take 500,000 units of overproduction where previously neither chain could handle more than 250,000. Distribution networks were optimized without being merged—Marshalls trucks could carry TJ Maxx merchandise when routes aligned, but maintained separate warehouses to preserve brand identity.

Creating the Marmaxx Group as an administrative structure for both chains was a masterpiece of corporate architecture. It centralized back-office functions like IT, finance, and real estate while keeping merchandise and marketing separate. Store managers from both chains attended the same training programs but competed fiercely for sales performance. It was cooperation and competition in perfect tension.

The cultural integration proved more challenging than anyone anticipated. Marshalls buyers, proud of their company's longer history (founded in 1956, same year as Zayre), initially resented being absorbed by their younger rival. TJ Maxx buyers, convinced their model was superior, struggled to appreciate Marshalls' different approach to vendor relationships. Cammarata spent months shuttling between buying offices, playing therapist and coach, convincing both sides they were on the same team while maintaining their distinct identities.

The first year after integration delivered numbers that silenced skeptics. Combined comparable store sales grew 7%, far exceeding the 2-3% analysts had projected. More importantly, vendor relationships strengthened dramatically. European fashion houses that previously played TJ Maxx and Marshalls against each other now dealt with a single entity controlling over $5 billion in purchasing power. Department stores closing locations would call TJX first, knowing they could move entire inventory cleanups through the combined network.

The acquisition also triggered an unexpected innovation: the "flexible format" store. With two brands under one roof, TJX could match store concepts to real estate opportunities. A former department store anchor space might become a massive Marshalls, while a strip mall location could house a smaller TJ Maxx. Some locations even tested dual-branded stores, with TJ Maxx and Marshalls sharing a building but maintaining separate entrances and checkout areas.

By 1997, the combined Marmaxx Group generated $7.4 billion in sales and $354 million in operating profit—margins that made traditional retailers weep with envy. The acquisition that doubled TJX's size had more than doubled its market power. Vendors spoke of the "Marmaxx price"—the discount they'd accept because TJX could move volume no one else could match. Competitors watched helplessly as TJX locked up exclusive deals for entire production overruns, leaving crumbs for smaller off-price players.

VII. International Expansion & Multi-Format Strategy (1990-2010)

The call came at 3 AM Boston time from a buyer stationed in London: "Harrods has 50,000 units they need gone by Friday. Can we do it?" By sunrise, TJX had wired payment, arranged shipping, and the merchandise was heading to a warehouse in Bristol. This was 1994, and TK Maxx—TJX's European beachhead—was teaching the Old World about New World retail aggression.

The international expansion started modestly in 1990 with the acquisition of Winners Apparel, a Toronto-based chain of five stores that was essentially practicing the TJX model with Canadian politeness. The $47 million purchase price was pocket change for TJX, but it provided something invaluable: proof the off-price concept could translate across borders. Canadian customers, it turned out, loved the treasure hunt just as much as Americans, perhaps more so given the limited retail options in many Canadian cities.

Winners became TJX's laboratory for international operations. Currency fluctuations, different vendor relationships, varying consumer preferences—every lesson learned in Canada would prove invaluable for larger expansions. The Canadian team discovered that hockey equipment sold brilliantly in November but not October, that Canadians preferred deeper discounts on outerwear, and that bilingual signage in Quebec was not optional but essential for success.

But Europe was the real prize. In 1994, TJX launched TK Maxx in the United Kingdom—the name change necessary because of a existing British retailer called TJ Hughes. The first stores opened in Bristol and Cardiff, deliberately avoiding London to perfect the model away from intense scrutiny. British customers initially seemed puzzled. Off-price retail existed in the UK, but it meant dingy stores selling damaged goods. TK Maxx, with its carpeted floors and designer merchandise, created cognitive dissonance.

The breakthrough came when Princess Diana was photographed carrying a TK Maxx shopping bag. Whether staged or serendipitous, the image transformed perception overnight. Suddenly, treasure hunting wasn't déclassé—it was clever. British newspapers ran features on "TK Maxx finds," celebrities bragged about their bargains, and the stores couldn't stock merchandise fast enough.

The European expansion revealed unexpected advantages. Fashion houses in Milan and Paris produced even more excess inventory than American brands, but had fewer outlets for it. TK Maxx became the discrete solution for luxury overproduction, moving merchandise from Mayfair boutiques to Manchester suburbs without damaging brand equity. The company discovered it could buy Italian leather goods at prices that made no sense, ship them to stores in Ireland, and still maintain 60% gross margins.

Meanwhile, back in America, TJX was experimenting with format proliferation. HomeGoods, launched in 1992, took the off-price model and applied it exclusively to home furnishings. The concept seemed risky—could treasure hunting work for sofas and soap dispensers? The answer was emphatically yes. HomeGoods tapped into a different psychology than apparel. Customers might need a specific dress size, but everyone could use another throw pillow, especially at 70% off suggested retail.

The format innovations kept coming. A.J. Wright, launched in 1998, targeted lower-income consumers with even deeper discounts on family basics. Bob's Stores, acquired in 2003, attempted to bring off-price to sporting goods and workwear. Sierra Trading Post, purchased in 2012, moved TJX into online off-price for outdoor gear. Not all succeeded—A.J. Wright closed in 2011, Bob's was sold in 2008—but each experiment taught valuable lessons about the boundaries of the off-price model.

The international expansion accelerated through the 2000s. TK Maxx entered Ireland in 2007, finding a market hungry for alternatives to expensive Dublin department stores. Germany welcomed TK Maxx in 2007, though success required adjusting to German shopping habits—customers expected fitting rooms to be immaculate and wouldn't tolerate the cheerful chaos that Americans found charming. Poland, Austria, and the Netherlands followed, each requiring subtle adaptations while maintaining the core treasure hunt premise.

HomeSense, the European version of HomeGoods, launched in 2008 and grew even faster than TK Maxx had. European consumers, living in smaller spaces, proved especially responsive to home décor deals. A designer lamp that might sit unsold in a Cleveland HomeGoods would fly off shelves in Copenhagen HomeSense, teaching TJX about the value of international inventory flows.

By 2010, TJX operated in eight countries with over 2,700 stores. International operations generated nearly $5 billion in annual revenue, contributing significantly to the company's recession resilience. When American consumers pulled back during the 2008 financial crisis, European operations cushioned the blow. When European economies struggled with sovereign debt crises, American stores picked up the slack.

The multi-format, multi-geography strategy created a complexity that would break most retailers. But TJX thrived on it. Buyers could shift merchandise between continents based on currency fluctuations. A fashion trend failing in America might succeed in Germany. Home goods oversupplied in Britain could fill shelves in Boston. The company had built not just an international presence but a global arbitrage machine, turning the entire world's excess inventory into profit.

VIII. The Data Breach Crisis & Recovery (2007)

Dave Merriman, TJX's Chief Financial Officer, received the call on a December morning in 2006 that every retail executive dreads: "We've been compromised." The IT security team had discovered unauthorized software on the company's computer systems, software that had been secretly transmitting customer credit card data to unknown recipients for months, possibly years. As forensic investigators would later determine, hackers had been inside TJX's systems since 2005, perhaps earlier, making it the longest undetected retail breach in history.

The public announcement on January 17, 2007, sent shockwaves through retail and technology circles. Initial estimates suggested 45 million credit and debit card numbers had been stolen. Later investigations would reveal the true scope: over 100 million customers potentially exposed, making it the largest security breach in history at that time. The hackers had exploited weaknesses in the wireless networks at two Miami-area Marshalls stores, using that foothold to penetrate corporate systems handling transaction data across all TJX chains.

The perpetrators weren't teenage hackers in basements but sophisticated international criminals. Albert Gonzalez, the mastermind eventually convicted for the breach, had simultaneously penetrated systems at BJ's Wholesale Club, Boston Market, Barnes & Noble, and others. His crew used the stolen data to manufacture counterfeit cards, withdrew millions from ATMs worldwide, and sold card numbers on digital black markets. They'd turned retail hacking into an industrial operation.

For TJX, the immediate crisis was existential. Would customers trust a company that had exposed their financial data? Would vendors continue relationships with a retailer whose security was so catastrophically compromised? Would regulatory penalties and lawsuits destroy decades of carefully built value? CEO Carol Meyrowitz, who had recently succeeded Ben Cammarata, faced the defining challenge of her tenure.

The response strategy mixed aggressive transparency with operational transformation. TJX immediately offered free credit monitoring to affected customers, established a dedicated call center to handle inquiries, and cooperated fully with law enforcement. More importantly, Meyrowitz made a decision that surprised observers: she refused to minimize or deflect. In earnings calls and public statements, she acknowledged the breach's severity and committed to making TJX the most secure retailer in America.

The financial hit was substantial but manageable. TJX recorded pre-tax charges of $216 million related to the breach, covering customer remediation, security improvements, and legal settlements. A consolidated class-action lawsuit settled for $41 million. Visa and Mastercard claims added tens of millions more. But the real cost was in the massive security overhaul that followed.

TJX essentially rebuilt its technology infrastructure from scratch. The company implemented end-to-end encryption for all payment data, years before it became industry standard. Wireless networks were eliminated or secured with military-grade encryption. The company hired former NSA cybersecurity experts to build what one insider called "Fort Knox for credit cards." The investment totaled hundreds of millions of dollars—money that could have opened dozens of new stores or funded acquisitions.

The customer response proved surprisingly resilient. Same-store sales in the quarter following the breach announcement actually increased 3%. Customers, it seemed, separated their love of treasure hunting from concerns about data security. Or perhaps the breach made TJX seem more important—if criminals worked that hard to penetrate their systems, the deals must be exceptional. It was perverse logic, but it worked in TJX's favor.

The long-term impact transformed not just TJX but entire retail industry's approach to cybersecurity. The Payment Card Industry Data Security Standard (PCI DSS) was strengthened directly in response to the TJX breach. Retailers worldwide upgraded their systems, understanding that what happened to TJX could happen to them. The breach became a Harvard Business School case study, analyzed in boardrooms and classrooms as the definitive example of crisis management.

Inside TJX, the breach created a cultural shift around technology and risk. The company had always prided itself on "appropriate technological restraint," avoiding expensive systems that didn't directly drive sales. Post-breach, security became sacred. Every technology decision now included security assessment. Vendors were required to meet stringent data protection standards. The company that had built its fortune on opportunistic buying became obsessively careful about operational risk.

By 2009, TJX had not only recovered but emerged stronger. The security investments, while costly, created competitive advantages. Smaller off-price competitors couldn't match TJX's security standards, making vendors more comfortable with TJX partnerships. The enhanced systems also improved inventory tracking and supply chain efficiency—unintended benefits from necessary upgrades.

Meyrowitz would later reflect that the breach, while painful, forced TJX to modernize in ways that complacency might have prevented. The company that emerged from the crisis was more technologically sophisticated, more operationally disciplined, and paradoxically, more trusted by customers who saw how seriously TJX took their security. The largest data breach in retail history had somehow strengthened the company it was meant to destroy.

IX. Modern Era: Digital Age Challenges & Opportunities (2010-Present)

Ernie Herrman stood in an empty TJ Maxx store in Natick, Massachusetts, on a March evening in 2020, the fluorescent lights illuminating rows of perfectly arranged merchandise that no customers would see. The governor had just ordered all non-essential businesses closed. For the first time in TJX's 43-year history, the treasure hunt was over—temporarily. Outside, the parking lot that typically buzzed with bargain hunters sat empty, a scene replaying across 4,500 stores worldwide. The company that had survived recessions, the dot-com bubble, and a massive data breach now faced something unprecedented: a world where physical retail simply stopped.

The irony was exquisite. TJX sees e-commerce as complementary to stores and operates six e-commerce sites, but e-commerce sales accounted for just about 2% of overall sales in fiscal 2020. The company that had deliberately resisted digital transformation, that had built its entire model on the visceral thrill of in-store discovery, was now watching pure-play e-commerce competitors feast while its doors remained locked. Amazon's stock soared. Shopify minted new millionaires daily. Meanwhile, TJX was hemorrhaging cash—net sales for the first quarter of Fiscal 2021 were $4.4 billion, with a net loss of $887 million.

Yet this crisis would reveal something profound about TJX's model. While other retailers scrambled to build digital capabilities from scratch, while department stores negotiated desperately with landlords, while specialty retailers liquidated inventory at any price, TJX's buyers were quietly preparing for what would come next. Every shuttered store, every canceled order, every brand desperate for cash—it all represented future inventory for the treasure hunt machine. The pandemic wasn't destroying TJX's model; it was creating the greatest buying opportunity in the company's history.

The Amazon-Proof Architecture

The question that haunts every brick-and-mortar retailer in the 2020s is simple: How do you compete with Amazon? For most, the answer involves massive technology investments, same-day delivery promises, and digital transformation initiatives that burn cash faster than a private jet burns fuel. TJX's answer is more radical: you don't compete with Amazon. You build something Amazon cannot replicate.

TJX continues to prioritize its brick-and-mortar presence. This dual approach caters to different shopping preferences. The treasure hunt experience—that dopamine hit when discovering a designer handbag at 80% off—cannot be digitized. Amazon can deliver predictability, convenience, and infinite selection. But it cannot deliver serendipity. It cannot create the social experience of shopping with friends, the tactile pleasure of feeling fabric, the immediate gratification of walking out with your find.

More fundamentally, TJX's buying model breaks when moved online. E-commerce requires predictable inventory, SKUs that can be photographed and cataloged, sizes and colors that remain in stock long enough for someone to click "buy." But TJX buyers are in the marketplace every week, with no walls between departments, shifting merchandise to take advantage of opportunities. A shipment that arrives Tuesday morning might be completely sold through by Thursday afternoon. The merchandise mix varies not just by region but by individual store.

This controlled chaos is precisely what makes the model defensible. TJX is well-positioned to overcome COVID-19 headwinds backed by a strong off-price model, likely to gain market share as retailers collapse or remain under pressure. While Pure-play e-commerce companies need massive warehouses to store predictable inventory, TJX's distribution centers are more like switching stations, with the ability to purchase quantities ranging from small to very large.

COVID's Crucible: Survival and Transformation

TJX announced closing all stores in Australia for two weeks, along with U.S. and Canadian locations based on government requirements, also closing online businesses tjmaxx.com, marshalls.com, and sierra.com, and temporarily closing distribution centers and offices. The company that prided itself on never closing, on being there whenever customers needed a bargain, was suddenly dark.

The financial impact was immediate and brutal. The group registered a net loss of $887 million in Q1 FY2021 ended May 2, 2020, and a net loss of $214 million in Q2 ended August 1, 2020. For comparison, TJX had been profitable every quarter for decades. The company that had weathered the 2008 financial crisis while growing same-store sales was now burning through cash reserves at an alarming rate.

But CEO Ernie Herrman and his team understood something critical: this wasn't a permanent shift in consumer behavior but a temporary disruption. People hadn't stopped wanting bargains; they just couldn't access stores. The buying team, working from home offices and kitchen tables, maintained relationships with vendors who were increasingly desperate. Department stores were canceling orders. Luxury brands had warehouses full of spring merchandise that never made it to stores. The entire global apparel supply chain was backed up like a clogged drain.

The company planned to pay store, distribution center and office Associates for two weeks during closures, a decision that cost hundreds of millions but preserved the workforce TJX would need for recovery. This wasn't altruism—it was strategic. The specialized knowledge of TJX buyers and store operators couldn't be easily replaced. Losing them would mean losing decades of relationships and expertise.

As stores began reopening in May and June 2020, something remarkable happened. Management believes it is in a strong position to take advantage of real estate availability to open new stores and relocate existing stores. Customers returned with pent-up demand and stimulus checks. The treasure hunt, it turned out, was one of the experiences people had missed most during lockdown. Store, distribution, and fulfillment center Associates physically came to work to keep the business open, implementing safety protocols that allowed shopping to continue even as the pandemic persisted.

The Recovery Playbook

By late 2020, TJX wasn't just recovering—it was accelerating. TJX Companies benefits from an abundance of inventory, with CEO Herrman noting ability to take advantage of excess inventories across e-commerce businesses, including vertical and full-line players with spill-off goods. Every failed e-commerce startup, every overoptimistic direct-to-consumer brand, every department store fighting for survival—they all needed someone to make their inventory problems disappear.

The numbers tell a story of remarkable resilience. In 2024, TJX generated net sales of approximately 54.2 billion dollars, up from about 49.9 billion a year earlier. This wasn't just recovery; it was acceleration beyond pre-pandemic levels. For the 52-week fiscal year ended February 1, 2025, net sales were $56.4 billion, up 4% with comparable store sales increasing 4%, net income of $4.9 billion and diluted EPS of $4.26, up 10%.

The pandemic had also accelerated trends that benefited TJX. Department stores, already struggling, collapsed faster. Macy's, Nordstrom, and others closed hundreds of locations, each closure representing both reduced competition and increased inventory availability for TJX. Brands that had previously been selective about off-price partnerships now viewed TJX as essential for survival.

Herrman expressed confidence in having exciting assortments of fresh goods across all stores and online throughout fall and holiday seasons. This wasn't corporate optimism—it was based on the reality that TJX now had more leverage with vendors than ever before. The company that started as a single experiment within a struggling discount chain had become the most important player in global inventory liquidation.

Digital Restraint as Competitive Advantage

While competitors rushed to build digital capabilities, TJX maintained its contrarian stance. The closing of HomeGoods' e-commerce business had a 0.3 percentage point negative impact to Q3 FY2024 pretax profit margin, with costs from closing the e-commerce business. The decision to actually close an e-commerce operation in 2024, when every retail consultant preached digital transformation, seemed like corporate suicide.

Yet the logic was impeccable. HomeGoods' treasure hunt model—finding that perfect lamp or unexpected piece of art—translated poorly online. The economics didn't work. The customer experience was inferior. Rather than throwing good money after bad, TJX did something almost unheard of in modern retail: they admitted digital wasn't always the answer.

This disciplined approach to technology investment freed capital for what actually drove returns: buying inventory and opening stores. TJX plans to expand its global footprint by over 1,300 additional stores. While other retailers were closing locations and investing in fulfillment centers, TJX was signing leases at historically attractive rates.

The Acquisition Engine Restarts

TJX announced a partnership with Mexico-based Axo to expand off-price into Mexico through a joint venture including Axo's discount physical store business with over 200 stores for Promoda, Reduced, and Urban Store banners, with TJX owning 49%. This wasn't just international expansion—it was TJX exporting its model to entirely new markets where the treasure hunt concept didn't yet exist.

In 2024, TJX made investments with established off-price retailers, forming a joint venture with Grupo Axo in Mexico and making a minority investment in Brands for Less in the Middle East, seeing these as ways to participate in off-price growth globally. These moves reflected a new phase in TJX's evolution: from operator to platform, licensing its expertise to partners who understood local markets but needed TJX's buying power and operational knowledge.

The international investments also created new opportunities for inventory flows. Excess merchandise from European brands could flow to Middle Eastern stores. Mexican overproduction could supply U.S. locations. The company was building a global arbitrage network that no competitor could replicate without decades of relationship building.

Current State: The Fortress Business

As 2024 draws to a close, TJX stands as one of retail's great success stories—not despite avoiding digital transformation but because of it. With over 5,000 stores and 1,300 buying Associates operating offices worldwide, sourcing from 100+ countries and a vendor universe of more than 21,000 vendors, the company has built a moat that gets wider every year.

The numbers validate the strategy. Q4 sales, profitability, and EPS were all well above expectations, with 5% comp store sales growth driven by strong increases in comp sales and customer transactions at every division, offering customers compelling values on brands and an exciting treasure-hunt experience. While other retailers struggle with inventory management and demand forecasting, TJX thrives on unpredictability.

The brand has "become a cooler place to shop" according to CEO Herrman—a remarkable transformation for a company that started as a discount chain spin-off. Young consumers who might have shopped at department stores now Instagram their TJ Maxx finds. The stigma of off-price has been completely inverted; it's now a mark of savvy rather than necessity.

The pandemic, rather than exposing weaknesses in TJX's physical-first model, revealed its antifragility. The worse things get for traditional retail, the better they get for TJX. Every supply chain disruption creates buying opportunities. Every failed digital native brand needs a liquidation partner. Every inflation spike makes treasure hunting not just fun but necessary.

Looking forward, TJX faces a retail landscape that seems almost designed for its success. Traditional department stores continue their slow-motion collapse. E-commerce companies struggle with profitability. Consumers, exhausted by inflation, seek value wherever they can find it. And somewhere, a buyer is on a call with a desperate vendor, negotiating a deal that will put designer goods in a strip mall at prices that make no sense, continuing the treasure hunt that began in a Hyannis discount store nearly 70 years ago.

X. The Competitive Moat: Why TJX Works

In the conference rooms of Amazon, Walmart, and Target, executives have spent countless hours and millions of dollars trying to decode TJX's success. They've hired consultants, built algorithms, launched copycat concepts—and almost universally failed. The reason isn't that TJX's model is complex; it's that the model requires capabilities that take decades to build and cannot be bought at any price.

Scale as Weapon and Shield

The mathematics of TJX's scale advantage compound in ways that escape casual observation. With over 1,300 Associates in the buying organization, operating offices around the world, and sourcing from more than 100 countries with a vendor universe of more than 21,000 vendors, TJX has built a sensing network that spans the entire global apparel and home goods supply chain.

Consider what this means in practice: When a fashion brand overproduces by 20%, TJX can absorb the entire overrun across its 5,000 stores. A competitor with 500 stores cannot make the math work—the per-store inventory would be too high, the risk too concentrated. This scale differential means TJX gets first call on the best deals, often exclusively. By the time smaller competitors learn about an opportunity, TJX has already wired payment and arranged shipping.

But scale alone doesn't explain the moat. Walmart has scale. Amazon has more scale. What TJX has is scale combined with flexibility—a rare combination in retail. Buyers operate with "no walls" between departments, able to shift merchandise categories to take advantage of opportunities and purchase quantities ranging from small to very large. A buyer focused on women's apparel might suddenly purchase kitchen appliances if the deal is compelling enough. This organizational flexibility, maintained at massive scale, is nearly impossible to replicate.

The University System Nobody Talks About

TJX has over 1,300 Associates in buying organization, but the number alone understates the asset. These aren't just employees—they're graduates of an internal university system that rivals any business school. TJX University isn't a corporate training program with PowerPoints and role-playing. It's an apprenticeship system where new buyers shadow veterans for months, learning to read the subtle signals that separate a great deal from a disaster.

The curriculum is unwritten but rigorous. Buyers learn to interpret the body language of a vendor who claims their inventory is "moving well" but needs cash by Friday. They develop networks of informants—production managers, shipping clerks, fashion show producers—who provide intelligence on which brands are struggling. They study the archaeology of failed retailers, understanding why Toys "R" Us inventory was toxic but Payless shoes sold brilliantly.

This knowledge is tacit, embedded in relationships and instincts that cannot be documented or digitized. When Amazon tried to build an off-price concept, they hired buyers from traditional retail who understood spreadsheets and seasonal planning. What they needed were traders who understood desperation and opportunity. The failure was preordained.

Vendor Relationships: The Unbreakable Network

The relationship between TJX and its vendors resembles a complex ecosystem more than traditional buyer-supplier dynamics. Department stores negotiate hard, demand payment terms, charge for prime floor placement, and return unsold merchandise. TJX does none of this. Cash on delivery, no returns, complete discretion. For a luxury brand with 100,000 units of last season's collection, TJX isn't just a customer—it's salvation.

This creates a virtuous cycle that strengthens with each transaction. Vendors who might initially view TJX skeptically—will their brand be damaged by appearing in off-price?—discover that TJX handles their merchandise with care. Products are mixed so thoroughly across brands and price points that customers rarely know whose overproduction they're buying. A vendor's mistake disappears without damaging their brand equity.

Over decades, these relationships evolve from transactional to strategic. Vendors begin planning for TJX, knowing that 20% overproduction isn't a mistake if TJX will buy it at acceptable margins. Some luxury brands allegedly produce extra units specifically for the off-price channel, though they'd never admit it publicly. The relationship becomes symbiotic—vendors get a reliable outlet for excess inventory, TJX gets first access to premium merchandise.

The Treasure Hunt Psychology

The psychological architecture of the treasure hunt is TJX's most underappreciated moat. Traditional retailers strive for consistency—a Gap store in Boston stocks the same merchandise as one in Boise. This predictability is comforting but boring. TJX weaponizes inconsistency, turning shopping into a game where winning means finding that incredible deal that might not be there tomorrow.

This isn't just marketing rhetoric. TJX stores deliberately create what behavioral economists call "variable reward schedules"—the same psychological mechanism that makes slot machines addictive. Sometimes you find amazing deals, sometimes you don't, but the possibility keeps you coming back. The inconsistency isn't a bug; it's the core feature.

Herrman said TJX has "become a cooler place to shop", reflecting a cultural shift where finding deals has become a form of social currency. Instagram accounts dedicated to TJ Maxx finds have millions of followers. The treasure hunt has been gamified and socialized in ways that traditional retail cannot match. Amazon can deliver convenience, but it cannot deliver the story you tell friends about that designer jacket you found for $40.

Flexible Real Estate and Operations

TJX's approach to real estate breaks every rule of retail location strategy. While traditional retailers obsess over demographics, traffic patterns, and co-tenancy clauses, TJX takes a simpler approach: go where the deals are. A former Sears anchor space? Perfect for a massive Marshalls. A strip mall in a declining neighborhood? Ideal for a TJ Maxx. The stores don't need to be beautiful; they need to be cheap.

This flexibility extends to operations. Store managers have unusual autonomy to adjust prices, refuse shipments that don't fit their market, and even rearrange floor layouts based on local preferences. A TJ Maxx in Scottsdale operates nothing like one in Detroit, and that's intentional. This localization, managed across 5,000 stores, creates complexity that would break most retail operations. For TJX, it's competitive advantage.

The company has also mastered the art of productive chaos. Traditional retailers aim for operational efficiency—predictable schedules, optimized staffing, standardized processes. TJX stores operate in controlled disorder. Merchandise arrives unpredictably, requiring staff to process shipments quickly. The sales floor needs constant attention as customers rifle through products. This operational intensity requires a different kind of employee—one who thrives on variety rather than routine.

Capital Allocation Discipline

While not sexy, TJX's capital allocation discipline creates a compounding advantage over time. The company resists the siren call of expensive technology investments that don't directly drive sales. While competitors pour billions into e-commerce platforms, same-day delivery capabilities, and artificial intelligence, TJX invests in buying inventory and opening stores—activities with proven returns.

For full year Fiscal 2025, the company generated $6.1 billion of operating cash flow and ended with $5.3 billion of cash. This cash hoard isn't sitting idle—it's ammunition for opportunistic buying. When a vendor needs immediate payment, TJX can wire funds within hours. This speed and certainty make TJX the buyer of first resort for distressed inventory.

The company also returns substantial capital to shareholders through dividends and buybacks, but only after ensuring adequate resources for growth. This balanced approach—growth investment first, shareholder returns second—has created trust with investors who understand the model's long-term potential.

The Moat Widens

Every year, TJX's competitive advantages compound. More stores mean better deals from vendors. Better deals mean happier customers. Happier customers mean more sales. More sales mean more stores. It's a flywheel that accelerates with scale, and TJX is already at escape velocity.

Competitors face an impossible catch-up game. To match TJX's buying power, they'd need similar scale. To achieve scale, they'd need great deals from vendors. To get great deals, they'd need buying power. The circular logic creates an impenetrable barrier to entry. Starting an off-price retailer today would be like starting a search engine to compete with Google—theoretically possible, practically futile.

XI. Playbook: Key Business Lessons

The Power of Opportunistic Buying at Scale

The conventional retail wisdom says success comes from predicting what customers want and delivering it consistently. TJX inverts this: success comes from buying whatever's available cheaply and convincing customers they want it. This isn't passive opportunism—it's aggressive opportunism backed by massive capital and decisive action.

When the Suez Canal blockage in 2021 left cargo ships floating for weeks, most retailers panicked about delayed inventory. TJX buyers were on phones with shipping companies, offering to buy entire containers of goods at distressed prices. When brands pivoted to direct-to-consumer during COVID and overestimated demand, TJX absorbed their excess inventory at pennies on the dollar. Every crisis becomes a buying opportunity when you have cash, courage, and the infrastructure to move quickly.

The lesson extends beyond retail: in any industry, the ability to act when others are paralyzed creates extraordinary value. But this requires preparation during calm periods—building cash reserves, maintaining credit facilities, developing processing capabilities. TJX spends the good times preparing for the bad times, knowing that dislocations are not just inevitable but profitable.

Creating Scarcity and Urgency

Every retailer claims their sale "ends Sunday" or supplies are "limited." Customers have learned to ignore these manufactured deadlines. TJX creates genuine scarcity through unpredictability. That designer coat really might not be there tomorrow—not because of artificial limits but because TJX bought all 500 units the vendor had and won't get more.

This authentic scarcity drives behavior traditional retailers can only dream about. Customers visit TJX stores frequently—not because they need something specific but because they might miss something amazing. The fear of missing out (FOMO) isn't manipulated through countdown timers or fake inventory meters; it's real because the inventory is genuinely unpredictable and unrepeatable.

The broader lesson: authentic scarcity beats manufactured urgency every time. Customers are sophisticated enough to recognize false pressure but respond powerfully to genuine limitations. Creating real scarcity might mean accepting lower margins or operational complexity, but the customer response justifies the investment.

Building a Differentiated Customer Experience

TJX stores violate every principle of modern retail design. They're not Instagram-worthy. The lighting is harsh. The racks are crowded. Merchandise is mixed seemingly at random. Yet customers love them, spending hours hunting through racks, returning week after week. Why?

Because TJX understood something profound: the experience isn't about the store—it's about the hunt. The cramped racks and jumbled merchandise aren't bugs to be fixed but features that enhance the treasure hunt psychology. Finding that perfect item feels earned, not given. The experience is active, not passive. Customers are participants, not recipients.

This runs counter to the retail trend toward frictionless experiences. Amazon's one-click ordering eliminates all friction. TJX adds friction deliberately. The lesson isn't that friction is always good, but that the right friction for the right customer can create engagement that convenience never could.

Training and Culture as Competitive Advantages

TJX operates buying offices around the world, but offices don't create advantage—people do. TJX's investment in training through TJX University isn't corporate philanthropy; it's building irreplaceable assets. The knowledge embedded in a 20-year TJX buyer—their vendor relationships, market intuition, deal-making skills—cannot be hired from outside or replicated quickly.

This long-term approach to human capital runs counter to modern corporate practice. Most retailers view store employees as interchangeable, investing minimally in training. TJX store managers receive weeks of training, learning not just operations but the philosophy of treasure hunting. They're taught to think like merchants, not clerks.

The cultural element amplifies the training investment. TJX employees at all levels understand they're not just selling clothes—they're creating experiences, enabling discoveries, democratizing fashion. This sense of mission, cultivated over decades, creates engagement that no amount of stock options could buy.

When to Resist Technology Trends

TJX's restraint regarding e-commerce seems almost anti-modern. Digital Commerce 360 projects web sales for TJX will reach $1.6 billion in 2024, a tiny fraction of total sales. While competitors chase digital transformation, TJX deliberately limits online presence. This isn't Luddism—it's strategic focus.

The company recognizes that technology is a tool, not a strategy. E-commerce makes sense for predictable inventory and convenience-seeking customers. It makes no sense for unpredictable inventory and experience-seeking customers. Rather than forcing a square peg into a round hole, TJX accepts that some opportunities aren't worth pursuing.

The broader lesson: every business faces pressure to adopt the latest technology trend—artificial intelligence, blockchain, metaverse, whatever comes next. The courage to say "not for us" might be the most valuable strategic capability. Not every innovation is an improvement, and not every trend deserves investment.

Capital Allocation: The Boring Superpower

Warren Buffett calls capital allocation the most important job of a CEO, but most executives treat it as an afterthought. TJX makes capital allocation central to strategy. Every dollar spent on technology cannot be spent on inventory. Every store opened is a bet that physical retail has a future. Every dividend paid is a promise that growth won't require that capital.

Strong financial results and cash flow generation have allowed simultaneous investment in business growth and returning significant value to shareholders. This isn't financial engineering—it's strategic discipline. The company has resisted the temptation to make transformative acquisitions, to launch new concepts outside their expertise, to chase growth at any cost.

The steady, boring approach to capital allocation—open stores, buy inventory, return excess cash—has created extraordinary long-term value. No financial headlines, no dramatic pivots, just consistent execution of a proven model. In a world obsessed with disruption, TJX proves that consistency can be its own form of competitive advantage.

XII. Bull vs. Bear Case Analysis

The Bull Case: An Unstoppable Flywheel

The optimistic view of TJX starts with a simple observation: the company gets stronger when retail gets weaker. Every department store closure, every brand bankruptcy, every supply chain disruption creates inventory that needs to disappear quickly and quietly. TJX has positioned itself as the global solution to retail's excess inventory problem, and that problem is growing.

As competition shrinks, notably from department store closures like Macy's, TJX is poised to capitalize on increased market share and vendor importance. The math is compelling. If department stores continue closing 50-100 locations annually, each closure represents both eliminated competition and increased inventory availability. Vendors who previously had multiple outlets for excess inventory increasingly depend on TJX as their primary liquidation partner.

International expansion provides another growth vector. TJX is exploring untapped territories, with Europe and Australia representing significant opportunities, and analysts highlight potential to grow European footprint and newer banners like Sierra and HomeSense. The off-price model that revolutionized American retail is still nascent in many international markets. TJX can essentially replay its U.S. success story across multiple geographies.

The resilience of the model provides downside protection that growth investors crave. During recessions, consumers trade down from department stores to off-price. During booms, they buy more because they have more disposable income. This "heads I win, tails I win more" dynamic has proven itself across multiple economic cycles. The 2008 financial crisis, which devastated traditional retail, saw TJX gaining market share and maintaining profitability.

Demographics favor the model. Millennials and Gen Z consumers have no stigma about off-price shopping—if anything, finding deals has become a form of social currency. These generations, entering prime spending years, view treasure hunting as smart, not desperate. The cultural shift from "keeping up with the Joneses" to "finding better deals than the Joneses" plays perfectly into TJX's model.

The balance sheet provides enormous flexibility. $5.3 billion of cash isn't just a safety net—it's dry powder for opportunistic moves. Whether buying distressed inventory, acquiring competitors, or accelerating store expansion, TJX has resources to act decisively when opportunities arise.

The Bear Case: Brick-and-Mortar's Last Stand

The pessimistic view starts with an uncomfortable truth: TJX is a physical retailer in an increasingly digital world. Yes, they've resisted e-commerce successfully so far, but past performance doesn't guarantee future results. Every year, a higher percentage of apparel sales move online. At some point, the treasure hunt psychology might not be enough to draw customers to physical stores.

The dependency on other retailers' mistakes is both strength and weakness. TJX needs department stores to over-order, brands to overproduce, and retailers to fail. But what happens if the retail ecosystem becomes more efficient? If artificial intelligence improves demand forecasting? If brands get better at right-sizing production? The inefficiencies TJX arbitrages might not exist forever.

Labor challenges pose operational risks. The treasure hunt model requires significant in-store labor—processing unpredictable shipments, maintaining the organized chaos, helping customers navigate constantly changing inventory. In an era of rising wages and worker shortages, this labor-intensive model faces pressure. Automation, which helps other retailers, doesn't work when every shipment is different and unpredictability is the point.

Despite the rise of e-commerce, TJX maintains robust physical presence. Analysts foresee a slowdown in e-commerce growth over next two years, potentially boosting brick-and-mortar opportunities. But this analyst optimism might prove temporary. If e-commerce growth reaccelerates—driven by improving logistics, virtual reality shopping, or generational change—TJX's physical-only stance could shift from strategic to stubborn.

Economic sensitivity remains a concern. While TJX performs well in recessions as customers trade down, a severe, prolonged downturn could challenge even off-price retail. If unemployment spikes and stays elevated, even bargain hunters might stop hunting. The company weathered COVID's storm, but that was accompanied by massive government stimulus. The next crisis might not include such support.

Competition, while currently manageable, could intensify. Amazon has failed at off-price so far, but they rarely give up. Walmart and Target are expanding their clearance operations. New digital-native off-price concepts launch regularly. While none have successfully challenged TJX yet, the law of large numbers suggests someone eventually might.

The Verdict: Asymmetric Risk-Reward

Weighing both cases, TJX presents an unusual investment profile: a mature company with startup-like growth potential, a traditional retailer with technology-resistant advantages, a simple business model with impossible-to-replicate complexity. The bull case doesn't require believing in transformation or disruption—just that TJX continues executing the same model it's refined for decades. The bear case requires multiple fundamental changes: consumer behavior shifting dramatically, retail becoming vastly more efficient, or digital alternatives successfully replicating the treasure hunt.

The asymmetry favors the bulls. TJX doesn't need to invent anything new or transform its business model. It just needs retail to remain somewhat inefficient, consumers to continue enjoying bargain hunting, and management to maintain discipline. These are much lower bars than most growth stories require.

XIII. Recent News### Q3 2024 Earnings: Momentum Continues

TJX reported strong third quarter fiscal 2025 results (ended November 2, 2024), with net sales of $14.1 billion, up 6% versus prior year, and consolidated comparable store sales increasing 3%. CEO Ernie Herrman expressed satisfaction with the results, noting comp store sales at the high-end of plan and both pretax profit margin and earnings per share coming in well above expectations, leading to raised full year guidance.

The fourth quarter is off to a strong start, with TJX offering consumers an ever-changing shopping destination for holiday gifts at excellent values. The company's ability to deliver consistent performance across all divisions reflects the strength of its diversified portfolio and the universal appeal of the treasure hunt model during economic uncertainty.

Inventory management remains disciplined, with consolidated inventories on a per-store basis down 2% on both reported and constant currency basis versus last year. The company is well-positioned to take advantage of outstanding marketplace availability and deliver an eclectic mix of exciting gifts throughout the holiday season.

Global Expansion Accelerates

TJX plans to add at least 1,300 stores "over the long term," with CEO Herrman citing the company's flexibility and opportunistic buying as key to attracting shoppers across a broad range of income and age groups. The company continues to attract new Gen Z and millennial shoppers, which management believes bodes well for future growth.

During fiscal year ended February 1, 2025, the company increased store count by 131 stores to 5,085 total stores. TJX surpassed $56 billion in annual sales, drove 4% comparable store sales increase, significantly increased profitability, and opened its 5,000th store during the year.

Strategic International Investments

TJX formed a joint venture with Grupo Axo in Mexico and made a minority investment in Brands for Less in the Middle East, seeing these as ways to participate in off-price growth globally over the long term. After Q3 2025, TJX completed its investment for a 35% non-controlling stake in Brands For Less for $344 million, with BFL operating over 100 stores primarily in UAE and Saudi Arabia plus e-commerce.

These international partnerships represent a new phase in TJX's evolution—from direct operator to platform provider, exporting its expertise to markets where the off-price concept remains underdeveloped. The capital-light approach through joint ventures and minority investments allows TJX to participate in global growth without the operational complexity of direct expansion.

Supply Chain and Operational Excellence

In its 48-year history, product availability has never been an issue even growing to over 5,000 stores, with over 1,300 Associates in buying organization, operating offices worldwide, sourcing from 100+ countries and a vendor universe of more than 21,000 vendors. Buyers are typically in the marketplace weekly, with "no walls" between departments allowing merchandise category shifts to take advantage of opportunities, willing to purchase less-than-full assortments and quantities from small to very large.

The operational complexity of managing this global sourcing network while maintaining the treasure hunt experience across 5,000+ stores would break most retailers. For TJX, it's the moat that gets wider every year.

XIV. Links & Resources

Annual Reports and Investor Presentations

- TJX Investor Relations: investor.tjx.com

- Latest 10-K Annual Report: SEC EDGAR Database

- Quarterly Earnings Calls: TJX.com Investor Section

- 2024 Global Corporate Responsibility Report: TJX.com

Industry Analysis and Reports

- National Retail Federation Off-Price Sector Reports

- GlobalData Retail Intelligence

- Euromonitor International Apparel & Footwear Reports

- Credit Suisse Retail Research Coverage

Books on Retail History and Off-Price Sector

- "The Everything Store" by Brad Stone (for contrast with e-commerce)

- "Retail Revolution" by Mark Pilkington

- "Bargain Fever" by Mark Ellwood

- Harvard Business School Cases on TJX Companies

Relevant Podcasts and Interviews

- CNBC Mad Money interviews with CEO Ernie Herrman

- Bloomberg Odd Lots episodes on retail and supply chains

- Retail Dive podcast coverage of off-price sector

- The Business of Fashion podcast retail episodes

Academic Case Studies

- Harvard Business School: "TJX Companies and the Off-Price Retail Model"

- Wharton: "Treasure Hunt Retailing"

- MIT Sloan: "Supply Chain Management at TJX"

- Stanford GSB: "Capital Allocation in Retail"

Trade Publications

- Women's Wear Daily (WWD)

- Retail Dive

- Chain Store Age

- Retail TouchPoints

Data and Analytics Providers

- Placer.ai for foot traffic analytics

- SimilarWeb for digital presence metrics

- Euromonitor for global retail data

- NPD Group for consumer behavior insights

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube