Hanover Insurance Group: From New England Fire Insurer to Specialty P&C Powerhouse

Introduction and Episode Roadmap

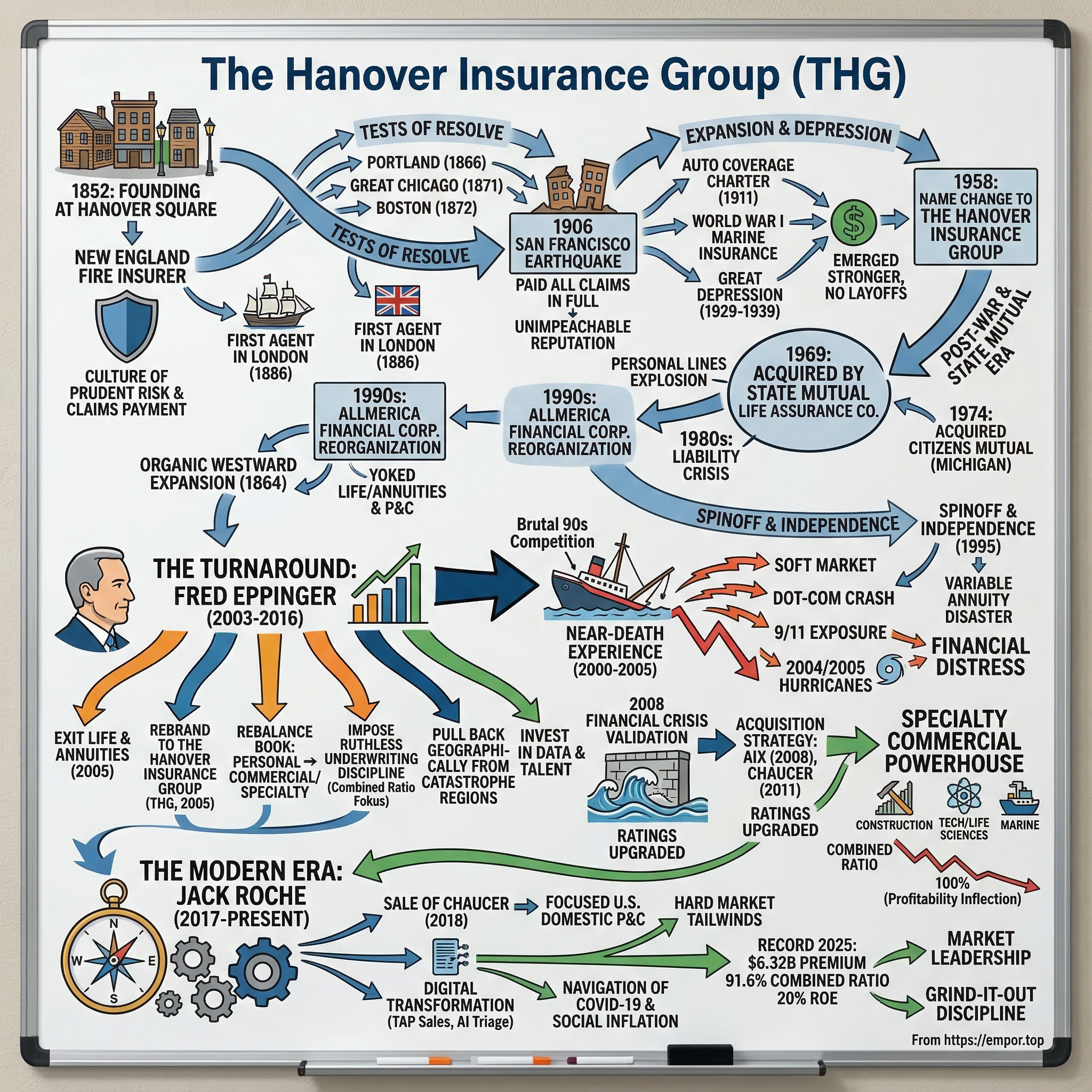

There is a building at Hanover Square in lower Manhattan where, in 1852, a group of businessmen pooled their capital to bet on something radical: that you could mathematically predict the likelihood of a wooden building catching fire and charge people accordingly. One hundred and seventy-four years later, the company they created writes more than six billion dollars a year in insurance premiums, sits in the S&P 400, and recently posted a twenty percent return on equity. The Hanover Insurance Group is not a household name. It does not run Super Bowl ads. It does not have a gecko or a spokeswoman named Flo. And that is precisely what makes its story so fascinating.

The central question of this deep dive is deceptively simple: how did a sleepy New England fire insurer transform into a specialty commercial lines powerhouse that survived multiple near-death experiences—including one where the company was genuinely hours away from being sold off for parts—and emerged as one of the best-run property and casualty insurers in America?

Insurance is the invisible backbone of capitalism. Nothing gets built, shipped, sold, or financed without it. Every skyscraper, every cargo ship, every doctor's practice, every software company—they all run on insurance. Warren Buffett built the greatest conglomerate in history largely on the economics of insurance float. And yet most investors treat insurance companies as black boxes: opaque, boring, and impossible to analyze. That is a mistake. The best insurance companies are extraordinary compounding machines, and the worst ones are ticking time bombs. The difference comes down to one word: discipline.

Hanover's arc takes us from horse-and-buggy era catastrophes through the gilded age of American industrialization, past the 1906 San Francisco earthquake, through the Great Depression, into the era of suburban sprawl and auto insurance, through a corporate acquisition that lasted decades, out into a chaotic independence, past a near-fatal catastrophe, into one of the most impressive corporate turnarounds in the insurance industry, and finally into the modern era of AI-enabled underwriting and specialty commercial dominance. Along the way, we will explore why insurance businesses are so hard to run, why Buffett loves them, and why the companies that get the culture right tend to win over very long periods of time.

This is a story about what happens when a company almost dies and then decides to become excellent. It is also a story about why boring businesses, done well, create more value than most investors realize—and why the companies that thrive in insurance are the ones that understand a truth that applies far beyond their industry: discipline, not brilliance, is the ultimate competitive advantage.

The Founding Era and Early Context (1850s–1900)

Picture lower Manhattan in 1852. The city is a tinderbox—wooden buildings packed shoulder to shoulder, gas lamps flickering in parlors, no fire codes to speak of, and a fire department that still relies heavily on volunteers pulling hand-drawn pumping engines through cobblestone streets. In this environment, The Hanover Fire Insurance Company opened its doors at Hanover Square, backed by a group of investors that included, remarkably, the author Washington Irving. The founding president, John Wyckoff, established something that would echo through the next century and a half: a culture centered on prudent risk-taking and, crucially, paying claims in full when disaster struck.

Mid-nineteenth century America was industrializing at a breakneck pace, and the primary risk that kept business owners awake at night was fire. Cities were essentially collections of kindling. The business model was elegant in its simplicity: pool premiums from many policyholders, invest the float, and pay out when fires inevitably came. But execution was everything. An insurer that mispriced risk or grew too aggressively could be wiped out by a single conflagration. An insurer that failed to pay claims would lose the trust of the agents who distributed its policies and the customers who depended on them.

From the very beginning, Hanover adopted the independent agent distribution model—appointing Samuel S. Coe, a prominent Cleveland businessman, as its first independent agent. This decision, made in 1852, still defines the company today. Hanover has never sold insurance directly to consumers. Every policy, for more than one hundred and seventy years, has been sold through an independent agent. That is extraordinary continuity in a world where business models tend to have the shelf life of a carton of milk.

The early decades tested Hanover's claims-paying resolve repeatedly. In 1866, the Portland, Maine fire burned eighteen hundred buildings in what was then the most destructive fire in American history. Hanover paid every claim. In 1871, the Great Chicago Fire devastated the city, and the "Chicago Merchants" publicly praised Hanover for meeting all obligations in full—a striking endorsement in an era when many insurers simply refused to pay and dared policyholders to sue. In 1872, Boston burned, and again Hanover honored its commitments.

By the 1880s, the company's reputation had attracted marquee clients including Marshall Field and J.P. Morgan. Capital had grown substantially, doubling to one million dollars. The growth was organic and methodical—Hanover expanded westward with the frontier, establishing a general agency in 1864 to service settlers pushing into new territory. The company's charitable tradition began formally in 1855 with a donation to the New York City Widows and Orphans Fund, establishing a pattern of community engagement that reflected the mutual obligation at the heart of the insurance relationship.

In 1886, Hanover appointed its first agent in London, establishing international connections that would prove significant more than a century later when the company acquired a Lloyd's of London platform. The London connection was prescient for a company that would not seriously pursue international business for another hundred and twenty-five years, but it reflected an awareness that risk is global even when business is local.

The DNA was set: conservative underwriting, independent agent distribution, claims-paying integrity above all else. These founding principles would be tested, abandoned, rediscovered, and ultimately vindicated over the next hundred and forty years. But they were always there, encoded in the institutional memory of a company that understood—even in the 1850s—that insurance is fundamentally a promise, and that promises kept are the only sustainable competitive advantage.

Survival Through Crisis: From San Francisco 1906 to the Great Depression

At 5:12 a.m. on April 18, 1906, the San Andreas fault ruptured beneath the Pacific Ocean floor just off the coast of San Francisco. The earthquake itself was devastating, but it was the fire that followed—burning for three days, consuming more than twenty-eight thousand buildings across five hundred city blocks—that defined the event as the most consequential catastrophe in the history of the American insurance industry.

The San Francisco earthquake and fire was the industry's first true stress test. Many insurers had written policies that covered fire but explicitly excluded earthquake damage. When the shaking stopped and the fires began, these companies seized on a legal technicality: they argued that because the earthquake had caused the fires, the damage was excluded under earthquake exclusions. Policyholders who had paid premiums for years were told they would receive nothing.

Hanover took a different path. The company paid all its San Francisco claims in full, absorbing significant losses but emerging with something far more valuable than short-term capital preservation: an unimpeachable reputation. In an industry where trust is the product, this decision echoed through decades. Agents remembered which companies stood behind their promises and which companies lawyered their way out. Hanover's claims-paying record in 1906 became a competitive advantage that compounded for generations.

In 1911, recognizing that the world was changing rapidly, Hanover expanded its charter beyond fire insurance to include marine and automobile coverage. The automobile was transforming American life, and an insurer that failed to cover this new risk class would find itself increasingly irrelevant. By 1915, the company wrote the first automobile insurance policy in the State of Michigan—a move that would take on outsized significance when Michigan later became the company's second-largest personal lines market through the Citizens Insurance subsidiary. That same year, in a delightful historical footnote, Hanover insured a young baseball player named Babe Ruth—a reminder that even in 1915, celebrity and risk were intertwined in ways that foreshadowed the modern entertainment liability market.

During World War I, Hanover provided insurance for U.S. ships carrying cargo across the Atlantic, navigating the real risks of German U-boat attacks. By 1921, the company had even established operations in China, demonstrating an international ambition that was unusual for a domestic fire insurer.

Then came the Great Depression. For most American businesses, the years between 1929 and 1939 were a story of layoffs, salary cuts, dividend suspensions, and survival by any means necessary. Hanover's response was remarkable: the company did not lay off a single employee throughout the entire Depression. It continued paying dividends to shareholders. There were no salary decreases. By 1935, Hanover emerged from the Depression better capitalized and financially stronger than before the collapse began.

This was not charity—it was strategy. By retaining its people and maintaining its agent relationships while competitors retrenched, Hanover positioned itself to capture market share when the economy recovered. The lesson is timeless: in cyclical businesses, the companies that maintain discipline and relationships through downturns tend to emerge disproportionately stronger. The Depression era reinforced the same principles that the San Francisco earthquake had established: pay your claims, keep your promises, maintain your relationships, and play the long game.

By the late 1930s, Hanover had evolved from a monoline fire insurer into a multiline property and casualty company with a geographic footprint that extended well beyond New York. In 1958, the company formally recognized this evolution by changing its name from The Hanover Fire Insurance Company to The Hanover Insurance Group. The fire was gone from the name, but the fire-forged principles remained. What Hanover did not yet know was that its next chapter would involve losing its independence entirely—and that the consequences of that loss would take decades to fully unfold.

Post-War Expansion and the State Mutual Era (1945–1990s)

The post-World War II era transformed the American insurance landscape as fundamentally as the industrial revolution had transformed it a century earlier. Millions of returning soldiers bought homes in newly built suburbs, purchased automobiles, and started businesses. The demand for personal lines insurance—homeowners policies, auto coverage, umbrella liability—exploded. Property and casualty insurers that had been primarily commercial fire companies suddenly found themselves competing for the suburban family's insurance wallet.

Hanover expanded aggressively into personal lines, building a substantial homeowners and auto insurance book. The numbers tell the story of an era: between 1945 and 1970, the number of registered automobiles in America roughly tripled, and the number of owner-occupied homes doubled. Every one of those cars and homes needed insurance, and the companies that captured that demand grew rapidly. For a fire insurer like Hanover, the pivot to personal lines was not optional—it was existential. Fire insurance alone was becoming a shrinking share of a rapidly expanding market.

But the company's most consequential moment of this era came not from organic growth but from a transaction that would reshape its identity for the next three decades.

In 1969, The Hanover Insurance Group was acquired by State Mutual Life Assurance Company of America, headquartered in Worcester, Massachusetts. State Mutual was one of the oldest and largest life insurance companies in New England, and the acquisition of Hanover gave it a property and casualty platform to complement its life insurance operations. As part of the deal, Hanover's headquarters moved from New York City—where it had operated for one hundred and seventeen years—to Worcester, Massachusetts, where it remains today.

Life under State Mutual brought capital, stability, and something that would prove less beneficial: bureaucracy. In 1974, Hanover acquired Citizens Mutual Insurance Company of Howell, Michigan, which became the vehicle for its Midwest personal lines expansion. Citizens Insurance Company of America remains Hanover's Michigan brand to this day, a tangible artifact of 1970s-era expansion strategy.

The 1980s brought the liability crisis—a hard market characterized by rapidly rising insurance costs, particularly in commercial general liability and professional liability lines. Lawsuits were multiplying, jury awards were escalating, and insurers were scrambling to reprice their books. For a company like Hanover, embedded within a life insurance conglomerate, the hard market presented both opportunity and constraint. The capital was there, but the strategic flexibility was not. Decisions about growth, underwriting standards, and capital allocation were filtered through the priorities of a parent company whose primary business was life insurance and annuities—a fundamentally different animal from property and casualty.

By the early 1990s, State Mutual had reorganized into what became Allmerica Financial Corporation, a holding company structure that encompassed both the life insurance operations and the P&C business. The 1990s competitive landscape was brutal: mega-mergers were reshaping the industry, direct writers like GEICO and Progressive were attacking personal lines with aggressive pricing and innovative distribution, and the independent agent channel—Hanover's exclusive distribution model—was under pressure from all sides.

The seeds of independence were being planted, though not entirely by choice. Allmerica Financial was dealing with its own strategic challenges, including a growing appetite for variable annuities—complex financial products that promised guaranteed returns to customers. Think of a variable annuity as a retirement savings product with a built-in guarantee: the insurance company promises that no matter what happens in the stock market, the customer will receive at least a minimum return. When markets are rising, these guarantees cost nothing because investment returns exceed the guaranteed minimums. When markets crash, the insurer is on the hook for the difference—and that difference can be enormous. This appetite for variable annuity sales would later prove nearly fatal. But in the mid-1990s, the focus was on rationalizing the corporate structure and accessing public capital markets.

For investors, the State Mutual era illustrates a pattern that recurs throughout insurance history: the dangers of combining fundamentally different insurance businesses under a single roof. Life insurance and annuities are long-duration liability businesses driven by mortality tables and investment returns. Property and casualty insurance is a short-duration business driven by underwriting skill and catastrophe exposure. The incentives, talent profiles, and risk management frameworks are entirely different. Yoking them together creates cross-subsidy temptations and management attention deficits that almost invariably lead to trouble.

The Spinoff and Independence (1995): Rebirth as a Public Company

On October 11, 1995, Allmerica Financial Corporation began trading on the New York Stock Exchange under the ticker AFC at an initial offering price of twenty-one dollars per share. This was not exactly a clean spinoff of Hanover as a standalone P&C company—it was the creation of a publicly traded holding company that owned both the life insurance operations and the property and casualty business. But it was the beginning of a journey toward independence that would take another decade to complete.

What Hanover inherited from its decades under State Mutual and Allmerica was a mixed bag. On the positive side: a respected brand with a one-hundred-and-forty-three-year heritage, deep independent agent relationships in the Northeast and Midwest, and a meaningful market presence in both personal and commercial lines. On the negative side: operational complexity from being embedded in a life insurance conglomerate, a personal lines-heavy book that was increasingly exposed to catastrophe risk, and a corporate parent that was about to make a spectacularly bad bet on variable annuities.

In 1997, Allmerica Financial completed the consolidation of its P&C operations by acquiring the remaining forty percent of its property and casualty subsidiary for approximately eight hundred million dollars. This made the P&C business a wholly owned subsidiary—cleaner structurally, but it also meant that the P&C operations were now fully exposed to whatever happened at the parent level.

The 1990s competitive landscape was unforgiving. Insurance industry consolidation was accelerating, with mega-carriers like AIG, Travelers, and Chubb pursuing scale advantages. Price competition in personal lines was intensifying as direct writers invested heavily in technology and advertising. And the independent agent channel, while still dominant in commercial lines, was losing ground in personal auto and homeowners to companies that sold directly to consumers.

Management's challenge was straightforward to articulate but enormously difficult to execute: prove that a mid-size, agent-distributed P&C insurer could compete against both the scale players above and the nimble specialists below. This is the classic "stuck in the middle" problem that strategy professors love to warn about—too small for scale advantages, too large for boutique flexibility. In most industries, companies in this position either grow up, slim down, or get acquired. Hanover would eventually find a third path: specialize.

The initial strategy was conservative—defend personal lines market share, grow commercial lines carefully, maintain agent relationships. Early performance was modest at best: growth was slow, profitability was inconsistent, and the stock languished. The company was still searching for an answer to the fundamental question that independence had posed: what is Hanover's reason to exist as a standalone company? The market was not patient, and the competitive environment was not forgiving.

But independence, even imperfect independence within a holding company structure, forced something invaluable: strategic clarity. When you are a division of a larger company, you can hide behind the parent's capital and brand. When you are visible to public market investors, you have to articulate what you are, what you are not, and why you deserve to exist. For Hanover, the answer to that question was still being formulated. The next decade would provide the crucible in which the answer was forged—through crisis, near-death, and ultimately, transformation.

The Catastrophe Years and Near-Death Experience (2000–2005)

The early 2000s were a perfect storm for Hanover, and the metaphor is painfully literal. Three forces converged to push the company to the edge of extinction: a soft insurance market characterized by brutal price competition and deteriorating underwriting discipline, a stock market collapse that devastated the parent company's variable annuity business, and a series of natural catastrophes that stress-tested every assumption the company had made about risk.

Start with the variable annuity disaster, because it was the wound that nearly proved fatal. During the late 1990s bull market, Allmerica Financial had become one of the hottest sellers of variable annuities in the country. These products were enormously profitable when stock markets were rising—the company collected fees while customers' investments grew, and the guaranteed minimum returns embedded in the contracts seemed safely theoretical. Nobody was going to need the guarantees as long as markets kept going up.

Then markets stopped going up. The dot-com crash, followed by the September 11 attacks, sent equity markets into a prolonged decline. Suddenly, the guaranteed returns that Allmerica had promised to annuity holders were no longer theoretical. The company could not generate investment returns sufficient to meet its guarantees, and the liability gap threatened the entire enterprise.

CEO John F. O'Brien, who had championed the variable annuity sales strategy, resigned in 2002 under pressure. The company was in genuine financial distress—simultaneously dealing with massive variable annuity guarantee shortfalls, significant post-September 11 catastrophe and terrorism exposure, and elevated property catastrophe losses across the broader P&C market.

Meanwhile, the P&C operations were dealing with their own crisis. The September 11 attacks had generated significant catastrophe and terrorism exposure across the industry. The soft market of the late 1990s had compressed pricing to levels that were inadequate for the risks being underwritten. And Hanover's personal lines book—heavily concentrated in the Northeast and Midwest—was exposed to severe weather events that were becoming more frequent and more costly.

The 2004 and 2005 hurricane seasons delivered the killing blow to any remaining complacency. In 2004, Hurricanes Charley, Frances, Ivan, and Jeanne struck Florida in rapid succession. In 2005, Hurricane Katrina devastated the Gulf Coast, followed by Rita and Wilma. While Hanover's direct exposure to Florida was limited compared to some competitors, the cascading impact on the broader insurance market—rating agency pressure, reinsurance cost spikes, capital market nervousness—hit every carrier.

The financial damage was severe. The combination of variable annuity liabilities, post-September 11 exposure, soft market underwriting losses, and catastrophe claims had depleted capital and sent the stock into a tailspin. Rating agencies were circling. In the insurance world, a rating downgrade triggers a vicious cycle: agents move business to better-rated carriers, which reduces premium volume, which further weakens the financial position, which invites another downgrade. It is a death spiral, and Hanover was staring straight into it.

Board-level discussions turned to existential questions. Was this a viable franchise, or was it a melting ice cube? Should the company sell itself? Could it sell itself for anything meaningful given the state of its balance sheet? There were moments when the company was, by some accounts, close to being acquired or liquidated—not as a strategic transaction, but as a distressed disposal.

The leadership question was urgent: who could save this company? The situation was made more dire by a dynamic unique to insurance: the reflexive relationship between financial strength and business viability. In most industries, a weak balance sheet is a problem but not immediately existential—customers do not care about your capital ratios when they buy a hamburger or a pair of shoes. In insurance, financial strength is the product. A policy is only as valuable as the company standing behind it, and agents who place business with a carrier that subsequently cannot pay claims face their own professional liability exposure. The moment agents sense that a carrier's financial position is deteriorating, they start moving business—which accelerates the deterioration, which triggers more business movement, which accelerates it further. It is the financial equivalent of a bank run, and Hanover was dangerously close to triggering one.

The answer came in the form of an outsider who would transform not just Hanover's strategy but its entire identity.

The Turnaround: Enter Fred Eppinger (2003–2016)

In August 2003, Frederick H. Eppinger Jr. was hired as President and CEO of what was still called Allmerica Financial. He walked into a company that was approximately a two-and-a-half-billion-dollar super-regional insurer, roughly two-thirds personal lines, burdened by a parent company dragging enormous life insurance liabilities, and hemorrhaging credibility with agents, investors, and rating agencies simultaneously. It was, by any measure, one of the most challenging turnaround assignments in the insurance industry.

Eppinger's background was unusual for an insurance CEO. He came from McKinsey and Company, the management consulting firm, and had spent time at Marsh and McLennan, the insurance brokerage giant. He was not a career underwriter. He had not spent decades in actuarial departments or claims operations. He was a strategist who could see the forest when everyone else was focused on the trees—and the forest was on fire.

His diagnosis was unflinching. The underwriting was terrible. The personal lines exposure was too large and too concentrated in catastrophe-prone geographies. The company had no competitive advantage in any line of business. And the life insurance and variable annuity legacy was an anchor around the company's neck that had to be cut immediately.

The strategic pivot that Eppinger executed over the next thirteen years was one of the most dramatic transformations in insurance industry history. The plan had several pillars, each of which was controversial and each of which required abandoning deeply held assumptions about what Hanover was supposed to be.

First, exit life insurance and annuities entirely. By December 30, 2005, Hanover sold its life insurance subsidiary through a stock purchase agreement and reinsured one hundred percent of its variable life insurance and annuity business. The Life Companies segment was placed in run-off. This was not a tweak—it was an amputation. Allmerica Financial had been, at its core, a life insurance company that happened to own a P&C operation. Eppinger was saying: we are a P&C company, period. The message to investors, agents, and employees was unmistakable: we are done being confused about what we are.

Second, rebrand around the heritage. On December 1, 2005, Allmerica Financial Corporation formally changed its name to The Hanover Insurance Group, Inc. and began trading under the ticker THG on the New York Stock Exchange. This was deeply symbolic—and strategically smart. The Allmerica name carried the taint of the variable annuity disaster and the corporate complexity of the holding company era. The Hanover name carried one hundred and fifty-three years of claims-paying reputation, agent trust, and institutional memory. Eppinger was reaching back through the decades of corporate confusion to reconnect with the founding identity.

The rebranding was not mere cosmetics. It was a signal to the independent agent community—Hanover's sole distribution channel—that the company was recommitting to the P&C business and to the agent relationships that had sustained it for more than a century.

Third, rebalance the book from personal to commercial and specialty lines. In 2003, the book was approximately two-thirds personal lines. Eppinger set out to flip that ratio, targeting a business mix where commercial and specialty lines would constitute the majority of premiums. This was the most controversial element of the strategy because it meant deliberately shrinking the personal lines book that had been Hanover's bread and butter for decades. Agents who had placed personal lines with Hanover for years were told, diplomatically but firmly, that the company's future lay elsewhere.

Fourth, impose ruthless underwriting discipline. Eppinger made combined ratios—not premium growth—the primary metric of success. In insurance, the combined ratio measures the percentage of premium that goes to paying claims and expenses. A combined ratio below one hundred means the company is making an underwriting profit; above one hundred means it is losing money on the insurance itself and hoping that investment income makes up the difference. Eppinger's message was simple: we will not write business that loses money, regardless of how much premium volume it represents.

Fifth, pull back geographically from catastrophe-exposed regions. Rather than chasing premium dollars in hurricane-prone coastal markets, Hanover would concentrate its personal lines in geographies where it could price risk accurately and maintain profitability through weather cycles.

Sixth, invest in data, analytics, and underwriting talent. Eppinger recognized that specialty commercial insurance is fundamentally a knowledge business. The companies that understand risks best—that have the most talented underwriters, the best data, the most sophisticated analytics—win over time. He began building dedicated underwriting teams for specific industry verticals: construction, technology, healthcare, marine, and others.

The execution was not smooth. Deliberately shrinking your personal lines book means telling agents you are walking away from business they want to place with you. In the independent agent world, this is heresy. Agents have options—they represent multiple carriers and will simply move business to competitors who are willing to write it. Eppinger was betting that the agents who mattered most—the ones writing the most profitable commercial business—would respect the discipline and reward Hanover with their best accounts.

The bet paid off, but it took years. The cultural transformation was perhaps the hardest part—and the most consequential.

Eppinger was trying to turn an insurance company into an underwriting company—a subtle but profound distinction. An insurance company focuses on selling policies. An underwriting company focuses on selecting risks. In practical terms, the difference shows up everywhere: in how employees are incentivized (growth targets versus profitability targets), in how agents are managed (rewarding volume versus rewarding quality), in how capital is allocated (chasing market share versus building reserves), and in how success is measured (premium growth versus combined ratio improvement).

Then came the 2008 financial crisis, and the turnaround faced its ultimate test. Banks were failing, AIG was being bailed out by the federal government to the tune of one hundred and eighty-two billion dollars, and the entire financial system seemed to be teetering on the edge of collapse. Lehman Brothers had vanished overnight. Bear Stearns was gone. The commercial paper market—the lifeblood of short-term corporate financing—had seized up. For a company that had nearly died just a few years earlier, this was a terrifying moment. Insurance companies are deeply embedded in the financial system through their investment portfolios, and a severe enough market dislocation could impair the capital base that supports the underwriting operation.

But Hanover not only survived—it emerged stronger. The conservative reserving practices, the disciplined underwriting, the deliberate avoidance of exotic financial products, the clean investment portfolio that Eppinger had insisted on—all of these looked prescient in the aftermath of the crisis. While AIG was being rescued because of its exposure to credit default swaps and other derivatives, Hanover's investment portfolio was invested conservatively in investment-grade bonds with no exposure to the toxic instruments that were destroying other financial institutions.

The validation came from an unexpected source. During the 2008 crisis, Hanover became the only insurer in the country to have its ratings upgraded by all three major rating agencies: A.M. Best, Moody's, and Standard and Poor's. In an industry where everyone else was being downgraded, Hanover was being upgraded. This was not luck. It was the result of three years of disciplined execution that had strengthened the balance sheet and cleaned up the underwriting book before the storm hit.

The acquisition strategy under Eppinger was surgical and disciplined. In 2008, Hanover acquired AIX Holdings, a specialty program and alternative risk transfer carrier with eighty-five million dollars in gross written premium. This gave Hanover capabilities in program business and excess and surplus lines—specialty niches that commanded better pricing and required deeper expertise. In 2009, Hanover acquired the renewal rights to approximately four hundred million dollars of OneBeacon's small and middle market commercial business, along with roughly two hundred new agent relationships and a hundred employees. This transaction accelerated the western expansion that Eppinger had been pursuing and brought in experienced commercial lines talent.

By the time Eppinger announced in September 2015 that he would step down in 2016, the transformation was essentially complete. The company had grown from two and a half billion dollars to approximately four billion in revenues. The business mix had shifted from two-thirds personal lines to a more balanced portfolio weighted toward commercial and specialty. The stock had recovered from its crisis-era lows. And the culture had fundamentally changed: Hanover was now an underwriting company that happened to sell insurance, not the other way around.

Eppinger's thirteen-year tenure is a masterclass in corporate turnaround. He inherited a company on the brink of death and left behind a franchise with a clear identity, disciplined underwriting, a strong balance sheet, and a culture that prioritized profitability over growth. The Wall Street Journal recognized Hanover for shareholder value creation in 2007. In 2011, the company absorbed record catastrophe losses of three hundred and sixty-two million dollars and remained financially sound—a stress test that would have been unthinkable five years earlier. By 2013, Hanover crossed the five-billion-dollar premium threshold, and in 2015, Standard and Poor's upgraded the operating subsidiaries to an A rating.

Building the Specialty Machine (2008–2018)

The new Hanover that emerged from the Eppinger turnaround was a fundamentally different animal from the sleepy personal lines carrier it had been a decade earlier. The company was now organized around a core conviction: that mid-size insurers win by knowing more about specific risks than anyone else, not by being the cheapest or the biggest.

The specialty niches that Hanover built out during this period each represented a deliberate strategic choice. Construction and contractors insurance required deep knowledge of project types, subcontractor risks, and completed operations exposure. Technology and life sciences demanded understanding of intellectual property risks, clinical trial liabilities, and rapidly evolving regulatory environments. Healthcare required expertise in medical malpractice trends, regulatory compliance, and the unique risk profiles of different provider types. Marine insurance drew on the company's century-old charter expansion and required specialized knowledge of cargo, hull, and liability risks. Each niche had a dedicated underwriting team staffed with specialists who understood their industries at a granular level.

This specialization strategy was the antithesis of the commodity insurance approach that had dominated the industry for decades. Rather than competing on price for generic commercial policies, Hanover was competing on expertise for complex risks where underwriting knowledge translated directly into better loss ratios. The agents who placed this business valued the expertise because it helped them serve their clients better—and because a specialist carrier was less likely to surprise them with unexpected claim denials or coverage gaps.

The agency model proved to be a genuine competitive advantage during this period. While direct writers and InsurTech startups were investing billions in consumer-facing technology and advertising, Hanover was investing in making its agents' lives easier. Technology that simplified the quoting process, claims handling that was responsive and fair, underwriting expertise that helped agents win and retain accounts—these were the weapons in Hanover's arsenal, and they were weapons that a direct writer could not easily replicate.

The most significant strategic move of this era was the 2011 acquisition of Chaucer Holdings PLC, a publicly listed specialist Lloyd's of London insurance group based in the United Kingdom. The price tag was approximately four hundred and seventy-four million dollars, and the rationale was compelling on paper: Chaucer gave Hanover direct access to the Lloyd's of London market for the first time, enabling it to serve agents whose clients had complex cross-border or specialty risks that exceeded the capabilities of a domestic insurer.

Chaucer brought recognized underwriting expertise in energy, marine, aviation, nuclear, and other complex specialty lines. It added meaningful geographic and product diversification to offset U.S. catastrophe exposure. And it positioned Hanover as a more complete carrier for its best independent agents handling larger accounts. The Lloyd's platform was, in many ways, the culmination of the specialty strategy—a statement that Hanover was no longer a regional personal lines carrier but a global specialty underwriter.

The integration was not without challenges. Operating a Lloyd's syndicate from Worcester, Massachusetts required navigating different regulatory environments, different market customs, and different talent pools. The London market operates on relationships and reputation in ways that are similar to but distinct from the U.S. independent agent channel. And the capital requirements of maintaining a Lloyd's platform competed with other investment opportunities in the domestic U.S. market.

Meanwhile, in small commercial insurance, Hanover was building what would become one of its most important competitive weapons. The company developed a bundled product approach—later formalized as TAP, or Tailored Account Protection—that combined property, liability, and specialty coverages in a single carrier solution with multi-line credits and harmonized policy language. For agents writing small commercial accounts—businesses with annual premiums under one hundred thousand dollars—this was transformative. Instead of piecing together coverage from multiple carriers, agents could place an entire account with Hanover through a simplified underwriting process.

The small commercial segment is a fundamentally different game from middle market or large account commercial insurance. The accounts are smaller, the margins are tighter, and the key to profitability is efficiency—processing more quotes and binding more policies with less human intervention. Hanover invested in technology that enabled agents to quote and bind small commercial policies quickly, reducing the friction that made small accounts economically marginal for many carriers.

The talent strategy was equally important. Eppinger and his team built what they called underwriting centers of excellence—concentrations of specialist talent focused on specific industry verticals. This was not just hiring; it was creating an institutional knowledge base that would compound over time. As underwriters gained experience in their specialties, they became better at selecting risks, pricing coverage, and identifying emerging trends. This knowledge was difficult for competitors to replicate because it was embedded in people and processes, not in technology or capital.

The economics of specialty underwriting deserve emphasis because they explain why Hanover's strategy worked. In commodity commercial insurance—a generic general liability policy for a small retailer, say—the product is essentially interchangeable across carriers, and agents shop primarily on price. The carrier with the lowest cost structure wins, which favors scale players. In specialty commercial insurance—a professional liability policy for a biotech company conducting clinical trials, or a construction wrap-up policy for a complex urban development—the product is not interchangeable. The underwriter's knowledge of the specific industry, the quality of the policy language, the carrier's claims-handling expertise in that niche, and the agent's confidence that the carrier will respond appropriately when a complex claim arises—these factors matter far more than price. This is the market where Hanover chose to compete, and it is a market where expertise creates genuine pricing power.

The profitability inflection was real and measurable. Combined ratios consistently came in below ninety-five, and return on equity improved steadily. By the mid-2010s, Hanover had established itself as one of the most consistently profitable mid-size P&C insurers in the country—a remarkable achievement for a company that had been on the brink of extinction just a decade earlier. The question was whether this performance could be sustained and extended under new leadership, and whether the Chaucer acquisition would deliver the strategic benefits that had justified its price tag.

The Modern Era: Digital Transformation and Market Leadership (2017–Present)

In October 2017, John C. "Jack" Roche was named President and CEO of The Hanover Insurance Group under circumstances that were, to put it delicately, not entirely planned. Joseph Zubretsky, who had been brought in from Aetna as Eppinger's successor in 2016, departed after barely a year to pursue an opportunity in healthcare. Roche, who had been with Hanover since 2009—having come over from OneBeacon as part of the commercial business acquisition—stepped into the role. He had risen through commercial lines leadership and was deeply embedded in the independent agent strategy that defined the company.

The CEO transition raised an important question: would Roche continue the Eppinger playbook, or would he chart a different course? Corporate turnaround experts note that the most dangerous moment in any transformation is the second leadership transition—the first new leader creates the new direction, but the second must decide whether to sustain it, evolve it, or replace it. The wrong choice at this juncture can unravel a decade of progress. Roche's answer turned out to be a nuanced combination of continuity and evolution. He doubled down on the domestic specialty commercial strategy while making one bold move that signaled a willingness to think independently.

In September 2018, Hanover announced the sale of Chaucer to China Reinsurance Group Corporation for total proceeds of nine hundred and fifty million dollars—roughly double the four hundred and seventy-four million dollar acquisition price paid seven years earlier. The sale closed on December 31, 2018. On its face, this was a successful trade: buy low, sell high, pocket a near two-times return in seven years. But the strategic implications were more significant than the financial math, and the decision revealed something important about Roche's leadership style: a willingness to admit that even a successful acquisition might not be the right long-term fit.

Roche and his team had concluded that Hanover was better positioned as a focused U.S. domestic P&C insurer. Chaucer had grown substantially and was performing well, but managing a Lloyd's platform from Worcester created operational complexity that distracted from the core U.S. business. The time zone challenges alone were significant—London market decisions needed to be made during London business hours, requiring either dedicated leadership in London or a management team in Worcester that was perpetually stretched across two continents. The capital freed up by the sale could be redeployed more productively—into U.S. specialty expansion, technology investments, and shareholder returns. In 2019, Hanover returned eight hundred and fifty million dollars to shareholders through buybacks and dividends—a number representing roughly fourteen percent of the company's market capitalization at the time. This staggering capital return demonstrated both the financial benefit of the Chaucer sale and management's confidence in the underlying business.

The technology acceleration under Roche has been substantive rather than cosmetic. In 2021, Hanover launched TAP Sales, a quote-and-issue platform specifically designed for small commercial insurance. The platform enabled agents to quote business owners policies, general liability, workers' compensation, and professional lines coverage through a streamlined digital interface. This was not technology for technology's sake—it was technology that solved a specific business problem: making small commercial accounts economically viable by reducing the time and cost required to process them.

More recently, Hanover has deployed artificial intelligence for submission triage in its specialty lines. When an agent submits a complex commercial risk for underwriting review, AI-powered tools now help prioritize and route submissions, identify key risk factors, and flag potential concerns before a human underwriter begins their analysis. Management has described this initiative as "delivering nicely," and its impact shows up in processing speed and underwriting efficiency metrics.

The COVID-19 pandemic in 2020 and 2021 tested the entire insurance industry. Business interruption claims, questions about pandemic coverage, remote work disruptions, and unprecedented economic volatility created challenges for every carrier. Hanover navigated the pandemic period better than many peers, in part because its specialty commercial focus meant its book was less exposed to the sectors hit hardest by lockdowns, and in part because its conservative reserving practices provided a cushion against unexpected claim development.

Social inflation—the trend of increasing litigation costs, larger jury verdicts, and expanded theories of liability—has been a persistent headwind for the entire property and casualty industry through the 2020s. Nuclear verdicts, where jury awards exceed ten million dollars, have become more common across casualty lines. Hanover has responded by tightening terms and conditions in its casualty book, increasing pricing on liability lines, and investing in claims management capabilities to identify and manage problematic claims earlier in their development.

The hard market that began in 2019 and extended through much of the 2020s has been a tailwind for disciplined underwriters like Hanover. To understand why this matters, consider the insurance pricing cycle. During soft markets—periods of intense competition and excess capital—insurers cut prices to retain and win business, often to levels that do not adequately cover the risks being assumed. The losses from underpriced policies emerge two, three, or five years later, depleting capital and forcing carriers to raise prices. This triggers a hard market, where pricing power returns and disciplined underwriters can earn attractive returns. The cycle then repeats, typically over five-to-ten-year intervals. Hanover's agency relationships and specialty expertise positioned it to retain business even as prices rose—agents were less likely to move accounts from a carrier they trusted and that provided genuine underwriting expertise.

The Workers' Comp Advantage product, which leverages technology to improve the workers' compensation underwriting and service experience, was live in seventeen states by 2025 with a national rollout targeted by the end of 2026. This product exemplifies Roche's approach: use technology to improve the agent and customer experience in specific product lines, creating competitive differentiation that is difficult to replicate quickly.

The ESG and climate risk conversation has become increasingly material for property and casualty insurers. Hanover's approach has been practical rather than aspirational: improve catastrophe modeling, tighten property underwriting in exposed geographies, adjust pricing to reflect changing risk profiles, and strengthen the reinsurance program. The company has been deliberately deconcentrating its personal lines exposure in the Midwest—particularly in Michigan, where Citizens Insurance has historically represented a large share of the book—to reduce the volatility impact of any single weather event. This is not glamorous work, but it is the kind of disciplined portfolio management that separates excellent insurers from average ones.

The results have been striking. Full year 2025 represented a record for the company: net written premium of six point three two billion dollars, a combined ratio of ninety-one point six percent, net income of six hundred and sixty-two million dollars, and an operating return on equity of twenty percent. The fourth quarter was particularly impressive, with a combined ratio of eighty-nine percent and an operating return on equity of twenty-three percent. Book value per share grew twenty-seven percent year-over-year to approximately one hundred and one dollars. The company's dividend has been increased for twenty-one consecutive years.

The current Hanover looks nothing like the company that nearly died in the early 2000s. Net written premium has more than doubled. The business mix has shifted decisively toward commercial and specialty lines, with core commercial and specialty now representing fifty-eight percent of the book. The combined ratio has improved by hundreds of basis points. Net investment income reached four hundred and fifty-four million dollars in 2025, up twenty-two percent year-over-year, reflecting both higher interest rates and portfolio growth.

And the balance sheet is at the strongest level in the company's history, with A.M. Best characterizing its risk-adjusted capitalization at the highest tier. The company's A.M. Best financial strength rating of A (Excellent) with a stable outlook, and its Standard and Poor's A rating, provide the credibility that agents and commercial buyers require when placing significant risks.

For 2026, management has guided for mid-single-digit premium growth, an expense ratio of thirty point three percent, and an ex-catastrophe combined ratio of eighty-eight to eighty-nine percent. The implied full-year combined ratio, including a catastrophe load of six and a half percent, would be approximately ninety-four and a half to ninety-five and a half percent—still solidly profitable but reflecting the inherent volatility that comes with writing property insurance in an era of increasing climate-related catastrophes.

The Business Model Deep Dive

Insurance is one of the most misunderstood businesses in capitalism. Most people assume insurance companies make money by collecting premiums and paying out less than they collect. That is part of the story, but it misses the most important part. The real economic engine of insurance is the float—the money that sits between when premiums are collected and when claims are paid. This float can be invested, and the investment income it generates is often the primary source of profit. Warren Buffett has described insurance as a "reverse financing" business: instead of paying interest to borrow money, you get paid premiums to hold other people's money.

The combined ratio is the single most important metric in property and casualty insurance, and it deserves a clear explanation. The combined ratio is the sum of two components: the loss ratio (claims paid plus adjustment expenses divided by premiums earned) and the expense ratio (operating expenses divided by premiums earned). A combined ratio of ninety-five means the company spends ninety-five cents on claims and expenses for every dollar of premium collected, earning a five-cent underwriting profit. A combined ratio of one hundred and five means the company loses five cents on every premium dollar and needs investment income to turn a profit. In the insurance industry, a combined ratio consistently below ninety-five is considered excellent. Hanover's 2025 combined ratio of ninety-one point six—and its fourth quarter ratio of eighty-nine—place it among the best performers in the industry.

Why does discipline beat growth in insurance? Because insurance is one of the few businesses where you price your product before you know what it costs. When an underwriter prices a five-year directors and officers liability policy, they are making a bet on legal trends, regulatory changes, and economic conditions over a half-decade horizon. If they underprice, the losses will show up years later when claims mature and are settled—long after the premium has been collected, the commission has been paid to the agent, and the underwriter's bonus has been deposited. This asymmetry creates a structural temptation to underprice in order to grow, and it is the single greatest source of value destruction in the insurance industry. The executives who grow premium aggressively get promoted during the boom years; the actuaries who discover the underpricing get blamed during the bust years. The incentive misalignment is chronic and systemic, which is why the companies that solve it—through culture, compensation design, and leadership—possess a genuine competitive advantage.

Hanover's specific model is built on several distinctive characteristics. The product mix is now weighted approximately forty-one percent personal lines, thirty-six percent core commercial, and twenty-two percent specialty—a far cry from the two-thirds personal lines mix that existed in 2003. The distribution model is one hundred percent through independent agents—no direct channel, no captive agent force, no online-only products. This commitment has been unwavering for more than one hundred and seventy years, and it is both a strength and a limitation.

The strength of the agency model is relational depth. Independent agents represent multiple carriers and place business where they get the best combination of coverage, price, and service. An agent who has worked with Hanover for twenty years, who knows the underwriters by name, who has seen the company pay claims fairly and promptly through multiple catastrophe seasons—that agent is not easily persuaded to move business to a new carrier offering a slightly lower price. The switching costs are real, even if they are not contractual.

The limitation is efficiency. Agents take a commission—typically fifteen to twenty percent of premium—that a direct writer avoids. This means Hanover must generate superior loss ratios to compensate for the higher distribution cost. The specialty focus addresses this directly: in specialty commercial lines, the underwriting expertise that agents value creates pricing power that offsets the commission drag. In commoditized personal lines, the math is harder, which is why Hanover has strategically de-emphasized volume personal lines in favor of "preferred accounts" where loss ratios are better.

Reserving discipline is another crucial element of Hanover's model. Insurance reserves are the estimated future cost of claims that have already occurred but have not yet been settled. Setting reserves is as much art as science, and the temptation to under-reserve—thereby inflating current-period profits—has destroyed more insurance companies than any catastrophe. Hanover's conservative reserving approach, established during the Eppinger turnaround, creates a margin of safety that protects against adverse claim development. When reserves prove to be more than adequate, the excess is released into income as a "reserve release"—a sign of quality when it reflects genuine conservatism rather than prior-period manipulation.

The reinsurance strategy is the final piece of the puzzle. Hanover purchases reinsurance to cap its catastrophe exposure—essentially buying insurance on its own insurance portfolio. Think of it this way: if Hanover writes homeowners policies across New England and a massive nor'easter generates five hundred million dollars in claims, the reinsurance program ensures that Hanover's actual loss is capped at a manageable level—perhaps fifty or seventy-five million dollars—with the reinsurer absorbing the rest. This limits the downside from any single event or series of events, protecting the capital base and the financial strength ratings that are essential for maintaining agent confidence. After the Chaucer sale in 2018, Hanover's reinsurance program became focused entirely on domestic U.S. catastrophe exposure, simplifying the program and reducing costs.

The investment portfolio is worth a brief mention because it generates meaningful income—four hundred and fifty-four million dollars in 2025, up twenty-two percent year-over-year. Hanover invests its float conservatively, primarily in investment-grade fixed income securities. The company does not take large credit risks or duration bets with its investment portfolio. This conservatism costs returns in benign environments but protects capital in stress scenarios—a trade-off that aligns perfectly with the underwriting-first culture that defines the company.

Competitive Landscape and Industry Dynamics

Hanover occupies a specific niche in the American property and casualty insurance landscape: a mid-size, independent agent-exclusive carrier with a specialty commercial focus. Understanding who it competes with—and why—requires understanding the industry's unusual competitive structure.

At the top of the market, national carriers like Travelers, Chubb, Hartford, and Liberty Mutual command massive scale, global reach, and brand recognition. Travelers alone writes nearly forty billion dollars in annual premium—more than six times Hanover's volume. Chubb, the world's largest publicly traded P&C insurer, brings global capabilities and a brand that commands premium pricing in every line it enters. These companies can spread fixed costs across enormous premium bases, invest hundreds of millions annually in technology, and attract the largest commercial accounts. Hanover does not compete head-to-head with these companies on their largest accounts. Instead, it targets the small and middle market commercial accounts—businesses with revenues typically between one million and twenty-five million dollars—where specialist knowledge matters more than brand and scale.

Among regional specialists, Cincinnati Financial is perhaps the closest comparison. Like Hanover, Cincinnati operates exclusively through independent agents, focuses on commercial lines, and emphasizes long-term agent relationships over short-term growth. Selective Insurance, RLI, and Erie Indemnity occupy similar niches with slightly different geographic and product emphases. These are the companies that Hanover competes with most directly for agency shelf space and commercial accounts.

In specialty lines, Markel and W.R. Berkley represent sophisticated competitors that have built profitable franchises on underwriting expertise in niche markets. These companies tend to be more focused on excess and surplus lines and specialty risks, with less personal lines exposure than Hanover.

The InsurTech question—whether technology startups can fundamentally disrupt the traditional insurance model—has been answered, at least partially, over the past decade. Companies like Lemonade, Root, and Hippo attracted enormous venture capital investment and generated significant media attention but have struggled to achieve profitability. Lemonade, the most prominent InsurTech, went public in 2020 at a sky-high valuation but has consistently reported combined ratios well above one hundred—meaning it loses money on every policy it writes. The fundamental challenge is that insurance is not a technology problem—it is an underwriting problem. Technology can improve efficiency, reduce friction, and enhance the customer experience, but it cannot substitute for the actuarial judgment and industry expertise required to price complex risks accurately.

Hanover's response to InsurTech has been pragmatic rather than defensive: invest in technology that makes its agents more efficient rather than trying to replace them. The company treated InsurTech not as a threat to its existence but as a source of ideas for improving agent workflows and customer experience within its existing distribution model.

The industry dynamics that shape Hanover's competitive environment are formidable. Social inflation—the trend toward larger jury verdicts and more aggressive litigation—is increasing the cost of casualty claims across the industry. Climate change is making catastrophe modeling more difficult and more important, as historical loss patterns become less reliable predictors of future losses. Regulatory complexity—insurance is regulated at the state level, meaning carriers must navigate fifty different regulatory environments—creates compliance costs that are disproportionately burdensome for smaller companies. And the cyclical nature of insurance pricing—alternating between soft markets where competition drives prices below sustainable levels and hard markets where pricing power returns—requires the discipline to maintain underwriting standards when competitors are cutting prices.

Why is insurance so hard? Because you price before you know your costs, the feedback loops are measured in years rather than months, and the commodity-like nature of the product creates relentless pressure to compete on price rather than quality. Consider a simple analogy: imagine running a restaurant where you have to set menu prices today but will not know the cost of your ingredients until three years from now. You might guess right, or inflation, supply chain disruptions, or ingredient shortages might make your prices look foolishly low in hindsight. Now multiply that uncertainty across thousands of policies and dozens of risk categories, and you begin to understand why insurance underwriting is so difficult.

The companies that win over long periods are the ones that resist the temptation to grow during soft markets and invest in the capabilities—underwriting talent, data analytics, agent relationships—that create durable competitive advantages. Hanover's post-turnaround performance suggests it has internalized these lessons, but the real test of any insurance company's discipline comes not during hard markets, when pricing power makes profitability easy, but during soft markets, when the temptation to sacrifice underwriting standards for growth becomes almost irresistible.

Porter's Five Forces Analysis

The threat of new entrants in property and casualty insurance is moderate. Capital requirements are substantial—you need hundreds of millions of dollars in surplus to write meaningful premium volume—and regulatory barriers are significant. Every state has its own insurance department, its own licensing requirements, and its own rate approval processes. But the barriers are not insurmountable. InsurTech companies and technology giants have probed the edges of the market, though none has achieved the scale or profitability required to fundamentally disrupt incumbents. Perhaps more importantly, distribution relationships take years to build. An agent who has worked with Hanover for two decades is not going to abandon that relationship for a startup with a slick app and no track record of paying claims.

The bargaining power of suppliers is low. The primary "suppliers" to an insurance company are capital providers, and capital for insurance operations is globally abundant. Reinsurance—the insurance that insurers buy to protect themselves—is cyclical but competitive, with dozens of global reinsurers competing for business. Talent is perhaps the most constrained supply factor, particularly specialist underwriting talent in niche commercial lines, but this is an industry-wide challenge rather than a Hanover-specific vulnerability.

The bargaining power of buyers is moderate to high and varies significantly by segment. Large commercial insurance buyers are sophisticated purchasers who use brokers to shop their programs across multiple carriers. Small commercial buyers are more price-sensitive but also more loyal once they find a carrier and agent they trust. The independent agents who distribute Hanover's products hold significant power—they control the customer relationship and can redirect business to competing carriers if they are dissatisfied with Hanover's pricing, service, or underwriting appetite.

The threat of substitutes is low to moderate. Insurance is legally required for many risks—workers' compensation, commercial auto, professional liability in certain fields—creating a baseline of mandatory demand. Self-insurance is an option for large corporations but is impractical for the small and middle market businesses that constitute Hanover's core clientele. Captive insurance companies and alternative risk transfer mechanisms are growing but remain niche solutions for specific risk profiles.

Competitive rivalry is the dominant force in this industry, and it is intense. The property and casualty insurance market is fragmented, with thousands of carriers competing for business. Price competition is brutal during soft markets, when excess capital and overcapacity drive premiums below sustainable levels. Product commoditization is a constant pressure—a commercial general liability policy from Hanover is not fundamentally different from one issued by Travelers or Hartford. And the cyclical nature of the market means that underwriting discipline is perpetually tested by competitors willing to sacrifice profitability for market share.

Hanover operates in a structurally challenging industry where the primary defense against these forces is operational excellence rather than structural moats. The Porter's framework reveals an important insight: in insurance, competitive advantages are earned through daily execution rather than established through structural barriers. There is no equivalent of a technology platform's network effects or a pharmaceutical company's patent portfolio. Every year, agents and clients make active choices about which carriers to use, and every year, those choices are influenced by pricing, service, claims handling, and financial strength. This creates both risk and opportunity: the risk of losing business to a competitor who offers a better deal, and the opportunity to gain business by consistently delivering superior underwriting and service.

Hamilton's Seven Powers Analysis

Scale economies in insurance are weaker than most investors assume, and this is one of the most important insights for anyone analyzing the industry. Unlike technology businesses where marginal costs approach zero—where serving the millionth user costs essentially nothing after the platform is built—insurance has relatively linear cost structures. More premium means more claims to adjust, more agents to service, more underwriters to employ, and more regulatory filings to submit. There are some scale benefits in technology infrastructure, claims management, and brand recognition, but they are modest compared to the underwriting expertise that drives profitability. A brilliantly run three-billion-dollar insurer will outperform a poorly run thirty-billion-dollar insurer every single time. This is why the insurance industry remains fragmented despite decades of consolidation pressure—scale alone does not confer a decisive advantage.

Network economies are essentially absent. Insurance is not a network business in the traditional sense—this is not Visa, where every additional merchant makes the card more valuable to every cardholder. More policyholders do not make a Hanover policy more valuable for other policyholders. Hanover's agent network is valuable in its own right, but it does not exhibit the flywheel dynamics of a true network effect. Adding one more agent does not make the platform meaningfully more attractive to other agents or to policyholders. The value is linear, not exponential.

Counter-positioning is historically relevant but fading. The Eppinger-era pivot to specialty commercial was a classic counter-positioning move: Hanover abandoned the personal lines business that mega-carriers were fighting over and invested in specialty niches that those same carriers were under-resourcing. The large carriers could not easily follow because their organizations, incentives, and agent relationships were built around high-volume personal lines distribution. A Travelers or Hartford executive who suggested shrinking the personal lines book by thirty percent to invest in specialty niches would have been shown the door—their boards, analysts, and investors expected premium growth, not premium shrinkage. Hanover, freed by its near-death experience and smaller scale, could make the pivot that larger competitors could not. But a decade later, many competitors have adopted similar specialty strategies, reducing the counter-positioning advantage. Counter-positioning is a wasting asset—it works until others catch on.

Switching costs are moderate and relationship-driven. Commercial insurance clients switch carriers with reasonable frequency—policies typically renew annually, and brokers actively shop the market on their clients' behalf. Industry data suggests that commercial account retention rates for the best carriers run in the mid-eighties to low-nineties percent range, meaning that even well-run insurers lose ten to fifteen percent of their accounts each year. But relationships matter. An agent who has worked with a Hanover specialty underwriter for years, who trusts that underwriter's judgment and responsiveness, is less likely to move an account over a small price difference. Claims experience is another powerful source of stickiness: a client who has had a complex claim—a construction defect lawsuit, a cyber breach, a professional liability action—handled efficiently and fairly by Hanover is genuinely reluctant to switch to an unknown carrier for their next renewal. The fear of an untested claims department during a future crisis creates a switching cost that is emotional as much as economic.

Branding in insurance is real but nuanced. Hanover is not a consumer brand like GEICO or State Farm—most insurance buyers have never heard of it. But among independent agents and commercial insurance buyers, the Hanover name carries weight. One hundred and seventy-four years of claims-paying history, an A.M. Best A rating, and a reputation for underwriting expertise create a brand advantage in the intermediated commercial market where Hanover competes.

Cornered resources are weak to moderate. Specialist underwriting talent in niche commercial lines—construction, healthcare, marine, life sciences—represents a quasi-cornered resource. These underwriters have deep industry knowledge, agent relationships, and proprietary loss data that are difficult to replicate quickly. But talent is ultimately mobile, and competitors can hire away key people.

Process power is Hanover's strongest competitive dimension. The underwriting discipline institutionalized during the Eppinger turnaround, the data analytics capabilities built over the past decade, the technology-enabled efficiency in small commercial, and the culture of profitability over growth—these are process advantages that compound over time and are difficult for competitors to observe and replicate. A competitor can copy a product form or match a price, but replicating an entire organizational culture built around underwriting excellence is a multi-year endeavor that most companies lack the patience to pursue.

The summary is important for investors to understand: Hanover's competitive position is built on process power and moderate switching costs, not on dominant scale or network effects. This is a business that requires grinding execution excellence every single day. There are no structural moats that protect against complacency. The moment Hanover's underwriting discipline slips—the moment growth becomes more important than profitability—the competitive advantages start eroding. This makes management quality and cultural continuity the most critical variables in any investment thesis.

The Hamilton Helmer framework reveals something else that is worth dwelling on: in businesses without strong structural powers, the quality of management matters more than in almost any other type of investment. A mediocre management team at a company with strong network effects—say, a dominant social media platform—can still generate attractive returns because the structural power does the heavy lifting. A mediocre management team at an insurance company will destroy value within two to three years by loosening underwriting standards, chasing premium growth, and under-reserving against future claims. The corollary is that an excellent management team at an insurance company—one that genuinely internalizes underwriting discipline as a cultural principle rather than a quarterly talking point—can compound value at rates that surprise investors accustomed to dismissing insurers as low-return businesses.

Bull vs. Bear Case

The bull case for Hanover begins with strategic positioning. The company's specialty commercial focus is precisely the right strategy in an environment of hardening commercial insurance rates. While personal lines carriers are fighting margin compression from inflation, climate costs, and regulatory constraints, specialty commercial writers like Hanover are enjoying pricing power and strong demand for complex coverage solutions. The combined ratio trajectory tells the story: from the mid-nineties in 2024 to ninety-one point six in 2025, with the fourth quarter coming in at an extraordinary eighty-nine percent. To put that in context, the industry average combined ratio typically hovers around ninety-eight to one hundred, meaning most insurers barely break even on their underwriting before investment income. Hanover's recent performance represents genuine underwriting profit at levels that only the best-run carriers achieve consistently.

The valuation argument adds another dimension. Hanover has historically traded at one to one-point-three times book value, a range that appears modest relative to the quality of the underlying franchise. With book value per share now exceeding one hundred dollars and the stock trading around one hundred and seventy-four dollars, the market is assigning a meaningful premium to book value—but one that remains well below the multiples commanded by peers with comparable or inferior underwriting track records. For value-oriented investors, the combination of consistent profitability, strong capital returns, and a reasonable valuation multiple is compelling.

The technology investments are creating compounding efficiency advantages. TAP Sales has reduced the time and cost required to quote small commercial accounts. AI-powered submission triage is improving productivity in specialty lines. The Workers' Comp Advantage product, expanding toward national availability, represents a meaningful growth opportunity. These investments do not show up as dramatic one-time gains—they show up as incremental improvements in expense ratios and underwriting accuracy that compound over years.

The agency distribution model, far from being the anachronism that InsurTech enthusiasts predicted, has proven remarkably resilient. Independent agents remain the dominant distribution channel for commercial insurance because commercial buyers need advice, not apps. An agent who understands a construction company's risk profile, who can design a coverage program that addresses project-specific exposures, who can advocate for the client during a complex claim—that agent provides value that cannot be replicated by an algorithm. Hanover's deep relationships with approximately two thousand independent agency partners represent decades of accumulated trust and mutual economic interest.

The agency distribution model, far from being the anachronism that InsurTech enthusiasts predicted, has proven remarkably resilient. Independent agents remain the dominant distribution channel for commercial insurance because commercial buyers need advice, not apps. An agent who understands a construction company's risk profile, who can design a coverage program that addresses project-specific exposures, who can advocate for the client during a complex claim—that agent provides value that cannot be replicated by an algorithm. Hanover's deep relationships with approximately two thousand independent agency partners represent decades of accumulated trust and mutual economic interest.

The capital allocation story is equally compelling. Twenty-one consecutive years of dividend increases, consistent share repurchases, and disciplined investment in growth opportunities demonstrate management's commitment to shareholder returns. The 2019 return of eight hundred and fifty million dollars following the Chaucer sale was a masterful deployment of capital that signaled both financial strength and strategic clarity.

The bear case centers on structural challenges that even excellent execution may not overcome. The "muddy middle" critique—that Hanover is too small to achieve the scale economies of Travelers or Chubb but too large for the nimbleness of a boutique specialty carrier like RLI or Kinsale Capital—has some validity. At six billion dollars in premium, Hanover is roughly one-sixth the size of Travelers but several times larger than the most focused specialty carriers. As the industry consolidates, mid-size carriers may find themselves squeezed between scale players who can invest more in technology and talent, and smaller specialists who can move faster into emerging niches.

The hard market will eventually soften. Insurance pricing is cyclical, and the favorable pricing environment that has boosted Hanover's recent results will inevitably give way to increased competition and margin compression. The question is not whether the soft market will return, but whether Hanover's underwriting discipline will hold when premiums start declining and agents are pressuring for competitive pricing.