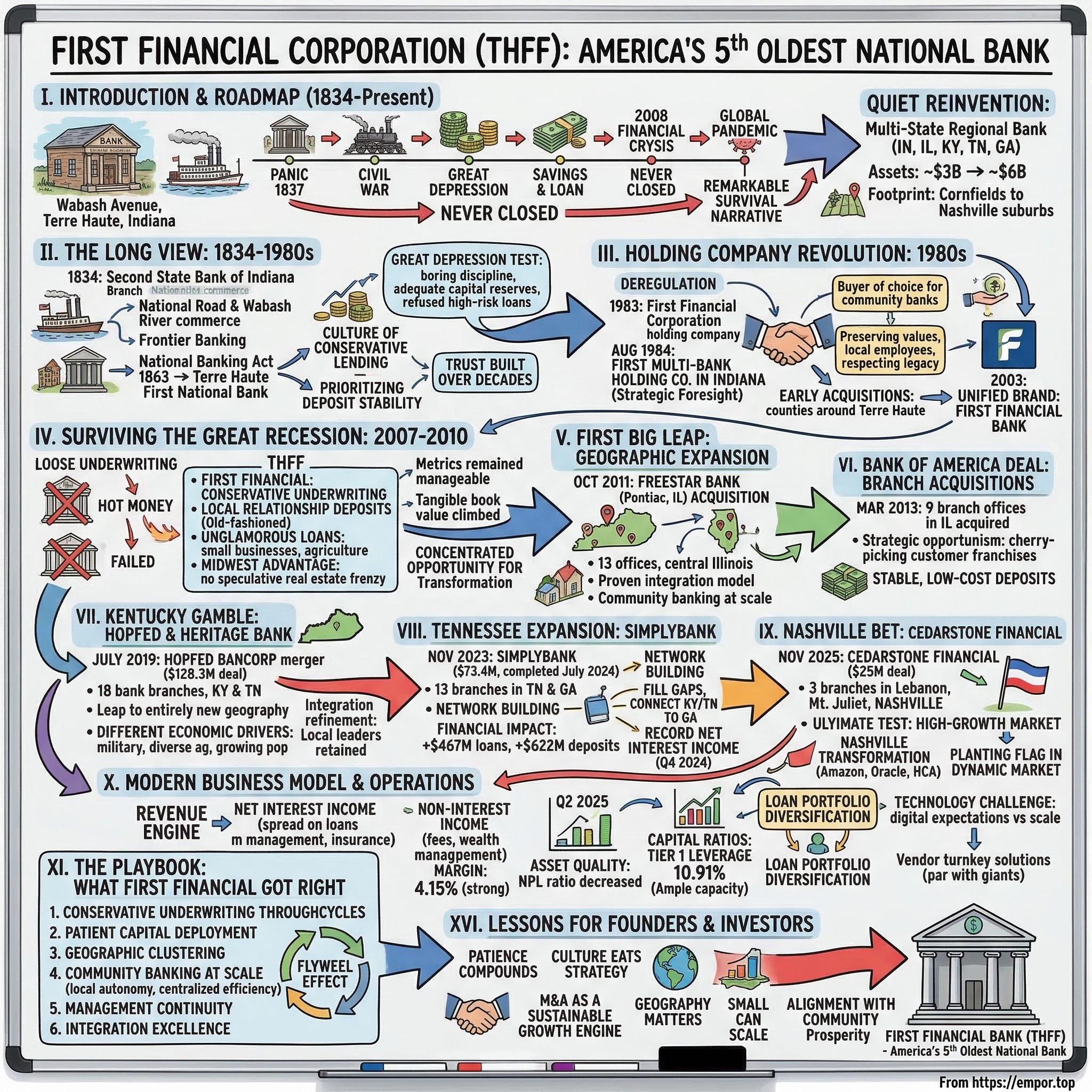

First Financial Corporation: The Story of America's Fifth-Oldest National Bank

I. Introduction and Episode Roadmap

There is a building on Wabash Avenue in Terre Haute, Indiana, that has been in the banking business since before the state of Indiana was even two decades old. The year was 1834. Andrew Jackson was president. The Second Bank of the United States was fighting for its life in a war against Jackson's populist fury. And in the Wabash River Valley, in a frontier town that served as a gateway to the American West, a branch of the Second State Bank of Indiana opened its doors.

That branch never closed. Not during the Panic of 1837. Not during the Civil War. Not during the Great Depression. Not during the savings and loan crisis. Not during the 2008 financial cataclysm that killed nearly five hundred American banks. And not during a global pandemic that shuttered businesses from coast to coast.

Today, that institution operates as First Financial Bank, a subsidiary of First Financial Corporation, ticker symbol THFF on the NASDAQ. It is the fifth oldest national bank in the United States. And its story is one of the most quietly remarkable survival narratives in American finance.

The central question of this episode is deceptively simple: How does a small-town Midwest bank not only survive but thrive through nearly two centuries of financial crises, consolidation waves, and digital disruption? The answer involves conservative banking philosophy tested against growth ambition, geographic expansion executed through disciplined mergers and acquisitions, and the enduring power of the community bank model in an era when most people assume that model is dead.

What makes First Financial worth studying is not just its longevity but its recent transformation. For most of its existence, this was a single-market bank serving the counties around Terre Haute. Over the past fifteen years, through a series of carefully sequenced acquisitions, it has quietly reinvented itself as a multi-state regional operator spanning Indiana, Illinois, Kentucky, Tennessee, and Georgia. Its consolidated assets have grown from around three billion dollars to nearly six billion, and its footprint now stretches from the cornfields of central Indiana to the booming suburbs of Nashville.

The market cap sits at roughly $767 million today, a figure that would barely register as a rounding error at JPMorgan Chase. But size, as this story demonstrates, is not the only measure of success. And the trajectory from Terre Haute to Nashville tells us something important about what it actually takes to build an enduring financial institution in America.

This is the playbook for regional bank survival. And it starts, as all great American stories do, on the frontier.

II. The Long View: 1834 to the 1980s

Before diving into the modern transformation story, we need to understand the soil from which First Financial grew. Because in banking, more than almost any other industry, history is not just context. It is competitive advantage.

Picture Terre Haute in 1834. The town sits on the high eastern bank of the Wabash River, its name a French phrase meaning "high land," a remnant of the fur traders and voyageurs who had passed through decades earlier. By the 1830s, it was becoming something more significant: a crossroads of westward expansion, a stop on the National Road — America's first federally funded highway stretching from Maryland to Illinois — and a hub for commerce moving along the Wabash from the Ohio River into the interior of the young nation. Steamboats plied the river carrying goods and settlers. The town was raw, ambitious, and growing fast.

When Indiana's legislature chartered the Second State Bank of Indiana in 1834, it established branches across the state to serve the financial needs of a rapidly growing population. The Terre Haute branch was one of them. This was frontier banking at its most elemental: taking deposits from farmers and merchants, making loans to fuel settlement and trade, and providing a measure of financial stability in a world where wildcat banks printed worthless currency and collapsed overnight.

The bank survived the Panic of 1837, which wiped out roughly a third of American banks. Think about what that means: within three years of opening, the institution faced a systemic collapse that destroyed many of its peers, and it came through intact. It navigated the tumult of the Civil War, when Indiana sent more than two hundred thousand men to fight for the Union and Terre Haute became a logistics hub for the western campaigns. It endured the National Banking Act of 1863, which fundamentally restructured American finance by creating a system of nationally chartered banks and a uniform national currency, and eventually became known as Terre Haute First National Bank.

The late nineteenth and early twentieth centuries brought further tests. The Panic of 1893, the banking crisis of 1907, and World War I each challenged the institution's resilience. Terre Haute itself was evolving, becoming an industrial center with coal mining, manufacturing, and railroad operations fueling the local economy. The bank's fortunes were intertwined with the community's, a dynamic that would define the institution for its entire existence.

Through each of these transformations, the institution maintained something that would prove far more valuable than any single business strategy: institutional memory. The culture of conservative lending, of knowing your borrowers by name, of prioritizing deposit stability over loan growth, was passed down through generations of bankers. In an industry where aggressive risk-taking periodically generates spectacular returns followed by spectacular failures, Terre Haute First National simply refused to play that game.

The Great Depression was perhaps the ultimate test. Between 1929 and 1933, roughly nine thousand American banks failed, wiping out the savings of millions of families and accelerating the worst economic contraction in the nation's history. Indiana was hit hard. The state's agricultural economy had been struggling since the early 1920s, and the Depression pushed many rural banks past their breaking point. Terre Haute First National survived, not by genius or innovation, but by the boring discipline of maintaining adequate capital reserves and refusing to make loans it could not underwrite with confidence. When the federal government created the FDIC in 1933 to restore public confidence in the banking system, the bank was already standing on solid ground.

This is the core insight of First Financial's early history: survival in banking is not about brilliance. It is about discipline, patience, and the compounding effect of trust built over decades. A bank that has served a community for a hundred years has relationships that no marketing budget can replicate and no fintech startup can disrupt overnight. That institutional capital, invisible on any balance sheet, would prove decisive in the chapters to come.

III. The Holding Company Revolution: The 1980s

The American banking landscape of the early 1980s was undergoing a tectonic shift. For decades, state-level regulations had kept banks confined to narrow geographic territories. In many states, branching restrictions meant a bank could operate in only a single county, sometimes even a single building. This created an industry of thousands of tiny institutions, each dominant in its own postage stamp of territory but unable to grow beyond it.

Then the walls started coming down. State after state began relaxing branching and interstate banking restrictions. The logic was straightforward: larger banks could achieve economies of scale, diversify their risk, and compete more effectively. The unspoken reality was more complex: deregulation would also unleash a wave of consolidation that would eventually reduce the number of American banks from roughly fifteen thousand to fewer than five thousand.

In Indiana, the leadership of Terre Haute First National Bank saw what was coming. In 1983, they established First Financial Corporation as a holding company structure. This was more than a corporate reorganization. It was a declaration of strategic intent. A holding company could own multiple bank subsidiaries, raise capital more efficiently, and acquire other institutions in ways that a standalone bank could not.

The watershed moment came in August 1984, when First Financial Corporation became the first multi-bank holding company in the state of Indiana. That distinction mattered enormously, and it reveals something about the leadership's strategic foresight. Being first meant having a head start in identifying acquisition targets, building the organizational muscle to integrate new institutions, and establishing a reputation as the buyer of choice for community banks whose founders were aging out and looking for a responsible successor.

Consider the psychology of a community bank founder facing retirement. You have spent thirty or forty years building relationships, serving your town, and growing your institution. Your name is on the community center you helped fund. Your employees have worked for you for decades. Your customers trust you with their life savings.

Now you need to sell. The buyer who shows up with a proven track record of preserving community banking values, retaining local employees, and respecting the legacy you built is vastly more attractive than the buyer who shows up with a spreadsheet full of cost cuts and a plan to consolidate branches. First Financial positioned itself as that preferred buyer early, and the reputational advantage compounded with each successful acquisition.

The early acquisitions were modest in scale but ambitious in vision. First Financial began purchasing banks in the counties surrounding Terre Haute, gradually building a regional network across west-central Indiana and east-central Illinois. Each acquisition followed a similar pattern: identify a well-run community bank, negotiate a fair price, bring it under the holding company umbrella, and maintain local management and relationships while centralizing back-office functions for efficiency.

This model, which would later become the defining playbook of First Financial's growth strategy, was being forged in these early years. The leadership learned what worked and what didn't. They learned that the human element of integration mattered more than the financial engineering. They learned that customers cared about whether their local banker still knew their name, not about what holding company owned the charter.

In 2003, First Financial took the logical next step: unifying its various affiliate banks under a single brand, First Financial Bank. For years, the holding company had operated its subsidiaries under their legacy names, reasoning that the local brand carried more goodwill than a corporate parent name. But by the early 2000s, the calculus had shifted. A unified brand enabled more efficient marketing, stronger cross-selling across the network, and a professional identity that signaled scale and stability to commercial customers who might otherwise view each subsidiary as just another small-town bank. The consolidation was both a cost-saving measure and a statement of maturity. The holding company was no longer a loose confederation of small-town banks. It was a regional institution with a coherent identity and a platform built for further expansion.

The stage was set. First Financial had spent two decades building the infrastructure, the culture, and the capabilities for growth through acquisition. What it needed now was opportunity. And opportunity, as it turned out, was about to arrive in catastrophic fashion.

IV. Surviving the Great Recession: 2007 to 2010

The financial crisis of 2008 was a sorting mechanism. It separated the disciplined from the reckless, the well-capitalized from the leveraged, and the conservative from the aggressive. For First Financial, it was the most important test the institution had faced since the Great Depression, and the results would define its trajectory for the next two decades.

To understand what happened to First Financial during the financial crisis, you first have to understand what happened to everyone else.

Between 2008 and 2013, nearly five hundred American banks failed. Not stumbled. Not struggled. Failed, as in seized by the FDIC, their deposits transferred to surviving institutions, their shareholders wiped out, and their names erased from the landscape of American commerce.

The carnage was concentrated among institutions that had done what the market rewarded in the years leading up to the crisis: they had grown aggressively, loosened underwriting standards, loaded up on construction and commercial real estate loans, and funded that growth with hot money, meaning brokered deposits and wholesale funding that could vanish overnight.

First Financial did none of those things.

To understand why, you need to understand what "hot money" means in banking. Imagine you run a restaurant. You can fill your dining room every night by offering fifty-percent-off specials, but the customers who come for the discount will leave the moment someone else offers a better deal. In banking, brokered deposits are the equivalent of those discount-chasing diners. They are large deposits, often placed through intermediaries, that flow to whichever institution offers the highest rate. They are cheap to acquire in good times and catastrophically expensive to lose in bad times, because when confidence falters, they vanish overnight, leaving the bank without the funding it needs to support its loans. First Financial funded itself the old-fashioned way: with deposits from local customers who kept their money at the bank because they had a relationship with their banker, not because they were chasing an extra quarter point of yield.

The bank's conservative lending culture, forged over 170 years of Midwest banking, proved to be exactly the right strategy for a world that suddenly realized it had been pricing risk incorrectly for the better part of a decade.

While banks in Florida, Nevada, and California were discovering that their residential construction portfolios were worth pennies on the dollar, First Financial's loan book was anchored in the kind of unglamorous credits that rarely make headlines: small business loans to manufacturers and retailers in the Wabash Valley, agricultural loans to farmers whose land had been in their families for generations, and residential mortgages underwritten with old-fashioned debt-to-income ratios and genuine down payments.

The Midwest advantage was real but underappreciated. Indiana and Illinois never experienced the kind of speculative real estate frenzy that inflated home prices in the Sun Belt and coastal markets. In Las Vegas, home prices roughly tripled between 2000 and 2006 before collapsing. In Miami, the same. In Terre Haute, home prices barely moved. You cannot have a housing bubble in a market where housing was never overvalued to begin with.

First Financial's portfolio reflected the steady, unspectacular economics of its home territory, and in 2008, steady and unspectacular turned out to be priceless.

The numbers told the story. While the industry's nonperforming loan ratios spiked to levels not seen since the Great Depression, First Financial's credit metrics remained manageable. Its tangible book value, which represents the hard equity backing each share of stock after stripping out intangible assets like goodwill, continued to climb while competitors saw theirs collapse.

Its capital ratios stayed well above regulatory minimums without requiring the kind of emergency capital raises that diluted shareholders at other banks or, worse, triggered FDIC intervention.

There is a deeper lesson here about the relationship between culture and strategy. First Financial operated with low leverage, modest growth targets, and an emphasis on local relationships over loan production quotas. These were not sophisticated risk management techniques. They were not the product of complex value-at-risk models or Monte Carlo simulations.

They were habits, embedded in the institution's DNA by generations of bankers who had seen what happened when you chased growth at the expense of prudence. The crisis validated what they had always believed: the tortoise beats the hare, especially when the racetrack is lined with landmines.

But the crisis did more than validate First Financial's defensive posture. It created the conditions for its transformation. As hundreds of banks failed or were absorbed by desperate competitors, a new reality emerged: well-capitalized survivors had their pick of expansion opportunities. Distressed banks, abandoned branches, and demoralized customer bases were available at prices that would have been unthinkable just a few years earlier.

First Financial had the capital, the culture, and the patience to take advantage. While many of its peers were scrambling to shore up their own balance sheets, accepting TARP money from the federal government, or negotiating emergency mergers to avoid failure, First Financial was quietly building its war chest. The crisis had not just preserved its capital. It had concentrated opportunity in the hands of the few institutions disciplined enough to have maintained it.

The question was whether it had the ambition.

V. The First Big Leap: Freestar Bank and Geographic Expansion

The answer to whether First Financial had the ambition came quickly.

The post-crisis mergers and acquisitions environment was unlike anything the banking industry had seen in decades. Regulators were encouraging consolidation, reasoning that fewer, stronger banks were preferable to a system cluttered with undercapitalized institutions clinging to life. Potential sellers were everywhere. Capital, however, was scarce, which meant that the few banks with strong balance sheets could be highly selective.

In October 2011, First Financial Corporation announced the acquisition of PNB Holding Company, parent of Freestar Bank, based in Pontiac, Illinois. Freestar operated thirteen offices across central Illinois, a meaningful geographic footprint that would extend First Financial's reach well beyond the Terre Haute border region where it had historically maintained a modest Illinois presence.

The strategic logic was clear. Central Illinois offered demographically stable markets with commercial and agricultural lending opportunities that matched First Financial's core competencies. The Freestar franchise came with established customer relationships, experienced local bankers, and a branch network that would have taken years and millions of dollars to build organically. And the price was right: post-crisis valuations for community banks remained well below pre-2008 levels, giving acquirers favorable economics.

But the Freestar deal was important for another reason beyond its immediate financial contribution. It served as a proving ground for First Financial's acquisition integration model. Every merger is a test of organizational capability. Can the acquirer retain the target's best employees? Can it maintain customer relationships through the inevitable disruption of system conversions and brand changes? Can it achieve the promised cost savings without gutting the franchise it just paid to acquire?

First Financial's approach was to preserve the community banking ethos within a larger platform. Local market presidents retained meaningful decision-making authority. Customers continued to interact with the same bankers they had trusted before the acquisition. Back-office functions were centralized for efficiency, but the front office remained local. This model, which might be described as community banking at scale, would become the template for every subsequent acquisition.

The Freestar deal also revealed something important about First Financial's appetite. This was not a one-time opportunistic purchase. It was the first deliberate step in a geographic expansion strategy that would, over the next decade and a half, transform the company from a two-state operator into a five-state regional platform. The leadership in Terre Haute had looked at the competitive landscape and made a calculated bet: in an industry where consolidation was inexorable, you either grew or you became someone else's acquisition target.

They chose to grow. And the Freestar integration, executed without major customer defections or employee departures, validated that choice. It was the equivalent of a startup's proof-of-concept moment: the strategy worked, and now it was time to scale it.

VI. The Bank of America Deal: Branch Acquisitions

While First Financial was learning to integrate whole-bank acquisitions, an entirely different opportunity was emerging in the post-crisis landscape. The mega-banks were retreating.

In the wake of the financial crisis and the sweeping regulatory reforms of Dodd-Frank, the largest American banks began a strategic reassessment of their branch networks. Dodd-Frank, passed in 2010, imposed a vast new regulatory apparatus on the banking industry, with compliance costs that fell disproportionately on the largest institutions. Every branch represented not just real estate and staffing costs but regulatory compliance obligations, Community Reinvestment Act commitments, and management attention. Institutions like Bank of America, JPMorgan Chase, and Citigroup had sprawling networks of branches in small towns and mid-sized cities that generated modest revenue but required ongoing investment in all of these dimensions. For a bank managing trillions of dollars in assets, a handful of branches in downstate Illinois was a rounding error on the expense line. For First Financial, those same branches were a strategic asset.

In March 2013, First Financial acquired nine branch offices in central and southern Illinois from Bank of America. The deal was a masterclass in strategic opportunism. Instead of buying an entire institution with all the complexity that entails, including legacy loans, unknown liabilities, and cultural integration challenges, First Financial was cherry-picking established customer franchises from a seller who was happy to walk away.

The brilliance of branch acquisitions lies in what you get and what you avoid. You get physical locations with established foot traffic, deposit customers with years of banking history, and often commercial relationships that the mega-bank never fully served. You avoid problem loans, because the selling bank typically retains those. You avoid cultural clashes, because you are not absorbing an entire organization with its own management hierarchy and corporate identity. And you avoid paying a premium for a bank charter, because you are simply adding branches to your existing charter.

The deposit franchise value was particularly compelling. In the low-rate environment that prevailed after the crisis, stable, low-cost deposits were the lifeblood of bank profitability. The customers who walked into those former Bank of America branches every week were exactly the kind of depositors that First Financial wanted: loyal, local, and unlikely to chase marginally higher rates at an online bank. These were farmers, small business owners, and retirees who valued face-to-face relationships and the comfort of a familiar branch location.

There was also a subtle competitive dynamic at work. When Bank of America exited these markets, the customers it left behind were temporarily orphaned, suddenly assigned to a distant branch or encouraged to use digital channels they might not have been comfortable with. First Financial stepped in as the local alternative, the bank that would actually show up in the community. It was a powerful sales pitch that required minimal marketing because the pitch was simply being present.

The nine-branch acquisition reinforced a principle that would guide First Financial's growth strategy going forward: sometimes the best acquisitions are not the biggest or most transformational. Sometimes they are the simplest, the deals with the lowest execution risk and the highest probability of immediate value creation. Building a regional banking franchise does not require a single blockbuster merger. It can be assembled brick by brick, branch by branch, customer by customer.

By the mid-2010s, First Financial had built a solid foundation across Indiana and Illinois. Its capital ratios were strong. Its credit quality was excellent. Its integration capabilities had been tested and proven through two distinct types of transactions: a whole-bank acquisition with Freestar and a branch purchase from Bank of America. This diversity of M&A experience was important. It meant the company's leadership had developed judgment about which type of deal was appropriate for which situation, a strategic flexibility that would serve them well as they contemplated larger moves.

The broader industry context was also shifting. The post-crisis regulatory environment had stabilized. Interest rates remained at historically low levels, compressing margins for deposit-dependent community banks and creating urgency around finding new sources of earnings growth. Across America, thousands of community banks were confronting the same existential question: grow or be acquired. First Financial had made its choice. The company was ready for something bigger.

VII. The Kentucky Gamble: HopFed and Heritage Bank

Every company has moments that divide its history into "before" and "after." Moments where the leadership makes a decision that fundamentally changes the company's trajectory, its risk profile, and its identity. For First Financial Corporation, the HopFed Bancorp merger was that dividing line.

To appreciate the magnitude of this decision, consider what First Financial looked like heading into 2019. It was a well-run, conservatively managed community banking organization headquartered in Terre Haute, with approximately three billion dollars in assets. Its footprint covered west-central Indiana and east-central Illinois, a territory it had served for decades and knew intimately. Its markets were stable, its relationships were deep, and its performance was consistent if unspectacular.

Now consider the target: HopFed Bancorp, headquartered in Hopkinsville, Kentucky, operating as Heritage Bank with roughly nine hundred million dollars in consolidated assets. Heritage ran eighteen bank branches and three loan production offices scattered across Kentucky and Tennessee. Hopkinsville sits about 150 miles south of Terre Haute, in the agricultural heartland of western Kentucky, near Fort Campbell and the Tennessee border.

This was not a tuck-in acquisition of a neighboring county bank. This was a leap into entirely new geography, new markets, and new competitive dynamics. For a bank that had spent its entire 185-year history operating within a radius of roughly a hundred miles from Terre Haute, it was a bold move. The distance matters because banking, particularly community banking, is intensely local. You need to understand the economic drivers of each market, the competitive dynamics, the regulatory environment across state lines, and the cultural expectations of customers who may have very different banking habits than those in your home territory. A farmer in western Kentucky and a manufacturer in the Wabash Valley both need loans, but the rhythms of their businesses, the risks they face, and the services they require can differ in ways that a centralized credit model might miss.

The deal structure reflected First Financial's characteristic discipline. Each HopFed stockholder could elect to receive either 0.444 shares of First Financial common stock or twenty-one dollars in cash per share, or some combination of the two. The total implied valuation came to approximately $128.3 million.

The mix of stock and cash consideration is worth noting because it reveals something about how First Financial thinks about its own currency. By offering stock as part of the deal, the company was implicitly saying: we believe our shares are fairly valued, and we are confident enough in our future to give you a stake in it. At the same time, the cash component provided certainty for HopFed shareholders who preferred liquidity.

The merger closed on July 29, 2019, and the resulting institution operated eighty-three banking centers and five loan production offices across four states: Indiana, Illinois, Kentucky, and Tennessee.

The strategic logic rested on several pillars.

First, Heritage provided entry into markets with different economic drivers than the mature Midwest territories First Financial already served. Western Kentucky and middle Tennessee offered exposure to military spending through Fort Campbell, one of the largest Army installations in the country, as well as agricultural diversity and growing population centers. The economic correlation between these markets and First Financial's Indiana heartland was low enough to provide genuine diversification benefits.

Second, the deal provided enough scale in the new geography to justify the investment in regional management, compliance infrastructure, and marketing required to operate effectively across state lines. This is a crucial distinction in banking M&A. A single branch in Kentucky would have been a curiosity, expensive to manage and too small to generate meaningful returns. Eighteen branches and three loan offices constituted a real franchise with the critical mass to support dedicated regional leadership and contribute meaningfully to the holding company's earnings.

But the big question hung in the air: could a Terre Haute bank successfully operate more than a hundred miles away, across state lines, in communities where the First Financial name meant nothing? The history of banking is littered with acquisitions that looked brilliant on a spreadsheet but failed because the acquirer could not replicate its culture in unfamiliar territory. Customers in Hopkinsville did not care about a bank's 185-year heritage in Indiana. They cared about whether their banker would still pick up the phone, whether their loan would still get a fair hearing, and whether the new owner would invest in their community or strip it for parts.

First Financial's integration approach, refined through the Freestar and Bank of America deals, was deployed at a larger scale. Local market leaders were retained. Decision-making authority remained close to the customer. The Heritage brand was eventually folded into First Financial Bank, but the people and the philosophy stayed in place. The early indications were encouraging. Customer retention held. Credit quality remained sound. The Kentucky and Tennessee operations began contributing to earnings without the kind of integration disruptions that often accompany cross-state mergers.

The HopFed deal was more than a geographic expansion. It was a proof of concept. It demonstrated that First Financial's community banking model was portable, that the values and practices honed over nearly two centuries in the Wabash Valley could be transplanted to new soil and take root.

For investors, the HopFed deal represented a step-function change in First Financial's growth profile. The company went from a reliable but slow-growing Indiana bank to a multi-state operator with exposure to different economic cycles and growth dynamics. The additional scale brought tangible benefits: greater efficiency in technology spending, improved negotiating leverage with vendors, and a deeper management bench. It also brought intangible benefits, chief among them the confidence that larger deals were possible and manageable. That confidence would become critical as the company turned its attention to an even more ambitious set of opportunities to the south.

VIII. The Tennessee Expansion: SimplyBank Acquisition

If the HopFed deal proved that First Financial could operate across state lines, the SimplyBank acquisition proved something even more important: that the company could use acquisitions as a deliberate tool for strategic repositioning, shifting its center of gravity from the slow-growth Midwest toward the faster-growing markets of the American Southeast.

The backdrop was significant. The banking industry emerged from the COVID-19 pandemic into a radically different operating environment. Digital adoption had accelerated by years in a matter of months. The Federal Reserve's aggressive rate hikes through 2022 and 2023 had transformed the interest rate landscape, creating both opportunities and challenges for deposit-dependent community banks. And the regional banking stress of early 2023, triggered by the failures of Silicon Valley Bank and Signature Bank, had sent tremors through the entire sector, reminding everyone that banking confidence is fragile and contagion is real.

Against this backdrop, in November 2023, First Financial announced the acquisition of SimplyBank, headquartered in Dayton, Tennessee, for $73.4 million. SimplyBank operated thirteen bank branches and one loan production office in Tennessee and Georgia, with total assets of approximately $702 million. The deal was expected to close in the second quarter of 2024 and ultimately completed on July 1, 2024.

The strategic significance was multidimensional.

SimplyBank's footprint in central and eastern Tennessee filled gaps in First Financial's emerging Southeastern network, connecting the western Kentucky and Tennessee markets acquired through HopFed with new territories stretching toward Chattanooga and into northern Georgia. Look at a map, and the logic becomes immediately apparent. The HopFed acquisition gave First Financial a presence in the western part of Tennessee and Kentucky. SimplyBank extended that presence eastward across the state, creating a corridor that approached the Chattanooga metropolitan area and crossed into Georgia. This was not random geographic expansion. It was deliberate network building, creating density in contiguous markets so that the cost of regional management, marketing, and compliance could be spread across a meaningful base of customers and assets.

The financial impact was immediate and substantial. SimplyBank added $467 million in loans and $622 million in deposits to First Financial's balance sheet. To appreciate what those numbers mean in context: the deposit addition alone was nearly equal to the entire asset base of CedarStone, the company's next acquisition. These were not hypothetical synergies on a management presentation. They were real customers, real accounts, and real funding that immediately began contributing to First Financial's earnings capacity.

The fourth quarter of 2024 produced record net interest income of $49.6 million, with the net interest margin expanding to 3.94 percent and total loans increasing to $3.84 billion, representing year-over-year growth of more than twenty-one percent. The SimplyBank acquisition was the primary driver of that growth.

But acquisitions always come with costs that extend beyond the purchase price. Integration expenses, system conversions, and the inevitable friction of combining two organizations with different cultures, processes, and technology platforms weighed on short-term profitability. First Financial was transparent about these challenges, acknowledging in its earnings communications that integration costs were impacting results even as the underlying franchise was strengthening.

The SimplyBank deal also marked First Financial's entry into Georgia, adding a fifth state to its operating footprint. While the Georgia presence was modest, consisting of a small number of branches in the northern part of the state, it established a toehold in one of the fastest-growing regions of the American South. For a bank that had spent most of its history in the slow-growth Midwest, having exposure to the demographic and economic dynamism of the Southeastern United States was a meaningful strategic upgrade.

More fundamentally, the SimplyBank acquisition revealed the maturation of First Financial's M&A strategy. The company was no longer simply buying banks that happened to become available. It was executing a deliberate plan to build a multi-state platform in the Southeast, using each acquisition as a stepping stone to the next. The pattern was becoming unmistakable: buy a community bank in a contiguous market, integrate it successfully, use the expanded platform to justify the next acquisition, and repeat. It was the compounding effect applied to corporate strategy.

There is a useful analogy here to franchise businesses. Think of how a fast-food chain expands: not by randomly opening locations across the country, but by clustering stores in regions, building brand awareness and supply chain density before moving to the next territory. First Financial was applying the same logic to banking. Each acquisition in Tennessee made the next one more efficient, because the regional management infrastructure, compliance systems, and marketing presence were already in place. The marginal cost of adding the next branch or the next bank in the same corridor was lower than the cost of the first one.

IX. The Nashville Bet: CedarStone Financial

Every good strategy eventually faces its ultimate test: can it work in a truly competitive, high-growth market where the easy pickings are long gone and every inch of territory is contested? For First Financial, that test was Nashville.

In November 2025, the company announced the acquisition of CedarStone Financial, Inc., for an aggregate value of $25.0 million. CedarStone, headquartered in Lebanon, Tennessee, held approximately $358 million in assets and operated three bank branches serving the communities of Lebanon, Mount Juliet, and Nashville.

The deal was small by the raw numbers, representing less than seven percent of First Financial's existing asset base. But its strategic significance was outsized.

Lebanon and Mount Juliet are suburbs in the Nashville metropolitan area, and understanding Nashville's trajectory is essential to understanding why this deal mattered. Over the past fifteen years, Nashville has undergone a transformation that few cities outside of Austin and Boise can match. Oracle moved its headquarters there. Amazon built a major operations hub. AllianceBernstein relocated its corporate headquarters from New York. The healthcare industry, anchored by HCA Healthcare, has made Nashville a national center for hospital management and health services. The city's population grew by roughly twenty percent in the decade ending in 2020, and the growth has continued since. Young professionals have flooded in, attracted by the combination of a vibrant cultural scene, no state income tax, and a cost of living that, while rising, remains well below coastal alternatives.

For a community bank looking for growth markets, Nashville checks every box. The population is growing. Businesses are relocating. Commercial lending demand is robust. Deposit gathering is facilitated by rising household incomes and an expanding base of small and mid-sized businesses that need local banking relationships. Its population growth, job creation, and real estate appreciation have consistently outpaced national averages.

For First Financial, planting a flag in the Nashville market was the logical culmination of the Southeastern expansion strategy that began with HopFed in 2019. Each acquisition had moved the company's center of gravity further south and east, from western Kentucky to central Tennessee to the Nashville suburbs. The CedarStone deal connected the dots, creating a presence in the most economically dynamic market in the company's five-state footprint.

Upon completion, First Financial's total consolidated assets were expected to rise from approximately $5.7 billion to $6.1 billion. More importantly, the deal positioned the company in a market where organic growth opportunities, commercial lending demand, and deposit gathering potential were substantially greater than in its legacy Midwest territories.

The pattern that had been emerging over a decade was now fully visible. First Financial had executed a serial acquisition strategy in contiguous markets, building density rather than dispersion. Unlike some regional banks that expand by buying franchises in far-flung markets with no geographic connection to each other, First Financial built a coherent corridor from Indiana through Illinois, Kentucky, and Tennessee into Georgia. Each new market connected to the last. Each acquisition made the next one more logical and more efficient to manage.

Norman L. Lowery, who serves as Chairman, President, and CEO, described CedarStone as "an opportunity to further expand our franchise in the attractive Nashville market." The language was characteristically understated. What it really meant was that a bank founded in a frontier town on the Wabash River in 1834 was now competing for customers in one of the hottest real estate and business markets in America.

Whether First Financial can win in Nashville the way it has won in Terre Haute remains to be seen. The competitive dynamics are vastly different. Nashville is served by national banks with unlimited marketing budgets, aggressive regional competitors like Pinnacle Financial Partners that have built dominant franchises through similar relationship-banking strategies, well-funded fintechs targeting the city's young professional population, and a sophisticated commercial lending market that demands capabilities beyond traditional community banking.

But First Financial has one advantage that its competitors cannot easily replicate: a 190-year track record of showing up, staying, and serving communities through every conceivable economic environment. In a city full of newcomers, both corporate and individual, there is something to be said for an institution that has been around longer than most of the country. The Nashville bet will likely be judged not by the CedarStone acquisition alone but by what First Financial does in the years that follow. If the company can build on its three-branch beachhead through additional tuck-in acquisitions and organic customer growth, the Nashville strategy could eventually become the most significant chapter in the company's modern history.

X. The Modern Business Model and Operations

Strip away the history and the narrative, and First Financial Corporation is, at its core, a diversified community banking platform generating revenue from a mix of traditional banking products and fee-based services. Understanding the current business model is essential for anyone evaluating the company as an investment or studying it as a case study in regional banking strategy.

The revenue engine runs on two cylinders. The first and by far the larger is net interest income, which is the spread between what the bank earns on loans and investments and what it pays for deposits and borrowings. Think of it as the bank's markup: it borrows money cheaply from depositors and lends it out at a higher rate, and the difference is its profit. The second cylinder is non-interest income, which includes fees from trust and wealth management, insurance, investment services, and deposit account charges.

Like most community banks, net interest income is the dominant contributor, and the company's recent performance demonstrates why the acquisition strategy has been so effective at driving this metric.

In the second quarter of 2025, First Financial reported net income of $18.6 million, or $1.57 per diluted share. More notably, net interest income reached a record $52.7 million, up thirty-four percent year-over-year, with the net interest margin expanding to 4.15 percent.

For context, a net interest margin above four percent is considered strong for community banks. The industry average for banks of First Financial's size typically ranges from three to three and a half percent, so exceeding four percent represents meaningful outperformance. This expansion reflects both the benefit of a higher-rate environment, which allows banks to earn more on their loan portfolios, and the accretive impact of recent acquisitions that brought in loan portfolios yielding above the company's existing average.

The efficiency ratio, which measures how many cents a bank spends to generate each dollar of revenue, improved to 59.37 percent from 64.56 percent a year earlier. In banking, lower is better, and a ratio below sixty percent indicates that a bank is generating meaningful operating leverage. Think of it this way: at an efficiency ratio of sixty percent, for every dollar of revenue the bank generates, it keeps forty cents as pre-provision profit.

This improvement reflects the cost synergies from integrating SimplyBank and the benefit of spreading fixed costs across a larger asset base. It is also evidence that the M&A strategy is achieving one of its primary financial objectives: using acquisitions to build a platform where the incremental revenue from each new branch or market exceeds the incremental cost of serving it.

Asset quality, always the most critical metric for a bank, remained robust. Nonperforming loans decreased to $13.3 million from $24.6 million year-over-year, a nearly fifty percent improvement. To put that in context, nonperforming loans now represent a tiny fraction of the total loan portfolio, suggesting that the underwriting discipline that saved the bank during the financial crisis continues to be applied rigorously across the expanded geographic footprint.

The allowance for credit losses stood at $46.7 million, representing 1.22 percent of total loans. This is the reserve the bank sets aside to cover expected future losses, and the level suggests conservative provisioning: enough to absorb a meaningful deterioration in credit quality without catastrophic impact, but not so excessive that it drags unnecessarily on current earnings.

The bank maintained strong capital ratios with a Tier 1 leverage ratio of 10.91 percent, well above the regulatory well-capitalized threshold and providing ample capacity for future growth. In banking, capital is the ultimate safety margin. It is the buffer between a bank and insolvency, the resource that allows an institution to absorb unexpected losses and continue operating. A Tier 1 leverage ratio above ten percent gives First Financial substantial room to make additional acquisitions, absorb credit losses, and weather economic downturns without imperiling its financial stability.

The deposit base reflects the community banking model. Non-interest-bearing demand deposits, essentially free funding for the bank because it pays no interest on them, are supplemented by interest-bearing checking accounts, savings accounts, and time deposits such as certificates of deposit. The mix matters enormously because the cost of deposits is the single largest variable in a bank's profitability equation. A bank with a high proportion of non-interest-bearing deposits has a built-in cost advantage over one that must pay market rates to attract funding.

The loan portfolio is diversified across commercial and industrial lending, commercial real estate, residential mortgages, construction, and home equity products. Supplemental revenue streams include lease financing, trust account management, and insurance services, providing fee income diversification that pure lending operations cannot deliver.

The company pays a dividend yielding roughly 3.18 percent at recent prices, a meaningful shareholder return that reflects the cash-generative nature of community banking and management's confidence in the sustainability of earnings. For income-oriented investors, the dividend provides a floor on total return even in periods of modest stock price appreciation. The company has maintained its dividend through multiple economic cycles, including the 2008 crisis and the COVID-19 pandemic, a track record of reliability that income investors prize.

The geographic diversification of the business model is worth dwelling on because it represents such a dramatic departure from the company's historical profile. A decade ago, First Financial's fortunes were almost entirely tied to the economic health of the Wabash Valley and surrounding communities in Indiana and Illinois. Today, the company operates across five states, with meaningful exposure to the faster-growing economies of Tennessee and Georgia. This diversification reduces the risk that a localized economic downturn in any single market can materially impair the company's earnings. It is a form of insurance that was purchased through acquisitions rather than derivatives.

The technology question looms large for any community bank, and it is worth unpacking because it illustrates the fundamental tension at the heart of the community banking model. Consider what a customer expects in 2026: instant mobile deposits, real-time payment notifications, seamless person-to-person transfers, integrated budgeting tools, and the ability to apply for a loan from a smartphone at midnight. Delivering these capabilities requires investment in core banking platforms, mobile application development, cybersecurity infrastructure, and data analytics. JPMorgan Chase spends roughly fifteen billion dollars annually on technology. First Financial's entire annual revenue is a fraction of that figure.

The gap is not as fatal as it might appear, however, because First Financial does not need to build this technology from scratch. A robust ecosystem of banking technology vendors, often called core processors, provides turnkey solutions that community banks can license for a fraction of the cost of in-house development. Companies like Fiserv, Jack Henry, and FIS provide mobile banking platforms, digital lending tools, and cybersecurity monitoring that allow institutions like First Financial to offer digital experiences comparable to those of much larger competitors. The trade-off is standardization: using a vendor platform means less customization and less differentiation, but it also means dramatically lower cost and faster deployment.

The deeper challenge is not technological parity in digital channels but the broader question of customer acquisition. Mega-banks and fintechs can acquire customers nationally through digital marketing at a cost per acquisition that community banks cannot match. First Financial's customer acquisition model remains fundamentally local and relationship-driven: branch presence, community involvement, and word-of-mouth referrals. This model works well in established markets but is slower and more expensive in new territories like Nashville where the bank lacks the brand recognition that drives organic customer growth.

XI. The Playbook: What First Financial Got Right

Step back from the individual deals and look at the pattern. Studying First Financial's evolution over the past four decades reveals a remarkably consistent set of strategic principles. These are not revolutionary concepts. They will not win anyone a Nobel Prize in economics. They are the boring fundamentals of banking, executed with unusual discipline and patience over an unusually long time horizon. But boring, executed well and compounded over decades, produces extraordinary results.

The first principle is conservative underwriting through cycles. In every economic era, there is pressure to loosen lending standards. During booms, competitors gain market share by making loans that a disciplined underwriter would reject. Bank executives face boards asking why growth is lagging peers. Loan officers face quotas that incentivize volume over quality. The temptation to follow the market is enormous, because the short-term penalty for conservatism is lost revenue, slower growth, and uncomfortable conversations with shareholders.

First Financial has consistently resisted this temptation, maintaining credit discipline even when it meant ceding business to more aggressive competitors. The payoff comes during downturns, when the conservative lender's portfolio holds up while the aggressive lender's portfolio collapses. It is a simple concept, but extraordinarily difficult to execute in practice because it requires the institutional fortitude to accept underperformance during good times in exchange for outperformance during bad times.

The second principle is patient capital deployment. First Financial does not do deals for the sake of doing deals. It waits for opportunities that meet its criteria for price, strategic fit, and integration feasibility. This patience is rare in an industry where executives are often measured on quarterly earnings growth and incentivized to demonstrate activity. The pressure to "do something" with excess capital is intense, particularly when competitors are announcing deals and analysts are asking on quarterly calls about the acquisition pipeline. There have been long periods in First Financial's history when no meaningful acquisitions occurred, not because the company lacked ambition but because the available deals did not meet its standards. The discipline to say "no" to a dozen mediocre deals in order to say "yes" to one great one is a competitive advantage that does not appear on any balance sheet.

The third principle is geographic clustering. Every major acquisition has been in a market contiguous to an existing one. First Financial builds density, not dispersion. This means that each new market can be managed by existing regional infrastructure, that marketing and brand-building can spill across borders, and that the company avoids the logistical nightmare of operating disconnected outposts in far-flung territories. The Indiana-to-Illinois-to-Kentucky-to-Tennessee-to-Georgia corridor is a textbook example of contiguous expansion.

The fourth principle is community banking at scale. First Financial preserves local market presidents and decision-making authority in acquired institutions. This is not sentimentality. It is strategic.

The value of a community bank franchise resides in its relationships, and relationships are maintained by people, not by corporate policies. When a business owner walks into a branch to discuss a loan, they want to talk to someone who understands their industry, their community, and their specific circumstances. That person is almost always a local banker, not a credit analyst in a distant headquarters.

When a bank acquires a community institution and immediately replaces local leadership with centrally deployed managers, it risks destroying the very asset it paid to acquire. First Financial understands this and has built an organizational structure that balances local autonomy with centralized efficiency. Local presidents make lending decisions. Corporate headquarters handles compliance, technology, and capital allocation. It is a federalist model applied to banking.

The fifth principle is management continuity. Norman L. Lowery's tenure as Chairman, President, and CEO has provided stable, consistent leadership through multiple strategic transitions. In an industry where executive turnover can derail multi-year strategies, this continuity has been a genuine competitive advantage. The M&A strategy in particular benefits from long-tenured leadership because acquisition capabilities are institutional muscles that take years to develop and are easily lost through leadership transitions.

The sixth principle is integration excellence. First Financial has completed multiple acquisitions without the kind of major stumbles that plague many serial acquirers. System conversions have been executed cleanly. Customer retention has been strong. Cost synergies have been achieved. This track record is itself a competitive advantage because it makes First Financial a more attractive buyer to potential sellers. Community bank founders and boards considering a sale care deeply about what will happen to their employees and customers after the deal closes. A buyer with a proven track record of respectful, competent integration has a significant edge over one with a history of post-merger chaos.

These six principles interact and reinforce each other. Conservative underwriting preserves capital. Patient deployment ensures that capital is deployed wisely. Geographic clustering makes integration easier. Community banking at scale preserves franchise value. Management continuity ensures that the strategy is executed consistently. And integration excellence makes the next deal possible. It is a flywheel, and it has been spinning with increasing velocity for the past fifteen years.

There is one more principle worth noting, though it is less a deliberate strategy than an emergent property of all the others: First Financial has become increasingly attractive as an acquirer precisely because it has been a successful acquirer. In community banking, reputation matters. When a bank's board is deciding whom to sell to, they talk to other boards who have gone through the process. Word travels fast in tight-knit banking communities. First Financial's track record of fair dealing, employee retention, and community commitment has created a referral network that surfaces acquisition opportunities before they reach the open market. In a competitive M&A environment, that informational advantage is invaluable.

XII. Porter's Five Forces Analysis

Understanding First Financial's competitive position requires examining the structural forces that shape profitability in community and regional banking. Michael Porter's Five Forces framework, which analyzes the competitive dynamics that determine an industry's profit potential, provides a useful lens. For those unfamiliar, Porter argued that industry profitability is determined by five forces: the threat of new entrants, the bargaining power of suppliers and buyers, the threat of substitutes, and the intensity of competitive rivalry. The stronger these forces, the harder it is for companies in the industry to earn attractive returns.

The threat of new entrants into community banking is moderate to high, though not in the traditional sense. De novo bank charters, meaning brand-new bank startups, remain relatively rare due to heavy regulatory requirements, significant capital needs, and the multi-year timeline to profitability. However, fintech companies have fundamentally altered this dynamic. Neobanks like Chime and SoFi offer deposit-like products with higher yields. Online lenders compete aggressively for consumer and small business loans. Payment platforms like Venmo and Cash App handle transactions that once required a bank account. These entrants do not need a bank charter to compete for the most profitable segments of traditional banking. Yet regulatory barriers still protect the full-service banking relationship, particularly for commercial clients who need treasury management, credit lines, and the kind of complex financial services that fintechs have not yet replicated at scale. Branch networks continue to matter for commercial relationships in ways that mobile apps cannot fully substitute.

The bargaining power of suppliers in banking is relatively low. A bank's primary "suppliers" are its depositors, who provide the raw material, funding, that the bank transforms into loans. While deposit holders have more options than ever, switching costs remain meaningful. Moving a primary checking account, with its associated direct deposits, automatic bill payments, and linked services, is a hassle that most consumers and businesses tolerate only when seriously dissatisfied. Commercial depositors are even stickier, because their banking relationships typically involve complex treasury management arrangements that are costly and time-consuming to migrate. FDIC insurance provides a baseline of trust that benefits all banks equally and reduces the incentive for depositors to move based on perceived safety differences.

The bargaining power of buyers, meaning borrowers and fee-paying customers, is moderate to high. Commercial clients are increasingly sophisticated, able to compare lending terms across multiple institutions and leverage competing offers. Retail customers have access to rate-comparison tools and can shop for mortgages, auto loans, and credit cards with unprecedented ease. However, community banking relationships create a stickiness that partially offsets this power. A business owner who has worked with the same banker for twenty years, who values the ability to walk into a branch and discuss a complicated loan request in person, is not easily lured away by a marginally better rate from an online lender. First Financial's value proposition is built on this relationship premium.

The threat of substitutes is high and growing. Fintech lenders compete for consumer and small business loans. Private credit funds, which have exploded in size since the financial crisis, compete for commercial lending. Registered investment advisors and robo-advisors compete for wealth management. Digital wallets and payment platforms compete for transaction volume.

Each of these substitutes attacks a different piece of the traditional banking revenue model. The bank's advantage is that it offers all of these services in an integrated package, reducing the friction of dealing with multiple providers. A business owner can get a checking account, a line of credit, a commercial mortgage, and wealth management advice all from the same institution. But that advantage erodes as fintech integration improves and consumers become more comfortable assembling their financial lives from multiple specialized providers.

Competitive rivalry in banking is intense and multidimensional. First Financial competes against mega-banks with enormous scale advantages in technology and marketing. It competes against regional banks of similar or larger size fighting for the same acquisition targets and commercial relationships. It competes against credit unions that enjoy tax-exempt status, allowing them to offer marginally better rates on both deposits and loans. And it competes against thousands of other community banks occupying similar market positions in overlapping geographies.

The intensity of rivalry is moderated by the geographic nature of banking: a bank's most important competitors are those operating in the same markets, not every bank in the country. In Terre Haute, First Financial's competitive position is dominant, built over nearly two centuries of continuous operation. In Nashville, it is a newcomer competing against entrenched players. The competitive dynamics vary market by market, which is both a challenge and an opportunity. First Financial's multi-state platform provides advantages over single-market community banks because it can offer the breadth of services associated with larger institutions, including sophisticated treasury management, wealth advisory, and commercial real estate lending, while maintaining the relationship depth that a local bank provides. In Porter's framework, this multi-market positioning creates differentiation that is difficult for either mega-banks or single-market community banks to replicate exactly.

XIII. Hamilton's Seven Powers Analysis

Hamilton Helmer's Seven Powers framework offers a complementary perspective on First Financial's competitive durability. While Porter's framework examines industry structure, Helmer focuses on company-specific sources of power that enable sustained differential returns, meaning profits that exceed what competitors can earn. In Helmer's view, there are only seven possible sources of such power, and most companies possess few if any of them. The question for First Financial is whether it possesses any of these powers in sufficient strength to sustain above-market returns over time.

Scale economies are weak for First Financial in absolute terms. The company, at roughly six billion dollars in assets, is a fraction of the size of JPMorgan Chase or Bank of America, and cannot match their technology spending, regulatory compliance infrastructure, or cost of capital. However, at the regional level, First Financial achieves meaningful scale advantages over smaller community banks in its markets. Its ability to spread technology costs, compliance expenses, and management overhead across a multi-state platform gives it a cost structure that single-market banks with five hundred million in assets simply cannot match. This regional scale advantage is real, even if it is modest compared to the industry's giants.

Network effects are essentially nonexistent in traditional banking. Unlike a payments platform or social network, a bank does not become more valuable to each customer as more customers join. There is no viral growth mechanism, no demand-side economies of scale. Each customer relationship must be won individually through pricing, service quality, and relationship building. This is one of the fundamental structural weaknesses of banking as a business model: growth is linear, not exponential. Every new customer requires dedicated effort to acquire and serve. There is no virality, no sharing, no organic multiplication of the customer base. This is why banking has historically been a modest-return business for most participants and why First Financial's strategy of growth through acquisition is so logical: if you cannot grow virally, you grow by absorbing existing customer bases.

Counter-positioning is moderate and represents one of First Financial's more interesting competitive dynamics. The community banking model is, in many ways, a counter-position against mega-bank impersonality. Large banks have invested billions in technology platforms and centralized underwriting models that optimize for efficiency and scale. Replicating First Financial's model of local decision-making, relationship-based lending, and community engagement would require large banks to fundamentally restructure their operations in ways that would undermine their scale advantages. They cannot easily become community banks in specific markets without sacrificing the operational consistency that their business models require. However, this counter-positioning advantage is not unique to First Financial. Any well-run community bank can make the same argument, which limits its value as a source of differential returns.

Switching costs are moderate. Commercial banking relationships involve treasury management systems, credit facilities, and institutional knowledge that create real friction when a business considers moving to a competitor. Retail checking accounts, while individually simple to move, benefit from inertia: most consumers avoid the hassle of redirecting direct deposits and automatic payments unless they have a compelling reason. But digital banking has reduced switching costs over time, making this power weaker than it was a generation ago.

Branding power is weak to moderate. First Financial has strong brand recognition in its core Terre Haute market, where it has operated for nearly two centuries. In newer markets like Kentucky, Tennessee, and Georgia, the brand is still being established. In competitive, brand-saturated markets like Nashville, First Financial's name carries no particular cachet. Banking is generally a category where brand matters less than in consumer goods or technology, because the products are largely commoditized and customer decisions are driven more by pricing, convenience, and relationships than by brand affinity.

Cornered resources are weak. First Financial does not possess proprietary technology, exclusive access to deposits, or a talent pool that competitors cannot replicate. Its management quality and institutional culture are genuine advantages, but they are not inimitable in the way that a patent or a network effect would be.

Process power is moderate and arguably represents First Financial's strongest competitive advantage under Helmer's framework. The company has developed a systematic, repeatable capability in identifying, acquiring, and integrating community banks. This capability has been built over decades through organizational learning and is embedded in the company's processes, relationships, and institutional knowledge. It is not easily replicated by competitors who lack the same track record and institutional memory.

Think of it this way: any bank can buy another bank. The hard part is buying a bank, converting its systems, retaining its employees, keeping its customers, extracting cost savings, and doing it again six months later without the first integration falling apart. That requires institutional knowledge about what to prioritize during the first hundred days, which employees are essential to retain, how to communicate with acquired customers, and when to push for system conversion versus when to wait. First Financial has built this knowledge through repetition, and each successful integration makes the next one more likely to succeed. The ability to successfully execute serial acquisitions, maintaining franchise value while achieving cost synergies, is a genuine process advantage that compounds over time.

Taken together, Helmer's framework reveals that First Financial lacks a dominant, category-defining competitive moat. It does not have the kind of durable power that characterizes companies like Visa, with its network effects, or Google, with its scale economies in search. What it has instead is a portfolio of moderate advantages that interact and compound. Conservative underwriting culture, proven M&A execution capabilities, geographic density in contiguous markets, and relationship-based customer loyalty are individually modest advantages. Together, they create a competitive position that is better than the sum of its parts. For investors, this means First Financial is unlikely to generate the kind of extraordinary returns that moat-protected businesses produce, but it is also unlikely to suffer the kind of catastrophic declines that afflict businesses with no competitive advantages at all. It occupies the middle ground: a well-run company in a competitive industry, differentiated primarily by execution rather than structural advantage.

XIV. Bull Case versus Bear Case

The investment debate around First Financial Corporation centers on whether the company's proven M&A strategy and conservative banking culture can continue generating attractive returns in an increasingly challenging competitive environment.

The bull case rests on several compelling arguments, and the most powerful one is also the simplest: this story is not over. The consolidation runway in American banking remains enormous. There are still thousands of community banks in the United States, many with aging ownership, subscale operations, and limited succession plans. Every year, a meaningful number of these institutions look for buyers, and First Financial has positioned itself as an attractive acquirer with a track record of respectful integration and fair pricing. The company's geographic focus on Tennessee and the Southeast provides exposure to some of the strongest demographic and economic growth trends in the country. Nashville, Chattanooga, and the broader middle Tennessee corridor are attracting corporate relocations, population growth, and investment at rates that dwarf the national average.

The company's financial performance supports the bull thesis. Record net interest income, margin expansion, improving efficiency ratios, and strong asset quality suggest that the acquisition strategy is working as intended. Capital ratios remain robust, providing the capacity for additional deals without excessive leverage. Keefe, Bruyette and Woods, a respected bank analyst firm, raised its price target for First Financial, reflecting growing confidence in the company's earnings trajectory. And insider buying has provided an additional signal of management confidence: Director James McDonald purchased 2,295 shares in mid-October 2025 at around $52.25, lifting his total holdings above 11,000 shares. That is not a token gesture from someone looking to generate a press release. That is a director putting meaningful personal capital behind his conviction in the company's future.

The dividend yield of roughly 3.18 percent provides income while investors wait for capital appreciation, and the stock has historically traded at valuations that offer some margin of safety relative to tangible book value.

There is also a "myth versus reality" dimension worth addressing. The consensus narrative about community banks is that they are relics of a bygone era, doomed to be consolidated out of existence by technology and scale. The reality, as First Financial demonstrates, is more nuanced. Well-managed community banking platforms with disciplined M&A strategies can actually benefit from the consolidation trend, growing stronger as weaker competitors exit. The myth is that consolidation kills community banks. The reality is that consolidation kills poorly managed community banks while rewarding the disciplined survivors. For investors who believe that this dynamic will continue, First Financial represents an attractive way to express that thesis.

The bear case, however, is not trivial, and serious investors must grapple with its arguments honestly. The most fundamental concern is the "too small to compete, too large to be nimble" challenge, sometimes called the "doughnut hole" of banking. At six billion dollars in assets, First Financial is large enough to face the regulatory burdens and compliance costs that affect all banks above certain thresholds, but too small to achieve the technology and scale advantages of institutions ten or twenty times its size. Every dollar spent on cybersecurity, digital banking platforms, and regulatory compliance is a dollar that a mega-bank can spread across a vastly larger revenue base.

Geographic concentration remains a risk. While the expansion into Tennessee and Georgia is encouraging, First Financial's markets are still heavily weighted toward the Midwest and Southeast. An economic downturn concentrated in these regions, whether driven by manufacturing decline, agricultural stress, or a correction in Nashville's overheated real estate market, could disproportionately impact the company's loan portfolio. Commercial real estate exposure, a concern for the entire banking industry in the post-COVID era of remote work and shifting space utilization patterns, represents a specific risk that investors should monitor.

Net interest margin compression is a perpetual concern for rate-sensitive community banks. To explain this risk simply: when interest rates fall, the rates banks earn on their loans decline, but the rates they pay on deposits often do not decline as quickly or as far. This asymmetry, known as deposit beta, can squeeze the spread between what a bank earns and what it pays, compressing the net interest margin that is the primary driver of earnings.

While the current environment has been favorable, any significant decline in interest rates could pressure margins, particularly if deposit competition intensifies as it tends to during rate-cutting cycles. The bank's recent margin expansion has been partly driven by the higher-rate environment and the accretive impact of acquisitions, both of which could reverse.

Integration execution risk is elevated with multiple recent deals. SimplyBank and CedarStone represent significant organizational complexity, and the risk of customer attrition, employee turnover, or technology integration failures is real even for experienced acquirers. Each acquisition adds new markets, new loan portfolios, and new operational processes that must be absorbed without disrupting the existing franchise.

The fintech threat, while sometimes overstated by Silicon Valley cheerleaders, is genuine over longer time horizons. Young consumers increasingly manage their finances through mobile apps and digital platforms that bypass traditional banking entirely. A twenty-five-year-old in Nashville is far more likely to open their first checking account with Chime or SoFi than with a community bank they have never heard of. While commercial banking relationships remain sticky, the retail deposit franchise that funds community bank lending is gradually being eroded by alternatives that did not exist a decade ago. The myth that fintechs would replace banks entirely has not materialized, but the reality that they are skimming the most profitable customer segments is undeniable.

There is also a broader macro risk that applies to all banks but weighs particularly on institutions with Midwest and Southeast exposure. The agricultural sector, which remains important to First Financial's Indiana and Illinois markets, faces long-term headwinds from climate variability, trade policy uncertainty, and consolidation that favors large corporate farming operations over the family farms that community banks have traditionally served. Manufacturing, another pillar of the Midwest economy, continues its long-term employment decline even as output remains strong. These structural economic trends do not create immediate risk, but they slowly erode the customer base in legacy markets, reinforcing the importance of the company's expansion into higher-growth Southeastern territory.

There are also important regulatory considerations to flag. As First Financial approaches the five billion dollar asset threshold and eventually the ten billion dollar mark, it will face progressively more intensive supervisory scrutiny. The Dodd-Frank Act's Durbin Amendment, which caps debit card interchange fees for banks above ten billion in assets, represents a material revenue headwind when that threshold is eventually crossed. Additionally, the company's growing commercial real estate portfolio should be viewed in the context of evolving regulatory guidance on CRE concentration limits. Regulators have historically viewed CRE concentrations exceeding three hundred percent of risk-based capital as warranting heightened scrutiny, and acquisitions that bring in CRE-heavy portfolios can push acquirers toward those limits.