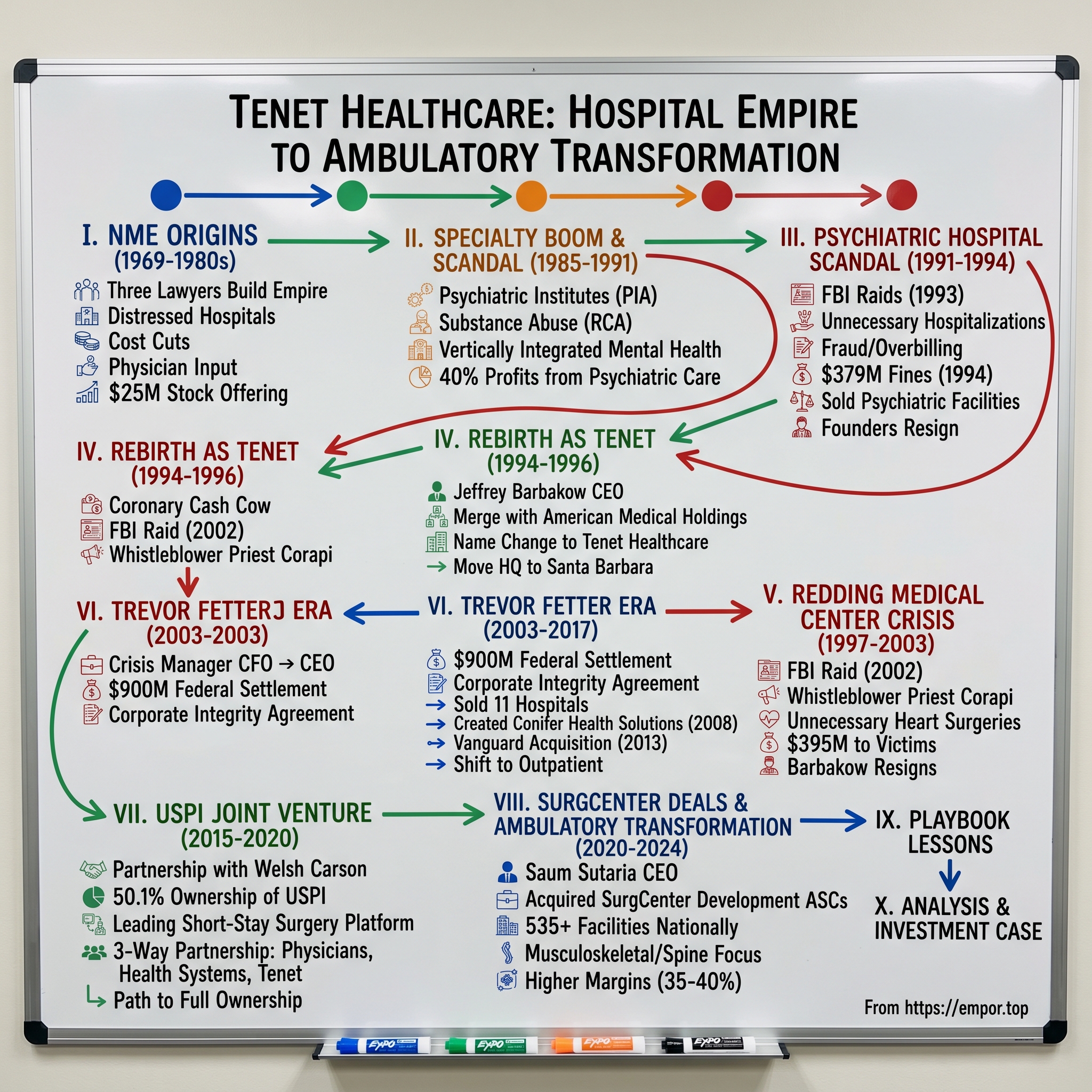

Tenet Healthcare: From Hospital Empire to Ambulatory Transformation

I. Introduction & Episode Roadmap

The conference room at Tenet Healthcare's Dallas headquarters hummed with tension in early 2024. CEO Saum Sutaria watched the numbers roll across the screen: fourth quarter net operating revenues of $5.072 billion, full-year net income of $3.2 billion. For any other healthcare company, these would be champagne-popping moments. But for Tenet—a company that had paid over $2 billion in fraud settlements, survived two major scandals, and reinvented itself more times than a phoenix—these numbers represented something more profound: vindication.

How does a company with one of the most checkered histories in American healthcare transform itself into the nation's largest ambulatory surgery platform? How does an organization that once imprisoned psychiatric patients for insurance money become a Wall Street darling operating over 535 surgical facilities? The answer lies not in a simple turnaround story, but in understanding how corporate DNA persists through rebranding, how regulatory settlements become balance sheet line items, and how the shift from hospital beds to operating tables changed everything.

This is the story of three lawyers who built a hospital empire, lost it to greed, rebuilt it under a new name, nearly lost it again, and ultimately found salvation in the most unlikely place: strip mall surgery centers. It's a tale of persistence—both admirable and troubling—where the same aggressive growth tactics that created scandals also built market dominance. From National Medical Enterprises to Tenet Healthcare, from psychiatric wards to ambulatory surgery centers, this is how American healthcare's most controversial survivor became its most unexpected winner.

The journey ahead takes us through boardroom coups, FBI raids, billion-dollar settlements, and strategic pivots that would make even the most seasoned turnaround artist dizzy. We'll examine how culture survives corporate death, why some companies get infinite second chances, and what happens when the economics of healthcare finally align with a troubled company's capabilities. Buckle up—this isn't your typical hospital story.

II. The NME Origins: Three Lawyers Build a Hospital Empire (1969-1980s)

The Los Angeles afternoon sun glinted off the windows of the modest office building on Wilshire Boulevard in 1968. Inside, three lawyers hunched over incorporation documents, their ties loosened, sleeves rolled up. Richard Eamer, a restless 38-year-old who had driven trucks before law school, pushed the papers across the table to his partners Leonard Cohen and John Bedrosian. "An orphan who dropped out of high school and drove trucks before returning to school and getting a law degree," Eamer had seen opportunity where others saw paperwork.

The timing was perfect—almost suspiciously so. The government's launch of Medicare and Medicaid programs offered guaranteed profits by spurring demand for health-care services and promising to pay providers 6% to 8% above their costs. For three attorneys specializing in healthcare law, this wasn't just policy change—it was a gold rush wearing a white coat.

Tenet was first incorporated in 1969, by attorneys Richard Eamer, Leonard Cohen and John Bedrosian, as National Medical Enterprises (NME) and headquartered in Los Angeles, California. But the real story started with six California hospitals and a $25 million stock offering in 1969—though various sources suggest the initial capital was closer to $7 million. What mattered wasn't the exact number but the velocity of what came next.

Eamer wasn't your typical healthcare executive. Reports suggest he suffered from bipolar disorder for which he took lithium, with a Wall Street Journal article from January 1993 painting a picture of a rather bizarre and unpredictable personality but with a fixation on the bottom line. This intensity would prove both blessing and curse—driving extraordinary growth while planting seeds of destruction.

The rollup playbook was elegantly simple: buy distressed community hospitals, slash costs, standardize operations, keep physicians happy. Attention to both cost management and physician input became trademarks as NME concentrated on building services around community hospitals. Eamer told Forbes, "in many ways, running a hospital chain is like operating a hotel or retail chain"—a quote that would haunt the company decades later.

By 1971, NME had launched seven construction projects and tripled in size within a year. The expansion was relentless: NME made its first foray outside of California in 1973, acquiring a general hospital in Seattle, Washington, and building another in El Paso, Texas. By 1975, NME owned, operated, and managed 23 hospitals and a home health care business.

The organizational structure Eamer created would prove fatefully important. He developed a decentralized structure, with each hospital reporting financial results separately, and gave hospital managers and other executives a great deal of autonomy to meet financial goals. This autonomy came with a price—or rather, a target. Eamer set out the financial results he expected each hospital to achieve (called "plan"), recording whether the hospitals "met plan" or not and praised, rewarded, penalized or fired depending on the extent to which they did so. "Exceeding plan" was the ultimate achievement for each hospital executive.

The decade culminated with two transformative acquisitions in 1979: Medfield Corporation and The Hillhaven Corporation, with Medfield adding five Florida-based hospitals including one psychiatric institution, and Hillhaven being the nation's third-largest chain of nursing homes. By the end of 1979, NME was the nation's fourth-largest publicly owned hospital chain, with the majority of its revenues coming from acute-care hospitals.

By 1981, the transformation was complete: NME owned or managed 193 hospitals and nursing homes, becoming the third-largest healthcare company in the United States. The three lawyers had built something unprecedented—a healthcare empire run like a manufacturing business, with "plan" as its North Star and physician partnerships as its engine. But the very culture that enabled this meteoric rise—the relentless focus on financial targets, the decentralized autonomy, the treatment of healthcare as commodity—would soon metastasize into something darker. The stage was set for specialty hospitals, and with them, a descent into one of American healthcare's most shocking scandals.

III. The Specialty Hospital Boom & Seeds of Scandal (1985-1991)

The boardroom at NME's Santa Monica headquarters in the mid-1980s was electric with possibility. Charts showing hockey-stick growth curves covered every wall. Richard Eamer, now in his mid-fifties and at the height of his power, paced the room with manic energy. The acute-care hospital business was getting squeezed—occupancy rates dropping, Medicare tightening, HMOs negotiating harder. But Eamer had found gold in the most unlikely place: the human mind.

In 1983, NME bought the Psychiatric Institutes of America (PIA), one of the nation's largest mental-health-care providers, based in Washington, D.C. From 1981 to 1983, corporate revenues doubled. Entry into the private psychiatric industry allowed NME to profit from a sector whose size doubled every two years throughout the 1980s. The timing was no accident. The Mental Health Systems Act of 1980 had promised federal support for community mental health, but Reagan's administration repealed it almost immediately, creating a vacuum that private operators rushed to fill.

In 1983, NME further streamlined its specialty interests by forming Recovery Centers of America (RCA), a subsidiary comprised of substance-abuse-recovery operations. The company was building a vertically integrated mental health empire—psychiatric hospitals for acute cases, substance abuse centers for the growing addiction crisis, and rehabilitation facilities for everything in between.

The business model was devastatingly simple and profitable. Medicaid accounted for 50 percent of Hillhaven's revenues, but less than 3 percent of the specialty hospitals division's revenues, and less than 6 percent of the general hospitals division's revenues. Because government programs had not kept pace with the rising cost of healthcare while private insurance rates had, NME began to focus on services that were less dependent on Medicare and Medicaid. Translation: target patients with good private insurance, especially employer-sponsored plans that paid generously and asked few questions.

By 1985 NME was the second largest, publicly owned, healthcare services company in the nation, but changes within the industry mandated adjustments and restructuring. The following year, NME sold its recent HMO purchase, as well as a number of unprofitable outpatient clinics and acute-care hospitals. Emphasis was placed on the specialty facilities—especially rehabilitation and substance-abuse centers and psychiatric hospitals—in an effort to bypass nonpayment problems by shifting away from Medicaid- or Medicare-dependent services.

The shift was working spectacularly. By 1990, the company had 200 hospitals in its network and was the second-largest hospital company in the United States. But here's the stunning part: of the company's $578 million in operating profits that year, profits from psychiatric care accounted for 40 percent. Think about that—40% of profits from a division that represented a much smaller portion of beds and revenue. The margins in psychiatric care were extraordinary.

The culture that enabled this profit engine was the same one Eamer had built from day one, only now supercharged with new incentives. Hospital administrators who "exceeded plan" in the psychiatric division received bonuses that dwarfed those in acute care. Norm Zober, Eamer's lieutenant in charge of specialty hospitals, ran the division with military precision, demanding monthly reports that tracked everything from admission rates to average length of stay to insurance reimbursement per patient day.

By 1991, under Eamer's leadership, NME had more than tripled the number of psychiatric facilities it operated. The company operated 35 general hospitals and 115 specialty hospitals, with the psychiatric and substance abuse facilities forming the crown jewels of the empire. The international expansion continued too—Singapore, Australia, Malaysia, Thailand, and the UK all had NME facilities, spreading the company's aggressive management style globally.

But beneath the surface, something sinister was brewing. The same autonomy and pressure to "meet plan" that had driven hospital acquisition success was morphing into something darker in the psychiatric hospitals. When your bonus depends on keeping beds full and insurance payments flowing, and when your patients are vulnerable people in mental health crisis, the incentives become perverse. Employees later testified about meetings where administrators explicitly discussed keeping patients until their insurance benefits ran out—a practice so common it had a name: "maxing out benefits."

The warning signs were already there for those willing to look. Former patients were beginning to speak out about being held against their will. Employees were quitting and talking to reporters about admission quotas and kickback schemes. The trouble began in 1991 when the Texas attorney general sued NME for alleged overbilling practices at its psychiatric facilities in that state.

In classic Eamer fashion, the response was to double down. More hospitals, more admissions, more aggressive collection of insurance benefits. After all, the formula had worked for over two decades. Why would this be any different? As one former executive later recalled, "We thought we were untouchable. We were making so much money, the board loved us, Wall Street loved us. We were the smartest guys in healthcare." The stage was set for one of the most spectacular corporate scandals in American history.

IV. The Psychiatric Hospital Scandal: A Company Unravels (1991-1994)

August 26, 1993. The sun had barely risen over Santa Monica when the convoy of black SUVs pulled into the parking lot of National Medical Enterprises' corporate headquarters. Inside, early-arriving executives watched in horror as 600 federal agents from a variety of agencies, including the FBI and the Internal Revenue Service, raided more than 20 of its facilities across the country, hauling out cartons of records.

At Springwood Psychiatric Institute near Leesburg, Virginia, the scene was surreal. Yesterday's search disrupted what was to have been a festive "employee appreciation week" picnic for staff members and patients. Federal agents showed a search warrant to John M. Midolo, the hospital's chief executive officer, who was dressed in shorts and a blue polo shirt, while staff members hustled patients away from a colorfully decorated gazebo. The balloons on the gazebo wilted in the afternoon heat, and a plywood booth set up for a game of "bean the CEO" stood abandoned.

The raids were the culmination of a three-year investigation that had begun with whispers and ended with screams. In the early 1990s as National Medical Enterprises, the company was accused of committing fraud by admitting thousands of psychiatric patients who did not need hospitalization and then charging these patients inflated prices. In 1991, the federal government investigated the company for fraud and conspiracy. In 1993, law enforcement raided company offices in an attempt to show that the company was defrauding patients and insurance companies.

The scope of what investigators uncovered was breathtaking. The company was accused of maintaining a corporate policy at its psychiatric facilities of paying doctors for patient referrals; imprisoning patients for insurance payments; charging insurance companies for treatment and medication that were not provided. "keeping patients longer than was necessary" in order to collect insurance, billing for false diagnoses and denying patients necessary services.

The human stories behind the statistics were harrowing. Teenagers admitted for minor depression were held for months until their insurance ran out. Children as young as six were diagnosed with disorders they didn't have and pumped full of medications they didn't need. Adults seeking help for anxiety found themselves locked in psychiatric wards, unable to leave, their pleas to family members intercepted by staff. One former patient later testified about being held for 147 days for what should have been a three-day evaluation.

The financial mechanics of the fraud were elegant in their simplicity and horrifying in their execution. Bounty hunters—that's what employees called the marketers who trolled emergency rooms and schools for potential patients—received bonuses for each admission. Psychiatrists who met admission quotas received luxury vacations and cash bonuses. Those who questioned diagnoses or recommended early discharge found themselves unemployed.

By September 1991, the dominoes had started falling. Texas sued Psychiatric Institutes of America, a unit of NME, charging it made illegal payments to gain patient referrals and defrauded the state's Crime Victims' Compensation Fund. Public hearings in Texas featured psychiatric patients telling stories about being held against their will, forcibly medicated, and subjected to unnecessary treatments.

The financial impact was immediate and devastating. NME's profits plummeted 29% in the first quarter of fiscal 1993. It blamed continued losses on its beleaguered psychiatric division. Operating profits from the psychiatric division fell from $234 million in 1991 to just $3 million in 1993.

In April 1993, the inevitable happened. NME co-founders Richard K. Eamer, its president and chief executive officer, and Leonard Cohen, its chief operating officer, announced their resignations. Both retained board positions. John Bedrosian, the third founder, would follow later. The architects of the empire were abandoning ship, though they clung to their board seats like life rafts.

The legal reckoning came in 1994. National Medical Enterprises Inc. agreed to pay an unprecedented $379 million in fines and penalties to settle federal charges that it provided unnecessary treatment to tens of thousands of patients to illegally collect insurance money. The company pleaded guilty to six counts of making unlawful payments to bribe doctors and other professionals to refer Medicare and Medicaid patients to their hospitals and one count of conspiracy to defraud the U.S. government.

Under the agreement, NME must pay about $357 million to the federal government, $16.3 million to several states and several million dollars to a number of programs and agencies, including $2 million to the federal Center for Mental Health Services. The state of Maryland will recover $1.4 million in Medicaid funds lost to kickbacks and fraud.

Beyond the financial penalties, In 1994, the company paid total $2.5 million to settle lawsuits from 23 patients at its psychiatric hospitals. Hundreds more cases remained pending. The settlements included not just fraud but allegations of false imprisonment, assault, and medical malpractice.

The company also entered into a five-year corporate integrity agreement with the U.S. government, requiring external monitoring, new compliance procedures, and regular reporting. It was corporate probation on an unprecedented scale.

To offset the cost of these settlements and to excise the source of corruption from its corporate identity, NME sold off all but 10 of its 81 psychiatric facilities for about $200 million in 1994. The specialty hospital strategy that had generated 40% of profits was dead. The culture that Eamer had built—"meet plan" at any cost—had finally extracted its ultimate price. But the company itself would survive, and the question now was: could it truly change, or would the same DNA that created the scandal simply find a new host?

V. Rebirth as Tenet: The American Medical Holdings Deal (1994-1996)

The Santa Barbara sun filtered through the windows of Jeffrey Barbakow's new office in June 1993. The 49-year-old former investment banker sat behind a mahogany desk that still smelled of lemon polish, surveying the wreckage he'd inherited. On one side: settlement documents, FBI correspondence, patient lawsuits. On the other: financial statements showing a company hemorrhaging cash and credibility. Between them sat a single sheet of paper with two words written in his handwriting: "Never Again."

Mr. Barbakow, an NME director since 1990 and former investment banking executive, was named chairman and CEO after the board forced out the founders. But Barbakow wasn't exactly an outsider riding to the rescue. Eamer's friend and mentor, Barbakow took over from him in 1993. For over a decade, Barbakow helped finance NME's growth for more than a decade as an investment banker for Merrill Lynch. He knew where the bodies were buried because he'd helped dig some of the graves.

His background was pure Wall Street glamour. Jeffrey C. Barbakow began his professional career as an investment banker with Merrill Lynch. During his 20-year tenure with the firm, working on Wall Street, in San Francisco and managing their Los Angeles Investment Banking office, he focused on entertainment, media and healthcare clients. While at Merrill Lynch, he served as chairman of ML Film Partners, and president of both ML Media and ML Opportunity Partners. From 1988 to 1991, he served as chairman, CEO and president of Metro-Goldwyn-Mayer/United Artists Communications Co (MGM/UA).

The immediate challenge was survival. Fellow NME board members asked him to fix the ailing company. They wanted him to end NME's billing scandals and find a merger partner. He did end the scandals with a then-record $379 million federal settlement. But finding a merger partner for a company with NME's reputation was like trying to sell a haunted house during an exorcism.

The answer came from an unexpected direction. American Medical Holdings, run by the Bedner family, operated 36 hospitals in California and Florida—clean, profitable facilities with no psychiatric baggage. The companies had complementary geographic footprints and, more importantly, AMH's reputation could help cleanse NME's toxic brand.

When National Medical Enterprises merged with American Medical Holdings in 1995, it changed its name to Tenet Healthcare Corp. for a reason: to remind itself of what it called an ongoing commitment to the "tenets" of quality patient care. The name change was more than cosmetic—it was meant to signal a complete break from the past. In 1994, NME bought American Medical Holdings for $3.35 billion, a deal that would close in 1995 with the rebranding.

The $3.3 billion acquisition ranks Tenet the second largest investor-owned healthcare provider in the United States with 83 acute care hospitals and numerous related businesses in 13 states and four foreign countries. "The combination of these two strong companies will create one of this country's preeminent healthcare providers," said Jeffrey C. Barbakow, chairman and chief executive officer. "Tenet has the cash flow and balance sheet necessary to be an aggressive leader in this rapidly evolving industry".

Following completion of the acquisition, NME changed its name to Tenet Healthcare Corporation. The transformation seemed complete—new name, new hospitals, new promise. In 1996, Tenet CEO Jeffrey Barbakow moved Tenet's headquarters from Santa Monica, California to Santa Barbara, physically distancing the company from its past.

Also that year, Tenet acquired OrNda, then the third-largest investor-owned hospital chain, further diluting the NME legacy hospitals in a sea of new acquisitions. The strategy was clear: grow so fast and so large that the old NME would become just a footnote in a much bigger story.

But here's what should have set off alarm bells: The NME management team that agreed to the record $379 million settlement in 1994, including Mr. Barbakow, Ms. Christi R. Sulzbach, and four out of ten members of the Board, remained largely intact after the name change to Tenet. The same people who had overseen the culture that created the scandal were now promising to fix it.

Until May 2003, eight out of twelve senior management positions were held by holdovers from NME, including Mr. Barbakow, Ms. Sulzbach, Michael Focht, Barry Schochet, Bernice Bratter, Maurice DeWald, Lester Korn, and Raymond Mathiasen. It was like treating an infection by changing the bandage but leaving the wound untouched.

The rebranding strategy worked—at least on Wall Street. Investors saw a company with fresh assets, strong cash flow, and aggressive leadership. The stock price began to recover. New hospital acquisitions grabbed headlines. The psychiatric scandal faded into yesterday's news. But beneath the surface, in the DNA of the organization, the same pressures that had created the first scandal were rebuilding. The "meet plan" culture hadn't died; it had simply found a new host. And this time, it would target a different kind of patient.

VI. The Second Act: Growth, Scandals, and the Redding Medical Center Crisis (1997-2003)

The operating room at Redding Medical Center gleamed under the fluorescent lights in early 2002. Dr. Chae Hyun Moon, director of the cardiology department, looked at the angiogram images with practiced concern. "You see this? You need bypass surgery immediately," he told yet another patient. The words had become a script, delivered with the same urgency whether the arteries showed 90% blockage or barely any narrowing at all.

In 1998, Tenet purchased eight Philadelphia hospitals owned by the bankrupt Allegheny Health, Education & Research Foundation for $345 million. The expansion continued relentlessly. By 2001, Tenet owned 111 hospitals in the United States, and profits were soaring. Jeffrey Barbakow's strategy of aggressive growth through acquisition was working spectacularly—on paper.

But in the small Northern California town of Redding, something extraordinary was happening. Coronary surgeries (especially on patients covered by Medicare) were a cash cow, giving Redding Medical Center more than $300,000 for each surgery. By 2002, the hospital was performing nearly 1,000 heart bypasses a year, one of the highest rates in the state.

As its profits in Redding skyrocketed, Tenet's stock price ballooned past $50 per share. That benefited Tenet CEO Jeffrey Barbakow, who exercised stock options that paid him $115 million in 2001. Moon and Realyvasquez, meanwhile, were also enjoying the high life, living on million-dollar properties with large acreage and enjoying a stream of adulation from people who believed the doctors had saved their lives.

The pattern was chillingly familiar to anyone who remembered the psychiatric scandal. The pattern was inevitably the same: The person had experienced some kind of chest pain or irregularity, went to Redding Medical Center and consulted Moon, who rushed them into surgery that he said prevented their death from blockage, stroke or some other debilitating effect. (Moon was the director of Redding Medical Center's cardiology department; Realyvasquez, Moon's right-hand man, was the center's chief of cardiac surgery, who performed many of the surgeries.)

Then came John Corapi, a Catholic priest who would become the unlikely whistleblower. Last June, shortly after his 55th birthday, John Corapi got the bad news from Dr. Chae H. Moon, director of the cardiology department at Tenet Healthcare Corp.'s Redding Medical Center. Corapi had splits in his arteries, according to Moon's June 11 report. His recommendation: bypass surgery. But Corapi sought a second opinion in Las Vegas. Friends suggested that he should go to Las Vegas for this as they could provide support. The surgeon there told him his heart was normal. Multiple other opinions confirmed this.

He repeatedly spoke to the hospitals administrators and told them of the problem. Instead of looking into this the administrator advised him to follow the Redding cardiologists advice. Instead he took his concerns to medical bodies and then to the FBI. He also lodged a Qui Tam court case.

The Redding Medical Center scandal breaks: On October 30th, 2002, 40 FBI Agents raided Tenet Healthcare's Redding Medical Center in Redding, California and the Cardiology Associates of Northern California offices of a cardiologist and cardiac surgeon. The scandal erupted after FBI agents raided the medical center in October 2002 and discovered that hundreds of its surgical patients' medical records did not support the need for surgery.

The scope was staggering. An FBI affidavit at the time alleged that as many as half the heart surgeries and tests performed by the doctors were unnecessary. And up to a quarter of the work was performed on patients who had no serious heart problems at all. The human toll was devastating: Some of the plaintiffs' complications from the surgeries included stroke, paralysis, and heart attack. Many patients now require assisted living, and 94 of the patients have died.

Stock price collapse: Since October 2002, the Senate Finance Committee, the Securities and Exchange Commission, the HHS Office of Inspector General, the Department of Justice and the Federal Trade Commission have launched separate investigations into Tenet related to alleged Medicare fraud and other issues. Federal investigations into the company's billing practices began late in 2002, leading to a decline in Tenet's stock price of about 70%.

The financial settlements came in waves. Last year, Tenet officials agreed to pay $54 million to settle federal allegations that the two of the hospital's physicians performed unnecessary heart surgeries and defrauded Medicare. But the bigger blow came in 2004: Tenet Healthcare Corporation, the country's second-largest hospital chain, agreed to pay $395 million to victims of unnecessary heart surgeries performed at Redding Medical Center. The treating cardiologists agreed to pay a total of $24 million.

The parallels to the psychiatric scandal were unmistakable—vulnerable patients, aggressive diagnosis, insurance maximization, corporate pressure for profits. The same cultural DNA that had created the first scandal had simply found a new expression. In cardiac surgery, the company had discovered an even more lucrative version of its old playbook: instead of holding patients for weeks to max out psychiatric benefits, they could generate $300,000 per surgery in a single day.

In 2003, as investigations multiplied and the stock price cratered, Jeffrey Barbakow's decade-long run came to an end. Trevor Fetter became CEO of Tenet and started what the company called its "Commitment to Quality." But the damage was done. Tenet had proven, once again, that changing a name doesn't change a culture, and that the same aggressive growth tactics that build empires can also destroy them—twice.

VII. The Trevor Fetter Era: Stabilization and Strategy Shift (2003-2017)

The Dallas morning was crisp in November 2002 when Trevor Fetter walked back into Tenet's offices—not as the triumphant former CFO who'd left to run his own company, but as a crisis manager returning to a burning building he'd helped construct. At 42, with thick-rimmed glasses and the methodical demeanor of a Harvard MBA, Fetter looked more like a management consultant than a turnaround artist. Which, in a way, was exactly what Tenet needed.

After graduating from HBS in 1986, Trevor worked in investment banking for two years before joining a client, Metro-Goldwyn-Mayer, ultimately becoming CFO. In 1995 he joined Tenet Healthcare Corporation, where he served as CFO through the end of 1999. He then founded and served as Chairman and CEO of Broadlane, a Tenet spin-off that was a leader in improving the performance of healthcare providers in the supply chain using emerging e-commerce technology. Broadlane was named one of Inc. magazine's 500 fastest growing private companies in multiple years. Trevor returned to Tenet in late 2002 and was named CEO in 2003.

The appointment was controversial. After working with Jeffrey Barbakow at Merrill Lynch, he decided to follow his colleague to movie and entertainment company Metro-Goldwyn-Mayer/United Artists as senior vice president and later CFO. His succession in 2003 was still questioned by experts, who felt the appointment might continue Tenet's criticized business practices. After all, Fetter had been Barbakow's protégé, his CFO during the late 1990s expansion that set the stage for Redding. Critics saw it as rearranging deck chairs on the Titanic.

But Fetter understood something his predecessors hadn't: the era of cowboy capitalism in healthcare was ending. Brought in to spearhead Tenet's turnaround amidst government investigations and allegations of wrongdoing in late 2002, Fetter has led the company through significant changes in strategy, culture and governance. Today, Tenet is recognized as a leader in quality, transparency and innovation in driving down the cost of health care. As he systematically tackled the company's problems, Fetter also positioned Tenet to thrive in a post health care reform environment.

His first priority was survival. To resolve multiple allegations, including that its hospitals systematically overcharged Medicare, Tenet reached a $900 million settlement with the federal government. It also agreed to a "corporate integrity agreement" that allowed it to continue as an ongoing concern, and arranged a payment plan that stretched to 2010. In June 2006, Tenet agreed to pay $725 million in cash and give up $175 million of Medicare payments for a total of $900 million in fees to resolve claims it defrauded the federal government for over-billing Medicare claims during the 1990s. To finance the settlement, they sold 11 hospitals.

The cultural transformation was harder than the financial one. Audrey Andrews, who was Tenet's chief compliance officer when Fetter was resolving those problems and is now senior vice president and general counsel, recalls Fetter announcing early on that he wanted Tenet to be more than just scrupulously honest in billing. "Trevor told all of us that we're going to be No. 1 in quality," she recalls. It sounded a bit audacious at the time, she admits. "Here we were on the verge of perhaps being cut off by the government. We were below average in quality. How is it possible we will go from black eye to the best?" But looking back, she says, Fetter "used the challenge of how we are doing in quality to really advance the company. We're years ahead of where we would have been if we were just on a normal trajectory."

As CEO, however, Mr. Fetter continued to focus on improving Tenet's reputation. He appointed a senior vice president of clinical quality and launched a system-wide initiative to improve patient care in Tenet hospitals. The creation of Conifer Health Solutions in 2008 represented a different kind of thinking—instead of just running hospitals, Tenet would provide revenue cycle management services to other healthcare providers. It was the beginning of a diversification strategy that would ultimately save the company.

The strategic shift accelerated with healthcare reform. Despite the generally disappointing rollout of the new insurance marketplaces, Tenet Healthcare Corp. President and CEO Trevor Fetter still views the insurance exchanges as a business opportunity. Tenet has incurred an annual $800 million expense caring for uninsured patients—which it expects to be significantly reduced under healthcare reform. Fetter said the trend in California—one of a few states that have seen early success with exchange enrollments, and where Tenet operates 11 hospitals—has been "much more positive."

The 2013 Vanguard acquisition marked another turning point. In October, it completed a $4.3 billion acquisition of Vanguard Health Systems, which bulked up Tenet, the nation's second-largest hospital chain, to include 77 acute care hospitals, 173 outpatient centers, 100,000 employees, and annual revenue of $15 billion to $16 billion. The acquisition created the third-largest investor-owned hospital company in the United States.

But the real transformation was happening outside the hospital walls. In October 2016, Tenet Healthcare and two of its subsidiaries agreed to pay $513M to resolve allegations that they had defrauded the United States and had made use of a kickback scheme—yet another settlement, but this time the company was strong enough to absorb it without existential crisis.

On May 7, 2015, the Tenet board of directors appointed Trevor Fetter, Tenet's then president and CEO, as chairman of the board. The student had fully replaced the master. But even as Fetter consolidated power, he was laying the groundwork for Tenet's most radical transformation yet—one that would finally break the cycle of scandal and reinvention by moving away from hospitals altogether. The answer lay in ambulatory surgery centers, and a company called United Surgical Partners International.

VIII. The USPI Joint Venture: Finding the Future in Ambulatory Care (2015-2020)

The conference room on the top floor of Welsh, Carson, Anderson & Stowe's Park Avenue offices hummed with anticipation on March 23, 2015. Trevor Fetter sat across from the private equity partners, studying the deal structure one final time. This wasn't just another acquisition—it was Tenet's bet on a fundamentally different future, one where hospitals would become the spokes, not the hub, of healthcare delivery.

The 2015 watershed moment: Tenet Healthcare Corporation (NYSE:THC) ("Tenet") has completed its previously announced joint venture transaction with Welsh, Carson, Anderson & Stowe that combines the short-stay surgery and imaging center assets of Tenet and United Surgical Partners International ("USPI") to create the leading U.S. short-stay surgery platform.

The structure was elegant in its complexity. Tenet contributed its interest in 49 ambulatory surgery centers and 20 imaging centers to the joint venture and refinanced approximately $1.5 billion of existing USPI debt, which will be allocated to the joint venture through an intercompany loan. Tenet also made an approximately $404 million payment to pre-existing USPI shareholders to align the respective valuations of the assets contributed to the joint venture.

Tenet owns 50.1% of the new USPI and will consolidate USPI's financial results. Welsh Carson and the other existing shareholders in USPI own the remaining 49.9%. A pre-determined put-call structure provides a path to full ownership of USPI by Tenet over the next five years.

The strategic rationale was compelling. "This joint venture significantly expands our ability to benefit from the growing demand for convenient, cost-efficient outpatient care and enhances our growth and earnings potential," said Trevor Fetter, Tenet's chairman and chief executive officer. But beneath the corporate speak lay a more fundamental truth: Tenet was finally escaping the hospital trap that had ensnared it for decades.

The numbers told the story. Following the combination, the new USPI now has more scale through its operation of 249 ambulatory surgery centers, 18 short-stay surgical hospitals and 20 imaging centers in 29 states, and is well-positioned to benefit from the growing demand for high quality and high value ambulatory solutions. This wasn't just adding capacity—it was changing the entire business model.

The economics of ambulatory surgery centers were fundamentally different from hospitals. Where a hospital might perform a knee replacement for $50,000, an ASC could do it for $15,000. The overhead was lower, the efficiency higher, the patient satisfaction better. And crucially, the regulatory scrutiny was lighter—no more FBI raids over unnecessary admissions when patients went home the same day.

Bill Wilcox will continue to lead USPI as chief executive officer and Brett Brodnax, president and chief development officer of USPI, will lead the company's strategy and growth efforts. This was critical—Tenet wasn't trying to impose its hospital culture on USPI. They were keeping the management team that had built the business, learning from them rather than teaching them.

The partnership model was also revolutionary for Tenet. The company will maintain the USPI brand, as well as USPI's innovative three-way partnership model with physicians and leading not-for-profit health systems. Instead of employing physicians or competing with them, USPI made them partners—giving them ownership stakes in the facilities where they operated. It aligned incentives in a way that Tenet's hospital model never could.

The put-call structure was particularly clever. By giving Welsh Carson the right to sell (put) and Tenet the right to buy (call) at predetermined prices over five years, both parties had certainty about the exit. Welsh Carson could realize their investment gains, while Tenet could gradually increase ownership without a massive upfront payment.

But the real genius of the deal wasn't in the structure—it was in the timing. Healthcare was shifting rapidly toward outpatient care. Medicare was pushing procedures out of hospitals through payment reforms. Commercial insurers were steering patients to lower-cost settings. Technology was making complex surgeries safer in outpatient settings. Tenet wasn't just buying assets; it was buying a position in healthcare's future.

The path to full ownership came faster than expected. Tenet Healthcare Corporation (NYSE: THC) today announced that it has purchased the remaining 15 percent ownership interest in United Surgical Partners International (USPI) owned by Welsh, Carson, Anderson & Stowe (WCAS). As a result, Tenet has increased its ownership in USPI from 80 percent to 95 percent, effective today. By 2018, Tenet had essentially completed the buyout, years ahead of schedule.

The transformation was more than financial. For the first time in its history, Tenet had a growth engine that didn't depend on buying or filling hospital beds. It had a business model that aligned physician incentives with corporate goals. Most importantly, it had found a way to provide healthcare that patients actually preferred—convenient, efficient, lower-cost procedures in modern facilities close to home. The company that had twice been brought low by hospital scandals was betting its future on getting patients out of hospitals entirely.

IX. The SurgCenter Deals & Ambulatory Transformation (2020-2024)

The PowerPoint slide glowed on the boardroom screen at Tenet's Dallas headquarters in November 2021. "USPI Growth Acceleration," read the title, with arrows pointing upward like a hockey stick. CEO Saum Sutaria, who had taken over from Trevor Fetter in 2019, studied the numbers with the intensity of a cardiac surgeon examining an angiogram. This wasn't just another acquisition—it was the validation of a strategy that had taken six years to mature.

The first SurgCenter acquisition had actually come a year earlier: Last year, Tenet and USPI inked a separate $1 billion deal with SurgCenter Development to acquire more than 40 ambulatory surgery centers. But that was just the appetizer. The main course was about to be served.

The mega-deal of 2021: Tenet Healthcare Corporation (NYSE: THC), and its subsidiary United Surgical Partners International (USPI), today announced that they have entered into a definitive agreement with the principals of SurgCenter Development (SCD) to acquire SCD. Tenet/USPI will acquire SCD's ownership interests in 92 ASCs and related ambulatory support services for approximately $1.2 billion.

The structure revealed how much Tenet had learned from its USPI experience. SCD owns a minority interest of approximately 39 percent on average in 86 of the ASCs and a majority interest of approximately 55 percent on average in six of the ASCs. This meant Tenet wasn't buying control outright in most cases—they were partnering with the existing physician owners, maintaining the alignment of incentives that made ASCs work.

Additionally, USPI plans to offer to acquire a portion of equity interests in the ASCs from physician owners for incremental consideration of up to approximately $250 million. This wasn't a forced buyout—it was an invitation. Physicians could sell if they wanted liquidity, or hold if they believed in the growth story. It was the opposite of the command-and-control culture that had created Tenet's previous scandals.

But the real genius was in the development agreement: the partners said they are committing to the development of at least 50 new ASCs led by the SurgCenter team. USPI will have the exclusive option to obtain an ownership position in these centers. This wasn't just buying existing centers—it was buying a growth engine, a pipeline of future facilities that would be built from scratch in partnership with physicians who wanted to own their destiny.

Building scale was critical. Following the addition, USPI will have more than 440 facilities in 35 states. But more importantly, With more than 535 facilities across the United States, the company serves patients in ambulatory surgery centers and surgical hospitals. The scale gave USPI negotiating power with insurers, operational efficiencies, and the ability to invest in technology and quality improvements that smaller operators couldn't afford.

The case mix was equally strategic. Eighty percent of the surgery centers specialize in musculoskeletal care, such as spine and total joint procedures—key opportunities for outpatient growth. These weren't simple procedures—they were complex surgeries that had traditionally been done in hospitals but were now safe in outpatient settings thanks to advances in anesthesia, surgical techniques, and pain management.

The financial performance validated the strategy. Ambulatory revenue climbed 31% for the full year from 2020. In the fourth quarter, ambulatory revenue gained 14% from the year-earlier period to $742 million. The margins were spectacular—ASCs operated at 35-40% EBITDA margins compared to 15-20% for hospitals.

But here's what really mattered: Tenet currently owns 95% of USPI, having gradually increased its stake through the put-call mechanism established in 2015. The company that had once been forced to divest its specialty hospitals as punishment for fraud now owned the largest ambulatory surgery platform in America through legitimate growth and strategic partnerships.

The transformation wasn't just financial—it was philosophical. "We are extremely pleased to announce this transformative transaction and partnership, which builds upon USPI's position as a premier growth partner and SCD's track record of developing high-quality centers with leading physicians," said Saum Sutaria, M.D., CEO of Tenet Healthcare. "By welcoming these centers into our company, USPI will maintain its reach as the largest ambulatory platform for musculoskeletal services, a high-growth service line. We are also creating a pathway for further expansion through a partnership that pairs the expert development and operational capabilities of our two organizations."

The language mattered. "Welcoming," "partnership," "physician-led"—these weren't the words of the old Tenet that demanded hospitals "meet plan" at any cost. This was a company that had learned that in healthcare, alignment of interests beats command and control every time.

The economics told the story. Where psychiatric hospitals had generated profits through extended stays and maxed-out insurance benefits, and cardiac units through unnecessary procedures, ASCs generated profits through efficiency and patient preference. Patients wanted outpatient surgery—it was more convenient, less scary, and got them home to their own beds. Physicians wanted it because they could maintain ownership and control. Insurers wanted it because it was cheaper. For once, Tenet had found a business model where doing the right thing was also the profitable thing.

The shift from high-cost hospitals to efficient outpatient centers wasn't just a strategic pivot—it was a fundamental reimagining of what a healthcare company could be. The company that had twice nearly destroyed itself chasing hospital profits had found salvation in helping patients avoid hospitals altogether.

X. Playbook: Lessons from Serial Scandal to Market Leader

The conference room walls at Harvard Business School displayed the timeline: 1969, founding as NME. 1993, psychiatric scandal. 1995, rebirth as Tenet. 2002, cardiac scandal. 2015, USPI joint venture. 2024, largest ambulatory platform in America. Trevor Fetter, now teaching a case study on corporate transformation, pointed to the pattern. "The question isn't why did the scandals happen," he told his MBA students. "The question is why did the same company create them twice—and then stop?"

The persistence of corporate culture through rebranding is perhaps the most sobering lesson from Tenet's journey. Changing a name from National Medical Enterprises to Tenet Healthcare didn't change the underlying DNA. The same "meet plan" culture that drove the psychiatric scandal simply found new expression in cardiac surgery. Corporate culture is like water—it finds its level regardless of the container. The aggressive, numbers-driven approach that Eamer built into NME's foundation survived multiple CEO changes, billion-dollar settlements, and even criminal convictions. It took a fundamental change in business model—from hospitals to ASCs—to finally break the pattern.

How regulatory settlements become "cost of doing business" reveals a troubling truth about American healthcare. Tenet paid over $2 billion in settlements across two decades, yet remained a viable company. The settlements were large enough to grab headlines but not large enough to destroy the company. This created a perverse incentive structure where the potential profits from aggressive practices outweighed the risk of getting caught. It wasn't until the reputational damage threatened the company's very existence that real change occurred.

The role of physician partnerships and financial incentives proved to be the double-edged sword of Tenet's story. In the hospital model, paying physicians for referrals created fraud. In the ASC model, making physicians equity partners created alignment. The difference wasn't in the presence of financial incentives—it was in their structure. When physicians own part of the facility, their incentive is to perform appropriate surgeries efficiently. When they're paid per referral, their incentive is volume regardless of necessity. The lesson: financial incentives aren't inherently good or bad—their structure determines their outcome.

Capital allocation: From buying hospitals to surgery centers represents one of the great strategic pivots in healthcare history. Hospitals are capital-intensive, highly regulated, and increasingly commoditized. ASCs are capital-efficient, lightly regulated, and differentiated by physician quality. Tenet spent decades and billions trying to build hospital scale. But in ASCs, they achieved market leadership with a fraction of the capital by partnering rather than acquiring. The lesson: sometimes the best capital allocation is changing what you're allocating capital toward.

The economics of ambulatory vs. hospital care tell a story of inevitable disruption. An ASC can perform a knee replacement for $15,000 that costs $50,000 in a hospital. The ASC has 40% margins; the hospital has 15%. The patient goes home the same day from the ASC; they stay three days in the hospital. The ASC is convenient and comfortable; the hospital is intimidating and infectious. Once technology made complex procedures safe in outpatient settings, the economic logic became irresistible. Tenet didn't create this trend—they recognized it and rode it.

Managing reputational risk while growing through M&A required a delicate balance. Every acquisition brought scrutiny—would this be another Redding Medical Center? Tenet managed this by keeping acquired management teams, maintaining local brands, and most importantly, by changing the incentive structure. Instead of imposing corporate mandates on acquired facilities, they offered partnership. Instead of demanding aggressive growth, they focused on quality metrics. The acquisitions worked because Tenet had finally learned to be a partner, not a predator.

Why the shift to outpatient finally worked comes down to alignment. In hospitals, Tenet's interests (fill beds), physicians' interests (practice medicine), and patients' interests (get well) were often in conflict. In ASCs, everyone's interests align: Tenet wants efficiency, physicians want ownership, patients want convenience, and insurers want lower costs. When a business model aligns all stakeholders' interests, success becomes sustainable rather than scandalous.

The transformation from serial scandal to market leadership wasn't just about changing strategy—it was about changing identity. The company that once epitomized healthcare fraud became a model for physician partnership. The organization that twice paid record settlements became a leader in quality metrics. The business that nearly collapsed from reputational damage became a Wall Street darling.

But perhaps the most important lesson is about redemption in corporate America. Companies, like people, can change—but only through fundamental transformation, not cosmetic rebranding. Tenet's journey shows that escaping a toxic culture requires more than new leadership or new promises. It requires a new business model that makes the old behaviors impossible.

The playbook, then, isn't just about how to transform a troubled company. It's about recognizing that in healthcare, sustainable success comes from alignment, not aggression. That profits and patient care aren't mutually exclusive when the business model is right. And that sometimes, the best way to fix a broken hospital company is to stop being a hospital company altogether.

XI. Analysis & Investment Case

Current market position: Tenet Healthcare Corporation (NYSE: THC) is a diversified healthcare services company headquartered in Dallas, Texas which operates ambulatory surgery centers and surgical hospitals through its crown jewel subsidiary, USPI. With over 535 facilities, Tenet has successfully transformed from a troubled hospital operator into the dominant force in ambulatory surgery. But the investment case isn't just about what Tenet has become—it's about where healthcare is going.

Competitive dynamics reveal Tenet's unique position. HCA remains the hospital giant with 180+ facilities and pristine operations, but it's wedded to the hospital model. Community Health Systems struggles with rural hospitals and crushing debt. Surgery Partners, with 180+ ASCs, is Tenet's only real competitor in ambulatory surgery, but at one-third the size. The competitive moat isn't just scale—it's the partnership model. USPI's three-way partnerships with physicians and health systems create switching costs that pure financial ownership can't match.

Bull case: The demographic tailwinds are hurricane-force. Baby boomers are entering peak surgical years—knee replacements, hip replacements, cataracts, all increasingly done in ASCs. Medicare is actively pushing procedures out of hospitals through site-neutral payments. Commercial insurers are steering patients to ASCs through lower copays. The total addressable market for ambulatory surgery is expected to double by 2030. USPI is adding 25-30 centers annually through development and acquisition. The math is compelling: growing market share in a growing market with expanding margins.

Operational improvements continue to drive margins higher. ASCs that USPI acquires typically operate at 25-30% EBITDA margins; within three years, USPI brings them to 35-40% through better supply chain management, improved scheduling, and revenue cycle optimization. With 100+ recent acquisitions still maturing, there's a built-in margin expansion story for years.

The capital allocation priorities have finally aligned with shareholder interests. Instead of empire-building through hospital acquisitions, Tenet is returning cash through buybacks and dividends while investing in high-return ASC development. The company generated over $1 billion in free cash flow in recent years, a remarkable transformation for a company that once lurched from crisis to crisis.

Bear case: The leverage remains elevated, though manageable. Tenet operates with significant financial leverage that adds both fixed costs and some refinancing risk to the organization. Net debt stands at approximately 4x EBITDA, which is acceptable for a company with stable cash flows but leaves little room for error. Rising interest rates increase refinancing risk when bonds mature.

Regulatory risk never fully disappears for a company with Tenet's history. Medicare continues to squeeze reimbursement rates, though ASCs are somewhat protected by their cost advantage. State certificate-of-need laws could limit expansion in certain markets. And there's always the risk that aggressive prosecutors might scrutinize past practices, though the company's compliance infrastructure is now robust.

The history of scandals creates a permanent discount. Despite a decade of clean operations, Tenet trades at a lower multiple than peers. Investors have long memories, and any whiff of impropriety sends the stock tumbling. This reputational overhang may never fully disappear.

Medicare pressures intensify as the program faces insolvency. While ASCs benefit from site-neutral payments, they're not immune to rate cuts. Medicare Advantage plans, which now cover nearly half of Medicare beneficiaries, are increasingly aggressive in managing utilization. The golden age of fee-for-service medicine is ending, and even efficient operators like USPI must adapt.

Competition from hospitals building their own ASCs is intensifying. Health systems recognize the threat and are developing their own ambulatory strategies. While USPI's scale and expertise provide advantages, the competitive landscape is becoming more crowded.

Valuation and margins analysis suggests a company in transition. Tenet trades at approximately 8-10x forward EBITDA, a discount to hospital peers like HCA (12x) but a premium to troubled operators like Community Health (6x). The blended multiple reflects the market's recognition of USPI's quality offset by concerns about hospital operations and leverage.

The margin story is compelling but complex. USPI generates 40% EBITDA margins, while hospitals operate at 15-20%. As the mix shifts toward ambulatory (now over 40% of EBITDA), consolidated margins should expand. But this requires continued execution and successful integration of acquired centers.

Free cash flow conversion has improved dramatically, with the company generating 15-20% FCF yields in recent years. This provides flexibility for debt reduction, growth investment, and shareholder returns—a luxury Tenet never enjoyed during its scandal-plagued years.

The investment case ultimately comes down to whether you believe in the ambulatory surgery megatrend and Tenet's ability to execute without reverting to old behaviors. The strategic logic is sound: demographics drive demand, technology enables outpatient migration, and economics compel adoption. USPI's market position seems unassailable, with scale advantages and partnership moats.

But investing in Tenet requires accepting irreducible risks. The company's history creates permanent skepticism. The leverage limits flexibility. The regulatory environment remains challenging. And healthcare's transformation toward value-based care threatens all fee-for-service models, even efficient ones.

For fundamental investors, Tenet represents a complex bet: that a company can truly change its DNA, that ambulatory surgery will continue taking share from hospitals, and that operational excellence can overcome reputational baggage. The transformation has been remarkable, but the journey isn't complete. The company that twice nearly destroyed itself through aggressive hospital practices has found redemption in helping patients avoid hospitals altogether. Whether that redemption translates into sustainable shareholder returns remains healthcare's billion-dollar question.

XII. Recent News**

Q3 2024 Earnings Exceed Expectations:** Net income available to common shareholders in third quarter 2024 was $472 million, or $4.89 per diluted share, including an after-tax gain of $209 million, or $2.16 per diluted share, primarily associated with previously announced hospital divestitures. Adjusted diluted earnings per share was $2.93 in third quarter 2024. Consolidated Adjusted EBITDA in third quarter 2024 of $978 million increased 14.5% over third quarter 2023. Third quarter 2024 Ambulatory Care Adjusted EBITDA of $439 million increased 18.6% over third quarter 2023. The results demonstrate the power of the ambulatory transformation strategy.

Ambulatory Growth Continues: Tenet has sold several of its hospitals in recent years to place more focus on its ambulatory segment, made up of United Surgical Partners International (USPI) and its 520 ambulatory surgery centers and 24 surgical hospitals across 37 states. Ambulatory revenue in the quarter grew by 21% year over year to $1.14 billion, with surgical business same-facility system-wide net patient revenues jumping 8.7% and net revenue per case increasing 7.6%. The shift from hospitals to ASCs continues to accelerate.

Hospital Divestitures Fund Transformation: Revenue declined 3.4% from the third quarter in 2023 mainly due to hospital divestitures in the first quarter of this year. Those first-quarter sales included nine hospitals: three South Carolina hospitals to Novant Health for $2.4 billion, four South California hospitals to UCI Health for $975 million, and two other California hospitals to Adventist Health for $550 million. The proceeds have been used to deleverage the balance sheet and invest in higher-margin ambulatory growth.

Full Year 2024 Guidance Raised: The company, once again, boosted its full-year 2024 guidance. Revenue is now projecting to reach $20.6 billion to $20.8 billion for the year. Adjusted EBITDA is forecast to be in the range of $3.9 billion to $4 billion, up $50 million from its prior range. This marks the third consecutive quarter of raised guidance.

Q4 2024 and FY 2025 Outlook: Net income available to common shareholders in fourth quarter 2024 was $318 million, or $3.32 per diluted share. Adjusted diluted earnings per share was $3.44 in fourth quarter 2024. Consolidated Adjusted EBITDA in fourth quarter 2024 was $1.048 billion, which represents an Adjusted EBITDA margin of 20.7%. Fourth quarter 2024 Ambulatory Care Adjusted EBITDA of $530 million increased 14.2% over fourth quarter 2023. FY 2025 Adjusted EBITDA Outlook is expected to be in the range of $3.975 billion to $4.175 billion.

CEO Commentary on Transformation: "2024 was an outstanding year for Tenet characterized by robust revenue growth, efficient operations, high levels of patient satisfaction and clinical quality, and a portfolio transformation that drove substantial balance sheet deleveraging," said Saum Sutaria, M.D., Chairman and Chief Executive Officer of Tenet.

Strategic Capital Deployment: "We will continue to deploy capital to enhance growth in our industry-leading ambulatory surgical business through M&A and de novo development, increase capital spending to fuel organic growth and return excess capital to shareholders via share repurchase, given that we believe our equity continues to trade at attractive multiples relative to the market," Sutaria said. "The combination of an established management team, a focused strategy and consistent operations and discipline capital deployment positions us to drive significant value for physicians, patients and, in turn, our shareholders".

Balance Sheet Strength: Cash on Hand: $4.1 billion as of September 30, 2024. Leverage Ratio: 2.2 times EBITDA or 2.8 times EBITDA less NCI. The company has achieved its lowest leverage ratio since the USPI joint venture, providing flexibility for growth investments and shareholder returns.

Share Buyback Authorization: Board of Directors has authorized a new $1.5 billion share repurchase program, demonstrating confidence in the company's future and commitment to returning capital to shareholders.

XIII. Links & Resources

SEC Filings and Investor Presentations

- Tenet Healthcare Investor Relations: https://investor.tenethealth.com

- Latest 10-K Annual Report: SEC EDGAR Database

- Quarterly Earnings Calls and Presentations: Available on investor relations website

Key Books and Investigative Reports

- "Coronary: A True Story of Medicine Gone Awry" by Stephen Klaidman (2007) - Definitive account of the Redding Medical Center scandal

- "Bedlam: Greed, Profiteering, and Fraud in a Mental Health System Gone Crazy" by Joe Sharkey (1994) - Investigation of NME psychiatric hospital scandals

- "Feeding Frenzy: Organizational Deviance in the Texas Psychiatric Hospital Industry" by Henry Vandenburgh (1999) - Academic analysis of systematic fraud

Government Settlement Documents

- 1994 NME Settlement with DOJ: $379 million psychiatric fraud settlement

- 2003 Redding Medical Center Settlement: $54 million Medicare fraud settlement

- 2006 Medicare Overbilling Settlement: $900 million resolution

- Department of Justice False Claims Act settlements database

Industry Research and Analysis

- American Hospital Association (AHA) Hospital Statistics

- Ambulatory Surgery Center Association (ASCA) Industry Reports

- CMS Medicare Payment Advisory Commission (MedPAC) Reports

- Kaufman Hall Healthcare M&A Reports

Historical News Coverage Archives

- Wall Street Journal Healthcare coverage archives

- Modern Healthcare historical articles

- Los Angeles Times investigative series on NME/Tenet

- Sacramento Bee coverage of Redding Medical Center

Academic and Policy Resources

- Harvard Business School case studies on Tenet transformation

- Health Affairs journal articles on hospital-to-ASC migration

- Institute for Healthcare Improvement resources

- Commonwealth Fund healthcare system performance reports

Current Analyst Coverage

- J.P. Morgan Healthcare Services research

- Jefferies Hospital & Healthcare Facilities coverage

- Deutsche Bank Healthcare Provider analysis

- Mizuho Securities healthcare equity research

Note: This analysis is for informational purposes only and does not constitute investment advice. All financial data and quotes are from public sources. Investors should conduct their own due diligence before making investment decisions.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube