Teradyne: The Silent Gatekeeper of the Silicon Age

I. Introduction & Episode Roadmap

There is a familiar way to tell the story of the semiconductor age, and it usually has two heroes. There is ASML of the Netherlands, the company that builds the impossibly complex extreme-ultraviolet lithography machines that print circuitry finer than a wavelength of visible light. And there is 台灣積體電路製造公司 TSMC, the Taiwanese foundry that takes those machines and turns sand into the brains of the modern world. Lithography and fabrication. The printer and the press. That is where the cameras point.

But there is a third actor in this drama, one that almost never makes the highlight reel, and yet sits at arguably the most consequential checkpoint of all. Before a single chip is allowed to leave a factory and find its way into an iPhone, a Tesla, or a $30,000 Nvidia AI accelerator, it must pass through a machine that asks one ruthless, binary question: does this thing actually work? That machine, more often than not, is built by Teradyne.

If ASML creates the press and TSMC runs it, Teradyne is the gatekeeper standing at the factory door, holding a clipboard, deciding which chips live and which chips die. Every transistor on a die can be perfect in theory and still fail in silicon. Automated Test Equipment, or ATE, is the industry's lie detector—and Teradyne has spent six decades making it.

This is a company that almost no consumer has heard of, trading under the ticker TER on the NASDAQ, that quietly built itself into a roughly $50 billion enterprise.1 Alongside Japan's 株式会社アドバンテスト Advantest Corporation, Teradyne occupies one half of one of the most durable and profitable duopolies in all of technology—a market structure so rational that gross margins sit comfortably in the high-fifties to low-sixties, year after year.1

And here is the modern twist that makes this story irresistible. Teradyne is using the enormous, if lumpy, cash flows from that mature testing fortress to fund a second act: a bet on collaborative robotics and what the industry now calls "Physical AI"—the integration of intelligence, sensing, and autonomous movement into the industrial shop floor.

So here is our roadmap. We start in a tiny loft above a Boston hot dog stand, where two MIT classmates who met by alphabetical accident decided to industrialize the act of testing. We trace the company's escape from low-margin commodity hardware into its pure-play destiny. We dissect an M&A playbook that contains both spectacular home runs and a half-billion-dollar lesson in humility. We crack open the engineering reality of the "AI Complexity Wall." And we finish with the war-game: the powers, the forces, and the bull and bear cases that will define the next decade. Let's dig in.

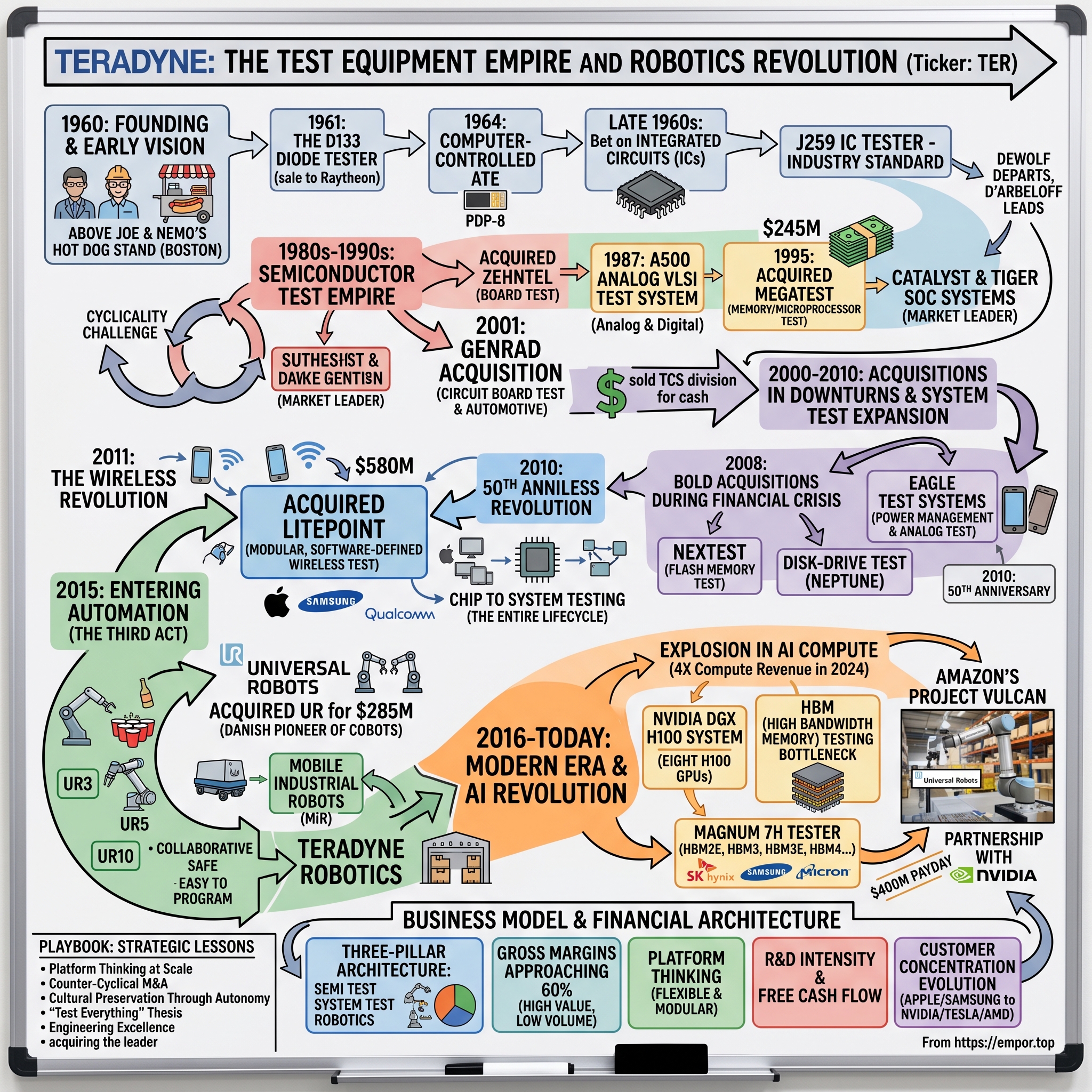

II. MIT, Alphabetical Luck, and the Hot Dog Stand (1960–1971)

Picture a crowded ROTC classroom at the Massachusetts Institute of Technology in the late 1940s. The instructor, doing what instructors have always done, lines the cadets up alphabetically. And so it happened that a young man named Alexander d'Arbeloff found himself standing next to a young man named Nick DeWolf. D and D. Two letters apart in the alphabet, and from that arbitrary adjacency would eventually spring a company that touches nearly every electronic device on Earth.2

The two could hardly have been more different in temperament, and that difference was the point. DeWolf was the wild engineering genius—restless, prolific, allergic to convention. d'Arbeloff, born in France to Russian émigré parents, was the strategist and businessman, the one who thought in terms of markets, capital, and the long game.2 One man would invent the machines; the other would build the enterprise. It is a pairing that recurs throughout the history of technology, from Hewlett and Packard to Jobs and Wozniak, and it almost always works for the same reason: the dreamer needs an adult, and the adult needs a dreamer.

On September 1, 1960, they founded Teradyne. The headquarters were the stuff of startup mythology before startup mythology was a genre: a cramped loft rented above Joe & Nemo's, a bustling hot dog stand in downtown Boston.3 They raised roughly $200,000 in seed money—some from people they knew, and crucially some from American Research and Development, the pioneering venture firm run by the legendary General Georges Doriot, the man often called the father of venture capital.3 Before there was Sand Hill Road, there was a hot dog stand in Boston and a French general's checkbook.

Why "Teradyne"? This is where DeWolf's mind announces itself. He combined "tera," the metric prefix for $10^{12}$, with "dyne," a unit of physical force. One trillion dynes of force. DeWolf liked to describe what that quantity of force actually felt like in the real world: it was, he said, roughly the effort of rolling a 15,000-ton boulder uphill.4 It was a name chosen not for marketing focus groups but for the sheer audacity of the image. These were men who wanted their company to feel like a force of nature.

The actual insight behind the business was deceptively simple and enormously valuable. In the late 1950s and early 1960s, testing electronic components was a slow, delicate, laboratory affair—precision instruments operated by skilled technicians, one component at a time, in conditions closer to a chemistry lab than a factory. DeWolf and d'Arbeloff understood that the coming explosion in transistors and diodes would require something completely different: rugged, fast, automated machines that could live on a noisy, dirty factory floor and test thousands of parts an hour without flinching. They were going to industrialize test.

Their first product, sold in 1961, was a logic-controlled go/no-go diode tester, and their first customer was Raytheon.3 A go/no-go tester does exactly what it sounds like—it makes a fast, binary judgment on each part. But the breakthrough that truly established the company came mid-decade. Teradyne began developing a computer-controlled transistor tester around 1963, and then turned its attention to the integrated circuit. In the mid-1960s, the company introduced the J259, the world's first computer-operated integrated circuit tester.4 Across his eleven years running the company, DeWolf is credited with designing more than 300 distinct test systems—an almost absurd rate of invention.4

Why did the J259 matter so much? Because the integrated circuit was about to remake civilization, and every single one of those circuits needed to be verified. By being first to automate IC testing under computer control, Teradyne planted its flag at the exact chokepoint where the semiconductor revolution would have to pass. It became the hardware gatekeeper of the silicon age before most people even understood there was an age coming.

Then, in 1971, the partnership reached its natural and amicable end. DeWolf—the boulder-roller, the inventor of 300 machines—walked away from the company at its commercial inflection point and decamped to Aspen, Colorado, where he would spend the rest of his life as a photographer and a fixture of the town's intellectual life.4 He left the keys to d'Arbeloff. And this is the quietly profound moment in Teradyne's early history: the visionary engineer handed the company to the strategist at precisely the moment when the challenge shifted from inventing test machines to scaling a global enterprise that sold them. The rugged, engineering-first culture DeWolf built would now be channeled through d'Arbeloff's commercial discipline. For investors, that founder-to-operator handoff is the under-appreciated reason the company survived its own genius. It is one thing to invent the future in a loft; it is another to build a multi-decade institution around it. The next forty years would test whether Teradyne could do the harder second thing.

III. The Pure-Play Pivot & The Smartphone Explosion (2005–2006)

Fast-forward four decades, and Teradyne had a problem that afflicts many successful industrial companies: it had become a bit of everything. By the early 2000s, the company that had been founded to test semiconductors had sprawled into a diversified industrial conglomerate. The most stubborn drag on the business was a division called Connection Systems—a maker of high-speed connectors, printed circuit boards, and backplane interconnect systems based in Nashua, New Hampshire.5

Connection Systems was not a bad business in the abstract. It was simply the wrong business for what Teradyne wanted to become. Connectors and backplanes are capital-intensive, commodity-adjacent products fought over on price. In 2004, the division accounted for fully 23% of Teradyne's revenue—nearly a quarter of the company—but it diluted margins and consumed capital that the high-value test business desperately wanted.5 It was a classic conglomerate trap: a sprawling revenue base that flattered the top line while strangling the company's identity and its returns.

So in October 2005, management made the decision that would define the modern company. Teradyne agreed to sell Connection Systems to Amphenol Corporation for $390 million in cash, with the deal closing on December 1 of that year.5 In one stroke, the company shed nearly a quarter of its revenue—and chose, deliberately, to become smaller, sharper, and more profitable. CEO Michael Bradley framed it plainly: the sale would sharpen Teradyne's focus on its core test businesses and free up financial flexibility to grow them.5

This is the moment Teradyne became a "pure-play"—a company that does one thing, the testing of semiconductors, and does it better than almost anyone. For long-term investors, the lesson here is one of the most important in all of capital allocation: subtraction can create more value than addition. Walking away from a quarter of your revenue takes more conviction than acquiring it. Teradyne traded breadth for depth, and the market would reward that focus for the next twenty years.

But focus alone is not a strategy; you have to focus on the right thing at the right moment. And here Teradyne's timing was extraordinary. As the company was streamlining itself into a dedicated test champion, it was simultaneously developing the platform that would carry it through the coming decade: the UltraFLEX. Launched in the mid-2000s, UltraFLEX was a modular, highly scalable test platform engineered specifically for the testing of System-on-Chip, or SoC, devices.

What is an SoC, and why does it matter? In plain terms, an SoC is a single piece of silicon that integrates many functions that used to live on separate chips—the processor, the graphics, the memory controllers, the radio, the power management—all packed onto one die. It is the architecture of the smartphone. And testing an SoC is exponentially harder than testing a simple logic chip, because the tester has to exercise dozens of different functional blocks, analog and digital, high-speed and low-speed, all on one device.

Then, in 2007, the iPhone arrived, and the world tilted on its axis. The smartphone era unleashed a tidal wave of demand for exactly the kind of densely integrated, multi-functional mobile processors that the UltraFLEX was built to test—the Apple A-series chips, the Qualcomm Snapdragons, and the long tail of mobile silicon that followed. Each new generation of phone packed more functions onto its primary chip, which meant more to test, which meant more demand for high-end testers. Teradyne had, by a combination of foresight and luck, positioned its flagship product directly in the path of the largest consumer electronics wave in human history. UltraFLEX became the industry gold standard for SoC test.

The pure-play pivot and the smartphone boom together transformed Teradyne from a diversified industrial company into the premium gatekeeper of the mobile revolution. But premium positions attract challengers, and downturns expose the weak. The company's next defining moment would come not from a product launch, but from how it behaved when the entire industry was on fire.

IV. The Great Financial Crisis and the Duopoly Consolidation (2008)

In 2008, the global financial system was seizing up, credit was evaporating, and the semiconductor industry—always among the most violently cyclical corners of the economy—was tipping into one of its sharpest down-cycles in memory. Capital equipment orders cratered. Across the ATE industry, the standard playbook was being executed: retrench, cut, conserve cash, survive.

Teradyne did the opposite. While its competitors hunkered down, Teradyne went shopping.

The logic was as cold as it was correct: the best time to buy is when everyone else is forced to sell. Asset prices were depressed, rivals were wounded, and Teradyne had the balance sheet and the nerve to act. In a single year, it made two acquisitions that would reshape the competitive landscape for a generation.

The first was Nextest Systems, which Teradyne acquired in a deal that closed in January 2008, paying $20.00 per share in cash for a total of roughly $325 million.12 Nextest was a specialist in testing flash memory—the non-volatile storage that was beginning to fill every digital camera, music player, and, soon, every smartphone. With one acquisition, Teradyne bought itself an immediate and dominant position in a fast-growing test segment it had previously underserved.

The second came later that same year. In November 2008, in the very teeth of the crisis, Teradyne agreed to acquire Eagle Test Systems for $15.65 per share, a deal valued at roughly $360 million.13 Eagle was a leader in high-volume analog and mixed-signal test—the testing of the chips that bridge the digital and physical worlds, handling power, sensors, and signals. This broadened Teradyne's reach into segments where it had been comparatively thin.

Step back and look at what just happened. In the worst year for the global economy since the Great Depression, while rivals were laying off engineers and pulling in their horns, Teradyne deployed close to $700 million to absorb two of its struggling competitors and consolidate the fragmented ATE landscape. This is counter-cyclical capital allocation in its purest form, and it is the single trait that most distinguishes great industrial operators from merely good ones.

The strategic consequence was profound. The ATE market had historically been a crowded, fragmented, brutally competitive arena—the kind of market where too many players chase too few orders and periodically destroy each other in price wars during downturns. The 2008 consolidation, with Teradyne mopping up rivals on its side and 株式会社アドバンテスト Advantest Corporation consolidating on the Japanese side (Advantest would go on to absorb Verigy in 2011), collapsed that fragmented field into something far more stable: a global duopoly.

And a rational duopoly is a beautiful thing if you happen to be one of the two. When two players control a market and both understand that mutually assured price destruction benefits no one, competition shifts away from price and toward technology and customer lock-in. The result, structurally, is durable pricing power. It is no accident that in the modern era Teradyne's gross margins sit consistently around the high-fifties to low-sixties percent.1 Those margins are not a quirk of any single year; they are the financial signature of a market that stopped fighting price wars and started competing on engineering. The crisis that broke weaker companies handed Teradyne the structure that would underwrite its profitability for the next two decades.

That structural advantage would soon embolden the company to push beyond its core—and in doing so, to learn an expensive lesson about the difference between a good market and a good deal.

V. The Winner's Curse: LitePoint and Customer Concentration (2011–2017)

Not every chapter in this story is a triumph, and the honest ones never are. The LitePoint saga is Teradyne's cautionary tale—a textbook illustration of how even a disciplined acquirer can walk into the oldest trap in the M&A playbook.

The strategic thesis was sound, even attractive. By 2011, the world was going wireless. Wi-Fi, Bluetooth, and the early stirrings of advanced cellular were turning every device into a radio, and those radios needed to be tested—not at the bare-chip level, where Teradyne already dominated, but at the system and module level, closer to the finished product. In October 2011, Teradyne acquired LitePoint Corporation of Sunnyvale, California, for a total purchase price of $646 million, the bulk of it cash paid for LitePoint's stock plus contingent consideration tied to revenue targets.14 On paper, this was Teradyne extending its gatekeeper role from the silicon all the way out to the assembled wireless device.

The problem was not the market. The problem was the customer base. LitePoint's business, it turned out, was dangerously concentrated on a single, massive consumer electronics giant—a customer that in various years represented somewhere between 51% and 73% of the entire segment's annual sales. When one buyer is most of your business, you do not have a customer; you have a landlord. Economists call this a monopsony—a market with essentially one buyer—and it inverts the power dynamic that makes the core ATE duopoly so lucrative. In the test business, Teradyne held the pricing power. In the LitePoint business, the customer did.

The reckoning came in 2016. The giant customer did what large, sophisticated companies eventually do: it got better at testing. By achieving major operational efficiencies in its own production-test processes—getting more throughput out of each tester, squeezing more devices through the same equipment—it abruptly needed to buy far fewer testers. There was no acrimony, no lost contract, nothing dramatic. The customer simply became more efficient, and a business that depended on that customer's tester purchases fell off a cliff.

The financial wreckage was severe. In 2016, Teradyne took an impairment charge against the LitePoint acquisition totaling roughly $338 million—comprised of about $255 million in goodwill impairment and another $83 million in acquired intangible assets written down.15 In plain English, the company formally admitted that more than half of what it had paid for LitePoint just five years earlier had evaporated. The boulder had rolled back down the hill.

What is the lesson here, the one worth carrying into every future deal you ever analyze? It is the winner's curse, and it is among the most important concepts in capital allocation. When you pay a premium multiple for a business, you are implicitly paying for the durability of its cash flows. But a business whose cash flows rest on a single customer is not durable—it is contingent. The premium you pay assumes diversification and bargaining power that simply isn't there. Teradyne paid a full price for LitePoint's growth, and that growth turned out to be borrowed entirely from one customer's purchasing decisions. When the customer changed its mind, the value Teradyne had capitalized vanished.

The irony, which we will return to, is that customer concentration is not a problem unique to LitePoint. It is a structural feature of Teradyne's entire industry, where a handful of titans—Apple, TSMC, Nvidia, Samsung—drive an outsized share of demand. LitePoint was simply the most acute and painful expression of a risk that runs through the whole enterprise. The episode chastened management, and it sharpened a question that would dominate the next decade: how do you decouple your fortunes from the lumpy, concentrated, violently cyclical world of semiconductor capital equipment? The answer they reached for was robots.

VI. Sowing the Seeds of Robotics: The Collaborative Automation Engine (2015–Present)

To understand why a semiconductor test company went looking for robots, you have to feel the pain of the semiconductor cycle from the inside. Teradyne's core business is magnificent, but it is also maddeningly lumpy. When chipmakers are expanding capacity, orders surge; when they pause, orders evaporate. Revenue can swing violently from one year to the next based on decisions made in a handful of boardrooms in Taiwan, South Korea, and California. For a management team trying to invest steadily and reward shareholders predictably, that volatility is a curse.

What Teradyne wanted was a hedge—a secular, structurally growing business that marched to a different drummer than the semiconductor capital-equipment cycle. And in 2015, it found one in, of all places, Odense, Denmark.

The company was Universal Robots, and it had pioneered an entirely new category: the cobot, or collaborative robot. To grasp why this mattered, you have to understand what industrial robots had been for the previous half-century. Traditional factory robots are enormous, powerful, and dangerous—they live inside steel safety cages, bolted to the floor, programmed by specialists, and kept far away from human workers because a single mistimed swing of a robotic arm can be lethal. They are brilliant for a car plant building a million identical vehicles, and useless for a small workshop that needs to do twenty different tasks a week.

Universal Robots inverted that model. Its cobots were lightweight, inherently safe arms designed to work alongside humans without a cage—they sense contact and stop, they can be programmed by a factory worker dragging the arm through the desired motion rather than by a software engineer writing code, and they can be redeployed to a new task in an afternoon. They democratized automation, bringing it within reach of the small and medium-sized manufacturers who make up the long tail of global industry.

In May 2015, Teradyne agreed to acquire Universal Robots for $285 million in cash up front, plus a performance-based earn-out of up to $65 million tied to hitting growth targets.6 On the surface, the valuation looked eye-watering for an industrial hardware company. UR had generated about $38 million in revenue in 2014, which put the deal at roughly 7.5 times trailing sales and something like 53 times profit—the kind of multiple you associate with software, not robot arms.6

So was Teradyne overpaying? This is exactly the kind of question that separates a static valuation from a dynamic one. Because UR was not a steady-state business; it was growing revenue at roughly 70% year-over-year, and it already held something on the order of a 60% global market share in the nascent cobot category.6 When you buy a business compounding at 70%, the trailing multiple is almost meaningless—what matters is the multiple against the earnings the business will produce after you own it. And here the numbers vindicated the deal spectacularly. By 2018, UR's annual revenue had surged to $234 million.[^7] Measured against that figure, Teradyne's effective acquisition multiple had compressed from a frightening 7.5x to something closer to 1.2x to 1.5x trailing revenue. What looked expensive in 2015 looked, in hindsight, like one of the best industrial acquisitions of the decade. It was the anti-LitePoint: a diversified, fast-growing, category-defining business bought at a price that growth quickly rendered trivial.

Encouraged, Teradyne built outward. In 2018, it acquired Mobile Industrial Robots, also of Odense, Denmark, for $272 million.7 If Universal Robots made the arms, MiR made the legs: autonomous mobile robots, or AMRs, the self-navigating carts that move materials around a warehouse or factory floor without the fixed tracks or guide-wires of older systems. Together, UR and MiR gave Teradyne a credible, two-pronged franchise in the fast-growing world of flexible factory automation—the arm that does the task and the robot that moves the goods.

Now, a crucial dose of perspective, because it is easy to get carried away with the robotics story. For all its strategic appeal, Teradyne Robotics remains the smaller sibling. In 2025, the robotics segment generated roughly $319 million of Teradyne's $3.19 billion in total revenue—about 10% of the company.10 This is not, today, the engine that pays the bills. The semiconductor test business does that.

So why care about a segment that is one-tenth of the company? Because its value lies less in its current revenue than in its optionality. Robotics is Teradyne's call option on the industrial future—specifically on the migration toward "Physical AI," the fusion of advanced sensing, machine learning, and autonomous path-planning that promises to make robots not just programmable but genuinely adaptive. Through partnerships with larger technology players, Teradyne is positioning its cobots and AMRs as the physical endpoints where artificial intelligence meets the shop floor. If that future arrives, a 10% segment could become something far larger. If it doesn't, the downside is contained. That asymmetry—limited downside, large potential upside—is precisely what a well-constructed strategic option looks like. For now, though, the cash that funds the option, and nearly all the profit, comes from one place. It is time to go there.

VII. The Core Engine: Inside the Semiconductor Testing Duopoly Today

Strip away the robotics narrative and the wireless detours, and you arrive at the beating heart of Teradyne: the semiconductor test business. In 2025, this single segment generated roughly $2.52 billion of the company's $3.19 billion in revenue—about 79% of the top line—and an even larger share of operating profit.10 When you own Teradyne stock, you are first and foremost an owner of this business. Everything else is a satellite orbiting it.

The competitive landscape, as we've established, is a duopoly. But it is a duopoly with an unusual texture, because the two players do not split the market evenly—they each dominate different territories. Across the total ATE market, 株式会社アドバンテスト Advantest Corporation holds the larger overall share, on the order of 58%, with Teradyne commanding roughly 30% to 40%.1 But that headline figure conceals two very different battles being fought in two very different rooms.

The first room is SoC test—the testing of the complex System-on-Chip processors we met earlier, a market worth on the order of $6.7 billion. This is Teradyne's fortress. Here the company is the undisputed powerhouse, capturing somewhere between 45% and 55% of the market with its flagship UltraFLEX and the newer UltraFLEXplus platforms.1 These are the testers favored by the designers of high-end mobile, automotive, and consumer processors—the chips that demand the broadest, most demanding test coverage. Advantest competes here with its V93000 platform, holding perhaps 35% to 45%, but in the SoC arena, Teradyne sets the pace.

The second room is memory test—a market of roughly $1.95 billion—and here the tables are reversed. Advantest is the dominant leader, with something like 60% to 70% share, and it enjoys a near-monopoly on the single most strategically important corner of the entire test market right now: the testing of high-bandwidth memory, or HBM.1 If you have followed the AI boom at all, you know that HBM—the stacked, ultra-fast memory (HBM3 and HBM3E) that sits beside the GPU in every AI accelerator—is one of the most supply-constrained and lucrative products in technology, produced principally by 삼성전자 Samsung Electronics and SK하이닉스 SK Hynix. Advantest has historically owned the testing of it. Teradyne, with perhaps 20% to 25% of the memory market, has been the clear number two.1

But the interesting story is the momentum. Teradyne has been clawing its way into memory test aggressively, and the AI build-out has handed it the opening. Demand for HBM testing has exploded so far beyond Advantest's capacity to serve it alone that the second supplier is winning meaningful new business, and Teradyne posted record memory test revenues entering 2026.10 In a duopoly, when demand outruns the leader's capacity, the laggard gets a seat at a table it could never have set itself.

Now, why is any of this such a good business? The answer lies in a concept worth dwelling on, because it is the single most important economic engine in this entire story: test intensity, and its modern accelerant, the "AI Complexity Wall."

Here is the intuition. For most of semiconductor history, chipmakers got richer by shrinking transistors—cramming more of them onto the same piece of silicon, generation after generation. But as the industry pushes to the bleeding edge of 3-nanometer and 2-nanometer manufacturing, and as it transitions away from single large chips toward "chiplets"—designs that stitch together multiple smaller dies into one package, stacked in complex 2.5D and 3D arrangements—testing gets harder at an exponential rate. More transistors means more things that can go wrong. More functional blocks means more tests to run. More interconnections between stacked dies means more failure points to hunt for. Each node shrink and each new packaging scheme lengthens the time each chip must spend sitting on a tester. That lengthening time-on-tester is "test intensity," and rising test intensity means chipmakers need to buy more testers to push the same volume of chips out the door.

Then there is the brutal arithmetic of the "cost of failure," which is what truly forces customers to pay up. Consider an advanced AI accelerator package. It might contain a large GPU die plus several stacks of expensive HBM, all assembled into a single module that can be worth $30,000 or more. Now imagine that one of the chiplets going into that package has a subtle defect that slips past testing. Once it is bonded into the finished package alongside thousands of dollars of other components, you cannot pull it back out. The single bad chiplet ruins the entire package. The expensive GPU, the pristine memory stacks—all of it, scrap.

This is the chipmaker's nightmare, and it is Teradyne's pricing power. As the value packed into each package soars, the financial consequence of letting a single bad die through becomes catastrophic. "Known good die"—the certainty that every chiplet entering a package is verified perfect—becomes non-negotiable. And there is no cheap way to get that certainty; you have to test, thoroughly, with the best equipment available. The cost of a Teradyne tester, however steep, is trivial next to the cost of scrapping a tray of $30,000 modules. That is why customers pay the premium, why the margins hold, and why the AI era is, structurally, a tailwind for the gatekeeper. The harder chips get to make, the more indispensable the company that certifies them becomes.

VIII. Modern Management & The Technoprobe Masterstroke (2023–Present)

Every era of a company is stamped by the people running it, and the modern Teradyne is shaped by a leadership team built for the dual nature of the business—half cyclical semiconductor cash cow, half emerging robotics growth play. Rather than march through every CEO since d'Arbeloff, it's the current custodians who matter for understanding where the company goes from here.

At the top sits Gregory S. Smith, a Teradyne veteran who joined the company in 2006—the very year of the pure-play pivot—and rose through its ranks for nearly two decades before taking the chief executive's chair. What makes Smith unusually well-suited to this particular company is the breadth of his internal résumé. He served as President of the core Semiconductor Test division from 2017 to 2020, learning the cyclical, technically ferocious heart of the business from the inside. Then, from 2020 to 2023, he ran the Industrial Automation Group—the robotics side. Few executives anywhere have operated both halves of a company this structurally split. Smith has lived in both worlds, which is precisely the qualification needed to allocate capital between a mature cash engine and a speculative growth bet.

Smith's incentives are aligned with shareholders in the way modern governance prefers. As of mid-2026, he held roughly 120,470 shares, worth on the order of $51 million—a stake large enough that the stock price is not an abstraction to him. His compensation under the company's long-standing incentive plan (originally the 2006 plan, amended in 2025) is heavily performance-weighted, tied directly to metrics like two-year rolling revenue growth and non-GAAP profitability, so that he is paid for sustained results rather than a single good quarter. And under stock ownership guidelines refreshed in 2025, he is required to hold at least six times his base salary in Teradyne stock. The structure is designed to make the CEO think like an owner, because to a meaningful degree he is one.

The newest face in the C-suite is Michelle Turner, who became Chief Financial Officer effective in November 2025, succeeding the long-serving Sanjay Mehta, who had held the role since 2019 and who stayed on as an executive advisor to help manage the test-capacity expansion before a planned retirement.11 Turner's pedigree is notable: she arrived from the role of CFO at defense and aerospace giant L3Harris Technologies, and before that had held senior financial positions across a string of demanding industrial and technology organizations.[^13] The choice signals intent. Bringing in a CFO seasoned in the high-precision, program-driven discipline of the defense world suggests a board that wants rigorous financial control layered over the company's engineering culture as it scales through the AI cycle.

But the single sharpest strategic move of the Smith era is not a personnel decision—it's a deal, and it deserves to be understood in detail because it shows the company's competitive instincts at their best.

In November 2023, Teradyne and the Italian company Technoprobe S.p.A. announced a strategic agreement to co-develop advanced semiconductor test solutions, and in May 2024 they closed the transaction.8 The mechanics had two parts. First, Teradyne sold its own Device Interface Solutions business to Technoprobe for $85 million. Second, and far more significantly, Teradyne acquired a 10% equity stake in Technoprobe for roughly €385 million—a total investment of about $516 million when the full structure was counted—taking a board seat in the process.9

To see why this was a masterstroke rather than just a swap, you have to understand the humble but increasingly critical component at the center of it. When a tester checks a chip, it cannot touch the silicon directly. In between sits an interface—an exquisitely engineered board, studded with probe cards and contacts, that physically connects the wafer or device to the multimillion-dollar tester. For decades this interface was a relatively quiet, almost overlooked piece of the puzzle. But as chips move to advanced packaging and chiplet architectures with thousands upon thousands of fine, densely packed contacts, that interface board has become fiendishly complex—and a potential bottleneck. Technoprobe is one of the world's leaders in exactly this technology: probe cards.

By taking a deep equity stake in Technoprobe rather than trying to build or buy the capability outright, Teradyne accomplished something elegant. The two companies can now co-design the interface card and the tester in tandem, optimizing the whole signal path from silicon to instrument as a single integrated system rather than two products bolted together. That tight coupling is a competitive weapon. Rivals attempting to win advanced-packaging test business—including the rising Chinese challengers 北京华峰测控技术股份有限公司 Beijing Huafeng Test & Control Technology and 杭州长川科技股份有限公司 Hangzhou Changchuan Technology—must now match not just Teradyne's tester, but the seamlessly integrated tester-plus-interface stack that the Technoprobe alliance produces. It is vertical integration achieved through partnership rather than ownership: Teradyne gets the strategic alignment and the co-design without absorbing the full cost and risk of owning a probe-card manufacturer outright. For a company that once learned the hard way (LitePoint) about the perils of bolt-on acquisitions, the Technoprobe structure is the mature, capital-efficient evolution of its M&A philosophy.

With the management and the strategic chessboard laid out, we can now formalize what makes this business so defensible—and where the cracks might appear.

IX. Playbook: Hamilton's 7 Powers & Porter's 5 Forces

Let's run Teradyne through two of the most useful frameworks in business analysis, because the structure of its moat is what ultimately justifies—or undermines—the entire investment case. We'll start with Hamilton Helmer's 7 Powers, focusing on the three that matter most here.

The dominant power, towering above all the others, is switching costs. This is the load-bearing wall of the entire Teradyne edifice, so it's worth making concrete. When a chip designer or an OSAT (an Outsourced Semiconductor Assembly and Test provider) commits to Teradyne's UltraFLEX platform, they do not simply buy a machine. They build an entire world around it. They write millions of lines of proprietary test code—the programs that tell the tester exactly how to exercise each chip. They design custom hardware interfaces. They train hundreds of engineers in the platform's quirks and tools. They embed it into their production lines and their qualification flows. Years of accumulated institutional knowledge live inside that ecosystem. Now imagine a salesperson from Advantest walks in and offers a comparable V93000 at a lower price. To switch, the customer would have to rewrite all that code, redesign the interfaces, requalify their products, and retrain their people—a multi-year, multi-million-dollar undertaking with enormous execution risk and no guarantee of improvement. The friction is so immense that customers stay locked in for decades. This is why the duopoly is stable: the two players are not really competing for each other's installed base; they are competing for each new design socket, and once a socket is won, it tends to stay won. Switching costs are the reason a price war is irrational and the reason margins endure.

The second power is scale economies. Teradyne spends well north of $300 million annually on ATE research and development. That is the entry fee just to stay current with the bleeding edge of chip technology—and it is an entry fee that scales with a customer base large enough to amortize it. A would-be new entrant faces an impossible chicken-and-egg problem: they cannot justify the R&D without a large guaranteed customer base, and they cannot win a large customer base without first having spent the R&D to build a competitive, trusted platform. The incumbents' scale lets them spread that fixed cost across a deep revenue base; a newcomer would have to eat it raw. This is the moat that protects the duopoly from being disrupted by a well-funded startup.

The third, more modest power is a cornered resource: human capital. The engineers who can design and program mixed-signal and analog test—people who deeply understand both the physics of analog signals and the software architecture of test systems—are genuinely rare in the broader technology ecosystem. They are not minted in large numbers, and the firms that have accumulated them hold an advantage that is difficult to replicate quickly. It's a medium-strength power, but a real one.

Now Porter's Five Forces, which tell a complementary story about the industry's structure.

Rivalry among existing competitors is best described as moderate and, crucially, rational. Teradyne and Advantest compete ferociously on technology—on who has the faster, more capable, more cost-effective platform for the next node. But they rarely compete on price in the destructive way that fragmented industries do, precisely because the switching costs discussed above make stealing an entrenched customer nearly impossible. Why start a price war you cannot win? The two coexist, each dominant in its own stronghold.

The threat of new entrants is extremely low, for all the reasons scale and switching costs imply: insurmountable software ecosystems, dense patent thickets, and R&D requirements that no rational investor would fund without a guaranteed market. The Chinese challengers are worth watching, especially as China pushes for semiconductor self-sufficiency, but they remain years behind at the high end.

The threat of substitutes is essentially non-existent, and this is the cleanest part of the bull case. There is no alternative to testing. Every physical semiconductor must be verified before it ships, full stop. You cannot substitute a software service or a different business model for the physical act of confirming that a chip works. As long as the world makes chips, the world must test them.

The bargaining power of suppliers is low-to-medium. Teradyne outsources much of its actual manufacturing to contract manufacturers, which keeps it capital-light, but it does rely on specialized component makers and advanced PCB designers—a dependency that the Technoprobe alliance was partly designed to manage and turn to advantage.

And finally, the bargaining power of buyers is very high—and this is the genuine vulnerability sitting inside an otherwise fortress-like business. Teradyne's demand is concentrated among a small set of titans: Apple, TSMC, Nvidia, Samsung, and a handful of others. When a single customer can represent a large slice of demand, that customer has leverage. A decision by one of these giants to slow purchasing, push out orders, or extract pricing concessions can dent quarterly margins meaningfully. We saw the extreme version of this risk play out with LitePoint. The duopoly protects Teradyne from its competitors; it does not protect Teradyne from its customers. That tension—immense supplier-side power, immense buyer-side concentration—is the defining strategic dynamic of the company, and it frames the bull and bear debate perfectly.

X. Analysis & Bear vs. Bull Case

So where does all of this leave a long-term, fundamentals-focused investor? Let's war-game both sides honestly, because the truth of Teradyne is that the same facts can be read optimistically or pessimistically depending on your view of the AI cycle and the company's execution.

The bull case begins and ends with the AI Complexity Wall. If you believe that chips are getting structurally harder to test—that the march to 2-nanometer nodes, the proliferation of chiplets, and the arrival of co-packaged optics are permanently increasing test intensity—then Teradyne is riding a secular tailwind, not just a cyclical one. More test time per chip means more testers per wafer of output, which means a rising demand floor that compounds with every node transition. This is the difference between a company whose fortunes merely rise and fall with the semiconductor cycle and one whose baseline keeps ratcheting upward regardless.

The second pillar of the bull case is HBM market-share expansion. Teradyne enters this fight as the underdog to Advantest in memory test, but the AI boom has created more HBM demand than the leader can satisfy, and Teradyne's record memory-test revenues entering 2026 suggest it is converting that opening into durable share gains.10 Every point of memory share it takes from Advantest is incremental revenue in the highest-growth corner of the entire market.

The third pillar is robotics optionality. If Universal Robots and MiR reach genuine scale and the "Physical AI" thesis plays out, the robotics segment could transform from a roughly 10% revenue contributor into a high-margin, high-growth franchise that re-rates the whole company and finally delivers the non-cyclical hedge management has chased for a decade.

The bear case is equally coherent, and it starts with the cyclicality the bulls want to wish away. The AI capital-expenditure boom is real, but it is also a boom—and booms have air pockets. If the hyperscalers digesting their massive AI infrastructure investments pause to absorb capacity, or if AI GPU deployment hits a temporary plateau, high-end ATE demand could fall off sharply and abruptly. Teradyne's revenue is geared to the most volatile part of the most volatile industry. The 2008 down-cycle and countless others are reminders that this business does not move in a straight line.

The second bear argument is "LitePoint Redux"—the customer-concentration risk we've traced throughout this story. The same handful of giant customers that drive Teradyne's growth could just as easily drive a painful contraction. Losing a major mobile socket to Advantest, or watching a primary customer optimize its own test times the way LitePoint's giant customer did in 2016, would hit revenue hard and fast. Concentration cuts both ways, and it has cut Teradyne badly before.

The third bear concern is robotics stagnation. The hedge has not yet proven itself. Industrial automation has had stretches of sluggishness, and if the robotics division remains stuck around a 10% revenue contribution without achieving meaningful, sustained operating profitability, then the bull's optionality argument collapses into a cash-consuming distraction. Optionality only has value if the option eventually pays off, and that is not yet certain.

How does a disciplined investor cut through this? By watching the right handful of metrics rather than the noise. Three KPIs matter most.

First, test intensity and tester utilization trends—essentially, the average time each chip spends on a tester as nodes advance. This is the single best leading indicator of whether the structural-tailwind thesis is real. Rising test intensity validates the entire bull case; flat or falling intensity undermines it.

Second, SoC and memory market share versus Advantest, with particular attention to Teradyne's wins in the high-growth HBM sockets. This is the scoreboard for the competitive battle. Holding the SoC fortress while gaining memory share is exactly what success looks like; losing ground in either is the warning sign.

Third, robotics segment operating margins. The question for this segment is no longer growth for its own sake—it is profitability. The metric to watch is whether Universal Robots and MiR are transitioning from cash-burning growth plays into genuinely profitable cash generators. Margins, not revenue, will tell you whether the option is maturing or stagnating.

Track those three, and you will understand Teradyne's trajectory better than any single quarter's headline number could tell you.

XI. Epilogue & Outro

It is worth pausing, at the end, on the sheer improbability of the arc. A company that began in 1960 in a rented loft above a Boston hot dog stand, capitalized with $200,000 and a name meaning a trillion dynes of force, has become a critical, roughly $50 billion-plus pillar of the modern technological order—the silent gatekeeper that decides which of the world's chips are fit to power the AI era.116

Three threads run through the whole story, and they are the takeaways worth carrying away.

The first is the power of transformation—the deliberate, disciplined evolution from a diversified hardware commodity player into a high-margin systems gatekeeper. The 2005 decision to sell off a quarter of the company's revenue in pursuit of focus was the inflection point, and it is a permanent reminder that in capital allocation, what you choose not to do often matters more than what you do.

The second is the strategic resilience of a rational, consolidated duopoly. The counter-cyclical consolidation of 2008 transformed a brutal, fragmented, price-warring industry into a stable two-player structure where competition flows through technology and switching costs rather than destructive discounting. That structure is the engine of Teradyne's enduring, high-fifties-to-low-sixties gross margins, and it is the single most important reason the business is worth owning over the long run.

The third is the central, unresolved tension of the modern company: the challenge of using a mature, fabulously profitable, but violently cyclical cash cow to fund a brand-new secular growth engine. The robotics bet is, in essence, an attempt to buy a smoother future with the proceeds of a bumpy present. Whether that bet pays off—whether Physical AI lifts robotics into a true second pillar, or whether it remains a perpetual 10% appendage—is the open question that will define Teradyne's next decade.

From the hot dog stand to the AI accelerator, Teradyne has spent sixty-six years answering one deceptively simple question, over and over, billions of times a day: does this work? As long as the world keeps making chips—and especially as those chips become almost unimaginably complex—someone has to stand at the gate and check. That, in the end, is the business.

References

-

Teradyne, Inc. Annual Report (Form 10-K) for the Fiscal Year Ended December 31, 2024 — SEC, 2025-02-20 ↩↩↩↩↩↩↩↩

-

Teradyne to Sell Connection Systems — Photonics Spectra, 2005-10 ↩↩↩↩

-

Teradyne to Acquire Universal Robots for $285 Million — Reuters, 2015-05-13 ↩↩↩

-

Mobile Industrial Robots (MiR) Strategic Overview — Mobile Industrial Robots ↩

-

Teradyne and Technoprobe Announce Strategic Agreement to Co-Develop Advanced Semiconductor Test Solutions — Teradyne News, 2023-11-07 ↩

-

Technoprobe and Teradyne — Transaction Closing Press Release — Technoprobe S.p.A., 2024-05-27 ↩

-

Teradyne Full Year Revenue Reaches $3.19 Billion in 2025 — AlphaStreet, 2026-01 ↩↩↩↩

-

Teradyne Announces Chief Financial Officer Transition — Teradyne Investor Relations, 2025 ↩

-

Teradyne Completes Acquisition of Nextest Systems (Form 8-K) — SEC, 2008 ↩

-

More ATE consolidation: Teradyne to buy Eagle Test — EE Times, 2008-09-16 ↩

-

Teradyne Completes Acquisition of LitePoint Corporation (Form 8-K) — SEC, 2011-10 ↩

-

Teradyne, Inc. Annual Report (Form 10-K) for Fiscal Year 2016 — SEC, 2017 ↩

-

SEC EDGAR Profile for Teradyne, Inc. (CIK: 0000097210) — U.S. Securities and Exchange Commission ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube