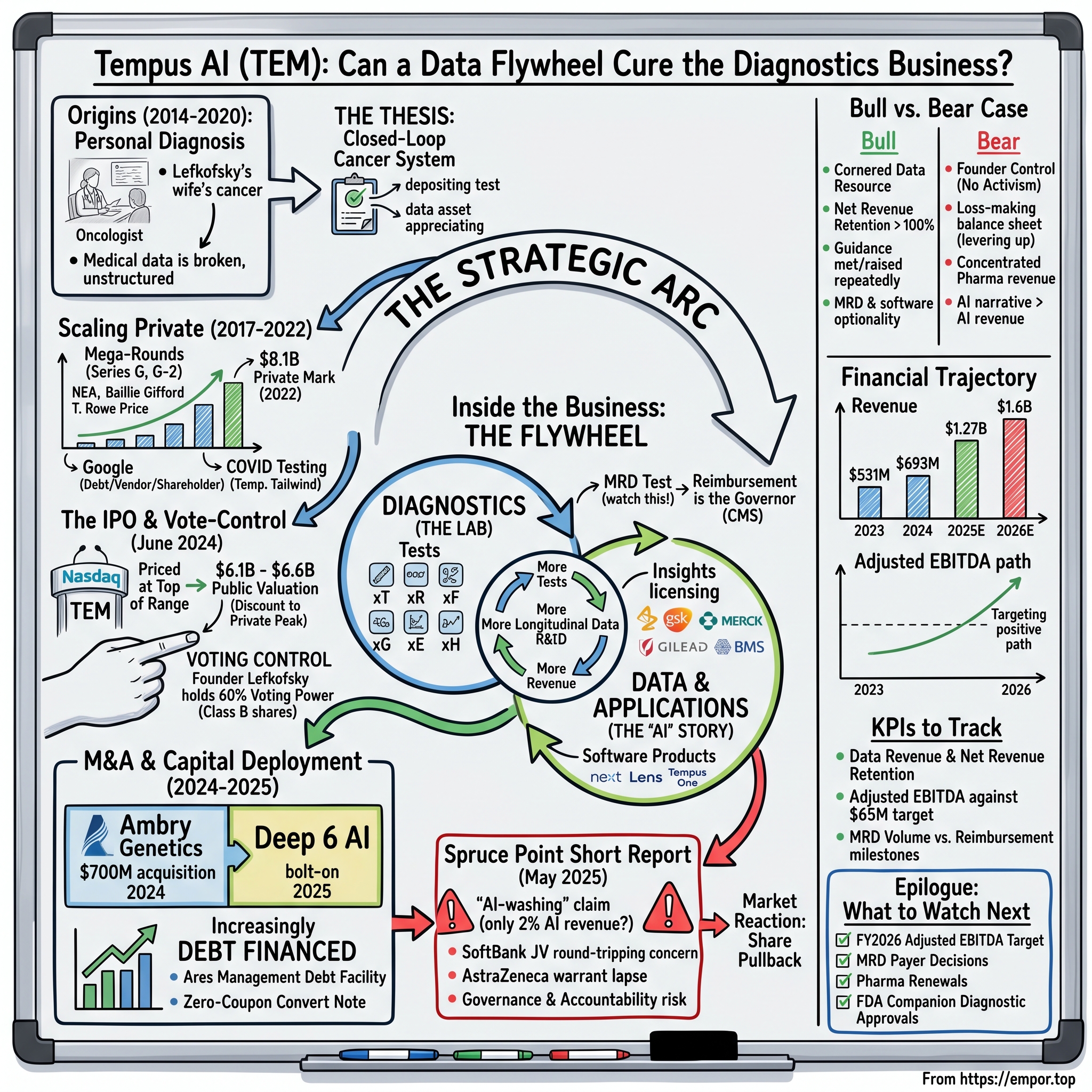

Tempus AI: Can a Data Flywheel Cure the Diagnostics Business?

I. Introduction & Episode Roadmap

Picture a company that stands on a Nasdaq podium in June 2024 wearing the letters "AI" not just in its logo but in its legal name — a name it had adopted only eighteen months earlier, swapping "Tempus Labs" for "Tempus AI, Inc." right before it went out to raise money from public investors.1 Now picture, less than a year later, a short seller standing up with a 100-plus-page report and a simple, uncomfortable claim: that in 2024, of the roughly $693 million Tempus booked in revenue, only about $12.4 million — barely 2% — came from products the company itself categorized as AI applications.9 The rest, the short seller argued, was a lab-testing business. A good one, maybe. A growing one, certainly. But a lab.

That tension — between the story a company tells about itself and the machinery that actually generates its cash — is the spine of this episode. Tempus AI (NASDAQ: TEM) is one of the most interesting Rorschach tests in public healthcare markets. Depending on where you stand, it is either a genuinely differentiated data company that happens to run labs to feed a proprietary dataset, or it is a capital-intensive genomics-testing business that borrowed the era's most valuable narrative to earn a richer multiple. Both readings can point at the same 10-K and find support.

So here is the core question we will keep returning to: is Tempus building a durable, hard-to-replicate data moat in oncology that pharmaceutical companies will pay to license indefinitely — or is it selling tests and calling it software?

To get to a fair answer, we will walk the whole arc. We start with the founding story — a cancer diagnosis inside the founder's own family that exposed how broken medical data really is. We trace the mega private financing rounds that pushed the valuation to $8.1 billion before a share ever traded publicly, and the June 2024 IPO that priced the whole thing lower. We map the dual-class control structure that hands the founder the steering wheel more or less permanently. We take apart the two-segment business and the "flywheel" that is supposed to connect them. We war-game the competitive field — Guardant, Foundation Medicine, Natera, Caris, Exact Sciences, and the real-world-data giants circling the same pharma budgets. We examine the Ambry Genetics acquisition and the shift toward debt financing. We put the pharma data-licensing deals under a magnifying glass — AstraZeneca, GSK, Merck, Gilead, Bristol Myers Squibb, and the SoftBank joint venture the short seller flagged. We work through the Spruce Point short report as a credibility stress test. We assess management incentives and track record, the financial trajectory and the still-unmet path to profitability, and finally the bull-versus-bear case, the KPIs worth tracking, and the lessons the whole saga teaches.

Throughout, the posture is neutral. This is not a shareholder letter and not a hit piece. When management says Tempus will win, we ask what evidence backs the claim and what would prove it wrong. Let's begin where the company began — not in a boardroom, but in an oncologist's office.

II. Origins: A Cancer Diagnosis Becomes a Company (2014–2020)

To understand Tempus, you first have to understand Eric Lefkofsky — because more than most companies, this one is an extension of one man's biography, his ambitions, and the baggage Wall Street attaches to his name.

Lefkofsky is a serial Chicago entrepreneur whose résumé reads like a highlight reel and a cautionary tale stacked on top of each other. In the late 1990s he co-founded Starbelly.com, a promotional-products dot-com that was sold into HA-LO Industries — which subsequently filed for bankruptcy, an early lesson in how quickly a hot internet asset can turn to ash. He went on to co-found InnerWorkings, a print-procurement company, and Echo Global Logistics, a freight-brokerage business. And then came the one everyone remembers: Groupon, the daily-deals juggernaut he co-founded that became, briefly, one of the fastest-growing companies in history — and then, after its 2011 IPO, restated its financials in a stumble that permanently colored how skeptical investors read anything with his name on it.

Hold that pattern in mind, because it becomes load-bearing later in this story. For now, the point is simpler: by the mid-2010s, Lefkofsky was a wealthy, battle-tested, pattern-matching entrepreneur who had built businesses by spotting inefficient markets drowning in unstructured information and imposing software on them. That is exactly the lens he brought to what happened next.

In 2014, Lefkofsky's wife, Liz, was diagnosed with breast cancer. As he tells the origin story, what shocked him during her treatment was not the science of oncology but the state of its data. Her clinical records, her genomic information, her molecular profile, her treatment history — almost none of it was structured, linked, or usable by the physicians actually making decisions at the point of care. In an era when Amazon could recommend a book and Google could route traffic in real time, a cancer patient's own doctors were flying largely blind, working off fragments in incompatible systems. To a man who had spent a career productizing messy information, that gap looked less like a tragedy and more like a business.

Tempus Labs was founded in Chicago in 2015 on a deceptively simple thesis: build a "closed-loop" system for cancer. Sequence tumors in-house. Feed the structured molecular and clinical results back to oncologists at the point of care, so the diagnostics actually change treatment decisions. And — this is the crucial part — aggregate all of that de-identified, longitudinal, multimodal data into a dataset so large and so richly linked that pharmaceutical and biotech companies would pay to license it for drug discovery and development.

That last move is what separates Tempus, at least conceptually, from a plain-vanilla testing lab. A lab sells a test and moves on. Tempus wanted the test to be the beginning of a relationship — the entry point that generates data, and the data to be the asset that compounds. The entire architecture of the company today, the two segments and the flywheel connecting them, exists to serve that original idea.

It is worth pausing on why this "closed-loop" framing is genuinely clever, because it is the intellectual core of everything Tempus later built. Most diagnostics companies think of a test as a transaction: sample in, report out, invoice sent. Lefkofsky's insight was to treat each test as a deposit into a growing account. The molecular result helps the patient today, yes — but the de-identified, structured record of that result, linked over time to how the patient actually responded to treatment, becomes an asset that appreciates. A single tumor sequence is a data point; ten years of sequences linked to outcomes is a research instrument. That is the difference between running a lab and building a dataset, and it is why Tempus insists it is not just another testing company. Whether the market should pay a software multiple for that distinction is the whole debate — but the distinction itself is real, and it was baked in from the founding.

One small but telling detail sits at the seam of this history: in January 2023, the company changed its name from Tempus Labs to Tempus AI, Inc.1 It was still more than a year before it would sell shares to the public, but the rebrand is worth noting not as a technical footnote but as a positioning decision — a company choosing, ahead of an AI-driven public listing, to lead with the two letters the market was rewarding most. Whether that name describes the business or dresses it up is a question we will keep testing. To fund the closed-loop vision, though, Lefkofsky first had to raise an extraordinary amount of private money — and the marks he raised at tell their own story.

III. Scaling Private: Mega-Rounds, COVID, and an $8.1B Mark (2017–2022)

There is a particular kind of company that late-stage growth investors fell in love with during the 2017–2021 bull market: pre-profit, story-rich, founder-led, and hungry for capital to buy its way to scale before anyone did the same. Tempus was a textbook case, and the marquee names lined up.

Through a rapid succession of private rounds, Tempus pulled in capital from New Enterprise Associates, Revolution Growth (Steve Case's firm), T. Rowe Price, Baillie Gifford, and Novo Holdings, among others — a roster that blended crossover public-market funds with deep healthcare specialists. The momentum crested with a $200 million Series G in December 2020 that valued the company at roughly $5 billion post-money. For a company barely five years old, still deeply unprofitable, that was a heady mark set in the frothiest financing environment in a generation.

Then the froth started to leak out, and Tempus's own cap table showed it before the public ever got a vote. In 2022, the company raised another $200 million — the Series G-2 — at an $8.1 billion post-money valuation. On its face, $8.1 billion sounds like a triumph: the valuation had jumped from $5 billion. But look closer at the structure and the timing. Enthusiasm for high-multiple, cash-burning healthcare names had already begun to cool as interest rates climbed through 2022, and the terms reflected caution. Alongside the equity, Tempus took on $250 million of convertible debt from Ares Management — the beginning of a reliance on structured and debt financing that becomes a recurring theme. The lesson for investors reading the tape: when a company starts topping up equity rounds with big slugs of convertible debt from credit shops, it is often a sign that pure equity appetite at the asking price is thinning.

Two other pieces of the private era deserve special attention because they resurface later. The first is Google's unusual, multi-hatted role. Google extended Tempus a convertible promissory note of roughly $330 million, structured so it could be drawn down against Google Cloud compute usage. Read that arrangement carefully: Google was simultaneously Tempus's infrastructure vendor (selling it cloud), its lender (holding a note), and, eventually, its shareholder (as the note converted into equity). That is a tidy arrangement for both sides, but it is exactly the kind of tightly interwoven commercial-and-financial relationship a skeptical analyst files away, because it blurs the line between an arm's-length customer relationship and a financing one.

The second is COVID-19. When the pandemic hit, Tempus — a company with sequencing labs, logistics, and reimbursement machinery already built — pivoted quickly into COVID testing. This was a genuinely useful bridge: it generated cash and exercised the lab infrastructure at scale during a period when the core oncology business was still ramping. Crucially, management did not let COVID testing become the company's identity; it was a temporary tailwind, not a pivot. But it did flatter the growth optics of the era, and it is worth remembering that some of the early revenue scale was pandemic-driven rather than structural.

By the eve of the IPO, cumulative private capital raised approached $1.5 billion — an enormous sum that tells you two things at once: investors were willing to bankroll the vision on a grand scale, and the vision required an enormous amount of capital to build. The right way to frame the June 2024 IPO, then, is as the first genuine public-market referendum on a story that private investors had already marked at $8.1 billion two years earlier. The question hanging over the roadshow was blunt: would the public pay up for the narrative, or mark it down?

IV. The IPO and the Vote-Control Question (June 2024)

The answer came on June 13, 2024, when Tempus priced its initial public offering at $37.00 per share — the top of its marketed range — selling 11.1 million Class A shares for gross proceeds of $410.7 million.3 Pricing at the top of the range is a signal of demand; a company that scrapes the bottom is a company nobody wanted, and Tempus was clearly wanted. The next morning, June 14, the stock did what hot IPOs are supposed to do: it popped, trading up as much as 15% intraday, before closing its first day around $40.25, up roughly 9%.45

But here is the number that mattered more than the pop. At its debut price, Tempus carried a market capitalization of roughly $6.1 to $6.6 billion — meaningfully below the $8.1 billion private mark from just two years earlier.4 In other words, even on a euphoric first-day pop, public investors were valuing the company at a discount to what the last private round had implied. The IPO "worked" in the sense that it got done at the top of the range and traded up, but it also quietly confirmed that public-market skepticism toward the story was real. The private-market peak had been a peak.

The pre-IPO investor roll call read like a who's-who of growth capital: SoftBank, Baillie Gifford, NEA, Novo Holdings, Franklin Templeton, T. Rowe Price, Revolution, and Google.5 That is validation of a sort — sophisticated money had committed. But it also meant the float was thin relative to a heavily concentrated, insider- and institution-dominated cap table, which matters enormously when you get to the governance structure.

And the governance structure is where every future chapter of this story has to be read. Tempus went public with a dual-class share arrangement in which Class A shares carry one vote each and Class B shares carry thirty votes each.1 Lefkofsky holds all of the outstanding Class B super-voting stock plus a substantial Class A position, which together give him roughly 60% of the combined voting power while owning a minority of the economic shares.1 Sit with what that means. A public shareholder buying TEM is buying into the economics of the business but essentially none of the control. There is no plausible path — no proxy fight, no activist campaign, no shareholder vote — by which outside investors can change the strategy, the board, or the CEO if they come to disagree with him. Regardless of performance, Lefkofsky cannot be outvoted.

Dual-class structures are common enough in founder-led tech that the market has partly normalized them, and there is a coherent argument for them: they let a founder pursue a long-term vision without being whipsawed by quarterly-minded shareholders. But they are not free. They remove the single most important external check on management — the ability of owners to fire the people running their company — and they concentrate key-person risk to an extreme degree. For a company whose founder carries the specific historical baggage we discussed, and whose most-scrutinized transactions involve related parties, the absence of any independent counterweight is not a footnote. It is a lens. Every subsequent decision — the Ambry acquisition, the response to the short report, the steady insider selling — has to be evaluated knowing that the person making them answers, functionally, to himself. With that lens in place, let's open the hood and look at what the business actually does.

V. Inside the Business: Two Segments, One Flywheel

Strip away the branding and Tempus is two businesses stapled together by a theory. Understanding how the two halves fit — and whether they genuinely reinforce each other or just coexist — is the single most important analytical task in evaluating this company.

The first business is Diagnostics (renamed from "Genomics" around the time the Ambry acquisition closed in 2025). This is the lab. It runs a portfolio of molecular tests, most of them known by their "x" nomenclature: xT and xR for tumor DNA and RNA profiling of solid cancers; xF for liquid biopsy (detecting tumor DNA circulating in a blood draw, so you don't always need to cut into a tumor); xG for hereditary and germline testing, the category deepened enormously by the Ambry acquisition; xE for whole-exome sequencing; and an upcoming xH for whole-genome sequencing. In plain terms, a physician sends Tempus a tumor sample or a tube of blood, and Tempus sends back a structured report on what mutations are driving that patient's cancer and which therapies or trials might match. It gets paid per test, largely by insurers and government payers.

The second business is Data and Applications (renamed from "Data and Services"). This is where the "AI company" identity lives. It has two parts. One is the licensing of de-identified, multimodal patient data — the aggregated exhaust of all those tests, linked to clinical outcomes — to pharmaceutical and biotech companies for drug R&D. The other is software: products like Lens (an analytics platform for researchers), Next (clinical decision support), and the Tempus One "copilot," an AI assistant meant to sit alongside physicians. This is the higher-margin, faster-growing, more "software-like" half.

Now the numbers, and what they reveal. In FY2024, Diagnostics/Genomics generated $451.7 million in revenue, up 24.4% year over year, while Data and Applications generated $241.6 million, up 44.6% — together making up the $693.4 million total.2 By the first quarter of 2026, Diagnostics had reached $261.1 million in a single quarter (up 34.7% year over year) against Data and Applications' $87.0 million (up 40.5%).15 Read those figures together and a clear picture emerges: the lab is roughly three-quarters of revenue and the larger absolute profit contributor, but the data business is growing faster and carries structurally higher margins. So the company's "AI" identity rests on the smaller, faster half — which is precisely the disconnect the short seller would later exploit.

Here is how the flywheel is supposed to work, in the company's own telling. More tests ordered means more longitudinal, outcome-linked data. A larger, more differentiated dataset — GSK has publicly described Tempus's dataset as roughly "34x larger than TCGA," a reference to The Cancer Genome Atlas, the standard public benchmark — becomes more valuable to pharma R&D.13 More value drives more licensing revenue, which funds more lab capacity, which drives more tests. Round and round. It is an elegant story, and if it works, it is a genuine compounding machine: the kind of self-reinforcing data advantage that is very hard for a competitor to replicate because you cannot buy years of linked longitudinal outcomes; you can only accumulate them.

But an elegant story is not evidence, and the outline's instruction is exactly right: test the flywheel, don't repeat it. Several facts complicate the clean version. The most important came straight from Lefkofsky on the Q1 2026 earnings call, where he described deliberately throttling his own sales force's access to the minimal residual disease (MRD) test — restraining demand — because Medicare and the MolDx program's reimbursement wasn't yet broad enough to make aggressive selling economic.15 That is a revealing admission. It says that for the newest, fastest-growing test categories, the binding constraint is not physician demand or data quality but reimbursement — the average selling price that payers will allow. In diagnostics, regulatory and payer milestones move economics more than ordering behavior does. The flywheel, in other words, has a governor on it called CMS.

To make the reimbursement point concrete for anyone who hasn't lived inside the diagnostics business: a lab can run a technically excellent test and still lose money on it if payers won't reimburse. In the United States, Medicare — through a program called MolDx that adjudicates molecular diagnostics — effectively sets the anchor price, and commercial insurers tend to follow. Until a test earns broad coverage, the lab either eats the cost or bills patients amounts they won't pay. So when Lefkofsky says he is holding his sales force back from selling MRD hard, he is not describing weak demand; he is describing a business decision to not sell a product aggressively before the economics of getting paid for it are settled. That is a rational move, but it also punctures the tidy version of the flywheel, in which more selling always means more data means more revenue. Here, more selling before reimbursement would just mean more uncompensated tests.

MRD is nonetheless the emerging growth vector worth watching. It is a test that looks for tiny amounts of residual cancer DNA circulating in the blood after treatment — a way to catch a recurrence months before it would show up on a scan — and the potential market is large because it applies across many cancer types and repeats over a patient's follow-up. Tempus reported MRD volumes up roughly 500% year over year to about 6,500 tests in Q1 2026.15 That is explosive growth, but off a tiny base; 6,500 tests is optionality, not yet an at-scale business. It is exactly the kind of number that can be true and impressive and still immaterial to this year's P&L — the sort of metric that belongs in the "watch this" column rather than the "this is working" column.

On the data side, the "Insights" licensing business showed year-over-year growth in the 44–69% range across 2025 into 2026, with total contract value (TCV) the company said exceeded $1.1 billion and a stated net revenue retention of 126%.1415 Those are strong figures — net revenue retention above 100% means existing pharma customers are spending more each year, the hallmark of a sticky, expanding relationship. But note the word "stated." TCV and net revenue retention are company-defined, non-GAAP metrics; there is no auditor certifying exactly how they are calculated, and TCV in particular can bundle multi-year commitments that may or may not fully convert to recognized revenue. They are worth tracking as directional signals, not accepting as audited fact. The healthiest way to hold this section: the two-segment architecture is real and the flywheel is a plausible mechanism, but the evidence that it compounds durably — rather than depending on a handful of big contracts and favorable reimbursement — is still being written. To judge that, you have to understand the industry Tempus competes in.

VI. Industry Structure and the Competitive Field

Oncology diagnostics is not one market; it is a value chain, and Tempus sits in the contested middle of it. Picture the chain running from the machines that read DNA down to the pharma companies that pay for insight, and you can see exactly who Tempus fights and who it depends on.

At the top sit the sequencing-platform makers, and here one name dominates: Illumina, the company whose sequencers are the picks-and-shovels of the entire genomics economy. Nearly every comprehensive genomic profiling lab, Tempus included, runs on Illumina hardware and consumables. That makes Illumina a concentrated supplier with real leverage — a classic Porter supplier-power problem. But the relationship got more interesting in 2025, when Illumina and Tempus struck a formal AI and data partnership, turning a pure vendor into something closer to a collaborator. This softens the supplier-power risk somewhat, but it also deepens Tempus's entanglement with a single upstream giant.

In the middle — Tempus's home turf — are the comprehensive genomic profiling and liquid-biopsy labs. The direct rivals here are Guardant Health, a liquid-biopsy pioneer whose flagship Guardant360 test carries an average selling price of roughly $3,000–$3,100, and Foundation Medicine, the Roche-owned incumbent that helped define tissue-based comprehensive genomic profiling. Adjacent to these are the hereditary and germline specialists — Ambry (now Tempus's own, more on that shortly) and GeneDx — and, in a related but distinct category, the cancer-screening players Exact Sciences (of Cologuard fame, which launched its Cancerguard multi-cancer early-detection test in 2025) and Natera.

Natera deserves a special callout because Tempus explicitly benchmarks its MRD ramp against it. Natera's Signatera MRD test blazed the reimbursement trail — securing Medicare coverage category by category, tumor type by tumor type — and in doing so became the pathfinder that proved MRD could be a real, reimbursed business. When Tempus talks about the reimbursement gating its own MRD test, Natera is the comparison it has in mind: the company that got there first and showed what "there" looks like.

Then there is the newest and most on-the-nose rival: Caris Life Sciences, a precision-oncology company that, like Tempus, pairs molecular profiling with an AI-and-data narrative — and which also went public, giving investors a direct, listed comparison for the "AI-driven diagnostics" thesis. NeoGenomics rounds out the testing field as a broad oncology-lab operator.

But the competition Tempus should worry about most may not be in diagnostics at all. It is in real-world data. The Data and Applications segment competes for pharma R&D dollars against a different set of giants: Flatiron Health (owned by Roche), IQVIA, and Datavant, all of which aggregate and sell real-world clinical data. This is the flank where the "cornered resource" thesis gets tested hardest, because pharma companies can — and increasingly do — build their own internal real-world-data capabilities, which is a substitute threat that grows as the tools commoditize.

Run the Porter's Five Forces on this and you get a nuanced picture. Barriers to entry are high — the capital intensity of building labs, the regulatory gauntlet, and above all the years it takes to accumulate a comparable longitudinal dataset all protect incumbents. Buyer power is moderate-to-high, but the buyers that matter most are payers and CMS, who set reimbursement and therefore cap pricing on the diagnostics side. Supplier power is concentrated in Illumina, softened by partnership. The substitute threat is real and rising, chiefly from pharma-internal real-world-data efforts and from cheaper testing alternatives. And rivalry is intense and consolidating — which is the direct strategic rationale for buying Ambry rather than competing with it.

Through Hamilton Helmer's 7 Powers lens, Tempus's most credible source of durable advantage is a cornered resource: a proprietary, longitudinal, multimodal oncology dataset that genuinely is hard to replicate, because you cannot compress the time it takes to accumulate linked outcomes. Reinforcing it, potentially, are early switching costs — as pharma R&D teams build workflows and models around Tempus's Lens platform, ripping them out gets costly. But "potentially" is the operative caveat. The honest test for both powers is evidence: are pharma contracts renewing and expanding? Are deal sizes growing? Is there exclusivity? A moat you assert is not a moat; a moat that shows up as rising net revenue retention and multi-year renewals is. We will hold the claim to that standard. And the clearest way Tempus has tried to widen its cornered resource is by buying more of it — which brings us to Ambry.

VII. M&A and Capital Deployment: The Ambry Genetics Bet

On November 4, 2024, alongside its third-quarter earnings, Tempus dropped its biggest strategic move as a public company: an agreement to acquire Ambry Genetics.6 The deal was structured as $375 million in cash plus $225 million in stock — a roughly $600 million headline figure that filings later reconciled to about $695.3 million in total consideration once all the accounting was done.67 It closed in the first quarter of 2025, and to finance it, Tempus increased its debt by $300 million through its facility with Ares Management.6

The strategic logic is coherent, which is worth saying plainly before poking at it. Ambry is a well-established hereditary and germline testing business — and crucially, it was already Tempus's primary reference lab in that category. Tempus was, in effect, buying a supplier it already depended on and folding a whole test category (inherited cancer-risk testing, the xG franchise) in-house. That is vertical integration that also expands the dataset: hereditary data is a complementary layer to the somatic tumor data Tempus already collected, thickening the multimodal record that feeds the licensing business. For a company whose entire thesis is "more linked data compounds," acquiring an adjacent data-generating asset is on-strategy rather than a diversification into something unrelated.

A month later, in March 2025, Tempus made a smaller, tuck-in acquisition: Deep 6 AI, an AI-powered clinical-trial-matching platform, for an undisclosed price.8 Deep 6's pitch was reach — it claimed connectivity across 750-plus provider sites and access to more than 30 million patient records for matching patients to trials.8 This was a capability bolt-on, not a scale deal: it plugs into the pharma-services side (helping fill clinical trials, a service pharma pays handsomely for) and, again, on-strategy. Together, Ambry and Deep 6 tell you what Tempus's M&A playbook looks like — buy adjacent capabilities and data that feed the core flywheel, rather than empire-building into unrelated categories.

So far, so disciplined. But there are two things a skeptical investor should press on. The first is valuation, and here honesty requires admitting the limits of the analysis: there are no clean public comps for the Ambry deal. Guardant, Natera, and Exact Sciences have not done comparably sized acquisitions recently, so there is no obvious yardstick to say whether ~$695 million for Ambry was cheap, fair, or rich. The right posture is to seek sell-side multiple estimates rather than assert a verdict — and to note that the absence of comps itself makes the deal harder to underwrite.

The second, and more important, is the financing pattern — because this is where capital allocation and governance intersect. The Ambry deal was debt-funded, not equity-funded. So was much of what followed: beyond the Ares increase, Tempus issued a further $726.5 million of debt in the third quarter of 2025, and in May 2026 priced a $400 million zero-coupon convertible note.17 For a company still posting GAAP net losses, a steady march up the leverage curve to fund acquisitions and growth is not automatically wrong — debt is cheaper than dilution, and a 0% convert is nearly free money if the stock cooperates — but it deserves scrutiny rather than a pass. There is a plausible read that the preference for debt over equity is partly about preserving Lefkofsky's voting percentage: issuing new Class A equity would dilute the economic base, whereas debt does not touch the control structure at all. Whether that read is correct or not, the fact stands that a loss-making company is increasingly funding itself with borrowed money, and rising leverage against continued losses is one of the first things a short seller circles. Which is a good segue, because the borrowed money and the acquisitions all exist to feed one thing: the pharma relationships that are supposed to justify the whole model.

VIII. The Pharma Data-Licensing Flywheel

If the diagnostics business is the engine, the pharma data-licensing deals are the reason anyone believes the car can eventually go fast without burning cash. This is where Tempus's cornered-resource thesis either proves out in hard contracts or reveals itself as a handful of concentrated bets. Let's go through the marquee relationships and, as the outline insists, hold each to a "verify, don't assume" standard.

Start with AstraZeneca, because it is the most instructive — and the most double-edged. In 2025, Tempus and AstraZeneca (together with Pathos AI) expanded a collaboration worth roughly $200 million over three years to build a multimodal oncology foundation model — essentially a large AI model trained on Tempus's data to help design and target cancer therapies.12 On its face, a $200 million commitment from one of the world's largest pharma companies is exactly the validation the flywheel needs. But there is a complicating detail that a promotional telling would bury: AstraZeneca separately held a warrant to buy roughly $100 million of Tempus stock at the IPO price — and let it lapse, unexercised. That is a genuinely ambiguous signal. A bull reads the $200 million data deal as AstraZeneca "doubling down." A bear reads the lapsed warrant as AstraZeneca declining to bet on the equity even as it buys the data — a distinction between valuing the dataset and valuing the company. Both can be true simultaneously, and the honest framing keeps both in view.

GSK signed a three-year expansion with a $70 million initial minimum commitment, and it was GSK that publicly vouched for the dataset's scale with the "34x larger than TCGA" line — a competitor-of-sorts effectively endorsing the cornered resource.13 On the Q1 2026 call, management disclosed new or expanded large collaborations with Merck and Gilead, though without attaching dollar figures — which means those are claims to verify against future disclosures rather than bankable numbers today.15 In May 2026, Bristol Myers Squibb signed on to a Lens-platform collaboration spanning five oncology and neuroscience trial programs, notable because it extends the data platform beyond pure oncology into neuroscience — a hint of category expansion.

Taken together, that is an impressive customer list: five or more of the largest pharmaceutical companies on earth paying to access Tempus's data and tools. The bullish read writes almost itself — this is contracted, increasingly recurring revenue from the most demanding buyers in healthcare, and net revenue retention above 100% says they keep spending more. But run the bear's counter-argument and it is equally coherent: this revenue is concentrated in a small number of very large counterparties whose enthusiasm can cool, whose budgets flex with their own pipelines, and whose commitment to the data does not necessarily mean commitment to the company — as the AstraZeneca warrant lapse showed in miniature. Concentration cuts both ways: a handful of whale contracts can look like a moat right up until one of the whales swims off.

And then there is the deal that earned the hardest scrutiny of all: the SoftBank joint venture. In June 2024, essentially concurrent with the IPO, Tempus and SoftBank formed "SB Tempus," a Japan-focused joint venture, with each side contributing ¥15 billion (roughly $95 million). This is the specific transaction the short seller would later flag as having "the appearance of potentially round-tripping capital to create revenue." The mechanism worth explaining plainly — without asserting wrongdoing — is this: if Tempus contributes capital into a JV, and that JV then pays Tempus for data or services, some portion of Tempus's contributed cash can flow back to Tempus as recognized revenue. To a critic, that risks manufacturing the appearance of arm's-length demand out of the company's own money. To the company, it is a legitimate structure to build a business in a new geography with a powerful local partner. The transaction is disclosed and the structure is not inherently improper — related-party JVs are common — but it is exactly the kind of arrangement where the burden of proof sits on management to show the revenue is genuinely independent. The fact that SoftBank was simultaneously a pre-IPO shareholder only sharpens the question. Whether Tempus ever specifically addressed the round-tripping mechanics — rather than deflecting — is a live issue we'll take up next, because in May 2025 a short seller put all of these threads together and pulled.

IX. The Spruce Point Short Report: A Credibility Stress Test (May 2025)

On May 28, 2025, Spruce Point Capital Management — an activist short seller with a reputation for detailed, accounting-focused reports — published "The Tempest Surrounding Tempus AI" and issued a "Strong Sell" opinion projecting 50–60% downside.910 For a company whose entire premium rested on a narrative of differentiated AI and a compounding data moat, this was the credibility stress test the bull case had been daring the market to run.

The report's allegations clustered into six threads, and it is worth laying them out precisely because the specific ones matter more than the sweeping ones. First, a leadership-history pattern argument: that Groupon and InnerWorkings both later restated accounting, and Starbelly.com (via HA-LO) ended in bankruptcy — a track record, Spruce Point argued, that should raise the burden of proof on any new Lefkofsky venture.9 Second, and most quotably, "AI-washing" — the claim that only about 2% of 2024 revenue, roughly $12.4 million of the $693.4 million total, came from AI-specific applications, undercutting the "AI company" name.9 Third, the SoftBank JV round-tripping concern. Fourth, the AstraZeneca warrant lapse as evidence of cooling insider conviction. Fifth, a decade without profitability or positive free cash flow. And sixth, a general aggressive-accounting allegation — the kind of broad claim that lacks a single smoking gun but colors everything around it.

The market's reaction was immediate and brutal. Tempus shares fell roughly 19% the same day, closing near $53.20 — and that was already down sharply from an all-time high above $100 earlier in 2025.9 For a stock that had roughly tripled from its IPO price at the peak, the report crystallized a de-rating that momentum had been papering over.

Tempus's response is itself part of the story, because how a management team answers a short report is a data point about its credibility. Tempus called the report "riddled with hypotheticals and inaccuracies," declined to respond point-by-point, and noted that Spruce Point's prior five short targets had, on average, risen afterward.11 Parse that. Attacking the short seller's track record is a rhetorical move, not a rebuttal; the fact that Spruce Point had been wrong before says nothing about whether it was wrong this time. The pointed analytical question — and one the outline rightly flags — is whether management ever specifically engaged the two most concrete, most falsifiable allegations: the SoftBank JV mechanics and the AI-revenue-mix claim. A blanket "riddled with inaccuracies" is a deflection; a line-by-line walk-through of how the SoftBank revenue is arm's-length, or how the company defines "AI revenue," would have been a rebuttal. Based on the public record through mid-2026, the response leaned closer to deflection than to detailed refutation — the company largely relied on continued growth and raised guidance to move the market past the report rather than dismantling its specifics.

It is worth being fair to both sides on the AI-washing charge specifically, because it is the most rhetorically potent and the most easily misused. The "2% of revenue is AI" figure depends entirely on how you draw the boundary around "AI." If you count only revenue from products explicitly sold as standalone AI applications, the number is small. But if you count the data-licensing business — which exists only because Tempus applies machine learning to structure and link otherwise-unusable multimodal records — the AI contribution looks far larger, because that structuring is itself an AI-enabled process. Spruce Point chose the narrow definition, which produced the damning headline; Tempus implicitly uses the broad one, which is why it calls itself an AI company at all. Neither is obviously dishonest; they are arguing about a boundary. What is fair to say is that the company invited the attack by naming itself "AI" while booking the overwhelming majority of its revenue from lab tests and data licensing — and that it has never published a clean, auditable reconciliation showing exactly how much economic value its AI models add versus the underlying testing and data-aggregation machinery. Until it does, the argument stays unresolved, which is precisely the vulnerability a short seller feeds on.

The aftermath adds nuance in both directions. On one hand, a plaintiffs' firm solicited investors for a securities-fraud investigation — the routine ambulance-chasing that follows any sharp short-report drop, and not itself evidence of wrongdoing. On the other hand, and this distinction matters, there was no evidence of any formal SEC enforcement action against Tempus as of mid-2026. A short report is an opinion, not an indictment; a plaintiffs' solicitation is a fishing expedition, not a finding. State it clearly: allegations were made and remain, in their specifics, largely unrebutted in detail — but no regulator had acted.

One ongoing behavior does keep the credibility question warm: Lefkofsky's insider selling. He has sold Tempus shares in nearly every quarter since the IPO, via pre-arranged 10b5-1 plans, with dispositions heavily outweighing acquisitions through mid-2026. Now, 10b5-1 plans are the proper, legal, pre-scheduled way for insiders to diversify, and steady selling by a founder who owns a huge stake is not inherently sinister. But it is a fair, checkable talking point precisely because of the voting-control structure: a controlling founder who can never be outvoted, steadily converting his paper wealth to cash quarter after quarter, is a pattern that a skeptical investor is entitled to weigh — not as proof of anything, but as a behavior to watch. The clean version of the skeptical-investor test is this: does management have concrete, falsifiable answers to the AI-mix and SoftBank questions, or has it mainly ridden growth momentum past the report? On the evidence so far, more the latter than the former. To judge whether that matters, you have to look hard at the people in charge.

X. Current Management: Incentives, Control, and Track Record

Every analysis of Tempus eventually collapses back onto one person, so let's assess Eric Lefkofsky directly — not with editorial venom and not with hagiography, but on behavior and incentives, which is where management credibility is actually forged.

Lefkofsky is Chairman, President, and CEO, and — through the Class B super-voting stock — the controlling shareholder. His 2025 total compensation was approximately $41.5 million, and the composition is telling: about $40.0 million of it was stock awards, against a modest base salary of roughly $783,000. On paper, that is textbook equity alignment — a CEO paid overwhelmingly in stock succeeds only if shareholders do. But the alignment mechanism is, in an important sense, toothless. Equity compensation disciplines a normal executive because a board of independent directors, answerable to shareholders, sets it and can claw it back. Here, the person receiving the equity also controls the votes that seat the board. Alignment of upside is real; alignment through accountability is largely absent. Those are different things, and conflating them is how investors talk themselves into ignoring governance risk.

The track record test has to be stated without editorializing, because the facts are strong enough on their own. Two of Lefkofsky's prior public companies — Groupon and InnerWorkings — later restated their accounting, and an earlier venture, Starbelly.com, ended in bankruptcy through its acquirer HA-LO.9 This is the exact pattern Spruce Point leaned on, and the fair way to use it is neither as a disqualifier nor as a dismissed irrelevance. It is a burden-of-proof setter. A founder with two prior restatements in his history has, reasonably, less benefit of the doubt on aggressive-looking accounting and related-party transactions than a founder without that history. It raises the bar Tempus must clear on disclosure; it does not by itself convict the company of anything.

Around Lefkofsky sits a management bench that investors got a much clearer look at in 2026. CFO Jim Rogers, whose 2025 total compensation was roughly $6.4 million, has been the voice on the financial-discipline questions — the leverage, the path to the roughly $65 million FY2026 Adjusted EBITDA target, and the May 2026 convertible-note pricing.17 The segment leaders were formally introduced at the company's inaugural Investor Day on May 29, 2026 — Ryan Fukushima, a founding-era executive, as CEO of Data and Applications, and Tom Schoenherr as CEO of Diagnostics.16 That Investor Day is a primary source worth weighting, because it was the company's first structured attempt to let segment leaders — not just the founder — narrate the business, a modest but real step toward institutionalizing the story beyond one person.

On capital allocation, the record is now legible: growth capex, one scale acquisition (Ambry), one bolt-on (Deep 6 AI), and a deliberate tilt toward debt over equity financing. Read charitably, that is a founder building patiently and avoiding dilution. Read skeptically, it is a pattern of preserving voting control at the cost of a cleaner balance sheet. Both readings coexist in the same facts.

The fairest overall verdict is a split decision. On the positive side of the ledger sits guidance discipline — Tempus met and raised its guidance every quarter through Q1 2026, which is one of the most concrete, low-noise credibility signals a management team can offer, and Tempus has offered it consistently. On the mixed side sits specificity under hard questions: management has been genuinely detailed and credible on reimbursement mechanics (the MRD throttling admission is the kind of candor that builds trust), but thin and deflective on the two questions that most threaten the narrative — the SoftBank JV and the AI-revenue mix. Incentive alignment is real; governance checks on it are minimal; and the burden of proof, set by history, is high. With the people assessed, the question becomes whether the financials are earning back that benefit of the doubt.

XI. Financial Trajectory: Growth, Guidance Discipline, and the Path to Profitability

Let's give the bull case its strongest fact first, because it is genuinely impressive and any fair analysis has to reckon with it: Tempus is growing fast at a scale where fast growth is rare. Total revenue went from $531.8 million in 2023 to $693.4 million in 2024 to $1,271.8 billion — $1.2718 billion — in 2025, a roughly 75% year-over-year jump, with management guiding to $1.59–1.60 billion for 2026.214 Growing revenue 75% when you are already past a billion dollars, in healthcare, is not a common feat. Much of the 2025 acceleration reflects the Ambry acquisition folding in, so it is not all organic — but even adjusting for that, the underlying growth rate is high.

Pair that with the guidance discipline already noted: Tempus raised full-year guidance every quarter of 2025 and again after its Q1 2026 beat.1415 This is the single most checkable trust signal in the whole story. A management team that consistently sets targets and then clears and raises them is demonstrating either genuine visibility into its business or conservative initial guidance — and either way, the pattern of beat-and-raise is a behavior that rewards belief. It is the strongest single argument on the bull side, precisely because it is behavioral rather than rhetorical.

Now the gap the bulls have to swallow, stated honestly. Tempus has never posted a GAAP profit, and the losses are large. GAAP net loss was $705.8 million in 2024 and $245.0 million in 2025.214 The 2024 figure was inflated by IPO-related stock compensation and one-time items, and the sharp narrowing to $245 million in 2025 is real progress — but "loss narrowed a lot" is not "profit." On the company's preferred non-GAAP measure, Adjusted EBITDA, Tempus turned positive in isolated quarters — Q4 2025 came in at roughly +$12.9 million — but had not achieved full-year positive Adjusted EBITDA as of Q1 2026.14 The roughly $65 million FY2026 Adjusted EBITDA target is therefore a forward claim, not an accomplished fact, and Adjusted EBITDA itself strips out the very real stock-based compensation that dilutes shareholders. The clean way to hold this: Tempus is on an improving trajectory toward profitability, but it is still a company that loses money, and the first year of positive full-year Adjusted EBITDA — let alone GAAP profit or positive free cash flow — remains in the future.

The balance sheet is where the growth story and the funding story collide. As of Q1 2026, following the May 2026 $400 million zero-coupon convertible note, Tempus held roughly $639 million in cash and short-term investments against approximately $1.32 billion in total debt — a net debt position of about $797 million.1517 That is adequate liquidity — the company is not in any near-term cash crunch — but the direction of travel is unmistakable: an increasingly debt-funded balance sheet supporting a business that does not yet generate its own cash. A 0% convert is cheap if the stock rises and the notes convert to equity; it is a real obligation if the stock falls and they come due as debt. The whole structure works as long as growth continues and access to capital markets stays open. What to listen for going forward is narrow and specific: does Adjusted EBITDA actually track toward the $65 million target quarter by quarter, and when it misses or wobbles, are the explanations concrete and operational or vague and macro-blamed? The quality of the misses will tell you more than the beats. With the numbers on the table, we can finally weigh the two sides against each other.

XII. Bull vs. Bear: The Investment Case

Here is where we war-game the whole thing — not to render a verdict, but to make the "why win / why not" spine explicit and test it against evidence rather than rhetoric.

The bull case rests on a genuinely differentiated asset and a track record of execution. The core is that proprietary, multimodal, longitudinal oncology dataset — the cornered resource — which cannot be replicated on any short timeline because you cannot manufacture years of linked patient outcomes. Layered on top: disciplined, on-strategy bolt-on M&A that widens the dataset (Ambry) rather than diworsifying into unrelated businesses; a data-licensing flywheel now spanning at least five of the world's largest pharma companies with a stated 126% net revenue retention, meaning existing customers keep spending more; guidance raised every quarter since the IPO, the most credible behavioral trust signal available; and real, if early, optionality in MRD and the Lens/Tempus One software franchises. If the flywheel compounds while guidance discipline and the FY2026 profitability target hold, this is a company converting a real moat into durable, high-margin revenue — and the current, post-pullback valuation could look cheap in hindsight.

The bear case is equally coherent and rests on structure, not just sentiment. A controlling founder with a personal history that includes two prior accounting restatements sits atop a governance structure with essentially zero external checks — no path to activism, no way to force change. The most specific short-seller allegations, on the SoftBank JV and the AI-revenue mix, remain unrebutted in detail rather than dismantled. The balance sheet is levering up while the business still posts GAAP losses, funding acquisitions with borrowed money. Management has itself admitted that reimbursement is throttling its fastest-growing new test category — meaning the flywheel has a CMS-shaped governor on it. And even after the 2026 pullback, the stock still prices in substantial future data-licensing growth, so the bar for disappointment is low. If the flywheel turns out to depend on a handful of concentrated, not-guaranteed pharma relationships, if reimbursement keeps capping newer categories, or if the "AI company" narrative and its thin AI-specific revenue base become a recurring credibility problem, the multiple compresses hard.

Put through the frameworks we set up earlier, the crux is whether the 7 Powers cornered resource is real and defended by switching costs. The evidence is suggestive but not conclusive: net revenue retention above 100% and marquee renewals point toward stickiness, but the AstraZeneca warrant lapse and the concentration of revenue in a few whales point toward fragility. On Porter's forces, the binding constraints are buyer power (payers/CMS capping diagnostics pricing) and substitute threat (pharma building real-world-data capability in-house) — both structural, both outside Tempus's control. The activist stress test writes itself: a skeptic would target the related-party SoftBank JV, the debt-funded M&A after a loss-making decade, the super-voting control that immunizes the founder, and the steady insider selling. The uncomfortable truth the bear surfaces is structural: because Lefkofsky's control makes activism near-impossible, the stock price itself is the only real disciplining mechanism on this company. That is exactly what played out on short-report day and around the Q1 2026 reaction — the market, not the board, is the check. Which means the right way to follow this story is to watch the specific gauges that would confirm or break each side of the case.

XIII. KPIs and Risk Radar to Track Going Forward

If you can only watch a few dials on this company, watch these three — chosen because they map directly onto the bull-bear crux rather than onto vanity metrics.

First, Data and Applications revenue growth and net revenue retention. This is the purest test of the cornered-resource thesis. If the data business keeps compounding at 40%-plus with retention holding above 100%, the flywheel is real and pharma is genuinely building on the platform. If growth decelerates or retention slips toward 100%, it signals the moat is shallower — a few big contracts rather than a compounding dataset advantage. This single metric is where the whole "AI company" claim lives or dies.

Second, Adjusted EBITDA against the roughly $65 million FY2026 target, quarter by quarter.14 This is the credibility gauge. Tempus has earned trust by beating and raising; the profitability target is the promise that trust is now underwriting. Tracking whether the company hits it — and, when it wobbles, whether the explanations are specific and operational — is how you keep management honest against its own guidance discipline.

Third, MRD and new-modality volume growth against reimbursement coverage. MRD volumes were up roughly 500% year over year in Q1 2026, but management is deliberately throttling the ramp until reimbursement broadens.15 The KPI that matters is not raw volume — it's volume relative to reimbursement milestones, because ASP, set by CMS and MolDx, is what converts test volume into real revenue. Watch the coverage decisions, not just the test counts.

On the risk radar, five items carry genuine mechanism rather than generic hand-waving. Reimbursement/CMS policy risk is the most concrete — by management's own admission, it directly caps how fast new tests can scale. Pharma-counterparty concentration risk is live and already demonstrated, with the AstraZeneca warrant lapse as the object lesson: a few large customers, whose commitment to the data does not guarantee commitment to the company. Governance and key-person risk flows from the super-voting control stacked on a scrutiny-inviting personal history — an extreme concentration with no external counterweight. Leverage risk grows with every debt-funded deal against a still-loss-making P&L; the model depends on capital markets staying open. And integration and execution risk is real because Tempus is doing several hard things at once — absorbing Ambry, integrating Deep 6 AI, and launching new assays simultaneously. Sitting behind all of them is reputational risk: unresolved specific allegations that could resurface if new evidence ever emerges. None of these is a prediction of failure; each is a mechanism by which the bull case could break, which is exactly what a risk radar is for. Step back from the dials, though, and the saga offers lessons that outlast any single quarter.

XIV. Playbook: Business and Investing Lessons

Every good business story leaves behind transferable lessons, and Tempus — precisely because it sits at the fault line between narrative and numbers — offers unusually sharp ones for long-term investors.

The first: data-and-diagnostics moat claims are only as good as their renewal evidence, not their headline deal announcements. A splashy "$200 million collaboration with a global pharma" press release is a starting gun, not a finish line. What proves a data moat is the boring stuff — contracts renewing, deal sizes expanding, net revenue retention holding above 100% year after year. The AstraZeneca episode is the whole lesson in miniature: a big new data deal and a lapsed equity warrant, side by side, from the same counterparty. Weigh the recurring evidence over the announcement.

The second: founder super-voting control removes the normal shareholder-discipline mechanism, which changes how you should read drawdowns. In a normally-governed company, a sharp selloff can invite activists, board changes, or a strategic review — outside forces that can fix things. When a founder cannot be outvoted, none of that is available; the stock price itself becomes the only disciplining force. That means volatility in a founder-controlled name carries different information than the same volatility in a widely-held one. The short-report day was not just a price move; it was the market doing the only job the governance structure left available to it.

The third: a management team's personal history at prior companies is a legitimate input to a credibility assessment — it sets the burden of proof, not a verdict. Lefkofsky's two prior restatements do not prove anything about Tempus's accounting. But they do reasonably raise the bar Tempus must clear on disclosure and related-party transactions, and they explain why a transaction like the SoftBank JV draws scrutiny it might not draw at another company. History is a prior, not a prophecy — but ignoring the prior is its own kind of error.

The fourth, and maybe the most useful for the daily grind of following a company: guidance discipline, met and raised quarter after quarter, is one of the most checkable, low-noise credibility signals available — weigh it more heavily than qualitative strategy claims. Anyone can narrate a compelling flywheel; far fewer can set numerical targets and clear them repeatedly. Tempus's beat-and-raise record through Q1 2026 is, genuinely, the strongest evidence on the bull side, and it is strong precisely because it is behavioral and falsifiable rather than rhetorical. When a management team's words and its delivered numbers point the same direction over many quarters, that consistency is worth more than any strategy slide. These lessons frame the last question: what, concretely, should you be watching next?

XV. Epilogue & What to Watch

So where does this leave us, in the summer of 2026, with Tempus a two-year-old public company still arguing about what kind of company it is?

The near-term checkpoints are concrete and datable. Watch the quarterly progress against the roughly $65 million FY2026 Adjusted EBITDA target — the first year of positive full-year Adjusted EBITDA would convert a forward promise into an accomplished fact, and a miss would put the beat-and-raise credibility record to its first real test.14 Watch MRD reimbursement decisions, because those, not test volumes, are the real ASP levers that determine whether the fastest-growing test category becomes a business or stays optionality.15 Watch for renewal and expansion news from the pharma cohort — AstraZeneca, GSK, Merck, Gilead, Bristol Myers Squibb — because renewals are the evidence that separates a data moat from a lucky run of contracts.1315 And watch, specifically, whether management ever directly addresses the two questions it has so far mostly ridden past: the SoftBank JV mechanics and the AI-revenue mix. A detailed, falsifiable answer to either would meaningfully change the credibility calculus.

One more lever deserves a place on the watchlist: FDA companion-diagnostic approvals. In May 2026, Tempus received FDA approval for a tumor-only version of its xT CDx test, enabling migration of its entire DNA solid-tumor portfolio onto an FDA-approved footing.18 The right way to read this is not as an ordering-behavior story — physicians were already ordering these tests — but as an ASP lever. Regulatory approval can unlock broader reimbursement and higher realized prices per test, which, in a business where CMS sets the governor on the flywheel, matters more than any marketing push.

Here is the final framing, and it is deliberately not a verdict. The interesting question about Tempus was never really whether AI can transform cancer diagnostics — it plausibly can, and the underlying science is real. The interesting question is narrower and harder: can a founder-controlled, debt-funded, still-loss-making company convert a genuinely differentiated dataset into durable, arm's-length pharma revenue — fast enough, and cleanly enough — before reimbursement limits cap its newest categories or a credibility crisis catches up with the growth story? The bull case says the flywheel is already spinning and the beat-and-raise record proves it. The bear case says the moat is a few concentrated contracts, the governance is a black box, and the AI label is doing more work than the AI revenue. Both are looking at the same 10-K. What resolves the argument will not be a slogan or a short report — it will be the next several quarters of renewals, reimbursement decisions, and delivered numbers. Those are the dials. The rest is narrative.

References

-

Tempus AI, Inc. — Form 424B4 IPO Prospectus, 2024-06 (SEC EDGAR) ↩↩↩↩

-

Tempus Announces Pricing of Initial Public Offering — Tempus IR, 2024-06-13 ↩

-

Google-backed Tempus AI pops as much as 15% in Nasdaq debut — CNBC, 2024-06-14 ↩↩

-

Medical Data Firm Tempus AI Rises After $410.7 Million IPO — Bloomberg, 2024-06-14 ↩↩

-

Tempus Reports Third Quarter 2024 Results and Agreement to Acquire Ambry Genetics — Businesswire, 2024-11-04 ↩↩↩

-

Tempus AI to buy genetic testing company for $600M — MedTech Dive, 2024-11-04 ↩

-

Tempus Announces Acquisition of Deep 6 AI — Tempus News, 2025-03-10 ↩↩

-

Spruce Point Capital Management — Research: Tempus AI, Inc. ↩↩↩↩↩↩

-

Spruce Point Capital Management Releases Strong Sell Opinion on Tempus AI (TEM) — Businesswire, 2025-05-28 ↩

-

Tempus AI Hits Back at Scathing Short Report — TheStreet, 2025-05-28 ↩

-

Tempus AI Line Up $200M AstraZeneca/Pathos Deal to Develop Cancer Model — Fierce Biotech, 2025 ↩

-

GSK Expands AI Footprint With $70M Tempus Deal — BioSpace, 2025 ↩↩↩

-

Tempus Reports Fourth Quarter and Full Year 2025 Results — Tempus News, 2026-02-24 ↩↩↩↩↩↩↩

-

Tempus Reports First Quarter 2026 Results — Businesswire, 2026-05-05 ↩↩↩↩↩↩↩↩↩↩

-

Tempus to Host Inaugural Investor Day on May 29, 2026 — Businesswire, 2026-04-29 ↩

-

Tempus Announces Pricing of Upsized Offering of $400.0 Million of Convertible Senior Notes — Businesswire, 2026-05-07 ↩↩↩

-

Tempus Receives FDA Approval for Tumor-Only xT CDx — Businesswire, 2026-05-29 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube