Bio-Techne Corporation: The Gold Standard Reagent Empire

I. Introduction & Episode Roadmap

On the morning of June 25, 2026, investors who owned a quiet Minneapolis life-science company woke up roughly a third richer. Merck KGaA — the 358-year-old German pharmaceutical and chemicals house from Darmstadt, not to be confused with the American Merck it was forced to split from a century ago — announced a definitive agreement to buy Bio-Techne Corporation for $73.00 per share in cash. The all-cash price valued the business at an enterprise value of roughly $11.3 billion, or about €9.9 billion, and represented a 36% premium to Bio-Techne's volume-weighted average share price over the prior month.1 For a company most people outside a research laboratory had never heard of, it was a staggering number.

Here is the puzzle worth sitting with. Bio-Techne generated only about $1.22 billion of revenue in its fiscal year ended June 30, 2025.[^2] Merck agreed to pay roughly 9.3 times that revenue and, by the outline's math against adjusted EBITDA of about $429.6 million, roughly 26 times cash earnings — for a business whose organic growth had actually gone negative in its most recent quarter.[^11] Why would one of Europe's most disciplined industrial acquirers hand over eleven billion dollars in cash, at the top of the price range, for a slow-growing supplier of biological chemicals? For context, it was Merck KGaA's largest life-science acquisition since it swallowed Sigma-Aldrich for around $17 billion in 2015 — the deal that made Merck a giant in laboratory reagents in the first place.

Consider the sheer improbability of the outcome for a moment. There is a well-worn pattern in the modern economy where the companies capturing the most value from a technological revolution are not the ones inventing the flashy end products but the ones supplying the essential inputs — the picks and shovels sold to everyone digging for gold, regardless of who strikes it. During a gold rush, selling shovels is a better business than mining, because the shovel-seller profits whether or not any given miner succeeds. Bio-Techne is one of the purest examples of that logic in all of biotechnology. It did not need any single drug to work; it needed drug development itself to keep happening, and it collected a toll on the process. That is a structurally superior position to being a drug company, where a failed clinical trial can erase a decade of work overnight. The toll-collector's revenue is diversified across thousands of experiments run by thousands of customers pursuing thousands of different goals.

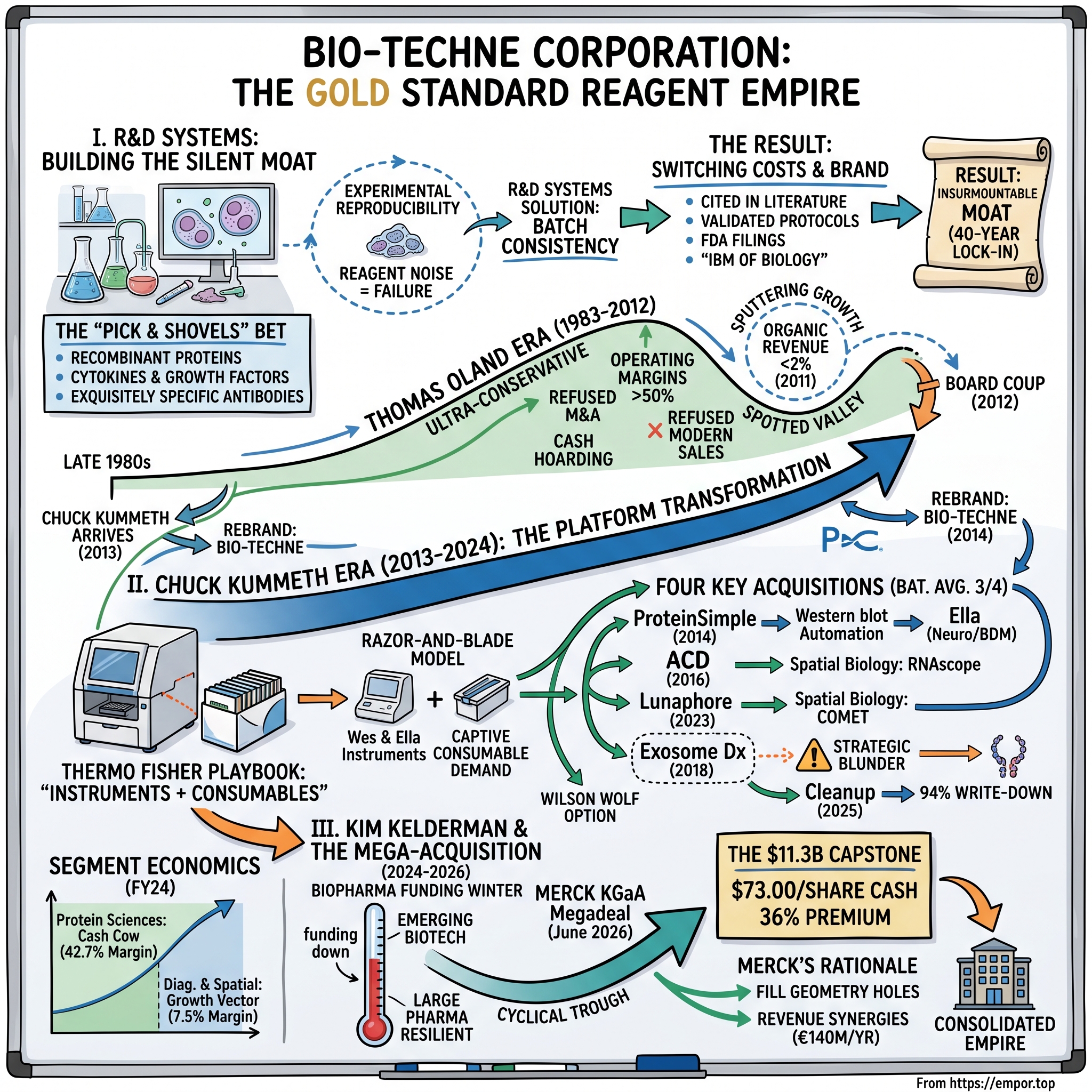

The answer is the whole story, and it is a story about the least glamorous, most defensible corner of the entire biotechnology economy. Bio-Techne does not cure diseases. It does not run clinical trials or sell blockbuster drugs. It makes the picks and shovels — the recombinant proteins, the cytokines and growth factors, the exquisitely specific antibodies — that every biologist on earth uses to do the actual experiments. And over four decades it built something close to a monopoly on trust: when a researcher publishes a landmark paper or a pharma company files a clinical protocol with the FDA, they name the exact catalog number of the reagent they used, and that reagent, more often than not, came from Bio-Techne's R&D Systems brand.

The narrative arc runs through four distinct regimes. First, the silent moat — how a scientist's supply shop became the reference standard written into the scientific literature itself, a switching cost so severe that changing suppliers can mean re-validating years of work. Second, the Oland era (1983–2012), a remarkable and ultimately maddening period in which the company ran operating margins north of 50%, hoarded cash, refused to do deals, and grew so slowly that its own shareholders eventually forced the CEO out. Third, the Kummeth transformation (2013–2024), when a hard-nosed veteran of 3M and Thermo Fisher arrived, rebranded the company Bio-Techne, and imported the "instruments-plus-consumables" playbook to turn a sleepy reagent house into a diversified tools platform — with one expensive misfire along the way. And fourth, the Kelderman capstone (2024–2026), a pragmatic successor who cleaned up the portfolio, navigated a brutal biopharma funding winter, and ultimately negotiated the premium cash exit.

It is also, quietly, a story about the entire life-science tools industry, an unglamorous sector that sophisticated investors have learned to love precisely because it sits upstream of the volatile drug-development gamble. The tools companies — Thermo Fisher, Danaher, Merck's Sigma-Aldrich, Agilent, and a dozen specialists like Bio-Techne — supply the reagents, instruments, and consumables that every pharmaceutical and academic lab must buy to function. Their revenue is recurring, their margins are high, their customer relationships are sticky, and their fortunes rise with the secular growth of biology itself rather than with any one molecule's odds in a clinical trial. Over the past two decades this sector has been one of the great quiet compounders of the market, and the reason it consolidates relentlessly is that scale in distribution and breadth in catalog are genuine advantages. Bio-Techne's arc — from independent specialist to acquisition target — is a microcosm of how that industry logic plays out.

Along the way this piece will examine the peculiar economics of biological reagents, the regulatory lock-in that competitors cannot buy their way around, the anatomy of four acquisitions (three brilliant, one a genuine blunder), and the strategic logic — and the limits — of Merck KGaA's bet. The posture here is neutral: management's claim that Bio-Techne owns an "insurmountable moat" is a hypothesis to be tested against evidence, not a slogan to be repeated. Let's start where the moat was poured, in a Minneapolis lab in the mid-1970s.

II. The Reagent King: R&D Systems & The Oland Era (1976–2012)

Picture a molecular biologist in 1990 trying to run an experiment on how a cell decides to grow. She needs a tiny quantity of a signaling protein — a cytokine — purified to near-perfection and, crucially, identical to the batch she used last month and the batch she will use next year. If the purity drifts, if a contaminant creeps in, if the biological activity varies by even a few percent, her results become noise. Months of work, and possibly a multi-year grant, evaporate. In that world, the supplier who can guarantee batch-to-batch consistency is not a vendor. He is a lifeline.

That was the business Dr. Roger C. Lucas and a small group of colleagues set out to build when they founded Research and Diagnostic Systems, Inc. — R&D Systems — in Minneapolis in 1976. The mission was unglamorous and enormous: supply high-purity proteins and antibodies to a research community that was just beginning to explode. Recombinant DNA technology was brand new; the biotech industry barely existed. But every experiment that industry would ever run needed reagents, and reagents that could be trusted were scarce. In 1985, R&D Systems merged into Techne Corporation, a small publicly traded shell, giving the operation a stock-market listing and the currency to scale up production.

The genius bet came in the late 1980s. Rather than chase the whole universe of laboratory chemicals, R&D Systems concentrated on cytokines and growth factors — the master signaling molecules of biology. Interleukins, interferons, TGF-beta, the whole vocabulary the immune system and developing tissues use to talk to themselves. These are ferociously difficult to manufacture consistently, which is precisely why they were valuable to sell. A protein that is hard to make well is a protein that a customer will pay a premium not to have to make himself.

To understand why this became a fortress, borrow Hamilton Helmer's language of switching costs and brand. In enterprise IT there was once a saying: "Nobody ever got fired for buying IBM." Biology has its own version, and R&D Systems is the IBM. Experimental reproducibility is the ultimate bottleneck in science; a reagent that behaves unpredictably is worse than useless because it produces confident, wrong answers. So researchers gravitate to the supplier with the deepest reputation for purity — and then something remarkable happens. They write that supplier's name into their published papers. Over decades, tens of thousands of peer-reviewed articles specify "reagents from R&D Systems." Clinical trial protocols submitted to the FDA name specific antibody clones. Once a drug target or a biological pathway has been validated using a particular R&D Systems antibody, switching to a cheaper competitor is not a purchasing decision — it is a re-validation project, potentially requiring regulators to sign off again. The cost of switching is not the price of the reagent. It is the risk of invalidating everything built on top of it.

This is a genuinely rare kind of moat, and it deserves neither cheerleading nor cynicism, just precision about its mechanism: the product embeds itself into the customer's record, not merely the customer's workflow. Once that happens, price sensitivity collapses. A cytokine might cost a few hundred dollars; the experiment it enables might cost millions. Nobody optimizes the cheap input when it endangers the expensive output.

It is worth dwelling on why the cytokine bet was so hard to replicate, because the difficulty is the moat. A recombinant protein is grown inside living cells — bacteria, yeast, or mammalian cell lines engineered to manufacture the target molecule — and then coaxed through a gauntlet of purification steps. Every variable along the way, from the fermentation temperature to the exact chromatography resin, subtly changes how the final protein folds and behaves. Two suppliers following the "same" recipe can produce proteins with meaningfully different biological activity. R&D Systems' edge was not a single patent; it was accumulated process knowledge — thousands of tiny manufacturing decisions, refined over years and documented in a way that let the company hit the same specification lot after lot after lot. That kind of tacit institutional know-how does not show up on a balance sheet and cannot be reverse-engineered by reading a paper. It is the industrial equivalent of a chef who can reproduce a dish identically ten thousand times when competitors cannot manage it twice.

Layer onto that the structure of who buys these products and why. The company later expanded the antibody catalog dramatically — including through the addition of the Novus Biologicals brand — until it spanned hundreds of thousands of individual research tools. But breadth alone was never the point. The point was that each item in the catalog was a small, high-margin, mission-critical purchase for a customer whose real cost was their own time and grant money. When the input is cheap relative to the experiment and irreplaceable relative to the result, the seller captures extraordinary economics. This is why a physical-goods manufacturer could earn software-like margins: it was, in effect, selling insurance against failed experiments, priced as a consumable.

Presiding over this money machine for nearly three decades was Thomas Oland, who took the top job in 1983 and ran the company with a conservatism that bordered on the monastic. The numbers he produced were, in isolation, spectacular. Gross margins ran north of 75%. Operating margins routinely exceeded 50%, at times pushing toward 55% — figures more typical of a software company than a manufacturer of physical goods. The balance sheet carried no debt and a growing mountain of cash. For a while, this looked like the platonic ideal of a wonderful business.

But there was a dark side to all that discipline, and it is the part of the story sophisticated investors should dwell on, because it is a lesson in how a great business can be under-managed. Oland treated R&D Systems as a static cash cow. He kept research and development spending under 8% of sales, refused to build a modern professional sales force, and — most consequentially — refused to participate in the wave of consolidation reshaping the life-science tools industry, as Thermo Fisher and Danaher assembled empires through relentless M&A. The cash pile simply sat there, earning near-nothing in an era of collapsing interest rates. And the growth engine sputtered: by 2011, organic revenue was crawling forward at 1% to 2% a year.

There is a genuine debate to be had about whether Oland was a poor steward or simply a different kind of one, and the fair answer is both. On the ledger of pure profitability and balance-sheet safety, he was nearly flawless — no debt, no dilution, no bad acquisitions, no impairments. Investors who prize downside protection got exactly what they wanted. But capital allocation is not only about avoiding mistakes; it is about the opportunity cost of inaction. A company that generates enormous free cash flow and then parks it in low-yielding securities is quietly handing shareholders a return on that cash far below what the underlying business earns. Every year Oland let the reagent catalog sit under-marketed and un-automated, rivals like Thermo Fisher and Danaher were compounding through acquisition, widening their distribution and product breadth. The moat around the reagents never eroded — but the company was letting the wider tools industry consolidate around it, and a fortress surrounded by a growing empire is eventually a target, not a stronghold.

Oland had built an exquisite fortress and then declined to expand it, leaving perhaps the most valuable under-commercialized catalog in the industry locked in a vault. For a patient long-term investor, the lesson is subtle: a business with a spectacular moat and a management team unwilling to reinvest can be a value trap dressed as a quality compounder, because the moat protects the margins without guaranteeing the growth. That gap between what the company was and what it could be would soon become intolerable to the people who owned it.

III. The Board Coup & The Advent of Chuck Kummeth (2012–2014)

Every value-trap has a breaking point, the moment when the owners of a business stop admiring the margins and start counting the missed decade. For Techne Corporation, that moment arrived in 2012. Institutional shareholders had run the arithmetic and did not like it: here was a company with pristine economics, a debt-free balance sheet, and an idle cash hoard, compounding shareholder value at a fraction of what its assets could support. The frustration that had simmered for years boiled over into the boardroom.

The resolution was swift and, by the standards of a sleepy Minnesota company, dramatic. On November 30, 2012, Thomas Oland stepped down as chief executive and president, with his board seat vacated effective November 1; chief financial officer Gregory Melsen took over as interim CEO while the board searched for a permanent leader.2 Robert Baumgartner, a director since 2003, was installed as chairman — the same Baumgartner who, fourteen years later, would sign off on the sale to Merck.1 The message was unambiguous: the era of managing R&D Systems as a static endowment was over. The board wanted a builder.

They found one in Charles "Chuck" Kummeth, appointed CEO effective April 1, 2013.3 Kummeth was cut from entirely different cloth than his predecessor. He was a career operator forged in the two most demanding schools of industrial management in America: he had spent years at 3M, the Minnesota conglomerate famous for its innovation discipline, and then at Thermo Fisher Scientific, the reigning heavyweight champion of life-science tools consolidation. Thermo Fisher's entire strategy was the roll-up — acquire, integrate, cross-sell, repeat — and Kummeth had watched it work at scale.

When Kummeth looked at Techne, he saw what an operator sees when handed an undermanaged asset: enormous latent value. The company sat on a catalog of tens of thousands of top-tier proteins and antibodies — an irreplaceable library assembled over nearly forty years — and had barely tried to sell it properly. There was little in the way of digital marketing, thin international distribution, and almost no presence in the automated instrument platforms that were beginning to reshape how laboratories worked. The reagents were a Ferrari that had been driven exclusively to church on Sundays.

Kummeth's temperament was the antithesis of Oland's, and the contrast explains why the board chose him. Where Oland's instinct was to protect and hoard, Kummeth's was to build and deploy. He talked the language of end markets, cross-selling, digital lead generation, and total addressable market — the operating vocabulary of a Thermo Fisher division head, not a founder-era treasurer. Crucially, he understood that in the modern life-science tools industry, the winners were not the companies with the best single product but the companies that could sell a customer an entire workflow and then own every recurring dollar that flowed through it. That was a fundamentally different theory of the business than the one that had governed the company for thirty years, and importing it required more than new slogans; it required the willingness to spend the cash pile Oland had so carefully guarded.

The transition also carried a small but revealing governance subplot. When the board reached outside for Kummeth rather than promoting from within, the interim CEO and CFO Gregory Melsen — who had run the company in the gap — departed after being passed over.2 It was a reminder that the 2012 upheaval was not a gentle retirement but a genuine changing of the guard, with the board asserting control over a company that had long been run in one man's image. For shareholders, the episode was a case study in why board independence matters: the same directors who had tolerated years of underperformance ultimately proved willing, under pressure, to force the hard reset that unlocked the next decade of value.

His first moves were about identity and ambition. In 2014, Kummeth unified the company's scattered legacy entities under a single modern brand: Bio-Techne. It was more than cosmetic. The old name, "Techne," carried the DNA of a stock-shell reverse merger; "Bio-Techne" announced a company that intended to compete across the breadth of the life sciences, not just sell proteins from a catalog.

The deeper shift was strategic, and it is worth stating plainly because it defined everything that followed. Kummeth resolved to keep the magnificent reagent margins intact while bolting on a second engine: instruments. The logic was the razor-and-blade model, adapted for biology. If Bio-Techne could sell a researcher an automated machine that ran a particular assay, it could then lock in years of recurring, high-margin sales of the proprietary consumables — the cartridges, capillaries, and reagents — that only that machine could use. Instruments create captive consumable demand; consumables are where the durable profit lives. The reagent business had proven that customers would pay for trust and convenience. Now Bio-Techne would sell them the workflow too. To build that second engine quickly, Kummeth reached for the tool his old employer knew best: acquisitions.

IV. The Thermo Fisher Playbook: Building the Platform via M&A

If the Oland era was defined by the deals Techne refused to do, the Kummeth era was defined by the deals it did. Over roughly a decade, Bio-Techne spent close to a billion dollars assembling a platform, and the four transactions that mattered most form a near-perfect case study in capital allocation — three of them textbook successes, one an instructive failure. Studied together, they reveal both the discipline and the fallibility of the playbook.

ProteinSimple (August 2014, ~$300 million). Kummeth's first major swing set the template. Bio-Techne agreed in June 2014 to acquire ProteinSimple for $300 million in cash, closing that August.4 The prize was automation of one of biology's most tedious rituals: the Western blot, a technique for detecting specific proteins that, done by hand, is a finicky, error-prone, roughly day-long ordeal. ProteinSimple's Wes and Maurice instruments turned that manual protocol into a hands-free, roughly three-hour automated run. The strategic beauty was the pull-through: every instrument placed was a franchise for years of proprietary capillary and reagent cartridge sales. To appreciate why this mattered, understand the ritual it replaced. A traditional Western blot required a scientist to run proteins through a gel by hand, transfer them onto a membrane, wash and stain them through a sequence of finicky manual steps, and pray that nothing went wrong across the roughly day-long process — a protocol so touchy that it became a running joke about irreproducibility in biology. ProteinSimple's automation removed the human hands, and with them the human error. But the deeper strategic prize was not the flagship Western-blot machines alone; it was the whole family of instruments that came with the deal and grew under Bio-Techne's ownership. The Ella platform, for instance, automates immunoassays into cartridges and has found a fast-growing niche in neurodegeneration research, where blood-based biomarkers for diseases like Alzheimer's are a hot frontier; the Maurice platform became embedded in biopharma manufacturing as a quality-control tool for checking the size, charge, and purity of therapeutic proteins.[^11] Each of these placed a piece of hardware in a lab that then consumed proprietary cartridges and reagents for years — the recurring-revenue flywheel Kummeth was hunting for. Bio-Techne paid around six times revenue — not cheap — but the asset became the growth engine of a new Analytical Solutions franchise and, by the standard of hindsight, looks like money extraordinarily well spent.

Advanced Cell Diagnostics / ACD (August 2016, $250 million upfront plus up to $75 million in milestones). The second deal was more visionary and, arguably, the best acquisition in the company's history.5 ACD had pioneered RNAscope, a proprietary technology for RNA in situ hybridization. The layman's version: before RNAscope, if you wanted to know which genes were switched on inside a piece of tissue, you had to grind the tissue into a slurry, destroying all information about where in the tissue the activity was happening. RNAscope let researchers see individual molecules of RNA lit up inside intact cells and tissue sections, preserving the spatial architecture. That was an early beachhead in what would become one of the hottest fields in biology — spatial biology, the study of not just what is happening in a cell but where. The genius of the ACD purchase, viewed with a decade's hindsight, was less about the price than about the timing relative to the field's maturation. In 2016 spatial biology was a niche interest of academic labs; buying the category's ISH pioneer then, before the field became fashionable, meant paying a growth multiple on a small base rather than a strategic-scarcity multiple on a proven one. By the time competitors and acquirers piled into spatial biology in the early 2020s — culminating in bidding wars and bankruptcies among the pure-plays — Bio-Techne already owned an entrenched, patent-protected franchise generating real revenue. This is the difference between buying an option early and paying up for certainty late, and it is the clearest evidence in the whole story that Kummeth's team could see around corners. Bio-Techne paid roughly ten times trailing revenue, a rich multiple that looked aggressive at the time and prescient later, as RNAscope grew into the cornerstone of the company's Diagnostics and Spatial Biology segment.

Exosome Diagnostics (August 2018, $250 million upfront) — the strategic blunder. Here the playbook broke, and the reasons it broke are more instructive than any of the wins. Exosome Diagnostics owned a liquid-biopsy technology — the headline product was the ExoDx Prostate (EPI) test — that hunted for cancer biomarkers in the exosomes shed into a patient's urine or blood. Scientifically elegant. Strategically, it was a trap. Bio-Techne's entire business model was selling kits and tools to other people, who then did the messy clinical work. Exosome Diagnostics was the opposite: a centralized clinical laboratory operating under the CLIA regulatory regime, which meant Bio-Techne now had to handle patient sample logistics, insurance billing, and reimbursement negotiations with payers. Those are the operating muscles of a diagnostics service company, and a reagent manufacturer simply did not have them. Selling, general, and administrative costs ballooned, reimbursement crawled in far slower than hoped, and the business dragged down the entire segment's profitability for years.

The reckoning came in 2025. Bio-Techne divested the Exosome Diagnostics laboratory business to MDxHealth, a specialist in urology and prostate diagnostics, in a deal that closed on September 15, 2025.[^9] The total consideration was a nominal $15 million — $5 million in MDxHealth stock at closing plus $2.5 million paid annually over the following four years, roughly a $10 million deferred stream.6 Against the $250 million of cash Bio-Techne had put in, that is on the order of a 94% write-down of the upfront price. The capital-allocation lesson is durable and worth generalizing: a company brilliant at manufacturing and selling tools is not automatically competent at running clinical services, because the two demand entirely different cost structures, sales forces, and regulatory competencies. Management's willingness to admit the mistake and cut the loss is, on balance, a credibility positive — but it does not erase the fact that roughly a quarter-billion dollars of shareholder capital was destroyed in the round trip.

Lunaphore (July 2023, ~$170 million). The final major deal returned to the winning theme.[^8] Lunaphore, a Swiss pioneer, made the COMET system, which automates hyperplex protein staining — the ability to visualize dozens of different proteins on a single tissue slide, in place. Where ACD's RNAscope reads RNA, Lunaphore's COMET reads proteins, and together they gave Bio-Techne a two-modality grip on spatial biology. The strategic point was as much defensive as offensive: it fortified the company's spatial position against rivals like Akoya Biosciences and Bruker at a moment when the field was becoming a battleground.

Beyond the four headline deals sat a quieter but strategically fascinating bet: Wilson Wolf. Bio-Techne took a 20% stake in this maker of the G-Rex, a single-use bioreactor that has become the market-leading vessel for growing cells in cell-therapy manufacturing, with a contractual path to acquire the remainder by the end of calendar 2027 (or sooner if certain milestones are hit).[^11] The logic is elegant and reveals how Kummeth and his successors thought about the razor-and-blade model in three dimensions rather than two. Bio-Techne already sold the GMP-grade cytokines and growth factors that cell therapies are grown in; Wilson Wolf sells the vessel those cells are grown in. Owning both means owning two of the essential consumables in every cell-therapy batch, with a roughly 50% attachment rate between Wilson Wolf's bioreactors and Bio-Techne's proteins.[^11] And the economics of the target are striking: on the fiscal Q3 2026 call, management noted Wilson Wolf was growing at low double digits on a trailing-twelve-month basis while sustaining EBITDA margins north of 70% — reagent-like economics in a hardware wrapper.[^11] It is a structured, optionality-rich way to lean into cell therapy without paying a full acquisition multiple up front.

Step back and grade the capital allocation as a portfolio, which is the only honest way to grade it. Three of the five major moves — ProteinSimple, ACD, and Lunaphore — bought genuinely differentiated, defensible technologies that deepened the razor-and-blade dynamic and pushed Bio-Techne into the fastest-growing corners of biology. Wilson Wolf looks smart and cheap. One move — Exosome Diagnostics — was a clear error that cost roughly a quarter-billion dollars. That is a batting average most acquisitive companies would envy, and it is a world away from the Oland era's refusal to deploy capital at all. But it also punctures any narrative of infallible management genius: the same appetite that produced the wins produced the loss, and an investor should hold both facts at once rather than rounding up to a hagiography. Having assembled the platform, the question investors must ask is what it actually earns — and that requires opening the machine and looking at the segments.

V. Inside the Machine: Segment Economics & Hamilton Helmer's 7 Powers

Strip away the branding and the scientific romance, and Bio-Techne is really two very different businesses wearing one logo. One is a cash-gushing utility with almost embarrassing margins. The other is a collection of high-growth, high-multiple bets that consume cash today in hope of dominance tomorrow. Understanding the company means understanding how those two halves relate — because the first quietly funds the second.

The Protein Sciences segment is the bedrock, and it is where the forty-year moat lives. In fiscal 2024 it generated $830.9 million of revenue — roughly 72% of the company's total — at an operating margin of about 42.7%, according to the company's segment reporting.7 That single figure explains the entire corporate story: a manufacturer earning 42 cents of operating profit on every revenue dollar is not competing on price; it is harvesting the trust it spent decades accumulating. Inside the segment sit two franchises. Reagent Solutions is the classic R&D Systems catalog — proteins, antibodies, and increasingly the GMP-grade cytokines used to actually manufacture cell and gene therapies, a fast-growing and strategically vital niche. Analytical Solutions is the ProteinSimple instruments-and-consumables franchise. Together they throw off the predictable free cash flow that pays for everything else. The most interesting growth hiding inside this otherwise mature segment is the GMP-grade cytokine business — the same signaling proteins the company has always made, but manufactured to the pharmaceutical-grade quality standards required to actually produce cell and gene therapies rather than merely study them. This is a subtle but powerful escalation of the moat: a research reagent gets used once in an experiment, but a GMP protein written into the manufacturing process of an approved therapy becomes a locked-in, recurring input for as long as that therapy is made and sold, with switching costs even higher than in research because changing a manufacturing input can trigger regulatory re-filing. As the cell-therapy field advances from clinical trials toward commercial-scale production, this niche converts Bio-Techne from a supplier of research consumables into a supplier of manufacturing consumables — a structurally stickier and faster-growing position, and one of the clearest reasons Merck wanted the asset.

The Diagnostics and Spatial Biology segment is the growth vector, and its economics look nothing like its sibling's. In fiscal 2024 it produced $326.4 million of revenue — about 28% of the total — but only a 7.5% operating margin, down sharply from 14.7% the year before.7 That collapse was not a demand problem; it was the arithmetic of building for the future. The segment was absorbing the integration costs of Lunaphore and still carrying the dead weight of Exosome Diagnostics before the divestiture. Inside it sit ACD's RNAscope genomics business, the Asuragen molecular diagnostic kits, and Lunaphore's COMET spatial platform — a portfolio deliberately optimized for long-term multi-omics leadership rather than near-term profit. The honest read is that this segment is an option on the future of spatial biology, and options cost money to hold.

Why is spatial biology worth holding an expensive option on at all? Because it addresses a limitation that has dogged molecular biology for decades. For a generation, the dominant way to measure gene and protein activity was to homogenize a tissue sample — to blend it into a smoothie — and measure the average. But a tumor is not an average; it is a battlefield of distinct cell populations, some cancerous, some immune, some structural, all interacting across microscopic distances. Blending the tissue destroys exactly the information a modern cancer researcher most wants: which cell is doing what, next to which neighbor. Spatial biology preserves that map. RNAscope reads the RNA in place; COMET reads dozens of proteins in place on the same slide. Together they let a pathologist or drug developer see the tumor microenvironment as a living architecture rather than a chemical average. The market is betting this becomes standard practice not just in research but eventually in clinical diagnosis — which is why relatively small revenue lines command relatively large strategic value. The bet is real, and so is the risk that adoption comes slower, and costs more, than the optimists model.

Run the whole enterprise through Hamilton Helmer's 7 Powers and three powers stand out clearly, while the rest are weaker than the bull case implies. Switching costs are the dominant power, and genuinely formidable: reagents validated into published papers and regulatory filings cannot be swapped without re-validation risk, which is why demand is so price-insensitive. Branded reputation and cornered resources come second — "R&D Systems" is shorthand for purity, and RNAscope is a patent-protected proprietary technology that competitors cannot simply copy. Scale economies are real but only moderate: a catalog spanning something on the order of half a million biological tools, distributed through one global sales force, gives Bio-Techne breadth few can match, but the reagent business is not a natural monopoly the way a network is. Notably, the company has no network-effects power and only limited process power — a useful corrective to the temptation to call this an unassailable franchise.

Porter's Five Forces sharpens the same picture. The bargaining power of buyers is low-to-moderate: researchers face real budget pressure, especially when NIH funding tightens, but they cannot casually substitute a generic reagent for a validated one without risking their results, which blunts their leverage. The threat of new entrants is low bordering on trivial in the core: replicating a library of tens of thousands of validated antibody clones, each with a forty-year record of batch-to-batch consistency, is close to impossible to do quickly at any price — the barrier is time itself. But competitive rivalry is intense and rising, which is the part of the story the moat narrative tends to underplay. Bio-Techne is no longer a niche player left alone; it is squeezed between multi-billion-dollar conglomerates. Thermo Fisher and Merck KGaA (via Sigma-Aldrich) are giants of scale. And in late 2023, Danaher acquired Abcam — Bio-Techne's most direct antibody competitor — for $5.7 billion, folding a primary rival into one of the most feared operating machines in the industry.[^3] It is worth naming what these giants can and cannot do to Bio-Techne, because it sharpens where the moat holds. What scale competitors can do is compete on distribution, on price for undifferentiated products, and on bundling — offering a lab a one-stop catalog so broad that convenience alone wins the order. What they cannot easily do is dislodge a specific R&D Systems antibody clone that a customer has already written into a validated protocol, because that is a switching-cost problem no amount of scale solves. So the competitive reality is asymmetric: Bio-Techne is highly defensible in its installed base of validated products and increasingly contested at the margin for new experiments, where a researcher starting fresh might reasonably choose an Abcam-via-Danaher or a Sigma-Aldrich product instead. The moat protects the past better than it guarantees the future — which is precisely the kind of nuance a promotional account glosses over and a serious investor must hold onto.

The moat around the reagents is deep. The moat around the company is contested. That tension is precisely what a new CEO inherited in 2024.

VI. Squeezing the Portfolio: Kim Kelderman's Cleanup & the Biopharma Funding Winter

Succession at a founder-shaped company is always a test, and Bio-Techne handled it with unusual calm. On February 1, 2024, Kim Kelderman took over as president and chief executive as Chuck Kummeth retired, having been named the successor the previous November.[^12] There was no drama this time, no shareholder revolt — just a planned handoff to an insider who had been running the Diagnostics and Genomics segment and who, like Kummeth, carried the Thermo Fisher pedigree, having spent years leading the Genetic Sciences Division there. Kelderman's compensation was structured to tell him exactly what the board wanted: reporting suggests his incentives were split roughly half against company-wide organic revenue growth and half against adjusted operating earnings, aligning him to grow the top line without surrendering the historic margin profile.

He inherited a company that needed two things: a portfolio cleanup and a steady hand through a genuinely nasty market. The cleanup came first, and its centerpiece was finally severing the Exosome Diagnostics albatross in September 2025, retaining the underlying exosome intellectual property for future kit development while offloading the money-losing clinical lab operation.[^9] Purely as accounting, it was a small transaction; as a signal, it mattered. It removed a chronic margin drag from the Diagnostics and Spatial Biology segment and demonstrated that this management team would prune, not just plant.

The harder problem was the macro environment, and it is the crux of why the Merck deal happened when it did. After the COVID-era boom flooded biotech with capital, the tide went out with a vengeance. Early-stage biotech venture funding dried up; big pharma launched sweeping cost-rationalization programs; and China — long a growth market for Western tools makers — slowed under macroeconomic pressure and policies favoring local sourcing. For a company whose customers are, quite literally, the people doing biology experiments, a funding winter among those customers hits directly. It helps to break the customer base into its constituent tribes, because each behaved differently and the aggregate number hides the story. Bio-Techne sells into four broad end markets: large pharmaceutical companies, emerging biotech, academia, and — geographically — China as a category of its own. During the funding winter these diverged sharply. Large pharma stayed resilient, even strong, because its research budgets are funded by the cash flows of marketed drugs rather than by capital markets; by fiscal 2026 this segment had strung together six consecutive quarters of double-digit growth for Bio-Techne.[^11] Emerging biotech, by contrast, lives and dies on venture funding and IPO windows, and when that capital vanished, its spending on reagents and instruments followed with a lag. Academia sat in between, hostage to government science budgets — in the United States, to the trajectory of NIH funding, grant approval rates, and even the disruption of a government shutdown that briefly froze grant outlays.[^11] China, long a reliable growth engine, slowed under a combination of macroeconomic weakness and a national push toward local sourcing that disadvantaged Western suppliers, before stabilizing and returning to modest growth by 2026.[^11]

The critical mechanism to understand is the lag. Funding does not translate into reagent purchases the instant a biotech raises money; there is typically a two-to-three-quarter delay between a funding rebound and the resulting customer spending, as newly capitalized companies staff up and spin up programs before they start buying consumables in volume. That lag is the source of both management's optimism and its repeated forecasting stumbles: funding metrics turned up sharply through 2025, which should mechanically pull spending up in the following quarters, but calling the exact quarter of inflection proved genuinely difficult. Organic growth, which had run in the double digits during the boom, decelerated to a crawl and then, in the most recent quarter, briefly turned negative.

The live version of that struggle is audible in the fiscal third-quarter 2026 earnings call on May 6, 2026, which is worth listening to closely because it reveals how management handles a miss. Revenue came in at $311.4 million, down 2% on both a reported and organic basis; adjusted EPS was $0.53, down three cents year over year, while GAAP EPS actually rose to $0.32 from $0.14.[^11] But the texture beneath the headline is where the credibility test lives. The quarter carried roughly a 400-basis-point self-inflicted headwind from order timing — two large cell-therapy customers had received FDA Fast Track designation, which paradoxically reduced near-term demand for Bio-Techne's GMP reagents because those customers had already stocked up, plus a large OEM order that slipped into an earlier quarter. Strip those out, and underlying organic growth was a positive 2%.

What is genuinely telling is management's candor about being wrong. Emerging biotech revenue fell high-single-digits — worse than the company had guided — and rather than blame the weather, Kelderman owned it directly: "the biotech end market was indeed our surprise," he told analysts, before walking through exactly why. Biotech funding had rebounded sharply, up over 90% and 50% in successive quarters, which had led the team to expect stabilization; instead, dissecting the data revealed that the mix had shifted, with funding pouring into late-stage clinical work (rising to about 82% of the total from 75%) while early-stage discovery — where Bio-Techne's core reagents are most exposed — actually shrank.[^11] CFO Jim Hippel's self-critical line — that the team "got the cart a little too far ahead of the horse" on calling the biotech bottom — is the kind of specific, non-defensive explanation that earns analytical benefit of the doubt.

There were real bright spots that complicate any simple "maturing business" verdict. Spatial biology grew mid-teens, with the COMET platform up over 65% and exiting the quarter at record backlog; GMP proteins for cell therapy grew nearly 50% year over year excluding the two Fast Track customers; large pharma delivered a sixth straight quarter of double-digit growth; and China posted its fourth consecutive quarter of positive growth.[^11] Management also leaned hard into an AI narrative — arguing that its five decades of proprietary biological data create a defensible training-data moat and that every AI-generated drug hypothesis ultimately requires physical reagents to validate. That is a plausible and even elegant thesis, but it remains largely a claim about future demand rather than a proven revenue driver, and a skeptical investor should file it under "watch," not "bank." There is also a disciplined-operator subplot in Kelderman's tenure that a credibility-focused investor should note. Rather than chase acquisitions to paper over slowing organic growth — the classic temptation for a management team under pressure — Bio-Techne largely held its fire on dilutive M&A, kept leverage well below one turn of EBITDA, and leaned on cost containment and a portfolio simplification (collapsing ten brands down to three: R&D Systems, Bio-Techne Spatial Biology, and Bio-Techne Diagnostics) to protect margins.[^11] The brand consolidation was more than housekeeping; it was an attempt to make the sprawling catalog legible to customers navigating from discovery through to the clinic, and — management argued — more discoverable to the AI-driven search tools that increasingly mediate how scientists find reagents. Whether that pays off is unproven, but the instinct to simplify rather than sprawl during a downturn is the behavior of a team managing for durability rather than optics.

Either way, a management team defending sector-leading margins through a downturn while being unusually transparent about its misses is exactly the profile that makes a company an attractive, low-drama acquisition target. Which brings us to the buyer.

VII. The $11.3 Billion Capstone: Merck KGaA's Mega-Acquisition & Valuation Comps

Consolidation in life-science tools tends to arrive in waves, and by mid-2026 the water was rising. Danaher had taken Abcam. Thermo Fisher kept buying. The strategic logic of scale — one global sales force carrying an ever-larger catalog — was pulling the industry toward a handful of giants. Into that current stepped Merck KGaA, and on June 25, 2026, it announced the definitive agreement to acquire Bio-Techne for $73.00 per share in cash.1

To understand the buyer is to understand why the price was set where it was. Merck KGaA is not a private-equity raider chasing a quick flip; it is a family-controlled, investment-grade industrial house with three legs — healthcare, electronics, and life science — and a long institutional memory of what happens when you overpay. Its life-science division had been built around the 2015 Sigma-Aldrich deal, and the years since had taught it both the power of a broad reagent catalog and the difficulty of staying at the technological frontier through internal R&D alone. Buying frontier capability, when the price is right, is often cheaper and faster than building it. That framing matters because it explains Merck's evident discipline on multiple: this was a strategic acquirer that could afford to walk away, negotiating against a seller whose growth was cyclically depressed, and the resulting price reflects that balance of power rather than an auction frenzy.

Merck's rationale was less about cost-cutting than about filling a specific hole in its shelf. Through Sigma-Aldrich, the Darmstadt company already owned one of the largest catalogs of laboratory chemicals and reagents on earth — but it lacked the cutting-edge franchises Bio-Techne had spent a decade assembling. It had no answer in high-end spatial biology to rival Lunaphore's COMET and ACD's RNAscope, and no automated protein-analysis platform comparable to the ProteinSimple instruments. Executive board member and Life Science CEO Jean-Charles Wirth framed the deal as strengthening Merck's presence "in exciting, fastest-growing life sciences areas including multi-omics and cell therapy," while group CEO Kai Beckmann called it "an important milestone" in the company's long-term strategy.1 The synergy math was concrete and, revealingly, weighted toward revenue rather than cuts: Merck guided to roughly €140 million in annual cost synergies to be fully realized by the third year after closing, primarily by pushing Bio-Techne's products through its vastly larger global distribution and clinical-customer network. Management said the deal would be immediately accretive to sales growth and EBITDA margin, and accretive to earnings per share by year three, financed through existing cash and new debt while preserving Merck's investment-grade rating.1 The transaction was expected to close in late 2026 or early 2027.

Now the question that matters for anyone judging the deal: did Merck overpay? The honest answer requires a comparison, and the natural one is Danaher's purchase of Abcam, announced in August 2023, at roughly $5.7 billion — a price that worked out to something like 12 times revenue and, on some estimates, north of 30 times adjusted EBITDA.[^3] Against that yardstick, Bio-Techne's ~9.3 times FY2025 revenue and ~26 times adjusted EBITDA looks not extravagant but disciplined.1[^2] Merck paid a lower multiple than Danaher did for a smaller, arguably less differentiated competitor.

There is a subtler point buried in the timing. Merck was buying at a cyclical trough. Bio-Techne's growth was temporarily depressed by the funding winter, which meant the trailing EBITDA the multiple was calculated against was suppressed relative to the company's demonstrated earning power at 42%-plus segment margins. If biopharma spending normalizes and spatial biology scales as management expects, the effective multiple on normalized earnings would be lower still, and the €140 million synergy target would drop almost entirely to the bottom line. That is the bull case for the buyer. The bear case is equally real and should not be waved away: Merck is paying a full price, in cash, for an asset whose most recent organic growth was negative, whose core reagent business is maturing, and whose growth engine competes in a capital-intensive arms race. A cyclical trough can also be a structural plateau, and only time distinguishes them.

One overhang worth flagging in the neutral spirit of this analysis: a cross-border acquisition of this size is not a closed matter on announcement day. The deal was expected to close in late 2026 or early 2027, subject to Bio-Techne shareholder approval and antitrust and regulatory clearances across multiple jurisdictions.1 Given the overlap between Merck's Sigma-Aldrich reagent catalog and Bio-Techne's, competition authorities in the United States and Europe will scrutinize whether the combination concentrates too much of the research-reagent market under one roof — a live question rather than a formality, particularly in an era of heightened antitrust attention to life-science consolidation. For arbitrage-minded investors, the spread between the trading price and the $73 offer is the market's real-time verdict on that closing risk; for the long-term observer, the regulatory review is simply a reminder that the deal is a process, not yet a fact.

What is not in dispute is that Bio-Techne's shareholders were handed a large, certain premium — and that certainty, at that moment in the cycle, is the heart of the strategic logic on the seller's side.

VIII. The Playbook: Key Strategic and Investing Lessons

Great business stories are worth reading twice — once for the narrative and once for the transferable principles. Bio-Techne's four-decade arc yields a handful of lessons durable enough to carry into the analysis of entirely different companies, and each is grounded in something concrete that actually happened here rather than in aphorism.

Lesson one: in some industries, the reagent is the standard. The deepest moats are not always technological; sometimes they are institutional. Bio-Techne's core advantage was that its products became embedded in the permanent record of science — published papers, regulatory filings, validated protocols — so that switching suppliers meant re-validating conclusions rather than merely re-ordering. That converts a commodity input into a pricing-power fortress capable of sustaining 50%-plus margins for decades. The investing tell is a business whose product, once adopted, becomes prohibitively expensive to un-adopt for reasons that have nothing to do with the product's price.

Lesson two: own the instrument, control the consumable. The ProteinSimple and Lunaphore acquisitions worked because placing a proprietary instrument in a lab manufactures years of captive, high-margin consumable demand. This razor-and-blade dynamic is one of the most reliable value-creation engines in all of instrumentation, and Bio-Techne's decade-long pivot toward it was the single most important strategic decision of the Kummeth era. The caution: it only works when the consumables are genuinely proprietary and the installed base is sticky; a machine that runs generic reagents is just capital equipment.

Lesson three: stay inside your business model. The Exosome Diagnostics debacle is the counter-example that proves the first two lessons. A CLIA clinical laboratory — with its insurance coding, billing departments, reimbursement fights, and clinical sales force — is a fundamentally different animal from an OEM tools manufacturer, and roughly a quarter-billion dollars of shareholder capital paid the tuition on that distinction. The lesson is not that diversification is bad; it is that adjacency on a slide deck ("we already work in diagnostics!") can conceal a total mismatch in the operating machinery a business actually requires.

Lesson four: certainty has a price, and cyclical bottoms are when it is cheapest to sell. Negotiating an all-cash exit at a 36% premium during a biopharma spending slowdown let long-term shareholders lock in a substantial, guaranteed return before any macro recovery had materialized — transferring the execution and timing risk of that recovery to Merck.1 Whether that was brilliant or merely prudent depends entirely on what happens to the sector next, which is unknowable today. But as a matter of decision-making under uncertainty, converting a contested, cyclical equity story into $73 of certain cash is a defensible act of discipline, not a failure of nerve.

There is a final, broader lesson embedded in the whole forty-year arc, and it concerns the relationship between a moat and its owner. Bio-Techne's reproducibility moat was largely inherited from the founders and the R&D Systems scientists who spent decades perfecting the manufacture of proteins; no CEO created it. What each era of management did control was how hard the moat was worked. Oland proved that an owner can under-earn a magnificent asset by refusing to invest, converting a growth business into a static one. Kummeth proved that the same asset, aggressively commercialized and extended through instruments and acquisitions, could grow into something far larger — while also proving, via Exosome Diagnostics, that not every extension respects the boundaries of the core competence. Kelderman proved that knowing when to prune, when to hold discipline, and ultimately when to sell can be as value-creating as any acquisition. The moat was the constant. The stewardship was the variable. For investors, that is the enduring takeaway: a great asset is necessary but not sufficient, and the returns a business ultimately delivers depend as much on the judgment of the people allocating its capital as on the quality of the fortress they inherited. The mirror image of that decision is the buyer's wager — and reasonable people can look at the same facts and reach opposite conclusions, which is exactly what the bull and bear cases do.

IX. Analysis: Bull vs. Bear Case & Activist Stress Test

Set the two views side by side and war-game them, because the gap between them is where the real analysis lives.

The bull case — essentially Merck's thesis — rests on complementarity and scale. Bio-Techne's portfolio slots into gaps in Merck's shelf almost without overlap: spatial biology, automated protein analysis, and GMP-grade cytokines for cell and gene therapy are precisely the fast-growing adjacencies a Sigma-Aldrich-anchored catalog lacked. Run Bio-Techne's differentiated products through Merck's far larger global commercial engine — more sales reps, more clinical accounts, deeper reach in geographies where Bio-Techne is subscale — and the same products should sell in greater volume than they ever could standalone. If biopharma funding normalizes and spatial biology migrates from research curiosity toward standard clinical practice, then $11.3 billion for a franchise earning 42%-plus core segment margins will, in a few years, look cheap. The COMET platform's 65% growth and record backlog, and the near-50% growth in GMP proteins, are cited as evidence the growth engines are already firing beneath the cyclical noise.[^11]

The bear case explains why Bio-Techne was smart to sell into that thesis rather than run it out alone. The core reagent business is maturing; its organic growth has slowed to a crawl and, in the latest quarter, gone negative.[^11] Danaher's absorption of Abcam created a formidable, well-capitalized integrated competitor squarely aimed at Bio-Techne's antibody heartland.[^3] And spatial biology — the growth story on which the premium valuation depends — is a capital-intensive battlefield contested by 10x Genomics, Bruker (which bought NanoString out of bankruptcy), and Akoya, where staying competitive demands continuous, margin-diluting R&D with no guarantee of winning. Against that backdrop, a guaranteed $73 in cash removes the execution risk of a multi-year, contested recovery dependent on variables — Chinese demand, biotech capital markets, the pace of clinical adoption — entirely outside management's control. Selling was not capitulation; it was risk transfer at a good price.

Now the activist stress test — what would a skeptical long/short investor have challenged before the deal, and where do those critiques land? Three lines of attack stand out. First, capital allocation: the Exosome Diagnostics round trip destroyed roughly a quarter-billion dollars, and an activist would rightly ask whether the same acquisitive impulse that produced ACD and Lunaphore also produced an avoidable, undisciplined blunder — the record is genuinely mixed, not uniformly excellent. Second, portfolio complexity and margin dilution: the Diagnostics and Spatial Biology segment's operating margin had fallen to 7.5%, dragging consolidated returns while management asked shareholders to fund an option on the future; a skeptic would question how long that option should be held at the expense of near-term profit.7 Third, narrative versus proof: the AI-and-data-moat story management leaned on in 2026 is attractive but unproven in the financials, and an activist would press for evidence that it is a revenue driver rather than an investor-relations frame.

Weighing it honestly, the fairest verdict is that Bio-Techne owned a genuinely elite core asset wrapped in a growth strategy of contested economics, and management chose — defensibly — to monetize the whole package at a cyclical low rather than bet shareholders' capital on winning the spatial-biology war alone. Whether that was the right call will be settled not in Bio-Techne's results but in Merck's, which is where the forward-looking investor's attention now shifts.

X. Epilogue & Key KPIs to Track

The Bio-Techne story, as an independent public company, is drawing to a close; if the deal closes as expected around the turn of 2026 into 2027, the ticker TECH will disappear into the vast machinery of Merck KGaA.1 But the underlying business will keep running, and its performance will now serve as the proof-of-thesis for one of the largest life-science acquisitions of the decade. For anyone tracking whether Merck's bet pays off — or watching the sector for what this deal implies — three key performance indicators matter more than any others, and each maps directly to one leg of the deal's logic.

First, synergy realization against the €140 million target. This is the cleanest scorecard on the deal's financial premise. Because the synergies are weighted toward revenue — pushing Bio-Techne's products through Merck's distribution — rather than pure cost-cutting, delivering them requires genuine commercial integration, which is harder and slower than closing plants. Progress against that number, and the timeline to full realization by year three, is the single most direct measure of whether Merck is extracting the value it paid for.1

Second, spatial biology instrument placements — specifically the COMET installed base and backlog. This is the growth vector on which the entire premium valuation rests. The relevant question is not quarterly revenue but the trajectory of placements within Merck's global account network: is COMET moving from research labs toward routine clinical and translational use, and is the installed base compounding the consumable pull-through that makes the razor-and-blade model work? The 65%-plus growth and record backlog reported in fiscal 2026 set the baseline to beat.[^11]

Third, GMP-grade cytokine growth tied to cell and gene therapy manufacturing. This is the highest-quality growth in the portfolio and the one most insulated from the research-funding cycle, because it scales with clinical progress and, ultimately, commercial manufacturing of approved therapies rather than with grant budgets. Watching contract wins with clinical-stage developers — and the reported near-50% underlying growth normalizing as the Fast Track order-timing noise rolls off — will show whether Bio-Techne's reagents ride the cell-therapy wave from the lab into the factory.[^11]

Deliberately, none of these three KPIs is a headline like "total revenue" or "EPS," because those aggregate numbers will soon be buried inside Merck's far larger results and will tell an outside observer little about whether this specific bet is working. The three chosen metrics each isolate one pillar of the deal's thesis — the synergy pillar, the spatial-growth pillar, and the cell-therapy pillar — so that a patient observer can grade the acquisition on its own terms rather than on the fog of consolidated accounting. If synergies land, COMET compounds, and GMP proteins scale, Merck will look to have bought a premier asset at a cyclical discount. If synergies slip, spatial adoption stalls, and cell-therapy demand disappoints, the same $11.3 billion will look like a top-of-market price paid for a business whose best growth was already behind it. The evidence will accumulate quarter by quarter, and the honest analyst's job is to keep score without deciding the verdict in advance.

From Dr. Roger Lucas's quiet antibody laboratory in 1976 Minneapolis to an $11.3 billion cash sale to a 358-year-old German house, Bio-Techne traveled an improbable distance on the strength of a single, unglamorous idea: that in biology, trust is the scarcest input, and the company that manufactures it can charge whatever trust is worth. It built a fortress out of reproducibility, nearly let it rust from under-management, rebuilt it into a platform through a decade of disciplined and occasionally flawed M&A, and finally sold it — at a premium, in cash, at the bottom of a cycle — to a buyer betting the fortress is worth even more inside a larger empire. Whether that bet succeeds is now Merck's story to tell. The lesson Bio-Techne leaves behind is older and simpler: the most durable moats in modern science are not always the cleverest technologies, but the reputations that competitors cannot manufacture and customers cannot afford to abandon.

References

-

Merck KGaA, Darmstadt, Germany, Agrees to Acquire Bio-Techne, Strengthening Leadership Position in Fast-Growing Life Sciences Markets — PR Newswire / Merck KGaA, 2026-06-25 ↩↩↩↩↩↩↩↩↩↩

-

Techne Corporation Announces Retirement of Thomas Oland; CFO Gregory Melsen To Assume CEO Duties on an Interim Basis — PR Newswire / Techne Corporation, 2012 ↩↩

-

Board of Directors Appoints Charles Kummeth as Chief Executive Officer and Director of Techne Corp. — Techne Corporation (SEC EDGAR 8-K), 2013-03-18 ↩

-

Bio-Techne Announces Agreement To Acquire ProteinSimple — PR Newswire / Bio-Techne, 2014 ↩

-

Bio-Techne Announces Agreement To Acquire Advanced Cell Diagnostics — PR Newswire / Bio-Techne, 2016-07-06 ↩

-

Mdxhealth Announces Closing of Exosome Diagnostics Acquisition from Bio-Techne — GlobeNewswire / MDxHealth, 2025-09-15 ↩

-

Bio-Techne Corporation SEC EDGAR Filer Profile (Form 10-K segment reporting, fiscal 2024) — US Securities and Exchange Commission ↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube