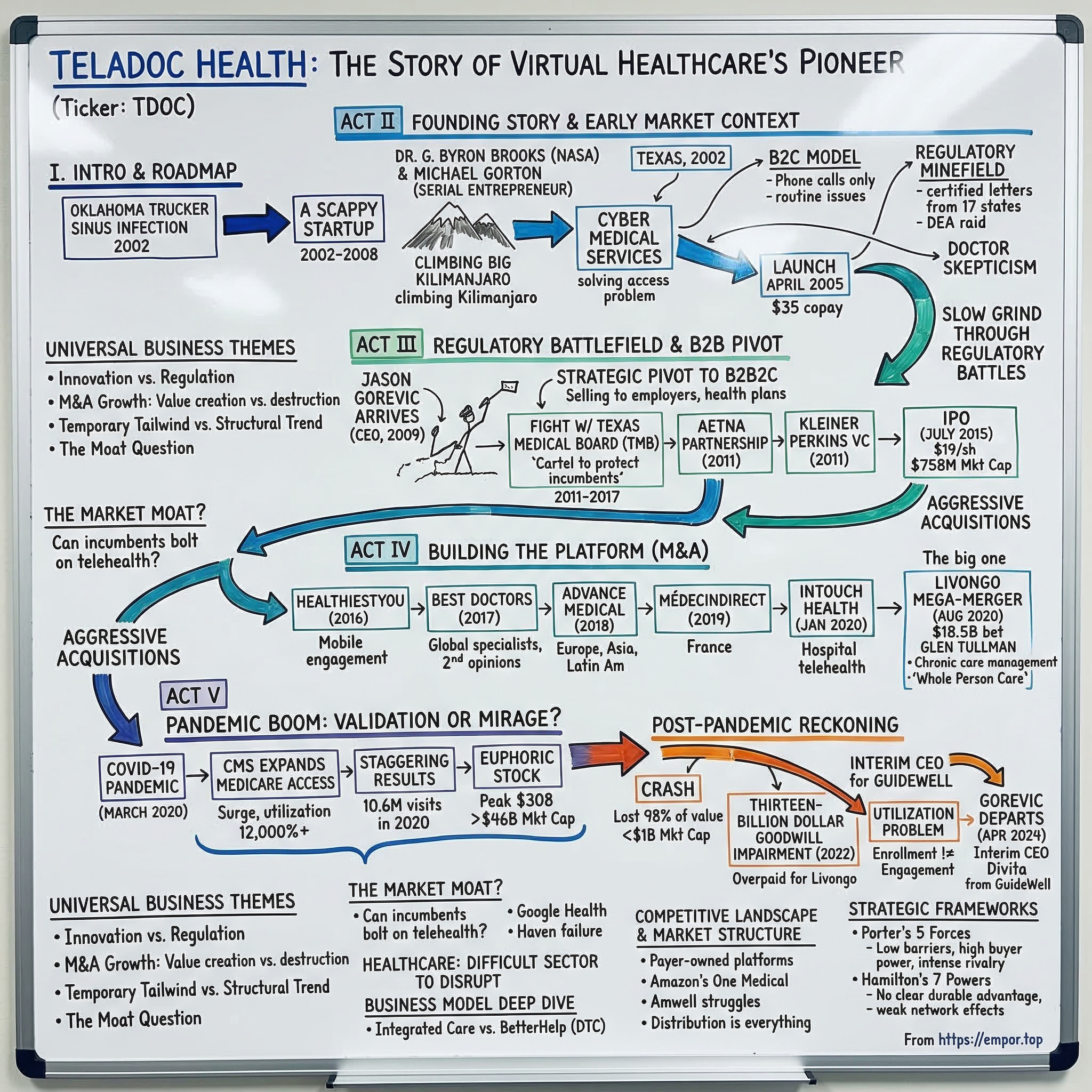

Teladoc Health: The Story of Virtual Healthcare's Pioneer

I. Introduction & Episode Roadmap

Picture this: a long-haul trucker somewhere in rural Oklahoma, parked at a rest stop at two in the morning, suffering from a brutal sinus infection. The nearest urgent care clinic is forty miles away and will not open until morning. The nearest emergency room will cost him a thousand dollars and half a night's sleep. In 2002, two entrepreneurs in Dallas, Texas looked at that trucker and saw the future of medicine—a future where a doctor could be summoned with a phone call, anytime, anywhere, for the price of a copay.

That company was Teladoc. Over the next two decades, it would grow from a scrappy startup that most of the medical establishment considered illegal into the world's largest virtual healthcare company, serving over ninety million members across more than a hundred and seventy countries. It would go public, execute an aggressive acquisition spree, and ride a global pandemic to a market capitalization exceeding forty-six billion dollars. Then it would lose ninety-eight percent of its value.

The Teladoc story is one of the most dramatic rise-and-fall arcs in modern healthcare—and arguably in all of technology investing. It touches on nearly every big theme that matters to business builders and investors: the tension between innovation and regulation, the promise and peril of M&A-driven growth, the difference between a temporary tailwind and a structural trend, and the fundamental question of whether telehealth is a standalone business or merely a feature that incumbents can bolt on whenever they choose.

The company's journey breaks naturally into distinct acts. There is the founding myth—a contrarian bet placed in an era when most states considered virtual medicine illegal. There is the slow, grinding climb through regulatory battles and the strategic pivot from selling to individual consumers to selling through employers and health plans. There is the IPO, followed by an aggressive acquisition strategy designed to transform Teladoc from a simple video-visit provider into a comprehensive virtual care platform. There is the Livongo mega-merger—an eighteen-and-a-half-billion-dollar bet on chronic care management that represented either strategic brilliance or peak-cycle hubris. There is the COVID-19 pandemic, which seemed to validate the entire thesis overnight. And then there is the reckoning—the crash, the thirteen-billion-dollar goodwill impairment, the leadership shakeup, and the existential question that still hangs over the company.

The themes running through this story are universal. How do you build network effects in healthcare, an industry where the customer, the payer, and the patient are often three different entities? When does acquisition-driven growth create value versus destroy it? How do you distinguish between a secular shift and a temporary surge of demand? And perhaps most importantly: in a market where UnitedHealth, CVS, Amazon, and every major hospital system can launch telehealth with the flip of a switch, what exactly is the moat?

Healthcare is one of the most difficult sectors in the American economy to disrupt. It is regulated at the state and federal level, reimbursed through byzantine insurance mechanisms, resistant to consumer-driven change, and structurally designed to protect incumbents. The companies that have tried to disrupt it—from Google Health to Haven, the joint venture between Amazon, Berkshire Hathaway, and JPMorgan that lasted barely three years—have a dismal track record. Teladoc was supposed to be different. For a brief, euphoric moment, it looked like it was.

Let us find out what happened.

II. The Founding Story & Early Market Context (2002-2008)

Around the year 2000, two men found themselves hiking up Mount Kilimanjaro in Tanzania, deep in conversation about a problem that had nothing to do with African peaks. Dr. G. Byron Brooks was a former NASA flight surgeon and United States Air Force medical officer who held the unusual combination of an electrical engineering degree and a medical doctorate—a man who thought about medicine as a systems problem. Michael Gorton was a serial entrepreneur who had recently sold an internet service provider that developed the world's first commercial DSL connection in a deal worth a hundred and twenty-two million dollars. Together, they began sketching out what they called "Cyber Medical Services"—the idea that modern telecommunications could solve one of American healthcare's most persistent failures: access.

The insight was deceptively simple. Tens of millions of Americans—particularly those in rural communities, those working mobile jobs like long-haul trucking, and those simply unable to get a timely appointment—faced a miserable choice whenever they came down with something routine. A sinus infection, an ear infection, a urinary tract infection, allergies acting up. They could wait days or weeks for a doctor's appointment, suffer through it, or go to an emergency room and pay ten to twenty times what the visit was worth. Brooks and Gorton believed that for a large category of straightforward, non-emergency medical issues, a phone call with a licensed physician could deliver the same outcome as an office visit—at a fraction of the cost and without the wait.

They incorporated TelaDoc Medical Services Inc. in Dallas, Texas in 2002. A third co-founder, Dr. Bruce Begia, a San Antonio family physician, joined early to help build the clinical model. But the actual launch would not come for three years, because the founders ran headlong into a wall that would define the company's first decade: in most of the United States, what Teladoc was proposing was essentially illegal.

The problem was rooted in state medical licensing laws written long before anyone imagined a doctor treating a patient without physically touching them. The legal doctrine in most states held that a physician-patient relationship required an in-person examination before a doctor could diagnose a condition or prescribe medication. A physician licensed in Texas could not legally treat a patient sitting in Oklahoma. And since Teladoc's entire model depended on connecting patients with doctors remotely—often across state lines—the regulatory landscape was a minefield.

Michael Gorton later recounted that seventeen states sent certified letters informing him that his company's activities were illegal and that he could go to prison. The DEA at one point raided Teladoc's offices. In a twist that Gorton loved to tell audiences about, some of those same DEA agents eventually became Teladoc customers.

When Teladoc finally launched publicly in April 2005 at the Consumer Directed Health Care Conference in Chicago, it was described by trade press as the only company in the country focused solely on offering telephone medical consultations. The model was deliberately simple: patients registered online, completed a detailed medical history form—which established the legal pre-existing patient record necessary to work around the in-person examination requirements—and then could call a toll-free number to speak with a board-certified physician licensed in their state.

Consultations covered non-urgent issues: allergies, bronchitis, sinus infections, pink eye, and similar acute but minor conditions. Doctors could prescribe medications, excluding controlled substances, and recommend follow-up care. The pricing was remarkably accessible—a monthly membership fee of around four dollars for individuals, a one-time registration fee of eighteen dollars, and a per-consultation fee of thirty-five dollars. Of that thirty-five dollars, roughly twenty went to the physician.

This was the pre-smartphone era. There were no video calls, no apps, no wearables. Teladoc was a phone-only service, and that was actually a strategic advantage. Broadband penetration in rural America was still limited, but phone networks were universal. The technology limitation—no video meant physicians could not visually assess patients—inflamed the skepticism of the traditional medical establishment, but it also meant the service worked for anyone with a telephone.

By the end of 2005, Teladoc had roughly twenty thousand members. By the end of 2007, that number had grown to approximately one million, driven largely by early employer partnerships. AT&T was among the first major corporations to offer Teladoc as an employee health benefit, recognizing that steering routine medical visits away from emergency rooms could meaningfully reduce healthcare spending. The seeds of the B2B model that would eventually define the company were already being planted.

But the early years were a grind. Doctors were deeply skeptical—the medical community viewed phone-only consultations as inherently inferior and potentially dangerous. Insurance companies would not reimburse for telehealth visits. By 2010, only eleven states had mandated that insurance payers cover telemedicine services, and even in those states implementation was inconsistent. The Ryan Haight Act of 2008 further restricted remote prescribing of controlled substances, reflecting the broader regulatory hostility toward virtual medicine.

Teladoc survived these years on the strength of its direct employer contracts and the sheer stubbornness of its founders, who believed that the regulatory environment would eventually catch up to the logic of their model. The company raised its first significant venture capital round—nine million dollars led by HLM Venture Partners—in 2009, bringing total outside funding to a still-modest level for a company with national ambitions. Revenue remained small, the path to profitability was nowhere in sight, and the medical establishment remained broadly hostile.

But the founders had identified something real. The American healthcare system was failing at access—not because there were not enough doctors in aggregate, but because the distribution of those doctors did not match the distribution of patients. Rural communities, shift workers, parents with sick children at midnight, elderly patients with mobility challenges—millions of people faced structural barriers to seeing a physician that had nothing to do with their ability to pay. A phone call that could triage symptoms, prescribe antibiotics for a straightforward infection, or recommend an emergency room visit for something serious was not a replacement for primary care. It was filling a gap that the healthcare system had been ignoring for decades.

They were right—it would just take much longer than anyone expected, and the path would run through courtrooms, state capitols, and one very contentious fight with the Texas Medical Board.

III. The Regulatory Battlefield & B2B Pivot (2009-2014)

In June 2009, a new CEO arrived who would lead Teladoc for the next fifteen years and transform it from a niche telehealth startup into a multi-billion-dollar public company. Jason Gorevic came from WellPoint—the Fortune 50 health insurer now known as Elevance Health—where he had served as Senior Vice President and Chief Marketing and Product Officer. He understood how large health plans and employers thought, what they bought, and why. His arrival signaled that Teladoc was serious about enterprise scale.

Gorevic's timing coincided with a critical strategic shift. The direct-to-consumer model—individual patients signing up and paying out of pocket—had obvious scaling limits. Customer acquisition costs were high, consumer awareness was low, and without insurance coverage there was friction at every point of purchase. The decisive pivot was toward B2B2C: selling to self-insured employers and health plans, who would then offer Teladoc as a benefit to their covered populations.

This was elegant in its simplicity. The employer paid a per-member-per-month subscription fee for all covered employees, regardless of whether they actually used the service. Teladoc got predictable, recurring revenue. Member acquisition cost dropped effectively to zero because employers pushed enrollment through their HR communications. And employers got a cost containment tool—every visit routed to Teladoc instead of an emergency room saved the self-insured employer hundreds of dollars.

But the regulatory battles were far from over. The most sustained fight was with the Texas Medical Board, which became a national test case for whether state medical boards could use their regulatory power to block telehealth competition. In October 2010, the TMB amended its telemedicine regulations to effectively exclude phone-only consultations by requiring that providers be able to "see and hear" the patient in real time.

The dispute escalated through 2011. When a Texas Court of Appeals ruled in Teladoc's favor at the end of 2014, the TMB responded just two weeks later with an emergency rule prohibiting physicians from prescribing medication via telehealth without first meeting the patient in person. Teladoc responded with an antitrust lawsuit in federal court, alleging the board was acting as a cartel to protect incumbent physicians from competition. A federal judge issued a preliminary injunction blocking enforcement of the TMB rule, and the Federal Trade Commission itself filed an amicus brief taking Teladoc's side. Texas eventually passed legislation in 2017 allowing first-time patient visits via telemedicine without a prior in-person meeting, and Teladoc dropped its lawsuit.

This fight mattered far beyond Texas. It established a legal and political precedent that state medical boards could not simply legislate telehealth out of existence, and it gave Teladoc credibility as a company willing to fight the regulatory wars that others would not.

Meanwhile, the commercial momentum was building. In 2011, Aetna—one of the three largest U.S. health insurers—began offering Teladoc for its fully insured members, starting in Florida and Texas and eventually expanding nationwide. That same year, Kleiner Perkins Caufield & Byers led an eighteen-million-dollar funding round, lending Silicon Valley's most prestigious venture imprimatur to the company.

By 2013, revenue had reached roughly twenty million dollars, and Teladoc made its first acquisition—Consult A Doctor for nearly seventeen million dollars—to expand its reach to smaller businesses. The following year, revenue more than doubled to forty-three and a half million dollars, powered by partnerships with Blue Shield of California, Oscar Health, and major employers like Home Depot and T-Mobile.

The competitive landscape was beginning to take shape. American Well, founded in 2006 by physician brothers Ido and Roy Schoenberg in Boston, took a different approach—focusing on video-based consultations and building a white-label platform that hospitals could brand as their own. Doctor on Demand launched in late 2013 with a consumer-first, video-first model and the marketing firepower of television personality Dr. Phil's son, Jay McGraw. MDLIVE competed directly with Teladoc for B2B2C contracts. But the investor consensus as of 2014 favored the employer-distribution model—recurring subscription revenue was more predictable, and the employer channel gave Teladoc a built-in growth flywheel.

By early 2015, Teladoc had ten and a half million members served through four thousand clients, including a hundred and sixty Fortune 1000 companies. The question was no longer whether virtual care could work—it was how fast it could scale.

On July 1, 2015, Teladoc became the first pure-play telemedicine company to list on the New York Stock Exchange, pricing its IPO at nineteen dollars per share—above the revised range, reflecting strong institutional demand. The offering was upsized to accommodate oversubscription, raising roughly a hundred and fifty-seven million dollars. On its first day of trading, shares opened near thirty dollars and closed at twenty-eight fifty, a fifty percent pop. The market cap stood at approximately seven hundred and fifty-eight million dollars.

The company was still unprofitable, but it was growing revenue at triple-digit rates and had proven that the B2B2C model could work at scale. Now it needed to figure out what to do with public-market capital and public-market expectations—and the answer would be acquisitions.

IV. The M&A Strategy: Building the Platform (2015-2019)

The post-IPO playbook that Teladoc pursued reflected a specific strategic bet: that the future of virtual care belonged not to the company with the best video-visit technology, but to the company that could offer the most comprehensive suite of virtual healthcare services across the broadest range of conditions and geographies. This was a roll-up thesis, and Gorevic executed it with purpose.

The first acquisition of real scale came in 2016 when Teladoc purchased HealthiestYou for a hundred and twenty-five million dollars, adding a mobile-first consumer engagement platform. But the real acceleration began the following year.

In the summer of 2017, Teladoc acquired Best Doctors for four hundred and forty million dollars—three hundred and seventy-five million in cash plus sixty-five million in stock. Best Doctors operated a network of more than fifty thousand medical specialists worldwide, offering expert second opinions for patients facing serious diagnoses. When a member received a cancer diagnosis or confronted a complex surgical decision, Best Doctors connected them with leading specialists who would review the case. Their data showed that expert opinions led to a change or refinement of diagnosis in thirty-seven percent of cases and altered treatment plans seventy-five percent of the time.

Critically, about forty percent of Best Doctors' revenue was international, with operations spanning Canada, Australia, Spain, Japan, and beyond. In one stroke, Teladoc went from a domestic urgent-care platform to a global presence.

The following year brought Advance Medical, a Barcelona-headquartered company acquired for three hundred and fifty-two million dollars. Founded in 1999, Advance Medical partnered with more than three hundred multinational employers and insurers across Europe, Asia, and Latin America, offering clinical risk assessment, virtual primary care, and chronic care capabilities that Teladoc had not yet built organically. The deal added operations in China and Brazil and gave Teladoc the ability to credibly market itself as the only global comprehensive virtual care platform.

Then came MédecinDirect in early 2019, a Paris-based telemedicine company that worked with nearly half of France's top thirty private medical insurers. The acquisition price was not disclosed, but the strategic logic was clear: France was a major European market where Teladoc had no presence, and MédecinDirect delivered instant market leadership. Each of these international deals followed the same pattern—buy the local leader, integrate them into the Teladoc platform, and sell the combined offering to multinational employers who wanted a single virtual care vendor.

But it was the two acquisitions in 2020 that would define Teladoc's trajectory for the next half-decade and beyond.

In January 2020, Teladoc announced it would acquire InTouch Health for approximately six hundred million dollars. InTouch, headquartered in Santa Barbara, California, was the leading provider of enterprise telehealth technology for hospitals and health systems. It served more than four hundred and fifty hospitals with software platforms that enabled specialists to deliver care remotely across facility networks—think a stroke neurologist in a major medical center consulting on a patient in a rural hospital's emergency room via a robot-mounted screen. InTouch generated roughly eighty million in revenue, growing at thirty-five percent annually. The deal filled the acute-care gap in Teladoc's portfolio.

Then came the deal that changed everything.

On August 5, 2020, Teladoc announced it would merge with Livongo Health in a transaction valued at eighteen and a half billion dollars—the largest digital health deal in history.

To understand why this deal mattered, you need to understand Livongo and its founder. Glen Tullman was born near Chicago in 1959, studied economics and psychology at Bucknell University, and spent a year at Oxford studying social anthropology—an unusual combination that gave him a lens on human behavior that most health tech founders lacked. He spent a decade at CCC Information Services before his prominent run as CEO of Allscripts, where he guided the company to become the leading provider of electronic health records and practice management software for physician offices. But the personal catalyst for Livongo was his son Sam being diagnosed with Type 1 diabetes at age eight. Tullman saw firsthand how fragmented and burdensome chronic disease management was for real families—the constant vigilance, the guilt when a reading was missed, the friction of analog systems in a digital world.

Tullman watched his son navigate the daily burden of chronic disease management—constant finger-sticking, manual logging, trying to remember what to eat and when to test—and decided there had to be a better way. Livongo, founded in 2014, built a technology platform for chronic condition management sold to self-insured employers.

The core product started with diabetes: members received a smart, cellular-connected glucose meter that automatically transmitted readings to the cloud. No manual logging required. The platform provided twenty-four-seven coaching from certified diabetes educators and delivered what Tullman called "Applied Health Signals"—personalized nudges sent at precisely the right moment to help members make better health decisions.

Think of it like a fitness tracker, but instead of counting steps, it was actively managing a chronic disease. The system aggregated health readings, claims data, and behavioral data into an AI engine that interpreted signal combinations, applied personalized interventions at the right moment, and then iterated based on outcomes. Each interaction trained the model to make subsequent nudges more effective. The company later expanded to hypertension, weight management, and behavioral health. By the time of the merger announcement, Livongo had over four hundred and ten thousand members and fifteen hundred clients, and had gone public on the Nasdaq in July 2019 at twenty-eight dollars per share, raising over four hundred million in its IPO.

The strategic logic of combining Teladoc and Livongo was seductive. Teladoc was fundamentally an episodic care platform—a patient felt sick, called a doctor, got treated, and the relationship ended. There was no longitudinal data, no ongoing engagement, no prevention. Livongo was the opposite: an always-on, persistent chronic care relationship. A diabetic Livongo member generated data multiple times a day, engaged with coaches regularly, and received continuous feedback.

The combined thesis, which Teladoc branded "whole person care," held that episodic visits could identify members who needed chronic condition programs, Livongo's longitudinal data could make episodic visits smarter, and employers would pay a premium for a single integrated vendor covering both acute and chronic needs.

The deal terms called for each Livongo share to receive roughly 0.59 Teladoc shares plus eleven dollars and thirty-three cents in cash. Pro forma revenue was projected at approximately one point three billion dollars, with a hundred million in revenue synergies by year two and five hundred million by 2025.

The market's reaction was swift and brutal. Teladoc stock fell roughly nineteen percent on the announcement day. Investors were alarmed by the price—Teladoc was paying approximately nineteen times forward revenue estimates at a moment when both companies' valuations were inflated by pandemic-driven enthusiasm. The deal closed on October 30, 2020, creating a combined entity valued at approximately thirty-seven billion dollars.

The integration challenges began almost immediately. All four of Livongo's top executives—CEO Zane Burke, President Jennifer Schneider, CFO Lee Shapiro, and SVP Business Development Steve Schwartz—departed after the close. The cultural clash was real: Teladoc was a traditional enterprise healthcare vendor; Livongo was a Silicon Valley startup that thought about consumer engagement and behavioral nudges. The thesis depended on cross-selling—routing Teladoc members into Livongo programs and vice versa—but this proved far harder to execute than anyone projected.

Whether the Livongo deal was strategic brilliance executed at the wrong price or empire-building dressed in strategic language would become the central question of Teladoc's next chapter. But first, a pandemic would make the whole question seem temporarily irrelevant.

V. The Pandemic Boom: Validation or Mirage? (2020-2021)

On March 13, 2020, President Trump declared a national emergency as COVID-19 swept across the United States. Four days later, the Centers for Medicare and Medicaid Services did something that telehealth advocates had spent two decades fighting for: CMS expanded Medicare telehealth access to all beneficiaries in any location, including their homes, effective retroactively to March 6.

Before the waivers, Medicare telehealth had been essentially restricted to rural areas and required patients to present at an approved clinical site. Overnight, geographic restrictions vanished, audio-only visits were permitted, more provider types could bill for telehealth, and the list of covered services expanded dramatically. Medicare telehealth utilization surged approximately twelve thousand percent in the six weeks between early March and mid-April 2020.

For Teladoc, it was as if someone had removed every structural barrier the company had spent eighteen years fighting to tear down.

The results were staggering. Virtual visits in the first quarter of 2020 nearly doubled year over year to approximately two million. By the second quarter, they had tripled to two point eight million. The fourth quarter saw three million visits. For the full year, Teladoc delivered ten point six million virtual visits, up a hundred and fifty-six percent from 2019. Revenue roughly doubled from five hundred and fifty-three million dollars in 2019 to one point zero nine billion in 2020. U.S. paid membership climbed to fifty-two million members, up forty-one percent year over year.

The stock market response was euphoric. Teladoc entered 2020 trading around eighty dollars per share. By early February 2021, it reached an intraday high near three hundred and eight dollars. The market capitalization exceeded forty-six billion dollars. The narrative was irresistible: "Ten years of telehealth adoption in ten weeks." Analysts fell over themselves upgrading the stock. The consensus view held that the pandemic had permanently altered consumer behavior—once people experienced the convenience of a virtual doctor visit, they would never go back to sitting in waiting rooms.

But beneath the euphoria, there were warning signs that the most clear-eyed observers noticed.

First, much of the demand surge was driven by emergency circumstances—people who could not or would not visit a doctor in person due to COVID restrictions, not people who had permanently shifted their preferences. When restrictions eased, utilization tended to stabilize at levels about forty percent above pre-COVID baselines—meaningfully higher, but not the exponential growth trajectory the stock price was pricing in.

Second, the competitive landscape was exploding. Every major hospital system rapidly deployed its own telehealth capabilities, often integrated directly into their Epic electronic health records systems. Insurance companies launched their own virtual care offerings. Amazon launched Amazon Care, a hybrid virtual-plus-in-person service. CVS leveraged its MinuteClinic infrastructure and Aetna insurance arm to offer seamless physical-to-virtual care.

The very regulatory changes that benefited Teladoc also lowered barriers for everyone else. When telehealth required state-by-state licensing battles and years of regulatory groundwork, Teladoc's first-mover advantage was a genuine moat. When CMS waved a wand and made it easy for any provider to offer telehealth, that moat evaporated.

Third, there were quality and fraud concerns. The rapid expansion of telehealth brought a flood of new providers and platforms into the market, some with questionable clinical standards. The experience for many patients—a hurried ten-minute video call that felt impersonal and transactional—did not always live up to the "future of medicine" narrative. For complex issues, for anything that required a physical examination, for ongoing relationships with a trusted provider, in-person care remained clearly superior.

The pandemic had validated the concept of telehealth. But it had also validated telehealth as a feature—something that any healthcare provider, insurer, or tech company could offer—rather than telehealth as a standalone business with defensible competitive advantages. This distinction would prove catastrophic for Teladoc's valuation, though the reckoning was still a few quarters away.

For investors, the 2020-2021 period offered one of the starkest lessons in the difference between narrative momentum and fundamental analysis. Teladoc's revenue doubled, its addressable market expanded, and consumer adoption accelerated. And yet the stock at three hundred dollars was pricing in a future that required everything to go right—that telehealth growth would continue at pandemic-era rates, that competition would not intensify, and that the Livongo integration would deliver on its synergy promises. All three assumptions would prove wrong.

VI. The Post-Pandemic Reckoning (2021-2023)

The crash, when it came, was one of the most dramatic in modern healthcare investing. From a peak near three hundred and eight dollars in February 2021, Teladoc's stock fell relentlessly—through two hundred, through one hundred, through fifty, through twenty. By late 2022, shares had lost more than ninety percent of their peak value. The decline was not a single shock but a slow-motion unraveling, each quarterly earnings report revealing another piece of the bear thesis.

Revenue kept growing—reaching two billion in 2021 and nearly two point four billion in 2022—but the growth rate decelerated sharply, from eighty-six percent in 2021 to eighteen percent in 2022 to eight percent in 2023. The problem was not that the business was collapsing but that the growth trajectory no longer justified anything close to the valuations investors had been paying. Organic growth in the core telehealth business was slowing as the pandemic-driven surge normalized. The Livongo integration was delivering revenue synergies far more slowly than promised. And the competitive environment had become brutally intense.

Then came the goodwill impairments—the accounting profession's formal way of admitting that an acquisition was overpaid.

For readers unfamiliar with the concept: when a company acquires another company for more than the fair value of its tangible assets, the difference is recorded as "goodwill" on the balance sheet. Goodwill represents the premium paid for intangible assets—brand value, customer relationships, technology, future growth potential. Each year, the company must test whether that goodwill is still worth what it originally recorded. If the acquired business has declined in value, the company must write down the goodwill—an impairment charge that flows through the income statement as a loss.

In the first quarter of 2022, Teladoc recorded a six-point-six-billion-dollar goodwill impairment charge. In the second quarter, another three billion. In the fourth quarter, another three point eight billion. For the full year 2022, non-cash goodwill impairments totaled approximately thirteen point four billion dollars, driving a net loss of thirteen point seven billion—the largest single-year loss in digital health history.

To put it plainly: roughly seventy-two cents of every dollar paid for Livongo had evaporated in approximately two years. The net loss per share for 2022 was eighty-four dollars and sixty cents.

These were non-cash charges—they did not affect Teladoc's ability to operate on a day-to-day basis—but they represented an unambiguous admission that the company had vastly overpaid. The deal had been struck at the peak of a speculative bubble in digital health valuations, and as interest rates rose and growth multiples compressed across the technology sector, the carrying value of that acquisition became indefensible.

The utilization problem compounded the financial challenges. Teladoc's B2B2C model meant that millions of members were enrolled through their employer-sponsored health plans, but enrollment did not equal engagement. Many of those members never used the service. The gap between members enrolled and members actively using Teladoc's products was a persistent drag on economics—ninety million members on paper, but if most of them forgot they had access, the per-member economics deteriorated.

In January 2023, Teladoc laid off three hundred employees—about six percent of its non-clinician global workforce—as part of a restructuring plan. The company took approximately seventeen million dollars in restructuring charges. Adjusted EBITDA improved from two hundred and forty-seven million in 2022 to three hundred and twenty-eight million in 2023, but the top-line story was sobering: a company that had doubled revenue in 2020 was now growing in the single digits.

On April 5, 2024, Jason Gorevic—the CEO who had led Teladoc for fifteen years, who had navigated the regulatory wars, the IPO, the acquisitions, the pandemic surge, and the crash—departed immediately. CFO Mala Murthy served as interim CEO until Chuck Divita III, an executive from GuideWell, was named permanent CEO in June 2024. Divita came from the payer side of healthcare, not the technology side, signaling that Teladoc's path forward would be defined by its ability to integrate into the existing healthcare infrastructure rather than trying to disrupt it from outside.

Meanwhile, the BetterHelp mental health segment—which Teladoc had acquired in January 2015 for a remarkable three point three million dollars and grown into a billion-dollar revenue business—began showing cracks. After peaking near one billion in annual revenue in 2022 and growing to one point thirteen billion in 2023, BetterHelp revenue declined to one point zero four billion in 2024 as pandemic-era demand for teletherapy normalized and competition intensified. In 2024, Teladoc recorded a seven hundred and ninety million dollar goodwill impairment charge specifically on BetterHelp, adding to the cumulative write-down tally.

The post-pandemic period raised the most fundamental question in telehealth: Is virtual care a product or a feature? This is the existential question that hangs over not just Teladoc but every independent telehealth company. If virtual care is a product—a standalone business with defensible competitive advantages, unique data assets, and proprietary clinical capabilities—then Teladoc's position as market leader has real and lasting value. If it is a feature—something that any insurer, hospital system, or technology company can bolt onto their existing platform with relatively modest investment—then Teladoc is selling a commodity in a market where the buyers have all the leverage and the barriers to entry are vanishingly low. The market, through its pricing of the stock, has increasingly voted for the latter interpretation.

VII. The Business Model Deep Dive & Unit Economics

To understand why Teladoc finds itself in its current position, you need to understand the mechanics of how the company actually makes money—and why healthcare services businesses face structural challenges that most technology companies do not.

Teladoc operates two primary segments. Integrated Care, which generated roughly one point five eight billion dollars in revenue in 2025, encompasses the core telehealth business, chronic condition management (the legacy Livongo products), and the hospital platform business inherited from InTouch Health. BetterHelp, the direct-to-consumer mental health platform, generated approximately nine hundred and fifty million in 2025 revenue.

Within Integrated Care, revenue comes from several sources. The largest is subscription fees—per-member-per-month payments from employers and health plans for access to Teladoc's virtual care services. Think of it as a SaaS-like recurring revenue model, except the "software" is access to a doctor. When an employee at a Fortune 500 company goes to their benefits portal and sees Teladoc listed, that employer is paying a small monthly fee for every covered life—whether or not that employee ever uses the service.

This model provides revenue predictability but creates the utilization challenge: the denominator (enrolled members) can be much larger than the numerator (active users). The company earns small amounts per member while paying real costs to maintain a physician network, technology infrastructure, and customer service apparatus sized for potential demand rather than actual demand.

Visit fees add a transactional component—either paid by the employer, the health plan, or the member depending on plan design. Integrated care revenue from chronic condition management includes the Livongo-derived programs for diabetes, hypertension, and weight management. Platform licensing fees come from hospital systems using the InTouch-derived technology.

BetterHelp operates on a fundamentally different model. It is primarily direct-to-consumer: individuals sign up, are matched with a licensed therapist, and pay a weekly subscription fee, typically out of pocket. This makes BetterHelp more like a consumer subscription business than a B2B healthcare enterprise, with all the associated dynamics—high customer acquisition costs through digital marketing, meaningful churn as consumers cycle in and out of therapy, and sensitivity to discretionary spending patterns.

The strategic pivot underway is to shift BetterHelp toward insurance-covered mental health services, which would reduce consumer price sensitivity but add the complexity of insurance billing and credentialing. By early 2026, BetterHelp insurance sessions exceeded twelve hundred per day with an annualized revenue run rate over forty million dollars, and management guided toward seventy-five to ninety million in BetterHelp insurance revenue for 2026. The April 2025 acquisition of UpLift, an insurance-enabled mental health platform, for thirty million dollars was designed to accelerate this transition.

The provider network presents its own economic challenge. Teladoc's physicians are independent contractors, not employees. The company must continuously recruit, credential, and compensate doctors willing to provide virtual consultations. At the original pricing, physicians earned about twenty dollars per consultation and were advised to limit sessions to roughly four per hour—meaning a physician working at maximum throughput earned approximately eighty dollars per hour through Teladoc. That is competitive with some outpatient primary care settings but well below specialist compensation, which constrains the range of services deliverable virtually.

Healthcare margins are structurally challenging because the cost of delivering care—paying doctors, maintaining clinical quality, ensuring regulatory compliance—does not scale the way software development costs do. When a software company adds its millionth user, the marginal cost is essentially zero. When a telehealth company adds its millionth visit, it needs a doctor on the other end of that call. Teladoc's adjusted EBITDA margin in 2025 was approximately eleven percent—meaningful but far below what investors in high-growth technology companies have come to expect.

The metrics that matter most for tracking this business going forward are straightforward. Revenue per member in Integrated Care tells you whether the company is extracting more value from its installed base through higher-acuity services, chronic care programs, and better engagement—or whether it is stuck in a low-value transactional model. BetterHelp paying users reveals whether the mental health segment can stabilize after its post-pandemic decline and whether the insurance pivot is working. These two KPIs are the vital signs of the business.

VIII. The Competitive Landscape & Market Structure

The competitive landscape that Teladoc navigates today bears almost no resemblance to the one it pioneered. When the company launched in 2005, it was essentially the only game in town—a lone startup fighting state medical boards for the right to exist. By 2026, telehealth has become table stakes, and the question is no longer whether virtual care will exist but who will own the relationship.

The most significant competitive development is not any single rival but the structural shift of telehealth capabilities into incumbent healthcare organizations. When Cigna's Evernorth health services subsidiary acquired MDLive in 2021 for approximately one billion dollars, it brought a major telehealth platform in-house. This created a captive competitor—MDLive serves Cigna's eighty-plus million covered lives without Teladoc getting a shot at that business. UnitedHealth's Optum arm built its own virtual care capabilities, though notably even Optum Virtual Care shut down its standalone offering, illustrating how difficult it is to operate telehealth as a separate business rather than integrating it into the care delivery fabric.

Amazon's journey in this space is particularly instructive, because if any company should have been able to make standalone virtual care work at scale, it was Amazon—with unmatched consumer distribution, world-class logistics, and a willingness to invest through years of losses. Amazon Care—a hybrid virtual-plus-in-person primary care service—launched with great fanfare but shut down on December 31, 2022. Amazon cited that it was "not a complete enough offering for the large enterprise customers" it had been targeting. But Amazon did not abandon healthcare; instead, it acquired One Medical, a primary care chain with over two hundred physical locations, in a three-point-nine-billion-dollar deal that closed in early 2023. Amazon later consolidated its Amazon Clinic telehealth offering into the One Medical platform. The lesson was telling: even Amazon concluded that virtual care alone was insufficient and that physical presence mattered.

Doctor on Demand and Grand Rounds merged in 2021 to form Included Health, positioning itself as an integrated care-plus-navigation platform for employers and health plans. The combined entity competes directly with Teladoc's "whole person care" value proposition.

Among public comparables, Amwell—Teladoc's most direct competitor and fellow IPO darling of the pandemic era—has fared even worse. Revenue declined six percent in 2023, its net loss ballooned to six hundred and seventy-nine million dollars including substantial impairment charges, and it received a NYSE delisting warning as its share price fell below minimum listing requirements for thirty consecutive trading days. Amwell's struggles reinforce the thesis that pure-play telehealth faces deep structural challenges rather than merely company-specific execution problems—this is a market structure issue, not a management issue.

The distribution challenge is perhaps the most underappreciated aspect of healthcare competition. Healthcare is sold, not bought—meaning that the companies who control the distribution channels (insurance plans, employer benefits brokers, hospital referral networks) have enormous power over which products reach consumers. Teladoc does not control any of these channels. It is a vendor selling into them, competing with the channel owners' own offerings. When UnitedHealth decides it wants its members using Optum's virtual care rather than Teladoc's, Teladoc has little recourse.

The mental health segment presents a somewhat different competitive picture. BetterHelp built a dominant position in direct-to-consumer online therapy, but competitors like Talkspace, Cerebral, and numerous smaller platforms have fragmented the market. More importantly, traditional health systems and insurers have expanded their own behavioral health offerings. BetterHelp's pivot toward insurance coverage is an attempt to shift from a discretionary consumer purchase to an insurance-covered benefit—expanding the addressable market but also subjecting BetterHelp to payer dynamics and reimbursement pressures.

Internationally, competitive dynamics differ by market, and Teladoc benefits from earlier entry through its acquired operations. But healthcare regulation is inherently local, and the advantages that accrue from being a global platform are limited when each country has its own licensing requirements and reimbursement structures.

IX. Strategic Frameworks: Porter's 5 Forces & Hamilton's 7 Powers

The most honest way to assess Teladoc's competitive position is through the lens of rigorous strategic frameworks, and the picture they paint is sobering.

Starting with Porter's Five Forces, the threat of new entrants is high and rising. The technology required to build a telehealth platform has become increasingly commoditized—video conferencing, electronic health records integration, secure messaging, and basic triage algorithms are available as off-the-shelf components. The regulatory moats that once protected Teladoc—hard-won state-by-state licensing and institutional knowledge of medical board resistance—have weakened substantially as interstate licensing compacts expand and post-pandemic regulations have made telehealth broadly accessible. Most critically, potential new entrants include some of the most formidable companies in the world: Amazon with its consumer distribution, Google and Apple with their device ecosystems, and every major insurance company with existing patient relationships.

The bargaining power of suppliers—primarily physicians—is moderate. Doctors have many options for how and where they practice, and the compensation Teladoc offers must compete with in-person practice, locum tenens work, and other platforms. Teladoc's scale provides some advantage in recruitment, but physicians are not locked into the platform in any meaningful way.

Buyer power is high and may be the most important force in Teladoc's competitive equation. The company's primary customers—large self-insured employers and health plans—are sophisticated, price-sensitive buyers with significant leverage. Switching costs are modest: an employer can change telehealth vendors during its annual benefits renewal cycle with relatively little disruption. And buyers have alternatives—they can build their own telehealth capabilities, buy from competitors, or rely on their health plan's integrated offering. When your customer can become your competitor, your pricing power is inherently limited.

The threat of substitutes is high. In-person care remains the gold standard for the majority of medical conditions, and for many patients the convenience advantage of telehealth is offset by the limitations of virtual diagnosis. Retail clinics at CVS and Walgreens, freestanding urgent care centers, and same-day primary care appointments all compete for the same pool of routine medical visits.

Competitive rivalry is intense. The market is fragmented, price competition is real, and differentiation in the core video-visit product is limited. Patients generally do not care whether their virtual visit is provided by Teladoc, Amwell, or their health system's branded telehealth service—they care about wait time, provider quality, and insurance coverage.

Turning to Hamilton Helmer's Seven Powers framework, the assessment is even more challenging.

Scale economies exist—Teladoc's ninety-million-plus member base gives it some unit cost advantages—but they are not definitive. A competitor with ten million members can deliver a comparable clinical experience at comparable cost per visit.

Network effects, the strongest source of durable competitive advantage in most technology businesses, are conspicuously weak in telehealth. Teladoc is not a true two-sided marketplace where more patients attract more doctors who attract more patients. Physicians do not choose to practice on Teladoc because it has the most patients; they choose based on compensation and scheduling. Patients do not choose Teladoc because it has the best doctors; they use whatever their employer provides. The intermediated B2B2C model short-circuits the network effect dynamic.

Counter-positioning—where an incumbent cannot adopt the challenger's model without damaging their existing business—is absent. Health systems, insurers, and primary care practices can add telehealth without cannibalizing their core revenue. For them, telehealth is additive.

Switching costs are low to medium. Employer contracts provide some friction, particularly for integrated chronic care programs where enrolled members have established data histories and coaching relationships. But for basic telehealth visits, switching is trivial.

Branding power is weak because the B2B2C model means most members encounter Teladoc through their employer's benefits portal rather than through direct brand engagement.

Cornered resources are absent. Teladoc does not possess proprietary technology that competitors cannot replicate, exclusive physician networks that rival platforms cannot access, or regulatory positions that others cannot obtain.

Process power—competitive advantage from unique organizational capabilities—represents perhaps Teladoc's best hope. The integration of episodic virtual care with chronic condition management, combined with AI-driven personalization across multiple modalities, is genuinely complex to build and execute. But "developing" is the operative word: this has not yet been proven at scale.

The framework analysis leads to an uncomfortable conclusion: Teladoc operates in a market with high buyer power, intense competition, low barriers to entry, readily available substitutes, and no clear source of durable competitive advantage. The company's best path to building defensibility lies in execution—proving that integrated, data-driven virtual care can deliver measurable value that fragmented alternatives cannot match.

X. The Path Forward: Can Teladoc Survive and Thrive? (2024-Present)

Teladoc today is a fundamentally different company than the one that traded at three hundred dollars per share. As of early March 2026, the stock trades near five dollars and thirty cents, with a market capitalization just under one billion dollars—a ninety-eight percent decline from the 2021 peak. The company generated two point five three billion in revenue in 2025, down two percent from the prior year, with Integrated Care growing three percent to one point five eight billion while BetterHelp declined nine percent to nine hundred and fifty million. Adjusted EBITDA was two hundred and eighty-one million dollars.

Under CEO Chuck Divita, who took the helm in June 2024, the company has declared 2026 an "execution year." The strategic priorities center on several interlocking themes.

First, proving the integrated care thesis that the Livongo acquisition was supposed to deliver—using AI-enabled risk stratification to identify members at rising risk for chronic conditions and proactively routing them into appropriate care programs. This is the "orchestration era" in management's language: dynamically coordinating care across settings, providers, specialties, and platforms.

Second, pivoting BetterHelp from a purely direct-to-consumer, cash-pay platform toward insurance-covered services. This is strategically important because it would transform BetterHelp from a discretionary consumer subscription—vulnerable to marketing efficiency fluctuations and economic sensitivity—into an insurance benefit with more stable demand dynamics. Management guides toward seventy-five to ninety million in BetterHelp insurance revenue for 2026, with an exit annualized run rate exceeding one hundred million.

Third, international expansion, where Integrated Care international revenues grew modestly in 2025 and the company's presence across more than a hundred and seventy countries provides a platform for growth in markets at an earlier stage of telehealth adoption.

The 2026 revenue guidance of two point four seven to two point five nine billion dollars is essentially flat with 2025 at the midpoint. Adjusted EBITDA guidance of two hundred and sixty-six to three hundred and eight million represents roughly flat performance. This is not a growth story in its current phase—it is a stabilization and turnaround story.

The strategic options available to Teladoc extend beyond organic execution. At its current valuation, the company is a plausible acquisition target for a larger health system, insurance company, or private equity firm. A major insurer could acquire Teladoc to bring its telehealth capabilities in-house, similar to what Cigna did with MDLive. A private equity firm could take the company private, strip out costs, and optimize for cash generation. Teladoc could also pursue strategic alternatives for individual segments—selling or spinning off BetterHelp as a standalone mental health business while focusing the core on Integrated Care.

The mental health opportunity remains one of the most compelling elements of the Teladoc story. Mental and behavioral health is the fastest-growing segment of telehealth, with higher engagement rates and greater willingness among both patients and payers to accept virtual delivery. If BetterHelp can successfully transition to insurance-covered services while maintaining its consumer brand, it could become the anchor of Teladoc's value proposition.

Technology and AI represent the wildcard. Management talks extensively about AI-driven care orchestration, predictive analytics, and personalized interventions. The question is whether these capabilities amount to genuine competitive differentiation or are marketing language wrapped around capabilities any well-funded competitor could replicate. In healthcare, the proof is always in outcomes data—and Teladoc has yet to publish the kind of large-scale, peer-reviewed outcomes studies that would demonstrate its integrated care model produces measurably superior results.

XI. Bull vs. Bear Case & Investment Perspective

The bull case for Teladoc rests on several pillars. Telehealth penetration, despite the post-pandemic normalization, remains far below its long-term potential. Most medical visits are still conducted in person, and structural forces—an aging population, a worsening primary care physician shortage, rising healthcare costs, and growing consumer comfort with digital interactions—all point toward continued secular growth in virtual care adoption.

Teladoc's position as the largest independent virtual care platform, with scale across both episodic and chronic care, gives it a foundation that would take years for a de novo competitor to replicate. The stock's decline from three hundred dollars to five dollars means that virtually all optimism has been stripped from the valuation—if management can simply stabilize the business and demonstrate modest profitable growth, the asymmetry could be meaningful. International markets, where telehealth adoption is at an earlier stage, offer growth opportunities. And the healthcare labor shortage—there simply are not enough primary care doctors to see patients in person—creates a structural tailwind for virtual care that will persist regardless of pandemic dynamics.

The bear case is equally compelling. Telehealth may be a feature rather than a product—something that every insurer, health system, and technology company can offer without building a standalone business around it. The Livongo acquisition was value-destructive by any measure: the company paid eighteen and a half billion dollars for an asset that prompted over thirteen billion in goodwill impairments within two years. The broader market structure—high buyer power, low switching costs, intense competition, and readily available substitutes—means that Teladoc may never achieve the kind of pricing power and margin expansion that its early supporters envisioned.

Revenue has now declined year-over-year. BetterHelp is losing paying users. Adjusted EBITDA is compressing. The technology and AI claims remain largely unsubstantiated by independent outcomes data. And the competitive threats from well-capitalized incumbents—UnitedHealth, CVS, Amazon—are structural, not cyclical.

The frameworks analysis reinforces the bear case. Porter's Five Forces reveal a market structure where virtually every force works against the independent telehealth provider. Hamilton's Seven Powers assessment finds no clear source of durable competitive advantage. The company's only plausible path to building process power—through the integration of episodic and chronic care—remains aspirational rather than demonstrated.

The KPIs to watch remain revenue per member in Integrated Care and BetterHelp paying user count. Revenue per member reveals whether the "whole person care" strategy is creating genuine engagement and willingness to pay at higher levels. BetterHelp paying users reveal whether the insurance pivot can offset the secular decline in cash-pay subscribers. If both metrics are trending positively over coming quarters, the turnaround thesis gains credibility. If both are flat or declining, the structural bear case gains further weight.

XII. Lessons for Founders, Operators, and Investors

Teladoc's story offers a masterclass in several of the hardest lessons in business building and investing.

The timing paradox in healthcare is perhaps the most important. Teladoc was founded in 2002 with a vision that was fundamentally correct—virtual care would become a mainstream component of healthcare delivery. But being right about the destination does not guarantee being right about the timing or the business model. The company spent thirteen years fighting regulatory battles, converting skeptical doctors, and building distribution before the pandemic provided the catalyst that proved its thesis. Being too early meant absorbing enormous costs—legal fees, lobbying expenses, below-scale unit economics—that a later entrant could avoid. Yet being early also established the brand and relationships that positioned Teladoc to capture the pandemic surge. The paradox is real: early movers bear the costs of market creation but may not capture the returns if the market eventually becomes easy enough for everyone to enter.

Distribution is everything in B2B2C healthcare. Teladoc's most important strategic decision was the pivot from direct-to-consumer to selling through employers and health plans, which gave the company access to millions of members without having to acquire them individually. But distribution through intermediaries comes with a profound vulnerability: permanent dependence on channel partners who may become competitors. When Cigna bought MDLive, Teladoc lost access to eighty million potential members. When UnitedHealth built its own virtual care capabilities, another hundred million members became harder to reach. The lesson is that in B2B2C models, the company that controls the channel ultimately controls the economics—and Teladoc never controlled the channel.

The M&A strategy reveals the razor-thin line between visionary platform building and value-destructive empire building. The earlier acquisitions—Best Doctors, Advance Medical, InTouch Health—followed a logical thesis and were priced at reasonable multiples. The Livongo deal was a different animal entirely: eighteen and a half billion dollars struck at the peak of a speculative bubble. The strategic logic was defensible—merging episodic and chronic care is a compelling thesis—but the price assumed a future that did not materialize. Integration is always harder than the deal, especially when the acquirer and target have fundamentally different cultures. The departure of all four top Livongo executives meant that the institutional knowledge and vision that built the product walked out the door.

Market structure matters more than market size, and this may be the single most important analytical lesson from the Teladoc story. The telehealth market is large and growing—analysts estimate it will reach hundreds of billions in the coming decade—but it is not a winner-take-all market. Teladoc bet that it could become the dominant platform through scale and breadth of offering, the way Uber dominates ridesharing or Amazon dominates e-commerce. But healthcare is fragmented by regulation, geography, clinical specialty, and payer—and the forces that drive consolidation in consumer technology do not apply with the same force in healthcare. The distribution channels are controlled by a small number of large insurers and benefits brokers who have no incentive to cede power to an intermediary. And the product itself—a doctor visit—is inherently commodity-like when delivered through a screen, lacking the differentiation that sustains pricing power in other technology categories.

The hype cycle lesson may be the most painful. During the pandemic, the narrative around telehealth achieved a level of consensus optimism that should have been a warning signal. When analysts, journalists, investors, and executives all agree that a trend is permanent and transformative, the consensus is usually pricing in more change than will actually occur. Telehealth usage settled at a permanently higher level than pre-pandemic baselines, but the rate of adoption growth did not sustain. The difference between a permanently higher level and permanently accelerating growth is the difference between a reasonable investment and a catastrophic one when the starting valuation is forty-six billion dollars.

Finally, valuation discipline is its own form of risk management. Teladoc may have been a great company in many respects—it pioneered a new category, won regulatory battles that others would not fight, and built a genuine franchise in virtual care. But even great companies can be terrible investments at the wrong price. At three hundred dollars per share, investors were paying for a future that required everything to go right. At five dollars per share, the question is different—and much harder to answer.

XIII. Epilogue & Future Scenarios

Where is Teladoc in five years? The honest answer is that the range of outcomes is unusually wide, and three distinct scenarios capture the plausible paths.

In the turnaround scenario, Chuck Divita's execution-focused leadership stabilizes the business, the BetterHelp insurance pivot generates meaningful new demand, and the integrated chronic care model finally delivers on the promise that the Livongo merger was supposed to unlock. Revenue stabilizes and then grows modestly, EBITDA margins expand as the company benefits from operating leverage, and the market rewards the improvements with a re-rating. This scenario requires disciplined execution, a cooperative competitive environment, and time.

In the acquisition scenario, a larger player—perhaps CVS, perhaps a major insurer, perhaps a private equity firm—concludes that Teladoc's assets are worth more inside a larger organization. The ninety-million-member installed base, the chronic care platform, the BetterHelp consumer brand, and the international presence all have strategic value to the right acquirer. At a sub-billion-dollar market cap, the price of entry is modest relative to the scale of the business.

In the slow-fade scenario, the structural challenges prove insurmountable. Revenue continues to erode as employers shift to integrated offerings from their insurance carriers, BetterHelp continues to lose paying users to cheaper alternatives and employer-provided behavioral health benefits, and the company lacks the resources to invest in the kind of meaningful technology differentiation needed to build a sustainable moat. Teladoc remains a subscale player in a market that has moved past it, generating enough cash to survive but not enough to thrive, gradually losing relevance as the industry consolidates around larger integrated players.

What does Teladoc's story tell us about digital health more broadly? Healthcare's digital transformation is real but it is slow, complex, and disproportionately favors incumbents who already have the patient relationships, the payer contracts, and the regulatory infrastructure. The companies that win in healthcare technology are not usually the pure-play disruptors—they are the ones that embed their technology into the existing care delivery infrastructure rather than trying to replace it. Epic Systems did not try to replace hospitals; it sold them the software that runs their operations and became indispensable in the process. Livongo's genius was not the glucose meter—it was the insight that chronic disease management could be augmented by technology without replacing the physician relationship. The irony is that this insight may ultimately prove more valuable inside an integrated health system or insurance company than it does inside a standalone digital health company.

Teladoc's story is ultimately one of ambitious vision meeting harsh market realities. The founders saw the future correctly: virtual care has become a permanent, growing component of healthcare delivery. But seeing the future and capturing the economic value of that future are very different things. The regulatory moats that protected Teladoc's early-mover advantage were temporary. The pandemic-driven adoption surge was real but unsustainable at peak rates. The Livongo acquisition represented a logical strategic move executed at an irrational price. And the competitive dynamics of healthcare—where the buyers are powerful, the switching costs are low, and the incumbents have structural advantages—have proven stubbornly unfavorable for pure-play virtual care companies.

What surprised most in researching this story was not the crash—given the valuation at peak, some correction was inevitable—but the speed and completeness with which the market turned. In less than five years, Teladoc went from being hailed as the future of medicine to trading below its IPO price, with a market cap smaller than what it paid for a single acquisition. That journey—from twenty thousand members in a Dallas office to forty-six billion dollars in market cap to less than one billion—is one of the most complete business cycles in modern healthcare, and its lessons will be studied for decades to come.

XIV. Further Learning

For those wanting to go deeper on the Teladoc story and the broader digital health landscape, these resources provide essential context.

Teladoc's 10-K and 10-Q filings from 2015 through the present offer the most detailed primary-source financial data, including granular disclosure of goodwill impairment methodology and segment economics. The Livongo S-1 filing from 2019 remains one of the best documents ever written about the chronic care management opportunity and the Applied Health Signals framework. Clayton Christensen's "The Innovator's Prescription" provides the theoretical foundation for understanding why healthcare disruption follows different patterns than other industries. Elisabeth Rosenthal's "An American Sickness" offers essential background on the structural complexity of the U.S. healthcare system.

Rock Health's annual digital health reports track venture funding, market trends, and adoption metrics across the sector. STAT News and Healthcare Dive have provided the most comprehensive ongoing coverage of Teladoc's strategic evolution and competitive positioning. Earnings call transcripts from 2020 through 2023 are particularly valuable for tracking how management's narrative shifted in real time from pandemic-era optimism to post-pandemic recalibration. The FTC's amicus brief in the Texas Medical Board case offers a fascinating window into how federal regulators viewed the competitive dynamics of telehealth regulation.

For investors tracking the company going forward, the two metrics that matter most—Integrated Care revenue per member and BetterHelp paying user count—are disclosed quarterly and provide the clearest signal of whether the turnaround thesis is gaining traction or fading.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube