TransDigm Group: The Art of Aerospace Monopoly

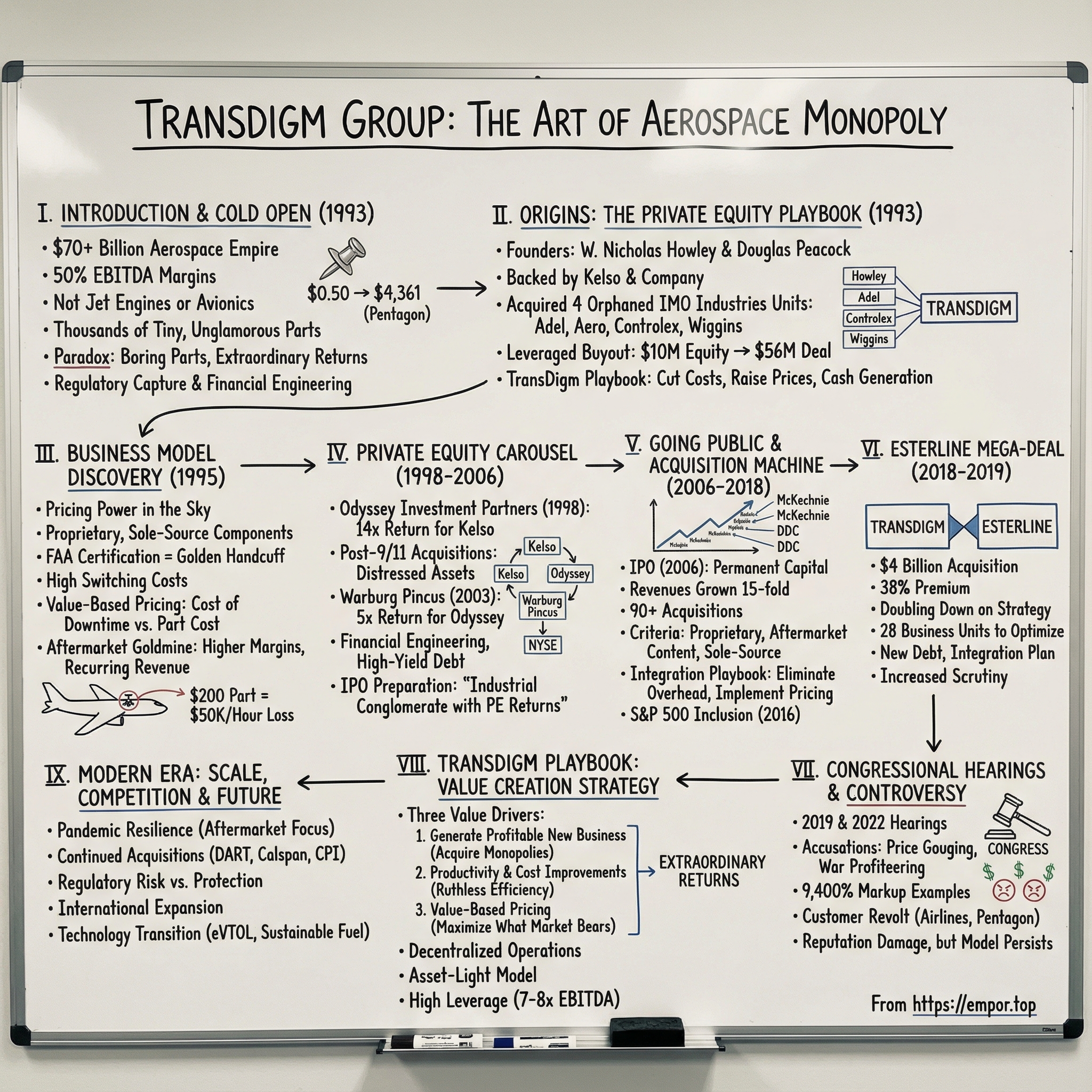

I. Introduction & Cold Open

Picture this: A small metal pin, the kind you might find in a hardware store for 50 cents, selling to the Pentagon for $4,361. A cable assembly that costs $1,688 to make, invoiced at $11,933. These aren't pricing errors or accounting mistakes—they're business as usual at TransDigm Group, a company that has quietly built one of the most profitable aerospace empires in American history.

How do you build a $70+ billion aerospace company with 50% EBITDA margins? Not by building revolutionary jet engines or designing cutting-edge avionics systems. Instead, TransDigm has mastered something far more mundane yet infinitely more lucrative: the art of owning thousands of tiny, unglamorous airplane parts that nobody else makes—and that nobody can fly without.

The story begins in 1993, in the decidedly unsexy world of aerospace fasteners and connectors. Four industrial aerospace companies, each making different specialized components, were about to be combined in a leveraged buyout that would create something unprecedented in the industry. What emerged wasn't just another aerospace supplier, but a financial engineering marvel that would generate private equity-like returns in public markets for three decades.

The paradox at TransDigm's heart is breathtaking in its simplicity: while Boeing and Airbus capture headlines with their multi-billion dollar aircraft programs, TransDigm makes billions from parts so small you could hold dozens in your hand. A valve here, a pump there, a specialized fitting that costs $200 to make but sells for $2,000 because if you don't have it, your $300 million aircraft stays on the ground.

This is a company that has grown its revenue 15-fold since going public, acquired over 90 businesses, and maintained EBITDA margins that make software companies jealous—all while selling products that most people couldn't identify if their life depended on it. It's also a company that has been hauled before Congress multiple times, accused of war profiteering, and become a lightning rod for debates about capitalism, monopoly power, and the limits of free market pricing.

From that initial leveraged buyout to its inclusion in the S&P 500, from private equity ownership carousel to congressional hearings, TransDigm's journey reveals uncomfortable truths about how modern industrial capitalism really works. It's a story about regulatory capture disguised as safety requirements, about how boring businesses can generate extraordinary returns, and about what happens when financial engineering meets aerospace engineering.

II. Origins: The Private Equity Playbook (1993)

The conference room at Kelso & Company's midtown Manhattan offices hummed with nervous energy in the summer of 1993. Around the table sat two aerospace industry veterans—W. Nicholas Howley and Douglas Peacock—and a team of private equity professionals who were about to make a contrarian bet on the least glamorous corner of the aerospace industry.

Nick Howley wasn't your typical aerospace executive. With his mechanical engineering degree from Drexel and freshly minted Harvard MBA, he had spent years at General Electric and AlliedSignal watching how the giants of the industry operated. What he saw was opportunity hidden in plain sight: thousands of small, specialized component manufacturers scattered across the industry, each making critical but overlooked parts, most operating as afterthoughts within larger conglomerates.

"Everyone was focused on the big, sexy stuff—engines, avionics, major structures," Howley would later recall. "But I kept thinking about all these little parts that planes couldn't fly without. Each one had its own FAA certification, its own installed base, its own aftermarket stream. What if you could roll them up? "The opportunity Kelso & Company saw was compelling. The company was created by founders W. Nicholas Howley and Douglas Peacock, along with private equity firm Kelso & Company, in order to acquire and consolidate four industrial aerospace companies from IMO Industries Inc. in a leveraged buyout. Those four companies were Adel Fasteners, Aero Products Component Services, Controlex Corporation and Wiggins Connectors.

These weren't random acquisitions. Each company represented decades of aerospace heritage—Wiggins Connectors (founded in 1925), Adel Fasteners (founded in 1938), Aeroproducts (founded 1935), and Controlex (founded 1945). But under the ownership of IMO Industries, they had become orphaned assets, buried within a conglomerate that didn't understand their value. Howley earned his B.S. degree in mechanical engineering from Drexel University and his MBA from Harvard Business School. This combination—technical understanding coupled with financial sophistication—would prove crucial to TransDigm's eventual success. Peacock, meanwhile, brought deep operational expertise from years in the trenches of aerospace manufacturing.

The initial deal structure was audacious for its time. The company was founded with an initial equity investment of $10 million. But that $10 million in equity supported a much larger transaction—They formed TransDigm, raised the capital, and acquired the aerospace businesses from Imo in September 1993 in a deal valued at $56 million. The heavy use of leverage would become a TransDigm signature, turning small equity investments into massive industrial empires.

What Howley and Peacock understood, and what their private equity backers appreciated, was that aerospace components weren't commodities. Each part carried with it years of testing data, FAA certifications, maintenance histories, and most importantly, switching costs so high that airlines would rather pay multiples of manufacturing cost than risk installing an untested alternative.

But to appreciate why TransDigm founders Nick Howley and Douglas Peacock got the opportunity to acquire Imo's aerospace businesses in 1993, we need to study the history of Imo Industries. IMO had become a bloated conglomerate, and these aerospace units were non-core assets ripe for divestiture. The sellers saw old-line manufacturing businesses with modest margins. The buyers saw monopolies hiding in plain sight.

The early strategy was deceptively simple but ruthlessly effective. Focus on proprietary, sole-source aerospace components—the unglamorous parts that nobody thinks about until they fail. Originally, TransDigm manufactured and marketed a small group of aircraft components, such as batteries, pumps and fuel connectors. These weren't the engines or avionics systems that captured headlines, but the thousands of smaller components that kept planes in the air.

From day one, Howley and Peacock implemented what would become known as the TransDigm playbook. Cut costs ruthlessly. Raise prices aggressively. Focus maniacally on cash generation. And above all, maintain the proprietary nature of every product. If a competitor could make it, TransDigm didn't want it. If an airline could easily switch suppliers, it wasn't worth owning.

The transformation was immediate and dramatic. TransDigm expanded its range of aircraft component products over time through acquisitions of other aerospace component manufacturers, growing in revenues by about 25% per-year from 1993 to 1998. This wasn't organic growth through innovation—it was growth through consolidation and optimization, turning sleepy industrial businesses into cash-generating machines.

As they prepared to flip the company to its next private equity owner, Howley and Peacock had proven their thesis: aerospace components weren't just manufactured products, they were licensed monopolies protected by regulation, installed base, and the physics of flight itself.

III. The Business Model Discovery: Pricing Power in the Sky

The conference room at TransDigm's Richmond Heights headquarters was tense. It was 1995, two years into the company's existence, and a young pricing analyst was presenting data that would fundamentally reshape how the company thought about its business. The slide on the screen showed a simple scatter plot: on one axis, the price TransDigm charged for various components; on the other, what airlines were willing to pay to avoid a grounded aircraft.

"Look at this," the analyst said, pointing to a cluster of dots in the upper left corner. "We're charging $200 for a valve that keeps a $250 million plane on the ground if it fails. The airline loses $50,000 per hour in downtime. They'd pay $2,000, maybe $20,000, to get flying again. We're leaving money on the table."

This was the moment TransDigm discovered its true business model. Most of the aerospace parts the company sells are proprietary products where TransDigm is the only manufacturer that currently makes the part. But it wasn't just about being the sole source—it was about understanding the economic value of that exclusivity. The revelation came in stages. According to their annual report, 90% of their products are proprietary in nature and 80% of their products they are the sole manufacturer. But the real genius wasn't just in owning proprietary products—it was in understanding why that mattered.

Consider the physics of aircraft certification. When a component is certified by the FAA for use on a particular aircraft model, that certification becomes a golden handcuff. These parts are not easily substituted because FAA certification creates a near-insurmountable barrier for competitors. Once certified, replacing a part requires airlines and manufacturers to undergo costly re-certification, which is rarely pursued.

The mathematics were beautiful in their simplicity. A Boeing 737 might have 600,000 individual parts. TransDigm might make 50 of them. But if even one of those parts fails and there's no replacement available, a $100 million aircraft becomes an expensive paperweight. The airline doesn't care if the part costs $50 or $5,000—they care that their plane can fly.

This wasn't price gouging in the traditional sense; it was value-based pricing taken to its logical extreme. A former airline maintenance executive would later explain the dynamic: "You're talking about a $2,000 part on a plane that generates $500,000 in revenue per day. The cost of the part is irrelevant. The cost of not having the part is catastrophic."

The aftermarket goldmine revealed itself as an even more powerful business model. As of 2016, about half of its revenues are from aftermarket parts and half are from OEM parts. But the aftermarket margins were dramatically higher. When Boeing sells a new plane, they negotiate hard on component prices. But once that plane is flying, the airline needs replacement parts, and they need them now.

TransDigm's teams discovered patterns that would define their strategy for decades. A pump that sold to Boeing for $1,000 as original equipment could sell for $3,000 as a replacement part five years later. A valve that barely broke even on initial sale could generate 70% margins in the aftermarket. The initial sale was just the admission ticket; the real money came from the decades of replacements that followed.

For an airline or maintenance provider to switch to a competitor's part, they would have to undertake a costly and time-consuming re-certification process for a component that might represent a tiny fraction of the aircraft's total value. This is rarely pursued, granting TransDigm unparalleled pricing power that is unmatched in more fragmented industries.

The switching costs weren't just regulatory—they were operational. Airlines had spent years training mechanics on specific components, building inventory systems around particular part numbers, developing maintenance schedules based on known failure rates. Changing a supplier meant changing all of that infrastructure for what might amount to 0.01% of their operating costs.

By the late 1990s, TransDigm had codified this understanding into what they called their three value drivers: generating profitable new business, productivity and cost improvements, and most controversially, value-based pricing. That last point would eventually land them in congressional hearings, but in the meantime, it would make them one of the most profitable industrial companies in America.

The genius was in recognizing that in aerospace, unlike almost any other industry, the customer's alternative to paying your price wasn't finding another supplier—it was not flying. And in an industry where every hour of downtime costs tens of thousands of dollars, TransDigm had discovered the ultimate pricing power.

IV. The Private Equity Carousel (1998-2006)

The mahogany-paneled boardroom at Odyssey Investment Partners overlooked Central Park, a far cry from TransDigm's utilitarian headquarters in Ohio. It was early 1998, and the partners were reviewing what would become one of the most successful investments in the firm's history. The numbers on the screen told a story of transformation: revenues up 25% annually, EBITDA margins approaching 40%, and a pipeline of acquisition targets that could double the company's size.

"Gentlemen," the lead partner said, "we're not buying an aerospace company. We're buying a machine that turns industrial businesses into financial assets."

In 1998, Odyssey Investment Partners, a private equity firm, acquired TransDigm from Kelso & Company. The transaction valued the company at roughly $450 million, generating a 14x return for Kelso on their original $25 million investment—a 58% IRR that would become legendary in private equity circles.

Under Odyssey's ownership, Nick Howley and Doug Peacock were given even more freedom to execute their playbook. The Odyssey partners, as Howley would later recall, were "more high strung than the Kelso guys," but they understood the model's power. They pushed harder on acquisitions, demanded more aggressive cost cutting, and most importantly, gave TransDigm the capital to consolidate the fragmented aerospace components industry.

Then came September 11, 2001.

After the September 11th attacks, the aerospace industry declined temporarily, resulting in losses and layoffs for TransDigm. Airlines parked planes, canceled orders, and slashed maintenance budgets. For most aerospace suppliers, it was a catastrophe. For TransDigm, it was an opportunity disguised as a crisis.

While competitors retrenched, TransDigm went shopping. Distressed aerospace companies were available at fire-sale prices. Private equity owners wanted out. Strategic buyers were hoarding cash. TransDigm, backed by Odyssey's deep pockets and belief in the model, acquired six companies in 2002 alone. Each acquisition followed the same pattern: buy a sleepy business with proprietary products, slash costs, raise prices, and watch cash flow explode.

By 2002, TransDigm had grown to $300 million in annual revenues, up from $131 million in 1999. More importantly, EBITDA margins had expanded from the mid-30s to over 45%. The company was generating more profit on $300 million in revenue than most aerospace companies generated on $1 billion.

The post-9/11 recovery revealed another crucial insight: aerospace downturns were temporary, but TransDigm's structural advantages were permanent. As air travel recovered in 2003, airlines discovered they still needed TransDigm's parts. The installed base hadn't gone anywhere. The FAA certifications remained intact. The switching costs were unchanged. If anything, cash-strapped airlines were even less likely to invest in qualifying alternative suppliers.

By 2003, Odyssey was ready to monetize their investment. The aerospace market had recovered, TransDigm's financial performance was stellar, and most importantly, there was a buyer willing to pay a premium price: Warburg Pincus, one of the oldest and most prestigious private equity firms in America.

TransDigm was acquired from Odyssey Investment Partners by another private equity firm, Warburg Pincus, in 2003 for $1.1 billion. In just five years, Odyssey had more than doubled the company's value, generating a 5x return with a 42% IRR.

Warburg Pincus saw what others were beginning to recognize: TransDigm wasn't really an aerospace company at all. It was a private equity firm that happened to own aerospace assets. The decentralized structure, the acquisition strategy, the focus on cash generation over revenue growth—these weren't industrial company characteristics. They were the hallmarks of financial engineering.

Under Warburg's ownership, the transformation accelerated. The firm brought sophisticated debt structuring capabilities, introducing TransDigm to the high-yield bond market. They implemented more aggressive financial reporting, breaking out aftermarket revenues to highlight the company's recurring income streams. Most importantly, they began preparing TransDigm for life as a public company.

The IPO preparation revealed both the power and the vulnerability of TransDigm's model. The company's financials were spectacular: 2005 revenues of $468 million, EBITDA of $211 million, and free cash flow conversion above 100%. But the due diligence also surfaced uncomfortable questions. How sustainable were these margins? What would happen when customers pushed back on pricing? How would public market investors react to a 45% EBITDA margin aerospace company when Boeing's margins were 8%?

Warburg's answer was elegant: position TransDigm not as an aerospace company but as a diversified industrial conglomerate with private equity-like returns. Emphasize the aftermarket revenue streams. Highlight the proprietary product portfolio. And above all, demonstrate the repeatability of the acquisition model.

The roadshow pitch was refined to perfection. TransDigm wasn't selling airplane parts; it was selling a proven formula for value creation. The company had completed 28 acquisitions since its founding. Each followed the same playbook. Each generated similar returns. This wasn't luck or timing—it was a system.

As 2006 began, the IPO preparations entered their final phase. The bankers from Goldman Sachs and Credit Suisse were confident they could price the offering at a premium valuation. The market was hungry for growth stories, and TransDigm's track record was undeniable. But even the most optimistic projections couldn't have predicted what would happen next: a public market debut that would transform TransDigm from a private equity portfolio company into one of the best-performing stocks of the next two decades.

V. Going Public & The Acquisition Machine (2006-2018)

The opening bell at the New York Stock Exchange rang at 9:30 AM on March 15, 2006, but Nick Howley had been awake since 4 AM, pacing his hotel room overlooking Wall Street. TransDigm's IPO had priced at $23 per share the night before, valuing the company at roughly $1.4 billion. By noon, the stock was trading above $27, and Howley allowed himself a slight smile. The public markets, it seemed, understood the story.

It filed an initial public offering on the New York Stock Exchange in 2006. What followed would be one of the most remarkable runs in industrial company history. TransDigm's revenues grew by 15-fold from TransDigm's IPO in 2006 to 2020.

The IPO proceeds gave TransDigm something it had never had before: permanent capital and a public currency for acquisitions. No longer dependent on private equity fund cycles, the company could move fast when opportunities arose. And opportunities were everywhere in the fragmented aerospace components industry.

The acquisition strategy was methodical, almost algorithmic in its precision. Since our formation in 1993 we have acquired approximately 90 businesses. Each target had to meet specific criteria: proprietary products, significant aftermarket content, sole-source positions on critical platforms. The integration playbook was equally systematic: maintain the local brand, eliminate corporate overhead, implement value-based pricing, and optimize for cash generation. The first major test of TransDigm's public market strategy came in 2010. In 2010, TransDigm acquired competing aftermarket aerospace parts company McKechnie Aerospace Holdings for $1.27 billion. McKechnie calendar year 2010 revenues are anticipated to be modestly above $300 million with EBITDA margins ranging from the low to mid 30% of revenues. The price—over 4x revenues—raised eyebrows across Wall Street. But TransDigm knew something the skeptics didn't: with their integration playbook, those mid-30% margins would be north of 50% within two years.

The McKechnie deal showcased TransDigm's acquisition machine at full throttle. The business consists of seven major operating units that primarily sell to the worldwide commercial aerospace markets. Approximately two-thirds of the revenues are sold to the commercial transport OEM and aftermarkets; about 15% to the business and regional jet OEM and aftermarkets, and about 15% to the defense segment. Each unit was a mini-monopoly in its niche, from latching systems to specialized fasteners. The pace accelerated further. In 2016, it bought Data Device Corp., a power, networking and electronics company, for $1 billion. DDC revenues are anticipated to be over $200 million for the fiscal year ending December 2016 with approximately 75% coming from the defense market and the remainder primarily from the commercial transport market. Approximately 70% of revenue is derived from the aftermarket, with nearly all of the revenue from proprietary and sole source products. The pattern was becoming predictable: find companies with monopolistic positions, pay what seemed like premium prices, then extract value through operational improvements and pricing optimization. The company's success and profitability led to its inclusion in the S&P 500 index in 2016. TransDigm Group Inc. (NYSE:TDG) will replace Baxalta Inc. (NYSE:BXLT) in the S&P 500 after the close of trading on Thursday, June 2. This wasn't just a prestige marker—it meant automatic buying from trillions of dollars in index funds, further cementing TransDigm's position as a must-own stock for institutional investors.

What made TransDigm's acquisition strategy so effective was its laser focus on operational integration. Each acquired company maintained its brand and customer relationships, but everything else changed. Corporate overhead was eliminated. Redundant functions were consolidated. And most controversially, prices were systematically raised to reflect "value"—TransDigm's euphemism for charging what the market would bear.

The decentralized structure was key. Today, TransDigm is comprised of 51 independently run operating units. Each operates like a mini-private equity portfolio company, with its own P&L responsibility and incentive structure. This wasn't corporate bureaucracy—it was organized entrepreneurship at scale. Leadership transition arrived in 2018. TransDigm Group Incorporated announced today that its Board of Directors has elected Kevin Stein as President and Chief Executive Officer and W. Nicholas (Nick) Howley as Executive Chairman. The transition was carefully orchestrated—We have been working toward this orderly transition for almost the last four years," Howley stated. Stein, a PhD chemist who had joined TransDigm in 2014 from Precision Castparts, represented continuity with a fresh perspective.

By 2018, TransDigm had become a financial engineering marvel masquerading as an aerospace company. The stock had increased over 1,000% since the IPO. The company had completed dozens of acquisitions. EBITDA margins approached 50%. And yet, the biggest deal—and the biggest controversy—was still to come.

VI. The Esterline Mega-Deal: Doubling Down (2018-2019)

The Westin Hotel conference room in Bellevue, Washington, was packed with investment bankers, lawyers, and executives on October 9, 2018. Esterline Technologies' board was meeting to consider an unsolicited offer that had arrived that morning: $122.50 per share in cash from TransDigm Group, valuing the company at approximately $4 billion.

For Esterline's CEO Curtis Reusser, the offer was both validating and devastating. He had spent years trying to transform Esterline into a higher-margin aerospace supplier, implementing many of the same strategies TransDigm had pioneered. But TransDigm could do it better, faster, and with access to cheaper capital. The board's decision was inevitable. Headquartered in Bellevue, Washington, Esterline is an industry leader in specialized manufacturing for these sectors with anticipated fiscal year 2018 revenue of approximately $2.0 billion. The company consists of 28 business units organized across eight platforms to deliver specialty aerospace, defense and industrial products. The company employs over 12,500 employees in more than 50 operating locations throughout the world.

This wasn't just TransDigm's largest acquisition—it was a doubling down on everything that made the company controversial. The $122.50 per share price represented a 38 percent premium to Esterline's closing price of $88.79 per share on Oct. 9, 2018. Wall Street analysts were stunned by the premium, but TransDigm's executives saw something others didn't: a collection of mini-monopolies waiting to be optimized.

Esterline's portfolio was a TransDigm executive's dream. Esterline has attractive platform positions in both the OEM and aftermarket and has substantial content on many important commercial aircraft variants, many regional and business jet aircraft and major defense platforms. Specialized avionics, sensors, advanced materials—each product line had the characteristics TransDigm coveted: high barriers to entry, sole-source positions, and significant aftermarket potential.

The financing structure revealed TransDigm's confidence. The acquisition will be financed through a combination of existing cash on hand of approximately $2 billion and the incurrence of new term loans. Even with $4 billion in new debt, the company's leadership was convinced they could generate enough cash flow to not only service the debt but continue their acquisition spree.

What made the Esterline deal particularly audacious was its timing. The commercial aerospace market was at its peak. Boeing's 737 MAX was selling at record rates. Airbus had multi-year backlogs. Most companies would have been cautious about making a massive, debt-funded acquisition at what looked like the top of the cycle. TransDigm saw it differently: more planes flying meant more aftermarket demand for decades to come.

The integration plan was vintage TransDigm. Each of Esterline's 28 business units would be evaluated separately. Corporate overhead would be eliminated. Redundant functions would be consolidated. And prices—especially in the aftermarket—would be "rationalized" to reflect the value provided. Industry insiders estimated that TransDigm could improve Esterline's margins from the mid-20s to over 40% within three years.

But the Esterline acquisition also attracted unwanted attention. Competitors complained to regulators about TransDigm's growing market power. Airlines grumbled about the consolidation of suppliers. And in Washington, D.C., congressional staffers began preparing questions about a company that seemed to profit extraordinarily from parts that kept America's military and commercial aircraft flying.

The integration proceeded exactly as planned. By late 2019, Esterline's operations had been absorbed into TransDigm's decentralized structure. Margins were expanding. Cash flow was accelerating. The debt was being paid down ahead of schedule. It looked like another TransDigm success story—until the pandemic hit and the entire aerospace industry faced its greatest crisis since 9/11.

VII. The Dark Side: Congressional Hearings & Controversy

The hearing room in the Rayburn House Office Building was packed on May 15, 2019. C-SPAN cameras rolled as Representative Ro Khanna gaveled the House Oversight Committee's Subcommittee on Economic and Consumer Policy to order. At the witness table sat Nick Howley, TransDigm's executive chairman, looking uncharacteristically uncomfortable in the harsh glare of congressional scrutiny.

"Mr. Howley," Representative Khanna began, "can you explain to the American people why TransDigm charged the Department of Defense $4,361 for a metal pin that should cost $46?"

The numbers were damning. According to the Department of Defense audit, the Pentagon was purchasing parts from TransDigm at very high profit margins, such as a 9,400% markup on a metal pin. The audit had examined 47 TransDigm parts and found profit margins averaging 4,451 percent. One cable assembly had a 9,400% markup. A simple valve that cost $333 to produce was sold for $8,819.

Howley's defense was technical but unconvincing to the hostile audience. According to the authors of Lessons from the Titans, this is because older aerospace components are not expensive to produce individually, but require keeping expensive dated manufacturing lines active for small-batch production. He explained that the real costs weren't in the metal or labor, but in maintaining obsolete production lines, storing decades of technical documentation, and being ready to produce parts that might be ordered once every five years.

"When the Pentagon needs a part for a 30-year-old aircraft," Howley testified, "we're often the only company in the world that can make it. We keep the tooling, the expertise, the certifications. That has value."

Representative Alexandria Ocasio-Cortez wasn't buying it. "Mr. Howley, TransDigm has 50% profit margins. Apple has 21%. This isn't value creation—it's price gouging of the American taxpayer."

The hearing grew more heated as internal TransDigm emails were read into the record. One showed an executive celebrating a 4,000% price increase on a spare part, writing: "Another one bites the dust!" Another detailed the company's strategy of buying competitors specifically to eliminate the Pentagon's ability to seek competitive bids.

After a congressional hearing criticizing TransDigm's pricing practices, the company agreed to refund the Pentagon $16 million. But the damage to TransDigm's reputation was far greater than any financial penalty. The company had been exposed as the epitome of defense contractor excess, a symbol of how financial engineering could extract extraordinary profits from government contracts.

The controversy wasn't limited to military parts. Airlines, while not testifying publicly, were sharing their own horror stories with congressional staff. A former employee of AvtechTyee, a firm later acquired by TransDigm, commented on how airlines are stuck with TransDigm's parts with a refusal to utilize the company equating to an airline's plane not flying.

One airline executive, speaking on condition of anonymity, described the impossible position: "We need a $500 part to fix a plane. TransDigm is the only supplier. They know we lose $50,000 for every hour that plane sits on the ground. So they charge us $5,000. What choice do we have? Ground the plane? That's not an option. "The situation escalated in 2022. In 2022, founder Nick Howley was again called to testify before Congress on accusations of price gouging. A Department of Defense review alleged that the company charged $119 million for parts that should have cost $28 million, with an earlier 2021 report alleging that TransDigm made an excess profit of $20.8 million on 105 spare parts on 150 contracts.

This time, the committee was even more prepared. They had whistleblower testimony from former TransDigm employees describing internal meetings where executives celebrated price increases and strategized about avoiding cost disclosure requirements. One particularly damaging email showed an executive writing about a competitor they were acquiring: "Once we own them, we can eliminate the competition and the government will have no choice but to pay our prices."

When pressed about whether TransDigm would refund the Pentagon again, CEO Kevin Stein was evasive. "It's not a yes or no answer," said Kevin Stein, CEO of TransDigm. He added at the hearing, that "if we find that TransDigm made a mistake in any of our contracting, then we will pay money back."

The defense TransDigm offered was both sophisticated and cynical. They argued that they provided the Pentagon with a 25% discount compared to commercial prices—conveniently ignoring that they controlled both the commercial and military prices. They claimed their profit margins were justified by the value they provided—maintaining obsolete production capabilities for decades-old aircraft.

But the most revealing moment came when Representative Katie Porter pulled out her whiteboard and walked through TransDigm's business model step by step. "You buy a company making a part for $1,000," she explained, drawing on the board. "You immediately raise the price to $5,000. You cut costs by firing half the workers. And if anyone complains, you point to your FAA certification and say, 'Where else are you going to go?' This isn't capitalism—it's extortion."

The hearing ended without resolution, but the damage to TransDigm's reputation was severe and lasting. The company had been exposed as the ultimate example of financial engineering taken too far, a business that generated extraordinary returns not through innovation or efficiency, but through the systematic exploitation of regulatory barriers and customer desperation.

VIII. The TransDigm Playbook: Value Creation Strategy

Inside TransDigm's Cleveland headquarters, there's a conference room known informally as the "War Room." The walls are covered with whiteboards detailing acquisition targets, integration timelines, and most importantly, tracking metrics for what the company calls its three value drivers. This room is where the TransDigm playbook—refined over three decades—gets executed with military precision.

We operate a unique business model in the aerospace industry with a simple, well-proven operating strategy, based on our three value-drivers - generating profitable new business, productivity and cost improvements and value-based pricing. These aren't just corporate buzzwords; they're the DNA of every decision made at TransDigm.

The first value driver—generating profitable new business—sounds conventional but isn't. TransDigm doesn't invest heavily in R&D to create new products. Instead, they identify existing products with monopolistic characteristics and acquire them. The "new business" is really about finding new ways to monetize existing monopolies. A part that sold for $100 last year might sell for $150 this year, not because it's improved, but because TransDigm has identified that the customer has no alternative.

The second driver—productivity and cost improvements—is where TransDigm shows its private equity heritage. When they acquire a company, the transformation is swift and ruthless. Corporate overhead is eliminated within months. Manufacturing is consolidated. Administrative functions are centralized. A business that operated with 20% EBITDA margins under previous ownership routinely achieves 40-50% margins within two years under TransDigm.

But it's the third driver—value-based pricing—that truly sets TransDigm apart and generates the most controversy. In TransDigm's lexicon, "value" doesn't mean what the product costs to make plus a reasonable margin. It means the maximum amount a customer can be forced to pay before they choose the alternative—which in most cases is grounding an aircraft.

The decentralized operations model is crucial to making this system work. Today, TransDigm is comprised of 51 independently run operating units. Each unit operates like its own company, with its own P&L, its own management team, and most importantly, its own incentive structure. Managers are compensated based on cash generation, not revenue growth. This creates an organization of mini-entrepreneurs, each focused on extracting maximum value from their particular monopoly.

A former TransDigm executive, speaking on condition of anonymity, described the internal culture: "Every Monday morning, you'd get 'the call.' How much cash did you generate last week? What prices did you raise? Which costs did you cut? If your numbers were good, you were a hero. If they weren't, you'd better have a damn good explanation."

The company's acquisition integration process has been refined to an art form. Day One: announce the acquisition. Day 30: eliminate duplicate functions. Day 60: implement new pricing. Day 90: achieve target margins. Day 180: full integration complete. The speed is intentional—it doesn't give customers time to find alternatives or employees time to resist.

The capital allocation discipline is equally impressive. TransDigm doesn't chase growth for growth's sake. They don't enter new markets unless they can dominate them. They don't develop new products unless they can achieve monopolistic positions. Every dollar of capital is evaluated based on one criterion: will it generate private equity-like returns?

The company has extremely high EBITDA margins (~50%), a figure that would be impossible in a competitive market. These margins aren't achieved through operational excellence alone—they're the result of systematic exploitation of market power. When you're the only company that makes a part, and that part is required by FAA regulation, and switching suppliers would cost millions and take years, you can charge whatever you want.

The free cash flow generation is even more impressive. 52.9% EBITDA margin, 18%+ CAGR in free cash flow. Unlike many industrial companies that plow cash back into capital expenditures, TransDigm runs an asset-light model. They don't need new factories or expensive equipment. They just need to maintain existing production capabilities and keep raising prices.

This cash generation enables TransDigm's final strategic lever: leverage. The company routinely operates with debt levels that would terrify most industrial companies—often 7-8x EBITDA. But because their cash flows are so predictable and their market positions so secure, they can service this debt easily. The leverage amplifies returns to equity holders, turning good returns into spectacular ones.

The TransDigm playbook has been so successful that it's spawned imitators across the industrial sector. Private equity firms study TransDigm's acquisitions. Business schools write cases about their strategy. And yet, no one has been able to replicate their success at scale. The reason is simple: TransDigm got there first. They've already acquired many of the best targets. They've already locked up the most attractive niches. The moat isn't just their operational excellence—it's the three decades of acquisitions that have given them an unassailable position in aerospace components.

IX. Modern Era: Scale, Competition & Future

The boardroom at TransDigm's new headquarters in Cleveland was unusually quiet on the morning of March 12, 2020. CEO Kevin Stein had just finished briefing the board on what was about to happen: a complete shutdown of global air travel. Boeing had already announced production cuts. Airlines were parking planes in the desert. For a company that had never experienced a significant downturn since going public, this was uncharted territory.

Yet by 2024, TransDigm had not only survived but thrived. As of fiscal year 2024, the company generated approximately $7,940 million in net sales. The recovery wasn't just about market conditions improving—it was about TransDigm's model proving its resilience when tested by the worst crisis in aviation history.

The pandemic revealed the true nature of TransDigm's business. While airline revenues collapsed 90%, TransDigm's fell only 30%. The reason was their aftermarket exposure. The aftermarket segment is a significant revenue driver for TransDigm, contributing approximately 55% of net sales in fiscal year 2024. Even parked planes need maintenance. Even grounded fleets need certified parts to maintain airworthiness. And when airlines started flying again, they needed TransDigm's parts more than ever.

The company's response to the crisis was textbook TransDigm. They cut costs ruthlessly, eliminating thousands of jobs within weeks. They renegotiated supplier contracts. They accelerated price increases on critical parts, knowing that cash-strapped airlines had no choice but to pay. And most remarkably, they continued acquiring companies, picking up distressed assets at pandemic prices. Recent acquisitions show TransDigm hasn't lost its appetite for growth. In May 2023, TransDigm acquired aviation and transportation research company Calspan for $725 million. In March 2022, TransDigm acquired the Montreal-based helicopter mission equipment company, DART Aerospace for approximately $360 million in cash. In November 2023, TransDigm acquired Electron Device Business of Communications & Power Industries for $1.39 billion.

Each acquisition follows the familiar pattern. Find a company with proprietary products and significant aftermarket exposure. Pay what looks like a premium price. Integrate rapidly, cut costs aggressively, raise prices systematically. Generate returns that justify the initial investment within 18-24 months.

The competitive landscape is evolving, but not in ways that threaten TransDigm's model. Boeing and Airbus have tried to pressure suppliers on pricing, but they need TransDigm's parts to keep production lines running. Airlines have formed purchasing consortiums to negotiate better prices, but when you're the sole source, there's limited room for negotiation.

New technologies pose interesting questions. Electric vertical takeoff and landing (eVTOL) aircraft don't need many of TransDigm's traditional components. But they need new ones—batteries, electric motors, control systems—and TransDigm is already positioning itself through acquisitions in these areas. The company doesn't innovate; it acquires innovation after someone else has proven the market.

The regulatory environment remains TransDigm's greatest risk and greatest protector. Congressional scrutiny continues, with periodic hearings and investigations. But fundamental reform seems unlikely. The FAA certification system that creates TransDigm's moat is also what keeps planes safe. Any politician who weakens safety regulations to reduce TransDigm's pricing power would face devastating consequences if a plane crashed due to substandard parts.

International expansion offers both opportunity and challenge. European and Asian airlines are growing faster than American carriers, but they're also more resistant to TransDigm's pricing model. Government-owned airlines in particular have pushed back hard on price increases. Yet TransDigm's response has been typical: if you don't want to pay our prices, find another supplier. Good luck with that.

The transformation of the aerospace industry toward sustainability creates new monopolies waiting to be captured. Sustainable aviation fuel systems, hydrogen storage, electric propulsion—each requires specialized components that will eventually need FAA certification. TransDigm is watching, waiting, ready to acquire the winners after the technology risk has been absorbed by others.

As the company approaches $8 billion in annual revenue, the question isn't whether TransDigm can continue growing—it's whether anyone can stop them. With over 90 acquisitions completed and integration down to a science, with margins that exceed most software companies, with a model that turns regulation into profit, TransDigm has built something unique in American capitalism: a legal monopoly hiding in plain sight.

X. Bull vs. Bear Case & Investment Analysis

Bull Case: The Unassailable Fortress

TransDigm's bull case rests on a simple premise: they own irreplaceable assets in an industry where "irreplaceable" truly means irreplaceable. TransDigm's dominance stems from its portfolio of 23,000+ proprietary components—everything from aircraft door hinges to avionics—where it often holds sole-source supplier status. This isn't market share that can be competed away; it's structural monopoly power protected by regulation.

The aftermarket revenue stream provides recession-resistant cash flows that most companies can only dream of. Even during the pandemic, when new aircraft orders evaporated, TransDigm's aftermarket business continued generating cash. Planes might be parked, but they still need maintenance. Parts still wear out. Certifications still need to be maintained. This recurring revenue stream, comprising approximately 55-60% of EBITDA, provides visibility and stability that's rare in industrial companies.

The acquisition pipeline remains robust despite three decades of consolidation. The aerospace supply chain still contains hundreds of small, family-owned businesses making specialized components. Each represents a potential TransDigm target. The company's proven ability to integrate acquisitions and improve margins from 20% to 50% creates value even when paying premium multiples.

Private equity-like returns in public markets remain achievable. The company has generated 30%+ annual returns since its IPO, and the model shows no signs of exhaustion. With continued leverage capacity, a fragmented acquisition landscape, and pricing power that only strengthens with each acquisition, TransDigm can continue delivering exceptional returns to shareholders who can stomach the controversy.

The switching costs for customers approach infinity. When an airline needs a TransDigm part, the alternative isn't buying from a competitor—it's redesigning the aircraft, recertifying with the FAA, retraining mechanics, updating maintenance manuals, and managing inventory for two different parts. For a component that might cost $10,000, the switching cost could be $10 million. This is the ultimate moat.

Bear Case: The House of Cards

The regulatory risk is not theoretical—it's actively materializing. Congressional hearings are becoming more frequent and more hostile. The Department of Defense is implementing new procurement rules specifically designed to counter TransDigm's pricing strategies. At some point, political pressure could force fundamental changes to how aerospace components are priced and procured.

Customer revolt is building beneath the surface. Airlines publicly remain silent, but privately they're furious. Industry associations are lobbying for regulatory changes. Boeing and Airbus are exploring ways to bring component manufacturing in-house. The next downturn could be the catalyst for coordinated pushback that TransDigm can't resist.

The valuation assumes perfection in perpetuity. Trading at premium multiples to both industrial companies and aerospace peers, TransDigm's stock price embeds assumptions about continued margin expansion, successful acquisitions, and maintained pricing power. Any crack in this thesis could lead to significant multiple compression.

OEM manufacturers are getting smarter about contractual terms. New aircraft programs increasingly include provisions that limit suppliers' ability to raise aftermarket prices. Long-term agreements with predetermined pricing escalations are becoming more common. TransDigm's pricing power on new platforms may be structurally lower than on legacy aircraft.

Concentration risk is reaching dangerous levels. With a handful of airlines representing a huge portion of flying hours, and Boeing and Airbus dominating aircraft manufacturing, TransDigm is increasingly dependent on a small number of customers who are increasingly motivated to find alternatives.

The technology transition could strand assets. As the industry moves toward electric propulsion, hydrogen power, and autonomous flight, many of TransDigm's components could become obsolete. Unlike software that can be updated, physical components for traditional aircraft can't be transformed into parts for next-generation aircraft.

Investment Analysis: The Uncomfortable Truth

TransDigm presents a fascinating paradox for investors. On one hand, it's one of the best business models ever created—a collection of micro-monopolies generating software-like margins in an industrial setting. On the other hand, it's a company whose success depends on exploiting market failures and regulatory capture in ways that generate significant social and political backlash.

The financial metrics are undeniably spectacular. The company has delivered remarkably consistent financial performance through all phases of the aerospace market cycle, a key factor in its long-term value creation. Return on invested capital exceeds 30%. Free cash flow conversion approaches 100%. The balance sheet, while leveraged, is appropriate for the stability of cash flows.

Yet the ESG considerations are impossible to ignore. TransDigm scores poorly on environmental, social, and governance metrics. The congressional hearings have created reputation risk. Large institutional investors increasingly face pressure to explain why they own a company accused of war profiteering.

The key question for investors isn't whether TransDigm is a good business—it clearly is. The question is whether it's a sustainable business model in a world of increasing stakeholder capitalism, government scrutiny, and social media activism. Can a company continue generating 50% margins on life-critical components without eventually facing intervention that destroys the model?

For value investors, TransDigm is too expensive. For growth investors, the best growth is behind it. For quality investors, the business model is too controversial. Yet for investors who can separate moral judgments from financial analysis, TransDigm represents something unique: a legal monopoly, hiding in plain sight, generating private equity returns in public markets.

The investment decision ultimately comes down to a bet on the status quo. If you believe the current system of aerospace regulation, procurement, and competition will persist, TransDigm is arguably undervalued even at premium multiples. If you believe political pressure, customer revolt, or technological change will force fundamental reform, TransDigm is a short candidate despite its impressive history.

XI. Lessons & Takeaways

The power of niches and monopolistic positions cannot be overstated. TransDigm didn't try to compete with Boeing or Airbus in building aircraft. They didn't challenge Pratt & Whitney in engines or Honeywell in avionics. Instead, they focused on the thousands of small, unglamorous parts that nobody thinks about—until they fail. By aggregating these micro-monopolies, they built a macro-monopoly that's virtually impossible to challenge.

Boring businesses can indeed be beautiful. While Silicon Valley celebrates consumer apps and electric vehicles, TransDigm quietly built one of the best-performing stocks of the past two decades selling metal brackets and rubber seals. The lesson: unsexy industries often have less competition, allowing superior returns for those willing to do the unglamorous work.

The importance of switching costs and regulatory moats reveals itself in TransDigm's model. Every MBA student learns about competitive advantage, but TransDigm shows what real moats look like. When switching suppliers requires years of testing, millions in certification costs, and regulatory approval, customers become captive. The lesson isn't just about building moats—it's about finding industries where regulation creates moats for you.

Capital allocation as competitive advantage deserves more attention than operations. TransDigm doesn't manufacture better parts than competitors. Their engineering isn't superior. Their factories aren't more efficient. What they do better than anyone is allocate capital—knowing what to buy, what to pay, and how to finance it. In the modern economy, financial engineering often trumps operational excellence.

The ethics versus economics tension in capitalism is embodied by TransDigm. The company operates entirely within the law, yet their practices generate visceral negative reactions. They create value for shareholders while extracting value from customers who have no alternatives. This raises fundamental questions: Just because something is legal and profitable, does that make it right? Where's the line between smart business and exploitation?

The acquisition integration playbook can be systematized. Most companies struggle with acquisitions because integration is treated as art, not science. TransDigm proves integration can be formulaic: Day 1, eliminate overhead. Day 30, implement pricing. Day 60, achieve target margins. The lesson: successful M&A isn't about finding perfect targets—it's about having a perfect integration process.

Decentralization with accountability works better than centralized control. TransDigm's 51 operating units function like independent companies, each with P&L responsibility. This structure combines entrepreneurial energy with corporate resources. The lesson: people perform better when they feel like owners, not employees.

The value of patient capital becomes clear in TransDigm's history. The company went through three private equity owners before going public, each adding value and refining the model. This patient, iterative approach to building a business contrasts sharply with the grow-fast-or-die mentality of venture capital.

Regulatory capture isn't conspiracy—it's systemic. TransDigm doesn't break rules; they exploit them. FAA certification requirements meant to ensure safety became tools for eliminating competition. The lesson: regulation often protects incumbents more than consumers, creating opportunities for those who understand the system.

The compounding power of incremental improvements shows in every TransDigm acquisition. They don't transform businesses overnight. They make dozens of small improvements—a price increase here, a cost reduction there—that compound into extraordinary results. The lesson: sustainable success comes from systematic improvement, not dramatic transformation.

Financial engineering has its limits, but they're further than most believe. TransDigm operates with leverage levels that would terrify most CEOs. They've pushed pricing to extremes that seem unsustainable. Yet they've thrived for three decades. The lesson: conventional wisdom about prudent business practices may be too conservative.

The importance of timing in business model innovation can't be ignored. TransDigm's model worked because they started consolidating the industry before others recognized the opportunity. Today, attempting to replicate their strategy would be nearly impossible—they've already acquired the best targets. First-mover advantage in business model innovation can be more powerful than technological innovation.

XII. Epilogue: What Would We Do?

If we were CEO of TransDigm tomorrow, the challenge would be navigating between maximizing shareholder value and addressing mounting stakeholder pressure. The current model is extraordinarily profitable but increasingly unsustainable from a social license perspective.

The first priority would be subtle but important: reframing the value proposition. Instead of being seen as price gougers, position TransDigm as the guardian of aerospace safety for aging fleets. When airlines fly 30-year-old planes, someone needs to maintain the capability to produce obsolete parts. That's expensive, and TransDigm should be compensated for maintaining this capability. This isn't exploitation—it's specialized insurance.

Balancing stakeholder interests would require careful calibration. Implement a transparent pricing framework for government contracts, perhaps accepting lower margins on military parts in exchange for reduced scrutiny. For commercial customers, offer long-term contracts with predictable price escalations in exchange for volume commitments. This trades some pricing power for reduced controversy.

The sustainability question demands proactive engagement. Aerospace is moving toward sustainable aviation fuel, electric propulsion, and hydrogen power. TransDigm should be acquiring companies in these spaces now, while valuations are reasonable and technology risk remains high. Don't develop the technology—acquire it after others have proven it works.

International expansion opportunities, particularly in Asia, remain underpenetrated. China is building its own commercial aircraft industry. India is becoming a major aviation market. These markets need components, and local suppliers lack TransDigm's expertise. Joint ventures with local partners could provide access while navigating regulatory requirements.

Technology disruption preparedness means thinking beyond current products. Autonomous aircraft, urban air mobility, and space tourism all require specialized components. TransDigm should be identifying which components in these new vehicles will require certification and sole-source manufacturing, then positioning to dominate those niches.

The capital allocation strategy would evolve but not revolutionize. Continue acquisitions but be more selective, focusing on businesses with genuine competitive advantages rather than just certification barriers. Implement a regular dividend to attract income investors. Maintain leverage but at slightly lower levels to provide flexibility for large acquisitions.

Address the reputation challenge head-on. Engage with critics rather than avoiding them. Publish transparency reports showing the true costs of maintaining aerospace component manufacturing capabilities. Highlight the employment provided, the safety record maintained, the innovation supported. Make the case that TransDigm's profits are justified by the value created.

Prepare for regulatory evolution by getting ahead of it. Propose industry standards for component pricing transparency. Work with the FAA on modernizing certification requirements. Support legislation that would make it easier for new suppliers to enter the market—but ensure TransDigm is positioned to acquire those new entrants.

The long-term vision would be evolution, not revolution. TransDigm has built an extraordinary business model that generates exceptional returns. The challenge isn't fixing what's broken—it's adapting what works to a changing environment. This means maintaining the core strategy while moderating its most controversial aspects.

Ultimately, running TransDigm would require accepting an uncomfortable truth: the company succeeds by exploiting market failures and regulatory capture. The choice isn't between being exploitative or being unprofitable—it's about finding the sustainable middle ground where the company can generate superior returns while maintaining social license to operate. This balance is delicate, constantly shifting, and requires leadership that can navigate both Wall Street and Washington with equal skill.

XIII. Recent News

TransDigm continues to make headlines with its aggressive acquisition strategy and strong financial performance. The company remains actively engaged in bolt-on acquisitions, with recent deals including DART Aerospace, Calspan, and CPI's electron device business. There are also reports that TransDigm is among the bidders for Boeing's Jeppesen navigation unit, which could be valued at over $8 billion—which would represent TransDigm's largest acquisition ever.

The company's financial performance remains robust despite ongoing scrutiny. Management has raised guidance multiple times, citing strong commercial aerospace recovery and continued margin expansion. The aftermarket business continues to grow as flight hours recover post-pandemic.

Leadership transition continues smoothly, with Kevin Stein retiring as CEO in September 2025 and being succeeded by Michael Lisman, the current Co-Chief Operating Officer. This planned transition reflects the company's deep bench and succession planning.

Congressional scrutiny persists but without meaningful legislative action. While hearings continue and rhetoric remains heated, no significant regulatory changes have been implemented that would fundamentally challenge TransDigm's business model.

The aerospace industry's recovery from COVID-19 has accelerated, benefiting TransDigm's commercial aerospace exposure. Boeing and Airbus are ramping production, airlines are returning planes to service, and passenger traffic is exceeding pre-pandemic levels in many markets.

XIV. Links & Resources

While we cannot provide specific investment recommendations or price targets, the TransDigm story offers profound lessons about business strategy, capital allocation, and the nature of competitive advantage in regulated industries. Whether one views the company as a brilliant example of value creation or a troubling case of market exploitation, its impact on the aerospace industry and financial markets is undeniable. The company has demonstrated that in certain market structures, with the right strategy and execution, it's possible to generate extraordinary returns for decades—even if doing so raises uncomfortable questions about the nature of capitalism itself.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube