The Toronto-Dominion Bank: The Fortress and the Penalty Box

I. Introduction & Episode Roadmap

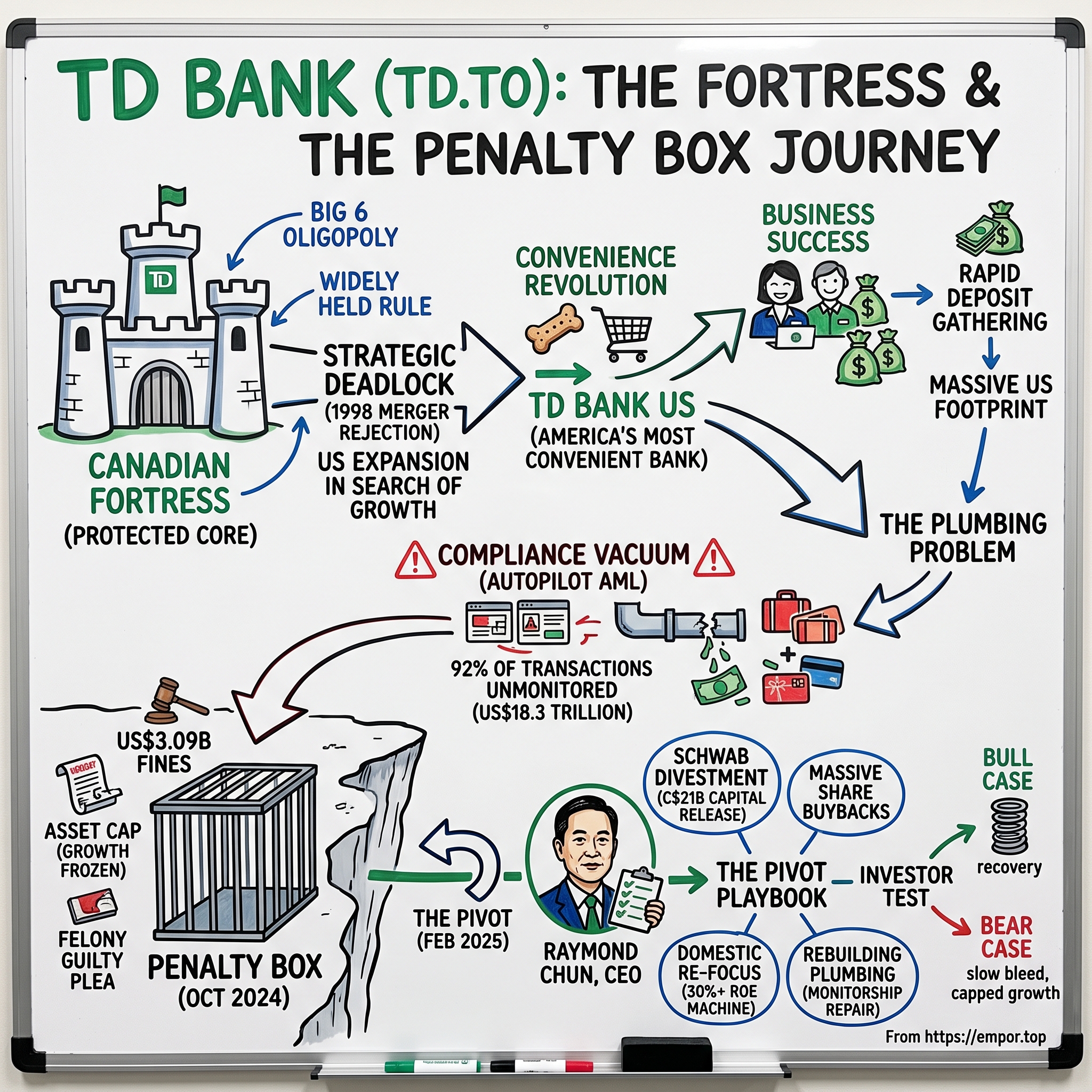

Picture two rooms on the same October morning in 2024, separated by a border and a chasm of reputation. In one — a wood-panelled boardroom in downtown Toronto — executives of a bank that has never failed in more than a century and a half are reviewing a domestic franchise so profitable it behaves less like a business than a utility with pricing power. In the other — a federal courtroom in Newark, New Jersey — lawyers for the very same institution stand up and enter a plea of guilty to conspiracy to commit money laundering, making The Toronto-Dominion Bank the largest bank in United States history to be branded a corporate felon.1

That is the dichotomy at the heart of this story, and it is genuinely strange. TD is, simultaneously, one of the most successful and one of the most disgraced banks in North America. North of the border it is a crown jewel of an oligopoly that governments have spent a century protecting; in the second quarter of its 2026 fiscal year, its Canadian Personal and Commercial Banking arm alone earned a record C$1.925 billion, up 15% year over year, on a return on equity north of 31%.2 South of the border, that same company operates under a Wells Fargo-style regulatory asset cap — a hard ceiling on how large its U.S. bank is legally permitted to grow — imposed by regulators who concluded it had, for the better part of a decade, run its anti-money-laundering program on autopilot while cartels wheeled suitcases of cash through its branches.

How did "America's Most Convenient Bank" — the outfit famous for open Sundays, free coin-counting machines, and dog biscuits at the drive-thru — become, in the words of the U.S. Department of Justice, the bank of choice for drug traffickers? The short version is that TD built a brilliant front office and neglected the plumbing behind it. Between January 2018 and April 2024, roughly 92% of the bank's transaction volume — approximately US$18.3 trillion in activity — flowed through TD's U.S. network without being screened by its automated monitoring systems.3 To put that number in human terms: it is a sum many times the size of the entire U.S. economy, waved through a decade of teller windows essentially unwatched. The bill for that neglect arrived in October 2024: a coordinated US$3.09 billion global settlement, a guilty plea, a four-year independent monitorship, and the asset cap.13

Then came the pivot. In February 2025, with the U.S. growth engine legally frozen, a new chief executive named Raymond Chun sold TD's entire 10.1% economic stake in The Charles Schwab Corporation for roughly C$21 billion, redirected the capital toward buybacks and the domestic core, and set about the unglamorous work of rebuilding a compliance culture under the eye of a federal monitor.4 Whether that pivot amounts to a genuine turnaround or merely elegant damage control is the central investment question, and this article does not intend to answer it for you so much as arm you to judge it.

There is a useful way to hold the whole story in your head. TD is a machine that converts a protected Canadian deposit base into cash at extraordinary rates of return, and the entire drama of the last decade is a drama about where that cash went. Sent into the American market in search of scale, it built a beloved retail brand and, underneath it, a compliance vacuum that criminals found before regulators did. The question now is whether the machine's owners have learned to respect the plumbing — or merely to hide it better.

Here is the roadmap. First, the Canadian fortress — the structure of the "Big Six" oligopoly and why it functions, for its members, as something close to a license to print money. Second, the expansion south: Ed Clark's customer-experience revolution and the birth of a retail brand that genuinely delighted Americans. Third, the rot under the hood — complacency, systems neglect, and the collapse of the First Horizon merger. Fourth, the money-laundering drama itself, in all its damning specificity. Fifth, the February 2025 pivot and the man executing it. Then the current earnings engine, the competitive powers at play, the bull and bear cases stress-tested against evidence, the durable lessons, and finally the ironies that make this a business story worth telling. We begin where the money is actually made.

II. The Canadian Fortress: Oligopoly, Paul Martin, and the "Big Six"

To understand why TD can absorb a US$3 billion fine and a felony conviction and still trade like a blue chip, you have to stop thinking about it as a bank competing for customers and start thinking about it as a member of a club. In Canada, six institutions — Royal Bank of Canada, Toronto-Dominion, Bank of Montreal, Scotiabank, CIBC, and National Bank — control the overwhelming majority of the nation's banking assets. This is not an accident of history or a temporary state of consolidation. It is the deliberate architecture of a country that decided, long ago, that it preferred a small number of large, safe banks to a large number of small, fragile ones.

TD itself is a product of that consolidating instinct. The modern bank was born in 1955 from the merger of two Victorian-era institutions: The Bank of Toronto, founded in 1855 by grain millers and merchants who wanted a reliable place to finance the wheat trade, and The Dominion Bank, founded in 1869. The combined entity was built to serve a booming post-war Canada — the resource extraction, the industrial expansion, the suburban mortgages of a country coming into its own. For our purposes the deep history matters less than the structure it produced, so hold onto one idea: from birth, TD was an instrument of scale in a market that rewarded scale and punished fragmentation. Everything that follows — the domestic dominance, the American overreach, the felony plea — flows from a bank built to be big in a country designed to keep banks few.

Why Canadian banking is a different animal

Why is Canadian banking so structurally different from the American model just across the lake? The United States spent most of its history with tens of thousands of small "unit banks," often confined by law to a single state or even a single location, fiercely competitive and chronically prone to failure. Canada chose the opposite: a handful of nationally branched banks operating coast to coast under a single federal regulator, the Office of the Superintendent of Financial Institutions (OSFI), with the Bank of Canada backstopping monetary stability. The regulator's animating priority was never dynamism or consumer choice; it was solvency. A nationally diversified bank could offset a bad year in the Alberta oil patch with a good year in Ontario manufacturing; a tiny American unit bank on the prairie had nowhere to hide when the local economy cratered.

The consequences showed up violently in the 1930s. When more than 9,000 U.S. banks failed during the Great Depression, wiping out savings and deepening the misery, Canada lost none of consequence. Canadians drew a lesson their institutions never forgot: in banking, resilience beats fragmentation, and safety is a feature worth paying for. That preference was institutionalized in the federal Bank Act, a piece of legislation Parliament reviews on a roughly five-year cycle in a recurring ritual that reconsiders the rules of the game. Two features of that law matter enormously. The first is the "widely held" rule, which limits how much of a large bank any single shareholder may own, making a hostile takeover of a major Canadian bank effectively impossible. The second is the long-standing political consensus, tested and confirmed as recently as the late 1990s, that Ottawa simply will not allow the biggest banks to combine with one another or be swallowed by foreigners.

The regulatory cornered resource

In the vocabulary of Hamilton Helmer's 7 Powers, the Canadian bank charter is close to a textbook Cornered Resource — control of a coveted asset that competitors simply cannot replicate. New charters for scaled, deposit-taking national banks are, in practice, not handed out. Foreign ownership is capped, which keeps global giants such as JPMorgan, Citigroup, and HSBC boxed out of the domestic retail market no matter how much capital they might be willing to deploy. The upshot is a walled garden, and the incumbents were handed the keys and told to tend it. The result shows up in the numbers that matter to investors: structurally high returns on equity, famously low credit losses through the cycle, and enormous, sticky retail deposit franchises that fund everything else the banks do.

There is an important analytical caveat here, and it is worth stating plainly because it cuts against the bank's own preferred narrative. TD's celebrated conservatism and profitability are not primarily a reward for cleverness or virtue. They are a reward for incumbency inside a structure the Canadian state has chosen to protect. A concentrated oligopoly with fat, protected margins simply has less need to reach for exotic risk than a fragmented, hyper-competitive market where thin margins push everyone toward the edge. That distinction matters enormously later in this story, because it turns out that TD's prudence was strongest exactly where the moat was strongest — at home — and evaporated almost entirely the moment the bank stepped outside the garden walls into the United States, where it enjoyed no such protection and, as we will see, behaved accordingly. Safety that is a byproduct of structural protection is not the same thing as safety that has been genuinely engineered into a culture, and only the second kind survives a change of scenery.

The 1998 turning point

The moment that locked this structure in place — and, in a delicious irony we will return to, the moment that inadvertently created TD's greatest liability — came in 1998. Sensing that global scale was the future, Canada's biggest banks proposed to merge with one another. Royal Bank of Canada announced plans to combine with Bank of Montreal; TD and CIBC announced their own tie-up in response. Two mega-deals were suddenly on the table that would have collapsed the Big Five into a Big Three, and the banks argued, not unreasonably, that they needed the heft to compete against American and European giants abroad.5

Then-Finance Minister Paul Martin killed both. Citing unacceptable concentration of economic power and the erosion of competition for ordinary Canadians, Ottawa rejected the mergers outright. The message reverberated for a generation: the incumbents could keep their protected, profitable market, but they could not use it to consolidate into an even smaller club, and they could not sell themselves to outsiders. The garden was walled — but the gardeners could not merge their plots either.

For TD, the ruling created a strategic deadlock with only one exit. Blocked from buying its neighbors and generating far more capital than a saturated home market could absorb, TD had to deploy its excess capital somewhere. It could not grow bigger in Canada by acquiring a rival. It could dominate its home turf more deeply — and it soon would, in a way that quietly wrote the DNA of its later American adventure — but for genuine expansion it had to look outward. It set its sights south, at the fragmented, hyper-competitive, unprotected U.S. retail market: the exact opposite of everything that had made it safe and rich at home. That decision would define the next quarter-century, and it began, improbably, with a Canadian trust company and a former civil servant who thought banking was needlessly hostile to the people it was supposed to serve.

III. The US Gold Rush: "America's Most Convenient Bank"

Before TD ever planted its green flag in America, it ran a test of the whole convenience philosophy at home — and it did so by buying the company that would give it both a customer-service religion and its next chief executive. On February 1, 2000, TD closed its acquisition of Canada Trust, the country's largest trust company, and immediately announced that the combined retail bank, rechristened TD Canada Trust, would adopt Canada Trust's service model wholesale, including branch hours that, in the bank's own words, "well exceed the industry average."6 Extended hours, a temporary freeze on retail service fees, elimination of certain ATM charges across a combined network of more than 3,000 machines — the playbook that would later conquer the U.S. East Coast was rehearsed first in Canadian strip malls.6

The man who ran Canada Trust, and who became chairman and CEO of the new TD Canada Trust division, was W. Edmund Clark — Ed Clark — and he is impossible to understand without his backstory. Clark held a doctorate in economics from Harvard, but he made his early reputation in Ottawa as a senior civil servant, where he helped design the 1980 National Energy Program, a nationalist intervention in the oil sector so loathed in Alberta that it earned him the nickname "Red Ed" in business circles.7 A Harvard-trained former Liberal mandarin was, on paper, an improbable candidate to run one of Canada's great capitalist institutions. But Clark reinvented himself in the private sector, ran Canada Trust with a retailer's instincts, and arrived at TD with a conviction that was, for a banker, almost heretical: that traditional banking was boring, hostile, and ripe for disruption by anyone willing to treat it like a retail store rather than a marble temple where supplicants came to be judged.

Clark takes the wheel

Clark became chief executive of the whole bank in 2002, inheriting an institution that had just posted its first full-year loss, gutted by soured telecom and technology loans in the dot-com bust.8 Over the next twelve years he engineered one of the great runs in Canadian banking: by his final quarter the bank was earning around C$2.1 billion in a single three-month stretch, running neck-and-neck with Royal Bank of Canada, and TD's stock had climbed roughly 287% during his tenure while its market value multiplied several times over.8 Two decisions defined his leadership, and they reveal a paradox worth sitting with. The first was defensive brilliance: in the mid-2000s Clark and his chief risk officer, Bharat Masrani, looked at the complex structured mortgage products then minting easy money across Wall Street, concluded the returns did not compensate for the risk, and pulled TD out of them before the 2008 crisis vaporized that market.8 It was a genuinely prescient act of risk management. The second decision was the aggressive one that would eventually curdle: Clark took the bank's excess Canadian capital and went shopping in the United States, spending on the order of US$18 billion to build an American retail bank almost from scratch.8 The same executive who could see the hidden risk in a mortgage derivative could not, or did not, see the hidden risk in the compliance systems of the branches he was buying.

The beachhead and the showman

The American build-out came in two moves. The first was disciplined and unglamorous: between 2004 and 2007, TD acquired Banknorth, a solid New England regional bank based in Portland, Maine, for roughly US$6 billion, establishing an operating presence and a seasoned management team along the American Northeast. It was a sensible platform acquisition, the kind that rarely makes headlines. The second move was the one that gave TD its soul in America.

In 2008, TD paid US$8.5 billion for Commerce Bancorp, a New Jersey bank headquartered in Cherry Hill and built in the image of one of the most eccentric figures in American retail finance: Vernon Hill. Hill was less a banker than a showman who had studied fast food. He had, in fact, cut his teeth in McDonald's franchise real estate, and he applied the logic of quick-service restaurants to deposit-gathering with evangelical zeal. He refused to call his locations branches; they were "stores." He kept them open seven days a week, with extended evening hours, when the rest of the industry bolted its doors at 3 p.m. on weekdays. He installed free "Penny Arcade" coin-counting machines in the lobby — a gimmick that pulled families in off the street and turned a jar of loose change into a marketing funnel. He handed out dog biscuits at the drive-thru and lollipops at the counter, and he trained his staff in a culture of relentless, almost theatrical hospitality. All of it served a single financial objective: pull in enormous quantities of cheap retail deposits that cost the bank next to nothing and could be lent out at a healthy spread.

One green brand, coast to coast

TD merged Banknorth and Commerce under a single brand that fused Hill's showmanship with the discipline of a Canadian parent: "America's Most Convenient Bank," rendered in an unmissable shade of green. It worked, spectacularly, as a deposit-gathering machine. TD expanded aggressively down the Eastern Seaboard from Maine to Florida, and over time built a footprint with more branch locations in the United States than it operated in Canada — an astonishing fact for an institution most Americans had never heard of a decade earlier. The strategic logic was elegant: use the theatrical convenience model to harvest sticky, low-cost deposits in a market where TD's Canadian moat did not apply, then fund a growing U.S. lending business off that cheap money.

Here is the mechanism a sophisticated investor should sit with, because it contained the seed of the disaster. The convenience model was extraordinarily good at one thing above all: velocity. It was engineered to make depositing money at TD frictionless, fast, and pleasant — no appointment, no judgment, no waiting, no awkward questions. That is a wonderful quality in a retail bank competing for honest paychecks. It is a catastrophic one in a bank whose back-office controls cannot keep pace, because "frictionless, fast, and no questions asked" is precisely the value proposition a money launderer is shopping for. The very features that made the front office beloved made the back office a target.

And behind the bright green branding and the smiling tellers, that back office was starved. TD's anti-money-laundering systems, IT infrastructure, and transaction-monitoring technology were treated as cost centers to be contained while the deposit engine was told to grow. For years nobody outside looked closely, because the money kept flowing and the earnings kept climbing, and a compliance department is invisible right up until the moment it fails. It would take an ambitious acquisition — one that finally required regulators to lift the hood — to expose what had been quietly rotting underneath. That acquisition, and the man who bet the bank's American future on it, is where the story turns dark.

IV. The Road to the Penalty Box: First Horizon & The AML Disaster

When Bharat Masrani succeeded Ed Clark as chief executive in 2014, he inherited both the crown jewel and a ticking clock that no one yet knew was running. Masrani was a lifelong TD man — he had joined in 1987, run the U.S. business through its formative expansion, and served as the chief risk officer who helped steer the bank away from the 2008 wreckage. If anyone should have understood the risks buried in the American operation, it was he. Instead, Masrani doubled down on scale. His signature move came on February 28, 2022, when TD announced it would acquire Memphis-based First Horizon Corporation for US$13.4 billion in cash, a deal designed to vault TD into the fast-growing U.S. Southeast and cement it as a genuine top-six American bank.9

On paper it was the logical culmination of two decades of southern expansion — the moment TD would graduate from an East Coast deposit-gatherer into a nationally significant American lender. In practice it was the acquisition that turned on the lights and revealed the infestation.

What the regulators found

A bank acquisition of that size requires regulatory blessing, and to grant it the Office of the Comptroller of the Currency (OCC) and the Federal Reserve had to examine the buyer's controls. What they documented inside TD was not a series of isolated lapses but a systemic, multi-year abdication. From roughly 2014 through 2022, TD's automated transaction-monitoring program remained, in the regulators' language, effectively static: the bank added no significant new monitoring scenarios and made no material upgrades to the systems meant to flag suspicious activity, even as its U.S. business and transaction volumes ballooned.3 Compliance budgets were capped while the front office was told to expand. The result was the staggering coverage gap already noted — roughly 92% of transaction volume, some US$18.3 trillion between 2018 and 2024, moving through the bank essentially unmonitored.3

To translate that from regulator-speak: imagine an airport that kept adding flights, terminals, and passengers every year for a decade while freezing the number of security scanners at the level of a small regional airfield, and then quietly waving most travelers through with no screening at all. That is, functionally, what TD did with its money flows. In a system that porous, criminals do not need sophistication. They need only to notice — and they did.

The suitcases and the gift cards

The human face of the failure was a money launderer named Da Ying Sze, who went by "David." Federal prosecutors described how Sze and his network moved more than US$470 million in illicit proceeds — much of it drug money — through TD by the crudest method imaginable: wheeling suitcases and bags of cash into TD stores across New York and New Jersey and depositing them, over and over.1 This was not financial engineering. It was cash in duffel bags, carried through the front door of America's Most Convenient Bank, and it kept working.

It kept working because Sze bought the cooperation of the people at the counter. He bribed TD employees with more than US$57,000 in gift cards to make sure his transactions were processed without triggering the Suspicious Activity Reports — SARs — that federal law requires banks to file when they spot likely money laundering.1 Insiders processed the deposits, suppressed the alarms, and looked away. Across the broader scandal, TD willfully failed to file SARs on thousands of transactions totaling roughly US$1.5 billion, and several TD insiders were later criminally charged and pleaded guilty for their roles in helping laundering networks move money through the bank.31 The gift-card detail is almost absurdly small next to the sums involved — a nine-figure laundering operation greased with the currency of a shopping-mall birthday present — and that grotesque mismatch is exactly what made it such a devastating symbol of how cheaply TD's controls could be bought.

The internal messages

What elevated this from negligence into something prosecutors could call willful was the paper trail, because TD's own staff knew, and said so in writing. The Department of Justice disclosed internal communications that read like a confession. When one branch employee flagged a suspicious deposit and asked, in writing, "how is that not money laundering?", a colleague answered: "oh it 100% is."1 Other employees traded messages joking that they were watching money laundering happen in real time, and telling one another that the activity really needed to be shut down.1

This is the detail that should trouble a governance-minded investor most, and it is worth being precise about why. The problem was not that TD's people failed to recognize the crime. They recognized it instantly, described it accurately, and joked about it — and the institution's controls and culture did nothing. A systems failure is, in a sense, the more comforting diagnosis, because systems can be rebuilt with money and technology. What the messages reveal is a cultural failure: an environment in which frontline staff could correctly identify felonies as they occurred and simply shrug, because nothing in the machinery around them was built to force a response. That is a far deeper defect, and it is the one that a four-year monitorship and a fresh compliance budget cannot be assumed to have cured.

The hammer falls

The consequences arrived in stages, each heavier than the last. First, the deal died. On May 4, 2023, TD and First Horizon mutually agreed to terminate the merger, with TD unable to give any timetable for regulatory approval "due to reasons unrelated to First Horizon" — a euphemism the market decoded instantly. TD paid roughly US$225 million to First Horizon to walk away, and First Horizon's stock collapsed on the news.9 The signal was unmistakable: regulators would not let TD grow by so much as an inch in America until its house was in order. A bank whose entire strategy had been built on acquiring scale had just been told that scale was off the table.

Then, on October 10, 2024, came the full reckoning. In a coordinated resolution with the DOJ, FinCEN, the OCC, and the Federal Reserve, TD agreed to pay US$3.09 billion in total penalties — including a record US$1.3 billion to FinCEN, the largest penalty ever levied against a depository institution in U.S. Treasury history, roughly US$1.8 billion to the DOJ, a US$450 million OCC penalty, and a US$123.5 million Federal Reserve fine.1310 TD pleaded guilty to conspiracy to commit money laundering and to Bank Secrecy Act violations, becoming the largest U.S. bank ever to enter such a plea, and accepted a four-year independent monitorship to oversee its remediation.1 It was also required to relocate to the United States the parts of its AML program responsible for U.S. compliance, so that American regulators could watch the watchmen directly.3

But the fines, brutal as they were, were survivable — TD earns more than US$3 billion in a good quarter. The truly consequential penalty was structural. The OCC imposed an asset cap holding TD's two U.S. banking subsidiaries at their September 30, 2024 total assets of approximately US$434 billion — the first time the regulator had ever used an asset cap in a Bank Secrecy Act consent order, and a tool borrowed straight from the Wells Fargo playbook.10 In a single stroke, TD's American growth engine was frozen in place. The bank could no longer expand its U.S. balance sheet; it could only reshuffle what was already inside it. And the executive who had presided over the strategy that led here would not be the one asked to fix it.

V. The February 2025 Pivot: Schwab Divestment and Raymond Chun's Playbook

Bharat Masrani did the honorable thing, which in banking is also the necessary thing: he took accountability and left, his planned retirement accelerated as the scandal crested. TD moved up its leadership transition, and on February 1, 2025, Raymond Chun stepped into the role of Group President and Chief Executive Officer of a bank in the penalty box.11

Chun was, in terms of strategic instinct, the anti-Masrani choice, and a very deliberate one. A three-decade TD veteran who had joined the bank in 1992, he had built his career not in the American adventure but in the businesses TD does best: he had led Canadian Personal Banking, then the Wealth and Insurance operations, mastering the machinery of the domestic crown jewel from the inside. His entire professional life had been spent within the fortress walls. Where the prior era had chased scale abroad, Chun's mandate was explicitly inward and remedial: fix the compliance culture, satisfy the regulators, wring maximum efficiency from assets TD already owned, and stop the erosion of shareholder value.[^12] Notably, TD did not reach outside for a turnaround specialist or a compliance heavyweight; it promoted the ultimate insider, a man who had spent thirty-three years absorbing the very culture that failed. That is a bet that the domestic culture was sound and only the American periphery was rotten — a comforting story for the board, and one an investor should hold up to scrutiny rather than accept.

The board did at least attach the incentives to the mission. Chun's compensation was restructured to be heavily weighted toward variable pay tied to precisely the priorities the moment demanded — risk remediation, cost discipline, and return on equity — and the bank simultaneously slashed pay for dozens of senior executives and cut the compensation of its outgoing U.S. chief, a governance signal that someone, finally, had connected accountability to money.12

The Schwab decision

Chun's first major act was audacious, and it doubled as a statement of everything that had changed. On February 10, 2025, TD announced it would sell its entire economic stake in The Charles Schwab Corporation.4 This was no ordinary holding. It traced back to TD's own history in U.S. brokerage: TD had built up TD Ameritrade over years, and when Schwab acquired Ameritrade in an all-stock deal that closed in 2020, TD emerged holding a large minority stake in the combined Schwab — a passive position of roughly 10% in one of America's dominant discount brokers, and a lingering thread connecting TD to the U.S. market even as its banking ambitions there unraveled.8

Within days the sale was done. TD offloaded all 184.7 million shares, representing 10.1% economic ownership, at US$79.25 per share, generating proceeds of approximately C$21 billion (US$14.6 billion) and booking a net gain of roughly C$8.6 billion (US$5.8 billion).13 Of that total, Schwab itself repurchased about US$1.5 billion of the shares directly, with the remainder sold into the market through a registered offering.13

Why sell a stake in a thriving business at what looked like an unremarkable price? The rationale, stripped of investor-relations gloss, comes down to control and capital. The Schwab position was capital-heavy under banking rules, volatile in its quarter-to-quarter mark-to-market swings, and — crucially — a passive minority stake in a company TD did not run and could not direct. In a moment when TD needed every ounce of capital flexibility to absorb fines, fund years of compliance remediation, and reassure skittish regulators, tying up billions of dollars of equity it could not control made little strategic sense. Selling converted a passive, volatile, capital-consuming holding into fungible cash, pushing TD's Common Equity Tier 1 (CET1) ratio — the core regulatory measure of a bank's loss-absorbing capital — to a fortress-like level, and removing, management argued, any lingering question of capital constraint.

There was a clever second move embedded in the exit. TD did not sever the relationship entirely; it retained the lucrative Insured Deposit Account (IDA) agreement with Schwab, under which TD holds sweep-account cash from Schwab's clients and earns a spread on it.13 In effect, TD kept the high-margin deposit cash flow — the part of the relationship it liked best — while shedding the equity ownership and its regulatory capital drag. Whether that reads as shrewd financial engineering or as squeezing the last drops from a relationship it was walking away from is a matter of interpretation, but it was unmistakably deliberate, and it tells you that Chun's team thinks about capital efficiency with real precision.

What the cash bought

The proceeds flowed overwhelmingly to shareholders rather than into reinvestment, and that choice tells you a great deal about how management views its own opportunity set. TD launched a large buyback, initially targeting up to 100 million of its own shares — on the order of C$8 billion — and by its September 2025 investor day had already repurchased roughly C$5 billion of stock, with a plan to buy back an additional C$6 billion to C$7 billion in fiscal 2026, subject to regulatory approval.414 On the investor-day stage, Chun was blunt about the reasoning: "TD has a bright future, and we don't believe our current share price reflects the Bank's intrinsic value."14 Management even told investors it was targeting a total payout ratio above 100% of earnings in fiscal 2026 — meaning it planned to return more cash to shareholders than it earned that year, funded by the Schwab windfall.14

Read that capital allocation carefully, because it is the most honest statement of strategy TD has made. When a bank chooses to shrink its own share count on this scale, and to pay out more than it earns, rather than plow the capital into growth, it is telling you — implicitly but clearly — that it does not currently have enough attractive places to deploy that capital. With the U.S. engine frozen by law and the domestic market already saturated, that is simply the truth of TD's position. Buybacks are the rational move for an over-capitalized bank whose best growth avenue has been closed by regulators. They mechanically grow earnings per share by dividing the same profit across fewer shares, and they concentrate each remaining owner's claim on the domestic cash machine. But they are emphatically not the signature of a growth story. They are the signature of a bank returning capital because it cannot productively invest it. A clear-eyed investor should hold both readings at once: this is disciplined capital return and an admission of constrained opportunity, simultaneously.

Can it be believed?

The harder question is management credibility, and here Chun deserves a genuine, if provisional, hearing. Consider his behavior against the standard tests. At the September 2025 investor day, he did something TD's prior leadership had conspicuously avoided in the depths of the crisis: he restored medium-term financial targets, re-anchoring the bank to public commitments after a period of having withdrawn guidance altogether.14 He laid out a plan for fiscal 2026 of roughly 13% adjusted ROE and 6-8% adjusted EPS growth, building toward a fiscal 2029 target of 16% ROE and 7-10% EPS growth, underpinned by a cost program aiming for C$2 billion to C$2.5 billion in run-rate expense reduction and a "mid-50s" efficiency ratio (the share of revenue eaten by operating costs; lower is better).14 He was also, unusually for a bank CEO, willing to name the failure plainly: "in recent years our performance has slipped in ROE, EPS growth, and total shareholder return. That's unacceptable."14

Setting concrete, falsifiable, multi-year targets after a crisis is a credibility-positive act — it hands the market a scorecard to hold management to, which a leader trying to obscure a weak hand would avoid. And Chun's willingness to state the failure without euphemism contrasts favorably with the corporate instinct to blur it. But targets are promises, not results, and TD's recent history is precisely a story of a strategy that looked coherent from the boardroom and rotted in the back office. The 2029 numbers depend on cost cuts that have barely begun, on a U.S. business under a monitor's thumb, and on a domestic economy TD does not control. The honest interim verdict is that Chun has said the right things and made a defensible opening move — the Schwab sale, the buyback, the restored guidance, the incentive realignment all cohere — but the proof lies in execution the market cannot yet observe. The engine that has to deliver those promises is what we turn to next.

VI. The Current Engine: Segment Performance & Materiality

Strip away the drama and TD is, at its core, a four-cylinder engine in which one cylinder does most of the work, one is quietly excellent, one has just found a second gear, and one is running with a governor bolted to it. The most recent quarter — the second quarter of fiscal 2026, reported May 28, 2026 — offers an unusually clean look at the machine, precisely because it no longer carries the distorting one-time Schwab gain that had inflated the prior year's headline numbers into meaninglessness. On an adjusted basis, TD earned C$4.168 billion in the quarter, up 21% year over year, with adjusted diluted earnings per share of C$2.38 and a CET1 ratio of 14.3%.2 The reported figure was lower and the year-over-year comparison optically brutal — the prior-year quarter had booked the multi-billion-dollar Schwab gain — which is exactly why the adjusted view is the honest one here.

The Canadian cash machine

The dominant cylinder is Canadian Personal and Commercial Banking, which typically generates roughly half of the bank's earnings and did so again with a record C$1.925 billion of net income in the quarter, up 15% year over year, on a return on equity of 31.3%.2 Sit with that ROE figure for a moment, because it is the single most important number in understanding TD. A return on equity above 30% is a level most banks on earth can only fantasize about; it is the mathematical fingerprint of the oligopoly. It reflects cheap, sticky deposits funding well-priced mortgages, credit cards, and commercial loans, with low credit losses, inside a market structure that quietly discourages price wars because no member of the club has much incentive to start one.

Notice how the profit was built, because the mechanism matters more than the number. Revenue in the segment grew a comparatively modest 5%, driven by loan and deposit volume growth and margin expansion, yet net income grew 15% — three times as fast.2 That gap is operating leverage at work: because the cost base is largely fixed and credit losses stayed contained, incremental revenue drops disproportionately to the bottom line. Management reported record penetration rates in consumer and small-business credit cards and roughly C$9 billion in closed referrals into the wealth business, a sign that the bank's grip on its primary-banking relationships is deepening rather than fraying.2 When TD's leaders call primacy in Canadian retail banking the "Holy Grail," this ROE and this operating leverage are what they mean, and the evidence supports the boast at home even as it collapses abroad.

The quiet compounder and the reawakened trader

The second cylinder is Wealth Management and Insurance — the very business Chun ran before his ascent, and it shows. In the quarter it delivered a record C$837 million of net income, up 18% year over year, powered by asset growth, strong flows into TD Direct Investing (Canada's leading direct-investing platform for do-it-yourself investors), and scale in home and auto insurance, where TD has built itself into the country's number-one direct insurer.214 This is arguably the segment investors should prize most highly, for a structural reason: it is capital-light. It earns fees on other people's assets and premiums on policies rather than tying up the bank's own balance sheet in loans, which means its returns consume far less regulatory capital per dollar of profit than lending does. In a company under pressure to conserve capital and lift its return on equity, an asset-light fee engine compounding at 18% is a genuinely valuable and under-appreciated asset.

The third cylinder, Wholesale Banking — TD Securities — has been the surprise of the recovery. It posted record earnings of C$612 million in the quarter, up 46% on a reported basis, as the integration of the 2023 acquisition of Cowen, a U.S. investment bank, finally began to pay off with expanded American equity sales, trading, and advisory capabilities.214 Management has framed this as building a genuine full-service North American investment bank rather than a bond-trading afterthought. The turnaround is real and welcome, but it comes with a caveat any investor should keep front of mind: trading and capital-markets earnings are inherently more volatile and market-dependent than the annuity-like income of Canadian retail. A record quarter for TD Securities is good news, but it is not the kind of durable, predictable profit that the domestic P&C franchise throws off year after year, and it should be weighted accordingly.

The frozen asset

The fourth cylinder is U.S. Banking, and it is running with the governor of the asset cap bolted firmly on. The segment is no longer the smoking wreck it appeared at the depths of the scandal: reported net income recovered to C$813 million in the quarter, with adjusted net income of C$960 million, up 8% year over year, as the bank restructured its U.S. balance sheet toward more profitable assets.2 But "recovering" is not "growing," and that distinction is the whole story. Because it must operate under a hard asset ceiling, TD has been actively shrinking its U.S. balance sheet — reducing assets by roughly 10% — not out of weakness but out of arithmetic: when you cannot add assets, the only way to raise returns is to jettison the lowest-yielding ones and redeploy the freed-up room into higher-yielding assets. It is portfolio pruning masquerading as strategy, and it can lift margins for a while, but it cannot manufacture growth.

Layer on the cost of the cleanup. TD spent US$507 million on remediation in fiscal 2025 and expects a similar figure — around US$500 million pre-tax — in fiscal 2026, with the most demanding milestones, including a SAR "lookback" review the OCC mandated to comb back through years of missed reports, not expected to be complete until calendar 2027.142 On its recent results, management described having completed the majority of its required management remediation actions while stressing that significant work and important milestones remained through 2026 and 2027.2 In plain terms: the U.S. business is being run for compliance and efficiency, not expansion, and it will be for years.

The materiality math is worth naming explicitly, because it is the crux of the entire investment case. The domestic engine is so overwhelmingly profitable that it comfortably funds the entire U.S. remediation bill — hundreds of millions of dollars a year — and still delivers record group earnings. That is simultaneously the bull case and a warning. It means TD can survive the penalty box indefinitely; the crisis is a drag, not a threat to solvency. It also means the U.S. business, once envisioned as the bank's growth frontier and the reason for two decades of southern expansion, has been demoted to a low-yielding utility that management is nursing rather than building — until, and only if, the cap is lifted. To judge how durable each of these four cylinders really is, and where TD genuinely has an edge versus where it is merely surviving, we need to war-game the competitive landscape on both sides of the border.

VII. Porter's 5 Forces & Hamilton Helmer's 7 Powers Analysis

Run TD through the standard strategy frameworks and you get a jarring result: it is two companies wearing one logo, sitting at opposite ends of the competitive-advantage spectrum. In Canada, TD possesses some of the most durable market power in global finance. In the United States, it possesses almost none. Most banks live somewhere in the muddled middle. TD is unusual in being simultaneously near the top and near the bottom, and the frameworks make the divide precise.

The Canadian powers

Start with Switching Costs, the first and perhaps most under-appreciated of TD's domestic powers. The average Canadian keeps their primary chequing account, direct deposit, mortgage, and investment relationships with the same bank not for years but for decades. Moving a primary bank is not a click; it means re-pointing payroll direct deposit, re-establishing every pre-authorized bill payment, migrating a mortgage and lines of credit, possibly moving a brokerage account, and trusting that nothing breaks mid-cycle — a chore most people will do almost anything to avoid. The friction is partly administrative and partly psychological: Canadians treat their bank the way they treat a family doctor, a relationship inherited and rarely questioned. This is why domestic customer churn is famously low, and it is the quiet engine behind that 30%-plus retail ROE. Management calls primacy the "Holy Grail" precisely because a primary-chequing relationship is the cheapest, stickiest deposit a bank can hold — money that sits there earning the bank a spread while paying the customer almost nothing — and TD holds an enormous base of them.

Layer on Scale Economies, the second power. Banking is a business of vast fixed costs — technology platforms, compliance departments, branch and ATM networks, cybersecurity, regulatory reporting — that must be spread across a customer base. TD serves well over 14 million Canadian customers and has told investors it is targeting roughly C$1 billion in annual value from artificial intelligence, split between revenue uplift and cost savings, deployed across a base large enough to amortize that spend thinly per head.14 A dollar of platform investment spread across 14 million customers is simply cheaper per customer than the same dollar at a smaller rival. TD leaned into this at its investor day, noting it already has some 13 million digital users across North America and can migrate routine branch transactions — the roughly 30 million simple deposits and bill payments its clients still do in branches each year — onto phones without a further dollar of investment, turning branches from transaction hubs into higher-value advice centers.14 Scale in banking is unglamorous, but it compounds quietly into the lowest cost of doing business.

And undergirding both is the Cornered Resource already described: the charter, the ownership limits, and the OSFI umbrella that together wall the garden and keep global giants out of Canadian retail. These three powers reinforce one another in a self-perpetuating loop — the charter protects the deposit base, the sticky cheap deposits fund the scale, the scale lowers unit costs, and low costs plus high switching frictions protect the returns that fund the next round of investment. This is what a durable moat looks like from the inside, and it is the deepest reason TD's stock proved so resilient even through a felony guilty plea. A challenger or fintech trying to break in has to offer higher deposit rates to attract money it cannot make sticky — the exact inverse of TD's position.

The American exposure

Now cross the border and run Porter's Five Forces on the U.S. business, and every protective wall vanishes. Competitive rivalry is ferocious: TD is a mid-sized regional player fighting JPMorgan Chase, Bank of America, Wells Fargo, and a swarm of aggressive regionals, all clawing for the same deposits with no oligopoly restraining a price war. The threat of new entrants is real and rising, as fintechs and digital-only banks chip directly at the retail deposit relationships TD's convenience model was built to capture. Buyer power is higher than in Canada because American consumers face lower switching frictions and vastly more choice. There is no cornered resource, no ownership wall, no friendly regulator prioritizing incumbent stability. TD is, in the U.S., simply one competitor among many — and an ordinary one at that.

Into that already-difficult environment, the asset cap injects a unique and self-reinforcing handicap. Scale is the currency of competition in U.S. banking — it buys pricing power, technology density, and regional branch density that let a bank serve customers more cheaply and cross-sell more effectively. By freezing TD's U.S. scale, the cap strips away the one lever a growing bank uses to compete, threatening to turn the American operation into a low-yield utility that cannot grow its way to relevance. Worse, capped growth tends to bleed talent and customers in a slow, compounding leak: top commercial bankers whose loan books cannot expand drift to rivals who can pay for growth, taking client relationships with them, and once that erosion starts it feeds on itself. A bank that cannot grow struggles to retain the very people whose job is to grow it.

The synthesis for an investor is stark and clarifying. TD's competitive advantage is almost entirely geographic. Where it enjoys structural power — Canada — it is close to unassailable and mints extraordinary returns that fund everything else. Where it does not — the United States — it is an ordinary, sub-scale competitor currently fighting with one hand tied behind its back by regulators. The entire investment case, bull and bear alike, reduces to how you weigh those two facts against each other, and to whether you believe the frozen half can ever be thawed.

VIII. Investment Case: Bull vs. Bear and Risk Radar

So let us war-game it directly. The bull and bear cases for TD are not vague sentiments; they are competing, testable claims about how the next several years unfold. The discipline is to hold each against the evidence rather than the rhetoric, and to notice which claims rest on things TD controls and which rest on decisions made in a regulator's office.

Why TD wins

The bull case rests on three pillars, and the first is simply arithmetic that has already been demonstrated. The Canadian cash machine is so structurally profitable — that 30%-plus retail ROE, those low through-cycle credit losses, that sticky deposit base — that it comfortably funds every dollar of U.S. compliance cost while still delivering record group earnings, exactly as the fiscal 2026 results show.2 A bank whose core engine is insulated enough to pay for its own mistakes without threatening its own survival has enormous staying power. TD does not need the U.S. business to work in order to remain a very good bank; it needs the U.S. business merely to stop bleeding, which it now largely has.

The second pillar is the buyback cushion. Flush with Schwab proceeds and generating what management estimates at more than C$5 billion of excess CET1 capital annually even after paying dividends, TD is among the most over-capitalized large banks in North America, and it is deploying that surplus to shrink its share count and lift per-share earnings.14 Buying back stock management believes trades below intrinsic value is a legitimate way to compound per-share value when organic growth is constrained. As a mechanism it is real and already in motion, not a promise.

The third pillar is the coiled spring, and it is the most speculative. The bull argues that when the asset cap is eventually lifted — analysts broadly expect no earlier than 2027, and possibly 2028 or 2029 — TD's remediated, right-sized U.S. business could snap back as a levered recovery play, a dormant engine suddenly permitted to run again in the world's most attractive banking market. This is the pillar an optimist leans on hardest, and it is precisely the one that depends least on TD and most on a regulatory decision the bank cannot schedule or guarantee.

Why TD loses

The bear case is equally concrete, and its lead exhibit has a name: Wells Fargo. That bank operated under a Federal Reserve asset cap for roughly seven years — far longer than almost anyone initially expected — as remediation proved slow, bureaucratic, and prone to regulatory goalpost-shifting, with each apparent finish line receding as examiners found new deficiencies. The base rate for these caps is measured in years, not quarters. If the Wells Fargo precedent holds, TD's "coiled spring" could stay compressed for the better part of a decade, and a multi-year freeze on the U.S. business is a multi-year drag on consolidated growth and a multi-year test of shareholder patience.

The second bear pillar is structural U.S. margin compression. Operating under an asset cap forces a bank toward lower-yielding, shorter-duration assets rather than the higher-yielding commercial and consumer loans it would prefer to write, mechanically depressing net interest margin in the capped unit. TD is managing this actively through balance-sheet restructuring, but restructuring is mitigation, not cure; the ceiling itself does not move. The third pillar is the attrition risk already flagged — capped growth quietly erodes the franchise from within as producers and customers migrate to unconstrained rivals, a leak that does not show up dramatically in any single quarter but compounds over years.

The activist's stress test

A skeptical activist or short-seller would press three points harder than management would like, and each is worth taking seriously. First, capital allocation: is a bank returning more than 100% of its earnings and buying back well over C$10 billion of its own stock across two years signaling supreme confidence, or quietly conceding it has run out of productive things to do with its capital? The intellectually honest answer is that it is both, and an investor who hears only the confidence is only half-listening. Second, governance and accountability: a felony guilty plea and the first-ever BSA/AML asset cap represent a control failure of historic magnitude, and while Masrani departed and executive pay was cut, the deeper unresolved question is whether a culture in which staff joked about laundering in real time can be genuinely re-engineered in four years — or merely policed until the monitor packs up and leaves. Promoting the ultimate insider to lead that cultural repair is a bet worth questioning. Third, disclosure discipline: management withdrew guidance during the crisis and only restored it in September 2025, which is defensible, but it means the market is being asked to extend fresh trust to an institution whose previous strategic plan ended in a criminal conviction. Trust, once broken this badly, is an asset that has to be re-earned quarter by quarter.

The risk radar

Three risks warrant specific, mechanism-level attention, because they are the live wires. Monitorship friction: the four-year independent monitor holds broad sway over new products, branches, and marketing, which means TD cannot simply spend or innovate its way to faster U.S. growth even where it wants to — there is a referee on the field with the power to blow the whistle. Asset-cap tightening as a penalty: the OCC retains the ability to ratchet the cap down further if TD misses remediation milestones, so the ceiling can fall as well as rise, and the bank's own disclosures flag significant milestones remaining through 2027 — meaning the single most important variable in the story is only partly in management's hands.2 Execution and cybersecurity risk: rebuilding an entire AML and technology stack against regulatory deadlines, while migrating the vast majority of the bank's data to the cloud and re-engineering core processes, is exactly the kind of large-scale transformation that breeds integration errors and operational outages when rushed.14 Each of these is a concrete business mechanism, not a generic macro worry, and each descends directly from the original controls failure.

The KPIs that actually matter

For an investor tracking this story over time, the noise-to-signal ratio is punishingly high, so it is worth narrowing to the two or three metrics that genuinely move the thesis and ignoring the rest. The first, and by a wide margin the most important, is AML remediation progress and the status of the U.S. asset cap. Every disclosure about monitor milestones, the SAR lookback, and any hint of when the cap might be eased is the single biggest swing factor in the entire investment case; nothing else comes close. The second is Canadian Personal and Commercial Banking net income and ROE — the pulse of the cash machine that funds everything. Any sustained crack in that 30%-plus ROE, whether from a Canadian housing downturn, rising credit losses, or belated competition, would be far more alarming to the long-term case than any U.S. headline, because it would threaten the source of the bank's resilience itself. The third, secondary gauge is the adjusted efficiency ratio, the cleanest single read on whether Chun's C$2-2.5 billion cost-reduction promise is translating from investor-day slideware into real operating leverage on the path to the mid-50s target.14 Watch those three, and the rest is largely commentary.

IX. Playbook & Durable Lessons

Step back from the specifics and TD's saga yields three durable lessons that outlast any single quarter, and each one is a mirror held up to a comfortable assumption that a lot of businesses share.

The first is the illusion of front-office excellence. TD built one of the most genuinely beloved retail-banking experiences in America — the open Sundays, the coin machines, the dog biscuits, the culture of radical hospitality — and it turned out to be worse than useless as a defense, because the bright, convenient front office was bolted onto broken back-office plumbing. The lesson is not that customer experience does not matter; it plainly does, and it built a real deposit franchise. The lesson is that compliance and risk management are not cost centers to be minimized in the service of growth. They are existential business requirements, and a firm that treats them as overhead is effectively running an unhedged short position on its own survival. TD's Ferrari-with-taped-plumbing was admired for years precisely because plumbing is invisible right up until the moment it bursts and floods the house. Any investor evaluating a fast-growing, customer-delighting company should ask, pointedly, what is happening in the unglamorous functions no marketing department ever features.

The second is the oligopoly trap. Success inside a protected, comfortable domestic market can breed exactly the complacency that gets punished savagely in an aggressive, litigious, politically charged foreign one. TD's Canadian moat did not merely fail to travel south; it may have actively disabled the bank's threat-detection instincts. An institution that has never faced genuine competitive or regulatory ferocity at home has no muscle memory for it abroad, and no cultural antibodies against the assumption that things will basically work out because they always have. Prudence that is a byproduct of structural protection is not the same as prudence engineered into the culture — and the American experience proved, at a cost of US$3 billion and a criminal record, that TD had far more of the former than the latter.

The third is capital as a strategic shield. The single reason TD could absorb a US$3 billion fine, a felony conviction, and the collapse of its entire U.S. growth strategy without diluting shareholders or facing anything resembling a liquidity crisis is that it entered the storm with a fortress balance sheet and a large, liquid, non-core asset — the Schwab stake — that it could monetize on demand.13 The durable lesson for any capital allocator is that over-capitalization and hidden liquid optionality look like laziness and inefficiency in good times and like salvation in bad ones. The Schwab holding sat on the balance sheet for years looking like idle, under-optimized capital that an activist might have demanded be returned. When the crisis hit, it was the lifeboat. A bank that had efficiently optimized that "waste" away would have met the same disaster with none of the cushion — and might have had to raise capital at the worst possible moment, diluting shareholders precisely when confidence was lowest.

Together these three lessons describe a company that was saved by its own conservatism from a disaster caused by its own complacency — the same institution exhibiting both traits at once, in different rooms. That paradox leads directly to the ironies that close the story.

X. Epilogue & Surprising Insights

Raymond Chun's strategy, reduced to a single sentence, is an act of deliberate un-doing: turning TD from a sprawling, cross-border retail explorer back into a hyper-focused, capital-efficient, high-return domestic and wealth giant. Sell the passive stakes, freeze and remediate the American adventure, pour the freed capital into buybacks and the core, sharpen the cost base, and let the Canadian cash machine do what it has always done. It is, in essence, a strategic retreat to the fortress — and, given where the bank found itself, a rational one. Whether it also proves to be a value-creating one depends on execution the market cannot yet observe, and on a regulator's timetable no one at TD controls.

The deepest irony is a matter of historical bookkeeping, and it is almost too neat. In 1998, Paul Martin blocked TD from merging with a domestic rival, forcing the bank to grow the only way left to it — southward, into the United States.5 For a quarter-century that forced expansion looked like a gift, building a franchise with more branches in America than at home and a brand millions of Americans genuinely loved. Then, twenty-six years later, that very same U.S. business became the bank's single greatest liability, the direct source of its felony conviction and its regulatory shackles. The government decision that made TD an international bank is the same decision that, through a long chain of unintended consequences, delivered it into the penalty box. Strategy is rarely so cleanly reversible in its meaning: the escape hatch and the trap turned out to be the same door.

The final and most instructive insight for a long-term investor is the one visible in the company's own resilience. Despite a historic money-laundering scandal, a felony guilty plea, a US$3 billion penalty, and a growth engine frozen indefinitely by regulators, TD remained throughout a systemically important, richly profitable, blue-chip institution. That resilience is not a verdict that the scandal did not matter — it did, it cost billions, and it will drag on U.S. returns for years to come. It is a verdict about where the value in this company actually lives. TD's American story is a cautionary tale about the price of complacency and neglected controls. Its Canadian story is a lesson in the almost gravitational durability of structural market power — the near-impossibility of destroying an oligopoly franchise even through spectacular self-inflicted damage. The bank is both stories at once, and any honest assessment of its future has to weigh the fortress against the penalty box without pretending either one is the whole truth. The fortress is why TD survived. The penalty box is why the next several years will be a test of whether it has genuinely changed, or merely paid to make the problem quieter.

References

-

TD Bank Pleads Guilty to Bank Secrecy Act and Money Laundering Conspiracy Violations in $1.8B Resolution — U.S. Department of Justice, 2024-10-10 ↩↩↩↩↩↩↩↩↩

-

TD Bank Group Reports Second Quarter 2026 Results — TD Bank Group Media Room, 2026-05-28 ↩↩↩↩↩↩↩↩↩↩↩↩

-

FinCEN Assesses Record $1.3 Billion Penalty Against TD Bank — Financial Crimes Enforcement Network, 2024-10-10 ↩↩↩↩↩↩↩

-

TD Bank Group Announces Intent to Sell its Equity Investment in Schwab — TD Bank Group Media Room, 2025-02-10 ↩↩↩

-

TD Bank Group Reports Fourth Quarter and Fiscal 2025 Results — TD Bank Group Media Room, 2025-12-04 ↩↩

-

TD Bank Financial Group Responds to Minister of Finance Decision on Acquisition of CT Financial Services Inc. — TD Bank Financial Group, 2000-01-31 ↩↩

-

Ed Clark: An Era Marked by Straight Talk and Results at TD — The Globe and Mail, 2014-09-05 ↩

-

Charles Schwab Announces Completion of Secondary Offering and Share Repurchase from TD Bank — The Charles Schwab Corporation, 2025-02-12 ↩↩↩↩↩

-

TD Bank and First Horizon Mutually Agree to Terminate Merger Agreement — TD Bank Group Media Room, 2023-05-04 ↩↩

-

OCC Assesses $450 Million Penalty Against TD Bank, Imposes Asset Cap and Growth Restrictions — Office of the Comptroller of the Currency, 2024-10-10 ↩↩

-

TD Bank's New CEO Raymond Chun Faces Steep Climb on Remediation — Reuters, 2025-02-03 ↩

-

TD Bank Group Management Proxy Circular Now Available; New Director Nominee Announced — TD Bank Group Media Room, 2025-03-04 ↩

-

TD Bank Group Announces Pricing of Offering of Schwab Stock — TD Bank Group Media Room, 2025-02-11 ↩↩↩↩

-

2025 Investor Day Conference Call Transcript — Raymond Chun, TD Bank Group, 2025-09-29 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube