Synchrony Financial: The Private Label Credit Card Empire That Escaped GE

I. Introduction & Episode Roadmap

Picture this: You walk into a Lowe's to buy a new refrigerator. The cashier asks if you'd like to apply for their credit card—12 months no interest. You swipe at Sam's Club for bulk groceries. Another branded card offer. You're getting LASIK surgery at a clinic, and they mention CareCredit for financing. What you don't realize is that behind all these seemingly different financial products sits one company, quietly powering the purchasing decisions of 70 million Americans.

That company is Synchrony Financial—a $100 billion colossus that most people have never heard of, yet touches their wallets daily. They're the invisible infrastructure of American retail credit, the largest provider of private label credit cards in the United States, and perhaps the most successful corporate spinoff story of the last decade. The central question we're exploring today is deceptively simple yet profoundly important: How did a division of GE Capital—buried deep in the conglomerate's sprawling financial empire—transform into the invisible payments infrastructure powering retail America? It's a story of patient empire-building, perfectly timed corporate maneuvering, and the unglamorous but essential business of helping Americans buy things they can't quite afford today.

In 2024 alone, Synchrony added 20 million new accounts, processed over $182 billion in purchase volume, and generated $3.5 billion in net earnings. Yet most investors couldn't tell you what they actually do. That anonymity is both their greatest weakness and their secret weapon.

What makes Synchrony fascinating isn't just their scale—it's their position at the intersection of three massive trends reshaping finance: the embedded finance revolution, the buy-now-pay-later disruption, and the great unbundling of traditional banking. They're simultaneously a 90-year-old incumbent and a digital disruptor, a boring utility and a growth story, a cyclical credit play and a secular technology bet.

Over the next few hours, we'll trace Synchrony's journey from Depression-era appliance financing to digital payments powerhouse. We'll explore how they built moats through merchant relationships, survived the financial crisis inside GE, orchestrated one of the decade's most successful IPOs, and are now betting their future on becoming the operating system for retail credit. Along the way, we'll uncover lessons about specialization versus diversification, the power of boring businesses, and why sometimes the best investment opportunities hide in plain sight.

II. The GE Capital Origins: Building America's Store Credit Empire

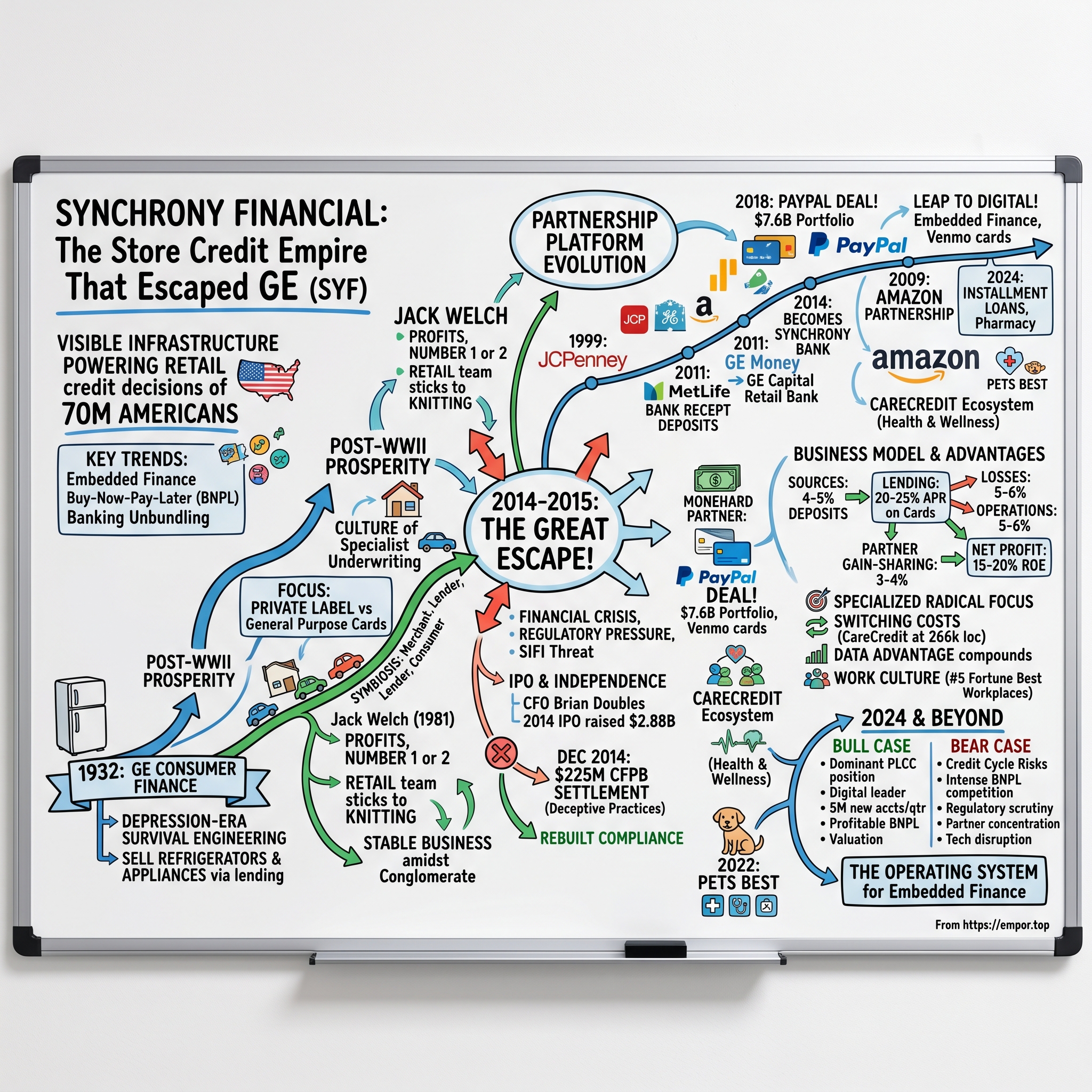

The year was 1932. Franklin Roosevelt hadn't yet taken office. The Dow Jones had fallen 89% from its 1929 peak. A quarter of Americans were unemployed. Banks were failing by the thousands. It was, by any measure, the worst possible time to start a consumer lending business.

Yet that's exactly when General Electric decided to create what would eventually become Synchrony Financial. The logic was simple, almost desperate: GE needed to sell refrigerators and washing machines, but nobody had any money. The solution? Lend them the money yourself.

This wasn't charity—it was survival engineering. GE's manufacturing plants were sitting idle. Retailers couldn't move inventory. Consumers desperately needed appliances but couldn't afford them. The creation of GE's consumer finance arm solved all three problems at once. It was financial innovation born of necessity, the kind that only emerges when traditional systems completely break down.

What started as a way to move refrigerators during the Depression evolved into something far more ambitious over the next 80 years. By the 1950s, as America emerged from World War II into unprecedented prosperity, GE Capital was perfectly positioned to ride the consumer credit boom. They had learned, through trial and error during the hardest economic period in American history, how to underwrite consumer risk when nobody else would.

The post-war suburban explosion created millions of new households that needed everything—appliances, furniture, televisions. GE Capital's private label credit cards became the financial lubricant for this consumption machine. While Bank of America was experimenting with the first general-purpose credit cards, GE was quietly building deeper, more profitable relationships through store-branded cards.

The strategic focus on private label versus general purpose cards was deliberate and prescient. General purpose cards—your Visas and Mastercards—are everywhere, accepted by millions of merchants. But that ubiquity comes at a cost: fierce competition, commoditized relationships, and thin margins. Private label cards are different. They work only at specific retailers, creating a three-way symbiosis between merchant, lender, and consumer that's nearly impossible to disrupt.

By the 1970s, GE Capital had partnerships with hundreds of retailers. But the real transformation came under Jack Welch, who took over GE in 1981. Welch saw GE Capital not as a support function for the industrial business but as a profit engine in its own right. Under his famous decree that every GE business be number one or two in its market, GE Capital went on an acquisition spree, buying everything from commercial real estate portfolios to equipment leasing companies.

The retail finance division—what would become Synchrony—grew alongside this empire but maintained its distinct focus. While other parts of GE Capital chased complex derivatives and leveraged buyouts, the retail team stuck to their knitting: partner with retailers, underwrite consumer credit, share the economics. It was boring. It was predictable. It was wildly profitable.

By 2000, GE Capital had become one of the world's largest financial institutions, with over 200,000 small and mid-sized business relationships. The retail finance arm alone was partnered with many of America's largest retailers. They had built something remarkable: a consumer lending machine that touched nearly every American household, yet remained largely invisible.

The beauty of their model was its simplicity. Retailers wanted to sell more stuff. Consumers wanted to buy stuff they couldn't immediately afford. GE Capital sat in the middle, taking credit risk in exchange for interest income and fees. They had turned the mundane act of installment purchasing into a sophisticated financial ecosystem.

But this success story was about to hit turbulence. The financial crisis would force a reckoning not just for GE Capital, but for the entire conglomerate model that Jack Welch had built. The retail finance division, despite being one of GE Capital's most stable businesses, would find itself caught in the undertow of a corporate crisis it didn't create.

III. The Digital Revolution & Major Partnerships (1999-2013)

The late 1990s marked a turning point. While the rest of the financial world was intoxicated by dot-com mania, GE Capital's retail finance division made a contrarian bet that would define its next chapter: doubling down on physical retail through digital innovation.

In 1999, they launched their partnership with JCPenney—a move that seemed almost quaint as Amazon was beginning its assault on traditional retail. Yet this partnership revealed sophisticated thinking about the future of commerce. The team recognized that credit wasn't just about lending money; it was about data, customer relationships, and creating switching costs that would survive any retail apocalypse.

The 2000s became a period of aggressive expansion, but not the reckless kind that characterized much of pre-crisis finance. Each new partnership was carefully selected, each integration meticulously planned. Belk, Phillips 66, Sleep Train, American Signature—these weren't random acquisitions but strategic positions in specific retail verticals where credit could drive meaningful incremental sales.

The real coup came in 2011 with the acquisition of MetLife Bank's retail deposits. This wasn't just about buying assets; it was about acquiring the regulatory infrastructure to operate as a standalone bank. The foresight here was remarkable. While still operating within GE Capital, the retail finance leadership was already preparing for independence, building capabilities they wouldn't fully need for another three years.

That same year, they rebranded from GE Money Bank to GE Capital Retail Bank. The name change seems cosmetic, but it signaled something deeper: a shift from being seen as GE's lending arm to becoming a legitimate retail banking platform. They were building dual capabilities—the front-end partnerships with retailers and the back-end deposit gathering from consumers.

By 2013, the transformation was nearly complete. The division had been incorporated in Delaware back in 2003 but had remained dormant—a legal entity waiting for its moment. That moment was about to arrive, driven not by strategic planning but by regulatory pressure that would force GE to fundamentally restructure its financial empire.

The partnerships secured during this period weren't just about growth; they were about building a moat. Each retailer integrated Synchrony's technology into their point-of-sale systems. Each customer database became intertwined with Synchrony's underwriting models. Each successful partnership made the next one easier to win. Network effects in financial services are rare, but Synchrony was systematically constructing them.

Meanwhile, the company was quietly building something even more valuable: a massive database of consumer purchasing behavior across multiple retail categories. While Google knew what you searched for and Facebook knew who your friends were, Synchrony knew what you actually bought, when you bought it, and how you paid for it. This data advantage would become crucial as retail continued its digital transformation.

IV. The Great Escape: IPO and Separation from GE (2014-2015)

April 10, 2014. In a conference room at GE's Fairfield headquarters, CEO Jeff Immelt made an announcement that would have been unthinkable under Jack Welch: GE Capital had to shrink. The financial crisis had transformed GE Capital from crown jewel to existential threat. Regulators were circling. The designation as a "systemically important financial institution" (SIFI) loomed, threatening to subject the entire conglomerate to bank-like regulation.

For the retail finance division, this corporate crisis presented an unexpected opportunity. While other GE Capital units were being sold to the highest bidder or simply shut down, retail finance had a different path: independence through public markets.

The IPO prospectus, filed in the summer of 2014, told a compelling story. Here was a business with 80 years of operating history, relationships with many of America's largest retailers, and a proven model that had survived multiple economic cycles. The numbers were staggering: $56 billion in loan receivables, 62 million active accounts, partnerships spanning from Amazon to Walmart.

Brian Doubles, the CFO who would orchestrate both the IPO and eventual separation, faced a unique challenge. How do you value a business that had never truly stood alone? GE Capital had provided funding, back-office support, and the corporate umbrella that made large partnerships possible. Synchrony would need to replicate all of this while simultaneously convincing public market investors they could thrive independently.

The IPO in July 2014 raised $2.88 billion, valuing the company at roughly $18 billion. The market's reception was cautiously optimistic. Here was a pure-play consumer finance company launching at a time when memories of the financial crisis remained fresh. The pitch was essentially: "We're the boring part of GE Capital, the part that actually worked."

But independence came with a price. In June 2014, just weeks before the IPO, GE Capital Retail Bank officially became Synchrony Bank. The rebrand was total—new name, new logo, new identity. Overnight, millions of cardholders discovered their GE-branded cards were now Synchrony cards. The brand recognition that had taken decades to build was voluntarily abandoned.

Then came the regulatory reckoning. In December 2014, the Consumer Financial Protection Bureau (CFPB) announced a $225 million settlement with Synchrony for deceptive and discriminatory practices that had occurred while operating as GE Capital Bank. The timing was brutal—a newly public company immediately dealing with regulatory sanction for the sins of its past life.

The settlement covered credit card add-on products that had been marketed deceptively, with particular harm to Spanish-speaking customers. It was exactly the kind of scandal that reinforced every negative stereotype about consumer lenders. Yet Synchrony's response was telling: they didn't fight it, didn't minimize it, but immediately set about rebuilding their compliance infrastructure from scratch.

The full separation from GE came in November 2015, when GE distributed its remaining stake to shareholders. Synchrony was now truly alone, without the GE safety net but also without its bureaucracy and complexity. The company that emerged was leaner, more focused, and surprisingly ambitious.

Looking back, the timing of the escape was perfect. Synchrony got out just before GE's complete dismantling of GE Capital, avoided the worst of the SIFI regulation, and entered public markets during a period of economic expansion. Sometimes in business, as in life, it's better to be lucky than good. Synchrony was both.

V. The PayPal Deal & Digital Transformation (2018)

The call came in late 2017. PayPal, the digital payments giant, wanted to talk about their credit portfolio. For Synchrony, this wasn't just another partnership opportunity—it was a chance to leap from the physical to the digital world in one transformative deal.

PayPal and Synchrony had actually been partners since 2004, offering co-branded credit cards to PayPal's users. But this was different. PayPal wanted to sell their entire $7.6 billion consumer credit receivables portfolio and make Synchrony the exclusive issuer for PayPal Credit through 2028. The deal would instantly position Synchrony at the center of the digital payments revolution.

The acquisition, completed in July 2018, was strategically brilliant for multiple reasons. First, it gave Synchrony access to PayPal's 237 million active users—digital-native consumers who were comfortable with online credit. Second, it provided entry into pure e-commerce transactions, complementing their traditional retail partnerships. Third, and perhaps most importantly, it positioned them for the coming wave of embedded finance.

But Synchrony didn't stop there. They acquired Loop Commerce, a small company with big ambitions in digital gifting. Loop's GiftNow platform allowed consumers to send digital gifts that recipients could exchange before shipping—solving the age-old problem of unwanted presents. It seemed like a small addition, but it revealed larger ambitions: Synchrony wanted to be present at every point in the digital commerce journey.

The PayPal partnership also opened doors to Venmo, the peer-to-peer payment app beloved by millennials. Synchrony began offering Venmo-branded credit cards, tapping into a younger demographic that traditional credit card companies struggled to reach. This wasn't your grandfather's GE Capital anymore.

The digital transformation went deeper than new partnerships. Synchrony rebuilt their technology stack, creating APIs that retailers could integrate directly into their e-commerce platforms. They developed sophisticated machine learning models that could approve credit in milliseconds, crucial for reducing checkout friction online. They even created a digital bank that consistently ranked among the highest in customer satisfaction.

The transformation was working. Digital originations grew from less than 30% of new accounts in 2015 to over 50% by 2020. The company that had built its fortune in physical retail stores was successfully pivoting to become a digital-first lender.

Yet this digital success created new challenges. Online transactions had higher fraud rates. Digital consumers were less loyal, more price-sensitive. Competition was fierce, with fintech startups offering instant credit decisions and seamless user experiences. Synchrony had to run faster just to stay in place.

VI. The Amazon Partnership & Platform Evolution (2009-2024)

The Amazon partnership tells you everything about Synchrony's evolution. Starting in 2009, when Amazon was primarily an online bookstore expanding into general merchandise, Synchrony (then still GE Capital) became the issuer for Amazon's private label credit card. It was a bet that this Seattle-based e-commerce company might become something special.

By 2024, that bet had paid off spectacularly. The Amazon partnership had grown into one of Synchrony's crown jewels, encompassing not just credit cards but installment loans, business credit, and even healthcare financing through Amazon's pharmacy services. The 15-year relationship had survived multiple contract renewals, competitive threats, and the complete transformation of retail.

But the Amazon partnership also revealed the precarious nature of Synchrony's business model. In 2022, rumors swirled that Amazon might switch to another issuer. The stock plummeted. When Synchrony ultimately retained the business, expanding it to include installment loans for purchases over $50, the stock soared. A single partnership renewal moved billions in market value.

This volatility drove Synchrony to evolve from a collection of partnerships to a platform strategy. They organized their business into four distinct ecosystems: Health & Wellness, Digital, Diversified & Value, and Lifestyle. Each platform had different economics, risk profiles, and growth trajectories.

CareCredit, their health and wellness platform, became the surprise star. What started as dental financing had expanded to 266,000 locations covering everything from veterinary care to cosmetic surgery. Healthcare financing was counter-cyclical, had lower loss rates, and created deeper customer relationships. When your dog needs surgery, you're not shopping around for the best credit terms.

They acquired Pets Best, a pet insurance company, in 2022, further expanding their health and wellness ecosystem. The logic was compelling: pet owners who financed veterinary procedures were perfect candidates for pet insurance. The data from insurance claims helped underwrite credit risk. The ecosystem reinforced itself.

The platform approach extended beyond vertical specialization. Synchrony built capabilities that could be deployed across all partnerships: buy-now-pay-later options, mobile apps, loyalty programs, data analytics. They became not just a lender but a technology platform that retailers could plug into.

By 2024, the transformation was complete. Synchrony managed over 90 million active accounts across hundreds of partnerships. They had successfully evolved from a monolithic credit card issuer to a diversified financial technology platform. The question was whether this platform was resilient enough to handle the next wave of disruption.

VII. Recent Developments: Walmart Return & BNPL Push (2024)

The text message from Walmart came in early 2024: "We want you back." Five years after losing the Walmart portfolio to Capital One in one of the most high-profile defeats in credit card history, Synchrony was being invited to return—not for credit cards, but for something potentially bigger: buy-now-pay-later.

The Walmart partnership, announced in Q2 2024, represented a stunning reversal of fortune. Working with FinTech OnePay, Synchrony would provide the infrastructure for Walmart's new credit programs, including BNPL options integrated directly into Walmart's checkout process. The retail giant had learned what many others discovered: building credit capabilities in-house was harder than it looked. Synchrony secured high-profile partnerships in Q2 with Walmart, Amazon and PayPal, significantly expanding its buy now, pay later (BNPL) presence. The company will power a new credit card program for Walmart through collaboration with FinTech OnePay, offering both a general-purpose card powered by Mastercard and a private-label card exclusively for Walmart purchases.

The BNPL battleground had suddenly become the most important strategic theater in consumer finance. Unlike traditional credit cards with their 20%+ interest rates and monthly statements, BNPL offered transparent, fixed payment schedules that resonated with younger consumers. Affirm, Klarna, and Afterpay had built billion-dollar valuations on this simple insight. Now the incumbents were fighting back.

Synchrony's approach was different from both the fintech disruptors and their traditional bank competitors. Rather than building a standalone BNPL brand, they white-labeled the technology for their retail partners. At Amazon, they launched "Synchrony Pay Later," letting approved customers split purchases of $50 or more into installment payments. With PayPal, they issued a physical PayPal Credit card, enabling cardholders to use BNPL options for everyday purchases.

The strategy was classic Synchrony: be the infrastructure, not the brand. Let retailers own the customer relationship while Synchrony handled the complex work of underwriting, funding, and servicing. It was less sexy than being the next Klarna, but potentially more profitable and defensible.

Brian Wenzel, Synchrony's CFO, noted the Walmart relationship would be fundamentally different from six years ago when they last held the co-brand, with a different value proposition attracting a different type of customer and underwritten differently for a lower loss position. The hard lessons from losing Walmart the first time had been internalized.

The competitive dynamics in BNPL were fascinating. The fintechs had proven consumer demand but were burning cash and facing rising credit losses as their rapid growth outpaced their risk management capabilities. Traditional banks had the balance sheets and risk expertise but lacked the technology and merchant relationships. Synchrony sat in the sweet spot: established merchant partnerships, proven underwriting capabilities, and surprisingly nimble technology.

By the end of 2024, Synchrony's BNPL push was showing results. They were integrated into checkout flows at thousands of merchants, processing billions in BNPL volume, and—crucially—doing so profitably. The fintechs might have invented BNPL, but Synchrony was demonstrating that the incumbents could play this game too, and perhaps play it better.

VIII. Business Model & Competitive Advantages

After nearly a century in business, Synchrony's model remains deceptively simple: they make money by lending money to people who want to buy things. The magic is in the details—how they source customers, price risk, and share economics with merchants.

The core economics work like this: Synchrony pays roughly 4-5% for deposits (their primary funding source), lends at 20-25% APR on credit cards, loses about 5-6% to credit losses, spends another 5-6% on operations and marketing, shares 3-4% with retail partners, and keeps what's left—typically a 15-20% return on equity. It's a model that would be instantly recognizable to a banker from the 1950s, just with better computers.

But several structural advantages make Synchrony's version of this model particularly powerful. First, private label cards have inherently better economics than general purpose cards. Customers can only use them at one retailer, creating natural spend concentration. The merchant relationship provides free customer acquisition. There's no interchange fee to Visa or Mastercard. The result: margins that are 300-400 basis points higher than traditional credit cards.

Second, Synchrony has achieved remarkable scale efficiencies. They support more than 400,000 small and midsize businesses and health and wellness providers. This isn't 400,000 different technology integrations—it's one platform with 400,000 access points. The marginal cost of adding another merchant approaches zero.

Third, the data advantage compounds over time. Synchrony knows not just that you shop at Lowe's, but what you buy, when you buy it, and how you pay for it. They can predict with remarkable accuracy who will renovate their kitchen next year, who's likely to default, and who should get a credit line increase. This data moat gets deeper with every transaction.

Fourth, switching costs create powerful lock-in effects. Once a retailer integrates Synchrony into their point-of-sale systems, trains their staff, and builds marketing campaigns around the credit offering, switching providers becomes enormously disruptive. CareCredit alone is accepted at 266,000 locations—imagine trying to coordinate that switchover. Fifth, and perhaps most importantly, Synchrony has built a culture that attracts and retains talent in an industry notorious for turnover. For the seventh straight year, Synchrony is proud to be named among the top Best Companies to Work For® list in the U.S. by Fortune magazine and Great Place to Work®, with the 2024 rankings seeing Synchrony move up 15 positions to number 5. In financial services, where talent wars are fierce and culture is often an afterthought, this is a remarkable achievement. Employees say "Synchrony is the BEST place to work. They are fair to the employees, offer great benefits, our leaders are easy to talk to, and truly care for the employees. It's like a family. I love that we have a flexible work arrangement and really LOVE flex Fridays which afford me to spend time with my kids or get personal tasks completed. The level of care and commitment from our ELT is unmatched. I truly am proud to say I work for Synchrony and hope I can retire from this company."

The digital bank itself has become an unsung hero of the business model. While competitors struggle with customer acquisition costs and deposit gathering, Synchrony has built an award-winning digital bank that consistently ranks highest in customer satisfaction. They gather deposits at competitive rates without the overhead of physical branches, funding their lending machine efficiently.

The business model's resilience was tested during COVID-19, and it passed with flying colors. While transaction volumes plummeted, Synchrony's diversified portfolio—spanning essential retail, healthcare, and digital commerce—provided stability. Their ability to quickly pivot to digital origination and servicing kept the business running while competitors scrambled.

What's remarkable is how all these advantages compound. The merchant relationships provide customer acquisition. The data improves underwriting. Better underwriting enables competitive pricing. Competitive pricing wins more partnerships. More partnerships generate more data. It's a virtuous cycle that gets stronger with scale.

IX. Playbook: Business & Investing Lessons

The Synchrony story offers a masterclass in several counterintuitive business principles that challenge conventional Silicon Valley wisdom. While tech entrepreneurs preach "move fast and break things," Synchrony built a fortune by moving deliberately and fixing things. Their playbook deserves careful study.

Lesson 1: The Power of Specialized Focus In an era when every fintech wants to be a "super app," Synchrony chose radical specialization. They don't do mortgages, auto loans, or wealth management. They do one thing—retail point-of-sale credit—and they do it better than anyone else. This focus creates expertise that generalists can't match. When Lowe's needs a credit partner, they don't want a bank that also does investment banking and foreign exchange. They want someone who lives and breathes retail credit.

Lesson 2: Timing Corporate Actions for Maximum Value The Synchrony IPO and separation from GE was a case study in perfect timing. They went public in 2014, after the financial crisis recovery but before the late-cycle concerns. They separated from GE just before the parent company's complete unraveling. They retained the Walmart partnership long enough to build other relationships, then pivoted when they lost it. In corporate finance, timing isn't everything—it's the only thing.

Lesson 3: Building Moats Through Deep Integration Synchrony doesn't just provide credit cards; they embed themselves into their partners' operations. Their technology powers the checkout. Their data informs merchandising decisions. Their marketing drives store traffic. This integration creates switching costs that protect against competition. It's not enough to be a vendor; you need to be infrastructure.

Lesson 4: Managing Credit Risk Through Cycles Consumer lending is inherently cyclical, but Synchrony has survived multiple recessions by maintaining disciplined underwriting. They don't chase growth by loosening standards during good times. They provision conservatively. They share risk with merchants through gain-sharing agreements. They diversify across sectors and geographies. When the cycle turns—and it always turns—they're prepared.

Lesson 5: The Importance of Regulatory Relationships The $225 million CFPB settlement in 2014 could have been catastrophic for a newly public company. Instead, Synchrony used it as a catalyst to build best-in-class compliance. They hired former regulators. They invested in systems. They became a model for responsible lending. In financial services, your relationship with regulators is as important as your relationship with customers.

Lesson 6: Platform Thinking in Financial Services Synchrony evolved from a product company (credit cards) to a platform company (financial solutions). This isn't just semantics. A product company sells things. A platform company creates ecosystems where value is created by participants. When a pet owner uses CareCredit for veterinary care, then gets pet insurance through Pets Best, that's platform thinking in action.

Lesson 7: Why Boring Businesses Can Be Great Investments There's nothing exciting about private label credit cards. No one's writing breathless Medium posts about the future of store credit. Yet Synchrony has generated tremendous shareholder value by executing brilliantly in a boring market. Boring businesses often have less competition, more rational pricing, and longer customer relationships. Sometimes the best opportunities are hiding in plain sight.

Lesson 8: The Value of Corporate DNA Synchrony's 90+ year heritage matters more than you might think. They've seen multiple credit cycles, technological disruptions, and regulatory regimes. This institutional memory creates pattern recognition that startups lack. When BNPL companies claim they're revolutionizing credit, Synchrony knows they're really just offering installment loans—something GE was doing in 1932.

Lesson 9: Culture as Competitive Advantage In financial services, where products are commoditized and regulation limits innovation, culture becomes the differentiator. Synchrony's consistent ranking as a top workplace isn't just nice to have—it's a strategic asset. Happy employees provide better customer service, stay longer (reducing training costs), and innovate more. Culture isn't soft stuff; it's hard economics.

Lesson 10: The Power of Patient Capital Synchrony plays long games. They invested in digital capabilities years before they needed them. They built banking infrastructure before separating from GE. They developed BNPL offerings before the market exploded. Patient capital allows for strategic positioning rather than reactive scrambling. In financial services, the tortoise often beats the hare.

X. Analysis & Bear vs. Bull Case

The Bull Case: Dominant Position with Secular Tailwinds

The optimist's view of Synchrony starts with market position. They're the undisputed leader in private label credit cards, a market with high barriers to entry and rational competition. New entrants face enormous challenges: building merchant relationships takes decades, developing underwriting expertise requires multiple credit cycles, and achieving scale economics demands massive upfront investment. Synchrony has all three.

The BNPL expansion represents a massive opportunity that the market hasn't fully appreciated. While pure-play BNPL companies burn cash acquiring customers, Synchrony can offer BNPL through existing merchant relationships with zero customer acquisition cost. They're using their balance sheet strength and underwriting expertise to win in a market where most competitors are subscale and unprofitable.

Digital transformation is another underappreciated strength. In Q4 2024, Synchrony added 5 million new accounts (20 million for the full year), processed $48 billion in purchase volume (over $182 billion for the full year), grew ending loan receivables 2% to $105 billion, generated net earnings of $774 million ($3.5 billion for the full year), and achieved earnings per share of $1.91 per diluted share ($8.55 for the full year). The company has successfully transformed from a legacy credit card issuer to a digital financial services platform.

The partnership pipeline looks stronger than ever. The renewed Walmart relationship, expanded Amazon partnership, and deepened PayPal integration position Synchrony at the center of American commerce. These aren't just credit card deals—they're embedded finance partnerships that will generate revenue for decades.

Valuation remains compelling despite recent appreciation. Synchrony Financial, with a market capitalization of $26.74 billion, is currently trading near its 52-week high of $71.88 and has demonstrated strong momentum with a 40.78% return over the past year. Yet the company still trades at a discount to book value and generates returns on equity that justify a premium valuation.

The Bear Case: Cyclical Risks and Structural Threats

The pessimist's counter-argument begins with credit cycle timing. We're potentially late in the economic cycle, with consumer debt at record levels and savings rates declining. Synchrony's business model is inherently leveraged to consumer health. When unemployment rises and consumers struggle, credit losses can spike dramatically, destroying years of profits in quarters.

BNPL competition is intensifying from every direction. Affirm, Klarna, and Afterpay have brand recognition with younger consumers. Apple and banks are entering the market with massive balance sheets. Even Synchrony's own partners like Walmart are building in-house capabilities. The BNPL gold rush could become a race to the bottom on pricing and credit standards.

Regulatory scrutiny remains a constant threat. The CFPB has increased focus on credit card fees, BNPL regulation, and fair lending practices. New regulations could cap interest rates, limit fees, or impose costly compliance requirements. In financial services, regulatory change can destroy business models overnight.

Partner concentration risk cannot be ignored. The top partnerships represent an outsized portion of revenue. Losing Amazon or PayPal would be catastrophic. Even successful partnership renewals often come with economic concessions that pressure margins. Synchrony is perpetually negotiating from a position of dependence.

Technology disruption looms larger than many appreciate. Embedded finance means every software company can offer credit. Blockchain could revolutionize payments. Artificial intelligence might commoditize underwriting. Synchrony's technology investments are impressive, but they're still fundamentally a legacy player trying to adapt rather than a native digital company.

The Synthesis: A Nuanced View

The truth, as always, lies somewhere between the extremes. Synchrony is neither invincible nor doomed. They're a well-run company in a challenging industry, with real competitive advantages but also real vulnerabilities.

The credit cycle will turn—it always does. But Synchrony has proven they can navigate downturns. Their underwriting has improved with better data and analytics. Their funding is more stable with a deposit franchise. Their partnerships provide some loss-sharing protection. The next recession will hurt, but it probably won't kill them.

Competition in BNPL and embedded finance is real, but Synchrony's response has been shrewd. Rather than competing head-on with fintechs, they're becoming the infrastructure provider. Let Klarna fight for consumer mindshare while Synchrony powers the actual lending. It's less glamorous but more profitable.

The regulatory environment is challenging but manageable. Synchrony has invested heavily in compliance and maintains good regulatory relationships. They're more likely to benefit from regulation that raises barriers to entry than suffer from targeted enforcement. The cowboys get shot; the professionals survive.

For investors, Synchrony represents a classic "quality at a reasonable price" opportunity. It's not a hypergrowth story that will generate 10x returns. It's a steady compounder that could generate market-beating returns with lower risk than the broader market. In a world of zero-yield bonds and overvalued tech stocks, that's increasingly attractive.

XI. Epilogue & "If We Were CEOs"

Standing at the intersection of finance and commerce in 2024, Synchrony faces choices that will define its next decade. The company that began selling refrigerators on credit during the Depression has evolved into something far more complex: a data company, a technology platform, a risk manager, and a consumer brand all rolled into one. The question isn't whether they'll survive—they've proven remarkably resilient. The question is whether they can thrive in a world where every assumption about financial services is being challenged.

If we were running Synchrony, we'd focus on three strategic imperatives that could transform the company from a successful legacy player into a defining force in embedded finance.

First, we'd make a bold bet on becoming the operating system for embedded finance. Rather than competing with every BNPL startup or neobank, we'd position Synchrony as the infrastructure layer that powers them all. Imagine a world where any software company could offer credit products through Synchrony's APIs, leveraging their balance sheet, underwriting, and compliance infrastructure. This isn't just white-labeling—it's creating an entirely new business model where Synchrony becomes the AWS of consumer credit.

Second, we'd expand internationally, but not in the traditional way. Instead of trying to replicate the U.S. model abroad, we'd export the technology and expertise while partnering with local financial institutions. The emerging markets are leapfrogging traditional banking. Synchrony could power that transformation without taking direct credit risk in unfamiliar markets.

Third, we'd build a consumer brand that matters. Today, most consumers don't know Synchrony exists, even if they have multiple Synchrony-issued cards. This anonymity was once strategic, but it's now a liability. We'd create a unified loyalty program across all partnerships, a single app that manages all Synchrony relationships, and financial tools that make Synchrony indispensable to consumers' daily lives.

The biggest surprise in researching Synchrony is how much innovation happens in seemingly boring businesses. While everyone watches the shiny fintech startups, Synchrony quietly processes billions in transactions, tests new products at massive scale, and generates profits that fund real innovation. They're proof that you don't need to be disruptive to be transformative.

Looking ahead, Synchrony's success will depend on navigating three converging trends: the democratization of financial services through technology, the increasing importance of data in credit decisions, and the blurring lines between commerce and finance. Every retailer wants to be a bank. Every bank wants to be a technology company. Every technology company wants to be everything. In this chaos, Synchrony's focused expertise becomes even more valuable.

The future of Synchrony is really the future of American consumer finance. As shopping habits evolve, payment methods multiply, and credit becomes increasingly embedded in daily life, companies like Synchrony will shape how Americans buy everything from groceries to healthcare. They're building the invisible infrastructure of commerce, one transaction at a time.

What's most remarkable about Synchrony is their consistency. Through multiple CEOs, economic cycles, and technological disruptions, they've maintained a clear focus on helping retailers sell more stuff and helping consumers buy it. That simple mission, executed brilliantly over 90 years, has created enormous value. Sometimes in business, the biggest opportunities come not from inventing the future but from perfecting the present.

The Synchrony story isn't over. In fact, it might just be beginning. As financial services become increasingly embedded, invisible, and intelligent, the companies that win won't necessarily be the ones with the best apps or the biggest marketing budgets. They'll be the ones with the best risk management, the deepest partnerships, and the most patient capital. On all three counts, Synchrony is remarkably well-positioned.

The next time you're offered a store credit card at checkout, remember: you're looking at a $26 billion company that most people have never heard of, processing over $180 billion in annual volume, partnered with many of America's largest retailers, and quietly revolutionizing how Americans pay for everything. That's the Synchrony paradox—omnipresent yet invisible, boring yet essential, old yet innovative.

In the end, Synchrony's greatest achievement might be making the complex simple. In a world of financial engineering and technological disruption, they've built a business on a timeless insight: people want to buy things they can't quite afford today, and merchants want to sell them those things. Everything else is just details.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube