Swarmer, Inc.: The Software-Defined Revolution in Autonomous Warfare

I. Introduction & Episode Roadmap

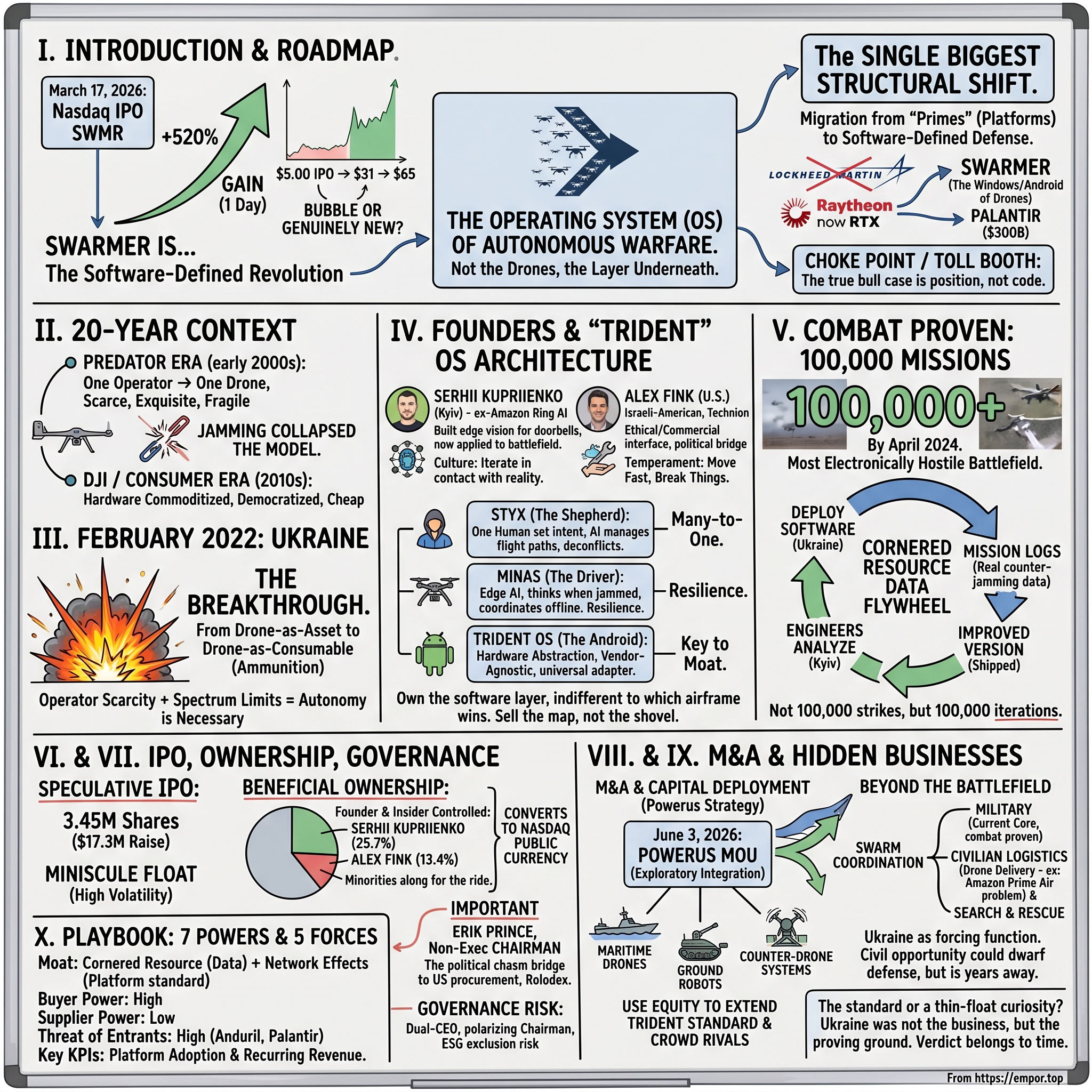

On the morning of March 17, 2026, a small block of stock began trading on the Nasdaq under four letters that almost nobody on Wall Street had heard of three months earlier: SWMR. The company, Swarmer, Inc., had priced its initial public offering the night before at exactly $5.00 a share — a deliberately humble number, the kind of price you attach to a micro-cap that wants to look accessible rather than ambitious. By the closing bell, the stock had finished at roughly $31. That is a 520% gain in a single session, the sort of one-day move that usually belongs to a meme stock or a biotech with surprise trial data, not to a defense-software company whose product had spent the previous two years being shot at over the trenches of eastern Ukraine.[^1]

It got stranger from there. Over the following two days the shares ran as high as $65 before settling into the low fifties, briefly carrying a company that had raised barely $17 million to a market capitalization north of $700 million.[^1] In the parlance of the 2026 defense-tech boom, this was the "March Madness" trade — and Swarmer was its Cinderella. The whole episode raised an obvious and uncomfortable question for serious investors: was this a bubble in a ticker, or the public market's first clumsy attempt to price something genuinely new?

That is the question this episode tries to answer. And to answer it, we have to set aside the share price for a moment and look at what Swarmer actually sells, because the thesis here is unusually clean. Swarmer does not build drones. It builds the software that makes drones fly together. Its pitch — and the reason a sober analyst might take the valuation seriously even while wincing at it — is that it intends to be the operating system of autonomous warfare. Not the airframe. The layer underneath. The Windows, or more precisely the アンドロイド Android, of the drone world: a vendor-agnostic software stack that any one of dozens of hardware makers can license, so that the cheap quadcopter coming off a Ukrainian workshop bench and the expensive fixed-wing built in Ohio can both run the same brain.

That framing matters because it locates Swarmer inside the single biggest structural shift in the defense industry since the end of the Cold War: the migration of value away from the "Primes" — Lockheed Martin, Raytheon (now RTX), Northrop Grumman, the cathedral-builders of the exquisite, billion-dollar platform — and toward what the venture world has christened "software-defined defense." It is the same intellectual lineage that produced Anduril and that turned Palantir Technologies into a $300-billion company on the back of software that, fundamentally, helps soldiers and analysts make decisions faster. Swarmer is making a bet that the next decision to be automated is the most consequential one of all: where a swarm of machines goes, what it looks at, and — the part nobody likes to say out loud — what it strikes.

There is a reason the comparison to a platform company keeps surfacing, and it is worth being precise about it up front, because it is the crux of every argument about this stock. When investors pay a high multiple for a software business, they are not paying for the code; code is cheap and gets cheaper. They are paying for a position — a place in the value chain where, once you arrive, everyone else has to route their value through you. Microsoft did not get rich because Windows was elegant. It got rich because every application developer and every PC maker had to build for Windows, and that mutual dependence calcified into a near-permanent toll booth. The entire bull case for Swarmer is that swarm autonomy has a similar choke point waiting to be occupied, and that a tiny company in Kyiv got there first. The entire bear case is that there is no choke point — only a crowded, fast-moving market where today's combat-proven leader is tomorrow's commoditized vendor. Hold both of those in your head; everything that follows is evidence for one or the other.

Over the next three hours we will trace how a former Amazon manager who built the artificial intelligence behind smart doorbells ended up running a drone-autonomy company out of a war zone; how that company went from a 2023 napkin sketch to 100,000 combat missions; why Blackwater founder Erik Prince ended up as its non-executive chairman; and whether the economics underneath the spectacle can possibly justify the price. Let us start where the technology started — not in Kyiv, but in the slow, twenty-year unlearning of everything the Pentagon thought it knew about drones.

II. The "Drone Revolution" & The 20-Year Context

Picture a windowless trailer on a U.S. Air Force base in Nevada in the mid-2000s. Inside, a pilot in a flight suit sits in front of a bank of monitors, a joystick under his right hand, flying an aircraft that is physically halfway around the world, loitering over the mountains of Afghanistan. The aircraft is a General Atomics MQ-1 Predator. It costs several million dollars. It is connected to its pilot by a satellite link routed through a ground station, and that link is the most precious and most fragile thing in the entire system. This was the first drone revolution, and for fifteen years it defined what the word "drone" meant to a generation of military planners: a remotely piloted, exquisitely expensive, intensely centralized instrument of surveillance and occasional precision strike.

The Predator era had a hidden assumption baked into its DNA — that drones were scarce and pilots were the bottleneck. You built a handful of them, you protected the datalink at all costs, and you flew them against an enemy that had no air force and no meaningful way to jam you. It worked beautifully against insurgents. It was, in retrospect, a luxury of uncontested skies.

The second inflection point came not from a defense contractor but from a consumer-electronics company in Shenzhen. 大疆 DJI, founded by 汪滔 Frank Wang, spent the 2010s doing to aerial hardware what the smartphone did to the camera: it made it cheap, good, and ubiquitous. A teenager could buy a stabilized, GPS-guided flying camera for a few hundred dollars. The strategic significance of this took years to register in Washington, because the Pentagon was conditioned to think of capability as something you procure through a multi-year program of record, not something you order online. But the democratization was real. By the late 2010s the marginal cost of putting a camera — and then a grenade — into the sky had collapsed by three or four orders of magnitude. The expensive part was no longer the airframe. The expensive part was the human watching the screen.8

Then came February 2022, and the third inflection point, which was less an inflection than an earthquake. The full-scale Russian invasion of Ukraine turned an entire country into the largest live laboratory of drone warfare in human history. The early viral footage — a $500 quadcopter dropping a munition into the open hatch of a multimillion-dollar tank — captured the asymmetry that everyone now takes for granted. But the deeper lesson took longer to surface, and it is the lesson on which Swarmer's entire existence rests: the model of "one operator, one drone" does not scale.8

Here is the problem in human terms. A skilled first-person-view drone pilot is a scarce, highly trained individual. Each one can fly exactly one aircraft at a time, and on a contested battlefield that aircraft has a short and violent life expectancy. Worse, the Russians learned to fight back not by shooting drones down but by jamming the radio link between drone and pilot — electronic warfare that severs the connection and turns a $500 weapon into a falling rock. So Ukraine faced a brutal piece of arithmetic: it needed to put thousands of drones over the front every day, it did not have thousands of elite pilots, and the enemy was actively breaking the one link that the entire one-operator-one-drone model depended on. You could not solve that problem by training more people. There were not enough people, and there was not enough radio spectrum.

It is worth dwelling on the economics of that collapse, because it is the foundation of everything. When a capability becomes a hundred times cheaper, it does not just get more affordable — it changes category. A multimillion-dollar Predator is a strategic asset that a commander agonizes over committing; you do not send it somewhere it might not come back. A $500 quadcopter is ammunition. You expend it the way an artillery unit expends shells, without sentiment, because the next one is on a pallet behind the lines. That shift — from drone-as-asset to drone-as-consumable — is what made saturation tactics possible, and saturation is what breaks defenses. A single expensive drone can be tracked and shot down. A swarm of fifty cheap ones overwhelms the defender's ability to respond, because every interceptor missile costs vastly more than the drone it kills. The defender wins every individual engagement and loses the war of arithmetic. That inverted cost curve is the deep reason swarms matter, and it is the reason the value migrates to whoever can coordinate the cheap many rather than perfect the expensive few.

The only way out was to remove the human from the inner loop. If one operator could supervise ten or fifty drones the way a shepherd watches a flock — setting intent rather than steering each animal — and if each drone could keep thinking for itself when the radio link died, then the arithmetic flipped. That is the bottleneck Swarmer set out to dissolve: not building a better drone, but building the autonomy that lets a small number of humans command a large number of machines, and lets those machines carry on when cut off. To understand why two specific people believed they could build that, we have to leave the battlefield and walk into, of all places, an Amazon office.

III. The Founders' Journey: From Ring to Resistance

Before he was building the software that coordinates swarms of attack drones, Serhii Kupriienko Сергій Купрієнко was teaching doorbells to recognize human beings. In the years before the invasion, Kupriienko ran the artificial-intelligence organization at Amazon's Ring division inside Ukraine — at its height, by accounts of the period, a research group of several hundred engineers working on the computer vision that powers smart-home security: the algorithms that decide whether the thing moving on your porch is a delivery driver, a raccoon, or a stranger who should not be there.[^5]

Sit with that for a second, because it is the single most important biographical fact in this entire story. The technical problem of a doorbell — given a noisy video feed, in bad light, from a cheap sensor, detect and classify the objects that matter and ignore the ones that do not, all on a tiny low-power chip with no help from the cloud — is, stripped of its domestic context, almost exactly the technical problem of a drone over a battlefield. The doorbell has to work when the Wi-Fi is flaky. The drone has to work when the radio is jammed. Both need to "think at the edge," on cheap silicon, without a fat pipe back to a data center. Kupriienko spent years building world-class edge computer vision for the most mundane consumer product imaginable, and when the war came he understood, faster than almost anyone, that he already possessed the core competency that the front line was screaming for.9

By his own telling, the decision to pivot was not a careful business plan; it was the response of an engineer who could not sit still while his country was invaded. Amazon's Ukrainian AI work wound down in the chaos of 2022, and Kupriienko found himself with a deep bench of computer-vision talent, a war on his doorstep, and a dawning conviction that the autonomy problem nobody had solved was the one thing that could let Ukraine fight above its weight. The AI visionary's instinct was to attack the hardest version of the problem first: not making one drone smart, but making many drones smart together.

His complement arrived in the form of Alex Fink, the company's U.S.-facing chief executive, and a very different kind of operator. Fink is Israeli-American, an engineer by training, shaped by the Technion — the Israel Institute of Technology, the country's MIT-equivalent and the intellectual engine room of its formidable defense and cyber sector. Before Swarmer, Fink founded and ran Otherweb, a startup with an almost philosophical mission: to fight "information junk," to use AI to filter the manipulative, low-quality noise of the modern internet and surface signal instead. Fink had spent years thinking and writing publicly about the ethics of autonomous information systems — about what it means to build machines that decide what humans see, and where the moral lines should sit.6

That background turns out to be more than a curiosity. A company whose product helps decide what a swarm of armed machines pays attention to is going to spend the rest of its corporate life answering hard questions about autonomy and human control. Having a co-founder who had already wrestled, in public, with the ethics of letting algorithms mediate human perception is a genuine asset — both intellectually and, frankly, in the eventual fights with regulators and procurement officers who will want to know exactly where the human sits in the loop.

There is also a cultural inheritance worth naming, because it shapes how the company builds. The Technion lineage matters not as a credential but as a worldview: the Israeli defense ecosystem is famous for a particular style of engineering — small teams, ruthless prioritization, comfort with dual-use technology, and a refusal to separate the lab from the field. Israel built an entire defense industry on the premise that you test in operations, not in committees, and that doctrine maps almost perfectly onto the Ukrainian wartime reality Kupriienko was living. Two founders from two different small countries that both survive by out-innovating larger, slower adversaries arrived at the same instinct from opposite directions: that speed of iteration is itself a weapon. In an industry where the incumbent culture treats a five-year development timeline as fast, that shared instinct is not a soft factor. It is arguably the company's most underappreciated competitive asset, because culture is the one thing a competitor genuinely cannot acquire.

The pairing — Kupriienko Сергій Купрієнко as the Kyiv-based product and engineering soul, Fink as the U.S.-based commercial and capital-markets face — is the classic two-body structure of a company that needs to live in two worlds at once. One world is the muddy, improvisational, "ship it to the front and see if it survives" reality of wartime Ukraine. The other is the buttoned-down world of American defense procurement and public-equity investors, where credibility is currency and the word "autonomous lethality" makes general counsels reach for the antacids. What the two men shared was a temperament unusual in defense: the Silicon Valley reflex to move fast, break things, and iterate in contact with reality, rather than the cost-plus, decade-long, fail-slowly cadence of the traditional defense industry. They set out to build a defense company that behaved like a software startup — and in May 2023, they did exactly that.

IV. Founding & The "Trident OS" Architecture

Swarmer was incorporated in May 2023, which is to say it was born not in a garage in Palo Alto but in a country under bombardment, where engineers wrote code between air-raid alerts and the customer was, quite literally, a soldier in a trench a few hundred kilometers away.9 That birthplace is not incidental color; it is the company's entire competitive identity. A startup founded in a war zone does not have the luxury of the multi-year development cycle. Feedback arrives within hours, and it arrives in the harshest possible currency: whether the drone came home or not.

The product the company built is best understood as a three-layer stack, and getting these layers straight is essential, because the financial story depends on the architecture. At the foundation sits TRIDENT, an embedded operating system that runs on the drone itself. Think of TRIDENT as the equivalent of アンドロイド Android on a phone: it handles the unglamorous plumbing — networking between drones, encryption, video streaming, and crucially "hardware abstraction," which is the technical term for making the software indifferent to whose airframe it is running on.[^3] This is the keystone of the whole strategy, so it is worth slowing down on.

Hardware abstraction means that Swarmer wrote its software once, against a kind of universal adapter, so that the same code can drive a cheap quadcopter from one Ukrainian workshop, a fixed-wing aircraft from another manufacturer, and — in principle — a ground robot or a maritime drone from a third. The drone makers do not have to rip up their designs. They integrate TRIDENT, and suddenly their dumb airframe inherits a brain. This is precisely the Android playbook. 谷歌 Google never built the definitive smartphone; it built the operating system that hundreds of handset makers adopted, and in doing so it made itself the unavoidable layer between the hardware and the user. Swarmer's wager is that it can occupy the identical position in unmanned systems: license the software to 50-plus different hardware manufacturers rather than betting the company on building the single best drone, and let the brutal, commoditizing economics of drone hardware be someone else's problem.[^3]

Why is vendor-agnosticism the deepest part of the moat? Because hardware in this market is a treadmill. Drone designs are obsolete in months; the Ukrainians iterate airframes faster than most companies iterate slide decks. A company that pins its fortunes to a specific drone is condemned to re-win the hardware race every quarter against thousands of competitors, many of them garage operations. A company that owns the software layer that all of those airframes need is, by contrast, indifferent to which airframe wins. It collects its toll no matter who makes the box. That is the difference between selling shovels and selling the map of the gold field.

On top of TRIDENT sit the two layers that give the company its edge and its menace. The first is STYX, the command-and-control system — the AI that lets a single human operator plan and supervise a mission flown by dozens or, in the company's stated ambition, a hundred-plus drones at once. STYX is the shepherd's crook: the human sets intent at the level of "search this grid" or "strike targets matching this profile in that sector," and the system decomposes that intent into individual flight paths, deconflicts the aircraft so they do not collide, and manages the swarm as a single coherent organism rather than a hundred joysticks.[^14] The second layer is MINAS, the autonomy and collaboration AI that lives at the edge, on the drone. MINAS is the answer to the jamming problem we met earlier: when the radio link to the operator is severed by electronic warfare — the single most common way drones die over Ukraine — MINAS is what lets the drone keep thinking, keep coordinating with its neighbors, and finish or abort its task on its own judgment rather than dropping out of the sky.

If the layered architecture still feels abstract, here is the everyday analogy. Imagine a fleet of delivery vans. TRIDENT is the standardized chassis and dashboard that every van shares, so a driver trained on one can operate any of them — it hides the differences between manufacturers. STYX is the dispatcher sitting in the depot, who does not drive any single van but assigns routes, reshuffles them when traffic shifts, and makes sure two vans are not sent to the same address — one human coordinating the whole fleet at the level of intent. And MINAS is the experienced driver inside each van who, when the radio to dispatch cuts out in a tunnel, keeps making sensible decisions on his own until the signal returns rather than coasting to a confused stop. The genius of the design is that the dispatcher's job does not get harder as you add vans, and no single van going dark brings down the operation. That is what it means to turn a hundred fragile, individually-piloted machines into one resilient organism.

Put the three together and the picture is a deliberate echo of the most successful software architectures in consumer tech: a low-level OS that abstracts the hardware (TRIDENT), an application layer where the operator works (STYX), and an on-device intelligence that works offline (MINAS). It is a strikingly familiar shape to anyone who has studied platform companies — and that familiarity is exactly the point Swarmer's backers want investors to internalize. The question, of course, is whether the platform actually works under fire. By the time the company filed to go public, it had an answer measured not in demos but in missions.

V. Combat Proven: 100,000 Missions in Ukraine

In April 2024, Swarmer's software went to war for the first time.9 There was no press release, no ribbon-cutting, no carefully staged demonstration on a sun-baked test range with a general nodding approvingly from a folding chair. There was a Ukrainian unit, a set of drones running unfamiliar code, and a stretch of contested ground where the only review that mattered was whether the system did something useful before the enemy figured out how to break it. That is the original sin and the original virtue of building a defense product in a war zone: you cannot fake it, and you cannot hide.

Contrast this with how autonomy has traditionally been "proven" in the Western defense world. The classic path runs through a test range in Nevada or a controlled exercise at a place like China Lake — environments where the GPS works, nobody is jamming you, the weather cooperates, and the adversary is a friendly pilot playing a role. Systems that look flawless in that sandbox have a long and embarrassing history of falling apart on contact with a real, adaptive enemy. Swarmer skipped the sandbox entirely. Its proving ground was the most electronically hostile battlefield on the planet, where Russian jamming, GPS spoofing, and constant tactical adaptation form a relentless adversarial gauntlet that no laboratory can simulate.

By the end of May 2026, the company crossed a number that became its central marketing fact and its genuine technical achievement: more than 100,000 real-world combat missions flown with its software, by roughly 50 Ukrainian military units, under active electronic warfare and GPS-denied conditions.1 It is worth pausing on what that figure does and does not mean, because in a market full of vaporware it is the load-bearing claim. One hundred thousand missions is not one hundred thousand successes — combat is attrition, and many of those drones did not come home. What the number represents is one hundred thousand iterations of feedback. Each mission, successful or not, generated data about what the software did, how the enemy responded, where the autonomy held and where it cracked.

This is where the strategy compounds into something a competitor cannot simply buy. Every one of those missions fed a loop: front-line unit flies the software, the software's behavior and the enemy's countermeasures get logged, engineers in Kyiv analyze it, and an improved version ships back to the front, often within days. Over two years, that loop ran tens of thousands of times against an adversary who was himself adapting as fast as he could. The result is a proprietary corpus of real combat-autonomy data — how swarms behave when jammed, which countermeasures the enemy deploys and how to defeat them, what edge cases break the system — that exists nowhere else on earth and that cannot be reconstructed from simulation.

This is the right place for a myth-versus-reality check, because the "100,000 missions" figure does a lot of narrative work and deserves scrutiny rather than applause. The myth, as it travels through headlines and Reddit threads, is that Swarmer has flown 100,000 fully autonomous swarm strikes — that a hundred thousand times, a flock of drones independently went out and prosecuted targets with no human in the loop. The reality is more nuanced and, for an investor, more useful to understand. A "mission" is a deployment of the software in support of a unit's operation; it spans the full range from a single drone using the autonomy stack to navigate through jamming, up to genuine multi-drone coordinated tasks. The degree of autonomy varies, the human remains in or on the loop for engagement decisions, and many missions are reconnaissance and coordination rather than strike. None of this diminishes the achievement — sustained, real-world use at that volume under electronic warfare is genuinely hard and genuinely rare. But an investor who buys the maximalist version of the myth is buying a more finished product than exists, and will be disappointed by the gap between "deployed in 100,000 missions" and "fully autonomous lethal swarms at scale," which remains a frontier the whole industry is still approaching rather than a solved problem on a shelf.

In Hamilton Helmer's vocabulary, which we will return to later, this is a Cornered Resource, and it is the asset the bulls are really paying for. A Western prime with a hundred times Swarmer's engineering budget cannot manufacture two years of front-line jamming data after the fact. It would need its own war, its own 50 units, its own two years. The data moat is a function of time and access, not money, and that is precisely what makes it durable. It is also, candidly, a moat with an expiration risk attached, because it is downstream of a specific, ongoing, and tragic conflict — a tension we will hold onto for the bear case. For now, the company had what no slide deck could fake: a combat record. The next problem was turning a combat record into a public company.

VI. The IPO & The Erik Prince Connection

The bell that rang for SWMR on March 17, 2026 was, by the numbers, a strange one. The offering was tiny: 3,000,000 shares at $5.00, with underwriters exercising a full overallotment of 450,000 more, for a total of 3,450,000 shares and gross proceeds of roughly $17.3 million.[^6] In the world of defense IPOs, where capital raises are measured in hundreds of millions or billions, this was a rounding error — closer in size to a seed round than to the public debut of a company that the market would within hours value at over half a billion dollars.[^1] That mismatch between the trivial amount raised and the enormous valuation conferred is the single most important fact to understand about this listing, and we will come back to what it implies for shareholders.

But the storyline that captured the market's imagination was not the float. It was a name on the board: Erik Prince, the founder of the private military company Blackwater, brought on as Swarmer's non-executive chairman.2 Few figures in the modern security world are as polarizing. To his admirers, Prince is the ultimate operator — a man who built a private army, who knows the inside of the U.S. defense and intelligence procurement apparatus the way a plumber knows pipes, and whose Rolodex is precisely the bridge a Ukrainian software startup needs to cross into American military contracts. To his critics, the Blackwater name is permanently attached to the 2007 Nisour Square killings in Baghdad and to every anxiety the public holds about the privatization of force. Swarmer hired the operator and accepted the baggage as part of the package.

The strategic logic, set aside the controversy, is coherent. Swarmer has a combat-proven product and a Cornered Resource of data, but its commercial center of gravity is in Ukraine, and the prize it ultimately covets is the U.S. defense budget — the largest pool of military procurement on earth, guarded by a labyrinth of relationships, clearances, and political access that a Kyiv-born startup cannot navigate cold. Prince is the human bridge across that chasm. His compensation reflected how the company valued that bridge: rather than cash, Swarmer granted him options to purchase up to 943,350 shares at roughly $6.27 each — an equity-heavy package that ties his payoff directly to the stock he is meant to help propel, and that aligns him with shareholders rather than with a salary line.11

The Prince appointment also slots Swarmer into a broader and more delicate 2026 story: the entanglement of a new generation of defense-tech ventures with politically connected American figures, a thread that runs through firms linked to the Trump family and the wider MAGA-adjacent investment world.2 For investors, this cuts both ways. On the bull side, political connection in defense is not a bug; it is the business — proximity to procurement decisions is worth more than almost any technical edge. On the bear side, a company whose narrative leans this heavily on a single, controversial, politically exposed individual inherits a governance and reputational concentration risk that has nothing to do with whether its software works.

There is a deeper point about why a company with a combat-proven product would choose to raise so little money, and it speaks to the unusual psychology of this listing. Most companies go public to raise capital — the listing is the means, the cash is the end. Swarmer appears to have done something closer to the opposite: it used the listing primarily to mint a public currency and a public profile, with the cash raised almost as an afterthought. Going public converted Swarmer from an obscure Ukrainian startup into a Nasdaq-listed company with a tradable stock, a market price, analyst coverage, and — critically — acquisition currency. For a company whose strategy depends on rolling up hardware endpoints, having liquid, high-multiple stock to spend is worth far more than $17 million of cash. The IPO, read this way, was less a fundraising and more an act of corporate transformation: the moment Swarmer acquired the financial machinery of a platform consolidator. The downside of the choice is the one already visible on the tape — a tiny float in the hands of a speculative market produces a price that swings on sentiment rather than fundamentals, and a stock that can round-trip its gains as fast as it made them.

And then there is the float itself, which is the quiet structural fact underneath the fireworks. By raising only $17 million and floating only about 3.45 million shares, Swarmer kept the publicly tradable supply of stock extraordinarily thin while insiders retained the overwhelming majority. A tiny float meeting a wave of speculative defense-tech demand is a recipe for exactly the kind of violent, 500%-and-up price action the stock delivered — and for the equally violent moves that thin floats can produce in the other direction. That dynamic, more than any DCF, explains the tape. To understand who actually owns this company, and how their incentives are wired, we have to read the ownership table.

VII. Management, Shareholding & Incentives

If you want to know who controls a freshly public company, you do not read the press release; you read the beneficial-ownership filings, and Swarmer's tell a clear story. Serhii Kupriienko, the founder and chief executive, holds a 25.7% stake.4 In a defense company — an industry historically run by professional managers cycling through diversified conglomerates, where no individual owns anything close to a quarter of the enterprise — a founder with that kind of position is an anomaly, and a meaningful one. It means the person setting product direction is also the person with the most to gain or lose from getting it right, and it means that for better or worse the company will reflect a single technical vision rather than a committee's compromise.

Alongside him, Alex Fink holds 13.4%, anchoring the U.S. side of the dual-CEO structure — Kupriienko as global chief executive driving product and engineering from Kyiv, Fink steering the American commercial and capital-markets relationship.4 Dual-CEO arrangements are notoriously fragile; they work only when the two principals have genuinely non-overlapping domains and real mutual trust, and they fail loudly when egos or strategy collide. Swarmer's version has a logical division — one man owns the war zone and the code, the other owns Washington and Wall Street — but investors should watch it as a live governance question rather than assume it away, because the failure mode of a co-CEO blowup at a founder-controlled company is expensive and public.

The combined insider position — well over a third of the company between the two founders alone, before counting other early holders and the board — explains both the stock's behavior and its risk profile. With so little stock in public hands, the founders are not just managers; they are control persons, and minority public shareholders are along for whatever ride the founders choose. That concentration aligns incentives beautifully when the founders are right and offers minimal recourse when they are not.

The compensation architecture is where the real long-term wiring shows, and the 2026 Equity Incentive Plan repays close reading. Two features stand out. The first is the four-year vesting schedule on the restricted stock units that compensate management — the standard Silicon Valley cadence, where equity is earned out over 48 months rather than granted outright, locking key people to the company across the period when execution matters most. The second, and the one investors should scrutinize, is the "evergreen" provision: a mechanism by which the pool of shares reserved for equity compensation automatically replenishes each year, typically as a percentage of shares outstanding, without a fresh shareholder vote.[^11]

A brief but material accounting and disclosure aside belongs here, because a freshly public micro-cap born in a war zone carries diligence flags that a mature defense contractor does not. Investors reading the filings should pay attention to a handful of things that the headline narrative skips over: how much of the company's claimed traction is binding revenue versus deployment-without-payment in a country fighting for its life; the going-concern and liquidity posture of a company operating with roughly $17 million of cash and significant operations inside an active conflict zone; the currency, sanctions, and operational-continuity risks of running the core engineering organization in Ukraine; and the related-party and revenue-recognition questions that naturally arise when a company's largest customer base is a wartime military and its chairman is compensated in deeply-in-the-money options. None of these is a red flag in itself — they are simply the questions a serious analyst asks before extrapolating a $700-million narrative from a $17-million raise, and the auditor's language and the risk-factors section of the S-1 are where the honest answers live.3

Evergreen provisions are common in technology IPOs and rare in traditional defense, and they embody a real trade-off. On one hand, they let a fast-growing company keep attracting and retaining engineering talent with equity, which is exactly how a software-first defense firm has to compete against Anduril and big tech for the same scarce AI researchers. On the other hand, an evergreen is a structurally embedded source of ongoing dilution — every year, the share count creeps up to feed the option pool, quietly transferring value from existing holders to employees and management. It is not nefarious; it is a choice, and it is one of the genuine costs of buying into a company that intends to grow the Silicon Valley way. Layer on the standard six-month post-IPO lockup that prevents insiders from selling immediately, and the picture is of a leadership team bound to the company for the medium term but compensated through a mechanism that will keep the share count rising. With incentives set, the question becomes what management does with its newly minted, high-multiple currency. The first answer arrived within weeks of the listing.

VIII. M&A & Capital Deployment: The Powerus Strategy

On June 3, 2026 — less than three months after the IPO and just days before this episode — Swarmer announced that it had signed a memorandum of understanding with Powerus, the operating identity of Autonomous Power Corporation, to explore integrating Swarmer's swarming and coordination software with Powerus's autonomous-systems architecture across air and maritime domains.510 Read the language carefully, because the company did, and so should investors: it is a memorandum of understanding, explicitly exploratory, committing neither side to any production, procurement, or financial obligation. It is a framework for "good-faith technical exchanges," integration testing, and demonstration planning — a courtship, not a marriage.10

So why does a non-binding handshake matter enough to warrant its own chapter? Because of what it reveals about the strategy. The Powerus MOU is the first public evidence of Swarmer executing the natural endgame of an Android-style platform play: extending TRIDENT beyond the air and into new physical domains — maritime drones, ground systems, critical-infrastructure protection, counter-drone missions, border security.10 Every new domain Powerus's hardware can reach is a new category of "endpoint" running Swarmer's brain. The software company does not have to build a boat or a ground robot; it has to make sure that when someone else builds one, it runs TRIDENT. The MOU is a probe to see whether the abstraction layer that conquered the quadcopter can conquer the sea drone too.

The deal also sits inside a more intricate corporate web that rewards a second look. Powerus is itself tied to merger activity involving Aureus Greenway Holdings, which trades under the ticker PUSA, in a combination that has been working its way through the market in 2026.7 For Swarmer, partnering with a company that is simultaneously consolidating its own assets is a way to attach itself to a hardware platform that is being built up and capitalized in parallel — to benchmark its integration against a counterpart that is itself in motion, rather than a static, legacy supplier. It is the kind of relationship that can evolve from an MOU into something deeper, and it is worth tracking precisely because the structure is fluid.

A word of caution is warranted on the optics of serial dealmaking, because the history of high-multiple companies using their stock to acquire is littered with cautionary tales as well as triumphs. The bull version is Microsoft and Google entrenching standards; the bear version is "diworsification" — the Peter Lynch coinage for companies that squander a great core business by using inflated paper to bolt on unrelated assets that dilute focus and value. The line between the two is whether each acquisition genuinely reinforces the platform's core advantage or merely adds revenue and complexity. For Swarmer, the discipline test is specific: does a given hardware endpoint expand TRIDENT's installed base and lock in the standard, or is it just buying a boat? Investors should hold management to that standard with every deal that follows the Powerus probe, because a company with a richly valued currency and an acquisitive instinct is exactly the kind of company that can destroy value quickly while looking busy and strategic. The MOU structure — exploratory, non-binding, low-cost — is actually reassuring on this front; it suggests a company testing integration before committing capital rather than spraying stock at every hardware maker that will take a meeting.

Step back and the capital-allocation logic comes into focus, and it is the most important strategic pattern to watch from here. Swarmer emerged from its IPO with two assets: a thin balance sheet of roughly $17 million in cash, and a wildly high-multiple stock. A company in that position does not pay for acquisitions with money it does not have; it pays with paper. The playbook — visible in embryo in the Powerus MOU — is to use richly valued equity as an acquisition currency to lock in hardware "endpoints," securing the airframes, hulls, and chassis that guarantee TRIDENT's reach and crowd out rival operating systems before they can establish their own installed base. It is the same move 微软 Microsoft and 谷歌 Google ran in their platform heydays: when your stock is your most valuable asset, you spend it to entrench the standard. Whether Swarmer can convert MOUs into binding integrations — and binding integrations into recurring software revenue — is the execution question on which the entire platform thesis rests. And it points toward a market far larger than the battlefield.

IX. Hidden Businesses: Beyond the Battlefield

Here is a thought experiment that Swarmer's most ambitious backers run, and it starts with a familiar company. Amazon — the same company where Serhii Kupriienko once built doorbell AI — has spent more than a decade and billions of dollars trying to make Prime Air, its autonomous drone-delivery service, actually work at scale. The hard part of drone delivery, it turns out, is not the flying. It is the autonomy: coordinating thousands of aircraft over populated areas, routing them around each other and around obstacles, keeping them flying safely when GPS is spotty or a link drops — managing a swarm. Which is to say, the central unsolved problem of civilian drone logistics is structurally the same problem Swarmer has spent two years solving under the far more punishing conditions of war.9

That is the entire basis of the "hidden business" thesis, and it deserves to be stated plainly rather than oversold. Swarmer's software stack is, at its core, domain-agnostic swarm coordination. Strip away the munitions and the targeting, and what remains — TRIDENT's hardware abstraction, STYX's many-to-one mission management, MINAS's keep-flying-when-jammed edge autonomy — is a general-purpose answer to the question "how do you get a large number of autonomous machines to operate together, reliably, in a contested or unreliable environment?" That question has at least three large answers, and only one of them is military.

The first segment is the current core: military and defense, where the combat record lives and where every dollar of the company's credibility was earned. The second is civilian logistics — the Prime Air-shaped opportunity, plus the broader build-out of drone delivery, port automation, and autonomous freight that the entire logistics industry has been promising for a decade and consistently failing to operationalize. The third is search-and-rescue and industrial monitoring: coordinated swarms inspecting pipelines, power lines, offshore wind farms, and disaster zones, or sweeping a collapsed building for survivors — exactly the sort of dull, dangerous, repetitive work that a self-organizing flock of cheap drones is ideally suited to and that human teams do slowly and at risk.

The genuinely provocative claim — and the one to hold at arm's length — is that the civilian opportunity could eventually dwarf the defense business. The reasoning is simple market sizing: defense budgets, while enormous, are finite and politically constrained, whereas the total addressable market for autonomous logistics and infrastructure services is the global movement of goods and the inspection of the physical world, a multi-trillion-dollar canvas. If swarm autonomy becomes the enabling layer for civilian drone operations the way it has for military ones, the company that owns the standard inherits a market many times the size of the Pentagon's.

There is a useful historical rhyme here for investors who have watched technology migrate from the military to the civilian world before. The internet was DARPA's. GPS was the Air Force's. The integrated circuit was driven to maturity by missile and Apollo programs before it ever reached a pocket calculator. The pattern is consistent: the military pays the brutal up-front cost of making a hard technology work under the most demanding conditions imaginable, and the civilian economy inherits the matured capability and builds the larger business on top of it. If swarm autonomy follows that arc — and there is a respectable argument that it will — then Ukraine is playing the role that the Cold War missile programs played for semiconductors: the unforgiving forcing function that drags an immature technology across the threshold of reliability. The company that owns the autonomy layer at the moment it crosses into civilian use would be positioned the way the early semiconductor firms were positioned in the 1960s. That is the grandest version of the bull case, and it is worth taking seriously even while discounting it heavily for the years and the regulatory battles between here and there.

The honest caveat is that this remains, today, almost entirely optionality rather than revenue. The civilian drone market has been "about to be huge" for over ten years, throttled less by technology than by regulation — aviation authorities are, for excellent reasons, conservative about thousands of autonomous aircraft over populated areas. Swarmer's combat pedigree is a double-edged sword here: it proves the technology works in the hardest environment imaginable, but "battle-tested in Ukraine" is not obviously the credential a civil aviation regulator wants to hear when approving drone delivery over a suburb. The civilian thesis is real, it is large, and it is years away. With the full strategic surface area now in view, it is time to put the company through the analytical wringer.

X. Playbook: 7 Powers & 5 Forces Analysis

Strip away the war footage and the 520% pop, and the question for a long-term investor is mechanical: does Swarmer possess durable, structural advantages, or is it a moment in time dressed up as a franchise? Hamilton Helmer's 7 Powers framework is the right scalpel, and two of the seven powers are doing almost all of the work in this story.

The first, and the one we have already met, is the Cornered Resource: the proprietary corpus of combat-autonomy data accumulated across 100,000-plus missions under live electronic warfare.1 What makes this a genuine power rather than a marketing line is that it cannot be replicated with capital. A competitor with ten times the funding still cannot buy two years of front-line jamming-and-adaptation data, because that data is a product of privileged access to an actual war over an actual period of time. The resource is cornered in the literal sense — Swarmer got there first, through circumstances no rival can re-create on demand. The vulnerability, which we will press in the bear case, is that a cornered resource tied to a specific conflict ages: if the war ends, the data stops refreshing, and a static dataset slowly loses value as warfare evolves.

The second power is the one that could turn a wartime advantage into a peacetime franchise: Network Effects, of the platform variety. The Android analogy is not decoration; it is the thesis. As more drone manufacturers integrate TRIDENT, the platform becomes the default target that mission-software developers, plugin authors, and integrators build against — and as more "mission sets" and capabilities accumulate on the platform, it becomes more valuable to the next manufacturer deciding whose OS to adopt. Hardware makers go where the software ecosystem is; software developers go where the installed base is; and the flywheel, once spinning, is brutally hard for a latecomer to stop. This is the power that would let Swarmer outlast the conflict that birthed it — if it can get the flywheel spinning before a better-capitalized rival builds its own.

Now Porter's Five Forces, which reframes the same company as a position in a competitive field. Start with the Bargaining Power of Suppliers, which for Swarmer is gloriously low. Its "suppliers" are drone-hardware makers, and the entire architecture was designed to commoditize them — TRIDENT's hardware abstraction means no single airframe vendor is irreplaceable, and the global glut of cheap drone manufacturing means Swarmer sits atop a fragmented, price-taking supply base. The software layer captures the value; the hardware layer fights it out on margin. That is the most attractive structural feature of the whole business.

The Threat of New Entrants is where the analysis gets honest, and it is high. The barriers that protect Swarmer — capital, AI talent, defense relationships — are exactly the barriers that the best-funded players in the industry have already cleared. Anduril Industries, with its enormous war chest and its own vertically integrated hardware-plus-software stack, is the obvious predator; Palantir Technologies sits adjacent with its battlefield software and could move toward autonomy; and the major Primes are all scrambling to bolt on drone-autonomy capabilities. Against that field, Swarmer's defense is narrow but sharp: it is the one with the combat record. In defense procurement, "proven in actual war" is a credential that money cannot fast-forward, and it is the single barrier that keeps a $700-million company standing in a ring full of giants.

It is worth war-gaming the Anduril threat specifically, because it is the one that keeps Swarmer's bulls up at night and it sharpens what the company actually has to defend. Anduril's model is the opposite of Swarmer's: it is vertically integrated, building both the hardware (its own drones, its own sensors, its own counter-drone systems) and the software brain (its Lattice operating system) as a single closed stack. The vertical model has real advantages — tight hardware-software integration, control of the full customer experience, and a U.S. pedigree that walks straight into the Pentagon. But it has a structural vulnerability that is precisely Swarmer's opening: a closed, build-everything-ourselves stack cannot be the neutral standard for an industry, because no rival hardware maker wants to adopt a platform owned by a company that also competes with them on hardware. Switzerland gets to be the banker precisely because it does not pick sides. Swarmer's vendor-agnosticism is not just a feature; it is the reason a drone manufacturer might trust TRIDENT in a way it would never trust a platform from a direct competitor. The war-game question, then, is whether the market wants a vertically integrated champion or a neutral standard — and the honest answer is that defense markets have historically supported both, which means the two can coexist longer than a winner-take-all framing suggests, but also that Swarmer must move fast to lock in the neutral position before Anduril's gravity or a Big Tech entrant pulls the ecosystem closed.

The remaining forces are quieter but not silent. Buyer power is real and concentrated — governments are monopsony-ish customers who negotiate hard and can be swayed by politics as much as performance, which is part of why a figure like Erik Prince is on the board in the first place. The threat of substitutes is more philosophical: the "substitute" for swarm autonomy is the old one-operator-one-drone model, and the entire bet is that the substitute is obsolete. Whether that bet holds determines whether any of the powers above matter at all — which brings us to the argument itself.

XI. The Bear vs. Bull Case

Let us steelman the skeptic first, because in a stock that rose 520% on day one the skeptic deserves the floor. The bear case begins with the uncomfortable observation that almost everything attractive about Swarmer is downstream of an active war. The Cornered Resource of combat data, the 100,000 missions, the "battle-tested" brand, the urgency that drove 50 units to adopt unfamiliar software in months — all of it is a function of Ukraine fighting for its survival.1 A negotiated settlement or a frozen conflict, which much of the world is actively hoping for, would be an unambiguous humanitarian good and a genuine problem for this specific investment thesis: the data stops refreshing, the most desperate customer's urgency fades, and a company valued for wartime relevance has to prove it can sell into a peacetime procurement cycle that moves at the pace of committees rather than casualties.

The second pillar of the bear case is the optics and regulation of autonomous lethality. Swarmer's software exists to let fewer humans direct more armed machines, and the natural extension of that — drones that select and engage with diminishing human involvement — runs straight into the global "killer robots" debate, the campaigns to ban lethal autonomous weapons, and the deep public unease about machines making kill decisions. This is not a hypothetical risk; it is a regulatory and reputational overhang that could constrain export markets, complicate the civilian pivot, and make institutional investors with ESG mandates avoid the name entirely. Co-founder Alex Fink's public engagement with the ethics of autonomy is a thoughtful hedge against this, but it does not make the controversy go away.6

Stack on the structural concerns we have already surfaced: a thin float that manufactures volatility in both directions; a barely-there balance sheet of roughly $17 million against ambitions that will require far more capital, implying future raises and dilution on top of the evergreen provision; a valuation north of $700 million attached to a company whose disclosed revenues are modest; a governance profile concentrated in two founders and anchored by a polarizing chairman; and an MOU-stage M&A strategy that has so far produced handshakes rather than binding contracts.[^1][^11]10 None of these is fatal alone. Together they describe a stock priced for a future that is mostly still a promise.

Now the bull case, which is not naive. The optimist's frame is "the Palantir of drones" — and the comparison is instructive precisely because Palantir spent years being dismissed as overvalued, controversial, and revenue-light before the market decided that owning the indispensable software layer of modern conflict was worth a three-hundred-billion-dollar valuation. The bull argues that Swarmer is early in the same arc: a first mover in swarm operating systems, holding a combat credential no competitor can buy, occupying the most defensible position in the value chain (the vendor-agnostic software layer), with two distinct paths to enormous markets — the militarization of autonomy that is already happening, and the eventual, regulation-gated transition of swarm autonomy into civilian logistics.

The strongest version of the bull case rests on the network-effects flywheel doing what platform flywheels do. If TRIDENT becomes the default standard across 50, then 100, then hundreds of drone and autonomous-system makers, the company's value detaches from any single war and attaches instead to its position as the unavoidable layer — collecting a toll on autonomous machines the way Android collects on phones, regardless of who is fighting whom or who makes the hardware. In that world, Ukraine was not the business; Ukraine was the proving ground that let the business reach escape velocity before anyone else. The entire investment question reduces to a single tension: is the war the company's foundation, or merely its first chapter? The bull and the bear are not arguing about the facts. They are arguing about the tense.

For an investor trying to adjudicate that without a crystal ball, the noise can be filtered down to a very small number of things that actually matter to track. The first and most important is platform adoption — the count of drone and autonomous-systems manufacturers that have integrated TRIDENT, and the breadth of domains (air, ground, maritime) they span, because that single metric is the direct readout of whether the network-effects flywheel is spinning or stalled. The second is the conversion of frameworks into revenue — whether MOUs like the Powerus arrangement and the political bridge into U.S. procurement turn into binding, recurring, dollar-denominated software contracts, ideally diversified beyond the Ukrainian theater. Those two KPIs, watched over the coming years, will tell the real story long before the share price settles on a verdict.

XII. Epilogue & Final Reflections

Where does Swarmer stand five years from now? Honestly, the distribution of outcomes is about as wide as it gets in public markets, and the width is the point. In one branch, TRIDENT becomes the genuine standard — the autonomy layer that hundreds of manufacturers build against across air, land, and sea, with the war that birthed it long settled and the platform humming on its own network effects, the civilian logistics business finally clearing its regulatory hurdles and growing into the larger half of the company. In that branch, the 520% first-day pop looks, in hindsight, like the market fumbling toward a truth it could not yet articulate. In the other branch, the conflict winds down, the data moat slowly stales, a better-capitalized rival out-executes the platform play, and Swarmer is remembered as a thin-float curiosity from the defense-tech mania of 2026.

What makes the company genuinely interesting — worth the three hours regardless of which branch wins — is the human improbability at its center. Serhii Kupriienko began this decade teaching a doorbell to tell a delivery driver from an intruder, building edge computer vision for the most domestic product imaginable inside a division of Amazon. He is on track to end it having built, by the company's own count, software that has directed more than 100,000 combat missions and that aims to become the most widely deployed autonomy layer in modern warfare.1[^5] The throughline is not the application; it is the competency. The same hard problem — make a cheap machine perceive and decide for itself, at the edge, when the network fails — turned out to sit underneath both the porch and the battlefield. That is a reminder, useful for any investor, that the most consequential technologies are often the ones that quietly migrate from the mundane to the existential.

It is worth closing on the legacy question with appropriate humility about how early it is. The companies that become essential infrastructure rarely look inevitable at the moment of their listing; they look, more often, like overpriced curiosities riding a thematic wave. Palantir was mocked for years. Amazon was a money-losing bookseller. The judgment that separates a franchise from a fad is almost never available in real time, and anyone who claims certainty about Swarmer's destiny in June 2026 is selling something. What can be said with confidence is narrower and more durable: that the bottleneck Swarmer identified — too few humans to command too many machines — is real, is growing, and will not be un-invented whether or not this particular company is the one to own the solution; and that Swarmer has, against long odds, produced the one credential that the entire industry agrees is hardest to fake. The rest is execution, capital, regulation, and the unknowable trajectory of a war.

Is this the "Standard Oil of the 21st century" — the company that corners an emerging essential and sets the terms for everyone else? The honest answer is that it is far too early, and the metaphor flatters a company that today is a micro-cap with a thin float, a modest cash pile, a single non-binding MOU, and a valuation built mostly on narrative and a genuinely remarkable combat record. What is not too early to say is that Swarmer sits precisely on the fault line of the most important shift in defense in a generation — the migration from hardware Primes to software-defined autonomy — and that it has done something none of its better-funded rivals can claim: it shipped its software to a real war and watched it survive. Whether that becomes a franchise or a footnote is the story the next five years will tell. The market, for its part, has already cast a loud and trembling first vote. The verdict belongs to time.

References

-

Ukraine's 'Swarmer' software completes 100,000th mission — NV.ua, 2026-05-30 ↩↩↩↩

-

Erik Prince Joins Swarmer Board as Chairman — Reuters, 2025-08-14 ↩↩

-

Serhii Kupriienko Beneficial Ownership Report (Schedule 13D) — SEC.gov, 2026-03-27 ↩↩

-

Swarmer and Powerus Sign MOU for Maritime Drone Integration — BusinessWire, 2026-06-04 ↩

-

Alex Fink on the Ethics of Autonomous Information and Defense — Otherweb Blog, 2026-01-10 ↩↩

-

Aureus Greenway Holdings (PUSA) and Powerus Merger Update — Bloomberg, 2026-06-02 ↩

-

The Drone Swarm Revolution: From Nagorno-Karabakh to Kyiv — Financial Times, 2024-02-15 ↩↩

-

This Ukrainian startup has re-invented drone swarming — Defense One, 2025-09 ↩↩↩↩

-

Powerus and Swarmer Sign MOU to Explore Autonomous Swarming Integration — GlobeNewswire, 2026-06-03 ↩↩↩↩

-

Flying High with Erik Prince: Swarmer IPO Brings Combat-Tested Tech To Public Markets — Yahoo Finance / Exec Edge, 2026-03 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube