Smurfit Westrock: The Transatlantic Packaging King

I. Introduction & Episode Roadmap

Picture the scene at the New York Stock Exchange on the morning of February 11, 2026. Tony Smurfit — grandson of the founder, President and Group CEO — stood in front of investors to deliver two things at once: the company's first full-year results as a combined entity, and a five-year plan stretching to 2030.[^4] His opening line was not modest. The company had generated $4.94 billion of adjusted EBITDA in 2025, which he called "by far the largest outturn by any packaging company in the world."[^4] Then came the more revealing admission: it had been achieved in what he described as the most difficult extended economic environment he had seen in his lifetime.[^4]

Both halves of that sentence matter, and they frame the whole investment question. Scale is real: $31.2 billion of sales, a footprint no competitor can replicate, the "largest outturn" boast that is, on the numbers, true.2 But scale is not the same as profitability, and Smurfit Westrock earned a 15.8% adjusted EBITDA margin in 2025 — a figure that would be enviable in most industries but sits conspicuously below the best operators in this one.2

That gap is the core paradox of the humble cardboard box. To the consumer it is a throwaway. To the operator it is a game of intense operating leverage, localized logistics, raw-material hedging, and relentless capital reinvestment, where the difference between a great business and a mediocre one is measured in a few percentage points of mill utilization and a few dollars a ton of freight. The economics reward integration and punish slack, and the spread between the winners and the also-rans is wide enough to build an entire strategy around closing it.

The competitive backdrop sharpens the stakes. While Smurfit and WestRock were combining, their largest global rival, International Paper, closed its own transatlantic deal — the roughly $7.2 billion acquisition of Britain's DS Smith, completed on January 31, 2025.4 The two giants of paper packaging spent 2024 and 2025 each swallowing a large cross-border partner, and now face each other across a consolidating industry in both North America and Europe. How an Irish family business out-consolidated the American paper industry to sit atop this structure — and whether it can defend that position — is the arc of this story.

Three themes run through it. The first is the Smurfit operational playbook, built on mill-to-plant integration: the idea that owning both the paper machine and the box plant that consumes its output is the structural advantage everything else rests on. The second is the margin gap — why a smaller domestic peer, Packaging Corporation of America, earned a 20.7% adjusted EBITDA margin in 2025 while Smurfit Westrock earned 15.8%, and whether Tony Smurfit's plan to close roughly 300 basis points of that spread by 2030 is a credible operating program or an aspiration.56 The third is the slow, secular substitution of paper for plastic — a genuine multi-decade tailwind, though one that management is prone to describe in more certain terms than the evidence yet supports.

Before going further, it is worth puncturing one myth that the headline numbers invite. "Largest packaging company in the world" reads like a verdict, but in this industry size and profitability are only loosely correlated — arguably inversely, over the last decade, given that the most profitable major has been one of the smallest. Smurfit Westrock's scale is a genuine asset, but it is not the same thing as an edge, and the company's own margin sits closer to the middle of the peer pack than the top. The interesting question is therefore not whether Smurfit Westrock is big — it plainly is — but whether it can convert that bulk into the per-ton profitability that the best operators already extract from far less. That is the reality the size masks, and it is the standard against which everything that follows should be measured.

To judge any of it, you have to start where the money started: with a Dublin box business, a protectionist economy, and a family that decided fragmentation was an opportunity rather than a fact of life.

II. The Irish Dynasty: Smurfit's Century-Long Conquest

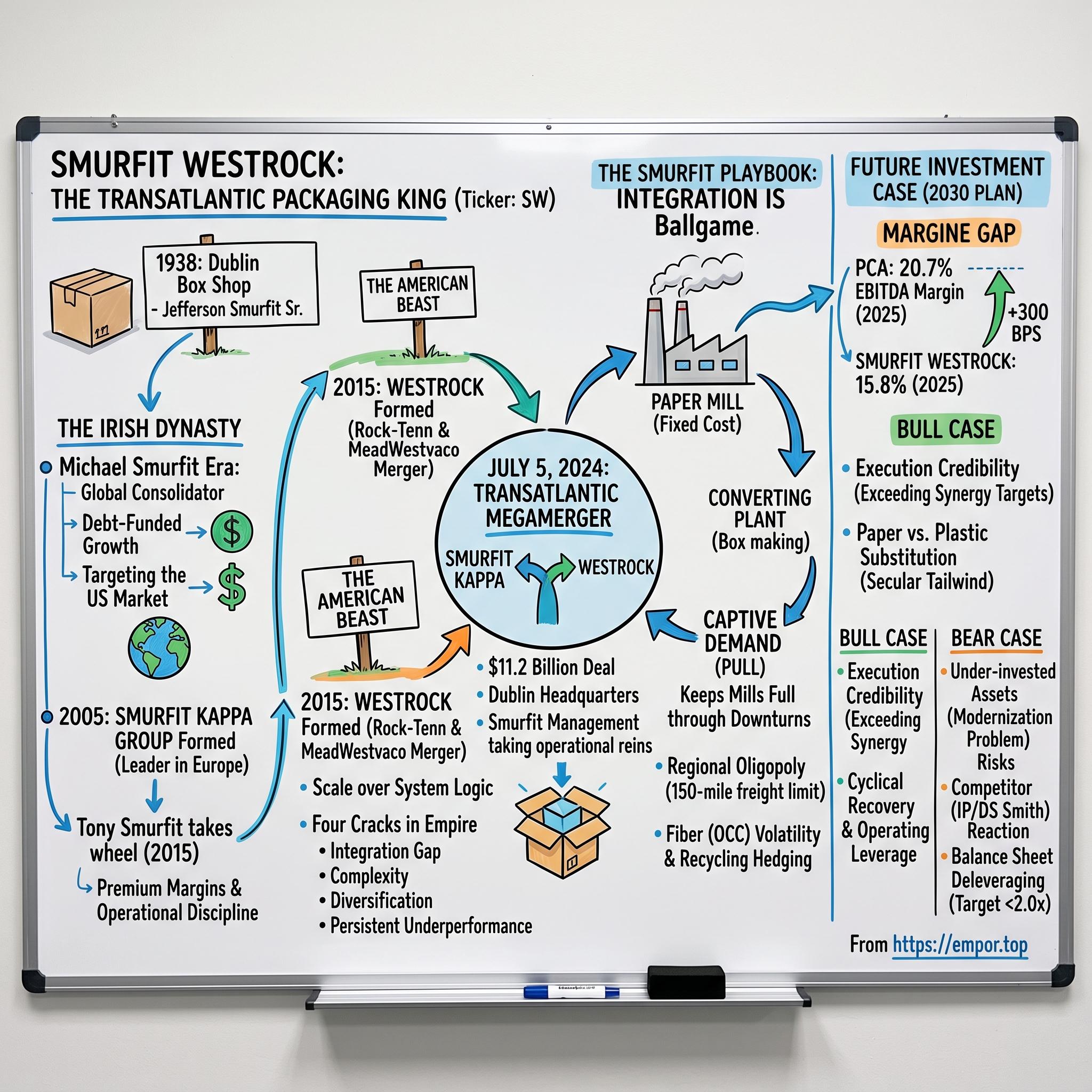

In 1938, Jefferson Smurfit Sr. bought a small, struggling box-making business in the Rathmines district of Dublin — a firm that had been founded a few years earlier, in 1934, and was barely surviving.3 Ireland in the late 1930s was a poor, protectionist, newly independent economy; a box maker's fortunes rose and fell with the local biscuit tin, the local bottle, the local grocer. Survival meant tight customer relationships and ruthless attention to cost, and those instincts — provincial, hands-on, penny-counting — became the cultural DNA that the company would carry, improbably, all the way to a Manhattan stock listing.

The transformation from parish box maker to global consolidator was the work of the founder's son. Michael Smurfit took over on his father's death in 1977 and ran the group until he stepped down as chief executive in October 2002.7 He grasped something about the industry earlier and more completely than most of his contemporaries: paper packaging is inherently fragmented and violently cyclical, and in a fragmented cyclical business, scale is the only durable defense. Small mills get whipsawed by input costs and price swings; large integrated systems can flex, absorb, and consolidate. So Michael Smurfit spent two decades doing deals, most of them debt-funded, most of them aimed at the one market that mattered: the United States.

The American land grab

The pattern began in 1979, when Smurfit took an initial 27% stake in Alton Box Board of Illinois, building to full control by 1981 — a modest Irish company planting its first flag in the American paper belt.8 The ambition escalated in 1986 with the roughly $1.2 billion acquisition of Container Corporation of America, bought from Mobil in partnership with a Morgan Stanley leveraged-equity fund — a genuinely large deal for a company of Smurfit's origins.8 It culminated in 1998, when Jefferson Smurfit Corporation merged with Chicago's Stone Container to create Smurfit-Stone Container Corporation, a combination with an enterprise value of roughly $11 billion that made the Irish family a heavyweight in North American containerboard.9 (That same Smurfit-Stone business would, through a later twist, end up inside WestRock — a detail worth filing away.)

What the acquisition record reveals is a management team comfortable using leverage as a tool and comfortable operating at scale across an ocean, decades before "globalization" became a boardroom cliché. Michael Smurfit ran the group with the swagger of a financier as much as an industrialist, and his central insight was almost embarrassingly simple: in a fragmented industry where hundreds of family box makers each lacked the scale to invest, a well-capitalized consolidator could buy them cheap, plug them into a larger network, and earn a return simply by being bigger and more integrated than the seller. Fragmentation, to him, was not a hazard to be endured but a permanent supply of acquisition targets. That thesis — that consolidation is the business — is the intellectual inheritance Tony Smurfit carried into the WestRock deal three decades later.

It also reveals the recurring risk in the model: debt. A serially acquisitive, debt-funded roll-up is only as safe as the next down-cycle, and by the early 2000s the group's capital structure was ripe for a reset.

Going private, then Kappa, then public again

That reset came in 2002. Chicago's Madison Dearborn Partners led a leveraged buyout of the Jefferson Smurfit Group valued at roughly €3.7 billion — at the time the largest such transaction ever involving an Irish company — taking the business private, stripping out cost, and re-engineering the balance sheet.10 Three years later, in December 2005, the group merged with the Dutch packaging company Kappa Packaging to form Smurfit Kappa Group, creating the clear leader in European containerboard and corrugated packaging.11 In March 2007, Smurfit Kappa returned to public markets with an IPO and listings in London and Dublin, closing the private-equity chapter.11

The strategic logic of the Kappa merger is the through-line of the entire company: build a dense, integrated network in a defined geography — here, continental Europe — where your own box plants consume the great majority of your own mills' paper. That internal demand is what keeps expensive paper machines running near full capacity through a downturn, and it is the single most important idea in this business. We will return to it in depth, because it is exactly the ingredient the company later argued WestRock lacked.

The grandson takes the wheel

On September 1, 2015, Tony Smurfit — Michael's son, Jefferson's grandson — became Group CEO, succeeding Gary McGann.12 The third-generation family member inherited not a struggling Dublin workshop but a pan-European champion, and he leaned into a model built on deep customer integration, design-led selling, capital discipline, and premium margins. Under his leadership Smurfit Kappa earned a reputation as one of the best-run industrials in Europe, compounding adjusted EBITDA at around 6.5% annually in the pre-combination years — more than double the peer average, by the company's own account — while expanding margins and steadily paying down debt.[^4]

The moment that cemented management's credibility, though, was defensive. In March 2018, International Paper — the American colossus — approached Smurfit Kappa with an unsolicited takeover proposal. After an initial rejection, IP came back with a revised bid of €37.54 per share, valuing the group at roughly €8.9 billion.13 Smurfit Kappa's board, with Tony Smurfit as CEO and Ken Bowles as CFO, rejected it flatly, declaring that the proposal "fundamentally undervalues the Group" and its standalone prospects.13 International Paper walked away that June, confirming it would not make an offer, citing the absence of engagement.14

It was, in hindsight, a defining act. A management team that turns down a full-premium cash-and-stock bid is implicitly making a promise: we can compound your capital better than the acquirer would pay you today. That promise is a debt that must eventually be repaid in performance — and it is the reason shareholders were willing, six years later, to back the same team when it proposed to swallow a company twice its size. To understand why that target was available at all, we have to cross the Atlantic and look at the American beast.

III. The American Beast: WestRock and the Great Consolidation

If the Smurfit story is a tightly controlled family saga, the American containerboard story is a demolition derby — decades of mills changing hands, names merging and vanishing, and a handful of survivors emerging from the wreckage. WestRock was one of those survivors, and for a while it looked like a winner.

To appreciate why WestRock ended up as prey rather than predator, it helps to understand the American industry's peculiar pathology. For most of the twentieth century, U.S. paper was a fragmented, capital-heavy, boom-and-bust business in which too many mills chased too little demand, each new capacity addition seeding the next price collapse. The rational response was consolidation, and from the 1990s onward the American majors merged with a vengeance — but they merged, too often, for size rather than for system logic, stitching together mills and plants that did not naturally feed one another. The result was a generation of large companies that were big without being efficient, and WestRock was the apotheosis of that pattern. Its problem was not a lack of scale; it was scale of the wrong shape.

WestRock was created on July 1, 2015, through the merger of Rock-Tenn and MeadWestvaco.15 The lineage on both sides was deep. Rock-Tenn traced its roots to a Southern box operation founded in 1936, though the entity bearing the Rock-Tenn name itself dated to a 1973 combination of Rock City Packaging and Tennessee Paper Mills.16 MeadWestvaco was itself the 2002 union of two nineteenth-century American paper names, Mead and Westvaco.17 Layer the mergers together and WestRock was, in effect, a consolidation of consolidations — a company assembled from the accumulated sediment of a century of American papermaking.

The Voorhees build-out

Under CEO Steven Voorhees, who ran the company from its 2015 formation until 2021, WestRock pursued scale aggressively.18 The Rock-Tenn side had already bought Smurfit-Stone Container — yes, the very business Michael Smurfit built — in 2011 for roughly $3.5 billion in equity value, folding the old Irish-American containerboard network into what would become WestRock.19 In 2018, WestRock acquired KapStone Paper and Packaging for about $4.9 billion including assumed debt, adding containerboard and distribution.20 By the end of the decade WestRock was one of the two largest paper packaging companies in the world by capacity.

And yet size masked a set of structural flaws that would eventually make it a target. Understanding them is essential, because they define the entire value-creation thesis of the merger that followed.

The four cracks in the empire

The first crack was the integration gap. Smurfit Kappa's European system consumed the overwhelming majority of its own mill output internally; the box plants "pulled" the paper, keeping mills full. WestRock's North American system was less tightly knit, leaving a larger share of its containerboard exposed to the open merchant market — where independent box makers buy paper at spot-influenced prices that swing with every twitch in supply and demand. (It is worth being precise here: this integration-gap framing is the consistent narrative advanced by Smurfit management and by industry analysts, and the merger's own logic depends on it; a clean, independent quantification of WestRock's merchant exposure is harder to pin to a single primary source, so treat the magnitude as directional rather than exact.)21

The second crack was complexity. WestRock had accumulated a mismatched network of paper mills of varying vintage and cost position, alongside converting plants that were not always scaled or located to feed off them efficiently. A system assembled through serial M&A is rarely optimized as a system; it is optimized deal by deal, and the seams show up in freight miles and idle capacity.

The third crack was diversification into lower-return adjacencies. WestRock was a major player in consumer packaging — folding cartons, beverage carriers, coated recycled board — a division generating on the order of $5 billion in revenue.21 These are decent businesses, but they diluted the profitability of the core corrugated and containerboard franchise and added managerial surface area.

The fourth crack was the consequence of the other three: persistent underperformance against the best operators. WestRock's margins and returns on capital trailed peers like Packaging Corporation of America, and a company that consistently earns less than its rivals on comparable assets is, by definition, a company whose assets are worth more in someone else's hands. That is the textbook setup for a strategic acquirer — and it is exactly the opening Tony Smurfit had been waiting for.

IV. The Transatlantic Megamerger: Behind the $11 Billion Deal

By 2023 both companies had arrived at the same crossroads from opposite directions. Smurfit Kappa was highly profitable and disciplined but structurally under-exposed to North America — a problem, because its largest customers, the global consumer-goods companies, increasingly wanted a packaging partner who could serve them on both sides of the Atlantic with one system and one design language. WestRock was enormous and North-America-heavy but operationally leaky, carrying more debt and thinner margins than its asset base should produce. Each had what the other lacked. The match was almost algebraic.

The structure of the deal

On September 12, 2023, the two companies announced a definitive agreement to combine.22 The mechanics were built to look and feel like a Smurfit-led transaction dressed as a merger of equals. Each WestRock share would convert into one share of the new Smurfit Westrock plc plus $5.00 in cash; each Smurfit Kappa share would convert into one new share on a one-for-one basis.22 Based on Smurfit Kappa's share price the day before the announcement, the terms implied total consideration of $43.51 per WestRock share, and the deal valued WestRock's equity at roughly $11.2 billion.22 When the dust settled, legacy Smurfit Kappa shareholders held about 50.4% of the combined company and legacy WestRock holders about 49.6% — a hair over half, but enough to make clear who was steering.22

The combination completed on July 5, 2024, with the new shares beginning to trade on the NYSE — the primary listing — and the London Stock Exchange on July 8.1 Crucially, the global headquarters was established in Dublin, and the Smurfit management team took the operational reins.1 A company that had started as a Dublin box shop now had its name first on the marquee of an $11 billion transatlantic giant, with the American partner's name second. For a family business that had spent forty years buying its way into the United States, the symbolism was hard to miss.

Did they overpay?

The bull and bear cases on price are worth stating plainly, because reasonable investors landed on opposite sides. The transaction combined the two companies at broadly similar enterprise-value-to-EBITDA multiples — in the region of seven times consensus EBITDA — so on a like-for-like basis it was not obviously dilutive in valuation terms.22 But WestRock shareholders received a meaningful premium and $5.00 a share in cash, and the bear could reasonably ask why Smurfit paid up for a structurally under-earning asset base that would require years of capital and management effort to fix.

The bull's answer was timing. Mid-2024 was a cyclical trough for packaging: volumes were still depressed by the long post-pandemic destocking, and paper prices were soft. Buying top-tier physical assets — mills that would cost billions to replicate from scratch — near the bottom of the cycle, at a fraction of replacement cost, is a classic value move if you have the operational capability to fix what you bought. The whole thesis, in other words, rested not on the price paid but on management's ability to close the performance gap. That shifts the entire question onto execution, which is where the synergy program comes in.

It is worth being clear-eyed about how the market initially received the deal, because it was not a coronation. The combination was structurally complex — a Dublin-domiciled company adopting a U.S. primary listing, moving out of major European indices in the process, and asking two shareholder bases with different currencies, tax treatments, and index memberships to hold the same new stock. Some legacy Smurfit Kappa holders were skeptical about swapping exposure to a clean, high-margin European compounder for a half-stake in a turnaround of neglected American mills, and the shares spent much of the first year after completion range-bound as investors waited for evidence rather than promises. That skepticism is itself part of the setup: the upside, if it materializes, comes precisely because the market has not yet paid for a fix it has not seen delivered. The burden of proof sits squarely on management — which is exactly where a neutral observer should want it.

The $400 million promise, and what actually happened

Management committed to $400 million of pre-tax run-rate synergies by the end of the first year.23 This is the number by which the deal would be judged early, and the evidence to date suggests it was cleared with room to spare. On the February 2026 results call, Tony Smurfit told investors the company had "well overachieved our initial synergy target of $400 million," and the CFO indicated a further $40 million to $50 million of synergies would still flow through in 2026.[^4] To get there, the company closed roughly 600,000 tons of high-cost, inefficient capacity and reduced headcount by more than 3,000 during 2025 alone; across North America, employment was cut by more than 4,600 people since the combination.23[^4]

The most concrete emblem of the approach was the decision, announced days before the February 2026 call, to shut a specialty bleached board machine at La Tuque, Quebec — one of a series of closures that took paper capacity offline where the company judged it surplus.[^4] Tony Smurfit's framing was characteristically blunt: "you're not going to make an omelet unless you break an egg."[^4] The company took $220 million of mill downtime cost across 2025, deliberately idling machines rather than building unnecessary inventory into weak demand.[^4]

There was a second, less obvious form of pruning that reveals the philosophy more clearly than any mill closure. During 2025 the company deliberately walked away from roughly 1.2 billion square meters of loss-making corrugated volume — contracts it judged to be priced below the cost of serving them — accepting a sharp, headline-ugly drop in North American box volumes in exchange for a cleaner book of business.[^4] North America's regional CEO framed the churn plainly: "we had very underperforming contracts. We needed to stop them at some point and be ready to take on more volume and very good margin conditions over time."[^4] About half of that shed volume was already being replaced with better-priced work, with a further pipeline behind it, and roughly 200 salespeople were freed up to chase profitable business rather than defend unprofitable accounts.[^4] Shedding revenue on purpose is the opposite of what a volume-obsessed operator does, and it is the single most telling behavioral signal in the first year: this management would rather be smaller and more profitable than big and mediocre. Whether the replacement volume actually arrives at the promised margins is the thing to watch — a bet the market cannot yet grade.

For an investor, exceeding a synergy target in year one is a genuine data point in management's favor — it is a promise made and kept, which is not to be taken for granted in large cross-border deals. But it is also the easy part. Synergies from closing high-cost plants and cutting overhead are largely self-help; the harder, multi-year task is lifting the earning power of the mills and box plants that remain. That task is where the economics of the box itself become the whole game.

V. Inside the Core: The Economics of the Cardboard Box

To understand why integration is worth building an entire corporate strategy around, you have to understand what a corrugated box actually is and how it gets made. It is simpler and stranger than most people assume.

Start with the anatomy. A corrugated box is a sandwich: two flat outer sheets of paper, called linerboard, glued to a wavy middle layer, called the medium or fluting. That wavy layer is the whole trick — it is what gives a thin, cheap sheet of paper the stiffness to stack a pallet six feet high and survive a delivery truck. The linerboard and medium are manufactured at paper mills, huge continuous factories where a slurry of fiber and water is pressed and dried into paper on machines the length of a football field. The paper is then shipped as giant rolls to converting plants, where it is glued into corrugated sheet, printed, die-cut, and folded into the boxes a customer actually orders. Mills make the paper; converting plants make the box. That two-step structure is the source of everything that follows.

Why integration is the whole ballgame

A paper mill is a monument to fixed cost. It runs best — often only profitably — when it runs flat out, near 90% or more of capacity, because the machinery, energy, and labor cost roughly the same whether the machine is full or half-empty. So the operator's central obsession is keeping the mill full. There are two ways to do that. You can sell your paper on the open merchant market to independent box makers, taking whatever price the spot market offers on any given day. Or you can own the box plants yourself, so that your own converting operations become a guaranteed, captive source of demand — a "pull" that keeps the mills fed even when the broader market softens.

This is what integration means, and why Smurfit management treats it as the holy grail. In an integrated system, the box plants absorb the mills' output internally at close to full utilization through the cycle; the operator is far less hostage to the whipsaw of merchant paper prices. In a non-integrated system, the mill is exposed — and in a downturn, exposure to the merchant market is where margins go to die. The entire WestRock thesis, stripped to its core, is that a more integrated system, run the Smurfit way, will simply lose less profit in bad times and capture more in good ones.

The 2025 numbers show this logic playing out in real time, and not always comfortably. With North American box demand weak, Smurfit Westrock's mill utilization there fell to around 85% in the fourth quarter, well below the mid-90s the operator considers optimal, and management chose to take machines offline rather than flood a soft market with paper it did not need.[^4] That deliberate idling — roughly $220 million of mill-downtime cost across the year — is the paradox of the fixed-cost model made visible. As the CFO explained, "downtime is worthwhile when you just don't see the demand for the product on the outside, but you're building unnecessary stocks"; the discipline is to manage inventory, protect price, and wait for demand rather than chase volume for its own sake.[^4] It is a counterintuitive but telling signal: a management team willing to accept lower utilization today to avoid destroying price tomorrow is behaving like an owner, not a volume-chasing operator. The bet is that mid-90s utilization returns when demand does — and the operating leverage that hurt in 2025 then swings the other way.

The 150-mile monopoly

Here is the counterintuitive part that makes the industry so attractive to incumbents: corrugated boxes are bulky and cheap, which makes them absurdly expensive to ship relative to their value. A truckload of empty boxes is mostly air. As a rule of thumb, hauling finished corrugated much beyond a radius of roughly 150 to 200 miles from the plant starts to cost more in freight than the boxes are worth — though this is an industry rule of thumb rather than a precisely documented constant, and the exact radius varies with box type and diesel prices.24 The economic consequence is profound. Boxes are not a global commodity traded across oceans; they are a local business. Whoever owns the dominant mill and the cluster of converting plants inside a given 150-mile radius enjoys something close to a regional oligopoly, protected not by patents or brands but by the plain physics of freight. New entrants cannot economically ship boxes into your territory from far away, and building a competing local network costs a fortune and takes years.

That localized structure is the deep, quiet moat of this industry — and it is why consolidation among the majors matters so much. When a few disciplined players own the dominant positions across most regions, the incentive to start ruinous price wars fades, because everyone understands that capacity discipline preserves everyone's returns.

The fiber question

The last piece of the cost structure is the raw material: fiber. Modern containerboard is made overwhelmingly from recycled fiber, and the dominant input is Old Corrugated Containers, or OCC — essentially, used cardboard reclaimed from retailers, warehouses, and municipal recycling. OCC is a genuinely volatile commodity. U.S. average prices fell to around $44 a ton in late 2025, down roughly 41% from a year earlier, and in earlier cycles have swung from $70 a ton to $25 within a matter of months.25 Those swings pass straight through the cost line of any mill that has to buy fiber on the open market.

Smurfit Westrock's partial defense is to run its own extensive recycling operations, reclaiming waste paper directly from large retail and commercial customers, which gives it a captive fiber stream and a natural hedge against price spikes. It is a real advantage — but it is a hedge, not immunity. In a year of rising OCC prices, a company that cannot pass fiber inflation through to customers quickly enough will still see margins compress, and fiber cost sits near the top of any honest list of the things that can go wrong. Which raises the question of who is steering the ship, and whether their interests are aligned with the shareholders bearing that risk.

VI. Management, Alignment, and the Smurfit Playbook

There is a moment on the February 2026 investor call that tells you most of what you need to know about how this company sees itself. Tony Smurfit, describing the culture he wants to preserve at 97,000-employee scale, defined the ideal operator as "the person who turns the lights off to reduce the costs. It's the salespeople who make that call at 6:30 instead of going home, and it's the manager who looks at the share price every day because he cares about it."[^4] It is a small-business owner's ethos, articulated by the man running the largest company in the industry — and whether that ethos survives the sheer scale of the combined enterprise is one of the real open questions.

The people at the top

Tony Smurfit is the rare thing in a $30-billion-plus multinational: a chief executive with meaningful, personal, dynastic skin in the game. As of the February 2026 record date, he beneficially owned 1,602,433 ordinary shares — a stake the proxy discloses as less than 1% of the company, and which works out to roughly 0.31% of the 524 million shares outstanding.26 At early-2026 prices that holding was worth on the order of $70 million, though that dollar figure is a derived estimate rather than a number the company discloses.26 The precise percentage matters less than what it signals: this is a CEO whose family name is on the building and whose personal wealth rides on the stock, which is a materially different alignment from the typical hired-gun executive of a company this size.

Alongside him sits Ken Bowles, Executive Vice President and Group Chief Financial Officer, and a director of the company.27 Bowles joined a Smurfit Kappa predecessor in 1994, rose through its finance function, and became Group CFO in 2016 — meaning he was in the CFO seat for the 2018 defense against International Paper and has been the steward of the balance sheet through the entire arc from that rejection to the WestRock integration.27 His public reputation is built on conservative leverage management and disciplined capital allocation, and his framing on the February 2026 call was pointedly continuity-minded: what investors were seeing, he said, was "not a change in philosophy, but a continuation and, most importantly, an acceleration of a business model that has proven itself over many years."[^4]

The pair are also worth judging on how they set targets, because that is where management credibility is either built or squandered over time. Two behaviors stand out, and a neutral observer should weigh them against each other. On the positive side, when Tony Smurfit presented the 2030 plan he was careful to insist it was built from the ground up — "not prepared top-down by myself and Ken," but assembled from opportunities "identified by the teams with boots on the ground."[^4] A bottom-up plan is harder to fudge and easier to hold managers accountable to than a number reverse-engineered to please the market, and it is consistent with the decentralized culture the company preaches. On the cautionary side, this is a management team that has now made a very public five-year commitment on margins, cash flow, and returns — and the same conviction that let it reject International Paper in 2018 could, in a weaker executive, curdle into an unwillingness to admit when a target is slipping. The test is not the plan; it is what management says on the quarterly calls when a number disappoints, and whether the explanations stay specific rather than drifting into blame on the cycle. So far the language has been concrete. That is a standard to hold them to, not a verdict to grant them.

How they are paid, and why it matters

Incentive design is where alignment either becomes real or reveals itself as theater, so it is worth looking at the actual structure. Executive compensation rests on three layers: base salary, an Annual Incentive Plan, and a Long-Term Incentive Plan.28

The Annual Incentive Plan is more rigorous than a simple profit bonus. For 2025 it was weighted 80% to financial metrics — adjusted EBITDA, free cash flow, and synergy delivery — and 20% to strategic measures including health and safety.28 Tying a fifth of the annual bonus to synergy capture and safety, rather than loading everything onto a single earnings number, is a design that at least tries to reward the right behaviors during an integration.

The long-term plan is where the real alignment lives. Long-term awards are delivered primarily as performance stock units, split 75% performance-based PSUs and 25% time-vesting restricted stock.28 The PSUs vest against three metrics measured over a three-year period: relative total shareholder return versus the S&P 500, adjusted cumulative earnings per share, and average return on capital employed.28 That last metric is the one to watch. Building ROCE into long-term pay directly confronts the central risk of the whole WestRock thesis — the danger that management spends billions of capital modernizing old mills and generates volume and EBITDA without generating adequate returns on the money deployed. If executives are paid partly on ROCE, they are paid to avoid exactly the value-destructive "growth at any cost" trap that a skeptic would most fear.

Reinforcing all of it are stringent shareholding requirements: the CEO must hold shares worth eight times base salary and the CFO four times, under a share-ownership policy adopted at the moment of combination.29 Roughly 90% of the CEO's target compensation and about 80% of other named executives' is at risk rather than guaranteed.28

Taken together, the governance picture is genuinely above-average: a founding-family CEO with real ownership, a long-tenured CFO with a conservative reputation, and pay tied to returns on capital rather than mere size. None of that guarantees success. But it does mean the people making the capital-allocation decisions are structurally incentivized to make them the way a long-term owner would — which is precisely the lens through which the competitive position deserves to be examined.

VII. Porter's 5 Forces and Helmer's 7 Powers Analysis

Strip away the family drama and the deal-making, and the question an investor actually needs answered is structural: is this a good business, and is the good part durable? Two frameworks — Michael Porter's five forces and Hamilton Helmer's seven powers — are useful precisely because they force you to separate the company's advantages from the industry's, and to ask which of them can actually be defended.

Porter's five forces

Rivalry among existing competitors is best described as medium. After a generation of consolidation, the field is dominated by a handful of giants — Smurfit Westrock, International Paper, and Packaging Corporation of America chief among them in North America — and concentrated industries with disciplined capacity management tend to compete less destructively on price. That said, containerboard remains a commodity at its core; discipline is a behavior, not a law, and it can break down when someone builds too much capacity or chases volume in a downturn.

The bargaining power of buyers is medium-to-high, and it is genuinely two-sided. The largest customers are the global consumer-goods companies — the makers of packaged food, household products, and beverages — and they are sophisticated, high-volume buyers who negotiate hard. But they also need global supply footprints, exacting quality specifications, and increasingly, credible sustainable-packaging credentials. Very few suppliers can serve a multinational on both sides of the Atlantic with one integrated system, and that scarcity is the counterweight to buyer power. It is, not coincidentally, the entire strategic rationale for combining a European champion with a North American one.

The bargaining power of suppliers is low-to-medium, blunted by the company's own recycling and fiber operations, as discussed. The threat of substitutes is low and arguably improving in the company's favor, and this is the theme worth handling with the most care, because it is the one management most likes to sell. The main substitute is plastic, and the regulatory and consumer tide is genuinely running against plastic: single-use plastic bans, extended-producer-responsibility rules, and corporate plastic-reduction pledges from the big consumer-goods buyers all push demand toward fiber-based alternatives. For a company that invests heavily in design centers developing recyclable, fiber-based replacements for plastic packaging, that is a real and durable tailwind, and it reframes the box from a commodity cost line into a sustainability and marketing asset for the brand on the shelf.

The neutral caveat is one of magnitude and pace. "Plastic-to-paper" is real but gradual: fiber cannot yet replace plastic in the many applications that need moisture barriers, flexibility, or transparency, and the substitution that does happen shows up as a slow tailwind of a percentage point or two a year, not a step-change. It is the kind of secular trend that flatters a long-term chart and does very little for any single quarter — which is precisely why management's tendency to invoke it as evidence of imminent structural growth deserves a raised eyebrow. The tide is running the right way; it is running slowly, and it will not on its own close the margin gap that the whole investment case turns on.

The threat of new entrants is very low, and this is where the analysis gets interesting. A modern recycled-containerboard mill is a $500-million-plus undertaking — real recent U.S. projects have run at or above that level — and building a competing local network of converting plants takes years and hundreds of millions more.30 Combine that capital intensity with the freight-radius economics that make boxes a local business, and greenfield entry against an entrenched incumbent is close to irrational. The barrier is not one thing; it is capital plus physics plus time.

Helmer's seven powers

Of Helmer's seven, three apply with real force here, and it is worth being disciplined about which.

Scale economies are the primary power. A footprint of 57 mills and roughly 450 converting plants lets the company optimize the distance between where paper is made and where boxes are cut, minimizing the freight cost that dominates this industry's unit economics, while extracting purchasing leverage on energy, starch, chemicals, and equipment.2 Scale in packaging is not vanity; it is a direct input into the cost per box.

Process power is the secondary claim — the accumulated organizational know-how of the "Smurfit operational system," the decades of design libraries, structural engineering, and margin-management discipline that the company argues lets it wring more profit from the same assets. This is real, but it is also the hardest power to verify from the outside and the one most at risk in an integration: process power only creates value if it can actually be transferred into WestRock's plants and people. Management's claim that it can is a hypothesis currently being tested in real time, not a proven fact.

Cornered resource is the emergent, more speculative power: privileged access to municipal and commercial recycling streams through proprietary networks, which could, in tight fiber markets, keep the company's mills fed while starving less-integrated competitors. It is a genuine edge at the margin, though "cornered" overstates it — no one has cornered used cardboard.

The honest read is that this is a structurally attractive industry — high barriers, local moats, consolidating discipline — in which Smurfit Westrock holds the strongest scale position, but in which its single most important firm-specific advantage, process power, is precisely the thing it has not yet proven it can export to its newly acquired American half. Which brings the analysis to the scoreboard: the margins.

VIII. The Financial Battle: Margin Benchmarking vs. PCA and IP

Numbers in this industry only mean something in comparison, so let us set the scoreboard clearly and then interpret it. In fiscal 2025, Smurfit Westrock generated net sales of $31.18 billion and adjusted EBITDA of $4.94 billion, for an adjusted EBITDA margin of 15.8%.2 The engine was North America, which produced roughly $3.0 billion of adjusted EBITDA on about $19 billion of revenue — roughly 60% of group earnings — with Europe, the Middle East, Africa and Asia-Pacific contributing about $1.6 billion, and Latin America about $485 million.31[^4] Through the first nine months of the year, North America alone had already delivered around $2.3 billion of adjusted EBITDA.32

The regional drivers

Underneath the group number sit three very different businesses, and the differences are instructive. North America is the volume engine and the problem child at once: about $19 billion of revenue and roughly $3 billion of adjusted EBITDA in 2025, but at a segment margin in the mid-teens — 14.7% in the fourth quarter — that is precisely the figure the whole strategy exists to lift.[^4] This is the WestRock inheritance in a single ratio: enormous scale, sub-par profitability, all the upside and all the risk concentrated in one place.

Europe, the Middle East, Africa and Asia-Pacific is the legacy Smurfit Kappa heartland — roughly $11 billion of sales and about $1.6 billion of adjusted EBITDA across some 27 countries, with margins that expanded back above 16% in the fourth quarter as the region's pricing and cost discipline reasserted itself.[^4] It is the proof that the operating model works when it is mature, and the template management says it will impose on North America.

The quiet standout, though, is Latin America. It is the smallest segment — about $485 million of adjusted EBITDA — but it is by some distance the most profitable, running fourth-quarter margins above 24%, and it was the only region posting genuine volume growth in 2025.31[^4] Over the prior decade the company doubled Latin American adjusted EBITDA and expanded the region's margin by more than 500 basis points, to around 23%, in markets with less competition and structural growth.[^4] It is a useful reminder that "packaging" is not one business but many, and that a well-positioned regional franchise with limited competition can out-earn a giant. On the February 2026 call, management set 2030 targets for each region: North America to grow toward $4.2 billion of adjusted EBITDA at a margin above 20%; Europe toward roughly $2.1 billion; and Latin America toward $800 million at margins approaching 28%.[^4] The arithmetic of the group plan, in other words, is really the arithmetic of dragging the North American margin up toward what the other two regions already achieve.

The PCA gap

Now place that against the industry's profitability benchmark. In fiscal 2025, Packaging Corporation of America — a company less than a third of Smurfit Westrock's size — reported net sales of $8.99 billion, adjusted EBITDA of $1.86 billion, and an adjusted EBITDA margin of 20.7%.5 That is a gap of nearly five full percentage points, and it is the single most important number in the entire Smurfit Westrock story, because it quantifies the prize.

Why does a smaller company earn so much more per dollar of sales? The answer is the integration and discipline themes made concrete. PCA runs a tightly integrated domestic containerboard system in which the large majority of its mill output is consumed by its own box plants; it runs its mills at very high operating rates; it stays largely out of the volatile merchant market; and it operates with a lean, decentralized, low-overhead structure.6 It is, in essence, the model Smurfit Westrock says it is trying to build at continental scale — which is why the comparison is so uncomfortable and so clarifying at once. PCA is not just a competitor; it is a live proof-of-concept for what the North American assets could earn if they were run differently.

There is a second, harsher gap that gets less attention: returns on capital. Smurfit Westrock's return on capital employed in 2025 sat in the mid-single digits, weighed down by the enormous asset and goodwill base it took on in the merger, against a PCA that earns returns on capital employed in the low-to-mid teens. Margins tell you about operating efficiency; ROCE tells you whether the whole enterprise, including the price paid for it, is creating value. On that measure the mountain is even steeper than the margin gap alone implies — and it is why the ROCE metric in the executive pay plan is more than a governance nicety.

The 2030 plan to close it

At the February 11, 2026 investor update, management laid out a medium-term plan explicitly built around closing this gap.33 The headline targets: group adjusted EBITDA of roughly $7 billion by the end of 2030, implying a compound growth rate of about 7% a year; margin expansion of more than 300 basis points, lifting the group toward a 19% margin; cumulative discretionary free cash flow of about $14 billion over 2026–2030; and a return on capital employed roughly 700 basis points higher, toward 15%.33[^4] The North American segment carries most of the load, with a target to grow from about $3 billion of adjusted EBITDA to $4.2 billion and to lift its margin above 20%.[^4]

Two features of the plan deserve an investor's attention, one reassuring and one cautionary. The reassuring feature is that management explicitly stated the margin targets do not depend on a pricing recovery. As the CFO put it, "the margin expansion we are targeting is not dependent on a pricing cycle" — the plan assumes only modest market volume growth of roughly 1.6% in North America and is built on self-help: cost, footprint optimization, and the transfer of value-selling techniques into the U.S.[^4] A plan that does not require the cycle to bail it out is a more credible plan.

The cautionary feature is simply that it is a five-year target from a company one year into an integration, and the history of this industry is littered with margin promises that dissolved when demand disappointed or a competitor broke ranks. The CFO's own rule of thumb — that each percentage point of volume growth is worth around $60 million of EBITDA — cuts both ways: the operating leverage that makes the upside so attractive makes a volume shortfall bite just as hard.[^4] The plan is coherent and, unusually, honest about its assumptions. Whether it is achieved is a question only the next several years of box volumes and mill utilization can answer.

IX. The Future Investment Case: Bull vs. Bear

Every good business story eventually collapses into a single argument between two reasonable people. Here it is, stated as fairly as possible on both sides.

Why this wins from here

The bull case rests on three pillars. The first is execution credibility. This management team has, so far, done what it said: it defended its independence in 2018, compounded capital in Europe at more than double the peer rate, and in year one of the WestRock integration exceeded a $400 million synergy target while cutting more than 4,600 North American jobs and shedding hundreds of thousands of tons of high-cost capacity.[^4] A team with a demonstrated ability to close plants, cut cost, and hold pricing discipline is exactly the team you want holding a fixable asset base. If the legacy Smurfit margin discipline can be applied to WestRock's mills, the earnings uplift is large and mechanical — the PCA benchmark shows how large.

The second pillar is the secular substitution of paper for plastic. As regulation tightens against single-use plastic and consumer-goods companies redesign packaging to meet plastic-reduction commitments, a supplier with deep design capability in recyclable fiber-based solutions is positioned to take share of a structurally growing addressable market. This is a genuine multi-decade tailwind — though it is worth noting that management tends to describe it with more certainty than the near-term volume data yet supports, and paper's share gains against plastic have historically been gradual rather than dramatic.

The third pillar is cyclical recovery. The industry spent 2024 and 2025 working through a severe post-pandemic destocking, with box volumes depressed and mills taking downtime. When volumes normalize, the operating leverage that makes this business painful on the way down works ferociously on the way up. A company running below optimal utilization has embedded earnings power that reappears the moment demand does.

Why the case could break

The bear case is equally concrete, and a serious investor should sit with it. The first risk is that they overpaid for a modernization problem. WestRock's mills were, by common account, under-invested for years; the capital required to bring them to the standard the plan assumes could run for years, consuming free cash flow and holding down returns on capital even if EBITDA rises. High EBITDA on a bloated asset base is not the same as value creation — and the current mid-single-digit ROCE is the warning light on the dashboard.

The second risk is cultural. Smurfit Kappa's edge was a lean, decentralized, entrepreneurial culture — the "turn off the lights" ethos. WestRock's was larger, more centralized, more process-heavy. Integrating two industrial cultures across an ocean is exactly the kind of soft problem that destroys hard synergy math, and it is the one thing management cannot fully control by decision.

The third risk is the competitor across the field. A newly enlarged International Paper, having absorbed DS Smith, is not a passive incumbent; it now competes with Smurfit Westrock in both North America and Europe with its own transatlantic scale and its own cost agenda.4 If either giant chooses to defend or grab share through price during a soft patch, the disciplined-capacity thesis that underpins everyone's margins could crack — and the 300-basis-point expansion plan is the first thing that would be sacrificed.

The fourth risk is input cost. Fiber inflation, if OCC prices reverse their 2025 slide and the company cannot pass the cost through fast enough, would squeeze exactly the margins the plan needs to expand.25

The fifth risk sits on the balance sheet. The company carried net debt of just under $13 billion at the end of 2025, a leverage ratio of about 2.6 times EBITDA, against a target of below 2.0x.[^4] On the reassuring side, the credit story has been moving the right way: Fitch upgraded the company to BBB+ with a stable outlook, and refinancings pushed the next meaningful maturity out to 2028 at an average interest rate of around 4.64%, buying time and reducing refinancing risk in a higher-rate world.[^4] But leverage above the target is why the promised buybacks cannot begin until 2027, and it means the plan's ambitious capital-return math depends on the free cash flow arriving on schedule. If EBITDA disappoints, deleveraging slows, buybacks slip, and the whole shareholder-return narrative is pushed to the right.

An activist looking at this company would press on the honest pressure points: a leverage position around 2.6 times EBITDA that constrains buybacks until it falls below 2.0x; the retained lower-return consumer-packaging businesses that management defends as "highly cash generating" — Tony Smurfit's line was "I don't think we should be throwing away good businesses, and it integrates well with our system" — but which a purist would argue dilute the corrugated core; the multi-year gap between the promised margins and the current ones; and the sheer capital intensity of the fix.[^4] There is also a live question of whether the crown jewel of the model — the "value selling" that lets Smurfit charge premium prices for design and service rather than compete on paper cost — actually transfers to American customers who have historically bought boxes as a commodity. Management concedes it is "really just at the beginning of this journey of value selling here in the U.S.," which is an honest admission that the single most important lever of the plan is unproven on this side of the Atlantic.[^4] To management's credit, the leadership has been unusually specific about its plan and unusually willing to name the North American margin gap as the problem to be solved rather than obscure it — which is more than many management teams offer. But specificity is a promise, not a result. The case turns entirely on delivery.

X. Playbook & Core Lessons for Founders & Investors

Step back from the ticker and the quarterly cadence, and the Smurfit Westrock story distills into a handful of durable lessons — the kind that outlast any single cycle.

The first is the power of integration in capital-intensive industries. Running a fixed-cost manufacturing business without securing downstream demand is a recipe for cyclical destruction; the operator who owns both the factory and its captive customer keeps the expensive machines running when the market turns. Smurfit spent ninety years learning and re-learning this lesson, and the entire logic of the WestRock deal is a wager that it still holds. The mill needs the "pull" of the box plant. Secure the pull, and the economics change.

The second is that conviction and credibility compound over time. The 2018 decision to reject International Paper looked, to some, like a family unwilling to sell. In hindsight it was the moment management staked its reputation on being able to create more value than an acquirer would pay for — and it was that banked credibility that let the same team ask shareholders, six years later, to trust it with a target twice its size. Credibility is capital. It is earned slowly, by keeping promises, and it is the currency that makes the audacious next move possible.

The third is that operational benchmarking is the ultimate reality check. Size flatters and conceals; margins do not. Set Smurfit Westrock's 15.8% against Packaging Corporation of America's 20.7%, and the exact shape of the problem — and the exact size of the prize — snaps into focus.25 For any investor, the discipline of asking "who earns the most on comparable assets, and why?" is worth more than any narrative a management team can tell.

The fourth is the value of buying at the cyclical bottom. The best acquisitions in commodity industries are made when the target's world is bleakest — when prime capacity trades at a discount to replacement cost because no one wants it. Smurfit bought into a packaging trough. Whether that timing proves brilliant or merely well-marketed depends on the recovery it was betting on. But the instinct — buy the assets when the cycle makes owners want to sell — is as old and as reliable as capitalism itself.

XI. Epilogue & Outro

As of mid-2026, the story is poised rather than settled. Management has guided to full-year 2026 adjusted EBITDA of $5.0 billion to $5.3 billion, a step up from 2025's $4.94 billion, achieved — if achieved — without assuming any help from a pricing recovery it has pointedly declined to bake in.33[^4] The balance sheet has been strengthened, with leverage brought down to about 2.6 times and a Fitch upgrade to BBB+ along the way, and the company has laid out a path to buybacks from 2027 once leverage falls below its 2.0x target.[^4]33 The pieces of the plan are in place. What remains is the execution, across a five-year horizon, in an industry that has humbled more than one confident consolidator.

The unresolved question is the one this story opened with. Can an Irish family business that spent nearly a century mastering the economics of the cardboard box take the largest, most complicated, most under-earning asset base in the industry and run it the way it runs its own — closing the margin gap, lifting returns on capital, and turning scale into profitability rather than just size? The bull says the team has earned the benefit of the doubt. The bear says a five-year self-help plan on a freshly merged, capital-hungry, cyclically exposed asset base is exactly the kind of promise that looks best on the day it is announced.

For the investor watching from here, the noise can be tuned out and attention fixed on a very small number of things. Track North American corrugated box volumes and mill utilization, because that is where the operating leverage lives and where a recovery — or its absence — will show up first. Track the adjusted EBITDA margin against that 300-basis-point ambition, and against the PCA benchmark that defines the ceiling. And above all, track return on capital employed, because in a business where it is trivially easy to grow EBITDA by spending capital, ROCE is the one number that reveals whether the American beast is being tamed or merely fed. Those are the leading indicators. Everything else is commentary.

References

-

Smurfit Kappa-WestRock acquisition finalized, trading begins on NYSE and LSE — Packaging Dive, 2024-07-08 ↩↩

-

Smurfit Westrock Reports Fourth Quarter and Full Year 2025 Results — Smurfit Westrock / Business Wire, 2026-02-11 ↩↩↩↩↩

-

International Paper Completes Acquisition of DS Smith — International Paper / PaperAge, 2025-02-03 ↩↩

-

Packaging Corporation of America Reports Fourth Quarter and Full Year 2025 Results — Packaging Corporation of America / Business Wire, 2026-01-27 ↩↩↩

-

Packaging Corporation of America Investor Relations — Packaging Corporation of America ↩↩

-

Jefferson Smurfit Group plc Company History — Company-Histories.com ↩

-

Jefferson Smurfit Corporation / Stone Container merger Form 8-K — U.S. Securities and Exchange Commission, 1998-11-18 ↩

-

Smurfit buyout takes the top slot — The Irish Times, 2002-09-03 ↩

-

Smurfit Kappa Group Form 20-F — U.S. Securities and Exchange Commission, 2007 ↩↩

-

Smurfit Kappa's Board Unanimously Rejects Revised Proposal from International Paper — Smurfit Kappa, 2018-03-26 ↩↩

-

International Paper Will Not Make Offer to Acquire Smurfit Kappa — International Paper / PR Newswire, 2018-06-06 ↩

-

WestRock Company completion of Rock-Tenn and MeadWestvaco combination Form 8-K — U.S. Securities and Exchange Commission, 2015-07-01 ↩

-

MeadWestvaco Corporation formation Form 8-K — U.S. Securities and Exchange Commission, 2002-01-29 ↩

-

Rock-Tenn Company / Smurfit-Stone Container combination Form 8-K — U.S. Securities and Exchange Commission, 2011-01-23 ↩

-

WestRock / KapStone Paper and Packaging combination Form 8-K — U.S. Securities and Exchange Commission, 2018-01-29 ↩

-

Smurfit Kappa and WestRock merger analysis — Fastmarkets, 2023 ↩↩

-

WestRock and Smurfit Kappa Announce Transaction to Combine — WestRock Form 425, U.S. Securities and Exchange Commission, 2023-09-12 ↩↩↩↩↩

-

Smurfit Westrock Fourth Quarter and Full Year 2025 press release (synergies and capacity closures) — Smurfit Westrock, 2026-02-11 ↩↩

-

Corrugated box cost and freight economics — CorrugatedBoxSuppliers.com ↩

-

Smurfit Westrock plc 2026 Definitive Proxy Statement (DEF 14A) — U.S. Securities and Exchange Commission, 2026-03-11 ↩↩

-

The Sunday Interview: Ken Bowles, Chief Financial Officer, Smurfit Kappa — Business Post ↩↩

-

Smurfit Westrock plc 2026 Definitive Proxy Statement — Executive Compensation — U.S. Securities and Exchange Commission, 2026-03-11 ↩↩↩↩↩

-

Smurfit Westrock Share Ownership Policy (adopted 2024-07-05) — Smurfit Westrock ↩

-

Green Bay Packaging announces $500 million mill investment — Urban Milwaukee, 2018 ↩

-

Smurfit Westrock plc Form 10-K for fiscal year 2025 — U.S. Securities and Exchange Commission, 2026-02-27 ↩↩

-

Smurfit Westrock plc Form 10-Q for the quarter ended September 30, 2025 — U.S. Securities and Exchange Commission, 2025-10-29 ↩

-

Smurfit Westrock Medium-Term Investor Update — Smurfit Westrock / Business Wire, 2026-02-11 ↩↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube