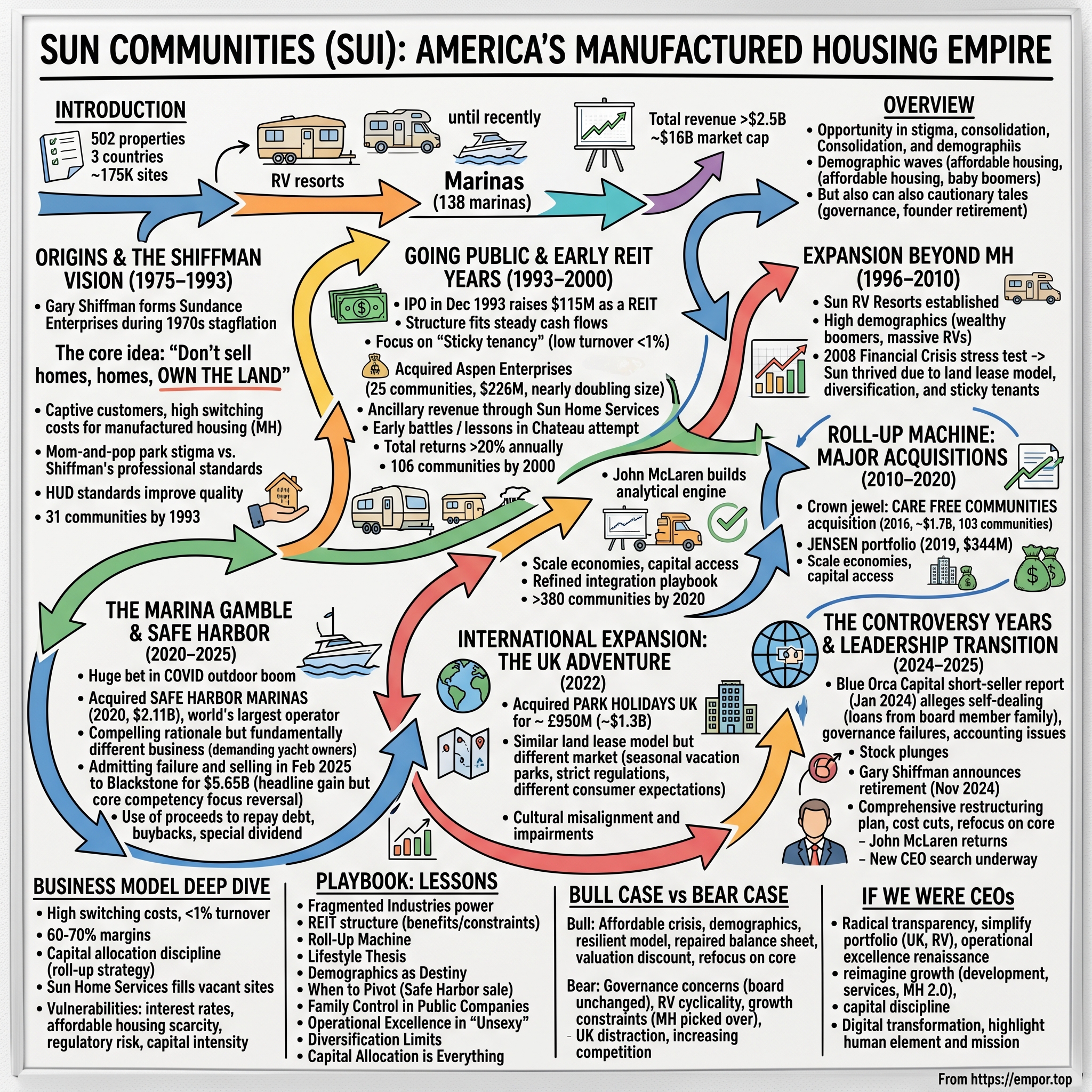

Sun Communities: The Story of America's Manufactured Housing Empire

I. Introduction & Episode Roadmap

Picture this: A sprawling manufactured housing community in Florida, palm trees swaying, golf carts humming along manicured paths, retirees gathering at the community center for water aerobics. Now multiply that scene by 502 properties across three countries. Add 174,850 sites where Americans, Canadians, and Brits call home—some permanently, others seasonally. Layer in RV resorts where road warriors park their million-dollar motorhomes next to families on budget camping trips. Until recently, throw in 138 marinas housing everything from modest fishing boats to superyachts. This is Sun Communities—a $16 billion real estate empire built on a simple insight: Americans need affordable places to live, and they're willing to rethink what "home" means to get them.

The company that Gary Shiffman founded in 1975 as a small Michigan manufactured housing operator has morphed into something far more complex—a lifestyle property REIT that's part affordable housing provider, part retirement community operator, part outdoor hospitality company. It's a business that generates over $2.5 billion in annual revenue by owning the land under mobile homes, the sites where RVs park, and until a recent strategic reversal, the slips where boats dock.

How did a company focused on what many consider the bottom rung of American housing climb to become one of the nation's largest REITs? How did it survive the 2008 financial crisis when traditional real estate collapsed? Why did it spend $2.1 billion on marinas only to sell them five years later for $5.25 billion? And what really happened when a short-seller accused the company of self-dealing, sending the stock tumbling and hastening the founder's retirement?

This is a story about seeing opportunity where others see stigma. About consolidating a fragmented industry one trailer park at a time. About riding demographic waves—from affordable housing shortages to baby boomer retirements. It's also a cautionary tale about governance, family control, and the challenges of managing a public company like a private fiefdom. Along the way, we'll explore the economics of "sticky" tenants who can't afford to move their homes, the surprising profitability of RV resorts, and why Warren Buffett's Clayton Homes is both Sun's biggest supplier and potential competitor.

What we're about to unpack isn't just a real estate story—it's a lens into American economic mobility, retirement dreams, and the trade-offs between affordability and aspiration. From Michigan trailer parks to UK holiday villages, from RV resorts to yacht harbors, Sun Communities has built an empire on unconventional property types that traditional REITs wouldn't touch. The question now: Can it survive its founder's departure and emerge stronger, or will the cracks exposed by critics prove too deep to repair?

II. Origins & The Shiffman Vision (1975–1993)

The year was 1975. Gerald Ford was president, trying to heal a nation scarred by Watergate and Vietnam. Gas lines from the oil embargo were fresh in Americans' minds. Inflation hit 9%. The economy was mired in stagflation—that toxic combination of stagnant growth and rising prices that economists said couldn't exist. In Detroit, the auto industry was reeling from foreign competition. Michigan's unemployment rate touched 12%. It was, by most measures, a terrible time to start a real estate company.

But Gary Shiffman saw something different in those economic tea leaves. The young entrepreneur recognized that America's post-war suburban dream was becoming unaffordable for millions. Traditional site-built homes required down payments and mortgages that factory workers, retirees, and service employees couldn't swing. Yet these same people needed quality housing. They had jobs, families, dignity—everything except access to conventional homeownership. Manufactured housing, despite its trailer park stigma, could bridge that gap.

Shiffman founded Sundance Enterprises, Inc. with a contrarian thesis: Don't sell the homes, own the land underneath them. While others in the manufactured housing industry focused on building and selling the units themselves—a low-margin, highly cyclical business—Shiffman would buy the communities where these homes sat. It was a brilliant insight that would define Sun's business model for the next five decades. A manufactured home might cost $30,000-$80,000, but moving it cost $6,000-$10,000. Once someone parked their home on your land, they effectively became a captive customer. The switching costs were too high to leave over modest rent increases.

The manufactured housing landscape of the 1970s was nothing like today's communities. These were true "trailer parks"—rows of single-wide units on rented lots, minimal amenities, often poor management. The stereotype wasn't entirely unfair. Many parks were owned by mom-and-pop operators who saw them as passive income, not active businesses requiring capital investment and professional management. Crime, drugs, and deteriorating conditions plagued poorly run communities. Banks wouldn't lend to buyers. Municipalities fought new developments. The entire sector was stigmatized.

Shiffman's approach was radically different. He targeted well-located communities near employment centers and invested in infrastructure—paved roads, proper utilities, community centers. He implemented professional property management, screened residents, and enforced community standards. This wasn't charity; it was smart business. Better communities attracted better residents who paid rent reliably and stayed longer. The average resident would stay 14 years, creating an incredibly stable revenue stream.

For the first 18 years, Sun operated as a private company, methodically acquiring properties across Michigan. The playbook was consistent: find undermanaged communities in good locations, buy them at distressed prices, invest in improvements, raise rents gradually, and maintain high occupancy through superior operations. By 1993, Shiffman had assembled 31 communities—a solid regional portfolio, but hardly an empire.

The timing of Sun's founding proved prescient. The late 1970s and 1980s saw manufactured housing evolve from "trailers" to legitimate homes. The federal government established HUD construction standards in 1976, dramatically improving quality and safety. Homes got wider—double-wides and triple-wides offered 1,500+ square feet of living space. Pitched roofs, drywall interiors, and residential appearances replaced the aluminum-sided boxes of earlier generations. By the early 1990s, manufactured homes comprised 7% of all new single-family homes sold in America.

What Shiffman understood, and what would drive Sun's growth for decades, was a fundamental economic reality: America had an affordable housing problem that was only getting worse. In 1975, the median home price was 3.5 times median household income. By 1993, it was approaching 4 times. For millions of Americans—retirees on fixed incomes, blue-collar workers, single parents—traditional homeownership was slipping out of reach. Manufactured housing offered 25% more space for 50% less cost per square foot than site-built homes. It wasn't just affordable; it was the only option.

The private years also allowed Shiffman to build his management philosophy without Wall Street scrutiny. He developed systems for evaluating acquisitions, standardized operations across properties, and most importantly, built a culture that balanced resident satisfaction with shareholder returns. This wasn't Silicon Valley disruption; it was Midwest operational excellence applied to an unglamorous but essential business.

By 1993, Shiffman faced a choice. The manufactured housing industry was consolidating. Larger players were emerging. Access to capital would determine winners and losers. He could remain a successful regional operator, or he could tap public markets and build something bigger. The decision to go public would transform Sun from a Michigan-based owner of trailer parks into one of America's largest REITs. But first, Shiffman had to convince Wall Street that manufactured housing communities weren't just investable—they were actually superior to traditional apartments.

III. Going Public & Early REIT Years (1993–2000)

December 1993. The Clinton administration was pushing healthcare reform. The North American Free Trade Agreement had just passed. The internet was still mostly academic. And in this pre-digital world, a Michigan manufactured housing operator named Sun Communities was about to attempt something audacious: convince Wall Street that trailer parks deserved public market valuations.

The IPO raised $115 million, valuing Sun's 31 communities at a price that seemed generous to skeptics but would prove laughably cheap in hindsight. The real coup wasn't the valuation—it was the structure. Sun went public as a Real Estate Investment Trust (REIT), a tax-advantaged vehicle that avoided corporate taxation by distributing 90% of taxable income as dividends. For a business generating steady cash flows from long-term tenants, the REIT structure was perfect. It forced capital discipline while providing tax-efficient returns to shareholders.

The 1990s were the golden age of REIT formation. The sector's market cap would grow from $8 billion in 1990 to $140 billion by 2000. But most REITs focused on traditional property types—offices, malls, apartments. Manufactured housing was different. Shiffman had to educate investors on the model's unique economics. Unlike apartment REITs where tenants could easily move, Sun's residents owned their homes but rented the land. Moving a manufactured home wasn't like loading a U-Haul. It required permits, professional movers, site preparation, and typically $6,000-$10,000 in costs. Most homes, once placed, never moved again.

This created what Shiffman called "sticky" tenancy. Annual turnover was less than 1%, compared to 50-60% for apartments. Rent increases faced less resistance because moving was so expensive. The business was essentially a land lease with predictable, growing cash flows. Operating expenses were minimal—Sun didn't maintain the homes, just the common areas and infrastructure. Margins were spectacular: 60-70% operating margins versus 30-40% for traditional apartments.

The public market validation came quickly. In March 1996, Sun announced its first major acquisition as a public company: 25 manufactured housing communities for $226 million. This single deal nearly doubled Sun's portfolio. The properties were acquired from different sellers across multiple states, demonstrating Sun's ability to source and execute complex transactions. The acquisition was funded through a combination of debt and equity, establishing the capital markets playbook Sun would follow for decades: use public equity for growth, maintain moderate leverage, and let operational improvements drive returns. The early operational philosophy was deceptively simple but revolutionary for the industry. Sun announced plans to purchase 25 new manufactured housing communities from Aspen Enterprises Ltd. for $226 million, nearly doubling its footprint in a single transaction. But what made Sun different wasn't just its appetite for acquisitions—it was how it thought about the business. While competitors focused on either manufacturing homes or operating communities, Sun recognized that the real value lay in land ownership combined with professional management.

The company also pioneered ancillary revenue streams that would become crucial to its model. Sun Home Services sold new and used homes to residents, capturing margins on both sides of transactions. This wasn't predatory—it actually helped residents by providing financing options banks wouldn't offer. Traditional lenders still viewed manufactured homes as depreciating assets like cars, not appreciating assets like real estate. Sun stepped into this financing gap, earning returns while enabling homeownership.

During the mid-1990s, manufactured housing was the fastest-growing segment of the U.S. real estate industry. Investors were encouraged by their financial planners to buy shares in manufactured housing REITs, transforming the sector from backwater to Wall Street darling. The numbers justified the enthusiasm. Sun's revenue grew from $32.4 million in 1994 to $45.1 million in 1995, while net income reached $11.7 million. By the end of 1996, revenue reached $73.2 million, up 62 percent over the previous year. The company's net income also rose to $18.6 million.

But 1996 also brought Sun's first major competitive battle—and defeat. The company attempted to acquire Chateau Properties, its largest competitor, in what would have created a manufactured housing colossus. The deal fell apart amid higher competing bids, teaching Shiffman an important lesson: in the consolidating world of manufactured housing REITs, speed and certainty of execution mattered more than price. Sun would rarely lose another bidding war.

The late 1990s validated Sun's model spectacularly. In 1997, Sun acquired nine communities from Park Realty Inc. for approximately $93 million, strengthening its foothold in the Southwest, Indiana, and Florida. Throughout the year, Sun acquired a total of 14 communities and developed 917 new sites. Through its Sun Home Services subsidiary, the company also sold 548 new homes and was involved in the resale brokerage of 555 additional homes. The company was firing on all cylinders—acquiring, developing, and facilitating home sales.

What's remarkable about this period is how Sun built competitive advantages that would prove durable for decades. First, scale economies: larger portfolios meant lower per-site management costs and better purchasing power with suppliers. Second, access to capital: as a public REIT with growing credibility, Sun could fund acquisitions cheaper than mom-and-pop operators. Third, operational expertise: standardized processes, professional management, and data-driven decision-making created value competitors couldn't match.

The REIT structure itself became a competitive weapon. By distributing 90% of taxable income as dividends, Sun attracted income-focused investors—pension funds, retirees, endowments—who provided patient capital. This shareholder base understood and appreciated the business's stability, unlike growth investors who might panic during downturns. The quarterly dividend also imposed discipline, forcing management to generate consistent cash flows rather than pursue speculative projects.

By 2000, Sun had grown to 106 communities with over 40,000 sites. The stock had delivered total returns exceeding 20% annually since the IPO. Shiffman had proven that manufactured housing communities weren't just investable—they were among the best-performing property types in real estate. The combination of affordable housing demand, sticky tenancy, and consolidation opportunities created a powerful flywheel that would spin for another two decades.

Yet even as Sun celebrated its public market success, Shiffman was already thinking bigger. The demographics of America were shifting. Baby boomers were entering their peak earning years and starting to think about retirement. They wanted active, amenity-rich communities in warm climates. And increasingly, they were buying RVs—not the pop-up campers of their parents, but luxurious motorhomes costing hundreds of thousands of dollars. These RVs needed places to park, and their owners wanted resort-style amenities. It was time for Sun to expand beyond its manufactured housing roots.

IV. Expansion Beyond Manufactured Housing (1996–2010)

The epiphany came to Shiffman during a Florida property tour in 1996. Driving past his manufactured housing communities, he kept noticing something peculiar: massive RVs parked in driveways, sometimes worth more than the homes themselves. These weren't weekend camping vehicles—they were 40-foot luxury motorhomes with marble countertops, king-size beds, and satellite dishes. Retirees were spending six months in their manufactured homes and six months traveling. They needed places to park these rolling mansions, and existing RV parks—mostly mom-and-pop operations with gravel lots and basic hookups—weren't cutting it.

In 1996, Sun RV Resorts was established, marking Sun's first major diversification beyond manufactured housing. The initial strategy was modest: acquire RV parks adjacent to or near existing manufactured housing communities, creating operational synergies. But Shiffman quickly realized the RV resort business had even better economics than manufactured housing. While manufactured home residents paid $400-$600 monthly for their lots, RV sites in premium locations could command $50-$100 per night from transient guests, or $800-$1,500 monthly from seasonal visitors.

The RV industry was exploding, driven by the same demographic forces benefiting manufactured housing. Baby boomers were entering their 50s with unprecedented wealth. They'd worked hard, saved aggressively, and now wanted to enjoy retirement. But this wasn't their parents' retirement of rocking chairs and early-bird specials. These were active retirees who wanted to explore America, visit grandchildren, escape winter. The RV gave them freedom; Sun's resorts gave them community.

Sun's approach to RV resorts mirrored its manufactured housing playbook: acquire undermanaged properties, invest in amenities, professionalize operations, and gradually raise rates. But the execution was different. RV resorts needed pools, clubhouses, organized activities, and increasingly, high-speed internet and cable TV. The customer base was more demanding—these were often affluent retirees comparing Sun's properties to Marriott hotels, not other RV parks.

The geographic expansion strategy was laser-focused: follow the snowbirds. Florida became Sun's laboratory for RV resort excellence. Properties in Fort Myers, Naples, and the Keys filled with Midwestern retirees from November to April. Michigan resorts captured the summer traffic. The seasonal arbitrage was beautiful—when one region slowed, another picked up. This natural hedge reduced revenue volatility compared to pure manufactured housing exposure.

By 2000, Sun operated 15 RV resorts with 6,000 sites. The segment was small—less than 10% of total revenue—but growing rapidly. More importantly, it was validating Shiffman's "lifestyle property" thesis. Whether manufactured homes or RV resorts, Sun was really in the business of providing affordable, community-oriented living solutions for America's middle class. The specific property type mattered less than understanding and serving this customer base.

Then came 2008. The financial crisis that devastated traditional real estate should have crushed Sun. Manufactured housing had been ground zero for subprime lending excess. Companies like Champion Enterprises and Fleetwood, major home manufacturers, filed for bankruptcy. Financing evaporated. Home sales plummeted 75%. Competitors like Affordable Residential Communities collapsed. Yet Sun not only survived—it thrived.

The key was Sun's diversified model and conservative balance sheet. While competitors had levered up during the boom, Sun maintained debt at just 50% of total capitalization. When others had focused on home sales and financing, Sun stuck to land leasing. And critically, Sun's residents couldn't leave even if they wanted to. That $6,000-$10,000 moving cost became an insurmountable barrier when credit markets froze. Occupancy remained above 80% even as unemployment spiked.

The crisis also revealed the resilience of Sun's RV resort business. Affluent retirees might postpone buying new RVs, but they didn't stop traveling. In fact, "staycations" and domestic travel increased as international trips became less appealing. RV resort occupancy held steady, and rate growth merely slowed rather than reversed. The lifestyle investment thesis was stress-tested and proven.

Sun emerged from the financial crisis in an enviable position. Competitors were bankrupt or desperate for capital. Lenders who'd sworn off manufactured housing were slowly returning, but only for established operators with proven track records. Distressed properties were available at fire-sale prices. The stage was set for Sun's greatest acquisition spree.

The operational lessons from this period would define Sun's strategy for the next decade. First, diversification across property types and geographies provided crucial stability. Second, conservative leverage enabled opportunistic acquisitions during downturns. Third, focusing on land ownership rather than home sales insulated Sun from manufacturing and financing cycles. Fourth, the RV resort business wasn't just a nice addition—it was a growth engine with superior returns and demographic tailwinds.

By 2010, Sun's portfolio had grown to 139 communities and RV resorts with over 50,000 sites. Revenue exceeded $300 million annually. The company had survived the worst real estate collapse since the Great Depression and emerged stronger. But Shiffman wasn't satisfied with organic growth and small acquisitions. The fragmented manufactured housing and RV industries were ripe for consolidation. It was time to build a roll-up machine that would transform Sun from a large regional operator into a national powerhouse.

V. The Roll-Up Machine: Major Acquisitions Era (2010–2020)

John McLaren arrived at Sun Communities in 2010 with a mandate: build an acquisition engine that could evaluate, execute, and integrate properties at unprecedented scale. The new Chief Operating Officer brought a military precision to what had been an opportunistic process. Every potential acquisition would be scored on 47 criteria. Integration playbooks would be standardized down to the day. Due diligence teams would descend on properties like SWAT units, examining everything from utility infrastructure to resident lease agreements. This wasn't just buying real estate—it was industrial-scale consolidation.

The transformation began with technology. Sun built proprietary models that could value properties based on location, demographics, competition, and dozens of other factors. They knew that a 55+ manufactured housing community in Sarasota with 85% occupancy and deferred maintenance was worth acquiring at 12x current NOI because post-renovation, it would generate 15x. They understood that an RV resort near Disney World with 60% seasonal occupancy could be transformed into a 90% destination property with the right amenities. This analytical edge allowed Sun to bid aggressively on properties others undervalued and walk away from those others overpaid for. The crown jewel came in June 2016: Sun agreed to acquire Carefree Communities from private equity firm Centerbridge Capital Partners II LP for approximately $1.7 billion. Carefree Communities added 103 manufactured housing and RV communities, comprising 27,554 total sites—9,829 developed manufactured housing sites and 17,725 RV sites—concentrated in California and Florida. This wasn't just Sun's largest acquisition to date; it was a transformative deal that established Sun as the clear number two player in the industry behind Equity LifeStyle Properties.

The Carefree deal showcased everything McLaren's acquisition machine had become. The pricing—roughly $61,000 per site—seemed expensive to outsiders but reflected Sun's sophisticated underwriting. The acquisition enhanced geographic diversity, deepened Sun's presence in key coastal markets, boosted age-restricted sites to 33% of the portfolio, and increased California holdings from under 1% to 6%. These weren't just numbers; they represented strategic positioning in supply-constrained markets with favorable demographics.

The integration was military-precise. Within 90 days, all Carefree properties were rebranded, systems converted, and employees onboarded or transitioned. Revenue management systems immediately began optimizing rents. Deferred maintenance backlogs were addressed. Amenities were upgraded. Within 18 months, same-property NOI at the acquired communities increased by double digits—validation of Sun's value creation thesis.

But the real genius of the roll-up strategy wasn't individual deals—it was the cumulative effect. Each acquisition made the next one easier. Lenders became more comfortable, offering better terms. Sellers sought Sun out, knowing they were the buyer of choice. Employees from acquired companies brought new ideas and best practices. The portfolio's geographic and demographic diversity reduced risk. It was a virtuous cycle that competitors struggled to replicate.

The competitive landscape during this period was fascinating. Equity LifeStyle Properties, led by Sam Zell, remained the 800-pound gorilla with superior coastal California and Florida properties. But Sun was closing the gap through sheer acquisition velocity. Smaller players like UMH Properties and Hometown America were left fighting for scraps. Private equity firms occasionally entered bidding wars but usually lost to Sun's certainty of execution and willingness to pay strategic premiums. In October 2019, Sun acquired a portfolio of 31 manufactured housing communities for $343.6 million through the acquisition of Jensen's Inc., a Connecticut-based operator. The Jensen portfolio comprised 5,230 developed sites and over 460 additional expansion sites, with 77% age-restricted properties and 92.5% occupancy. The deal structure—$274.8 million in stock and the remainder in cash—showed Sun's flexibility in structuring transactions to meet seller needs while preserving capital for future deals.

What made the roll-up machine truly formidable was operational integration. McLaren oversaw the acquisition and integration of approximately 350 manufactured housing and RV communities during his tenure. Each property went through the same transformation: immediate rebranding, system conversions within 30 days, capital improvement plans implemented within 90 days, and rent optimization strategies deployed within six months. The playbook was so refined that Sun could close a deal on Friday and have new management in place Monday morning.

The numbers tell the story. Between 2010 and 2020, Sun's portfolio grew from 139 to over 380 communities. Revenue increased from $300 million to over $1.3 billion. Same-community NOI grew at an average annual rate of 5.0%—remarkable consistency for a real estate business. The stock delivered total returns exceeding 15% annually, outperforming both the broader REIT index and the S&P 500.

Yet even as the roll-up machine hummed, cracks were forming. The best properties were getting expensive. Competition from private equity was intensifying. And most importantly, the manufactured housing and RV sectors were becoming picked over. Sun needed new growth avenues. In 2020, management would make its boldest bet yet—entering an entirely new vertical that would either transform the company or nearly destroy it.

VI. The Marina Gamble & Safe Harbor (2020–2025)

September 2020. The world was six months into COVID-19 lockdowns. Traditional real estate sectors—office, retail, hotels—were in freefall. Yet somehow, outdoor recreation was booming. RV sales hit records as Americans sought safe vacation options. Boat sales exploded as people craved outdoor activities. Against this backdrop, Gary Shiffman made the biggest bet of his career: Sun Communities would acquire Safe Harbor Marinas for $2.11 billion, instantly becoming the world's largest owner and operator of marinas. Safe Harbor wasn't just any marina company—it was the largest and most diversified marina owner and operator in the United States, with 101 owned marinas, five managed properties, and a 40,000-member network across 22 states. Founded in 2012 and backed by sophisticated investors including American Infrastructure Funds, Koch Real Estate Investments, and Guggenheim Partners, Safe Harbor had rolled up the fragmented marina industry much like Sun had consolidated manufactured housing.

The strategic rationale seemed compelling. Marinas shared characteristics with Sun's existing businesses: fragmented ownership, stable cash flows from long-term slip rentals, high barriers to entry due to limited waterfront property, and wealthy baby boomer demographics. "Safe Harbor's scale and unique positioning, coupled with the fragmented marina industry, should provide us with incremental channels to drive shareholder value in the coming years," said Gary A. Shiffman, Sun's Chairman and CEO. "This transaction increases our geographic and customer diversity and introduces a new platform that can enhance our ability to generate industry leading returns."

But marinas were fundamentally different from manufactured housing or RV resorts. The customer base was ultra-high-net-worth individuals with yachts worth millions. Operations required specialized knowledge of everything from dredging to fuel systems to maritime regulations. Weather risks—particularly hurricanes—were exponentially higher. And critically, Safe Harbor would operate independently under CEO Baxter Underwood rather than being integrated into Sun's existing operations.

The deal structure reflected both Sun's ambition and the sellers' sophistication. Subject to closing adjustments, the aggregate purchase price for Safe Harbor was approximately $2.11 billion. At the closing, the Company would (i) assume debt in the estimated amount of approximately $808 million, (ii) issue the sellers REIT operating partnership common and preferred OP units in the estimated amount of approximately $130 million, and (iii) pay the balance of the purchase price in cash. The mix of consideration would depend on the amount of common and preferred OP units the sellers elect to receive and other factors.

The timing seemed perfect. COVID had created a boom in outdoor recreation. Boat sales were surging as wealthy Americans sought safe leisure activities. Marina occupancy was at record highs. The acquisition would be immediately accretive to funds from operations. What could go wrong? Everything, as it turned out. By 2024, operational challenges were mounting. Hurricane damage, insurance costs, and maintenance capital requirements far exceeded initial projections. The ultra-wealthy customer base proved demanding and fickle. Integration with Sun's core business never materialized—Safe Harbor remained a standalone operation with its own management, systems, and culture. Most critically, the marina business's capital intensity and weather exposure made it incompatible with REIT dividend requirements.

In February 2025, Sun announced it would sell Safe Harbor to Blackstone Infrastructure for $5.65 billion in an all-cash transaction. The headline number looked fantastic—a $3.5 billion gain in less than five years. Sun's pre-tax cash proceeds after transaction-related costs were approximately $5.25 billion. The base purchase price represented an approximate 21x multiple on Safe Harbor's estimated 2024 FFO, validating the quality of the assets.

But the sale was really an admission of strategic failure. "This transaction allows Sun to focus on our core businesses which operate at high margins and produce durable income streams," said Jeff Blau, Chair of Sun's Capital Allocation Committee, putting the best spin on the reversal. The reality was that Sun had spent five years and enormous management attention on a business that never fit its core competencies.

The financial engineering around the sale proceeds revealed both opportunity and constraint. Sun would use the $5.25 billion to repay approximately $3.3 billion of debt, allocate $1.0 billion into 1031 exchange accounts for potential MH and RV acquisitions, pay a special dividend of $4.00 per share ($520 million total), increase the quarterly dividend by 10.6%, and authorize a $1.0 billion stock buyback program. The debt paydown would generate annualized interest expense savings of approximately $160 million and reduce Sun's weighted average interest rate to approximately 3.5%.

What made the Safe Harbor saga particularly revealing was what it said about Sun's strategic discipline—or lack thereof. The company had correctly identified marinas as an attractive asset class with favorable demographics and limited supply. The execution of the initial acquisition was flawless. Operations under Sun's ownership were competent. Yet none of this mattered because the fundamental thesis was flawed. Marinas weren't manufactured housing or RV resorts with boats. They were a completely different business requiring different skills, capital allocation, and risk management.

The Safe Harbor experience would prove to be a turning point for Sun Communities. It demonstrated that even the best operators could overreach, that diversification for its own sake destroyed value, and that sticking to core competencies wasn't just conservative wisdom—it was essential for survival. As Sun prepared to close the Safe Harbor chapter and return to its roots, another international adventure was already underway, one that would prove equally challenging.

VII. International Expansion: The UK Adventure

March 2022. Brexit uncertainties were fading. UK staycations were booming post-COVID. And Sun Communities was about to make another bold diversification bet, this time across the Atlantic. The acquisition of Park Holidays UK for £950 million (approximately $1.3 billion) would add 40 owned and two managed holiday park properties to Sun's portfolio. It was Sun's first international expansion, entering a market with different regulations, customer expectations, and competitive dynamics. The UK holiday park industry looked deceptively similar to American manufactured housing. Park Holidays UK was the second-largest owner and operator of holiday communities in the UK, with 40 owned and two managed properties primarily located in irreplaceable seaside locations in southern England. The business model seemed familiar: rent sites to owners of static caravans (the UK equivalent of manufactured homes) on annual contracts, sell new units to customers, and provide resort-style amenities.

"We are incredibly excited to expand Sun's footprint into the UK by acquiring Park Holidays, which allows us to leverage our land lease community expertise in a growing market," said Gary Shiffman. "This transaction provides Sun with immediate scale in the UK as well as a platform for future growth in a fragmented landscape." The acquisition would represent approximately 7% of Sun's properties and 8% of its total pro forma real estate asset value.

But the UK market was fundamentally different from the US in ways that weren't immediately apparent. British holiday parks were primarily vacation properties, not primary residences. Occupancy was seasonal—bustling in summer, ghost towns in winter. The regulatory environment was complex, with planning permissions, environmental regulations, and local council oversight far more restrictive than American zoning. Most critically, the customer base had different expectations shaped by decades of British holiday park culture.

The operational challenges emerged quickly. UK consumers expected different amenities—entertainment programs, on-site restaurants and bars, arcade games. Labor laws made staffing more expensive and less flexible. Currency fluctuations added complexity to financial reporting and capital allocation. Weather patterns meant shorter operating seasons than Florida or Arizona properties. And Brexit uncertainties continued to cloud the economic outlook.

Park Holidays' experienced operating team, led by CEO Jeff Sills, remained in place, similar to the Safe Harbor structure. This arm's-length approach preserved local expertise but limited synergies. Sun couldn't apply its American playbooks directly. Best practices from Michigan manufactured housing communities didn't translate to seaside caravan parks in Cornwall. The promised "platform for future growth" remained elusive as integration challenges mounted.

The financial performance was mixed. For the twelve months ended September 30, 2021, Park Holidays had generated £73.9 million in EBITDA. But currency headwinds, inflation, and the cost-of-living crisis in the UK pressured results. The domestic staycation boom that had driven the acquisition thesis began to fade as international travel resumed. Competition from Airbnb and other short-term rental platforms intensified. More troubling were the accounting implications. In 2023, Sun took massive goodwill impairment charges related to Park Holidays. The decline in fair value was driven by "recent uncertainty in the macroeconomic environment in the region, including higher borrowing costs and changing market dynamics, resulting in a decline in projected future cash flows." Translation: the UK expansion wasn't working as planned, and the accounting caught up with reality.

The Park Holidays experience paralleled Safe Harbor in revealing Sun's limitations. International expansion sounded strategic—geographic diversification, new growth markets, currency hedging. But executing across borders with different regulations, cultures, and business practices proved far more challenging than anticipated. The fragmented UK market that seemed ripe for consolidation turned out to be fragmented for good reasons—local preferences, regulatory complexity, and limited economies of scale.

What's particularly striking about the UK adventure is its timing. Sun was simultaneously trying to integrate Safe Harbor's marinas, expand Park Holidays in the UK, and maintain its core US manufactured housing and RV operations. The management bandwidth required to execute three distinct strategies in three different sectors across two continents was enormous. Something had to give.

By 2024, Sun's UK operations were a small contributor to overall results but a large consumer of management attention and capital. The promised "platform for future growth" remained theoretical. Additional UK acquisitions hadn't materialized at attractive prices. The operational synergies with US operations were minimal. Currency headwinds persisted. And most importantly, the UK holiday park business was becoming a distraction from Sun's core challenges in the US market.

The international expansion, like the marina acquisition, revealed a pattern: Sun's success in US manufactured housing had created overconfidence about its ability to operate in adjacent sectors and geographies. The skills that made Sun exceptional at consolidating American trailer parks didn't automatically transfer to British holiday villages. As Sun prepared to navigate its most challenging period—governance controversies and leadership transition—the UK operations would become another complexity in an already complex story.

VIII. The Controversy Years & Leadership Transition (2024–2025)

January 2024 started quietly enough. Sun Communities' stock was trading around $130, down from its 2022 peak but still representing a respectable market cap above $15 billion. Then, on January 30, everything changed. Blue Orca Capital, a short-selling firm known for aggressive corporate takedowns, published a scathing report accusing Sun of self-dealing, governance failures, and accounting manipulation. Within hours, the stock plunged 15%. Within weeks, it would fall below $100. The empire Gary Shiffman had built over five decades was under assault. The Blue Orca report was devastating in its specificity. The headline allegation: CEO Gary Shiffman had taken an undisclosed $4 million loan from the family of Brian Hermelin, who chaired the board's compensation committee. Shiffman allegedly used the loan to buy one of Michigan's most expensive homes—from a Hermelin relative—for $2 million below the last public listing price. Blue Orca also claimed Hermelin was Shiffman's stepcousin, a relationship never disclosed to investors.

"Put simply, undisclosed to investors, the family of a Board member overseeing the CEO's compensation and Company controls has been lending the CEO money to finance the purchase of luxury real estate," the Blue Orca report stated. The short-seller also alleged Shiffman admitted in a deposition to borrowing $700,000 from Arthur Weiss, another board member whose law firm served as Sun's general counsel and had received $27.9 million in legal fees over three years.

Beyond the governance allegations, Blue Orca attacked Sun's financial reporting, claiming the company underreported recurring capital expenditures by as much as 75%, inflating adjusted funds from operations (AFFO) and making the business appear more profitable than reality. They argued Sun's capital spending "defies industry norms and common sense," with other REITs reporting recurring capital expenditures four to eight times higher as a percentage of total spending.

The report also dredged up Sun's past SEC troubles. In 2006, the Securities and Exchange Commission had filed an injunctive action against Shiffman, the CFO, and controller for allegedly manipulating financial statements. While claims against Shiffman and the controller were dismissed, the CFO served a two-year suspension and paid a fine. Blue Orca argued this "history of alleged accounting shenanigans" cast a shadow over current financials.

Sun's initial response was defensive and dismissive. Management called the allegations "misleading" and stood by its financial reporting. But the damage was done. The stock continued sliding as institutional investors questioned whether they could trust management. Governance-focused funds began selling. Short interest spiked. What had been a boring dividend stock became a battleground. On November 6, 2024, just over a month after the Blue Orca report, Sun Communities announced Gary Shiffman would retire in 2025 after over 40 years of service. The company insisted "Mr. Shiffman's retirement is not the result of any disagreement with the Company on any matter relating to its operations, policies or practices." Nobody believed it. The timing was too convenient, the denials too emphatic.

Alongside Shiffman's retirement announcement came a comprehensive restructuring plan expected to save $15-20 million annually. John McLaren, the former COO who'd built Sun's acquisition machine, was returning as President to oversee the turnaround. The board created a CEO Succession Planning Committee led by independent directors Jeff Blau (CEO of Related Companies) and Tonya Allen (President of the McKnight Foundation). Notably, Brian Hermelin—the board member at the center of Blue Orca's allegations—was appointed to the succession committee.

The restructuring acknowledged what critics had been saying: Sun had become bloated and unfocused. "These proposed changes have been planned for throughout the year and we are accelerating the implementation in the context of our disappointing third quarter performance," Shiffman admitted. The company would cut costs, sell non-strategic assets, reduce debt, and refocus on core operations. It was a tacit admission that the empire-building era was over.

The market's reaction was mixed. Some investors saw the leadership change as necessary cleansing. Others worried about losing Shiffman's vision and relationships. The stock stabilized around $140—well below its peak but above the post-Blue Orca lows. Institutional ownership remained stable, suggesting large investors were willing to give new leadership a chance.

What's striking about the controversy and transition is how it exposed the dark side of Sun's success. The same family control and insider relationships that enabled quick decision-making and long-term thinking also created governance failures and conflicts of interest. The operational excellence that drove industry-leading returns masked questionable accounting practices. The aggressive acquisition strategy that built scale also created complexity and distraction.

The Blue Orca report, whether fully accurate or not, forced a reckoning. Sun Communities could no longer operate like a family business masquerading as a public company. The cozy board relationships, the aggressive accounting, the imperial CEO model—all had to change. The question was whether Sun could transform its governance and culture while maintaining operational excellence.

As 2025 began, Sun was in transition. The Safe Harbor sale provided financial flexibility. The restructuring promised operational improvements. New leadership offered fresh perspectives. But challenges remained enormous. The RV business was struggling. The UK operations needed attention. Competition was intensifying. And most critically, Sun had to prove it could generate consistent returns without financial engineering or accounting games. The controversy years had ended an era. What came next would determine whether Sun Communities could survive and thrive without its founder.

IX. Business Model Deep Dive

To understand Sun Communities' future, you must first understand the economic engine that's powered five decades of growth. At its core, Sun operates one of the most elegant business models in real estate: owning the land under homes that cost tens of thousands of dollars to move. It's a modern twist on feudalism—residents own their castles but rent the ground beneath them. And once those castles are placed, they almost never leave.

The numbers tell the story. The average manufactured home costs between $60,000 and $120,000—affordable by almost any standard. But moving that home requires specialized equipment, permits, site preparation, and typically $6,000 to $10,000 in cash. For a family paying $500 monthly lot rent, that moving cost represents 12-20 months of payments. It's cheaper to accept annual rent increases of 3-5% than to relocate. This creates what economists call high switching costs and what Sun executives call "sticky" customers.

The stickiness translates into extraordinary tenant retention. Sun's manufactured housing communities experience less than 1% annual turnover from residents moving their homes. The average resident stays 14 years. Compare that to apartment REITs with 50-60% annual turnover and you understand why Sun's revenue stream is so predictable. It's not quite as stable as a utility, but it's close.

The revenue model is beautifully simple. Sun collects monthly lot rent—typically $400-$700 for manufactured housing sites and $800-$1,500 for RV sites. The company provides basic infrastructure: roads, utilities, common areas. Residents maintain their own homes. This creates operating margins of 60-70% for manufactured housing, among the highest in real estate. Even RV resorts, with more amenities and services, generate 40-50% margins.

But the real magic happens in the capital allocation. Sun targets a 7-9% unlevered return on new acquisitions. With 50% leverage at 4% interest rates, that translates to 10-14% cash-on-cash returns. Layer in 3-4% annual rent growth, 1-2% from occupancy improvements, and another 1-2% from operational efficiencies, and total returns reach the high teens. Do this across hundreds of properties over decades, and you've built a compounding machine.

The home sales business adds another dimension. Through Sun Home Services, the company sells new and used manufactured homes to residents. This isn't predatory—it's solving a market failure. Traditional lenders view manufactured homes as depreciating assets like cars, not appreciating assets like real estate. Interest rates are high, down payments substantial, terms short. Sun steps into this gap, offering financing at competitive rates while earning both sales margins and interest income.

The numbers are compelling: Sun sells 500-1,000 homes annually at average prices of $80,000-$100,000. Gross margins run 20-25%. But the real value isn't the one-time profit—it's filling vacant sites that generate lot rent for decades. Every home sale that fills a vacant site adds $6,000-$8,000 in annual revenue at 70% margins. Capitalize that income stream and you've created $60,000-$80,000 in value from a single transaction.

The RV resort business operates on different dynamics but similar principles. Instead of permanent residents, Sun caters to two customer types: transient guests staying days or weeks, and seasonal visitors—snowbirds—who park their RVs for months. Transient sites command $50-$100 nightly, generating $18,000-$36,000 annually at 60-70% occupancy. Annual sites lease for $8,000-$15,000, providing stable income similar to manufactured housing.

What makes RV resorts particularly attractive is the demographic tailwind. Ten thousand Americans turn 65 every day, and they're the wealthiest generation in history. Many buy $200,000-$500,000 motorhomes and need places to park them. Sun's resorts offer pools, clubhouses, golf courses, marinas—amenities that justify premium pricing. It's not just parking; it's a lifestyle product for affluent retirees.

The development opportunity adds another growth vector. Sun owns thousands of undeveloped sites adjacent to existing properties. Developing a new manufactured housing site costs $15,000-$25,000 and generates $6,000-$8,000 in annual NOI—a 30-40% return on investment. RV sites cost more—$30,000-$50,000—but generate proportionally higher returns. With 8,000+ development sites in inventory, Sun has years of high-return growth without acquiring another property.

But the model has vulnerabilities. First, it's sensitive to interest rates. Not because residents have mortgages—most own their homes outright—but because Sun itself carries substantial debt. At 6x debt-to-EBITDA, every 100 basis point increase in rates costs $30 million annually. Second, the model depends on affordable housing remaining scarce. If traditional housing became cheap, the value proposition erodes. Third, regulatory risk is real. Rent control initiatives regularly appear on state ballots. While most fail, California and New York have enacted restrictions that limit pricing power.

The capital intensity is often misunderstood. While operating margins are high, capital requirements are substantial. Roads need repaving, utilities require updates, amenities demand maintenance. Sun spends $200-$300 per site annually on recurring capital expenditures—2-3% of asset value. That's lower than apartments (3-4%) but higher than industrial or office properties (1-2%). And major infrastructure projects—new water systems, electrical upgrades—can cost millions.

The biggest challenge might be growth. The manufactured housing industry consolidation is largely complete. Sun and Equity LifeStyle control the best properties. Mom-and-pop operators still exist but often own inferior locations. New development is virtually impossible—no municipality wants a new "trailer park." The RV resort sector offers more opportunity, but competition from private equity has driven up prices. International expansion proved challenging. Marina diversification failed.

What remains is operational excellence and financial engineering. Sun must squeeze maximum value from existing properties through rent increases, occupancy improvements, and cost controls. The company must optimize its capital structure, refinancing debt at lower rates and recycling capital from non-core assets. It's less exciting than empire-building but potentially more profitable.

The 20-year average annual same-community NOI growth of 5.0% demonstrates the model's durability. Through recessions, housing booms, and pandemics, Sun has delivered consistent cash flow growth. That's the ultimate test of a business model—not how it performs in perfect conditions, but how it survives and thrives through cycles. Sun's manufactured housing communities aren't glamorous, but they're essential infrastructure for millions of Americans. And that's a business model worth owning.

X. Playbook: Business & Investing Lessons

Every great business story contains lessons that transcend the specific company and industry. Sun Communities' five-decade journey from Michigan trailer parks to international lifestyle property empire offers a masterclass in roll-up economics, REIT management, and the perils of diversification. Here are the key takeaways for operators and investors.

Lesson 1: The Power of Fragmented Industries

Sun's initial opportunity wasn't revolutionary technology or brilliant innovation—it was recognizing that thousands of mom-and-pop operators owned manufactured housing communities with no succession plans, limited access to capital, and substandard operations. The fragmentation created an arbitrage opportunity: buy at 6-8x EBITDA from individual sellers, improve operations to grow EBITDA 20-30%, and own assets worth 10-12x EBITDA in institutional markets.

This playbook works across industries. Whether it's funeral homes, car washes, or veterinary clinics, fragmented industries with aging owners create consolidation opportunities. The key is having better access to capital, superior operations, and patience to integrate acquisitions. Sun spent 30 years rolling up manufactured housing—true value creation takes time.

Lesson 2: REITs as a Structure—Benefits and Constraints

The REIT structure was perfect for Sun's business model. By distributing 90% of taxable income, Sun avoided corporate taxes while attracting income-focused investors who provided patient capital. The regular dividend imposed discipline—management couldn't hoard cash for vanity projects. The public market valuation provided currency for acquisitions.

But REITs also impose constraints. The dividend requirement limits retained earnings for growth. The need for consistent FFO growth encourages financial engineering over operational improvements. The investor base—often retirees seeking yield—may resist necessary investments that temporarily depress dividends. Sun's struggles with Safe Harbor partly stemmed from forcing a capital-intensive business into a REIT structure designed for stable, high-margin properties.

Lesson 3: Building a Roll-Up Machine

Successful consolidation requires more than capital—it demands systems. Sun built proprietary models for evaluating acquisitions, standardized integration playbooks, and centralized operations while maintaining local management. The company could evaluate 100 deals, bid on 20, win 5, and integrate them seamlessly. This machine enabled Sun to acquire 350+ properties without major integration failures.

The lesson: treat acquisitions as a repeatable process, not one-off events. Document everything. Measure integration success. Learn from mistakes. Build teams dedicated to sourcing, evaluating, and integrating deals. Most importantly, walk away from bad deals. Sun's discipline in losing auctions to competitors who overpaid preserved capital for better opportunities.

Lesson 4: The Lifestyle Investment Thesis

Sun recognized early that manufactured housing wasn't just about affordable shelter—it was about community and lifestyle. The company invested in amenities, activities, and community-building that transformed "trailer parks" into desirable neighborhoods. This insight extended to RV resorts and (unsuccessfully) to marinas.

The broader lesson: understand what business you're really in. McDonald's isn't in the hamburger business; it's in the real estate and franchising business. Similarly, Sun isn't in the affordable housing business; it's in the land-lease community business. This distinction drives capital allocation, operational focus, and growth strategy.

Lesson 5: Demographics as Destiny

Sun rode three demographic waves: the affordable housing crisis, baby boomer retirements, and the RV boom. Each provided decades of tailwinds. The company positioned itself where demand would grow regardless of economic cycles. Even during recessions, people needed affordable housing and retirees kept traveling.

For investors, the lesson is to identify long-term demographic trends and position accordingly. Aging populations, urbanization, climate change—these forces will reshape real estate demand for decades. Companies aligned with these trends have structural advantages over those fighting demographic headwinds.

Lesson 6: When to Pivot—The Safe Harbor Sale Decision

Sun's acquisition of Safe Harbor for $2.1 billion and sale for $5.65 billion looks brilliant in hindsight. But the real lesson is recognizing when a strategy isn't working and having the courage to reverse course. Marinas never integrated with Sun's core business. The capital requirements were higher than expected. The operational complexity was overwhelming.

Many companies double down on failed strategies due to sunk cost fallacy or ego. Sun's willingness to exit marinas—even at a substantial gain—showed strategic discipline. The lesson: regularly reassess whether businesses belong in your portfolio. If synergies don't materialize and the business requires different skills or capital, sell it to someone better suited to operate it.

Lesson 7: Family Control in Public Companies

The Shiffman family's control enabled long-term thinking and quick decision-making but also created governance challenges. Related-party transactions, board conflicts, and the Blue Orca allegations all stemmed from mixing family control with public ownership. The lesson: strong governance matters more than strong performance eventually. Independent boards, transparent disclosures, and avoiding conflicts of interest aren't just compliance—they're value preservation.

Lesson 8: Operational Excellence in "Unsexy" Businesses

Manufactured housing carries stigma. RV resorts evoke images of retirees in polyester. These aren't glamorous businesses that attract top talent or media attention. Yet Sun generated exceptional returns by executing brilliantly in these "unsexy" sectors. The company proved that operational excellence matters more than industry attractiveness.

For operators, this means focusing on businesses others ignore due to stigma, complexity, or boredom. For investors, it means looking beyond exciting narratives to find companies with sustainable competitive advantages in mundane industries. The best investments are often hiding in plain sight, dismissed by those seeking the next big thing.

Lesson 9: The Limits of Diversification

Sun's ventures into marinas and UK holiday parks demonstrated that related diversification isn't always successful. Despite surface similarities—land lease models, lifestyle properties, fragmented ownership—each business required different expertise. The company spread itself too thin, lost focus, and destroyed value despite operational competence in each vertical.

The lesson: stick to your core competencies unless diversification brings genuine synergies. Revenue diversification that increases operational complexity often destroys more value than concentration risk. Sun's post-Safe Harbor focus on North American manufactured housing and RV represents a return to core competencies—less exciting but more profitable.

Lesson 10: Capital Allocation is Everything

Ultimately, Sun's story is about capital allocation. Every decision—which properties to buy, how much leverage to employ, whether to develop or acquire, when to sell—shaped returns. The company's best decisions (early MH consolidation, Carefree acquisition) created billions in value. Its worst (UK expansion, aggressive leverage) destroyed hundreds of millions.

For investors, the lesson is that management's capital allocation track record matters more than current earnings or assets. For operators, it's that every capital decision compounds over time. The difference between 8% and 12% returns seems small annually but becomes enormous over decades. Sun's 20-year average annual same-community NOI growth of 5.0% turned a small Michigan operator into a $16 billion REIT. That's the power of consistent execution and intelligent capital allocation.

XI. Analysis & Bear vs. Bull Case

The investment case for Sun Communities in late 2025 presents a fascinating study in contrasts. On one hand, you have a proven business model with decades of consistent cash flow growth, irreplaceable assets, and powerful demographic tailwinds. On the other, you have governance concerns, operational challenges, and questions about growth potential. Let's examine both sides.

The Bull Case: Affordable Housing Crisis Meets Demographic Destiny

The bulls start with an undeniable reality: America faces an affordable housing shortage that's getting worse. The median home price nationally exceeds $400,000, putting traditional homeownership out of reach for millions. Meanwhile, apartment rents in major metros average $2,000+ monthly. Sun's manufactured housing communities offer modern, spacious homes at fraction of these costs. This isn't temporary—housing supply constraints, NIMBY resistance, and construction costs ensure the affordability gap persists for decades.

Demographics provide another tailwind. Every day, 10,000 Americans turn 65. These baby boomers are the wealthiest generation in history, many owning RVs worth more than most people's homes. They need places to park them, communities to join, amenities to enjoy. Sun's RV resorts cater perfectly to this demographic. The trend has decades to run—the last boomers won't turn 65 until 2030.

The business model's resilience is proven. Through the 2008 financial crisis, COVID-19, and multiple recessions, Sun's manufactured housing communities maintained 80%+ occupancy and generated positive same-property NOI growth. The 14-year average residency and <1% move-out rate create recession-resistant cash flows. When economic uncertainty rises, demand for affordable housing increases.

Post-Safe Harbor, Sun's balance sheet is transformed. Net debt-to-EBITDA dropped from 6.0x to approximately 4.0x. The company has $1 billion earmarked for acquisitions, $1 billion authorized for buybacks, and raised the dividend 10.6%. This financial flexibility enables opportunistic capital deployment just as rising rates pressure leveraged competitors.

Valuation looks compelling. At current levels around $140, Sun trades at roughly 17x 2025 estimated FFO—a discount to historical averages and peer multiples. Equity LifeStyle Properties trades at 20x+ FFO despite similar growth rates. If Sun simply returns to its 5-year average multiple of 19x, the stock offers 20%+ upside.

The restructuring under McLaren's leadership should deliver $15-20 million in annual savings—meaningful for a company generating $650 million in annual FFO. More importantly, refocusing on core North American MH and RV operations eliminates distractions. The UK can be fixed or sold. Management can concentrate on blocking and tackling rather than empire building.

The Bear Case: Governance Concerns and Growth Constraints

The bears counter with equally compelling arguments. Start with governance: the Blue Orca allegations may be partially addressed by Shiffman's retirement, but the board remains largely unchanged. Hermelin sits on the CEO search committee despite being central to conflict allegations. Related-party transactions continue. True governance reform requires board refresh, not just CEO change.

The RV business faces structural headwinds. NOI declined 5% in 2024 as post-COVID normalization continued. Young families who bought RVs during lockdowns are selling them. Gas prices and inflation pressure travel budgets. The sector's cyclicality makes it unsuitable for a REIT requiring steady FFO growth. Sun might need to exit RVs like it exited marinas.

Growth potential looks limited. Sun already owns most of the premium manufactured housing communities in America. Equity LifeStyle owns the rest. New development is virtually impossible due to zoning restrictions. The acquisition pipeline is picked over. Organic growth from rent increases faces political pressure as affordable housing becomes a crisis-level issue. Rent control initiatives proliferate.

The UK operations remain problematic. Despite multiple write-downs, Park Holidays struggles with post-Brexit economic challenges, weather seasonality, and cultural misalignment. Further impairments seem likely. International expansion has proven to be a costly distraction that destroyed shareholder value.

Competition intensifies from unexpected sources. Clayton Homes, backed by Berkshire Hathaway's balance sheet, increasingly develops new manufactured housing communities. Private equity firms flush with capital bid aggressively for RV resorts. Even traditional apartment REITs eye manufactured housing as an affordable housing solution. Sun's first-mover advantage erodes.

The accounting concerns raised by Blue Orca haven't been fully addressed. Does Sun understate maintenance capex? Are same-property NOI calculations aggressive? Is FFO quality deteriorating? Until new management provides clearer, more conservative reporting, these questions linger.

Competitive Analysis: David vs. Goliath

Sun's primary competitor, Equity LifeStyle Properties (ELS), offers an instructive comparison. ELS, led by Sam Zell's protégé Marguerite Nader, owns 451 properties with 173,000 sites—similar scale to Sun. But ELS trades at a premium multiple, reflecting superior assets (more California and Florida exposure), better governance (no family control), and cleaner accounting (conservative capex reporting).

ELS's operational metrics are marginally better: 95% occupancy vs. Sun's 93%, 5.5% same-property NOI growth vs. Sun's 5.0%. But the real difference is trust. Investors believe ELS's numbers and management. That trust translates to a lower cost of capital, enabling ELS to win competitive acquisitions. Sun must rebuild credibility to close this valuation gap.

Target Leverage and Financial Analysis

Sun's stated target leverage of 3.5x to 4.5x net debt-to-EBITDA seems appropriate for the asset quality. At 4.0x leverage with a 3.5% weighted average interest rate, the company generates substantial free cash flow after dividends. Each 100 basis point reduction in rates adds $0.30 to annual FFO per share—material upside if the Fed continues cutting.

The current dividend of $4.16 annually represents a 3% yield—reasonable but not exceptional. With a 65% FFO payout ratio, the dividend is well-covered with room for growth. But investors seeking yield have better options in other REITs. Sun is really a total return story requiring NOI growth and multiple expansion.

Valuation: Multiple Scenarios

-

Base Case: Sun delivers 4-5% same-property NOI growth, successfully transitions leadership, and gradually rebuilds trust. The stock re-rates to 18x FFO, implying a $155 price target—10% upside.

-

Bull Case: New leadership drives operational improvements, governance reforms restore confidence, and demographic tailwinds accelerate. Multiple expansion to 20x FFO drives the stock to $175—25% upside.

-

Bear Case: RV weakness persists, UK requires further write-downs, and governance concerns limit multiple expansion. The stock trades at 15x FFO, implying $130—7% downside.

The risk-reward appears balanced but uninspiring. Sun isn't obviously cheap enough to compensate for governance concerns, nor expensive enough to short. It's a "show me" story requiring execution under new leadership.

The CEO Succession Challenge

Everything hinges on the next CEO. Sun needs a leader who can restore credibility, improve governance, drive operational excellence, and identify new growth avenues. The ideal candidate combines REIT experience, public company governance expertise, and manufactured housing knowledge—a rare combination.

Internal candidates like McLaren know the business but may be tainted by association with past practices. External candidates bring fresh perspective but face a steep learning curve in a specialized industry. The board's choice will signal whether Sun truly embraces change or merely rearranges deck chairs.

Final Assessment

Sun Communities represents a classic "fallen angel" opportunity. A good business with strong assets and favorable industry dynamics has been damaged by self-inflicted governance wounds. The question is whether new leadership can restore the company's luster or whether structural challenges prove insurmountable.

For long-term investors, Sun offers exposure to powerful themes—affordable housing, aging demographics, lifestyle properties—at a reasonable valuation. But near-term uncertainty around leadership, strategy, and execution creates volatility. This isn't a "set it and forget it" investment but rather a situation requiring active monitoring.

The bear case isn't catastrophic—Sun won't zero or cut its dividend. But the bull case requires everything going right: successful CEO transition, operational improvements, multiple expansion. The probability-weighted return appears modest. Sun Communities is neither a strong buy nor a clear sell, but rather a hold awaiting clarity on leadership and strategy. Sometimes the best investment decision is patience.

XII. Epilogue & "If We Were CEOs"

The afternoon sun casts long shadows across a Sun Communities property in Florida. Golf carts return from the community center where residents just finished water aerobics. Children play in the pool while their grandparents chat on benches nearby. These scenes play out across 502 properties, touching 174,850 families who call Sun Communities home. Whatever happens to the stock price, whatever governance reforms emerge, this human reality remains: Sun provides affordable housing and community to millions of Americans who have few other options.

If we were taking the CEO reins in 2025, we'd start with a fundamental question: What business is Sun Communities really in? Not manufactured housing, not RV resorts, not marinas or UK holiday parks. Sun is in the business of providing affordable, community-oriented lifestyle properties to America's middle class. Everything else is tactics.

First Priority: Restore Trust Through Radical Transparency

The Blue Orca allegations, whether fully accurate or not, revealed a trust deficit that transcends any specific accusation. Our first act would be commissioning an independent review of all related-party transactions, capital expenditure classifications, and same-property NOI calculations. Publish the findings, acknowledge mistakes, and commit to industry-leading disclosure standards.

We'd reconstitute the board with truly independent directors—no family members, no service providers, no conflicts. Governance isn't just about compliance; it's about earning the market's trust. Every basis point of multiple expansion from improved governance translates to hundreds of millions in market value.

Second Priority: Simplify the Portfolio

Sun has become a conglomerate of related but distinct businesses. We'd establish clear criteria: Does this business generate predictable, growing cash flows? Can we operate it better than competitors? Does it share customers, operations, or economics with our core? If not, sell it.

The UK operations would face immediate scrutiny. Despite sunk costs and pride, if Park Holidays can't generate acceptable returns with reasonable management attention, find a buyer. The proceeds could fund North American acquisitions at better returns with less complexity.

The RV business requires nuanced thinking. The transient RV business is volatile and seasonal—potentially incompatible with REIT requirements. But annual RV sites with snowbird customers resemble manufactured housing economics. We'd consider splitting the portfolio, keeping annual-focused properties and selling transient-heavy resorts to hospitality REITs better equipped to manage volatility.

Third Priority: Operational Excellence Renaissance

John McLaren's return signals renewed operational focus, but we'd go further. Implement zero-based budgeting across all properties. Every expense gets justified annually. Deploy technology aggressively—automated rent collection, predictive maintenance, dynamic pricing algorithms. Sun's scale justifies significant technology investment that mom-and-pop operators can't match.

Create "Sun University" to train property managers in best practices. The quality difference between the best and worst-run properties is enormous. Standardizing excellence across 500+ properties could add 100-200 basis points to NOI growth without acquiring anything.

Fourth Priority: Reimagine Growth

Traditional acquisition opportunities have diminished, but growth avenues exist:

-

Development: Sun owns 8,000+ undeveloped sites. Accelerate development with modular construction techniques and bulk purchasing power. Each developed site adds $60,000-$80,000 in value at minimal risk.

-

Redevelopment: Many older communities have inefficient layouts. Reconfiguring sites, updating infrastructure, and adding amenities can increase income 20-30% with attractive returns on invested capital.

-

Adjacent Services: Sun touches customers at critical life moments—retirement, downsizing, lifestyle changes. Consider adjacent services like insurance, home warranty programs, or broadband/cable provision that leverage customer relationships.

-

Manufactured Housing 2.0: Partner with innovative manufacturers creating modern, energy-efficient homes that challenge traditional housing. Position Sun communities as sustainable, affordable alternatives to conventional suburbs.

Fifth Priority: Capital Allocation Discipline

With $5.25 billion in Safe Harbor proceeds, capital allocation becomes paramount. We'd establish clear hurdle rates: 8% unlevered returns for acquisitions, 15% for development, 20% for redevelopment. If opportunities don't meet these thresholds, return capital to shareholders through dividends and buybacks.

The $1 billion authorized for buybacks should be deployed opportunistically. Below 16x FFO, buy aggressively. Above 20x, become sellers. Let valuation, not emotion, drive capital allocation.

The Technology Opportunity

Sun has underinvested in technology. We'd launch "Project Connect"—a comprehensive digital transformation:

-

Resident Portal: Online rent payment, maintenance requests, community calendars, social features. Increase satisfaction while reducing administrative costs.

-

Property Management System: Real-time dashboards showing occupancy, collections, maintenance backlogs. Enable regional managers to identify and address issues before they become problems.

-

Revenue Management: Dynamic pricing algorithms that optimize rents based on local market conditions, seasonality, and demand. Even 1% improvement in pricing across the portfolio adds $20 million annually.

-

Predictive Analytics: Use data to predict which residents might leave, which sites need maintenance, which markets offer expansion opportunities. Transform from reactive to proactive management.

The ESG Narrative

Environmental, Social, and Governance considerations aren't just buzzwords—they're value drivers. Sun has an incredible ESG story that's poorly told:

-

Environmental: Manufactured homes use fewer materials and less energy than site-built homes. Sun communities preserve open space through density. Solar installations and efficiency upgrades could make communities carbon-neutral.

-

Social: Sun provides affordable housing to teachers, nurses, retirees—essential workers priced out of conventional housing. Every property houses real families building real communities.

-

Governance: Post-reform, Sun could become a governance exemplar, demonstrating that change is possible.

We'd hire a Chief Sustainability Officer reporting directly to the CEO. Publish comprehensive ESG reports. Set ambitious but achievable targets. Link executive compensation to ESG metrics. Make Sun the REIT that institutional investors buy to meet both return and impact objectives.

The Human Element

Behind every site, every property, every financial metric is a human story. We'd launch "Sun Stories"—a campaign highlighting residents whose lives were transformed by affordable housing. The retired teacher who couldn't afford conventional housing but found dignity and community in a Sun property. The young family saving for their children's education while living in quality manufactured housing.

These stories aren't just marketing—they're motivation. Every employee should understand that their work enables these human outcomes. Culture eats strategy for breakfast, and Sun's culture should celebrate its mission of providing affordable community living.

Final Reflections on Gary Shiffman's Legacy

Whatever his governance failures, Gary Shiffman built something remarkable. From 31 Michigan trailer parks to an international lifestyle property empire, his vision and execution transformed an industry. He saw opportunity where others saw stigma. He consolidated a fragmented sector through operational excellence. He created billions in shareholder value while housing millions of Americans.

But empires built on individual brilliance rarely survive their founders. Sun's next chapter requires institutional excellence—systems over personalities, governance over relationships, transparency over opacity. The company must evolve from founder-led to professionally-managed while retaining the entrepreneurial spirit that created its success.

The path forward is clear: restore trust through governance reform, simplify the portfolio to core competencies, drive operational excellence through technology and training, allocate capital with discipline, and tell the powerful story of affordable housing and community. Do these things consistently and Sun Communities can deliver another 30 years of value creation.

The residents in that Florida community don't care about board composition or FFO calculations. They care about safe, affordable homes in communities where they belong. Serve them well, and the stock price will follow. That's the ultimate lesson of Sun Communities: business success comes from solving real problems for real people. Everything else is just keeping score.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube