Seagate Technology: The Physics of Spinning Rust and the Billion-Dollar AI Bet

I. Introduction & Episode Roadmap

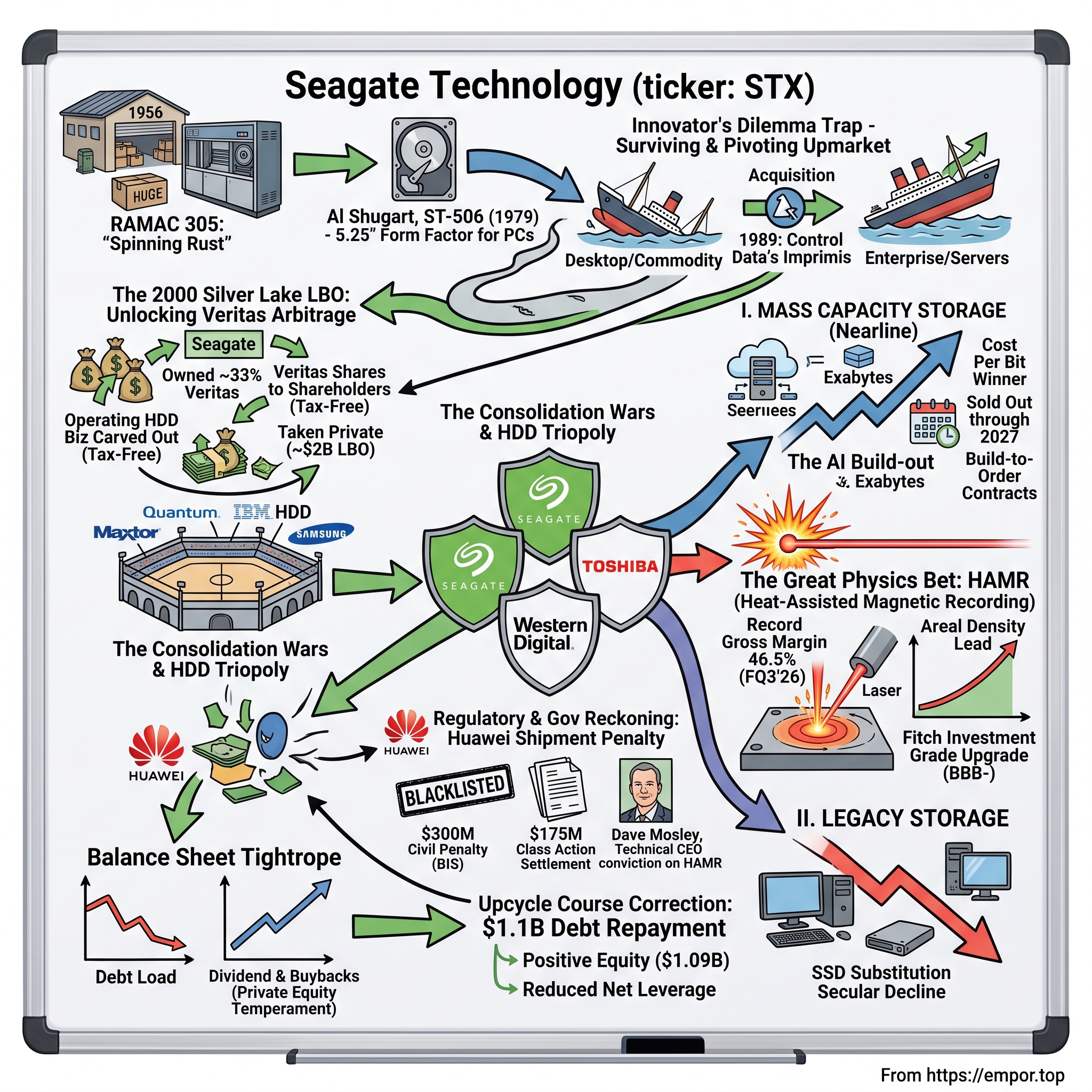

In April 2023, a technology company that most investors had long since filed under "melting ice cube" received a piece of mail that made the front page of the Financial Times. The U.S. Department of Commerce's Bureau of Industry and Security — the agency that polices which American technologies can cross which borders — informed Seagate Technology that it owed the United States government $300 million. The alleged crime: shipping roughly 7.4 million hard disk drives, worth more than $1.1 billion, to 华为 Huawei, the blacklisted Chinese telecommunications giant, after rivals had stopped.39 It was the largest standalone administrative penalty in the agency's history.3

The timing could hardly have been worse. The storage industry was in the middle of the most violent downcycle it had ever endured. Hyperscale cloud customers — the Amazons and Microsofts of the world — had over-ordered drives during the pandemic and were now working through mountains of inventory, ordering almost nothing. Seagate's revenue was collapsing, its balance sheet groaned under roughly $5 billion of debt, and its shareholders' equity had gone negative — an accounting way of saying the company had, over the years, paid out more to shareholders than it had earned and retained. And hovering over all of it was the oldest obituary in computing: the spinning hard disk drive, that whirring relic of magnetic platters and flying heads, was finally dead, strangled at last by the silent, chip-based solid-state drive.

Now fast-forward roughly three years. In its fiscal third quarter of 2026, reported in late April, Seagate posted a gross margin of 46.5% — a level the company had never before reached in its four-decade history — and non-GAAP earnings of $4.10 per share in a single quarter.26 Management told analysts its high-capacity "nearline" drives, the workhorses of the cloud, were essentially sold out through calendar 2027 under build-to-order contracts.6 In March 2026, the credit-rating agency Fitch had restored Seagate to investment grade at 'BBB-', reversing the junk downgrade of the downturn, after the company paid down more than a billion dollars of debt in under a year.7

So here is the question this story tries to answer honestly, without cheerleading: How did a company manufacturing a technology that a generation of engineers had dismissed as a relic of the 1980s survive near-insolvency, a landmark export-control scandal, and the secular threat of substitution — and emerge, at least for now, as an indispensable, high-margin bottleneck in the generative-AI and hyperscale-cloud build-out?

To get there, we need to travel through six distinct chapters. There is the founding era, when disk drives were the textbook case study for how incumbents get destroyed by their own success. There is the legendary 2000 leveraged buyout that helped invent modern technology private equity. There are the consolidation wars, which turned a bloodbath of dozens of manufacturers into a disciplined club of three. There is the physics — the reason SSDs have not, in fact, killed the hard drive in the data center. There is the enormous engineering gamble of heat-assisted magnetic recording. And there is the present: a technical CEO, a regulatory reckoning, and a business model rebuilt around long-term contracts. Let's start where all of it started — with rust.

II. The Origins of "Spinning Rust" & The Early Wild West

Picture a warehouse in San Jose in 1956. Technicians in short-sleeved shirts wheel in a machine the size of two large refrigerators bolted together. Inside spin fifty aluminum platters, each two feet across, coated in a thin film of iron oxide — literally, rust. This was IBM's RAMAC 305, the first commercial hard disk drive. It stored five megabytes of data — not gigabytes, megabytes, roughly one modern smartphone photo — weighed more than a ton, and leased for around $3,200 a month in 1950s dollars. Engineers affectionately, and accurately, came to call the technology "spinning rust," a nickname that has clung to it for seventy years.

The physics that IBM demonstrated that day has never fundamentally changed, and understanding it is the whole ballgame. A hard drive is a record player of almost supernatural precision. A platter coated in magnetic material spins thousands of times per minute. A tiny read/write head, mounted on an arm, floats a few nanometers above the surface — proportionally, if the platter were the size of a football field, the head would fly at the height of a few blades of grass, never once touching down. To write a "1" or a "0," the head flips the magnetic orientation of a microscopic patch of the coating. To read it back, it senses that orientation. Everything that follows in this story — every margin point, every technology war, every physics gamble — is a variation on one question: how many of those magnetic patches can you cram into a square inch before they become unstable?

The modern company enters the story in 1979. Al Shugart was a restless, charismatic industry veteran who had already helped invent the floppy disk at Shugart Associates before being pushed out of his own namesake firm. Together with Finis Conner and a small band of engineers — Tom Mitchell, Doug Mahon, and Syed Iftikar among them — he founded Seagate Technology in Scotts Valley, California. Their bet was on form factor. Mainframe drives of the era were fourteen-inch monsters. Seagate's breakthrough product, the ST-506, was a 5.25-inch drive that stored five megabytes and, crucially, fit inside the new desktop personal computers that IBM and its clones were about to sell by the millions. By shrinking the drive to fit the PC, Seagate hitched itself to the single greatest volume ramp in the history of electronics.

Here is where the story becomes a business-school parable. Clayton Christensen's landmark book The Innovator's Dilemma was, quite literally, built on the disk-drive industry of exactly this period. Christensen documented a brutal, repeating pattern. A dominant maker of, say, eight-inch drives would be serving its best, most demanding customers with ever-better eight-inch drives — and would rationally ignore the crummy, low-capacity 5.25-inch newcomer, because it wasn't good enough for those customers yet. Then the smaller drive would find a new market (the desktop), improve rapidly, and sweep upward to eat the incumbent alive. It happened at fourteen inches, then eight, then 5.25, then 3.5. The graveyard filled with names — Miniscribe, Micropolis, Priam, Kalok — companies that did everything their existing customers asked and died anyway.

Seagate survived not by avoiding this trap but by repeatedly, painfully, jumping across it. When desktop drives became a low-margin knife fight, the company pivoted upmarket into the far more lucrative world of enterprise servers and workstations. The pivotal move was the 1989 acquisition of Control Data Corporation's Imprimis disk-drive division, which handed Seagate the high-end technology it lacked — the voice-coil actuators that positioned heads with fine precision, and the SCSI interfaces that connected drives to servers. That deal transformed Seagate from a commodity desktop supplier into a genuine enterprise player, and it planted the DNA that still defines the company: when the low end commoditizes, climb toward capacity and performance, where the money is. That instinct would be tested almost immediately by a stock market that had lost its mind.

III. The 2000 Silver Lake LBO: Unlocking the Veritas Arbitrage

By late 1999, Seagate's management was living inside one of the strangest valuation puzzles the public markets have ever produced. It was the height of the dot-com bubble, and the market had developed an insatiable appetite for anything with the word "software" attached and a deep contempt for anything that involved factories and physical inventory. Seagate had both problems and, oddly, both opportunities.

Years earlier, Seagate had sold its software operations, and through a series of transactions it ended up owning roughly a third of Veritas Software, a hot enterprise-storage-software company whose shares were levitating along with the rest of the bubble.12 The arithmetic became surreal. The market value of Seagate's stake in Veritas grew to exceed the entire market capitalization of Seagate itself. Read that again. If you bought all of Seagate's stock, you would get the Veritas stake — worth more than what you paid — and the world's largest disk-drive manufacturer would be, in effect, thrown in for free. Worse than free: the market was implicitly valuing Seagate's profitable, cash-generating core drive business at something like negative $1.5 billion. Investors were so bubble-drunk on software that they were assigning a real, operating industrial business a value below zero.

For Seagate's CEO Stephen Luczo, this was intolerable and irresistible. A former Bear Stearns banker turned technology executive, Luczo had the rare combination of financial imagination and operating credibility to see the trapped value and figure out how to spring it. The obstacle was tax. Simply selling the Veritas shares would trigger an enormous corporate capital-gains bill, vaporizing much of the arbitrage. The solution, hammered out with a young private-equity firm called Silver Lake Partners — led by Glenn Hutchins, Roger McNamee, and their partners — together with the buyout giant TPG, was a piece of financial engineering elegant enough to be taught for decades.12

The transaction, structured through 2000 and completed that November, worked in two linked moves. First, Seagate's Veritas shares were folded back into Veritas Software itself in a stock-for-stock merger, structured to be tax-free to Seagate's shareholders, who received Veritas stock directly. Second, the operating disk-drive business — the factories, the patents, the people — was carved out and taken private by Silver Lake, TPG, and Seagate's own management in a leveraged buyout valued at roughly $2 billion. The public shell dissolved; the industrial company disappeared into private hands.

This mattered far beyond Seagate. It was, in many tellings, the first true mega-buyout of a technology company, and it helped write the playbook for an entire industry. The prevailing wisdom had been that technology firms were un-buyoutable: too volatile, too dependent on fickle innovation, too light on the hard assets that lenders liked as collateral. Silver Lake's entire founding thesis was that maturing technology companies could, in fact, be run like classic private-equity targets — for cash flow and operational discipline rather than for growth at any cost. Seagate was the proof of concept.

Inside the private-equity cocoon, away from the quarterly earnings theater, Seagate got a hard scrubbing. Management stripped non-core assets, sharpened R&D toward the products that actually earned their keep, and — most importantly — converted the company's operating religion from "market share at all costs" to "cash flow first." The business was re-engineered for high operating leverage: keep fixed costs disciplined so that when the cycle turned up, profits would explode. In 2002, Seagate returned to the public markets through an IPO, and its private-equity sponsors exited with large multiples on their money. What they left behind on the public tape was not the old Seagate. It was a leaner, cash-obsessed machine with a capital-allocation temperament — return cash aggressively, run lean, treat the balance sheet as a tool — that would define, and occasionally endanger, the company for the next quarter-century. That temperament was about to meet an industry still busy destroying itself.

IV. The Consolidation Wars and the HDD Triopoly

For most of its history, the hard-drive business was a case study in how not to make money in a growing market. Demand for storage rose relentlessly, decade after decade, and yet the companies making the storage frequently lost their shirts. The reason was structural, and it is worth sitting with, because escaping it is the single most important thing that ever happened to Seagate's economics.

Through the 1990s and into the 2000s, the industry was a crowded, bloody arena. Maxtor, Quantum, Fujitsu, Samsung, Western Digital, IBM's drive division, Hitachi, Conner Peripherals — a dozen serious players slugging it out. Every eighteen months, someone would bring a new, higher-capacity generation to market, everyone would race to match it, factories would run flat out, supply would overshoot demand, and prices would collapse. The gains from Moore's-law-like density improvements flowed almost entirely to customers, not manufacturers. Capital poured into fabs and cleanrooms was routinely incinerated by the next glut. It was, in the language of game theory, a decades-long exercise in mutually assured destruction, where any player's attempt to earn a decent return was punished by a rival willing to cut price for share.

The escape came through consolidation, and it played out in a decisive sequence. In 2005 Seagate agreed to acquire Maxtor, a chronic price-cutter and the number-three player, in a stock deal valued at roughly $1.9 billion, closing in 2006.11 The integration was rocky, and Seagate arguably overpaid relative to the near-term cash flows of Maxtor's low-end desktop franchise, which was already fading — the deal produced write-downs and indigestion. But strategically it did something valuable: it removed one of the industry's most reckless discounters from the board. Sometimes in a commodity business you are not buying assets; you are buying the retirement of a competitor's willingness to fight on price.

The endgame arrived in 2011 and 2012, in a remarkable near-simultaneous reshuffling. In late 2011, Seagate agreed to acquire Samsung's hard-drive operations for about $1.375 billion, in a cash-and-stock arrangement that also knitted the two firms together as component partners.13 At almost the same moment, Western Digital acquired Hitachi Global Storage Technologies — itself the descendant of IBM's storied drive business — a deal that closed in March 2012.[^16] When the smoke cleared, an industry that had once held dozens of manufacturers had collapsed into just three: Seagate, Western Digital, and Toshiba.

That number — three — changed everything about the economics. A triopoly behaves nothing like a free-for-all. With only three rational actors, the incentive to torch prices for a point of share evaporates, because everyone understands that a price war has no winners and three losers. The industry's culture shifted, in the language management teams now use, from share-grabbing to "rational capacity management": you add manufacturing capacity cautiously, in line with visible demand, rather than building ahead and praying. Just as importantly, the survivors' attention swung away from the shrinking, commoditized world of PC drives and toward a new and voracious customer — the cloud. The great data-center build-out was beginning, and it would need somewhere to put the exabytes. Which brings us to the two very different businesses that live inside Seagate today.

V. The Mass Capacity Engine vs. The Legacy Decline

If you want to understand Seagate as an investment rather than as a piece of nostalgia, you have to stop thinking of it as "a hard-drive company" and start seeing it as two businesses stapled together — one ascending, one in managed decline — and appreciate why the ascending one is so unusually good.

The first business is what Seagate calls Mass Capacity Storage. These are the high-capacity "nearline" drives — big, dense 3.5-inch units that live by the thousands in the racks of hyperscale data centers run by Amazon Web Services, Microsoft Azure, Google Cloud, and Meta, plus the broader universe of enterprise and specialized-cloud customers. "Nearline" is an old industry term for storage that sits between the blazing-fast, expensive stuff your application touches constantly and the deep-freeze tape archives you almost never read — data you want reasonably available but don't need in a millisecond. This is where the world's photos, videos, backups, database archives, and increasingly its AI training corpora physically reside. By fiscal 2026, mass capacity had grown to roughly 88–89% of Seagate's hard-drive revenue — the overwhelming bulk of the company.

The second business is Legacy Storage: the 2.5-inch and 3.5-inch drives that go into desktop PCs, notebooks, gaming consoles, and the external backup drives you buy at a retail store. This is the old empire, and it is in secular retreat — perhaps 11–12% of revenue and shrinking — because for a laptop or a PlayStation, the customer genuinely is better served by a solid-state drive. It is quieter, faster, and more rugged, and at the modest capacities a consumer needs, the price premium is bearable. On the client side, the SSD obituary for the hard drive is essentially correct.

So why hasn't that same substitution swept through the data center and killed the mass-capacity business too? This is the crux, and the answer is not sentiment or inertia — it is arithmetic. An SSD stores data in NAND flash chips; a hard drive stores it on spinning magnetic platters. Manufacturing a terabyte of NAND flash requires vastly more expensive semiconductor fabrication than coating a terabyte onto a magnetic platter. As of 2026, the price-per-terabyte gap between a nearline hard drive and an enterprise SSD remained stubbornly wide — on the order of five to seven times. For a hyperscaler that is not storing a few terabytes but storing exabytes — millions of terabytes — of warm and cold data, ripping out hard drives and replacing them with flash would inflate the storage bill by a factor that no chief financial officer would survive proposing. The consequence is that hard drives still hold the large majority of the bytes sitting in public-cloud data centers. The hard drive did not beat flash on speed; it beat flash on the only axis that matters at exabyte scale — cost per bit.

But before we crown Seagate, look at the other side of the table, because it complicates the moat. Seagate and Western Digital enjoy a cozy supply structure — but they sell into an extraordinarily concentrated set of buyers. A handful of hyperscalers — Amazon, Microsoft, Google, and Meta in the U.S., plus 阿里巴巴 Alibaba, 腾讯 Tencent, and 百度 Baidu in China — account for an enormous share of nearline demand. That is an oligopsony facing an oligopoly: a few giant sellers, a few giant buyers. Historically, those buyers used their volume as a club, squeezing Seagate's and Western Digital's margins mercilessly during downcycles, when the manufacturers were desperate to fill factories. The pricing power runs in both directions, and which side holds the whip depends heavily on where you are in the cycle. Keep that tension in mind, because Seagate's entire recent strategy — long-term contracts, build-to-order — is an attempt to tilt that balance. The other thing tilting it is a physics bet that Western Digital chose not to make.

VI. The Great Physics Bet: HAMR vs. MAMR

Every hard drive engineer lives in fear of the same three-syllable phrase: the superparamagnetic limit. To understand the defining technology gamble of modern Seagate, you have to understand this ghost, and it is worth slowing down because everything expensive and clever the company has done in the last decade descends from it.

Recall that writing data means flipping the magnetic orientation of a tiny patch of the platter's coating. To store more data per platter, you make each patch smaller, so you can fit more of them into a square inch — what engineers call areal density. But there is a catch buried in physics. As you shrink a magnetic patch, it holds less energy, and eventually it becomes so small that the ordinary thermal jostling of atoms at room temperature can spontaneously flip it — turning a stored 1 into a 0 with no one touching it. Your data rots on its own. By the late 2010s, the conventional recording technology of the era, Perpendicular Magnetic Recording, was slamming into this ceiling at roughly two terabytes per platter. Pack the bits any tighter with that method and they became unstable. The industry had run out of road on the old highway.

There were two ways forward, and this is where Seagate and Western Digital consciously diverged. The physics offered a devilish trade-off: you can defeat spontaneous bit-flipping by using a more magnetically "stubborn" material for the coating — one that holds its orientation tenaciously — but that same stubbornness makes the bits extremely hard to write in the first place. So both companies needed some way to momentarily make a hard-to-write material easy to write.

Western Digital chose the cautious road. It leaned on energy-assisted PMR and Microwave-Assisted Magnetic Recording, or MAMR, which uses a tiny microwave-generating structure on the head to nudge the magnetic material and ease the write. It was evolutionary, lower-risk, and it let Western Digital scale capacities into the low-to-mid twenties of terabytes per drive. But MAMR carries its own hard ceiling not far beyond, in the neighborhood of the low thirties of terabytes, and then it too runs out of road.

Seagate, under CEO Dave Mosley, chose the moonshot: Heat-Assisted Magnetic Recording, or HAMR. And when you understand what HAMR actually does, "moonshot" starts to sound like an understatement. Seagate's engineers built platters from an iron-platinum alloy so magnetically stubborn that it essentially cannot be written to at ordinary temperature. To write a single bit, the recording head carries a minuscule laser — a plasmonic device that focuses light to a spot smaller than the wavelength of the light itself — which heats a tiny point on the spinning disk to roughly 450 degrees Celsius in well under a nanosecond. In that instant of heat, the material becomes writable; the head flips the bit; and then the spot cools back to room temperature almost immediately, locking the data into that stubborn, thermally stable alloy. All of this happens while the head flies nanometers above a platter spinning thousands of times per minute. The engineering tolerances are savage: if the laser is too weak, the write fails and you lose data; if it is too hot, you cook the microscopic film of lubricant that keeps the head from crashing into the disk. Seagate spent the better part of two decades and, by most accounts, billions of dollars getting this to work reliably at manufacturing scale — a gestation so long that skeptics inside and outside the industry openly doubted it would ever ship in volume.

In January 2024, it shipped. Seagate launched its commercial HAMR platform under the brand Mozaic 3+, achieving more than three terabytes per platter and enabling drives of 30 terabytes and up for cloud customers.4 The "3" refers to that 3TB-per-platter density; the "+" is the promise of a roadmap climbing toward four, five, and beyond.

Now, why does this obscure materials-science victory show up so dramatically in the financial statements? Because of a beautiful piece of unit economics. A hard drive's cost is driven heavily by how many platters and how many read/write heads it contains — those are the expensive, precisely manufactured parts, and each one must be assembled and tested in a cleanroom. If you can store more terabytes on each platter, you need fewer platters and fewer heads to build a drive of a given capacity. A 30-terabyte HAMR drive can be built with fewer platters than a 24-terabyte drive using the older technology — which means less material, less assembly labor, and less cleanroom time per terabyte sold. Higher areal density is not just a capacity story; it is a cost story. That is the mechanism beneath Seagate's record 46.5% gross margin in early 2026 — the company was, for the first time, selling drives whose capacity had jumped while their bill of materials had barely moved.26

A neutral observer should add two cautions here, because the bull case for HAMR is also its bear case. First, HAMR's margin advantage is real only so long as the drives are reliable in the field over many years; a laser that degrades or a lubricant that fails at scale would turn the density advantage into a warranty catastrophe. Second, the advantage is a lead, not a monopoly — Western Digital and Toshiba are working on their own HAMR roadmaps, and a fast-follower could compress the gap. For now, though, Seagate is shipping volume HAMR while its rivals are not, and that head start is the difference between the company's two possible futures. That future, however, has to be underwritten by a management team whose credibility is genuinely contested.

VII. The Huawei Settlement, Class Actions, and Management Credibility

To assess whether you can trust Seagate's numbers and its strategy, you have to assess the man who runs it, and Dave Mosley is a genuinely unusual chief executive — impressive and problematic in roughly equal measure, which is exactly why his tenure deserves scrutiny rather than applause.

Mosley is not a finance executive parachuted in to run a mature cash machine. He is a physicist. He holds a Ph.D. in physics from the University of California, Davis, and he joined Seagate in 1995 as a senior scientist, working his way up through the deeply technical guts of the business — recording heads, media, manufacturing operations — before becoming CEO in October 2017. For a company whose survival was about to hinge on whether it could heat a spot of iron-platinum to 450 degrees in a nanosecond a trillion times without failure, having a CEO who could actually follow the engineering arguments in the room was not a luxury. It was arguably decisive. When the 2022–2023 downturn tempted every instinct to slash R&D and protect the quarter, Mosley kept funding HAMR. A finance-first CEO might not have had the conviction, or the technical literacy, to hold that line.

But the same appetite for calculated risk that protected HAMR also produced the ugliest chapter in the company's modern history. In 2020, as the U.S.-China technology conflict escalated, the U.S. government tightened the Foreign Direct Product rule, an export-control mechanism that extends American jurisdiction to certain foreign-made goods produced using U.S.-origin technology or software. The tightened rule was aimed squarely at Huawei, and it effectively barred shipping many products, including hard drives made with U.S.-derived technology, to the Chinese firm without a license. Western Digital and Toshiba read the rule, saw the risk, and halted their shipments to Huawei.

Seagate did not. According to the Commerce Department's findings, Seagate's management took an aggressive legal interpretation — reasoning that because its drives were manufactured outside the United States and its production equipment was not itself a direct product of specific U.S. software or technology, the rule did not reach its products.35 With its two rivals gone, Seagate became Huawei's sole hard-drive supplier and, over roughly a year, shipped more than 7.4 million drives worth over $1.1 billion.310 It was, in the coldest commercial terms, a chance to capture a rival-free market. It was also a bet against the most powerful export regulator on earth.

The bet lost. In April 2023, the Bureau of Industry and Security announced a $300 million civil penalty against Seagate — the largest standalone administrative penalty in BIS history — to be paid in $15 million quarterly installments over five years, alongside audit requirements and a suspended denial of export privileges.359 For a company already reeling from the cyclical downturn, the penalty landed like a second recession stacked on the first.

The pain did not stop with the government. Shareholders, arguing that Seagate had made misleading statements about its export-compliance posture even as it kept shipping to Huawei, filed a securities class action. In June 2026, Seagate agreed to a preliminary $175 million settlement to resolve that litigation.8 Add the two figures together and the Huawei episode cost shareholders on the order of $475 million in direct penalties and settlements, quite apart from the reputational damage and the management distraction. Seagate did not admit wrongdoing in settling the class action, and the settlement removed a significant litigation overhang — but a neutral reading is unambiguous: this was self-inflicted, it was expensive, and it flowed directly from a risk-taking culture at the top.

So how should an investor weigh Mosley's record, on balance? The honest verdict is that it is genuinely mixed, and anyone who tells you it is all triumph or all scandal is selling something. On the debit side: an appetite for regulatory brinkmanship that vaporized the better part of half a billion dollars and dented the company's credibility on disclosure — a real governance concern, not a footnote. On the credit side: an unusual strategic steadiness. Through the deepest trough in the industry's history, Mosley defended the HAMR budget, restructured manufacturing capacity, cut roughly 8% of the workforce to right-size costs, and shepherded the company onto the high-margin Mozaic platform on a timeline that skeptics doubted. The market's grudging respect is earned, but it should be respect with its eyes open. And the clearest test of whether the discipline is real, rather than rhetorical, is what the company did next with its dangerously stretched balance sheet.

VIII. The Balance Sheet Tightrope: Debt, Dividends, and the Investment-Grade Upgrade

Every company inherits a temperament, and Seagate inherited its from that 2000 buyout — a private-equity conviction that idle equity is lazy equity, that cash should be pushed out to owners and the balance sheet run hot. For more than a decade this served shareholders handsomely, and then it very nearly served them a disaster.

The playbook was straightforward and, in good years, wonderful. Seagate historically returned the large majority of its free cash flow to shareholders — routinely more than three-quarters of it — through a fat dividend that often yielded north of 4% and through aggressive, relentless share buybacks. Buybacks shrink the share count, so each remaining share owns a bigger slice of the earnings; done at sensible prices in a cash-rich business, they are a powerful engine of per-share value. The trouble is what happens when you buy back stock year after year for amounts that exceed your cumulative net income. On the accounting statements, sustained buybacks in excess of retained earnings drive shareholders' equity down and, eventually, negative. Seagate operated for years with an accumulated deficit and negative book equity — reaching a deficit reported around negative $453 million as of mid-2025.1

Negative equity is not, by itself, a death sentence; it is a signal. It says a company has chosen to fund itself heavily with debt and to return capital rather than hoard it, and it means there is very little cushion to absorb a shock. When the 2022–2023 downcycle hit, that thin cushion turned into a genuine scare. Revenue and cash flow cratered, the roughly $5 billion debt load suddenly looked enormous against shrunken earnings, and the rating agencies moved. Seagate was downgraded into junk territory, at 'BB+', which raises borrowing costs and narrows the pool of investors permitted to hold your bonds. For a company built on a leveraged model, a downgrade in a downturn is the moment the whole design is stress-tested.

To management's credit — and this is the behavior that matters more than any press release — the response was a genuine course correction rather than a doubling-down. As the storage cycle turned violently upward in fiscal 2026, Seagate pointed the torrent of cash at the balance sheet instead of back at shareholders. The upcycle threw off enormous free cash flow — on the order of $953 million in the fiscal third quarter of 2026 alone — and the company used it to retire roughly $1.1 billion of gross debt across fiscal 2026, bringing total debt down toward the high-three-billion range, around $3.86 billion.26

The external validation followed. In March 2026, Fitch upgraded Seagate's long-term issuer default rating to 'BBB-', restoring the company to investment grade and explicitly citing the balance-sheet repair and improved leverage.7 And the accounting scar healed: shareholders' equity swung back to positive territory, reported at roughly $1.09 billion by late April 2026, erasing one of the loudest lines in the bear thesis.2

The analytical takeaway is not simply "Seagate fixed its balance sheet." It is that management, having promised discipline, actually delivered it when the cash arrived — choosing deleveraging over the buybacks its own DNA would have preferred. That is a meaningful data point on credibility, and it partially offsets the Huawei black mark. But the skeptic's question writes itself, and it is the right one to hold onto: now that the company is investment grade again and minting cash, will the old private-equity temperament reassert itself and push capital back out to shareholders at the first opportunity — or has the near-death experience genuinely changed the institution? That question is exactly why leverage remains one of the metrics worth watching, and it sets up the deeper strategic question of how durable this whole edifice really is.

IX. Strategic Frameworks: Hamilton Helmer's 7 Powers & Porter's 5 Forces

Strip away the drama — the fine, the laser, the debt scare — and ask the cold structural question a long-term investor actually cares about: is Seagate's advantage real and durable, or is it a cyclical mirage dressed up as a moat? Two classic frameworks help pressure-test the answer, and the honest conclusion is that some of the moat is genuinely deep and some of it is shallower than the bulls suggest.

Start with Hamilton Helmer's 7 Powers, which asks what specifically prevents a competitor from eroding your returns. Seagate has a strong claim to at least three of the seven. The first is scale economies. Building the specialized facilities that fabricate magnetic recording heads and media is a multi-billion-dollar undertaking, and the cost per drive falls dramatically with volume. A hypothetical new entrant would have to sink billions into capacity and then somehow win enough volume to reach competitive unit costs — while the incumbents, already at scale, price below the newcomer's costs. The math simply does not close for a challenger. The second, and arguably the deepest, is a cornered resource in the form of intellectual property. Decades of patents blanket HAMR, the glass and alloy substrates, the plasmonic write heads, and the manufacturing processes. A newcomer cannot simply buy the ability to make a competitive nearline drive; the knowledge and the legal right to practice it are locked up inside two companies. The third is switching costs, which are real but more moderate. Hyperscale storage systems are tuned to specific drive firmware, to particular commands for technologies like Shingled Magnetic Recording, and to precise power and thermal profiles; re-qualifying a data center's storage on a different vendor's drives is a serious engineering project, which gives incumbents stickiness — though large buyers deliberately maintain dual sources to preserve their own leverage, which caps how much that stickiness is worth.

Now run Porter's Five Forces, which maps the balance of power around the business, and the picture sharpens further — including its weak points. The threat of new entrants is, for the reasons above, close to zero; this is a closed club of three with insurmountable capital and IP barriers. Competitive rivalry is disciplined rather than destructive: in the mass-capacity nearline market that actually matters, the contest is effectively a duopoly between Seagate and Western Digital, with Toshiba a smaller third presence, and all three have learned the hard lessons of the price-war era. Those two forces are the strong walls of the fortress.

The other three forces are where a skeptic should focus. The bargaining power of buyers is high and structural — the handful of hyperscalers command enough volume to hurt. Seagate's countermeasure is the most important strategic shift of this cycle: moving customers onto build-to-order contracts and long-term agreements that lock in both capacity and pricing out toward 2027.6 This is a deliberate attempt to convert a volatile spot market, where buyers squeeze during gluts, into a contracted book that smooths pricing and demand. It is working now, in a tight market — but it is worth remembering that contracts are easiest to sign when buyers are desperate for supply; their durability through the next glut is unproven. The threat of substitutes — enterprise SSDs — is medium-to-high and permanent. As long as HAMR keeps pushing hard-drive density and cost-per-terabyte down the curve, the five-to-seven-times cost gap holds and flash stays penned into the applications where speed justifies the premium. But that gap is a moving target, and it is defended by continuous execution, not by a law of nature. Finally, the power of suppliers is modest but not nil, given specialized inputs like the laser diodes and glass substrates that make HAMR possible.

The synthesis: Seagate sits behind a genuinely formidable barrier to entry and inside a rational oligopoly — those are durable. But it faces powerful concentrated customers and a permanent, capable substitute — those require it to keep running. The moat is real; it is just not the kind you can stop maintaining. Which is precisely why the specific lessons of this history are worth extracting before we weigh the two futures.

X. Playbook & Investing Lessons

Step back from Seagate the ticker and look at Seagate the case study, because this forty-seven-year saga distills into a handful of durable lessons that travel well beyond hard drives.

The magic of consolidation. The single most important thing that ever happened to Seagate's economics was not a product; it was the disappearance of its competitors. For decades, a growing market delivered miserable returns because a crowded field competed the profits away as fast as technology created them. The same technology, sold into the same growing demand by only three disciplined players, produces record margins. The lesson for investors is that industry structure often matters more than industry growth. A brutal commodity business can become a genuinely good business the moment it consolidates into a rational oligopoly — and the transition point, when the last mergers close, is frequently the most rewarding and most underappreciated moment to be paying attention.

The technical-CEO premium. When a company's survival hinges on a hard materials-science transition, leadership fluency in the actual science can be the difference between execution and obsolescence. Mosley's willingness to fund HAMR through the depths of a downturn — a bet a finance-first executive might have lacked the conviction or the literacy to protect — is the clearest example. The caveat, which the Huawei episode supplies, is that the very risk-appetite that makes a founder-engineer defend a moonshot can also make them dangerous when pointed at regulators. Technical brilliance is not the same thing as judgment, and investors should price both.

The danger of regulatory arbitrage. In an era of intensifying technological conflict between the United States and China, export controls are not paperwork; they are live rails. Seagate's decision to read the Foreign Direct Product rule aggressively and keep shipping to Huawei after its rivals stopped was a calculated grab for a rival-free market — and it cost roughly $475 million in penalties and settlements plus a lasting credibility dent. When two competitors interpret the same rule conservatively and one interprets it aggressively, the aggressive one is not being clever; it is being the test case. That is a general warning for any company tempted to treat a gray-zone regulation as an opportunity.

Capital structure as both weapon and liability. Seagate's private-equity DNA — high leverage, aggressive returns, negative book equity — was a magnificent amplifier on the way up and a genuine threat to solvency on the way down. The same balance sheet that juiced per-share returns in good years pushed the company toward a credit crisis in bad ones and forced a painful, cash-consuming restructuring. Leverage does not create value or destroy it by itself; it magnifies whatever the operating business is already doing, in both directions. For a company as cyclical as this one, that magnification is the whole risk. With those lessons in hand, we can finally frame the two competing versions of Seagate's future.

XI. The Investment-Story Spine: Bull vs. Bear Case

Every stock is an argument between two stories, and with Seagate the two stories are unusually clean — a bull case that is essentially "structural demand meets a widening technology lead" and a bear case that is essentially "it's still a commodity cycle, and the cycle always turns." Before laying them out, it helps to fix on the small number of metrics that will actually adjudicate the debate over time.

There are, realistically, three KPIs that matter most. The first is mass-capacity gross margin, because it is the single clearest readout of whether HAMR's density advantage is truly converting into structurally lower manufacturing cost — or whether the current margin is just the flattering peak of a tight cycle. The second is average capacity per drive shipped, measured in terabytes, because it tracks how quickly customers are actually adopting 30-terabyte-plus HAMR drives over older models — the real-world velocity of the technology transition, as opposed to the press-release version. The third is net debt-to-EBITDA leverage, because it reveals, quarter by quarter, whether management is holding to its newly won investment-grade discipline or quietly reverting to the aggressive capital-return temperament in its DNA. These three — cost advantage, adoption, and discipline — are the dials to watch, and readers should track them directly rather than take any single quarter's headline at face value.

The bull case. Start with technology. If Seagate's Mozaic HAMR platform sustains a real areal-density lead over Western Digital — shipping higher-capacity drives at lower cost per terabyte generation after generation — then the recent 40%-plus gross margins are not a cyclical fluke but a new structural floor, defended by a lead that compounds as the roadmap climbs past three terabytes per platter toward four and five.26 Layer on demand: the generative-AI build-out is fundamentally a demand for data at rest — enormous, cheap data lakes to train models, plus the exploding volume of AI-generated content that has to be stored somewhere economical. That is nearline hard-drive demand, and the bull argues it runs for a decade. Finally, add visibility: the build-to-order contracts and long-term agreements that lock capacity and pricing toward 2027 promise to tame the vicious storage cycle that has always made this business un-ownable for conservative investors, turning a boom-bust commodity into something closer to a contracted industrial franchise.

The bear case. Each bull pillar has a mirror. The most serious threat is a NAND cost collapse: if a genuine manufacturing breakthrough in 3D NAND flash sharply narrows the cost-per-terabyte gap, enterprise SSDs could become viable for warm and even cold storage, and the hyperscalers — who would love to standardize on all-flash for its speed and density — would migrate fast, cannibalizing nearline hard drives. The five-to-seven-times gap is a lead, not a moat carved in stone, and it has narrowed before. The second is HAMR reliability: this is bleeding-edge physics running at scale, and if the lasers degrade or the glass substrates fail at higher-than-expected rates in the field, Seagate faces not just warranty costs but the far more damaging loss of hyperscaler trust — and in a duopoly, a customer who loses confidence has exactly one place to go. The third is the oldest one of all — hyperscaler capex digestion. If the AI investment wave crests and the cloud giants pause to absorb what they have bought, or if the broader AI narrative deflates, drive orders can evaporate almost overnight, as they did in 2022, and the current sold-out-through-2027 comfort would prove exactly as durable as the demand behind it.

Where does the stress-tested balance land? Both stories are legitimate, and which one wins is not knowable in advance — that is the whole point of watching the three KPIs. What can be said neutrally is this: the structural forces (consolidation, entry barriers, the cost-per-bit reality) genuinely favor Seagate, while the situational forces (buyer concentration, substitution risk, and the sheer cyclicality of end demand) genuinely threaten it. An activist skeptic would press hardest on three things — whether the long-term agreements survive contact with the next glut, whether management's freshly minted discipline outlasts the next cash windfall, and whether a single reliability stumble in HAMR could undo years of margin gains in a quarter. Those are the right questions. They do not have answers yet.

XII. Epilogue

It is worth ending where we began — with the sheer improbability of the machine itself. A modern hard drive flies a read/write head the size of a grain of sand roughly sixty miles an hour, less than a hair's breadth above a platter spinning ten thousand times a minute, and uses a laser to heat a spot to 450 degrees and back to room temperature in a fraction of a nanosecond, all to write a magnetic bit smaller than a virus — and it does this billions of times, for years, without error. That a device this baroque is also the cheapest way humanity has found to store a bit of data is one of the quiet marvels of the age.

Seagate's forty-seven-year journey is, in the end, a rebuttal to a comfortable investing cliché — the idea that a technology tagged as "legacy" is automatically a value trap. The spinning hard drive was declared dead by serious people in the 1990s, and again in the 2000s, and again during the SSD boom of the 2010s. It is not dead. It has instead retreated to the one enormous stronghold — mass, cheap, warm storage at the foundation of the cloud — where its physics still win, and it has been made more profitable than ever by the disappearance of its competitors and the arrival of a technology that most doubted would ever ship.

The verdict this story leaves is deliberately not a verdict on the stock. It is an observation about how durable niches are made. Secular disruption is real, and much of Seagate's old empire genuinely was disrupted. But a company with relentless engineering focus, a disciplined industry structure, and — belatedly — financial restraint can carve out a lucrative, defensible position even inside a technology the world keeps trying to bury. Whether that position proves as durable as the bulls hope or as cyclical as the bears fear will be written in three numbers over the next several years: the margin, the terabytes per drive, and the leverage. The rest is narrative. The machine, meanwhile, keeps spinning.

References

-

Seagate Technology plc Form 10-K for the Fiscal Year Ended June 27, 2025 — U.S. Securities and Exchange Commission, 2025-08-20 ↩

-

Seagate Technology Reports Fiscal Third Quarter 2026 Financial Results — Seagate Investor Relations, 2026-04-28 ↩↩↩↩↩

-

BIS Imposes $300 Million Civil Penalty Against Seagate Technology — Bureau of Industry and Security, U.S. Department of Commerce, 2023-04-19 ↩↩↩↩↩

-

Seagate Launches Era of 3TB+ Per Platter with Mozaic 3+ Hard Drive Platform — Seagate Newsroom, 2024-01-17 ↩

-

Seagate Technology LLC Order Relating to Settlement of Administrative Charges — Bureau of Industry and Security, U.S. Department of Commerce, 2023-04-19 ↩↩

-

Seagate FQ3 2026 Earnings Call Transcript — Seeking Alpha, 2026-04-28 ↩↩↩↩↩↩

-

Fitch Upgrades Seagate Technology to 'BBB-'; Outlook Stable — Fitch Ratings, 2026-03-12 ↩↩

-

Seagate Reaches $175 Million Settlement in Shareholder Class Action Over Huawei Sales Disclosures — Bloomberg, 2026-06-15 ↩

-

Seagate Fined $300m for Shipping Hard Drives to Huawei — Financial Times, 2023-04-19 ↩↩

-

Seagate Fined $300 Million for Shipping Hard Drives to China's Huawei — Reuters, 2023-04-20 ↩

-

Seagate to Buy Maxtor for $1.9 Billion in Stock — The New York Times, 2005-12-21 ↩

-

Veritas, Seagate PE Partners Agree to Complex Restructuring — Wall Street Journal, 2000-03-30 ↩↩

-

Seagate, Samsung Complete Deal on Hard-Drive Business — Reuters, 2011-12-19 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube