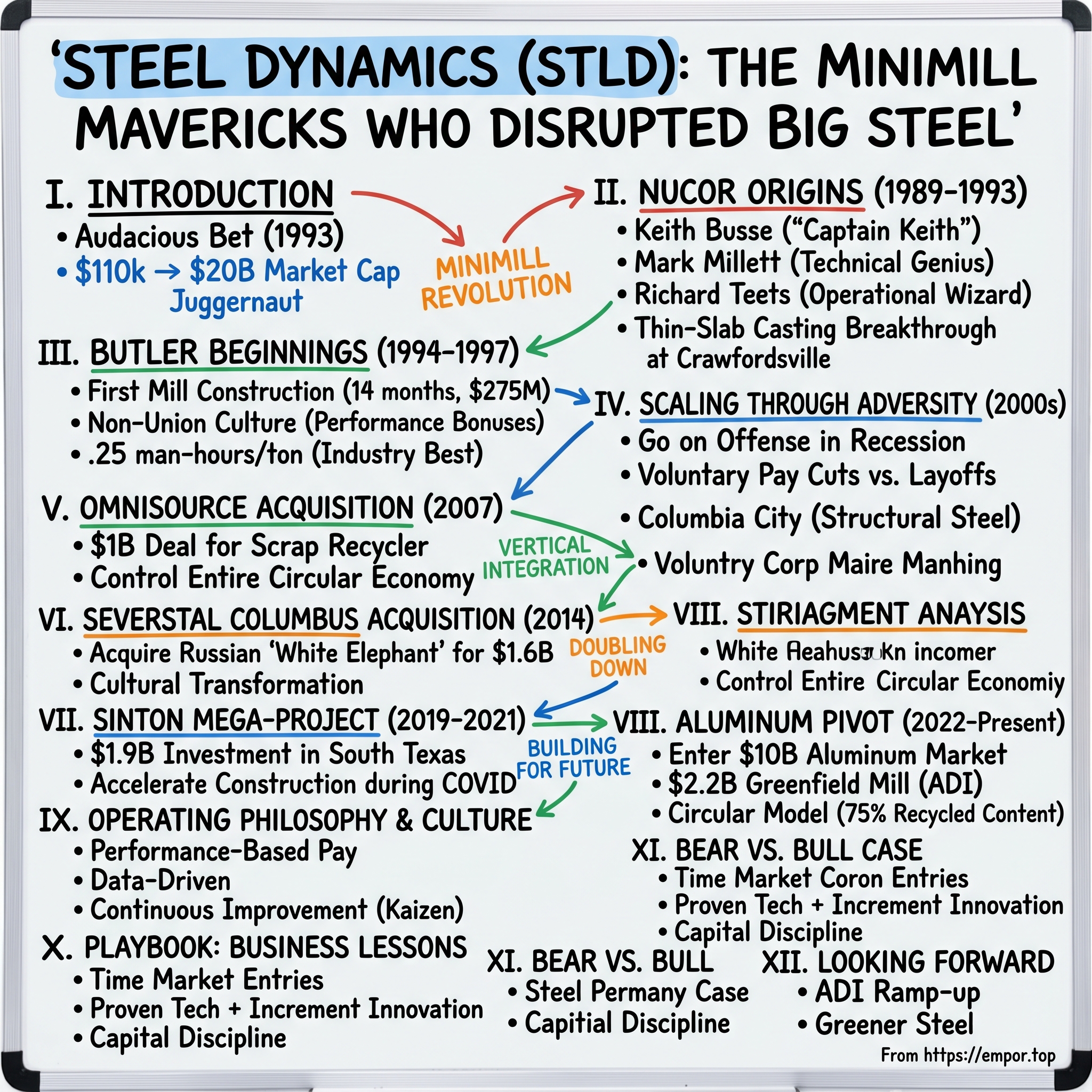

Steel Dynamics: The Minimill Mavericks Who Disrupted Big Steel

I. Introduction & Episode Setup

Picture this: It's December 1993, and three executives are walking away from one of the most successful steel companies in America. They have $110,000 between them—barely enough to buy a decent house in Indiana. Their audacious plan? Raise $370 million from investors and build a steel company to compete with their former employer, the legendary Nucor Corporation. The venture capitalists they're pitching to are skeptical. The integrated steel giants think they're delusional. Even some of their former colleagues at Nucor are betting against them.

Twenty-eight years later, that $110,000 bet has transformed into Steel Dynamics—a $20 billion market cap juggernaut that's not just surviving but thriving in an industry most investors wrote off as permanently declining. While U.S. Steel struggles to maintain relevance and gets acquired by foreign buyers, while Bethlehem Steel rusts in bankruptcy's graveyard, Steel Dynamics has quietly become the third-largest steel producer in America, generating returns that would make a software company jealous.

This is the story of how Keith Busse, Mark Millett, and Richard Teets didn't just build another steel company—they created a new playbook for American manufacturing. It's a tale of perfect timing meeting operational excellence, of turning the supposed disadvantages of being small and scrappy into competitive moats, and of building a culture so strong that workers voluntarily take pay cuts during downturns to keep the company profitable.

The minimill revolution that Nucor pioneered in the 1970s and 80s had already proven you could make steel without blast furnaces, without iron ore, without the massive integrated plants that defined American steel for a century. But Steel Dynamics would take that revolution further—proving you could start a steel company from scratch in the 1990s, compete against both the minimills and the integrated producers, and create more shareholder value than almost any industrial company of its generation.

What makes Steel Dynamics different isn't just their electric arc furnace technology or their strategic acquisitions. It's their ability to see around corners—to recognize that the scrap metal business wasn't just a supply chain necessity but a profit center waiting to be unlocked. To understand that aluminum wasn't a competitive threat to steel but an adjacent opportunity. To realize that in commodity businesses, the spoils don't go to the biggest player but to the most nimble.

As we dive into this story, we'll explore three critical tensions that define Steel Dynamics: How do you maintain entrepreneurial culture while scaling to massive size? How do you balance aggressive growth with the cyclical brutality of commodity markets? And perhaps most importantly—how do you build a company that can survive and thrive when your product is essentially identical to everyone else's?

The answers lie not in revolutionary technology or protected markets, but in something far more difficult to replicate: a management philosophy that treats steelworkers like tech employees, a capital allocation strategy that would impress Warren Buffett, and an operational excellence that turns the phrase "commodity business" from an investor warning into a competitive advantage.

II. The Nucor Origins: Keith Busse, Mark Millett & Richard Teets

The conference room at Nucor's Crawfordsville plant was thick with tension in early 1989. Keith Busse, the plant's general manager, was facing down a room full of skeptics—engineers, metallurgists, and executives who thought his latest proposal was nothing short of corporate suicide. Busse wanted to build the world's first thin-slab casting minimill, a technology so unproven that even Nucor's legendary CEO Ken Iverson had initially called it "a disaster waiting to happen."

But Busse had something the skeptics didn't: a vision of what American steelmaking could become. Standing 6'2" with the build of a former college athlete and the intensity of a drill sergeant, Busse didn't just manage—he evangelized. His leadership style was equal parts inspiring and intimidating. Workers called him "Captain Keith" behind his back, a nickname that captured both their respect and their slight fear of disappointing him. The thin-slab minimill project that Busse led at Crawfordsville was considered "doomed to failure" by many in the late 1980s. The technology was so unproven that traditional steelmakers viewed it as a pipe dream—a two-inch thick ribbon of steel that could be rolled directly into sheet? Impossible. But Busse had assembled a team that would prove them wrong.

Mark Millett, who earned a degree in metallurgy from the University of Surrey, England, joined Nucor in 1981 as chief metallurgist and was tapped to oversee the design, construction, staffing, and operation of the melting and casting facility when the SMS agreement was signed. Where Busse was the visionary leader, Millett was the technical genius—a soft-spoken Brit whose understanding of metallurgy bordered on the mystical. He could look at a piece of steel and tell you not just its composition but its entire thermal history.

Richard Teets joined Nucor in 1987 as engineering manager at Crawfordsville, managing the design and construction of the new thin-cast slab facility, paying particular attention to environmental and other standards. Teets was the operational wizard, the man who could take Millett's metallurgical theories and Busse's grand visions and turn them into functioning machinery.

The breakthrough came in the summer of 1989, when SMS and Nucor put the first thin slab casting-rolling plant into operation in the middle of cornfields at the edge of Crawfordsville. The technology worked. The German equipment manufacturer SMS had developed a revolutionary steelmaking technique that turned melted steel into a continuous ribbon measuring roughly two inches thick that could be rolled into sheet steel faster and with substantially less machinery than conventional 10-inch-thick slabs.

But success at Nucor created an unexpected problem for the trio. They had proven thin-slab casting could work, had made Nucor millions, had revolutionized American steelmaking—and now what? They were vice presidents at the top of their game, but they weren't running the show. Ken Iverson, Nucor's legendary CEO, showed no signs of retiring. The path to the top was blocked. The moment of truth came at a Holiday Inn, where Busse pitched his vision to Millett and Teets over beers. He suggested they could go out and launch their own brand new steelmaking entity. "Of course they looked at me like I was absolutely nuts," Busse later recalled. The idea was audacious beyond belief: They were attempting to start a new U.S. steel company without corporate backing, endeavoring to independently finance a start-up venture without preexisting financial credentials.

Think about what they were proposing. What they were attempting to accomplish had not been achieved in a century. The last time someone had successfully started an independent steel company in America, Grover Cleveland was president. The steel industry wasn't a place where entrepreneurs thrived—it was where capital went to die. Between 1980 and 1993, more than half of America's steel companies had gone bankrupt.

But Busse had something the skeptics didn't understand: perfect timing. The thin-slab technology had just been proven. Scrap metal prices were at historic lows. The integrated steel producers were bloated and slow. And most importantly, They had "an acute and intimate knowledge of what worked and what the shortcomings were" from their Crawfordsville experience.

The founders put in just $110,000 of their own money—split three ways, that's roughly $37,000 each. For context, that's less than a Tesla Model 3 today. Yet by September 1993 Busse had raised $370 million. How? The three founders parlayed their reputations and vision into a substantial amount of cash. Investors weren't betting on a business plan—they were betting on the team that had just revolutionized steelmaking at Nucor.

The fundraising itself was a masterclass in leverage. Busse didn't just ask for money; he created a bidding war. States competed to host the new mill. Indiana won with a package of tax incentives and infrastructure improvements. Equipment suppliers offered favorable payment terms to be part of the next revolution. OmniSource, a scrap merchant, became an early investor in exchange for a long-term purchase agreement at favorable terms.

Even the utility companies played ball. Once the Butler plant was equipped with furnaces, securing inexpensive electricity became intrinsic to achieving profitability—one of the company's 190-ton electric arc furnaces consumed 100 megawatts of electricity in a single firing, enough to light up a small city. Busse secured a beneficial deal, signing an agreement with American Electric Power for 2.8 cents per kilowatt-hour, considered to be at the low end of the price scale paid by minimills.

The decision to leave Nucor wasn't just about money or titles. It was about proving a hypothesis: that the minimill revolution wasn't over, that there was room for innovation beyond what Nucor had achieved, that you could build a steel company culture that was even more entrepreneurial, even more aligned with workers, even more efficient than the best in the business.

As Busse would later put it, they were taking the Nucor culture "from the 80th percentile to the 99th percentile." It was a bold claim. Nucor was already the most admired steel company in America. To suggest you could improve on perfection took either supreme confidence or dangerous delusion. As it turned out, Busse, Millett, and Teets had the former—and they were about to prove it in Butler, Indiana.

III. The Butler Beginnings: Building the First Mill (1993-1997)

The cornfields of Butler, Indiana, stretched endlessly under a gray November sky in 1994. Population: 2,700. Main industries: farming and a small plastics factory. Notable features: absolutely nothing that would suggest this sleepy town was about to become ground zero for the next revolution in American steelmaking. But Keith Busse saw something others didn't—a perfect confluence of logistics, labor, and luck.

With an initial capital cost of $275 million, the Butler plant began construction in the fall of 1994. The site selection wasn't random. Butler sat at the intersection of major rail lines, close to the automotive scrap yards of Detroit and Chicago, near the steel-consuming factories of the Midwest, and crucially, in a state desperate enough for jobs to offer generous incentives. It was Moneyball for manufacturing—finding value where others saw rust.

The construction itself became the stuff of legend in steel circles. On November 10, 1995, construction was completed and commercial operation began in January 1996. Both the cost and the 14-month construction period were record lows. For context, a typical integrated steel mill took 3-5 years to build and cost billions. Nucor's Crawfordsville plant, considered lightning-fast at the time, took 18 months. Steel Dynamics had just built a state-of-the-art facility in 14 months for $275 million.

How? By inverting the traditional construction playbook. Their philosophy in designing production facilities was to hire the people early who were going to operate the plant and get them deeply involved in the design of plant layout and equipment. Instead of hiring construction experts who would hand off to operations teams, they hired steelworkers during construction. These future operators helped design their own workstations, suggested equipment modifications, and essentially built their own factory.

This wasn't feel-good management theory—it was ruthlessly practical. When you're going to work 12-hour shifts at a furnace that reaches 3,000 degrees Fahrenheit, you care deeply about where the controls are placed, how the platforms are arranged, where the break rooms are located. The workers who helped build Butler didn't just understand the mill; they owned it psychologically before producing a single ton of steel.

The technology itself was evolutionary, not revolutionary. They took the thin-slab casting process proven at Crawfordsville and refined it. Where Nucor's slabs were roughly 2 inches thick, Steel Dynamics pushed for even thinner profiles. Where Nucor had one caster, Steel Dynamics designed for two, allowing continuous operation even during maintenance. Every design decision focused on one metric: tons of steel per man-hour.

But technology was only half the equation. The other half was people, and here Steel Dynamics made its most radical bet. In an industry dominated by unions, where work rules could fill phone books and grievance procedures could shut down production, Steel Dynamics would be completely non-union. Not through union-busting or intimidation, but through a compensation structure so generous that unions became irrelevant.

The deal was simple but revolutionary: base pay comparable to union shops, plus performance bonuses that could reach 40% of salary. But here's the kicker—the bonuses weren't based on individual performance or even department performance. They were based on the entire mill's profitability. Every worker, from the furnace operator to the janitor, got the same percentage bonus. When the mill made money, everyone made money. When it didn't, everyone suffered together.

This created dynamics that old-line steel executives couldn't fathom. Workers would come in on their days off to fix equipment because downtime hurt their bonuses. Office workers would help load trucks during shipping crunches. Engineers would train operators on maintenance procedures because every minute saved went straight to the bottom line—and their paychecks.

It began production at its $275 million Butler, Indiana, flat roll mill in 1996 and reported its first annual profit in 1997. But the path to profitability was anything but smooth. During its first six months of operation, the company reported $14 million in operating losses, but the streak stopped there; by July 1996 Steel Dynamics broke even for the first time.

The turnaround was swift and decisive. In August, the company posted $1.75 million in net income, followed by $2.45 million in September, beginning a pattern of escalating profitability that earned the esteem of many within the steel industry. This wasn't supposed to happen. New steel mills typically took years to reach profitability. Steel Dynamics did it in months.

The secret sauce was operational intensity that bordered on obsession. Busse instituted daily production meetings at 7 AM—not weekly or monthly like most mills. Every department head had to report their previous day's performance, explain any misses, and commit to the next day's targets. These weren't friendly check-ins; they were interrogations. Busse's questions were legendary for their specificity: "Why did furnace #2 take 3 minutes longer to tap yesterday?" "What's the silicon content variance on heat 447?" "Who authorized the overtime in shipping?"

This granular focus on operations created a culture of continuous improvement that made Japanese manufacturers look casual. Workers formed informal quality circles without management prompting. Maintenance crews developed predictive maintenance schedules that prevented breakdowns before they happened. The shipping department reorganized truck flows to save minutes per load.

SDI's Butler flat-roll mill produces steel at a rate of .25 man-hours per ton of steel. To understand how remarkable this is, consider that integrated steel mills typically required 3-4 man-hours per ton. Even efficient minimills like Nucor averaged 0.4-0.5 man-hours per ton. Steel Dynamics was producing steel with half the labor of the most efficient competitors.

The early customer wins were crucial validators. When General Motors agreed to buy steel from Butler for their stamping plants, it sent a signal to the market: this wasn't experimental steel from a startup, this was automotive-grade material that met the most demanding specifications. Orders from Whirlpool, Caterpillar, and other blue-chip manufacturers followed.

By 1997, the first full year of operations, the results spoke for themselves. Shipments increased more than 50 percent, eclipsing 1.2 million tons. Sales for the year jumped as well, swelling by 66 percent to reach $420 million. The company that many predicted would fail was now generating nearly half a billion in revenue and preparing for an IPO.

The IPO preparation revealed another dimension of Busse's strategy. By December 1996 the company's losses had grown to $50.7 million since its September 1993 inception, and Busse wanted to clear the company from some of its debt. Rather than wait for perfect financials, Busse pushed to go public while the momentum was building. Busse hoped to raise $140 million from an initial public offering of stock, earmarking $75 million for capital expansion and the remainder for refinancing the company's debt.

The Butler mill had proven the model worked. A steel company started from scratch could compete with anyone—Nucor, the integrated producers, imports. The lean, hungry culture that Busse, Millett, and Teets had instilled was creating operational metrics that shouldn't have been possible. But Butler was just one mill making one product. To truly disrupt the industry, Steel Dynamics needed to expand. And expansion in the steel industry during the late 1990s meant navigating one of the most challenging periods in the industry's history—the import crisis that would destroy dozens of American steel companies.

IV. Scaling Through Adversity: Early 2000s Growth

March 2001. The NASDAQ had crashed. The dot-com bubble was a smoking crater. And steel prices were in freefall as Asian imports flooded the American market at prices below the cost of production. LTV Steel, once America's third-largest steelmaker, was preparing for bankruptcy. Bethlehem Steel, which had built the Golden Gate Bridge and the Empire State Building, was months from collapse. In this environment, Keith Busse called an all-hands meeting at Butler and announced something that defied all logic: Steel Dynamics was going on offense.

"Gentlemen," Busse said, his voice carrying across the mill floor, "while our competitors are hiding under their desks, we're going to build." The room was silent. Everyone knew the numbers. Steel was selling for $210 per ton, below the cost of production for most mills. Companies with century-long histories were failing. And Steel Dynamics, not even a decade old, was planning expansion?

But Busse understood something fundamental about commodity cycles that most executives miss: the best time to build capacity is when nobody else will. Construction costs were down 30% as contractors begged for work. Equipment manufacturers were offering payment terms that bordered on charity. And most importantly, when the cycle turned—and cycles always turn—Steel Dynamics would have new, efficient capacity while competitors were still nursing wounds.

During the early 2000s recession, the company offered many incentive programs for employees to cut costs and improve standards. But these weren't typical corporate cost-cutting measures. Instead of layoffs, Steel Dynamics implemented something unprecedented: voluntary pay cuts tied to company performance. The deal was elegant—take a 5% pay cut now, but if the company hit certain operational metrics, you'd get it back plus a bonus.

The psychology was brilliant. Instead of demotivated workers angry about pay cuts, Steel Dynamics had employees obsessed with efficiency because every improvement directly impacted their take-home pay. A maintenance worker figured out how to extend furnace electrode life by 10%, saving $50,000 a month. A shipping clerk reorganized truck routes to eliminate two hours of daily overtime. The ideas came from everywhere because everyone had skin in the game. The second major move came in 2002 when Steel Dynamics' second-largest steel operation began operating in Columbia City, Indiana. This wasn't just another flat-roll mill copying Butler's playbook. Columbia City would produce structural steel—the wide-flange beams that form the skeletons of skyscrapers, the I-beams that hold up bridges, the heavy sections that integrated producers had dominated for decades.

The strategic logic was beautiful. The plant produces a variety of products including wide flange beams, American Standard Beams, Manufactured Housing Beams, H Piling and Channel sections for the construction, transportation and industrial machinery markets. While flat-rolled steel from Butler went into cars and appliances—consumer products vulnerable to economic cycles—structural steel went into infrastructure and commercial construction, different cycles with different timing.

But Columbia City represented something more profound: proof that Steel Dynamics could innovate beyond its initial success. The mill used a different technology, served different customers, required different skills. If Butler proved Steel Dynamics could execute, Columbia City proved they could evolve.

Going public on NASDAQ as STLD during this period wasn't just about raising capital—it was about transparency as a competitive weapon. While private competitors could hide poor performance in complex corporate structures, Steel Dynamics' quarterly earnings calls became masterclasses in operational excellence. Busse would get on calls and explain, in granular detail, exactly how they were outperforming: "We reduced electrode consumption by 2.3% through better scrap mix. We increased yield by 1.1% through tighter temperature controls. We cut maintenance costs by $2 per ton through predictive analytics."

Competitors listened to these calls in disbelief. Busse was essentially giving away trade secrets. But he understood something they didn't: execution matters more than information. You could know exactly how Steel Dynamics achieved 0.25 man-hours per ton, but replicating their culture was impossible without starting from scratch.

The company also began its vertical integration strategy during this period, though not through dramatic acquisitions. They built Steel's first joist and deck facility in Butler, Indiana. These downstream products—the joists that support roof decks, the metal decking that forms floors in commercial buildings—weren't sexy, but they were brilliant. Every ton of steel processed into joists generated 30-40% higher margins than selling raw steel. More importantly, it created pull-through demand for Butler's flat-rolled products during slow periods.

The numbers from this period tell the story of contrarian success. While 42 American steel companies filed for bankruptcy between 2000 and 2003, Steel Dynamics grew revenue from $600 million to over $1.5 billion. While competitors laid off thousands, Steel Dynamics added 500 employees. While the industry's average operating margin was negative, Steel Dynamics maintained double-digit profitability.

The cultural innovations during the downturn became permanent fixtures. The voluntary pay flexibility program evolved into a formal profit-sharing system where bonuses could reach 50% of base pay in good years. The daily production meetings expanded to include customer service, quality, and even accounting. The idea suggestion system, informal at first, became systematized with rewards ranging from $100 for small improvements to $10,000 for major innovations.

One story from this period captures the culture perfectly. During a particularly tough quarter in 2002, a furnace operator named Jim Patterson noticed that certain scrap dealers' materials consistently produced better yields. Rather than just noting it, Patterson spent his weekends visiting scrap yards, analyzing their sorting methods, even helping them improve their processes. His work increased yield by 2% across the entire mill—worth millions annually. His reward? A $25,000 bonus and a promotion to procurement. At U.S. Steel, Patterson would have been told to stick to his furnace.

But perhaps the most important development during this period was what didn't happen: Steel Dynamics didn't diversify into non-steel businesses, didn't make desperate acquisitions, didn't chase commodity trading profits. While competitors were buying everything from real estate to oil assets to escape steel's brutal economics, Steel Dynamics doubled down on making steel better than anyone else.

By 2004, as steel prices began recovering on Chinese demand, Steel Dynamics was perfectly positioned. They had new, efficient capacity. They had a battle-tested workforce that knew how to profit even in downturns. They had a balance sheet strengthened by public markets access. And most importantly, they had proven that being small and nimble beat being big and integrated.

The next phase would test whether Steel Dynamics could execute another type of growth entirely: acquisitive expansion. The scrap metal industry was fragmented, inefficient, and ripe for consolidation. And Keith Busse had his eye on a target that would transform Steel Dynamics from a steel producer into something more ambitious—a fully integrated circular economy before anyone knew what that meant.

V. The OmniSource Acquisition: Vertical Integration Play (2007)

The boardroom at OmniSource Corporation's Fort Wayne headquarters was unusually quiet on a humid July morning in 2007. The Rifkin family, who had built OmniSource from a single scrap yard into one of North America's largest metal recyclers over three generations, sat across from Keith Busse and Mark Millett. On the table between them: a term sheet that would end 95 years of family ownership and create something the American steel industry had never seen—a fully integrated scrap-to-steel powerhouse.

"This isn't just about buying a supplier," Busse said, leaning forward with his characteristic intensity. "This is about reimagining what a steel company can be."

The Rifkins exchanged glances. They'd heard plenty of acquisition pitches over the years from financial buyers promising synergies and efficiency gains. But Busse was proposing something different—what he called "a quantum leap" into scrap recycling. The price was staggering: 9.7 million shares of Steel Dynamics stock plus $425 million in cash, valuing OmniSource at roughly $1 billion.

To understand why this deal mattered, you need to understand the economics of electric arc furnace steelmaking. Unlike integrated producers who turn iron ore into steel—a process requiring massive blast furnaces and coking ovens—minimills like Steel Dynamics melt scrap metal in electric furnaces. Scrap is literally their raw material, typically representing 50-60% of their cost structure. Every penny saved on scrap acquisition drops straight to the bottom line.

But the scrap industry in 2007 was medieval in its inefficiency. Dominated by small, family-owned yards operating on handshake deals and spot pricing, it was a world where relationships mattered more than technology, where pricing was opaque, and where quality varied wildly. Most steel companies treated scrap dealers as necessary evils—vendors to squeeze when possible, tolerate when necessary.

OmniSource was different. As one of the earliest investors in Steel Dynamics, they had signed a long-term purchase agreement at favorable terms when Butler was being built. This wasn't just a vendor relationship; it was a partnership that had helped Steel Dynamics survive its early years. Now, with OmniSource processing 5.3 million tons of ferrous scrap annually and generating $2.3 billion in revenue, they were a giant in their own right.

The strategic logic of the combination was compelling on paper. Steel Dynamics consumed about 6 million tons of scrap annually across its mills. OmniSource could supply most of that, eliminating middleman margins and ensuring quality control. But Busse saw something bigger—a chance to control the entire circular economy of steel.

Think about the lifecycle of steel: A car is manufactured using Steel Dynamics' flat-rolled steel. After 10-15 years, that car is scrapped. OmniSource buys the hulk, shreds it, sorts the metals, and sells the ferrous scrap back to Steel Dynamics, who melts it into new steel for new cars. It's an infinite loop where Steel Dynamics captures value at every stage.

The timing seemed perfect. Scrap prices had soared from $100 per ton in 2001 to over $300 by 2007, driven by insatiable Chinese demand. Controlling scrap sourcing wasn't just about cost savings—it was about securing supply in an increasingly competitive global market. But the timing was also terrible. Credit markets were beginning to seize up as the subprime mortgage crisis spread. Lehman Brothers was a year from collapse. Committing $1 billion to an acquisition when storm clouds were gathering took either courage or foolishness.

The integration challenges were immense. OmniSource operated over 40 facilities across the Midwest with a culture completely different from Steel Dynamics. Where Steel Dynamics was engineering-focused and data-driven, OmniSource was relationship-based and intuitive. Where Steel Dynamics workers wore uniforms and followed standardized procedures, OmniSource yards operated like independent fiefdoms, each with its own methods and metrics.

Mark Millett led the integration, and his approach was quintessentially Steel Dynamics: don't impose, improve. Rather than forcing OmniSource yards to adopt Steel Dynamics' systems wholesale, Millett created tiger teams mixing employees from both companies. A Steel Dynamics engineer would spend a month at an OmniSource yard, learning their methods while suggesting improvements. An OmniSource buyer would embed at Butler, understanding exactly what specs the furnaces needed.

The cultural fusion produced unexpected innovations. OmniSource had developed sophisticated metal recovery techniques that Steel Dynamics hadn't imagined. Their non-ferrous separation technology—pulling copper, aluminum, and other valuable metals from the waste stream—generated margins that dwarfed steel production. Steel Dynamics' operational discipline transformed OmniSource's productivity. Yards that had relied on visual inspection began using spectrometers for precise composition analysis. Routes that had been planned on intuition were optimized using logistics software.

The first major test came quickly. In September 2008, as Lehman collapsed and credit markets froze, scrap prices plummeted from $400 to $100 per ton in three months. Steel companies with long-term scrap contracts at high prices faced massive losses. But Steel Dynamics, now processing its own scrap through OmniSource, could adjust instantly. While competitors bled cash on scrap inventory writedowns, Steel Dynamics managed costs in real-time.

More importantly, when the financial crisis crushed steel demand, OmniSource became a profit center in its own right. The non-ferrous business—copper, aluminum, brass—remained relatively stable. The scrap processing equipment business, where OmniSource designed and installed shredders and sorting systems for other recyclers, actually grew as competitors sought efficiency improvements.

The acquisition also opened doors Steel Dynamics hadn't anticipated. OmniSource's relationships with industrial manufacturers—the Big Three automakers, Caterpillar, Whirlpool—weren't just about buying their scrap. These companies needed sophisticated scrap management programs: How do you efficiently collect and sort manufacturing waste? How do you maximize recovery value? How do you ensure environmental compliance?

OmniSource began offering "Total Materials Management" programs where they would handle all of a manufacturer's waste streams—not just metal but paper, plastic, everything. For a company like General Motors, this meant one vendor, one invoice, one point of accountability for dozens of plants. The margins on these comprehensive programs far exceeded simple scrap buying.

The data advantage became equally powerful. Through OmniSource, Steel Dynamics could see scrap generation patterns weeks before they showed up in steel demand. When automotive plants increased scrap generation, it meant production was rising—a leading indicator for steel demand. When construction demolition scrap spiked, it suggested new building was coming. Steel Dynamics was no longer reacting to market changes; they were anticipating them.

By 2010, as the economy recovered, the OmniSource acquisition was revealing its true value. The combined company generated over $1 billion in EBITDA, with OmniSource contributing nearly 30%. The vertical integration had reduced Steel Dynamics' cash cost per ton by roughly $30—a massive advantage in a commodity business where $10 per ton can determine profitability.

But perhaps the most important outcome was strategic. Steel Dynamics was no longer just a steel company competing on operational efficiency. They had become a materials company with multiple profit centers, diverse revenue streams, and strategic advantages that couldn't be replicated without similar vertical integration. Competitors could build new mills, install better equipment, even poach employees. But they couldn't recreate the OmniSource network, built over decades through thousands of relationships.

The success of OmniSource integration established a template for future acquisitions: Buy assets with strategic logic beyond simple capacity addition. Preserve what works while improving what doesn't. Create value through combination, not just cost cutting. And most importantly, be patient—transformational deals take years to fully realize.

This patience would be tested in Steel Dynamics' next major move. While OmniSource was about controlling inputs, the next acquisition would be about pure scale—and it would come at a price that made the OmniSource deal look conservative.

VI. The Severstal Columbus Acquisition: Doubling Down (2014)

The gleaming Severstal Columbus mill stood like a monument to bad timing in the Mississippi Delta. Built by Russian oligarch Alexei Mordashov for $2.2 billion and opened just as the 2008 financial crisis crushed steel demand, it was simultaneously one of the most advanced steel mills in the world and one of the biggest financial disasters in American manufacturing history. By 2014, Mordashov wanted out, and Keith Busse saw opportunity where others saw a cautionary tale.

The negotiation took place in conditions of absolute secrecy. Steel Dynamics' code name for the project was "Project Magnolia"—a nod to Mississippi's state tree. Severstal called it "Project Exit." The stakes were enormous: at $1.625 billion in cash, this would be Steel Dynamics' largest acquisition ever, increasing their steelmaking capacity by 40% overnight to 11 million tons.

"Everyone thinks we're crazy," Mark Millett told his team during a strategy session in Fort Wayne. "Severstal lost $500 million on this plant last year. The street thinks it's a white elephant. But they're looking at what it is, not what it could be."

What it was: one of the newest and most technologically advanced mini-mills in North America, built with no expense spared. The facility featured automation that looked like science fiction—automated cranes that moved materials without human intervention, quality control systems that detected defects invisible to the human eye, environmental controls that exceeded anything in the industry.

The Columbus mill could produce 3.4 million tons of flat-rolled steel annually, but that wasn't what excited Millett. It was the plant's capability to produce specialized products, particularly steel for oil country tubular goods (OCTG)—the pipes used in fracking operations. With the shale revolution transforming American energy production, OCTG demand was soaring, and Columbus was perfectly positioned to capture it.

The financing strategy revealed how much Steel Dynamics had matured as a company. Rather than diluting shareholders with equity issuance or taking on dangerous levels of debt, they structured a complex financing package that maintained their investment-grade credit rating. They negotiated a bridge loan that would be replaced by long-term bonds, timed the closing to optimize cash flow, and even negotiated a working capital adjustment that reduced the effective price by $75 million.

The due diligence process was unlike anything Steel Dynamics had attempted. They sent 50 engineers and operators to Columbus for three months, examining every system, every process, every piece of equipment. What they found was both inspiring and infuriating. The technology was world-class, but it was being operated by a demoralized workforce under Russian management styles that emphasized hierarchy over initiative.

One example crystallized the opportunity: The mill's advanced coating line, capable of producing sophisticated galvanized products for automotive applications, was running at 40% capacity. Why? Because Severstal's centralized sales force in Michigan didn't understand the regional Mississippi market. Local fabricators who desperately needed coated products were buying from competitors hundreds of miles away while Columbus's line sat idle.

The cultural transformation began the day the deal closed. Busse flew to Columbus and held an all-hands meeting in the mill's cafeteria. "The Russian winter is over," he declared to nervous laughter. "You're not Severstal employees anymore. You're owners. And owners think differently."

Steel Dynamics immediately implemented their performance-based compensation system. Workers who had been making $25 per hour under Severstal's rigid pay scales suddenly had the opportunity to earn $35-40 per hour with bonuses. But the bonuses came with accountability. Daily production meetings replaced weekly reports. Quality metrics were posted in real-time on screens throughout the mill. Every worker knew exactly how their shift's performance affected everyone's paycheck.

The operational improvements came fast. Within six months, Columbus was producing 20% more steel with the same workforce. The key wasn't working harder—it was working smarter. Steel Dynamics engineers found that Severstal had been running the furnaces at conservative temperatures to avoid equipment stress, sacrificing productivity for theoretical longevity. By optimizing temperature curves and accepting slightly higher maintenance costs, they increased melt rates by 15%.

The commercial strategy was even more transformative. Instead of trying to serve the entire Southeast from Mississippi, Steel Dynamics focused Columbus on specific products where its capabilities provided genuine advantage. The mill became the go-to supplier for exposed automotive parts requiring perfect surface quality. It dominated the OCTG market as fracking boomed across Texas and Louisiana. It even developed new products, like ultra-high-strength steel for wind turbine towers.

Geographic expansion to the South proved prescient. The Southeast was America's new manufacturing belt—BMW in South Carolina, Mercedes in Alabama, Toyota in Mississippi. These plants needed sophisticated steel products delivered just-in-time. Columbus, with its river access, rail connections, and proximity to the Gulf Coast, could serve them better than mills in Indiana or Ohio.

The integration with existing Steel Dynamics operations created unexpected synergies. Columbus's excess slab capacity could supply Butler's finishing lines during peak demand. OmniSource expanded into Mississippi and Alabama, securing scrap supply for Columbus while building relationships with Southern manufacturers. The company's fabrication division opened facilities near Columbus to process its steel into construction products.

The pro forma metrics were staggering: $9.7 billion revenue, $965 million EBITDA. But more important than size was strategic position. Steel Dynamics now had mills in the Midwest and South, serving different markets with different products. They had geographic diversification that protected against regional downturns. They had scale that provided negotiating leverage with suppliers and customers.

The Columbus acquisition also marked a philosophical evolution. The early Steel Dynamics had been scrappy insurgents, building greenfield mills and proving minimills could compete with anyone. The mature Steel Dynamics was becoming a consolidator, acquiring and improving underperforming assets. It was a different skill set—financial engineering as much as metallurgical engineering—but the core remained the same: operational excellence and cultural transformation.

Wall Street's reaction was initially skeptical. Steel Dynamics' stock dropped 8% on announcement of the deal. Analysts worried about integration risk, leverage ratios, and whether Steel Dynamics was abandoning its disciplined approach for empire building. But as quarterly results rolled in showing Columbus's rapid improvement, skepticism turned to admiration.

By 2016, Columbus was generating over $200 million in EBITDA, validating the acquisition price in less than three years. The mill that had been Severstal's $2.2 billion mistake became Steel Dynamics' $1.6 billion masterstroke. More importantly, it proved that Steel Dynamics could execute large-scale M&A while maintaining their entrepreneurial culture.

The success at Columbus set the stage for Steel Dynamics' most ambitious project yet. If they could transform an underperforming acquisition into a profit machine, what could they do with a greenfield mill built from scratch with everything they'd learned over 25 years? The answer would emerge in the unlikely location of Sinton, Texas, and it would cost more than Butler, Columbia City, and Columbus combined.

VII. The Sinton Mega-Project: Building for the Future (2019-2021)

The South Texas sun blazed at 105 degrees as Mark Millett stood on a wooden platform overlooking 2,400 acres of scrubland outside Sinton, Texas. It was August 2019, and where others saw desolate emptiness, Millett envisioned the future of American steelmaking. "This," he told the assembled engineers and contractors, "will be the most advanced steel mill in the Western Hemisphere."

The numbers were staggering: a $1.9 billion investment, 3 million tons of annual capacity, 600 direct jobs, and 1,000 construction workers who would build it during a global pandemic. But the real audacity wasn't the scale—it was the timing. Steel prices were weak, trade wars were disrupting global supply chains, and no one had heard of COVID-19 yet.

The strategic rationale for Sinton was multilayered, like geological strata revealing Steel Dynamics' evolution. First layer: geographic expansion into the Southwest and Mexico, markets growing faster than anywhere in North America. Second layer: proximity to energy infrastructure as petrochemical investment boomed along the Gulf Coast. Third layer: next-generation steelmaking technology that would leap beyond even Columbus's capabilities.

But the deepest layer, the one Millett didn't advertise, was about a specific customer with specific needs. Tesla was planning something called the Cybertruck, requiring steel with properties that didn't exist yet—ultra-high strength, perfect flatness, and a surface quality that could be left exposed as the vehicle's exoskeleton. Traditional automotive steel wouldn't work. Elon Musk needed something revolutionary, and Steel Dynamics saw opportunity.

The technology choices for Sinton reflected 25 years of learning compressed into one facility. The electric arc furnace would be 20% larger than industry standard but use 15% less electricity through recuperative energy systems. The caster would produce slabs just 1.5 inches thick—thinner than even Butler's pioneering design—allowing faster rolling and better metallurgical properties. The rolling mill would have seven stands instead of the typical six, enabling production of steel as thin as 0.5mm.

But the real innovation was in the details invisible to outsiders. The scrap yard would use artificial intelligence to optimize charge mixes, with cameras and sensors analyzing incoming materials to predict exact chemical compositions. The furnace would use quantum cascade laser technology to monitor off-gas composition in real-time, adjusting inputs instantly. The rolling mill would employ machine learning algorithms that predicted surface defects before they occurred.

Construction began in January 2020. Two months later, the world shut down.

The COVID pandemic should have killed Sinton. Construction sites across America closed. Supply chains shattered. Steel demand cratered as auto plants shuttered and construction stopped. Steel Dynamics' stock plummeted from $35 to $18 in three weeks. Wall Street analysts called for suspending the project, conserving cash, weathering the storm.

Keith Busse's response was vintage Steel Dynamics: "We don't stop. We accelerate."

The logic was counterintuitive but compelling. Construction costs were dropping as contractors desperate for work cut prices. Equipment suppliers facing cancelled orders offered discounts and extended payment terms. The Federal Reserve's emergency rate cuts made financing essentially free. And most importantly, when demand recovered—and Busse was certain it would—Steel Dynamics would have new capacity while competitors remained frozen.

Managing construction during COVID required innovation that no one had planned for. Steel Dynamics created worker "pods" that lived and worked together, isolated from other groups to prevent virus spread. They chartered buses to transport workers directly from their homes to the site, avoiding airports and hotels. They built temporary medical facilities with testing capabilities that rivaled hospitals.

The supply chain challenges were even more complex. When Italian equipment suppliers couldn't ship due to lockdowns, Steel Dynamics flew engineers to Italy—navigating byzantine travel restrictions—to oversee final assembly via video link to Sinton. When semiconductor shortages threatened automation systems, they pre-purchased two years of chip inventory. When shipping containers became scarce, they bought their own.

The workforce development program revealed Steel Dynamics' long-term thinking. Rather than just hiring experienced operators, they partnered with Del Mar College to create a steelmaking curriculum. Students learned metallurgy, automation, safety, and maintenance while the mill was being built. By the time Sinton started production, Steel Dynamics had a trained workforce that understood the facility's advanced systems from day one.

The cultural transplantation was delicate. Texas had no steelmaking tradition like Indiana or Ohio. Workers came from oil fields, chemical plants, ranches—backgrounds completely different from typical steel workers. But this became an advantage. Without preconceived notions about how steel mills "should" operate, they embraced Sinton's automation and data-driven approach more readily than veterans might have.

The ramp-up began in late 2021, just as steel markets went parabolic. Prices that had been $500 per ton in 2020 soared past $1,800 as post-pandemic demand collided with constrained supply. Sinton's timing, which had seemed dangerous two years earlier, now looked prescient. The mill was producing at 50% capacity within three months, 80% within six months—a ramp-up speed that shattered industry records.

The Tesla relationship materialized as envisioned. Sinton began producing specialized steel for the Cybertruck's exoskeleton, with properties that pushed metallurgy boundaries. The steel needed to be strong enough to be bulletproof yet formable enough for automotive stamping. It required a surface finish that looked good unpainted yet resisted corrosion. The technical challenges were immense, but Steel Dynamics' engineers, working directly with Tesla's designers, cracked the code.

But Sinton's impact extended beyond one customer. The mill's ability to produce advanced high-strength steel (AHSS) with properties previously achievable only by integrated producers changed the game. Automotive manufacturers designing electric vehicles, which needed lighter yet stronger materials to offset battery weight, found a domestic supplier who could meet their specifications. Wind turbine manufacturers requiring massive yet precise steel towers had a partner who could deliver.

The financial performance validated every decision. Despite building during a pandemic, Sinton came in on budget and on schedule. The mill generated positive EBITDA in its first full quarter of operation—unheard of for a greenfield facility. By 2022, with steel prices remaining elevated, Sinton was generating cash flows that would pay for the entire investment in less than five years.

Perhaps most remarkably, Steel Dynamics funded the entire $1.9 billion project through free cash flow while simultaneously increasing their dividend 39% and buying back $1.5 billion in stock. No dilution, no dangerous leverage, no financial engineering—just operational excellence generating cash that funded growth while rewarding shareholders.

The Sinton success crystallized Steel Dynamics' evolution. They had started as scrappy entrepreneurs building a single mill in Indiana cornfields. Now they were executing billion-dollar projects with complexity rivaling any industrial company in America. Yet the culture remained unchanged: performance-based compensation, operational transparency, continuous improvement, employee ownership mentality.

As Sinton reached full production in 2022, Steel Dynamics faced a new question: What do you do after you've conquered steel? The answer would surprise everyone—including most people within Steel Dynamics. The company that had spent 30 years perfecting steel production was about to make a massive bet on an entirely different metal.

VIII. The Aluminum Pivot: New Frontiers (2022-Present)

The Steel Dynamics board meeting on July 18, 2022, began like dozens before it—operational updates, financial reviews, market analysis. Then Mark Millett stood up and dropped a bombshell: "We're proposing to invest $2.2 billion to enter the aluminum business."

The room went silent. Board members who had supported every previous expansion looked stunned. Steel Dynamics building steel mills made sense. Steel Dynamics buying scrap companies was logical. But aluminum? That was like Toyota announcing they were going to build airplanes.

"Hear me out," Millett continued, pulling up a slide showing North America's aluminum market. "The continent has a 2+ million tonne supply deficit. We import 60% of our aluminum, mostly from China and Russia. Every beverage can, every Tesla Model 3, every F-150 Lightning relies on a supply chain controlled by our geopolitical adversaries."

The strategic logic began to crystallize. Through OmniSource, Steel Dynamics was already North America's largest nonferrous recycler, processing over 500,000 tons of aluminum scrap annually. But instead of selling that scrap to others, often overseas, why not melt it themselves? The circular economy model that worked for steel could work for aluminum.

The beverage can market alone was compelling. Americans consume 100 billion beverage cans annually, each containing about 14 grams of aluminum. That's 1.4 million tonnes of demand, growing 3% annually as consumers shift from plastic to infinitely recyclable aluminum. But North American aluminum rolling capacity hadn't meaningfully expanded in two decades.

The announcement specified ambitious targets: 650,000 tonnes of flat-rolled aluminum capacity, with two slab centers in Mississippi and Florida feeding a massive rolling mill in Columbus, Mississippi—right next to their steel operations. Production would begin in Q1 2025, using 75% recycled content, with offtake agreements already being negotiated with major beverage companies.

Wall Street's reaction was brutal. Steel Dynamics' stock dropped 12% in two days. Analysts who had praised every previous move suddenly turned skeptical. "Aluminum isn't steel," Goldman Sachs wrote. "Different technology, different customers, different economics. This is a dangerous departure from core competencies."

But Millett and his team had done their homework. They'd spent two years secretly studying aluminum, hiring consultants, visiting plants, even sending engineers to work undercover at aluminum facilities to understand operations. What they found was an industry desperately needing Steel Dynamics' operational approach.

The North American aluminum industry in 2022 looked remarkably like the steel industry in 1993: dominated by slow-moving incumbents, plagued by old technology, suffering from decades of underinvestment. Alcoa, once America's industrial titan, had split itself into pieces. Century Aluminum struggled with energy costs. Noranda had gone bankrupt. The industry was ripe for disruption.

The technology choices reflected lessons from steel. Rather than building traditional aluminum smelters—which require massive amounts of electricity and produce significant emissions—Steel Dynamics would focus on recycling. Their furnaces would melt aluminum scrap using 95% less energy than primary production. The rolling mill would employ the same data-driven approach that made Sinton successful, with sensors monitoring every aspect of production.

The circular economy angle was even more powerful in aluminum than steel. A beverage can could go from consumer to recycling bin to OmniSource shredder to Steel Dynamics furnace to rolling mill to can manufacturer to store shelf in just 60 days. The same aluminum could be recycled indefinitely without quality degradation. It was the ultimate closed-loop system.

The automotive opportunity was equally compelling. Electric vehicles use 40% more aluminum than traditional cars—for battery enclosures, body panels, structural components. Tesla alone would need 200,000 tonnes annually by 2025. Ford's F-150 Lightning used 500 pounds of aluminum per vehicle. These manufacturers desperately wanted domestic supply, especially after COVID exposed the fragility of global supply chains.

But aluminum also represented a strategic hedge. For decades, aluminum had been stealing market share from steel—in vehicles, construction, packaging. Rather than fight this trend, Steel Dynamics would profit from it. If customers wanted to switch from steel to aluminum, Steel Dynamics would supply both. It was portfolio theory applied to materials.

The cultural challenge was real. Aluminum metallurgy is completely different from steel. The melting points, alloying elements, rolling dynamics—everything required new expertise. Steel Dynamics responded by hiring entire teams from competitors, offering compensation packages that made headlines in the usually staid aluminum industry. They also partnered with universities, funding research programs and hiring top graduates.

The execution timeline was aggressive, even by Steel Dynamics standards. Ground breaking to production in 30 months. Three facilities in two states. $2.2 billion investment. All while steel markets were softening and recession fears mounted. It was the kind of bet that defined companies—either as visionaries or cautionary tales.

Early signs were promising. By mid-2023, Steel Dynamics had signed letters of intent with major beverage companies covering 60% of planned production. The Mississippi slab center was 40% complete, on schedule and on budget. The rolling mill equipment, ordered from SMS group (the same company that supplied Nucor's first thin-slab caster), was being fabricated in Germany.

The sustainability story resonated powerfully. In an era of ESG investing and climate concerns, Steel Dynamics' recycled aluminum had a carbon footprint 90% lower than primary production. Beverage companies facing pressure to reduce emissions saw Steel Dynamics as a solution. The plant would even use renewable energy credits to claim carbon neutrality.

The combined EBITDA potential from the aluminum operations and other new projects was projected at $1.4 billion. If achieved, aluminum would represent 25% of Steel Dynamics' earnings within five years. It would transform them from a steel company that recycled into a materials company that happened to make steel.

The talent migration was remarkable. Engineers who had spent careers at Alcoa and Novelis joined Steel Dynamics, attracted by the entrepreneurial culture and performance-based compensation. One senior executive from a competitor told me: "At my old company, it took six months and five committees to approve a $100,000 equipment purchase. At Steel Dynamics, if it makes sense, we do it tomorrow."

By early 2024, the transformation was tangible. The Mississippi slab center conducted its first test melts. The rolling mill building, a massive structure covering 50 acres, neared completion. Customer qualification trials were scheduled. The impossible timeline suddenly looked achievable.

The aluminum pivot represented more than diversification—it was a test of institutional capability. Could Steel Dynamics' model work beyond steel? Could their culture translate to different metals, different markets, different challenges? The answer wouldn't be clear until 2025, when production began and financial results emerged.

But regardless of outcome, the aluminum investment demonstrated something crucial: Steel Dynamics at 30 years old remained as ambitious as the three entrepreneurs who met at a Holiday Inn in 1993. They weren't content being America's most efficient steel producer. They wanted to be America's most efficient materials producer, period. The aluminum bet might fail, but the ambition itself was the true competitive advantage.

IX. Operating Philosophy & Culture

The sign hanging in Keith Busse's office read: "In God we trust. Everyone else bring data." It was meant as humor, but it captured something essential about Steel Dynamics' operating philosophy. This was a company that treated steelmaking—an industry often described as artisanal, where old-timers claimed they could tell steel quality by sound—with the analytical rigor of a Silicon Valley algorithm.

The performance-based compensation model wasn't just about money; it was about psychological ownership. Every employee, from furnace operators to janitors, received the same percentage bonus based on company profitability. Not their department. Not their mill. The entire company. When Steel Dynamics had a record quarter, a maintenance worker might take home a $20,000 quarterly bonus on top of a $60,000 base salary. When times were tough, everyone tightened their belts together.

This created behaviors that traditional management consultants couldn't explain. Workers would come in on weekends, unpaid, to fix equipment because downtime hurt everyone's bonus. Office staff would help load trucks during shipping crunches without being asked. Engineers would train operators on maintenance procedures they technically weren't supposed to know, because knowledge hoarding hurt the bottom line.

The stories became legendary. There was the time a furnace operator noticed unusual slag patterns and spent three months developing a new flux mixture that improved yield by 1.5%—worth millions annually. His reward? A $50,000 bonus and a patent in his name. Or the shipping clerk who redesigned truck routes to save 20 minutes per load, generating $2 million in annual savings. Her innovation earned her a promotion to logistics manager and a $30,000 bonus.

Decentralized decision-making pushed authority to the lowest practical level. A maintenance supervisor could approve $50,000 in equipment purchases without corporate approval if they could justify the ROI. A production manager could adjust product mix based on market conditions without waiting for headquarters' blessing. This wasn't chaos—it was organized entrepreneurialism, with clear metrics and accountability but freedom to execute.

The safety-first approach seemed to contradict the aggressive production culture, but it was actually complementary. Steel Dynamics understood that injuries didn't just hurt people—they hurt productivity. A lost-time accident meant experience walking out the door, temporary workers who didn't know the systems, and a demoralized workforce. So safety became another performance metric, with bonuses tied to accident rates.

The environmental approach was similarly pragmatic. While competitors fought regulations and lobbied for exemptions, Steel Dynamics embraced environmental standards as competitive advantages. Their electric arc furnaces produced 75% less CO2 than blast furnaces. Their recycling-based model kept millions of tons of scrap from landfills. When customers increasingly demanded sustainable steel, Steel Dynamics had the credentials to win business.

The data infrastructure was revolutionary for manufacturing. Every piece of equipment had sensors feeding real-time information to centralized databases. Operators could see live productivity metrics on screens throughout the mill. Managers had dashboards showing everything from energy consumption to quality rates updated every minute. Machine learning algorithms predicted equipment failures before they happened, scheduled maintenance to minimize disruption, and optimized production schedules based on order books.

But data without culture is just numbers. Steel Dynamics created what they called "operational transparency"—every metric was visible to everyone. The CEO could see the same production data as a furnace operator. There were no hidden reports, no secret analyses. This radical transparency created trust and alignment. When everyone saw the same numbers, arguments about facts disappeared, leaving only discussions about solutions.

The daily production meetings were choreographed intensity. Every morning at 7 AM, department heads gathered—in person or via video—to review the previous 24 hours. These weren't casual check-ins. Busse or Millett would drill into specifics: "Why did heat 3847 take four minutes longer than standard?" "What caused the yield variance on order 7829?" "Who authorized the maintenance delay on caster 2?"

The questions weren't about blame but about understanding. Every variance was a learning opportunity. Every problem was a chance to improve. The meetings created a rhythm of continuous improvement that made the Japanese kaizen approach look leisurely. Problems identified at 7 AM had solutions implemented by noon, results measured by the next morning's meeting.

Training investment far exceeded industry standards. Steel Dynamics spent 3% of payroll on training compared to the industry average of 0.5%. But this wasn't traditional classroom instruction. Operators learned metallurgy to understand how their actions affected steel properties. Maintenance workers studied automation to troubleshoot sophisticated systems. Office staff visited mills to understand operations they supported.

The variable cost structure was a hidden superpower. While integrated producers had massive fixed costs—blast furnaces that couldn't shut down, coking ovens that required constant operation, thousands of union workers with guaranteed hours—Steel Dynamics could flex production instantly. When demand dropped, they could idle furnaces and reduce costs within days. When demand surged, they could ramp up just as quickly.

This flexibility extended to product mix. The same mill that produced commodity hot-rolled steel on Monday could make sophisticated automotive grades on Tuesday. The ability to shift products based on margin opportunities, rather than being locked into production schedules, generated millions in additional profit during market transitions.

Among the most profitable American steel companies per ton wasn't just a tagline—it was measurable reality. Steel Dynamics consistently generated EBITDA margins 5-10 percentage points higher than competitors. In 2018, they produced $230 EBITDA per ton while the industry averaged $140. This wasn't from charging more—steel is a commodity with transparent pricing. It was from producing more efficiently.

The circular economy model, built through OmniSource, created competitive advantages beyond cost. Steel Dynamics knew scrap availability weeks before competitors, allowing them to adjust production schedules proactively. They controlled quality from scrap to finished product, ensuring consistency that customers valued. They captured value at every stage of the steel lifecycle, from collection to processing to production to fabrication.

Managing through cycles required discipline that most companies lacked. During downturns, Steel Dynamics didn't panic and slash capacity. They used weak markets to perform maintenance, train workers, and develop new products. During upturns, they didn't get greedy and over-expand. They maintained investment discipline, focusing on projects with returns above their cost of capital regardless of steel prices.

The innovation pipeline never stopped. Even during the 2020 pandemic, Steel Dynamics filed 17 patents, developed 23 new steel grades, and implemented over 200 process improvements. Innovation wasn't a department—it was everyone's job. The worker who figured out how to extend electrode life by adjusting power curves was just as celebrated as the PhD metallurgist who developed new alloys.

The cultural transmission mechanisms ensured continuity as the company scaled. New employees went through three-month orientations, not just learning their jobs but absorbing the Steel Dynamics way. Experienced workers became mentors, teaching not just technical skills but cultural values. The performance-based compensation system created natural selection—those who thrived in the entrepreneurial environment stayed and advanced; those who preferred traditional structures left.

By 2024, Steel Dynamics employed over 12,000 people across dozens of facilities. Yet the culture remained remarkably consistent. A visitor to the newest Sinton mill would find the same daily production meetings, the same performance metrics, the same entrepreneurial energy as at the original Butler mill. The company had scaled culture—perhaps the hardest challenge in business.

This operating philosophy created a virtuous cycle. Operational excellence generated superior returns. Superior returns enabled strategic investments. Strategic investments created new platforms for operational excellence. Each turn of the cycle strengthened Steel Dynamics' competitive position, making them harder to displace even as the industry consolidated and competition intensified.

X. Playbook: Key Business Lessons

Standing before a class of Harvard Business School students in 2023, Mark Millett was asked the question every executive dreads: "What's your moat?" The students expected to hear about technology, scale, or patents. Instead, Millett smiled and said, "Our moat is that everything we do is visible, but no one can copy it. It's like publishing your workout routine—knowing it and doing it are completely different things."

The art of timing market entries and expansions became Steel Dynamics' signature capability. They built Butler during the 1994 steel recession when construction costs were low. They acquired Columbus in 2014 when Severstal was desperate to exit. They constructed Sinton during COVID when competitors were paralyzed. Each move looked risky at announcement but brilliant in hindsight.

The pattern was consistent: invest during downturns when assets are cheap and competition is weak, then harvest returns during upturns when capacity is scarce. But executing this required two rare qualities: financial strength to invest when revenues are weak, and emotional fortitude to act when consensus says wait.

Consider their 2020 decision to continue Sinton construction during COVID lockdowns. Steel prices had collapsed to $400 per ton. Competitors were idling capacity and cutting capital spending. Wall Street analysts called Steel Dynamics irresponsible for continuing a $1.9 billion project. Two years later, with steel at $1,800 per ton and Sinton ramping production, those same analysts called them visionary.

The art of raising capital without diluting founders revealed financial sophistication that belied Steel Dynamics' manufacturing roots. The original $370 million funding kept the founders in control despite contributing just $110,000. They used convertible bonds that only diluted if the company succeeded. They negotiated vendor financing that aligned equipment suppliers with Steel Dynamics' success. They structured state incentives as performance-based tax credits rather than upfront grants.

This wasn't financial engineering for its own sake—it was about alignment. Every stakeholder had incentives to help Steel Dynamics succeed. Equipment vendors who provided favorable payment terms got more orders when Steel Dynamics expanded. States that provided tax incentives saw job creation that exceeded promises. Early investors who took risk earned returns that venture capitalists would envy.

Building on proven technology while innovating incrementally sounds boring but proved brilliant. Steel Dynamics never bet the company on unproven technology. Their thin-slab casting was proven at Nucor. Their electric arc furnaces were industry standard. Their rolling mills used established designs. But within these proven frameworks, they innovated relentlessly.

Butler's furnace used standard technology but operated 15% faster through process optimization. Columbus's coating line was conventional but achieved quality levels that redefined industry standards. Sinton's automation was cutting-edge but built on established platforms. Each innovation was a single step forward, but thousands of single steps created revolutionary advancement.

Strategic M&A became a core competency, with clear criteria: Buy assets with strategic value beyond capacity. Never overpay regardless of cycle timing. Integrate culturally before operationally. Preserve what works while fixing what doesn't. Create value through combination, not just cost cutting.

The OmniSource acquisition exemplified this approach. They paid $1 billion—a fair price, not a steal. They kept OmniSource management who understood the business. They gradually integrated systems while preserving relationships. They found synergies neither company could achieve alone. Five years later, OmniSource generated returns exceeding any greenfield investment.

Managing commodity cycles with operational excellence turned a supposed weakness into strength. Conventional wisdom says commodity businesses are terrible investments—no pricing power, brutal competition, boom-bust cycles. Steel Dynamics proved this wrong by focusing on what they could control: costs, quality, service, flexibility.

During the 2015-2016 steel recession, when prices dropped below $400 per ton, Steel Dynamics remained profitable while competitors hemorrhaged cash. How? Their variable cost structure allowed them to cut expenses faster than revenues declined. Their product flexibility let them shift to higher-margin items. Their financial strength let them gain market share while competitors retreated.

Creating alignment through incentives went beyond compensation to encompass every stakeholder relationship. Customers got consistent quality and reliable delivery, earning their loyalty. Suppliers got prompt payment and long-term contracts, ensuring reliable support. Communities got stable employment and tax revenues, generating political support. Investors got superior returns and transparent communication, providing patient capital.

This stakeholder capitalism wasn't altruism—it was strategy. When Chinese imports flooded America in 2015, Steel Dynamics' customers lobbied for trade protection because they needed domestic supply. When COVID disrupted supply chains, vendors prioritized Steel Dynamics because they were reliable partners. When environmental regulations tightened, communities supported Steel Dynamics because they were responsible neighbors.

The power of vertical integration in cyclical industries proved transformative. Controlling scrap through OmniSource didn't just reduce costs—it provided market intelligence, supply security, and cycle protection. When scrap prices spiked, OmniSource profits offset steel margin compression. When scrap prices collapsed, steel margins expanded more than competitors who bought spot.

But vertical integration only works with operational excellence at every level. OmniSource had to be best-in-class at recycling, not just captive supply for steel mills. The fabrication division had to win external customers, not just process Steel Dynamics' steel. Each business had to stand alone while benefiting from combination.

Capital allocation discipline separated Steel Dynamics from empire builders. Every investment required 20% IRR at mid-cycle pricing. Growth projects competed with dividends and buybacks for capital. M&A opportunities were evaluated against greenfield alternatives. This discipline meant walking away from deals others won, but it also meant never destroying value through bad investments.

Between 2010 and 2023, Steel Dynamics invested $8 billion in growth while returning $6 billion to shareholders through dividends and buybacks. They grew capacity from 5 million to 13 million tons while improving returns on capital. They expanded into new products and geographies while maintaining the industry's best margins. This wasn't choosing between growth and returns—it was achieving both through discipline.

The technology adoption strategy balanced leading and following. Steel Dynamics was rarely first with new technology but often best at implementation. They let others prove concepts, then improved execution. When Nucor proved thin-slab casting, Steel Dynamics built better mills. When automation became viable, Steel Dynamics implemented it more thoroughly. When data analytics emerged, Steel Dynamics applied it more systematically.

This fast-follower approach reduced technology risk while capturing innovation benefits. Steel Dynamics avoided the failures that plague pioneers—the dead-ends, debugging, and development costs. But they moved quickly enough to gain advantage before technology became commoditized.

Cultural scaling mechanisms ensured that Steel Dynamics at 12,000 employees maintained the entrepreneurial spirit of 300 employees. Decentralized decision-making pushed authority down, preventing bureaucratic ossification. Performance-based compensation maintained ownership mentality despite corporate scale. Daily production meetings created urgency that prevented complacency.

New facilities inherited culture from day one. Experienced operators from existing mills trained new hires, transmitting not just technical knowledge but behavioral norms. The first employees at Sinton came from Butler and Columbus, bringing Steel Dynamics DNA to Texas. This cultural consistency created operational consistency—customers got the same quality and service from every mill.

The learning organization mindset treated every mistake as tuition for education. When a furnace campaign ended prematurely, engineers studied why and improved procedures. When a customer complained about quality, metallurgists investigated and enhanced processes. When an acquisition underperformed projections, managers analyzed causes and adjusted integration approaches.

This wasn't blame-free culture—accountability was fierce. But accountability focused on learning and improving, not punishing and hiding. The question wasn't "who screwed up?" but "what can we learn?" This subtle difference created psychological safety that encouraged innovation while maintaining performance standards.

By 2024, the Steel Dynamics playbook was studied in business schools and boardrooms worldwide. But knowing the playbook and executing it were vastly different. The playbook required patient capital, operational excellence, cultural alignment, and strategic discipline—a combination rare in any industry, nearly extinct in steel.

XI. Bear vs. Bull Case & Competitive Analysis

The conference room at Cleveland-Cliffs' headquarters was tense in early 2024. CEO Lourenco Goncalves, known for his combative style, was reviewing competitive intelligence on Steel Dynamics. "They're not invincible," he growled to his team. "Every company has weaknesses. Find theirs."

The bear case against Steel Dynamics was substantial, starting with trade policy dependencies. With a production capacity of 13 million tons of steel, the company is the third largest producer of carbon steel products in the United States, but this position depended heavily on Section 232 tariffs that protected domestic producers from imports. If trade policy shifted—through new administrations, WTO rulings, or diplomatic agreements—Steel Dynamics' margins could compress dramatically.

The China overcapacity overhang loomed like a storm cloud. China produced over 1 billion tons of steel annually, more than the rest of the world combined. Their excess capacity alone exceeded total U.S. production. While tariffs currently protected American markets, China was increasingly exporting through third countries, finding creative ways around trade barriers. A flood of Chinese steel, even indirect, could crater pricing.

The EV transition presented an existential question: opportunity or threat? Electric vehicles used 25% less steel than traditional cars—no engine blocks, transmissions, or exhaust systems. While EVs needed specialized steel for battery enclosures and motors, total tonnage declined. If U.S. automotive production shifted entirely to EVs, steel demand could drop by millions of tons.

Competition was intensifying from unexpected directions. Nucor, the company Steel Dynamics' founders left, remained formidable with superior scale and resources. Cleveland-Cliffs had transformed through acquisitions from an iron ore miner into America's largest flat-rolled steel producer. U.S. Steel, despite its struggles, was investing billions in modernization. Even aluminum companies were competing for traditional steel applications.