STERIS plc: The Invisible Moat of Global Healthcare

I. Introduction & Episode Roadmap

Lie down on an operating table—any operating table, in Cleveland or Riyadh or Singapore—and look up. The surgical light burning overhead was almost certainly engineered by a company most patients have never heard of. The steel table beneath you, the same. Somewhere down the hall, in a windowless room the hospital calls the Sterile Processing Department, a two-ton steam autoclave is cooking a tray of instruments back to sterility, and the biological indicator that will prove those instruments are safe to reopen your body with came from the same firm. Even the scalpel itself may have passed through a contract sterilization plant owned by that firm before it ever reached the tray.

That firm is STERIS plc. It is not a household name, and it never will be. It has no consumer brand, runs no Super Bowl ads, and sells nothing you can buy at a pharmacy. And yet by the middle of 2026 it commanded a market capitalization in the neighborhood of $21 billion and generated roughly $5.9 billion in annual revenue—very close to the $6 billion milestone management celebrated on its fiscal 2026 earnings call.1 STERIS is, in the most literal sense, an infrastructure company. It sits underneath the global surgical economy the way a toll operator sits underneath a highway: invisible to the driver, unavoidable on the journey, and paid a small amount every single time a vehicle passes.

Why does a company like this even exist as an outsourced specialist, rather than something hospitals and drug makers do for themselves? Because sterilization sits at a peculiar intersection: it is absolutely mission-critical, it is heavily regulated, it is capital-intensive, and it is nobody's core competence. A hospital's core competence is treating patients; a device maker's is designing devices; a pharma company's is discovering drugs. Sterilization is the thing they all must do perfectly and none of them want to own. That is the definition of a great outsourcing market—an essential, high-stakes, specialized function that customers are relieved to hand to someone who does nothing else. STERIS's entire history is the story of colonizing that gap, one product and one acquisition at a time.

The thesis of this story is that STERIS is a masterclass in three unglamorous forms of advantage. The first is razor-and-blade economics, where a piece of capital equipment installed once seeds decades of high-margin consumables and service revenue. The second is the regulatory moat, where the very rules meant to keep patients safe end up making it prohibitively expensive for a hospital or a device maker to switch vendors. The third is programmatic M&A—the patient, repeated absorption of adjacent businesses to become the "one throat to choke" for infection prevention. Whether those advantages are as durable as the company's admirers believe is exactly what we intend to test, not assume.

To do that we have to unpack the machine. STERIS today runs three engines: Healthcare, the largest, which sells the equipment and consumables that flow through hospital sterile processing and operating rooms; Applied Sterilization Technologies, or AST, which sterilizes medical devices under contract before they ship; and Life Sciences, which serves pharmaceutical and biotech cleanrooms. Each has different economics, different competitors, and different risks, and we will take them apart one at a time.

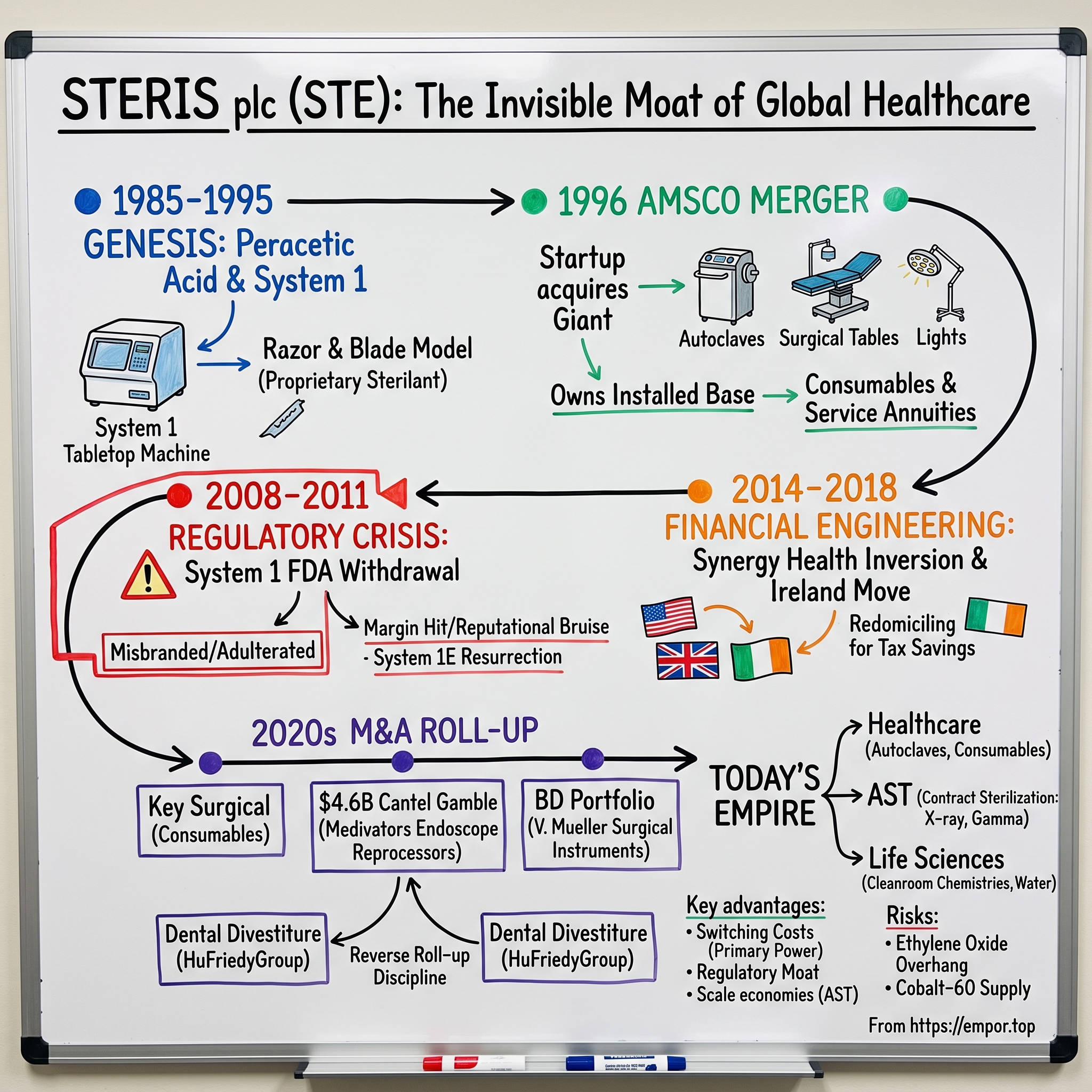

But first, the origin story—because the whole edifice began with a single, faintly toxic chemical and a bet that hospitals would pay to sterilize things without heat. The roadmap from here runs through that early "peracetic acid" gamble; the company-defining AMSCO merger that turned a startup into a giant; the near-death regulatory crisis of 2008 that nearly killed its most profitable product; the tax-inversion saga that moved its legal home twice across two countries; the aggressive Cantel integration; the dental divestiture that sharpened its focus; and the current "focused-growth" era under a CEO who has spent his entire adult career inside the company. Let's start in Ohio, in the mid-1980s, with an idea that most hospital administrators thought was faintly absurd.

II. The Genesis: Peracetic Acid and the "System 1" Foundation (1985–1995)

Here is a problem you have probably never considered. A steam autoclave—the workhorse of hospital sterilization for over a century—is essentially a pressure cooker that hits your instruments with saturated steam at around 121 to 134 degrees Celsius. It is brutally effective on stainless steel. It is also a wrecking ball for anything delicate. By the mid-1980s, medicine was filling up with delicate things: flexible fiber-optic endoscopes, plastic-bodied instruments, heat-sensitive optics. Run one of those through a steam cycle and you have a melted, warped, ruined piece of equipment worth tens of thousands of dollars.

The alternative was ethylene oxide gas—a chemical we will meet again, and not fondly. EtO could sterilize at low temperature, but it was slow, requiring hours of aeration to purge the toxic, carcinogenic residue, and it was dangerous to the workers running it. Hospitals wanted a third way: fast, cold, safe. That gap in the market is where STERIS was born.

In 1985, Raymond A. Griffin and a small group of co-founders started a company in Ohio—first under the name Innovative Medical Technologies, rechristened STERIS in 1987—built around a single bet.13 Their bet was on peracetic acid, a liquid chemical sterilant that kills microorganisms aggressively at room temperature and breaks down into little more than water, oxygen, and vinegar. If you could build a tabletop machine that flooded a delicate instrument with a precisely dosed peracetic acid solution, rinsed it, and delivered it sterile in under half an hour, you would own a slice of the hospital that steam and gas simply could not reach.

That machine became the STERIS System 1. It was, for its moment, a genuinely clever piece of engineering: a self-contained processor that let a hospital reprocess an endoscope in roughly 30 minutes rather than the hours EtO demanded, without cooking it in steam. It slotted directly into the workflow of the operating room and the endoscopy suite, and it created something more valuable than a one-time equipment sale. Each cycle consumed a single-use container of the proprietary sterilant. The machine was the razor; the chemical cup was the blade. Once a hospital standardized on System 1, it bought STERIS chemistry, cycle after cycle, for as long as the machine ran.

It is worth pausing on why this was such a shrewd chemistry to build a company on. Peracetic acid occupies a genuine sweet spot in the sterilization world: it is a powerful oxidizer that destroys bacteria, viruses, fungi, and spores quickly, yet it decomposes into benign byproducts, leaving no toxic residue that must be aired out before an instrument touches a patient. Steam is cheaper but destroys delicate optics; EtO is thorough but slow and hazardous. Peracetic acid, delivered in a controlled liquid cycle, threaded the needle—fast, cold, and clean enough to turn an endoscope around between cases. For a young company with limited capital, choosing a chemistry rather than a heavy machine as the core of the value proposition was a decision that would echo for decades. The intellectual property lived in the formulation and the process, not in a hunk of steel that competitors could reverse-engineer.

And yet the very thing that made System 1 brilliant—its proprietary, single-source consumable—also planted the seed of the company's future near-death experience. A product that a hospital cannot source anywhere else is a wonderful annuity until a regulator decides that product has drifted out of compliance. STERIS would learn that lesson the hard way. But that reckoning was two decades off. In the early and mid-1990s, the story was pure momentum.

This is the moment to name the pattern that will recur for the next forty years. STERIS did not really sell a sterilizer. It sold an annuity, front-loaded with a piece of capital equipment and back-loaded with a stream of consumables the customer could not source anywhere else. The equipment margin was fine; the consumables margin was the point.

Riding that model, STERIS went public on the New York Stock Exchange in 1992 under CEO Bill Sanford, converting clinical credibility into capital.13 And with that capital came ambition that outran a single tabletop device. A company selling one clever machine into the endoscopy suite is a niche player. Sanford wanted the whole room—and, eventually, the whole building. The problem was that STERIS was small, and the "physical real estate" of the hospital's sterilization and surgical infrastructure was already owned by someone else: a century-old giant that was, at that very moment, stumbling. That collision is the next chapter.

III. The AMSCO Transformation: Transitioning from Start-up to Giant (1996–2007)

To understand what STERIS did in 1996, picture the corporate equivalent of a minnow swallowing a whale that has beached itself.

The whale was AMSCO International—the American Sterilizer Company, founded in Pittsburgh in 1894. For a hundred years AMSCO had been the establishment: the maker of the big steam autoclaves, the surgical tables, the operating-room lights, the washer-disinfectors—the literal furniture of American surgery. It had more than 2,000 employees and roughly $400 million in annual sales, making it something on the order of five times the size of STERIS.13 But by the mid-1990s the whale was in trouble: FDA compliance headaches, softening sales, and a revolving door in the executive suite. AMSCO needed rescue. STERIS needed everything AMSCO had.

In a stock-for-stock merger completed in May 1996, the minnow swallowed the whale.13 The financial mechanics were almost secondary to the strategic logic. Overnight, STERIS stopped being a single-product endoscopy company and became the owner of the hospital's sterile-processing and operating-room hardware. The effect on the income statement was staggering: revenue jumped roughly 544% to $587.8 million for the fiscal year ending March 1997.13 But the number that mattered was not the one on the top line. It was the installed base.

Consider what it means to install a two-ton steam autoclave in a hospital. It is plumbed into the water and steam supply, wired into the building, and physically built into the architecture of the sterile processing department. It will sit there for twenty, sometimes thirty years. Ripping it out and replacing it with a competitor's unit is not a purchasing decision; it is a construction project, complete with re-validation of the entire sterile workflow. So the moment STERIS owned that installed base, it owned a multi-decade footprint in thousands of hospitals—and every one of those footprints threw off two kinds of recurring, high-margin revenue.

The first was consumables. Steam sterilization is useless unless you can prove it worked, and proving it requires chemical and biological indicators—the little spore tests and color-change strips that confirm a load actually reached sterility—along with specialized detergents and sterilization wraps. These are cheap per unit, consumed constantly, and, crucially, validated into the hospital's protocols. The second was service. When a two-ton autoclave breaks down, the hospital's surgical schedule does not slow; it stops. An operating room that cannot get sterile instruments cannot cut. That reality gives the service contract enormous pricing power, because the alternative to a fast repair is canceled surgeries and lost revenue.

Dwell on the biological indicator for a moment, because it captures the elegance of the model better than any spreadsheet. A biological indicator is a tiny vial containing a known population of highly resistant bacterial spores. You run it through the sterilization cycle alongside a real load, then incubate it. If the spores are dead, your cycle worked and your instruments are safe; if they grow, something failed. It is a consumable that a hospital cannot skip, cannot cheaply substitute, and must buy in volume forever, because every sterilization load in a modern hospital is a potential patient-safety and legal liability if it cannot be documented as sterile. STERIS did not invent the biology, but by owning the autoclave and the indicators and the detergents and the wraps that go with it, it turned the entire proof-of-sterility ritual into a recurring purchase order. This is the difference between selling a machine and selling a system: the machine is bought once; the system is bought every day.

There is a subtler strategic point buried in the AMSCO deal that is easy to miss. STERIS did not merely acquire a product line; it acquired an incumbency. AMSCO's real asset was not its factories but the relationships—the fact that a purchasing manager who needed a new sterilizer in 1997 had been buying AMSCO for their entire career and would default to it again. Incumbency in a risk-averse, regulated, mission-critical purchase is worth more than any patent, because the cost of being wrong is measured in dead patients rather than dollars. STERIS bought a hundred years of that default setting in a single transaction.

These two revenue streams share a quiet superpower: they are counter-cyclical to the equipment sale that spawned them. When hospital budgets tighten and capital purchases stall, the installed base does not stop needing indicators, detergents, and repairs—if anything, a hospital that defers buying a new autoclave leans harder on servicing the old one. So the very downturns that hurt the equipment line tend to prop up the consumables and service lines that ride on top of it. A business with that internal hedge is structurally steadier than its capital-equipment exposure alone would suggest, and it is the single most important reason STERIS can grow earnings through cycles that batter pure equipment makers.

The AMSCO era, running through the mid-2000s, is where STERIS learned the business it is still in. The lesson was that the equipment is a Trojan horse. You accept modest margins on the box in exchange for a captive, decades-long relationship built on consumables the customer must buy and service the customer cannot defer. It is a beautiful model—right up until the moment a regulator decides your flagship product has been quietly breaking the rules for two decades. That is precisely what happened next, and it nearly took the company down.

IV. The Near-Death Regulatory Crisis: The System 1 FDA Withdrawal & Resurrection (2008–2011)

Every razor-and-blade company has a nightmare scenario: the razor gets banned. STERIS lived that nightmare, and it started with a letter.

On May 15, 2008, the FDA sent STERIS a Warning Letter with a devastating premise.[^13] The original System 1 had been cleared by the agency years earlier. But over roughly two decades, STERIS had made more than a hundred modifications to the device—tweaks to hardware, software, and process—without filing the new 510(k) clearances the FDA believed those changes required. In the regulator's telling, the machine humming away in thousands of hospitals was no longer the machine the FDA had approved. It was, in the agency's language, a modified device operating outside its clearance.

For a while, this looked like a paperwork dispute. It was not. In December 2009, the FDA escalated to a full public safety communication, advising healthcare facilities to stop using the System 1 and to transition to legally marketed alternatives, and characterizing the device in the harshest regulatory vocabulary available—"adulterated" and "misbranded."12 For a company whose most profitable cash cow was the System 1 and its proprietary sterilant, this was close to an extinction-level event. The razor had been declared illegal, and with it the blade.

What followed is a genuine case study in crisis management, and it is worth being clear-eyed about, because it cuts against the tidy "great American company" narrative. The crisis was, at bottom, self-inflicted—a governance and regulatory-discipline failure stretched over twenty years. STERIS had grown comfortable improving its flagship product without going back to the agency, and it got caught.

The recovery, though, was fast and expensive. STERIS designed and pushed through the FDA a compliant successor, the System 1E, which received clearance in the spring of 2010.12 Then came the brutal logistics: transitioning a legacy installed base of tens of thousands of System 1 units across US hospitals onto the new machine. The company effectively had to convince its most loyal customers—many of them furious, all of them nervous—to swap out working equipment on the regulator's timetable, absorbing discounts and goodwill costs to keep those relationships intact. It was a margin hit and a reputational bruise. It was not, however, fatal.

The reason it was survivable is the same reason the crisis was so dangerous in the first place: the switching costs cut both ways. A hospital that had built its endoscope reprocessing workflow around System 1 could not easily jump to a rival overnight—the staff were trained, the room was configured, the protocols were validated for the STERIS process. So when STERIS showed up with a compliant successor engineered to slot into the same workflow, most customers gritted their teeth and made the transition rather than rip out the whole system and start over with a competitor. The moat that management had spent two decades building became the lifeboat that carried the company through the regulatory storm. That is a genuinely important insight for investors: deep switching costs do not just protect a company against competitors in good times; they buy it forgiveness and time when it stumbles.

But it would be too generous to end the episode there. The System 1 saga is also a permanent black mark on the "regulation is our friend" narrative that STERIS bulls like to tell. The same FDA whose site-specific filing requirements build the AST moat is the FDA that can, with a single alert, declare your flagship product misbranded and adulterated and tell every hospital in the country to stop using it. Regulation is not a one-way tailwind; it is a force that can flatten you if you get sloppy with it. STERIS got sloppy, and it cost the company dearly in cash, credibility, and management attention at the exact moment it should have been playing offense.

The deeper lesson management took from the fire is the one that shaped the next fifteen years of strategy. A company that lives and dies by a single flagship device is one warning letter away from catastrophe. The System 1 crisis is the moment STERIS's diversification instinct hardened into doctrine—away from dependence on any one hero product and toward a broader base of contract sterilization, consumables, and service that no single regulatory action could topple. The clearest expression of that new doctrine would arrive a few years later, wrapped inside one of the most controversial financial maneuvers in the company's history: it moved to a different country.

V. The Financial Engineering & Geopolitical Ballet: The Synergy Health Inversion & Ireland Move (2014–2018)

In October 2014, STERIS announced it would acquire Synergy Health plc, a UK-based leader in outsourced terminal contract sterilization, in a deal valued at roughly $1.9 billion.10 On its face, this was a logical extension of the diversification doctrine: Synergy did at industrial scale exactly the kind of outsourced sterilization that hedged against single-product risk. But the strategic rationale was not what made the deal notorious. The structure was.

The Synergy transaction was engineered as a corporate tax inversion. Rather than simply buying Synergy, STERIS reorganized so that the combined company's legal parent was domiciled in the United Kingdom, where the corporate tax rate was meaningfully lower than in the United States. The goal, in plain terms, was to drop the group's effective tax rate—from the low-thirties percent range toward the mid-twenties—by relocating the corporate shell abroad while keeping the actual business running from Mentor, Ohio.10 This was, to be blunt, financial engineering. The sterilization plants did not move. The jobs did not move. What moved was the address on the top of the org chart, and with it a stream of tax savings.

The timing made it explosive. In 2014, tax inversions had become a political lightning rod in Washington, and the Obama administration's Treasury Department was actively writing rules to stop them. STERIS pressed ahead, and when the deal closed in 2015 it did so as one of the first inversions to complete after those tighter Treasury guidelines took effect—structured to fall outside their reach. From an investor's standpoint, it was a clever, legal exploitation of a closing window. From a public-policy standpoint, it was exactly the kind of maneuver the new rules were meant to prevent. Both things are true, and a neutral reading has to hold them together: STERIS extracted real, durable value for shareholders through a mechanism many would call gaming the system.

It is worth being precise about what an inversion actually buys, because the mechanism is widely misunderstood. STERIS did not stop paying US tax on US profits—it could not, and does not. What a foreign domicile changes is the treatment of foreign earnings and the flexibility to move cash around the world without triggering the full US repatriation tax that, pre-2018, penalized American multinationals for bringing overseas profits home. For a company with a growing international sterilization footprint, that flexibility was worth real money, and it compounded every year. The catch, as we will see, is that the same cross-border cash movement that the structure was designed to ease can itself trigger withholding taxes—an irony that would surface years later in the company's buyback math.

Then geopolitics intervened. The 2016 Brexit vote put the UK's future tax relationship with the European Union in doubt, and the specific treaty benefits that had made a UK domicile attractive suddenly looked fragile—reportedly worth tens of millions of dollars a year to STERIS. So management executed a second redomiciling. In late 2018, STERIS announced it would shift its legal home again, this time from the United Kingdom to Ireland, an EU member state where the relevant tax treaties would remain intact after Brexit.[^11] The operational headquarters stayed, as always, in Ohio.

The Ireland move is the kind of decision that separates a management team that treats its corporate structure as a living instrument from one that sets it and forgets it. The UK domicile had been chosen for a specific tax logic; the moment Brexit threatened that logic, STERIS did not wait to find out how bad the damage would be. It moved again, pre-emptively, to preserve the arrangement's benefits. Admirers call this proactive stewardship. Skeptics call it a company whose earnings are unusually dependent on staying one step ahead of tax authorities on two continents. Again, both readings are defensible, and the honest investor holds them in tension rather than picking the flattering one.

Step back and the pattern is revealing. Within four years, STERIS's corporate nationality had migrated from the United States to the United Kingdom to Ireland—three flags in three countries—while a single molecule of the actual business never left Mentor. For investors, this is a genuine double-edged sword. On one edge, it demonstrates a management team willing to do the unglamorous, controversial work of optimizing the after-tax cash that ultimately funds buybacks and acquisitions. On the other, it is a reminder that a meaningful chunk of STERIS's earnings quality rests on a tax structure that lives at the mercy of politics on two continents. A future US administration, or a future EU directive, could reprice that advantage overnight. Having reorganized its balance sheet and its passport, STERIS turned back to what it does best: buying things. And the next decade of buying would be its most aggressive yet.

VI. The M&A Roll-up Machine: Key Surgical, the $4.6B Cantel Gamble, and the BD Portfolio (2020–2023)

There is a phrase hospital executives use when they describe what they want from a vendor: "one throat to choke." When a surgical site infection can kill a patient and bankrupt a reputation, a hospital does not want to manage forty suppliers of sterilization gear, indicators, endoscope reprocessors, and repair services. It wants one accountable partner. The entire STERIS M&A strategy of the 2020s is an attempt to become that single throat—and to do it in the highest-margin corners of the field: consumables and services.

The opening move was Key Surgical. In October 2020, STERIS agreed to buy the Minnesota-based maker of sterile processing, operating room, and endoscopy consumables for approximately $850 million—effectively around $810 million once an anticipated tax benefit was factored in—against roughly $170 million of annual revenue and about $50 million of adjusted operating profit.5 Key Surgical was pure razor-blade fuel: a catalog of the small, repeatedly purchased items that flow through the sterile processing department every day. It deepened the consumables annuity without adding a single heavy machine.

Then came the swing-for-the-fences move. In January 2021, STERIS announced the acquisition of Cantel Medical for approximately $4.6 billion in cash and stock—a transformational bet more than five times the size of Key Surgical.4 Cantel brought two prizes. The first was Medivators, the global leader in automated endoscope reprocessors—the machines that clean and disinfect flexible endoscopes between patients. Given that STERIS's own founding product had been an endoscope reprocessor, this was a homecoming at industrial scale, cementing STERIS as the dominant force in a workflow it had helped invent. The second was a large dental business, which—foreshadowing—would prove to be a bolt-on that did not really fit.

The Cantel math deserves scrutiny rather than applause, because the price was steep. At roughly $4.6 billion of enterprise value against approximately $1 billion of revenue and only about $134 million of operating profit, STERIS paid something on the order of 34 times operating income—a rich multiple by any standard, the kind that only makes sense if you are certain about synergies. Management's case rested on extracting roughly $110 million of annual run-rate cost synergies; on those synergy-adjusted numbers, the effective multiple compressed toward the high-teens, a far more defensible figure. That gap between the ~34x you pay on day one and the ~19x you hope to reach is the entire risk of the deal in a single spread. A roll-up works only if the synergies are real and the integration lands; STERIS was betting a leveraged balance sheet that it could execute where a lot of acquirers fumble.

The timing of the Cantel integration made the bet harder still. STERIS closed the deal in mid-2021 and then walked straight into the worst supply-chain environment in a generation—the era Carestio would later refer to, half-joking, as the "golden screw" diaries, when a single missing low-value component could hold up an entire finished machine. Integrating a billion-dollar acquisition while your factories cannot reliably source parts is a stress test few management teams would choose. That STERIS came through it with the synergy program broadly on track, rather than issuing the string of profit warnings that so often follow ambitious healthcare roll-ups, is a meaningful data point on execution—though it is worth remembering that the ultimate verdict on whether $4.6 billion was too much will only be clear years from now, in the return on invested capital the combined business generates.

The third piece rounded out the operating room. In 2023, STERIS acquired the surgical instrumentation assets of Becton, Dickinson—the storied V. Mueller and related surgical and laparoscopic instrument lines—for about $540 million, pushing STERIS deeper into the physical toolkit of the surgeon.11 Consumable steel, repeatedly reprocessed, repeatedly replaced: another annuity.

Notice the logic that connects these three deals. Key Surgical added the small consumables flowing through the sterile processing department. Cantel added the machines and consumables of endoscope reprocessing. BD's V. Mueller added the reusable surgical instruments themselves. Each purchase pushed STERIS to own another station along the single physical loop that a surgical instrument travels: from the operating room, to the sterile processing department to be cleaned and sterilized, and back to the operating room for the next patient. By 2023, STERIS had assembled a position at nearly every point on that loop. That is what "one throat to choke" actually looks like when you build it deal by deal—not a slogan, but a map of a hospital's instrument journey with a STERIS product at every waypoint. The strategic elegance is real. The risk, equally real, is that a company assembled from a dozen acquisitions carries a dozen integration seams, a complex chart of accounts, and the constant temptation to keep buying past the point of discipline. Which is why the next move mattered so much.

And then, in a move that told you something important about management's discipline, STERIS reversed course on part of Cantel. Having concluded that the inherited dental business (operating as HuFriedyGroup) was lower-growth, lower-strategic-fit, and a distraction from the core infection-prevention story, STERIS sold it in 2024 to private equity firm Peak Rock Capital for $787.5 million—roughly 2.6 times its revenue—and used the proceeds to pay down the debt it had taken on for the acquisition spree.6 This is the part of the record that deserves genuine credit. Plenty of acquirers buy a mixed bag and then cling to the pieces that do not fit, unwilling to admit a portfolio built by accretion contains mistakes. STERIS bought a whale to get the good half, and then had the discipline to sell the half it did not want at a healthy price and deleverage. The roll-up machine, in other words, was willing to run in reverse. What it left behind was a cleaner, more focused company—and that company is the one we can finally take apart segment by segment.

VII. Today's Empire: Segment Deep Dives & Economic Engines

With the dental business gone, STERIS entered fiscal 2026 as a pure-play medical, pharmaceutical, and medtech infrastructure company. The consolidated numbers set the stage: total revenue of roughly $5.9 billion, up 9% as reported and 7% on a constant-currency organic basis, with adjusted earnings of $10.17 per diluted share—about 10% growth—despite an 80-basis-point drag on margins from tariffs.1 But the consolidated figure hides the real story, which is that STERIS is three very different businesses wearing one logo. Here is how each engine actually runs.

1. Healthcare (the volume engine)

Healthcare is the giant. In fiscal 2026 it crossed two symbolic milestones at once: roughly $4 billion in revenue and $1 billion in operating income, growing 9% as reported and 8% organically.1 This is the segment that owns the sterile processing department and the operating room—the autoclaves, washer-disinfectors, surgical tables, surgical lights, endoscope reprocessors inherited from Cantel, and the river of consumables that flows through all of it.

The most telling detail from the fiscal 2026 results is the mix of that growth. Service revenue grew 12%, consumables 7%, and capital equipment 6%.1 Read that ordering carefully, because it is the razor-and-blade model showing up in the data. The fastest-growing, stickiest, highest-margin lines—service and consumables—outgrew the equipment they depend on. On the earnings call, CEO Dan Carestio framed the consumables gains as share capture "thanks to the breadth of our portfolio and the performance of our commercial teams," and described the segment's transformation from a "products and services" vendor into an operational "partner" helping hospitals push more procedures through their sterile processing departments.2 That language is worth flagging as management narrative rather than proven fact—but the underlying number, double-digit service growth on a $4 billion base, is real evidence that the installed base is doing its job.

The competition here is credible but structurally disadvantaged. STERIS's chief rival is Sweden's Getinge AB, a global player in sterilizers and surgical workflow; below them sit the specialized Belimed AG and Steelco operations and the hygiene conglomerate Ecolab Inc. The reason STERIS wins is not that its autoclave is magically better. It is that hospitals are pathologically risk-averse about sterilization, and switching brands means retraining staff, re-plumbing rooms, and re-validating the entire sterile workflow—cost and risk that the incumbent almost never has to justify. The installed base is the distribution channel, and it is very hard to dislodge. The vulnerability is that capital equipment—the big-ticket autoclaves and tables—is exposed to hospital capital budgets, which freeze in downturns. Capital equipment backlog ended fiscal 2026 just under $400 million, with orders up only 2% in the fourth quarter, a reminder that the "razor" half of the model is lumpier and more cyclical than the blades.2

There is a strategic evolution buried in the fiscal 2026 Healthcare commentary that deserves attention, because it is where management's story gets genuinely interesting—and where a skeptic should press hardest. Carestio and his team have begun describing Healthcare not as an equipment vendor but as a workflow and software partner. On the call, Carestio talked about helping hospitals "drive compliance"—putting instructions-for-use at the technician's fingertips, making it "harder to move products down the line" without confirming each step, and layering on what he called an ERP for the sterile processing department to track and trace instruments and inventory from the operating room to the SPD and back.2 Translated, STERIS wants to sell hospitals not just the machines but the software system that runs the room, deepening the lock-in from physical to digital. If that works, it is a powerful extension of the moat: software embedded in a clinical workflow is even harder to rip out than a plumbed-in autoclave. But it is also, as of fiscal 2026, more promise than proof. Software is a different competence from steel, the enterprise-software graveyard is full of hardware companies that thought they could pivot, and STERIS has not yet shown investors a scaled, high-margin software revenue line to back the ambition. This is exactly the sort of management claim to file under "watch, don't credit."

2. Applied Sterilization Technologies (the crown jewel)

If Healthcare is the volume engine, AST is the profit jewel. In fiscal 2026 it crossed $1 billion in revenue and, for the first time, more than $500 million in operating profit—implying operating margins in the mid-40s that dwarf anything else in the company.2 AST is the contract sterilization business: medical device makers and pharmaceutical companies ship their products to STERIS facilities, which sterilize them in bulk—using gamma radiation, electron beam, X-ray, or ethylene oxide—and ship them back, sterile and ready for distribution.

Before the economics, a quick tour of the physics, because AST's competitive position rests on which sterilization methods it can offer. There are four workhorses, and they solve the same problem in very different ways. Gamma radiation blasts products with high-energy photons from decaying Cobalt-60; it penetrates deeply and sterilizes sealed packages, but it depends on a scarce, radioactive isotope with a constrained supply chain. Electron beam, or E-beam, does something similar using a focused stream of electrons from an electrically powered accelerator—faster and requiring no radioactive source, but with shallower penetration. X-ray is the newer entrant: it converts E-beam electrons into high-energy X-rays, marrying gamma's deep penetration with E-beam's freedom from Cobalt-60, at the cost of heavy capital investment and electricity. And ethylene oxide gas remains the go-to for heat- and radiation-sensitive products, sterilizing at low temperature but carrying the carcinogenic and regulatory baggage we will revisit. The strategic point is that a contract sterilizer able to offer all four modalities can match nearly any device or material a customer throws at it—and STERIS's ongoing, near-complete push into X-ray is a deliberate bet to reduce its dependence on the one input it does not control.

Why are the margins so extraordinary? Because AST is a duopoly protected by the single most powerful switching cost in the entire STERIS empire. Its principal competitor is Sotera Health, through its Sterigenics business, and between them they dominate outsourced terminal sterilization in their core regions. Here is the moat mechanism, and it is worth slowing down on. When a medical device manufacturer files its product with the FDA, it must specify the exact sterilization facility—the physical address—used in production, because the sterilization process is part of the validated manufacturing of the device. Moving that product to a different sterilizer is not a procurement decision; it triggers a re-validation that can cost hundreds of thousands of dollars and take six to eighteen months, during which the manufacturer risks supply disruption. In practical terms, once your device is validated at a STERIS plant, you are married to that plant. That is why AST can hold pricing that Healthcare can only envy.

The fiscal 2026 story also exposed the segment's real-world vulnerabilities. AST grew 10% as reported and 7% organically—"a bit lighter than what we had anticipated," Carestio admitted, blaming two things.2 First, severe US snowstorms early in the calendar year shut STERIS plants and their customers in the Midwest and on the coasts, costing an estimated 150 to 200 basis points of fourth-quarter growth. Second, and more strategically interesting, medtech customers were "managing inventory levels carefully"—pulling back on how much sterilized product they stockpiled even as underlying procedure volumes kept growing.2 That inventory-destocking dynamic is the one genuinely soft spot in the AST armor: the moat protects pricing, but volume still rides the inventory cycles of the device industry, which is why management guided AST conservatively for fiscal 2027.

3. Life Sciences (the quiet compounder)

The smallest of the three, Life Sciences, generated something under $600 million in revenue in fiscal 2026 but crossed $250 million in operating profit for the first time—another mid-40s-margin business hiding in plain sight.2 It sells formulated cleaning chemistries, water purification systems, and steam sterilizers into pharmaceutical and biotech cleanrooms.

The moat here is a cousin of the AST filing lock-in, but it lives inside drug manufacturing. Pharmaceutical production runs under Good Manufacturing Practice rules, and a drug maker's cleaning and sterilization procedures are documented and validated as part of the approved process for making the drug. STERIS's cleaning chemistries are not commodity soap; they are written into the customer's validated protocols. Swapping them out means revisiting that validation—so the customer generally doesn't. The result is a steady, high-margin consumables stream that grew 8% in fiscal 2026 even as the more cyclical capital-equipment line whipsawed.2

It is worth confronting a common myth about STERIS here, because Life Sciences is where it is most tempting. The consensus narrative treats STERIS as a smooth, recession-proof "medical utility" whose revenue simply grinds higher with demographics. The reality is more textured. Two of its three segments—AST and Life Sciences—are meaningfully cyclical, tied to medtech inventory swings and pharma capital cycles respectively, and even Healthcare's capital-equipment line rises and falls with hospital budgets. The company is defensive relative to, say, a discretionary consumer business; it is not immune to cycles. The consumables and service annuities are the ballast that keeps the whole thing steadier than its end markets, but an investor who buys the "utility that never wobbles" story will be surprised by the quarter-to-quarter lumpiness that management itself openly describes on nearly every call. The durable-compounder thesis is defensible. The zero-cyclicality version of it is a myth.

Life Sciences also offers a live read on a macro theme. On the fiscal 2026 call, Carestio noted that capital spending had returned as pharma came out of its post-pandemic "boom-bust" cycle—capital equipment grew 15%—and pointed to reshoring of drug manufacturing to the US East Coast and the Carolinas as a genuine tailwind. But he was candid about the catch: "it's all big pharma right now that's doing well," with smaller biotech investment still weak.2 For investors, that is the honest texture of the segment: a durable consumables annuity riding on top of a capital cycle that is recovering but concentrated. Three engines, then—one big and cyclical, two small and spectacularly profitable. The question is who steers them, and how. That brings us to the CEO.

VIII. Current Management & Strategy: Dan Carestio's Lean Architecture

Daniel A. Carestio is not a hired-gun executive parachuted in to fix a company he barely knows. He is a STERIS lifer. He joined the company in 1997 as an associate product manager, spent more than two decades climbing through its operating units, became chief operating officer in 2018, and took the top job as President and CEO in July 2021—right in the thick of the Cantel integration. When Carestio talks about the sterile processing department or the "golden screw" supply-chain nightmares of the early 2020s, he is not reading a briefing. He lived them.

That insider credibility cuts both ways, and a neutral observer should hold both. On one hand, Carestio understands the operational plumbing of STERIS at a level an outsider never could, and his compensation is structured to be overwhelmingly performance-based—weighted toward equity and incentive pay tied to organic revenue growth, operating margins, and free cash flow rather than a fat guaranteed salary. On the other hand, a CEO who has never worked anywhere else can be a prisoner of the company's own orthodoxies, less likely to question the roll-up reflex or the tax-arbitrage instinct that defines the place. The record so far tilts favorable, but it is worth watching.

A useful way to judge a management team is to compare what it said it would do with what it actually did, across cycles. On this test STERIS scores reasonably well. The five-year record Carestio cited on the fiscal 2026 call—average constant-currency organic revenue growth of roughly 9% and an adjusted-EPS compound annual growth rate of about 11%—was compiled through a genuinely brutal stretch: a pandemic that scrambled surgical volumes, a supply-chain meltdown, a $4.6 billion integration, and a wave of tariffs.2 A management team that hits mid-to-high single-digit organic growth and double-digit earnings growth through that gauntlet is demonstrating that the underlying model is robust, not just that a rising market lifted it. The guidance discipline has also been credible: management tends to frame conservative outlooks, flag specific risks by name, and then explain misses concretely rather than blaming the weather in vague terms—though, notably, the weather did get specific billing for the soft AST quarter.

The defining management initiative of Carestio's tenure has been an efficiency and restructuring push launched in response to the post-pandemic squeeze—supply-chain chaos and hospital capital budgets under pressure. STERIS trimmed its global workforce by roughly 1.7%, consolidated facilities, restructured European operations, and rescrubbed its capital projects, targeting on the order of $25 million in annualized run-rate savings largely realized by fiscal 2026. The point of the exercise shows up in the margin line: total company EBIT margin expanded a modest 10 basis points to 23.3% in fiscal 2026—modest, but achieved while eating roughly $46 million of incremental tariff cost that alone knocked 80 basis points off margins.12 Absorbing an 80-basis-point external hit and still expanding margins is the kind of unglamorous operational grind that this management style is built for.

Carestio's fiscal 2027 plan also reveals where he is willing to spend for the long term rather than dress up the near term. Two commitments stand out. The first is a new sterility-assurance manufacturing plant in Mentor, Ohio—a roughly $60 million, two-year investment in a highly automated "center of excellence" that will consolidate three existing US facilities and serve the high-growth indicator-and-consumable business feeding both Healthcare and Life Sciences.2 The second is a multiyear initiative to rebuild the company's field-service workflows around new technology, including artificial intelligence, to lift quality and technician productivity. Both carry upfront operating-expense drag in exchange for later payoff, and a management team optimizing purely for the next quarter would not take them on. That willingness to accept near-term cost for durable capability is, in itself, a small but real signal about how Carestio thinks—though, as always, the proof will be in whether the automated plant and the AI service tools actually deliver the promised efficiency rather than becoming expensive projects that quietly underwhelm.

On capital allocation, the behavior largely matches the rhetoric, which is not something you can say of every industrial roll-up. Management preached discipline; then it actually sold the non-core dental business and put the $787.5 million toward debt reduction, leaving the balance sheet at roughly $1.9 billion of total debt and gross leverage of about 1.2 times EBITDA—well below its own 2.0-to-2.5x comfort zone.26 Then, in May 2026, the board approved a new $1 billion share repurchase authorization, double the size of the prior program, with management signaling $200 million to $300 million of annual buybacks going forward.12

But here the neutral lens matters, because the buyback story contains a genuinely revealing wrinkle that management, to its credit, disclosed plainly. CFO Karen Burton explained on the fiscal 2026 call that STERIS's foreign domicile—the very inversion structure that lowers its tax rate—imposes a hidden cost on buybacks. Because the company earns most of its profit in the US but is domiciled abroad, moving cash across borders to fund repurchases can trigger US withholding taxes. That "incremental hurdle," Burton said, is why STERIS has historically bought back only enough to offset dilution and why it favors a "measured approach" rather than an aggressive, opportunistic buyback even when the stock is under pressure.2 In other words, the tax structure that flatters the income statement quietly taxes the capital-return program. It is a subtle example of a theme running through this whole company: the moats and the maneuvers all have an underside, and the honest version of the STERIS story keeps both in view. To see the moats and their undersides together, it helps to run the business through the two frameworks every serious analyst reaches for.

IX. The Competitive Moat: Porter's 5 Forces & Hamilton Helmer's 7 Powers Analysis

Strip away the segment detail and STERIS becomes a useful test case for the two canonical frameworks of competitive analysis. Neither framework is a verdict; both are lenses. Used honestly, they sharpen the "why it wins / why it might not" question rather than answering it by assertion.

Hamilton Helmer's 7 Powers

Switching costs are the primary power, and they are unusually deep. We have now seen the mechanism in three distinct forms, and it is worth consolidating them rather than repeating them. In Healthcare, the lock-in is physical and procedural—plumbed-in capital equipment, validated consumables, and retrained staff. In AST, it is regulatory and site-specific—the FDA product filing that names the exact sterilization facility, turning a vendor switch into a multi-month re-validation. In Life Sciences, it is embedded in the drug maker's own GMP-validated manufacturing process. Three different flavors of the same power, each strong, and together they are the load-bearing wall of the entire investment case.

Scale economies are real but concentrated in AST. STERIS's global network of contract sterilization plants gives it redundant capacity a smaller regional operator cannot match: when a facility goes offline—as several did during the fiscal 2026 snowstorms—work can, in principle, be rerouted. That redundancy is a genuine advantage in a business where a device maker cannot afford a sterilization outage. But note the limit the snowstorms exposed: redundancy protects against permanent loss, not against a bad quarter, because re-validated volume cannot always simply move plants on short notice.

Brand power is qualitative but not trivial. The STERIS and AMSCO names carry more than a century of clinical trust between them, and in a field where the failure mode is a dead patient and catastrophic liability, no hospital procurement officer wants to be the person who bought the cheap generic sterilizer. This is a real barrier to a low-cost entrant. It is also the softest of the powers to quantify, and it does nothing to protect STERIS against a credible, trusted incumbent like Getinge competing on price.

Cornered resource is where STERIS is deliberately playing defense. Gamma sterilization depends on Cobalt-60, whose supply chain is highly constrained—and, awkwardly for STERIS, the primary Cobalt-60 supplier, Nordion, is owned by its AST rival Sotera Health. Rather than depend on a competitor for a critical input, STERIS has invested heavily in X-ray and electron-beam sterilization, technologies that need no Cobalt-60 at all. Management noted on the fiscal 2026 call that it is "nearly done" with a multiyear global X-ray expansion.2 This is less a power STERIS holds than a vulnerability it is engineering around—an important distinction.

Porter's 5 Forces

Threat of new entrants: very low. Building a contract sterilization facility requires enormous capital, environmental permitting, and regulatory licensing, and then persuading device makers to re-validate onto an unproven site. The regulatory filing requirement that locks in incumbents also locks out newcomers.

Bargaining power of buyers: low to moderate. Individual hospitals have been consolidated into Group Purchasing Organizations that squeeze pricing, and large medtech customers can time their inventory—as they did in fiscal 2026, pressuring AST volumes. But the clinical necessity of sterilization and the switching costs blunt that power. Buyers can push on price at the margin; they cannot credibly threaten to leave.

Threat of substitutes: very low. There is no substitute for sterilization. A medical device is either sterile or it is a hazard, and no cost-saving workaround changes that binary. This is perhaps the single most durable feature of the whole business: demand is mandated by the biology of infection, not by a discretionary purchasing choice.

The frameworks converge on a consistent picture: STERIS occupies a genuinely defensible position, anchored by switching costs and the non-optional nature of what it sells. What the frameworks cannot tell you is whether that position is already fully priced, or what could crack it. For that we need to name the specific risks—and stress-test the bull case against them.

X. The Risk Radar, Bull vs. Bear Case, and KPIs

A moat is only as good as the specific threats it faces. STERIS's risks are not vague macro worries; they are concrete, mechanical, and mostly chemical.

The Risk Radar

Ethylene oxide is the overhang that will not fully go away. EtO is a known human carcinogen, and the EPA's NESHAP emissions rules—finalized in 2024 and revisited in 2026—impose stringent controls on the facilities that use it, requiring capital investment in scrubbers and monitoring.9 Beyond compliance capex, EtO carries litigation risk: nearby communities have sued sterilization operators over emissions. STERIS settled its legacy Cook County, Illinois EtO claims in 2025 for $48.15 million—a contained outcome, and a strikingly modest one when set against the roughly $408 million Sotera Health agreed to pay to resolve its own Illinois EtO litigation in 2023.78 That ~8x gap in settlement size is itself a data point: STERIS's EtO exposure, while real, has so far proven far more manageable than its closest peer's. Notably, on the fiscal 2026 call, Carestio said STERIS is "pretty much fully spent" on upgrading its EtO facilities, so the potential rollback of EtO regulations under a new US administration would bring "no significant capital impact"—the money is already spent.2 The remaining EtO settlement payments will run off over fiscal 2027.

Cobalt-60 supply is a geopolitical bottleneck, as discussed—an input concentrated in a handful of reactors, some in higher-risk jurisdictions, which is precisely why the X-ray and E-beam pivot matters.

Tariffs and input inflation are the live P&L issue. Incremental tariffs cost STERIS roughly $46 million in fiscal 2026—about 80 basis points of margin—and management modeled total tariff spend of $60 million to $65 million continuing into fiscal 2027.2 The wrinkle here is almost comic: Burton told analysts that recent tariff changes were actually "favorable" going into fiscal 2027 and would help offset volume-driven cost increases—"in an odd twist, tariffs are an okay thing for us looking at '27."2 Meanwhile, oil-linked freight and raw-material costs (metals, plastics, electronics, chemicals make up under 20% of cost of goods) are the inflation lines management is watching, with Burton candidly flagging that a prolonged spike in oil "for the whole year" could leave guidance "a little short."2 That is the kind of specific, falsifiable disclosure that builds credibility.

The Bull vs. Bear Stress Test

The bull case is demographic and structural. The global population is aging, surgical and diagnostic procedure volumes grow relentlessly—US procedure volume was still growing mid-single digits in fiscal 2026—and STERIS collects a small, high-margin toll on a rising tide of surgeries it does not have to forecast or market. Layer on the segment mix shifting toward high-margin AST and Life Sciences, the ongoing X-ray transition capturing share from Cobalt-constrained gamma, the cleaner post-dental portfolio, and a five-year track record of roughly 9% average organic revenue growth compounding into an 11% adjusted-EPS CAGR through a genuinely turbulent stretch, and you have the profile of a defensive compounder.2 The activist's dream here would be simple: with leverage at just 1.2x, this balance sheet is arguably underworked.

Where would an activist actually push? Not on the obvious levers—there is no bloated cost structure to slash, no scandal, no wildly misallocated capital. The sharper activist critique would be about ambition and balance-sheet timidity. With gross leverage at roughly 1.2 times EBITDA against a stated comfort range of 2.0 to 2.5 times, STERIS is carrying far less debt than its own policy permits, and it has chosen a deliberately "measured" buyback constrained by the withholding-tax friction of its own tax structure.2 A pointed shareholder could argue that management is under-utilizing the balance sheet—hoarding capacity for a transformational deal that may never come at a sensible price while returning cash at a trickle. The counter-argument is that discipline is precisely what protected STERIS through the Cantel integration and the supply-chain crisis, and that a company burned once by an over-reliance on a single product and once by a rich acquisition price has earned the right to be conservative. That debate—too cautious versus prudently patient—is the most legitimate governance question hanging over the stock, and reasonable investors land on both sides of it.

The bear case is that the defensiveness is fully priced and the growth is quietly cyclical. The two most profitable segments both ride cycles the company does not control—medtech inventory destocking in AST, pharma capital spending in Life Sciences—and the largest segment, Healthcare, has a big-ticket capital-equipment line hostage to hospital budgets. EtO and tariff costs are permanent taxes on the model, not one-time hits. A well-capitalized Getinge competing harder on price could compress Healthcare margins. And the earnings quality rests partly on a two-country tax structure that politics could reprice. None of this is a thesis-breaker on its own; collectively, it is the reason to be skeptical of paying a premium multiple for "boring."

The KPIs That Actually Matter

For an investor tracking STERIS over time, three numbers cut through the noise—and, per the spirit of this analysis, they are numbers to monitor, not targets to celebrate.

First, constant-currency organic revenue growth. This strips out acquisitions and currency to reveal the true underlying health of procedure-driven demand. Management frames the durable range as mid-to-high single digits; fiscal 2026 came in at 7%, with fiscal 2027 guided to 6–7%.1 A sustained slip below that band would signal the demographic tailwind is stalling or share is being lost.

Second, AST segment operating margin. This is the single cleanest gauge of pricing power and asset utilization in the whole company. AST margins in the mid-40s are the crown jewel; watch whether they hold as X-ray capacity comes online and if inventory destocking persists. Erosion here would matter more than a soft quarter anywhere else.

Third, free cash flow conversion. STERIS's ability to turn earnings into cash is what funds the buybacks, the dividend (raised for a 20th consecutive year in fiscal 2026), and the next tuck-in. Fiscal 2026 free cash flow was an exceptional $982.9 million; fiscal 2027 is guided lower, to about $850 million, as the working-capital tailwind of prior years normalizes.12 The trajectory of that conversion, more than any single year's figure, is the tell on capital-allocation health.

One more overlay belongs on the radar, integrated rather than listed: the quiet dependence of STERIS's reported earnings on things other than pure operations. The tax structure discussed earlier is one; the incentive-compensation swing is another. On the fiscal 2026 call, Burton walked analysts through a roughly $20 million favorable move in fiscal 2027 earnings simply from resetting bonus accruals to 100% achievement after an over-achieving fiscal 2026, and a modest $2 million bonus "tailwind."2 These are small numbers against a company earning over $1 billion, but they are a reminder that a portion of any single year's earnings growth can come from accounting resets and cost items rather than from more surgeries or more sterilized devices. A careful reader separates the operating engine from the below-the-line arithmetic. The KPIs above are chosen precisely because they track the engine—organic demand, segment pricing power, and cash generation—rather than the arithmetic.

Those three numbers are the dashboard. The story they will tell over the next few years is, ultimately, the story of whether the invisible moat holds.

XI. Epilogue & Outro

STERIS is the purest expression of an investing idea that rarely makes headlines: boring, essential, and quietly compounding. It is an industrial utility dressed as a medical-device company—a toll operator on the flow of surgical and pharmaceutical volume, protected less by brilliance than by biology, regulation, and the simple fact that no hospital or drug maker can afford to get sterilization wrong.

But the neutral version of this story refuses the temptation to call it a sure thing. The same regulatory rules that build STERIS's moat also expose it to EtO liability and compliance capex. The same tax structure that flatters its earnings quietly penalizes its buybacks and hangs on the whims of politics in Washington, Dublin, and beyond. The same roll-up machine that built the empire paid a rich multiple for Cantel and had to sell off the dental piece it should not have owned. And the two segments that generate the fattest margins ride industry cycles the company cannot command. The moat is real. So are its undersides.

There is a deeper reason the STERIS model is so hard for markets to price, and it is the same reason it is easy to underrate. Great toll roads are boring precisely because nothing dramatic ever happens on them—no viral product, no winner-take-all platform war, just a small levy collected reliably on traffic that has to keep flowing. The intellectual challenge for an investor is that the durability is invisible in any single quarter and only becomes obvious across a decade. A snowstorm can dent a quarter; a device-industry destock can soften a year; a tariff can shave a margin point. None of it changes the underlying fact that the world will perform more surgeries next decade than this one, and that each of those surgeries requires something STERIS sells. The art is separating the noise from the toll.

What to watch from here is execution, plainly measured. Dan Carestio has guided STERIS to a fiscal 2027 outlook of 7–8% reported revenue growth and adjusted earnings of $11.10 to $11.30 per share, while deploying a doubled $1 billion buyback authorization at a measured pace.1 The interesting tension is whether a lifer's operational discipline can keep expanding margins against tariffs and input inflation, whether the X-ray transition delivers the share gains management promises, and whether AST's crown-jewel margins survive the medtech inventory cycle. STERIS has spent forty years turning an invisible, non-negotiable service into an annuity. The next few years will test whether that annuity can keep compounding—or whether the market has already paid in full for the privilege of owning it.

References

-

STERIS Announces Financial Results for Fiscal 2026 Fourth Quarter and Full Year — GlobeNewswire, 2026-05-11 ↩↩↩↩↩↩↩↩↩

-

STERIS plc (STE) Q4 Fiscal 2026 Earnings Call Transcript & Analyst Q&A — Seeking Alpha, 2026-05-12 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

STERIS plc Annual Report on Form 10-K for Fiscal Year Ended March 31, 2025 — SEC, 2025-05-28 ↩

-

STERIS to Acquire Cantel Medical — GlobeNewswire, 2021-01-12 ↩

-

STERIS Expands Healthcare Consumables Offering with Acquisition of Key Surgical for approximately $850 million — GlobeNewswire, 2020-10-06 ↩

-

STERIS Completes Divestiture of Dental Segment to Peak Rock Capital for $787.5 Million — FierceBiotech, 2024-06-03 ↩↩

-

STERIS Reaches $48.15 Million Settlement in Waukegan Ethylene Oxide Litigation — Cook County Record, 2025-03-24 ↩

-

Sotera Health Announces $408 Million Settlement to Resolve Illinois EtO Claims — Bloomberg, 2023-01-09 ↩

-

Proposal: Amendments to Commercial Sterilizer Ethylene Oxide NESHAP Rule — Environmental Protection Agency, 2026-03-13 ↩

-

STERIS to Acquire Synergy Health for $1.9 Billion in Tax Inversion — Reuters, 2014-10-13 ↩↩

-

STERIS to Acquire Becton Dickinson Surgical Instrumentation Assets for $540 Million — Medtech Dive, 2023-06-05 ↩

-

STERIS Gets FDA Clearance for System 1E — Medical Device and Diagnostic Industry (MDDI), 2010-04-12 ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube