Spire Inc.: The Story of America's Gas Utility Consolidator

I. Introduction and Episode Roadmap

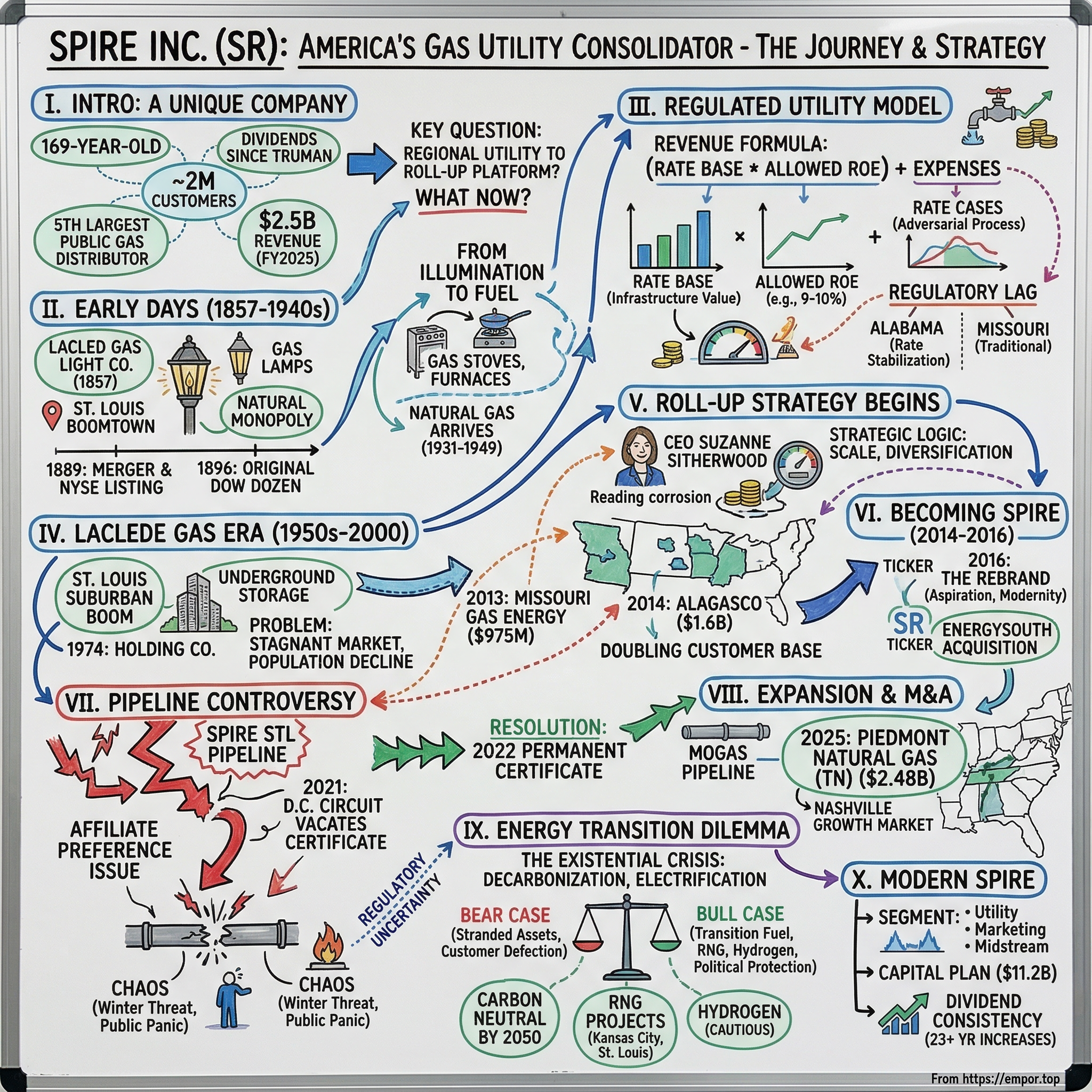

There is a peculiar category of company that most investors walk past without a second glance. It does not make headlines. It does not disrupt anything. It does not have a charismatic founder tweeting at three in the morning. And yet, it has been paying dividends since Harry Truman was president, it serves nearly two million customers who literally cannot take their business elsewhere, and its stock was trading on the New York Stock Exchange before most people alive today were born.

Meet Spire Inc., ticker SR. Based in St. Louis, Missouri, Spire is the fifth-largest publicly traded natural gas distribution utility in the United States. It generated roughly $2.5 billion in revenue in fiscal 2025 and serves approximately 1.7 million customers across Missouri, Alabama, and Mississippi. If you have ever turned on a gas stove in St. Louis, switched on a furnace in Birmingham, or heated water in Mobile, there is a good chance you were a Spire customer, whether you knew it or not.

The central question of this story is deceptively simple: how did a 169-year-old St. Louis gas company transform itself from a regional utility lighting street lamps before the Civil War into a multi-state roll-up platform buying billion-dollar businesses? And what happens to that strategy when the entire world starts asking whether we even need natural gas anymore?

This is a story about regulated utility economics, the hidden world of rate cases, M&A as a growth strategy in an industry where organic growth barely exists, and the existential question facing every gas utility on the planet: what happens when the world electrifies? Along the way, we will encounter a controversial pipeline that a federal court ordered shut down while it was serving 650,000 homes, a CEO who started her career reading corrosion meters, a stock that was one of the original twelve companies in the Dow Jones Industrial Average, and a corporate rebrand that asked customers to forget 150 years of history.

If you think utilities are boring, you are not paying attention. The numbers tell a story of quiet but relentless compounding. Since listing on the NYSE in 1889, making it the eighth-oldest continuously listed stock on the exchange, the company has survived two world wars, the Great Depression, the rise and fall of manufactured gas, the near-shutdown of its primary pipeline by a federal court, and the beginning of what may be the greatest energy transition since the invention of electricity itself. Through all of it, the dividends kept flowing.

II. The Early Days: Gaslight and Industrial America (1857-1940s)

Picture St. Louis in the 1850s. The city sits at the confluence of the Mississippi and Missouri Rivers, a roaring boomtown that had tripled in population in a single decade, from roughly 36,000 souls in 1840 to over 100,000 by 1850. Only New Orleans handled more river commerce. The streets are unpaved, the riverfront is choked with steamboats, German and Irish immigrants are pouring in by the thousands, and the air smells of coal smoke, horse manure, and ambition. This is the gateway to the American West, and everyone knows it.

But St. Louis had endured a catastrophic year in 1849 that tested the city's very survival. A cholera epidemic killed roughly 8,500 people, about one-tenth of the population. Then, on May 17, a fire that started on the steamboat White Cloud leapt to 22 other vessels and raced through the riverfront, destroying 418 buildings across 15 city blocks. The city rebuilt with characteristic stubbornness, but the experience underscored a fundamental truth: urban infrastructure mattered. Lighting, sanitation, water, gas, these were not luxuries. They were the difference between civilization and chaos.

The first gas company in St. Louis, the St. Louis Gas Light Company, had been chartered back in 1837, making St. Louis only the seventh American city to form one. But the company provided poor service and jacked up rates, prompting the Missouri legislature to authorize competition. On March 2, 1857, the legislature chartered the Laclede Gas Light Company, named after Pierre Laclede, the French fur trader who had founded St. Louis in 1764. The new company's mandate was straightforward: light the streets of St. Louis with gas lamps and deliver gas through underground pipelines to residents and businesses.

This was a full quarter century before Thomas Edison's practical incandescent light bulb. In 1857, if you wanted light after dark, your options were candles, whale oil lamps, kerosene, or gas. Gas was the high technology of its era, and the business of manufacturing it was both capital-intensive and technically demanding. You took coal, heated it in sealed ovens called retorts to keep oxygen out, purified the resulting gas, pressurized it, and piped it underground to your customers. The infrastructure required, gasworks, purification plants, miles of underground pipe, created a natural monopoly. It made no economic sense for two companies to dig up the same streets and lay competing pipe networks.

By 1889, Laclede had grown powerful enough to swallow its competitors entirely. That year, it merged with the original St. Louis Gas Light Company, the Carondelet Gas Company, and the St. Louis Gas Fuel and Power Company, keeping the Laclede Gas Light name. The consolidation was arranged with financing from Emerson McMillin, who brought Laclede into the American Light and Traction fold. On November 14, 1889, Laclede listed on the New York Stock Exchange, an event that makes it the eighth-oldest continuously listed stock still trading on the NYSE today.

Then came a remarkable distinction. In 1896, when Charles Dow and Edward Jones created the first Dow Jones Industrial Average, they selected twelve companies to represent American industry. Laclede Gas Light was one of the original "Dow Dozen," alongside names like American Tobacco, General Electric, and U.S. Leather.

It was removed a few years later as the index evolved toward heavier industrial and manufacturing firms, but the inclusion tells you something about how important gas utilities were to the industrial economy of that era. Of those original twelve companies, Laclede is one of the very few that survived in recognizable form through to the present day. General Electric, the only other original Dow component that lasted deep into the modern era, was finally removed from the index in 2018.

The early twentieth century brought two existential challenges.

First, electric lighting arrived and rapidly displaced gas lamps, the very product that had justified Laclede's existence. The company adapted by pivoting from illumination to fuel. Gas stoves, gas furnaces, gas water heaters. By 1906, Laclede was actively promoting gas cooking in St. Louis and offering financing programs for gas appliances. The strategic lesson was clear: when your core product gets disrupted, find new applications for the underlying infrastructure. This lesson, as we will see, is directly relevant to the challenge Spire faces today with building electrification.

Second, in 1909, North American Company, the large utility conglomerate that had acquired Laclede, decided to sell after lawyers warned of potential Missouri antitrust violations. The buyer was a consortium of St. Louis capitalists led by two remarkable figures: George Herbert Walker, whose grandson and great-grandson would both become president of the United States, and Adolphus Busch, the brewing magnate behind Anheuser-Busch. The Walker-Busch syndicate paid $7 million for a controlling stake and had grand plans to bring natural gas to St. Louis by pipeline from gas fields they owned in Caddo Parish, Louisiana.

That pipeline vision took decades to realize. Natural gas finally arrived in St. Louis in 1931, and by 1932, Laclede began supplying a blend of natural and manufactured gas. The full conversion to all-natural gas would not come until 1949, when a parallel 24-inch pipeline was completed. But the shift was transformative. Natural gas was cleaner, more efficient, and cheaper to deliver than manufactured coal gas. The company dropped "Light" from its name in 1950, becoming simply Laclede Gas Company, a recognition that its business had fundamentally changed from illumination to fuel distribution.

Through the Great Depression and two world wars, Laclede survived as regulated utilities do: by providing an essential service that people needed regardless of economic conditions. The regulatory compact that had emerged in the early twentieth century, states began creating public service commissions around 1907, with Missouri establishing its own in 1913, provided the framework. In exchange for a monopoly franchise, the utility submitted to rate regulation, and in return received the opportunity to earn a reasonable return on its invested capital. It was not glamorous. But it was durable. And that durability would prove to be the foundation of everything that came next.

III. The Regulated Utility Business Model: A Deep Dive

Before we can understand why Spire made the strategic choices it did, we need to understand how regulated utilities actually make money, because it is genuinely unlike any other business model in capitalism. Most people assume utilities just charge customers for gas and pocket the difference between revenue and costs. The reality is far more interesting, and far more constrained.

Think of a regulated utility as a business operating inside a box built by the government. The box has very specific rules. Rule one: you have a monopoly. No one else can sell piped natural gas in your territory. Rule two: because you have a monopoly, you cannot charge whatever you want. A state public service commission sets your prices. Rule three: in exchange for accepting price regulation, the commission will set rates high enough for you to earn a "reasonable return" on your invested capital. And rule four: if you want to change anything significant, your rates, your investments, your operations, you need to go through the commission.

The key formula is elegantly simple. A utility's allowed revenue equals its rate base multiplied by its allowed return on equity, plus its operating expenses and depreciation.

The rate base is essentially the total value of all the physical infrastructure the utility has invested in: pipes, meters, compressor stations, buildings, vehicles. Think of it as the denominator of the return equation. The allowed return on equity, or ROE, is the profit margin the commission permits, typically in the range of 9 to 10 percent for gas utilities. Think of it as the numerator.

So if you have a $4 billion rate base and an allowed ROE of 10 percent, you are entitled to earn roughly $400 million in profit before interest, shared between debt holders and equity holders. It is a fundamentally different model from competitive businesses where profit is the residual after costs and is determined by market dynamics. In the utility world, profit is predetermined by a government body, and the only real variable is how large your rate base grows.

This creates a fascinating set of incentives. The single most important thing a utility can do to grow its earnings is to grow its rate base. Every dollar of new capital investment, whether it is replacing an aging pipeline, installing new meters, or upgrading a compressor station, adds to the rate base and thus to the revenue the utility is allowed to collect. This is why utilities love capital expenditure. It is not a cost center the way it is at most companies. It is the engine of earnings growth.

The mechanism for adjusting rates is called a rate case, and it is worth understanding in some detail because rate cases are the beating heart of the utility business.

When a utility believes its costs have risen enough to justify higher prices, it files a formal request with the state commission. What follows is an adversarial, quasi-judicial proceeding that can take a year or more. The utility presents its case for higher rates. Consumer advocates argue for lower increases. Commission staff conducts independent analysis. Expert witnesses testify about the appropriate ROE, the prudence of the utility's investments, and whether every dollar of spending was justified. At the end, the commission issues an order setting new rates, and those rates remain in effect until the next rate case.

The process is expensive. A major rate case can cost a utility several million dollars in legal fees, consulting costs, and expert testimony. But the stakes are enormous: the difference between a 9.5 percent allowed ROE and a 10 percent allowed ROE on a $4 billion rate base is $20 million per year in additional profit. That is why utilities employ full-time regulatory affairs teams and treat rate cases with the seriousness of a Supreme Court argument.

Understanding this process is essential because it explains so much about utility behavior. Why do utilities have conservative cultures? Because a commission can disallow imprudent spending, and regulators have long memories. Why is organic growth so hard? Because you cannot simply sell more product to existing customers; they use what they use, governed by weather and building square footage. Why do utilities pay such reliable dividends? Because cash flows are predictable when your prices and volumes are essentially set by the government.

There is a concept called "regulatory lag" that shapes everything about utility management. Regulatory lag is the delay between when a utility incurs costs and when it receives rate relief through a commission order. If a utility spends $500 million on new pipelines in 2024 but does not file a rate case until 2025 and does not receive new rates until 2026, it is earning below its allowed return for two years. This is why utilities time their rate case filings carefully and why some states have adopted mechanisms like infrastructure trackers or formula rate plans that reduce lag. Alabama's Rate Stabilization and Equalization mechanism, which Spire benefits from, is specifically designed to minimize this lag by adjusting rates automatically within an allowed ROE band. Missouri's traditional rate case process, by contrast, can leave Spire under-earning for extended periods between filings. This jurisdictional difference matters enormously for understanding why geographic diversification across regulatory frameworks has real financial value.

For investors, regulated utilities offer something rare: inflation-protected, bond-like returns with equity upside. When costs rise, the utility files a rate case and passes those costs through to customers. The dividend is covered by predictable earnings. The downside is limited because people need heat. The upside is limited because the commission caps your returns. It is, in the words of one utility executive, "a business where you trade home runs for the fact that you never strike out."

But here is the problem for an ambitious management team: if your only lever for growth is capital investment in your existing territory, and your territory is a mature market with flat or declining customer count, you are on a treadmill. You can replace old pipes with new ones, and that grows the rate base a bit. But you cannot fundamentally change the trajectory. To really grow, you need to do something dramatic.

You need to buy another utility.

IV. The Laclede Gas Era: St. Louis Consolidation and Stability (1950s-2000)

The postwar decades were Laclede Gas's golden age of quiet growth. As millions of returning GIs married, had children, and bought houses in the suburbs, the demand for natural gas heating exploded. St. Louis County's population nearly doubled from roughly 406,000 in 1950 to over 700,000 by 1960. More than 83,000 new homes were built in St. Louis County during the 1950s alone, and another 96,000 in the 1960s. Nearly all of them connected to natural gas for heating, cooking, and hot water. Laclede's customer base swelled to nearly 100,000 by 1950 and kept climbing.

The company invested in underground natural gas storage in Florissant, Missouri during the 1950s, a smart operational move that allowed it to purchase gas during low-demand summer months when prices were cheap and store it for the winter heating season when demand peaked. This "buy low, store, deliver high" approach became a cornerstone of gas utility economics nationwide.

In 1974, Laclede reorganized into a holding company structure, creating The Laclede Group with Laclede Gas Company as its primary subsidiary. The move was a classic utility playbook: holding company structures provided flexibility for future diversification and, eventually, acquisitions that pure utility charters did not easily accommodate.

But beneath the surface stability, trouble was brewing. The city of St. Louis was hollowing out. From its peak population of roughly 857,000 in 1950, the city shed residents at an alarming rate: down to 750,000 by 1960, 622,000 by 1970, and continuing to plummet through subsequent decades. The culprit was a peculiar 1876 decision, known locally as "The Great Divorce," in which St. Louis had separated from St. Louis County and fixed its city boundaries permanently at 61 square miles. The city could never annex again. So as suburban development boomed, all that growth, all those new gas customers and their property taxes, accrued to the county while the city's tax base and population cratered. One local businessman later called it "roughly equivalent in economic consequence to England giving up the thirteen colonies."

The impact on Laclede was significant but not fatal. The company served both the city and ten surrounding counties in eastern Missouri, so it captured suburban growth even as the urban core declined. But by the late 1990s and early 2000s, the math was getting grim. St. Louis was not a growth market. New housing construction had plateaued. Customer count was essentially flat. The company was a reliable dividend payer, well-run, conservative, deeply embedded in the civic fabric of St. Louis. But it was stuck.

In 1996, the company created Laclede Energy Resources to market natural gas wholesale across multiple states, its first real step outside the regulated utility box. In 2001, The Laclede Group became a full public holding company. These were incremental moves, tentative fingers reaching beyond the comfort zone. But the leadership team was beginning to grapple with a question that would define the company's next two decades: if you cannot grow organically in a mature, shrinking market, how do you grow at all?

The answer, when it came, would transform a 150-year-old local utility into something its founders could never have imagined.

V. The Roll-Up Strategy Begins: Alabama Acquisitions (2000s-2014)

The pivot point came not from a flash of strategic brilliance but from cold arithmetic. By the early 2010s, The Laclede Group served roughly 632,000 customers in eastern Missouri. Growth was essentially zero. The population of the St. Louis metropolitan area was stagnant. New housing starts were modest. The company was earning a reasonable return on its rate base, paying its dividend, and slowly replacing old pipes. It was a perfectly adequate business with no path to meaningful growth.

Then came Suzanne Sitherwood.

Sitherwood arrived at Laclede in 2011 as president and was promoted to CEO in 2012. Her background was unusual for a gas utility chief executive and worth dwelling on, because it explains the ambition that followed. She had spent 31 years at AGL Resources in Atlanta, now part of Southern Company Gas, starting as a corrosion technician who read cathodic protection measurements at customer meters while attending college at night. She became AGL's first female field engineer, then its first female vice president of engineering, then senior vice president of gas operations. She eventually served as president of Atlanta Gas Light, Chattanooga Gas, and Florida City Gas, overseeing more than 1.6 million customers. She knew gas utility operations from the pipeline up, literally. And she had seen what scale could do.

At AGL Resources, Sitherwood had watched the utility consolidation wave build through the 2000s and understood the strategic logic. Regulated utilities in small, single-state territories were subscale. They paid higher costs per customer for shared services like IT, billing, and procurement. They had concentrated regulatory risk, meaning one hostile commission could torpedo your returns. And they had no growth story to tell Wall Street. The solution was consolidation: buy adjacent utilities, spread fixed costs across a larger customer base, diversify regulatory exposure, and create a credible growth narrative.

The first major deal under Sitherwood's watch landed in September 2013 with the acquisition of Missouri Gas Energy from a subsidiary of Energy Transfer Partners for $975 million. MGE served over 155 communities in western Missouri, including the Kansas City and Joplin areas. The acquisition doubled Laclede's Missouri service territory from roughly 632,000 customers to more than 1.1 million, making it the largest natural gas distribution company in the state. This was not a small bolt-on. It was a transformative deal that gave Laclede statewide coverage in Missouri and proved the management team could execute large-scale M&A in a regulated environment.

The regulatory approval process was instructive. Missouri Public Service Commission review of a utility acquisition involves public hearings, expert testimony, consumer advocate scrutiny, and conditions that the acquiring company must accept. The commission wanted assurance that Missouri ratepayers would not be harmed by the deal, that service quality would be maintained, and that acquisition costs would not be passed through to customers. Laclede navigated this successfully, establishing a playbook for the bigger deals to come.

Barely a year later, in April 2014, The Laclede Group announced an even more ambitious move: the acquisition of Alabama Gas Corporation, known as Alagasco, from Energen Corporation for $1.6 billion. This was the deal that truly changed the company. Alagasco was the largest natural gas utility in Alabama, serving more than 422,000 customers, with roots tracing back to the Montgomery Gas Light Company in 1852. The deal price included the assumption of $250 million of Alagasco's long-term debt plus approximately $1.35 billion in cash. The effective purchase price after tax benefits was roughly $1.34 billion.

The strategic rationale was compelling on multiple dimensions. Geographic diversification moved the company beyond Missouri's regulatory jurisdiction for the first time. Alabama's Public Service Commission operated under a different regulatory framework, including a Rate Stabilization and Equalization mechanism that provided more predictable rate adjustments. Scale economies would flow from spreading corporate overhead across a 55 percent larger customer base. And the deal made Laclede the largest natural gas distribution company in both Missouri and Alabama.

The Alabama PSC approved the acquisition after public hearings that concluded in July 2014, and the deal closed on August 31, 2014. The combined company now served approximately 1.55 million customers. In barely two years, Sitherwood had more than doubled the company's size and established it as a multi-state platform.

These were not the only utilities changing hands. The 2000s and 2010s saw a broad wave of gas utility consolidation. Southern Company acquired AGL Resources, Sitherwood's former employer, for roughly $12 billion in 2016. Duke Energy bought Piedmont Natural Gas. AltaGas of Canada acquired WGL Holdings for $4.5 billion. Low interest rates made debt-financed acquisitions cheap. Predictable utility cash flows made them reliable targets. And the growth limitations of single-state territories made consolidation strategically obvious. The Laclede Group was not inventing the playbook, but it was executing it with exceptional speed and discipline.

The proof of concept was in the numbers. Before the M&A campaign, The Laclede Group was a $700 million revenue company serving 632,000 customers in one state. After Alagasco, it was approaching $2 billion in revenue, serving 1.55 million customers across two states. Market value had more than doubled. The question was no longer whether the roll-up strategy worked. The question was: what comes next?

VI. The Rebrand and Laclede/Alagasco Integration: Becoming Spire (2014-2016)

Walk into the corporate offices at 700 Market Street in downtown St. Louis in the fall of 2015, and you would find a company experiencing an identity crisis. The Laclede Group was the parent. Laclede Gas served eastern Missouri. Missouri Gas Energy served western Missouri. Alagasco served Alabama. Each had its own brand, its own regional identity, and its own century-plus of local history. Customers in Birmingham had never heard of Laclede. Customers in St. Louis had no idea what Alagasco was. And the corporate name, The Laclede Group, meant nothing outside of Missouri.

Sitherwood recognized that if the company was going to continue its growth trajectory, it needed a unified brand that transcended regional identities. More importantly, it needed a name that signaled ambition, modernity, and scale rather than provincial heritage. The decision to rebrand was not cosmetic. It was strategic.

On April 28, 2016, shareholders of The Laclede Group voted to rename the company Spire Inc. The next day, trading began on the NYSE under the new ticker symbol SR, replacing the historic LG that had graced the exchange since 1889. In 2017, all the individual utility subsidiaries, Alagasco, Laclede Gas, Missouri Gas Energy, and the recently acquired Mobile Gas and Willmut Gas, would officially transition their names and customer-facing identities to the Spire brand.

The name Spire was chosen carefully. It evoked aspiration, elevation, something pointed upward. Sitherwood explained the rationale bluntly: "We needed a name to better reflect the company we are becoming." And the numbers supported the ambition. In three years, the company had added nearly one million natural gas customers, expanded across three states, and more than quadrupled in market value.

In September 2016, even before the subsidiary rebranding was complete, Spire closed its third major acquisition: EnergySouth, purchased from Sempra U.S. Gas and Power for $344 million including the assumption of $67 million in debt. EnergySouth owned Mobile Gas, serving about 85,000 customers in southern Alabama, and Willmut Gas, serving roughly 19,000 customers in Mississippi. The deal expanded Spire's Alabama footprint and, critically, gave it a presence in a third state.

The combined company now served more than 1.7 million customers. From a standing start of 632,000 customers in a single state just three years earlier, Spire had nearly tripled its customer base through acquisitions. Revenue had grown from roughly $700 million to approximately $2 billion. Enterprise value had increased more than sixfold.

But the integration was not seamless. Culture clashes between 100-plus-year-old utilities are real. Missouri PSC staff raised pointed concerns about cost allocation in the merged entity, concluding in one report that "acquisition and integration costs have improperly been allocated to Laclede Gas" and that "all the utility-managing expertise at the company lies with Laclede Gas, not Spire," suggesting the parent company was extracting value from its Missouri utility to support the broader corporate structure. Spire disputed these findings as "flawed, unfounded, and erroneous," arguing that the shared services model "saves money for our customers and lowers rates."

This tension, between creating corporate scale and protecting individual jurisdictions' ratepayers, is the fundamental challenge of multi-state utility holding companies. Missouri customers did not want to subsidize Alabama acquisitions. Alabama regulators did not want their utility's culture homogenized by a St. Louis parent. Mississippi was so new that nobody knew what to expect. Navigating these competing interests required diplomatic skill, regulatory sophistication, and patience.

For investors watching from the outside, the rebrand accomplished something important: it transformed the narrative. Laclede Gas was a value stock, a Midwestern dividend payer. Spire Inc. was a growth story, a utility platform with demonstrated M&A capability and runway for further consolidation. Whether the market valued that transformation appropriately is a debate worth having. But the transformation itself was undeniable.

And then, just as the integration story was settling into a rhythm, the company made a bet on infrastructure that would blow up in the most dramatic way a regulated utility can experience.

VII. Spire Storage and the Pipeline Controversy (2016-2021)

In 2015, even as the Alagasco integration was underway, Spire's leadership identified what they called a "critical need" for supply diversification in the Greater St. Louis region. The argument went like this: St. Louis depended on a handful of third-party interstate pipelines for its natural gas supply, and those pipelines drew primarily from Gulf Coast and Midcontinent production basins. If the company could build its own pipeline connecting to the Rockies Express Pipeline, it would gain access to Appalachian shale gas from the Marcellus and Utica formations, creating redundancy and potentially lower costs.

In July 2016, Spire filed with the Federal Energy Regulatory Commission to build the Spire STL Pipeline: 65 miles of new 24-inch-diameter underground pipe running from Scott County, Illinois to Spire's existing distribution system in St. Louis. The project was estimated to cost around $220 million and would be capable of transporting 400,000 dekatherms per day.

Here is where the story gets complicated, and where understanding regulatory dynamics becomes essential. To follow it, you need to know the difference between two completely different regulatory worlds.

State public service commissions regulate the distribution of gas to homes and businesses. They care about reliability, affordability, and safety for end-use customers. FERC, the Federal Energy Regulatory Commission, regulates interstate pipelines. FERC cares about whether there is genuine market demand to justify new pipeline construction, and it uses a framework called the 1999 Certificate Policy Statement to evaluate applications.

The standard evidence of need under FERC's framework is precedent agreements: contracts with shippers who commit to use the pipeline's capacity. These are supposed to be arm's-length transactions demonstrating real market demand. Spire STL Pipeline LLC solicited third-party shippers and came up empty. No independent gas buyer wanted to commit to long-term capacity on the new line. So Spire STL did what seemed obvious from the inside but would prove legally catastrophic: it signed its sole precedent agreement with Spire Missouri, its own corporate affiliate, for 87.5 percent of the pipeline's capacity.

The optics were terrible. A company wanted to build a pipeline. It could not find any outside customer willing to sign a contract. So it signed a contract with itself and presented that to the federal regulator as evidence of market need.

This is the "affiliate preference" issue that would haunt the project for years. The concern is straightforward: when a pipeline's only customer is a corporate sibling, is there really independent market demand, or is the parent company just funneling captive ratepayer money to a pipeline subsidiary it also owns? Environmental groups and pipeline competitors seized on this question with vigor.

On August 3, 2018, FERC approved the pipeline in a 2-1 vote, issuing a Certificate of Public Convenience and Necessity. But the dissents were fierce. Commissioner Richard Glick wrote that FERC had "ignored record evidence of self-dealing" and that the affiliate precedent agreement was "hardly probative" of genuine market need. Commissioner Cheryl LaFleur raised similar concerns about inadequate scrutiny.

Their dissents would prove prescient.

Construction began in early 2019 and was plagued by historic flooding along the Mississippi and Illinois Rivers that drove costs up to roughly $287 million. Spire prosecuted eminent domain actions against more than 100 landowners across 200-plus acres. The pipeline went into service in late 2019.

Then, on June 22, 2021, the roof caved in.

The U.S. Court of Appeals for the District of Columbia Circuit, in a unanimous ruling in Environmental Defense Fund v. FERC, vacated the pipeline's certificate entirely. The opinion was devastating. The court found that FERC had "ignored record evidence of self-dealing" between the pipeline developer and its affiliate. It ruled that FERC had "refused to seriously engage with non-frivolous arguments challenging the probative weight of the affiliated precedent agreement." And it concluded that FERC had failed to conduct the interest-balancing analysis required by its own policy, weighing the pipeline's benefits against adverse effects on existing pipelines, landowners, and ratepayers.

In practical terms, a federal court had just ordered the effective shutdown of a pipeline serving 650,000 homes and businesses. In the middle of a city. With winter approaching.

Pause on that for a moment. This was not a theoretical regulatory dispute. This was a court saying that an operational piece of critical infrastructure, one that was already built, already flowing gas, already integrated into the supply network for a major American metropolitan area, had to be shut down because the original approval process was flawed. It was, as one analyst described it, "an unprecedented mess."

What followed was a drama that played out across multiple branches of government. Spire launched an aggressive public communications campaign warning customers of potential gas outages, so aggressive that the Missouri PSC accused the company of creating "unnecessary panic and confusion" and characterized the messaging as "an attempt by Spire to mobilize public opinion, through fear, in order to potentially pressure federal authorities." The Environmental Defense Fund demanded Spire halt "false and defamatory" messaging after EDF staff received threatening communications from alarmed citizens.

Missouri's Republican Congressional delegation rallied behind the pipeline, with Representative Blaine Luetkemeyer leading letters to FERC Chairman Glick urging emergency authorization. The Missouri PSC intervened in the FERC proceedings. Spire filed emergency applications with FERC, sought a stay from the D.C. Circuit, and eventually petitioned the U.S. Supreme Court.

FERC issued a 90-day temporary certificate in September 2021, then an extended temporary certificate in December 2021, allowing continued operations while it reconsidered the pipeline on remand. In April 2022, the Supreme Court declined to hear Spire's appeal, definitively upholding the D.C. Circuit's ruling.

The financial impact was significant but manageable. Morgan Stanley estimated the pipeline represented roughly $0.35 per share in annual earnings and approximately $5.00 per share in potential asset write-off risk. The stock sold off on the initial ruling and remained under pressure through 2022. This came on top of a separate $2.29 per share charge Spire had already taken in August 2020 for an 80 percent write-down of its compressed natural gas storage investment, further eroding investor confidence in management's non-utility capital allocation.

On December 15, 2022, FERC reissued a permanent Certificate of Public Convenience and Necessity for the pipeline. All five commissioners voted in favor, though Chairman Glick, who had originally dissented in 2018, voted "reluctantly," acknowledging that the record now showed the pipeline was needed, largely because Spire's actions had created a fait accompli. The pipeline was built, customers depended on it, and shutting it down would harm the very people the law was supposed to protect.

The lessons of the Spire STL Pipeline saga are worth lingering on. First, regulatory strategy matters enormously. Relying on an affiliate contract as the sole evidence of need for a major infrastructure project was a calculated gamble that failed spectacularly. Second, FERC and state commissions operate in different universes. State regulators want to ensure reliable supply. Federal regulators are supposed to conduct rigorous need assessments. When those imperatives collide, the result is chaos. Third, building first and asking permission later is a dangerous strategy that can work, as it ultimately did here, but at enormous cost to credibility and shareholder value. The pipeline saga prompted FERC to begin broader reform of its affiliate transaction policies, a lasting institutional consequence.

For Spire, the permanent certificate resolved the immediate crisis. But the episode left scars on the company's relationship with regulators, environmental groups, and investors who questioned whether management had been too aggressive in pursuing the project.

VIII. Geographic Expansion and Recent M&A Activity (2017-Present)

Even as the pipeline drama consumed management attention and investor confidence, Spire continued building its utility platform through targeted acquisitions. The strategy remained consistent: identify adjacent gas distribution territories with favorable regulatory environments and reasonable customer economics, acquire them, integrate them into Spire's operational platform, and grow the rate base.

In January 2024, Spire completed the acquisition of the MoGas Pipeline and Omega Pipeline Company, adding approximately 263 miles of natural gas transmission infrastructure in Missouri. These were smaller, infrastructure-focused deals that expanded Spire's midstream capabilities and complemented its distribution network. FERC approved the merger of the STL and MoGas pipelines, which was completed on January 1, 2026, with the combined entity operating as Spire MoGas Pipeline.

Then, in July 2025, Spire announced its most ambitious deal since the Alagasco acquisition: the purchase of Piedmont Natural Gas's Tennessee distribution business from Duke Energy for $2.48 billion on a cash-free, debt-free basis. The deal would add more than 200,000 customers in the Nashville metropolitan area and approximately 3,800 miles of distribution and transmission pipelines. Piedmont Natural Gas is the largest investor-owned gas utility in Tennessee, and the Nashville market is one of the fastest-growing metropolitan areas in the United States.

The purchase price represented roughly 1.5 times the estimated 2026 rate base, a premium that reflected the quality of the customer base and growth potential of the Nashville market. Financing was planned through a balanced mix of debt, equity, and hybrid securities. Spire was also evaluating the potential sale of its natural gas storage assets to partially fund the transaction. As of early 2026, all required regulatory approvals had been obtained except from the Tennessee Public Utility Commission, with closing expected in the first calendar quarter of 2026.

If completed, the Piedmont Tennessee deal would push Spire's total customer base to approximately two million across four states, Missouri, Alabama, Mississippi, and Tennessee. It would also mark a return to the bold, transformative M&A that had defined the Sitherwood era, after several years of smaller, incremental deals. The Nashville market is particularly interesting because it represents a fundamentally different growth profile than anything in Spire's portfolio. Nashville's population grew by more than 20 percent in the 2010s and has continued expanding rapidly, driven by corporate relocations, a booming healthcare industry, and cultural cachet that makes it a magnet for young professionals. For a gas utility, population growth means new housing starts, new gas connections, and organic rate base expansion that does not require filing a rate case.

The Tennessee regulatory environment adds another dimension. The Tennessee Public Utility Commission, while less familiar to Spire's management team than Missouri or Alabama's regulators, is generally considered constructive for utilities. Tennessee allows formula-rate mechanisms and infrastructure riders that can reduce regulatory lag. If Spire can replicate the operational integration success of Alagasco in a faster-growing market with a supportive regulatory framework, the Piedmont deal could become the most value-creative acquisition in the company's history.

The M&A criteria had evolved but remained recognizable. Adjacent or complementary territories with manageable regulatory environments. Customer economics that supported the purchase multiple. Growth markets where possible, a notable shift from the mature St. Louis and Birmingham territories that formed the core. Nashville's demographics, young, growing, economically vibrant, offered something Spire's existing markets largely did not: organic customer growth.

The limits of the strategy are also becoming apparent. There are only so many gas distribution utilities of sufficient size and quality available for acquisition. Each deal adds regulatory complexity, since every state commission has its own culture, precedents, and political dynamics. And each acquisition requires capital, which means either issuing equity that dilutes existing shareholders or taking on debt that pressures credit ratings. Spire's total long-term debt stood at approximately $3.4 billion as of fiscal 2025, and its credit ratings, while investment-grade, have come under pressure. S&P had moved the outlook to negative, and Moody's rated subordinated debt at Baa3, the lowest rung of investment grade.

The question going forward is whether Spire can continue to acquire without overleveraging, and whether the returns on these acquisitions justify the capital deployed. The early deals, MGE at $975 million and Alagasco at $1.6 billion, created clear strategic value. Whether paying $2.48 billion for 200,000 Nashville customers generates comparable returns remains to be seen.

IX. The Energy Transition Dilemma: Gas Utilities in a Decarbonizing World (2018-Present)

There is a question that hangs over every natural gas utility in America, and it is the closest thing this industry has to an existential crisis: what happens when the world decides it does not need your product anymore?

The threat is not theoretical. Building electrification, the movement to replace gas furnaces, gas stoves, and gas water heaters with electric heat pumps and induction cooktops, has gone from environmental fringe to mainstream policy in barely a decade. More than 70 California cities adopted gas bans or all-electric building codes before legal challenges began rolling some back. New York has pushed aggressive electrification mandates. The International Energy Agency projects that heat pumps will overtake gas furnaces in global heating equipment sales. For a gas distribution utility whose entire business model depends on buildings connecting to and staying connected to the gas grid, this is not an abstract policy debate. It is a mortal threat to the rate base.

Spire's response has been a blend of advocacy, investment, and hedging that reflects the company's regulated nature and Midwestern pragmatism.

In July 2020, Spire announced a commitment to achieve carbon neutrality by 2050, becoming one of the first U.S. natural gas utilities to make such a pledge. The path to that goal runs through several strategies. First, infrastructure modernization. By replacing aging cast iron and bare steel pipes with modern polyethylene and coated steel, Spire reduces methane leaks, which are both an environmental problem and a safety concern. The company reported achieving a greater than 50 percent reduction in methane emissions from its distribution system since 2005, with a target of 73 percent reduction by 2035. More than 57 percent of Spire's capital investment goes to infrastructure upgrades, which serves the dual purpose of reducing emissions and growing the rate base.

Second, renewable natural gas. RNG is produced by capturing methane from organic waste sources, landfills, wastewater treatment plants, agricultural operations, and processing it to pipeline-quality standards. In January 2024, Spire announced a partnership with KC Water to build Kansas City's first RNG facility at the Blue River Wastewater Treatment Plant, a roughly $20 million project expected to produce about 0.3 billion cubic feet per year, enough for approximately 4,300 homes. A separate landfill RNG project near St. Louis was expected to come online in early 2025, producing roughly 1.2 billion cubic feet annually.

These are real projects with real environmental benefits. But they are also small relative to Spire's total throughput. An internal email that surfaced from a Spire engineer stated bluntly: "RNG will not sustain our industry at its present size." This is the uncomfortable truth that every gas utility faces. RNG is a useful incremental tool, but the total supply of organic waste methane in the United States is a small fraction of total natural gas consumption. The American Gas Foundation has estimated that RNG could supply roughly 4 to 7 percent of current U.S. natural gas demand by 2040 under optimistic scenarios.

You cannot replace a trillion-cubic-foot-per-year industry with landfill gas. The math simply does not work at scale, no matter how many individual projects succeed.

Third, and perhaps most debated among energy analysts, hydrogen.

Spire's position on hydrogen has been notably more cautious than some peers. SoCalGas, for example, has more than ten active hydrogen pilot projects and is the most aggressive gas utility in the country on hydrogen blending. National Grid has set targets for its gas mix to include 20 percent green hydrogen by 2040. Spire's leadership, by contrast, has said hydrogen is "clearly ten years down the road before it makes economic sense." The company describes itself as in "the very beginning stages of considering it." Whether this is prudent conservatism or strategic lag depends on how quickly hydrogen technology and economics evolve.

Fourth, and perhaps most importantly for investors, political protection. In July 2021, Missouri Governor Mike Parson signed House Bill 734, which bars any Missouri subdivision from adopting ordinances that prohibit utility connections based on energy type. Missouri is one of roughly 20 states that have passed such preemption laws, effectively shielding gas utilities from local electrification mandates. This does not eliminate the long-term threat of customer choice shifting away from gas, but it removes the most immediate risk of regulatory bans forcing disconnection.

The competitive landscape is worth noting. Among Spire's peer group, SoCalGas faces the most hostile regulatory environment in California but has responded with the most aggressive alternative fuel strategy. National Grid has committed to fossil-free gas and electric networks in Massachusetts and New York by 2050 but recently canceled a geothermal pilot project after determining it was not economically viable. Atmos Energy focuses on transporting RNG through its existing system, currently handling about 8 billion cubic feet annually from six active projects.

The bull case for gas utilities in the energy transition rests on several arguments: natural gas is a "transition fuel" needed for decades while renewable electricity scales; electrification of space heating is technically difficult in cold climates; RNG and hydrogen can partially decarbonize the gas grid; and the infrastructure itself has value even if the molecules flowing through it change. The bear case is equally compelling: heat pump technology is improving rapidly and is already cheaper to operate than gas furnaces in many climates; new construction is increasingly all-electric; declining customer counts would spread fixed costs over fewer ratepayers, raising bills and accelerating defection; and stranded asset risk means today's pipeline investments may be worthless in 30 years.

For Spire specifically, the Missouri and Alabama markets offer some insulation. These are not coastal progressive states rushing to ban gas. They are politically conservative jurisdictions where preemption laws protect gas utility connections and where electrification mandates are unlikely in the near term. But "near term" and "forever" are different things. The energy transition is real, even if its timeline is uncertain. And a company whose entire business model depends on buildings connecting to gas pipes cannot afford to be wrong about how fast that transition moves.

The timeline question is perhaps the most important variable in valuing any gas utility stock. If electrification takes 50 years, Spire's current investments will generate returns for decades and the company has ample time to evolve. If it takes 20 years, the math gets dramatically harder. Consider that a pipeline installed today has a regulatory useful life of 40 to 60 years. If building electrification reduces gas demand materially within 25 years, that pipeline still has book value that ratepayers are paying for but may no longer need. This is the stranded asset problem, and it is not hypothetical. It is the central analytical challenge for anyone trying to value a gas utility on a long-term basis. The honest answer is that nobody knows how fast the transition will move, and the uncertainty itself is a form of risk that the market may not be fully pricing.

X. Modern Business Deep Dive: Operations, Culture, and Strategy (2020-Present)

Spire's corporate structure reflects its evolution from a single-state utility to a multi-segment energy platform. The Gas Utility segment, which generates the vast majority of earnings, encompasses Spire Missouri, serving approximately 1.2 million customers, Spire Alabama, serving roughly 430,000 customers, and Spire Gulf and Spire Mississippi, serving a combined 100,000 customers. In fiscal 2025, the Gas Utility segment produced adjusted earnings of $231.4 million.

The Gas Marketing segment, operating as Spire Marketing from a Houston office, provides non-regulated natural gas marketing and related services across the United States. This is the evolved version of Laclede Energy Resources, created back in 1996. It contributed $25.9 million in adjusted earnings in fiscal 2025, a small but growing piece of the business.

The Midstream segment, which includes the Spire STL Pipeline, Spire MoGas Pipeline, and Spire Storage operations in Wyoming and Oklahoma, produced $56.3 million in adjusted earnings in fiscal 2025, up sharply from $33.5 million the prior year. The growth was driven by additional storage capacity and the MoGas acquisition. Management projects the fiscal 2026 midstream earnings mix at roughly 65 percent storage and 35 percent pipeline.

Capital allocation tells you everything about a utility's priorities. Spire invested approximately $875 million in fiscal 2025, up from $800 million in fiscal 2024. More than 90 percent flows into the regulated rate base, which is the foundation of earnings growth. The company raised its 10-year capital investment target to $11.2 billion through fiscal 2035, up significantly from a prior $7.4 billion target. This is not a company pulling back on investment. It is a company doubling down on infrastructure.

To put that $11.2 billion figure in context, it represents roughly three times Spire's current market capitalization being plowed into physical assets over a decade. The strategy is essentially a bet that regulators will continue to approve these investments and allow Spire to earn returns on them. If the regulatory compact holds, that capital deployment translates into substantial rate base growth and, by extension, earnings growth that underpins the dividend. If the compact frays, whether through ROE compression, disallowance of investments deemed imprudent, or stranding risk from the energy transition, those capital dollars become liabilities rather than assets. The ratio of capex-to-depreciation is another telling metric: Spire is investing roughly twice what it depreciates each year, meaning the rate base is growing in real terms, not just treading water through asset replacement.

The technology modernization story, while not flashy, is operationally significant. Spire has been upgrading its metering infrastructure to Advanced Metering Infrastructure, starting with the Mobile, Alabama region where more than 92,000 meters were upgraded beginning in 2020. AMI meters use low-power radio frequency signals for automated meter reading, replacing manual drive-by reads. The technology enables hourly and on-demand meter reads, meaning anomalies like gas leaks or emergency situations can be detected in near real-time rather than waiting for monthly readings. Geographic Information Systems support engineering design, cost estimation, and asset management across the entire pipeline network.

The workforce comprises approximately 3,500 employees. Like most utilities, Spire faces the challenge of an aging workforce and a nationwide shortage of skilled trades workers. Pipeline technicians, field engineers, and construction crews are difficult to recruit and take years to train. The company has invested in training programs and competitive compensation, but the demographic challenge is industry-wide and has no quick fix. The American Gas Association has estimated that roughly half the utility workforce will be eligible to retire within the next decade, and the skilled trades pipeline, both figuratively and literally, has not kept pace. Spire has responded with apprenticeship programs and partnerships with community colleges in Missouri and Alabama, but the labor constraint is real and could become a bottleneck for the ambitious capital investment plan if not managed carefully.

Safety culture in a gas utility is not an HR talking point; it is an operational imperative with life-or-death stakes. Gas leaks can cause explosions. Pipeline failures can devastate neighborhoods. The memory of the 2018 Merrimack Valley gas disaster in Massachusetts, where overpressurization of a gas system caused dozens of fires and an explosion that killed one person, hangs over the entire industry. Spire has invested in advanced leak detection technology, including satellite-based methane monitoring and mobile leak detection units, and operates a 24/7 emergency response capability across all service territories. The company's pipeline replacement program, which prioritizes the oldest cast iron and bare steel mains, is as much a safety program as it is a rate base growth strategy.

Leadership underwent a significant transition in recent years. Sitherwood retired as CEO on October 1, 2023, after roughly 12 years at the helm, succeeded by Steven L. Lindsey, who had served as president of Spire Missouri. Lindsey's tenure was brief; he was replaced by Scott Doyle as President and CEO effective April 25, 2025. Doyle came from CenterPoint Energy, where he had served as executive vice president and chief operating officer of utility operations overseeing gas and electric distribution across six states. His appointment brought an external perspective to a company that had been led by internal executives since Sitherwood's departure. Doyle's CenterPoint background is notable because CenterPoint operates both gas and electric utilities, giving him firsthand exposure to the competitive dynamics between the two fuel sources that will define Spire's future.

Adam Woodard was appointed CFO effective January 1, 2025, succeeding Steven Rasche, who had held the role since 2013. Steve Greenley was appointed EVP and COO in October 2025, rounding out a substantially refreshed C-suite. The breadth of these leadership changes, a new CEO, CFO, and COO within roughly a year, is unusual for a utility and suggests the board recognized the need for fresh perspectives as the company enters a more complex strategic chapter.

The dividend, perhaps the most important signal to Spire's investor base, tells a story of extraordinary consistency. Spire has paid continuous cash dividends since 1946, an 80-year streak. It has increased the dividend for 23 consecutive years. The current annualized payout of $3.30 per share, increased from $3.14 in November 2025, yields roughly 3.8 to 4.0 percent. The payout ratio of approximately 72 percent is well-covered by earnings and leaves room for continued increases aligned with the 5 to 7 percent long-term earnings growth target.

XI. The Regulatory Chess Game: Rate Cases and Returns

If the energy transition is the existential question, rate cases are the quarterly exam. Every few years, Spire goes before the Missouri PSC and the Alabama PSC to justify its infrastructure investments and request higher rates. The outcome of these proceedings directly determines the company's earnings power, making them arguably the most important events in the corporate calendar that most investors never hear about.

Missouri and Alabama operate under fundamentally different regulatory frameworks, and understanding the distinction matters. Missouri uses traditional rate cases: the utility files, interveners respond, commission staff conducts analysis, and after a year or so of proceedings, the commission issues an order setting new rates. It is adversarial, time-consuming, and uncertain. In November 2024, Spire Missouri filed a rate case requesting a $235.9 million rate increase based on a filed rate base of $4.386 billion, which represented 32 percent growth since the prior filing. Commission staff recommended a midpoint ROE of 9.63 percent with a 53.19 percent equity ratio. New rates became effective October 24, 2025, following settlement, though the settlement did not specify an explicit ROE or equity ratio.

Alabama operates under a Rate Stabilization and Equalization mechanism that is far more utility-friendly. Rather than filing traditional rate cases, Spire Alabama operates within an allowed ROE band of 9.70 to 10.30 percent with a 9.95 percent midpoint. If the utility's actual returns fall below or above the band, rates are automatically adjusted. This mechanism provides more predictable revenue recovery and eliminates much of the regulatory lag that plagues traditional rate-case states. The RSE terms were effective through September 2025 and have been extended through September 2026.

The ROE trends across the industry are worth noting because they directly impact utility valuations. Allowed ROEs have been gradually compressing over the past two decades, from the 11 to 12 percent range common in the early 2000s to the 9 to 10 percent range that prevails today. Every 50 basis points of ROE compression on a multi-billion-dollar rate base translates to tens of millions of dollars in lost earnings. Spire's allowed returns are roughly in line with industry averages, which provides comfort that neither Missouri nor Alabama is an outlier jurisdiction.

The arguments utilities make in rate cases have evolved. Twenty years ago, the pitch was simple: we need to replace aging infrastructure for safety and reliability. Today, Spire adds technology modernization, cybersecurity investment, methane emissions reduction, and customer experience improvements to the justification. Each dollar of approved capital investment grows the rate base and thus future earnings. The tension is that consumer advocates push back on affordability grounds, arguing that utilities are incentivized to overinvest because every capital dollar earns a return for shareholders. This is sometimes called the "Averch-Johnson effect," named after the economists who identified it in 1962: when a regulated firm earns a fixed return on capital, it has an incentive to over-capitalize. Consumer advocates in Missouri have raised this concern explicitly in Spire's recent rate proceedings, questioning whether all of the company's proposed investments are truly necessary or whether some represent gold-plating that benefits shareholders at ratepayer expense. The commission's job is to adjudicate that tension, and the outcome varies depending on the evidence, the political climate, and the commissioners' philosophical leanings.

This tension is particularly acute in Missouri, where the PSC has historically been more scrutinizing than Alabama's RSE mechanism. Missouri commissioners are politically appointed, and the commission's composition can shift between utility-friendly and consumer-friendly orientations depending on the political climate. Alabama's mechanism, by contrast, has been notably stable and predictable, which is one of the reasons Alagasco was such an attractive acquisition target.

Future regulatory risk comes from several directions. Climate-focused commissioners could challenge the prudence of natural gas infrastructure investments, arguing that ratepayers should not fund assets that may become stranded. Consumer advocates may push back on the rate base growth strategy itself, questioning whether all that capital spending truly benefits customers. And at the federal level, the Spire STL Pipeline saga demonstrated that FERC's evolving approach to affiliate transactions could complicate future midstream investments.

For investors tracking Spire's performance, the most important KPIs are rate base growth and allowed ROE. Rate base growth drives earnings growth in the regulated utility model, and Spire has been targeting 7 to 8 percent annualized rate base growth at Spire Missouri and 6 percent equity growth at Spire Alabama and Spire Gulf. Allowed ROE determines the return earned on that rate base. A secondary but critical KPI is customer count trends: are new buildings connecting to gas, or is the electrification trend beginning to erode the customer base? These three metrics, rate base growth, allowed ROE, and net customer additions, together paint the clearest picture of whether Spire's fundamental thesis is intact.

XII. Playbook: Business and Investing Lessons

The Spire story offers several transferable lessons about building value in regulated industries.

The utility M&A playbook works, but it has expiration dates. Spire demonstrated that consolidation can transform a subscale regional utility into a credible multi-state platform. The sequence matters: establish credibility with a same-state deal (Missouri Gas Energy), then expand geographically (Alagasco), then fill in (EnergySouth), then go for transformative growth (Piedmont Tennessee). Each deal builds the operational capability and regulatory relationships needed for the next one. But the strategy eventually runs into limits: attractive targets become scarce, regulatory scrutiny increases with scale, and balance sheet capacity constrains deal size.

Managing regulated businesses requires patience and stakeholder sophistication that would be alien in most competitive industries. You cannot simply announce a strategy and execute it. Every significant action must be justified to multiple regulators across multiple jurisdictions, each with their own political dynamics, precedents, and institutional cultures. The companies that succeed are the ones that invest in regulatory relationships as deliberately as they invest in pipelines, understanding that a hostile commission can destroy value faster than any competitor.

The dividend aristocrat model works in utility investing because of the fundamental alignment between the business model and investor needs. Utilities generate predictable, inflation-protected cash flows from essential services provided under monopoly franchises. Dividends are well-covered by earnings. And the regulatory compact provides a built-in inflation adjustment mechanism through rate cases. Spire's 80-year streak of continuous dividends and 23 consecutive years of increases is not accidental. It is the natural output of the regulated utility business model when managed competently. For income-oriented investors, the near-4 percent yield combined with mid-single-digit earnings growth offers a total return profile that, while never spectacular, compounds reliably through economic cycles, market panics, and presidential administrations.

The capital allocation discipline is worth studying as well. Utilities that allocate 90-plus percent of capital to the regulated rate base, as Spire does, are essentially converting shareholder capital into government-guaranteed returns. Each dollar of prudently invested capex earns the allowed ROE in perpetuity, or at least until the asset is fully depreciated. This is a fundamentally different value proposition from competitive industries where capital investments carry market risk. The risk in utility capital allocation is not demand or competition but regulatory disallowance, the possibility that a commission deems an investment imprudent and refuses to include it in the rate base. Spire's pipeline experience demonstrated that this risk, while rare, is real.

But the pipeline saga illustrates the flip side: even in "boring" regulated utilities, management can make bets that create significant risk. The decision to build a $287 million pipeline with no third-party shipper support and an affiliate contract as the sole evidence of need was either visionary or reckless, depending on your vantage point. The permanent certificate ultimately validated the project, but the two-year uncertainty, the stock price damage, the credibility loss, and the institutional consequences at FERC were real costs that shareholders bore.

The leadership lesson is perhaps the most nuanced. Sitherwood transformed Laclede from a sleepy regional utility into a growth platform, a remarkable achievement. She brought operational expertise, strategic ambition, and the willingness to make big moves in an industry that rewards incrementalism. But the pipeline controversy and the storage write-down suggest that the same aggressiveness that drove the M&A success may have led to overreach in non-utility investments. The best utility leaders understand where the boundaries of the regulated model lie and respect them, even when ambition tempts them to push past.

XIII. Analytical Frameworks: Porter's Five Forces and Hamilton's Seven Powers

Applying Porter's Five Forces to Spire reveals a business with an extraordinarily strong structural position on four dimensions and one growing vulnerability that could unravel everything.

The threat of new entrants is essentially zero. Regulated monopoly franchises, massive capital requirements for underground pipeline infrastructure, and the practical impossibility of laying duplicate pipe networks in urban areas create an impenetrable barrier. No one is going to build a competing natural gas distribution system in St. Louis.

Bargaining power of suppliers is moderate. Spire purchases natural gas on commodity markets with diversified sourcing across multiple interstate pipelines and production basins. No single supplier has pricing power, but the company is exposed to commodity price volatility, which is passed through to customers via purchased gas adjustments. Pipeline access can be a constraint, as the STL Pipeline controversy demonstrated.

Bargaining power of buyers is structurally low because customers cannot switch providers, but effectively moderate because state regulators act as their collective bargaining agent. The PSC negotiates rates, terms, and conditions on behalf of all captive customers, and a motivated commission can squeeze utility returns significantly.

Competitive rivalry within franchise territories is nonexistent by design. However, competition from electric utilities for new construction hookups is real and growing. When a developer builds new homes, the choice between gas and all-electric is made once and lasts decades. This inter-fuel competition at the point of construction is where the existential risk manifests.

Which brings us to the threat of substitutes, the force that should keep Spire's management awake at night. Heat pumps are improving in efficiency and declining in cost. Induction cooktops are gaining mainstream acceptance. Building codes in progressive jurisdictions increasingly favor all-electric construction. This is not a near-term revenue threat for Spire's existing customer base, switching from gas to electric heating requires significant investment that most homeowners will not make voluntarily. But it is a long-term threat to new customer additions, and in a rate-base-growth model, the inability to add customers eventually compounds into a serious problem.

Through Hamilton Helmer's Seven Powers lens, Spire's primary power source is cornered resource. Franchise territories are irreplaceable monopoly rights granted by the state. You cannot buy them on the open market. You cannot replicate them. And they provide the legal foundation for the entire business model. This is perhaps the strongest form of competitive moat in all of business, a government-granted monopoly with legal prohibitions on competition.

Scale economies provide a secondary power that the M&A strategy has enhanced. Spreading corporate overhead, technology platforms, and shared services across 1.7 million customers generates cost advantages that smaller utilities cannot match. This makes Spire both a more efficient operator and a more credible acquirer.

Switching costs are high for existing customers, as converting from gas to electric heating requires replacing furnaces, water heaters, and cooktops at significant expense. But the switching cost advantage applies only to the installed base. New construction faces no switching cost; the choice between gas and electric is made at the design stage.

Process power exists in moderate form through Spire's accumulated expertise in regulatory management, pipeline operations, safety compliance, and rate case execution. These capabilities are developed over decades and difficult to replicate quickly.

Network economies, counter-positioning, and branding provide essentially no competitive advantage. Gas distribution is not a network effects business. Regulated monopolies do not need counter-positioning. And brand means little when customers have no choice of provider.

Compared to peers, Spire occupies a middle ground. SoCalGas, operating in California's hostile regulatory environment, faces the most immediate policy threat but has responded with the most aggressive alternative fuel strategy. National Grid, straddling gas and electric in the Northeast, is attempting a dual-fuel transition that hedges its bets. Atmos Energy, focused on the Sun Belt, benefits from population growth but faces the same long-term substitution risk. CenterPoint Energy, from which Spire's new CEO Scott Doyle came, operates a combined gas and electric utility, providing natural diversification that pure-play gas utilities lack. Spire's advantage over smaller regional utilities is scale and regulatory diversification. Its disadvantage relative to combined gas-electric utilities is the lack of a hedge against fuel switching.

The synthesis: Spire has a powerful moat built on cornered resources and switching costs, enhanced by scale economies from consolidation. But the moat faces policy disruption from the energy transition that could erode its value over decades. The critical question is not whether the moat exists today, it clearly does, but whether the asset it protects will still be valuable in 2050.

XIV. Bull vs. Bear Case and Investment Considerations

The bull case for Spire rests on the fundamental durability of the regulated utility model combined with credible strategic execution. This is a company with predictable cash flows derived from an essential service, a monopoly franchise, and 80 years of continuous dividends with 23 consecutive annual increases. The multi-state diversification across Missouri, Alabama, Mississippi, and soon Tennessee reduces regulatory concentration risk. The Piedmont Tennessee acquisition, if completed, adds a high-growth market (Nashville) that offers organic customer additions that Spire's legacy territories cannot. Management has guided for 5 to 7 percent adjusted EPS growth compounding off a fiscal 2027 midpoint of $5.75 per share. The fiscal 2026 guidance of $5.25 to $5.45 excludes the Piedmont acquisition, suggesting meaningful earnings lift once Tennessee is integrated. At roughly 16 times forward earnings with a near-4 percent dividend yield, the stock offers a credible total return in the high single digits.

The rate base growth story is real and funded. The $11.2 billion ten-year capital plan provides visibility on infrastructure investment that drives rate base expansion at 7 to 8 percent annually in Missouri and 6 percent in Alabama. Each dollar of rate base growth, approved by regulators, translates directly to earnings power. The company's methane reduction achievements, over 50 percent since 2005, provide both environmental credibility and a justification for continued infrastructure spending. The Missouri preemption law shields Spire from the most aggressive electrification mandates that threaten coastal gas utilities.

RNG investments, while small, demonstrate management awareness of the transition. The pipeline controversy's resolution removes what was the largest single overhang on the stock. And the gas-as-transition-fuel argument, that electrification will take decades and gas remains essential for reliability and affordability, is not unreasonable, particularly in Spire's politically conservative service territories.

The bear case starts with the inescapable question of peak gas. New residential construction in the United States is increasingly all-electric. Every home that connects to the grid without gas is a customer Spire will never have. Over a 30-year horizon, this trend could erode the customer base even in Spire's protected markets, as economics and technology rather than mandates drive the shift. A declining customer base means fixed costs spread over fewer ratepayers, raising per-customer bills, which accelerates defection, creating a potential death spiral that regulators would eventually have to address.

Allowed ROE compression continues to pressure returns. If the utility industry's average allowed ROE drops from 9.5 percent to 8.5 percent over the next decade, a not-implausible outcome given interest rate dynamics and regulatory trends, that is a meaningful hit to earnings on a $4-plus billion rate base.

The balance sheet bears watching. With approximately $3.4 billion in long-term debt, a pending $2.48 billion acquisition, and credit ratings hovering near the bottom of investment grade, Spire has limited margin for error. The company issued $200 million in junior subordinated notes in January 2026 to redeem $250 million of preferred stock, a financial engineering move that suggests capital structure optimization is being pushed hard. Any credit downgrade to junk would dramatically increase borrowing costs and could force dividend reconsideration.

The M&A strategy may be reaching diminishing returns. The early deals, MGE and Alagasco, were transformative at reasonable prices. Piedmont Tennessee at $2.48 billion for 200,000 customers (roughly 1.5 times rate base) is a full price for a growth market. If the deal's returns disappoint, shareholders will question whether management is empire-building rather than value-creating.

Finally, the pipeline saga demonstrated execution risk in regulated infrastructure. The December 2022 permanent certificate resolved the STL Pipeline issue, but the episode consumed years of management attention, damaged credibility, and exposed the company to regulatory and legal risks that nearly destroyed a $287 million asset.

The three KPIs that matter most for tracking Spire's ongoing performance: rate base growth (the engine of earnings), allowed ROE outcomes in rate cases (the return on that engine), and net customer additions versus losses (the long-term viability signal). If rate base grows at target, ROE holds steady, and customer counts stay flat or grow, the thesis is intact. If any of those three metrics deteriorate meaningfully, the investment case weakens.

XV. Epilogue: The Utility in Transition

Spire Inc. stands at an inflection point that is both company-specific and industry-defining. Under new leadership with Scott Doyle at the helm since April 2025, the company is pursuing its most ambitious acquisition since the Alagasco deal a decade ago, targeting a return to transformative M&A with the Piedmont Tennessee purchase. First quarter fiscal 2026 results were encouraging: adjusted earnings of $108.4 million, or $1.77 per share, up from $81.1 million in the prior year's quarter. Revenue of $762.2 million grew nearly 14 percent year over year. The gas utility segment drove most of the improvement, with higher Missouri rates from the October 2025 rate case contributing meaningfully.

The broader gas utility sector is navigating what may be the most consequential transition in its history. The competition between electricity and gas for the home energy market, which began in the 1880s when electric lighting threatened gas lamps, is entering a new chapter. This time, the stakes are different. When electricity disrupted gas lighting, gas pivoted to heating. If electricity disrupts gas heating through heat pumps and building electrification, it is unclear what gas pivots to next. RNG and hydrogen are possibilities, but neither has proven it can operate at the scale necessary to sustain a trillion-cubic-foot-per-year industry.

Spire's management has the advantage of operating in politically favorable jurisdictions with explicit legal protections against gas bans, a demographic base that is less likely to adopt electrification mandates than coastal counterparts, and a substantial capital investment program that keeps regulators aligned through shared infrastructure interests. The disadvantage is that technology and economics do not care about politics. If heat pumps become decisively cheaper and more effective than gas furnaces, market forces will drive the transition regardless of preemption laws.