Simon Property Group: America's Mall Empire

I. Opening & Context Setting

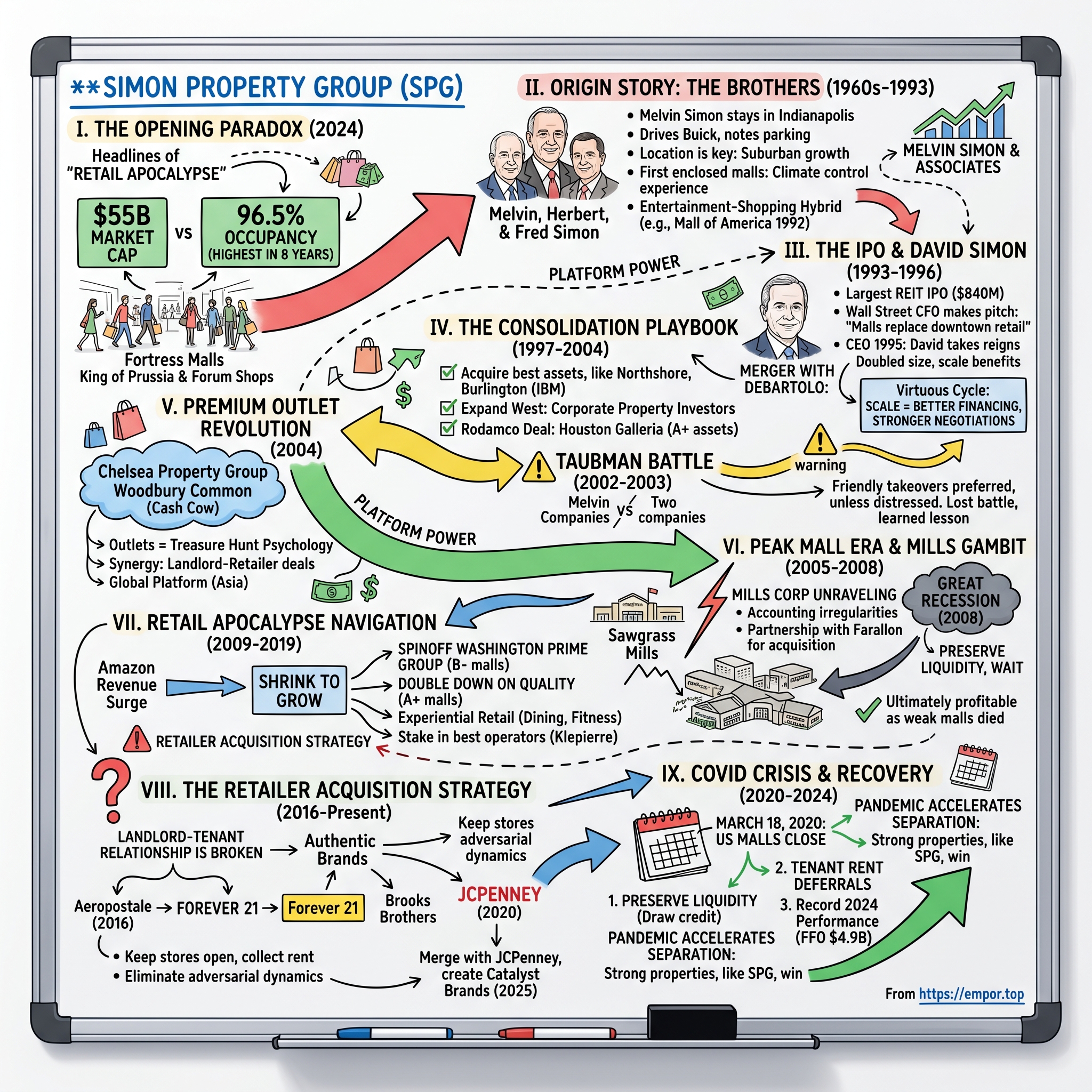

Picture this paradox: In 2024, while headlines scream about the "retail apocalypse" and dead malls becoming Amazon fulfillment centers, Simon Property Group sits atop a $55 billion market capitalization, generating record funds from operations of $4.9 billion. Their malls—those supposedly dying relics of American consumerism—are 96.5% occupied, the highest level in eight years.

Walk through King of Prussia Mall outside Philadelphia on a Saturday afternoon, or The Forum Shops at Caesars in Las Vegas any evening, and you'll witness something that shouldn't exist according to conventional wisdom: throngs of shoppers, lines outside luxury stores, restaurants with two-hour waits. These aren't just malls; they're retail fortresses that have somehow grown stronger while their weaker peers collapsed.

The numbers tell a story that defies the narrative: 230+ properties across North America, Europe, and Asia. Annual sales per square foot averaging $700+ at their premium centers—double the industry average. Tenant sales that have not just recovered from COVID but exceeded 2019 levels by 15%. This isn't survival; it's dominance.

How did two brothers from the Bronx, starting with a few strip centers in Indianapolis, build what would become America's mall empire? How did their successor—a Wall Street banker turned mall mogul—navigate the company through the rise of e-commerce, a global pandemic, and the supposed death of physical retail? And perhaps most intriguingly, why is Simon Property Group now buying the very retailers that lease space in their malls?

This is a story of three acts: the creation of the American mall as we know it, the consolidation of an entire industry, and the radical reinvention of what a mall company can be. It's about understanding that real estate is never just about buildings—it's about power, relationships, and most importantly, adapting faster than your environment changes.

II. Origin Story: The Simon Brothers (1960-1993)

The year was 1959, and Melvin Simon had just finished his army service at Fort Benjamin Harrison in Indianapolis. Most New Yorkers stationed in the Midwest couldn't wait to get back to the coasts. But Melvin saw something different in Indianapolis—wide open spaces, growing suburbs, and most importantly, no established real estate dynasties to compete against. While his fellow servicemen headed home, Melvin stayed, taking a job as a leasing agent for a local shopping center developer.

Within months, he was making more in commissions than most executives earned in salary. He'd drive through Indianapolis suburbs in his Buick, counting cars in parking lots, timing how long families spent shopping, noting which stores had lines. His notebooks from this period, discovered years later, contained meticulous observations: "Woolworth's—17 minute average visit, 73% leave with bags" or "Parking lot 85% full at 2pm Saturday—need more spaces."

By 1960, Melvin had saved enough to start his own company, but he needed help. He called his brothers Herbert and Fred in the Bronx. "Come to Indianapolis," he told them. "There's something happening here with shopping centers that's going to change everything." Herbert, the detail-oriented accountant, arrived first. Fred, the natural dealmaker who could charm anyone, followed six months later. Together, they formed Melvin Simon & Associates (MSA).

Their first property wasn't glamorous—a small strip center anchored by a supermarket and a drugstore in Bloomington, Indiana. Total cost: $75,000, mostly borrowed. But it taught them the fundamental rule that would guide everything: location trumps everything, but only if you understand what makes a location valuable. For the Simons, that meant being where suburban families were moving, not where they already lived. The transition from strip centers to enclosed malls came in 1964, and it happened almost by accident. Montgomery Ward executives approached MSA about developing sites, and through this relationship, the Simons brought their enclosed-mall concept back to Indiana, opening the first two enclosed malls in Indiana, in Anderson and Bloomington. The enclosed mall was revolutionary—climate-controlled shopping that turned a mundane errand into a social experience. No more dodging rain between stores, no more sweltering summer heat deterring shoppers.

The company continued to expand rapidly, adding an average of 1,000,000 square feet of retail space each year. By 1967, MSA owned and operated more than 3,000,000 square feet. But the Simons weren't just building bigger; they were building smarter. In 1975, MSA opened Towne East Square in Wichita, Kansas, the first enclosed mall with more than 1,000,000 square feet.

In the mid-1970s, MSA formed a separate management division charged with tending to its existing properties, providing marketing and technical services, quality control, and landscaping and design assistance to ensure consistent managerial and operational quality throughout the Simon portfolio. This was crucial—most developers built and flipped; the Simons built and operated, understanding that the real money wasn't in construction fees but in decades of rent collection.

The 1980s brought a surprising pivot. In the early 1980s, Simon, which was by that time opening three or more enclosed malls each year, turned its attentions to urban redevelopment. The company was asked to become involved in three redevelopment projects in midwestern cities with declining downtowns. While everyone else was fleeing city centers for suburbs, the Simons saw opportunity in the abandoned urban cores.

MSA's success with urban redevelopment led the Simons to consider mixed-use properties. Based on the theory that sites located right next to large metropolitan areas could be used for retail, business, and residential construction, MSA began its first mixed-use project in Arlington, Virginia, developing an 800,000 square foot retail complex, coupled with a Ritz-Carlton hotel and a 160,000 square foot office building.

By the early 1990s, the brothers had built something remarkable: a portfolio of 147 shopping centers across 30 states, all managed from their Indianapolis headquarters. By the early 1990s, the Simon company was one of the largest and most successful developers of Shopping Centers in the country. They weren't just mall developers anymore; they were entertainment architects.

One of the first examples of Simon's entertainment-shopping hybrid was The Forum Shops at Caesars in Las Vegas, developed in partnership with The Gordon Company of Los Angeles. Built between Caesars Palace and The Mirage hotels, this development was designed to recreate a Roman street, complete with robotic animated statues, fountains, and simulated Mediterranean sky.

Then came their moonshot: In August 1992, MSA developed the Mall of America, a vast 4.2 million square foot entertainment and retail complex near the Minneapolis/St. Paul airport, including four anchor stores, more than 500 specialty shops, a seven-acre family theme park, and a walk-through aquarium. It was audacious, almost absurd in scale. Critics called it a white elephant. Visitors called it amazing.

But even as the Mall of America opened its doors, the Simon brothers knew they needed something their family business had never had: institutional capital. The properties were getting bigger, the competition fiercer, and the capital requirements astronomical. It was time to tap the public markets.

III. The IPO and Public Market Debut (1993-1996)

December 14, 1993. The trading floor at the New York Stock Exchange buzzed with unusual energy. Simon Property Group was about to price what would become the largest initial public offering of a real estate investment trust to date—$840 million. For the Simon brothers, standing in Indianapolis watching the ticker, this was validation of three decades of work. For one young executive in particular, it was the beginning of a transformation.

David Simon had joined the family business in 1990 as Chief Financial Officer, leaving behind a lucrative Wall Street career where he'd spent five years specializing in mergers and acquisitions. From 1985 to 1990, he'd been an investment banker at two Wall Street firms, specializing in mergers and acquisitions and leveraged buyouts. His uncle Herbert and father Melvin had built an empire on handshake deals and local bank financing. David understood something different: capital markets were about to reshape real estate forever.

The decision to structure as a REIT wasn't obvious. REITs required distributing 90% of taxable income to shareholders—money that couldn't be reinvested in growth. But David saw the flip side: REITs paid no corporate taxes, creating a massive competitive advantage. More importantly, being public meant access to institutional capital at a scale the private Simon company could never achieve.

He led the efforts to take Simon Property Group public with a nearly $1 billion initial public offering, meticulously preparing the company for public scrutiny. Every lease was digitized, every property appraised, every contract reviewed. The roadshow was grueling—14 cities in 10 days, David presenting to skeptical institutional investors who wondered why anyone would invest in malls when everyone was moving to suburbs.

His pitch was counterintuitive: suburban migration wasn't the enemy of malls; it was their greatest opportunity. The further people moved from city centers, the more they needed centralized shopping destinations. Malls weren't competing with downtown retail—they were replacing it.

The IPO priced at $15.50 per share, raising $840 million. Within hours of trading, the stock jumped 8%. The Simon brothers had built a great real estate company. David Simon was about to build something else entirely: a consolidation machine.

He became CEO in 1995, taking over from his father at age 34. The timing was deliberate. Melvin, then 69, understood that the public markets required a different kind of leadership—someone who spoke the language of Wall Street, who understood leverage ratios and FFO multiples, who could execute complex M&A transactions.

David's first major move as CEO would test everything he'd learned on Wall Street. In 1996, he orchestrated Simon Property's merger with the newly public DeBartolo Realty Corporation, owner of the real estate assets of Edward J. DeBartolo Sr. The DeBartolo name carried weight—they owned some of America's most productive malls, including properties that generated over $500 per square foot in sales.

But the deal was complicated by family dynamics. The DeBartolo family was reeling from Edward Jr.'s involvement in a Louisiana gambling scandal. They needed a clean exit, but they also wanted to maintain face. David structured a merger that technically made it a partnership, allowing the combined company to briefly operate as Simon DeBartolo Group.

The newly combined Simon DeBartolo Group owned 7 percent of all regional malls in the United States and managed or owned almost 200 properties in 33 states. Overnight, Simon had doubled in size. But more importantly, David had proven something crucial: in the fragmented world of mall ownership, scale created a virtuous cycle. Larger portfolios meant better financing terms, stronger negotiating power with retailers, and the ability to spread operating costs across more properties.

The integration was masterful. Rather than impose Simon's Indianapolis culture on DeBartolo's Youngstown operations, David cherry-picked the best practices from each organization. DeBartolo's leasing strategies were superior; Simon's financial controls were tighter. The combined company kept both strengths.

Within months, the benefits were obvious. Retailers who previously played Simon and DeBartolo against each other now faced a unified negotiator. Insurance costs dropped 15% through pooled purchasing. Marketing programs that worked in Simon's Midwest malls were rolled out to DeBartolo's Sun Belt properties.

The public market debut had transformed Simon from a family business into an institutional powerhouse. But David Simon wasn't satisfied with being big. He wanted to be dominant. The consolidation of the mall industry was just beginning.

IV. The Consolidation Playbook (1997-2004)

David Simon's playbook for consolidation was elegant in its simplicity: identify the best assets, wait for moments of weakness, and deploy capital aggressively. Between 1997 and 2004, he would execute this strategy with the precision of a chess grandmaster, transforming Simon from a large player into the undisputed king of American mall ownership.

The first major move came in 1997. In partnership with Macerich, the company acquired 12 malls from IBM's pension plan for $974.5 million. IBM, focused on its technology turnaround, wanted out of real estate. The portfolio included crown jewels like Northshore Mall in Massachusetts and Burlington Mall—properties generating over $450 per square foot in sales. David structured the deal as a joint venture, sharing risk while maximizing returns.

One year after these acquisitions, the company acquired Corporate Property Investors and was renamed Simon Property Group. Corporate Property Investors owned 16 regional malls and had something Simon desperately wanted: a presence in California and the Southwest. The $1.8 billion deal brought properties like Del Amo Fashion Center in Los Angeles and La Jolla's Westfield UTC. The DeBartolo name, no longer needed for credibility, was quietly dropped.

Then came 2002, in partnership with Westfield Group and the Rouse Company, the company acquired 13 properties from Rodamco North America including Copley Place, Houston Galleria, and SouthPark Mall. Rodamco, the U.S. arm of a Dutch company, was retreating to Europe. The properties were A+ assets in A+ markets—exactly what Simon wanted. The Houston Galleria alone was worth the effort, generating over $700 per square foot in sales with waiting lists for retail space.

But not every acquisition attempt would go smoothly. The Taubman battle of 2002-2003 would become David Simon's white whale—and a cautionary tale about the limits of financial engineering when faced with entrenched family control.

Simon sought judicial intervention in its takeover effort after the Board rejected its unsolicited offer to purchase all of TCI's outstanding common stock at $18 per share on December 5, 2002. The Taubman portfolio was exceptional—30 properties including Beverly Center in Los Angeles and Short Hills in New Jersey, averaging over $550 per square foot in sales. For David Simon, it was the missing piece to complete national dominance.

Westfield America ("Westfield") joined the Simon offer on January 15, 2003. Then, the offer was increased to $20.00 per share. Even with Australia's Westfield as a partner, even with a 35% premium to market price, the Taubmans wouldn't budge. Robert S. Taubman, the Bloomfield Hills-based company's chairman, president and chief executive, said Simon's offer doesn't accurately reflect the company's value. "There's no way that this deal can get done. The board has said this company is not for sale," Taubman said.

The legal battle was Byzantine. Robert Taubman filed a Schedule 13D/A with the Securities and Exchange Commission advising that he had entered into Voting Agreements with three, unrelated shareholders. The Voting Agreements granted him the sole and absolute right to vote their shares on any and all matters coming before the TCI shareholders. With the Voting Agreements, Robert Taubman asserted to the SEC that he and the Taubman family controlled 33.6% of the vote of the capital stock of TCI, and that the Voting Agreements had been entered into "for the purposes of preventing an unsolicited takeover of the company." Thus, it was impossible for anyone to achieve a two-thirds vote to approve a sale or amend the Articles of Incorporation over the Taubman family's opposition.

Initially, Simon won in federal court, with the judge ruling Taubman's voting arrangements violated Michigan law. But then came the nuclear option: Michigan-based Taubman thwarted the 2003 hostile takeover bid from Simon by getting the state legislature to enact a bill that that allowed the Taubman family to use its shares to block any takeover bid. The day after Michigan's governor signed the bill into law, Simon withdrew its offer, and the Taubmans and Simons have been bitter rivals ever since.

David Simon had lost his first major battle. But the loss taught him something valuable: hostile takeovers in retail real estate were nearly impossible when families controlled voting rights. Future acquisitions would need to be friendly—or the targets would need to be in distress.

The consolation prize came quickly. In the following year, Simon acquired a majority interest The Kravco Company, owner of the King of Prussia, for $300 million. King of Prussia wasn't just any mall—it was the second-largest in America, a Philadelphia powerhouse generating over $700 million in annual sales. Kravco, unlike Taubman, needed liquidity. Simon provided it.

The chess game continued. Each acquisition made the next one easier. More properties meant more cash flow, which meant more borrowing capacity, which meant more acquisitions. It was a virtuous cycle that only worked if you never overpaid and never overleveraged. David Simon, the former Wall Street banker, understood this better than anyone.

By 2004, Simon Property Group owned or had interests in over 280 properties. They were generating $2.3 billion in annual revenue. But David saw a gap in the portfolio: outlets. The outlet business was growing at 8% annually while traditional malls grew at 2%. He needed to be in that business. And he knew exactly who to buy.

V. The Premium Outlet Revolution: Chelsea Acquisition (2004)

David Bloom had built Chelsea Property Group from a small outlet developer into America's premium outlet powerhouse. By 2004, Chelsea owned 31 centers generating over $3 billion in annual tenant sales. Their crown jewel, Woodbury Common Premium Outlets just outside New York City, was arguably the most profitable shopping center per square foot in America—tourists from Manhattan would take buses specifically to shop there, Chinese tour groups included it on their itineraries.

Simon Property Group Inc., the world's largest manager of shopping malls, agreed to buy Chelsea Property Group Inc., the biggest U.S. owner of factory-outlet shopping centers, for about $3.5 billion in cash and stock. Simon, based in Indianapolis, said it will pay $66 a share for the firm, a 13 percent premium to Chelsea's closing stock price of $58.24 on Friday. Simon also will assume debt and preferred stock that totaled $1.3 billion as of March 31.

The deal structure was complex but brilliant. Rather than an all-cash offer that would have strained Simon's balance sheet, David Simon offered $36 in cash plus 0.2936 shares of Simon stock for each Chelsea share, plus assumption of $1.3 billion in debt and preferred stock. This preserved cash while giving Chelsea shareholders upside in the combined company.

But the real genius wasn't the price—it was understanding why outlets were different from malls and why that mattered. Traditional malls were about full-price retail, creating environments where middle-class Americans could shop for aspiration. Outlets were about treasure hunting—wealthy consumers seeking deals on premium brands. The psychology was completely different, yet complementary.

Roseland, N.J.-based Chelsea's 31 outlets lease space to retailers including Coach Inc. and Brooks Brothers, and will help Simon expand in the U.S. cities of New York, Boston, Las Vegas and Los Angeles. Chelsea also has four centers in Japan, allowing Simon to enter Asia for the first time.

The outlet business had another advantage: tourism. Chelsea's real estate assets include the Woodbury Common Premium Outlets, near New York City, and the Desert Hills Premium Outlets, near Palm Springs, Calif. These weren't just shopping centers; they were destinations. International tourists, particularly from Asia and Latin America, would plan entire trips around outlet shopping. The average visitor to Desert Hills drove 67 miles and spent four hours shopping.

David Bloom would continue running Chelsea as a division, maintaining the operational expertise that made the outlets successful. Chelsea Chairman and Chief Executive David Bloom will continue in his current role, leading Chelsea as a division of Simon, and will join Simon's board as an advisory director. "Our international presence in Asia and Simon's presence in Europe will result in a combined organization with a truly global platform from which to grow," Bloom said.

The integration revealed unexpected synergies. Retailers who had separate teams negotiating with Simon for mall space and Chelsea for outlet space now dealt with one landlord. Simon could offer package deals: prime mall space in exchange for outlet presence, or vice versa. Brands that previously couldn't justify outlets due to minimum location requirements suddenly had access to the entire Chelsea portfolio.

The Las Vegas market showcased the power of the combination. Simon owns the Forum Shops at Caesars on the Las Vegas Strip. The 500,000-square-foot high-end mall, one of the most successful in the nation in terms of spending per square foot, is being expanded by 175,000 square feet. Simon and Chelsea are partners in the 435,000-square-foot Las Vegas Premium Outlets, a new outlet mall credited with launching a revival of interest in downtown Las Vegas business.

Within eighteen months of the acquisition, Simon had rebranded all Chelsea properties as "Premium Outlets," investing $200 million in upgrades—better signage, improved parking, enhanced food courts. Sales per square foot jumped 12% in the first year alone. The outlets weren't competing with Simon's malls; they were extending the shopping ecosystem.

The international expansion accelerated immediately. Chelsea's four Japanese properties became the beachhead for Asian expansion. Within two years, Simon announced Premium Outlets in Korea and negotiations for sites in China. European outlets followed, leveraging Simon's existing relationships from their mall holdings in France and Italy.

But perhaps the most important lesson from the Chelsea acquisition was about timing. David Simon didn't buy at the peak of the outlet boom in the late 1990s when prices were astronomical. He waited until 2004, when Chelsea needed capital for expansion but public markets were skeptical of retail real estate. Patience, as always, was profitable.

The outlet acquisition also prepared Simon for what was coming: a retail environment where price-conscious shopping would become not just acceptable but fashionable. As the Great Recession loomed, Simon's Premium Outlets would prove more resilient than anyone expected. But first, David Simon had one more massive acquisition to complete—one that would test every lesson he'd learned about deal-making, integration, and the dangers of buying at the peak.

VI. Peak Mall Era & The Mills Gambit (2005-2008)

The Mills Corporation represented everything that was both magnificent and dangerous about American retail real estate at its peak. Their properties weren't just malls—they were retail theme parks. Potomac Mills in Virginia stretched over 1.6 million square feet. Sawgrass Mills in Florida drew 26 million visitors annually. These weren't places you went to buy a shirt; they were destinations where families spent entire days.

But by 2006, Mills was unraveling. The Securities and Exchange Commission opened an investigation in to the company over accounting irregularities. The $350 million accounting error wasn't just a number—it represented years of aggressive accounting, capitalizing costs that should have been expensed, inflating net operating income to meet Wall Street expectations. CEO Mark Ordan, brought in to clean up the mess, discovered the problems went deeper than anyone imagined.

David Simon saw opportunity in the chaos. On February 5, 2007, Simon Property Group, Inc. and Farallon Capital Management, L.L.C. announced they have sent a letter to the Board of Directors of The Mills Corporation proposing to enter into a merger agreement to acquire Mills for $24.00 per share in cash. Funds managed by Farallon currently own approximately 10.9 percent of Mills outstanding common shares, making these funds the largest reported Mills shareholder.

The partnership with Farallon was strategic. Tom Steyer's hedge fund brought not just capital but credibility—they already owned 10.9% of Mills and understood the assets. More importantly, splitting the equity commitment meant Simon could acquire a massive portfolio without overleveraging its balance sheet. Each party committed $650 million in equity.

The bidding war that followed was instructive. Brookfield Asset Management had already agreed to buy Mills for $21 per share. Simon and Farallon offered $24. Brookfield had three days to counter. Instead of getting into a prolonged battle, they walked away. By March 2007, Simon and Farallon had raised their offer to $25.25 per share—a total acquisition price of $1.64 billion plus assumption of significant debt.

David Simon, Chief Executive Officer of SPG, said, "This is a unique opportunity to acquire a portfolio of quality retail assets. SPG's experience operating upscale regional mall and outlet centers; previous ownership interest in certain Mills properties; and successful track record with acquisitions, integration, and property management, uniquely position us to maximize the value of these assets."

The integration strategy was sophisticated. The 17 traditional Mills properties will be operated as a separate retail real estate platform. SPG will integrate management and administrative support functions of the Mills regional malls into its existing 172 regional mall portfolio. This dual approach recognized that Mills properties were fundamentally different—they required different tenant mixes, marketing strategies, and capital allocation.

The properties themselves were a mixed bag. Gems like Sawgrass Mills and Potomac Mills were generating strong cash flow. But projects like Meadowlands Xanadu in New Jersey—a $2 billion development nightmare that would eventually become American Dream—were bleeding money. Ontario Mills in California was successful; Arundel Mills in Maryland needed work.

The financial engineering was complex. Simon provided replacement financing for Brookfield's loan plus additional capital needs. Individual property mortgages needed refinancing. The entire Mills corporate structure had to be unwound and integrated into Simon's REIT structure. It took months of work by teams of lawyers and accountants.

But just as the integration was gaining momentum, the world changed. In August 2007, the credit markets froze. By September, Northern Rock was collapsing in the UK. By March 2008, Bear Stearns was gone. The Great Recession had arrived, and Simon Property Group was sitting on billions in debt from acquisitions made at the absolute peak of the market.

The Mills properties, massive and expensive to operate, were particularly vulnerable. Tourist traffic evaporated. Retailers stopped paying rent. Properties that had been valued at 6% cap rates were suddenly worth 10% cap rates—if buyers existed at all. Simon's stock price fell from $118 in 2007 to $24 in March 2009.

David Simon's response was methodical. First, preserve liquidity—Simon drew on credit lines, suspended acquisitions, cut the dividend. Second, help tenants survive—rent deferrals, percentage rent deals, anything to keep stores open. Third, wait. The Mills properties might have been bought at the peak, but they were still great real estate. If Simon could survive the recession, the assets would recover.

By 2012, the patience paid off. Simon Property Group announced that it has signed a definitive agreement under which it is acquiring a 28.7% equity stake in Klépierre for approximately $2.0 billion. Simultaneously, Simon bought out Farallon's 50% stake in the Mills properties. Mr. Simon added, "The Mills transaction is a compelling opportunity for SPG to expand our investment in a portfolio of assets we know well and already manage. We were pleased to have partnered with Farallon since our initial investment in 2007, and we have made significant progress improving The Mills' assets."

The Mills acquisition, made at the worst possible time, ultimately worked because David Simon understood something fundamental: great retail real estate survives recessions. The weak malls died. The strong ones—including most of the Mills properties—emerged stronger. By 2012, Mills properties were generating over $400 million in annual NOI. The acquisition that nearly broke Simon became one of its most profitable.

VII. Retail Apocalypse Navigation (2009-2019)

The decade from 2009 to 2019 would test every assumption about physical retail. Amazon's revenue grew from $24 billion to $280 billion. Department stores—the traditional anchors of malls—began collapsing like dominoes. Sears, JCPenney, Macy's, Bon-Ton, Lord & Taylor—each bankruptcy or closure rippled through the mall ecosystem. The media had a name for it: the retail apocalypse.

David Simon's response was counterintuitive but brilliant: shrink to grow. On May 28, 2014, the company completed the separation of Washington Prime Group Inc., which is now an independent public company. Washington Prime holds interests in 98 retail assets, including the strip center business, formerly owned by Simon. Each Simon stockholder received one Washington Prime common share for every two shares of Simon common stock held.

The properties spun into Washington Prime weren't necessarily bad—they included 54 strip centers and 44 smaller enclosed malls across the United States, comprising approximately 53 million square feet. But they were the wrong properties for what was coming. Green Street said Washington Prime properties are at greater risk to Internet retailing, partly because many have both Sears and J.C. Penney as anchor stores.

The spinoff was surgical precision. Simon kept the A+ malls in major markets, the Premium Outlets, and the Mills properties. Washington Prime got properties generating less than $300 per square foot in sales, malls in secondary markets, and the entire strip center portfolio. It was like a ship captain throwing cargo overboard before a storm—painful but necessary for survival.

The financial engineering was elegant. Simon shareholders received the Washington Prime shares as a tax-free dividend. The properties went to Washington Prime debt-free, giving the new company a fighting chance. Mark Ordan, the former Mills CEO, would run it. Simon would initially continue providing leasing services. It looked generous, even supportive.

But David Simon knew what was coming. Department store bankruptcies would accelerate. Secondary market malls would struggle. Strip centers would face competition from e-commerce. Better to let Washington Prime deal with those challenges while Simon focused on fortress assets. Seven years later, in June 2021, Washington Prime filed for Chapter 11 bankruptcy, validating Simon's timing.

Meanwhile, Simon doubled down on quality. Failed department store spaces became opportunities for redevelopment. At Phipps Plaza in Atlanta, a former Belk became a Life Time Fitness and co-working space. At The Florida Mall, dead anchors became dining pavilions and entertainment venues. The mantra was simple: if you can buy it online, we won't lease space for it. If you can't do it online—dining, fitness, entertainment, services—we want you.

The international strategy accelerated. Rather than building or buying internationally, Simon took stakes in the best operators. The Klépierre investment in Europe, McArthurGlen in European outlets, stakes in Japanese and Korean retail properties. Each investment came with local expertise and established relationships. Simon provided capital and best practices; local partners provided market knowledge.

But the real innovation came in 2016 with a shocking move: In September 2016, in partnership with Authentic Brands Group and GGP Inc., the company acquired Aéropostale. A mall landlord buying a retailer? It seemed backwards. But David Simon saw something others missed: vertical integration could solve the mall's biggest problem—tenant instability.

The model was simple but revolutionary. When retailers failed—and in the retail apocalypse, many did—Simon and partners would acquire the brand, restructure operations, and keep stores open in Simon malls. The rent kept flowing, the malls stayed occupied, and Simon participated in any brand recovery upside.

The General Growth Properties battles continued through this period. Simon tried repeatedly to acquire its largest competitor—in 2010, 2011, and again in 2015. Each time, Brookfield Asset Management outmaneuvered them, eventually acquiring GGP in 2018. It was frustrating, but it forced Simon to grow differently—through redevelopment, mixed-use, and the retailer acquisition strategy.

Technology became a differentiator. Simon launched Inception, a retail incubator, identifying and nurturing emerging brands. Simon Venture Group invested in retail technology companies. The malls themselves evolved—mobile apps for parking and navigation, buy-online-pickup-in-store infrastructure, community gathering spaces.

The numbers told the story. While overall mall traffic declined 10% from 2010 to 2019, Simon's comparable property NOI grew every single year. Occupancy stayed above 94%. Rental rates increased. The retail apocalypse was real, but it was claiming the weak, not the strong.

By 2019, Simon Property Group had transformed from America's largest mall owner into something else entirely: a retail platform company that happened to own real estate. The malls were platforms for brands, whether Simon owned them or just leased to them. The outlets were treasure-hunting destinations. The mixed-use developments were miniature cities.

But even David Simon couldn't have predicted what was coming next. In late 2019, reports emerged from Wuhan, China, about a novel coronavirus. Within months, every mall in America would be closed, retail sales would crater, and Simon would face its greatest test yet. The retail apocalypse had been a slow-motion crisis. COVID-19 would be instantaneous catastrophe.

VIII. The Retailer Acquisition Strategy (2016-Present)

The strategy seemed insane when David Simon first proposed it: why would a landlord want to become a retailer? But as he explained to skeptical investors in 2016, the traditional landlord-tenant relationship was broken. Retailers would expand aggressively during good times, then use bankruptcy to shed leases during downturns. Landlords absorbed all the downside, none of the upside.

In September 2016, in partnership with Authentic Brands Group and GGP Inc., the company acquired Aéropostale. The teen retailer had filed for bankruptcy with 800 stores and $2 billion in annual sales just three years prior. The structure was elegant: Authentic Brands would own the intellectual property, while a new entity would operate the stores. Simon got to keep its mall spaces occupied; Authentic got licensing fees; the brand survived.

This wasn't charity. The economics were compelling. By eliminating the adversarial landlord-tenant relationship, costs dropped immediately. No more lease negotiations, no more tenant improvement allowances, no more disputes over common area maintenance. The stores became more profitable simply by removing friction from the system.

The model evolved quickly. Forever 21's 2019 bankruptcy created a larger opportunity. Authentic Brands bought the Forever 21 brand name out of bankruptcy in February 2020 and licensed it to Sparc to operate through a fleet of about 500 stores, some of which were leased by Simon Property. The fast-fashion retailer had been paying $450 million annually in rent; now that money stayed within the Simon ecosystem.

Then came COVID-19 and the tsunami of retail bankruptcies. Brooks Brothers, the 202-year-old menswear icon, filed in July 2020. A company known as Sparc LLC, which is comprised of the U.S. mall owner Simon Property Group and the apparel-licensing firm Authentic Brands Group, is making a $305 million bid for bankrupt Brooks Brothers. The offer was to keep at least 125 of Brooks Brothers' stores open for business.

The most audacious move came with JCPenney. The department store chain, with 850 locations and a century of history, filed for bankruptcy in May 2020. JCPenney filed for bankruptcy protection in 2020 and was acquired by Simon Property and Brookfield Asset Management Inc., another mall owner, for $800 million. This wasn't just keeping a few stores open—this was preserving hundreds of anchor spaces across America.

SPARC Group—the operating entity Simon created with Authentic Brands—became a retail conglomerate almost overnight. Sparc runs Forever 21, Brooks Brothers, Aéropostale, Eddie Bauer, Lucky Brand, Nautica and Reebok. Each brand maintained its identity while benefiting from shared back-office functions, distribution networks, and most importantly, guaranteed space in prime mall locations.

The financial engineering was sophisticated. Simon didn't own these brands outright—that would have been too capital-intensive and risky. Instead, it held minority stakes in operating companies that licensed brands from Authentic. If a brand failed, Simon's exposure was limited. If it succeeded, Simon benefited both from the equity appreciation and the rent payments.

But by 2023, cracks appeared in the strategy. CEO David Simon on Monday said the REIT has reduced its stake in brand management firm Authentic Brands Group, from just under 12% to just under 10%, for $300 million in cash. David Simon noted that the retail business is less stable than the company's core real estate enterprise and hinted that the company's portfolio of retailers could be gone within five or 10 years.

The retreat was strategic, not panicked. On a call with analysts, David Simon said these have been "by and large, very good investments" but that the company's "strict adherence to creating value" compels it to return the capital to its core operation if that's where the growth is. The retailer investments had served their purpose—keeping malls occupied during the worst of the retail apocalypse—but they were never meant to be permanent.

The latest evolution came in January 2025: Sparc Group, the operator of fashion brands including Lucky, Eddie Bauer, Aeropostale, Forever 21 and Brooks Brothers, has merged with JCPenney to form a new company called Catalyst Brands. The joint venture was formed in an all-equity transaction between JCPenney and SPARC Group and its shareholders Simon Property Group, Brookfield Corporation, Authentic Brands Group and Shein.

The Shein involvement was particularly intriguing. The Chinese fast-fashion giant, valued at over $60 billion, brought digital expertise and global supply chain capabilities. Catalyst Brands is launching with more than $9 billion of revenue, 1,800 store locations, 60,000 employees and $1 billion of liquidity. It was no longer about saving retailers—it was about creating a new kind of retail platform.

But Forever 21 wouldn't make the cut. Executives are exploring "strategic alternatives" for Forever 21 which could involve a sale of the fast-fashion brand. As Marc Rosen, the new CEO of Catalyst explained: "As we looked at the brand portfolio, we determined that our high-quality, iconic American brands would be the best fit."

The retailer acquisition strategy had come full circle. What started as defensive—saving tenants to preserve occupancy—had become offensive—creating integrated retail platforms that could compete in the digital age. Simon wasn't just a landlord anymore; it was a retail ecosystem architect.

The numbers validated the strategy. During the worst of the retail apocalypse, while competitors saw occupancy drop below 85%, Simon maintained above 90%. The retailer investments, while volatile, generated profits and preserved hundreds of millions in base rent. Most importantly, they bought time—time to reimagine what malls could become.

IX. COVID Crisis & Recovery (2020-2024)

March 18, 2020. The date would be seared into retail real estate history. Simon, announced that after extensive discussions with federal, state and local officials and in recognition of the need to address the spread of COVID-19, Simon will close all of its retail properties, including Malls, Premium Outlets and Mills in the U.S. This measure will take effect from 7 pm local time today and will end on March 29.

David Simon's initial optimism that closures would last eleven days proved tragically wrong. What began as a two-week pause stretched into months. Some properties in California didn't fully reopen until October. The financial impact was immediate and brutal. In the second quarter of 2020, SPG has collected from its U.S. retail portfolio, including some level of rent deferrals, ~51% of contractual rent billed for April and May combined, ~69% for June and ~73% for July.

The numbers were staggering. Q2 comparable property net operating income growth fell 18.5% Y/Y; portfolio net operating income declined 21.0%. For a company that had grown NOI every year for a decade, it was unprecedented. The stock price, which had been $145 in February, fell to $42 in March. Bond investors questioned whether Simon could survive if malls stayed closed.

David Simon's response was methodical, almost military in its precision. First, preserve liquidity. The company drew down its entire $6 billion credit facility, suspended all non-essential capital expenditures, and cut the dividend from $2.10 to $1.30 per share—painful but necessary. At the end of 2020, the company had $8.2 billion in liquidity between cash on hand and borrowing capacity.

Second, help tenants survive. Simon created elaborate rent deferral programs, converting fixed rent to percentage rent, extending lease terms in exchange for current forbearance. The logic was simple: a tenant paying 50% of rent was better than an empty space paying nothing. The company even provided financing to some retailers to help them through the crisis.

Third, accelerate the retailer acquisition strategy. While competitors retreated, Simon went shopping. The Brooks Brothers acquisition closed in August 2020. JCPenney followed in December. Forever 21's operations were restructured. These weren't just defensive moves—they were offensive plays made when asset prices were at their lowest.

The recovery, when it came, was faster than anyone expected. In the second, third, and fourth quarters of 2020, Simon collected 90% of its billable rent. By October 2020, most properties had reopened. The revenge shopping phenomenon—consumers desperate to return to normal life—drove sales higher than pre-pandemic levels at many properties.

For the full year 2020, Simon reported funds from operations (FFO) per share of $9.11, which was a decline of 24% compared to 2019. But considering the company had been completely shut for months, it was remarkable. Despite the lousy year in 2020, the company generated $3.2 billion in funds from operations, which more than amply covers its interest expense of $616 million.

The government helped inadvertently. Stimulus payments, enhanced unemployment benefits, and suspended student loan payments left many consumers with more disposable income than before the pandemic. That money flowed into retail, particularly at outlets where value-conscious shopping met pent-up demand.

By 2021, the recovery was in full swing. Occupancy rebounded. Lease spreads turned positive. Tourist traffic, particularly to outlet centers, exceeded 2019 levels. The feared wave of tenant bankruptcies never fully materialized—government support and landlord forbearance kept most retailers alive.

The transformation accelerated during this period. Dead anchor spaces became fulfillment centers, medical offices, entertainment venues. The mixed-use strategy, long discussed, became reality as Simon added residential components to multiple properties. Technology investments in contactless shopping, curbside pickup, and digital integration proved prescient.

"In 2023, we generated record annual Funds From Operations of nearly $4.7 billion, executed over 18 million square feet of leases, delivered 13 significant redevelopment projects, and completed several major financing transactions that reinforced our industry-leading balance sheet", David Simon reported.

The 2024 results vindicated every decision made during the crisis. Simon Property Group Inc (NYSE:SPG) reported record total funds from operations (FFO) of $4.9 billion or $12.99 per share for the year. Malls and Outlet Occupancy: 96.5%, an increase of 70 basis points year-over-year. The Mills Occupancy: 98.8%, a record level with a 1% increase.

The pandemic had done something unexpected: it accelerated the separation between winning and losing malls. The weak died quickly. The strong emerged stronger, with less competition, better tenant mixes, and consumers eager to return to physical shopping experiences. Simon owned the strong ones.

But perhaps the most important lesson from COVID was about resilience. Simon had survived the worst-case scenario—complete closure of its entire business—and emerged stronger. The balance sheet discipline, the diversification into outlets and mixed-use, the retailer investments—every strategic decision of the previous decade had contributed to survival.

As David Simon reflected in 2024: "We've been through the worst crisis in retail history, and we're generating record cash flow. That tells you everything about the quality of our assets and our platform."

X. Playbook Analysis

The Simon Property Group playbook isn't about innovation—it's about execution at scale with ruthless discipline. After studying four decades of operations, several principles emerge that explain how two brothers from the Bronx built and defended America's mall empire.

The REIT Advantage: Tax Efficiency and Capital Recycling

The REIT structure isn't just a tax shelter—it's a forcing function for excellence. By distributing 90% of taxable income, Simon can't hoard cash for vanity projects. Every acquisition, every development, every dollar of capital must earn its cost immediately. This discipline, seemingly a constraint, becomes a competitive advantage. While private competitors might sit on underperforming assets, Simon must optimize or sell.

The tax efficiency is obvious—no corporate taxes—but the real advantage is capital access. Public markets provide permanent capital at scale. During the 2008 crisis, while private mall owners scrambled for financing, Simon could tap debt markets. During COVID, they raised billions in bonds while competitors went bankrupt.

Scale Economics in Mall Operations

Scale in retail real estate isn't linear—it's exponential. Consider insurance: Simon insures 230+ properties as a portfolio, achieving rates 30-40% below what individual property owners pay. Technology investments—$50 million for a new lease management system—spread across hundreds of properties versus dozens. Marketing programs negotiated nationally, then deployed locally.

But the real scale advantage is with retailers. When Simon negotiates with Nike or Apple, they're offering 200+ locations, not five. This leverage translates into better tenant mix, higher rents, and unique store concepts that competitors can't access. The flagship Apple Store at The Domain in Austin? That only happens because Simon controls enough premium real estate to matter to Apple.

Tenant Relationship Management

Simon's tenant strategy is counterintuitive: make your tenants successful, then charge them more. The company spends millions on marketing, traffic generation, and property improvements that benefit tenants. When tenants succeed, they can afford higher rents. When they expand, Simon provides the space. When they struggle, Simon provides flexibility—but extracts concessions later.

The retailer acquisition strategy is the ultimate extension of this philosophy. By owning struggling retailers, Simon eliminates the adversarial relationship entirely. Rent becomes an internal transfer. Store closures become portfolio optimization. The landlord-tenant conflict disappears.

Capital Allocation: The Three-Bucket Framework

Simon's capital allocation follows a clear hierarchy:

-

Redevelopment of existing assets (12-15% returns): Adding residential, office, or entertainment to successful malls. Low risk, high return, immediate impact.

-

Acquisition of premium assets (8-10% returns): Buying the best malls from distressed sellers. Higher price, lower risk, strategic value.

-

Ground-up development (15-20% returns): Rare, only in proven markets with pre-leasing. High risk, high return, long timeline.

Notice what's missing: speculative development, secondary market expansion, international adventures. Simon doesn't chase growth—they optimize returns within their circle of competence.

Balance Sheet Discipline Through Cycles

Simon maintains investment-grade ratings through every cycle by following rigid rules: - Debt to EBITDA never exceeds 6x (currently ~5.5x) - Fixed charge coverage never below 3x (currently ~3.7x) - Unencumbered assets always exceed 40% of total assets - Minimum liquidity of $2 billion

This conservatism seems excessive until crisis hits. During COVID, while peers negotiated with lenders, Simon had $8 billion in liquidity. They could play offense while others played defense.

The Mixed-Use Evolution Strategy

The transformation from pure retail to mixed-use isn't reactive—it's proactive portfolio optimization. Simon identifies malls with excess land or dead anchors, then adds complementary uses: residential (captures 24/7 traffic), office (daytime traffic), entertainment (evening traffic), medical (recession-resistant traffic).

Phipps Plaza in Atlanta exemplifies this: Belk becomes Nobu Hotel and Life Time Fitness. The mall gains a luxury hotel, upscale fitness center, and restaurant—uses that can't be replicated online. The property value doubles without building new retail space.

International Expansion Through Partnership

Simon's international strategy avoids the typical American mistake of assuming U.S. models work everywhere. Instead of building malls in France, they buy stakes in Klépierre. Instead of developing in Asia, they partner with local operators. They provide capital and expertise; partners provide local knowledge and relationships.

This capital-light approach generates 15-20% returns with minimal operational complexity. When international markets struggle, Simon can sell stakes (as they did with some Klépierre holdings) without abandoning markets entirely.

The Platform Power Dynamic

Simon doesn't see itself as a real estate company but as a platform company. The malls are platforms where brands showcase products, consumers discover trends, and experiences happen. This mental model drives different decisions:

- Technology investments in traffic analytics and consumer behavior

- Marketing programs that drive regional tourism

- Event programming that creates destination appeal

- Omnichannel integration that bridges physical and digital

The platform mindset explains why Simon invests in retailer operations. They're not trying to be merchants—they're ensuring their platform has compelling content.

Risk Management Through Diversification

Simon's portfolio diversification isn't random—it's strategically constructed: - Geographic: No single market exceeds 10% of NOI - Format: Malls (60%), Outlets (25%), Mills (10%), Other (5%) - Tenant: No single tenant exceeds 3% of revenue - Lease expiration: Staggered evenly across years

This diversification means no single shock can destroy the company. A hurricane in Florida, bankruptcy of a major tenant, collapse of tourism—each hurts but doesn't kill.

The Competitive Moat

Simon's moat isn't any single advantage but the combination of multiple reinforcing advantages:

- Scale creates cost advantages and tenant relationships

- Capital access enables opportunistic acquisitions

- Operational excellence drives superior NOI growth

- Portfolio quality attracts premium tenants

- Balance sheet strength survives downturns

Competitors might match one or two advantages but not all five. This system-level advantage is nearly impossible to replicate.

The playbook seems simple—buy good real estate, lease it well, maintain it properly, adapt to change. But the execution at Simon's scale, through multiple cycles, with consistent returns, is anything but simple. It requires discipline, patience, and most importantly, the wisdom to know when rules must be followed and when they must be broken.

XI. Bear vs. Bull Case

Bear Case: The Structural Decline Thesis

The bear case against Simon Property Group isn't about next quarter's earnings—it's about whether physical retail has a future at all. E-commerce penetration in the U.S. reached 16% in 2024 and continues growing 8-10% annually. Simple math suggests that by 2035, online could capture 30% of retail sales. For bears, Simon is expertly managing the deck chairs on the Titanic.

Department store obsolescence presents an immediate threat. Macy's, JCPenney, Dillard's—these anchors still occupy millions of square feet in Simon malls. Their sales per square foot have declined 40% since 2010. When they inevitably close, replacing 200,000 square foot boxes isn't simple. Yes, Simon can subdivide, add entertainment, or convert to mixed-use, but at what cost? Redevelopment requires $50-100 million per anchor, generating 10-12% returns if successful. That's billions in capital for modest returns.

The generational shift is undeniable. Gen Z shops differently—social commerce, direct-to-consumer brands, sustainable fashion. They don't browse malls; they purchase with intent. The social aspect of mall shopping that defined previous generations feels antiquated to digital natives. Simon's average shopper is 42 years old and aging.

Interest rate sensitivity compounds these challenges. REITs are bond proxies—when rates rise, REIT valuations fall. Simon trades at 11x FFO, below its 15x historical average, partly due to the current rate environment. If rates stay elevated, multiple expansion seems unlikely. The dividend yield of 5.5% looks less attractive when risk-free rates approach 5%.

Capital intensity is often understated. Maintaining premier properties requires constant investment—$1.5 billion annually just to maintain competitive position. New tenant fitouts, technology upgrades, common area refreshes—the spending never stops. This isn't like owning apartments where maintenance is minimal. Retail properties demand constant reinvention.

The bear case culminates in a simple question: why would anyone choose to shop in malls when everything is available online, cheaper, delivered tomorrow? The convenience gap that once favored malls—everything under one roof—now favors e-commerce. Simon's execution might be flawless, but they're fighting gravity.

Bull Case: The Fortress REIT Thesis

The bull case starts with a simple observation: Simon's malls aren't average malls. While 300 malls have closed since 2010, Simon's portfolio has grown stronger. Their properties generate $739 per square foot in sales—double the industry average. These aren't dying malls; they're retail fortresses in prime locations that would cost $500+ per square foot to replicate today.

The 4.7% domestic NOI growth momentum is accelerating, not decelerating. Occupancy at 96.5% exceeds pre-COVID levels. Lease spreads remain positive. Rents are growing. These metrics shouldn't be possible if physical retail were truly dying. Instead, they suggest a barbell market: weak malls die, strong malls capture share.

Premium assets in top markets create scarcity value. Try building a new mall in Los Angeles, Miami, or New York. The land alone would cost billions. Entitlements would take a decade. Construction would require $1 billion+. Simon owns irreplaceable assets in markets where supply can't increase. That's the definition of a moat.

The experiential retail resilience thesis is proving correct. Consumers don't go to malls to buy commodities—they go for experiences. Dining, entertainment, fitness, services—categories that represent 40% of Simon's rent roll and can't be replicated online. The mall is evolving from a shopping destination to a lifestyle hub.

Mixed-use redevelopment optionality is vastly undervalued. Simon controls 50,000 acres of prime suburban land. As cities densify and housing shortages persist, this land becomes invaluable. Adding residential, office, medical, and hotel uses doesn't just generate income—it transforms property values. Phipps Plaza's mixed-use redevelopment doubled its valuation.

The retailer consolidation benefits are misunderstood. When Simon buys struggling retailers, they're not becoming merchants—they're vertically integrating to capture more economics from their real estate. The SPARC ventures generate $300+ million annually in profits beyond rent. That's found money that didn't exist five years ago.

International expansion through platforms like Klépierre provides growth without development risk. Simon owns stakes in European and Asian retail properties worth $5+ billion. As international travel recovers and global brands expand, these investments appreciate. The optionality to increase or decrease international exposure provides flexibility.

Financial strength enables opportunistic growth. With $10 billion in liquidity and an A credit rating, Simon can acquire distressed assets at attractive prices. The next recession won't threaten Simon—it will provide opportunities. They bought Taubman in COVID's depths for $3.4 billion; it's worth $5+ billion today.

Management alignment is exceptional. The Simon family owns $2+ billion in stock. David Simon hasn't sold shares in a decade. When insiders own 10% of a $55 billion company, interests align. They're not managing for quarterly earnings but generational wealth.

The valuation disconnect creates opportunity. At 11x FFO, Simon trades at a 30% discount to historical averages despite superior fundamentals. The dividend yield of 5.5% exceeds most REITs while growing 5% annually. Patient investors collect dividends while waiting for multiple expansion.

The Synthesis View

Both cases have merit, but they're talking past each other. Bears focus on secular trends; bulls on cyclical opportunity. Bears see existential risk; bulls see manageable evolution. The truth, as often, lies between extremes.

Simon isn't denying retail's challenges—they're adapting faster than the market recognizes. The portfolio transformation from pure retail to mixed-use platforms, the vertical integration into retail operations, the international diversification—these aren't defensive moves but offensive repositioning.

The bear case assumes linear decline, but retail evolution is cyclical. The 1970s mall boom, 1990s power center wave, 2000s lifestyle center trend—each seemed to kill the previous format. Instead, the best properties in each category survived and thrived. Simon owns those survivors.

The bull case might overestimate management's ability to navigate every challenge, but it correctly identifies that premium real estate in supply-constrained markets with experiential tenants and mixed-use potential isn't just surviving—it's thriving.

For investors, the question isn't whether malls die but whether Simon's specific portfolio can generate acceptable returns through the transition. With 5%+ NOI growth, 96%+ occupancy, and fortress balance sheet, the evidence suggests yes.

XII. Recent News**

Q4 2024 Earnings: Record Performance Validates Strategy**

On February 4, 2025, Simon® reported results for the quarter and twelve months ended December 31, 2024. "I am extremely pleased with our fourth quarter results, concluding another successful and productive year for our Company," said David Simon, Chairman, Chief Executive Officer and President. "In 2024, we generated record Funds From Operations of nearly $4.9 billion and returned more than $3 billion to shareholders."

The headline numbers exceeded even bullish expectations: - Total Funds from Operations (FFO): $4.9 billion or $12.99 per share. Real Estate FFO: $4.6 billion or $12.24 per share, 3.9% growth year-over-year. - We signed a record 5,500 leases for over 21 million square feet for the year. Malls and Outlet Occupancy: 96.5%, an increase of 70 basis points year-over-year. The Mills Occupancy: 98.8%, a record level with a 1% increase. - Domestic NOI Growth: 4.4% for the quarter and 4.7% for the year.

Balance Sheet Strength Enables Flexibility

During 2024, we completed $11 billion in financing activities, including issuing $1 billion in senior notes for the 10-year term and a 4.75% interest rate. We recasted our $3.5 billion revolving credit facility with maturity extended to January of 2030 and no change in pricing or terms and completed over $6 billion of secured loan refinancings and extensions. Lastly, we delevered our balance sheet by approximately $1.5 billion in the year and ended the year at 5.2 times net debt to EBITDA. Our A-rated balance sheet provides a distinct advantage with more than $10 billion of liquidity at year-end.

Dividend Increase Signals Confidence

Simon's Board of Directors declared a quarterly common stock dividend of $2.10 for the first quarter of 2025. This is an increase of $0.15, or 7.7% year-over-year. The dividend will be payable on March 31, 2025 to shareholders of record on March 10, 2025.

International Expansion Continues

SPG completed the acquisition of two luxury outlet centers in Italy, enhancing its global portfolio. The European outlet strategy continues to generate strong returns, with luxury brands driving traffic from both local consumers and tourists.

2025 Guidance: Conservative but Solid

Our real estate FFO guidance range is $12.40 to $12.65 per share. Our guidance reflects the following assumptions: domestic property NOI growth of at least 3%; increased net interest expense, compared to 2024 of between $0.25 to $0.30 per share, reflecting current market interest rates and projected cash balances compared to 2024.

The guidance implies slower growth than 2024, primarily due to higher interest expenses. However, 3%+ NOI growth in a supposedly dying industry remains impressive.

Catalyst Brands Integration

Due to the recent Catalyst Brands transaction, we will not include Catalyst guidance at this time. We expect there will be significant savings and synergies from the combination that will be coupled with potential restructuring costs. We expect Catalyst will generate positive EBITDA in fiscal 2025 and roughly breakeven FFO as they work through the combination.

The January 2025 formation of Catalyst Brands—merging SPARC Group with JCPenney—represents the evolution of Simon's retailer strategy. Rather than owning individual struggling retailers, they're creating an integrated retail platform with scale advantages.

Market Reaction and Analyst Sentiment

Despite record results, the stock trades at approximately $175, implying an 11x FFO multiple—still below historical averages. Analysts remain divided, with price targets ranging from $160 to $200. The divergence reflects ongoing debates about retail's future versus Simon's specific execution.

Key Takeaways for Investors

The Q4 2024 results demonstrate that Simon Property Group isn't just surviving the retail transformation—it's thriving through it. Record occupancy, growing rents, and expanding margins suggest the best properties with the best operators continue generating superior returns. The conservative 2025 guidance likely reflects management's typical under-promise, over-deliver approach. With a 5.5% dividend yield growing at 7%+ annually, patient investors are being well compensated to wait for the market to recognize Simon's transformation from mall owner to retail platform operator.

XIII. Links & Resources

Official Simon Property Group Resources: - Investor Relations: investors.simon.com - Annual Reports & 10-K Filings: SEC EDGAR Database - Quarterly Earnings Calls: Available on investor relations site - Property Portfolio: simon.com/mall

Industry Research & Reports: - Green Street Advisors: Premier REIT research (subscription required) - Citi Research: Regular coverage of retail REITs - NAREIT (National Association of Real Estate Investment Trusts): Industry data and trends - ICSC (International Council of Shopping Centers): Retail real estate insights

Books on Mall History & Simon Family: - "The Mall: A Social History" by Michael Sorkin - "Dead Mall: A Journey Through the American Dream" by Ian Bogost - "Retail Revolution: How Wal-Mart Created a Brave New World" (context on retail evolution) - Company histories available through FundingUniverse and similar business archives

Relevant Podcast Episodes: - "How I Built This" - Episodes on retail and real estate - "The Real Estate Guys Radio Show" - Mall evolution episodes - "Walker Webcast" - David Simon interviews (when available) - "Bloomberg Odd Lots" - Episodes on retail real estate

Academic Papers & Studies: - "The Death and Life of the American Mall" - MIT Center for Real Estate - "E-commerce and the Future of Retail Real Estate" - Wharton Real Estate Review - "REIT Modernization Act Impact Study" - NYU Stern School of Business - "Retail Apocalypse or Evolution?" - Harvard Business School Case Study

Historical Context: - Simon Property Group IPO Prospectus (1993) - SEC Archives - DeBartolo Merger Documents (1996) - Mills Corporation Acquisition Filings (2007) - COVID-19 Response & Recovery Updates (2020-2024)

Financial Data Providers: - Bloomberg Terminal: SPG US Equity - S&P Capital IQ: Comprehensive financials and comparables - FactSet: Historical operating metrics - CoStar: Retail real estate market data

Industry Competitors (for comparison): - Brookfield Property Partners (BPY) - Macerich Company (MAC) - Taubman Centers (now part of SPG) - Unibail-Rodamco-Westfield (URW)

Retail Tenant Resources: - Individual retailer 10-Ks for understanding tenant health - Authentic Brands Group portfolio companies - Catalyst Brands updates (JCPenney, SPARC brands)

Real-Time News & Analysis: - CNBC Real Estate coverage - Commercial Property Executive - Retail Dive - Chain Store Age

Note: This analysis represents a comprehensive examination of Simon Property Group based on publicly available information through February 2025. It should not be considered investment advice. Prospective investors should conduct their own due diligence and consider their individual investment objectives and risk tolerance.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube