SpaceX: The $2.1 Trillion AI Frontier

I. The Goldilocks Debut

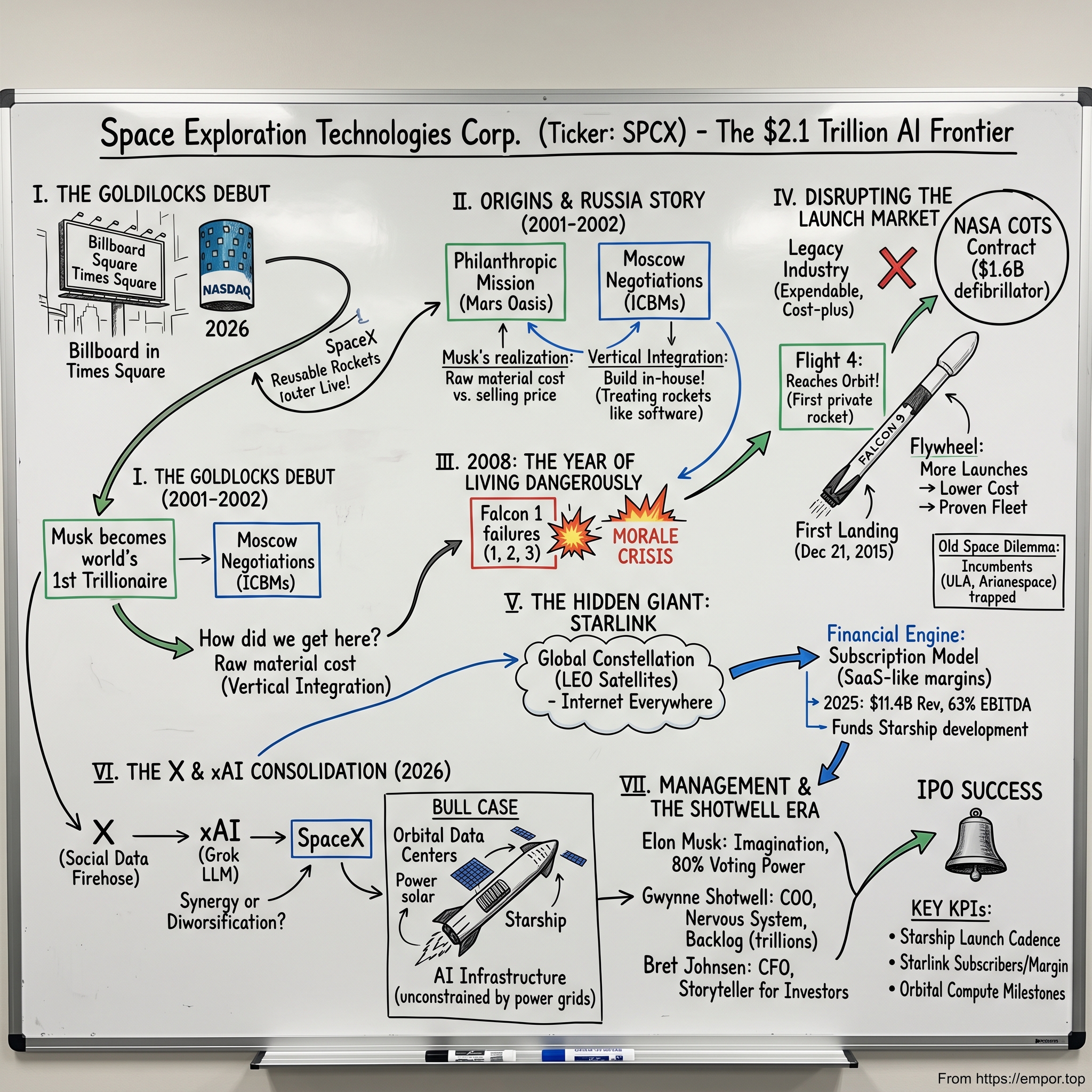

On Friday morning, June 12, 2026, the most photographed object in New York City was not a person. It was a billboard. The electronic canyons of Times Square—those manic, oversized screens that normally hawk Broadway musicals and energy drinks—glowed in a single, coordinated palette of black, white and rocket-exhaust orange. Tourists tilted their phones upward. And at the center of it all, on the facade of the Nasdaq MarketSite, a number kept climbing that would, by the closing bell, rearrange the global wealth rankings: Space Exploration Technologies Corp.—ticker SPCX—had become a public company valued at roughly $2.1 trillion, the largest initial public offering in the history of capitalism.1

There is a phrase Wall Street traders use for an IPO that lands exactly right—not so cheap that the company leaves money on the table, not so expensive that the stock craters on day one. They call it a "Goldilocks debut." SpaceX got one. Shares opened, surged 19% in their first session, and by the time Gwynne Shotwell and a clutch of grinning executives rang the closing bell, the company had done something no rocket maker, no telecom, no defense contractor had ever managed: it had convinced everyday investors—not just sovereign wealth funds and crossover hedge funds, but retail buyers clicking "buy" from their phones—to fund a vision that includes a million-person city on Mars.1

And here is the strange, almost vertiginous fact that frames everything in this episode. Elon Musk, who founded this company in 2002 with a plan so modest it involved mailing plant seeds to Mars, became, on that Friday afternoon, the world's first trillionaire—his net worth tipping past the thirteen-figure threshold as the value of his roughly 80% voting stake re-rated in real time.[^2]

So how did we get here? How did a company that blew up three rockets in a row between 2006 and 2008, that was hours from payroll insolvency, that the entire aerospace establishment dismissed as a dot-com millionaire's expensive hobby—how did that company become, in the language of its own S-1, an "AI infrastructure utility for the solar system"?

That is the question of this episode. Because SPCX is not, fundamentally, a rocket story anymore. The rockets are the moat. The real business—the thing that produced the cash flows that made this IPO mathematically defensible—is a satellite internet network that became a telecom giant, wrapped around an artificial-intelligence ambition that the company values at the center of a $26.5 trillion total addressable market.2 It is a story of counter-positioning, of one of the great vertical-integration plays in industrial history, and of a founder whose single most consistent strategy across twenty-four years has been deceptively simple: chase superlatives, and let the superlatives do the marketing.

We're going to trace the whole arc—from a Moscow negotiating table where Russian rocket executives reportedly spat at the Americans, to the December night a booster came down on its tail like something from a 1950s pulp magazine, to the IPO roadshow that priced humanity's expansion into space. Let's get into it.

II. Origins and the Russia Story

Rewind to 2001. Elon Musk is thirty years old, freshly and obscenely rich. The sale of his stake in PayPal would soon hand him roughly $180 million after taxes—generational money, the kind that buys islands and never working again.3 Most people in that position optimize for comfort. Musk did something closer to the opposite. He had become quietly obsessed with a single statistic that bothered him: NASA, he discovered when he went looking on its website, had no actual plan and no timeline to send humans to Mars. The public, he concluded, had simply lost interest. The Apollo-era dream had gone cold.

His first instinct was not to build anything. It was a publicity stunt. Musk wanted to fund a small philanthropic mission he called "Mars Oasis"—land a tiny robotic greenhouse on the Martian surface, sprout green plants against that rust-colored desert, and beam back a photograph. "The public tends to respond to precedence and superlatives," he explained later at Stanford. "This would be the furthest that life's ever traveled, the first life on Mars."[^5] The image, he reasoned, would shame Congress into reopening the country's wallet for space. It is worth pausing on how revealing this is. Before SpaceX existed, before a single bolt was tightened, Musk's theory of change was a marketing theory: capture imagination, manufacture excitement, and money and political will would follow. That theory is the throughline of this entire company—and, eventually, of its IPO.

To get his greenhouse to Mars, though, he needed a rocket. And rockets, he found, were absurdly expensive. So in late 2001 and into 2002, Musk did one of the more cinematic things a newly minted millionaire has ever done: he flew to Moscow to try to buy refurbished intercontinental ballistic missiles—decommissioned Soviet ICBMs, the very instruments built to end the world—to repurpose as space launchers. He went back two or three times. At one meeting, as the story has been told and retold, the Russian negotiators from the old-line rocket bureaus connected to Роскосмос Roscosmos treated this brash foreigner with open contempt, reportedly viewing him as a naive tourist, and quoted him a price—$8 million apiece—that he considered a deliberate insult.

On the flight home, deflated and somewhat humiliated, Musk did the thing that defines him. He opened a spreadsheet. He started calculating the raw cost of the materials that go into a rocket—the aluminum, the titanium, the carbon fiber, the fuel—and arrived at a now-famous realization: the raw materials were on the order of 2% of the typical price of a finished rocket. The other 98% was the way the industry built them—bespoke, one-off, cost-plus, and thrown away after a single use. "I can build them myself," he concluded. The realization was not really about Russia. It was about a business model. The legacy space industry had no incentive to lower costs; it was paid a margin on top of whatever it spent, so spending more was, perversely, more profitable.

In June 2002, Musk founded Space Exploration Technologies with roughly $100 million of his own PayPal proceeds—a sum he has repeatedly described as a bet he expected to lose.3 He gave the company, by his own telling, low odds of success. This is the part of the origin myth that gets flattened over time: Musk did not start SpaceX believing it would work. He started it believing the attempt itself might reignite a dormant national appetite for space, and that if it failed, he'd at least have tried.

What he built into the company's DNA from day one would become its single greatest structural advantage: radical vertical integration. Where Boeing and Lockheed Martin assembled rockets from a sprawling supply chain of subcontractors—each adding cost and margin—SpaceX would make as much as possible in-house. Engines, avionics, flight software, the structures themselves. This was partly ideology, partly necessity (few suppliers wanted to deal with a startup), and partly the "hardcore" engineering culture Musk imported from software: move fast, test hardware to failure, iterate. In an industry where a single failure could mean a decade-long government inquiry, SpaceX would blow things up on purpose to learn faster. That cultural choice—treating rockets like software releases rather than cathedrals—is the seed of everything that follows. But first, the culture nearly killed the company.

III. 2008: The Year of Living Dangerously

By the summer of 2008, Elon Musk was, in the most literal sense, running out of everything. Money. Marriage. Margin for error. The financial world was collapsing around him—Lehman Brothers would file for bankruptcy that September, dragging the global economy into the worst crisis since the Depression—and inside that macro catastrophe, a much smaller drama was reaching its own breaking point on a remote atoll in the Pacific.

SpaceX's first rocket, the Falcon 1, was a slim, single-engine vehicle launched from Omelek Island, a speck of coral in the Marshall Islands. And it kept failing. The first flight, in March 2006, caught fire seconds after liftoff and crashed back toward the island—the culprit, a corroded aluminum nut. The second, in March 2007, made it to space but the upper stage sloshed its fuel and tumbled. The third, in August 2008, suffered a timing error during stage separation; the stages collided. Three launches, three failures, and—this is the gut-punch—the third flight had been carrying payloads, including ashes belonging to NASA astronaut Gordon Cooper and actor James Doohan, Star Trek's Scotty. They were lost in the Pacific.

Here is the financial reality nobody outside the company fully understood at the time. Musk had enough money for, at most, one more attempt. Tesla was simultaneously hemorrhaging cash and weeks from its own insolvency. He has since described having to choose, mentally, how to split his last reserves between the two companies, knowing that one wrong move would sink both. Employees later recalled the morale crisis—the sense, after the third failure, that they had given years of their lives to something that was about to die. Musk gathered the team and told them, essentially, that they would fly a fourth time, and that he would find the money somehow.

They scrambled. The fourth Falcon 1, assembled partly from spare parts, was rushed to the pad. On September 28, 2008, it lifted off Omelek Island and, this time, everything worked. Falcon 1 reached orbit—the first privately developed, liquid-fueled rocket ever to do so.[^5] In the control room, the celebration was less joy than collapse, the sound of people who had been holding their breath for two years. It is one of the genuinely mythic moments in modern business history: a company that bet its entire existence on being first, and got there with what Musk has said was essentially the last of the capital.

But the fourth flight, for all its symbolism, did not save SpaceX. A working rocket with no paying customers is just a very expensive fireworks display. What saved SpaceX arrived three days before Christmas. On December 23, 2008, NASA awarded SpaceX a Commercial Orbital Transportation Services contract—part of a program structured to pay private companies to resupply the International Space Station—worth $1.6 billion for twelve cargo flights.[^6] For a company that had been counting payroll in weeks, $1.6 billion was not a contract. It was a defibrillator.

And this is where the 2008 story rhymes with the broader 2008 story in a way that matters for investors. While the financial crisis was teaching the world that scale and government backstops separated the survivors from the dead, SpaceX learned the same lesson in miniature. The COTS contract was not charity; NASA needed a cheaper ride to the station and was willing to seed a competitor to the old guard. But the effect was that the U.S. government became SpaceX's anchor customer and de facto venture backer at the exact moment private capital had vanished. Survival, in a year when survival was the only thing that counted, became the company's first real competitive advantage. The lesson Musk drew—that being indispensable to a deep-pocketed customer is its own kind of moat—would shape every strategic decision that followed. Now he needed a rocket worthy of that customer. The Falcon 1 was a proof of concept. The next vehicle would be the business.

IV. Disrupting the Launch Market

To understand the leap from Falcon 1 to Falcon 9, picture the difference between a kit plane and a commercial airliner. The Falcon 1 had one engine and could lift a few hundred kilograms—enough to prove the physics, not enough to make money. The Falcon 9, which first flew in 2010, had nine engines clustered at its base (hence the name), could carry serious commercial and government payloads, and was designed from the outset around an idea the entire industry considered borderline crackpot: that the most expensive part of the rocket, the first-stage booster, could fly back down, land intact, and be used again.

Think about what "expendable" actually meant in legacy aerospace. Every single launch threw away a machine that cost tens of millions of dollars to build. Musk's favorite analogy was devastating in its simplicity: imagine if every Boeing 747 were scrapped after one flight from Los Angeles to New York. A transcontinental ticket wouldn't cost a few hundred dollars; it would cost a quarter of a million. That, he argued, was exactly the economics strangling spaceflight. The industry had quietly accepted that rockets were disposable, the way you'd accept that a bullet is disposable. SpaceX's entire counter-positioning thesis was to reject that premise.

The attempts to land a booster were, for years, a public comedy of explosions. SpaceX even released a blooper reel of boosters cartwheeling into the ocean and detonating on landing barges—again, the software-culture instinct to fail in public and learn fast. Then came the night that changed the industry's math. On December 21, 2015, the first stage of a Falcon 9 lifted a payload to orbit, separated, flipped around, reignited its engines, and descended through the Florida dark to settle upright on a landing pad at Cape Canaveral—the first time an orbital-class booster had ever been recovered intact.[^5] Inside SpaceX's Hawthorne headquarters, employees reportedly chanted "USA, USA" so loudly that Musk could barely be heard. It looked, frankly, like science fiction: a skyscraper-sized rocket lowering itself tail-first onto a bullseye.

The economics of what that unlocked are the whole ballgame. A recovered booster could be inspected, refurbished, and reflown. Over the following decade, SpaceX drove the marginal cost of a launch down and the cadence up to a level that made the rest of the world's launch providers look like horse-drawn carriages at an auto show. The company came to perform the majority of the planet's orbital launches by mass—the largest space-launch operation on Earth.1 Reusability didn't just make SpaceX cheaper; it made the competition's entire cost structure obsolete.

Now, the "Old Space" response. This is where it gets almost painful to watch. Boeing and Lockheed Martin had jointly formed a launch venture, United Launch Alliance, that for years enjoyed a comfortable government monopoly on national-security launches—a cost-plus arrangement with little pressure to innovate. Arianespace, Europe's launch champion, had a CEO who, as late as the mid-2010s, publicly doubted reusability would ever be economical. The incumbents were trapped by a classic disruptor's dilemma: to match SpaceX, they would have had to cannibalize the lucrative expendable-rocket businesses they were built on, and admit their core model was dead. They couldn't, and they didn't, fast enough. Counter-positioning works precisely because the incumbent's rational self-interest prevents them from copying you. By the time the establishment took reusability seriously, SpaceX had a half-decade head start and a flight-proven fleet.

But here's the twist that turns this from a great launch business into a trillion-dollar one. Reusability gave SpaceX something nobody else had: cheap, abundant access to orbit. And the most valuable thing you can do with cheap, abundant access to orbit is not launch other people's satellites. It's launch your own.

V. The Hidden Giant: Starlink

For most of SpaceX's life, the launch business was the face of the company and the source of its mythology. But somewhere in the late 2010s, a second business began quietly growing inside it that would, by the time of the IPO, become the actual financial engine of the entire enterprise. That business is Starlink, and to understand why it changed everything, you have to understand the problem it solved—and the problem it created for SpaceX's own balance sheet.

The pitch was deceptively simple: blanket the planet in a "constellation" of thousands of small satellites flying in low Earth orbit—close enough to the ground that the signal latency feels like terrestrial broadband—and beam high-speed internet down to a pizza-box-sized dish anywhere on Earth. Rural Montana. The middle of the Atlantic. A battlefield in Ukraine. A village with no fiber and no prospect of ever getting it. Previous satellite-internet ventures had tried versions of this and gone spectacularly bankrupt in the 1990s; the names Iridium and Teledesic were industry shorthand for capital incineration. The economics had never worked because launching that many satellites was ruinously expensive.

Unless, of course, you happened to own the world's cheapest rocket. This is the strategic elegance of the thing, and it's worth saying plainly: Starlink is only possible because of reusability. SpaceX could launch its own satellites, by the dozen, on its own boosters, at internal cost. The launch business and the satellite business fed each other in a loop no competitor could replicate without first building a reusable rocket fleet of their own. By the mid-2020s, Starlink operated the largest satellite constellation in history—more than ten thousand active satellites in low orbit, by far the biggest such system ever flown.1

For years, the bears called it exactly what it looked like: a capital-incinerating moonshot, billions of dollars launched into the sky on a bet that consumers and governments would pay monthly subscriptions for space internet. And then, somewhere around 2023 and 2024, the curve bent. The subscriber base crossed into the millions. And in 2025, the numbers turned genuinely staggering. According to reporting on the segment's financials, Starlink generated roughly $11.4 billion in revenue in 2025, at EBITDA margins around 63%.4 Sit with that margin figure for a moment. A 63% EBITDA margin is not a hardware-company number. It is a software-company number, a toll-road number, the kind of margin you see from a business that built an enormously expensive asset once and now collects recurring rent on it.

That is the conceptual shift investors had to make to underwrite this IPO. SpaceX stopped being a launch company that happened to run a satellite side project and became a telecom and connectivity utility that happens to own a launch company. Starlink is a recurring-revenue, subscription business with the gross margins of a SaaS firm and a customer base spanning consumers, airlines, maritime fleets, and—critically—militaries that now treat space-based connectivity as essential infrastructure. The launch business is cyclical and lumpy; the satellite business is a monthly check that arrives whether or not a rocket flew that week.

This is the scale-economies flywheel that funds everything else in the Musk empire's space wing. More launches lower the cost per launch; lower launch costs make more Starlink satellites economical; more satellites mean more subscribers and more cash; more cash funds the next, larger rocket—Starship—which lowers launch costs further still. Each turn of the wheel widens the gap between SpaceX and anyone trying to start the race from zero. And it was this cash flow, finally, that gave Musk the financial credibility to do the most audacious thing in the entire SPCX story: fold his artificial-intelligence ambitions directly into the rocket company.

VI. The X and xAI Consolidation

Every Elon Musk company is, eventually, revealed to be a single company wearing different costumes. For years observers joked about the "Musk Master Plan"—the way Tesla, SpaceX, X, the Boring Company, Neuralink, and xAI seemed to share engineers, capital, data, and a founder's attention in ways no governance textbook would endorse. In 2026, the joke became a balance sheet. SpaceX absorbed xAI, Musk's artificial-intelligence company, in a stock consolidation that turned the rocket maker into something genuinely without precedent: a vertically integrated space-launch, satellite-telecom, and AI-compute conglomerate under one ticker.[^8]

To follow the logic, you have to trace the corporate Russian nesting dolls. In 2023, xAI—Musk's startup built to develop the Grok large language model as a rival to OpenAI and Anthropic—acquired X, the social-media platform formerly known as Twitter that Musk had bought in 2022 for $44 billion. The rationale was data: a frontier AI model is only as good as the text it trains on, and X was a firehose of real-time human conversation. Folding the social network into the AI lab gave Grok a proprietary, constantly refreshing training corpus. Then, in 2026, SpaceX acquired the combined xAI-X entity, bringing the model, the data, and the social platform under the rocket company's roof just ahead of the public listing.[^8]

The obvious question—the one every Acquired listener is already shouting—is: did SpaceX overpay? Folding a money-losing social network and a cash-burning AI lab into a profitable space company is exactly the kind of "diworsification" that has destroyed conglomerates before. The ghost haunting this deal is AOL–Time Warner, the 2000 merger that fused a hot internet company onto an old-media giant and vaporized something like $100 billion in value when the synergies turned out to be fictional. Skeptics look at SpaceX-xAI and see the same pattern: a founder using the inflated currency of one beloved business to bail out his troubled others.

But the bulls point to the opposite historical analogy: Google's 2006 acquisition of YouTube, a then-unprofitable site that looked like a reckless overpay and turned out to be one of the great bargains in corporate history, because the acquirer's infrastructure—Google's ad engine and server farms—was exactly what the target needed to become a giant. The SpaceX bull case rests on an analogous claim of genuine, physical synergy, and it is the single most important idea in the entire IPO. It is called the orbital data center.

Here is the concept in plain terms. Training and running advanced AI models consumes staggering amounts of electricity and, just as critically, water and land for cooling—terrestrial data centers are colliding with the physical limits of the power grid. SpaceX's argument, laid out in its IPO materials and supporting projections, is that the best place to put AI compute may not be on Earth at all. In orbit, solar power is constant and free of atmosphere, the cold of space offers a cooling sink, and there are no neighbors to object to a new substation. Use Starship to haul data-center-grade compute into orbit, power it with vast solar arrays, network it through the Starlink constellation, and you have AI infrastructure unconstrained by the terrestrial power grid that is currently bottlenecking every other AI company on Earth.5 That is the synergy story: rockets to lift it, satellites to connect it, AI to run on it. The S-1 framed the prize as a slice of a $26.5 trillion total addressable market spanning launch, connectivity, and artificial intelligence.2

Whether the orbital data center is a genuine engineering roadmap or the most expensive sci-fi pitch deck ever filed with the SEC is, quite literally, the trillion-dollar question—and we'll return to it in the bear case. What's undeniable is that it gave investors a narrative that converted a rocket company's IPO into an AI IPO, at a moment when AI is the only story the public market wants to hear. Pulling that off required more than a visionary founder making promises. It required someone who could actually run the place.

VII. Management and the Shotwell Era

If Elon Musk is the imagination of SpaceX, Gwynne Shotwell is its nervous system. For most of the company's history she has been, in the affectionate shorthand of employees and analysts alike, "the adult in the room"—the person who turns Musk's superlatives into signed contracts, met payrolls, and on-time launches. As President and Chief Operating Officer, she has run the actual business of SpaceX for nearly two decades, and her fingerprints are all over the operational machine that made the IPO bankable.6

Shotwell's background is instructive. She is a mechanical engineer and applied mathematician by training, not a financier and not a showman. She joined SpaceX in 2002 as employee number eleven, in charge of business development—which, in a company that had no product and a habit of exploding, mostly meant convincing skeptical customers to trust a startup with their multimillion-dollar satellites. Her defining skill is the one Musk most conspicuously lacks: she builds and keeps relationships. Where Musk antagonizes—regulators, customers, the occasional head of state—Shotwell repairs and reassures. Industry lore holds that she personally landed the early commercial contracts that, alongside the NASA lifeline, kept the company breathing in the lean years. The operational result of that patient relationship-building is the metric the IPO leaned on hardest: a contracted backlog reported in the trillions of dollars, a pipeline of launch and connectivity commitments that gives the revenue forecasts something concrete to stand on.6

Alongside her, Chief Financial Officer Bret Johnsen handled the unglamorous, essential work of turning a chronically loss-making venture into an entity that public markets could digest. The bridge a CFO must build for an IPO like this is treacherous: SpaceX spent years deliberately plowing every dollar into Starship development and the Starlink constellation, the kind of spending that produces red ink today for the promise of cash tomorrow. Johnsen's task was to tell that story in a way that disciplined public investors—who punish unexplained losses—would accept as investment rather than profligacy. The Goldilocks pricing of the debut suggests the story landed.

Then there is the governance, which any fundamental investor must look at clearly. Musk holds roughly 80% of the voting power.[^2] In Hamilton Helmer's framework this is a kind of Cornered Resource all its own—but it cuts both ways. It means the company's single greatest asset, Musk's vision and fundraising gravity, is locked in and cannot be ousted by activist shareholders. It also means public investors are, in effect, passengers. They are buying a minority economic interest in an enterprise where a single, famously mercurial individual controls every major decision, from capital allocation to which political causes the company's brand gets associated with. There is no board that can meaningfully overrule him. For some investors that concentration is the whole appeal; for others it is the central risk.

The human texture of this company is worth dwelling on, because it explains the loyalty. SpaceX's "hardcore" culture asks engineers for punishing hours in exchange for a shot at building the future—and, increasingly, life-changing wealth. A robust secondary market valued employee shares at tens of billions of dollars in aggregate before the listing, and the IPO minted a new class of paper millionaires across an engineering workforce, many of them clustered in the company town that has grown up around the Starship launch site.[^11] Starbase, Texas—a stretch of South Texas coastline near Brownsville that incorporated as an actual municipality—is the physical embodiment of the culture: a place where people live, work, and launch rockets in the same few square miles, a 21st-century industrial company town. That concentration of talent, willingly working at an intensity competitors can't match, is itself a competitive advantage. Which brings us to the framework portion of our show.

VIII. The Playbook: Powers and Forces

Let's war-game this thing properly, using the two lenses we always reach for: Hamilton Helmer's 7 Powers and Michael Porter's Five Forces. Because a $2.1 trillion valuation is not a fact, it is a claim—a claim that SpaceX possesses durable advantages that will let it earn extraordinary returns for decades. Let's test it.

Start with Helmer's Powers. The first and most important is Counter-Positioning, which we've already seen in action: reusability versus the legacy expendable model. The genius of counter-positioning is that the incumbent can see exactly what you're doing and still can't follow, because copying you would destroy their existing profit pool. Boeing and Lockheed could not embrace reusability without admitting their cost-plus expendable business was obsolete—so they didn't, and SpaceX ran away with the market. This power is real and largely already cashed in.

The second is Scale Economies, embodied in the Starlink constellation and the launch flywheel. With the largest satellite network and the highest launch cadence in the world, SpaceX's per-unit costs fall as it grows in a way a new entrant simply cannot match. A competitor starting today would have to spend tens of billions just to reach the cost structure SpaceX already enjoys—and by the time they got there, SpaceX would be a generation ahead. Scale economies of this kind are among the most durable powers in the entire framework, because they compound.

The third is Cornered Resource, which here takes an unusual, double form. There is the human cornered resource—the concentration of elite "hardcore" engineering talent and the irreplaceable Musk-Shotwell leadership pairing, one supplying vision and capital gravity, the other supplying operational execution. And there is the regulatory and orbital cornered resource: spectrum rights and the physical orbital "slots" that Starlink has claimed by being first to fill low Earth orbit at scale. There is only so much room in the most desirable orbits, and SpaceX got there first.

Now Porter's Five Forces, which test the structure of the industry itself. Barriers to entry are, almost comically, the highest of any industry on Earth—this is literally rocket science, requiring billions in capital, decades of accumulated know-how, and a tolerance for spectacular public failure that few organizations possess. This force is overwhelmingly in SpaceX's favor.

Buyer power is where the picture gets more nuanced and more interesting. For most of its life, SpaceX had essentially one buyer that mattered—NASA—and a single dominant customer is a vulnerability, because that customer can squeeze your margins. The strategic brilliance of Starlink was diversification: it transformed SpaceX from a contractor dependent on government largesse into a company with millions of individual consumer and enterprise subscribers, plus airlines, shipping fleets, and allied militaries. When your buyers number in the millions, no single one has power over you. That diversification is arguably the most important strategic de-risking in the company's history.

Threat of substitution is the force the bears press hardest, and it applies most to Starlink. The substitute for satellite internet is terrestrial fiber, which is faster and cheaper where it exists. In dense cities, fiber wins, and Starlink will never be the connection of choice in Manhattan. But Starlink's market was never the city; it is the vast geography fiber will never economically reach—oceans, mountains, war zones, the developing world's countryside. The substitution threat caps Starlink's addressable market at the edges but does not threaten its core. The genuine substitution risk lies further out: if rivals field competing constellations, satellite internet could commoditize. For now, the first-mover scale advantage holds that threat at bay.

Add it up and the framework says the moat is wide and the powers are real—particularly counter-positioning and scale, which are the two most durable. The harder question isn't whether SpaceX has advantages. It plainly does. The question is whether those advantages, however formidable, can possibly justify a price tag that assumes the company will more or less colonize new industries. That's the bull and bear case.

IX. Bull versus Bear

Let's steelman both sides, because at $2.1 trillion the gap between the optimists and the skeptics is itself one of the widest in market history.

The bull case is breathtaking in scope, and it goes like this. SpaceX is not a rocket company, a telecom, or an AI lab—it is becoming the foundational utility for the entire solar system, the company that owns the road to space and charges a toll on everything that travels it. The launch business is already a near-monopoly on Western access to orbit. Starlink is a high-margin connectivity utility with a structural cost advantage no one can match, and its addressable market—global connectivity for everyone fiber can't reach—is still in early innings. And layered on top is the orbital data center thesis: the argument that as terrestrial AI slams into the hard ceiling of the power grid, the only place left to scale compute is space, where SpaceX alone has the rockets to lift it, the solar exposure to power it, and the constellation to connect it.5 If even a fraction of that AI vision materializes, the bulls argue, $2.1 trillion will look cheap, because you are buying the infrastructure layer of two simultaneous revolutions—the expansion of humanity off Earth and the expansion of intelligence beyond the grid. It is the Standard Oil argument for the 21st century: own the indispensable resource at the base of an entire emerging economy.

The bear case is just as forceful, and it starts with arithmetic. To justify $2.1 trillion, SpaceX must deliver growth that one analyst characterized as "borderline comical"—it must not merely dominate launch and connectivity, both of which are already substantially in the price, but successfully birth entirely new industries that do not yet exist. The orbital data center, for all its conceptual elegance, has not been demonstrated at scale; powering, cooling, servicing, and upgrading a data center in orbit poses engineering problems that may prove far harder or far costlier than the pitch deck suggests. Strip out the speculative AI optionality and ask what the proven businesses—launch plus Starlink—are actually worth, and the gap between that figure and $2.1 trillion is the bear's entire thesis. The valuation, in this telling, is a bet on a future that may arrive late, arrive expensive, or not arrive at all.

The bear case also carries risks that have nothing to do with engineering. There is key-person risk of an extreme kind: a company whose value is inseparable from a single founder who controls 80% of the votes, splits his attention across multiple companies, and has shown a capacity to become, in the words of his own supporters, his own worst enemy—wading into polarizing politics in ways that can alienate customers and governments alike. There is geopolitical risk: China's 中国国家航天局 CNSA and state-backed champions are racing to field their own mega-constellations and reusable rockets, and a meaningful slice of SpaceX's business depends on government relationships that politics can sour. And there is concentration of regulatory exposure: spectrum, orbital slots, and launch licenses all sit in the hands of agencies that can move against a company that has made itself this powerful, this fast.

So what should a long-term investor actually watch? Not the share price, and not Musk's social media feed. Three KPIs cut through the noise. First, Starship launch cadence—the rate at which the next-generation vehicle reaches reliable, high-frequency, fully reusable operation, because Starship is the lever under both cheaper launch and the entire orbital data center dream; if its cadence stalls, the AI thesis stalls with it. Second, Starlink subscriber and margin trajectory—whether the connectivity utility keeps compounding subscribers while holding those remarkable margins, because that is the cash engine funding everything speculative. Third, the orbital compute milestones—any concrete, demonstrated progress on space-based AI infrastructure and Grok adoption, the proof points that would turn the bull case's biggest assumption from faith into fact. Track those three, and you will understand this company's fundamentals better than any headline about Musk's net worth.

X. Epilogue: The Ball That Rose

There is a detail from Friday that is almost too on-the-nose, the kind of thing a screenwriter would cut for being heavy-handed. In Times Square, where the famous New Year's ball descends each December as a symbol of time running out, SpaceX arranged for a ball to rise—lifting up the pole rather than dropping down it, lit in the company's colors, a small piece of theater staged for the largest IPO ever held.1 It was pure Musk: a superlative, an image engineered for the imagination, a photograph designed to make people feel that the direction of travel is up.

And that, in the end, is the throughline from the seeds-to-Mars stunt of 2001 to the trillion-dollar listing of 2026. Musk's first and most enduring insight was never about propulsion or margins. It was that the public responds to precedence and superlatives—that if you can make people believe the future is being built, the capital and the talent and the political will follow. The IPO was the ultimate proof of that thesis. Everyday investors, not just institutions, bid the stock up 19% on day one, validating a quarter-century-old bet that excitement itself could be a business model.1

Is this the Standard Oil of the 21st century—a company positioned to own the indispensable infrastructure of an entire new economy, with all the dominance and all the antitrust and geopolitical scrutiny that comparison implies? Or is it the most spectacular act of narrative financial engineering in modern history, a profitable rocket-and-internet business wrapped in a trillion dollars of unproven space-AI dreams? The honest answer, on June 15, 2026, is that both can be true at once, and the market has chosen to price the dream.

What is not in dispute is the legacy. Whatever happens to the orbital data centers and the Martian city, SpaceX has already done the thing the seeds were meant to do. It reignited interest in space. It spawned a private space economy, a real rivalry with Jeff Bezos's Blue Origin, and a generation of hard-tech founders who can now raise capital for ideas that would have been laughed out of the room twenty years ago. The AI labs queuing up behind SPCX to test the public markets later this year are, in a sense, its heirs. Musk's deepest contribution may not be any single rocket or satellite or model. It is the permission he gave a generation to chase their own superlatives—and the proof, ringing from a Nasdaq bell on a Friday in June, that sometimes the market will pay for the dream before the dream comes true.

References

-

SpaceX, Now Worth $2.1 Trillion, Pulls Off Goldilocks Debut — WSJ, 2026-06-12 ↩↩↩↩↩↩

-

SEC Form S-1 Registration Statement (SPCX) — SEC EDGAR, 2026-05-15 ↩↩

-

SpaceX Investor Relations & IPO Documentation — SpaceX, 2026-05-14 ↩↩

-

Starlink 2025 Revenue and Profitability Report — Bloomberg, 2026-01-10 ↩

-

Starship Progress and Orbital Data Center Projections — Reuters, 2026-04-20 ↩↩

-

Gwynne Shotwell: The Architect of SpaceX's Operational Success — Financial Times, 2025-11-05 ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube