SoundHound AI: The Voice Interface Pioneer's Journey from Independent Dream to AI Arms Race Survivor

Introduction and Episode Roadmap

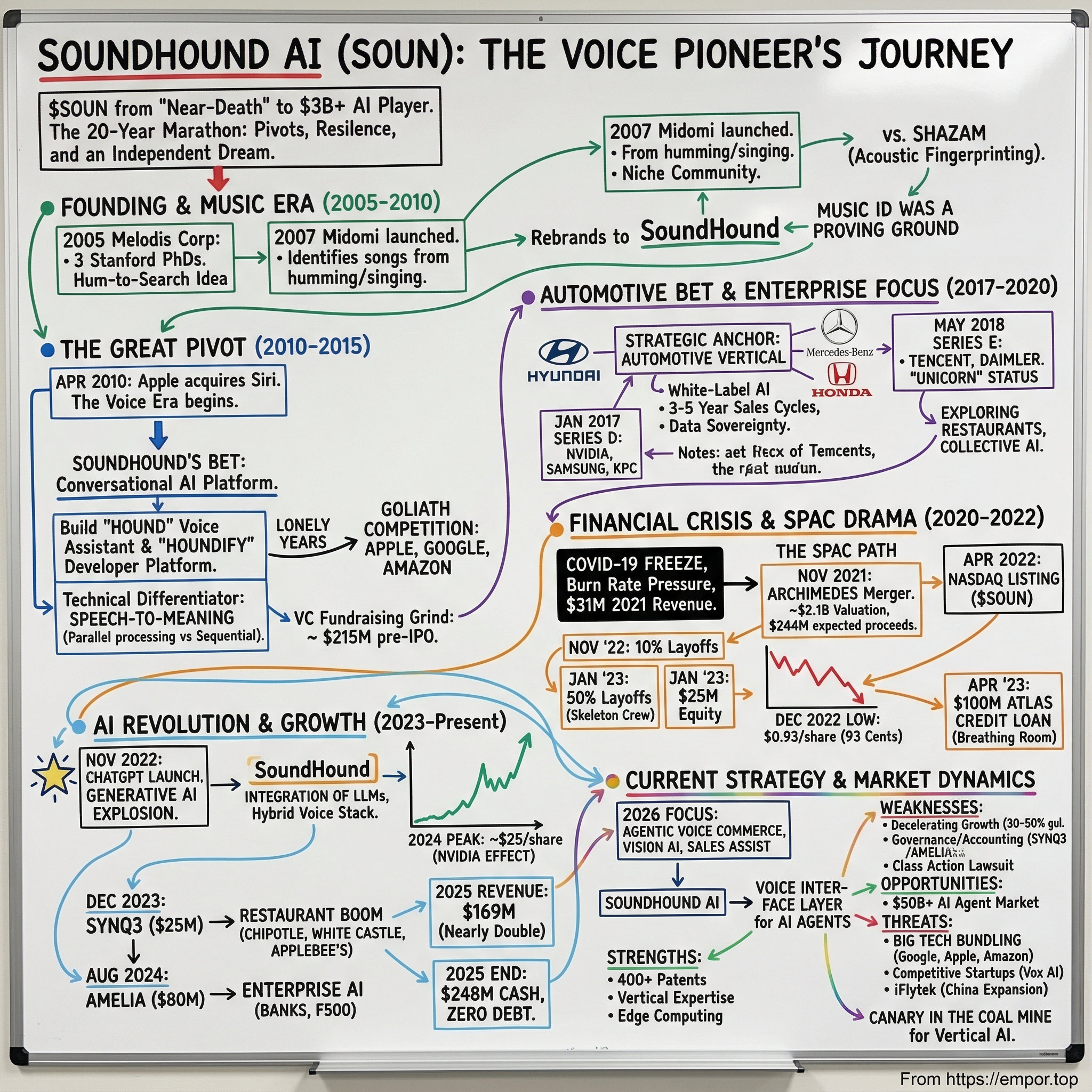

Picture this: a company worth barely two hundred million dollars in late 2022, its stock trading for ninety-three cents, half its workforce gone, and the tech industry convinced that voice AI was a solved problem owned by Apple, Google, and Amazon. Now zoom forward to early 2026. That same company, SoundHound AI, commands a market capitalization north of three billion dollars, has nearly doubled its revenue to $169 million, sits on $248 million in cash with zero debt, and counts some of the world's largest automakers and restaurant chains as customers. It holds roughly four hundred patents in voice AI technology. And it is still led by the same founder who started it all in a Stanford dorm room twenty-one years ago.

How did a music recognition app compete with Shazam, pivot to conversational AI, survive multiple near-death experiences, and emerge as a sleeper player in the generative AI revolution? That is the question at the heart of this story. SoundHound AI's journey is not a tale of overnight success or Silicon Valley glamour. It is a twenty-year marathon through technology pivots, financial crises, layoffs, SPAC dramas, and a relentless bet on a future that kept arriving later than expected.

The themes that run through this narrative will feel familiar to anyone who has studied the great technology survival stories: the peril of being too early, the art of the strategic pivot, the difference between building a product and building a platform, and the peculiar resilience required to stay independent when giants control the landscape. But SoundHound adds its own twist. This is also a story about voice, about the conviction that humans would eventually talk to machines as naturally as they talk to each other, and about a team that refused to abandon that vision even when the market stopped believing in it.

The timing of this story matters. Voice AI has entered a new phase. Large language models have transformed what conversational interfaces can do. Automotive companies are redesigning the cockpit around AI assistants. Restaurants are automating phone orders and drive-thru lanes. Enterprise call centers are deploying AI agents that handle millions of customer interactions.

The market SoundHound is chasing is enormous and growing. The conversational AI market was valued at approximately $12 billion in 2024 and is projected to exceed $40 billion by 2030, growing at roughly twenty-four percent annually. The narrower voice AI agent market is growing even faster, at a projected forty-six percent compound annual rate. These are not pie-in-the-sky projections from optimistic analysts; they reflect real enterprise spending on voice automation that is already happening.

And SoundHound, after two decades of building, pivoting, and surviving, finds itself positioned at the intersection of all these trends. Whether it can capitalize on this moment, or whether the giants will once again absorb the opportunity, remains one of the most compelling questions in the AI landscape today.

Founding Story and The Music Recognition Era (2005-2010)

Two weeks before Christmas in 2004, three Stanford electrical engineering doctoral students locked themselves in a dorm room and refused to leave until they had built something extraordinary. Keyvan Mohajer, James Hom, and Majid Emami had an idea that sounded almost absurd: take a database of twenty thousand songs and build a system that could identify any of them from a person's humming. Not from a clean recording. Not from a studio track played through a speaker. From the imperfect, off-key, rhythmically challenged humming of an ordinary person. When they finally emerged, bleary-eyed and running on caffeine, they had a working prototype. That sleepless sprint in a Stanford dorm would become the founding mythology of a company that would take twenty-one years to find its stride.

To understand why this mattered, you need to understand Keyvan Mohajer. Born in Iran, Mohajer immigrated to North America at seventeen, speaking barely any English. He was the kind of kid who started his first business before age ten, buying bread dough from a bakery and reshaping it into mini-breads to sell at a markup. It was a comically humble origin for a future AI CEO, but it revealed something essential about his character: Mohajer saw value transformation everywhere, even in bread dough. At the University of Toronto, he earned his engineering degree before moving to Stanford for his PhD, where he founded three software startups before graduating, all of which eventually became profitable. But the driving force behind everything Mohajer built was a childhood dream shaped by science fiction. He grew up watching Star Trek, mesmerized by the idea of talking to computers. "In twenty years we will talk to computers," he told anyone who would listen. "And I want to build a company around that." He later described his entrepreneurial philosophy in blunt terms: "Every attempt, you should think of it as this is the one that's going to succeed. Do not just throw darts randomly at the target."

His co-founders brought complementary strengths. James Hom, with a Stanford Computer Science background, would become Chief Product Officer and the person responsible for translating the team's technical ambitions into usable products. Majid Emami, as Chief Science Officer, led the deep R&D on speech recognition and machine learning that would form the company's technical backbone. Together, the trio represented a complete founding team: vision and business acumen in Mohajer, product thinking in Hom, and scientific depth in Emami.

In 2005, they formally incorporated their venture as Melodis Corporation. Their first product, launched in 2007, was Midomi, a music identification tool with a crucial difference from the dominant player, Shazam. While Shazam relied on acoustic fingerprinting, matching recorded audio against a database of studio tracks, Midomi used a fundamentally different approach. It employed "sound-to-sound" matching that could identify songs from humming, singing, or playing a snippet. This was a harder technical problem with a more human solution. People do not always have a recording playing. Sometimes they just have a melody stuck in their head. To put it in non-technical terms: Shazam was like a music librarian who could match any recording to its catalog. Midomi was like a music teacher who could recognize a song even when a student hummed it off-key.

The early community that formed around Midomi was passionate and niche. Users would record themselves humming songs, building a crowdsourced database that made the system smarter over time. This crowdsourcing approach was ahead of its time, creating a virtuous cycle where more user contributions made the recognition engine better, which attracted more users, which generated more data. When Apple launched the App Store in 2008, Midomi was among the early music apps, suddenly competing in what became a brutal mobile music identification war. In 2009, the team rebranded the app as SoundHound, and by 2010, the company itself changed its name from Melodis to SoundHound Inc. The growth was encouraging: two million users by January 2010, one hundred million by September 2012, and in 2014, SoundHound became the first music search product available on wearable devices.

But here is the strategic inflection that separates SoundHound's story from a simple music app narrative. Mohajer never saw music identification as the endgame. It was a proving ground, a way to demonstrate that machines could understand the messiest, most imperfect forms of human audio input. If you could build a system that recognized a badly hummed melody in a noisy room, you were already solving a harder version of the voice recognition problem. The seed of the pivot was planted from the very beginning, long before anyone outside the company realized the music app was just the opening act.

Why did SoundHound not become the next Shazam? Partly because Shazam had first-mover advantage in the simpler, more commercially scalable use case of identifying recorded music. Shazam's path to scale was clean: record the music playing around you, identify it, link to a streaming service. It was a utility that worked brilliantly within a narrow use case and eventually attracted Apple's attention, which acquired Shazam for $400 million in 2018. But more importantly, SoundHound did not become the next Shazam because the SoundHound team was already looking beyond music. They were not trying to win the music ID war. They were building the foundation for something far more ambitious: a world where machines could understand human speech as naturally and instantly as a human listener. And they were willing to spend a decade in relative obscurity to make it happen. The Midomi web version, a relic of those early days, remained available at midomi.com until February 2025, a quiet monument to the company's origins.

The Great Pivot: From Music ID to Voice AI Platform (2010-2015)

In April 2010, Apple quietly acquired a small startup called Siri Inc. for a reported two hundred million dollars. Within eighteen months, Siri launched as a built-in feature on the iPhone 4S, and the entire technology industry pivoted overnight to voice assistants. For Mohajer and his team, this was both validation and alarm. Validation because it proved that the future they had been building toward, conversational AI, was real enough for Apple to bet on it. Alarm because it meant the biggest company on Earth had just entered their intended market.

The SoundHound team read the tea leaves with unusual clarity. Siri, Google Now (which launched in 2012), and eventually Amazon Alexa (unveiled in late 2014) were not just products. They were the opening salvos of a platform war. Voice assistants would become the interface layer through which hundreds of millions of people interacted with their devices, their cars, their homes, and their services. Whoever controlled that interface would control an enormous amount of commercial value. The parallels to earlier platform wars, Windows versus Mac, iOS versus Android, were unmistakable. And in platform wars, the winners tend to capture disproportionate value.

Most companies in SoundHound's position would have doubled down on music identification, trying to compete with Shazam for app store downloads. That was the safe bet, the incremental path, the strategy that would have made sense in any VC pitch deck. Instead, Mohajer made a bet that would define the next decade: SoundHound would build a conversational AI assistant called Hound, powered by a fundamentally different technical architecture, and it would license that technology to anyone who wanted to add voice AI to their products through a platform called Houndify. It was the kind of decision that either looks visionary or delusional, depending entirely on how it turns out.

The technical differentiation was real and significant. Traditional voice assistants, including Siri and Google Now, used a two-step pipeline. First, an automatic speech recognition system converted audio into text. Then, a separate natural language understanding system parsed that text for meaning and intent. This sequential approach introduced compounding latency and compounding errors. If the speech recognition made a mistake, the natural language understanding system had no way to recover.

SoundHound's approach, which they branded Speech-to-Meaning, was radically different. Think of it like the difference between reading a foreign language by translating each word one at a time versus understanding the whole sentence in real time as it unfolds. The traditional pipeline is like the word-by-word approach: first transcribe, then understand. Speech-to-Meaning processes speech and meaning simultaneously, the same way the human brain does.

Here is a practical example of why this matters. When someone says, "Find me a restaurant near the hotel where I am staying that has Italian food and is open past ten PM and has at least four stars," a traditional two-step system would first transcribe the entire sentence into text, then pass that text to a separate system to figure out what the speaker wants. If the transcription gets one word wrong, say "hotel" becomes "motel," the entire downstream understanding can be thrown off.

Speech-to-Meaning processes the audio and meaning in parallel. As the word "restaurant" comes in, the system already knows the user is looking for a dining establishment. As "near the hotel" follows, it is already querying location data. As each additional constraint, Italian, open past ten, four stars, arrives, the system is refining the answer in real time. The result was dramatically faster response times and better accuracy, particularly for complex, multi-part queries. When Hound later demonstrated this in public, the speed advantage was not incremental. It felt like a different generation of technology.

The "lonely years," as company insiders would later describe them, stretched from roughly 2010 to 2015. While the tech press obsessed over Siri, Google Now, and Alexa, SoundHound's team was heads-down building Hound in near-total secrecy. The outside world barely knew the pivot was happening. To most observers, SoundHound was still a music recognition company, a Shazam competitor that had missed its moment. Inside the company, an entirely different reality was unfolding: a small team was attempting to build a conversational AI platform that could rival the efforts of companies with a thousand times their resources.

Fundraising during this period was a grind. The company was asking venture capitalists to believe that a music recognition startup could somehow compete with Apple and Google in conversational AI. Most VCs passed, unable to see past the David-versus-Goliath mismatch. One investor later recalled that the pitch was "technically impressive but commercially suicidal." The total pre-IPO funding across eight rounds was approximately $215 million, respectable but modest compared to the billions that Big Tech was pouring into voice. For context, Google's annual R&D spending during this period exceeded $10 billion. SoundHound was trying to outbuild Google on a fraction of a fraction of the budget.

Two decisions during this period proved critical in hindsight. First, the team chose to build a platform, Houndify, rather than just an app. This meant that even if SoundHound could never beat Siri or Alexa in consumer adoption, it could still win by powering voice AI for companies that did not want to depend on Big Tech. Second, Mohajer insisted on staying independent. Every year brought acquisition interest, and every year the founding team said no. Independence was not just pride. It was strategy. If SoundHound got absorbed by one tech giant, every other company would lose a neutral voice AI provider. Staying independent preserved optionality for the entire ecosystem.

The fundraising during this period was revealing. Between 2007 and 2015, the company raised approximately forty million dollars across its early rounds from firms like Global Catalyst Partners, Translink Capital, and Walden Venture Capital. These were modest sums by Silicon Valley standards, especially for a company attempting to build a platform to rival Siri and Google Now. But they were enough to keep the lights on and the R&D advancing. The team's frugality during these years, born of necessity rather than choice, would prove to be unexpected preparation for the much more severe financial crises that lay ahead.

By December 2015, the quiet years were over. Hound launched as a voice search app, and Houndify debuted as a developer platform for businesses. The company was about to have its moment in the spotlight.

The Hound Launch and David vs. Goliath Positioning (2015-2017)

The demo video started with a simple enough premise. Keyvan Mohajer, sitting at a desk with an Android phone, began firing complex voice queries at the Hound app. "What is the population of Japan?" Quick answer. Normal enough. Then he escalated. "How many days are there between the day after tomorrow and three days before the second Thursday of November in 2022?" The app answered correctly and instantly, with no perceptible lag between the end of his question and the beginning of the response. Then came the showstopper: "What is the population and capital for Japan and China and their area in square miles and square kilometers and also tell me how many people live in India and what is the area code for Germany, France, and Italy?" A compound query spanning multiple countries, multiple data types, and multiple units of measurement, rattled off in a single breath. Hound answered every piece of it, correctly, in under a second.

The video hit the internet in June 2015 and became a minor phenomenon. It accumulated ten thousand views within minutes of the announcement, one hundred thousand views within an hour, and 2.2 million views by the end of the day. For a B2B voice AI platform demo, these were extraordinary numbers. The reason was obvious to anyone who watched: this was not incremental improvement over Siri or Google Now. This was a qualitative leap. The speed was almost unsettling. People were accustomed to voice assistants that paused, processed, and occasionally misunderstood. Hound felt like talking to a system that was thinking ahead of you.

The technical explanation for this speed advantage was SoundHound's Speech-to-Meaning architecture. Because the system did not need to wait for a complete audio-to-text transcription before beginning to parse meaning, it could start constructing responses while the user was still speaking. The Deep Meaning Understanding layer, a companion technology, enabled the handling of those compound, multi-part queries that tripped up every competitor. Where Siri would ask you to repeat yourself or answer only the last part of a complex question, Hound could decompose a single query into its constituent parts and resolve them simultaneously.

The consumer launch of Hound, however, revealed a hard truth about the voice assistant market. Technical superiority does not automatically translate into user adoption when your competitors are pre-installed on every smartphone, smart speaker, and laptop on Earth. Apple users already had Siri. Android users had Google Assistant. Amazon Echo owners had Alexa. Asking people to download a separate app and actively choose to use it instead of the built-in option was a marketing challenge that no amount of impressive demos could solve.

Expedia signed on as an early partner, allowing Hound users to search for and book hotels by voice. Samsung integrated Houndify into some of its devices. Deutsche Telekom explored voice AI for its European customer base. But the consumer adoption numbers never reached the kind of hockey-stick growth that would have justified a consumer-first strategy. SoundHound's technology was undeniably impressive. Its distribution was undeniably limited. And in technology markets, distribution almost always trumps technical superiority. VHS beat Betamax. Windows beat Mac for decades. Google Assistant beat Hound, not because it was better, but because it came pre-installed on every Android phone on Earth.

This realization drove a strategic recalibration that, in retrospect, saved the company. If competing directly with Big Tech for consumer eyeballs was a losing game, then the winning game was something different: become the voice AI platform that powers everyone else. The Houndify platform, which launched alongside Hound in December 2015, offered a white-label solution. Automakers, device manufacturers, restaurant chains, and IoT companies could integrate SoundHound's voice AI into their own products, under their own branding, without handing their user data to Google or Apple or Amazon.

The platform play was not just a business model pivot. It was a philosophical statement about the future of voice AI. SoundHound was betting that many companies would resist depending on Big Tech for such a critical capability, especially companies like automakers that fiercely guarded their brand identity and customer relationships. Consider the psychology from an automaker's perspective: you have spent a century building a brand identity around driving experience, craftsmanship, and customer loyalty. The last thing you want is to hand the most intimate touchpoint in the vehicle, the voice your customers speak to every day, to Google or Amazon, companies that might one day sell their own cars or use driver data in ways you cannot control. SoundHound offered an alternative that let automakers keep their brand, their data, and their strategic independence. That bet would take years to fully pay off, but the early signals were encouraging. Automotive OEMs, in particular, were hungry for alternatives.

The Automotive Bet and Enterprise Focus (2017-2020)

Imagine you are the head of product at a major automaker in 2017. Your engineering team has just finished designing a beautiful new infotainment system. Your marketing team wants a voice assistant that feels premium, responsive, and distinctly yours. You have three choices. You can integrate Google Assistant, which means plastering Google's branding in your cockpit and sending all your driver data to Mountain View. You can use Apple's CarPlay, which means ceding control to Cupertino and accepting whatever interface Apple decides to offer. Or you can build something yourself, which means spending hundreds of millions of dollars and years of development time on a problem that is not your core competency.

There is a fourth option, and it is the one SoundHound was designed for: a white-label voice AI platform that lets you control the branding, the data, and the experience, while leveraging technology built by specialists. This was the pitch, and it resonated.

The automotive vertical became SoundHound's strategic anchor during this period, and for good reasons beyond just business model fit. Cars represent a captive audience in the best sense. Drivers have their eyes on the road and their hands on the wheel. Voice is not just convenient in a car; it is the safest way to interact with technology while driving. The regulatory environment was pushing automakers toward better hands-free interfaces, and consumers were beginning to expect the same voice capabilities in their cars that they had on their phones.

The partnership roster that SoundHound assembled during this period reads like an automotive industry who's who. Hyundai was the earliest major win, with a relationship that began in 2014 and deepened into a seven-year agreement covering voice AI, music recognition, voice commerce, and multi-language conversational intelligence across a broad range of global vehicle models. The Hyundai deal provided something invaluable for a young platform company: long-term, multi-year revenue visibility. Mercedes-Benz's parent company, Daimler, went further than a mere partnership. It participated in SoundHound's hundred-million-dollar Series E funding round in May 2018, putting its money where its strategic interest was. Honda partnered to integrate Houndify into electric cars and Jazz models in Europe and Japan.

These deals did not happen overnight. Enterprise sales in the automotive industry move at a pace that would test the patience of a Buddhist monk. From initial contact to production deployment, the timeline is typically three to five years. An automaker does not just bolt on a new voice assistant; it has to validate the technology against its own quality standards, integrate it with dozens of other vehicle systems, test it in multiple languages and regional accents, and certify it for safety. Consider the complexity: a single voice command to adjust the car's climate control must interface with the HVAC system, the vehicle's sensor network, the infotainment display, and potentially the cloud backend, all within a sub-second response window, while the driver is moving at highway speed with road noise and passenger chatter in the background. Multiply that by hundreds of possible commands across navigation, entertainment, communication, and vehicle controls, and you begin to understand why automotive voice AI integration is not a plug-and-play proposition. The sales cycles were long, the integration work was deep, and the cash burn was relentless.

The financial dimension of this period tells the story of a company investing aggressively in a future it could see but had not yet arrived. In January 2017, SoundHound raised $75 million in a Series D round led by some of the most strategically significant names in technology: NVIDIA, Samsung, and Kleiner Perkins. The NVIDIA participation was particularly notable in hindsight. Jensen Huang's company was already establishing itself as the infrastructure backbone of AI, and its investment in SoundHound signaled that the chip giant saw voice AI as a critical application layer for its hardware.

A year later, the Series E brought in $100 million from Tencent, Daimler, and Hyundai, among others, valuing SoundHound at one billion dollars. The investor roster told a story: a chip company (NVIDIA), an automaker (Daimler/Mercedes), a tech conglomerate with massive distribution in Asia (Tencent), a leading VC firm (Kleiner Perkins), and a Korean automotive giant (Hyundai). These were not financial investors looking for a quick flip. They were strategic partners with a direct interest in SoundHound's technology succeeding in their own products.

The unicorn status was a milestone, but it also set expectations. The company was now valued like a high-growth enterprise, but its revenues were still in the low tens of millions. The gap between valuation and revenue created pressure that would intensify dramatically over the next few years.

Beyond automotive, SoundHound was exploring other verticals where voice AI could add immediate value. The restaurant industry emerged as a surprisingly strong fit. Phone orders are a major revenue stream for many restaurant chains, and every call that goes unanswered or handled poorly is lost revenue. SoundHound began building voice AI solutions for restaurant ordering, a use case that would later become one of its most important growth drivers.

The broader strategic vision crystallized into what the company called "Collective AI." The idea was elegant and worth understanding in detail, because it remains central to SoundHound's competitive thesis today. Traditional voice AI systems are siloed: a restaurant ordering system knows about menus but nothing about navigation, while a car assistant knows about directions but nothing about food. Collective AI connects these domains so that knowledge flows between them. A user in a car can ask, "Find an Italian restaurant near my hotel that is open past ten PM with at least four stars and has outdoor seating," and the system draws simultaneously on restaurant domain knowledge, navigation, reviews, and scheduling to construct a coherent answer. Each new domain added to the collective improves performance for all connected domains. It is, in essence, a bet on breadth creating depth, a network of specialized intelligences that collectively outperform any individual system. The concept was genuinely innovative. The cash required to build it was compounding too, and by 2020, the distance between vision and financial reality would become dangerously wide.

The Near-Death Experience and Financial Crisis (2020-2022)

The darkest chapter in SoundHound's history does not begin with a dramatic event. It begins with a slow tightening, like a boa constrictor. COVID-19 arrived in early 2020 and scrambled every assumption the company had about its trajectory. Enterprise deals that were months from closing suddenly froze as corporate budgets went into survival mode. Automotive OEMs, facing their own existential challenges with supply chain disruptions and factory shutdowns, pushed back timelines on everything that was not immediately essential. Restaurant chains were fighting for their survival, not investing in voice AI for phone ordering.

At the same time, the broader venture capital environment was shifting. The low-interest-rate era that had fueled a decade of generous startup funding was ending. The Federal Reserve's pivot to rate hikes sent shockwaves through growth-stage technology companies. SoundHound, which had been burning cash at a significant rate to fund R&D, long-cycle enterprise sales, and a growing workforce, found itself in an increasingly precarious position. The company's 2021 revenue was approximately $31 million against a cost structure built for much higher growth. The math was unforgiving: at that burn rate, without new capital, the company would run out of money.

The irony of the situation was thick. Voice AI was clearly the future. Every day brought more evidence: Amazon was shipping millions of Echo devices, Google was embedding Assistant into everything, Apple was redesigning Siri. And yet the company that had been working on voice AI longer than any of them was running out of money to continue. The market had validated the vision but not the company.

The company pursued a SPAC merger as its path to public markets. To understand why, you need to understand the SPAC moment. In 2021, 613 SPACs went public, an all-time record. SPACs offered pre-revenue technology companies something that traditional IPOs could not: the ability to make forward-looking revenue projections in investor materials, which SEC rules prohibited in standard IPO prospectuses. For a company like SoundHound, whose value was almost entirely in future potential rather than current earnings, the SPAC route was not just convenient. It was one of the only feasible paths to public markets and the capital infusion the company desperately needed.

On November 16, 2021, SoundHound announced a definitive merger agreement with Archimedes Tech SPAC Partners. The deal valued SoundHound at approximately $2.1 billion in pro-forma enterprise value and was expected to provide up to $244 million in gross proceeds, composed of $133 million from the SPAC's cash in trust and $111 million from a fully committed PIPE at ten dollars per share. The PIPE investor list was impressive: Oracle, Koch Industries, VIZIO, HTC, Foxconn's FIH Mobile, and others.

The timing was simultaneously perfect and catastrophic. Perfect because the SPAC window was still open and SoundHound managed to secure the deal before the market turned. Catastrophic because by the time the merger actually closed on April 28, 2022, with shares beginning to trade on the Nasdaq under the ticker SOUN, the world had changed. The SPAC market was imploding. Of the roughly three hundred SPACs that completed mergers through 2022, eighty-five percent would end up trading below their ten-dollar IPO price. The average post-merger SPAC share price by year-end was $3.85, representing a sixty-percent decline from the redemption price. SoundHound was about to become part of that grim statistical reality.

Through the summer and fall of 2022, SOUN shares declined steadily as the broader tech selloff intensified and investors fled speculative growth stories. On December 22, 2022, the stock hit its all-time low: ninety-three cents per share. A company that had been valued at $2.1 billion less than a year earlier was now worth roughly two to three hundred million dollars. The unicorn valuation from the Series E round was a distant memory.

The human toll was severe.

In November 2022, SoundHound laid off ten percent of its workforce, citing challenging market conditions. The cuts were positioned as "right-sizing," the corporate euphemism that everyone in Silicon Valley recognizes as a signal of deeper trouble to come.

The deeper trouble came two months later. In January 2023, the company laid off nearly half of its remaining staff, reducing headcount from approximately 450 to around 200. In just three months, the company had gone from a full-sized organization to a skeleton crew. The severance was, by multiple accounts, minimal: two weeks, no healthcare continuation, and the payments were conditional on the company securing new funding. Think about that for a moment: employees who had spent years building voice AI technology at below-market compensation, sustained by equity that was now nearly worthless, were shown the door with severance that might not even be paid if the company failed to raise money.

January 2023 brought the emergency fundraise that kept the lights on. SoundHound raised $25 million in equity, enough to pay the conditional severance and maintain operations. In April 2023, the company secured a more substantial lifeline: a $100 million loan facility from Atlas Credit Partners, replacing existing debt with more favorable terms extending maturity to 2027. The Atlas deal provided breathing room, but it was survival financing, not growth capital.

What kept SoundHound alive during this period was a combination of stubborn conviction and accumulated strategic assets. The automotive contracts were still in place. Hyundai's seven-year deal continued. The technology still worked, and arguably worked better than ever as the team refined its models with years of production data. The patents still held, providing at least theoretical protection against copying. And Keyvan Mohajer, who had spent eighteen years building this company, who had turned down acquisition offers during the good times, was not about to let it die during the bad times.

Consider what this period felt like from the inside. You are the CEO of a company whose stock trades for less than a dollar. You have just laid off half your colleagues, people who trusted you and worked alongside you for years. Your severance offer was so thin that former employees openly criticized it. Your remaining team is demoralized, overworked, and watching the stock ticker with a mixture of hope and dread. Your competitors, Apple, Google, Amazon, have essentially unlimited resources and are investing billions in the exact technology category you pioneered. And you wake up every morning and decide, again, to keep going. The founder's resolve during this period was tested in ways that most technology CEOs never experience. The belief that voice AI's time would come was not just a corporate talking point. It was the operating thesis that held the company together when every financial indicator suggested otherwise. For investors, this period is the strongest evidence of both the company's greatest strength and greatest risk: everything depends on the conviction and judgment of one founder.

The Lifeline and Strategic Reset (2022-2023)

When a company survives a near-death experience, the scars change its DNA. SoundHound emerged from 2022 and early 2023 as a fundamentally different organization. Smaller, leaner, and stripped of any illusions about the forgiving nature of technology markets. The approximately two hundred people who remained were, almost by definition, the true believers, the ones who had stayed through stock price collapse and mass layoffs because they believed in the technology and the mission.

The strategic reset that followed was ruthless in its focus. Gone was any pretense of competing broadly across consumer voice AI. Gone were the ambitious plans to become a general-purpose voice platform for everything from smart home devices to wearables to IoT. The company concentrated its resources on the verticals where it had demonstrated traction and where the economics made sense: automotive and restaurants, with enterprise customer service as a growing third pillar.

This was not just a resource allocation decision. It was a philosophical transformation. The pre-crisis SoundHound wanted to change the world. The post-crisis SoundHound wanted to survive and then grow by being the best voice AI provider in specific, high-value niches. Every dollar of R&D spending, every sales call, every partnership negotiation was evaluated through the lens of these core verticals. If it did not serve automotive, restaurants, or enterprise customer service, it did not get funded.

Two things happened in late 2023 and 2024 that transformed SoundHound's trajectory. The first was the AI hype cycle triggered by ChatGPT's launch in November 2022 and the subsequent explosion of interest in generative AI throughout 2023. Suddenly, every company on Earth wanted an AI strategy. Voice AI, which had felt like a niche concern during the SPAC bust, was suddenly relevant again. Investors who had written off the category began looking at it with fresh eyes. The connection between large language models and conversational voice interfaces was obvious, and SoundHound was one of the few pure-play public companies positioned to benefit.

The second catalyst was more specific and illustrates how, in the stock market, narrative can matter as much as fundamentals. In Q4 2023, NVIDIA disclosed that it had invested approximately $3.7 million for a 0.6 percent stake in SoundHound, one of five AI investments NVIDIA made that quarter. Three point seven million dollars. For a company with NVIDIA's market capitalization, this was the financial equivalent of pocket change. But the signal was enormous. Jensen Huang's company was the most important player in the AI infrastructure stack, and it had chosen SoundHound as one of its bets. The NVIDIA imprimatur sent the stock soaring and brought institutional investor attention that had been absent since the SPAC days. From its ninety-three-cent low in December 2022, SOUN shares climbed steadily through 2023 and 2024, reaching an all-time high of $24.98 on December 26, 2024, a twenty-six-fold increase from the bottom. It was one of the most dramatic stock recoveries in the AI sector, though it would subsequently pull back significantly as enthusiasm moderated and governance concerns emerged in early 2025.

In December 2023, SoundHound made its first acquisition: SYNQ3, a leading provider of voice AI solutions for the restaurant industry, for approximately $25 million in a mix of cash and stock. The deal was strategic rather than financial. SYNQ3 brought relationships with over twenty-five national and multinational restaurant chains and more than ten thousand signed locations. Overnight, SoundHound became the preeminent voice AI provider for restaurants in the United States.

The Amelia acquisition in August 2024 was a bigger, bolder move. SoundHound paid approximately $80 million in cash and equity for Amelia, formerly known as IPsoft, one of the world's largest privately held conversational AI companies. Amelia had been recognized in Gartner's Magic Quadrant as a market leader in enterprise conversational AI and served customers including some of the top fifteen global banks and Fortune 500 organizations. The deal added over $45 million in recurring AI software revenue and opened entirely new verticals: financial services, insurance, healthcare, and large enterprise customer service.

The Amelia deal exemplified SoundHound's post-crisis strategy: use acquisitions to buy established customer relationships and recurring revenue in adjacent verticals, then integrate them into the SoundHound platform. Rather than building from scratch in each new market, the company was assembling a portfolio of vertical capabilities through targeted M&A. The logic was sound in theory: organic growth in enterprise AI is slow because each new vertical requires years of domain expertise, regulatory knowledge, and customer trust. Acquisition lets you buy time, which for a company that has already spent twenty years building, is a precious commodity.

But there is a tension in this strategy that investors should recognize. Each acquisition adds complexity: different codebases that need to be integrated, different customer expectations that need to be managed, different cultures that need to be merged. For a company with only about two hundred employees at the time of its first acquisition, absorbing three companies in rapid succession was a high-wire act. The subsequent disclosure of accounting weaknesses related to these acquisitions suggests that the integration challenged the company's back-office infrastructure. Growth through acquisition is a powerful tool, but only if the acquiring company has the operational maturity to execute it cleanly.

Leadership continuity was a quiet but essential part of the story. Mohajer remained as CEO through the entire journey, now stretching beyond two decades, an increasingly rare feat in technology. Consider the comparison: by 2024, the average tenure of a public company CEO was about seven years. Mohajer had been at the helm for nearly three times that. Founder-led companies have a peculiar advantage during crises: the person making the survival decisions is the same person who made the original founding bet. There is no principal-agent problem. The founder's reputation, identity, and life's work are on the line. That alignment of incentives explains why Mohajer held the company together when a hired CEO might have accepted an acqui-hire or wound things down. But it also raises a question that investors should consider: at what point does founder conviction become founder stubbornness? The line between visionary persistence and irrational attachment is thin, and only outcomes reveal which side you were on.

The AI Revolution Era and Current Strategy (2023-Present)

The launch of ChatGPT in late 2022 changed the competitive landscape for every AI company on the planet, and SoundHound was no exception. Suddenly, the question was not whether machines could have natural conversations with humans. That was settled. The question was what role specialized voice AI companies would play in a world dominated by large language models that could generate fluent text on any topic.

SoundHound's answer was nuanced and, so far, effective. The company did not try to build its own general-purpose large language model to compete with OpenAI or Google. Instead, it integrated LLMs into its existing stack, using them to enhance the generative capabilities of its voice assistants while preserving the speed and accuracy advantages of its proprietary Speech-to-Meaning architecture. The result was a hybrid system: SoundHound's own engine handled the core voice recognition and intent understanding at machine-speed, while LLMs provided the open-ended conversational depth that earlier systems lacked.

The differentiation in the LLM era crystallized around four advantages.

First, speed. Speech-to-Meaning's single-step processing is inherently faster than feeding audio through a speech-to-text system and then into an LLM. In a drive-thru lane, the difference between a half-second response and a two-second response is the difference between a customer who feels they are having a natural conversation and a customer who hangs up.

Second, accuracy in noisy environments. SoundHound's Polaris ASR engine, launched in 2024, was specifically designed for the acoustically challenging conditions of real-world deployment: drive-thru lanes with car engines idling, restaurant kitchens with clanging pots, vehicle cabins at highway speed. Polaris achieved a forty-percent improvement in accuracy over its predecessors, and brands that switched from Big Tech generic voice AI reported a threefold error reduction.

Third, edge computing capability. SoundHound can run its entire voice AI stack on-device without cloud connectivity, a critical feature for automotive applications where cellular coverage is unreliable. When you are driving through a rural area or a tunnel, a cloud-dependent voice assistant goes silent. SoundHound's edge deployment keeps working.

Fourth, domain expertise. Twenty years of building voice AI for specific industries had produced specialized knowledge that generic LLMs simply did not have. Knowing that "a number three with no onions and add bacon" is a specific menu item modification at a specific restaurant chain, and being able to price it correctly and send it to the kitchen, is domain knowledge that a general-purpose AI does not possess out of the box.

The restaurant vertical became SoundHound's breakout use case, and it is worth dwelling on why this particular market proved so receptive. The typical quick-service restaurant in America faces a perpetual staffing crisis. Employee turnover in the restaurant industry routinely exceeds one hundred percent annually. Training a new employee to handle phone orders costs time and money that gets wasted when that employee leaves three months later. Meanwhile, every unanswered phone call is a lost order, and research suggests that up to thirty percent of incoming calls to restaurants go unanswered during peak hours. The math is simple: an AI system that answers every call on the first ring, never takes a break, never calls in sick, and consistently upsells appropriate items generates more revenue per phone line than the most diligent human employee.

Smart Ordering, the company's AI-driven restaurant order management system, powered over ten thousand locations across the United States by 2025, processing more than a hundred million customer interactions and handling hundreds of millions of dollars in food orders. The customer list read like a tour of American dining: Chipotle, Jersey Mike's, Applebee's, IHOP, White Castle, Five Guys, Casey's General Stores, Red Lobster, and many others. The system handled orders across phone, SMS, in-app voice, and in-vehicle infotainment systems through a single integration, meaning a restaurant chain could activate AI order management across its entire off-premise ecosystem without building separate solutions for each channel. For restaurant operators facing chronic labor shortages and rising wages, the value proposition was concrete and measurable. By early 2025, SoundHound had expanded to over fourteen thousand restaurant locations.

In automotive, the design wins continued to accumulate. Stellantis deployed SoundHound's Chat AI in select Jeep vehicles across Europe, featuring generative AI-powered conversational experiences. Lucid Motors launched the Lucid Assistant, a hands-free voice assistant powered by SoundHound's technology running on NVIDIA's AI Enterprise platform. The technical partnership with NVIDIA deepened at GTC in March 2025, integrating NVIDIA's NIM and NeMo microservices for low-latency AI processing and real-time retrieval-augmented generation. A seven-year agreement with Hyundai continued to expand across global vehicle models. New partnerships with Tencent Intelligent Mobility opened doors to Chinese automotive brands deploying voice AI globally.

The financial trajectory told a compelling turnaround story. Revenue grew from $31 million in 2022 to $46 million in 2023 to $85 million in 2024 to $169 million in 2025. To put that in context: the company nearly doubled revenue in both 2024 and 2025, a growth rate that put it among the fastest-growing public AI companies during that period. The full-year 2025 GAAP net loss narrowed to $14 million, a ninety-six percent improvement from 2024, suggesting that operating leverage was finally emerging after years of losses. Cash on hand at year-end 2025 was $248 million with zero debt, meaning the company had eliminated the existential financial risk that nearly destroyed it in 2022.

The customer backlog stood at $1.2 billion as of late 2024, up seventy-five percent year-over-year, with average contract terms of approximately seven years. That backlog number is important because it provides forward revenue visibility that most software companies at SoundHound's scale do not have. Seven-year contracts in automotive mean that once a vehicle model launches with SoundHound's technology, the revenue continues for the life of that model's production run. Management issued 2026 revenue guidance of $225 million to $260 million, implying continued strong growth, though the consensus expectation of roughly thirty to fifty percent growth represents meaningful deceleration from the near-doubling of 2024 and 2025.

In September 2025, SoundHound completed its third major acquisition, purchasing Interactions LLC for approximately $60 million in cash. Interactions was a different kind of target than SYNQ3 or Amelia. Founded as a pioneer in AI-powered customer service, it served Fortune 100 companies across retail, insurance, automotive, and technology. More importantly, it was immediately accretive to operating profitability, a signal that management was becoming more disciplined about acquisition economics after the accounting challenges of earlier deals. The acquisition brought the total patent portfolio to nearly four hundred and expanded the combined customer base across virtually every major enterprise vertical. By late 2025, SoundHound had a combined workforce of approximately 430 employees and a product line spanning automotive voice AI, restaurant ordering, enterprise customer service, and financial services conversational AI.

At CES in January 2026, SoundHound unveiled its most ambitious product yet: Agentic Voice Commerce, a platform that enables AI agents in vehicles and smart TVs to order food, make restaurant reservations through OpenTable, pay for parking, and book tickets, all through natural voice conversation. Think about the implications: you are driving home from work, and your car's voice assistant proactively asks if you want to reorder last Tuesday's takeout from your favorite restaurant, processes the payment, and has it ready for pickup by the time you arrive. That is the vision SoundHound is building toward, and it represents a shift from reactive voice assistants that wait for commands to proactive AI agents that anticipate needs.

The company also debuted Vision AI at CES, combining camera-enabled visual perception with voice recognition and agent orchestration, allowing in-car assistants to listen, see, and interpret the surrounding world. A driver could point at a restaurant while passing by and ask, "What are the reviews for that place?" and the system would identify the restaurant visually, pull up reviews, and offer to make a reservation. At MWC in February 2026, SoundHound launched Sales Assist Agent, bringing real-time agentic AI to retail sales floors, enabling store associates to access product information, inventory data, and customer history through voice interaction.

These product launches represent a strategic bet on voice as the command layer for agentic AI. Rather than competing to build the agents themselves, SoundHound is positioning its platform as the voice interface through which humans interact with any agent, regardless of who built it. It is, in essence, a play to become the voice operating system for the AI agent era.

It is worth noting, however, that not all developments during this period were positive, and intellectual honesty requires addressing them directly.

NVIDIA subsequently sold its entire stake in SoundHound, though the technical partnership continues. The sale removed a signal of confidence that had been important to the stock's narrative. More significantly, a securities class action lawsuit was filed in March 2025, alleging material weaknesses in SoundHound's internal controls that impaired its ability to properly account for the SYNQ3 and Amelia acquisitions. The company disclosed on March 4, 2025, that it would be unable to timely file its 2024 annual report due to what it described as "unresolved accounting complexities." The stock dropped nearly six percent on the news.

The specific allegations are concerning. The lawsuit claims SoundHound inflated goodwill values from the acquisitions, delayed SEC filings, and obscured integration costs. Financial corrections disclosed in March 2025 included decreases in contingent earnout consideration, accounts payable, and accrued liabilities, along with increases in deferred revenue and deferred tax liabilities. These are the kinds of adjustments that suggest the initial accounting for the acquisitions was not as clean as investors were led to believe.

Combined with CEO insider selling totaling over twelve million dollars in December 2024, while the stock was trading near all-time highs, these governance issues represent real risks that investors should weigh carefully. Insider selling under Rule 10b5-1 plans is common and does not necessarily indicate pessimism, but the timing and magnitude invite scrutiny.

Competitive Landscape and Market Dynamics

SoundHound operates in one of the most contested spaces in technology: the intersection of voice AI, conversational interfaces, and enterprise automation. The competitive landscape is best understood as a multi-front war where the combatants have radically different resources, strategies, and motivations.

The Big Tech incumbents, Google, Apple, Amazon, and Microsoft, represent the most obvious competitive threat. Google's Android Automotive OS is on track to become the predominant automotive operating system, expected to feature in nearly ninety percent of mid-to-high-level vehicle models shipped in 2026. But here is the critical nuance: less than six percent of vehicles shipped with Android Automotive OS will feature Google Automotive Services, the bundle that includes Google Assistant. Automakers are adopting Google's OS while resisting Google's services, precisely because they do not want to cede control of the driver experience and data to a tech giant. That gap between OS adoption and services adoption is the strategic window SoundHound is targeting.

Apple's approach with CarPlay Ultra, launched in May 2025, is a projection model, meaning it mirrors the phone experience onto the car's display rather than running natively on the vehicle's computing platform. This limits deep vehicle integration compared to embedded solutions. Amazon's Alexa+, unveiled in February 2025 with BMW as the flagship automotive partner, represents a serious escalation with over seventy large language models powering its capabilities. Each of these players has advantages that SoundHound cannot match: billions in R&D budgets, pre-installed distribution on hundreds of millions of devices, and consumer brand recognition.

But each also has a strategic vulnerability that SoundHound exploits. When automakers integrate Google Assistant, they send their driver data to Google, a company that owns Waymo and has autonomous vehicle ambitions. When they use Apple CarPlay, they accept Apple's design constraints and cede the dashboard experience to Cupertino. When they choose Amazon Alexa, they empower a company that could theoretically use driving data for insurance, retail targeting, or other purposes automakers cannot control.

This is not abstract competitive theory. It is a real concern discussed in boardrooms at every major automaker. Data sovereignty, the ability to control where driver data goes and how it is used, has become a first-order strategic priority. European automakers, in particular, face strict GDPR requirements that make data sharing with U.S. tech companies legally complex. SoundHound's white-label approach lets OEMs keep their data, their branding, and their independence. For an automaker spending years and billions designing a vehicle experience, the appeal of a neutral, customizable voice AI provider is significant. The question is how long this advantage persists as Big Tech adapts its offerings to address data sovereignty concerns.

Among specialized competitors, Cerence is the most direct comparison. Spun off from Nuance Communications in 2019, Cerence is the legacy leader in automotive voice AI with technology embedded in over 525 million cars. But Cerence's story recently has been one of decline. Its fiscal year 2025 revenue fell to $252 million, a twenty-four percent decline, as OEMs shifted away from its older embedded voice solutions. The stock collapsed to an all-time low of $2.34 in August 2024. Under CEO Brian Krzanich, the former Intel chief, Cerence is attempting a pivot to generative AI with its xUI platform, but it is doing so from a position of shrinking revenue and market share. Nuance itself was acquired by Microsoft for $19.7 billion in 2022 and subsequently focused almost entirely on healthcare, effectively exiting the broader voice AI competitive landscape.

In the restaurant vertical, competition is intensifying rapidly. Google Cloud powers Wendy's "Fresh AI" system, deploying to over five hundred restaurants in 2025 with results showing AI-driven drive-thru service twenty-two seconds faster than average. A wave of startups, Vox AI, Loman AI, ConverseNow, Certus AI, and others, has emerged since 2023, enabled by advances in LLMs that lowered the barriers to building voice ordering systems. SoundHound's advantage in restaurants is scale and incumbency: over ten thousand locations and relationships with major national chains. But that advantage is not permanent.

The Chinese market presents a different dynamic. iFlytek, with roughly $3.4 billion in revenue and over sixty percent market share in China's education and healthcare AI sectors, is approximately twenty times SoundHound's size. However, iFlytek operates primarily in the Chinese domestic market and is on the U.S. Entity List, limiting its international expansion. The competitive threat is indirect but worth monitoring, particularly as Chinese automakers like BYD, NIO, and Xpeng expand globally and potentially bring domestic AI suppliers with them. If Chinese EVs gain significant market share in Europe, Asia, and Latin America, they may carry iFlytek or similar Chinese voice AI systems, displacing the opportunity for SoundHound in those vehicles.

The emerging AI agent paradigm deserves particular attention because it may be the most consequential competitive dynamic of the next five years. Gartner predicts that forty percent of enterprise applications will include task-specific AI agents by 2026, up from less than five percent in 2025. The AI agent market itself is projected to grow from approximately $8 billion to over $50 billion by 2030. In this world, voice is not just a feature. It is the primary interface through which humans interact with networks of specialized AI agents that handle everything from customer service to supply chain management to retail sales. The company that provides the voice layer for agentic AI systems captures a strategic chokepoint in the enterprise AI stack.

SoundHound's Agentic Voice Commerce platform, unveiled at CES 2026, is its bid for this position. The question is whether SoundHound's specialized voice stack will be the preferred integration point for agent orchestration, or whether the companies building the agents themselves, OpenAI, Google, Anthropic, will also build the voice interfaces, making specialized providers redundant. The answer likely varies by use case. In high-noise, mission-critical environments like drive-thrus and car cabins, specialized voice AI may retain its edge. In quieter, lower-stakes environments like desktop customer service, general-purpose models may suffice.

Perhaps the most important competitive question is philosophical: as large language models continue to improve, what remains defensible for a specialized voice AI company? SoundHound's answer is that voice AI in real-world production environments is not just about language generation. It is about handling noisy audio in a drive-thru lane, understanding a customer's accent while a car engine idles, integrating with a restaurant's specific menu and POS system, running on-device without cloud connectivity in a moving vehicle, and doing all of this with sub-second latency, every time, at scale. General-purpose models are getting better at conversation, but the specialized engineering required to deploy voice AI reliably in mission-critical production settings is a different problem entirely. Whether that differentiation holds over time is the central question for SoundHound's long-term competitive position.

Strategic Frameworks Analysis

Porter's Five Forces

Threat of New Entrants: High.

The software-centric nature of voice AI means capital requirements are relatively modest, and the democratization of AI through large language models has dramatically lowered technical barriers. Since 2023, a wave of restaurant voice AI startups like Vox AI and Loman AI has demonstrated how quickly new competitors can emerge. Vox AI raised $8.7 million in seed funding in August 2025 specifically for autonomous drive-thru ordering, directly targeting SoundHound's core restaurant use case.

However, two friction points slow newcomers: deep enterprise integration requirements, particularly in automotive where three-to-five-year qualification cycles create natural barriers, and the domain-specific training data accumulated over years of production deployments. A startup can build a voice ordering demo in weeks; getting it certified for installation in millions of vehicles takes years.

Bargaining Power of Suppliers: Medium-High.

SoundHound depends on cloud infrastructure providers and, increasingly, on foundation model providers for the generative AI components of its stack. NVIDIA's hardware and software platform powers critical edge computing capabilities. The mitigation is SoundHound's proprietary Speech-to-Meaning technology, which reduces pure LLM dependence for core voice recognition and understanding. As LLMs become more commoditized with multiple competitive providers, this supplier power should moderate over time.

Bargaining Power of Buyers: High.

Automotive OEMs have enormous leverage. They buy in bulk, negotiate multi-year contracts, and can credibly threaten to build in-house or switch to Big Tech alternatives. Restaurant chains face lower switching costs than automakers, though once SoundHound's AI is integrated with a chain's POS system, menu database, and operations, the friction of switching increases meaningfully.

One particularly concerning datapoint: analysts have flagged that over thirty percent of SoundHound's revenue may come from a single customer, creating significant concentration risk. If that customer renegotiates, delays, or defects, the impact on SoundHound's revenue trajectory would be material.

Threat of Substitutes: Very High.

This is the force that keeps SoundHound's leadership awake at night. Big Tech can bundle voice AI for free as part of broader platform deals. Google can offer Android Automotive with Google Assistant at no incremental cost to OEMs. Amazon can subsidize Alexa to gain in-vehicle data. Apple can improve Siri within the closed Apple ecosystem.

In-house development is another substitute, with major automakers and restaurant chains occasionally investing in proprietary solutions. McDonald's, for example, ended its drive-thru AI partnership with IBM and is now seeking a new partner, potentially including an in-house option. The traditional substitute in customer service, human agents, still handles the majority of interactions and remains the benchmark against which AI must prove its value.

Industry Rivalry: Very High.

The voice AI market combines deep-pocketed incumbents with unlimited resources, a growing number of specialists, pricing pressure as capabilities converge, and a race to demonstrate AI agent capabilities across every vertical. SoundHound is simultaneously competing with trillion-dollar companies in automotive, venture-backed startups in restaurants, and enterprise software giants in customer service. Differentiation is increasingly difficult to maintain as the underlying AI technology converges.

Hamilton Helmer's Seven Powers

Hamilton Helmer's framework asks a more fundamental question than Porter: not just what competitive forces exist, but whether a company has durable strategic power that creates persistent differential returns. For SoundHound, the assessment is mixed.

Scale Economies: Weak to Moderate. Voice AI benefits from data scale, as more interactions improve model accuracy, but the improvement curve flattens, and competitors can achieve similar accuracy with different data sources. Infrastructure costs scale reasonably well, and R&D costs amortize across a growing customer base. But this is not a business where scale creates the kind of crushing unit cost advantages seen in semiconductors or cloud infrastructure.

Network Effects: Moderate. SoundHound's Collective AI architecture creates a form of network effect where more domains produce a better overall experience. A system that understands both restaurant menus and car navigation performs better at food-related queries in vehicles. But these are indirect network effects that competitors can replicate with sufficient data. There are no strong direct network effects (users do not benefit from other users being on the platform in the way that social networks or marketplaces create).

Counter-Positioning: Moderate and Eroding. SoundHound's independence was historically a powerful counter-position. OEMs did not want to depend on Big Tech, and SoundHound offered a neutral alternative.

But as Google has modularized its automotive offerings and Amazon has embraced white-labeling, the counter-positioning advantage has narrowed. Big Tech has adapted to the concern rather than ignoring it. When the incumbent adjusts its strategy to address the insurgent's counter-position, the power diminishes.

Switching Costs: Moderate to High. This is SoundHound's strongest structural advantage. Once voice AI is integrated into a car's infotainment system or a restaurant chain's ordering infrastructure, the cost of ripping it out and replacing it is substantial.

Integration with vehicle systems, POS terminals, menu databases, and CRM systems creates operational lock-in. Training data and customization specific to each deployment add another layer. The seven-year average contract term in SoundHound's backlog reflects this stickiness.

But switching costs only apply to deployed customers. For prospects evaluating options before deployment, switching costs are zero. The race is to sign and deploy as many customers as possible before competitors offer viable alternatives.

Branding: Weak. SoundHound is a B2B company operating behind white-label deployments. The consumer SoundHound music app has some brand recognition, but it does not drive enterprise purchasing decisions.

In B2B contexts, technical reputation matters more than brand, and technical reputation is fragile, particularly given the recent governance issues and delayed SEC filings.

Cornered Resource: Moderate. Twenty-one years of voice AI research, over four hundred patents, the Speech-to-Meaning architecture, and a massive corpus of domain-specific training data represent genuine intellectual property advantages. The founding team's deep expertise is a cornered resource of sorts. However, the accelerating capabilities of general-purpose LLMs are eroding the value of some traditional speech recognition patents. The question is whether SoundHound's specific architectural innovations retain value as the technology landscape shifts.

Process Power: Moderate. SoundHound has accumulated deep operational knowledge in automotive integration, restaurant ordering deployment, and enterprise conversational AI through years of production experience. These processes, the specific steps for qualifying a voice assistant for a new vehicle model, the procedures for integrating with a restaurant chain's menu systems, are not written in any whitepaper. They exist in the institutional knowledge of the team. But process power is inherently copyable over time; it creates a lead, not a permanent advantage.

Overall Power Assessment: SoundHound possesses moderate competitive power, concentrated in switching costs and domain expertise. The company's survival through multiple near-death experiences demonstrates remarkable organizational resilience, but the structural advantages are not overwhelming. Success depends on execution velocity: deepening vertical moats through more deployments and more domain-specific data faster than competitors can catch up. The window for establishing durable advantage is measured in years, not decades.

Compare this to a company like Verint, which was acquired by Thoma Bravo for $2 billion in August 2025 and combined with Calabrio to create a customer experience automation powerhouse. Or consider that Microsoft paid $19.7 billion for Nuance, primarily for its healthcare voice AI capabilities. These transactions suggest that the market values specialized voice AI companies with deep vertical expertise and established customer relationships. SoundHound's moderate power position is not a death sentence; it is a starting point that can deepen if the company executes well in its chosen verticals. The risk is that it fails to deepen fast enough before Big Tech or well-funded startups close the gap.

The Playbook: Strategic and Investing Lessons

SoundHound's twenty-one-year journey offers a masterclass in the peculiar challenges of building a technology company that is right about the future but too early to profit from it. Several lessons stand out for investors and entrepreneurs alike.

The curse of seeing the future too clearly. Mohajer and his team recognized in 2005 that voice would become the dominant human-machine interface. They were right. But the market they envisioned took two decades to materialize at scale, and during most of that period, the company was burning cash while waiting for the world to catch up. Being early and being wrong are financially indistinguishable for long stretches. The difference only becomes apparent in hindsight. As the venture capital adage goes: "Being early is the same as being wrong, except it costs more money." SoundHound lived this aphorism more painfully than most.

The pivot from consumer to enterprise is a survival decision, not a retreat. When Hound's consumer launch demonstrated that no standalone app could displace pre-installed voice assistants, SoundHound's pivot to B2B white-labeling was not a concession of defeat. It was an acknowledgment of distribution reality. In technology, the best product does not always win. The product with the best distribution wins. By pivoting to B2B, SoundHound traded the impossible task of acquiring hundreds of millions of individual users for the achievable task of signing dozens of enterprise customers who would deploy to millions of end users on SoundHound's behalf.

Founder resilience is not just a Silicon Valley cliché. Mohajer's refusal to sell during the good times and refusal to quit during the bad times is the single most important reason SoundHound still exists. Many companies with similar technology and market position did not survive 2022. What separated SoundHound was not its technology or its business model or its customer relationships, though all of those mattered. It was the founder's willingness to endure stock collapse, mass layoffs, emergency fundraising, and years of personal financial uncertainty for the sake of a vision he had carried since childhood. Investors should note that founder-led conviction is a double-edged sword: it creates extraordinary resilience, but it can also lead to anchoring on a vision past the point of rationality.

Vertical specialization beats horizontal ambition against giants. SoundHound tried to be everything, a consumer music app, a consumer voice assistant, a developer platform, an automotive provider, a restaurant ordering system, and an enterprise AI company. The company almost died trying to do too many things with too few resources. The survivors' version of SoundHound is dramatically more focused: automotive, restaurants, and enterprise customer service. The lesson is that against competitors with essentially unlimited resources, the only viable strategy is to go deeper, not broader. A restaurant chain does not care that Google's Assistant can answer trivia questions; it cares that SoundHound's system can handle its specific menu, its specific POS integration, and its specific operational requirements better than any generic alternative.

Financial discipline is learned through near-death. The company that emerged from 2022-2023 handles capital with a seriousness that the pre-crisis company did not. The $248 million cash balance with zero debt, the immediately accretive acquisition of Interactions, and the narrowing losses all reflect a management team that has stared into the abyss of insolvency and does not want to go back. For investors, the question is whether this discipline persists as the company grows and opportunities multiply.

The independence premium is real but fragile. SoundHound's value proposition to OEMs rests heavily on being independent from Big Tech. This is a genuine competitive advantage, but it depends on remaining independent. The moment SoundHound gets acquired by a tech giant, every OEM that chose it specifically because of its independence has reason to reconsider. This creates an interesting dynamic where staying independent is itself a strategic asset, which in turn makes the company potentially more valuable as an acquisition target, which in turn makes it harder to stay independent. Investors should consider the company's independence not just as a business strategy but as a structural feature that affects its valuation.

Acquisition integration is a skill, not just a strategy. SoundHound completed three acquisitions in less than two years: SYNQ3, Amelia, and Interactions. Each brought valuable customer relationships and revenue, but integration is where most acquisition strategies fail. The securities class action lawsuit alleging accounting weaknesses related to the SYNQ3 and Amelia acquisitions is a warning sign. Building a company through acquisition requires a different organizational muscle than building one through organic growth, and SoundHound is still developing that muscle. The track record here is mixed: the acquisitions expanded revenue and customer reach meaningfully, but the governance and accounting challenges they introduced have created real investor anxiety and legal risk. For a company of SoundHound's size, absorbing three acquisitions this quickly is an ambitious undertaking, and the jury remains out on whether it was executed well enough to avoid lasting damage.

Technical differentiation has a shelf life. Speech-to-Meaning was a genuine breakthrough when it was developed. The single-step processing architecture provided measurable speed and accuracy advantages over the traditional two-step pipeline. But technology advantages decay over time as competitors innovate and the underlying science advances. The question SoundHound must keep answering, every quarter, is whether its technical edge still matters in a world where cloud-scale compute and large language models can shrink the performance gap between specialized and general-purpose approaches. The company's continued investment in Polaris ASR and edge computing suggests it understands this dynamic, but staying ahead on technology alone is a treadmill that never stops.

Bull vs. Bear Case and Investment Considerations

Myth vs. Reality

Before diving into the bull and bear cases, it is worth fact-checking several consensus narratives around SoundHound.

Myth: SoundHound is a pure AI play riding the ChatGPT hype. Reality: SoundHound has been building voice AI since 2005, predating the modern AI hype cycle by nearly two decades. Its technology stack is purpose-built for voice interaction, not adapted from a general-purpose LLM. While the company has benefited from AI enthusiasm in the stock market, its underlying technology and customer base are grounded in years of production deployment. The AI hype lifted the stock, but the business underneath is more real than many SPAC-era AI companies.

Myth: SoundHound's technology is unique and cannot be replicated. Reality: Speech-to-Meaning was genuinely innovative when developed, but the gap between specialized and general-purpose voice AI has narrowed significantly with the advent of large language models. Google's Whisper, OpenAI's voice capabilities, and Amazon's Alexa+ all demonstrate that well-resourced competitors can build fast, accurate voice systems. SoundHound's edge is increasingly about deployment expertise and domain integration rather than raw technology.

Myth: The $1.2 billion backlog guarantees future revenue. Reality: Backlogs in enterprise software, particularly automotive, are real but contingent. OEMs can delay, renegotiate, or cancel contracts if market conditions change or if they find better alternatives. A seven-year average contract term provides visibility but also locks in pricing that may not keep pace with rising costs or competitive pressure. Backlog is a leading indicator, not a guarantee.

The Bull Case

Voice AI may be reaching the adoption inflection point that SoundHound has been building toward for two decades. The convergence of generative AI capabilities, enterprise AI budgets, automotive digitization, and restaurant labor shortages creates a demand environment unlike anything the voice AI industry has previously experienced. SoundHound's automotive design wins provide predictable, long-term revenue with seven-year average contract terms and a $1.2 billion customer backlog. The AI agent wave, which analysts project will grow from approximately $8 billion to over $50 billion by 2030, makes conversational voice interfaces essential infrastructure rather than optional features.

The company's position as a non-Big Tech provider creates structural advantage. Automakers, restaurant chains, and enterprise customers face a real tension between wanting AI capabilities and wanting to avoid dependency on companies that may compete with them or exploit their data. SoundHound offers a neutral alternative with twenty-one years of specialized expertise. The financial trajectory is encouraging: revenue roughly doubled in both 2024 and 2025, losses are narrowing dramatically, and the balance sheet is clean with $248 million in cash and no debt. Management's 2026 guidance of $225 million to $260 million implies continued strong growth.

The acquisition strategy, assembling SYNQ3, Amelia, and Interactions, has rapidly scaled the company's vertical reach and customer base. If SoundHound can successfully integrate these acquisitions and cross-sell across verticals, the revenue synergies could be substantial. And at roughly $3 billion in market capitalization as of March 2026, the stock trades at a significant discount to its December 2024 peak, potentially offering an entry point for long-term investors who believe in the voice AI thesis.

The Bear Case