SoFi: Building the AWS of Fintech

I. Introduction & Episode Teaser

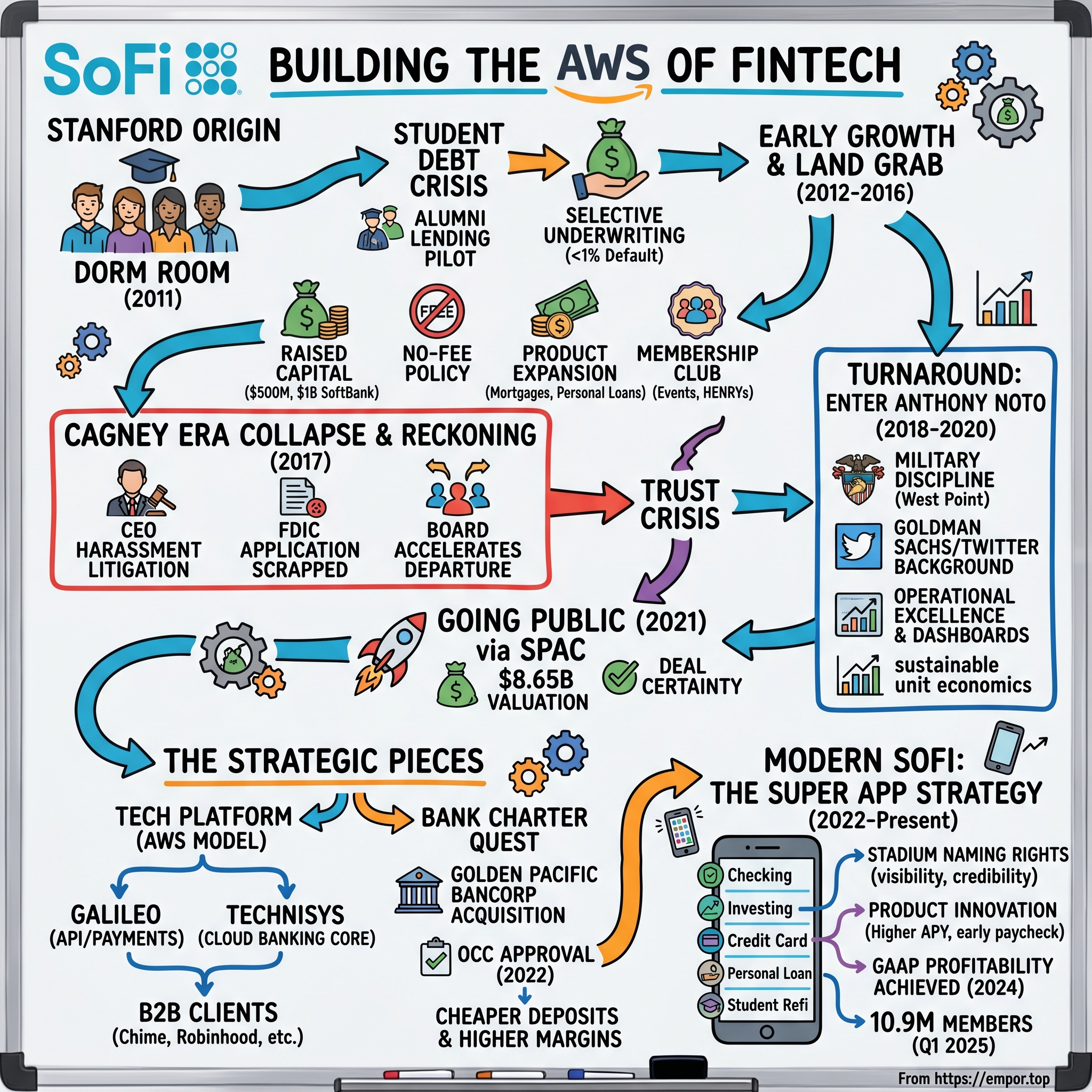

Picture this: It's fall 2011, and four Stanford Business School students are huddled in a dorm room, staring at a staggering number on their laptops—$1 trillion. That's how much Americans owed in student loans, surpassing credit card debt for the first time in history. While their classmates were pitching photo-sharing apps and social networks, Mike Cagney, Dan Macklin, James Finnigan, and Ian Brady saw something different: a financial crisis hiding in plain sight, wrapped in diploma ribbons and graduation caps.

What started as a radical experiment—convincing Stanford alumni to lend money directly to current students—would evolve into something far more ambitious. Today, SoFi stands as a $28 billion fintech powerhouse, a full-stack digital bank that processes billions in loans, powers competitors through its technology platform, and serves over 9 million members. The company that began by refinancing student loans now offers everything from mortgages to cryptocurrency trading, from checking accounts to a backend infrastructure that rivals the biggest names in financial technology.

But here's the real question that drives our story: How did a startup focused on solving one specific pain point—expensive student debt—transform into a financial super-app challenging JPMorgan Chase? And perhaps more intriguingly, how did it survive a spectacular founder meltdown, navigate a SPAC merger during peak market froth, and emerge as one of the few profitable neobanks in an era of fintech casualties?

This is a story of audacious ambition meeting harsh reality, of Silicon Valley disruption colliding with Wall Street regulation, and ultimately, of how a company built to democratize finance nearly destroyed itself before finding redemption under unlikely leadership. It's about building not just a bank, but the infrastructure layer that could power the next generation of financial services—what CEO Anthony Noto calls "the AWS of fintech."

The journey from Stanford dorm room to public company spans multiple acts: the scrappy startup years when default rates defied industry expectations, the hypergrowth era fueled by SoftBank billions, the cultural implosion that nearly killed the company, and the methodical reconstruction under a former Twitter executive who understood that in financial services, trust is the ultimate currency. Each phase offers lessons about disruption, governance, and what it really takes to challenge century-old financial institutions.

II. The Stanford Origin Story & Student Debt Crisis

The Stanford Graduate School of Business has produced its share of unicorns, but in 2011, the atmosphere was particularly electric. Facebook had just crossed 800 million users, demonstrating the power of network effects. Airbnb was revolutionizing hospitality. Yet for Mike Cagney, a serial entrepreneur who'd already sold a trading systems company, the most interesting opportunity wasn't in social media or marketplaces—it was in the growing anxiety he saw among his classmates. Cagney wasn't your typical MBA student. He'd already worked as a trader at Wells Fargo in the 1990s, founded and sold Finaplex (a wealth management software company to Broadridge), and run Cabezon Investment Group, a global macro hedge fund. This was someone who understood both the mechanics of capital markets and the inefficiencies that technology could solve.

The moment of clarity came when Cagney and his three co-founders—Dan Macklin, James Finnigan, and Ian Brady—started running the numbers on their classmates' debt loads. Stanford MBAs were graduating with an average of $100,000 in loans, paying interest rates of 6-8% regardless of their job prospects or earning potential. Meanwhile, these same graduates were landing jobs at McKinsey, Google, and Goldman Sachs with starting salaries north of $150,000. The risk profile didn't match the pricing.

"The founders hoped SoFi could provide more affordable options for those taking on debt to fund their education," but their initial approach was radically different from traditional lending. Instead of going to banks or venture capitalists for loan capital, they turned to Stanford's own alumni network. The pitch was elegant: invest in the next generation of your alma mater while earning returns better than bonds. It was peer-to-peer lending with a twist—the peers all shared the same prestigious pedigree.

The pilot program was modest but revolutionary: "40 alumni loaned about $2 million to approximately 100 students, for an average of $20,000 per student." This wasn't just about the money; it was about creating alignment. Alumni had skin in the game, students felt accountable to their community, and SoFi positioned itself as the trusted intermediary.

What happened next shocked even the founders. While federal student loan default rates hovered around 10% nationally, SoFi's borrowers achieved "extremely low default rates—less than 1%." This wasn't luck; it was selection bias weaponized as a business model. By starting with Stanford students—and later expanding to other elite schools—SoFi had discovered what venture capitalists would later call "adverse selection arbitrage." Traditional lenders treated all student borrowers similarly, but SoFi recognized that a Stanford MBA was fundamentally different credit risk than the average borrower.

The underwriting innovation went deeper than school pedigree. SoFi looked at factors traditional lenders ignored: job offer letters, career trajectory, field of study, even social connections. They built algorithms that considered earning potential, not just current income. A medical resident making $50,000 but headed for a $400,000 salary was a good bet; SoFi's models knew this while traditional FICO scores didn't.

By September 2012, institutional investors had taken notice. The company raised "$77.2 million, led by Baseline Ventures," with participation from DCM and Renren, plus angel investor Ron Suber. The message was clear: this wasn't just another peer-to-peer lending platform. This was a fundamental rethinking of credit risk in higher education.

The social element—hence "Social Finance"—was more than marketing. Early SoFi created communities around borrowing. They hosted networking events, career coaching sessions, even singles mixers (dubbed "SoFi Singles" before that became problematic). The idea was to reduce default rates through social pressure and support. If you knew your lender personally, if they helped you get a job, you were far less likely to default.

But perhaps the most audacious part of the early SoFi model was what it represented: a direct challenge to the federal student loan monopoly. While the government offered one-size-fits-all rates regardless of creditworthiness, SoFi could cherry-pick the best borrowers and offer them better deals. It was classic disruption theory—start with the overserved (high-earning graduates paying too much) and work your way down market.

The Stanford pilot had proven something profound: there was massive inefficiency in student lending, and technology combined with network effects could unlock billions in value. The only question now was how fast they could scale before traditional finance caught on.

III. Early Growth & The Fintech Land Grab (2012-2016)

If the Stanford pilot was the proof of concept, October 2013 marked SoFi's arrival as a serious force in fintech. The company announced it had raised "$500 million in debt and equity to fund and refinance student loans," including "$90 million in equity, $151 million in debt, and $200 million in bank participations." This wasn't just venture capital—it was a sophisticated capital stack that included lines of credit from Morgan Stanley and Bancorp. Wall Street was buying into the SoFi thesis.

Mike Cagney had a gift for timing. Just as millennials were hitting peak student debt anxiety, he positioned SoFi as their financial champion. The company's marketing wasn't subtle: "Don't Bank. SoFi." They weren't offering a better banking experience; they were offering an escape from banking itself. Members weren't customers; they were part of a movement. The expansion beyond student loans revealed Cagney's true ambition. In 2014, SoFi launched mortgages—a direct assault on the most profitable segment of traditional banking. By February 2015, they'd added personal loans. Each product followed the same playbook: identify where traditional banks were overcharging good customers, underwrite using better data, and wrap it all in a membership experience that felt more like joining a club than taking out a loan.

By 2015, four years after its launch, SoFi had over $6 billion in loans issued, becoming one of the largest marketplace lenders. The company's no-fee policy—maintaining "a policy of no fees for their loans, aside from the interest"—was revolutionary in an industry built on hidden charges. This wasn't charity; it was strategy. Every eliminated fee was a marketing message, every transparent interaction a contrast with Wells Fargo's fake account scandal unfolding in parallel.

Then came the SoftBank moment. September 30, 2015: SoFi announces "$1 billion in Series E funding led by SoftBank—marking the largest single financing round in the fintech space to date." Nikesh Arora, then President of SoftBank, explained the thesis: "This investment gives SoftBank exposure to the financial services sector, which is one of the largest and most important industries in the world."

The billion-dollar check changed everything. This wasn't just growth capital; it was a war chest. The Series E round brought total equity investment in SoFi to $1.42 billion. More importantly, the firm had been profitable since 2014—a rarity in the grow-at-all-costs fintech landscape.

The May 2016 milestone seemed to validate everything: SoFi became "the first startup online lender to receive a triple-A rating from Moody's." This wasn't just a rating; it was institutional validation. The rating agencies that had blessed subprime mortgage securities were now giving their highest mark to a five-year-old startup. It meant pension funds and insurance companies—the most conservative institutional investors—could now buy SoFi bonds.

The securitization innovation deserves special attention. While Lending Club was selling individual loans to investors, SoFi was packaging loans into securities that looked and traded like traditional asset-backed securities. They'd essentially created a new asset class: super-prime consumer debt. The economics were beautiful—originate at 5%, sell the securities at 3%, pocket the spread, repeat.

Behind the financial engineering was a cultural phenomenon. SoFi was building what Cagney called the "HENRY" strategy—High Earners, Not Yet Rich. These were the junior associates at Goldman Sachs, the first-year doctors, the Google engineers. They had elite credentials and high future earnings but limited current wealth. Traditional banks saw them as risky; SoFi saw them as undervalued options on human capital.

The company's member events became legendary in certain circles. Wine tastings in Napa. Cooking classes with celebrity chefs. Career coaching sessions. Speed dating events that promised you'd meet other "financially responsible" singles. It was financial services as lifestyle brand, banking as social network. Members weren't just borrowers; they were part of an aspirational community.

By September 2016, SoFi had launched SoFi at Work, an employee benefit program, and announced it had more than 600 corporate partners. As of October 2016, SoFi had funded more than $12 billion in total loan volume and had 175,000 members. The growth was hyperbolic, the ambition unlimited.

But beneath the rocket ship growth, warning signs were emerging. The culture that had driven SoFi's early success—aggressive, confident, irreverent—was morphing into something darker. The same attributes that made SoFi a formidable competitor were creating an internal environment that would soon explode into public view. The company that had disrupted banking was about to disrupt itself.

IV. The Cagney Era Collapse & Cultural Reckoning (2017)

September 11, 2017. That Monday morning, Mike Cagney sent an all-hands email that would mark the beginning of the end. "Recently... the focus has shifted more toward litigation and me personally," he wrote. "The combination of HR-related litigation and negative press have become a distraction from the company's core mission." He would resign by year's end, he announced. Four days later, after a New York Times exposé detailed SoFi's "frat house" culture, the board accelerated his departure. Cagney was out immediately.

The unraveling had actually begun weeks earlier with a lawsuit from Brandon Charles, a former employee who claimed he was fired after reporting that managers had sexually harassed their subordinates. But the Charles lawsuit was just the tip of the iceberg. Cagney's harassing conduct had been reported by more than 30 current and former employees. The allegations painted a picture of a CEO who had fostered a work environment at SoFi where sexual harassment was acceptable and employees were expected to turn a blind eye to it.

The specifics were damning. Cagney, who is married, was accused several years ago of sending sexually explicit text messages to an executive assistant, an incident that resulted in a five-figure settlement. Cagney had engaged in at least one inappropriate relationship with a female employee, with suggestions of others. The CFO was accused of discussing women's breasts and offering female employees financial incentives for losing weight. Several supervisors at SoFi's main office reportedly had sex with employees.

This wasn't just a case of a few bad actors. The culture Cagney had built—aggressive, boundary-pushing, winner-take-all—had metastasized into something toxic. The same disregard for convention that had allowed SoFi to challenge banks had created an environment where normal workplace rules didn't seem to apply. The "move fast and break things" ethos had broken the most basic professional boundaries.

The timing couldn't have been worse. SoFi had filed an application with the Federal Deposit Insurance Corporation (FDIC) to become a bank—a move that would have given it access to cheap deposits and eliminated its reliance on expensive wholesale funding. But becoming a bank meant submitting to strict regulatory oversight, including character and fitness requirements for executives. The FDIC doesn't grant bank charters to companies embroiled in sexual harassment scandals.

As the scandal deepened, SoFi scrapped its FDIC application "amid the turmoil surrounding the CEO's resignation." Years of work toward obtaining a bank charter—the holy grail for any fintech company—evaporated overnight. Institutional partners grew nervous. The company that had been preparing for an IPO was suddenly fighting for survival.

The board's response revealed how unprepared SoFi was for crisis. Initially allowing Cagney to stay through year-end showed either naivety or complicity. Only after the Times article made Cagney's position "untenable" did they act decisively. Tom Hutton, brought in as executive chairman, would serve as interim CEO with a mandate that had nothing to do with growth: "There is no more important work than paving the way for future success by building a transparent, respectful and accountable culture."

The comparisons to Uber were inevitable. Both companies had built massive valuations on cultures of aggressive disruption. Both had founders whose personal behavior undermined their companies' futures. Both learned that the traits that make for successful startup founders—relentless drive, rejection of constraints, winner-take-all mentality—can become liabilities at scale.

But SoFi's situation was uniquely precarious. Uber could survive a culture crisis because people still needed rides. Financial services, however, runs on trust. Why would anyone trust their money to a company whose executives couldn't be trusted with their employees? The member events that had built community now seemed creepy in retrospect. The "SoFi Singles" mixers took on a darker cast.

The venture capital community, which had poured $1.4 billion into SoFi, watched nervously. This wasn't just about one company; it was about the entire fintech thesis. If SoFi—the poster child for fintech disruption—collapsed, it would cast doubt on every startup claiming to challenge traditional finance. The vultures began circling, with traditional banks quietly preparing to poach SoFi's best people and acquire its loan portfolios at distressed prices.

For employees, the whiplash was severe. Many had joined SoFi to change the world of finance, attracted by Cagney's vision and charisma. Now they found themselves at a company whose name was synonymous with scandal. The recruiter calls that had been easy to ignore when SoFi was flying high suddenly seemed more interesting.

The lesson was brutal but clear: culture debt, like technical debt, compounds invisibly until it suddenly comes due. Cagney had built a rocket ship but forgotten to install proper controls. The same attributes that had made him a visionary founder—his aggression, his disregard for convention, his absolute confidence—had made him a toxic CEO. SoFi would survive, but it would need entirely new leadership to do so.

V. Enter Anthony Noto: The Turnaround Begins (2018-2020)

January 23, 2018. The announcement came via press release, not leaked to TechCrunch or whispered through Silicon Valley back channels. Anthony Noto would become SoFi's new CEO, effective March 1, 2018, leaving his role as chief operating officer of Twitter. The choice was both surprising and inevitable—surprising because Noto had no fintech experience, inevitable because SoFi needed someone with unimpeachable credentials who could restore trust.

Noto's resume read like a preparation course for crisis management. West Point graduate, where he was a star linebacker on the football team, earning All-East and Academic All-American honors. In 1991, he was the highest-ranked mechanical engineering major in his graduating class. After graduating from Army Ranger School at Fort Benning, he served as a Communications Officer with the 24th Infantry Division. This was someone who understood discipline, hierarchy, and how to rebuild broken units.

His financial credentials were equally impressive. Noto joined Goldman Sachs in 1999 and was voted the top analyst by Institutional Investor magazine for research on the Internet industry. He led the firm's communications, media and entertainment research team, became a managing director in 2003, and a partner in 2004. He returned to Goldman Sachs in October 2010 as the co-head of Goldman's global media group. In 2013, Noto helped the company win the role of lead underwriter for Twitter's initial public offering, working as the main banker dealing with Twitter.

The Twitter connection was crucial. Twitter CEO Dick Costolo announced that Noto would join Twitter as the company's CFO on July 1, 2014. The two men built a good relationship the previous year when Noto managed Twitter's account while at Goldman Sachs. At Twitter, Noto had navigated public markets, activist investors, and constant media scrutiny—perfect preparation for SoFi's challenges.

Tom Hutton, SoFi's interim CEO and board chairman, captured the board's thinking: We are simply thrilled to have found someone of Anthony's expertise and knowledge to lead SoFi. The SoFi board unanimously agrees that Anthony's deep understanding of technology, consumer, and financial businesses make him the perfect fit to be SoFi's CEO.

Noto's first moves were telling. Unlike Cagney's bombastic style, Noto operated with military precision. He didn't give splashy interviews or make grand pronouncements. Instead, he spent his first months listening—to employees traumatized by the scandal, to investors nervous about their stakes, to members wondering if their financial partner could be trusted.

The cultural transformation began immediately. Out went the "work hard, play harder" ethos. In came what Noto called "operational excellence." The party atmosphere was replaced with metrics dashboards. The freewheeling startup became a disciplined operation. Employees describe the shift as jarring but necessary—like a college fraternity suddenly subject to military inspection.

By the end of 2017, just before Noto's arrival, SoFi had reached new milestones: $25 billion in funded loans since inception and over 430,000 members. But the numbers masked deeper problems. Employee morale was shattered. The bank charter application remained dead. Institutional partners were skittish. The IPO that had seemed imminent under Cagney was now impossible.

Noto's strategic vision emerged gradually. Where Cagney had chased growth at any cost, Noto focused on sustainable unit economics. Where Cagney had prioritized headline-grabbing products, Noto emphasized infrastructure. Most importantly, where Cagney had built a lending company with tech features, Noto envisioned a technology platform that happened to offer financial services.

The shift wasn't just philosophical. Under Noto, the company has continuously expanded its offerings, but with a different approach. Each new product had to contribute to a larger ecosystem. Student loan refinancing wasn't just about that loan—it was about acquiring a member who would later need a mortgage, investment account, and checking account. The "one-stop shop" vision that Cagney had articulated was finally being executed with operational discipline.

Behind the scenes, Noto was rebuilding SoFi's technology stack. The company had grown through acquisitions and rapid product launches, creating a patchwork of systems that barely talked to each other. Noto initiated a massive re-platforming effort, building what he called a "single source of truth" for member data. This wasn't sexy work, but it was essential for the integrated financial services platform he envisioned.

The acquisition strategy also shifted. Where Cagney had bought companies for their loan books or member lists, Noto looked for technology assets. The seeds of what would become SoFi's platform strategy were being planted, though few recognized it at the time.

By 2019, Noto felt confident enough to make a bold declaration to the board: "It's a matter of when, not if, we become a top 10 financial institution." Board members were stunned. SoFi had just emerged from crisis. It still lacked a bank charter. It was a minnow compared to JPMorgan or Bank of America. But Noto saw something others didn't: the convergence of technology and finance was accelerating, and SoFi was positioned at the intersection.

The COVID-19 pandemic would test this vision almost immediately. As markets crashed and unemployment soared, SoFi faced its first real credit crisis. But Noto's operational improvements paid off. The company's underwriting models held. Member engagement increased as people sought digital financial services. Most importantly, the cultural transformation was complete—SoFi could now be trusted in crisis.

VI. The SPAC Era & Going Public (2021)

January 7, 2021. Markets were still digesting the GameStop saga when SoFi dropped its bombshell: it would go public via merger with Social Capital Hedosophia Holdings Corp V, Chamath Palihapitiya's fifth SPAC. The merger with Palihapitiya's SPAC values SoFi at $8.65 billion. For a company that had been valued at $5.7 billion in private markets, this represented a meaningful step-up—but in the frothy SPAC market of early 2021, it almost seemed conservative.

The deal structure was a masterclass in financial engineering. It includes $2.4 billion in cash, encompassing $1.2 billion from a confirmed private placement (a PIPE instrument being led by Palihapitiya himself with participation from Altimeter, Baron Capital Group, BlackRock, Coatue and others), $805 million in funding from the SPAC's balance sheet. The blue-chip PIPE investors—BlackRock, Coatue, T. Rowe Price—signaled institutional confidence that had been absent during the Cagney era.

Palihapitiya's involvement brought instant credibility and controversy in equal measure. The self-proclaimed "SPAC King" had already taken Virgin Galactic and Opendoor public through his vehicles. His pitch for SoFi was characteristically grandiose: "What I did was systematically try to future out what was broken in banking, and try to figure out which company was the best representative of the solution people wanted. SoFi was the top of the list when I looked across all the companies."

But Noto's reasoning for choosing the SPAC route was more pragmatic. "Deal certainty" was among the reasons SoFi chose to go with a SPAC instead of the traditional IPO process, he told CNBC. In the volatile markets of early 2021, with interest rates near zero but inflation concerns mounting, the ability to lock in valuation and funding was worth the SPAC stigma.

The timing seemed perfect. COVID had accelerated digital banking adoption by years. Traditional banks were still operating with legacy systems while consumers had grown comfortable managing their entire financial lives through apps. SoFi's all-digital model, once seen as limiting, now looked prescient. As the economy moves online during the coronavirus pandemic, he highlighted SoFi's strategic advantage of building a mobile-first financial company. "We create faster experiences, provide better selection, content and convenience to really capture those looking for that banking experience online," Noto told CNBC.

The investor presentation that accompanied the deal announcement revealed Noto's transformation of SoFi. Gone were the vanity metrics and aggressive growth projections of the Cagney era. Instead, Noto presented a path to profitability built on three pillars: growing the member base, increasing products per member, and building a technology platform that could serve other financial institutions. The company projected reaching 3 million members by 2025—a target that seemed aggressive but achievable.

Behind the scenes, the SPAC process had been anything but smooth. The SEC was beginning to scrutinize SPACs more closely, particularly around revenue projections and warrant accounting. SoFi had to restate its financials to comply with new SEC guidance on warrant treatment, delaying the merger completion. But these were technical issues, not fundamental problems with the business.

On June 1, 2021, SoFi Technologies Inc. jumped 12% in its Nasdaq debut. The shares, which trade under the ticker SOFI, rose to $22.65 Tuesday from $20.15 Friday, when it still traded under the SPAC ticker IPOE. That compares with an all-time high of $25.78 in February.

The market's initial enthusiasm reflected both SoFi's potential and the broader SPAC mania. Retail investors, many of whom were SoFi members themselves, piled into the stock. The r/wallstreetbets crowd embraced SOFI as their fintech play, creating a feedback loop where SoFi customers became SoFi shareholders.

But the honeymoon was brief. As the Federal Reserve began signaling rate increases and SPAC valuations collapsed across the board, SOFI stock fell hard. By late 2021, it was trading below $15, well under the $10 SPAC price. The de-SPAC curse had struck again.

Yet Noto remained focused on execution rather than stock price. The SPAC had delivered what SoFi needed: capital to fund growth, a public currency for acquisitions, and most importantly, a stepping stone to the ultimate prize—a bank charter. The public listing was never the end goal; it was a means to an end.

As of a June 2025 report, SoFi was the only SPAC in Palihapitiya's portfolio to show a positive return since its launch, up 46.6%. This distinction matters. While Clover Health collapsed and Virgin Galactic struggled, SoFi actually delivered on its promises. The difference wasn't the SPAC structure—it was the operator.

VII. The Bank Charter Quest & Galileo Acquisition

April 7, 2020. While the world was grappling with the first wave of COVID-19, Anthony Noto made a move that would define SoFi's future: acquiring Galileo Financial Technologies for $1.2 billion in stock and cash. To outsiders, the timing seemed insane. Markets were in freefall. Venture capital had frozen. But Noto saw opportunity where others saw chaos.

Galileo was founded in 2000 by Clay Wilkes and was bootstrapped to profitability over the intervening two decades. This wasn't some venture-backed unicorn burning cash for growth. Galileo had quietly become the infrastructure layer for modern fintech, providing APIs that allow fintech companies like Monzo and Chime to easily create bank accounts and issue physical and virtual credit cards. Globally, it processed an annualized $45 billion in transaction volume last month, up from $26 billion in October 2019—nearly doubling in just six months.

The strategic logic was compelling. SoFi Money was already tightly integrated with Galileo's payment platform including several of its leading account and events API functionalities. But this wasn't just about improving SoFi's own products. Noto was playing a different game entirely—building what he would later call "the AWS of fintech."

The analogy to Amazon Web Services was precise. Just as Amazon built infrastructure for its own e-commerce operations then offered it to others, SoFi would build financial infrastructure for itself while serving competitors. Galileo also works with many of SoFi's competitors, including Robinhood, Chime, Monzo, Revolut, Varo and TransferWise. Rather than viewing this as a conflict, Noto saw it as validation. If SoFi's competitors needed Galileo, the platform had real value. But the Galileo acquisition was just the opening move in a three-part chess game. In March 2022, SoFi acquired Technisys, a cloud-based banking system, for $1.1 billion. The combined technology stack will create what is expected to be the only end-to-end vertically integrated banking technology stack, from user interface development capabilities to a customizable multi-product banking core and ledger with fully integrated processing and card issuing available for SoFi products and Galileo/Technisys partners.

The Technisys deal revealed Noto's full vision. Galileo provided the payment rails. Technisys provided the core banking system. Together, they created a complete financial services technology stack that SoFi could use internally while selling to others. The combination of Galileo and Technisys should be attractive for banks and fintech companies because they potentially can get all of their core and payment-processing systems from a single vendor.

While building the technology infrastructure, Noto was simultaneously pursuing the regulatory piece: a national bank charter. The quest had begun under Cagney but was derailed by the sexual harassment scandal. Noto restarted the process, but rather than wait years for de novo approval, he found a shortcut.

In March 2021, SoFi announced it would acquire Golden Pacific Bancorp, a small California community bank with approximately $150 million in assets, for $22.3 million. This wasn't about Golden Pacific's three branches or its loan book. It was about its national bank charter issued by the Office of the Comptroller of the Currency (OCC).

The strategy was clever. Rather than apply for a new charter—a process that could take years and face political opposition—SoFi would acquire an existing one. The company would contribute $750 million in capital and pursue its national, digital business plan while maintaining GPB's community bank business and footprint.

January 18, 2022. The announcement came after markets closed: "SoFi Technologies, Inc. today announced that the Office of the Comptroller of the Currency (OCC) and the Federal Reserve have approved its applications to become a Bank Holding Company." After years of trying, SoFi had finally become a bank.

The significance cannot be overstated. "With a national bank charter, not only will we be able to lend at even more competitive interest rates and provide our members with high-yielding interest in checking and savings," Noto explained. As a bank, SoFi could fund loans with deposits rather than expensive warehouse lines. It could hold loans on its balance sheet rather than immediately selling them. It could offer FDIC-insured accounts directly rather than through partners.

Acting Comptroller Michael J. Hsu's statement was telling: "Today's decision brings SoFi, a large fintech, inside the federal bank regulatory perimeter, where it will be subject to comprehensive supervision and the full panoply of bank regulations, including the Community Reinvestment Act. This levels the playing field and will ensure that SoFi's deposit and lending activities are conducted safely and soundly."

The market reaction was immediate. Shares of SoFi's stock surged over 16% in after-hours trading following the announcement. Investors understood what the charter meant: lower funding costs, higher margins, and the ability to compete directly with traditional banks.

The B2B2C strategy was now complete. SoFi could serve consumers directly through its app while powering other financial services companies through Galileo and Technisys. It was both a competitor and a supplier—the same model that had made Amazon and Microsoft so valuable. When your competitors need your infrastructure to compete with you, you've built a real moat.

By 2022, Galileo was processing over $100 billion in annualized payment volume and serving 100 million enabled accounts. The platform powered not just fintechs but increasingly traditional financial institutions looking to modernize. The fear that competitors would abandon Galileo after the SoFi acquisition proved unfounded. If anything, the combination made Galileo more valuable—it now had the resources and regulatory framework of a bank behind it.

VIII. Modern SoFi: The Super App Strategy (2022-Present)

January 27, 2025. SoFi announces its fourth quarter 2024 results: net revenue of $734 million, net income of $332 million, and most remarkably, its first full year of GAAP profitability with $498.7 million in net income. The company that nearly collapsed seven years earlier now had 10.1 million members and was growing at 34% annually. "2024 was SoFi's best year ever," Anthony Noto declared.

The transformation from scandal-plagued lender to profitable super-app represents one of the most successful turnarounds in fintech history. But understanding modern SoFi requires looking beyond the headline numbers to the fundamental strategy shift Noto orchestrated.

The super-app vision is best understood through member behavior. The average SoFi member now has 1.57 products, up from 1.2 just three years ago. This might seem modest, but it represents billions in lifetime value. A member who starts with student loan refinancing adds a checking account, then an investment account, then a credit card. Each product deepens the relationship and increases switching costs. The marketing masterstroke that exemplifies modern SoFi's approach is the stadium naming rights. In September 2019, SoFi agreed to pay "$30 million annually" for 20 years to name the new Los Angeles stadium. The deal, totaling over $600 million, was "a record for any naming rights for a sports venue." For a company that had nearly collapsed two years earlier, it was an audacious bet.

But Noto, a former NFL CFO, understood what others missed. "We're going to be associated instantly with by far the largest aggregator of audiences in one event—the NFL," he explained. "We'll instantly have the credibility of being partners with the largest media sports brand in the U.S." The stadium would host Super Bowl LVI, the 2028 Olympics opening ceremony, and 16 NFL games annually. Each mention of "SoFi Stadium" was a brand impression money couldn't buy through traditional advertising.

The strategy worked. Member acquisition costs dropped as brand awareness soared. Young professionals watching football now associated SoFi with the glamour of LA sports, not the scandal of 2017. The stadium became a physical manifestation of SoFi's transformation—from troubled startup to established financial institution.

Product innovation accelerated under the bank charter. SoFi Money, the company's checking and savings product, reached 5.1 million accounts by Q4 2024. The key was the ability to offer up to 1.00% APY—"33 times the national average interest"—funded by the bank's deposit base rather than expensive partner banks. Members could now get their paycheck two days early, earn high interest, and invest in stocks all within the same app.

The Financial Services segment has become the growth engine. For the fourth quarter of 2024, Financial Services and Tech Platform segments made up a record 49% of SoFi's adjusted net revenue, up from 40% in the year-ago quarter. This shift is crucial—these fee-based revenues have higher margins and lower capital requirements than lending.

Cross-selling has become an art form. A member who starts with a personal loan receives targeted offers for SoFi Money. Once they have direct deposit set up, they're offered investment products. The credit card comes next, then insurance. Each product makes the next one stickier. The lifetime value of a multi-product member is 3-4x that of a single-product user.

The numbers tell the story of execution. Member growth up 34% to a record 10.9 million members in Q1 2025. Product growth up 35% to a record 15.9 million products. Fee-based revenue up 67% to a record $315 million. These aren't the metrics of a lending company; they're the metrics of a platform.

But perhaps the most remarkable achievement is cultural. The company that was once synonymous with Silicon Valley excess has become boringly profitable. Five consecutive quarters of GAAP profitability. Full-year 2024 GAAP net income of $498.7 million. This isn't growth at any cost; it's disciplined execution.

The technology platform continues to scale. Galileo and Technisys now serve over 160 million accounts globally. Major banks that once dismissed SoFi as a startup are now customers of its technology. The B2B revenue provides stability and validation—when JPMorgan uses your technology, you're no longer just a disruptor.

Modern SoFi has also embraced its role as a consumer advocate. During the student loan payment pause, while other lenders lobbied for resumption, SoFi focused on helping members understand their options. The company launched free financial planning services, career coaching, and even mental health resources. This isn't altruism—it's smart business. Financially healthy members are better customers.

The super-app strategy is working because it solves a real problem. Traditional banks force customers to use different apps for different services. Fintechs offer point solutions that don't talk to each other. SoFi provides everything in one place, with data flowing seamlessly between products. Your investment gains can automatically pay down your student loans. Your direct deposit triggers higher interest rates. Your spending patterns inform your investment recommendations.

Management expects to add at least 2.8 million new members in 2025, which represents 28% growth from 2024 levels. At this rate, SoFi will surpass 15 million members by 2026, making it larger than all but the biggest regional banks. The path to becoming a top-10 financial institution no longer seems impossible.

IX. Technology Platform & B2B Strategy

The AWS comparison deserves deeper examination. Amazon Web Services generates over $100 billion in annual revenue by providing infrastructure that powers both Amazon's competitors and partners. SoFi's technology platform follows the same playbook: build infrastructure for internal use, perfect it at scale, then sell it to others—including competitors.

Galileo processes payments. Technisys provides core banking. Together, they offer "the only end-to-end vertically integrated banking technology stack, from user interface development capabilities to a customizable multi-product banking core and ledger with fully integrated processing and card issuing." This isn't just technology; it's the entire nervous system of modern banking.

The client list reads like a who's who of fintech: Chime, Robinhood, Revolut, Monzo, Varo, TransferWise. These companies compete with SoFi for consumers, yet they depend on SoFi's infrastructure to operate. It's a beautiful paradox—the more successful SoFi's competitors become, the more money SoFi makes from them.

The economics are compelling. Galileo charges basis points on payment volume. As digital payments grow—and they're growing exponentially—Galileo's revenue grows automatically. No additional sales effort required. No customer acquisition costs. Just pure, high-margin revenue growth tied to secular trends in digital finance.

Technisys adds another layer. Traditional core banking systems from FIS, Fiserv, and Jack Henry were built in the 1970s and 80s. They're written in COBOL, run on mainframes, and require armies of consultants to modify. Technisys is cloud-native, API-first, and can be updated in real-time. For banks trying to compete in the digital age, it's the difference between a Tesla and a horse-drawn carriage.

The strategic value goes beyond revenue. Every institution using Galileo or Technisys provides data on payment patterns, user behavior, and product adoption. SoFi can see trends before they become obvious, spot opportunities before competitors, and understand the entire financial services ecosystem in real-time. It's like having a spy satellite over the entire industry.

The platform strategy also provides competitive insulation. Would-be SoFi competitors face a dilemma: build their own infrastructure (expensive and time-consuming) or use SoFi's (feeding revenue to a competitor). Most choose the latter, accepting the trade-off because the alternative is worse. This dynamic creates a virtuous cycle where SoFi's scale advantage compounds over time.

Risk diversification is another benefit. Lending is cyclical—when the economy weakens, defaults rise and origination slows. But payment processing is counter-cyclical—when times are tough, people actually make more small transactions as they manage cash carefully. The technology platform provides ballast during economic storms.

The international opportunity remains largely untapped. Galileo and Technisys already serve clients in Latin America, but expansion into Europe and Asia could multiply the addressable market. Every country needs modern financial infrastructure. Every bank needs to digitize. SoFi's technology can power this transformation globally.

The three-segment model—Lending, Financial Services, Technology Platform—creates multiple ways to win. If interest rates rise, lending margins compress but deposit gathering becomes more profitable. If fintech funding dries up, competitors struggle but SoFi's platform revenue remains stable. If regulation tightens, SoFi's bank charter becomes more valuable. There's no single point of failure.

X. Playbook: Lessons in Disruption

The SoFi story offers a masterclass in financial services disruption, but the lessons extend beyond fintech. Understanding what worked—and what didn't—provides a template for challenging entrenched industries.

Lesson 1: Start with a specific, underserved market. SoFi didn't try to replace banks initially. It focused on one problem—expensive student loans for creditworthy borrowers—and solved it better than anyone else. This narrow focus allowed rapid iteration and clear value proposition. Only after dominating student loan refinancing did SoFi expand horizontally.

Lesson 2: Regulatory arbitrage is temporary. SoFi's early advantage came from operating outside traditional banking regulations. But regulators eventually catch up. Smart disruptors use their head start to build capabilities that matter when the playing field levels. SoFi's technology platform and member relationships matter more than its initial regulatory advantages.

Lesson 3: Culture is not optional at scale. The Cagney era proved that toxic culture eventually becomes a business problem. When SoFi was 50 people, the fraternity atmosphere might have driven intensity. At 500 people, it became a liability. At 5,000, it would have been fatal. Noto's boring professionalism saved the company.

Lesson 4: Vertical integration versus partnering is a false choice. SoFi does both. It owns its core technology (Galileo/Technisys) but partners for commoditized services. It originates its own loans but also sells loans for others. The key is owning the pieces that provide competitive advantage while partnering where scale doesn't matter.

Lesson 5: Brand permission matters in financial services. Consumers will try a new social app impulsively but think carefully before trusting a company with their money. SoFi Stadium wasn't just marketing—it was buying credibility. The message: we're established enough to put our name on an NFL stadium, so we're safe enough for your savings.

Lesson 6: The bundle is powerful in consumer finance. Every additional product a member uses increases lifetime value and reduces churn. But the bundle only works if products are genuinely integrated. SoFi Money feeding SoFi Invest feeding SoFi Loans creates lock-in that's hard to replicate.

Lesson 7: Distribution is destiny. SoFi's member acquisition costs have declined even as competition intensified. Why? Because existing members become distribution. They bring their partners, recommend to friends, and consolidate accounts. The network effects aren't as strong as social media, but they exist.

Lesson 8: Capital allocation in regulated industries requires patience. SoFi spent years and hundreds of millions pursuing a bank charter. Traditional VCs would have balked. But patient capital (from SoftBank, then public markets) allowed long-term strategic moves that created lasting advantage.

Lesson 9: Technology ages rapidly; customer relationships endure. SoFi's original loan underwriting algorithms are now table stakes. But the millions of members who trust SoFi with their financial lives? That's irreplaceable. Technology enabled the relationship, but the relationship transcends the technology.

Lesson 10: Founder transitions can be opportunities. The Cagney-to-Noto transition could have killed SoFi. Instead, it allowed necessary evolution. Founders excel at creation but sometimes struggle with operation. Recognizing when to change leadership—and executing that change well—can unlock new growth.

XI. Bull vs Bear Case & Competitive Analysis

The Bull Case:

SoFi is building the first true financial super-app in America, combining the product breadth of traditional banks with the user experience of modern technology companies. The tailwinds are powerful and multiplicative.

Demographics favor SoFi overwhelmingly. Millennials and Gen Z, who comprise the bulk of SoFi's members, are entering prime earning years. They're digital-native, distrustful of traditional banks, and comfortable managing finances through apps. As this cohort accumulates wealth, SoFi is positioned to capture an outsized share.

The unit economics improve with scale. Customer acquisition costs decline as brand awareness grows. Funding costs decrease as deposit base expands. Technology platform margins expand as volume increases. This is a business where being twice as big makes you three times as profitable.

The competitive moat widens daily. Every new member makes the platform more valuable. Every technology client creates switching costs. Every product innovation raises the bar for competitors. The bank charter provides permanent advantages that venture-backed competitors can't match.

Valuation remains compelling despite recent gains. At current multiples, SoFi trades at a discount to both traditional banks (on a price-to-book basis) and fintech peers (on a revenue multiple basis). As the company proves durability, multiple expansion seems likely.

The Bear Case:

Credit risk remains untested in a true recession. SoFi's borrowers are prime, but even prime borrowers default during severe downturns. The company has never operated through a deep recession. When unemployment spikes among white-collar workers—SoFi's core demographic—losses could surprise to the upside.

Regulatory scrutiny intensifies as SoFi scales. Banking regulators tolerate innovation from small players but scrutinize systemically important institutions. As SoFi approaches top-10 status, regulatory burden will increase, potentially slowing growth and increasing costs.

Competition from both sides squeezes margins. Traditional banks are finally digitizing, offering competitive rates and improved user experiences. Meanwhile, tech giants like Apple and Google are entering financial services with massive distribution advantages. SoFi could get caught in the middle.

Technology platform risks exist. If major clients like Chime or Robinhood build their own infrastructure or switch providers, platform revenue could decline sharply. The concentration risk is real—top 10 clients likely represent majority of platform revenue.

Interest rate sensitivity cuts both ways. Rising rates help deposit margins but hurt loan demand and increase credit losses. Falling rates boost refinancing but compress net interest margins. There's no interest rate environment where everything works perfectly.

Competitive Positioning:

Against traditional banks, SoFi wins on user experience and speed but loses on product depth and branch presence. The battleground is generational change—can SoFi capture enough young customers before banks modernize?

Against neobanks like Chime or Dave, SoFi wins on product breadth and bank charter advantages but faces questions about focus. The tension: can you be everything to everyone while maintaining simplicity?

Against big tech, SoFi has regulatory advantages and financial services focus but lacks distribution power. Apple Card and Google Pay have instant access to billions of users. SoFi must build its audience organically.

Against specialized fintechs (Robinhood for investing, Rocket for mortgages), SoFi offers convenience of integration but may lack best-in-class features. The question: do consumers want one good-enough solution or multiple excellent ones?

The path to top-10 status requires flawless execution. SoFi must grow loans without taking excess risk, expand deposits without paying too much, develop technology without losing focus, and maintain culture without losing edge. It's possible but not inevitable.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube