Sun Country Airlines: From Charter Carrier to Ultra-Low-Cost Maverick

I. Introduction and Episode Roadmap

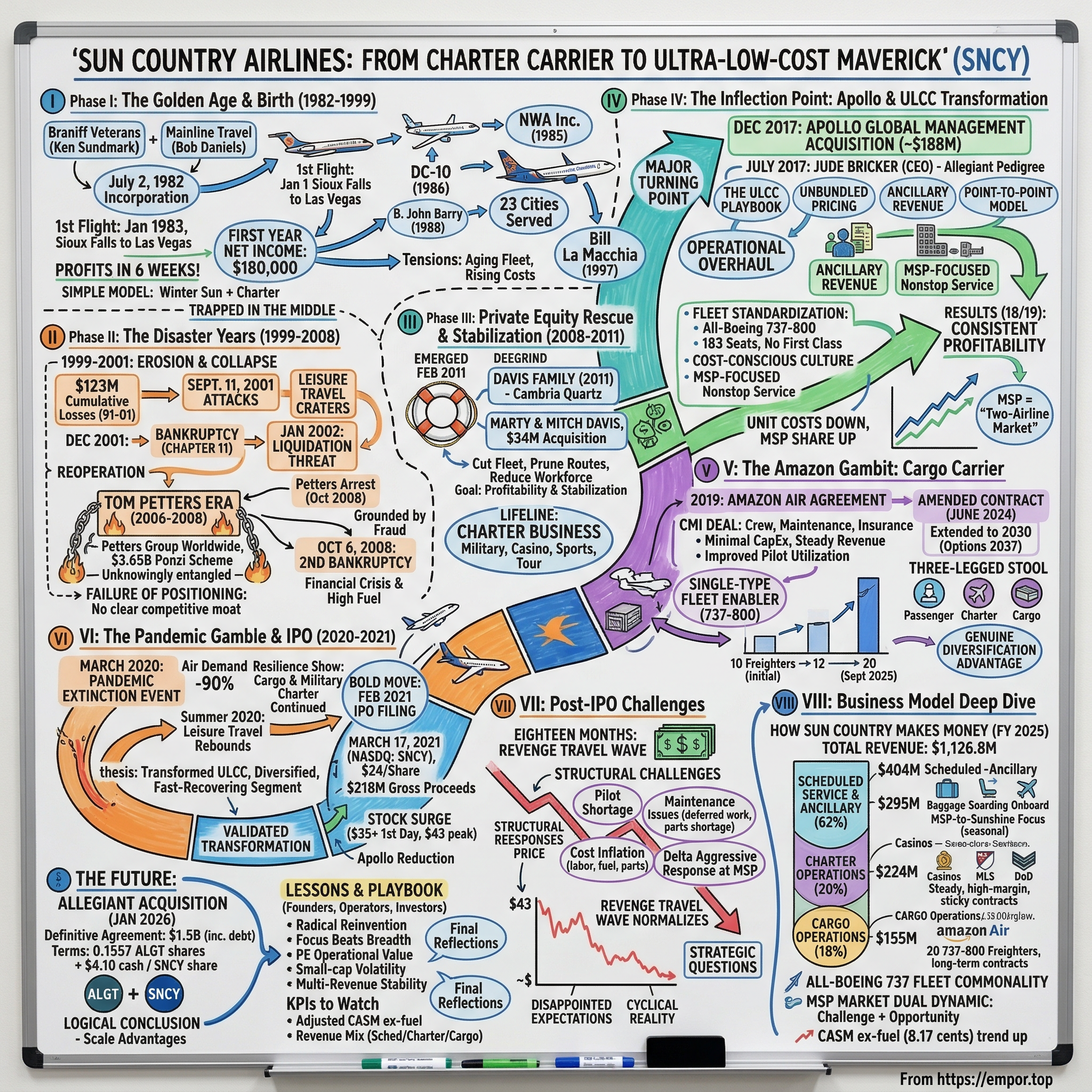

Minneapolis-Saint Paul International Airport sits at the geographic heart of the upper Midwest, a place where January wind chills routinely hit negative thirty and the only sensible escape is a direct flight to somewhere warm. For decades, that escape was controlled almost entirely by one airline: Northwest, and then its successor, Delta. But quietly, improbably, a scrappy hometown carrier has carved out a second lane at MSP, survived two bankruptcies, reinvented itself under private equity ownership, gone public during a global pandemic, and inked a deal to fly Amazon packages in the middle of the night.

Sun Country Airlines, ticker SNCY, is one of the most unusual stories in American aviation. The question at the center of this episode is deceptively simple: how does a bankrupt regional charter airline become a profitable, publicly traded, ultra-low-cost carrier with three distinct revenue streams? The answer involves a Ponzi scheme, a Marine turned airline executive, a quartz countertop fortune, and the relentless economics of a brutally competitive industry.

What makes Sun Country different from the other ULCCs, from Spirit and Frontier and even Allegiant, is its hybrid model. This is an airline that flies college basketball teams to the NCAA tournament, hauls Amazon packages across the country in converted freighters, and sells you a $49 base fare to Fort Myers where a carry-on bag costs extra. No other carrier in the United States operates across all three of those businesses simultaneously. Whether that diversification is genuine strategic advantage or simply the product of a small airline doing whatever it takes to survive is one of the central tensions of this story.

The arc of Sun Country maps onto nearly every major theme in modern aviation: deregulation, the rise and fall of leisure carriers, private equity's role in turnarounds, the ULCC revolution, the pandemic's reshaping of travel demand, and the question of whether small airlines can survive at all in an industry that relentlessly rewards scale. By the time this story reaches the present day, with Allegiant Travel announcing its acquisition of Sun Country in January 2026, the question shifts from whether Sun Country can survive independently to whether its model was always destined to be absorbed by a larger player.

II. The Golden Age of Regional Aviation and Sun Country's Birth (1982-1999)

The story begins, as so many airline stories do, with a bankruptcy. Not Sun Country's bankruptcy, but someone else's. In May 1982, Braniff International Airways collapsed, leaving thousands of pilots and crew members suddenly without work. Among them was Ken Sundmark, a Braniff captain based in the Midwest who looked at the wreckage of his former employer and saw an opportunity rather than a catastrophe.

Sundmark connected with Bob Daniels, co-founder of Mainline Travel, a Minneapolis-based tour and vacation company that had been chartering aircraft to fly Minnesotans to warm-weather destinations. Mainline had the customers and the market knowledge. Sundmark and his fellow Braniff veterans had the operational expertise. Together with Captain Jim Olsen, who would become the airline's first president, CEO, and chief pilot, they incorporated Sun Country Airlines on July 2, 1982.

The founding team was almost comically lean: sixteen pilots, sixteen flight attendants, three mechanics, and a single office worker. In an era before social media, online booking engines, or even widespread personal computers, launching an airline was an exercise in raw operational hustle and personal networks. They leased a solitary Boeing 727-200 from Air Florida and launched revenue service on January 20, 1983, with an inaugural flight from Sioux Falls, South Dakota, to Las Vegas. The ownership split reflected the partnership's nature: Mainline Travel held fifty-one percent, with the remaining forty-nine percent divided among the pilots, two flight attendants, an attorney, and a financial consultant. This was an airline built by the people who would actually fly its planes.

What happened next was remarkable. Sun Country turned profitable within six weeks of its first flight, an almost unheard-of feat in an industry where new carriers typically burn through cash for years before reaching breakeven. The airline repaid Mainline Travel's startup loan within eight months and posted net income of $180,000 in its first fiscal year, growing to nearly $1.5 million the following year. The model was simple and effective: fly Midwesterners to sunshine during the winter, operate charter flights for tour groups and sports teams, and keep overhead ruthlessly low.

The fleet expanded cautiously. A second 727 arrived in late 1983, a third by the 1986 winter season. In June 1986, Sun Country took the ambitious step of leasing a McDonnell Douglas DC-10 wide-body for longer-range routes. The airline was threading a needle at MSP, competing in Northwest Airlines' fortress hub by focusing on leisure routes that Northwest largely ignored or overpriced. This was not a carrier trying to challenge Northwest on business travel to Chicago or New York. This was the airline that would get you to Cancun or Phoenix for a reasonable fare when you needed to escape the Minnesota winter.

Ownership changed hands multiple times during the late 1980s and 1990s, each transition reflecting the fragility of small airline economics. In 1985, Mainline Travel was sold to NWA Inc., Northwest Airlines' parent company, for $22 million, but NWA ultimately declined to acquire Sun Country itself, leaving the airline independent. In 1988, B. John Barry, a Midwest banker who owned a dozen community banks across Minnesota and Wisconsin, purchased majority control. Then in 1997, Bill La Macchia, owner of Mark Travel Corporation, one of the largest tour operators in the country, bought Barry's stake. By this point Sun Country employed about a thousand people and served twenty-three cities.

La Macchia's acquisition came at a telling moment. The airline had posted $11.7 million in net losses in fiscal 1997, and the following summer he acquired the remaining shares, taking complete ownership of a company that was burning cash. The original founders had long since exited. The profitable charter-and-sunshine formula that had worked so brilliantly in the early years was being squeezed by larger carriers adding leisure routes and by the rising costs of maintaining an aging, mixed fleet. Sun Country entered the new millennium as a mid-size leisure carrier with no clear competitive moat, trapped between the scale advantages of the majors and the emerging cost discipline of a new breed of low-cost carriers. The stage was set for disaster.

III. The Disaster Years: Bankruptcy, 9/11, and Death Spirals (1999-2008)

If the 1990s were a slow erosion for Sun Country, the 2000s were a series of body blows that nearly killed the airline. Between 1991 and 2001, Sun Country accumulated over $123 million in cumulative losses, a staggering figure for a carrier of its size. The fundamental problem was structural: Sun Country was too small to achieve the cost efficiencies of the major carriers, too unfocused to compete with purpose-built low-cost airlines like Southwest, and too dependent on leisure travel that evaporated whenever the economy softened.

Then came September 11, 2001. The terrorist attacks devastated the entire airline industry, but leisure-focused carriers like Sun Country were hit with particular ferocity. Business travel eventually returned as companies resumed operations, but discretionary vacation flying, the core of Sun Country's revenue, cratered and stayed down. By December 2001, Sun Country suspended all operations and filed for Chapter 11 bankruptcy protection. Creditors, skeptical that the airline could restructure successfully, initiated involuntary Chapter 7 liquidation proceedings in January 2002, threatening to shutter the carrier permanently.

Sun Country did emerge from that first bankruptcy, resuming operations and attempting to rebuild. But the reprieve was temporary. The airline's second death spiral was even more dramatic than the first, and it involved one of the most spectacular financial frauds in Minnesota history.

Tom Petters, a Minneapolis-area businessman, had built Petters Group Worldwide into what appeared to be a legitimate conglomerate of consumer electronics and retail companies. In reality, Petters was orchestrating a $3.65 billion Ponzi scheme, fabricating purchase orders from major retailers to secure loans, then using new loans to pay off old ones. Along the way, Petters acquired Sun Country Airlines in 2006, purchasing full ownership in November 2007. For a brief period, Petters' money provided a financial lifeline, allowing the airline to invest in operations and maintain service.

The scheme's scale was staggering. Between 1998 and 2008, Petters raised over $4 billion through a constellation of fraudulent investment funds with names like Arrowhead, Lancelot, Palm Beach, and Stewardship. The fraud involved fabricating purchase orders from major retailers to secure loans, then using proceeds from new loans to repay old ones. Sun Country, as one of Petters' legitimate businesses, was unknowingly entangled in this web of deceit.

On September 24, 2008, federal agents raided Petters Group Worldwide's offices in Minnetonka, Minnesota. On October 3, Petters was arrested. Three days later, on October 6, Sun Country filed for Chapter 11 bankruptcy. The timing was almost cruelly precise: the airline had been depending on an operating loan from Petters to bridge it through to the profitable winter flying season, when Minnesotans would start booking flights to warm destinations. With Petters' assets frozen, that money vanished overnight. The airline was grounded not by its own operational failures, but by the criminal acts of its owner.

Petters was eventually convicted and sentenced to fifty years in federal prison. Sun Country, meanwhile, was left to navigate Chapter 11 with the added stigma of being a Ponzi scheme casualty. The 2008 financial crisis, which was simultaneously sending fuel prices to record highs and consumer confidence to record lows, made the situation even more dire. For the second time in seven years, Sun Country was fighting for survival, and this time the odds looked considerably worse.

What went wrong, beyond the Petters catastrophe, was a failure of positioning. Sun Country had spent two decades trapped in the middle of the airline industry, unable to match the scale and network of the majors, unable to match the cost structure of the low-cost carriers, and unable to build a brand strong enough to command premium pricing. The charter business that had been so profitable in the early years had become just one piece of a muddled strategy. The airline needed not just a financial rescue but a fundamental rethinking of what it was supposed to be.

The broader lesson from the disaster years is one that repeats throughout airline history: there is no viable middle ground between premium service and ultra-low cost. Carriers that try to be "pretty good" at everything tend to be outcompeted by rivals that are excellent at one thing. Sun Country had tried to be a reasonably priced, reasonably comfortable leisure airline, and the market punished it from both directions. Delta could match its routes with better service and frequent flyer benefits. Southwest could match its fares with better operational execution. The only way forward was to pick a lane and commit.

IV. The Private Equity Rescue: The Davis Family and Stabilization (2008-2011)

Sun Country emerged from its second bankruptcy in February 2011, battered but alive. The rescue came from an unexpected source: the Davis family of St. Peter, Minnesota, owners of Cambria, a privately held quartz countertop manufacturer that had grown into a major national brand. Marty Davis, Cambria's CEO, and his brother Mitch purchased Sun Country for approximately $34 million, a fraction of what the airline had been worth before the Petters collapse.

The Davis acquisition was driven partly by local pride, the desire to keep Minnesota's hometown airline alive, and partly by a businessman's eye for undervalued assets. At $34 million, the Davises were essentially buying the airline for the value of its gates, slots, and brand recognition at MSP, with the aircraft and operating infrastructure thrown in at a steep discount to replacement cost.

The initial years under Davis ownership were about survival, not transformation. The new leadership's diagnosis was straightforward: the cost structure was unsustainable, the route network was unfocused, and the airline had no clear competitive identity. The medicine was brutal but necessary. Fleet was cut, routes were pruned, and the workforce was reduced. The goal was not growth but profitability, not expansion but stabilization.

The charter business proved to be the lifeline during this period. Military contracts provided steady, predictable revenue, transporting service members to and from bases across the country. Casino charter flights, carrying gamblers from upper Midwest cities to destinations like Laughlin, Nevada, and Atlantic City, offered high margins and long-term relationships. Tour operator charters and sports team flights filled additional capacity. While the scheduled service side of the business struggled to find its footing, the charter operation kept cash flowing and aircraft utilization rates from falling to unsustainable levels.

By 2014 and 2015, Sun Country had stabilized. Costs were under control, cash reserves were rebuilding, and the airline was posting modest profits. But modest profits in the airline industry are not enough. The Davises had saved Sun Country from extinction, but the airline still lacked a compelling strategic vision. It remained a small, regional carrier with limited growth prospects, competing against Delta's fortress hub with a cost structure that could not support the low fares needed to attract price-sensitive leisure travelers. The airline needed a partner with deeper pockets, sharper strategic thinking, and the willingness to blow up the existing model and rebuild from scratch. That partner arrived from New York.

V. The Inflection Point: Apollo's Arrival and the ULCC Transformation (2011-2017)

This is the chapter where the story changes. Everything that came before, the founding, the bankruptcies, the Davis rescue, was prologue. The transformation of Sun Country from a generic regional carrier into a hybrid ultra-low-cost airline is the pivot that created the company investors know today.

On December 14, 2017, Apollo Global Management, one of the world's largest alternative asset managers, announced it would acquire Sun Country from the Davis family. The deal closed in April 2018 for approximately $188 million. But Apollo's influence on Sun Country had actually begun months earlier, with a single hiring decision that would prove more consequential than the acquisition itself.

In July 2017, before the Apollo deal was even announced, the Davis family hired Jude Bricker as Sun Country's new president and CEO. Bricker's background was, in retrospect, a near-perfect blueprint for what Sun Country needed. He held a civil engineering degree from Texas A&M and an MBA from the University of Texas. He had served as an infantry officer in the United States Marine Corps from 1996 to 2002, an experience that instilled a discipline and directness that would define his leadership style. After a stint in finance at American Airlines, he joined Allegiant Travel Company in 2006 and spent over a decade rising through the ranks, eventually becoming chief operating officer in January 2016.

The Allegiant pedigree was critical. Allegiant Air had pioneered a distinctive model in American aviation: flying leisure routes from small and mid-size cities to warm-weather destinations, using older aircraft purchased cheaply, maximizing ancillary revenue, and achieving some of the highest profit margins in the industry. Bricker had been instrumental in building that model, overseeing marketing, network planning, operations, fleet strategy, pricing, and distribution. When he arrived at Sun Country, he brought the Allegiant playbook with him, but adapted it to Sun Country's unique circumstances.

The strategic pivot was radical. Bricker and Apollo did not want to improve Sun Country's existing model. They wanted to replace it entirely. The airline would become an ultra-low-cost carrier, a concept that deserves unpacking because it is widely misunderstood. ULCC does not simply mean "cheap airline." It means a fundamentally different approach to pricing air travel. In the traditional model, an airline ticket includes the seat, checked bags, carry-on bags, seat selection, snacks, and drinks, all bundled into a single price. The ULCC model strips all of that apart. The base fare covers nothing more than transportation from one airport to another in a randomly assigned seat. Everything else, a checked bag, a carry-on bag larger than a personal item, the ability to choose your seat, priority boarding, a bottle of water, each becomes a separate purchase. The result is a base fare that looks impossibly low, sometimes under $50 for a cross-country flight, but an all-in cost that can approach traditional carriers once a customer adds the services they want.

The genius of the model, and the reason it works economically, is that it allows the airline to capture revenue from customers based on their actual preferences rather than forcing everyone to pay for an identical bundle. A business traveler who needs a checked bag, a carry-on, and a specific seat pays more. A college student who can fit everything in a backpack and does not care where they sit pays less. The airline maximizes revenue per flight while keeping headline fares low enough to stimulate demand from the most price-sensitive customers. Spirit Airlines had pioneered this approach, and Frontier had adopted it. Bricker intended to execute it at Sun Country with the operational discipline he had learned at Allegiant.

The operational overhaul touched every aspect of the airline. Fleet standardization was the foundation. Sun Country's hodgepodge of aircraft types was replaced with an all-Boeing 737-800 fleet. A single aircraft type meant pilots could fly any plane in the fleet without requalification, maintenance crews needed to stock parts for only one airframe, and training costs dropped dramatically. The 737-800s were reconfigured to 183 seats by eliminating first class entirely and reducing seat pitch to ULCC-standard levels. Every additional seat on every flight was additional revenue potential with minimal additional cost.

The route strategy shifted to a point-to-point model centered on MSP. Rather than trying to build a hub-and-spoke connecting network, which required the scale and complexity that had overwhelmed Sun Country in the past, Bricker focused on nonstop service from Minneapolis to leisure destinations: Florida, the Southwest, Mexico, the Caribbean. These were routes where demand was strong, where Delta's pricing left room for a low-cost alternative, and where Sun Country could achieve high load factors during the peak winter travel season.

But here is where Sun Country diverged from the pure ULCC playbook: Bricker did not abandon the charter and cargo businesses. In fact, he doubled down on them. This was the hybrid model's genesis, the insight that an airline could operate ULCC-style scheduled service while simultaneously running a charter operation for sports teams, military contracts, casinos, and tour groups, and eventually a cargo operation for Amazon. The fleet standardization was the key enabler. Because every aircraft was a 737-800, the same planes could fly scheduled passengers during peak demand periods, operate charters on weekends or during special events, and even be converted to freighter configuration for cargo operations. Aircraft that would otherwise sit idle during off-peak periods could generate revenue in entirely different business lines.

The culture change was as significant as the strategic shift. Sun Country's workforce had grown up in a legacy airline environment, with legacy airline expectations about service levels, operating procedures, and cost tolerance. Bricker had to instill a cost-consciousness that permeated every decision, from how many napkins were stocked on each flight to how quickly aircraft were turned at the gate. This was not about being cheap in a way that degraded the customer experience. It was about eliminating costs that did not directly contribute to getting passengers safely and reliably from point A to point B.

Consider what this meant in practice. A traditional carrier might turn an aircraft at the gate in forty-five minutes, allowing time for a thorough cleaning, catering restocking, and crew changeover. A ULCC targets thirty minutes or less, because every additional minute an aircraft spends on the ground is a minute it is not generating revenue in the air. The math is unforgiving: an airline that achieves twelve hours of daily aircraft utilization versus ten hours extracts twenty percent more productivity from its most expensive asset. When you multiply that across a fleet of dozens of aircraft over an entire year, the efficiency gains compound dramatically. Bricker understood this math intuitively from his Allegiant years, and he drove it into every aspect of Sun Country's operations.

The results were swift and dramatic. By 2018 and 2019, Sun Country was posting consistent profitability. Margins expanded as ancillary revenue grew and unit costs declined. The airline's CASM, the industry's fundamental measure of operating efficiency, dropped toward levels competitive with the established ULCCs. The MSP market, long dominated by Delta, began to shift. Sun Country grew its share of MSP-originating traffic from roughly twelve percent to over twenty percent, establishing itself as the clear second-largest carrier at the airport. Bricker publicly articulated a vision of making MSP a "two-airline market," a direct challenge to Delta's dominance that would have been unthinkable just a few years earlier.

For investors considering what made this transformation work, the answer is the combination of three factors that are rarely found together: a disciplined operator in Bricker, a well-capitalized owner in Apollo willing to fund the transition, and a structural market opportunity in MSP where Delta's dominance had created pricing umbrellas that a ULCC could exploit. The transformation was not inevitable. It required someone who had seen the ULCC model work at Allegiant and could adapt it to Sun Country's specific circumstances, geography, and existing capabilities.

VI. The Amazon Gambit: Becoming a Cargo Carrier (2017-2020)

In a conference room somewhere in Seattle, Amazon's logistics team was looking at a map of the United States and doing math. The e-commerce giant's Prime program had promised two-day and then one-day delivery to customers across the country, and the existing air cargo infrastructure, dominated by FedEx and UPS, was both expensive and capacity-constrained. Amazon needed its own air network, and it needed it fast.

Sun Country's entry into the cargo business began around 2019 with an initial agreement to operate Boeing 737-800 freighters for Amazon Air. The arrangement was structured as a CMI deal: Crew, Maintenance, and Insurance. Amazon would own or lease the aircraft, specifically 737-800s converted from passenger to freighter configuration. Sun Country would supply the pilots, flight crews, maintenance, and insurance. The economics were elegant from Sun Country's perspective. There was minimal capital expenditure, since Amazon owned the planes, but steady, contract-based revenue that was largely insulated from the volatility of consumer airfares and fuel prices.

The strategic rationale extended beyond simple revenue diversification. The Amazon cargo flights operated primarily at night and during early morning hours, precisely the times when Sun Country's passenger aircraft were parked at gates generating zero revenue. By adding cargo operations, Bricker could dramatically improve the utilization of his pilot workforce without needing to add proportional passenger capacity. Pilots could fly cargo routes during off-peak hours and then rotate to passenger or charter duty during the day. The single-type 737 fleet was the enabler: a pilot qualified on the 737-800 could fly passengers to Fort Lauderdale in the morning, a charter to Las Vegas in the evening, and an Amazon cargo run to Cincinnati at midnight, all without requalification.

The initial deal started with ten subleased freighter aircraft, later expanded to twelve. The revenue was modest relative to the scheduled service business but highly profitable and remarkably stable. Amazon volumes grew steadily as the e-commerce giant built out its air logistics network, and Sun Country proved to be a reliable operating partner. The relationship deepened further in June 2024, when Amazon transferred eight additional 737-800 freighters, previously operated by Atlas Air, to Sun Country under an amended and restated agreement. The expanded contract extended through 2030 with options to 2037, growing the cargo fleet to twenty aircraft, all of which were operational by September 2025. The improved economics of the new contract, with significantly better rate structures that reached full effect in the second half of 2025, drove cargo revenue up 44.6 percent to $155 million for the full year.

The impact on Sun Country's business model was profound. For the first time, the airline had three distinct revenue streams: scheduled passenger service, charter operations, and cargo. Each stream had different demand drivers, different seasonal patterns, and different risk profiles. Scheduled service was driven by consumer leisure travel demand and was highly seasonal, peaking during the winter months when Minnesotans fled south. Charter was driven by long-term contracts with sports teams, the military, and casinos, providing stable but lumpy revenue. Cargo was driven by e-commerce volume, which followed its own seasonal pattern (peaking during holiday shopping season) and was largely uncorrelated with leisure travel demand.

This three-legged stool gave Sun Country a diversification advantage that no other ULCC could match. Spirit Airlines was pure scheduled service. Frontier was pure scheduled service. Even Allegiant, with its ancillary revenue from hotel and car rental bookings, was fundamentally a one-trick pony when it came to aviation operations. Sun Country's hybrid model provided genuine resilience against the demand shocks that periodically devastate the airline industry, a quality that would prove its worth within months of the Amazon deal's expansion.

VII. The Pandemic Gamble: IPO in the Storm (2020-2021)

March 2020 was an extinction event for the airline industry. In the span of roughly two weeks, air travel demand collapsed by more than ninety percent as COVID-19 shutdowns swept across the world. Airlines that had been operating hundreds of daily flights were suddenly parking fleets in desert storage facilities and furloughing thousands of employees. The industry would ultimately lose tens of billions of dollars and consume hundreds of billions in government bailouts.

Sun Country's response followed the same initial playbook as every other carrier: aggressive cost cuts, flight cancellations, and workforce reductions. But what happened next was different. The cargo business kept flying. Amazon's e-commerce volumes were not declining during the pandemic; they were exploding. Consumers trapped at home were ordering everything online, and Amazon needed its air logistics network more than ever. Sun Country's cargo freighters continued operating throughout the darkest months of the pandemic, providing a revenue stream that most airlines simply did not have.

Military charter contracts also continued, as the Department of Defense still needed to transport service members regardless of civilian travel demand. The combination of cargo and charter revenue did not make the pandemic painless for Sun Country, but it provided a cash flow cushion that prevented the kind of existential financial crisis that pushed other carriers to the brink.

When leisure travel demand began rebounding in the summer of 2020, Sun Country was well-positioned to capture it. The airline had maintained operational readiness, kept its workforce largely intact, and benefited from a structural shift in travel patterns that favored exactly its kind of flying. Business travel remained deeply depressed as companies embraced remote work, but leisure travel, particularly to warm-weather destinations accessible by car or short flight, recovered with surprising speed. Sun Country's MSP-to-sunshine route network was essentially purpose-built for this recovery.

Then came the truly bold move. In February 2021, with the pandemic still raging, vaccines just beginning to roll out, and most airline stocks still trading well below pre-COVID levels, Sun Country filed for an initial public offering. The timing seemed audacious, even reckless. Airlines were still losing money. International borders remained largely closed. The recovery, while underway, was anything but certain.

But the IPO thesis was compelling. Sun Country was not just an airline recovering from the pandemic. It was a transformed airline with a ULCC cost structure, a diversified revenue model, and exposure to the fastest-recovering segment of air travel demand. The S-1 filing told the story of the Bricker-era transformation, the three revenue streams, and the MSP market opportunity. Institutional investors, starved for growth stories in a recovering economy, responded enthusiastically.

On March 17, 2021, Sun Country began trading on the Nasdaq Global Select Market under the ticker SNCY, priced at $24 per share. The offering of approximately 9.1 million shares raised roughly $218 million in gross proceeds. On its first day of trading, the stock surged to approximately $35, a gain of nearly forty-five percent. Within a month, shares hit an all-time high of $43.08, valuing the company at well over $2 billion.

Apollo Global Management, which had paid $188 million for the entire company in 2018, was sitting on a return that justified every risk it had taken. The private equity firm remained a significant shareholder after the IPO, holding more than sixty percent of outstanding shares, but would begin systematically reducing its position through secondary offerings over the following years. The IPO proceeds were used primarily to repay amounts outstanding under the CARES Act loan, cleaning up the balance sheet and positioning the airline for growth.

The market reception validated the transformation narrative, but it also set expectations that would prove difficult to meet. At $43 per share, investors were pricing in years of profitable growth, continued margin expansion, and successful execution of everything Bricker had promised. The question was whether the post-pandemic boom in leisure travel represented a new normal or a temporary sugar high.

VIII. Post-IPO Challenges and Adjustments (2021-2023)

The eighteen months following the IPO were intoxicating. Revenge travel, the phenomenon of consumers spending freely on trips they had postponed during lockdowns, drove leisure demand to historic levels. Airlines that had slashed capacity during the pandemic found themselves selling every seat at premium prices. Sun Country rode the wave, posting strong revenue growth and healthy margins that seemed to validate the IPO thesis.

But beneath the headline numbers, structural challenges were building. The industrywide pilot shortage, caused by pandemic-era retirements and reduced training pipeline capacity, hit smaller carriers disproportionately hard. Sun Country's pilot costs began rising as the airline competed for talent with majors that could offer higher compensation and more predictable schedules. Maintenance issues, exacerbated by deferred work during the pandemic and a global shortage of aircraft parts, created operational headaches. These were not Sun Country-specific problems; they afflicted every airline in the country. But for a small carrier with limited financial cushion, each disruption had an outsized impact.

The competitive landscape at MSP also intensified. Delta, observing Sun Country's growth in its fortress hub, responded aggressively. When Sun Country launched service to leisure destinations like Asheville, Destin, Charleston, and Myrtle Beach, Delta followed with competing flights, often at fares low enough to poach Sun Country's price-sensitive customers. This dynamic, a large incumbent using its scale to discipline a smaller competitor, is one of the classic threats facing upstart airlines. Sun Country could survive it because its cost structure was genuinely lower than Delta's, but the competitive intensity capped fare levels and squeezed margins.

By 2022 and 2023, the revenge travel wave was receding. Demand did not collapse, but it normalized from pandemic-era peaks. Cost inflation, driven by rising labor expenses, elevated fuel prices, and expensive aircraft parts, eroded the margin advantage that had underpinned the ULCC model. Sun Country's CASM ex-fuel, which had been trending downward during the transformation years, began creeping upward, rising from approximately 7.49 cents in 2023 to 7.59 cents in 2024 as wage pressures took hold.

The stock price told the story of disappointed expectations. From its April 2021 high of $43.08, SNCY shares declined steadily, hitting $13.61 by September 2022. A brief recovery in late 2022 and early 2023 faded, and by mid-2025, the stock touched $8.10, a decline of more than eighty percent from the all-time high and sixty-six percent below the IPO price. Investors who had bought the growth story were getting the cyclical reality of airline economics.

Strategic questions multiplied. How fast should Sun Country grow its scheduled service network? Which new markets should it enter? Should the fleet expand, and if so, how quickly? The Amazon relationship was evolving as well. While cargo revenue remained strong, Amazon was also diversifying its own air logistics strategy, shifting aircraft between contract operators and building its own capabilities. Sun Country's position as an Amazon cargo partner was valuable but not guaranteed in perpetuity.

The post-IPO period exposed the fundamental tension in Sun Country's investment thesis. The hybrid model provided genuine resilience and diversification, but the scheduled service business, which represented the largest revenue stream, was subject to all the same competitive and cyclical forces that made airline investing so treacherous. The stock market, which had initially celebrated the transformation story, began pricing Sun Country as just another small airline in a difficult industry.

IX. The Business Model Deep Dive: How Sun Country Actually Makes Money

To understand Sun Country's economics, start with a single number: $1,126.8 million. That was total revenue for full year 2025, a record, up 4.7 percent from the prior year. But the number itself matters less than how it breaks down across the three business segments, because the mix reveals the airline's strategic direction.

Scheduled Service and Ancillary Revenue

Scheduled passenger service generated $404 million in 2025, while ancillary revenue, the fees charged for bags, seat selection, priority boarding, and onboard purchases, added another $295 million. Together, these two categories represent the ULCC model in action. The base fare gets passengers interested. The ancillary revenue generates the margin. Think of it like a software company with a freemium model: the base product is priced to drive adoption, and the premium features generate the actual profit.

Sun Country's route network is overwhelmingly focused on MSP. The airline connects Minneapolis to approximately 140 destinations, with heavy concentration on Florida (Fort Myers, Tampa, Fort Lauderdale, Orlando), the desert Southwest (Phoenix, Las Vegas), Mexico (Cancun, Puerto Vallarta), and the Caribbean. These are leisure routes with strong seasonal demand patterns. The seasonality is dramatic: Q1 is by far the strongest quarter, when Minnesotans flee the cold for warm destinations, generating operating margins above seventeen percent. Q3, the summer months when there is less urgency to escape Minnesota weather, is the weakest, with operating margins that dip to single digits. This seasonality is a defining characteristic of the business and something investors must account for when evaluating quarterly results. Sun Country competes primarily with Delta on these routes, and the competitive dynamic is straightforward. Delta offers a full-service experience at a higher fare. Sun Country offers a stripped-down experience at a significantly lower fare. The customer who cares most about price chooses Sun Country. The customer who values Delta's ecosystem, the SkyMiles program, the lounges, the first class cabin, pays the premium.

Charter Operations

Charter revenue reached $224 million in 2025, growing nearly fourteen percent year-over-year. This is the business that has been part of Sun Country's DNA since its founding, and it remains one of its most distinctive competitive advantages. The charter customer base is remarkably diverse. Caesars Entertainment signed a five-year agreement for Sun Country to fly its rewards program members to casino properties across the country. Major League Soccer designated Sun Country as its official carrier in 2022. The NCAA contracts Sun Country as a primary carrier for its basketball tournament flights. College athletic programs throughout the Midwest use Sun Country for team travel. And the United States Department of Defense contracts Sun Country for approximately half of all domestic narrow-body military charter flights, a relationship that provides steady, high-margin revenue backed by government contracts.

Charter economics are fundamentally different from scheduled service. The customer is not an individual buying a ticket; it is an organization buying the entire aircraft for a specific mission. Margins are higher because pricing is negotiated on a contract basis rather than driven by real-time competitive dynamics. Relationships tend to be long-term and sticky: once a sports team or military branch establishes an operating relationship with a charter carrier, switching costs are meaningful. The customer knows the service, trusts the reliability, and does not want to risk disruption by changing providers.

Cargo Operations

Cargo revenue hit $155 million in 2025, a 44.6 percent increase over the prior year, driven by the expanded Amazon relationship. Under the amended and restated agreement signed in June 2024, Sun Country grew its cargo fleet from twelve to twenty Boeing 737-800 freighters, with all twenty operational by September 2025. The contract extends through 2030 with options to 2037, providing long-term revenue visibility.

The cargo CMI model is capital-light from Sun Country's perspective. Amazon owns the freighter aircraft. Sun Country provides the crew, maintenance, and insurance. This means Sun Country earns steady operating fees without bearing the capital cost of the aircraft themselves. The revenue is predictable, contract-based, and largely insulated from the fare volatility that plagues scheduled service.

Fleet and Cost Structure

The all-Boeing 737 fleet, consisting of forty-seven passenger aircraft, twenty cargo freighters, and three leased to other airlines, is the operational foundation that makes the hybrid model work. Fleet homogeneity drives savings across maintenance, training, and crew scheduling. A pilot qualified on the 737-800 can fly any mission: passenger, charter, or cargo. This flexibility allows Sun Country to optimize crew utilization in ways that airlines operating multiple fleet types cannot match.

Sun Country's system CASM was 12.95 cents in 2025, higher than pure ULCCs like Frontier (approximately 8.9 cents) in part because the system figure includes cargo operations, which have different cost characteristics. The more relevant comparison is adjusted CASM ex-fuel, which stood at 8.17 cents in 2025. This is competitive but not best-in-class, and it has been trending upward due to labor cost inflation, a pressure that is affecting every airline in the industry.

The MSP Advantage

Minneapolis-Saint Paul is not JFK or LAX or ORD. It is a large but not enormous airport serving a metropolitan area of about 3.7 million people. Delta controls approximately seventy percent of passenger traffic, a dominance that creates both a challenge and an opportunity for Sun Country. The challenge is obvious: competing against an airline with vastly greater scale, a comprehensive loyalty program, and the ability to add capacity on any route Sun Country enters. The opportunity is more subtle. Delta's dominance means it prices like a dominant carrier, maintaining fare levels that provide significant margin for a ULCC competitor. In markets where Delta charges $300 for a roundtrip, Sun Country can offer the same route for $99 plus fees and still operate profitably. The MSP market generates strong origin-and-destination traffic, meaning most travelers are going to or from Minneapolis specifically, rather than connecting through the hub. This O&D traffic is exactly the kind of demand that favors a ULCC: price-sensitive leisure travelers who care about the fare, not the connecting network.

X. Leadership and Culture: The Bricker Era and Beyond

Jude Bricker's leadership of Sun Country has been defined by a relentless focus on simplicity and cost discipline. The Marine Corps background is not incidental to his management style; it is foundational. Bricker runs the airline with the directness and clarity of mission that military service instills. When he arrived at Sun Country in 2017, the airline's culture was that of a legacy regional carrier: accustomed to a certain way of doing things, resistant to the kind of radical change that the ULCC transformation demanded. Bricker changed everything, from fleet composition to seating density to the fundamental relationship between the airline and its customers.

His public communications are notably frank for a CEO, particularly in the airline industry, where corporate euphemism is an art form. Bricker has described his vision of making MSP a "two-airline market" without hedging, a direct declaration of competitive intent that most airline executives would avoid. He has been equally candid about the challenges: the difficulty of competing against Delta's scale, the reality that ULCC economics require constant cost vigilance, and the fact that growth must be disciplined rather than opportunistic.

The leadership team around Bricker has experienced significant transition in recent years. CFO Dave Davis departed in April 2025 to become CEO of Spirit Airlines, a move that speaks to the talent Sun Country has developed under Bricker's leadership. D. Torque Zubeck, formerly of Alaska Airlines, was appointed as the new CFO in September 2025. The COO position also turned over, with Stephen Coley stepping in as SVP and Head of Operations after Gregory Mays's departure.

Employee relations present ongoing challenges, and this is not a minor footnote. Labor is the largest controllable cost in the airline business, and the post-pandemic environment has shifted bargaining power decisively toward workers. Sun Country's flight attendants, represented by Teamsters Local 120, ratified a new contract in March 2025 after five years of negotiations, delivering a twenty-one percent immediate pay increase and up to fifty-eight percent over the contract's duration. This agreement set a high bar for the pilot contract negotiations that followed. Sun Country's pilots, represented by ALPA, filed a formal notice to bargain in September 2025, seeking a contract that reflects the airline's transformation and sustained profitability. The tension between ULCC cost discipline and rising labor costs is perhaps the defining challenge for the airline's economic model going forward.

The Minnesota identity is not just marketing. Sun Country's community relationships, from the University of Minnesota athletics partnership to the casino charter connections throughout the upper Midwest, create genuine customer loyalty and operational advantages that are difficult for out-of-state competitors to replicate. When the Vikings or Twins need a charter, they call Sun Country. When the military needs narrow-body charter capacity in the Midwest, Sun Country is the natural choice. These relationships, built over decades, represent a form of competitive advantage that does not show up on the balance sheet but matters enormously in practice.

XI. Competitive Analysis: Porter's Five Forces

Competitive Rivalry: High

The airline industry is one of the most intensely competitive in the American economy, and Sun Country operates in the most contested segment. At MSP, Delta's seventy-percent market share means that every Sun Country flight faces competition from an airline with vastly greater resources. When Sun Country launches a new leisure route, Delta can and does respond with matching or lower fares, using its scale advantages to make Sun Country's expansion expensive. Southwest, American, and United each hold approximately five percent of MSP traffic, adding further competitive pressure.

Beyond MSP, Sun Country competes with every ULCC in the country for leisure travelers. Before its bankruptcy filings, Spirit Airlines was a direct competitor on price-sensitive routes. Frontier continues to expand aggressively. And Allegiant, which has announced its intention to acquire Sun Country, operates a strikingly similar model. The industry's fundamental challenge is that seats on competing airlines are largely interchangeable from the consumer's perspective, making price the primary competitive variable in the leisure segment.

Threat of New Entrants: Medium

Starting an airline requires substantial capital, regulatory approval, fleet acquisition, and the establishment of maintenance and operational infrastructure. These barriers keep casual entrants out. But the real threat comes not from new airlines launching but from existing carriers adding capacity in Sun Country's markets. Delta can add a daily flight from MSP to Fort Myers with minimal incremental effort, effectively functioning as a new entrant in that specific market.

Supplier Power: High

Boeing effectively operates a duopoly with Airbus for commercial aircraft, and Sun Country's all-737 fleet means it is entirely dependent on a single manufacturer. Boeing's widely publicized production problems and delivery delays have constrained fleet growth across the industry, and Sun Country has limited leverage to accelerate deliveries or negotiate favorable terms. Jet fuel, the airline's largest variable cost, is priced on global commodity markets with no ability for individual carriers to influence pricing. And pilot labor, perhaps the most critical input, has gained substantial bargaining power due to the industrywide shortage, as evidenced by the rich contract Sun Country's flight attendants recently secured.

Buyer Power: High

Leisure travelers are perhaps the most price-sensitive consumers in transportation. They face essentially zero switching costs: comparing fares across airlines takes seconds, and loyalty to any particular carrier is minimal in the ULCC segment. Online travel agencies and metasearch engines make price comparison trivially easy, ensuring that Sun Country cannot maintain prices meaningfully above competitors without losing volume. The airline's counter-strategy is to push direct bookings through its own website and app, minimizing distribution costs and capturing customer data, but this only partially offsets the transparency of the market.

Threat of Substitutes: Medium

For routes under four hundred miles, driving is a real substitute, particularly when ULCC add-on fees push the all-in cost of flying close to the cost of gas and tolls. But for Sun Country's core routes, MSP to Florida and the Southwest, driving is impractical. Video conferencing is largely irrelevant, since Sun Country's customers are leisure travelers, not business travelers. The more meaningful substitute threat is competition for discretionary spending broadly: the consumer who might fly to Cancun could also spend that money on a home renovation, a new car, or simply saving.

XII. Hamilton's Seven Powers Framework Analysis

Scale Economies: Weak

Sun Country operates approximately seventy aircraft compared to Delta's fleet of over nine hundred. At this scale, the airline cannot match the procurement leverage, maintenance efficiencies, or overhead absorption of the major carriers. The airline is right-sized for the MSP market and its charter and cargo niches, but it does not benefit from the kind of scale economies that create durable cost advantages.

Network Economies: Weak

Sun Country's point-to-point model generates no network effects. Unlike Delta's hub-and-spoke system, where each additional spoke increases the value of the hub for connecting passengers, Sun Country's routes are largely independent of one another. The loyalty program is basic and does not create the kind of ecosystem lock-in that Delta's SkyMiles or United's MileagePlus programs achieve.

Counter-Positioning: Moderate to Strong

This is Sun Country's most significant structural advantage, and it deserves careful examination. The hybrid model, combining ULCC scheduled service with charter and cargo operations in a single fleet, is genuinely counter-positioned against both legacy carriers and pure ULCCs. Delta cannot match Sun Country's low fares from MSP without cannibalizing its premium revenue. Spirit and Frontier cannot replicate Sun Country's charter relationships or cargo operations because they lack the institutional capabilities and customer relationships that took decades to build. The Amazon cargo contract requires a specific kind of operational flexibility, the willingness to fly freighters at night with rapid turnaround and shared pilot pools, that traditional carriers are structurally unwilling to accept.

Counter-positioning works when the incumbent would damage its own business by copying the challenger's model. Delta could theoretically launch a ULCC subsidiary at MSP, but doing so would undermine its own premium pricing and risk confusing its brand. Spirit could theoretically pursue military charter contracts, but it lacks the operational track record and institutional relationships that Sun Country has built over decades. The hybrid model is not unassailable, but it creates genuine friction for competitors who might want to replicate it.

Switching Costs: Weak

Consumer switching costs in the airline industry are minimal, particularly in the ULCC segment. A passenger who flew Sun Country to Phoenix last winter can just as easily book Frontier or Southwest next winter. The charter business has somewhat higher switching costs, since organizations like the NCAA or Department of Defense value operational reliability and established relationships, but these are not structural lock-in mechanisms.

Branding: Weak to Moderate

Sun Country has strong brand recognition in Minnesota but limited awareness nationally. The ULCC model inherently constrains premium branding, since the core value proposition is low price, not aspirational lifestyle. The Minnesota identity is both an asset and a limitation: it creates genuine local loyalty but caps the airline's ability to build a national brand.

Cornered Resource: Moderate

Sun Country's cornered resources include its MSP gates and slots, its decades-long charter relationships with sports teams, casinos, and the military, and its management expertise in operating the hybrid model. The Amazon cargo contract, extended through 2030 with options to 2037, represents a significant cornered resource, though it is subject to renewal and renegotiation risk.

Process Power: Moderate

Sun Country's operational efficiency in managing a single fleet type across three business lines represents genuine process power. The ability to rotate pilots between passenger, charter, and cargo duty, to optimize aircraft utilization across time of day and season, and to maintain a cost-conscious culture that minimizes waste at every level, these are the results of years of process refinement under Bricker's leadership. However, this process power is replicable by a well-managed competitor with sufficient time and investment.

The framework summary points to a company whose competitive position is real but not dominant. Counter-positioning and cornered resources provide moderate protection, but the absence of strong scale economies, network effects, and switching costs means Sun Country's advantage depends heavily on continued operational excellence and management quality rather than structural moats.

XIII. The Bull Case vs. Bear Case

The Bull Case

The optimistic thesis for Sun Country centers on the resilience and uniqueness of the hybrid model. To appreciate how rare this diversification is, consider the fates of Sun Country's peers. Spirit Airlines filed for bankruptcy twice, in November 2024 and again in August 2025, ultimately succumbing to the brutal economics of a single-revenue-stream ULCC business. Frontier has struggled to achieve consistent profitability. Even Southwest, the most successful low-cost carrier in history, has faced margin pressure as its model matures. Against this backdrop, Sun Country's three-legged stool stands out. No other airline in the United States simultaneously operates ULCC scheduled service, a diversified charter business, and a major cargo operation for Amazon. This three-legged stool provides genuine revenue diversification that insulates the company from the demand shocks that periodically devastate single-revenue-stream airlines. When leisure travel demand weakened in 2022 and 2023, cargo and charter revenue helped stabilize total performance. When pandemic lockdowns crushed passenger flying in 2020, Amazon packages kept the freighters flying.

The MSP market opportunity remains compelling. With Spirit Airlines in bankruptcy and other low-cost carriers pulling back from Minneapolis, Sun Country faces less competitive pressure in its home market. Delta's dominance creates a pricing umbrella that allows Sun Country to operate profitably at fare levels well below Delta's, and the Twin Cities' strong origin-and-destination traffic base means there is genuine demand for a low-cost alternative. The airline's growth from twelve to twenty-one percent of MSP-originating market share demonstrates that this opportunity is real, not theoretical.

Management has delivered five consecutive years of profitability and fourteen straight profitable quarters. Bricker's track record of cost discipline and operational focus gives confidence that the airline can navigate industry headwinds without the kind of overreach that has destroyed other small carriers. The expanding Amazon relationship, now covering twenty freighters with a contract extending potentially to 2037, provides long-term revenue visibility that most airlines lack entirely.

The Bear Case

The pessimistic thesis starts with scale. Sun Country operates seventy aircraft in an industry where the major carriers operate hundreds. This size disadvantage manifests in every aspect of the business: limited negotiating power with Boeing for fleet purchases, limited ability to absorb cost shocks from fuel or labor, limited route network to spread fixed costs, and limited brand recognition outside the upper Midwest.

Delta's willingness to compete aggressively at MSP represents an existential threat that cannot be wished away. When Delta matches Sun Country's fares on a leisure route, Delta absorbs the margin compression across its massive revenue base while Sun Country feels it acutely on a handful of flights. This competitive dynamic caps Sun Country's growth potential in its home market and could squeeze margins during economic downturns when both carriers are fighting for a smaller pool of leisure travelers.

The labor cost trajectory is concerning for every ULCC, but especially for smaller ones. The flight attendant contract, which delivers up to fifty-eight percent pay increases over its term, and the upcoming pilot negotiations set a trajectory of rising labor costs that directly erodes the cost advantage on which the ULCC model depends. If CASM ex-fuel continues rising at seven to eight percent annually, Sun Country's pricing advantage over legacy carriers narrows considerably.

Amazon uncertainty adds another dimension of risk. While the expanded contract provides revenue visibility through 2030, Amazon has a history of building its own capabilities over time and reducing dependence on third-party operators. If Amazon eventually decides to bring air cargo operations in-house or shift volume to other carriers, Sun Country would lose its fastest-growing revenue stream. The concentration risk is real: a single customer accounts for approximately fourteen percent of total revenue.

The stock's post-IPO performance speaks for itself. A decline from $43 to under $10 before the Allegiant acquisition announcement suggests that the public market concluded Sun Country could not generate the growth and returns needed to justify a standalone investment thesis. The Allegiant merger offer of $18.89 per share is still twenty-one percent below the $24 IPO price, meaning investors who bought at the IPO and held through to the acquisition announcement lost money. For a company that was supposed to be a growth story, that is a sobering outcome.

Key KPIs to Watch

For investors tracking Sun Country's ongoing performance, whether as a standalone entity or as part of the combined Allegiant-Sun Country operation, two metrics deserve primary attention.

First, adjusted CASM ex-fuel is the single most important indicator of whether the ULCC model is working. This metric strips out fuel costs, which the airline cannot control, and reveals the underlying efficiency of operations. The trend from 7.49 cents in 2023 to 8.17 cents in 2025 is moving in the wrong direction, and reversing it is essential for the business model's sustainability.

Second, the revenue mix between scheduled, charter, and cargo reveals whether the hybrid model's diversification advantage is growing or shrinking. If cargo and charter continue growing as a percentage of total revenue, it strengthens the resilience thesis. If scheduled service remains dominant and the other segments stagnate, the diversification story weakens. In 2025, charter and cargo combined represented approximately thirty-four percent of total revenue, up from roughly twenty-eight percent two years earlier. That trend is encouraging, but it needs to continue.

XIV. Current State and Recent Developments (2024-2025)

Full year 2025 represented the culmination of Bricker's transformation thesis. Sun Country posted record total revenue of $1,126.8 million, crossing the billion-dollar mark for the third consecutive year. Operating income came in at $100.6 million, representing an 8.9 percent operating margin. Net income was $52.8 million, or $0.96 in diluted earnings per share. The airline achieved its fourteenth consecutive profitable quarter and fifth consecutive profitable year, a streak of consistency that would have been unimaginable during the bankruptcy years.

The revenue story was one of deliberate strategic rebalancing. Scheduled service revenue actually declined modestly to $404 million, down 1.3 percent, as the airline intentionally reduced capacity to allocate aircraft to higher-margin segments. Ancillary revenue dipped 4.2 percent to $295 million, reflecting softer scheduled service volumes. But charter revenue surged 13.8 percent to $224 million, driven by the Caesars Entertainment partnership, military contracts, and expanding sports team relationships. And cargo revenue jumped 44.6 percent to $155 million as the expanded Amazon fleet reached full operational strength.

The balance sheet strengthened meaningfully. Net debt declined seventeen percent to $364 million, while total liquidity nearly doubled to $303 million. Sun Country entered 2026 with the healthiest balance sheet in its history, an ironic achievement given that the airline would not remain independent much longer.

Apollo Global Management completed its exit in February 2025, selling its remaining 6.3 million shares through a secondary offering at $16.50 per share. After approximately seven years of ownership, during which it transformed the airline from a struggling regional carrier into a profitable publicly traded company, Apollo walked away with returns that, while modest by private equity standards on the secondary sales, vindicated the original investment thesis. The airline simultaneously authorized a $10 million share buyback program, a modest signal of confidence in the stock's valuation.

The fleet grew to seventy aircraft by year-end, including five 737-900ERs, a slightly larger variant offering approximately fifteen percent more seats per flight than the standard 737-800. Two of these entered revenue service in 2025, with three more expected by the end of 2027. The 737-900ER acquisition represented a subtle but important evolution in fleet strategy: Sun Country could add capacity on its highest-demand routes without increasing the number of flights or gate turns, effectively generating more revenue per departure while maintaining the fleet commonality that underpins the hybrid model.

On the network front, Sun Country trimmed five seasonal routes from MSP for summer 2025, reallocating that capacity to the higher-margin cargo and charter segments. The airline also launched service to Montreal and Toronto, testing international markets, and added Milwaukee-to-Caribbean routes. Cincinnati-Northern Kentucky International Airport was announced as a new operational base, the first significant geographic expansion beyond MSP and a signal that the airline was ready to replicate its playbook in other mid-market cities. The total number of employees grew to 3,281, a 4.5 percent increase that reflected the cargo fleet expansion.

The competitive landscape continued evolving in Sun Country's favor at MSP. Spirit Airlines' second bankruptcy filing in August 2025 further reduced low-cost competition in Minneapolis, reinforcing Bricker's "two-airline market" thesis. But Delta showed no signs of ceding ground, continuing to add leisure routes and match Sun Country's pricing where it felt threatened.

XV. The Future: Where Does Sun Country Go From Here?

The most consequential fact about Sun Country's future is that the airline is unlikely to face it alone. On January 11, 2026, Allegiant Travel Company announced a definitive agreement to acquire Sun Country for approximately $1.5 billion, inclusive of $400 million in Sun Country net debt. Under the terms, Sun Country shareholders will receive 0.1557 shares of Allegiant stock plus $4.10 in cash per share, implying a value of $18.89 per share, a 19.8 percent premium over the January 9 closing price.

The strategic logic of the combination is clear. Allegiant and Sun Country operate strikingly similar models: leisure-focused ULCC service, point-to-point routing, cost-disciplined operations, and a focus on underserved markets. The combined entity will serve approximately twenty-two million annual passengers across more than 175 cities and 650 routes, creating a more formidable competitor against Delta, Southwest, and the remaining low-cost carriers. Allegiant CEO Gregory C. Anderson will lead the combined company, headquartered in Las Vegas, with a significant operational presence maintained in Minneapolis.

Pending regulatory approval and expected to close in the second half of 2026, the merger represents the logical conclusion of Sun Country's trajectory. The airline proved that its hybrid model could work at a small scale, but the public market's valuation suggested that investors did not believe it could generate attractive returns over the long term as a standalone entity. Joining with Allegiant provides the scale advantages that Sun Country always lacked while preserving the hybrid model's core elements.

If the deal closes, the strategic questions shift from Sun Country-specific to those facing the combined entity. Can Allegiant successfully integrate Sun Country's operations, culture, and customer base? Will the charter and cargo businesses receive the same strategic emphasis under new ownership? How will the combined carrier navigate the ongoing challenges of labor cost inflation, Boeing delivery delays, and cyclical demand fluctuations?

Industry trends will shape the outcome regardless of ownership structure. Sustainable aviation fuel mandates are approaching, adding cost complexity that will affect all carriers. Boeing's production challenges continue constraining fleet growth across the industry. Consumer preferences are evolving, with younger travelers showing different loyalty patterns and booking behaviors than previous generations. And the fundamental cyclicality of leisure travel, driven by consumer confidence, disposable income, and the unpredictable rhythms of economic expansion and contraction, will continue to make airline investing one of the most challenging exercises in public markets.

The Minnesota question persists. Whether under its own flag or as part of Allegiant, the MSP franchise that Sun Country spent four decades building is a genuine strategic asset. The local relationships, the community trust, the charter partnerships, and the brand recognition among Twin Cities travelers do not transfer easily to an out-of-state acquirer. How Allegiant handles the Minnesota identity will be a telling indicator of whether the merger preserves Sun Country's unique advantages or gradually subsumes them into a larger, more generic operation.

There is also the question of whether the combined entity's expansion plans change the fundamental economics. With approximately 175 aircraft between them, the merged Allegiant-Sun Country carrier will be large enough to negotiate more favorable terms with Boeing, to spread corporate overhead across a bigger revenue base, and to offer pilots more career progression, reducing one of the key cost pressures facing both airlines. Whether those scale benefits materialize in practice, or whether the integration introduces new complexities that offset them, will determine whether this merger creates value or destroys it. Airline merger history offers cautionary examples in both directions.

XVI. Lessons and Playbook

For Founders and Operators

Sun Country's story offers a master class in radical reinvention. The airline that went public in 2021 bore almost no resemblance to the carrier that filed for bankruptcy in 2008 or even the one the Davis family rescued in 2011. Bricker and Apollo did not iterate on the existing model. They replaced it entirely, recognizing that incremental improvement could not overcome the structural disadvantage of being a mid-size carrier with a muddled competitive identity.

The hybrid model's success demonstrates that business model innovation remains possible even in mature, commoditized industries. The insight that a single fleet type could serve three distinct revenue streams was not technologically complex or intellectually novel. It was operationally demanding, requiring the discipline to manage scheduling, crew utilization, and maintenance across passenger, charter, and cargo operations without the complexity spiraling out of control. The lesson is that competitive advantage in mature industries often comes not from new technology but from new combinations of existing capabilities.

Focus and discipline beat breadth and ambition. Bricker's decision to concentrate on MSP rather than attempting nationwide expansion allowed Sun Country to build density, brand recognition, and operational efficiency in a single market. The temptation for any small airline is to chase growth by adding cities and routes, spreading resources thin in pursuit of scale. Sun Country's restraint, its willingness to be the best airline in Minneapolis rather than the twentieth-best airline nationally, was a strategic choice that many operators would find difficult to make but that proved essential to success.

Private equity's role in this story contradicts the simplistic narrative that financial buyers always strip assets and load debt. Apollo invested in operational transformation, hired a best-in-class operator in Bricker, funded the fleet standardization and business model pivot, and exited through a public offering rather than a leveraged recapitalization. The relationship worked because Apollo's financial interests were aligned with operational improvement: the airline became more valuable not through financial engineering but through becoming a genuinely better business.

For Investors

Small-cap airlines remain among the most challenging investments in public markets. Sun Country's journey from $24 IPO price to $8.10 trough before the Allegiant announcement at $18.89 illustrates the brutal volatility that accompanies even well-managed carriers. The airline posted five consecutive years of profitability and record revenue while its stock declined by more than sixty percent from peak. In few other industries do operational success and stock performance diverge so dramatically.

The multi-revenue-stream model provides measurable stability. Compare Sun Country's consistent profitability with Spirit Airlines' spiral into double bankruptcy, and the diversification advantage becomes concrete rather than theoretical. But diversification does not eliminate cyclicality, and investors should be wary of paying premium valuations for airlines that are, ultimately, still exposed to fuel costs, labor inflation, and demand cycles that management cannot control.

Market structure matters more than most investors appreciate. Sun Country's performance at MSP cannot be replicated in markets like JFK or LAX, where competition is more fragmented and no single carrier holds the kind of pricing umbrella that Delta provides in Minneapolis. The geography-specific nature of the advantage means that generalizing from Sun Country's experience to other airline investments requires careful analysis of local competitive dynamics.

Broader Themes

The ULCC revolution reshaped American aviation over the past two decades, democratizing air travel by offering fares that made flying accessible to consumers who previously drove or did not travel at all. But the revolution has also consumed many of its pioneers. Spirit's bankruptcy, Frontier's persistent unprofitability, and Sun Country's decision to sell to Allegiant all suggest that the pure ULCC model faces structural headwinds that operational excellence alone cannot overcome. Labor costs are rising. Fleet costs are rising. Airport fees are rising. And fare levels, constrained by intense competition and consumer price sensitivity, cannot rise commensurately. The ULCC model created enormous consumer surplus. Whether it can create durable shareholder value remains an open question.

Sun Country's story also illuminates how turnarounds actually work. The popular narrative of corporate turnarounds emphasizes cost-cutting: fire people, close offices, eliminate waste. Bricker did all of those things. But the real turnaround came from building something new, the hybrid model, the Amazon partnership, the charter expansion, not just eliminating something old. Cutting costs creates a leaner company. Reimagining the business model creates a different company. Sun Country needed both.

XVII. Final Reflections

Several aspects of the Sun Country story warrant particular attention as the airline approaches its likely absorption into Allegiant.

The charter and cargo diversification proved to be genuinely valuable, not merely a marketing talking point for investor presentations. When COVID-19 grounded leisure travel, Amazon packages kept the cargo fleet flying. When scheduled service margins compressed in 2023 and 2024, charter revenue growth offset the decline. The three-legged stool was not a gimmick. It was the reason Sun Country posted fourteen consecutive profitable quarters while Spirit Airlines went through two bankruptcies.

Apollo's contribution went beyond capital. The private equity firm's role in recruiting Bricker, supporting the ULCC transformation, and maintaining patience through the multi-year transition period represented genuine operational value-add. The common criticism that private equity firms merely extract value through financial engineering does not apply here. Apollo bought a struggling airline for $188 million, spent years and resources transforming it, and exited through a public offering that valued the business at multiples of its purchase price.

Surviving two bankruptcies and thriving is extraordinarily rare in any industry, but especially in aviation, where failed airlines almost never return. Sun Country's persistence owed something to luck, something to geography, and a great deal to the succession of owners and leaders who refused to let the airline die even when the rational economic decision might have been to walk away.

The IPO timing, March 2021 in the middle of a pandemic, appeared audacious but was grounded in a clear-eyed assessment of the recovery trajectory. Bricker and Apollo correctly anticipated that leisure travel demand would rebound strongly and that Sun Country's ULCC model was positioned to capture a disproportionate share of that recovery. That the stock subsequently declined from its post-IPO highs reflects not a failure of the original thesis but the market's reassessment of how much of that recovery was already priced in at $43 per share.

The question going forward is whether Sun Country's unique attributes, the Minnesota identity, the charter relationships, the cargo operation, the cost-conscious culture, will survive integration into a larger entity. Mergers in the airline industry have a mixed track record of preserving the best elements of both carriers. If Allegiant proves to be a thoughtful acquirer that maintains Sun Country's hybrid model while providing the scale advantages that come with a larger operation, the combination could create something genuinely formidable. If the integration follows the more common pattern of standardization and homogenization, the qualities that made Sun Country special may gradually erode.

What to watch: the combined carrier's CASM trajectory, the retention of charter and cargo contracts post-merger, and whether MSP passengers notice any difference in the service they receive. Those three signals will tell the story of whether Sun Country's final chapter is an acquisition that amplifies its strengths or one that absorbs them into something generic.

XVIII. Further Reading and Resources

For those interested in exploring this story further, the following resources provide depth across different dimensions of the Sun Country narrative. Given that the Allegiant merger is pending regulatory approval and expected to close in the second half of 2026, these resources will also be valuable for tracking the integration process and its impact on the combined entity.

Sun Country Airlines' S-1 prospectus, filed with the SEC in early 2021, provides the most comprehensive single document on the company's history, business model, and financials at the time of the IPO. The IPO prospectus is particularly valuable for understanding the Bricker-era transformation in management's own words.

For the aviation industry context that shaped Sun Country's evolution, Thomas Petzinger's book "Hard Landing" remains the definitive account of airline deregulation and its aftermath. Understanding how deregulation created the competitive landscape in which Sun Country was born and nearly died is essential context for appreciating the ULCC revolution that saved it.

Allegiant Air's own investor presentations and annual reports provide the closest comparable business model and offer insight into the strategic logic behind the merger announcement. Since Allegiant pioneered many of the operational practices that Bricker adapted for Sun Country, studying Allegiant's evolution illuminates what the combined entity might look like.

The Department of Transportation's T-100 data provides granular route-level capacity and traffic statistics that allow detailed analysis of Sun Country's MSP market position and competitive dynamics with Delta.

Sun Country's quarterly earnings calls and investor presentations from 2021 through 2025 document the post-IPO evolution in real time, including management's commentary on strategic priorities, competitive dynamics, and the Amazon relationship. The Q4 2025 earnings call, in particular, provides the most current assessment of the business heading into the Allegiant merger.

Aviation Week and FlightGlobal have provided ongoing coverage of regional carrier economics, the ULCC competitive landscape, and the Amazon Air logistics network that has become so central to Sun Country's story. Minnesota business press, particularly the Star Tribune and MinnPost, has covered Sun Country's community role and local competitive dynamics with depth that national publications cannot match.

Finally, the MinnPost feature on how Sun Country survived the Tom Petters Ponzi scheme provides gripping narrative detail on the most dramatic chapter of the airline's history, a story that deserves to be better known outside of Minnesota.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube