Snap-on: The Mobile Tool Empire

I. Introduction & Episode Roadmap

Picture this: It's 6:30 AM on a Tuesday morning in Detroit. A bright red van pulls into the service bay of a Chevy dealership, and suddenly, mechanics drop what they're doing and gather around like kids hearing an ice cream truck. But this isn't about treats—it's about tools. Premium, expensive, lifetime-guaranteed tools that these professionals will gladly pay three to four times retail price for. The van belongs to a Snap-on franchisee, and this weekly ritual has been playing out across America for nearly a century.

How did a company that started with two guys in Milwaukee inventing a simple socket system that could "snap on" to interchangeable handles build one of the most formidable distribution moats in American business? Today, Snap-on commands a $17.16 billion market cap, generates $4.7 billion in annual revenue, and maintains operating margins north of 22%—selling wrenches and screwdrivers at luxury goods pricing.

The Snap-on story isn't just about tools. It's about turning your sales force into owners, building a financing empire one wrench at a time, and creating such deep customer relationships that competition becomes almost irrelevant. It's about a company that survived the Great Depression by lending money to broke mechanics, supplied every tool NASA used on the Space Shuttle program, and somehow convinced professional technicians that paying $300 for a ratchet is not just reasonable—it's smart.

This is the story of how convenience, quality, and a fleet of 3,200 franchise vans created an unbreakable competitive advantage. It's about understanding that in business, sometimes the most powerful moat isn't technology or patents—it's simply being there, every week, with exactly what your customer needs, before they even know they need it.

We'll journey from those first ten sockets in 1920s Milwaukee through the franchise revolution of the 1990s to today's high-tech diagnostic empire. Along the way, we'll uncover how Snap-on built what might be America's most unusual retail model: one where the store comes to you, the salesperson becomes your friend, and somehow everyone makes money—except maybe the mechanic's spouse wondering why that toolbox cost more than their car.

II. Founding Story & The Innovation That Changed Everything

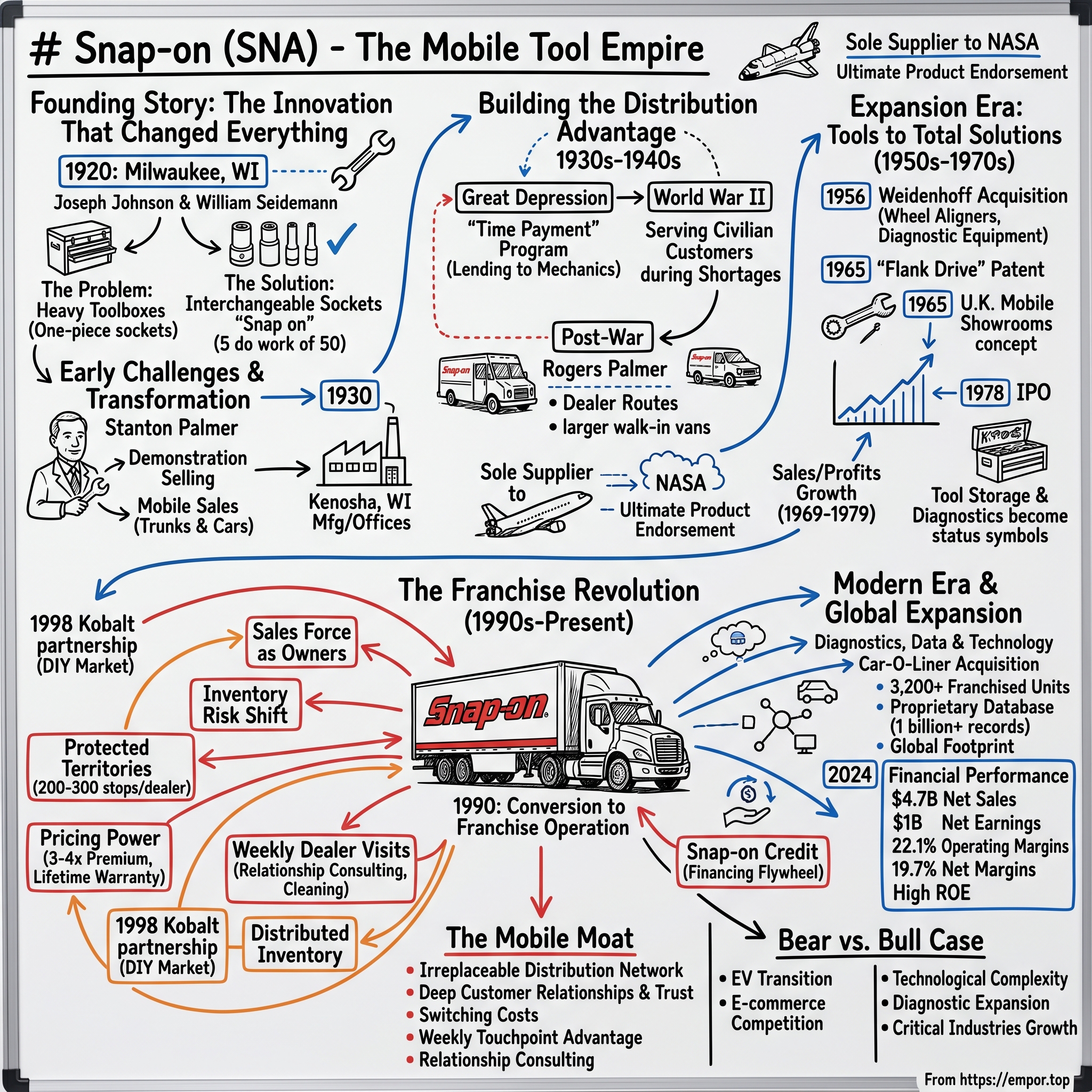

The year was 1920, and in a modest workshop in Milwaukee, Wisconsin, Joseph Johnson was having his eureka moment. A grease-stained mechanic himself, Johnson spent his days wrestling with the fundamental inefficiency of early automotive repair: carrying a massive, back-breaking toolbox filled with dozens of one-piece socket wrenches, each designed for a single nut size. Picture it—fifty different tools when five would do, if only someone could figure out how.

Johnson's breakthrough was elegantly simple: ten different socket heads that could "snap on" to just five interchangeable handles. No more lugging around redundant tools. No more cluttered toolboxes. The marketing slogan practically wrote itself: "5 do the work of 50." Together with William Seidemann, a fellow mechanic who understood the daily frustrations of their trade, Johnson filed for a patent and founded the Snap-on Wrench Company on April 29, 1920, with $500 in capital.

But here's where the story takes its first crucial turn. Johnson and Seidemann were brilliant inventors but mediocre businessmen. They built a superior product but had no idea how to sell it beyond their local Milwaukee market. Mechanics were skeptical—why pay for this newfangled system when their existing tools worked just fine? The company was bleeding cash, and by 1921, bankruptcy loomed. Enter Stanton Palmer—a former factory sales representative from Chicago who understood something Johnson and Seidemann didn't: selling tools wasn't about the product, it was about the demonstration. Palmer, who served as president of the corporation from 1921 until his death in 1931, took the tools directly to customers at their places of business and demonstrated the benefits, which became the cornerstone of the company's marketing success.

Palmer didn't just save Snap-on—he transformed it. Within months of joining, he enlisted Newton Tarble, another sales visionary, and together they identified something revolutionary: mechanics didn't want to shop for tools; they wanted tools to come to them. In December 1920, Palmer and Tarble identified 20 cities where branch offices would be established. This wasn't just geographic expansion—it was the birth of direct selling in the tool industry.

The expansion was breathtaking in its speed and audacity. By 1925, there were 17 branches and 165 salesmen selling Snap-on hand tools direct to mechanics. Palmer had taken a company on the brink of failure and, within four years, built a national sales force. The secret? Each salesman didn't just carry a catalog—they carried the actual tools, demonstrating the satisfying "snap" that gave the company its name, letting mechanics feel the quality in their hands before buying.

But Palmer's masterstroke came in 1930, just before his death. An eleven-acre site was purchased on the outer edge of Kenosha to consolidate manufacturing and its general offices, then located in Chicago. The Kenosha Chamber of Commerce had actively recruited Snap-on to diversify their economy, and Palmer negotiated a deal that would make Kenosha synonymous with premium tools for the next century.

The early sales model was deceptively simple but psychologically brilliant. Salesmen would walk into a garage, pull out the Snap-on set, and demonstrate how five handles could replace fifty tools. They'd let the mechanic use them for a few minutes, feel the precision, experience the time savings. Then came the clincher: "Keep them for a week. Try them on real jobs. I'll be back." Few mechanics returned the tools. Most became customers for life.

III. Building the Distribution Advantage: Depression to WWII

The death of Stanton Palmer in 1931 could have destroyed Snap-on. The company had just moved to its new Kenosha facility, the Great Depression was devastating American industry, and mechanics—Snap-on's core customers—were struggling to keep food on the table, let alone buy premium tools. At Palmer's death Newton Tarble left the corporation. Mr. Myers became the second president of Snap-on Tools, as a largest creditor after the depression.

William E. Myers, who came from Blue Point Tools (which Snap-on had acquired), took the helm with a radical idea: if mechanics couldn't afford tools, Snap-on would help them buy them anyway. This wasn't charity—it was calculated brilliance. During the Great Depression, struggling mechanics couldn't afford the tools they needed and no institution at the time would lend them money. Snap-on became the first tool company to do so, offering "Time Payment" selling, or "T.P." The program allowed mechanics to earn while they paid.

Think about the audacity of this move. While banks were failing and credit was frozen across America, a tool company decided to become a financial services provider. The "T.P." program wasn't just about moving inventory—it created an entirely new relationship between Snap-on and its customers. Salesmen became financial advisors, counselors, and collection agents. They knew which mechanics were getting steady work, who was reliable, who needed an extra week to pay.

At the same time, it enabled salesmen to build long-lasting goodwill. T.P. became a precursor to the Revolving Account payment plan used today. This Depression-era innovation would eventually evolve into Snap-on Credit, formally launched in the 1960s, creating a financing arm that would generate hundreds of millions in additional revenue.

But the real transformation came during World War II. As American factories converted to wartime production, tools became scarce. Most companies would have sold everything to the military at premium prices. Snap-on made a different choice—one that would define its relationship with customers for generations. The company made the strategic decision to continue serving its civilian customers even during wartime shortages, maintaining those critical relationships while competitors chased government contracts. The post-war era brought another crucial innovation. After World War II, Rogers Palmer, as senior Vice President Sales, advertised for a military officer to organize and develop a larger sales force for the expected post war sales boom. Routes were developed for company dealers to see mechanics on a weekly basis. Eventually these salesmen became independent businessmen and authorized dealers using larger walk in vans to carry a growing product line. This wasn't just about scaling the sales force—it was about creating a new class of entrepreneur.

The transformation from carrying tools in personal cars to fully stocked vans didn't happen overnight. In the early days, salesmen would stuff their trunks with as much inventory as they could carry. By the late 1940s, some were using station wagons. But the real revolution—the birth of the mobile tool store—was still to come.

IV. The Expansion Era: Tools to Total Solutions (1950s–1970s)

In 1956, Snap-on made a move that would transform it from a hand tool company into something much more ambitious. The acquisition of Weidenhoff Corporation brought wheel aligners into the product line, followed quickly by voltmeters, ammeters, and alternator testers. This wasn't just product expansion—it was a fundamental reimagining of what Snap-on could be. The company was no longer selling tools; it was selling the complete solution to fix any vehicle that rolled into a shop.

The patent wars of the mid-1960s revealed just how seriously Snap-on took innovation. After years of legal battles, the company secured its 1965 "flank drive" wrench patent—a design that gripped the flat sides of fasteners rather than the corners, dramatically reducing the chance of rounding off bolts. This wasn't just a minor improvement; it was the kind of innovation that mechanics would pay premium prices for, reinforcing Snap-on's position as the technology leader in hand tools.

But the real breakthrough came from an unexpected place: the United Kingdom. The concept of selling tools from a van, like they do today, started in the U.K. in 1965. British Snap-on dealers, dealing with narrower roads and more concentrated mechanic populations, had begun outfitting panel vans as mobile showrooms. When Snap-on executives saw this in action, they immediately recognized they were witnessing the future of tool distribution.

The numbers from this era tell a story of explosive growth that would make any Silicon Valley startup jealous. Sales increased from $66.2 million in 1969 to $373.6 million in 1979, while profits increased from $6 million to $42.6 million. That's a 5.6x revenue increase and 7x profit increase in a decade—selling wrenches and screwdrivers.

The company opened their wrench forging plant in Elizabethton, Tennessee in 1974. This wasn't just about manufacturing capacity; it was about vertical integration and quality control. By controlling the entire process from raw steel to finished tool, Snap-on could guarantee the kind of quality that justified its premium pricing.

Norman E. Lutz, who became president in 1974, understood something crucial: Snap-on wasn't really in the tool business—it was in the productivity business. Under his leadership, the worldwide sales force grew to more than 3,000. But more importantly, he formalized the relationship between Snap-on and its dealers, setting the stage for the franchise revolution that would come in the 1990s.

The 1978 IPO on the New York Stock Exchange marked Snap-on's arrival as a major American corporation. That year Snap-on stock was first listed on the New York Stock Exchange. But going public meant new pressures. Wall Street wanted growth, margins, and predictability. Snap-on would have to prove that a company built on weekly van visits and lifetime warranties could deliver the kind of returns that investors demanded.

The late 1970s also saw Snap-on perfect what would become its signature move: turning every product category it entered into a premium segment. When the company moved into tool storage, it didn't just make toolboxes—it created $10,000 rolling monuments to craftsmanship that became status symbols in shops across America. When it entered diagnostics, it didn't just make code readers—it built sophisticated systems that could diagnose problems faster than competitors' equipment.

V. The NASA Years & Premium Positioning (1980s)

During the 1980s, Snap-on became the sole supplier of tools to NASA for the space shuttles. Think about what that means: when American astronauts needed to fix something 200 miles above Earth, where there's no second chance and no backup arriving tomorrow, they reached for Snap-on tools. This wasn't just a contract—it was the ultimate product endorsement.

The NASA relationship transformed Snap-on's brand in ways that no advertising campaign ever could. Every dealer could now walk into a shop and say, "These are the same tools they use on the Space Shuttle." In an industry where reputation is everything, where mechanics stake their livelihoods on their tools working every single time, that association with NASA precision and reliability was marketing gold.

But the early 1980s weren't all smooth sailing. The company faced rapid management turnover and the brutal 1982 recession that devastated American manufacturing. A slight decrease in both revenue and earnings in 1982 was attributed to that year's recession. Snap-on examined operations and took measures to improve profitability through reducing expenses as well as marketing more aggressively. Yet while competitors slashed prices and quality to survive, Snap-on doubled down on its premium strategy, maintaining 8.7% net margins even in the depths of the downturn.

The recession response revealed the genius of Snap-on's business model. Because dealers owned their inventory and had deep relationships with customers, they could extend credit selectively, work out payment plans, and keep tools flowing to mechanics who needed them to earn a living. The company didn't just survive the recession—it deepened customer loyalty by being there when mechanics needed them most.

By the mid-1980s, Snap-on had achieved something remarkable: tools that cost 3-4 times what competitors charged, yet mechanics gladly paid the premium. How? It wasn't just about quality—though the lifetime warranty certainly helped. It was about the entire ecosystem Snap-on had built. The frequency of visits to customers had increased to weekly in some cases, and the vans carried $50,000 to $200,000 of hand tools and equipment inventory. Additional services provided by dealers, such as cleaning previously purchased Snap-on tools every six months, allowed dealers to identify and recommend replacement of worn-out tools.

The tool cleaning service was particularly brilliant. Ostensibly, it was about maintaining tools. In reality, it was about maintaining relationships. Every six months, the dealer would clean your tools, inspect them for wear, and—coincidentally—show you the latest products that might make your job easier. It was relationship selling at its finest, creating touchpoints that competitors selling through retail stores could never match.

VI. The Franchise Revolution (1990–2000s)

The year 1990 marked the most significant transformation in Snap-on's history since the invention of the interchangeable socket. In 1990, Snap-on became the first mobile tool company in the United States to convert to a franchise operation. This wasn't just a business model change—it was a masterstroke that would create one of the most powerful distribution networks in American business.

The franchise conversion solved multiple problems simultaneously. It transformed Snap-on's dealers from employees or independent contractors into true business owners with skin in the game. It shifted inventory risk from the company to the franchisees. And most importantly, it aligned incentives perfectly: franchisees only made money when they sold tools, and they only sold tools by building deep, lasting relationships with customers.

The economics of a Snap-on franchise reveal why this model works so brilliantly. Initial investment ranges from $222,000 to $500,000 to start a Snap-on Tools franchised store. With average unit volume of $797,000 in revenue per year, franchisees pay an 8% royalty fee on gross sales and a 1% marketing fee. These aren't small numbers—but they buy something invaluable: a protected territory and exclusive access to customers who have been trained over decades to buy tools from the van that visits every week.

The protected territory model is crucial to understanding Snap-on's moat. Each franchisee gets an exclusive list of customers—typically 200 to 300 stops they visit weekly. No other Snap-on dealer can call on these customers. This creates a powerful dynamic: the franchisee has every incentive to nurture these relationships because they're the only source of revenue, and customers develop loyalty to their specific dealer, not just the brand.

In 1998, Snap-on made a move that surprised industry watchers: partnering with Lowe's to create the Kobalt tool line. This wasn't abandoning the premium strategy—Kobalt was positioned as a separate brand entirely. Instead, it was recognition that there was a massive market of DIY enthusiasts and semi-professionals who wanted better-than-average tools but couldn't justify Snap-on prices. By keeping the brands completely separate, Snap-on could capture this market without diluting its premium positioning.

The franchise model also created an unexpected benefit: a distributed inventory system that would make even Amazon jealous. With 3,000+ vans carrying $50,000 to $200,000 in inventory each, Snap-on effectively had thousands of micro-warehouses positioned exactly where customers needed them. A mechanic could see a tool, try it, buy it, and use it within minutes—no waiting for shipping, no wondering if it would meet their needs.

But perhaps the most powerful aspect of the franchise model was how it turned selling into consulting. Franchisees weren't just order-takers; they became trusted advisors who understood their customers' businesses. They knew which shops were expanding, who was hiring new technicians, what types of vehicles were coming in for service. This intelligence allowed them to recommend tools before customers even knew they needed them.

VII. Modern Era: Diagnostics, Data & Global Expansion (2000s–Today)

As cars evolved from mechanical devices to computers on wheels, Snap-on faced an existential question: what happens to a wrench company when fixing cars requires software more than sockets? The answer would transform Snap-on from a tool company into a technology company that happens to make tools.

The diagnostic revolution began with a simple insight: mechanics needed to read error codes from increasingly complex vehicle computer systems. But Snap-on didn't just build code readers. The company assembled what might be the most valuable automotive database in existence: a proprietary database of over 1 billion repair records to offer mechanics the best possible diagnosis and repair decisions. This wasn't just data—it was decades of collective mechanical wisdom, digitized and searchable.

Think about the competitive advantage this creates. Every time a Snap-on diagnostic tool is used, it adds to this database. Every problem solved, every successful repair, every diagnostic path—it all feeds back into the system, making it smarter. Competitors can copy the hardware, but they can't replicate millions of repair records accumulated over decades.

The acquisition strategy of the 2010s showed Snap-on's evolution from tool maker to total solution provider. In 2014, the company acquired New Hampshire–based Pro-Cut for $42 million. In October 2016, the company acquired Car-O-Liner Holding AB, a Swedish collision repair tool company, for $155 million. In May 2017, the company acquired Norbar Torque Tools Holdings Limited for $72 million. These weren't random purchases—each acquisition brought either specialized technology or access to new markets, particularly in Europe and Asia.

Today's Snap-on operates at a scale that would astonish its founders. The company runs 3,344 locations total, including 3,201 franchised units and 143 company-owned units. Despite this massive footprint, the basic model remains remarkably unchanged: vans visit shops weekly, dealers build relationships, and mechanics pay premium prices for tools they trust.

The financial performance tells the story of a mature company that has figured out how to maintain extraordinary margins in what should be a commodity business. In 2024, net sales came in at $4,707.4 million with net earnings of $1,043.9 million, or $19.51 per diluted share. The real headline numbers are the margins: 22.1% operating margins in Q4 2024, with return on equity at 17.9% and net margins of 19.7%. These are software-like margins in a hardware business.

But perhaps the most impressive aspect of modern Snap-on is how it has maintained its premium positioning in an era of Amazon, Harbor Freight, and direct-to-consumer brands. The company still commands price premiums of 3-4x over alternatives, and mechanics still gladly pay them. Why? Because Snap-on has built something that can't be replicated with overnight shipping or rock-bottom prices: trust, relationships, and a century of being there when mechanics need them.

VIII. Playbook: The Mobile Moat

The Snap-on playbook is deceptively simple yet nearly impossible to replicate. At its core is a distribution advantage that would require massive time and capital to duplicate. A fleet of vans operated by Snap-on franchisees provides what no e-commerce platform or retail store can match: weekly, personalized, consultative selling directly at the point of use.

Consider what it would take to compete with Snap-on's distribution. You'd need to recruit 3,000+ entrepreneurs, each willing to invest $200,000-$500,000. You'd need to build relationships with hundreds of thousands of mechanics who have been trained over generations to buy from their weekly visitor. You'd need to develop the logistics, training, and support infrastructure to keep those vans running and stocked. And you'd need to convince customers to switch from a dealer they've likely known for years to an unproven alternative.

The relationship model creates switching costs that go far beyond the financial. Franchisees visit customers at their workplaces, providing a convenient and personalized shopping experience. But it's more than convenience—it's about trust. The dealer knows which tools you own, what you work on, how you like to pay. They've been there when you needed a replacement immediately, when you needed extra time to pay, when you needed advice on a tricky job. That relationship is Snap-on's real product.

The capital efficiency of the model is remarkable. Snap-on has substantially lower working capital requirements than most businesses exposed to the industrial cycle due to the franchise sales model. The company doesn't carry massive inventory—franchisees do. It doesn't manage thousands of retail locations—franchisees operate from their vans. This asset-light model enables best-in-class returns on capital that make Snap-on a favorite among value investors.

The financing flywheel adds another layer to the moat. Snap-on Credit allows mechanics to buy premium tools over time, but it's not just about making tools affordable. Every financing relationship creates recurring touchpoints, payment interactions, and opportunities to deepen the relationship. A mechanic making weekly payments is seeing their Snap-on dealer weekly, creating habitual interaction that reinforces the buying pattern.

The pricing power dynamics are fascinating. Price competition in this space is intense—Harbor Freight sells similar-looking tools for 75% less. Yet the warranty conditions, speedy delivery and brand perception are all cited as much more relevant in making a purchase decision than having the lowest price. Snap-on has trained its customers to value total cost of ownership over initial price, a remarkable achievement in a blue-collar industry where every dollar matters.

The weekly touchpoint advantage might be the most underappreciated aspect of the model. By visiting customers every week, Snap-on has inserted itself into the rhythm of the shop. Tuesday morning isn't just Tuesday morning—it's when the Snap-on dealer comes. This habitual interaction creates a psychological commitment that transcends rational purchasing decisions. The van visit becomes part of the shop's culture, a brief break from work to browse tools, chat with the dealer, and maybe treat yourself to that ratchet you've been eyeing.

IX. Bear vs. Bull Case

The Bear Case:

The bears have legitimate concerns about Snap-on's future. Start with the recent financial headwinds: negative earnings growth of -3.2% over the past year suggests the model might be reaching maturity. In a world where growth is prized above all else, a shrinking bottom line raises red flags about whether Snap-on's century-old playbook still works.

The electric vehicle transition poses an existential threat that's hard to quantify but impossible to ignore. EVs have fewer moving parts, require less maintenance, and concentrate complexity in software and electronics rather than mechanical systems. What happens to demand for traditional hand tools when there's no engine to rebuild, no transmission to service, no exhaust system to replace? The optimistic take is that EVs still need suspension work, brake service, and collision repair. The pessimistic take is that we're watching the slow-motion obsolescence of the internal combustion expertise that Snap-on has served for a century.

Competition from direct-to-consumer and e-commerce models is intensifying. Companies like Tekton and GearWrench sell directly online with lifetime warranties at fraction of Snap-on's prices. younger mechanics who grew up buying everything online might not value the weekly van visit the way previous generations did. Amazon can deliver tools same-day in many markets—why wait a week for the Snap-on dealer?

The franchise model, while powerful, has its vulnerabilities. High franchise failure rates during economic downturns can damage the brand and disrupt customer relationships. When a franchisee fails, those customers might turn to alternatives rather than wait for a new dealer. The high initial investment required to become a franchisee might also limit the pool of qualified candidates, potentially constraining growth.

Premium pricing vulnerability in recessions is a perpetual risk. When shops are struggling and mechanics are getting laid off, that $300 ratchet becomes a luxury nobody can afford. Snap-on weathered the 2008 financial crisis and the COVID pandemic, but each economic cycle tests whether customers will continue paying premium prices when cheaper alternatives exist.

The Bull Case:

The bulls see Snap-on's challenges as opportunities in disguise. Start with the complexity tailwind: the hugely increased technological complexity of newer cars has necessitated more repairs, with specialized equipment required. Modern vehicles have dozens of computer modules, advanced driver assistance systems, and sophisticated electronics that fail in ways mechanical systems never did. Every new technology creates new repair needs and new tool requirements.

The diagnostic expansion opportunity is massive and plays directly to Snap-on's strengths. As vehicles become more computerized, the value shifts from the tool that turns the bolt to the system that diagnoses which bolt to turn. Snap-on's billion-record repair database and decades of diagnostic expertise position it perfectly for this transition. The company isn't just selling diagnostic tools—it's selling the accumulated knowledge of millions of repairs.

International growth potential remains largely untapped. While Snap-on has presence globally, the penetration outside North America is nowhere near domestic levels. As automotive markets in Asia, Latin America, and Africa mature, demand for premium tools and equipment should grow. The franchise model that worked in Milwaukee can work in Mumbai.

The industrial and critical industries expansion represents another growth vector. Snap-on's push into aerospace, military, and industrial markets leverages its reputation for quality into segments where tool failure isn't just inconvenient—it's catastrophic. These markets value reliability over price even more than automotive mechanics do.

The irreplaceable distribution network might be Snap-on's greatest asset. In an era where everyone talks about digital transformation and disruption, Snap-on has something that no amount of venture capital can replicate: thousands of vans, tens of thousands of customer relationships, and a century of trust. The weekly touchpoint, the personal relationship, the immediate availability—these create value that transcends the tool itself.

X. Epilogue & Lessons

The Snap-on story offers profound lessons about building enduring competitive advantages in seemingly commodity businesses. The first and perhaps most important: turning your sales force into owners changes everything. When Snap-on converted to a franchise model, it didn't just change its org chart—it aligned the interests of thousands of entrepreneurs with the company's success. Every franchisee has skin in the game, every dealer's success is Snap-on's success, and every customer relationship is owned by someone who cares deeply about maintaining it.

How does a premium brand survive and thrive in commoditized markets? Snap-on's answer: by selling something more than the product. When a mechanic buys a Snap-on wrench, they're not just buying hardened steel formed into a tool. They're buying the security of a lifetime warranty, the convenience of weekly delivery, the relationship with a dealer who understands their business, the status that comes with owning professional-grade tools, and yes, the story they can tell about using the same tools as NASA.

Distribution as the ultimate moat is a lesson that transcends industries. While Silicon Valley obsesses over network effects and switching costs, Snap-on built a physical network that's even harder to disrupt. Those 3,000+ vans visiting hundreds of thousands of customers weekly represent relationships that can't be downloaded, can't be copied, and can't be replaced by an algorithm. In an increasingly digital world, Snap-on's stubbornly analog distribution model might be its greatest strength.

Building a 100-year company through multiple technology transitions requires a clear understanding of what business you're really in. Snap-on isn't in the wrench business or even the tool business—it's in the business of making professional mechanics more productive. That mission survived the transition from Model T to Tesla, from carburetors to fuel injection to electric drivetrains. As long as things break and need fixing, there's a place for Snap-on.

The "convenience premium" might be the most underrated business model in capitalism. Amazon proved people will pay for convenience in consumer goods. Uber proved it in transportation. Snap-on proved it in professional tools decades before either existed. By bringing the store to the customer, by being there exactly when needed, by removing friction from the buying process, Snap-on created value that customers gladly pay for. The premium isn't for the tool—it's for the entire experience around acquiring and owning that tool.

The company that started with two mechanics in Milwaukee solving their own problem has evolved into a $17 billion enterprise that still solves that same fundamental problem: how to give professional technicians the tools they need, when they need them, where they need them. The tools have gotten more sophisticated, the vans have gotten bigger, the prices have gotten higher, but the core value proposition remains unchanged.

In an era of disruption, when century-old companies regularly get steamrolled by startups, Snap-on stands as a testament to the power of customer relationships, quality products, and a business model so deeply embedded in its industry that it becomes part of the culture itself. Every Tuesday, in thousands of shops across America, mechanics take a break from their work when they hear that familiar horn honk in the parking lot. The Snap-on dealer is here. It's been that way for generations, and if Snap-on has its way, it'll be that way for generations to come.

The genius of Snap-on isn't in any single innovation or strategy. It's in the accumulation of advantages over a century: the brand built through millions of satisfied customers, the distribution network constructed one van at a time, the relationships nurtured through weekly visits, the trust earned through standing behind products for life. These advantages compound on each other, creating a business that's far more than the sum of its parts.

For investors, Snap-on represents a fascinating paradox: a traditional industrial company with software-like margins, a century-old business with a moat that internet-native companies would envy, a premium brand in a price-conscious market. It's proof that in business, as in mechanics, sometimes the old tools—properly maintained and thoughtfully evolved—are still the best tools for the job.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube