Semtech Corporation: The Quiet Giant Behind IoT's Infrastructure

I. Introduction and Episode Roadmap

Picture this: a sensor the size of a postage stamp, buried in Iowa farmland, runs on a single coin-cell battery for a decade. It talks to a gateway ten kilometers away, relaying soil moisture data that helps a farmer decide when to irrigate. The radio chip inside that sensor, the one that makes this magic possible, was designed by a company most people have never heard of. That company is Semtech.

Semtech Corporation is a roughly two-billion-dollar analog and mixed-signal semiconductor company headquartered in Camarillo, California. It designs the invisible chips that sit inside everything from data center switches to smart water meters to electric vehicle charging stations. For most of its sixty-five-year existence, Semtech was the definition of an "unexciting" semiconductor firm: steady, reliable, unsexy. Protection circuits. Voltage regulators. The kind of components that engineers need but investors yawn at.

Then something extraordinary happened. In 2012, Semtech acquired a tiny French startup called Cycleo for five million dollars. That acquisition gave Semtech ownership of LoRa, a long-range, low-power wireless technology that would become the global standard for connecting billions of IoT devices. It was the kind of deal that, in hindsight, looks like one of the greatest small acquisitions in semiconductor history.

The story of Semtech is really three stories braided together. First, it is the story of how a struggling analog chip company reinvented itself as a platform company by building an ecosystem rather than just selling silicon. Second, it is a cautionary tale about the risks of bold M&A, as the company's 1.2-billion-dollar acquisition of Sierra Wireless in 2023 nearly sank the ship. And third, it is a story about timing, because just as the IoT bet was maturing, the AI infrastructure boom arrived and handed Semtech an entirely new growth engine in its signal integrity business.

What follows is a deep dive into all of it: the origins, the near-death experiences, the brilliant bets, the painful integration, and the question of whether Semtech can pull off the rare feat of surviving sixty-five years in semiconductors and emerging stronger than ever.

II. The Semiconductor Landscape and Semtech's Origins

To understand Semtech, you first need to understand the world it inhabits. When most people think of semiconductors, they think of Intel processors, NVIDIA GPUs, or Qualcomm mobile chips. These are digital semiconductor companies, designing the complex logic circuits that power computation. Semtech exists in a different universe: the analog and mixed-signal world.

Here is the simplest way to think about it. Digital chips deal with ones and zeros, the clean abstraction of computation. Analog chips deal with the messy reality of the physical world. They convert real-world signals like temperature, voltage, and light into digital data, regulate the power flowing to every component on a circuit board, protect sensitive electronics from lightning strikes and voltage spikes, and ensure that data signals travel cleanly across cables and fiber optics without degrading into noise. If digital chips are the brains of electronics, analog chips are the nervous system, the sensory organs, and the immune system all rolled into one.

The analog semiconductor business has a very different economic profile from its flashier digital cousin. Design cycles are long. Products stay in production for years, sometimes decades, because the physical world does not change with Moore's Law. A voltage regulator designed in 2010 can still be selling profitably in 2025. Gross margins tend to be decent, in the fifty to sixty percent range for well-run companies, but growth is slower and more cyclical, tied to industrial production, infrastructure spending, and end-market demand rather than the exponential curve of compute scaling. The biggest players are Texas Instruments and Analog Devices, companies with tens of billions in revenue and massive scale advantages that allow them to amortize R&D across enormous product portfolios. Smaller analog companies face a brutal reality: not enough scale to compete on cost, not enough differentiation to command premium pricing. It is a business where you can make a good living but rarely a great fortune, unless you find a way to transcend the component trap.

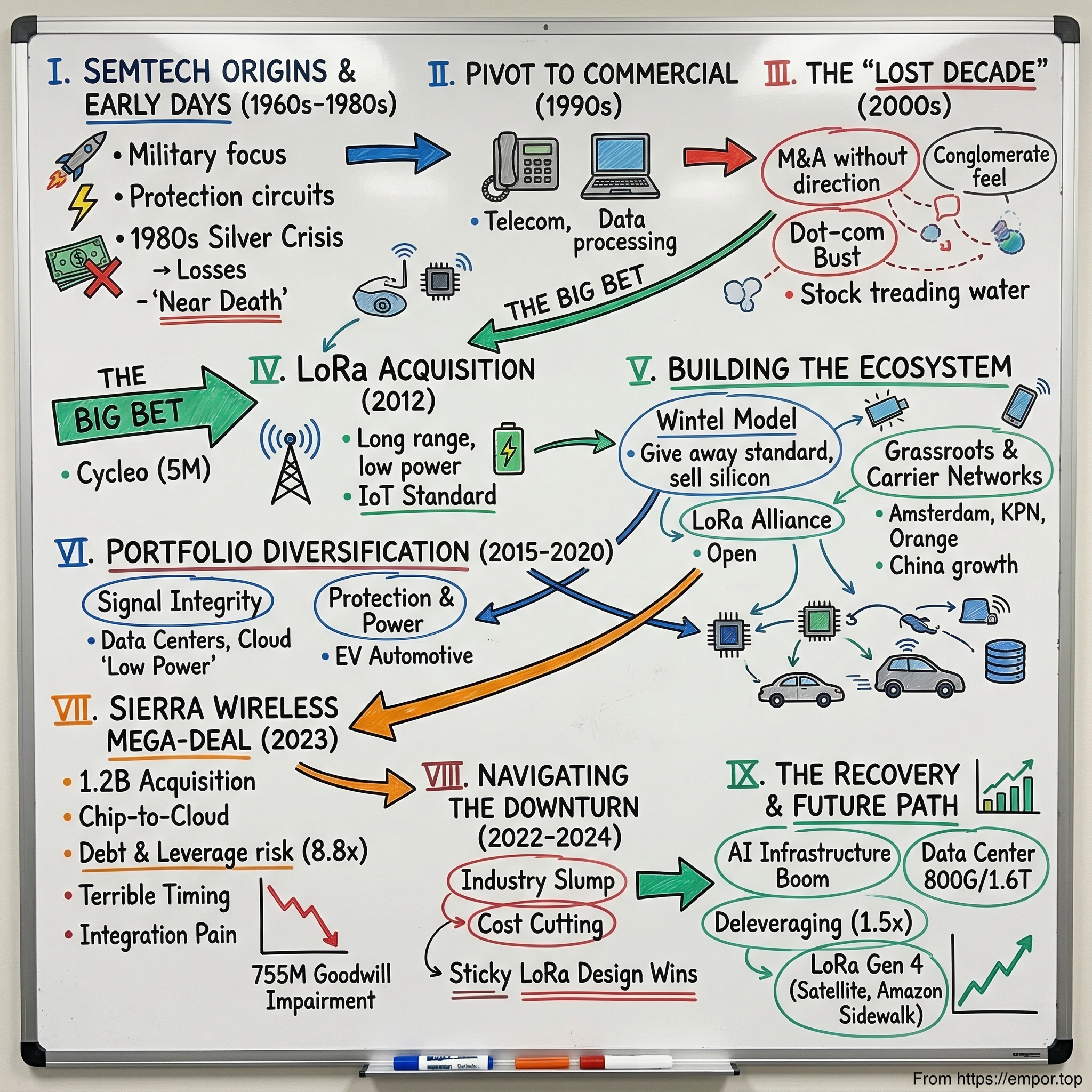

It was into this world that Gustav H.D. Franzen and Harvey Stump Jr. launched Semtech Corporation in 1960, setting up shop in Newbury Park, California. The two men had actually founded a different semiconductor company, Diodes Inc., the year before. But when investors seized control of Diodes after just twelve months, Franzen and Stump walked away and started fresh with Semtech. Their focus was narrow and practical: manufacturing power rectifiers, the semiconductor devices that convert alternating current to direct current. These were the components that went inside jet engines, X-ray machines, and missile guidance systems. If your product powered something that absolutely could not fail, you called Semtech.

The company went public in 1967 on the American Stock Exchange, and for the next decade-plus, it grew steadily if unremarkably. By the late 1970s, Semtech was doing about fifteen million dollars in annual sales with a million dollars in net income. It was a small, specialized, military-focused chip maker. Profitable, stable, and completely dependent on defense spending.

Then the silver crisis hit, and it nearly killed the company. Semtech's rectifiers used pure silver for their leads, and when the Hunt brothers' famous attempt to corner the silver market drove prices from five dollars to fifty dollars an ounce in 1979-1980, the company's cost structure was obliterated overnight. Management scrambled to switch to copper as a substitute. The substitution was rushed and poorly tested.

Copper could not withstand the high temperatures that silver handled effortlessly, and Semtech's products started failing in the field. Shipments halted for nearly a year while the company worked to fix the problem. The financial damage cascaded: losses of thirty-six thousand in fiscal 1982, then a hundred and thirteen thousand, then six hundred and sixty-eight thousand, and finally a devastating 3.97-million-dollar loss in fiscal 1985 on just under eleven million in sales. The company was bleeding out.

Management turmoil followed the financial collapse. Co-founder Harvey Stump became chairman in February 1984 but resigned six months later. His successor lasted barely a year.

By September 1985, when John "Jack" Poe arrived as the new CEO, Semtech was on life support. Poe later recalled walking into a company where his secretary was out for surgery, the SEC was asking compliance questions, and there was not enough cash to cover the next payroll. It was the kind of crisis that separates founders from operators, and Poe was very much an operator.

His survival strategy was blunt: "Absolutely anything that is not essential to keep the company going, you don't spend it." He slashed the workforce by fourteen percent, from 264 to 227 employees. He sold off a warehouse in Nevada. He imposed draconian spending controls where every purchase order above a minimal threshold required his personal approval.

It worked. By fiscal 1987, Semtech posted its first annual profit since 1981, a modest 179,000 dollars that felt like a triumph after years of hemorrhaging cash. But the near-death experience left a lasting imprint on the company's DNA. Semtech had learned the hard way that dependence on a single customer base, in this case the military, was an existential risk. When the Cold War ended and defense budgets contracted through the early 1990s, that lesson proved prescient.

Semtech was already pivoting toward commercial markets. In 1990, it acquired the Lambda Semiconductors division from Lambda Electronics, a maker of voltage regulators and power transistors for commercial and industrial applications. That single deal reduced military and aerospace revenue from ninety percent to roughly fifty percent of total sales. The company also launched commercial transient voltage suppressor diodes, or TVS, in 1993, targeting telecommunications, data processing, and consumer electronics. These were the same protection circuits that Semtech had honed for military applications, now repackaged for the booming commercial electronics market. By fiscal 1994, commercial and industrial orders exceeded military orders for the first time.

The mid-1990s acceleration was remarkable. Semtech moved its stock listing from the American Stock Exchange to the NASDAQ in March 1995, timing the move perfectly with a semiconductor industry recovery. Revenue more than doubled from twenty-six million in fiscal 1995 to sixty-two million in fiscal 1996, and net income surged over four hundred percent to 7.5 million dollars. Fortune magazine ranked Semtech among the hundred fastest-growing companies in America. By fiscal 1998, annual sales crossed the hundred-million-dollar mark for the first time in the company's history. The stock, which had traded at two dollars before the NASDAQ listing, touched nineteen dollars within six months.

But beneath the growth numbers, a familiar problem was forming. Semtech was accumulating product lines and technologies without a unifying strategic vision, setting the stage for a decade of drift.

III. The Lost Decade: Acquisitions Without Direction (2000-2011)

Imagine a semiconductor executive standing at a whiteboard in 2008, trying to answer the simplest of questions from an analyst: "What does Semtech do?" The honest answer would have been: "A lot of things, none of them dominant." That was the lost decade in a sentence.

The seeds were planted in the late 1990s, when rapid growth gave Semtech the confidence and currency to go shopping. The acquisitions came fast: Edge Semiconductor for fifty million dollars in 1997, adding automated test equipment capabilities. Acapella Ltd. in the UK in 1998, bringing fiber-optic mixed-signal design. Practical Sciences in 1999, expanding into high-speed communications. Each deal made sense in isolation, adding some technology or customer relationship. But taken together, they never cohered into a unified strategy.

The problem was structural. Semtech was serving fragmented end markets: a bit of industrial, some telecom, some computing, some consumer electronics. Each product line had its own design cycles, its own competitive dynamics, its own customer relationships. There was no platform leverage, no flywheel effect, no reason why winning in protection circuits should help you win in power management. Semtech was, to use a harsh but accurate metaphor, a semiconductor conglomerate without the benefits of conglomeration. Compare this to Texas Instruments, which used its massive scale to drive down costs and serve thousands of customers across every conceivable end market, or Analog Devices, which concentrated its engineering talent on the highest-performance signal processing applications. Semtech had neither TI's scale nor ADI's focus.

The 2000s brought the pain of this approach into sharp relief. The dot-com bust of 2001 crushed demand for high-speed telecom components, exactly the area Semtech had been investing in through its Acapella and Practical Sciences acquisitions. Overnight, the fiber-optic buildout that had driven insatiable demand for mixed-signal chips evaporated. Semiconductor cycles, which are brutal under any circumstances, hit analog companies particularly hard because they lacked the high-growth narrative that could sustain digital chip valuations through downturns. When investors are scared, they flee to quality, and in semiconductors, quality meant Intel, Texas Instruments, and a handful of other names with fortress balance sheets and clear strategic identities. Semtech was not on that list. The stock, which had soared in the late 1990s, gave back most of those gains and then some.

Through the 2000s, Semtech continued its acquisition-driven strategy, picking up smaller companies and technology portfolios to fill out its product lines. The company developed genuine expertise in USB and HDMI protection with ultra-low-capacitance TVS arrays, and made meaningful progress in power-efficient designs for mobile and networking devices. These were solid products serving real needs. By 2005, the company achieved record sales. But the fundamental question remained unanswered: what was Semtech's right to win? What made it different from a dozen other mid-size analog companies grinding out modest growth in cyclical markets?

The stock told the story. After surging in the late 1990s, Semtech shares spent most of the 2000s going nowhere. The company was profitable but not exciting, growing but not differentiated, acquiring but not transforming. It was the semiconductor equivalent of treading water: enormous effort to stay in the same place.

Mohan Maheswaran arrived as CEO in April 2006, coming from Intersil Corporation where he had run the Analog Signal Processing business unit. Born in Sri Lanka and educated in England with a BSEE from Surrey University and an MBA from Henley Executive Management College, Maheswaran had a résumé that read like a tour of the analog semiconductor industry's finest institutions: IBM Microelectronics, Texas Instruments, Hewlett-Packard, Nortel Communications, and a stint at Allayer Communications before it was acquired by Broadcom. He was the rare executive who combined deep technical understanding of analog design with the strategic vision to see beyond individual product lines.

Maheswaran's diagnosis of Semtech was blunt. The company had good products and talented engineers, but no strategic identity, no coherent answer to the question "why Semtech?" that would drive a sustainable premium valuation. Every product line faced at least three credible competitors, and none of them generated the kind of platform leverage that could compound over time. Semtech needed a breakthrough, not another incremental acquisition, but something that could fundamentally redefine the company's identity and competitive position.

That breakthrough was about to walk in the door from Grenoble, France.

IV. The LoRa Acquisition: Semtech's Defining Bet (2012)

In the early 2010s, the Internet of Things was the industry's favorite buzzword and biggest disappointment. The vision was intoxicating: billions of connected devices monitoring everything from soil moisture to pipeline pressure to parking spaces, generating data that would make the world smarter and more efficient. The reality was far more frustrating. The connectivity options for IoT were terrible.

Cellular networks worked fine for high-value, high-bandwidth applications, but at ten to twenty dollars per module and ongoing subscription fees, they were absurdly expensive for a five-dollar sensor that needed to send a few bytes of data once an hour. Wi-Fi was cheap but its range topped out at about a hundred meters, and it devoured battery life. Bluetooth was even shorter range. Zigbee and Z-Wave worked for smart homes but could not reach across a farm or a city. The IoT had a connectivity gap: there was no good way to connect low-cost, battery-powered devices over long distances.

Three thousand miles from Semtech's California headquarters, two friends in Grenoble, France had been thinking about exactly this problem. Nicolas Sornin and Olivier Seller, both RF engineers, had been experimenting since 2009 with an old technique called chirp spread spectrum modulation, or CSS. The idea behind CSS is elegant. Instead of transmitting data as a burst at a fixed frequency, the way most radios work, you encode information as a signal that continuously sweeps from a low frequency to a high one, a rising "chirp" like a bird call. Think of it this way: imagine you are in a loud stadium trying to get a message to someone far away. Instead of shouting a word that gets lost in the noise, you sing a slowly rising note. The listener knows to listen for that rising pattern, so they can pick it out even when the crowd noise is louder than your voice. That is the key insight: a CSS signal can be detected even when it is twenty decibels below the noise floor, meaning the radio can decode a message that is literally one hundred times weaker than the background noise.

CSS was already used in sonar and radar, military technologies where the ability to detect faint signals in noisy environments was literally a matter of life and death. But Sornin and Seller's innovation was applying it to low-power commercial data transmission. In 2010, they met a third engineer, Francois Sforza, and together they founded Cycleo in Grenoble, initially targeting the metering industry: gas, water, and electricity meters that needed wireless connectivity but could not afford cellular connections.

The technology they developed, which they called LoRa, short for Long Range, could transmit small data payloads over distances of ten or even fifteen kilometers in rural areas, with devices running on a single coin-cell battery for years. To put that in perspective: a LoRa sensor installed in 2016 could still be transmitting data in 2026, having never had its battery changed. For applications like water meter reading, pipeline monitoring, or wildlife tracking, this kind of longevity changed the entire economics of connectivity.

The trade-off was data rate: LoRa topped out at about twenty-seven kilobits per second in its fastest mode, and in typical long-range configurations, it ran at well under one kilobit per second. To put this in context, a modern 5G connection can transmit data more than a hundred thousand times faster. You could send a soil moisture reading, a temperature value, or a GPS coordinate over LoRa. You could not stream video or even send an email. But here is the insight that made LoRa transformative: the vast majority of IoT use cases do not need speed. They need reach, they need battery life, and they need to cost almost nothing. A water meter does not need to stream video. It needs to send a four-digit reading once a day. LoRa was exactly enough for exactly enough use cases to build a massive market.

In May 2012, Semtech acquired Cycleo for five million dollars in cash at closing, with up to an additional sixteen million in earn-out payments tied to revenue and profit milestones over the next four years. Even at the maximum twenty-one million, this was a rounding error for a company with more than five hundred million in annual revenue. It was the kind of deal that does not require board-level drama or Wall Street fanfare. A small team of Semtech engineers had evaluated the technology, seen its potential, and recommended the acquisition. Maheswaran approved it. The transaction barely registered on the semiconductor industry's radar.

After the acquisition, Semtech worked closely with Sornin, Seller, and Sforza to turn the laboratory prototypes into commercial silicon. The result was a family of transceiver chips, the SX1272 and SX1276 for end devices, and the SX1301 concentrator chip for gateways, that would become the foundation of the entire LoRa ecosystem.

But inside Semtech, the acquisition triggered a fierce strategic debate that would determine the company's trajectory for the next decade. The question was deceptively simple: should Semtech treat LoRa as another chip product, license it narrowly, and maximize short-term revenue from silicon sales? Or should it open the technology up, build an ecosystem around it, and play the long game of becoming a platform company?

Maheswaran chose the platform path, and it was controversial. The decision meant giving away the LoRaWAN network protocol specification for free, allowing anyone to build gateways, network servers, and applications on top of it. Semtech would retain ownership of the LoRa physical layer, the patented CSS modulation technology embedded in its silicon, but everything above the chip would be open.

Critics within the company and industry argued that this was leaving money on the table. Why not charge licensing fees for the protocol? Why not try to own the entire stack? The semiconductor industry's instinct is to control, to capture, to protect. Giving away intellectual property felt like surrender. Some board members worried that Semtech was creating a standard that competitors could exploit without paying for the privilege.

The answer drew from one of the most powerful playbooks in technology history: the Wintel model. In the 1990s, Microsoft gave away its Windows operating system specification to hardware makers, ensuring that any PC could run Windows. Intel, meanwhile, defined the x86 instruction set that Windows ran on. Together, they created a two-sided market where more Windows software drove demand for Intel chips, and more Intel chips drove demand for Windows software. The value accrued not to whoever owned the specification but to whoever owned the irreplaceable component that every device needed.

Maheswaran wanted to replicate this model. LoRaWAN would be the open standard that attracted network operators, device makers, and application developers. Semtech would be Intel, controlling the silicon underneath. The more the ecosystem grew, the more chips Semtech would sell. And because the patented CSS modulation was baked into the physical layer of the silicon, no one could build a LoRa radio without using Semtech's technology or licensing its patents.

In January 2015, the LoRa Alliance was formally established as an open, non-profit association, with Semtech as a founding member alongside IBM, Cisco, Actility, Bouygues Telecom, KPN, SingTel, Swisscom, and about a dozen other technology companies and telecom operators. IBM's contribution was particularly important: its research lab in Zurich had co-developed the LoRaWAN MAC layer protocol, lending the project the technical credibility and corporate gravitas that a small French startup could not have provided alone. The Alliance would manage the LoRaWAN specification, certify interoperable devices, and evangelize the standard globally.

Semtech had given away the keys to the kingdom, or so it seemed. In reality, it had done something far more clever: it had created an ecosystem that everyone could participate in, but one where every single device needed a Semtech chip to function. It was open on top and proprietary at the bottom, a structure that is almost impossible to compete against once it achieves critical mass.

V. Building the LoRa Ecosystem: Network Effects and Platform Strategy (2014-2018)

The playbook was set: give away the standard, monetize the silicon. Simple to state, brutally difficult to execute.

The challenge was the chicken-and-egg problem that kills most platform businesses. Device makers would not build LoRa sensors unless there were networks to connect them to. Why invest engineering resources in a product that has nowhere to transmit its data? Network operators would not deploy LoRa infrastructure unless there were devices to generate traffic. Why spend millions on gateways and servers if no one is building sensors? And neither side would move until they believed the other was committed.

Breaking this deadlock required simultaneous action on multiple fronts, and the LoRa Alliance's early members proved remarkably effective at it.

The first breakthrough came from an unlikely place: a hackerspace in Amsterdam. In June 2015, a Dutch entrepreneur named Wienke Giezeman set an audacious goal: cover all of Amsterdam with LoRaWAN connectivity in six weeks, using nothing but crowdsourced gateways. The Things Network, as the project was called, rallied the local tech community to deploy cheap LoRa gateways on rooftops across the city. They pulled it off. The crowdfunding campaign that followed raised nearly three hundred thousand dollars to develop open-source hardware, and The Things Network grew into a global community of over 190,000 members across more than a hundred countries. It was a grassroots demonstration that LoRaWAN networks could be deployed without waiting for a telecom operator to lay infrastructure. The implications were profound: for the first time, anyone with a hundred-dollar gateway and a broadband connection could become a piece of the IoT infrastructure.

The telecom operators were not far behind. KPN in the Netherlands launched LoRaWAN coverage in Rotterdam and The Hague in November 2015 and, driven by customer demand, completed nationwide coverage by mid-2016, making the Netherlands the first country in the world with a coast-to-coast LoRaWAN network. SK Telecom in South Korea, partnering with Samsung, achieved ninety-nine percent population coverage by June 2016. Swisscom blanketed Switzerland on a similar timeline. Orange began rolling out across France in early 2016, starting with seventeen major cities and eventually reaching thirty thousand municipalities and ninety-five percent of the French population.

In the United States, Comcast launched machineQ in 2016, deploying LoRaWAN trial networks in Philadelphia and San Francisco as a B2B IoT venture. Senet, a U.S.-based network operator, built out LoRaWAN coverage for enterprise applications. MultiTech, Kerlink, and a growing roster of gateway manufacturers were shipping hardware. It was a signal that even in the cellular-dominated American market, there was appetite for a different kind of connectivity.

But the real scale came from China. In 2018, three of China's largest technology companies, Alibaba, Tencent, and JD.com, joined the LoRa Alliance as top-tier members. Alibaba set up commercial LoRa networks in Hangzhou and Ningbo and partnered with China Unicom for smart city applications. Tencent announced plans for a LoRaWAN network in Shenzhen. ZTE backed the China LoRa Application Alliance, or CLAA, which developed an entire Chinese LoRa ecosystem. The scale was staggering: China represented billions of potential connected devices across smart metering, agriculture, industrial automation, and logistics.

While the LoRa ecosystem was building momentum, Semtech was locked in a standards war with the most powerful forces in telecommunications. Qualcomm, Huawei, Ericsson, and the major mobile operators were pushing NB-IoT, or Narrowband IoT, a cellular LPWAN technology standardized by 3GPP in June 2016. NB-IoT had powerful backers, licensed spectrum, and the full weight of the global telecom industry behind it.

On paper, it looked like NB-IoT should have crushed LoRa. The cellular industry had vastly more resources, existing infrastructure, and regulatory relationships. Qualcomm alone spent more on R&D in a single quarter than Semtech's entire annual revenue. When the telecom giants lined up behind a standard, smaller alternatives usually withered and died.

It did not, for several structural reasons that reveal a lot about how technology standards actually win in the real world.

First, cost. LoRa operated on unlicensed spectrum bands, the same kind of radio frequencies used by garage door openers and baby monitors, meaning no spectrum licensing fees and no ongoing carrier subscriptions. A farmer could deploy a LoRaWAN network covering her entire property for the cost of a single gateway, about a hundred dollars, and a handful of five-dollar sensors. NB-IoT required a cellular subscription for every device, plus more expensive modules, plus dependence on a carrier's coverage map.

Second, deployment flexibility. This was perhaps LoRa's most underappreciated advantage. Anyone could set up a LoRa network anywhere, on a remote vineyard in Napa Valley, in a warehouse complex in rural Germany, on a wildlife preserve in sub-Saharan Africa. There was no need to wait for a cellular operator to build infrastructure. NB-IoT required existing cellular towers, which meant it worked well in cities but left vast rural areas uncovered, precisely the areas where many IoT use cases, like agriculture and environmental monitoring, were most valuable.

Third, time to market. LoRa had a massive first-mover advantage. National LoRaWAN networks were operational in multiple countries by 2015-2016, while NB-IoT only completed standardization in June 2016 and did not see widespread commercial deployment until 2017-2018. In technology, two years of head start is an eternity. By the time NB-IoT was ready for prime time, thousands of enterprises had already built their IoT solutions on LoRa and were not interested in ripping them out.

The result was a market split that defied the predictions of both camps. NB-IoT, backed by government mandate and massive carrier subsidy programs, came to dominate China's public LPWAN market, eventually accounting for about eighty-four percent of all NB-IoT connections globally. China's Ministry of Industry and Information Technology essentially mandated NB-IoT adoption for smart metering, and the three state-owned carriers, China Mobile, China Unicom, and China Telecom, subsidized both modules and connectivity to drive adoption. In a top-down, state-directed market, the cellular approach won convincingly.

Outside China, the story was entirely different. LoRa held roughly forty-one percent of all LPWAN connections, more than double NB-IoT's share. The reasons mapped precisely to LoRa's structural advantages: in market economies where connectivity decisions were made bottom-up by individual enterprises rather than top-down by governments, the lower cost, faster deployment, and greater flexibility of LoRa won out. LoRa carved out dominance in smart agriculture, remote asset tracking, smart buildings, water and gas metering, and environmental monitoring, the unglamorous but enormous use cases where cost, battery life, and deployment flexibility mattered more than the higher data rates and indoor penetration that NB-IoT offered.

By fiscal year 2018, LoRa had delivered record annual net sales within Semtech's Wireless and Sensing Products Group. By fiscal 2019, total Semtech revenue reached 627 million dollars, with LoRa gateway deployments tripling to 243,000, capable of supporting over a billion end nodes. The five-million-dollar acquisition was proving to be one of the shrewdest bets in semiconductor history. And Semtech's stock, which had languished through the lost decade, was beginning to re-rate as investors recognized the platform story. For an investor, the key revelation was not LoRa's technical specifications but rather its business model: Semtech had built a two-sided network effect where more gateways attracted more devices, more devices attracted more application developers, and all of it ran on Semtech silicon.

VI. Portfolio Diversification: Beyond LoRa (2015-2020)

The LoRa story was compelling, but Maheswaran understood a dangerous truth about semiconductor companies: being a one-trick pony is a death sentence. Markets shift, technologies get disrupted, and a single product line, no matter how dominant, cannot sustain a company through the inevitable downturns. While LoRa was scaling, Semtech was quietly building a second growth engine that would prove just as important.

The signal integrity business, which designs chips that ensure data travels cleanly across cables and fiber optics at extremely high speeds, was riding a powerful secular trend: the explosion of data center construction driven by cloud computing and, increasingly, artificial intelligence. Every time a hyperscaler like Amazon, Google, or Microsoft built a new data center, it needed thousands of high-speed interconnects linking servers, switches, and storage. Each of those interconnects needed Semtech's chips.

The company's approach was characteristically analog-engineering clever. To understand why, consider what happens inside a data center. Thousands of servers need to talk to each other at blinding speeds, sending data across cables and fiber optics. As those speeds increase from 100 gigabits to 400 gigabits to 800 gigabits per second, the electrical signals degrade, like a whisper getting lost in a noisy room. The industry's dominant solution was to use Digital Signal Processors, essentially tiny computers embedded in each cable connector, to clean up and reconstruct those degraded signals. Companies like Broadcom and Marvell led this DSP-based approach, and it worked well, but DSPs consumed enormous amounts of power and generated significant heat.

Semtech bet on a different approach. Its CopperEdge platform used linear equalizers and redrivers for Active Copper Cables. Think of it as the difference between using a powerful amplifier system to boost a fading audio signal versus using a more elegant analog circuit that gently corrects the signal as it travels. The result consumed less than two watts per cable end, ninety percent less power than DSP-based alternatives. Its FiberEdge and DirectEdge platforms offered Linear Pluggable Optics, or LPO, that removed the power-hungry DSP from optical modules entirely. In a world where data center operators were increasingly constrained by power budgets, where every watt saved on networking meant a watt available for computation, Semtech's lower-power approach was not just a nice-to-have but a genuine competitive differentiator. When you are building a data center that consumes as much electricity as a small city, reducing interconnect power consumption by ninety percent is a very big deal.

The protection circuit business, Semtech's original bread and butter, also found new life in unexpected places. The rise of electric vehicles created massive demand for transient voltage suppression in automotive applications. An electric vehicle's drivetrain operates at voltages of 400 to 800 volts, and the power electronics that control motor speed, battery charging, and regenerative braking generate significant electromagnetic interference and voltage transients. Every sensitive electronic component in the car, from the infotainment system to the ADAS sensors to the battery management system, needs protection from these spikes. Semtech's decades of TVS experience, honed in military and industrial applications where failure was not an option, gave it deep credibility in this emerging market. The automotive qualification process is notoriously rigorous, with product lifetimes measured in decades and quality standards measured in parts per billion, which created another form of competitive moat for incumbents who had already passed the tests.

By 2020, Semtech had achieved a portfolio balance that looked something like forty percent LoRa-related wireless and sensing, thirty percent signal integrity for data centers, and thirty percent protection and other analog products. This was a far cry from the unfocused conglomerate of the 2000s. Now each business had a clear strategic rationale: LoRa provided the growth engine and platform story, signal integrity offered exposure to the secular data center buildout, and protection products generated steady, high-margin cash flows from automotive and industrial customers.

The strategy was clear: use LoRa's growth and cash flows to fund expansion in adjacent high-value markets, reducing dependence on any single product line. It was a sensible plan, and it was working. Revenue had grown from about 600 million in fiscal 2018 to nearly 700 million by fiscal 2020, with margins holding steady. But Maheswaran was looking at the LoRa value chain and seeing something that bothered him: Semtech was capturing only a thin slice of the total economic value that its technology was creating. Module makers, gateway companies, and cloud platforms were all profiting from the LoRa ecosystem, and Semtech was limited to selling the silicon at the bottom of the stack. The question was whether Maheswaran would have the patience to let the organic strategy play out gradually, or whether he would reach for something bigger to capture more of that value chain.

VII. The Sierra Wireless Mega-Deal and Integration (2023)

By 2020, Semtech dominated LoRa at the silicon level, but the company sat at only one layer of the IoT value chain. Above the chip, the module makers, Quectel, Fibocom, Sierra Wireless, and others, assembled Semtech's LoRa chips into finished wireless modules and sold them to device manufacturers. Above the modules, gateway makers, network server providers, and cloud platforms captured yet more value. Semtech made the most critical component, but it captured only a fraction of each IoT deployment's total value.

Sierra Wireless was a tempting target. Founded in 1993 and headquartered in Vancouver, British Columbia, it was a pioneer in wireless IoT connectivity with nearly three decades of cellular module expertise and relationships with major enterprise customers. Its product line included cellular modules, gateways, routers, and an IoT cloud platform offering managed connectivity services. Sierra Wireless also had something Semtech badly wanted: capabilities in licensed-spectrum technologies like LTE-M and NB-IoT, which would allow Semtech to offer customers both LoRa (unlicensed spectrum) and cellular (licensed spectrum) connectivity from a single vendor.

But Sierra Wireless was also a company in distress. Founded by the legendary wireless engineer Daniel Bowman, it had been a pioneer in the cellular module space, shipping some of the first 3G and 4G embedded modules in the industry. At its peak, Sierra Wireless had been valued at over four billion dollars. But by 2022, the company was a shadow of that former glory, with a market capitalization hovering around eight hundred million. Its financials had been mediocre for years, with low margins in the brutally competitive module business. Cellular IoT modules were commoditizing rapidly under pricing pressure from Chinese competitors, particularly Quectel, which held roughly forty percent of the global market and was undercutting Western vendors on price by thirty to forty percent.

Sierra Wireless had something that could not be easily replicated: strong customer relationships with enterprise IoT buyers, certifications across dozens of carriers and regulatory jurisdictions, and a cloud platform called Octave that simplified IoT data management. But its business model was fundamentally different from Semtech's high-margin chip business. Selling modules at twenty to thirty percent gross margins is a volume game that rewards manufacturing efficiency, not design innovation. Combining it with a sixty-percent-margin chip business was, to be charitable, an unusual strategic choice.

On August 2, 2022, Semtech announced it would acquire Sierra Wireless for thirty-one dollars per share in an all-cash transaction, valuing the company at approximately 1.2 billion dollars including debt. The deal closed on January 12, 2023. The financing package totaled 1.815 billion dollars, including refinancing of existing debt, pushing Semtech's net leverage ratio to approximately 8.8 times, a dangerously high level for a cyclical semiconductor company.

The strategic thesis was ambitious: create a "chip-to-cloud" IoT platform. The deal would nearly double Semtech's annual revenue, add approximately a hundred million dollars of high-margin IoT Cloud recurring revenues, and generate an estimated forty million in annual run-rate operational synergies within twelve to eighteen months. On paper, it was the kind of vertical integration that could transform Semtech from a component supplier into a solutions company, controlling more of the value chain and competing directly with the likes of Qualcomm and Telit Cinterion in end-to-end IoT.

The timing, however, was terrible. This is a pattern that repeats itself across M&A history: the deals that look most strategically compelling are often announced at the worst possible moment, because the strategic urgency that drives the deal is itself a product of peak-cycle confidence. Semtech closed the Sierra Wireless deal in January 2023, at the peak of the semiconductor cycle, just as the industry was heading into one of its sharpest downturns in years. The integration had to be executed while demand was cratering, the balance sheet was groaning under nearly two billion dollars of debt, and the cultures of two very different organizations, a lean, high-margin fabless chip company based in Camarillo and a sprawling, lower-margin hardware-and-services business headquartered in Vancouver, had to be somehow merged into a cohesive whole.

The results were painful. In fiscal year 2024, the first full year with Sierra Wireless, Semtech recorded a staggering 755.6 million dollars in goodwill impairment and 131.4 million in intangible asset impairment, essentially writing down the majority of the premium it had paid. The GAAP diluted loss per share hit negative seventeen dollars and three cents. GAAP gross margin fell to 34.1 percent, dragged down by the lower-margin module business, though non-GAAP gross margin was a more respectable 49.5 percent.

Then came the management upheaval. Maheswaran, who had orchestrated both the LoRa triumph and the Sierra Wireless gamble, announced his retirement on March 15, 2023. His successor, Paul Pickle, took over on June 30, 2023, but lasted less than a year before being abruptly fired on June 6, 2024, with the board citing "differences on how the chief executive and the board should work together." Pickle subsequently sued Semtech for corporate records. Three CEOs in fourteen months is the kind of turmoil that makes investors deeply nervous.

The board turned to Dr. Hong Q. Hou, a semiconductor industry veteran who had been serving as a Semtech board member since July 2023. Hou's background was unusually well-suited to the challenge. He held a Ph.D. in electrical engineering and had spent over two decades in senior semiconductor roles. At Intel, he had run the Cloud and Edge Networking Group with full P&L responsibility, overseeing a multi-billion-dollar business that sold precisely the kind of data center interconnect products that Semtech's signal integrity division competed against. Before Intel, he had led Brooks Automation's Semiconductor Group. He understood both the chip side and the systems side of the business, which was exactly what the Sierra Wireless integration required.

Hou moved quickly to set priorities. The company streamlined its organizational structure, consolidated product lines, and refocused R&D spending on the highest-return opportunities. The messaging to investors was consistent and disciplined: deleverage the balance sheet, improve gross margins, and execute on the signal integrity growth opportunity. No more grand strategic pronouncements. Just blocking and tackling.

For investors, the Sierra Wireless deal represented both the opportunity and the peril of transformational M&A. The strategic logic, owning more of the IoT value chain, was sound. But the execution risk of integrating a struggling business while carrying enormous debt during a cyclical downturn nearly proved fatal. The lesson echoed through semiconductor history: timing matters as much as strategy.

VIII. Navigating the 2022-2024 Semiconductor Downturn

The semiconductor industry's 2022-2024 downturn was a perfect storm, and Semtech was standing in the worst possible spot when it hit.

After years of pandemic-driven demand that led to chip shortages and double-ordering by customers, the cycle reversed violently in the second half of 2022. Customers who had stockpiled inventory during the shortage, sometimes ordering twelve months of supply when they only needed six, began working through their excess. New orders dropped off a cliff. Industrial customers, a key Semtech end market, were among the hardest hit as capital expenditure budgets were frozen. China's economic slowdown, property market stress, and geopolitical tensions further dampened demand from what had been a major growth driver.

Semtech was exposed on multiple fronts. Its industrial and infrastructure customers slashed orders just as the company was digesting the Sierra Wireless acquisition and carrying a massive debt burden. The interest expense on that debt ran to roughly seventy-five million dollars annually, a punishing drag on cash flow at a time when revenue was declining. The combination was reflected brutally in the stock price: from an all-time high of nearly ninety-five dollars per share in November 2021, Semtech shares plummeted to around twenty-four dollars by 2024, a decline of roughly seventy-five percent.

Management responded with the classic downturn playbook, but with an urgency born of survival rather than optimization. The cost-cutting was aggressive: facility closures, workforce reductions, restructuring charges, and an intense focus on cash flow generation to pay down debt. Every discretionary dollar was scrutinized. Product lines that could not justify their existence were rationalized. The operational synergies from the Sierra Wireless integration, which had been planned for a leisurely twelve-to-eighteen-month timeline, were accelerated out of necessity. Ironically, the crisis may have helped the integration. Nothing focuses an organization quite like the shared awareness that the alternative to rapid execution is financial distress.

But even through the downturn, something important was happening beneath the surface. LoRa design wins continued to accumulate. In the semiconductor business, a design win is when a customer commits to using your chip in a new product. The product might not ship for twelve to twenty-four months, but the design win is a binding commitment that creates long-term revenue. Because LoRa's sales cycles were so long and switching costs so high, customers who had spent a year integrating LoRa into their products were not going to rip it out during a downturn. The installed base was sticky, and the design win pipeline kept growing even as current revenue fell. In a perverse way, the long sales cycles that made LoRa frustrating to investors in the short term were protecting Semtech's moat in the long term.

The recovery, when it came, was driven by two forces. First, the semiconductor inventory correction began to normalize in late 2024 and early 2025, with customers resuming more normal ordering patterns. Second, and more powerfully, the AI infrastructure buildout was accelerating. Hyperscalers were pouring billions into data centers, and every new data center needed thousands of high-speed interconnects, exactly the products Semtech's signal integrity division made. The company's CopperEdge and FiberEdge products, with their power-efficient analog approach, were winning design slots at multiple major hyperscalers for 800G and 1.6T connectivity.

The financial turnaround was dramatic in both speed and magnitude. In fiscal year 2025, revenue reached 909 million dollars, up nearly five percent year-over-year, not a blowout number, but a meaningful inflection after the downturn. More importantly, the quality of the recovery was impressive.

GAAP gross margin recovered to 50.2 percent, a sixteen-percentage-point improvement from the impairment-ravaged prior year. Free cash flow turned decisively positive at fifty million dollars, up 141 percent. Most impressively, Signal Integrity revenue grew forty-eight percent for the full year, driven by design wins at multiple hyperscalers for 800G connectivity.

The balance sheet repair was even more dramatic. The company paid down 656 million dollars of debt during fiscal 2025, including fully retiring the 441-million-dollar term loan that had been the most restrictive piece of the capital structure. By the third quarter of fiscal year 2026, Semtech's adjusted net leverage ratio had plummeted from the terrifying 8.8 times post-acquisition to a much more manageable 1.5 times. Annualized interest expense collapsed from seventy-five million to below three million dollars, freeing up roughly seventy-two million dollars of annual cash flow that had previously been consumed by debt service.

The stock responded in kind, recovering from its twenty-four-dollar trough to trade around eighty-seven dollars by early March 2026. It was a remarkable round trip, from the brink of financial distress to a position of relative strength, accomplished in roughly two years. For investors who had the conviction to hold through the crisis, or the courage to buy during it, the return was substantial. But the experience left scars. The lesson, painfully learned, was that even a company with strong technology assets and genuine competitive moats can see its equity nearly destroyed by the combination of excessive leverage and unfortunate timing. Balance sheet risk, not business risk, had been the primary threat to Semtech shareholders, and the company spent two years proving it understood the difference.

IX. The Competitive Landscape and Market Position (2024-Present)

When the dust settled on a decade of IoT connectivity wars, the landscape looked very different from what anyone predicted in 2015. The LPWAN connectivity market has sorted itself into a surprisingly clear hierarchy. LoRa and NB-IoT emerged as the two dominant technologies, together accounting for roughly eighty-seven percent of all LPWAN connections. By late 2024, analysts projected the combined total would reach 3.5 billion connections by 2030. Sigfox, the French startup that had once been LoRa's most direct competitor with its ultra-narrowband proprietary technology, filed for bankruptcy protection in January 2022 after burning through over three hundred million dollars in venture capital. Its assets were acquired by Singapore-based UnaBiz, but the installed base of just fifteen million devices was a fraction of LoRaWAN's 125 million and shrinking. Sigfox's collapse validated Semtech's open-ecosystem strategy: a proprietary, closed standard with a single vendor created exactly the lock-in concerns that scared away operators and device makers.

In signal integrity, Semtech occupies a different competitive niche than the dominant players. Broadcom and Marvell dominate the DSP-based transceiver market for the highest-bandwidth data center applications. Broadcom's semiconductor revenue runs at roughly eleven billion dollars per quarter, dwarfing Semtech's quarterly revenue by a factor of forty. But Semtech is not trying to compete head-to-head. Instead, it leads in the emerging market for power-efficient Linear Pluggable Optics and Active Copper Cables, products that avoid the power-hungry DSP entirely. As data center operators become increasingly constrained by power envelopes, especially in the dense AI training clusters where cooling is a bottleneck, Semtech's low-power approach is gaining traction. The company has secured LPO design wins with several top U.S. hyperscalers.

The module business, inherited from Sierra Wireless, sits in the most competitive segment. The five largest cellular module vendors, Quectel, China Mobile, Fibocom, SIMCom, and Telit Cinterion, hold a combined seventy-two percent of the market. Chinese vendors dominate on cost, with Quectel alone holding roughly forty percent market share. However, geopolitical tensions are creating an opening for Western vendors. In January 2025, the U.S. Department of Defense added Quectel to the 1260H list, prompting some Western OEMs to evaluate alternatives. Telit Cinterion and Semtech's Sierra Wireless unit are the primary beneficiaries of this "dual-sourcing" trend.

China remains both Semtech's greatest opportunity and its most complex challenge. The country is the world's largest IoT market, and LoRa has been adopted extensively for private network deployments, campus-wide industrial applications, and logistics. But the Chinese government officially favors NB-IoT through Ministry of Industry and Information Technology mandates, and local competitors like ASR Microelectronics offer lower-cost LoRa-compatible chipsets. ASR is the number-two LoRa chipset maker globally, though its products require either licensing from Semtech or use of alternative modulation schemes, since Semtech's CSS patents provide a fundamental IP moat.

Emerging threats are real but manageable. Fifth-generation RedCap, standardized in 3GPP Release 17 and its more power-efficient successor eRedCap in Release 18, could encroach on LoRa's territory in mid-tier IoT applications that need moderate data rates and mobility. But RedCap module costs remain significantly higher than LoRa, and it requires licensed spectrum with ongoing carrier fees. Satellite IoT, via Starlink's direct-to-device service and AST SpaceMobile, could reduce the addressable market for remote asset tracking. But here, Semtech is playing offense rather than defense: its LoRa Gen 4 transceiver, the LR2021, supports both terrestrial and satellite communication from a single chip, and two LoRa Alliance members, Lacuna Space and Plan-S, already operate commercial LoRaWAN services from LEO satellites.

Smart home standards like Matter and Thread, while generating significant consumer buzz, operate in a fundamentally different domain. Thread's mesh networking works over short distances within buildings using 2.4 GHz radio. LoRa operates over kilometers using sub-gigahertz frequencies. There is virtually no competitive overlap. The simplest way to think about it: Thread is for the smart thermostat in your living room. LoRa is for the water meter under the street, the soil sensor in the field, the asset tracker on the shipping container. Different problems, different physics, different economics. The real risk to LoRa is not from any single competing technology but from the possibility that cellular IoT costs drop low enough, and coverage extends far enough, that the cost advantage of operating on unlicensed spectrum becomes marginal. That day has not arrived, but it gets a little closer with each new cellular generation.

X. Business Model Deep Dive and Unit Economics

To understand Semtech's economics, picture three very different businesses under one roof.

Semtech's revenue model has become meaningfully more complex since the Sierra Wireless acquisition. The company now reports three segments: Signal Integrity, which designs high-speed interconnect chips for data centers; Analog Mixed Signal and Wireless, which includes LoRa and the traditional protection and power management business; and IoT Systems and Connectivity, which encompasses the Sierra Wireless module, gateway, and cloud platform business. Each segment has its own margin profile, growth trajectory, and competitive dynamics, and the interaction between them is what makes Semtech either a compelling investment or a confusing conglomerate, depending on your perspective.

The gross margin profile varies dramatically across these segments, and understanding this mix is essential for any investor. The legacy chip business, both signal integrity and analog mixed signal, generates gross margins in the fifty-five to sixty-five percent range, typical of well-run fabless semiconductor companies. The IoT Systems business, selling hardware modules and managed connectivity services, runs at much lower margins, typically in the twenty to thirty percent range. The blended gross margin has been recovering as the company optimizes the Sierra Wireless portfolio: from the distorted 34.1 percent GAAP figure in fiscal 2024, influenced by massive impairment charges, to 50.2 percent in fiscal 2025, to above fifty-two percent in the most recent quarters.

R&D intensity runs at fifteen to eighteen percent of revenue, in line with analog semiconductor peers. Semtech operates on a fabless model, meaning it designs chips but contracts out manufacturing to foundries like TSMC and GlobalFoundries. Importantly, Semtech's chips use mature semiconductor process nodes, not the bleeding-edge technology that digital chips require. This means manufacturing capacity is generally more available and less expensive, though it also means Semtech does not benefit from the massive transistor-density improvements that drive Moore's Law in digital chips.

The sales cycle for design wins is twelve to twenty-four months, after which a product typically goes into production for several years. To appreciate what this means, consider a real example. A smart water meter manufacturer decides in 2024 to build a new product using Semtech's LoRa transceiver. The engineering team spends six months selecting the chip, six months designing the circuit board, six months testing and qualifying the product, and another six months getting regulatory certifications. The first production units ship in 2026. The product then stays in production for five to seven years.

Once that customer has invested two years of engineering effort into designing around Semtech's chip, switching to a competitor's product means repeating the entire process. The switching cost is not the price difference between a three-dollar chip and a two-dollar-fifty-cent chip. It is the two-year delay and the millions of dollars in re-engineering. This is why the design win pipeline, while not always disclosed in detail, is the single most important leading indicator of future revenue. It is also why semiconductor downturns, painful as they are, do not destroy the business: the design wins secured during the downturn guarantee revenue when the recovery arrives.

The ecosystem flywheel that Maheswaran envisioned is now clearly visible in the numbers. More LoRaWAN networks deployed globally lead to more device manufacturers designing LoRa chips into their products, which leads to more network traffic, which attracts more network operators. The LoRa Alliance now counts over 350 members. Amazon's Sidewalk network, which uses LoRa as its core radio technology, announced international expansion in March 2026, potentially turning every Ring doorbell and Echo speaker into a LoRaWAN gateway. If Sidewalk scales, it could add millions of LoRa access points to the global network without Semtech spending a dollar on infrastructure.

Capital allocation has shifted dramatically under new management, and this shift tells a story about institutional learning. The historical pattern of acquisition-heavy spending, which peaked with the Sierra Wireless deal, has given way to an almost single-minded focus on deleveraging. The company reduced total debt by 656 million dollars in fiscal 2025 and fully repaid its 441-million-dollar term loan. Remaining debt consists of approximately 503 million dollars in convertible notes maturing in 2027 and 2030, with annualized interest expense below three million dollars, a stunning reduction from the seventy-five million in annual interest that was suffocating the company just eighteen months earlier.

Free cash flow generation, which hit fifty million in fiscal 2025, is expected to inflect higher as integration costs fade and the revenue mix shifts toward higher-margin products. The math is compelling: with interest expense effectively eliminated and restructuring charges winding down, every incremental dollar of revenue improvement falls much closer to the bottom line.

In March 2026, the company completed the acquisition of HieFo Corporation for approximately thirty-four million dollars, gaining Indium Phosphide laser technology critical for 1.6T and 3.2T optical modules. This was a very different kind of deal from Sierra Wireless: small, targeted, and directly tied to the company's fastest-growing product segment. If the Sierra Wireless acquisition represented Semtech's appetite for transformation, the HieFo deal represented something more mature: a company that has learned to make surgical bets on adjacent technology rather than swinging for the fences.

XI. Porter's Five Forces Analysis

Strategy frameworks exist to cut through narrative and expose the structural realities of a business. Applied rigorously to Semtech, they reveal a more nuanced picture than either the bull or bear narrative alone would suggest.

The threat of new entrants is moderate. Analog chip design is an art form that takes decades to master. Building an ecosystem like LoRaWAN, with 350-plus alliance members, 125 million deployed devices, and partnerships with telecom operators across a hundred countries, cannot be replicated overnight. However, the open nature of the LoRaWAN standard means that competitors can, in theory, build LoRa-compatible chips. ASR Microelectronics in China has done exactly this, though it must either license Semtech's CSS patents or develop alternative modulation approaches. The barriers to entry are high for the full platform play, but moderate for individual product segments.

Supplier bargaining power is low. As a fabless company using mature semiconductor process nodes, Semtech has multiple foundry options and does not face the same capacity constraints that plague companies designing at the leading edge. TSMC and GlobalFoundries provide manufacturing capacity that is generally abundant for Semtech's needs.

Buyer bargaining power is moderate to high, and this varies by segment. In the LoRa chip business, once a device maker has designed in Semtech's transceiver, switching costs are substantial, and the LoRa Alliance ecosystem creates lock-in. But in the module business, buyers have multiple alternatives and can easily switch between vendors. Large customers like major device OEMs and telecom operators have significant negotiating leverage.

The threat of substitutes is high and constant. Cellular IoT technologies, NB-IoT, LTE-M, and the emerging 5G RedCap, offer alternatives backed by the enormous resources of the global telecom industry. Wi-Fi HaLow targets the middle ground between traditional Wi-Fi and LPWAN. Satellite IoT could eventually address the remote coverage use cases where LoRa currently has an advantage. Technology evolution risk is simply a fact of life in semiconductors.

Competitive rivalry is moderate to high across all three business segments. In LoRa, Semtech remains dominant but faces persistent cellular lobbying and the ASR Microelectronics challenge in China. In signal integrity, it competes against much larger players like Broadcom, Marvell, and MACOM, though its power-efficient niche provides differentiation. In modules, the market is intensely competitive and commoditizing, with Chinese vendors offering aggressive pricing that Western companies cannot profitably match.

The overall Porter's assessment is sobering but not alarming. Semtech operates in an industry where substitute threats are high and competitive rivalry is intense, but where its specific competitive moats, LoRa ecosystem network effects and signal integrity differentiation, provide meaningful protection in the segments that matter most. The module business, where all five forces are unfavorable, is the weakest link and the primary source of investor concern about blended margin compression.

XII. Hamilton's Seven Powers Analysis

Hamilton Helmer's framework identifies seven sources of durable competitive advantage. Applied to Semtech, it reveals where the company's moat is strongest and where it is most vulnerable.

Scale economies are moderate. The module business benefits from manufacturing scale, but the chip business, operated on a fabless model, does not generate the same kind of fixed-cost leverage that a vertically integrated manufacturer would. Semtech's R&D costs are spread across a relatively modest revenue base compared to giants like Texas Instruments.

Network effects are strong, and this is Semtech's crown jewel power. The LoRaWAN ecosystem exhibits classic two-sided network effects: more gateways make the network more valuable for device makers, more devices make the network more valuable for operators, and more participants of both types attract more application developers and cloud platforms. The LoRa Alliance serves as the orchestrating mechanism for this flywheel. With 125 million deployed devices, 350-plus alliance members, and Amazon Sidewalk extending the network into consumer homes, these network effects are substantial and growing.

Counter-positioning was initially strong. When LoRa launched, it offered a "good enough" alternative to the cellular industry's "high performance, high cost" approach. Cellular operators could not easily match LoRa's cost structure because doing so would cannibalize their existing subscription-based business models. However, as LoRa has become mainstream and cellular LPWAN technologies have dropped in price, this counter-positioning advantage has faded.

Switching costs are moderate to high in the chip business, where an eighteen-to-twenty-four-month design cycle creates significant lock-in once a customer commits. In the module business, switching costs are lower because modules are more interchangeable.

Branding power is low to moderate. Semtech is a B2B company; its brand matters less than its specifications and ecosystem. That said, "LoRa" has become a recognized brand within the IoT community, and developers who learn the LoRaWAN protocol tend to stick with it.

Cornered resource is moderate. Semtech's LoRa CSS patents and early ecosystem leadership are valuable but can be competed away over time as patents expire and alternatives improve. The company's deep bench of analog design engineers is another cornered resource, though talent can be hired away.

Process power is moderate and still developing. Decades of analog design expertise provide institutional knowledge that is difficult to replicate. The integration of Sierra Wireless could eventually build process power in solutions selling, combining hardware, software, and services in ways that competitors cannot easily match, but this remains a work in progress.

The verdict is clear: network effects are Semtech's primary and most durable moat. Scale and switching costs provide secondary protection. Everything else is either moderate or fading.

XIII. The Bull vs. Bear Debate

The bull case for Semtech rests on several converging tailwinds. LoRa has established itself as the de facto standard for LPWAN outside China, with an installed base of 125 million devices and a global alliance of over 350 members. The IoT market remains in its early innings, with smart cities, precision agriculture, logistics, and asset tracking representing massive addressable markets projected to reach billions of connected devices by 2030. The signal integrity business is riding the AI infrastructure wave, with data center operators pouring hundreds of billions into facilities that need exactly the kind of power-efficient interconnect solutions Semtech sells. Signal integrity revenue grew forty-eight percent in fiscal 2025 and continues to accelerate. The Sierra Wireless integration, while painful, is expanding Semtech's addressable market from silicon-only to full IoT solutions. The balance sheet has been dramatically de-risked, with net leverage falling from 8.8 times to 1.5 times. And the stock, even after its recovery, trades well below its 2021 highs, offering potential for re-rating as execution improves.

The bulls also point to specific near-term catalysts that could accelerate the story.

LoRa Gen 4, launched in late 2025, addresses prior criticisms about LoRa's technical limitations by offering data rates up to 2.6 megabits per second in its FLRC mode, a nearly hundred-fold improvement over the original LoRa specification. It supports multi-band operation including licensed satellite S-band, and is compatible with Amazon Sidewalk, Meshtastic, W-MBUS, and Wi-SUN. This is not incremental improvement; it is a generational leap that significantly expands the range of applications LoRa can address.

Amazon Sidewalk's international expansion, announced in March 2026, could add millions of LoRa access points to the global network. If every Ring doorbell and Amazon Echo becomes a LoRa gateway, the coverage problem that has historically limited LoRa adoption in urban environments could be solved without Semtech or any carrier spending a dollar.

The HieFo acquisition secures a critical supply chain position in Indium Phosphide laser technology for the upcoming 1.6T and 3.2T optical interconnect cycles, the next generation of data center connectivity where Semtech aims to be a dominant supplier.

The bear case is equally well-substantiated, and intellectually honest investors need to wrestle with each point.

IoT has been "five years away" for fifteen years, and adoption consistently runs slower than forecasts. The grand visions of smart cities with every streetlight, manhole cover, and garbage bin connected remain largely unrealized. Cellular technologies, particularly 5G eRedCap arriving in 2026, could commoditize LoRa in key verticals if module costs drop sufficiently.

The Sierra Wireless acquisition destroyed enormous shareholder value through impairments and has not yet proven its strategic worth beyond the initial thesis. The module business is low-margin and commoditizing, with Chinese competitors undercutting on price in ways that Western companies cannot match. ASR Microelectronics and other Chinese LoRa chipset makers are pressuring Semtech's core LoRa margins even in the chip business that was supposed to be the protected high-ground.

Semiconductor cyclicality means unpredictable quarters, and any slowdown in AI infrastructure spending, which is currently the dominant growth driver, could hurt the signal integrity business just as quickly as it accelerated it. The management instability, with three CEOs in fourteen months, raises governance concerns, even though Hou appears to have stabilized the situation. And the convertible notes maturing in 2027 and 2030 represent a potential dilution risk depending on the stock price at conversion.

The bears also note the accounting complexity. The massive goodwill and intangible impairments in fiscal 2024 suggest that the Sierra Wireless deal was done at a significant overpay. Semtech's GAAP earnings remain distorted by acquisition-related charges, and investors must carefully distinguish between reported and adjusted metrics.

The honest assessment lies between these poles. Semtech has successfully built two genuine competitive advantages: LoRa's network effects and signal integrity's power-efficient differentiation. But it also carries the weight of an imperfectly integrated acquisition in a commoditizing market segment, and it faces the constant evolutionary pressure of an industry where today's moat can become tomorrow's irrelevance.

The myth versus reality check is important here. The consensus narrative that "IoT is always five years away" contains a kernel of truth but misses the bigger picture. LoRa connections have grown from near zero in 2015 to 125 million by 2024, a genuine adoption curve, just one that unfolded more slowly than the breathless forecasts of 2016 predicted. Similarly, the narrative that the Sierra Wireless deal was a disaster needs nuance: the impairments were painful, but the strategic assets, customer relationships, cellular module capabilities, and IoT cloud platform, remain intact and are now generating revenue with an improving cost structure. The question is whether these advantages can generate enough growth and cash flow to justify the company's current valuation while the lower-margin module business drags on blended profitability.

XIV. Key Performance Indicators: What to Watch

Strip away the noise of quarterly earnings beats and misses, management commentary, and analyst estimates. For investors tracking Semtech's ongoing performance, three metrics cut through the complexity and tell you what is actually happening at the business level.

First and most important, signal integrity revenue growth rate. This is the single best proxy for Semtech's participation in the AI data center buildout, which represents the company's highest-growth and highest-margin opportunity. Signal integrity grew forty-eight percent in fiscal 2025, and the trajectory of this number over the coming quarters will reveal whether Semtech is gaining or losing share in the race to wire the AI infrastructure. Design wins with hyperscalers, product launches for 1.6T and 3.2T connectivity, and the contribution of the HieFo laser technology acquisition will all flow through this metric.

Second, blended gross margin. This single number captures the evolving mix between the high-margin chip business and the lower-margin module business. The trend from 34.1 percent GAAP in fiscal 2024 to above fifty-two percent in recent quarters tells the story of integration progress and portfolio optimization. A sustained move toward fifty-five percent or higher would signal that the module business is either improving its margins or shrinking as a percentage of revenue, either of which would be positive.

Third, free cash flow generation. After nearly going bust under the weight of Sierra Wireless acquisition debt, Semtech's ability to generate free cash flow is existential. The fifty million in fiscal 2025 was a meaningful inflection, but the company needs to sustain and grow this number to continue deleveraging, fund R&D, and eventually return to a more offensive capital allocation posture. With debt now manageable and interest expense minimal, free cash flow should improve, but the proof will be in the quarterly numbers.

XV. Lessons for Founders, Operators, and Investors

Semtech's sixty-five-year journey is one of the longest continuous narratives in the semiconductor industry. Not many chip companies founded in 1960 are still independent and still relevant in 2026. The lessons embedded in that journey transcend the specifics of analog semiconductors and speak to fundamental questions about strategy, timing, and competitive advantage.

Platform beats product. The single most important decision in Semtech's modern history was not the Cycleo acquisition itself but the choice to open the LoRaWAN protocol and build an ecosystem rather than trying to capture all the value through proprietary licensing. By making LoRaWAN open, Semtech attracted hundreds of partners who collectively built the market for LoRa chips. This is the lesson that many hardware companies struggle to learn: sometimes the best way to capture value from a technology is to give most of it away and own the one piece that everyone needs. Semtech gave away the standard and monetized the silicon.

Open standards can be proprietary in disguise. LoRaWAN is technically an open standard, but every single LoRaWAN device in the world needs a Semtech chip, or at minimum a chip that licenses Semtech's patented CSS technology, to function. This "open on top, proprietary at the bottom" model is one of the most powerful business structures in technology, echoing the Wintel playbook of the 1990s.

The "good enough" trap cuts both ways. LoRa won against cellular LPWAN in many verticals precisely because it was good enough: not the highest data rate, not the best indoor penetration, but cheap, easy to deploy, and with phenomenal battery life. But "good enough" technologies must continuously improve to stay ahead of competitors whose "better" technology keeps getting cheaper. LoRa Gen 4, with its dramatically improved data rates and satellite support, shows Semtech understands this treadmill.

Acquisition timing is everything. The Cycleo deal at five million dollars at the start of the IoT cycle was brilliant. The Sierra Wireless deal at 1.2 billion at the peak of the semiconductor cycle, financed with leverage that pushed the debt ratio to 8.8 times, was reckless, even if the strategic logic was sound. Both deals teach the same lesson from different angles: in cyclical industries, when you buy matters almost as much as what you buy.

Network effects work in B2B, not just consumer. The conventional wisdom associates network effects with consumer platforms like Facebook and Uber. LoRaWAN demonstrates that industrial networks can exhibit equally powerful flywheels.

Each new gateway makes the network more valuable for device makers. Each new device makes it more valuable for operators. And the entire ecosystem becomes stickier over time. This dynamic is often overlooked by investors who focus on consumer tech, but it may be even more durable in B2B contexts because switching costs are higher, sales cycles are longer, and decisions are made by committees rather than individuals.

Semiconductor survival requires differentiation or death. This may be the most important lesson of all.

Semtech's first thirty years as a commodity analog chip maker produced modest returns and multiple near-death experiences. Its transformation into a platform company through LoRa, and a differentiated analog specialist through signal integrity, is a case study in the brutal economics of analog semiconductors. Companies that sell undifferentiated components in cyclical markets are grinding on a treadmill where they run faster and faster to stay in the same place. Companies that build ecosystems or deliver unique performance advantages can command premium valuations and generate the kind of cash flow that lets them invest through downturns rather than merely survive them.

Integration is everything. The difference between a good acquisition and a bad one is rarely in the strategic thesis. Most acquisitions have compelling PowerPoint logic. The difference lies in execution: cultural integration, organizational alignment, speed of synergy capture, and the ability to maintain customer confidence through the transition. Semtech's ongoing Sierra Wireless integration, with its impairments, management turnover, and margin pressure, illustrates how difficult this is in practice.

The China dilemma is universal. Semtech's experience in China, massive market opportunity alongside intense local competition and regulatory complexity, mirrors the challenge facing virtually every Western technology company. China accounts for the majority of global NB-IoT connections and a significant share of LoRa deployments, but local competitors like ASR Microelectronics can undercut on price, and government policy can shift the competitive landscape overnight. The lesson is not to avoid China, which would mean forfeiting the world's largest IoT market, but to build competitive moats that local competitors cannot easily replicate. Semtech's CSS patents and ecosystem orchestration provide some protection, but the moat is not infinitely deep.

XVI. Epilogue: The Road Ahead