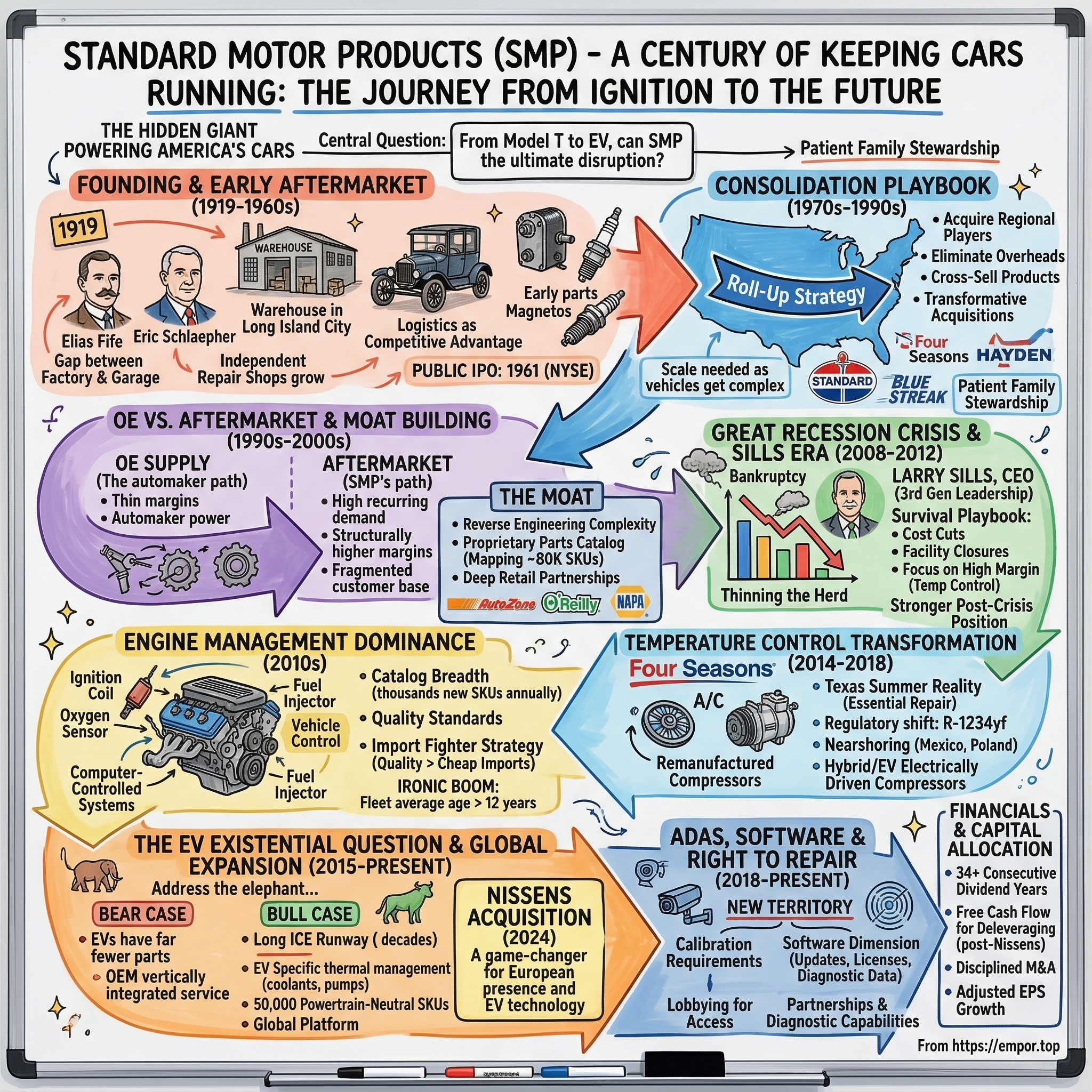

Standard Motor Products: The Hidden Giant Powering America's Cars

I. Introduction & Episode Roadmap

Walk into any AutoZone, O'Reilly, or NAPA store in the United States. Ask the counter guy for an ignition coil, a fuel injector, or an A/C compressor. Chances are strong that the box he hands you—whether it carries a store brand or something called Standard, Blue Streak, or Four Seasons—was manufactured, cataloged, and distributed by a company most investors have never heard of: Standard Motor Products.

SMP, as the industry calls it, is a nearly $1.8 billion revenue business listed on the New York Stock Exchange under the ticker SMP. It has been in continuous operation since 1919—over a century of making the parts that keep America's cars running after they roll off the factory floor. Not the glamorous, headline-grabbing parts. Not the self-driving software or the battery packs. The ignition coils. The oxygen sensors. The A/C compressors. The mundane, essential guts of the automobile that fail after 80,000 miles and need replacing.

Here is the central question: How did a small ignition parts distributor founded in a Long Island City warehouse during the Model T era become the dominant force in automotive aftermarket electronics and temperature control—and can it survive the most disruptive technological shift the automobile has ever faced?

The paradox of Standard Motor Products is that it is simultaneously one of the most boring and one of the most fascinating companies in American industry. Boring because its products are invisible to consumers. Fascinating because the business model is a masterclass in complexity management, customer intimacy, and the quiet art of compounding. SMP manages a catalog of over 80,000 individual part numbers. It serves a vehicle fleet of 285 million cars and trucks on American roads, with an average age now exceeding twelve years. It has survived world wars, oil crises, the Great Recession, a global pandemic, and the semiconductor shortage. And now it faces the existential question that haunts every company built around the internal combustion engine: What happens when the engines disappear?

The answer, as it turns out, is more nuanced and more interesting than the bears think. This is the story of a century-old company trying to reinvent itself in slow motion—and what it teaches about the nature of durable competitive advantage in industries that never make the front page.

II. Founding & The Early Automotive Aftermarket (1919–1960s)

In 1919, the automobile was barely two decades old as a mass consumer product. Henry Ford's Model T had put America on wheels, but those wheels came with a problem nobody had fully anticipated: cars broke down. Constantly. The roads were terrible, the engineering was primitive, and the ignition systems—magnetos, distributors, spark plugs—were the most failure-prone components of all. A car that wouldn't start was, in the language of the era, "dead on the road."

Into this gap stepped Elias Fife and Eric Schlaepher, who founded Standard Motor Products in Long Island City, Queens, in 1919. The original business was straightforward: distribute replacement ignition parts to the growing network of garages and repair shops springing up across the northeastern United States. There was no proprietary technology, no manufacturing. Just a warehouse, a catalog, and a willingness to stock the parts that car owners desperately needed when their vehicles failed.

The timing was prescient. America's automobile fleet was exploding—from roughly 6 million registered vehicles in 1919 to over 23 million by 1930. Every one of those vehicles would eventually need replacement parts, and the original equipment manufacturers—Ford, General Motors, Chrysler—had little interest in the low-margin, high-complexity business of stocking parts for vehicles they had already sold. This gap between the factory and the repair shop was the birthplace of the automotive aftermarket, and Standard Motor Products planted itself squarely in the middle of it.

The post-World War II era supercharged everything. Returning GIs bought cars in record numbers. The interstate highway system, authorized in 1956, put more miles on more vehicles than ever before. Suburbanization meant families needed cars, plural. By the late 1950s, America had over 67 million registered vehicles, and the independent repair shop—the corner garage with the grease-stained mechanic—was a fixture of every town in America. These shops needed a reliable supply of replacement parts, and companies like SMP were their lifeline.

During these decades, SMP expanded beyond ignition parts into electrical components and fuel delivery systems. The product line broadened as vehicles themselves grew more complex. But the core business model remained remarkably consistent: catalog the parts, stock the inventory, deliver reliably to the repair channel. It was logistics as competitive advantage—boring, repetitive, essential.

The company went public in 1961, listing on the New York Stock Exchange. The IPO was not a Silicon Valley spectacle. It was the quiet capitalization of a profitable, growing distribution business that needed scale capital to keep pace with America's automobile fleet. The public listing gave SMP access to equity markets for acquisitions, and it established the governance framework that would carry the company through the next six decades. But the more important development was happening behind the scenes: the Greenwald family, which had become involved in the company's management, was beginning to exert the kind of patient, multi-generational influence that would prove to be one of SMP's most distinctive characteristics.

For investors, the early history of SMP is less about specific milestones and more about the establishment of a business model that has proven remarkably durable. The automotive aftermarket exists because of a fundamental economic reality: cars are expensive, cars break down, and people would rather repair them than replace them. That dynamic is as true in 2026 as it was in 1919. The question is whether the parts that break down will remain the ones SMP knows how to make.

III. The Consolidation Playbook: Building Through Acquisition (1970s–1990s)

Picture the American automotive aftermarket in 1975: thousands of small, regional parts manufacturers and distributors, each specializing in a narrow slice of the market. One company made ignition rotors. Another made heater cores. A third distributed fuel pumps across three midwestern states. The industry was a patchwork quilt of tiny players, none with the scale to invest in modern manufacturing, sophisticated cataloging, or national distribution.

SMP looked at this fragmented landscape and saw an opportunity that private equity firms would not discover for another two decades: the classic roll-up. The logic was irresistible. Each small acquisition brought a product line, a customer base, and usually some manufacturing capability. By combining these under one roof, SMP could eliminate redundant overhead, cross-sell products to existing customers, and amortize the growing cost of parts cataloging—the increasingly complex work of matching aftermarket parts to the right vehicle applications—across a larger revenue base.

The acquisitions that defined this era were transformative. The Blue Streak brand, which SMP acquired and built into its premium professional-grade line, became the company's quality flagship. Professional technicians consistently rated Blue Streak as the top aftermarket brand—a critical distinction in an industry where the mechanic, not the car owner, decides which replacement part goes into the vehicle. The Hayden acquisition added cooling products. And the crown jewel of the period was Four Seasons, which made SMP the dominant player in mobile climate control—A/C compressors, condensers, evaporators, and the full ecosystem of components that keep car interiors comfortable.

The geographic expansion followed the acquisitions. From its northeastern roots, SMP built distribution capability across the entire United States. Each acquisition brought regional relationships and local market knowledge that would have taken years to develop organically. By the 1990s, SMP had evolved from a New York-based ignition parts distributor into a national manufacturer and distributor with the broadest product portfolio in aftermarket engine management and temperature control.

What made the aftermarket uniquely suited to consolidation was the complexity barrier. As vehicles grew more sophisticated through the 1970s, 1980s, and 1990s—adding electronic ignition, fuel injection, computerized engine management, and emissions controls—the number of distinct part numbers required to serve the vehicle fleet exploded. A small manufacturer might be able to reverse-engineer and produce ignition coils for Chevrolets. But covering Chevrolets, Fords, Chryslers, Toyotas, Hondas, BMWs, and the dozens of other makes on American roads required a scale of engineering and cataloging investment that most small players simply could not afford. Consolidation was not just attractive; it was necessary for survival.

Throughout this period, the Greenwald family maintained its influence on SMP's management and strategic direction. The family's approach was distinctly old-school: patient capital, reinvestment in the business, careful stewardship rather than financial engineering. While other industries were being reshaped by leveraged buyouts and hostile takeovers, SMP quietly compounded. The family's long-term orientation meant that acquisitions were evaluated not just for near-term earnings accretion but for strategic fit and integration feasibility—a discipline that would serve the company well in the decades ahead.

The roll-up strategy accomplished something that is easy to describe but difficult to execute: it made SMP the default supplier for an increasingly complex product category. When a parts store needed to stock engine management components, SMP could supply everything from ignition coils to oxygen sensors to fuel injectors, all backed by a single catalog system and a single logistics relationship. The one-stop-shop advantage, once established, proved remarkably sticky.

IV. The OE vs. Aftermarket Split & Business Model Evolution (1990s–2000s)

To understand SMP's business model, one must first understand a distinction that is invisible to most consumers but absolutely fundamental to the auto parts industry: the difference between Original Equipment (OE) and aftermarket.

When Toyota assembles a Camry on the factory floor, every component—from the engine computer to the fuel injector to the A/C compressor—is an Original Equipment part, manufactured to Toyota's proprietary specifications by Toyota's designated suppliers. These OE suppliers (companies like Denso, Bosch, Continental) operate under long-term contracts with the automakers, producing parts in enormous volumes at thin margins. The relationship is lucrative in aggregate but brutal on a per-unit basis: the automaker holds all the negotiating power, demands annual price reductions, and can switch suppliers if a competitor offers a better deal.

The aftermarket is a fundamentally different business. When that Camry's fuel injector fails at 120,000 miles, the car owner takes it to a repair shop. The mechanic orders a replacement part—not from Toyota, but from an aftermarket supplier like SMP. The aftermarket part is designed to be functionally identical to the OE part—same fit, same performance, same specifications—but it is manufactured independently, often through a process of reverse engineering the OE design.

SMP made the strategic choice to focus primarily on the aftermarket, and the economics explain why. Aftermarket margins are structurally higher because the customer base is fragmented (thousands of repair shops and parts stores rather than a handful of automakers), the pricing dynamics are more favorable (repair shops buy on availability and quality, not just price), and the demand is inherently recurring (every car on the road will eventually need replacement parts). SMP's consolidated gross margins have historically run in the 28-30% range—not eye-popping by software standards, but excellent for a manufacturing business and meaningfully above what OE supply contracts typically deliver.

The 1990s and 2000s brought a technological revolution that played directly to SMP's strengths. Vehicles became dramatically more complex. The carburetor gave way to fuel injection—think of it as the difference between a mechanical faucet and a computer-controlled precision spray system. Emissions regulations tightened, adding catalytic converters, oxygen sensors, and exhaust gas recirculation systems. Engine management went electronic, with onboard computers (called ECUs, or Electronic Control Units) replacing mechanical systems. Each of these advances multiplied the number of distinct electronic components in a vehicle and, consequently, the number of aftermarket replacement parts needed to service the fleet.

This complexity explosion was SMP's moat under construction. Reverse-engineering an OE part is not trivial. An engineer must obtain the original part, analyze its design and materials, develop manufacturing specifications, build tooling, produce prototypes, test them for fit and function, and then catalog the part against every vehicle application where it is used. Multiply that process by tens of thousands of part numbers across hundreds of vehicle platforms spanning two decades of production, and the scale of the challenge becomes clear. This is not a business where a new competitor can show up with a factory and a price list.

SMP built what may be its most underappreciated competitive asset during this period: its proprietary parts catalog database. This database maps every aftermarket part number to every vehicle application where it fits—a matrix of staggering complexity that requires continuous investment to maintain and update. When a parts store counter person types in a vehicle's year, make, model, and engine, the catalog system tells them exactly which SMP part number they need. Accuracy matters enormously: an incorrect part wastes the mechanic's time, damages the repair shop's reputation, and can cost SMP the account. The catalog is, in effect, the connective tissue between SMP's manufacturing and the end customer—and it represents decades of accumulated knowledge that cannot be easily replicated.

By the mid-2000s, SMP had cemented its relationships with the channel masters: AutoZone, O'Reilly Auto Parts, and NAPA (owned by Genuine Parts Company). These three retailers, plus Advance Auto Parts, controlled the vast majority of aftermarket parts distribution in the United States. The relationships were symbiotic but unequal—SMP's top three customers accounted for roughly 61% of revenue, a concentration that creates both stability (deep, multi-decade partnerships) and risk (losing any single account would be devastating). O'Reilly named SMP its 2020 Supplier of the Year, a distinction that reflects the depth of these partnerships—but also the dependency.

V. The Great Recession Crisis & The Larry Sills Era (2008–2012)

In September 2008, Lehman Brothers collapsed. General Motors and Chrysler teetered toward bankruptcy. The American automobile industry—both manufacturing and aftermarket—entered a crisis that threatened to destroy companies that had survived every previous disruption for nearly a century.

SMP was not immune. Revenue cratered as consumers stopped spending on everything, including car repairs. Credit markets froze, making it difficult to finance inventory—the lifeblood of a parts distribution business. The company's stock price plunged to roughly $2 per share, a level that implied the market was pricing in a meaningful probability of bankruptcy. Covenant violations on the company's credit facilities added technical urgency to the existential crisis.

It was into this maelstrom that Larry Sills stepped up as CEO in 2008. Sills represented the third generation of family leadership at SMP—a connection to the Greenwald family that had stewarded the company for decades. But Sills was no figurehead inheriting a comfortable sinecure. He took over a company that was, by several measures, fighting for its life.

The survival playbook Sills executed was textbook crisis management, but the discipline and speed of execution were notable. Facility closures, workforce reductions, and cost cuts hit fast and deep. Non-core operations were rationalized. Working capital was squeezed. The company focused its limited resources on the product categories where it held the strongest competitive positions and the best margin profiles.

But Sills did something more interesting than just cut costs. He recognized that the crisis, while terrifying, was also thinning the competitive herd. Weaker aftermarket suppliers—the small, undercapitalized players that had survived in the fragmented pre-crisis landscape—were going under. OE suppliers, reeling from the collapse in new vehicle production, were retreating from the aftermarket to focus on their core factory-supply business. In the wreckage of the worst economic crisis since the Great Depression, SMP had an opportunity to emerge stronger—if it could survive.

The strategic pivot during this period included doubling down on the Temperature Control segment, particularly A/C compressors. Air conditioning repair is one of the highest-dollar services in a repair shop—a compressor replacement can cost the vehicle owner $800 to $1,500—and the parts carry attractive margins for both the supplier and the installer. Sills recognized that climate control was a growth category where SMP's Four Seasons brand already held a strong position, and he allocated resources to strengthen it further even as other parts of the business were being cut.

The recovery, when it came, was swift and dramatic. From the $2 stock price nadir, SMP's shares began a multi-year ascent as the company demonstrated both operational excellence and strategic foresight. Revenue stabilized and then grew. Margins improved as the cost cuts took hold and the competitive landscape thinned. By 2012, the company had not just survived the Great Recession—it had used it as a springboard to a stronger competitive position.

The Sills era established a management template that persists at SMP: family-influenced leadership with a bias toward operational discipline, strategic patience, and the willingness to make tough short-term decisions in service of long-term positioning. The Great Recession was SMP's near-death experience, and the lessons learned—about the importance of balance sheet strength, the danger of overextension, and the opportunity embedded in industry crises—shaped every subsequent strategic decision.

For investors, the 2008-2012 period is the crucial stress test in SMP's history. The company proved that its business model was resilient enough to survive a genuine financial crisis, and that its management was capable of the hard decisions required to navigate one. The aftermarket's counter-cyclical characteristics—people repair cars when they cannot afford to buy new ones—provided a natural floor that pure OE suppliers did not have. That structural advantage became the foundation of the bull case for the next decade.

VI. The Engine Management Dominance Strategy (2010s)

To understand why SMP's Engine Management business—now rebranded as Vehicle Control—is so defensible, consider what it actually involves. Think of a modern car's engine as a symphony orchestra. The ignition system provides the spark (the percussion section). The fuel injection system delivers precisely metered fuel (the woodwinds). The emissions system monitors and cleans exhaust gases (the brass section keeping everything in compliance). And the engine control unit—a sophisticated computer—serves as the conductor, coordinating everything dozens of times per second based on inputs from sensors measuring temperature, pressure, airflow, and oxygen levels.

When any component in this orchestra fails, the car either runs poorly or does not run at all. And every one of those components—from the ignition coil to the mass airflow sensor to the oxygen sensor to the fuel injector—is an aftermarket replacement opportunity for SMP.

The 2010s were the decade when SMP consolidated its dominance in this category. The company's strategy rested on several interlocking pillars. First, catalog breadth. SMP expanded its part number coverage relentlessly, releasing thousands of new part numbers annually. In 2024 alone, the company released 2,367 new part numbers—a pace that reflects both the growing complexity of the vehicle fleet and SMP's commitment to covering it comprehensively. The Standard brand's gasoline fuel injection program alone encompasses over 2,100 part numbers covering direct injection, multi-port injection, and throttle body injection systems.

Second, quality improvement. The aftermarket has always fought a perception problem: mechanics and car owners often assume that aftermarket parts are inferior to the OE originals. SMP invested heavily in closing this quality gap, applying OE-grade manufacturing standards, materials, and testing to its aftermarket parts. The Blue Streak brand was positioned explicitly as a premium professional-grade line, and the company's engineering labs—including a 20,000-square-foot test facility—enabled rigorous validation against OE specifications.

Third, what might be called the "import fighter" strategy. Through the 2010s, a growing flood of cheap Chinese-manufactured aftermarket parts entered the U.S. market. These imports often carried attractive price points but inconsistent quality—fitment issues, premature failures, and reliability problems that eroded trust with mechanics. SMP positioned itself as the quality alternative: yes, more expensive than the cheapest Chinese import, but reliable, accurately cataloged, and backed by professional support. This positioning proved effective. Mechanics who had been burned by a no-name Chinese oxygen sensor that failed after 5,000 miles were willing to pay more for a Standard or Blue Streak part they could trust.

Fourth, the proprietary catalog and data systems. The sheer complexity of mapping tens of thousands of part numbers across decades of vehicle platforms, with their different engines, trim levels, and regional variations, created a data management challenge that was itself a competitive moat. SMP's proprietary databases represent decades of accumulated fitment knowledge—information about which parts fit which vehicles, which superseded part numbers replace which discontinued ones, and which technical specifications apply to which applications. This is not the kind of asset that shows up on a balance sheet, but it is arguably one of the most valuable things SMP owns.

By the middle of the decade, SMP had achieved a market-leading position in aftermarket engine management. The company does not publicly disclose exact market share figures, but industry analyses consistently placed SMP as the number one or number two independent manufacturer in the category. The combination of catalog breadth, quality reputation, and entrenched distribution relationships created a position that proved remarkably difficult for competitors to challenge.

The strategic acquisitions continued throughout the decade, filling portfolio gaps and eliminating smaller competitors. Each acquisition followed the same playbook established in the 1970s: buy the product line, integrate the manufacturing, add the part numbers to the catalog, and cross-sell through the existing distribution network. The compounding effect of this strategy—more parts, more coverage, more reasons for a parts store to consolidate its purchasing with SMP—was powerful and self-reinforcing.

The irony of SMP's engine management dominance is that it was built on a product category that many analysts believe is in secular decline. Internal combustion engines, after all, are supposed to be going away. But the vehicle fleet on American roads tells a different story: the average age of vehicles in operation continues to climb, exceeding twelve years for the first time. Older vehicles need more replacement parts. And the 285 million ICE and hybrid vehicles currently registered in the United States will not be replaced overnight, even in the most aggressive EV adoption scenarios. SMP's engine management business has a runway measured in decades, not years.

VII. Temperature Control: The Four Seasons Transformation (2014–2018)

In the middle of a Texas summer, when the dashboard thermometer reads 108 degrees and the A/C system starts blowing warm air, the car owner does not care about automotive aftermarket industry dynamics. They care about one thing: getting cold air back. And they will pay whatever it costs.

This simple human reality underpins the economics of SMP's Temperature Control segment. Air conditioning and cooling system repairs are among the highest-dollar services in any repair shop. A compressor replacement—the most common major A/C repair—typically runs between $800 and $1,500 installed. The parts themselves carry healthy margins, and the complexity of modern automotive climate systems means that DIY repair is impractical for most vehicle owners. This is a "Do It For Me" category, driven to the professional installer channel where SMP's brands carry the most weight.

The 2014-2018 period marked a decisive transformation in SMP's temperature control business. The company undertook a comprehensive integration and operational improvement program centered on the Four Seasons brand, which had become the largest aftermarket mobile climate control parts supplier—and the largest compressor remanufacturer—in the world. Remanufacturing is an important distinction: rather than building new compressors from raw materials, SMP takes in used compressor cores, disassembles them, replaces worn components, reassembles them to OE specifications, and ships them as remanufactured units. The process is environmentally beneficial, capital efficient, and produces parts that perform comparably to new units at a lower cost.

The technical evolution during this period created a regulatory-driven tailwind. The automotive industry was transitioning from R-134a refrigerant to R-1234yf, a newer refrigerant with a dramatically lower global warming potential. This transition, mandated by environmental regulations in both the United States and Europe, meant that new vehicle models required redesigned A/C systems—and, eventually, that the aftermarket would need to supply replacement parts for these new systems. For SMP, this was a product development opportunity: each new refrigerant generation requires new compressors, condensers, hoses, and other components, all of which need to be reverse-engineered, manufactured, cataloged, and distributed.

Perhaps more importantly, the transition to hybrid and electric vehicles created a new growth vector within temperature control. A traditional ICE vehicle uses a belt-driven compressor powered by the engine. A hybrid or EV uses an electrically driven compressor—a fundamentally different part with different engineering requirements. But the need for climate control is identical: every vehicle needs A/C, regardless of its powertrain. SMP recognized early that thermal management would be a critical bridge between the ICE and EV worlds, and it invested accordingly.

The manufacturing footprint decisions during this period were strategically significant. SMP expanded production in Poland and Mexico—nearshoring manufacturing capacity to serve both the North American and European markets while managing labor costs. The Poland facility, a 145,000-square-foot operation in Bialystok, provided engineering and manufacturing capability for both aftermarket and OE products. The Mexican facilities in Reynosa handled labor-intensive assembly operations. This diversified manufacturing footprint—roughly 70% North American—positioned SMP ahead of the nearshoring trend that would accelerate dramatically after the pandemic and the U.S.-China trade tensions.

Competing in temperature control meant going up against global industrial giants: Denso (the massive Japanese supplier that is also Toyota's OE A/C supplier), Valeo (the French automotive technology company), and other multinational manufacturers. SMP competed not on scale against these behemoths but on aftermarket specialization—the ability to cover a broader range of vehicle applications, deliver faster to the repair channel, and provide the catalog accuracy and technical support that independent mechanics required.

By the end of this period, SMP had established Four Seasons as the undisputed category leader in aftermarket temperature control, with a dominant market position in North America. The segment contributed roughly a quarter of the company's total revenue, with margins that were improving as integration efficiencies took hold and the product mix shifted toward higher-value components.

VIII. The EV Existential Question (2015–Present)

Let's address the elephant in the room directly: Standard Motor Products built its business on the internal combustion engine. The ignition coils, fuel injectors, oxygen sensors, and exhaust components that compose the heart of the Vehicle Control segment exist because engines burn gasoline. Electric vehicles do not burn gasoline. They do not have ignition systems, fuel injection, or exhaust. The most obvious reading of the EV transition is that it represents an existential threat to SMP's core business.

This is the bear case, and it deserves to be taken seriously. A fully electric vehicle has dramatically fewer mechanical parts than an ICE vehicle—some estimates suggest 60-70% fewer moving components. Fewer parts means fewer things that can break, which means fewer replacement parts needed, which means a shrinking addressable market for aftermarket suppliers. Add Tesla's vertically integrated service model—which deliberately restricts third-party access to parts and diagnostic information—and the threat crystallizes: not just fewer parts, but potentially locked-out access to the parts that remain.

But the bull case is more nuanced than the bears acknowledge, and SMP's management has articulated it consistently. Start with the timing. Even under aggressive EV adoption scenarios, the ICE vehicle fleet will dominate American roads for decades. With 285 million ICE and hybrid vehicles registered in the U.S. and new ICE vehicles still being sold in significant numbers, the installed base is not going away quickly. These vehicles will age, their parts will wear out, and they will need aftermarket replacements. SMP's core business has a long tail that extends well into the 2040s.

Then consider what EVs actually need. While they eliminate engine-related components, they introduce new ones—and many of those fall squarely within SMP's existing competencies. EV battery packs require sophisticated thermal management systems to maintain optimal operating temperature. Think of it like this: a lithium-ion battery pack is like a very large, very expensive laptop battery. It performs best within a narrow temperature range (roughly 68-86 degrees Fahrenheit), and both excessive heat and excessive cold degrade its performance and lifespan. Managing that temperature requires cooling loops, electric water pumps, heat exchangers, and sophisticated control systems—all of which are variations on the thermal management technology SMP already makes through Four Seasons.

Beyond thermal management, EVs use the same sensors, switches, and electronic components as ICE vehicles for everything unrelated to the powertrain. Brake position sensors, ABS wheel speed sensors, power window switches, HVAC blower motors, park assist cameras—none of these care whether the vehicle is powered by gasoline or electricity. SMP currently offers over 50,000 "powertrain-neutral" part numbers that fit vehicles regardless of their propulsion system. Additionally, the company has developed over 1,900 parts specifically for fully electric vehicles covering more than 40 models, and over 4,000 parts for hybrids covering more than 150 models.

SMP's strategic response to the EV transition has centered on three pillars. First, expanding the powertrain-neutral product portfolio—particularly ADAS components like park assist cameras and sensors, which represent growing repair demand as equipped vehicles age into the aftermarket. Second, investing in EV-specific thermal management capabilities, leveraging the Four Seasons platform and the transformational Nissens acquisition. Third, maintaining and strengthening the core ICE business to maximize cash flows during the long transition period.

The Nissens acquisition, completed in November 2024 for approximately $390 million (360 million euros), was the most significant strategic move in this direction. Nissens, a Danish company with a century of its own history, is a leading European aftermarket thermal management manufacturer. The acquisition gave SMP a major European presence for the first time, doubled down on thermal management as a core competency, and brought capabilities in next-generation cooling technologies—including electric water pumps explicitly targeting EV thermal systems. With Nissens contributing $305 million in revenue during its first full year within SMP, and generating adjusted EBITDA margins near 16%, the deal transformed SMP from a primarily North American player into a global aftermarket platform.

The honest assessment is that the EV transition represents both a genuine long-term threat and a genuine near-term non-event for SMP. The threat is real because ICE-specific parts content will eventually decline as the fleet electrifies. The non-event is real because that decline will unfold over decades, during which SMP's thermal management, sensor, and electronic component businesses can grow to offset the ICE declines. The key variable is the rate of transition—and that rate has proven slower and less linear than the most aggressive forecasts of 2020-2022 suggested.

IX. The ADAS, Connected Car & Software Challenge (2018–Present)

Modern vehicles are not just machines—they are rolling computer networks. The average new car sold today contains more lines of software code than a fighter jet. Advanced Driver Assistance Systems, or ADAS, represent the most visible manifestation of this transformation: adaptive cruise control, lane departure warning, automatic emergency braking, blind spot monitoring, and park assist systems all rely on arrays of cameras, radar units, ultrasonic sensors, and the electronic control modules that process their data.

For the aftermarket, ADAS creates both a challenge and an opportunity. The challenge is access. Many ADAS components require calibration after replacement—meaning that when a radar sensor or camera is installed, it must be precisely aligned and programmed using manufacturer-specific diagnostic tools. This calibration requirement creates a technical barrier that threatens to lock independent repair shops out of an increasingly large portion of vehicle service work. If only the dealer has the software tools needed to calibrate a replacement camera, then the aftermarket for that camera is effectively closed.

SMP has entered the ADAS aftermarket through its traditional strength: parts. The company has aggressively expanded its offerings in park assist cameras (adding 53 new SKUs recently), park assist sensors (76 new SKUs), and related electronic components. These are high-value, technically complex parts that play directly to SMP's reverse-engineering capabilities and its catalog management expertise.

But the software dimension represents genuinely new territory for SMP. When a vehicle is a "computer on wheels," the traditional aftermarket model—physical parts that bolt on and work—begins to break down. Over-the-air software updates can change vehicle behavior without any physical intervention. Subscription-based features (heated seats, advanced navigation, performance modes) create a model where vehicle capabilities are determined by software licenses rather than hardware. And the diagnostic data generated by modern vehicles—the real-time stream of sensor readings, fault codes, and performance metrics—represents a potential competitive asset for whoever can capture and interpret it.

The right-to-repair movement has become the political battleground where these dynamics play out. SMP, along with the broader aftermarket industry, has lobbied aggressively for legislation ensuring that independent repair shops and aftermarket parts suppliers retain access to the vehicle data and diagnostic tools needed to service modern vehicles. The Auto Care Association and MEMA (Motor & Equipment Manufacturers Association), of which SMP is a prominent member, have advocated for the Data Access and Right to Repair Act at the federal level. Massachusetts passed its own right-to-repair law in 2020, though implementation has been contested in court.

This is not a hypothetical concern. If automakers succeed in locking down diagnostic access and parts interchangeability, the entire aftermarket industry—and SMP's business model with it—faces a structural threat far more immediate than the EV transition. The right-to-repair outcome is, in some ways, more important to SMP's future than the pace of EV adoption.

SMP has responded by building partnerships and investing in diagnostic capabilities. The company's approach has been characteristically pragmatic: rather than trying to become a software company, it has focused on integrating electronic components and diagnostic compatibility into its parts portfolio. A replacement sensor that comes pre-programmed with the correct calibration parameters eliminates the need for separate calibration equipment—and that kind of embedded intelligence represents the future of aftermarket parts for ADAS-equipped vehicles.

The connected car challenge is fundamentally about whether SMP can evolve from a company that makes physical things into a company that integrates physical things with software intelligence. The jury remains out, but the track record of adapting to previous technological transitions—from carburetors to fuel injection, from mechanical ignition to electronic, from analog controls to digital—suggests that declaring SMP incapable of adaptation would be premature.

X. Supply Chain, Manufacturing, & The Pandemic Era (2020–2023)

In March 2020, when COVID-19 shutdowns emptied American roads, the automotive aftermarket faced an immediate demand collapse. If nobody was driving, nobody was wearing out parts. SMP's revenue dropped sharply in the second quarter of 2020 as repair shops closed or operated at reduced capacity and consumers postponed maintenance.

What happened next surprised almost everyone in the industry. As the economy partially reopened, a surge in DIY repair activity materialized. Stuck at home with time on their hands and stimulus checks in their bank accounts, Americans turned to projects—including the cars sitting in their driveways. YouTube tutorials on replacing brake pads, spark plugs, and A/C components saw viewership spikes. DIY repair parts sales surged through AutoZone and O'Reilly, and SMP's revenue recovered faster than most analysts had projected.

The more lasting impact of the pandemic era came from the supply chain disruptions that followed. The global semiconductor shortage, which began in late 2020 and persisted through 2022, created cascading effects throughout the automotive ecosystem. New vehicle production was curtailed—automakers simply could not get enough chips to build cars. This had a paradoxical benefit for the aftermarket: with new cars scarce and used car prices soaring, consumers held onto their existing vehicles longer, driving increased demand for replacement parts.

SMP's supply chain strategy during this period reflected decades of operational learning. The company had already been diversifying its manufacturing footprint away from exclusive China dependence, with roughly 70% of production occurring in North American facilities. The four manufacturing plants in Reynosa, Mexico, the engineering and manufacturing facility in Bialystok, Poland, and the domestic operations in Greenville (South Carolina), Independence (Kansas), and other U.S. locations provided geographic diversification that pure importers lacked.

The logistics advantage proved equally important. SMP's distribution network—which was in the process of a significant expansion, including the new 575,000-square-foot national distribution center in Shawnee, Kansas, which opened in 2025—enabled three-day order fulfillment nationwide and the ability to process thousands of emergency orders daily. In an industry where a parts store's value proposition is getting the right part on the shelf quickly, SMP's distribution reliability translated directly into competitive advantage.

The pricing power that emerged during the inflationary period of 2021-2022 was a revelation for investors. SMP successfully passed through raw material and freight cost increases to its customers—the parts retailers who, in turn, passed them through to consumers. This was not a given: in many manufacturing businesses, customer concentration translates to pricing power for the buyer, not the seller. But SMP's catalog breadth and the essential nature of its products gave it enough leverage to maintain and even slightly expand margins during a period of significant cost inflation. Temperature Control gross margins improved from 28.4% in 2023 to approximately 31% in 2024—a meaningful expansion driven by both pricing and operational efficiency.

The "drive cycle" tailwind that emerged from the pandemic era continued to benefit SMP into 2025 and 2026. The average age of vehicles on U.S. roads continued to climb. Economic pressure on consumers—higher interest rates, elevated new car prices—kept older vehicles on the road longer. Every year that a vehicle stays in service beyond its warranty period represents another year of aftermarket parts demand. This dynamic is the fundamental economic engine of SMP's business, and the pandemic era reinforced it dramatically.

Working capital management became a competitive weapon during this period. SMP's ability to maintain adequate inventory levels when competitors were struggling with supply disruptions meant that parts stores could rely on SMP to have the part in stock when they needed it. Inventory is not glamorous, but in the aftermarket parts business, having the right part available at the right time is the single most important competitive differentiator. SMP's disciplined approach to inventory management—stocking deeply in high-velocity SKUs while managing the long tail of slower-moving parts—was a tangible expression of the operational excellence that Sills had built during the post-recession recovery.

XI. Capital Allocation & Shareholder Returns (2000s–Present)

In a world obsessed with high-growth technology stocks, SMP's capital allocation story reads like a manual from a different era—and that is precisely the point. The company has paid dividends for over 34 consecutive years, a streak that spans the dot-com bust, the Great Recession, the pandemic, and every other crisis in between. The current annual dividend stands at $1.24 per share (quarterly payments of $0.31), representing a yield in the 3-4% range depending on the stock price. The payout ratio on adjusted earnings of $4.02 per share sits at approximately 31%—comfortably sustainable and leaving ample room for reinvestment.

The dividend is more than a financial return; it is a signal. When a company pays a dividend through a crisis—as SMP did during 2008-2009 and again during 2020—it tells the market that management is confident in the durability of cash flows. For a family-influenced company where the Greenwald family remains significant shareholders, the dividend also represents a tangible alignment of interests: family members receive their share of the same dividend that public shareholders receive, creating a natural incentive to maintain and grow it.

Share buybacks have historically complemented the dividend, with SMP executing opportunistic repurchase programs when management believed the stock was undervalued. However, buybacks were paused following the Nissens acquisition in late 2024 as management prioritized debt reduction. The company ended 2024 at approximately 3.7 times leverage following the $390 million acquisition, and management publicly committed to reducing leverage below 2.0 times by the end of 2026. This deleveraging priority is sensible—SMP's business generates the free cash flow to support rapid debt paydown, and restoring balance sheet flexibility positions the company for future acquisitions and capital return.

The M&A discipline deserves particular attention. SMP's acquisition track record over five decades demonstrates a consistent framework: buy product lines that fill gaps in the catalog, integrate them into existing manufacturing and distribution, and cross-sell to existing customers. The Nissens acquisition represented a step-change in scale—at $390 million, it was by far the largest deal in company history—but it followed the same strategic logic that guided the Blue Streak, Four Seasons, and Pollak acquisitions that preceded it. Integration execution has historically been a strength: SMP's operational playbook for absorbing acquired businesses is well-practiced, and the Nissens integration appears to be proceeding ahead of expectations, with the European business contributing $305 million in revenue and approximately 16% adjusted EBITDA margins in its first full year.

The "compounder" thesis for SMP rests on the combination of a steady dividend, modest organic growth (low-to-mid single digits), margin expansion through operational improvement and mix shift, and periodic acquisitions that add revenue and capabilities. This is not a double-your-money-in-twelve-months story. It is a compound-at-ten-percent-for-twenty-years story—the kind of returns that look modest on any given quarterly earnings call but prove powerful over a full market cycle.

Total shareholder returns relative to the broader market have been mixed over various periods, reflecting the market's ambivalence about a company caught between a durable present and an uncertain future. Adjusted earnings per share grew 27% in fiscal 2025 to $4.02, driven by Nissens accretion and organic margin improvement—a strong showing that demonstrated the earnings power of the expanded platform. But the stock's valuation—typically trading in the 12-15 times earnings range—reflects the market's discounting of long-term EV transition risk. Whether that discount represents opportunity or appropriate caution is the central question for any investor evaluating SMP.

XII. Competitive Landscape & Industry Dynamics

The automotive aftermarket is a business where everyone knows everyone, relationships span decades, and competitive dynamics play out not in dramatic confrontations but in the slow, grinding accumulation of catalog coverage, distribution reliability, and customer trust. SMP's competitive landscape is best understood through concentric circles of competition—from direct rivals to adjacent players to disruptive newcomers.

The closest pure-play competitor is Dorman Products. Dorman generated approximately $2.13 billion in revenue in fiscal 2025—larger than SMP in top-line terms—and competes in overlapping but not identical categories. Dorman's strategic emphasis has been on "new-to-aftermarket" parts: components that were previously available only from the vehicle dealer because no aftermarket equivalent existed. This strategy targets a different economic proposition than SMP's—Dorman is creating new market segments rather than competing for share in existing ones—but the two companies increasingly bump up against each other in electronic and electrical categories. Dorman typically earns higher operating margins (14-16% range) than SMP, reflecting its differentiated positioning and lower customer concentration.

Genuine Parts Company, the owner of NAPA Auto Parts, represents a different kind of competitive dynamic. GPC is SMP's customer, not a direct manufacturing competitor—NAPA stores are among SMP's largest distribution channels. But GPC is also vertically integrated to a degree, sourcing some products under its own brand names and maintaining relationships with multiple suppliers. The relationship is collaborative and competitive simultaneously—SMP needs NAPA's distribution, but NAPA could, in theory, shift volume to alternative suppliers.

LKQ Corporation, with approximately $14 billion in revenue, operates primarily in the recycled and remanufactured parts space. LKQ's focus on collision repair parts and its extensive European presence make it a less direct competitor to SMP's engine management and temperature control businesses, but the two companies compete for wallet share within the broader independent repair channel.

Private equity has been an increasingly active force in the aftermarket, executing roll-up strategies similar to what SMP pioneered decades ago. PE-backed platforms acquire regional distributors and specialty manufacturers, consolidating them into larger operations with improved procurement leverage and operational efficiency. For SMP, PE competition is a double-edged sword: it validates the attractiveness of the aftermarket business model, but it also creates larger, better-capitalized competitors in categories where SMP might otherwise face fragmented opposition.

The retail channel dynamics deserve careful analysis. AutoZone, O'Reilly, and Advance Auto Parts (which includes Carquest) are not just SMP's customers—they are the gatekeepers to the end market. These retailers own the customer relationship, control shelf space, and have the data to understand what sells and what does not. The concentration of roughly 61% of SMP's revenue among its top three customers creates a structural tension: SMP's catalog breadth and quality make it a preferred supplier, but the retailers' purchasing power gives them leverage on pricing and terms.

The DIY versus DIFM (Do-It-For-Me) trend is shifting in SMP's favor. As vehicles grow more complex, fewer consumers attempt their own repairs. The professional installer—the mechanic at the independent repair shop—is becoming the dominant buyer of aftermarket parts. Professional installers care more about quality, reliability, and catalog accuracy than about price, which aligns with SMP's strengths. The professional channel is also where SMP's Blue Streak and Standard brands carry the most recognition and credibility.

E-commerce represents both opportunity and threat. Amazon and online-only retailers like RockAuto have made aftermarket parts accessible to a broader consumer base, but they have not fundamentally disrupted the professional installer channel. A mechanic does not order parts from Amazon and wait two days—the mechanic calls the local parts store and expects delivery within an hour. SMP's distribution network and its relationships with brick-and-mortar retailers protect it from e-commerce disruption in the professional channel, though the DIY segment is more exposed.

XIII. Analytical Framework: Porter's 5 Forces & Hamilton's 7 Powers

Understanding SMP's competitive position requires moving beyond descriptive analysis to a structured assessment of the forces that shape industry profitability and the sources of durable competitive advantage.

Starting with Michael Porter's framework, competitive rivalry in the aftermarket parts manufacturing space runs medium-high. The market is consolidated at the top—SMP, Dorman, and a handful of other significant players—but remains competitive on price, catalog coverage, and service levels. The saving grace for industry profitability is product differentiation: aftermarket parts are not commodities. Quality differences, catalog accuracy, and delivery reliability create meaningful differentiation that prevents pure price competition from erasing margins entirely.

Supplier power is moderate. SMP sources materials and components globally, with manufacturing operations spanning the United States, Mexico, Poland, and Denmark, along with sourcing offices in Hong Kong and Taiwan. This geographic diversity provides alternatives when any single source becomes problematic—a resilience that proved valuable during the pandemic-era supply disruptions. However, for specialized inputs and proprietary components, switching costs can be significant.

Buyer power is the most concerning force. SMP's top three customers—O'Reilly (approximately 28% of revenue), AutoZone (approximately 19%), and NAPA (approximately 14%)—collectively represent about 61% of sales. This concentration gives the retailers meaningful leverage on pricing and terms. The mitigating factor is mutual dependency: these retailers need SMP's catalog breadth and quality as much as SMP needs their distribution reach. Losing SMP as a supplier would create coverage gaps that no single alternative could fill. But the power imbalance is real and represents a structural constraint on margin expansion.

The threat of new entrants is low to medium. The barriers are formidable: the capital required to build manufacturing capacity, the engineering investment needed to reverse-engineer and catalog tens of thousands of parts, and the time required to build distribution relationships all protect incumbents. Chinese manufacturers represent the most credible competitive threat, offering lower-cost alternatives. But quality inconsistency, longer lead times, and the difficulty of managing complex catalogs from overseas have limited their penetration in the professional installer channel where quality and reliability are non-negotiable.

The threat of substitutes is the force that keeps SMP's management up at night—and rightly so. In the near term, there are no true substitutes for aftermarket replacement parts: a broken fuel injector must be replaced with another fuel injector. But in the long term, electric vehicles reduce the total parts content per vehicle, improved vehicle reliability extends the interval between repairs, and OE direct-to-consumer strategies could bypass the aftermarket entirely. The Tesla model—where service is controlled by the manufacturer, parts are proprietary, and software updates replace some physical maintenance—represents the most aggressive version of this threat.

Turning to Hamilton Helmer's 7 Powers framework, SMP's competitive position reveals a mixed but instructive picture. The company possesses genuine scale economies: the cost of maintaining an 80,000-plus SKU catalog, the engineering expense of reverse-engineering thousands of parts annually, and the fixed costs of manufacturing and distribution are amortized over a revenue base that most competitors cannot match in engine management and temperature control. This scale advantage is real and durable.

Process power is SMP's most underappreciated strength. The operational excellence built over decades—in SKU management, logistics, quality control, catalog accuracy, and customer service—represents organizational capabilities that are difficult to observe, difficult to replicate, and deeply embedded in the company's culture and systems. A competitor can copy SMP's product list, but replicating the operational infrastructure that enables SMP to manage that product list profitably is a fundamentally different challenge.

Switching costs exist but are moderate. Retailers are unlikely to switch aftermarket suppliers frequently—the costs of retraining counter staff, updating inventory systems, and managing the transition are meaningful. But they are not locked in. A retailer unhappy with SMP's pricing, fill rates, or quality could, over time, shift volume to an alternative supplier. The switching costs create friction, not barriers.

Network effects are not applicable in this business. Branding provides moderate protection—Four Seasons and Standard carry genuine recognition among professional mechanics, but these are professional brands, not consumer brands. The person paying for the car repair does not know or care which brand of A/C compressor is being installed. Cornered resources are limited: SMP's proprietary databases and engineering expertise are valuable, but not unassailable by a well-capitalized competitor willing to invest over time.

Counter-positioning—Helmer's power describing a situation where an incumbent's business model prevents it from responding to a challenger—cuts both ways for SMP. SMP's aftermarket focus represents a counter-position against OE suppliers who cannot easily shift resources to the lower-volume, higher-complexity aftermarket. But Tesla's vertically integrated model represents a potential counter-position against the entire aftermarket industry, and SMP has limited ability to respond if that model spreads to other automakers.

The aggregate assessment is a medium-strength moat: real competitive advantages in scale, process, and distribution that support above-average returns on capital, but with long-term structural pressures from the EV transition, OEM integration strategies, and customer concentration that prevent any declaration of invulnerability.

XIV. Bull vs. Bear Case & Investment Considerations

The bull and bear cases for SMP are both internally consistent and logically sound—which is exactly what makes the investment debate interesting.

The bull case rests on several interlocking propositions. The ICE vehicle fleet provides a multi-decade revenue runway. With 285 million ICE and hybrid vehicles on American roads, averaging over twelve years of age and climbing, the installed base of vehicles needing traditional aftermarket parts is enormous and growing older every year. Older vehicles need more repairs. Economic pressure on consumers—elevated interest rates, high new car prices, insurance costs—keeps vehicles on the road longer. This is not a temporary tailwind; it is a structural feature of the American vehicle market.

The EV transition, counterintuitively, may actually increase the complexity and value of electronic components in vehicles—playing to SMP's strengths in sensors, switches, and thermal management. An EV battery cooling system is a more complex and higher-value assembly than an ICE radiator. The ADAS cameras and sensors proliferating across all new vehicles, regardless of powertrain, represent a growing category where SMP is actively expanding. And the Nissens acquisition positioned SMP as a global leader in automotive thermal management—the technology that is arguably most critical to both ICE and EV platforms.

Market share gains continue as weak competitors exit and Chinese imports face quality and logistics headwinds. SMP's pricing power, demonstrated during the 2021-2022 inflationary period, suggests that the company's market position is strong enough to protect margins. The dividend provides a steady return, and the management team has demonstrated discipline in capital allocation and strategic execution. At a valuation that has typically ranged between 12 and 15 times earnings, the stock appears to reflect meaningful skepticism about the long-term outlook—which could represent an opportunity if the transition unfolds more slowly than feared.

The bear case is equally rigorous. If the EV transition accelerates faster than current adoption curves suggest, SMP's core engine management business faces a declining addressable market that no amount of thermal management or sensor revenue can fully offset. Tesla and other OEMs that vertically integrate their service and parts operations could systematically shrink the aftermarket opportunity. Vehicle reliability improvements—particularly in EVs, which have fewer moving parts and less wear-and-tear—could reduce repair frequency even for vehicles that remain in the aftermarket-accessible fleet.

Customer concentration is a structural risk that no amount of operational excellence can eliminate. If O'Reilly, AutoZone, or NAPA decided to shift significant volume to an alternative supplier, SMP's revenue and margins would suffer immediately and meaningfully. Chinese competition on price, while manageable today, could intensify if quality levels improve—as they have in many other manufacturing categories over time. And the long-term question of autonomous vehicles, while still speculative, raises the possibility of dramatically reduced accident rates and wear-and-tear, further shrinking the aftermarket.

The terminal value question—is this a "melting ice cube" whose core business will eventually decline to zero?—is the most consequential analytical challenge. The honest answer is that it depends entirely on execution: can SMP grow its EV-relevant, powertrain-neutral, and thermal management businesses fast enough to offset the eventual decline in ICE-specific parts? The company's strategic moves—the Nissens acquisition, the ADAS expansion, the investment in EV-compatible product lines—suggest that management understands the challenge and is actively working to address it. But the outcome remains genuinely uncertain.

For investors tracking SMP's ongoing performance, three KPIs stand above all others. First, gross margin trajectory: this single metric captures SMP's pricing power, operational efficiency, and product mix evolution. Improving gross margins signal that the company is successfully shifting toward higher-value products and maintaining competitive positioning. Second, organic revenue growth by segment: this reveals whether SMP is gaining or losing market share in its core categories and whether EV-relevant revenues are growing fast enough to become meaningful. Third, free cash flow conversion: given the capital-intensive nature of inventory management and the current priority of debt reduction, SMP's ability to convert earnings into free cash flow will determine both its deleveraging pace and its future capacity for dividends, buybacks, and acquisitions.

XV. Epilogue & Reflections

There is a certain beauty in unglamorous excellence. Standard Motor Products will never be featured on the cover of a technology magazine. Its CEO will never be profiled in Vanity Fair. Its products will never inspire a midnight product launch with lines around the block. And yet, for over a century, this company has done something that most businesses—including most of the glamorous, headline-grabbing ones—fail to do: it has survived.

Not just survived. Compounded. Through two world wars, the Great Depression, the oil crises, the Japanese automotive invasion, the Great Recession, a global pandemic, and the dawn of the electric vehicle era, SMP has adapted, consolidated, and grown. The company that started distributing ignition parts from a Long Island City warehouse in 1919 now operates 54 facilities across four continents, generates nearly $1.8 billion in annual revenue, and holds market-leading positions in both of its core aftermarket categories.

The lessons from SMP's story are not the ones that dominate business school case studies. They are quieter, more patient, and ultimately more applicable to the vast majority of businesses that operate outside the venture-capital-funded spotlight.

First, the power of focus. SMP has resisted the temptation to diversify into adjacent businesses where its competitive advantages do not apply. It makes aftermarket auto parts. It has made aftermarket auto parts for 107 years. That focus has enabled the depth of catalog, manufacturing, and distribution expertise that constitute its competitive moat.

Second, the advantage of patient capital. Family-influenced management with a multi-generational time horizon made decisions differently than a PE-backed platform optimizing for a five-year exit. The willingness to invest in capabilities—catalog systems, manufacturing quality, distribution infrastructure—that pay off over decades rather than quarters is a genuine competitive advantage that most publicly traded companies struggle to replicate.

Third, the strategic value of operational consistency. SMP's moat is not built on patents, proprietary technology, or network effects. It is built on the accumulated result of doing difficult, unglamorous things well, every day, for a very long time. Managing 80,000 SKUs. Filling orders accurately. Maintaining catalog accuracy across thousands of vehicle applications. Reverse-engineering parts to OE quality standards. None of these activities is individually remarkable. Together, they create a position that is genuinely difficult to replicate.

The "picks and shovels" analogy is apt. During the California Gold Rush, the most reliable fortunes were made not by the miners but by the merchants who sold them picks, shovels, and blue jeans. SMP occupies a similar position in the automotive industry: regardless of whether Ford, GM, Toyota, or Tesla wins the battle for market share, all of their vehicles will eventually need replacement parts. SMP makes those parts.

Perhaps the most surprising revelation in studying SMP is the depth and defensibility of parts cataloging as a competitive asset. From the outside, a parts catalog looks like a database—a mundane, table-driven mapping of part numbers to vehicle applications. From the inside, it is a living knowledge system that represents decades of reverse-engineering, testing, application research, and customer feedback, maintained by teams of engineers who understand the subtle differences between a 2016 Camry with the 2.5L engine and a 2016 Camry with the 3.5L V6 and why they need different ignition coils. This knowledge is SMP's true cornered resource, even if it does not fit neatly into an analyst's framework.

The big question—can SMP pull off the EV transition?—remains open. The company's management has articulated a credible strategy, executed a transformational acquisition in Nissens, and demonstrated a track record of adapting to previous technological disruptions. But the EV transition is different in kind from the shift from carburetors to fuel injection or from mechanical ignition to electronic: it involves the potential obsolescence of the engine itself, which has been the central organizing principle of SMP's business for a century.

What makes this story worth following is not the certainty of the outcome but the quality of the attempt. SMP is a case study in how a century-old company navigates technological disruption—not with dramatic pivots or billion-dollar bets, but with the methodical, disciplined, operationally excellent approach that has defined it since 1919. Whether that approach proves sufficient for the electric age remains to be seen. But the aftermarket itself—a $400 billion-plus global industry supporting millions of jobs—is watching closely. The answer matters far beyond a single stock ticker.

XVI. Further Reading & Resources

For those seeking to deepen their understanding of Standard Motor Products and the automotive aftermarket, several resources provide valuable context. Bain & Company's "The Aftermarket Imperative" and McKinsey's analysis of the trillion-dollar automotive aftermarket opportunity offer industry-level frameworks. SMP's own annual reports—particularly the CEO letters from 2008, 2015, and 2023—are surprisingly candid about the company's strategic thinking and the challenges it faces.

The right-to-repair debate, which carries existential implications for the entire aftermarket industry, is covered extensively in policy papers from the Electronic Frontier Foundation and in the advocacy materials of the Auto Care Association and AASA (Automotive Aftermarket Suppliers Association). Dorman Products' investor presentations provide the best publicly available competitive analysis for benchmarking SMP's performance and strategic positioning.

On the technical side, SAE International's papers on ADAS calibration and EV thermal management illuminate the engineering challenges that will shape the aftermarket's future. For industry data and trends, the Auto Care Association's annual reports and MEMA (Motor & Equipment Manufacturers Association) research are essential primary sources.

Aftermarket industry podcasts—including "Remarkable Results Radio" and "The Weekly Blitz"—feature interviews with technicians, shop owners, and industry executives that provide ground-level perspective on the trends shaping parts demand. Larry Sills' appearances on automotive industry podcasts during the 2015-2020 period offer direct insight into SMP's management philosophy and strategic thinking from the executive who guided the company through its most critical transformation.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube