VanEck Semiconductor ETF (SMH): The Gold-Bug Dynasty's Silicon Bet

I. Introduction: The Industry Benchmark

Picture the trading floor of the New York Stock Exchange at the open on any given Tuesday in the spring of 2026. The opening bell rings. Within sixty seconds, somewhere between two and three million shares of a single ticker have already changed hands. That ticker is not Apple. It is not Tesla. It is not even the SPDR S&P 500. It is three letters that have, against all probability, become the universal Wall Street shorthand for an entire global industry: SMH.

If you wanted to bet on the "picks and shovels" of the artificial intelligence revolution that consumed financial markets between 2023 and 2026, you bought SMH. If you were a hedge fund hedging out single-name semiconductor risk, you shorted SMH. If you were a sovereign wealth fund expressing a long-cycle thesis on 半導體產業 the semiconductor industry, you accumulated SMH. The VanEck Semiconductor ETF had become, almost by accident and entirely by design, the world's reference price for silicon.[^1]

By the close of the first quarter of 2026, the fund managed north of twenty billion dollars in assets, with daily dollar volume routinely exceeding the GDP of small island nations.[^1] It tracked the MarketVector US Listed Semiconductor 25 Index, a basket so concentrated that a single name — 엔비디아 Nvidia — could move the entire portfolio by two percent on an ordinary trading session.1

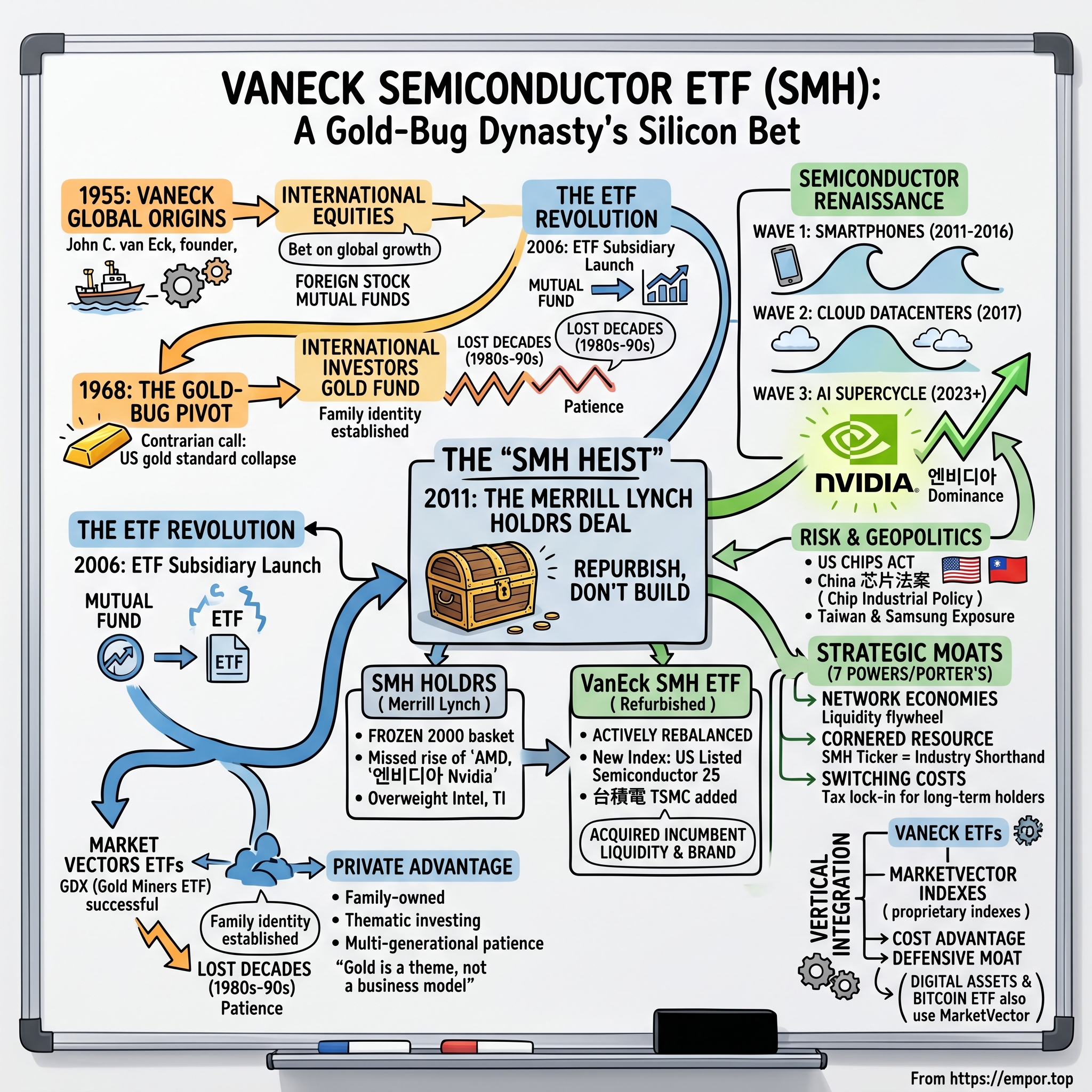

But here is the part nobody talks about on CNBC. SMH is not a Vanguard product. It is not a BlackRock product. It is not a State Street product. It is the flagship vehicle of a privately held, family-controlled asset manager founded in 1955 by a Dutch immigrant who wanted Americans to buy European stocks, and who spent the second half of his career obsessed with one commodity: gold.2

This is the story of how a seventy-year-old gold-bug dynasty — three generations of the van Eck family, with Jan van Eck now at the helm — hijacked the most important ticker in modern technology investing from one of the largest investment banks in American history. It is the story of a "refurbishing" strategy so elegant that Wall Street still has not figured out how to replicate it. It is the story of a private, founder-controlled firm that bet on Bitcoin before Bitcoin was respectable, bought the semiconductor narrative before the AI supercycle was visible, and built an in-house index provider quietly while its larger competitors paid licensing fees to MSCI and S&P.

It is the story of how betting on silicon, when your family's entire identity was built on gold, can turn out to be the most lucrative pivot in the history of asset management.

Let us begin in 1955, in a small office on Park Avenue, with a Dutchman who could not understand why Americans were not buying foreign stocks.

II. VanEck Origins: The Gold-Bug Legacy

In the years immediately following the Second World War, the typical American investor regarded the rest of the world the way a Manhattanite regards New Jersey: aware that it exists, vaguely suspicious of what happens there, and entirely uninterested in spending money to visit. Foreign equities were exotic curiosities reserved for J.P. Morgan partners and Boston Brahmins with steamship connections. Mutual funds, when they bothered to allocate abroad at all, did so in the rounding error of a portfolio.

John C. van Eck saw this and saw, instead, the smoldering reconstruction of Europe. He had watched the Marshall Plan dollars flow across the Atlantic and into rebuilding economies whose factories, ports, and middle classes were about to compound at rates that would humiliate the postwar American economy. In 1955, in a modest office in New York, he founded Van Eck Global with a single, mildly heretical product idea: a mutual fund that allowed ordinary US investors to own foreign stocks.2 At the time, this was so unusual that the firm's earliest marketing materials had to explain what a "foreign security" actually was.

For thirteen years, the firm built itself patiently around international equities. Then, in 1968, John van Eck made the call that would define his family's identity for the next half century. He looked at the Bretton Woods system — the postwar architecture pegging the dollar to gold at thirty-five dollars an ounce — and concluded it was structurally doomed. The United States was funding the Vietnam War and the Great Society simultaneously, the gold window was bleeding reserves, and the moment de Gaulle started demanding bullion delivery from Fort Knox, the fix was in. Van Eck launched the first US mutual fund dedicated to gold mining equities.2

It was three years early. The gold standard officially collapsed on August 15, 1971, when Richard Nixon closed the gold window. By the end of that decade, gold had moved from thirty-five dollars an ounce to more than eight hundred. The International Investors Gold Fund, as it became known, was not just early; it was the only mainstream American product positioned to capture the trade. The van Eck family became, in industry parlance, "the gold-bug family." It was a label that would prove both a moat and a burden.

The moat: when gold ran, nobody ran with it like VanEck. The burden: the 1980s and 1990s were not kind to bullion. While the rest of the asset management industry rode the equity bull market of Reagan, Greenspan, and the dot-com euphoria, VanEck spent two decades watching its core franchise grind sideways through what gold-bugs now ruefully call "the lost decades." Other firms would have capitulated. They would have closed the gold fund, hired growth-equity managers, and chased whatever Morningstar happened to be ranking five stars that quarter. VanEck did not, because VanEck could not. The firm was private, family-owned, and answerable to nobody but itself.

By the late 1990s, the founder's sons — Jan van Eck and Derek van Eck — were taking increasingly senior roles. They had been raised inside the firm and inside the worldview. They believed, as their father did, that the asset management business was not about distribution muscle or quarterly performance rankings. It was about identifying durable, multi-decade themes and being patient enough to own them while everyone else laughed.

That cultural DNA — call it "thematic investing with multi-generational patience" — was the inheritance Jan and Derek received. The question, by the turn of the millennium, was what to do with it. Gold was still a religion at the firm, but the broader fund industry was undergoing a structural revolution. The product wrapper was changing.

The mutual fund was dying. Something else was coming. And in 2006, the van Eck brothers were going to bet the family franchise on it.

III. The Lost Decade & The ETF Pivot

The dot-com crash did something subtle and enormous to the American asset management industry. On the surface, the carnage looked like a tech story. Underneath, it was a distribution story. The 1990s mutual fund boom had been built on broker-sold A-share, B-share, and C-share products laden with sales loads and 12b-1 fees, marketed through wirehouses whose financial advisors collected the commissions. After 2000, two things happened in parallel: investors discovered they had been paying too much for performance that was often worse than the index, and a strange product structure that had quietly existed since 1993 — the exchange-traded fund — began to gain critical mass.

The ETF wrapper offered something the mutual fund could not: intraday liquidity, dramatically lower expense ratios, and brutal tax efficiency thanks to the in-kind creation and redemption mechanism. By the mid-2000s, the writing was on the wall. Vanguard was building an ETF complex. iShares, owned at that time by Barclays Global Investors, was minting ETFs at industrial scale. State Street's SPDR franchise was the original and still the largest. Mutual fund assets would continue to grow in absolute terms for another fifteen years, but the marginal flow — the future — was unmistakably leaving for the ETF wrapper.

Jan van Eck saw this and made what was, in retrospect, the most important strategic call of his career, but it did not feel obvious at the time. He realized that the firm's identity — gold, emerging markets, "themes" — was not a product. It was a worldview. And a worldview could be wrapped in any structure you wanted. "Gold is a theme, not a business model" became, in essence, the internal framing. The business model needed to be re-architected for the ETF era.

In May 2006, VanEck launched Market Vectors, its ETF subsidiary. The first product was almost predictable in retrospect: the Market Vectors Gold Miners ETF, ticker GDX. It held the world's largest gold mining equities, charged a fraction of the expense ratio of a traditional mutual fund, and traded on the NYSE Arca like a stock. Within a few years, GDX would become the dominant vehicle for gold mining exposure on the planet — the gold-bug religion, repackaged for the ETF generation.2

But the deeper innovation was not GDX itself. It was the realization that VanEck could systematically convert its mutual fund themes into ETFs, and could launch ETFs in categories the giants had ignored. The Vanguards and BlackRocks of the world were optimizing for broad-market, low-cost exposure. They were leaving entire thematic verticals — gold miners, emerging market debt, MLPs, biotech, eventually semiconductors and digital assets — wide open. A small, focused, family-owned firm with a contrarian DNA could pick them off one by one.

Then, in 2010, came the moment that nearly broke the family.

Derek van Eck, John's elder son and the firm's longtime investment strategist, died unexpectedly. He had been the public face of the firm's investment process for years, the one who fronted the gold thesis on CNBC, the brother investors associated with the brand. The shock inside the firm was profound. Jan, who had been the operational mind to Derek's investment voice, suddenly inherited both roles. He took over as Chief Executive Officer.2

What happened next is, in many ways, the most interesting thing about VanEck. A grieving family-owned firm, in the depths of the post-financial-crisis ETF land grab, with founder-era mutual fund assets bleeding to the BlackRocks of the world, could very easily have sold to a larger asset manager. The price would have been generous. The story would have been clean. Instead, Jan van Eck doubled down. He looked at the ETF industry's competitive map and made a contrarian observation: the giants were great at building, but they were terrible at refurbishing.

He had spotted something specific, something nobody else in the industry seemed to fully appreciate. There was a graveyard of dying ETF-like products sitting on the books of one of Wall Street's largest investment banks, and nobody was doing anything with them.

The graveyard was called HOLDRS. And Jan van Eck was about to walk through it with a flashlight.

IV. The "SMH Heist": The Merrill Lynch HOLDRS Deal

To understand the audacity of what VanEck pulled off in 2011, you have to understand what HOLDRS were and why they had become, by the late 2000s, financial archaeology.

In 1998, at the absolute peak of the late-1990s structured products renaissance, Merrill Lynch invented a vehicle called the Holding Company Depositary Receipt, or HOLDR. The idea was deceptively elegant. Rather than a mutual fund or an ETF, a HOLDR was a literal grantor trust holding a basket of underlying stocks. Investors who bought a HOLDR owned direct fractional shares of the underlying companies, voted those shares, received dividends from them, and could even physically separate the basket back into its component stocks if they held a round lot.[^8]

It was an audaciously simple piece of financial engineering, and Merrill rolled out HOLDRS for every fashionable sector of the late-1990s technology boom: Internet HOLDRS, Biotech HOLDRS, Broadband HOLDRS, Wireless HOLDRS. And, in May 2000 — almost exactly at the peak of the dot-com bubble — the Semiconductor HOLDRS, ticker SMH. It was originally a basket of twenty companies, weighted by their market capitalization at launch and frozen there by design.[^8]

That last part is critical. HOLDRS did not rebalance. They did not add new constituents as the industry evolved. They did not delete bankrupt or acquired companies in any clean way. Once Merrill set the basket on day one, the basket was set. Forever. If a company in the basket got acquired, the HOLDR holders received the merger consideration. If a company went bankrupt, the slot simply vanished from the trust, leaving the basket smaller. New industry leaders that emerged after launch were never added.

For most of the HOLDRS family, this was a slow-motion catastrophe. By 2010, the Internet HOLDRS still owned 1999-era companies that no longer existed in their original form. The Biotech HOLDRS was a museum exhibit. The Wireless HOLDRS held an industry that had reorganized itself three times over.

The Semiconductor HOLDRS was a particularly poignant case. Its 2000-vintage basket overweighted Intel and Texas Instruments — the giants of the PC-era semiconductor industry — while completely missing the rise of the fabless model. It held no 엔비디아 Nvidia of any meaningful weight, no AMD rebirth, no foundry exposure to 台積電 TSMC because TSMC was not in the original American-listed basket. It was, in the words of an ETF Trends retrospective, a "frozen-in-time" portfolio that had become structurally incapable of representing the industry whose name it bore.[^8]

Merrill Lynch, after the financial crisis, had bigger problems than a graveyard of zombie HOLDRS. Bank of America had absorbed it in 2008. The combined firm was deleveraging, slimming product lines, and looking to offload anything that did not generate scale revenue. By 2011, the HOLDRS were on the block, except nobody really wanted to buy them in their existing form.

This is where Jan van Eck's genius — and it deserves to be called that — became visible.

He did not propose buying the HOLDRS as products. He proposed acquiring the tickers and holder bases, then transitioning each one into a properly structured, actively rebalanced VanEck ETF wrapped around a new index. In effect, he was offering Merrill a graceful exit from a dying franchise while acquiring, for VanEck, the single most valuable asset a thematic ETF can possess: incumbent liquidity.

In August 2011, VanEck announced it had reached an agreement to transition six HOLDRS — including the Semiconductor HOLDRS, the Pharmaceutical HOLDRS, the Oil Services HOLDRS, the Retail HOLDRS, the Regional Bank HOLDRS, and the Biotech HOLDRS — into newly constituted VanEck ETFs.[^3] The deal closed in December of that year. On day one of the transition, the SMH ticker was no longer a frozen 2000-vintage basket. It was a properly structured exchange-traded fund tracking a freshly designed MarketVector index of the twenty-five largest US-listed semiconductor companies, including the global foundry titans that the HOLDRS structure had been incapable of holding.1

The genius was in what Jan van Eck did not have to pay for. He did not have to spend a decade building organic AUM in semiconductor ETFs against entrenched competitors. He did not have to pay for marketing campaigns to drag traders away from existing benchmarks. He inherited, in a single transaction, an already-trading ticker that institutional traders had been using for eleven years. Every options market maker, every prime broker, every hedge fund's compliance department already had SMH wired up in their systems. The "switching cost" of a new ETF — the friction of getting the Street to adopt a new symbol — was the very thing VanEck got for free.

It was a capital-light acquisition of brand and liquidity. And the immediate post-conversion rebalance added 台積電 TSMC and other modern semiconductor leaders to the basket for the first time, just as the smartphone supercycle was preparing to break.1

The seventy-year-old gold-bug dynasty had just bought itself the keys to the most important emerging trade in technology, and almost nobody in the financial press at the time understood what had happened.

The decade that followed would prove the point spectacularly.

V. The Semiconductor Renaissance: Riding the AI Wave

For the first eighteen months after the HOLDRS conversion, SMH did roughly what one would expect a re-indexed semiconductor ETF to do in 2012: it tracked an industry caught between the late-PC slowdown and the early-smartphone ramp. It was not yet obvious that VanEck had acquired the future. It was, however, becoming visible that the underlying industry was about to enter a multi-wave secular bull market unlike anything in its history.

The first wave was the smartphone. From roughly 2011 through 2016, the world's pocket computers went from a developed-market luxury to a five-billion-unit installed base. Every one of those devices required a dense stack of silicon: a baseband modem, an application processor, image sensors, NAND and DRAM memory, power management, RF front-ends. Every link in the chain was inside SMH's reconstituted index. Qualcomm, Broadcom, Texas Instruments, Micron, the foundry titans manufacturing it all — the smartphone supercycle was, from the standpoint of SMH's NAV, the equivalent of having pre-purchased oil futures in 1999.

The second wave arrived without much fanfare. Sometime around 2017, hyperscale cloud datacenters quietly overtook smartphones as the marginal driver of semiconductor unit demand. The build-out of 亚马逊 AWS, Microsoft Azure, and Google Cloud required a fundamentally different mix of silicon: server CPUs, networking ASICs, custom accelerators, vast quantities of high-bandwidth memory. The companies positioned for it — Intel briefly, AMD increasingly, Broadcom permanently — were already inside SMH. The pure-play datacenter foundry play, 台積電 TSMC, was now the second-largest position by weight.1

But the third wave was the one that changed the firm's destiny.

In late 2022, a chatbot called ChatGPT was released to the public. By the spring of 2023, every Fortune 500 board was asking what its AI strategy was, and every cloud hyperscaler was placing emergency orders for one specific kind of silicon: the GPU. And one company, more than any other, had spent the previous fifteen years building the hardware, the software, and the developer ecosystem that made large language model training possible. That company was 엔비디아 Nvidia. It was already SMH's largest holding.

What followed was, in the literal sense of the word, unprecedented. Between the start of 2023 and the close of 2025, Nvidia's market capitalization went from roughly three hundred and sixty billion dollars to multiple trillions. The MarketVector US Listed Semiconductor 25 Index, which weights by free-float market capitalization but caps the largest single name, found Nvidia bumping repeatedly against the cap.1 At various rebalances, Nvidia constituted roughly one-fifth of the entire fund. SMH was no longer simply a semiconductor benchmark. It had become, for all practical purposes, the most liquid leveraged-Nvidia plus picks-and-shovels-AI vehicle on Earth.

By early 2024, the Financial Times noted that the rise of Nvidia had effectively turned every major semiconductor ETF into a backdoor Nvidia trade — but SMH, with its concentration weighting, was the purest expression of the phenomenon.3 Where rival benchmark SOXX (managed by iShares) used an equal-weighting methodology that diluted single-name exposure, VanEck embraced the concentration. It was a deliberate, philosophical choice rooted in the firm's seven-decade thematic DNA: if you believe in a theme, you want concentrated exposure to its leaders, not diluted exposure to its laggards.

The bet worked, but it also exposed the fund to a new layer of risk that had nothing to do with semiconductors and everything to do with geopolitics. The U.S. CHIPS and Science Act, signed in August 2022, allocated tens of billions of dollars to onshoring American semiconductor manufacturing. Beijing, in response, accelerated its own 芯片法案 chip industrial policy, pouring state subsidies into domestic foundries and pressuring the global supply chain in dual-use technologies. Export controls on advanced GPUs to Chinese customers — first under the Biden administration, then sharpened further — created sudden, unpredictable revenue holes in companies that VanEck's index was structurally required to hold.

For a fund whose largest single holding was Nvidia, the largest geographic exposure was Taiwan-based TSMC4, and whose third pillar was 삼성전자 Samsung Electronics' memory franchise5, geopolitics was no longer a footnote in the risk section of the prospectus. It was the dominant input variable. Tariff cycles, export-control updates, and cross-strait tensions could move the NAV by single-digit percentages in a session.

VanEck's response was, characteristically, to lean into the volatility rather than diversify it away. The firm's marketing materials embraced the concentration. The pitch became simple: SMH is not designed to be a diversified technology fund. It is designed to be the purest possible exposure to the most important industrial value chain of the twenty-first century, with all the geopolitical risk that implies.

For institutional investors building thematic AI exposure, that pitch was magnetic. By the close of 2025, SMH's AUM had multiplied many times over from its post-HOLDRS launch base, and its daily trading volume had made it one of the most liquid thematic ETFs on the planet.[^1] The HOLDRS heist had paid for itself many times over.

But the asset manager underneath was not, on the surface, the kind of firm you would expect to be running it.

VI. Management & The Private Advantage

If you walked into VanEck's New York offices in 2026, you would notice something almost immediately. The vibe is not Citadel. It is not BlackRock. It is closer, in some indefinable way, to a top-floor European private bank: oak, restraint, family photographs, the unhurried energy of a firm that does not need to answer to anyone next Tuesday.

Jan van Eck is the reason. As Chief Executive Officer and President, he has run the firm for over fifteen years since taking over after his brother Derek's passing.2 He is, by temperament, an unusual asset management CEO. Trained as a lawyer, fluent in the firm's gold-bug history because he grew up inside it, and fundamentally indifferent to the quarterly earnings rhythm that drives behavior at every publicly traded competitor. The reason is structural. There are no quarterly earnings. The firm is private. The family controls it.

In a 2023 Bloomberg Wealth profile, Jan van Eck described the operating philosophy in a way that captured the entire firm in two sentences. The asset management industry, he argued, had become an oligopoly of giants competing on cost in commoditized broad-market index products. The opportunity for a smaller, private firm was the opposite: to make concentrated bets on niche themes that the giants either could not move into without cannibalizing their core, or could not approve internally without years of committee work.2

That permission structure — the ability to make "crazy" bets — was the single most undervalued asset on VanEck's balance sheet. It was why, while the rest of the asset management industry treated cryptocurrency as a regulatory toxic-waste site through the late 2010s, VanEck filed for one of the earliest Bitcoin ETF applications. It was why, when Wall Street's biggest names regarded gold mining funds as embarrassing legacy products in the 2010-2020 bull market for growth stocks, VanEck kept building and marketing them. And it was why, in 2011, Jan could authorize a HOLDRS refurbishment deal that would have died in a public asset manager's product committee on the grounds that "it doesn't move the needle this quarter."

The Jan van Eck personal style reinforces all of this. He gives interviews. He speaks at conferences. But he is not a CNBC ubiquity in the manner of, say, Cathie Wood. The firm's public communications are heavy on research notes and light on personality cult. The implicit message to institutional clients is that the firm is not, and will not be, a vehicle for promoting a single charismatic individual whose departure could blow up the franchise. It is a multi-generational family business that happens to manage a globally consequential ETF complex.

The "skin in the game" pitch lands particularly hard with allocators. When a public asset manager launches a new product, the natural question is whether the launch is being driven by genuine investment conviction or by the need to grow fee revenue for next quarter's earnings call. When a private, family-owned firm launches the same product, the question shifts. The van Eck family's own wealth is largely tied to the firm's enterprise value. They are, in effect, the largest economic stakeholders in every decision the firm makes. Allocators notice.

The cultural tension inside the firm — and it is a tension that Jan van Eck has been remarkably explicit about over the years — is between the "old school" value-investing identity built around gold and natural resources and the "new school" thematic identity built around semiconductors, digital assets, and emerging-market technology. Both are alive simultaneously in the product complex. The gold equity funds still exist. The semiconductor ETF dominates a future-oriented industry. The Bitcoin ETF, launched after years of regulatory wrangling, sits in the same product menu as the original International Investors Gold Fund. A firm that openly carries that much philosophical contradiction is either deeply confused or genuinely disciplined about owning multiple long-cycle themes simultaneously. With VanEck, it is the latter.

There is one other ingredient in the firm's identity, and it does not get nearly enough attention in the financial press, because it operates one layer below the products that most investors actually see.

VanEck does not just sell ETFs. It owns the factory that builds the indexes those ETFs track. And that factory has a name.

VII. The "Hidden" Business: MarketVector & Digital Assets

In 2014, a small German indexing operation called Market Vectors Index Solutions — internally referred to as MVIS — began to attract attention in the corners of the ETF industry that paid attention to such things. It was the in-house indexing arm of VanEck. Most asset managers licensed their indexes from MSCI, S&P Dow Jones, FTSE Russell, or Bloomberg. VanEck owned its own.

In 2021, MVIS was rebranded as MarketVector Indexes, signaling its emergence as a free-standing index provider serving both VanEck's internal ETF lineup and external clients. It now publishes the MarketVector US Listed Semiconductor 25 Index that SMH tracks1, the indexes underpinning VanEck's gold miners products, and a rapidly expanding suite of digital asset benchmarks.

To understand why this matters, you have to think about the ETF industry's economic anatomy. When BlackRock launches an iShares S&P 500 ETF, it pays S&P Dow Jones an index licensing fee — typically a small but non-trivial percentage of the fund's expense ratio. That fee is, in effect, a margin leak from the asset manager to the index provider. For a single mega-cap product, the leak is small. For a complex of dozens of niche thematic ETFs, the cumulative leak is enormous.

VanEck does not have the leak. By owning MarketVector, VanEck captures the indexing economics inside the same corporate envelope. The result is a structural cost advantage that compounds with every new thematic product launch. The firm can stand up a new index — say, a digital infrastructure index or a rare-earth mining index — without paying a license fee to a third party, without going through a third-party committee process, and without exposing its product roadmap to a competitor that might tip off rivals. The cook owns the recipe, and the recipe never leaks.

It is also a defensive moat. If a competing asset manager tried to launch a copycat semiconductor ETF tracking the same methodology as SMH, they could not simply license the MarketVector index — it is not for outside ETF use against VanEck's products. They would have to commission a new index from S&P or MSCI, which would carry a different methodology, different constituents, and a different track record. That methodology divergence is precisely what has kept SOXX, the iShares competitor, from being a perfect substitute for SMH despite years of effort and significant cost-advantage marketing.

The same vertical integration logic has driven VanEck's aggressive push into digital assets. Through the late 2010s and into the 2020s, the firm laid the regulatory groundwork for a Bitcoin ETF with a persistence that bordered on stubborn. The original applications were rejected by the SEC. VanEck refiled. They were rejected again. They refiled again. By the time the SEC finally approved spot Bitcoin ETFs in January 2024, VanEck was among the cohort of issuers launching on day one with the HODL ticker, supported by months of pre-launch index work from MarketVector and a regulatory architecture detailed in successive S-1 filings.6

The firm's broader digital assets research — its 2024 Digital Assets Outlook explicitly framed crypto as a structural allocation rather than a tactical trade[^9] — was a long way from the gold-bug identity John C. van Eck had built the firm around. And yet, in another sense, it was the most natural extension imaginable. Both gold and Bitcoin are non-sovereign stores of value. Both attract investors skeptical of fiat-currency debasement. Both spend long periods in the wilderness followed by violent rallies. A firm whose institutional memory was built on surviving "lost decades" in one such asset was uniquely psychologically equipped to underwrite another.

The result, by 2026, is a firm whose product lineup looks almost theatrically eclectic — gold miners, semiconductors, Bitcoin, emerging market debt — but whose internal logic is remarkably coherent. Identify long-duration, contrarian themes. Build them in an ETF wrapper. Own the index. Compound the franchise across decades, not quarters.

The firm does not publicly disclose detailed segment economics — it is private. But it is widely understood within the industry that ETFs constitute roughly nine-tenths of total assets, with the legacy mutual fund business shrinking and the indexing business operating as a margin amplifier rather than a standalone revenue driver. In 2018, the firm acquired Think ETF Asset Management in the Netherlands, expanding its European ETF footprint and inheriting a Dutch family-business culture not entirely unlike its own.[^5] The seller, BinckBank, disclosed the transaction in its 2018 annual report as a meaningful book gain.[^6]

The picture, then, is of a firm that has quietly become a multi-product thematic powerhouse by relentlessly executing the same playbook. The next question is what makes that playbook structurally defensible.

VIII. Strategy: 7 Powers & Porter's 5 Forces

If you sat Jan van Eck down with Hamilton Helmer's 7 Powers on one side of the table and Michael Porter's Five Forces on the other, the resulting whiteboard would be a master class in how a small thematic ETF franchise can sustain advantage against giants with a hundred times its AUM.

Start with what Helmer would call Scale Economies and the asset management industry's brutal version of them. The big three — Vanguard, BlackRock, State Street — have built unassailable cost moats in broad-market index products. Their expense ratios on S&P 500 ETFs are essentially zero. VanEck cannot compete there. It does not try. SMH carries an expense ratio that is several times higher than a Vanguard total-market fund.[^1] The firm's strategic decision was to surrender the broad-market beta game entirely and play a completely different one.

Where VanEck does have power is in Network Economies, expressed through the unique liquidity dynamics of an ETF. An ETF's liquidity is self-reinforcing. The more traders use a ticker, the tighter the bid-ask spreads. The tighter the spreads, the lower the all-in cost of trading the ticker. The lower the cost, the more traders use it. This is the same dynamic that makes a stock exchange a winner-take-most market. SMH's incumbency, inherited from the 2011 HOLDRS conversion, gave it a head start on this flywheel that competitors have spent fifteen years failing to overcome. Today, SMH is the casino of the global semiconductor industry. Traders go there because everyone else is there.

The closest concept Helmer offers to this is Cornered Resource, and in SMH's case it is almost literal. The ticker itself — three letters, S-M-H — has become industry shorthand. When a CNBC anchor says "the semis," every trader on the desk knows the next data point they will quote is SMH's intraday move. When a hedge fund analyst writes a memo titled "Long SMH, Short SOXX," nobody asks what those tickers mean. The cornered resource is not a patent or a lease on a mine. It is a piece of language. And language, once it has been adopted, is very hard to dislodge.

Switching Costs show up in a place most ETF analysis misses: the taxable account. An investor who has held SMH in a taxable account for several years through the AI rally is now sitting on an enormous embedded capital gain. Selling that position to move to a competing semiconductor ETF — even a marginally cheaper one — triggers immediate capital gains tax. The math, for any long-term holder, is brutal: the after-tax cost of switching wipes out a decade or more of expense ratio savings. This is the same lock-in dynamic that has kept SPY dominant despite the existence of cheaper alternatives like IVV and VOO. The taxable cohort is, in effect, a captive customer base.

Now run the five forces.

Threat of New Entrants is, on paper, very high. Anyone with regulatory approval and a few million dollars in seed capital can launch a semiconductor ETF. There are no patents to defend, no factories to build, no exclusive distribution agreements. And yet new entrants consistently fail to gain meaningful traction, because the liquidity moat — that self-reinforcing network economy — is invisible until you try to crack it. New competitors offer lower expense ratios. The market shrugs. Nobody wants to be the first whale in an empty pool.

Bargaining Power of Suppliers is, in this context, an unusual question. The "suppliers" of an ETF are the underlying companies in the index. They do not negotiate with the fund. But they do, collectively, determine its fortunes. If 台積電 TSMC stumbles on a node transition, if ASML faces a sudden export-control hit, if 엔비디아 Nvidia suffers a competitive setback from a custom-silicon program at a hyperscaler customer, the ETF's NAV moves accordingly.45 This is supplier power expressed through the fundamentals rather than through pricing. It is a real risk, particularly given the index's deliberate concentration.

Bargaining Power of Buyers — meaning end investors — is increasing but slowly. Retail investors have access to tools that let them compare expense ratios and tracking error across competing products. Institutional allocators run detailed pre-trade transaction cost analysis. Both of these dynamics push expense ratios down over time. VanEck's defense is not cost; it is concentration, brand, and the structural pull of incumbent liquidity.

Threat of Substitutes is more interesting. The biggest substitute for SMH is not another ETF; it is owning Nvidia directly. Many institutional investors who want semiconductor exposure simply buy Nvidia stock outright, plus perhaps a few peer names, and skip the ETF wrapper entirely. The counter-pull is the basket logic: the AI supercycle does not necessarily mean Nvidia wins forever; it means somebody in the silicon stack wins continuously. The ETF expresses that thesis without requiring the investor to pick the winner.

Competitive Rivalry is the most visible force. The iShares Semiconductor ETF, SOXX, is the direct rival, with a different methodology (modified equal-weighting), lower expense ratio, and the full distribution muscle of BlackRock behind it. The Invesco PHLX Semiconductor ETF and a smaller pure-play SOXQ also exist. VanEck cannot win the cost game. It wins by being the concentrated product, the narrative product, the one institutional traders use because that is where the liquidity lives.

Pulled together, the strategic position is: a vulnerable cost moat, but a powerful liquidity moat, a cornered linguistic resource, and a deliberate philosophical positioning as the concentration-and-narrative-driven semiconductor benchmark rather than the diversified-and-cheap one.

It is not a fortress. It is a flywheel. And flywheels, once spinning, are remarkably hard to stop.

IX. Playbook: Business & Investing Lessons

Strip away the specifics — the gold, the silicon, the Bitcoin — and the VanEck story collapses into three repeatable lessons that any operator or investor can take away.

The first is refurbish, don't build. The semiconductor benchmark that became SMH was not invented by VanEck. It was invented by Merrill Lynch in 2000, mismanaged into structural obsolescence by 2011, and acquired in a transition that nobody else in the ETF industry had thought to propose. The deeper lesson is that established financial products carry latent liquidity and brand value that survives even severe operational decay. A "zombie" ETF with billions in stale AUM, a recognized ticker, and an entrenched holder base is more valuable, all else equal, than a freshly minted competitor with better mechanics but zero adoption. The trick is recognizing the asymmetry and being structurally able to act on it. A public asset manager would have struggled to justify the deal's optics to a board. A private, family-controlled firm could simply do it.

The second is embrace concentration. The dominant business model in asset management since the rise of indexing has been the relentless commoditization of broad-market exposure. Vanguard wins that game permanently. Smaller firms that try to compete on cost in broad-market beta lose, slowly, until they are absorbed or wound down. VanEck recognized this earlier than most and built a deliberately opposite franchise: high-conviction thematic products that are explicitly not diversified, deliberately not cheap, and unapologetically narrative-driven. The product is not exposure. The product is a thesis. And a thesis, well-marketed, supports a higher expense ratio than a commoditized index does.

The third is the family-office advantage, applied to the asset management business. Most asset managers are stuck in a quarterly performance cycle. They must defend last quarter's flows on this quarter's earnings call. They cannot, structurally, underwrite multi-decade themes that require five years in the wilderness before paying off. Gold's lost decade. Bitcoin's regulatory exile. The semiconductor industry's mid-2010s consolidation period before the AI wave broke. A public firm would have closed those product lines. VanEck kept them. The willingness to sit through the cold years, supported by family ownership and an operating model that does not depend on any single product's quarterly flows, is itself the franchise.

Underneath all three lessons is a meta-lesson about industries that look mature. The asset management business in 2010 looked like an oligopoly closing in around three giants. The thematic ETF opportunity that VanEck exploited was, in retrospect, the kind of opening that exists in every "mature" industry: a category that the incumbents have written off as too small or too weird, but that becomes large and respectable later. The lesson is to read the incumbents' product strategies for what they are not doing, and ask why.

That meta-lesson is what makes VanEck interesting to study as a business case beyond the specifics of any one product. The next product they launch — whatever it is — will follow the same pattern. The franchise is the playbook, not the SMH ticker.

X. Analysis & Bear vs. Bull Case

The Bull Case

The bull thesis on SMH is, at its core, a thesis on computation itself.

Every meaningful trend in the global economy over the next decade — generative AI, autonomous vehicles, edge computing, electrified industrial automation, sovereign data infrastructure — requires more silicon per unit of GDP than the previous generation of any of those trends did. The arrow of demand is structural. Even if the specific application layer fashionable in any given year (chatbots, then agents, then something else) changes, the underlying picks-and-shovels demand for semiconductors continues.

SMH is the cleanest publicly available exposure to that demand. Its concentration in the global leaders — 엔비디아 Nvidia in compute, 台積電 TSMC in foundry4, 삼성전자 Samsung in memory5, ASML in lithography — captures the most economically critical links in the chain. The vertical integration with MarketVector keeps the product economically efficient for VanEck even as the broader ETF industry races to zero on expense ratios. And the liquidity flywheel, once established, is self-perpetuating: SMH gets used because it gets used.

There is also the convexity argument. Semiconductors are a famously cyclical industry, but the cycles have been getting smaller in amplitude and the secular trend line has been getting steeper. AI workloads have created a new layer of demand that is fundamentally different from the legacy PC and smartphone cycles. The downcycles, when they come, may be shallower than they used to be — not because cyclicality has been repealed, but because the base load of compute demand keeps stepping up with each AI capability iteration.

The Bear Case

The bear thesis is concentration risk dressed up as diversification.

The same feature that gives SMH its bull case — heavy weighting in Nvidia, TSMC, and a handful of other giants — gives it a brittle downside profile. If Nvidia faces what bears like to call a "Cisco 2000 moment" — a sudden recognition that capex from hyperscaler customers has overshot durable AI workload demand, leading to inventory corrections and multiple compression — SMH offers very little structural protection. The basket simply rides Nvidia down. An equal-weighted competitor like SOXX would soften the blow. A market-cap-weighted broad tech ETF would diversify across software and platforms. SMH does neither. By design.

Geopolitical concentration compounds the issue. A substantial fraction of SMH's underlying revenue exposure ultimately funnels through Taiwan-based manufacturing. A Taiwan Strait crisis, escalating export controls, or unexpected sanctions on Chinese semiconductor customers would hit the fund's holdings in correlated, hard-to-hedge ways. The U.S. and Chinese policy responses — CHIPS Act subsidies on one side, 芯片法案 industrial policy on the other — have created the most heavily politicized supply chain in the modern global economy. That risk does not show up on the cover page of the fund prospectus, but it is real.

There is also a competitive dynamic worth flagging. Custom silicon programs at hyperscalers — Amazon's Trainium and Inferentia, Google's TPUs, Microsoft's Maia, Meta's MTIA — have begun to capture a growing share of AI training and inference workloads. If those programs continue to mature, the value capture in the AI compute stack could migrate from the merchant silicon vendors (Nvidia, AMD) toward the hyperscalers themselves. Hyperscalers are not in SMH's index. The fund could find itself owning yesterday's AI value capture rather than tomorrow's.

The KPIs That Matter

For a long-term investor watching SMH as a business case rather than as a market call, three indicators carry the most signal.

First, the bid-ask spread relative to SOXX. As long as SMH's spread remains tight relative to its direct competitor, the liquidity moat is intact. If SOXX's spread tightens to match or beat SMH's — even occasionally — the network effect underlying VanEck's franchise is eroding.

Second, the net inflow trajectory relative to SOXX. AUM growth is, ultimately, the scoreboard for an ETF franchise. If VanEck is gaining share against BlackRock in the semiconductor category, the concentration-and-narrative strategy is working. If BlackRock is gaining share, the cost moat is winning. The flow data is publicly reported and easy to monitor.

Third, the performance of MarketVector's other indexes. SMH is the flagship, but the long-term durability of VanEck's franchise depends on its ability to repeatedly launch successful thematic products on top of its proprietary index machine. The success rate of new MarketVector-indexed ETF launches — measured by AUM growth two and three years post-launch — is the leading indicator of whether the franchise compounds for another twenty years or peaks with SMH.

The honest summary is that SMH is neither the safest nor the cheapest semiconductor exposure on the market. It is the most concentrated, most liquid, and most narrative-driven one. Whether that is a feature or a bug depends entirely on the investor's view of the underlying industry and their tolerance for volatility in the largest single name in their portfolio.

XI. Epilogue

In 1955, a Dutch immigrant founded a small mutual fund company on Park Avenue because he believed Americans should own European stocks. In 1968, he made one of the most prescient calls in postwar finance by launching a gold equity fund three years before the gold standard collapsed. He spent the rest of his career building a firm whose entire identity was wrapped around a single precious metal.

Seventy years later, his son runs what is, by virtually every relevant measure, a technology investing powerhouse. The largest single product on the firm's shelf — by AUM, by daily trading volume, by cultural footprint — is an ETF that owns shares of companies that design, manufacture, and supply the world's most advanced semiconductors. The largest holding inside that ETF is the most important AI hardware company in human history. The second-largest holding is a Taiwanese foundry whose process technology has become a flashpoint of global geopolitics.

The man who oversaw this transformation, Jan van Eck, did not abandon the firm's original DNA. The gold fund still exists. The thematic worldview that drove the 1968 bullion bet drives the 2026 semiconductor bet and the parallel push into digital assets. The cultural insistence on multi-decade themes, contrarian positioning, and family ownership has been preserved through three generations of leadership transitions, including one tragic one. The firm has compounded by knowing what it is and what it is not.

What is next is, in a sense, already visible. The convergence of artificial intelligence, energy infrastructure, and digital assets is producing exactly the kind of long-duration, narrative-heavy, fundamentally contrarian investment thesis that VanEck was structurally built to capture. Datacenter power demand is creating a re-rating of nuclear, natural gas, and grid infrastructure. The proliferation of agentic AI is creating new compute architectures that may or may not favor incumbents. Stablecoins and tokenized real-world assets are creating an institutional on-ramp to the digital asset infrastructure that VanEck has spent a decade laying.

Each of those themes lives, in some form, on VanEck's product roadmap. Each is being built on top of a MarketVector index. Each is being underwritten with the assumption that the firm has another twenty years to be right.

The gold-bug dynasty's silicon bet was never about silicon, really. It was about the thesis that a small, private, family-controlled asset manager could survive, and occasionally thrive, by doing the exact opposite of what the giants do. By 2026, that bet had paid for itself many times over. The ticker SMH was no longer a quirky 2011 HOLDRS refurbishment. It was an institution.

Somewhere, John C. van Eck would have been quietly pleased. The man who once bet that the post-war American investor would learn to own foreign stocks had built a firm that, two generations later, taught the same investor to own the picks and shovels of the AI revolution.

The product changes. The playbook does not.

References

References

-

MarketVector US Listed Semiconductor 25 Index Methodology — MarketVector Indexes ↩↩↩↩↩↩

-

Jan van Eck: The Man Behind the $100 Billion ETF Firm — Bloomberg Wealth, 2023-01-12 ↩↩↩↩↩↩↩

-

Nvidia's Dominance in Semiconductor ETFs — Financial Times, 2024-02-15 ↩

-

Taiwan Semiconductor Manufacturing Co. (TSMC) Investor Relations — TSMC ↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube