SM Energy Company: The Permian Pivot

I. Introduction & Episode Roadmap

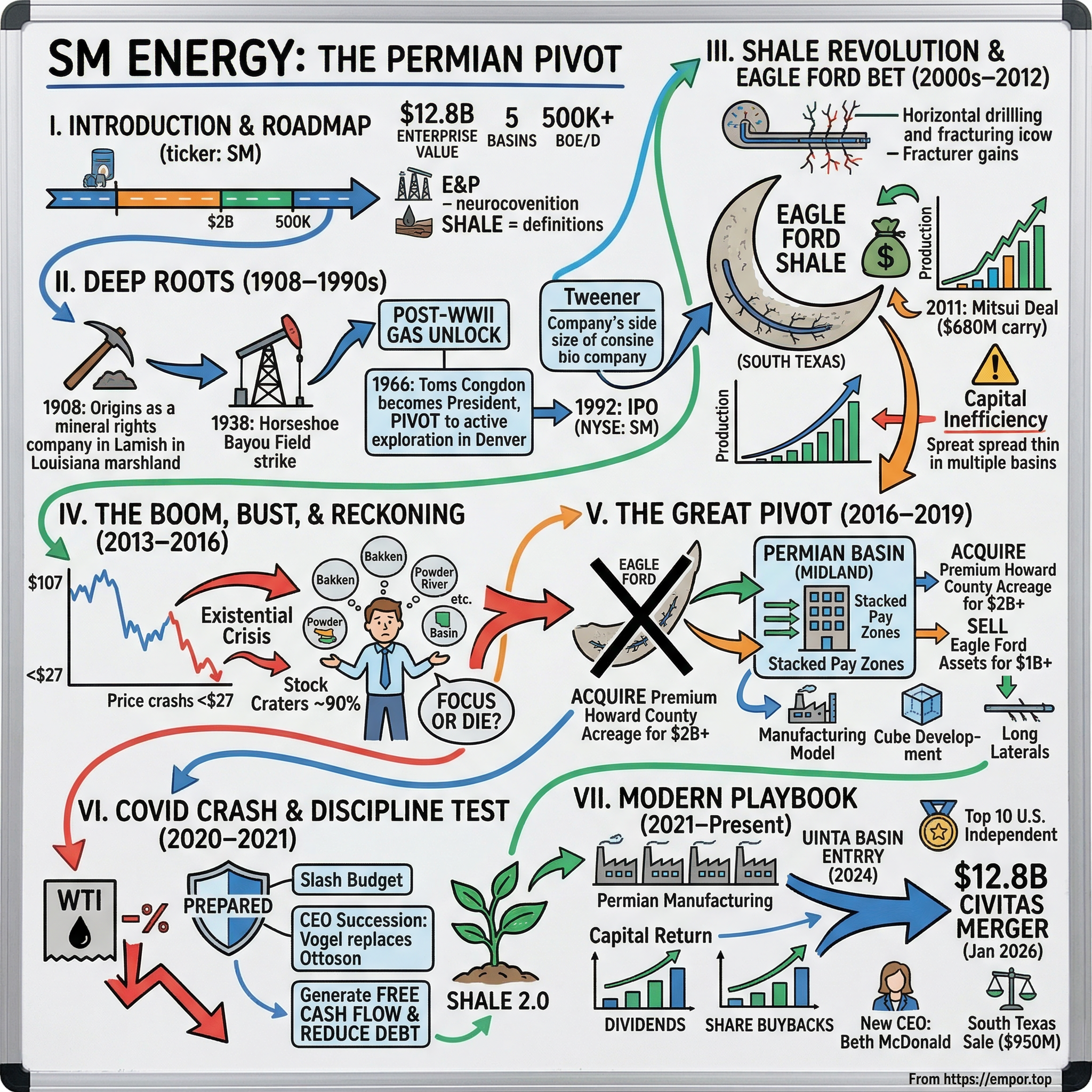

Picture a company that started in 1908 as a group of Minnesota mining magnates buying Louisiana marshland, survived two world wars, multiple oil busts, and a hundred-year transformation of the American energy industry — only to stake its entire future on a single geological basin in West Texas. That company is SM Energy, and its story is one of the most instructive corporate reinventions in the modern oil patch.

SM Energy trades on the NYSE under the ticker SM. As of early 2026, the combined company — following its transformational merger with Civitas Resources — commands an enterprise value of roughly $12.8 billion, operates across approximately 823,000 net acres spanning five basins, and produces over half a million barrels of oil equivalent per day. But those numbers obscure the far more interesting narrative: how a mid-tier, geographically scattered independent exploration and production company almost destroyed itself chasing growth, then engineered one of the sharpest strategic pivots in shale history to become a disciplined, returns-focused operator.

The hook is this: How did a 1908 Louisiana mineral rights company transform into one of the most efficient shale operators in America? The answer involves near-death experiences, radical portfolio surgery, a contrarian bet on the Permian Basin at exactly the right moment, and a management team that learned — the hard way — that in commoditized shale, only the lowest-cost, highest-conviction operators survive.

Three themes run through SM Energy's story. First, survival through volatility: this company has weathered oil crashes in 2008, 2014-2016, and 2020, each time emerging leaner and more focused. Second, the art of the pivot: SM Energy's willingness to sell its crown jewel assets at peak value and reinvest into a basin with superior long-term economics is a masterclass in strategic discipline. Third, geography is destiny in oil and gas: where your wells sit determines your cost structure, your inventory depth, and ultimately whether you survive or get acquired.

For those unfamiliar with the oil and gas industry's alphabet soup, a quick primer. E&P stands for exploration and production — these are the companies that find and extract oil and gas from the ground. "Independent" means SM Energy does not refine or sell gasoline; it only produces crude oil and natural gas and sells them to others. The Permian Basin, located in West Texas and southeastern New Mexico, is the single most important oil-producing region in the United States, responsible for roughly forty percent of all domestic crude production. And "shale" refers to the tight rock formations from which modern horizontal drilling and hydraulic fracturing extract hydrocarbons — a technology revolution that transformed American energy over the past two decades.

What makes SM Energy's story worth telling today is that it sits at a fascinating inflection point. The company just closed the largest deal in its history — the $12.8 billion all-stock merger with Civitas Resources in January 2026 — vaulting it into the top ten U.S. independent producers. A new CEO, Beth McDonald, took the helm on March 1, 2026. And the question every investor is asking is whether this company, forged through decades of adaptation, can maintain its edge at a scale it has never operated before.

II. Deep Roots: From Mineral Rights to Mid-Continent Wildcatting (1908–1990s)

The origin story of SM Energy does not begin in the oil fields. It begins in the offices of Chester Congdon, a Duluth, Minnesota attorney who had made his fortune in iron mines and copper claims across the upper Midwest and Arizona. In 1900, Congdon and four business partners — Guilford Hartley, David Adams, A.L. Ordean, and A.S. Chase — paid $11,000 to acquire 17,700 acres of marshland in St. Mary Parish, Louisiana, roughly eighty-five miles southwest of New Orleans.

The investors envisioned farming. The land had other plans. The marshes proved wholly unsuited to agriculture, and for years the partnership collected modest revenues from trapping licenses and livestock grazing. But Congdon and his partners had made one prescient decision that would prove extraordinarily valuable: they secured both surface and mineral rights when they bought the land. In an era before anyone imagined what lay thousands of feet below Louisiana's bayous, that seemingly mundane legal detail would become the foundation of a multi-billion dollar company.

The venture was formally incorporated as St. Mary's Parish Land Company, a Minnesota corporation, on April 15, 1908 — named not for any religious reference but for the Louisiana parish where the land sat. The company reincorporated in Delaware in early 1915 for greater corporate flexibility. For the next three decades, it functioned essentially as a passive holding company — collecting lease payments, managing surface rights, and waiting. This is a pattern that recurs throughout American resource history: patient capital that holds mineral rights through decades of uncertainty, only to be rewarded spectacularly when technology catches up to geology.

The transformative moment came on May 6, 1938, when the St. Mary No. 1 well struck oil at 9,910 feet, producing 335 barrels per day and anchoring what became known as the Horseshoe Bayou Field. Suddenly, the worthless marshland was sitting atop a producing oil reservoir. Atlantic Richfield subsequently developed the adjacent Bayou Sale Field in 1941, the same year St. Mary began paying cash dividends — a practice that would continue uninterrupted for decades. The mineral rights business model had proven spectacularly correct: own the subsurface, lease it to operators, collect royalties without bearing drilling risk.

Post-World War II pipeline infrastructure unlocked the natural gas potential of south Louisiana. By 1950, Sun Oil Company was leasing adjacent St. Mary lands and completed the company's first gas well in 1955. The business was profitable, steady, and entirely dependent on the geological luck of one Louisiana parish.

The modern era of the company began in 1966, when Thomas E. Congdon — Chester's grandson — became president. The fact that the company was still family-controlled nearly sixty years after its founding says something about the patience embedded in its DNA. Tom Congdon recognized that a single-parish mineral rights company had a ceiling — the Louisiana acreage, however productive, was finite, and the company needed to diversify both geographically and operationally to grow.

He relocated headquarters to Denver, Colorado — already emerging as the capital of America's independent oil industry — and began pursuing geographic diversification through drilling partnerships across the Rocky Mountains and Mid-Continent regions. This was the first strategic pivot in the company's history: from passive royalty collector to active exploration company. It would not be the last.

The next quarter-century saw St. Mary evolve into a conventional exploration and production outfit, operating vertical wells across Kansas, Oklahoma, the Texas Panhandle, and the Rockies. The economics were straightforward but demanding: identify promising geology, acquire mineral leases, drill vertical wells, and hope the reservoir delivered. Cycle times were long, geological risk was high, and success rates were modest. The company developed expertise in mid-continent geology but remained a "tweener" — too small to compete with the majors on capital and technology, too large to fly entirely under the radar.

On October 13, 1992, the company changed its name to St. Mary Land & Exploration Company and completed its initial public offering on the NASDAQ exchange under the ticker symbol MARY. The IPO opened new capital pathways for more aggressive exploration, but it also introduced the discipline — and the scrutiny — of public markets. For the first time, the Congdon family's patient, long-horizon approach would need to coexist with quarterly earnings expectations and stock price performance.

By the late 1990s, St. Mary Land & Exploration was a respectable but unremarkable mid-tier E&P company, generating steady returns from conventional vertical wells across the Rockies and Mid-Continent. The company had survived and grown for nearly a century on the strength of its mineral rights foundation and disciplined conventional exploration. But being a "tweener" independent — too small to compete with the majors on capital and technology, too large to be nimble like a private operator — was becoming increasingly difficult. The industry was consolidating, the easy conventional discoveries had been made, and the geological risk on each new vertical well was substantial.

What nobody at St. Mary could have predicted was that the conventional oil playbook that had served the company for decades was about to be rendered obsolete by a revolution brewing in the shale formations of north Texas. The company's next transformation would dwarf anything that had come before.

III. The Shale Revolution Arrives: Early Moves & The Eagle Ford Bet (2000s–2012)

To understand what happened to SM Energy in the 2000s, you need to understand what happened in a gritty stretch of north Texas in the late 1990s. George Mitchell, the tenacious founder of Mitchell Energy & Development, had spent nearly two decades and over $250 million trying to crack the code on extracting natural gas from the Barnett Shale — a dense, seemingly impermeable rock formation near Fort Worth that geologists had long dismissed as a source rock, not a reservoir. The conventional wisdom was that shale was where hydrocarbons were born, not where you went to produce them.

Mitchell's breakthrough, achieved through relentless experimentation with a technique called slickwater hydraulic fracturing, proved that conventional wisdom spectacularly wrong. For those unfamiliar with the technology, here is the simple version: traditional oil wells are drilled straight down, like pushing a straw through a layer cake. They access only the thin slice of rock that the wellbore passes through. Horizontal drilling changed the game by turning the wellbore sideways once it reached the target formation, running it horizontally through the productive layer for a mile or more — like laying a straw on its side through the richest layer of the cake. This exposed dramatically more rock to the wellbore. Then, hydraulic fracturing — pumping millions of gallons of water, sand, and chemicals at enormous pressure — cracked that rock open, creating pathways for oil and gas to flow into the wellbore.

By combining these two techniques, Mitchell demonstrated that America was sitting on vast reserves of oil and gas that had previously been considered unrecoverable. When Devon Energy acquired Mitchell Energy in 2002 for $3.5 billion and scaled up the technique across the Barnett, the shale revolution was born.

The implications rippled across the entire exploration and production industry. Suddenly, every company with acreage over a shale formation was scrambling to understand whether its land might contain unconventional resources. For a mid-tier independent like St. Mary Land & Exploration, the shale revolution presented both existential threat and extraordinary opportunity. The conventional vertical wells that had been the company's bread and butter were being superseded by a fundamentally different drilling model. But if the company could adapt, the prize was enormous.

SM Energy's initial response was to experiment across multiple shale plays — dipping its toe into several basins to evaluate which formations offered the best economics. In May 2010, the board took the symbolic step of renaming the company SM Energy Company, shedding the geographic constraints of the old St. Mary name and signaling that this was now a modern, multi-basin shale operator.

The big bet landed in the Eagle Ford Shale of South Texas. For non-geologists, the Eagle Ford is a crescent-shaped formation of organic-rich shale stretching roughly 400 miles across south Texas, buried thousands of feet underground. What made it special was its oil content: unlike many early shale plays that produced primarily natural gas (which was trading at depressed prices), the Eagle Ford contained significant crude oil — the higher-value hydrocarbon that every E&P company craved. The formation also sat beneath Texas, where the regulatory environment was friendly, permitting was fast, and decades of existing pipeline and refining infrastructure meant that any oil produced could reach market quickly.

SM Energy moved aggressively into the play between 2009 and 2012, targeting the wet-gas window in Webb County while also building non-operated positions in Dimmit and Maverick Counties through partnerships with larger operators like Anadarko.

By the third quarter of 2010, SM had two operated rigs running in the Eagle Ford, with nine wells spud and nine completed in just that quarter alone. The company allocated sixty percent of its entire drilling capital budget to the Eagle Ford and another twenty percent to the Bakken — an unmistakable signal about where management saw the future.

Then came a deal that turbocharged the build-out. In June 2011, SM Energy announced a $680 million carry agreement with a subsidiary of Mitsui & Co., the Japanese trading giant. Under the arrangement, Mitsui received a 12.5 percent working interest in SM's non-operated Eagle Ford position and in exchange agreed to pay ninety percent of SM's drilling and completion costs until $680 million had been spent on SM's behalf. Think about what that meant: SM Energy was essentially getting free drilling capital from a deep-pocketed Japanese partner to accelerate development of its best acreage. The deal closed in December 2011 and provided the rocket fuel for an aggressive scale-up.

The results were staggering. By mid-2012, SM's operated net Eagle Ford production averaged over 200 million cubic feet equivalent per day, up sixteen percent from just one quarter earlier. The company was drilling multi-well pads — twenty-six wells in just the first half of 2012 — developing acreage with a speed and efficiency that would have been unimaginable in the conventional era. At peak activity in 2013, the company drilled and completed ninety-five wells in the Eagle Ford with 246 net producing wells, driving quarterly production above 144,000 barrels of oil equivalent per day. The stock surged to an all-time closing high of $81.02 on November 26, 2013.

For context, that stock price represented a roughly tenfold increase from where the company had traded in the aftermath of the 2008 financial crisis. SM Energy had ridden the Eagle Ford from obscurity to shale stardom in less than four years. Wall Street loved the growth story. Analysts touted the company's production trajectory, its Texas-focused acreage, and the apparent abundance of remaining drilling locations.

SM Energy had become a shale success story. But success brought its own problems. The company now operated across multiple basins — Eagle Ford, Bakken, Permian, Powder River, Williston — each demanding capital, management attention, and operational resources. Geographic diversity looked like prudent risk management on paper. In practice, it was capital inefficiency dressed up as strategy. The company was spread too thin, competing for services and talent across too many geographies, and the returns on incremental wells were beginning to diverge meaningfully across basins. The seeds of the next crisis were already planted.

IV. The Boom, The Bust, and The Reckoning (2013–2016)

In retrospect, the period from 2011 to mid-2014 was the golden age of American shale drilling. Oil prices hovered above $90 per barrel for nearly four years, occasionally touching and surpassing $100. Wall Street was throwing capital at any E&P company with a growth story, and the metric that mattered most was production growth — not returns, not free cash flow, not capital discipline. The mantra was simple: drill baby, drill.

SM Energy was not immune to this intoxication. Like virtually every independent E&P of its era, the company was spending more than it earned, funding the difference with debt and equity issuance, and justifying it all with impressive production growth curves. The logic seemed unassailable: oil was above $90, well costs were coming down with scale, and the Eagle Ford was delivering spectacular initial production rates. Why would you slow down?

The answer, of course, is that the growth-at-all-costs model contained the seeds of its own destruction. When every company in an industry simultaneously increases production as fast as possible, supply eventually overwhelms demand — especially when that supply growth coincides with slowing economic growth in China and increased production from OPEC members. But in 2013, with stock prices rising and capital markets wide open, virtually no one in the E&P industry was sounding the alarm. The few contrarian voices that warned of overproduction were drowned out by the triumphalism of the shale boom.

The answer came in the second half of 2014, when oil prices began a collapse that would reshape the entire industry. The proximate cause was a geopolitical decision by Saudi Arabia. Faced with relentlessly growing American shale production that was eating into OPEC's market share, Saudi Arabia's oil minister Ali al-Naimi made a fateful choice at the November 2014 OPEC meeting: instead of cutting production to support prices — the cartel's traditional playbook — Saudi Arabia would maintain or even increase output, flooding the market to discipline the American shale upstarts. The Kingdom calculated, not unreasonably, that shale operators with high breakeven costs and heavy debt loads could not survive a sustained low-price environment.

The signal was clear, and the market reacted accordingly. WTI crude, which had been $107 in June 2014, fell below $50 by January 2015. It kept falling. By February 2016, oil traded below $27 per barrel — a seventy-five percent decline in eighteen months. Saudi Arabia was right about one thing: many shale operators could not survive. But it underestimated the resilience of the survivors and the speed at which they could cut costs.

For SM Energy, the crash exposed every vulnerability in the growth-at-all-costs model. The company had entered the downturn with a meaningful debt load accumulated during its Eagle Ford buildout, spread across too many basins with too little scale in any single one. Negative cash flow, debt covenant pressure, and a plummeting stock price created an existential crisis.

The numbers told a brutal story. From the all-time high of $81.02 in November 2013, SM Energy's stock cratered into the single digits during the worst of the 2016 downturn — a decline of roughly ninety percent. To put that in perspective: a shareholder who had invested $100,000 at the peak saw their position shrink to roughly $10,000 in barely two years. The dividend was suspended. Capital budgets were slashed. Drilling crews were laid off across the industry — not just at SM Energy but at virtually every independent E&P in the country. The company was fighting for survival.

For employees in the oil patch, the human toll was devastating. Entire drilling crews — roughnecks, derrickmen, company men — who had been working sixty-hour weeks during the boom suddenly had no work at all. Service companies that had been turning away business in 2013 were laying off thousands by 2015. The small towns of West Texas, South Texas, and North Dakota that had boomed with shale activity saw housing prices collapse and restaurants shutter. This was not an abstract financial downturn; it was a community-wide reckoning.

SM Energy was far from alone. The 2014-2016 oil crash produced the worst wave of E&P bankruptcies since the 1980s. According to the Haynes and Boone Oil Patch Bankruptcy Monitor, over 100 North American oil and gas producers filed for bankruptcy between 2015 and 2016, with aggregate debt exceeding $70 billion. Companies that had been stock market darlings just two years earlier were selling assets at fire-sale prices or disappearing entirely.

Management's response was necessarily aggressive. Asset sales accelerated, with non-core properties divested to raise cash and reduce debt. Operating costs were attacked from every angle — renegotiating service contracts with vendors who were themselves desperate for business, high-grading the drilling program to focus only on the highest-return wells, and cutting overhead to the bone. Every line item on the budget was scrutinized with the intensity of a company fighting for its life — because it was.

But cost-cutting alone could not solve the fundamental strategic problem: SM Energy was a $3-4 billion company trying to operate competitive positions in five different basins. Each basin required its own geological expertise, its own relationships with local service providers, its own supply chain, and its own management attention. The overhead of running five small operations was inherently higher per barrel than running one large one. The math did not work at $30 oil, and honestly, it barely worked at $60.

The existential question crystallized in the minds of CEO Jay Ottoson and his team: focus or die. In commoditized shale, where the product is undifferentiated and the only competitive advantages are cost structure and operational efficiency, having a mediocre position in five basins was worse than having a dominant position in one. The survivors of the shale bust would be companies that picked the best geography, concentrated capital, drove down costs through repetition and scale, and generated free cash flow rather than just production growth.

Ottoson, a Colorado School of Mines-trained chemical engineer who had spent sixteen years at ARCO before joining SM Energy as COO in 2006, understood this better than most. His ARCO background included stints running operations at Prudhoe Bay and in the Permian Basin — he knew what great rock looked like, and he knew the difference between good acreage and great acreage. The question was whether the board and the market would support a radical repositioning.

There is a pattern in commodity industries that plays out with metronomic regularity: high prices encourage overinvestment, overinvestment creates oversupply, oversupply crashes prices, and crashed prices force the weakest operators to sell or die. The 2014-2016 oil crash was this pattern at its most brutal. For SM Energy, it delivered the most important strategic lesson the company would ever learn: in a commoditized business, there is no prize for being average across many basins. There is only survival for being excellent in one.

The oil crash of 2014-2016 was the crucible that forged SM Energy's future strategy. The company that emerged from the wreckage would look nothing like the one that entered it.

V. The Great Pivot: Going All-In on the Permian (2016–2019)

The decision that defined SM Energy for the next decade was made in the darkest period of the oil bust. While competitors were hunkering down, slashing budgets, and praying for a price recovery, Jay Ottoson and his team were plotting one of the boldest strategic repositionings in independent E&P history: selling the Eagle Ford at peak value and going all-in on the Permian Basin.

To appreciate the audacity of this move, consider the context. SM Energy had spent half a decade and billions of dollars building its Eagle Ford position. The play had made the company. Analysts and investors associated SM Energy with the Eagle Ford the way they associated Pioneer with the Permian or Continental with the Bakken. Selling your signature asset while oil was trading in the $40s felt counterintuitive, even reckless. But Ottoson saw something that many of his peers missed: the Permian Basin's Midland sub-basin had fundamentally superior economics, and the window to acquire premium acreage there would not stay open forever.

The Permian advantage boiled down to geology. The Midland Basin features what geologists call "stacked pay zones" — multiple productive formation layers sitting on top of each other, like floors in an apartment building. Where the Eagle Ford offered one or two productive intervals, the Midland Basin offered six, eight, sometimes ten or more. This meant that a single surface location could access dramatically more oil and gas than a comparable Eagle Ford lease. Layer that on top of the Permian's superior infrastructure — decades-old pipeline networks, readily available water disposal, proximity to refineries — and you had a basin where breakeven costs were consistently lower and well economics consistently better.

SM Energy executed the pivot with remarkable speed. In August 2016, while oil was still below $50, the company acquired approximately 24,783 net acres in Howard County, West Texas, from Rock Oil Holdings for $980 million. Howard County sits in the heart of the Midland Basin — this was not fringe acreage; it was some of the best rock in North America. The deal added roughly 4,900 barrels of oil equivalent per day in production and expanded SM's Midland footprint to approximately 46,750 net acres.

Just two months later, in October 2016, SM announced a second transformational acquisition: approximately 35,700 net acres in Howard and Martin Counties from QStar LLC, a portfolio company of EnCap Investments, for approximately $1.1 billion in cash plus 13.4 million shares of SM common stock. Combined with the Rock Oil deal, SM Energy had committed roughly $2.08 billion to building a dominant Midland Basin position in the span of ninety days.

Then came the sell side. In January 2017, SM announced the sale of its non-operated Eagle Ford assets to Venado EF, an affiliate of KKR, for $800 million gross — with net cash proceeds of $754 million. The deal included approximately 37,500 net acres in the Maverick Basin and a 12.5 percent interest in the Springfield Gathering System. SM also divested a portion of its operated Eagle Ford position in a separate $225 million transaction. Combined, these sales generated over $1 billion in proceeds to fund the Permian build-out and reduce debt.

The timing was masterful. SM sold its Eagle Ford assets near the peak of their perceived value — when the play was still considered premium by the market — and deployed the capital into Permian acreage that was priced at what, in retrospect, turned out to be a generational low. The company was simultaneously selling high and buying low, the rare corporate transaction that looks even smarter with hindsight than it did at the time.

Within roughly twelve to eighteen months, SM Energy transformed from a multi-basin operator whose identity was tied to the Eagle Ford into a Permian-focused company with approximately 87,600 net acres in the Midland Basin. The portfolio had been radically simplified. Capital that had been scattered across five basins was now concentrated in one of the most prolific oil-producing regions on earth.

The pivot also coincided with — and was reinforced by — a broader industry shift. The 2014-2016 crash had fundamentally altered how investors valued E&P companies. Pre-crash, the market rewarded production growth above all else. Post-crash, investors punished companies that outspent their cash flow and rewarded those that demonstrated capital discipline, generated free cash flow, and returned capital to shareholders. SM Energy's new Permian-focused model was perfectly aligned with this shift.

Operationally, the company embraced what the industry calls the "manufacturing model" — treating well drilling not as exploration but as a repeatable industrial process. In the Midland Basin, SM began drilling longer laterals, initially two miles and eventually pushing toward three miles, which dramatically improved per-well economics by spreading fixed costs over more productive rock. Drilling cycle times fell as crews gained experience on the same acreage, and completion designs were continuously optimized to maximize initial production rates and ultimate recovery.

The concept of "cube development" became central to SM's approach. Rather than drilling individual wells, the company developed entire blocks of acreage simultaneously — drilling multiple wells from a single pad, targeting different formation layers at different depths, and completing them in coordinated sequences. This reduced surface disruption, improved logistics, and allowed for better reservoir management.

There is a useful analogy here from manufacturing. Toyota's production system — the famous Toyota Way — is built on the principle that eliminating variation and standardizing processes produces superior quality at lower cost. SM Energy was essentially building the Toyota factory of oil wells. Every well was drilled using the same basic playbook, refined incrementally based on data from the previous wells. This was as far from the wildcatting culture of the company's first century as you could possibly get — and it was exactly right for the Permian's geology.

By 2019, SM Energy had emerged as a fundamentally different company: leaner, more focused, and increasingly respected by investors who valued discipline over growth. The Permian pivot had worked. But the ultimate test was yet to come.

VI. COVID Crash and The Discipline Test (2020–2021)

On April 20, 2020, something happened that no oil industry veteran had ever imagined possible: the price of West Texas Intermediate crude oil went negative. Not just low. Negative. Producers were literally paying buyers to take their oil off their hands, because storage tanks at Cushing, Oklahoma — the delivery point for WTI futures contracts — were nearly full and there was simply nowhere left to put it. The May 2020 futures contract settled at negative $37.63 per barrel, a number that would have seemed like science fiction six months earlier.

Global oil demand had cratered overnight as COVID-19 lockdowns shuttered economies worldwide. Flights were grounded. Cars sat in driveways. Factories went dark. In the span of weeks, roughly thirty percent of global oil demand simply vanished. For the second time in five years, SM Energy faced an existential crisis.

But this time, the company was better prepared. The Permian pivot had given SM a cleaner balance sheet, better-quality assets, and operational efficiency that its pre-2016 self could not have imagined. When the pandemic hit, SM Energy entered 2020 with a capital budget of approximately $825-850 million. Within weeks, management slashed that budget by roughly twenty percent and kept cutting. By the time the dust settled, full-year 2020 capital expenditure landed at approximately $605-610 million — a reduction of nearly thirty percent from the original plan.

The cuts were painful. Executive salaries were reduced. All employee compensation increases were postponed. Drilling crews were released. The company ran a minimal program, focused exclusively on its highest-return Midland Basin wells, and preserved every dollar of liquidity it could.

CEO Jay Ottoson, who had architected the Permian pivot and navigated the company through the 2014-2016 crisis, announced his retirement effective November 2, 2020. His successor was Herb Vogel, a University of Colorado-trained mechanical engineer who had spent his career at ARCO and BP before joining SM Energy in 2012. Vogel had risen through the ranks from SVP of Portfolio Development to COO, and he understood the company's assets and operations intimately. He also understood that the crisis — as brutal as it was — had validated the strategic choices of the prior five years.

The results proved the point. Despite the savage capital cuts, SM Energy generated $239.5 million in free cash flow during full-year 2020 — a remarkable achievement for a company that had slashed its drilling program in the teeth of the worst oil market in modern history. Even more impressively, the company reduced its long-term debt by $492 million during 2020, from $2.77 billion to $2.28 billion. Cash flow and debt reduction both exceeded management's own expectations.

Full-year 2020 production came in at approximately 123,500-126,200 barrels of oil equivalent per day — lower than pre-COVID levels but far from catastrophic. The company had bent but not broken.

The recovery, when it came, was swift. Oil prices rebounded through late 2020 and into 2021 as vaccines rolled out and demand returned. But the industry that emerged from COVID was fundamentally transformed. The pre-2014 playbook of drill-everything, grow-at-all-costs was dead. In its place arose what commentators called "Shale 2.0" — a new paradigm where E&P companies prioritized returning capital to shareholders over production growth, maintained discipline even as prices recovered, and treated investors as partners rather than ATMs.

SM Energy was among the first mid-cap independents to embrace this new philosophy. Under Vogel's leadership, the company launched share buyback programs, continued reducing debt, and maintained relatively flat production rather than chasing growth. The message to the market was clear: the days of spending every dollar on drilling are over. This company will generate free cash flow and return it to shareholders.

There is a Warren Buffett maxim that applies here: "Only when the tide goes out do you discover who's been swimming naked." The COVID crash was the ultimate tide going out, and SM Energy was wearing a suit. The Permian pivot, executed four years earlier when the decision seemed risky, had given the company higher-quality assets with lower breakeven costs, which in turn allowed it to generate positive cash flow even in the most hostile oil price environment since the 1990s. The balance sheet improvements of 2017-2019, which had come at the cost of growth, provided the financial cushion to absorb the shock without tripping debt covenants or being forced into distressed asset sales.

Companies that entered the pandemic overleveraged and geographically scattered did not survive — many were acquired at distressed valuations or pushed into bankruptcy. Callon Petroleum, Extraction Oil & Gas, Whiting Petroleum, and dozens of others either filed for bankruptcy or were absorbed by stronger operators during the 2020-2021 period. SM Energy, by contrast, emerged stronger, with a cleaner balance sheet and a reinforced commitment to discipline.

The transition from Jay Ottoson to Herb Vogel in November 2020 was remarkably smooth — unusual in a CEO succession during a crisis. Ottoson had built the strategic foundation; Vogel would execute the next phase. The baton passed without disruption, a credit to both men and to the clarity of the strategy they shared.

VII. The Modern Playbook: Permian Manufacturing & Capital Return (2021–Present)

By 2022, SM Energy had completed its transformation from a growth-obsessed multi-basin driller into a disciplined, returns-focused Permian operator. The company's Midland Basin position encompassed over 82,000 net acres of premium rock in Howard and Martin Counties — the heart of the most prolific oil basin in the Western Hemisphere. Every dollar of capital was flowing into repeatable, predictable, manufacturing-style development.

The "manufacturing" mentality deserves explanation, because it represents a fundamental shift in how modern shale companies operate. In the early days of the shale revolution, drilling was still partly exploratory — operators were learning the formations in real-time, experimenting with well spacing, lateral lengths, and completion designs. By the early 2020s, the Midland Basin had matured to the point where SM Energy could predict, with remarkable accuracy, what a new well would produce based on its location, target formation, and completion design.

Think of it like a factory. The inputs are known: drill bit, casing, fracturing fluid, proppant. The process is standardized: drill horizontally for two-plus miles, fracture the rock in precise stages, flow back the well, put it on production. The outputs are predictable: a defined initial production rate that declines along a known curve. SM Energy's job was to run this factory as efficiently as possible — shaving days off drilling times, optimizing fracture designs to maximize recovery, and managing the supply chain to keep costs low.

Technology played an increasingly central role. Real-time drilling data allowed engineers to make adjustments on the fly, steering wellbores through the most productive zones with precision measured in feet. Completion designs evolved continuously — the optimal number of fracture stages, the volume and composition of fluid, the type and amount of proppant sand pumped downhole. Each generation of wells tended to outperform the last, not because the rock was getting better but because the company was getting better at extracting hydrocarbons from it.

The financial results reflected this operational machine. SM Energy's breakeven costs fell below $40 per barrel — meaning the company could generate positive returns even if oil prices dropped well below prevailing levels. To contextualize that number: a $40 breakeven in the Permian Basin is roughly analogous to having the lowest manufacturing cost in an industry. When oil trades at $70, a company with $40 breakevens earns a $30 margin on every barrel, while a competitor with $55 breakevens earns only $15. And when oil drops to $45, the $40 breakeven company is still making money while the $55 company is bleeding cash. In a commodity business, cost structure is destiny.

In the third quarter of 2022, the board approved a formal return of capital strategy: a $500 million share repurchase authorization through year-end 2024 and an increased fixed dividend of $0.60 per share annually. These were not token gestures; they signaled a fundamental reorientation of capital allocation priorities. For the first time in its modern history, SM Energy was formally committing to return a meaningful share of its cash flow to shareholders rather than reinvesting every dollar into drilling.

But Herb Vogel was also thinking about the next phase of growth. By 2023, a quiet concern was spreading through the Permian: inventory depth. Every shale well has a finite productive life, and every acre of leasehold contains a finite number of drilling locations. The best operators — those who had been drilling aggressively for a decade — were beginning to see their premium inventory thin out. The question was not whether SM Energy had enough locations to drill today, but whether it would have enough in five or ten years.

Vogel's answer was to look beyond the Permian. In 2024, SM Energy made its most significant acquisition in nearly a decade: a $2.55 billion deal to acquire XCL Resources and affiliated entities in Utah's Uinta Basin. SM took an eighty percent interest for approximately $2.04 billion, with Northern Oil and Gas acquiring the remaining twenty percent. The Uinta assets comprised 37,200 net acres producing approximately 43,000 barrels per day — eighty-eight percent oil, a strikingly rich crude mix. SM subsequently exercised an option for an additional 26,100 adjacent acres, bringing total Uinta net acreage to approximately 63,700.

The Uinta deal was strategic on multiple levels. It provided SM with a third productive basin — diversifying inventory risk without reverting to the unfocused multi-basin model of the pre-2016 era. The Uinta Basin crude is a waxy, high-gravity oil that commands premium pricing in certain refining markets, particularly those configured to process heavier crude streams. And critically, the basin was significantly less competed-over than the Permian, where acquisition multiples had been bid up to eye-watering levels by Exxon, Chevron, and other majors flush with cash. By going to a less fashionable basin where competition was thinner, SM was applying the same contrarian logic that had served it during the Permian pivot: buy quality assets where the crowd is not looking.

Full-year 2024 results were records across the board. Total production hit 170.5 thousand barrels of oil equivalent per day, up twelve percent from 2023, with oil production jumping twenty-three percent. Adjusted EBITDAX reached $2.0 billion. Cash flow from operations exceeded $1.77 billion. The company generated $485 million in adjusted free cash flow while spending $1.29 billion on capital expenditures — drilling 142 net wells and completing 135. Year-end proved reserves reached 678 million barrels of oil equivalent, with a reserves-to-production ratio of nearly eleven years.

The dividend was increased to $0.80 per share annually, and the share repurchase program was reloaded with a fresh $500 million authorization. SM Energy was delivering on the shareholder return promise while simultaneously expanding its asset base.

Then came the deal that changed everything — the kind of transformational merger that redefines a company's identity. On November 3, 2025, SM Energy and Civitas Resources announced a definitive all-stock merger valued at approximately $12.8 billion. Civitas, based in Denver like SM, had been assembled through its own series of acquisitions in Colorado's DJ Basin — making it the dominant operator in that play. Each Civitas share would be exchanged for 1.45 SM Energy shares, giving Civitas shareholders roughly fifty-two percent ownership of the combined entity. Both sets of shareholders approved the merger at special meetings on January 27, 2026, and the deal closed on January 30, 2026. The combined entity became a top-ten U.S. independent producer with approximately 823,000 net acres across five basins — the Permian, the DJ Basin in Colorado (Civitas's flagship), the Eagle Ford, the Uinta, and Midland Basin extensions. Pro forma production guidance pointed toward 650,000-700,000 barrels of oil equivalent per day, with anticipated annual synergies of at least $200 million by 2027 and potential for an additional $100 million beyond that.

The merger also brought a significant capital structure change. SM issued $1.0 billion in new 6.625% senior notes due 2034 to support the combined entity, and amended its revolving credit facility, lifting the borrowing base to $5.0 billion, expanding the bank group to eighteen institutions, and extending the maturity to 2031. The capital markets, clearly, believed in the combined company's creditworthiness. The company also announced a target of at least $1 billion in asset divestitures within the first year of closing to reduce post-merger leverage.

The combined entity retained the SM Energy name and NYSE ticker. Herb Vogel retired on March 1, 2026, and Beth McDonald — a twenty-year Pioneer Natural Resources veteran who had joined SM as COO in September 2024 — stepped in as President and CEO at age forty-six.

The company also moved quickly to optimize the combined portfolio. In March 2026, SM announced the sale of certain South Texas assets to Caturus Energy for $950 million — approximately 61,000 net acres and 260 producing wells in Webb County. The proceeds were earmarked primarily for debt reduction, addressing the leverage that inevitably accompanied a $12.8 billion merger. Full-year 2025 results — the last year reflecting primarily legacy SM operations — showed record production of 206.8 thousand barrels per day, adjusted EBITDAX of $2.26 billion, and adjusted free cash flow of $620 million. Net debt-to-EBITDAX improved to 1.05 times.

The question for investors now is whether the combined SM Energy can maintain the operational excellence and financial discipline that defined the standalone company — but at more than triple the scale. The remaining challenges are real: commodity price exposure that no operational efficiency can fully offset, inventory depth questions that grow more pressing with each passing year, ESG pressures that limit certain investors' willingness to hold fossil fuel equities, and the integration complexity of merging two significant organizations with different cultures, systems, and geographies.

VIII. The Competitive Landscape & Industry Dynamics

SM Energy's competitive position changed fundamentally with the Civitas merger. Pre-deal, the company was a roughly $6 billion market cap Midland Basin specialist — respected for its operational execution but subscale relative to the Permian's dominant players. Post-deal, it operates across 823,000 net acres producing over half a million barrels per day, placing it in the same conversation as Diamondback Energy, Devon Energy, and Coterra.

Consider the scale comparison, because scale matters enormously in the modern oil business. Diamondback Energy, following its landmark acquisition of Endeavor Energy in September 2024 for $26 billion, now controls over 722,000 net acres in the Midland Basin alone and produces north of 570,000 barrels of oil equivalent per day. Diamondback has become, in many ways, the company that SM Energy might aspire to be — a focused Permian operator with dominant scale in the basin's core.

EOG Resources, the gold standard for operational efficiency among independents, operates a diversified multi-basin portfolio producing roughly 700,000 barrels per day with one of the strongest balance sheets in the industry. EOG is famous for its proprietary technology culture — a belief that developing drilling and completion innovations in-house, rather than relying on service companies, provides a durable cost advantage. ConocoPhillips, which acquired Marathon Oil in 2024, has become a global super-independent with production approaching two million barrels per day.

And then there are the true behemoths: Exxon, which absorbed Pioneer Natural Resources in its $60 billion megadeal, and Chevron, which is digesting its own string of acquisitions. These are companies with market capitalizations measured in hundreds of billions, balance sheets that can weather any downturn, and the ability to deploy capital at a scale that no independent can match.

Against this backdrop, the combined SM Energy occupies an interesting middle ground. At roughly 650,000-700,000 barrels per day of guided production and an enterprise value of $12.8 billion, it is large enough to matter — to attract institutional capital, to negotiate favorable terms with service providers, and to justify the infrastructure investments that drive down per-unit costs. But it is still meaningfully smaller than the mega-independents and integrated majors that have come to dominate the Permian through the consolidation wave of 2023-2025.

The advantages of being in this middle weight class are real but nuanced. SM Energy can still high-grade its inventory — focusing capital on the very best locations rather than being forced to drill lower-quality wells to feed a massive production machine. Management remains closer to the rock, with shorter decision-making chains and less bureaucracy than a $200 billion integrated major. And the company's diversified basin exposure — Permian, DJ, Uinta, Eagle Ford — provides some hedge against basin-specific risks like regulatory changes or infrastructure bottlenecks.

The disadvantages are equally real. Cost of capital is higher for a mid-cap independent than for an investment-grade major. Acquisition firepower is limited — SM Energy cannot outbid Exxon or Chevron for the next transformational deal. And in a basin as consolidated as the Permian has become, the remaining independents must be exceptional operators to justify their independence. Mediocrity is a death sentence; you will simply be acquired, likely at a price below what you believe your assets are worth.

The M&A dynamics of the last three years illuminate this reality starkly. Exxon's $60 billion acquisition of Pioneer Natural Resources — the deal that sent shockwaves through the industry in 2023 and signaled that even the most successful independents were not safe from the majors' consolidation appetite. Chevron's $7.6 billion purchase of PDC Energy, which added DJ Basin scale. Occidental's $12 billion CrownRock deal in the Permian. Diamondback's $26 billion Endeavor acquisition. Each deal reduced the number of independent Permian operators and increased the scale of the survivors. The implication was clear: in the modern Permian, you are either big enough to compete with the majors or you will eventually be absorbed by one.

SM Energy's own merger with Civitas was, in part, a response to this consolidation pressure — a recognition that standing still at the old scale was not a viable long-term strategy.

The question that hangs over every remaining independent is stark: can you compete with the majors on a sustained basis, or is consolidation inevitable? The answer may depend on what you mean by "compete." If the question is whether a mid-cap independent can generate comparable returns on capital to an integrated major in a supportive oil price environment, the answer is clearly yes — SM Energy's returns have been competitive with much larger peers in recent years. But if the question is whether a mid-cap independent can survive a sustained multi-year downturn as well as an Exxon or Chevron with $30 billion in annual cash flow and AAA-rated balance sheets, the answer is far less certain.

SM Energy's answer, through its actions, has been to grow through disciplined acquisition, maintain operational excellence, and return enough capital to shareholders to justify its independence. Whether that answer proves durable through the next cycle remains to be seen.

Matador Resources, focused on the Delaware Basin sub-basin of the Permian, represents a different approach — smaller, more concentrated, with meaningful midstream infrastructure ownership that provides a margin buffer when commodity prices weaken. Laredo Petroleum, concentrated in Howard County, occupies the role that SM Energy used to fill as a smaller-scale Midland Basin operator. Each company is making its own bet on the optimal scale and geographic focus for an independent E&P. Devon Energy, which merged with WPX Energy in 2021, represents the path of scale-through-merger that SM Energy has now followed with Civitas.

The broader dynamic is that the Permian Basin has evolved from a fragmented landscape of hundreds of operators into an increasingly oligopolistic structure dominated by a handful of very large players. Rising barriers to entry — the best acreage is spoken for, regulatory costs are increasing, and the capital required to operate efficiently grows with each technology cycle — mean that the competitive landscape will likely continue to consolidate. The question is not whether further consolidation will occur, but when and at what price.

IX. Strategic Frameworks: Porter's Five Forces & Hamilton's Seven Powers

Understanding SM Energy's competitive position requires moving beyond financial metrics to examine the structural forces that shape the industry and determine which companies can generate sustainable returns. Two frameworks — Michael Porter's Five Forces and Hamilton Helmer's Seven Powers — illuminate the challenge and the limited sources of competitive advantage available to an independent oil producer. Together, they paint a picture that is sobering for any E&P investor but instructive for understanding what separates the survivors from the casualties.

Threat of New Entrants: Medium-Low. Building a credible Permian Basin operator from scratch is extraordinarily difficult today. The capital requirements are measured in billions, not millions. The best acreage has been locked up through decades of leasing and acquisition. Technical expertise in horizontal drilling and multi-stage hydraulic fracturing takes years to develop. And the regulatory and environmental compliance burden — particularly in Colorado's DJ Basin, where SM now operates extensively post-merger — creates additional barriers. However, the threat is not zero: private equity-backed E&P companies regularly assemble Permian acreage positions, operate them for several years, and then sell to larger players. This private equity recycling machine ensures that competitive pressure persists even if traditional new entry is difficult.

Bargaining Power of Suppliers: Medium. SM Energy's primary suppliers are oilfield service companies — the drillers, fracturers, and equipment providers that execute the physical work of extracting hydrocarbons. These are the companies that own the drilling rigs, the frac fleets, and the specialized equipment without which no E&P company can produce a single barrel of oil.

This market is cyclical and somewhat oligopolistic, dominated by firms like SLB (formerly Schlumberger), Halliburton, and Liberty Energy. When oil prices are high and drilling activity surges, service companies gain pricing power and can push costs higher — sometimes dramatically. The 2022 oil price surge, for example, saw service costs rise twenty to thirty percent as every E&P company competed for limited rigs and frac crews. When activity declines, the dynamic reverses and E&P companies can renegotiate aggressively.

SM Energy's post-merger scale provides some bargaining leverage — a half-million-barrel-per-day producer commands more attention from service companies than a 100,000-barrel operator. But no single E&P company, short of the integrated majors, has truly transformative purchasing power.

Bargaining Power of Buyers: High. This is the fundamental challenge of the oil business. SM Energy is a price taker. The company sells a global commodity — crude oil and natural gas — at prices determined by supply and demand dynamics that it cannot influence. No amount of operational excellence changes the fact that SM Energy's realized oil price is essentially set by OPEC decisions, global economic growth, and geopolitical events. Downstream buyers — refiners, midstream companies, commodity traders — have abundant choices and face essentially zero switching costs.

Threat of Substitutes: High and Rising. The electrification of transportation, the growth of renewable energy, and tightening carbon regulation represent long-term structural threats to oil demand. The timeline is debated endlessly — some analysts see peak oil demand this decade, others push it to the 2040s — but the directionality is not in doubt. For SM Energy, this creates a capital allocation challenge: every dollar invested in new drilling is a bet that oil demand will remain robust for the twenty-to-thirty-year productive life of that well. The ESG movement has also narrowed SM's potential investor base, as certain institutional investors restrict or eliminate fossil fuel holdings. This is a material consideration: when a meaningful segment of the global investment community refuses to buy your stock on principle, your cost of equity capital is structurally higher than it would otherwise be.

Industry Rivalry: Very High. This is the most important force. SM Energy competes in one of the most intensely rivalrous industries on earth. The product is undifferentiated — a barrel of SM Energy's Midland Basin oil is functionally identical to a barrel of Diamondback's. Competition occurs on cost structure, operational efficiency, and capital allocation — variables that are important but incremental, not transformative. In a high oil price environment, nearly every Permian operator generates strong returns. In a low price environment, the lowest-cost producers survive and everyone else suffers. There is no loyalty, no brand, no lock-in. Just relentless competition for margins measured in single-digit dollars per barrel.

Turning to Hamilton Helmer's Seven Powers framework — which asks a different and arguably more important question than Porter. Porter asks about the structure of the industry. Helmer asks: does this specific company have a durable source of competitive advantage that allows it to earn persistent above-market returns? For SM Energy, the picture is sobering but honest.

Scale Economies exist but are limited. The combined post-merger SM Energy enjoys some benefits from operating a large, contiguous acreage position: shared infrastructure like water recycling facilities and tank batteries, bulk purchasing of services and materials, and the ability to run simultaneous operations across multiple pads. These drive down per-unit costs — perhaps by five to ten percent relative to a much smaller operator.

But the scale advantages are modest compared to truly dominant scale players like Diamondback or Exxon's Permian operations, and they are categorically different from the exponential scale economies found in software or network businesses. Google's cost to serve its billionth search query is essentially zero; SM Energy's cost to drill its thousandth well is roughly the same as its hundredth. In E&P, scale provides linear cost benefits, not exponential ones.

Network Effects are nonexistent. Oil production has no network dynamics — SM Energy's product does not become more valuable as more producers enter the market. If anything, the opposite is true: more production means more supply, which means lower prices. This is the fundamental inversion of the network effects that make technology companies so valuable.

Counter-Positioning provides an interesting historical lens. SM Energy's decision to sell its Eagle Ford assets when the rest of the industry still coveted the play was a form of counter-positioning — an incumbent's (the market's) inability to recognize that the Permian was the superior long-term bet. But counter-positioning is only durable when the incumbent structurally cannot imitate you. In E&P, any company with capital can eventually acquire Permian acreage, so this advantage was temporary.

Switching Costs are zero. Buyers of SM Energy's oil can switch to any other producer's oil with no friction, no cost, and no loss of functionality.

Branding is irrelevant. Oil is the ultimate commodity — no one cares who produced the barrel.

Cornered Resource is perhaps SM Energy's strongest power, though it is moderate rather than strong. The specific Midland Basin, DJ Basin, and Uinta Basin acreage that SM controls represents a finite, non-replicable resource. Another operator cannot drill SM's wells — those specific geological locations, with their specific rock characteristics and formation depths, are exclusively SM's. This is a real form of competitive advantage: you cannot create new Midland Basin acreage; what exists is what exists, and SM owns a meaningful portion of it.

But acreage is finite in two senses. First, at current development pace, SM's proved reserves represent roughly eleven years of production. Second, while the rock is excellent, it is not so unique that comparable quality cannot be found elsewhere in the Permian — Diamondback, EOG, and others control similar-quality acreage. The cornered resource power is real but bounded.

Process Power is where SM Energy has invested most heavily — and where its competitive edge, while real, is perpetually at risk. The company's drilling and completion efficiency, its manufacturing-style development approach, and its continuous improvement culture produce measurable cost advantages. Drilling cycle times have fallen consistently over the past five years. Well productivity has improved as completion designs have been optimized. Per-unit costs remain competitive with or below larger peers.

But process advantages in E&P are fundamentally copyable — and this is the critical distinction from true Process Power in Helmer's framework. Best practices diffuse through the industry with remarkable speed, carried by engineers who move between companies, by service companies that share techniques across clients, and even by investor presentations that reveal operational details in pursuit of stock price appreciation. The drilling technique that gives SM Energy a six-month cost advantage today is likely to be replicated by Diamondback and Matador within a year. Maintaining a process edge requires relentless investment in improvement — standing still is falling behind.

The honest assessment is that SM Energy operates in a structurally challenging industry with few durable competitive advantages in Helmer's framework. No oil company, no matter how well-run, possesses the kind of economic moat that a software platform or a pharmaceutical company with patent protection enjoys. This is not a criticism of SM Energy's management — it is a structural reality of the commodity extraction business. The best oil companies are not good because they have moats; they are good because they execute relentlessly in an industry that punishes even momentary lapses.

Success in E&P requires continuous execution across four dimensions: superior asset positioning, operational excellence, financial discipline, and — increasingly — the option value of being acquired at the right price by a larger player. SM Energy has demonstrated all four at various points in its history. The challenge is maintaining all four simultaneously, through multiple commodity cycles, without a single misstep severe enough to be existential. That is the fundamental difficulty of being an independent oil producer, and it is why the industry's history is littered with companies that were excellent for a decade and then disappeared.

X. Bull vs. Bear Case & Investment Considerations

The Bull Case

Start with the assets. SM Energy's post-merger portfolio — 823,000 net acres across the Permian, DJ Basin, Eagle Ford, and Uinta — represents one of the most diversified, high-quality acreage positions among independent E&P operators. The Midland Basin core delivers sub-$40 breakeven economics. The DJ Basin, inherited from Civitas, offers long-duration inventory in Colorado's Niobrara and Codell formations. The Uinta Basin provides a differentiated crude stream at attractive economics. This is not a one-basin company anymore; it is a multi-basin platform with optionality.

Operational execution has been consistently strong. SM Energy has demonstrated the ability to drive down drilling cycle times, optimize completion designs, and generate industry-competitive well productivity. The manufacturing model — repeatable, predictable, continuously improving — produces the kind of consistent results that enable confident capital allocation.

The capital return framework is well-established. The company has committed to returning a meaningful share of free cash flow to shareholders through fixed dividends, share repurchases, and opportunistic buybacks. Full-year 2025 adjusted free cash flow of $620 million, with $104 million returned to shareholders, demonstrates the engine is functioning.

Valuation tells an interesting story. At a stock price in the mid-$20s range — with shares trading between roughly $25 and $26 in early March 2026 against a fifty-two week range of $17.45 to $32.26 — the post-merger SM Energy trades at a free cash flow yield that is attractive relative to the broader market. This is a common characteristic of E&P companies, reflecting both the genuine opportunity and the market's persistent skepticism of oil companies' ability to sustain returns across commodity cycles. E&P stocks have, over the past decade, consistently traded at discounted valuations relative to the S&P 500, a reality that partly reflects the industry's historical tendency to destroy shareholder value through overleveraged growth and partly reflects the energy transition overhang.

The $200 million-plus in annual merger synergies expected by 2027 provide a near-term catalyst that is largely within management's control. And the ongoing divestiture program — anchored by the $950 million South Texas sale — should bring post-merger leverage down to more comfortable levels.

Finally, there is the takeout premium. In a consolidating Permian Basin, a well-run independent with 650,000-700,000 barrels per day of production, premium acreage, and a clean balance sheet is an attractive acquisition candidate for any major looking to add scale. Whether SM Energy is ultimately acquired is unknowable, but the optionality has value. The precedent set by Exxon's acquisition of Pioneer at a roughly thirty percent premium to the unaffected stock price suggests that well-run Permian independents can command meaningful premiums in takeout scenarios.

The Bear Case

Start with the fundamental structural reality: SM Energy has no durable competitive moat. Oil is a commodity. Operational advantages are temporary and copyable. There is no pricing power, no switching costs, no network effects, and no brand value. The company's fortunes are inextricably linked to global oil prices, which are set by OPEC, macroeconomic conditions, and geopolitical events that SM cannot influence or predict.

Inventory depletion is a slow-moving but inevitable risk. Every well drilled depletes the company's finite inventory of premium drilling locations. Year-end 2025 proved reserves of 673 million barrels of oil equivalent, at current production rates, represent roughly nine to ten years of supply. Probable and possible reserves extend this runway, but the quality of locations tends to decline as the best are drilled first. Without continuous acquisition, inventory quality will erode over time.

The energy transition, while uncertain in its timing, represents a genuine long-term threat to oil demand. Electric vehicle adoption is accelerating globally. Renewable energy costs continue to fall. Climate regulation is tightening. The IEA's central scenarios show oil demand plateauing and eventually declining, though the exact timing ranges from the 2030s to the 2050s depending on assumptions. For a company whose assets have twenty-to-thirty-year productive lives, this uncertainty matters.

Post-merger integration risk should not be underestimated. Combining two companies with different cultures, different operating systems, and different geographic focuses is complex and can destroy value even when the strategic logic is sound. The Civitas merger added the DJ Basin — a play with its own regulatory challenges in Colorado — and expanded SM's organizational complexity significantly.

Leverage is elevated following the merger. While the company is actively deleveraging through the South Texas asset sale and debt reduction efforts, the post-merger balance sheet carries significantly more debt than the standalone SM Energy did in 2025. In a sustained oil price downturn, this leverage could become a vulnerability.

And there is the simple mathematical reality of capital intensity in shale. Shale wells decline rapidly — a new well might produce 1,000 barrels per day in its first month but only 200 barrels per day after a year. This steep decline curve means that SM Energy must continuously invest billions in new drilling just to maintain its current production level. Stop drilling, and production falls off a cliff. This "Red Queen" effect — named after the Lewis Carroll character who must run constantly just to stay in the same place — limits the amount of free cash flow that can actually be returned to shareholders. Unlike a software company that generates marginal revenue at near-zero cost, SM Energy's revenue stream requires constant, capital-intensive replenishment.

There is also the risk that the Civitas integration proves more difficult than anticipated. Merging two E&P companies involves harmonizing drilling programs, rationalizing overlapping overhead, integrating IT systems, and — perhaps most challenging — blending corporate cultures. Civitas was a Colorado-born DJ Basin operator; SM Energy was a Denver-headquartered Permian specialist. The geographies, regulatory environments, and operational characteristics of their respective assets differ meaningfully. History shows that E&P mergers frequently destroy value through integration stumbles, even when the strategic rationale is sound.

Key Performance Indicators to Watch

For investors tracking SM Energy's ongoing performance, three metrics matter most.

First, free cash flow per barrel of oil equivalent produced. This single number captures the intersection of commodity prices, operating costs, capital efficiency, and production volumes. It tells you how much cash the company is generating for each unit of production — the truest measure of value creation in E&P. Tracking this metric over time, and comparing it to peers, reveals whether SM Energy is maintaining its operational edge or falling behind.

Second, net debt-to-EBITDAX. Leverage is the primary survival variable in a cyclical commodity business. The company that enters a downturn with low leverage survives; the company that enters overleveraged does not. SM Energy's year-end 2025 ratio of 1.05 times is comfortable, but the post-merger combined entity will carry higher debt until divestitures and organic cash flow bring it down. Watching this ratio normalize — ideally below 1.0 times — will be critical to assessing financial health.

Third, capital efficiency ratio — measured as the ratio of capital expenditure to production growth (or maintenance). This tells you how efficiently SM Energy is converting drilling dollars into barrels. In the manufacturing model, this ratio should improve over time as operational efficiencies compound. If it deteriorates — if it takes more capital to produce the same or fewer barrels — that is a signal that inventory quality is declining or operational discipline is slipping.

XI. Lessons & Reflections: The Playbook

SM Energy's 118-year journey from Louisiana marshland to Permian Basin powerhouse offers several lessons that extend well beyond the oil patch.

Strategic focus beats diversification in commoditized industries. This is the central lesson of SM Energy's story. When the company operated across five basins, it was mediocre in all of them — spread too thin, unable to achieve the kind of concentrated excellence that drives down costs and creates operational moats. The decision to sell the Eagle Ford, exit the Bakken and Powder River, and concentrate in the Permian was the single most important strategic choice in the company's modern history. In businesses where the product is undifferentiated and the only competitive advantages are cost and execution, focus is not a luxury — it is a survival requirement.

Timing exits is as important as timing entries. SM Energy's sale of its Eagle Ford assets to KKR-backed Venado for $800 million came when the Eagle Ford was still widely considered premium acreage. The company sold near the top of the market for those assets and deployed the proceeds into Permian acreage that, in retrospect, was priced at a generational bottom. Most corporate managers struggle with selling successful assets — it feels like admitting failure, like abandoning a play that made the company what it is. The institutional inertia, the emotional attachment, the analyst relationships built around the asset — all of these create friction against selling.

SM Energy's willingness to exit a play that had defined the company showed unusual strategic discipline. It is worth noting that this is extraordinarily rare in corporate America, not just in E&P. The vast majority of companies hold assets too long, sell too late, and reinvest at inferior returns. SM got this one exactly right.

Financial flexibility is survival. The companies that emerged from the 2014-2016 oil crash and the 2020 COVID crash shared one common characteristic: they had the balance sheet flexibility to endure sustained periods of low commodity prices without triggering debt covenant violations or forced asset sales. SM Energy's aggressive debt reduction — from $2.77 billion to $2.28 billion during the worst of 2020 — was not a nice-to-have; it was existential. In a cyclical commodity business, the companies that survive the downturns are the ones that manage their balance sheets as aggressively as they manage their drilling programs.

Adapting to capital markets is a core competency. SM Energy's management team recognized the post-2016 shift in investor sentiment — from rewarding production growth to demanding capital discipline and shareholder returns — faster than many peers. This was not just financial savvy; it was organizational adaptation. The entire company, from the CEO to the field engineers, had to internalize a new definition of success. Production growth was no longer the north star. Free cash flow was.

This shift is easy to describe in retrospect but was genuinely difficult in real-time. For decades, the entire E&P industry had been structured around growth metrics — reserves growth, production growth, acreage additions. Compensation structures, career advancement, and corporate identity were all built around the idea that bigger is better. Pivoting to a return-of-capital model required not just a new strategy but a new culture. Companies that failed to make this mental shift — that continued chasing growth when the market was demanding returns — saw their stocks languish and their access to capital shrink.

Operational excellence is a margin of safety, not a moat. SM Energy's drilling and completion efficiency, its manufacturing-model approach, and its continuous improvement culture are genuine competitive advantages — but they are advantages that must be re-earned every quarter. In E&P, operational best practices diffuse rapidly. Today's innovative completion design is tomorrow's industry standard. The company that stops improving, even for a quarter or two, will find its peers closing the gap.

Operational excellence in shale is less like a castle wall and more like a treadmill: you have to keep running just to stay in place. But here is the nuance that matters for investors: while no single operational advantage is durable, a culture of continuous improvement — the organizational muscle memory of always finding the next efficiency gain — can be surprisingly persistent. It is the culture, not any specific technique, that creates sustained value.

Commodity cycles are inevitable; preparation is a choice. SM Energy has now survived three major oil price crashes: 2008, 2014-2016, and 2020. Each time, the company was tested. Each time, it emerged — battered but intact — because it had the assets, the balance sheet, and the organizational resilience to weather the storm. The lesson is not that cycles can be avoided or predicted — they cannot, and anyone who claims otherwise is selling something. The lesson is that companies must build organizations that can absorb fifty percent price drops without breaking. That means conservative debt levels, flexible cost structures, and a culture that prioritizes long-term survival over short-term optimization. The companies that enter downturns with the most flexibility exit them in the strongest position. SM Energy learned this lesson in 2015 and has applied it ever since.

The independence paradox. For a mid-tier independent E&P company, staying independent requires constant excellence across every dimension — operations, finance, strategy, and capital allocation. One mistake — an overleveraged acquisition, a poorly timed growth surge, a failure to adapt to shifting investor expectations — and you are either acquired at a discount or pushed into bankruptcy. SM Energy has maintained its independence for over a century, but every year brings new challenges and new threats. The Civitas merger, while a growth move, was also a recognition that scale is increasingly necessary for survival. The paradox is that the very excellence required to remain independent also makes you an attractive acquisition target.

For investors, the meta-lesson is this: Understanding commodity cycles, knowing how to value E&P companies on a free cash flow yield and reserves basis rather than on earnings multiples, and recognizing when structural changes in an industry are creating permanent winners and losers — these are the skills that separate successful energy investors from those who get whipsawed by the cycle. SM Energy's story is a case study in all three.

XII. Epilogue: What's Next for SM Energy?

SM Energy enters the post-merger era in the strongest competitive position of its modern history. The company has gone from a $4 billion Permian pure-play to a $12.8 billion enterprise with multi-basin diversification, top-ten independent production scale, and a management team with deep operational experience.

Beth McDonald, the new CEO, deserves particular attention. At forty-six, she represents a generational shift in E&P leadership. Her two decades at Pioneer Natural Resources — the company that Scott Sheffield built into the Permian's dominant independent before selling it to Exxon for $60 billion — means she has seen firsthand how the Permian's most successful operator scaled, optimized, and ultimately monetized its position at maximum value. She understands both the operational playbook for running a world-class Permian operation and the strategic calculus of knowing when to sell. Whether she applies that experience to running SM Energy as a long-term independent or to positioning it for an eventual exit remains one of the most consequential leadership questions in the mid-cap E&P space.

Three paths lie ahead, and they are not mutually exclusive.

The first path is to stay independent and execute — generate free cash flow, return capital to shareholders, and prove that a mid-major independent can sustain competitive returns across cycles. This is the default path, and it is viable as long as oil prices remain supportive, integration synergies materialize, and inventory depth holds up. The company's guidance for $2.65-2.85 billion in 2026 capital expenditure, combined with divestiture proceeds and debt reduction, suggests management is prioritizing financial strength alongside operational execution.

The second path is to be acquired. In the current consolidation environment, a 650,000-barrel-per-day independent with premium acreage across four active basins is an obvious target for any major seeking scale. Whether Exxon, Chevron, ConocoPhillips, or another suitor comes calling is unknowable, but the optionality exists.

The third path is to be an acquirer — to continue building scale through bolt-on acquisitions that extend inventory life and fill in geographic gaps. SM Energy has demonstrated the ability to execute accretive acquisitions, from the 2016 Midland Basin deals to the 2024 Uinta entry to the Civitas merger itself. If attractive opportunities emerge at reasonable valuations, the company has the platform to absorb them. This path carries its own risks — acquisition-driven growth can lead to overpaying, integration distractions, and balance sheet strain — but it also offers the clearest route to maintaining competitive scale in an industry where the minimum viable size keeps growing.