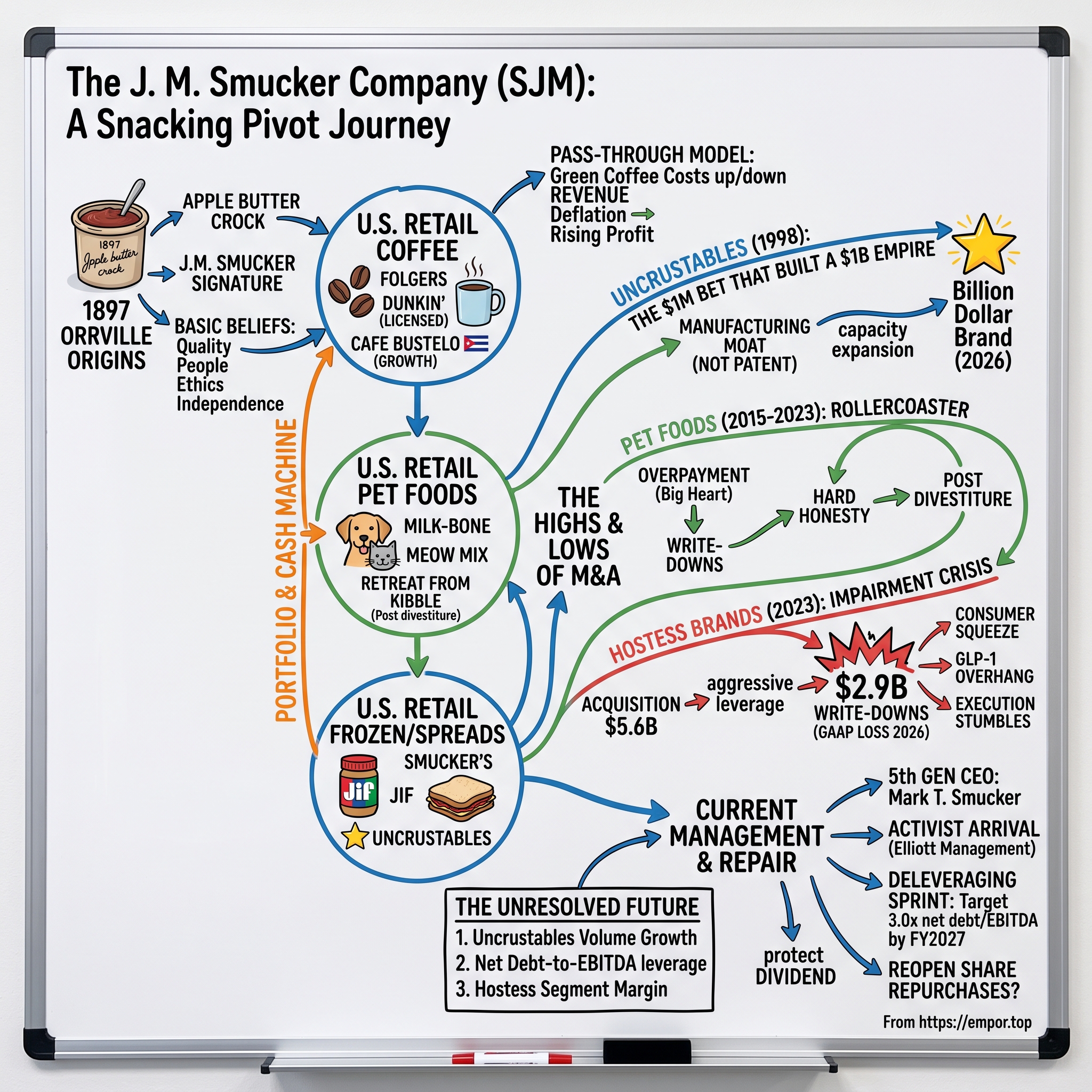

The J. M. Smucker Company: The $9B Food Empire's High-Stakes Snacking Pivot

I. Introduction & Episode Roadmap

Here is a number that would have been unthinkable in Orrville, Ohio, for most of the last century: for the fiscal year ended April 30, 2026, one of America's most conservative, family-controlled food companies reported a net loss of $1.30 per share.1 Not a slowdown. Not a soft quarter. A loss — at a business that had paid a dividend without interruption for longer than most of its shareholders had been alive.

The loss was not because Folgers stopped selling or because Americans stopped eating peanut butter. It was almost entirely an accounting confession. In the space of two years, The J. M. Smucker Company had written down more than $2.9 billion of value it had paid for a single acquisition — the maker of Twinkies, Ding Dongs, and Donettes.4 Strip out those non-cash impairments and the underlying business still earned $9.15 of adjusted profit per share and generated a record $1.16 billion of free cash flow.1 Both statements are true at once, and the gap between them is the entire story of modern Smucker.

So how did a 129-year-old fruit-spread company — one whose founder, according to company lore, hand-signed every crock of apple butter as a personal guarantee of quality — end up owning Folgers coffee, Milk-Bone dog biscuits, and Hostess snack cakes, and taking billion-dollar write-downs on the last of them?

That is the central tension. Smucker is a multi-generational, dividend-disciplined, risk-averse family legacy. And yet over the past two decades it transformed itself into an aggressive, debt-financed consolidator of mature grocery brands, executing two of the largest deals in its history — Big Heart Pet Brands and Hostess — that together stretched its balance sheet to the edge of investment-grade comfort. The market's skepticism is not academic. It is asking whether management systematically overpays for growth, dilutes a good core with mediocre assets, and then asks investors to look past the wreckage as "one-time" charges.

The portfolio at a glance. In fiscal 2026, Smucker generated $9.05 billion in net sales and roughly $2.01 billion in total segment profit.1 The engine room breaks down as follows:

- U.S. Retail Coffee — $3.30 billion in net sales and $701.5 million in segment profit, more than a third of both the top line and the profit pool. This is the cash machine.1

- U.S. Retail Frozen Handheld and Spreads — $1.85 billion in sales and $444.7 million in profit, home to the Uncrustables phenomenon and the Jif/Smucker's spreads franchise, at a segment margin near 24%.1

- U.S. Retail Pet Foods — $1.60 billion in sales and $473.3 million in profit, a 29.6% margin that is quietly the highest in the company after years of painful surgery.1

- Sweet Baked Snacks — $971.3 million in sales but only $97.2 million in profit, a 10.0% margin, the Hostess business still bleeding after the write-downs.1

- Away From Home — $879.0 million in sales and $220.1 million in profit, now broken out as its own segment; and a residual International (reported as "Other") at $441.8 million.1

That last point is a small tell worth flagging up front: in the fourth quarter of fiscal 2026, Smucker quietly re-cut its segments, elevating Away From Home to a standalone reporting unit and parking international in an "Other" bucket.1 Segment redefinitions are not sinister, but they do reset the comparison base, and a careful reader learns to watch what a company chooses to spotlight versus bury.

Here is the roadmap. We start in 19th-century Orrville, where the family DNA was written. We move to the 2008 Folgers deal that doubled the company overnight, and to the coffee franchise that still funds everything else. We tell the almost comic story of a $1 million school-cafeteria sandwich that became a $1 billion brand. We walk through the pet-food rollercoaster — overpay, write down, retreat, and re-emerge with the best margins in the house. We dissect the Hostess acquisition and its cascading impairments. We examine management, leverage, and the arrival of an activist. We revisit the 2022 Jif recall. And we close with the strategic frameworks and the bull-versus-bear debate that will decide whether this transformation was courage or capital destruction.

Let us begin where the trust was minted.

II. Orrville Origins & The Family Dynasty

Picture rural Wayne County, Ohio, in 1897. The land around the small town of Orrville is thick with apple orchards planted, according to local legend, from seed stock left behind by the wandering nurseryman John Chapman — Johnny Appleseed. A quiet, devout Mennonite named Jerome Monroe Smucker builds a cider mill and begins pressing apples. Cider alone is seasonal and unglamorous, so he does the sensible thing: he cooks the surplus down into apple butter, ladles it into crocks, and sells it off the back of a horse-drawn wagon.6

The detail that has become the company's origin myth — and it is retold as myth because the primary record is thin — is that Jerome hand-signed each crock. In an era before national brands, before packaged-goods marketing, before the FDA, a signature on a container of food was a radical act. It said: I personally stand behind what is inside this. Whether or not every crock literally bore his signature, the idea encoded something durable in the company's culture — that a family name attached to a product is a promise, and that promises are expensive to break. Decades later, in 1962, a Cleveland copywriter named Lois Wyse distilled that instinct into six words that became one of the most recognizable slogans in American advertising: "With a name like Smucker's, it has to be good."7 It is a self-deprecating line — the name is faintly ridiculous — that turns the awkwardness into a badge of authenticity.

What makes Smucker genuinely unusual is not the origin story; plenty of food companies have one. It is that the family never let go. The torch passed from Jerome to his son Willard, to Willard's son Paul, and then — in a governance arrangement rare among large public companies — to Paul's two sons, Tim and Richard, who ran the business for years as co-CEOs and co-chairmen, a shared-cockpit model that outside investors usually distrust and that the Smuckers made work. In May 2016, the fifth generation took over when Mark T. Smucker became president and chief executive, with Richard moving to executive chairman.8 Five generations of one family steering a public company across more than a century is not merely sentimental; it is a structural fact that shapes incentives, time horizons, and risk appetite.

It is worth being precise about the nature of that control, because it is easily overstated. Smucker is not a dual-class fortress in which a founding family holds a lock on the votes; the family's influence has been exercised through culture, board presence, and continuity rather than a super-voting share structure. That distinction matters enormously to the story's ending — it is precisely why an activist could take a position and win a seat at the table in 2026, something that would be far harder at a family that controlled the ballot outright. The Smuckers built their authority on stewardship and reputation, not on legal insulation, and stewardship has to be re-earned every time the company allocates a few billion dollars of capital.

The culture the family institutionalized is codified in a set of "Basic Beliefs" — quality, people, ethics, growth, and independence — that Smucker has published for decades and that sound like corporate wallpaper until you notice how literally the company has taken them. The commitment to "people" showed up for years in a place on lists of the best large companies to work for and in employee tenure that is unusual for consumer packaged goods. The commitment to "independence" is the one now under the most strain: for most of its history it meant staying private-minded, patient, and un-levered. The 21st-century acquisition spree tested every one of those beliefs, and the question the rest of this story asks is whether the culture bent or broke.

That culture has a measurable financial signature. Smucker keeps its headquarters in Orrville — not Chicago, not New York — a deliberate rootedness that the company treats as a competitive asset in employee retention and cultural continuity. And it has treated its dividend as close to sacred. Smucker is a member of the Dividend Aristocrats, having raised its payout for roughly 29 consecutive years through early 2026.9 (One correction worth making early, because it recurs in secondary summaries: the streak is on the order of three decades, not the half-century some sources loosely claim.) For a large slice of Smucker's retail shareholder base, that unbroken record is the whole investment thesis — a proxy for stability.

Which sets up the paradox at the heart of this company. A culture built on organic, patient, low-drama growth — apple butter, jam, peanut butter — spent the 21st century behaving like the opposite: a leveraged buyer of other people's mature brands, repeatedly betting billions on acquisitions and repeatedly explaining the morning-after impairments. The conservative steward and the aggressive dealmaker are the same institution. To understand how the quiet apple-butter company learned to swing that hard, you have to start with the deal that changed its scale forever — a cup of coffee.

III. The Coffee Juggernaut: Folgers, Dunkin', and Café Bustelo

In June 2008, as the financial system was quietly beginning to crack, Procter & Gamble and Smucker announced a transaction that most Americans never noticed and that remade Smucker overnight. P&G would spin off Folgers — the best-selling coffee brand in America, the one with the "best part of waking up" jingle — and merge it into Smucker in an all-stock deal structured as a Reverse Morris Trust, valued at roughly $3.3 billion including assumed debt.10

Pause on the structure, because it explains why the deal happened at all. A Reverse Morris Trust is a piece of financial engineering that lets a large parent (P&G) shed a division to a smaller partner (Smucker) tax-free, provided the parent's shareholders end up owning more than half of the combined entity. When the deal closed that November, former P&G holders owned roughly 53.5% of Smucker.10 In plain terms: Smucker did not pay cash and did not trigger a giant tax bill; it printed shares and effectively swallowed a company nearly its own size. Overnight, Smucker roughly doubled in revenue and became the leader in U.S. retail coffee — a jam company that suddenly made most of its money from caffeine.

Why does coffee matter so much to the thesis? Because coffee is simultaneously the best and most nerve-wracking business Smucker owns. It is a mature, high-volume, daily-habit category — Americans brew it at home every morning, recession or boom — which makes the revenue defensive. But the economics run through green (unroasted) coffee, a globally traded commodity whose price swings violently on weather in Brazil and Vietnam, on currency, and increasingly on tariffs. Smucker's model is to treat coffee as a pass-through: when green coffee costs rise, it raises prices; when they fall, it gives price back. On the Q4 fiscal 2026 call in June 2026, CEO Mark Smucker put it bluntly — "Coffee is a pass-through category. We do pass through up and down costs to our customers and our consumers."[^3] The catch is timing and elasticity: push prices too high and volume drops; the art is passing cost through without breaking the consumer's habit.

The industry map. To understand Smucker's position, picture the packaged-coffee aisle as a battlefield with a handful of entrenched armies. Smucker is the leader in at-home coffee, but it is surrounded. Kraft Heinz owns Maxwell House, the old rival now largely run for cash. Starbucks is the premium giant, though its packaged grocery business is licensed and distributed by Nestlé under a multi-billion-dollar "Global Coffee Alliance," which means Smucker effectively competes with a Nestlé-Starbucks combine at the top of the shelf. Keurig Dr Pepper controls the single-serve platform economics through the K-Cup system. And beneath all of them sits private label — the retailer's own store brand — which in a commodity like coffee is a permanent, price-driven threat that gains ground every time beans get expensive and shoppers get anxious. Smucker's job is to hold premium and mainstream shelf space across roast-and-ground cans and single-serve pods against every one of these at once.

The coffee franchise is really three different animals. Folgers is the mainstream cash cow — enormous volume, fierce private-label competition, slow growth, and a job description that is mostly about defending share and managing cost. Dunkin' packaged coffee is the premium tenant: Smucker has manufactured and sold Dunkin'-branded bagged coffee in grocery stores since 2007, and in 2015 the partnership expanded to put Dunkin' K-Cup pods on retail shelves, under a license that runs all the way to 2039.12 It is a cornered resource of sorts — a premium, exclusive brand Smucker gets to monetize without owning. And then there is the growth star: Café Bustelo, the espresso-style brand rooted in Cuban-American coffee culture that Smucker picked up in 2011 when it bought the brands of Miami's Rowland Coffee Roasters for $360 million.11

Bustelo is the closest thing the coffee segment has to a growth engine, and it is a genuinely instructive marketing story. Rather than treat it as a niche "Hispanic" product, Smucker leaned into cultural authenticity while broadening the audience — its "Está Aquí" ("It's here") campaign deliberately reframed the brand as present and current rather than nostalgic, courting younger, multicultural, non-Hispanic drinkers.13 By fiscal 2026, management said Bustelo had grown past $500 million in annual sales.[^3] The lesson for investors is that even inside a "sleepy" commodity category, a brand with a distinct identity can compound — Bustelo is doing to premium coffee what Uncrustables did to the freezer aisle.

There is a fourth animal worth naming because it shows how the pass-through model actually behaves under stress: tariffs. Green coffee is not grown in the United States at commercial scale, so it is almost entirely imported — which makes it acutely exposed to trade policy. Management disclosed that unmitigated tariffs cost the coffee segment roughly $75 million in fiscal 2026, a hit it expected to lap and recover in fiscal 2027, while still carrying a standing 10% tariff drag into the new year.3[^3] A tariff on an imported commodity you cannot substitute domestically is a near-pure margin tax until you can price around it — a live reminder that Smucker's largest profit pool sits downstream of geopolitics it does not control.

The materiality is straightforward. Coffee is the single largest source of both revenue and profit at Smucker.1 So the FY2027 guidance carries an important subtlety: management projected total company net sales to fall 3% to 4%, driven largely by passing green-coffee deflation back to consumers.1 On the surface that looks like shrinkage. But CFO Tucker Marshall was explicit that deflation "benefits both the absolute profit dollar and the profit margin percentage," and management guided the coffee segment margin back toward the high-20s as cheaper beans work through inventory and prior tariff hits lap.3 This is the crucial thing to internalize about Smucker's coffee: in a pass-through model, falling revenue can coincide with rising profit. Revenue is the least interesting line. What matters is the spread management captures between commodity cost and shelf price — and whether the consumer keeps buying as prices move.

That last clause is where the analysts pushed. On the Q4 call, Barclays' Andrew Lazar asked the natural question: if you are cutting price as costs fall, why not model a bigger volume rebound — shouldn't cheaper coffee win back shoppers? Mark Smucker's answer was a study in deliberate conservatism. Elasticities had run "more favorable than expected" during the inflationary years — meaning consumers kept buying even as prices rose — and rather than assume that generosity persists on the way down, management chose to model volume "prudently."[^3] This is the right posture, but it also quietly concedes the franchise's core vulnerability: Smucker does not actually know how loyal the coffee consumer is until prices move, and it is being careful not to bet the guidance on that loyalty. A defensive category is not the same as an immovable one.

That distinction — between a business that grows by getting genuinely bigger and one that manages a spread — is exactly what makes the next chapter so remarkable. Because tucked inside this commodity conglomerate was a product that actually did get bigger, ten years running, starting from a school cafeteria in North Dakota.

IV. Uncrustables: The $1M Bet that Built a $1B Empire

In 1995, in and around Fargo, North Dakota, two fathers named David Geske and Len Kretchman got tired of the same small domestic problem: peanut-butter-and-jelly sandwiches made in the morning went soggy by lunch, and kids hated the crusts. Their fix was almost aggressively unglamorous — a machine that pressed two circles of bread around a filling, crimped the edges into a sealed pocket, cut off the crust, and froze the result. They called it, with more enthusiasm than modesty, "Incredible Uncrustables," and they sold it to schools tired of assembling lunches by hand.14

In 1998, Smucker bought the little business — and, crucially, its pending patent — for about $1 million.15 It stands as arguably the highest-return capital allocation decision in the history of the packaged-food industry. A company that would later write off billions on marquee acquisitions built a billion-dollar brand from a rounding-error check. The irony is almost too neat, and it is worth holding onto, because it complicates any simple story about Smucker as a serial overpayer. When Smucker buys small and organic, it has been brilliant. When it buys big and mature, it has struggled. That pattern is not a coincidence; it is close to a thesis.

The early strategy was to defend the idea with intellectual property. In December 1999, the U.S. Patent and Trademark Office granted Patent No. 6,004,596 for a "sealed crustless sandwich," and Smucker began enforcing it against regional imitators.[^17] The legal saga that followed became a business-school punchline. Challenged on the grounds that pressing and sealing bread around a filling was hardly novel — pie crimping is centuries old — the patent's broad claims were rejected on appeal in 2005 and effectively cancelled for prior art, with the patent lapsing in 2007.[^17] Smucker had lost the legal moat.

And here is the strategic pivot that actually matters. Denied a patent wall, Smucker built a manufacturing wall instead. If you cannot legally stop competitors from making a crustless sandwich, you can make it uneconomical for them to match your scale, your cost, and your freezer distribution. So Smucker poured capital into purpose-built plants. It opened a roughly $340 million, 430,000-square-foot facility in Longmont, Colorado in July 2019 to break production bottlenecks.16 Then it went much bigger: a $1.1 billion, 900,000-square-foot plant in McCalla, Alabama, which opened in November 2024 and was designed to feed years of double-digit demand.17 Building a billion-dollar factory to make frozen PB&J sounds absurd until you realize it is the moat — the barrier to entry is no longer a patent claim but the willingness and ability to sink a billion dollars into capacity and fill national freezer space before anyone else does.

The payoff arrived in fiscal 2026, when Uncrustables crossed $1 billion in annual net sales — more than half of the entire Frozen Handheld and Spreads segment — adding roughly 3 million new households in a single year.2 Inside a low-growth conglomerate, this is a genuine growth stock hiding in plain sight, and at segment margins in the mid-20s it is a profitable one.

The capacity story and the growth story are the same story, and it is worth making the causation explicit because it is a genuinely elegant piece of strategy. For years, Uncrustables' constraint was not demand — it was supply. The brand could sell everything it made, which meant the binding limit on growth was freezer capacity, and every new plant unlocked both more production and more distribution, because a retailer will only give you freezer space if you can reliably fill it. As new McCalla and Longmont capacity came online, Smucker could simultaneously widen distribution, deepen household penetration, and turn on national marketing — a flywheel where the factory, the shelf, and the advertising reinforce one another. On the Q3 call, management quantified the channel runway: it had tripled its convenience-store sales and was still adding households by the millions, with Away From Home (schools, foodservice, travel) growing faster than retail off a smaller base.3

But a neutral read requires noting where the story is now bending. On the Q4 fiscal 2026 call, management was candid that the era of double-digit Uncrustables growth is ending: FY2027 guidance is for mid-single-digit growth, "no longer double-digit."[^3] That is the natural physics of a brand that has gotten large — the law of big numbers catches everyone. The forward drivers management points to are distribution (only about 75% of Uncrustables volume runs through traditional U.S. retail, with 25% through Away From Home and a fast-growing convenience-store channel), household penetration, and innovation like higher-protein sandwiches aimed at the breakfast occasion and a new "fridge-friendly" format — a version that survives in the refrigerator rather than requiring the freezer — rolling out across the entire line by mid-2026.[^3] The fridge-friendly move is subtle but strategically important: a product that no longer needs freezer space escapes the single most constraining shelf limitation the brand has, opening lunchbox, pantry, and impulse placements the frozen SKU could never reach.

The bet is that Smucker can trade some of its explosive percentage growth for durable, high-margin volume growth off a much larger base. Whether the brand can keep adding households at scale, or whether it is approaching saturation as private-label imitators — the "store brands filling out the section," in Mark Smucker's own phrase — erode its lead, is the single most important organic question in the entire company.3 The bullish evidence is that Smucker remains the runaway category leader with by far the largest share of voice; the bearish evidence is that a crustless sealed sandwich is, in the end, not that hard to copy once the patent is gone, and the moat is capital and distribution rather than anything a competitor is legally barred from doing.

Uncrustables proves Smucker can build. The next chapter asks whether it can buy — and it is a far more uncomfortable read.

V. The Pet Foods Rollercoaster: From Overpayment to Post Holdings

In February 2015, Smucker announced it was paying about $5.8 billion for Big Heart Pet Brands — the former Del Monte pet business, home to Milk-Bone, Meow Mix, Kibbles 'n Bits, 9Lives, and a long tail of value and private-label pet food.18 The strategic pitch was seductive and, on its face, sensible: pet food was a large, growing, emotionally sticky category where owners "humanize" their animals and trade up. Smucker wanted in, and it wanted in at scale.

The trouble was what it actually bought. A great deal of Big Heart's volume sat in exactly the wrong places — low-growth, low-margin, canned and dry dog food, plus private-label production where Smucker had no brand pricing power at all. Owning Milk-Bone and Meow Mix was genuinely attractive; owning tonnage of commodity kibble was not. Integration proved harder than promised, and the impairments began: the company took successive charges against pet goodwill and trademarks in the years that followed, including a $176.9 million impairment in fiscal 2018 tied to pet goodwill and brand values.19 Each write-down was, in effect, an admission that the price paid in 2015 assumed growth and margins that the acquired portfolio could not deliver.

Rather than retreat, Smucker doubled down on the premium thesis. In May 2018 it completed the $1.9 billion acquisition of Ainsworth Pet Nutrition, whose flagship was Rachael Ray Nutrish — a celebrity-branded, "natural" line meant to ride the humanization trend into higher-margin territory.20 The strategic logic was to fix a low-margin problem by adding a premium brand on top. But the balance sheet was now doing a lot of work, and the pet segment had become a place where Smucker kept spending to correct the last thing it had spent on.

The turning point came in 2023, and it was an act of hard-nosed honesty that deserves credit. Smucker admitted structural defeat on the low-margin end of pet. In an announced $1.2 billion divestiture, it sold a package of brands — Rachael Ray Nutrish, 9Lives, Kibbles 'n Bits, Nature's Recipe, Gravy Train, and its private-label pet operations — to Post Holdings, a deal signed in February 2023 and completed that April.21 Smucker had bought Ainsworth's Nutrish for $1.9 billion in 2018 and, five years later, sold it (bundled with other brands) as part of a $1.2 billion exit. On the specific brand, that is capital destruction, plain and stated.

And yet — this is the redemption arc — the surgery worked. What remained was a tighter portfolio anchored by two genuinely advantaged franchises: Milk-Bone in dog snacks and Meow Mix in cat food, categories with better growth, real brand equity, and pricing power. There is an important economic reason snacks and treats beat main-meal pet food: a dog biscuit is a small, frequent, emotionally-driven "reward" purchase where the owner is buying affection, not nutrition-per-dollar, which supports far higher margins than the commodity bag of kibble a shopper price-shops. Smucker, in effect, retreated from the low-margin center of the bowl to the high-margin edges — the treat jar and the cat bowl — riding the same "humanization" and "premiumization" trends that had lured it into the category in the first place, but this time from the profitable end.

By fiscal 2026, the pet segment generated $1.60 billion in sales but $473.3 million in profit — a 29.6% margin, the highest of any segment in the company.1 Management's commentary reinforced the mix shift: on recent calls they highlighted Meow Mix as the number-one dry cat food with roughly 5% top-line growth, Milk-Bone returning to growth on both premium innovation (the Peanut Buttery Bites platform) and value "base biscuits," and new formats like Gravy Bursts extending the line — while candidly conceding that the "tail" brands like Pup-Peroni and Canine Carry Outs remained soft against private label and needed a brand refresh.3 The strategy is explicitly to win across price tiers within the categories it has chosen rather than to be everything to everyone. The competitive context is not trivial: the segment still faces private label, the big platforms of Nestlé Purina and Mars, and the fresh/refrigerated insurgent Freshpet nibbling at the premium end. But a 29.6% margin on a defensible snack-and-cat core is a materially better business than the sprawling, low-return pet conglomerate Smucker assembled a decade ago.

The investor takeaway is a genuinely double-edged one. On one hand, Smucker demonstrably traded empty volume for high-margin, defensive assets — proof that management will cut its losses and that a smaller, better business beats a bigger, worse one. On the other, the round trip from a $5.8 billion buy and a $1.9 billion buy to a $1.2 billion sell is an expensive tuition bill, and it is the clearest evidence in the entire company for the bear's core claim: that Smucker overpays for big M&A and only creates value after painful subtraction. Hold both thoughts, because the very next deal ran the same playbook — except this time the write-downs came faster and larger than almost anyone expected.

VI. Hostess Brands & The Impairment Crisis

On September 11, 2023, Smucker announced it would buy Hostess Brands — the resurrected maker of Twinkies, Ding Dongs, CupCakes, and Donettes — for about $5.6 billion, roughly $34.25 per Hostess share in cash and stock.[^24] The strategic story was "convenient snacking": Hostess indexed heavily to the impulse purchase, the grab-and-go breakfast, the checkout lane and the convenience store, a set of occasions Smucker argued it could supercharge with its distribution and its Uncrustables/coffee adjacencies. The deal closed on November 7, 2023.22

Then look at what Smucker paid. The purchase valued Hostess at approximately 17.2 times adjusted EBITDA, or about 13.2 times once you credited an anticipated $100 million of cost synergies.[^24] Even the synergized multiple was a full, private-equity-style price for a mature, indulgent-snacking business. The market did not applaud. Smucker's own stock fell roughly 7% on the announcement — an unusually sharp rebuke to an acquirer — as investors did the arithmetic on the multiple and the leverage.23 And the leverage was the real alarm: to fund a largely cash deal, Smucker took its pro forma net-debt-to-EBITDA ratio to about 4.4 times, up from roughly 2.2 times, an aggressive posture for a company whose entire brand with shareholders was conservatism.24 Analysts asked the obvious question: why pay a premium multiple for high-calorie packaged cake at the exact moment consumers were pinching pennies and a new class of weight-loss drugs was arriving?

The answer, unfortunately for Smucker, came in the form of the largest sustained impairment sequence in the company's history. In three brutal installments, Smucker wrote down the Hostess goodwill and the Hostess trademark:

- In its fiscal 2025 third quarter (reported early 2025), it took $794.3 million of goodwill plus $208.2 million of trademark impairment — roughly $1.0 billion.25

- In the fiscal 2025 fourth quarter (June 2025), it took another $867.3 million of goodwill and $112.7 million of trademark charges — about $980 million.26

- In the fiscal 2026 third quarter (February 2026), it took a further $507.5 million of goodwill — wiping out essentially all the remaining goodwill in the reporting unit — and $454.2 million against the Hostess brand.4

Add it up and Smucker recognized roughly $2.94 billion in non-cash impairments in under two years — more than half of the entire premium it had paid.4 These charges are the direct cause of the fiscal 2026 GAAP net loss with which this story opened. They are non-cash, and management is right that they do not drain the bank account. But they are not meaningless. An impairment is the auditors and the company jointly conceding that the future cash flows they modeled at the time of purchase will not materialize. Three write-downs in a row is not a surprise; it is a trend, and it says the original underwriting was wrong.

Why did the business deteriorate so fast? Three structural headwinds converged. First, a consumer squeeze: lower-income households, the core buyers of brand-name indulgent snacks, cut back hard on discretionary treats under persistent inflation, trading down to private label or simply buying less. A Twinkie is the definition of a discretionary purchase — nobody needs one — which makes the brand acutely sensitive to how much slack is in a household budget.

Second, the GLP-1 overhang. This one deserves a plain-English explanation because it is the most-cited and least-understood risk to the business. Drugs like Ozempic and Wegovy — originally diabetes treatments now used widely for weight loss — work in part by blunting appetite and, for many users, specifically dampening cravings for sweet, high-calorie, low-satiety food. That is, almost precisely, a description of the Hostess menu. If even a modest and growing slice of the population is pharmacologically less interested in a package of Donettes, the entire long-run demand curve for indulgent baked snacks shifts down. Management has publicly downplayed a measurable near-term hit to its own volumes, and that may well be true today. But an impairment test does not care about this quarter; it discounts decades of future cash flow, and a slow, secular appetite-suppressant trend is exactly the kind of assumption-killer that forces a company to lower its long-term growth rate — which is precisely what Smucker did.

Third, execution stumbles: Smucker cut roughly 25% of Hostess SKUs to focus on the icon brands (Twinkies, CupCakes, Donettes), consolidated the bakery network — closing the Indianapolis plant at greater cost than expected — and absorbed a plant fire in Emporia, Kansas, all of which pressured a business that needed stability.273 A turnaround requires operational calm; Hostess got operational turbulence.

The portfolio pruning continued in parallel. In December 2024, Smucker sold the Voortman cookie brand, acquired with Hostess, to Second Nature Brands for about $305 million, narrowing Sweet Baked Snacks to its core sweet-baked lineup.[^31] And in a telling technical move on the Q3 fiscal 2026 call, CFO Tucker Marshall disclosed that Smucker would begin amortizing the Hostess trademark rather than carrying it as an indefinite-lived asset — after cutting the brand's long-term growth assumption to just 2% — with full-year amortization guided to about $210 million.3 Putting a brand "on a life" is quiet accounting language for a loud admission: management no longer believes Hostess is a perpetual-growth franchise.

There is also a credibility problem management has had to answer for directly, and the Q&A on it is revealing. For several quarters, Smucker guided this business one way and delivered another — profit pressure that was supposed to peak in one quarter kept reappearing in the next. On the Q4 call, Wells Fargo's Chris Carey put it to management plainly: "The visibility of this business has been a bit challenged in recent quarters. Can you just give us a sense on your ability to forecast accurately this business?"[^3] Mark Smucker's response was that the team had finally "gotten our arms around this business in terms of visibility."[^3] Maybe. But an investor is entitled to weigh a fresh promise of forecasting accuracy against a track record of forecasting misses — and on a business the company has already written down three times, the burden of proof sits squarely with management. A related exchange a quarter earlier, when TD Cowen's Robert Moskow asked whether the departure of much of Hostess's original leadership had hollowed out the business, drew a firm denial — Smucker insisted it had "the right team in place" — but the fact that the question was asked at all captures how much integration risk this deal carried.3

The segment economics tell the rest. In fiscal 2026, Sweet Baked Snacks produced $971.3 million in sales but only $97.2 million in profit — a 10.0% margin, roughly half of what a healthy CPG snacking business earns.1 There are faint green shoots: management noted Donettes grew 13% and now represents about 40% of the portfolio, and it guided segment profit up roughly 30% in FY2027 on cost control and a list-price increase.[^3] But growing off a "low watermark," in the CFO's own phrase, is a low bar. On the Q4 call, Bank of America's Peter Galbo pressed directly on trade-press chatter about a possible further portfolio action on Hostess; Mark Smucker's reply — that the focus is "stabilizing that business and improving profitability" and that a return to top-line growth "is going to take some time" — was notably not a denial that the asset could eventually be sold.[^3]

That open question — what does Smucker ultimately do with an asset it has already written down by more than half? — leads straight into the people making the call, and the pressure now bearing on them.

VII. Current Management & The Balance Sheet Deleveraging Sprint

Every earnings call now opens the same way. On the February 2026 call, the very first analyst question from Barclays' Andrew Lazar was not about coffee or snacks — it was about Elliott Management, the activist hedge fund that had built a position and opened a dialogue with the company.3 Mark Smucker's response was measured and, by activist-engagement standards, warm: "The engagement with Elliott is recent and has actually been very constructive... there's really good alignment between what they're seeing and what we are seeing."3 Around the same period, Smucker added two new directors, Bruce Chung and David Singer, and framed it as ongoing board evolution focused on capital allocation and governance.3 Read the subtext: a family-controlled company that had spent a decade making big, contentious acquisitions was now hosting an activist at the table and refreshing its board around the question of how it deploys capital. That is a meaningful shift in the balance of power, and it is the single most important governance development in the story.

What does an activist like Elliott actually want here? Its playbook at consumer companies is well-worn, and the pressure points at Smucker are easy to map: sharper portfolio focus (which is code for "consider selling Hostess and anything else sub-scale"), tighter cost discipline, a clear capital-allocation framework that stops the pattern of premium acquisitions, and board and governance refreshment to enforce all of it. That two of the new directors, Bruce Chung and David Singer, bring financial and M&A backgrounds is not incidental — it signals that future capital deployment will face harder internal scrutiny.3 The neutral framing is that Elliott's arrival is simultaneously a criticism and a catalyst: a criticism because activists show up where they smell value trapped by management decisions, and a catalyst because external pressure tends to accelerate exactly the discipline this story has lacked.

At the center sits Mark T. Smucker, now Chief Executive Officer, President, and Chair of the Board — the fifth-generation leader who took over in 2016. His scorecard is genuinely mixed, and a neutral read has to hold both sides. On alignment: he is beneficially credited with 563,826 common shares in the 2026 proxy (a figure that includes 291,644 options exercisable within 60 days and 34,497 restricted shares), and his fiscal 2026 total compensation was about $10.9 million, weighted heavily toward equity — his stock awards alone exceeded $6.2 million.5 For scale, the company's own pay-ratio disclosure put the median employee's compensation at $77,698, a roughly 140-to-1 ratio that is unremarkable for a company this size but worth naming.5 The equity weighting does tie his outcomes to the share price over time. A governance skeptic would note the concentration of roles — Mark Smucker is simultaneously CEO, president, and chair of the board — which fuses management and oversight in one person and is precisely the kind of arrangement activists press to unwind; the recent board additions can be read partly as a counterweight.

On capability, the record is the tale of two Smuckers we have already seen. Give him full credit for scaling Café Bustelo and Uncrustables — organic, high-return value creation executed with real skill. But the same leadership presided over the Ainsworth and Hostess acquisitions and the multi-billion-dollar impairments that followed. A skeptical investor — an Elliott, say — would frame it precisely: this is a management team that is excellent at operating and building brands and demonstrably poor at pricing large acquisitions. The pattern of promising disciplined capital allocation and then executing expensive, quickly-impaired deals is exactly the kind of behavior that invites an activist, and one has now arrived.

Which is why the defining strategic mandate of the moment is not growth — it is repair. Having stretched to roughly 4.4 times leverage for Hostess, Smucker exited fiscal 2026 at about 3.8 times net debt to EBITDA and has committed to reaching approximately 3.0 times by the end of fiscal 2027.2 The plan is concrete and, to management's credit, specific: on the Q4 call, CFO Tucker Marshall laid out the arithmetic — pay down another roughly $500 million of debt in FY2027 (on top of $720 million repaid in FY2026), funded by roughly $1 billion of free cash flow.[^3] The capital-allocation priorities are stated in strict order: capital expenditure to support organic growth, including a $120 million-plus expansion of the Hostess bakery in Columbus, Georgia; debt paydown toward the 3.0x target; protecting and growing the dividend; and, notably, no share buybacks until the leverage goal is reached.[^3]30 As Marshall put it, only "as we begin to achieve our leverage objectives" does the door reopen to repurchases.[^3]

Behind the deleveraging is a genuine cash engine, and it is the strongest card in management's hand. Fiscal 2026 free cash flow of $1.16 billion — a company record — funded $720 million of debt repayment and roughly $465 million of dividends with room to spare, and management guided to about $1 billion again in FY2027 against roughly $325 million of capital expenditure.1[^3] The company is also running a "transformation office" under supply-chain executive Rob Ferguson, targeting on the order of a couple of points of revenue in gross annual cost savings to fund reinvestment, offset inflation, or drop to the bottom line.[^3] This matters for the credibility question: a business that consistently converts profit into cash has the raw material to both deleverage and keep raising the dividend, which is more than many indebted CPG peers can say.

Here the management-credibility test becomes concrete and, refreshingly, falsifiable. Smucker has attached numbers and a deadline to its promise: 3.0x by the end of fiscal 2027. Either the leverage ratio prints near 3.0x on schedule or it does not. The record free cash flow lends real support to the plan; the risk is that a further deterioration in Hostess or a commodity shock knocks EBITDA and pushes the ratio out, since leverage is a ratio and a falling denominator hurts as much as rising debt.1 After a decade of "trust us on the next acquisition," a specific, checkable deleveraging commitment — under activist observation — is exactly the kind of discipline the story has been missing. And there is an option embedded in it: the CFO was explicit that once leverage nears target, the door reopens to share repurchases, which have been suspended entirely in the meantime.[^3] Whether management hits 3.0x on schedule is the clearest near-term read on whether this team has genuinely changed.

Before we war-game the competitive position, there is one more episode that tests a different kind of management competence — not capital allocation, but operational execution and food safety.

VIII. Operational Drama: The 2022 Jif Salmonella Crisis

In May 2022, Smucker issued a sweeping voluntary recall of dozens of Jif peanut butter products after they were linked to a multi-state Salmonella outbreak traced to its plant in Lexington, Kentucky — one of the largest peanut butter facilities in the world.[^32] Jif is not a side brand; it is the leading peanut butter in America and a cornerstone of the spreads franchise. Pulling it from shelves nationwide, and idling a flagship plant, was a serious operational and financial event.

The direct costs — product returns, destroyed inventory, lost sales, and manufacturing downtime — landed in a band of roughly $120 million to $175 million, and management guided an unfavorable adjusted EPS impact of about 80 cents for fiscal 2023.28 For a company that measures its self-worth in the reliability of Folgers and Jif, a self-inflicted supply-chain crisis in a core brand was a genuine embarrassment.

The uncomfortable part, from a diligence standpoint, is what regulators found. The FDA's subsequent warning letter documented that the outbreak strain of Salmonella was not a freak, one-off contamination. Environmental samples matching the outbreak cluster had been found at the Lexington facility repeatedly over years, with genetic evidence pointing to a resident strain present in the plant environment as far back as 2010.29 In other words, this was not lightning striking a spotless operation; it was a latent execution gap in food-safety controls that finally produced an outbreak. For investors, that reframes the event: the cost was one-time, but the process weakness it exposed is the kind of thing that recurs if the underlying culture and controls are not fixed.

And yet the brand's recovery is itself an analytically important data point. Once production resumed, Jif rapidly clawed back its shelf space and market share.28 Consumers did not defect en masse; they waited for their brand to come back. That resilience is real evidence of brand strength and habitual loyalty in a category where trust and taste memory run deep — peanut butter is a childhood staple, and shoppers form brand attachments that survive a scare. It is a genuine asset, and it is the same asset that makes the coffee and Uncrustables franchises defensible: in staple foods, habit is a moat.

But the neutral reading is careful: brand loyalty buffered a supply-chain catastrophe, and that is powerful, but it should not be mistaken for a free pass. The recall cost real money and revealed a real control failure; the lesson is that a strong brand can survive an operational stumble, not that operational stumbles are costless. The second-layer diligence point is that food safety is a recurring, not a one-off, risk for a company that runs some of the largest peanut butter and baking plants in the world — the same operational-execution muscle that failed in Lexington in 2022 is the muscle now being asked to stabilize the Hostess bakery network. An investor watching Smucker should treat manufacturing execution not as a solved problem but as an ongoing line item in the risk budget, precisely because the company's edge — those billion-dollar plants — is also a concentration of operational risk.

Brand strength buffering a shock is, in fact, the perfect segue into the strategic core of this story — because "how strong, really, are these brands, and against whom?" is exactly the question the frameworks are built to answer.

IX. Strategic Analysis: Helmer's 7 Powers & Porter's 5 Forces

Strip away the narrative and Smucker is a war of position — a collection of mature brands fighting for the most valuable real estate in America: the eye-level shelf in a store owned by someone far more powerful than any single brand. Two frameworks help war-game whether Smucker's positions are genuinely defensible or merely comfortable.

Hamilton Helmer's 7 Powers asks where a company has durable advantages that a competitor cannot easily replicate.

Scale Economies (genuinely high, but concentrated). Smucker's real structural edge is manufacturing scale in specific categories. The billion-dollar McCalla plant and its sister facilities give Uncrustables unit economics a would-be competitor cannot match without sinking comparable capital, and Smucker's peanut butter and coffee volumes spread fixed costs thin. This is the most credible power in the portfolio — but note it is category-specific, not company-wide. It does nothing to protect Hostess.

Brand (high, but not uniform). Folgers, Jif, and Milk-Bone carry real consumer trust that supports pricing power and shelf presence, and the Jif recovery quantified that trust in action. But "brand" is doing uneven work across the portfolio: it is powerful in peanut butter and coffee, and it has been actively written down in sweet baked snacks. A brand that requires a $454 million impairment is, by definition, not exercising much pricing power.

Cornered Resource (moderate). The Dunkin' licensing agreement, exclusive and running to 2039, is a legitimate cornered resource — a premium, differentiated coffee franchise Smucker monetizes without owning. Its deep distribution across both grocery and the convenience-store channel is a real, if replicable, advantage that it is now leveraging hard for Uncrustables. What Smucker largely lacks are the other Helmer powers — there are no meaningful network effects in shelf-stable food, essentially no switching costs (a shopper substitutes brands in a second), and no counter-positioning against a rival who cannot copy its model. That absence is the point: Smucker's moats are scale, brand, and distribution, and where those are weak — Hostess — there is no moat at all.

Porter's Five Forces explains why even a good brand portfolio is a hard place to earn.

Bargaining power of buyers (very high). Smucker does not sell to consumers; it sells to Walmart, Costco, Kroger, and Target, and those retailers hold the whip. They control the shelf, demand trade spending and price concessions, and can favor their own private label. Every quarter, Smucker must prove its "velocity" — how fast a product sells per unit of shelf space — to justify premium placement. This is the force that most constrains Smucker's economics, and it never relents.

Threat of substitutes (high). Private label is a direct, potent substitute in coffee, peanut butter, and basic snacks, and it gains share precisely when inflation squeezes consumers — which is to say, exactly when Smucker most needs pricing power. In indulgent snacks, the substitute is broader still: the GLP-1 user simply eats less cake.

Competitive rivalry (high). Smucker fights for "share of stomach" against far larger and well-capitalized giants — Nestlé, Mondelez, Kraft Heinz, General Mills, and Starbucks in packaged coffee — each with its own scale and marketing firepower. Smucker is a focused number one or number two in several categories rather than the biggest player overall, which is a defensible niche strategy but not a dominant one.

The two remaining forces are milder. Supplier power is real but familiar — green coffee, peanuts, wheat, and packaging are volatile commodities Smucker manages through hedging and pass-through pricing rather than owning outright. The threat of new entrants at national scale is low: the capital, distribution, and brand-building required to challenge a Folgers or an Uncrustables is precisely the barrier Smucker itself relies on.

One point of scale worth putting in perspective: at roughly $9 billion in revenue, Smucker is a mid-sized player in a field of giants. Nestlé and Mondelez are multiples of its size; even Kraft Heinz and General Mills are considerably larger. Smucker's answer to that scale gap is not to be bigger overall but to be number one or two in specific categories — coffee, peanut butter, fruit spreads, dog snacks, frozen sandwiches — where category leadership, not corporate heft, drives the shelf negotiation. That is a coherent strategy, and it is why the company's true scale economies are category-specific rather than company-wide. It also explains the appeal, and the danger, of a Hostess: buying category leadership in one stroke is faster than building it, but only if you do not overpay for a category that is itself in structural decline.

Myth versus reality. Three consensus narratives about Smucker deserve correction. The first is that it is a "56-year dividend grower" — a figure that circulates in secondary summaries; the verifiable streak of annual increases is closer to 29 years, still a Dividend Aristocrat record but not a half-century one.9 The second is that Smucker is a sleepy, no-growth value stock; in reality it houses one of packaged food's best organic growth stories in Uncrustables, alongside genuinely declining assets in Hostess — the "sleepy conglomerate" label hides enormous internal dispersion. The third, and most important for investors, is that the Hostess write-downs are "just non-cash accounting." They are non-cash, but they are also the auditors and management jointly certifying that reality fell short of the underwriting — which makes them the single most honest number in the whole story about how this management prices acquisitions.

Net assessment: Smucker's competitive position is strong where it is built on manufacturing scale and beloved single-purpose brands (coffee, peanut butter, Milk-Bone, Uncrustables) and structurally weak where it overpaid for a category — indulgent snacking — facing simultaneous buyer power, private-label substitution, and a secular demand headwind. The frameworks, in other words, largely corroborate the market's suspicion: the core is a fortress, and the most expensive recent acquisition sits outside its walls.

That split verdict is the perfect frame for the closing debate.

X. SJM Investment Story: Bull vs. Bear Case

Every investment case for Smucker comes down to a single question: is this a high-quality, cash-generative brand portfolio temporarily obscured by the wreckage of one bad deal — or a serial overpayer whose good brands merely subsidize a pattern of value destruction? Here is the honest version of both sides.

The bull case. The core is genuinely excellent and getting cleaner. Uncrustables is a $1 billion brand with real runway in convenience stores, schools, and new formats, backed by a just-built billion-dollar plant and defended by manufacturing scale rather than a fragile patent.2 Coffee is a resilient, market-leading cash engine where falling revenue in FY2027 is expected to lift profit as green-coffee deflation flows through, with Café Bustelo compounding past $500 million.[^3] The pet segment, after painful surgery, now throws off the company's highest margins at 29.6% on a defensible Milk-Bone/Meow Mix core.1 Management has attached a specific, checkable deleveraging commitment — 3.0x by end of FY2027 — supported by record free cash flow of $1.16 billion, and it has demonstrated with the Post and Voortman divestitures that it will cut losing assets.1[^31] And underpinning it all is a rock-solid dividend and a family owner with a multi-decade time horizon. The activist's arrival, on this read, is a catalyst that forces the last mile of discipline.

The bear case. The acquisition track record is the whole problem, and it is not one deal. Ainsworth was bought for $1.9 billion and exited inside a $1.2 billion package; Hostess was bought for $5.6 billion and written down by roughly $2.9 billion in under two years.421 That is a repeated behavior — pay a premium multiple for mature "growth," then impair it — and it directly undercuts management's credibility on capital allocation. The Hostess assets face a rare triple threat: a squeezed low-income consumer, aggressive private label, and the structural, long-duration demand risk from GLP-1 weight-loss drugs, which is precisely the kind of headwind that keeps depressing terminal-value assumptions. Coffee's guided revenue decline highlights how hard organic top-line growth is without simply raising prices. And the margin structure remains hostage to volatile green coffee, peanut, and packaging costs plus a standing 10% tariff drag.[^3] A skeptic would add that segment redefinitions and a steady drumbeat of "one-time" charges make the underlying trajectory harder to audit — and that the presence of an activist is a symptom, not a solution.

The activist stress test. Put yourself in the seat of a skeptical long/short investor and the challenges write themselves. Capital allocation: three impaired or exited large deals (Big Heart, Ainsworth, Hostess) is a pattern, not a run of bad luck, and it argues that the reflex to buy mature "growth" at premium multiples is a structural flaw in how the company thinks. Governance: a combined CEO/president/chair, a fifth-generation leader, and a board only now being refreshed under external pressure. Portfolio complexity: coffee, spreads, frozen sandwiches, pet snacks, and cake are five quite different businesses whose only obvious synergy is shared retail distribution. Disclosure: a mid-year segment redefinition and a steady cadence of "one-time" charges make the clean underlying trajectory harder to see. Leverage: a company that promised conservatism levered to 4.4x for a deal it then wrote down by more than half. Each of these is a fair criticism, and together they explain exactly why an Elliott is in the stock. The bullish rebuttal is that every one of these is fixable — and that the presence of an activist raises the odds the fixes actually happen.

The current risk radar. Beyond the segment debates, three mechanisms deserve monitoring. Refinancing and cost of capital: with roughly $6.9 billion of net debt and interest expense guided near $345 million in FY2027, Smucker's equity value is sensitive to where rates sit when its debt matures — deleveraging is partly a race to shrink that exposure.2[^3] Input-cost and geopolitical risk: green coffee, peanuts, wheat, sugar, and packaging are all volatile, and the coffee franchise in particular is now hostage to tariff policy on an un-substitutable import. Execution risk in the Hostess turnaround: the plant fires and cost overruns of the past year show how quickly a stabilization plan can slip. Notably absent from Smucker's radar is the technology-disruption risk that dominates other sectors — nobody is going to disrupt peanut butter with software — which is part of why the business is defensive; its risks are old-economy risks of cost, consumer, and capital, not obsolescence.

Where the evidence actually points. The bull and bear are arguing about two different parts of the same company, and both are right about their part. The disagreement that matters is about the future: does the excellent core (coffee, Uncrustables, pet, peanut butter) compound fast enough and deleverage cleanly enough to more than offset a Hostess business that may never earn its keep? The honest answer is that it is unresolved, and the resolution is observable rather than a matter of faith. Three things will settle it.

KPIs to watch.

-

Uncrustables volume growth. This is the organic growth engine, and the question is whether it can sustain mid-single-digit growth and keep adding households off a $1 billion base, or whether it is approaching saturation as private label fills the freezer. If Uncrustables stalls, the bull case loses its motor.

-

Net debt-to-EBITDA leverage. The clearest, most falsifiable test of management credibility. Management promised roughly 3.0x by the end of fiscal 2027, from 3.8x. Hitting it on schedule would be concrete evidence that the team has genuinely turned toward discipline; missing it would validate every doubt about capital allocation.

-

Sweet Baked Snacks segment margin. Fiscal 2026's 10.0% margin is roughly half a healthy CPG snacking margin.1 Whether Smucker can drive it back toward the high teens or twenties — or whether it eventually divests the business it just wrote down — is the referendum on the entire Hostess adventure, and on whether Smucker's big-M&A instincts can ever be trusted again.

The apple-butter company that hand-signed its crocks built its whole identity on a promise that what was inside would be good. A century and a quarter later, the question for investors is narrower but rhymes: when this management team signs its name to a multi-billion-dollar acquisition, is that still a guarantee of quality — or just a guarantee of the write-down to come? The next two fiscal years, measured against numbers management has itself put on the record, will answer it.

References

-

The J.M. Smucker Co. Announces Fiscal Year 2026 Fourth Quarter Results and Provides Full-Year Fiscal 2027 Outlook — PR Newswire, 2026-06-09 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Fiscal Year 2026 Fourth Quarter Earnings Prepared Management Remarks — The J. M. Smucker Company, 2026-06-09 ↩↩↩↩

-

The J. M. Smucker Company (SJM) Q3 2026 Earnings Call Transcript — Seeking Alpha, 2026-02-26 ↩↩↩↩↩↩↩↩↩↩↩↩

-

The J.M. Smucker Co. Form 10-Q for the quarter ended January 31, 2026 (Q3 FY2026, Sweet Baked Snacks impairments) — U.S. Securities and Exchange Commission ↩↩↩↩

-

The J.M. Smucker Company Definitive Proxy Statement (DEF 14A), 2026 — U.S. Securities and Exchange Commission ↩↩

-

The J.M. Smucker Company — Encyclopedia of Cleveland History, Case Western Reserve University ↩

-

With a name like Smucker's, it had to be good — Akron Beacon Journal / Ohio.com, 2015-06-15 ↩

-

The J.M. Smucker Company Announces Leadership Transition to Foster Next Chapter of Growth and Success — PR Newswire, 2016-03-14 ↩

-

Dividend Aristocrats in Focus: The J.M. Smucker Company — Sure Dividend, 2026-03-05 ↩↩

-

Smucker Completes Folgers Acquisition — IndustryWeek, 2008-11 ↩↩

-

The J.M. Smucker Company Acquires Leading Hispanic Brands From Rowland Coffee Roasters — PR Newswire, 2011-05-16 ↩

-

Dunkin' Brands, The J.M. Smucker Company and Keurig Expand Partnership to Make Dunkin' K-Cup Packs Available at Retail — PR Newswire, 2015-02 ↩

-

Smucker targets coffee margin efficiency after leadership reset — FoodNavigator-USA, 2026-02-19 ↩

-

J.M. Smucker Co. opens new Colorado facility — Food Business News, 2019-07-31 ↩

-

JM Smucker opens Uncrustables facility in Alabama — Manufacturing Dive, 2024-11 ↩

-

The J. M. Smucker Company to Acquire Big Heart Pet Brands — The J. M. Smucker Company, 2015-02-03 ↩

-

The J. M. Smucker Company Form 10-K, Fiscal Year 2019 — U.S. Securities and Exchange Commission ↩

-

The J. M. Smucker Company Completes Acquisition of Ainsworth Pet Nutrition, LLC, Maker of Rachael Ray Nutrish — PR Newswire, 2018-05-14 ↩

-

The J.M. Smucker Co. Completes the Divestiture of Several Pet Food Brands to Post Holdings, Inc. — PR Newswire, 2023-04-28 ↩↩

-

The J. M. Smucker Co. Completes the Acquisition of Hostess Brands — PR Newswire, 2023-11-07 ↩

-

Smucker agrees to buy Twinkies maker Hostess Brands for $5.6 billion — CNBC, 2023-09-11 ↩

-

J.M. Smucker to Buy Twinkies Maker Hostess Brands for $5.6 Billion — Reuters, 2023-09-11 ↩

-

The J.M. Smucker Co. Form 10-Q for the quarter ended January 31, 2025 (Q3 FY2025 impairments) — U.S. Securities and Exchange Commission ↩

-

The J.M. Smucker Co. Announces Fiscal Year 2025 Fourth Quarter Results — PR Newswire, 2025-06-10 ↩

-

J.M. Smucker ramps up work on Hostess turnaround — Baking Business, 2025 ↩

-

The J.M. Smucker Co. Announces Fiscal 2023 First Quarter Results — PR Newswire, 2022-08-23 ↩↩

-

Warning Letter: J.M. Smucker LLC — 638042 — U.S. Food and Drug Administration, 2023-01-24 ↩

-

J.M. Smucker to spend over $120M on Hostess plant expansion in Columbus, Georgia — Food Dive, 2025-10 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube