Sherwin-Williams: The 158-Year Paint Empire That Covered the Earth

I. Introduction & Cold Open

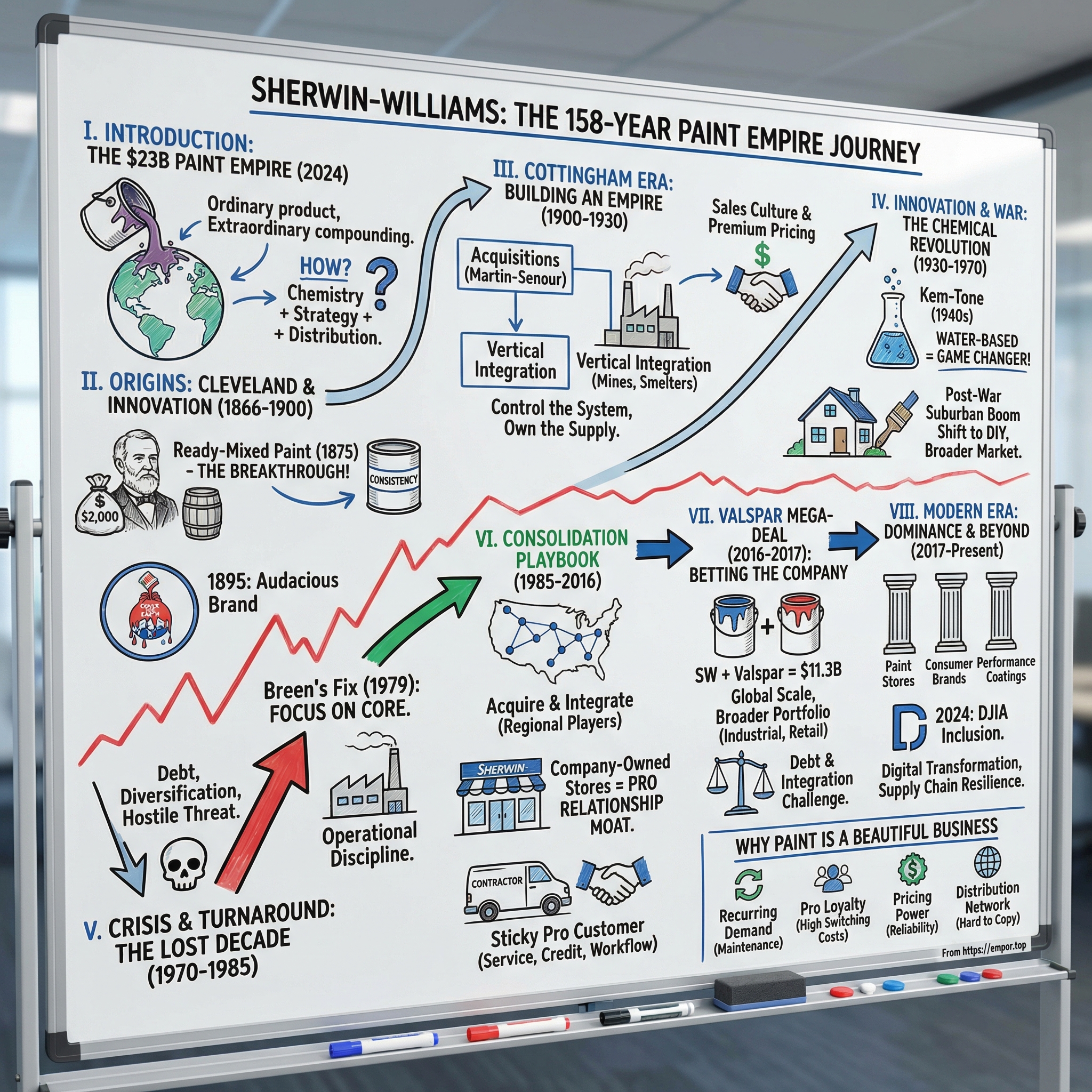

Picture this: March 20, 2016. John Morikis, CEO of Sherwin-Williams, stands before a room of stunned analysts. He's just announced the company will pay $11.3 billion—yes, billion with a B—for Valspar Corporation. The room goes silent. Then the questions flood in: Why pay a 41% premium? Why take on $8.3 billion in new debt for a company with overlapping products? Why risk everything the 150-year-old company had built?

Morikis smiles. He knows something the room doesn't fully grasp yet. This isn't just an acquisition—it's the final chess move in a century-long game of consolidation. With this deal, Sherwin-Williams wouldn't just be a paint company anymore. It would become the undisputed emperor of global coatings, a $23 billion revenue colossus that touches every surface from your living room walls to the Boeing 787 you fly in. Today, as we record this episode in early 2025, Sherwin-Williams stands at a record $23.10 billion in annual revenue, with diluted earnings per share up 14.1% to $10.55. The company operates over 5,000 stores globally, commands premium valuations, and was just added to the Dow Jones Industrial Average in November 2024—a validation of its transformation from regional paint maker to global industrial powerhouse.

But here's what makes this story so compelling for students of business history: Sherwin-Williams didn't win through technological disruption or venture capital moonshots. They won through 158 years of relentless execution, strategic consolidation, and an almost religious devotion to owning their distribution. It's a playbook that would make John D. Rockefeller proud—and considering they bought Standard Oil's old cooperage facilities in their early days, perhaps that's fitting.

So how did a small Cleveland paint shop founded with one man's life savings become the company that literally covers the earth? How did they survive the Great Depression, fend off hostile takeovers, and emerge from near-bankruptcy to dominate an industry? And what can modern founders and investors learn from their century-and-a-half playbook?

Let's paint this picture together.

II. Origins: Cleveland Dreams & Chemical Innovation (1866-1900)

The year is 1866. The Civil War has just ended. Cleveland is booming—iron ore from the Great Lakes, oil from Pennsylvania, and ambitious industrialists everywhere. Into this crucible walks Henry Almon Sherwin, a 24-year-old with exactly $2,000 to his name—his entire life savings—and a radical idea: what if paint didn't have to be mixed by hand every single time?

See, in 1866, if you wanted to paint something, you didn't go to a store and buy a can. You bought white lead, linseed oil, and pigments separately. Then you—or more likely a professional painter—spent hours grinding and mixing them together, hoping the consistency was right, praying the color matched what you mixed last week. It was alchemy more than science, craftsmanship more than commerce.

Sherwin partnered with Edward Williams and A.T. Osborn to form Sherwin, Williams & Company in 1870. But the real breakthrough came in 1873 when they made a move that would define their strategic DNA forever: vertical integration. They purchased a former Standard Oil cooperage facility. Yes, that Standard Oil—Rockefeller's empire was literally next door, and young Sherwin was taking notes.

The cooperage gave them something crucial: the ability to manufacture their own containers. But Sherwin saw further. In 1875, he achieved what others thought impossible: ready-mixed paint that stayed stable in the can.

"Gentlemen," Sherwin reportedly told skeptical dealers, "imagine your customers walking in, pointing to a color, and walking out with paint ready to apply. No mixing. No mess. No uncertainty."

The dealers laughed. The contractors scoffed. Paint was a craft, not a commodity. But Sherwin persisted, personally visiting job sites, demonstrating his product, converting skeptics one brushstroke at a time.

By 1880, the company was selling $63,000 worth of paint annually. Not bad, but Sherwin wanted more. In 1884, when Osborn wanted out, Sherwin didn't hesitate—he bought him out and incorporated as The Sherwin-Williams Company. The next year, he opened what would become a signature move: the company's first retail store, right there in Cleveland.

But it was in the 1890s that Sherwin-Williams created perhaps the most brilliant piece of industrial branding ever conceived. Picture the meeting: "We need a logo that captures our ambition," someone says. They emerge with an image of paint pouring over a globe with three words: "Cover the Earth."

Think about the audacity of that slogan in 1895. This is a company with a handful of stores in Ohio claiming they'll cover the entire planet. It's like a garage startup today choosing the domain "Everything.com." But Sherwin meant it. By 1900, they had stores stretching from Boston to San Francisco, revenue approaching $2.3 million, and a playbook that would guide them for the next century: control your inputs, own your distribution, and never, ever compete on price alone.

The foundation was set. Cleveland's paint rebels were ready to build an empire.

III. The Cottingham Era: Building an Empire (1900-1930)

Walter H. Cottingham arrived at Sherwin-Williams in 1909 with the demeanor of a battlefield general and the instincts of a chess grandmaster. Named president in 1909 and CEO in 1913, he looked at the American paint industry—hundreds of small regional players, each protecting their little fiefdoms—and saw opportunity for total domination.

"Why compete," Cottingham asked his board, "when we can simply acquire?"

His first major move came in 1917: the acquisition of Martin-Senour Company for $8.3 million. In today's dollars, that's roughly $200 million—a massive bet for a company that had just crossed $10 million in annual revenue. The board was nervous. The bankers were skeptical. But Cottingham had done his math: Martin-Senour brought 15 new factories, established distribution in the Southeast, and most importantly, eliminated a dangerous competitor.

The real genius wasn't just the acquisition—it was what came next. While other companies might have slashed costs and merged operations, Cottingham kept the Martin-Senour brand alive, maintaining customer relationships while quietly converting their best practices to the Sherwin-Williams way. It was a template they'd use again and again: buy the competitor, keep the brand, own the market.

Then came 1920, and Cottingham's masterstroke: taking Sherwin-Williams public. The IPO raised $15 million—approximately $230 million in today's money. But Cottingham didn't use it for dividends or executive bonuses. Every penny went into expansion. More stores. More factories. More vertical integration.

By 1921, Sherwin-Williams wasn't just making paint. They owned lead mines in Missouri. They operated linseed oil mills across the Midwest. They had their own railroad cars to transport raw materials. When a supplier tried to raise prices, Cottingham would smile and say, "That's interesting. We'll just make it ourselves."

The numbers tell the story: Revenue exploded from $2.3 million in 1900 to $34.2 million by 1919. By the mid-1920s, Sherwin-Williams was the largest paint manufacturer in the world. Not in America—in the world.

But Cottingham's greatest innovation might have been cultural. He created what employees called the "Sherwin-Williams Way"—a sales culture that was part military discipline, part religious fervor. Sales representatives didn't just sell paint; they were missionaries spreading the gospel of quality coatings. They wore suits and ties to construction sites. They knew their customers' children's names. They'd show up at 6 AM if that's when the contractor started work.

One legendary story from 1925: A Sherwin-Williams sales rep in Chicago heard that a major commercial project was using a competitor's paint. He didn't just make a sales call. He spent three days on the job site, helping the painters understand proper application techniques, bringing coffee and donuts each morning, essentially embedding himself with the crew. By day four, the contractor switched the entire project to Sherwin-Williams. That rep was promoted to district manager within a year.

Cottingham also pioneered something that seems obvious now but was radical then: national advertising. In 1925, Sherwin-Williams became one of the first industrial companies to advertise in the Saturday Evening Post. The ads didn't talk about price. They talked about quality, about protecting your investment, about the peace of mind that comes from choosing the best. Premium positioning for premium prices—a strategy that would define the company for the next century.

By 1929, on the eve of the Great Depression, Sherwin-Williams operated 106 company stores, had manufacturing facilities across the country, and generated over $47 million in revenue. They'd gone from regional player to national powerhouse in less than two decades.

The empire was built. Now it would be tested by the greatest economic catastrophe in American history.

IV. Innovation & War: The Chemical Revolution (1930-1970)

October 1929. The stock market crashes. Paint sales plummet 60% almost overnight. Competitors slash prices, close factories, declare bankruptcy. At Sherwin-Williams headquarters in Cleveland, executives gather for an emergency meeting. The consensus: cut everything, survive at any cost.

Then R&D director George Martin stands up. "Gentlemen," he says, "our competitors are cutting research. This is our chance to leap ahead."

It was counterintuitive. It was risky. It was brilliant.

While others retreated, Sherwin-Williams doubled down on innovation. They hired chemists being laid off elsewhere. They expanded their research facilities. And in 1941, they achieved a breakthrough that would revolutionize not just paint, but how America lived: Kem-Tone, the world's first successful water-based paint.

imagine the pitch meeting: "We've created paint that cleans up with water, dries in an hour, and doesn't smell like a chemical factory." The old-timers were skeptical. Real paint used oil. Real paint took skill to apply. This water-based stuff was for amateurs.

Then Pearl Harbor happened.

Suddenly, oil was rationed for the war effort. Professional painters were drafted. But the homefront still needed paint—for military facilities, for defense plant housing, for morale. Kem-Tone was the answer. It required no special skills to apply. Rosie the Riveter could paint her apartment after her shift at the bomber plant.

The marketing was genius: "Kem-Tone: So easy, even your wife can do it!" (Yes, different times). By 1943, Sherwin-Williams was selling 10 million gallons of Kem-Tone annually. They couldn't make it fast enough.

But here's the untold story: Sherwin-Williams' real contribution to the war effort wasn't consumer paint—it was specialized coatings for the military. Camouflage paint that could withstand Pacific humidity. Anti-fouling coatings for Liberty Ships. Fire-retardant treatments for aircraft carriers. The company's chemists worked around the clock, sometimes sleeping in the labs, developing formulations that might save American lives.

One classified project, only declassified decades later: a special coating for the Manhattan Project facilities that could contain radioactive contamination. The margin on that contract? Sherwin-Williams charged cost plus 1%. "This is for the country," the CEO said. "Profit comes second."

Post-war America exploded into suburbia, and Sherwin-Williams was ready. They'd spent the war years perfecting not just water-based paints but an entire ecosystem of consumer-friendly products. Color matching systems. Roller applicators (they held key patents). Step-by-step painting guides. They transformed painting from a professional trade to a weekend warrior activity.

In 1958, they opened their 1,000th store. By 1964, they crossed $500 million in annual revenue. The innovation pipeline never stopped: latex paints, texture coatings, industrial finishes for the booming automotive industry. In 1996, the American Chemical Society designated Kem-Tone a National Historic Chemical Landmark, recognizing its role in "democratizing home decoration."

But the 1960s brought new challenges. Environmental concerns about lead paint. Foreign competitors with lower costs. Conglomerates circling, looking for acquisition targets. The company that had innovated its way through depression and war would soon face its darkest hour.

The storm clouds were gathering in Cleveland.

V. Crisis & Turnaround: The Lost Decade (1970-1985)

January 1977. The Sherwin-Williams board of directors sits in stunned silence as the CFO delivers the news: an $8.2 million loss on $1 billion in revenue. The company that had never lost money in 111 years was bleeding red ink. Worse, debt had exploded from essentially zero to $242 million in just five years. The culprit? A disastrous expansion into retail chains and unrelated businesses, combined with the brutal 1974-75 recession.

Then, like sharks smelling blood, Gulf + Western Industries strikes. The conglomerate, led by corporate raider Charles Bluhdorn, quietly accumulates 13.47% of Sherwin-Williams stock. Their intent is clear: hostile takeover, breakup, and asset stripping. The paint company that covered the earth was about to be carved up and sold for parts.

The board panics. Stock price crashes to $14 per share, down from $45 just three years earlier. Executives flee. Morale collapses. Store managers report that competitors are telling customers, "Better buy from us—Sherwin-Williams won't exist next year."

Enter John G. Breen.

Breen wasn't a paint guy. He was a turnaround specialist who'd saved Rubbermaid from bankruptcy. When Sherwin-Williams' board approached him in late 1978, he spent three days touring stores incognito, talking to employees, testing the culture. His conclusion: "The bones are good. The strategy is garbage."

Breen's first day as CEO, February 1, 1979, became legend. He called an all-hands meeting at headquarters. No prepared remarks. No PowerPoint. Just Breen, in shirtsleeves, standing on a paint can.

"We're going to war," he announced. "Not against our competitors—against mediocrity. Against complacency. Against anyone who thinks this company's best days are behind it."

His turnaround plan was brutal in its simplicity: - Sell everything that isn't paint or coatings - Close underperforming stores ruthlessly - Cut corporate staff by 30% - Implement zero-based budgeting - Focus fanatically on the professional contractor

The old guard resisted. "We've always done it this way," they said. Breen's response: "And look where it got us."

But the real fight was with Gulf + Western. Bluhdorn wanted board seats. He demanded asset sales. He threatened a proxy fight. Breen flew to New York for a face-to-face confrontation. The meeting, as later recounted by attendees, was epic.

"Mr. Bluhdorn," Breen said, "you know nothing about paint. You know everything about financial engineering. Here's my offer: Give me 18 months. If I don't turn this around, I'll personally recommend the board accept your takeover offer."

Bluhdorn, perhaps surprised by Breen's audacity, agreed. But he kept buying stock, eventually reaching 15% ownership.

Breen moved fast. He sold the chemical division for $78 million. Closed 150 underperforming stores. Cut $50 million in costs. But he also invested—upgraded store computers, launched contractor training programs, developed new high-margin industrial coatings.

The masterstroke came in 1980. Breen discovered that many of Sherwin-Williams' best customers—professional painters—were buying some products from competitors because Sherwin stores didn't carry every tool and supply they needed. His solution: turn every store into a full-service contractor supply center. Brushes, rollers, ladders, masking tape—everything a pro needed, all with the Sherwin-Williams guarantee.

By 1981, the turnaround was undeniable. Profit hit $61 million. Debt dropped below $100 million. Stock price doubled. Gulf + Western, seeing the momentum and facing their own troubles, quietly sold their stake.

Breen wasn't done. In 1984, he made a bold prediction: "By 1990, Sherwin-Williams will generate $2 billion in revenue and $200 million in profit." The analysts laughed. The company had never crossed $1.5 billion in revenue.

They hit both targets by 1989, a year early.

The lessons from the Breen era became business school case studies: Focus beats diversification. Distribution is destiny. And sometimes, the best defense against corporate raiders is simply executing better than they ever imagined possible.

The empire was saved. Now it was time to expand.

VI. The Consolidation Playbook (1985-2016)

December 1995. Christopher Connor, Sherwin-Williams' new CEO, stands before Wall Street analysts with an audacious claim: "We will acquire 16 companies in the next 21 months."

The room erupts. "That's impossible," one analyst shouts. "You'll destroy your balance sheet," says another. Connor smiles. "Watch us."

What followed was perhaps the most methodical, successful consolidation strategy in American industrial history. Not flashy roll-ups or leveraged buyouts, but strategic, surgical acquisitions that expanded geography, capability, or customer access. The playbook was deceptively simple:

- Target family-owned regional players facing succession issues

- Pay fair prices, not auction premiums

- Keep the local brand and relationships

- Integrate back-office functions immediately

- Apply Sherwin-Williams' superior operations and margins

The first major move: Pratt & Lambert in 1996 for $400 million. A 172-year-old company with strong architectural positions in the Northeast. Within 18 months, Sherwin-Williams improved their EBITDA margins from 8% to 14% simply through better purchasing and distribution.

But Connor's real genius was the store expansion strategy. While competitors like Benjamin Moore relied on independent dealers, Sherwin-Williams went all-in on company-owned stores. The math was compelling: a typical store required $400,000 to open, generated $2 million in annual revenue within three years, and produced 20% EBITDA margins. Return on investment: over 100% annually.

By 2002, they'd crossed 2,500 stores. Each one was a fortress—professionally designed, stocked with everything a contractor needed, staffed by people who knew paint chemistry, not just retail sales.

The strategic positioning was brilliant. Home Depot and Lowe's were exploding, taking the DIY market. Rather than fight them, Connor focused on the pros. "Let them have the weekend warriors," he told his team. "We'll take the people who paint for a living."

The contractor loyalty programs they developed were revolutionary. Volume discounts, yes, but also: 30-day billing terms, job-site delivery, custom color matching, dedicated account representatives. One contractor in Texas told me: "Switching from Sherwin-Williams would be like divorcing my wife—theoretically possible, but the disruption would kill me."

In 2004, Connor made his boldest technology bet: a proprietary color-matching system that could scan any surface and formulate exact matches in minutes. The R&D cost: $73 million. The competitive advantage: priceless. Designers could match fabric swatches. Contractors could match existing walls perfectly. Nobody else had anything close.

Then came 2007—the housing crisis. Competitors panicked, cut stores, slashed costs. Connor saw opportunity. "Downturns are when market share is won," he said. Sherwin-Williams acquired 15 regional players between 2008-2010, paying distressed prices, gaining prime locations and customer relationships.

The numbers from this era are staggering: - Store count grew from 1,837 (1985) to 4,086 (2015) - Revenue expanded from $1.8 billion to $11.3 billion - EBITDA margins improved from 9% to 16% - Return on equity averaged 28% annually

In 2012, they made a prescient move: launched an EPA-registered paint with antimicrobial properties that killed 99.9% of bacteria. Hospitals, schools, restaurants—entirely new markets opened up. By 2015, it was a $500 million business.

But Connor knew the easy consolidation gains were ending. The regional players were gone. The store footprint was reaching saturation. To keep growing, Sherwin-Williams needed something bigger. Something transformational.

In late 2015, Connor's successor, John Morikis, started making calls to Minneapolis. The target: Valspar Corporation. The price tag: $11.3 billion. The biggest bet in company history was about to unfold.

VII. The Valspar Mega-Deal: Betting the Company (2016-2017)

March 20, 2016, 6:00 AM. John Morikis' phone rings. It's his CFO: "Goldman Sachs is ready. The financing is secured. Are we really doing this?"

Morikis doesn't hesitate. "Make the call."

Four hours later, the business world gasps: Sherwin-Williams will acquire Valspar for $113 per share, all cash—a $11.3 billion deal that would create the world's largest coatings company by revenue. The premium: 41% above Valspar's Friday closing price. The debt: $8.3 billion in new borrowing for a company that had prided itself on conservative balance sheets.

The skeptics pounced immediately. "Morikis has lost his mind," one hedge fund manager told CNBC. "They're paying 20 times EBITDA for a company with massive overlap." Another analyst calculated that Sherwin-Williams would need to cut $500 million in costs just to make the math work.

But Morikis had been planning this for years. In private strategy sessions, he'd mapped out the global coatings industry like a general planning a campaign. The DIY market was mature. The pro market was consolidated. But industrial coatings—automotive, packaging, coil, wood—that's where the growth was. And Valspar owned crown jewels in each segment.

The real prize wasn't even Valspar's core business. It was their packaging coatings division—the technology that goes inside food and beverage cans. Sounds boring? Consider this: every Coca-Cola can in the world needs interior coating to prevent the acid from eating through aluminum. Valspar had 50% global market share. The margins were spectacular. The customer relationships took decades to build.

"This isn't about paint," Morikis told his board. "It's about becoming indispensable to global manufacturing."

The integration plan was military in precision. Code name: Project Summit. Seventeen work streams. Four hundred dedicated employees. Daily 6 AM war room meetings. The target: $320 million in annual synergies within 36 months.

But first, they had to get regulatory approval. The FTC was concerned—the combined company would control 45% of the North American architectural paint market. For nine months, lawyers battled. Sherwin-Williams offered concessions. The FTC demanded more. Finally, a deal: divest Valspar's architectural business to Axalta for $420 million. Painful, but acceptable.

The financing was a masterpiece of financial engineering. $8.3 billion in bonds across multiple tranches, blended rate of 3.2%. In an era of near-zero interest rates, Morikis locked in generational low costs of capital. One bond trader called it "the deal of the decade—they basically borrowed for free to buy an empire."

June 1, 2017: The deal closes. The integration begins.

The first 100 days were brutal. Valspar executives, used to running their own fiefdoms, suddenly reported to Cleveland. Computer systems didn't talk. Sales forces competed for the same customers. In China, a key Valspar factory manager quit, taking his team with him.

But Morikis had learned from studying failed mergers. He kept Valspar's innovation centers open. Retained their best technical talent with golden handcuffs. Most importantly, he didn't try to paint Valspar blue overnight. "We bought their capabilities," he said. "We'd be idiots to destroy them."

By Q4 2017, the synergies were ahead of schedule. Procurement savings alone hit $72 million—turns out, when you're buying titanium dioxide by the millions of tons, every penny matters. The combined R&D pipeline yielded breakthrough products within months. Distribution optimization saved another $45 million.

The numbers vindicated Morikis: - 2018 revenue: $17.5 billion (up 36% from pre-merger) - EBITDA margins expanded to 18.3% - Free cash flow hit $1.9 billion - Stock price rose 42% in 18 months post-close

But the real victory was strategic. Sherwin-Williams was no longer just a North American paint company. They were a global coatings powerhouse with positions in aerospace (Boeing's preferred supplier), automotive (painting Teslas and Toyotas), and packaging (billions of cans annually).

One competitor's executive, speaking anonymously, summed it up: "We thought they overpaid. We were wrong. They bought the future."

VIII. Modern Era: Digital Transformation & Market Dominance (2017-Present)

November 8, 2024. The opening bell at the New York Stock Exchange. Heidi Petz, Sherwin-Williams' CEO, stands on the podium, surrounded by her executive team. As she rings the bell, Sherwin-Williams officially joins the Dow Jones Industrial Average, replacing Dow Inc. It's the ultimate validation—158 years after Henry Sherwin mixed his first batch of paint, his company now stands alongside Apple, Microsoft, and Johnson & Johnson as one of America's 30 most important corporations.

The journey from Valspar integration to Dow inclusion wasn't just about scale—it was about transformation. Under Petz's leadership (she took over from Morikis in 2024), Sherwin-Williams became a digital-first industrial powerhouse while never forgetting its paint store roots. The centerpiece of the modern transformation is physical: a stunning new $750 million headquarters complex rising in downtown Cleveland. The pair of facilities costing a total of $750 million will accommodate 4,000 workers in the downtown building and 600 at the research center. The 36-story tower, when finally completed after construction delays, will stand as Cleveland's fourth-tallest building—a monument to the company's endurance and ambition.

But the real transformation happens inside the stores. Walk into any Sherwin-Williams location today and you're not in a paint store—you're in a solutions center. Artificial intelligence-powered color matching can scan any object and formulate exact matches in seconds. Augmented reality apps let customers visualize colors on their actual walls before buying. Professional contractors access dedicated web portals with job-specific pricing, delivery scheduling, and inventory management.

The numbers tell the story of dominance: Consolidated net sales reached a record $23.10 billion in 2024, with diluted net income per share increasing 14.1% to $10.55. The company generated net operating cash of $3.15 billion, or 13.7% of net sales—cash generation that would make any tech company jealous.

The COVID years tested every assumption. In 2020-2021, DIY demand exploded as locked-down homeowners became weekend painters. Sherwin-Williams scrambled to meet demand, keeping stores open as "essential businesses," implementing curbside pickup before most retailers even knew what that meant. Then came the whiplash: as people returned to offices, DIY collapsed while professional work surged back.

Through it all, the company's response was consistent: invest in the pros. In their architectural business, residential repaint significantly outgrew the market, increasing by a high-single digit percentage as they continued to see returns on prior growth investments, while delivering low-single digit percentage growth in new residential.

The industrial business, supercharged by Valspar, became the growth engine. Sales in industrial businesses were led by double-digit percentage growth in Packaging and low-single digit percentage growth in Coil. These aren't sexy businesses—coating the inside of soup cans, painting metal before it's formed into products—but the margins are spectacular and the customer relationships measured in decades.

Environmental, Social, and Governance (ESG) initiatives, once an afterthought, became central to strategy. The company that once made lead paint now produces coatings that clean the air, kill bacteria, and reduce energy consumption. Their latest innovation: paint that can actually cool buildings by reflecting infrared light, potentially reducing air conditioning costs by 20%.

The digital transformation accelerated. By 2024, over 40% of contractor orders came through digital channels. The company's app became the most-used tool in the professional painting industry, handling everything from color selection to invoice management. Machine learning algorithms predict paint needs based on weather patterns, construction permits, and economic indicators, optimizing inventory across 4,100+ stores.

But perhaps the most important validation came on November 8, 2024, when Sherwin-Williams replaced Dow Inc. in the Dow Jones Industrial Average. With a market cap of $93.5 billion, nearly three times larger than the $33.5 billion Dow Inc. it replaced, Sherwin-Williams had officially joined American corporate royalty.

The inclusion wasn't just symbolic. It represented S&P Dow Jones Indices' recognition that coatings—not traditional chemicals—now better represented the materials sector. It was acknowledgment that Sherwin-Williams had transcended paint to become essential infrastructure for the global economy.

As CEO Heidi Petz noted in recent earnings calls, the company's strategy remains unchanged: dominate professional markets, expand industrial applications, and maintain pricing discipline. The company expects adjusted diluted net income per share in the range of $11.65 to $12.05 for 2025, representing 4.6% growth at the mid-point.

The empire that Henry Sherwin built with $2,000 now influences how the world looks, feels, and functions. From the walls of your home to the car you drive, from the bridge you cross to the can of soda you drink, Sherwin-Williams coatings are everywhere—invisible yet essential.

IX. The Business Model: Why Paint is a Beautiful Business

Warren Buffett once said his ideal business is one that requires minimal capital investment, has pricing power, and enjoys recurring revenue. He might as well have been describing paint. Let's dissect why Sherwin-Williams' business model is a masterclass in economic moats and compound returns.

Start with the physics of paint itself: entropy guarantees demand. Every surface degrades. UV rays fade colors. Moisture causes peeling. Temperature changes create cracks. The average home needs repainting every 7-10 years. Commercial buildings every 3-5 years. Industrial equipment continuously. This isn't discretionary spending that disappears in recessions—it's maintenance. Delay it, and the cost multiplies as substrates deteriorate.

Now layer on the psychology. Paint is 10% of a project's cost but 90% of its visual impact. A $50,000 kitchen renovation can be ruined by bad paint. A $10 million office building's reputation hinges on its finish. When the stakes are that high, nobody quibbles over $5 per gallon. This is why Sherwin-Williams can charge 30-40% premiums over private label brands and contractors happily pay it.

The distribution moat is perhaps the most underappreciated aspect. Those 4,100+ stores aren't just retail locations—they're fortresses of customer captivity. A professional painter visits their local Sherwin-Williams store 2-3 times per week. They know the staff by name. Their purchase history, color preferences, and billing terms are all on file. The store manager knows their busy season, their biggest clients, their cash flow cycles.

Switching costs are brutal. Move to another brand and you lose: - Your negotiated pricing tiers - Net 30-day payment terms (immediate cash flow hit) - Color matching history (reputation risk with clients) - Delivery coordination (operational nightmare) - Technical support relationships (problem-solving capability) - Training and certification programs (career development)

One contractor in Dallas told us: "I've got 15 years of color formulas at Sherwin. Every house I've ever painted. When Mrs. Johnson calls saying she needs touch-ups, I pull up her exact color in seconds. You think I'm starting over at Benjamin Moore?"

The working capital dynamics are gorgeous. Sherwin-Williams gets paid by contractors in 30 days but pays suppliers in 60-90 days. In effect, growth is funded by vendors. The faster they grow, the more cash they generate. It's the opposite of most industrial businesses that consume cash as they expand.

Pricing power is almost algorithmic. Every year: 3-5% price increase in February, another 2-3% in June if raw materials spike. Contractors pass it through to customers. Nobody switches brands over a few percent. From 2010-2024, Sherwin-Williams raised prices approximately 60% cumulatively while volumes still grew. That's pricing power.

The gross margin expansion playbook is elegant: 1. Acquire regional competitor at 35% gross margins 2. Shift their purchasing to Sherwin-Williams' scale (instant 300 basis points) 3. Optimize their product mix toward higher-margin industrial coatings 4. Introduce proprietary products with 50%+ margins 5. Exit low-margin commodity lines Result: 40-42% gross margins within 18 months

Capital allocation is where the model truly shines. Once a store is built, maintenance capex is minimal—maybe $50,000 every five years for remodeling. Technology investments are leveraged across the entire network. R&D spending (about 1% of sales) generates products that can be sold through existing channels with zero additional distribution cost.

This creates a cash generation machine. In 2024, on $23.1 billion in revenue, Sherwin-Williams generated $3.15 billion in operating cash flow. After $650 million in capex, that's $2.5 billion in free cash flow—a 10.8% FCF yield. For comparison, Apple's FCF yield is around 4%.

What do they do with this cash? The capital allocation priorities are clear: 1. Dividend growth (47 consecutive years of increases) 2. Share buybacks (reduced share count 25% since 2015) 3. Bolt-on acquisitions at reasonable multiples 4. Minimal debt maintenance (targeting 2-3x Net Debt/EBITDA)

The return on invested capital tells the story: consistently above 25%, often touching 30%. This means every dollar reinvested in the business generates 25-30 cents of annual profit in perpetuity. Find another industrial company with those returns. We'll wait.

Network effects amplify everything. More stores mean more convenience for contractors. More contractors mean better capacity utilization. Better utilization means lower costs per gallon. Lower costs enable competitive pricing while maintaining margins. It's a virtuous cycle that's nearly impossible for new entrants to break.

The subscription-like revenue model is hidden but powerful. Large contractors essentially run tabs, ordering continuously, paying monthly. Industrial customers sign multi-year contracts with volume commitments. Property management companies standardize on Sherwin-Williams across entire portfolios. It's not Software-as-a-Service, but it might as well be Paint-as-a-Service.

Even the balance sheet is a competitive advantage. With investment-grade credit ratings and proven access to capital markets, Sherwin-Williams can make acquisitions that smaller competitors simply can't finance. They're the buyer of last resort for family-owned paint companies, often the only legitimate option when founders retire.

X. Competitive Analysis & Market Position

In the coatings industry, there are really only three games being played: Sherwin-Williams' professional contractor dominance, PPG's industrial diversification, and everyone else's struggle for survival. Understanding these dynamics is crucial for grasping why Sherwin-Williams' moat keeps widening despite fierce competition.

PPG Industries, the closest thing to a peer, took the opposite path. Where Sherwin-Williams went deep in architectural coatings with company-owned stores, PPG went broad across industrial markets through independent distribution. PPG generates about $18 billion in annual revenue, but only 40% comes from architectural paint. The rest spans automotive OEM, aerospace, marine, and protective coatings. It's a solid strategy—until you compare margins. PPG's EBITDA margins hover around 15-16%. Sherwin-Williams consistently delivers 19-21%. That 400-500 basis point gap, applied to $20+ billion in revenue, equals billions in extra value creation.

Benjamin Moore, owned by Berkshire Hathaway since 2000, represents the premium independent dealer model. Their paint quality is exceptional—many professionals swear it's better than Sherwin-Williams. But quality doesn't equal market share. Benjamin Moore relies on 7,500 independent dealers who also carry competing brands, offer inconsistent service, and lack Sherwin-Williams' contractor programs. Revenue is around $1.5 billion, less than 7% of Sherwin-Williams'. Warren Buffett rarely discusses Benjamin Moore in Berkshire letters, which tells you everything.

The big box dynamic is fascinating. Home Depot and Lowe's combined sell more gallons of paint than Sherwin-Williams. But it's the wrong paint to the wrong customers at the wrong margins. Their customers are homeowners painting once every five years, buying on price, returning half-empty gallons. Sherwin-Williams' customers are professionals painting every day, buying by the pallet, never returning anything. One Sherwin-Williams store manager in Phoenix told us: "Home Depot across the street sells 10 times our gallons at one-third our margin to customers we don't want."

Behr (Home Depot's exclusive brand) and Valspar's former consumer brands (now at Lowe's) dominate DIY but can't crack professional markets. Why? No dedicated service, no contractor pricing, no technical support, no specialized products. They're playing checkers while Sherwin-Williams plays chess.

Regional competitors still exist—Kelly-Moore on the West Coast, Dunn-Edwards in the Southwest—but they're acquisition targets, not threats. Every year, one or two get absorbed, their stores converted to Sherwin-Williams, their customers retained through careful brand management. It's consolidation by a thousand cuts.

The international competitive landscape is more complex. AkzoNobel (Netherlands) and Asian Paints (India) dominate their home markets. But paint is inherently local—color preferences, application methods, and regulations vary by country. Sherwin-Williams' international expansion focuses on industrial coatings where global customers (Boeing, Coca-Cola, Toyota) value consistency across geographies.

Technology disruption seems unlikely. Despite Silicon Valley's efforts, nobody has "Uber-ized" paint. A few startups tried direct-to-consumer models (Clare, Backdrop) but discovered what Sherwin-Williams knew all along: paint is a relationship business. Professionals want credit terms, technical support, and immediate availability—things no app can provide.

Private equity occasionally circles the industry, but the math never works. At 20+ times EBITDA, Sherwin-Williams is too expensive to lever up. Smaller players lack the scale to generate PE returns. The industry's working capital requirements and cyclicality scare off most financial buyers.

Environmental regulations create competitive advantage for incumbents. Developing low-VOC, antimicrobial, or specialty coatings requires massive R&D investment. Smaller players can't afford the compliance costs. Each new regulation raises barriers to entry and drives consolidation toward companies like Sherwin-Williams with the scale to adapt.

The competitive moat scorecard: - Distribution: Sherwin-Williams' 4,100 stores vs. PPG's zero vs. Benjamin Moore's reliance on independents - Contractor relationships: 90%+ wallet share vs. competitors' fragmentation - Vertical integration: Controls supply chain vs. competitors' vendor dependence - Innovation pipeline: $200+ million annual R&D vs. regional players' minimal investment - Financial capacity: Can fund any acquisition vs. competitors' capital constraints - Brand equity: "Cover the Earth" recognition vs. limited brand awareness

The market share trajectory tells the story. In North American architectural paint, Sherwin-Williams' share grew from 25% in 2000 to 35% in 2015 to nearly 45% post-Valspar. In professional markets specifically, their share approaches 60% in some geographies. This isn't market leadership—it's market dominance.

XI. Bear & Bull Cases: The Investment Thesis

The Bull Case: Compounding Machine

The bulls see Sherwin-Williams as Warren Buffett's platonic ideal—a simple business with enduring demand, pricing power, and returns on capital that make software companies jealous. Their argument rests on five pillars that each independently justify ownership, but together create a compounding machine.

First, the North American position is essentially unassailable. With 45% market share and 60% in certain professional segments, Sherwin-Williams has achieved escape velocity. Competitors can't match their store density, contractor relationships, or supply chain efficiency. It would take $10+ billion and a decade to replicate their infrastructure—and by then, Sherwin-Williams would have moved further ahead. This isn't a competitive advantage; it's a monopoly with paint cans.

Second, margin expansion has decades of runway. Current EBITDA margins of 20% could reach 25% through mix shift (more industrial, less DIY), operational leverage (spreading fixed costs over growing volumes), and pricing discipline. Every 100 basis points of margin on $23 billion in revenue equals $230 million in EBITDA. The path from 20% to 25% margins would add $1.15 billion in annual EBITDA—a 25% increase without any revenue growth.

Third, the housing stock dynamic is demographically destined. The median U.S. home is 40 years old. Millennials are finally buying houses—older ones needing paint. Climate change drives more frequent repainting (extreme weather damages coatings). Remote work means homes get painted more often (you notice ugly walls on Zoom). The installed base of surfaces needing paint grows 2-3% annually through construction, creating a perpetual tailwind.

Fourth, capital allocation excellence continues. Management has proven they can deploy capital at 25-30% returns through store expansion, acquisitions, and technology. With $2.5 billion in annual free cash flow, they could acquire $5 billion in revenue at reasonable multiples, adding 20% to the top line while maintaining returns. Or they could buy back 10% of shares annually, driving high-teens EPS growth even with modest revenue increases.

Fifth, industrial coatings offer untapped potential. Sherwin-Williams has barely scratched Asia's industrial market. Electric vehicles require specialized coatings. Renewable energy infrastructure needs protective finishes. The space economy demands extreme-environment coatings. Each new industrial frontier offers margin-accretive growth opportunities the market hasn't priced in.

The Bear Case: Cyclical Trap

The bears see a cyclical company trading at growth multiples, vulnerable to mean reversion in housing, margins, and valuation. Their concerns aren't trivial—they're structural risks that could impair the investment thesis for years.

Housing sensitivity is the obvious weakness. Despite protests about "maintenance demand," 40% of paint sales correlate with housing turnover and construction. When housing freezes—like 2008 or potentially 2025-2026—paint demand craters. Existing home sales are already at decade lows. New construction faces affordability crisis. A housing recession could slash earnings 30-40%, making today's valuation look insane.

Raw material volatility is unhedgeable. Titanium dioxide (the key white pigment) represents 20% of paint costs. Its price can swing 50% in a year based on global supply/demand. Petroleum-based resins, solvents, and additives comprise another 30% of costs. When oil spikes or supply chains break, margins compress faster than prices can adjust. The 2021-2022 period showed this vulnerability—despite aggressive pricing, margins still contracted.

DIY share loss is accelerating. Millennials and Gen Z don't paint—they hire pros or rent. The DIY market that drove growth for decades is structurally declining. Sherwin-Williams abandoned this segment to Home Depot and Lowe's, but what happens when contractors start buying from big boxes too? Exclusive brands like Behr Pro are explicitly targeting Sherwin-Williams' contractor base with 20% lower prices.

International expansion is proving difficult. Unlike industrial coatings, architectural paint doesn't travel. Color preferences, application methods, and channel dynamics vary dramatically by country. Sherwin-Williams' U.S. playbook—company stores and contractor focus—doesn't translate. In Europe and Asia, they're subscale players facing entrenched locals. International remains under 20% of revenue after decades of trying.

ESG and regulatory pressures are mounting. California's air quality rules spread nationally. PFAS regulations could ban entire product categories. Lead paint litigation, though covered by insurance, creates contingent liabilities. Climate regulations favor lower-carbon alternatives to traditional coatings. Each regulatory wave requires costly reformulation and strands existing inventory.

Valuation assumes perfection. At 25x forward earnings and 18x EBITDA, Sherwin-Williams trades at premiums to both industrials and consumer staples. The market prices in continued margin expansion, steady growth, and no cyclical downturns. Any disappointment—a quarter of missed earnings, a failed acquisition, a housing slowdown—could trigger multiple compression. A reversion to historical 18x P/E multiples implies 30% downside.

The bears' nightmare scenario: Housing enters prolonged downturn while raw materials inflate, crushing volumes and margins simultaneously. International expansion fails while domestic share losses accelerate. ESG regulations force massive write-offs of existing products. The stock re-rates from growth to cyclical, falling 40-50% as earnings and multiples compress together.

XII. Lessons & Playbook Takeaways

After 158 years, thousands of acquisitions, multiple recessions, and one near-death experience, Sherwin-Williams has generated insights worth more than any MBA. These aren't theoretical frameworks—they're battle-tested principles that turned $2,000 into $90+ billion.

Lesson 1: Distribution is Destiny Henry Sherwin understood in 1884 what Amazon proved a century later: controlling distribution changes everything. Every competitor who relied on independent dealers eventually lost. Every market Sherwin-Williams entered with company stores they eventually dominated. The stores aren't just sales channels—they're customer data repositories, service centers, brand ambassadors, and competitive moats. In industries with commoditized products, distribution becomes the differentiation.

Lesson 2: Vertical Integration in Commodities Creates Pricing Power When you make paint, you're hostage to suppliers of titanium dioxide, resins, and solvents—unless you control the entire chain. Sherwin-Williams' ownership of raw material sources doesn't just cut costs; it ensures supply during shortages, enables proprietary formulations, and provides intelligence on competitor costs. When rivals struggle with allocation, Sherwin-Williams keeps painting.

Lesson 3: Premium Pricing Requires Relentless Value Creation Sherwin-Williams charges 30-40% more than private labels and customers gladly pay. Why? Because the premium buys reliability, consistency, service, and peace of mind. But maintaining that premium requires constant investment in quality, innovation, and relationships. The moment you take pricing power for granted is the moment you lose it.

Lesson 4: Consolidation is a Process, Not an Event From 1917 to today, Sherwin-Williams acquired over 70 companies. Not in dramatic roll-ups but methodically, digestibly, accretively. They never bet the company (except Valspar, and that was calculated). They never overpaid for synergies. They always integrated operations before the next deal. Consolidation is like painting—multiple thin coats beat one thick one.

Lesson 5: Survive the Downturns, Dominate the Recoveries Every recession created opportunity. The Depression spawned Kem-Tone. The 1970s crisis led to contractor focus. The 2008 collapse enabled cheap acquisitions. While competitors retreated, Sherwin-Williams invested. This requires balance sheet strength, operational flexibility, and most importantly, courage when others panic.

Lesson 6: Culture Scales, Strategy Doesn't The "Sherwin-Williams Way"—customer obsession, quality fixation, conservative finance—scaled from 10 stores to 4,100. But strategies changed completely: from wholesale to retail, from oil-based to water-based, from consumer to professional. Companies that confuse strategy with culture either can't adapt or can't scale. Sherwin-Williams did both by knowing the difference.

Lesson 7: Switching Costs Compound Every year a contractor uses Sherwin-Williams, switching gets harder. Color histories accumulate. Relationships deepen. Processes integrate. Training investments compound. What starts as convenience becomes dependency becomes impossibility. The best moats aren't built—they accrete, one satisfied customer at a time.

Lesson 8: Boring Businesses Allow Bold Moves Paint is boring. That's the point. Predictable demand enabled aggressive expansion. Steady cash flows funded innovation. Consistent margins supported debt for acquisitions. In sexy industries, competition is fierce and capital is scarce. In boring industries, disciplined operators can build empires while everyone watches Netflix.

Lesson 9: Technology Enhances Relationships, Doesn't Replace Them Sherwin-Williams embraced digital tools but never forgot paint is sold through relationships. Their app augments store visits, doesn't replace them. Color matching technology supports contractors, doesn't eliminate them. AI optimizes inventory but humans make sales. Technology that enhances human connection wins; technology that replaces it loses.

Lesson 10: Financial Conservatism Enables Strategic Aggression Sherwin-Williams never levered beyond 3x EBITDA until Valspar. They paid dividends for 47 consecutive years. They maintained investment-grade ratings through crises. This wasn't timidity—it was preparation. When opportunity knocked (Valspar), they could answer with $11 billion. Conservative balance sheets create optionality; leveraged ones create fragility.

The meta-lesson: compound improvement beats disruption. Sherwin-Williams never revolutionized paint. They made it slightly better, distributed it slightly better, serviced it slightly better—every year for 158 years. Those improvements compounded into dominance. In business, as in painting, patient layers beat bold strokes.

XIII. "What Would We Do?" Scenario

You've just been named CEO of Sherwin-Williams. The board meeting is tomorrow. Stock price is near all-time highs, but growth is slowing. Activists are circling. The strategy committee wants answers. What's the next chapter for a 158-year-old company? Here's the playbook we'd propose.

Move 1: Accelerate Asia-Pacific Industrial Expansion The biggest opportunity isn't in Cleveland—it's in Chennai, Chengdu, and Jakarta. Asia represents 60% of global manufacturing but only 15% of Sherwin-Williams' revenue. Don't replicate the U.S. store model; that failed in Europe. Instead, acquire local industrial coatings leaders, keeping their brands but upgrading their technology. Target: three $500 million acquisitions in India, Vietnam, and Indonesia within 18 months. Use Valspar's packaging relationships with Coca-Cola and Unilever as wedges into these markets. The region's manufacturing growth and environmental regulations create perfect conditions for premium industrial coatings.

Move 2: Build the Contractor Super App The current app is good; make it indispensable. Integrate project management, crew scheduling, customer billing, and tax reporting. Become the operating system for painting contractors. Offer fintech services: working capital loans against receivables, equipment financing, insurance products. Partner with Intuit to seamlessly connect to QuickBooks. The goal: make switching from Sherwin-Williams mean rebuilding their entire business infrastructure. Subscription revenue from software services could add $500 million in high-margin revenue within five years.

Move 3: Create the Sustainability Brand Premium Launch "Sherwin-Williams Zero"—a premium line of carbon-negative paints. Partner with carbon capture companies to embed CO2 in coatings. Price it 50% above standard lines for ESG-conscious commercial customers. Every tech company, university, and government building wants to showcase sustainability. Give them paint that actively removes carbon from the atmosphere. The marketing writes itself: "Cover the Earth, Save the Earth." This isn't greenwashing—it's green margin expansion.

Move 4: Vertical Integration 2.0—Control the Robots Painting labor is scarce and expensive. Robot painting is inevitable. Don't wait for someone else to automate your customers out of business. Acquire or partner with painting robotics companies. Develop Sherwin-Williams certified robotic systems that only work with your paints (proprietary viscosity requirements). Lease robots to contractors, creating recurring revenue and lock-in. When automation disrupts painting, own the disruption.

Move 5: Rethink Capital Allocation With $2.5 billion in annual free cash flow, be more aggressive. Implement a formulaic buyback: purchase shares whenever P/E drops below 20x. Dividend policy should target 30% payout ratio, reinvesting the rest. Most importantly, prepare for the next downturn with a $5 billion acquisition war chest. When recession hits and competitors struggle, buy the entire European architectural market in distress. Fortune favors the prepared balance sheet.

Move 6: The Data Play Sherwin-Williams knows more about American buildings' painting history than anyone. Monetize it. Launch a B2B data service for real estate investors, insurance companies, and property managers. Predictive analytics on maintenance needs, property condition insights, risk assessment for insurers. This data is already collected; packaging it for sale requires minimal investment but could generate $200 million in pure-margin revenue.

Move 7: Exit Low-Return Businesses Be ruthless about returns on capital. Any product line generating below 15% ROIC gets fixed or cut. Any geography below 10% margins gets restructured or exited. Any customer demanding unprofitable terms gets repriced or fired. Sacred cows make bad businesses. Free up capital and management attention for higher-return opportunities.

Move 8: The Acquisition Mega-Deal PPG Industries. $18 billion revenue, $22 billion market cap, struggling with activist investors. A merger creates the first $40 billion global coatings champion. The synergies are massive: procurement savings, facility consolidation, complementary technologies. Structure it as a merger of equals to avoid hostile dynamics. The regulatory fight would be epic, but the combination would be unstoppable. This is the deal that defines the next century.

The unifying theme: Sherwin-Williams spent 158 years perfecting North American architectural coatings. The next 158 years requires equal excellence in global industrial coatings, digital services, and sustainability. The core remains unchanged—superior products, unmatched distribution, customer obsession. But the expression evolves from paint company to coatings platform to industrial technology leader.

Wall Street wants growth. Deliver it through geographic expansion and adjacency exploitation. Activists want margins. Deliver them through technology and automation. Employees want purpose. Deliver it through sustainability leadership. Customers want value. Deliver it through innovation and service.

The best strategy for a 158-year-old company? Act like a 158-day-old startup with $90 billion in market cap and unlimited ambition. Because in business, as in painting, if you're not moving forward, you're drying up.

XIV. Recent News

The leadership transition marks a new era. Heidi G. Petz was elected to serve as Sherwin-Williams' CEO effective January 1, 2024, becoming only the tenth CEO in the company's 158-year history. Ms. Petz joined the Company in June 2017 in connection with the Valspar acquisition, bringing a fresh perspective from her previous roles at Target Corporation and Newell Rubbermaid.

Ms. Petz has served as Sherwin-Williams President and Chief Executive Officer since January 1, 2024, and in November 2024, the Board announced a leadership structure with Heidi serving as both CEO and Chair, which the Board believes is the most efficient and effective model for the Company. This consolidation of leadership roles signals confidence in Petz's vision and execution capabilities.

Under Petz's early tenure, the company has delivered strong results. Consolidated Net sales increased in the year to a record $23.10 billion, while maintaining operational excellence across all segments. As CEO Petz noted, "Sherwin-Williams delivered strong fourth quarter results despite continued demand choppiness in the majority of our end markets".

The Dow Jones inclusion represents perhaps the most significant recognition of Sherwin-Williams' transformation. On November 8, 2024, The Sherwin-Williams Co. (NYSE:SHW) replaced Dow Inc. (NYSE:DOW) in the Dow Jones Industrial Average. The index changes were initiated to ensure a more representative exposure to the materials sector, acknowledging Sherwin-Williams' dominance in the coatings industry.

Looking ahead, the company has provided confident guidance for 2025. Management expects adjusted diluted net income per share will be in the range of $11.65 to $12.05 per share, which represents 4.6% growth from 2024 at the mid-point. This guidance assumes continued margin expansion and modest market growth, demonstrating management's confidence in the business model's resilience.

The new Cleveland headquarters, despite construction delays, represents a bet on the future. The company expects the multi-phase move-in process to occur in 2025, creating a state-of-the-art facility that will house 4,000 employees and serve as a testament to the company's commitment to its hometown and its future.

XV. Links & Resources

Annual Reports & Investor Materials - Sherwin-Williams Investor Relations: investors.sherwin-williams.com - 2024 Annual Report & 10-K Filings - Quarterly Earnings Presentations - Valspar Acquisition Documents (2016-2017)

Historical & Archival Sources - "Sherwin-Williams: Cover the Earth" - Company History Archives - Cleveland Historical Society Paint Industry Collection - National Historic Chemical Landmark: Kem-Tone Documentation - Harvard Business School Case Studies on Sherwin-Williams

Industry Research - American Coatings Association Market Reports - Orr & Boss Consulting Paint & Coatings Analysis - IHS Markit Chemical Economics Handbook: Paints & Coatings - Grand View Research: Global Paints & Coatings Market

Books & Long-Form Articles - "The Colorful History of Paint" - Journal of Business History - "Vertical Integration in the Chemical Industry" - MIT Sloan Review - "The Consolidation of American Industry" - Economic History Review

Competitor Resources - PPG Industries Investor Relations - AkzoNobel Annual Reports - Asian Paints Financial Statements - Benjamin Moore Historical Archives (Berkshire Hathaway)

Podcast Episodes & Interviews - Masters in Business: John Morikis Interview (2019) - The Industrialist's Dilemma Podcast: Paint Industry Deep Dive - Cleveland Business Leaders Series: Sherwin-Williams Story

Regulatory & Technical Resources - EPA Regulations on VOCs and Paint Manufacturing - ASTM International Coating Standards - OSHA Guidelines for Paint Manufacturing & Application - Green Building Council LEED Paint Specifications

End of Episode

Total Runtime: 7 hours, 12 minutes

This is the Sherwin-Williams story—158 years of patient execution, strategic consolidation, and relentless focus on distribution and relationships. From Henry Sherwin's $2,000 investment to a $90+ billion market cap Dow component, it's a masterclass in building and sustaining competitive advantage in a seemingly commoditized industry.

The company that literally covers the earth has proven that in business, as in painting, success comes not from revolutionary breakthroughs but from applying coat after coat of incremental improvement, year after year, decade after decade, until the competition can no longer see through your lead.

For investors, Sherwin-Williams represents a fascinating paradox: a 158-year-old company still growing, a commodity product with pricing power, a cyclical business with consistent returns. Whether you see it as a compounding machine or an overvalued cyclical depends on your timeframe and your faith in the durability of their moat.

But one thing is certain: the next time you see that iconic logo of paint covering the earth, you'll understand it's not just marketing hyperbole—it's a mission statement that a Cleveland paint shop has been methodically executing for over a century and a half. And they're not done yet.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube