Shopify: Arming the Rebels

I. Introduction and The Thesis

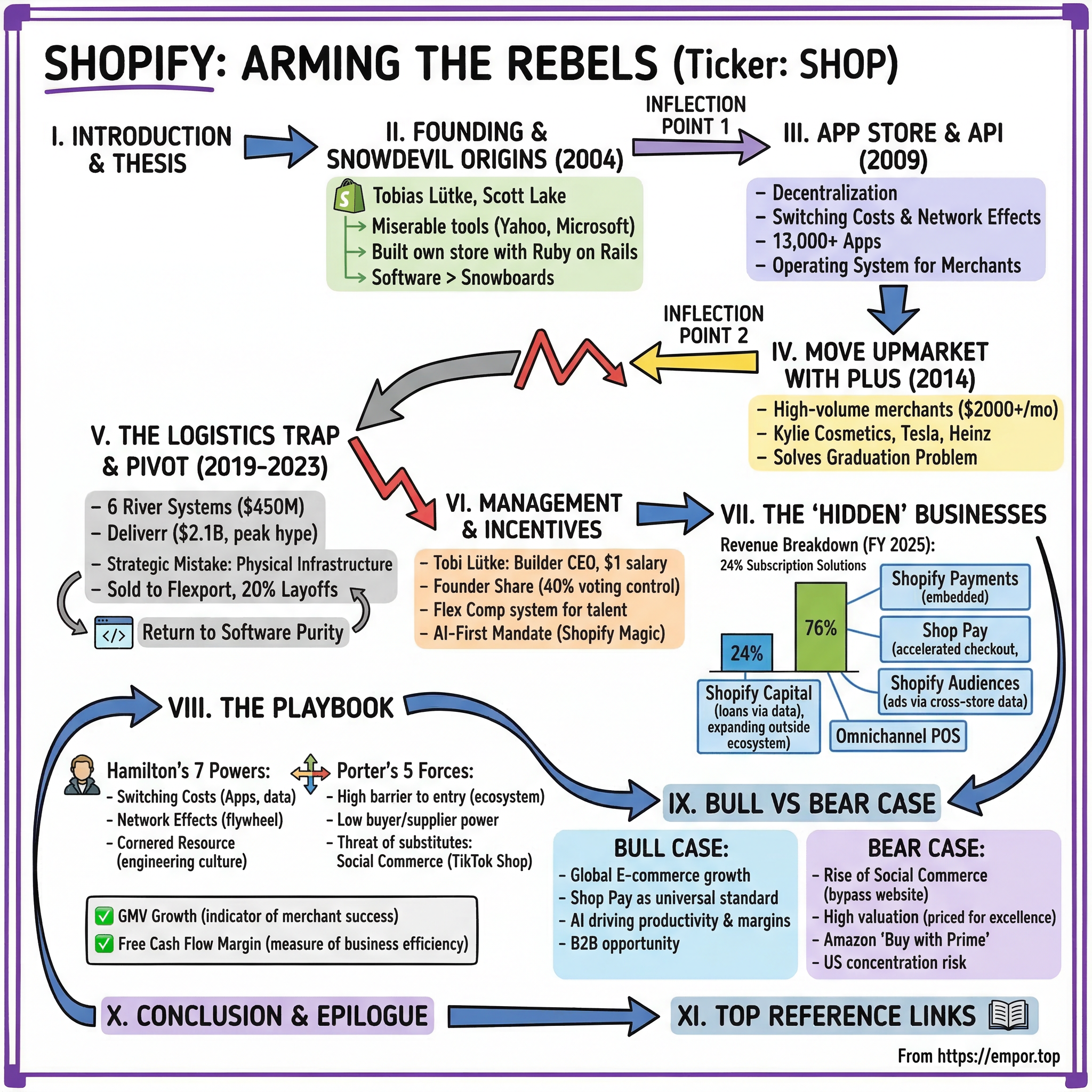

In the summer of 2004, a twenty-three-year-old German programmer named Tobias Lütke sat in his apartment in Ottawa, Canada, staring at a screen full of broken code. He was not trying to build the future of commerce. He was trying to sell snowboards. Lütke and his friend Scott Lake had launched an online snowboard shop called Snowdevil, and the experience of trying to get a simple store online using the tools available at the time—Yahoo Stores, Microsoft Commerce Server, osCommerce—was so miserable, so infuriating, that Lütke decided to do what any self-respecting programmer would do: he built his own.

Twenty-two years later, that side project processes more than ten percent of all U.S. e-commerce. Shopify powers millions of merchants across 175 countries, and in fiscal year 2025, it generated $11.6 billion in revenue—a figure that would have seemed absurd to anyone watching the company's quiet IPO in May 2015, when revenue barely crossed $200 million. As of mid-March 2026, Shopify commands a market capitalization of roughly $160 billion, making it one of the most valuable technology companies in the world.

But here is the thesis that makes Shopify genuinely interesting, not just as a stock, but as a strategic case study. Shopify is not a "store builder." It is the decentralization of retail. In a world where Amazon has become the Everything Store—a gravitational force that pulls merchants, logistics, and customer relationships into its orbit—Shopify represents the only credible counter-force. It arms the rebels. It gives independent merchants the tools to compete without surrendering their brand, their data, or their customer relationships to a marketplace overlord.

The story of how it got here involves a Ruby on Rails side project that became a platform, a platform that became an ecosystem, an ecosystem that nearly destroyed itself by trying to become a logistics company, and a dramatic pivot back to being what it always should have been: a lean, high-margin software business that functions as a Merchant Operating System. This is the story of strategic clarity won through expensive mistakes, and of a founder who pays himself one dollar a year but controls forty percent of the voting power. Buckle up.

II. Founding and The "Snowdevil" Origins

The year was 2004, and the internet was in its awkward adolescence. Google had just gone public. Facebook was a dorm room experiment. And if you wanted to sell something online, your options ranged from terrible to catastrophic. Yahoo Stores charged merchants for the privilege of looking like every other Yahoo Store. Microsoft Commerce Server was enterprise software priced for enterprises, not for two guys who wanted to move snowboards. The open-source alternatives were functional in the same way a Soviet apartment block was functional—they worked, technically, but nobody wanted to live there.

Tobias Lütke had arrived in Canada from Koblenz, Germany, largely because he had fallen in love with a Canadian woman he met online. Born in 1981, Lütke was a self-taught programmer who had dropped out of school and completed a computer science apprenticeship in Germany. He was not a business school graduate with a startup playbook. He was a craftsman—someone who thought about code the way a cabinetmaker thinks about joints. Clean. Precise. Elegant.

Scott Lake was the business mind. Together, they launched Snowdevil, an online store for snowboards. The snowboards were fine. The software was the problem. After weeks of wrestling with existing e-commerce platforms, Lütke made a decision that would change everything: he would build the storefront himself, using a brand-new web framework called Ruby on Rails that had been released by Danish programmer David Heinemeier Hansson just months earlier.

This is one of those details that seems minor but is actually foundational. Ruby on Rails was not just a programming language; it was a philosophy. Rails emphasized convention over configuration, clean code, and rapid iteration. It was the anti-enterprise framework—designed to let small teams build powerful applications quickly, without the bureaucratic overhead of Java or .NET. Lütke did not just use Rails; he became one of its earliest and most influential contributors. He wrote code for the Rails core. He spoke at Rails conferences. He lived and breathed the philosophy that software should be simple, beautiful, and fast to ship.

That philosophy became Shopify's DNA. When people ask why Shopify can ship features faster than competitors ten times its size, the answer traces back to a twenty-three-year-old in Ottawa who believed that clean code was not a luxury but a competitive advantage. The culture of "craftsmanship"—of hiring people who care deeply about the elegance of their work—starts here, in a snowboard shop that nobody remembers.

The "aha moment" came when Lütke and Lake realized something that sounds obvious in retrospect but was genuinely counterintuitive at the time: the software they had built to sell snowboards was more valuable than the snowboards themselves. Other merchants started asking if they could use the platform. By 2006, Snowdevil had quietly evolved into Shopify, initially called Jaded Pixel Technologies. The company officially rebranded to Shopify Inc. in November 2011, but the mission was clear much earlier: give every merchant on the internet the tools that only big companies could afford.

The early years were lean. Shopify was bootstrapped, then took modest venture capital. It was not a Silicon Valley rocket ship burning through cash. It was a Canadian company, built by immigrants, growing methodically. By 2010, Shopify had roughly 15,000 merchants. By 2012, the platform had processed over $740 million in gross merchandise volume. The numbers were growing, but Shopify was still a small player in a market dominated by Magento, BigCommerce, and the enterprise behemoths like Hybris and Demandware.

What separated Shopify was not its features—it was its simplicity. A merchant could sign up, choose a theme, add products, and be selling online within hours. No developer required. No enterprise sales call. No six-month implementation. This was the democratization of e-commerce, and it was about to get a rocket booster.

III. Inflection Point 1: The App Store and API

In 2009, Shopify made a decision that would define its trajectory for the next two decades. Most SaaS companies, when they reach a certain scale, do the obvious thing: they build more features. They add inventory management. They add email marketing. They add shipping calculators. They try to become the everything-tool, the Swiss Army knife of their category. Shopify did the opposite. It opened an API and launched an App Store.

This was not an obvious move. Opening your platform means giving up control. It means other developers can build things that might be buggy, or ugly, or that might compete with your own features. It means trusting that the ecosystem will create more value than you lose in curation. For a small company with limited resources, it was a bold bet.

The logic was elegant, and it came from Lütke's engineering instincts. Shopify could never build every feature that every merchant needed. A jewelry store in Brooklyn has different needs than a supplement company in Austin, which has different needs than a fashion brand in London. Instead of trying to be everything to everyone, Shopify would be the foundation—the operating system—and let thousands of developers build the specialized tools on top.

The App Store turned competitors into partners. A company that might have built a competing e-commerce platform instead built a Shopify app. An email marketing startup that could have tried to displace Shopify's basic tools instead built a deeper integration. The app ecosystem became a moat—not because of any single app, but because of the cumulative weight of integration. Think about it this way: a merchant who has connected their store to fifteen different apps—their email tool, their accounting software, their loyalty program, their shipping optimizer, their review platform—has built a web of dependencies that makes switching to a competitor genuinely painful. This is not a lock-in strategy in the cynical sense. It is a natural consequence of building a platform that works so well that an ecosystem grows around it.

In the language of Hamilton Helmer's "7 Powers" framework, this is a textbook example of switching costs reinforced by network effects. The more merchants on Shopify, the more developers build apps. The more apps available, the more attractive the platform becomes to new merchants. The more merchants, the more data Shopify has to improve its tools. It is a flywheel, and by the early 2010s, it was spinning fast.

By 2013, the Shopify App Store had hundreds of apps. By 2015, it had thousands. Today, the ecosystem includes over 13,000 apps built by independent developers, many of whom have built multi-million-dollar businesses on top of Shopify's platform. This is a crucial detail that often gets lost in the financial analysis: Shopify's platform has created an entire economy of developers, designers, and agencies whose livelihoods depend on the platform's success. These are not employees. They are not on Shopify's payroll. But they are, in every meaningful sense, part of the Shopify machine—and they evangelize the platform with the fervor of true believers because their businesses depend on it.

The App Store also solved a critical business problem: it allowed Shopify to remain simple for beginners while being infinitely customizable for advanced users. A first-time merchant could launch a store with zero apps and have a clean, easy experience. A sophisticated brand could layer on dozens of tools to create a custom tech stack rivaling anything an enterprise platform could offer. This "simple at the surface, deep underneath" architecture became Shopify's defining product philosophy.

The strategic brilliance of the platform move becomes clear when you look at what happened to the competition. Magento, which was the dominant open-source e-commerce platform in the late 2000s, tried to be everything itself. It became bloated, complex, and expensive to maintain. Adobe eventually acquired it in 2018 for $1.68 billion, but by then, the developer community had already begun migrating to Shopify's ecosystem. BigCommerce, Shopify's most direct competitor, has a capable platform but never achieved the same ecosystem density. The app ecosystem was not just a feature—it was the feature that made all other features possible.

IV. Inflection Point 2: The Move Upmarket with Shopify Plus

There is a problem that every successful bottoms-up software company eventually faces, and it goes like this: you build a product for small customers. The small customers love it. Some of those small customers grow into big customers. And then the big customers leave—because your product was never built for their scale, their complexity, their demands.

Shopify hit this wall hard in the early 2010s. The platform was beloved by independent merchants—the Etsy sellers, the side-hustle entrepreneurs, the direct-to-consumer brands just getting started. But when those brands got big, they graduated. They moved to Magento Enterprise, to Hybris, to Demandware—platforms built for companies processing millions of dollars in transactions and needing custom checkout flows, dedicated support, and guaranteed uptime during traffic surges.

This was not just a revenue problem. It was a narrative problem. If Shopify could only serve small merchants, it would forever be seen as a "starter" platform—training wheels for companies that would eventually outgrow it. The ceiling on the business would be low, and the best growth stories would always be merchants who left.

In 2014, Shopify launched Shopify Plus, its enterprise-tier offering. The product was designed to serve high-volume merchants with dedicated support, customizable checkout, automation tools, and the ability to handle massive traffic spikes. The pricing started at $2,000 per month—a far cry from the $29/month basic plan—but still dramatically cheaper than the enterprise alternatives, which often ran into six or seven figures annually when you factored in implementation costs, hosting, and ongoing maintenance.

The timing was perfect. The direct-to-consumer revolution was just beginning. Brands like Allbirds, Gymshark, and MVMT Watches were proving that you did not need a retail store or a wholesale distribution deal to build a major consumer brand. You needed a great product, a strong social media presence, and a commerce platform that could handle the spikes when a viral moment hit.

No story captures this better than the Kylie Cosmetics launch. In November 2015, Kylie Jenner launched her Lip Kit line exclusively through a Shopify-powered store. The product sold out in under a minute. The traffic was staggering—the kind of sudden, concentrated burst that crashes most websites and would challenge even Amazon's infrastructure. Shopify Plus handled it. The store stayed up. The orders processed. And the beauty industry took notice.

Kylie Cosmetics became Shopify's most famous case study, but it was far from the only one. Tesla used Shopify for its merchandise store. Red Bull, Heinz, Staples Canada, Fashion Nova—the list of enterprise brands that chose Shopify Plus over traditional enterprise platforms grew rapidly. Each one validated the thesis that you did not need to sacrifice simplicity for scale.

What made Plus work was not just the technology—it was the go-to-market strategy. Shopify did not try to build a traditional enterprise sales organization with long sales cycles, RFPs, and proof-of-concept engagements. Instead, it built a lean Plus sales team that could close deals quickly, often in weeks rather than months. The pitch was simple: you can be live on Shopify Plus faster and cheaper than any alternative, and you will never worry about your site going down during a flash sale.

By 2019, Shopify Plus was contributing a meaningful share of subscription revenue and had become the fastest-growing segment of the business. More importantly, it changed the perception of Shopify. The company was no longer "just for small merchants." It was a platform that could serve the entire spectrum—from a first-time seller to a billion-dollar brand. This versatility became one of Shopify's most powerful advantages, because merchants who started small and grew large never had to leave. The graduation problem was solved.

The financial impact was significant. Shopify's revenue doubled from roughly $1.07 billion in 2018 to $1.58 billion in 2019, and Plus was a major driver. But more importantly, Plus merchants had higher average revenue per user, lower churn, and deeper platform engagement. They used more apps, processed more payments through Shopify Payments, and became anchors for the ecosystem. For investors, Plus transformed Shopify from a high-volume, low-ARPU business into something with genuine pricing power.

V. M&A, Capital Deployment, and the "Logistics Trap"

Every great company has a chapter it would rather forget. For Shopify, that chapter is called logistics.

The setup was seductive. By 2019, Shopify had built a dominant software platform for merchants. But merchants did not just need software—they needed to ship products. And the shipping experience for small and medium merchants was, to put it bluntly, terrible. They were at the mercy of expensive carriers, slow delivery times, and a fulfillment process that was complex, manual, and error-prone. Meanwhile, Amazon was setting the standard with Prime—free two-day shipping that had become the baseline consumer expectation.

Shopify looked at this problem and saw an opportunity. If it could build a fulfillment network—a distributed web of warehouses, technology, and logistics infrastructure—it could offer its merchants Amazon-level shipping without Amazon's marketplace. Merchants could stay independent, keep their brand, own their customer relationships, and still deliver packages in two days. It was the ultimate "arm the rebels" move: give the rebel army its own supply chain.

The vision was grand. The execution was expensive.

In September 2019, Shopify acquired 6 River Systems for $450 million. 6 River Systems built collaborative warehouse robots—autonomous mobile units that guided workers through fulfillment centers, optimizing pick paths and increasing productivity. The idea was to bring automation and efficiency to Shopify's emerging fulfillment network.

Then, in 2022, came the blockbuster deal. Shopify acquired Deliverr, a fulfillment and logistics startup, for approximately $2.1 billion. The timing could not have been worse. The deal closed at the peak of the "instant delivery" hype—a period when the market was irrationally exuberant about anything related to fast shipping, last-mile delivery, and logistics technology. By traditional third-party logistics valuations, Shopify paid a massive premium. Deliverr was a technology-enabled 3PL, not a software company, and its unit economics were far from proven at scale.

The combined logistics operation—branded as the Shopify Fulfillment Network—was Shopify's attempt to build a physical version of Amazon Prime. The company was investing hundreds of millions in warehouse capacity, robotics, and operational infrastructure. It was hiring logistics specialists, warehouse managers, and supply chain engineers. For a company that had built its identity around clean code and elegant software, it was a jarring transformation. Shopify was becoming, in part, a trucking company.

The financial toll was visible in the numbers. In fiscal year 2022, Shopify reported a net loss of $3.46 billion—driven in part by acquisition-related charges and impairments, but also reflecting the operational burden of building physical infrastructure. Operating cash flow turned negative for the first time, coming in at negative $136 million. Free cash flow was negative $186 million. The company that had been a capital-light software business was suddenly capital-intensive, and the margins reflected it.

But the real cost was not financial—it was strategic. The logistics ambition distracted management attention from the core software platform. It created organizational complexity. It forced the company to compete in a domain—physical logistics—where it had no structural advantage. Amazon had spent twenty years and tens of billions of dollars building its fulfillment network. The idea that Shopify could replicate even a fraction of that capability in a few years was, with hindsight, unrealistic.

In May 2023, Tobi Lütke made the hardest decision of his career. Shopify sold the bulk of its logistics operations to Flexport, the freight forwarding startup led by Ryan Petersen. The deal included the Deliverr assets and the fulfillment network infrastructure. Shopify took a minority equity stake in Flexport as part of the transaction, maintaining a partnership without the operational burden. Simultaneously, Shopify laid off roughly twenty percent of its workforce—approximately 2,300 employees—in what Lütke candidly described as a necessary correction.

In a memo to employees, Lütke was remarkably transparent. He acknowledged that the bet on logistics had not worked as planned and that the company needed to return to its core identity as a software company. He wrote that Shopify was "not a logistics company" and that the attempt to become one had been a mistake in strategic direction, even if the underlying instinct—to help merchants ship faster—was correct.

Was the Deliverr deal a "productive failure"? In a sense, yes. The logistics detour forced a strategic clarity that might never have emerged otherwise. By trying to become everything—software platform, payment processor, and logistics operator—Shopify learned where its competitive advantages truly lay. The painful pivot back to software set up the "Year of Efficiency" that would define 2023 and beyond. The company cut costs, focused on high-margin software and payments, and began generating free cash flow at a remarkable rate. Free cash flow swung from negative $186 million in 2022 to positive $905 million in 2023, then $1.6 billion in 2024, and $2.0 billion in 2025. The Flexport divestiture did not just save money—it saved the company's soul.

VI. Current Management and Incentive Structures

To understand Shopify, you have to understand Tobi Lütke. Not just his biography—his temperament. Lütke is not a typical CEO. He does not do keynote speeches with the polish of a Satya Nadella or the showmanship of a Marc Benioff. He is a programmer who happens to run a $160 billion company. He pays himself a salary of one dollar. He spends his time writing code, reviewing product decisions, and thinking about the long-term architecture of the platform. He is, in the deepest sense, a builder—and he has structured the entire company around the idea that builders should be in charge.

In June 2022, Shopify shareholders approved a new dual-class share structure that gave Lütke a "Founder Share"—a special class of stock that guarantees him approximately forty percent of the total voting power for as long as he remains actively involved with the company. This is an extraordinary governance arrangement. It means that despite significant dilution over the years—Shopify has roughly 1.3 billion shares outstanding—Lütke maintains effective control over major corporate decisions. He cannot be ousted by activist investors. He cannot be pressured into short-term moves by quarterly earnings misses. He has, in essence, the same structural protection that Mark Zuckerberg has at Meta or the Google founders have at Alphabet.

The Founder Share is controversial in corporate governance circles. Critics argue it insulates management from accountability. Supporters argue it allows long-term thinking in a market obsessed with quarterly results. For Shopify specifically, the case for founder control was strengthened by the logistics pivot. The decision to sell the fulfillment network and refocus on software was exactly the kind of painful, long-term strategic move that a publicly traded company with dispersed ownership might never make—because the short-term headline would be ugly. Lütke made the call because he could.

Harley Finkelstein, Shopify's President, born in 1983, plays a complementary role. If Lütke is the engine room, Finkelstein is the bridge. A trained lawyer who started as a Shopify merchant himself—he sold T-shirts online while in law school—Finkelstein joined the company in 2010 and has risen through roles including Chief Platform Officer before becoming President. He is the public face of Shopify: the one who gives the conference talks, meets with enterprise clients, and evangelizes the "arm the rebels" narrative. His compensation of roughly $930,000 in base pay reflects the structure of a company where equity, not cash, is the primary incentive.

Jeff Hoffmeister serves as CFO, bringing a background in investment banking and corporate finance. Jessica Hertz, the Chief Operating Officer, joined in 2022 and has been instrumental in the operational restructuring following the logistics divestiture. The leadership team is lean by the standards of a company generating nearly $12 billion in annual revenue—Shopify has approximately 8,100 full-time employees, giving it revenue per employee of over $1.4 million, a figure that rivals the most efficient software companies in the world.

One of the most interesting management innovations at Shopify is the "Flex Comp" system, introduced in 2022. Under Flex Comp, employees can choose their own mix of cash and equity compensation. Want more cash stability? Dial up the cash. Believe in the stock? Take more equity. This seemingly simple idea was radical in the context of a tech industry where compensation packages were standardized and often optimized for tax efficiency rather than employee preference. Flex Comp was designed to attract and retain talent during the brutal tech downturn of 2022-2023, when layoffs were widespread and employees were anxious about the value of their equity.

Lütke has also been vocal about organizational philosophy. He has pushed the concept of "Crafters vs. Managers"—the idea that Shopify should be led by people who make things, not people who manage people who make things. In practice, this means flatter hierarchies, fewer meetings, and a cultural emphasis on shipping product. In early 2023, Shopify famously deleted over 12,000 recurring meetings from employee calendars, a move that was part stunt and part genuine organizational reset. The company also introduced "Chaos Monkey" for meetings—randomly canceling recurring meetings to force teams to justify whether they were actually necessary.

More recently, Lütke made headlines in early 2025 with a company-wide memo stating that before any team at Shopify can request additional headcount, they must first demonstrate why AI cannot do the job. This directive signaled that Shopify views artificial intelligence not as a bolt-on feature but as a fundamental restructuring of how work gets done. The company has integrated AI across its platform—from Shopify Magic, which helps merchants write product descriptions and marketing copy, to Sidekick, an AI assistant for store management. For investors, the key takeaway is that Shopify's management team is aggressively leveraging AI to drive productivity, which helps explain how the company grew revenue by thirty percent in 2025 while keeping headcount essentially flat.

VII. The "Hidden" Businesses: Beyond the Subscription

There is a common misunderstanding about Shopify that goes something like this: "Shopify makes money by charging merchants $29 to $399 per month for an online store." This is true in the same way that saying "Apple makes money by selling phones" is true—it captures one piece of the picture while missing the larger and more interesting story underneath.

Shopify's revenue breaks into two segments. Subscription Solutions—the monthly fees merchants pay for access to the platform—generated $2.75 billion in fiscal year 2025, representing about twenty-four percent of total revenue. The remaining seventy-six percent, or $8.8 billion, came from what Shopify calls Merchant Solutions. This segment includes everything from payment processing and lending to shipping and advertising tools. In other words, the subscription is the anchor—the recurring, high-margin foundation—but the real growth engine is the suite of services that sit on top.

The crown jewel of Merchant Solutions is Shopify Payments, the company's integrated payment processing system. When a merchant uses Shopify Payments, Shopify takes a percentage of every transaction—typically around 2.9% plus 30 cents for online credit card payments, with lower rates for in-person transactions. This is the same model as Stripe or Square, but with a crucial difference: Shopify Payments is embedded directly into the platform. There is no integration to set up, no separate account to create. It just works. And because it just works, adoption is remarkably high. The vast majority of Shopify merchants use Shopify Payments, generating a massive and growing stream of transaction revenue that scales directly with merchant GMV.

Shop Pay, Shopify's accelerated checkout solution, deserves special attention. Shop Pay stores a customer's shipping and payment information, enabling one-click purchases that dramatically reduce cart abandonment. This is not a small thing—cart abandonment rates in e-commerce typically exceed sixty percent, and every point of friction in the checkout process costs merchants real money. Shop Pay has processed hundreds of billions of dollars in cumulative GMV and has become one of the most recognized checkout buttons on the internet.

What makes Shop Pay strategically fascinating is that Shopify has begun extending it beyond the Shopify ecosystem. Through the "Buy with Shop Pay" initiative, merchants who do not even use Shopify as their platform can offer Shop Pay as a checkout option. This is a direct play to become a universal checkout standard—a payments network that transcends the platform itself. If Shop Pay achieves that kind of ubiquity, it transforms Shopify from a commerce platform into a payment network, with all the scale economics and network effects that implies.

Shopify Capital is another hidden giant. Launched in 2016, Shopify Capital provides cash advances and loans to merchants based on their sales history. Because Shopify has real-time visibility into every merchant's revenue, it can underwrite loans with extraordinary precision—far better than a traditional bank looking at quarterly financial statements. The loans are repaid automatically as a percentage of daily sales, which means repayment rates are high and default rates are low. Shopify does not disclose the exact size of its lending portfolio, but it has extended billions of dollars in cumulative capital to merchants since inception.

Then there is Shopify Audiences, the company's quiet entry into advertising technology. In a post-iOS 14 world—where Apple's privacy changes decimated the ability of platforms like Facebook and Google to target ads effectively—merchants have been desperate for new ways to find customers. Shopify Audiences uses aggregated, anonymized data from its merchant network to help individual merchants identify high-intent buyers. Because Shopify sees purchase behavior across millions of stores, it has a data asset that no individual merchant, and few ad platforms, can match. Early results suggest that Audiences significantly improves ad performance for participating merchants, and it represents a potentially massive revenue opportunity as it scales.

On the physical retail side, Shopify's Point of Sale hardware and software has been growing rapidly. The POS system integrates directly with the online store, unifying inventory, customer data, and sales reporting across channels. This omnichannel capability puts Shopify in direct competition with Square and Toast in the physical retail and restaurant space—markets with enormous total addressable size.

The geographic breakdown tells its own story. The United States accounts for roughly sixty-one percent of revenue, with EMEA contributing about eighteen percent, Asia-Pacific about ten percent, and Canada roughly five percent. Latin America, at just over one percent, represents the earliest stage of what could be a significant growth vector. Shopify's international expansion—particularly in Europe and Asia—is still in relatively early innings, and the company has been investing in localized payment methods, multi-currency support, and cross-border commerce tools to accelerate adoption.

For investors parsing the revenue mix, the key insight is this: Shopify's subscription business provides high-margin, predictable recurring revenue that covers the company's fixed costs. The Merchant Solutions business provides high-growth, variable revenue that scales with merchant success. This dual structure means that as merchants grow—processing more payments, shipping more orders, borrowing more capital—Shopify grows with them without needing to sell them anything new. It is the software equivalent of a tollbooth on a highway that gets busier every year.

VIII. The Playbook: Hamilton's 7 Powers and Porter's 5 Forces

The question every serious investor asks about a high-multiple technology company is: "Why can't someone just build this?" For Shopify, the answer requires a framework, and the best ones come from Hamilton Helmer and Michael Porter.

Start with Helmer's 7 Powers. The primary power Shopify possesses is switching costs—and the depth of these switching costs is genuinely underappreciated. When a merchant sets up a Shopify store, they are not just uploading products and picking a theme. They are configuring tax settings for every jurisdiction where they sell. They are building SEO equity in their URL structure. They are integrating with fifteen or twenty different apps—their email marketing tool, their inventory management system, their loyalty program, their reviews platform, their accounting software. They are training their team on the Shopify admin. They are building workflows and automations. The cumulative cost of ripping all of that out and rebuilding it on a competitor's platform is enormous—not just in dollars, but in time, disruption, and risk. This is why Shopify's merchant churn rate, particularly among Plus merchants, is remarkably low.

The second power is network effects, driven by the ecosystem. More merchants attract more app developers. More app developers create better tools. Better tools attract more merchants. More merchants generate more data for Shopify Audiences. More data improves ad performance. Better ad performance attracts more merchants. This is a multi-layered flywheel that compounds over time and creates a structural advantage that is nearly impossible for a new entrant to replicate from scratch.

The third power—and this is the most debatable one—is what Helmer calls a "cornered resource." In Shopify's case, the cornered resource is Tobi Lütke himself and the engineering culture he has built. The Rails-first, craft-driven development philosophy creates a velocity of product shipping that larger, more bureaucratic competitors cannot match. Adobe Commerce (formerly Magento) has far more resources. Salesforce Commerce Cloud has a massive sales force. But neither can iterate on product with the speed and taste that Shopify demonstrates quarter after quarter. Culture is hard to copy, and Shopify's culture is deeply rooted in its founder's personality.

Now apply Porter's Five Forces. The threat of new entrants is low, because building a full e-commerce ecosystem—platform, payments, apps, developer community, enterprise support—takes years and billions of dollars. Squarespace and Wix offer website builders with commerce features, but they lack the depth of Shopify's merchant tools and the richness of its app ecosystem. Amazon is not a new entrant but an entirely different business model. The barrier to building a credible Shopify competitor is not the software itself—it is the ecosystem surrounding it.

The bargaining power of buyers, meaning merchants, is low. Shopify's merchants are extraordinarily fragmented—millions of individual businesses, none of which represents a meaningful share of Shopify's revenue. No single merchant has leverage to negotiate pricing. And because the switching costs are high, merchants are not in a position to credibly threaten to leave. This gives Shopify pricing power, which it has exercised judiciously—raising Plus pricing, for example, with minimal churn impact.

The bargaining power of suppliers is also low. Shopify has built its own payments infrastructure, reducing dependence on third-party payment processors. Its cloud infrastructure runs on Google Cloud, but the relationship is one of mutual dependence—Google benefits enormously from having Shopify as a customer. The app developers in the ecosystem are not suppliers in the traditional sense; they are complementors who depend on Shopify far more than Shopify depends on any individual developer.

The threat of substitutes is the most interesting force to analyze. The traditional substitute—building a custom e-commerce site from scratch using Magento or a similar open-source platform—has become less attractive over time as Shopify's capabilities have expanded. But the non-traditional substitute is more concerning: social commerce. Platforms like TikTok Shop and Instagram Shopping allow merchants to sell directly within the social media environment, potentially bypassing the need for a standalone store entirely. This is the single biggest strategic risk to Shopify's long-term thesis, and it deserves serious consideration.

Rivalry among existing competitors is moderate. BigCommerce is the most direct competitor but operates at a fraction of Shopify's scale. Salesforce Commerce Cloud and Adobe Commerce serve the enterprise market but are expensive and slow to implement. WooCommerce, the WordPress plugin, has significant market share by count but primarily serves very small merchants with limited needs. None of these competitors has the combination of simplicity, ecosystem depth, and merchant solutions breadth that Shopify offers.

The two KPIs that matter most for tracking Shopify's ongoing performance are Gross Merchandise Volume (GMV) growth and free cash flow margin. GMV growth tells you whether the merchants on the platform are thriving—whether they are selling more products, reaching more customers, and growing their businesses. Because Shopify's Merchant Solutions revenue scales directly with GMV through payment processing fees, shipping fees, and capital advances, GMV growth is the leading indicator of revenue growth. Free cash flow margin tells you whether Shopify is translating that revenue growth into actual cash generation, which is the ultimate measure of whether the business model is working. In 2025, free cash flow reached $2.0 billion on $11.6 billion of revenue, representing a free cash flow margin of roughly seventeen percent—a remarkable number for a company still growing revenue at thirty percent annually.

IX. Bear vs. Bull Case

The Bull Case

The bull case for Shopify starts with a simple observation about the size of the addressable market. Global e-commerce is a multi-trillion-dollar market that continues to take share from physical retail. Within that market, Shopify's ten-percent-plus share of U.S. e-commerce represents significant scale but still leaves enormous room for growth—particularly internationally, where adoption is earlier-stage. If Shopify can replicate even a fraction of its U.S. success in Europe, Asia, and Latin America, the revenue opportunity is measured in multiples of the current base.

Shop Pay is the bull case's secret weapon. If Shop Pay achieves widespread adoption as a universal checkout standard—used not just on Shopify stores but across the internet—it becomes a payment network with network effects that compound independently of the commerce platform. Think about what PayPal was supposed to become but never quite did: a ubiquitous, trusted, one-click checkout that consumers reach for instinctively. Shop Pay, with its existing scale and Shopify's distribution advantage, has a credible path to that vision.

The AI opportunity amplifies the bull case. Shopify's early and aggressive adoption of AI—both internally, to drive productivity, and externally, through tools like Shopify Magic and Sidekick—positions it to be the platform where AI-native commerce is built. If AI transforms how merchants create products, write marketing copy, manage inventory, and interact with customers, the platform that best integrates these capabilities gains a massive competitive advantage. Lütke's mandate that teams must justify headcount requests against AI capabilities suggests that Shopify is not treating AI as a feature but as a fundamental restructuring of the business.

The margin expansion story is also compelling. After the logistics divestiture, Shopify's cost structure has become dramatically leaner. Operating income went from negative $1.4 billion in 2023 to positive $1.07 billion in 2024 to positive $1.47 billion in 2025. Free cash flow margins are expanding as revenue grows while headcount remains flat. If this operating leverage continues—and there is reason to believe AI-driven productivity will sustain it—Shopify could generate free cash flow margins of twenty percent or more at scale, which would put it in the rarified air of the world's most profitable software companies.

The B2B commerce opportunity adds another layer. Shopify has been quietly building tools for wholesale and B2B transactions, a market that is dramatically larger than consumer e-commerce but far less digitized. If Shopify can bring its consumer-grade simplicity to B2B commerce, the addressable market expands significantly.

The Bear Case

The bear case centers on a single existential question: what happens if the standalone online store becomes less important?

The rise of social commerce—TikTok Shop, Instagram Shopping, YouTube Shopping—represents a fundamental challenge to Shopify's thesis. If consumers increasingly discover and purchase products within social media platforms, they may never visit a merchant's website at all. The entire concept of "arming the rebels" assumes that rebels need their own storefront. But what if the battle moves to the marketplace of attention, where TikTok and Instagram are the landlords?

Shopify has responded by integrating with social platforms—merchants can sell on TikTok, Instagram, and Facebook directly through the Shopify admin. But this integration makes Shopify a backend tool rather than the center of the merchant's commerce experience. If social platforms continue to build their own native commerce features, the value of Shopify's frontend—the storefront, the checkout, the brand experience—could erode.

Valuation is the other bear concern. At a market cap of roughly $160 billion and an enterprise value-to-sales ratio of approximately eighteen times trailing revenue, Shopify is priced for sustained excellence. The stock trades at a significant premium to software peers and a massive premium to payment companies. This valuation leaves little room for execution missteps or deceleration in revenue growth. If growth slows from thirty percent to fifteen or twenty percent—still an impressive rate by any standard—the multiple compression could be severe.

There is also the competitive risk from Amazon itself. Amazon has been building its "Buy with Prime" offering, which allows merchants on their own websites to offer Prime shipping and checkout. This is a direct assault on Shopify's territory—it says to merchants, "Keep your own store, but use Amazon's fulfillment and trust badge." If Buy with Prime gains traction, it could commoditize the very merchant-solutions revenue that drives Shopify's growth.

Finally, the concentration risk in the U.S. market deserves attention. With sixty-one percent of revenue coming from the United States, Shopify's fortunes are heavily tied to the U.S. consumer economy. A significant slowdown in U.S. consumer spending—or regulatory changes that affect e-commerce—would disproportionately impact Shopify relative to more geographically diversified competitors.

X. Conclusion and Epilogue

In the final accounting, Shopify's story is one of the most remarkable in modern technology. A snowboard shop that could not find decent software became the software that powers millions of merchants. A side project built on a new programming framework became a $160 billion company that processes over ten percent of all U.S. e-commerce. Along the way, there were brilliant strategic decisions—the App Store, the move upmarket with Plus—and expensive mistakes—the logistics detour that cost billions before being unwound.

What makes the Shopify story resonate beyond the financials is the thesis at its core. In a world where Amazon offers the path of least resistance for merchants—"list your product on our marketplace, use our fulfillment, and we will find you customers"—Shopify offers something harder but more valuable: independence. The right to own your customer relationship. The right to build your brand. The right to control your data. The right to not be one of ten million listings on a marketplace where the only way to compete is on price.

Tobi Lütke has spoken about building a "100-year company," and the structural decisions he has made—the Founder Share, the return to software purity, the AI-first mandate—suggest he means it. Whether Shopify achieves that longevity depends on questions that cannot be answered today: Will the standalone online store remain the center of digital commerce? Will social platforms subsume the shopping experience? Will AI create new distribution channels that render current platforms obsolete?

What can be said is that Shopify has built something rare: a platform with genuine network effects, high switching costs, and a culture of product excellence that has survived rapid growth, strategic missteps, and the relentless pressure of public markets. It emerged from a snowboard shop in Ottawa, survived a $2.1 billion logistics mistake, and came out the other side leaner, more focused, and generating $2 billion a year in free cash flow.

The Rebel Alliance has its operating system. The question for the next decade is whether the rebels can hold the line.

XI. Top 5 Reference Links

-

Tobi Lütke's Early Blog Posts and Ruby on Rails Contributions — The primary source material for understanding Shopify's engineering philosophy and the cultural DNA that still drives product development speed.

-

Shopify's 2015 IPO Prospectus (SEC Filing, May 2015) — The original "Arming the Rebels" manifesto and the clearest articulation of the company's mission, filed with the SEC ahead of its NASDAQ listing.

-

Shopify's Flexport/Logistics Divestiture Press Release (May 2023) — The most important strategic pivot in a decade, documenting the sale of logistics operations to Flexport and the accompanying workforce reduction.

-

Shopify's 2023 Shareholder Letter and "Year of Efficiency" Communications — Management's candid assessment of the logistics mistake, the AI-first mandate, and the operational restructuring that restored the company's financial profile.

-

Stratechery: "Shopify and the Power of Platforms" by Ben Thompson — The definitive external analysis of Shopify's platform strategy, ecosystem dynamics, and competitive positioning within the broader commerce landscape.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube