Somnigroup International: The Empire of Sleep

I. Introduction & Episode Thesis

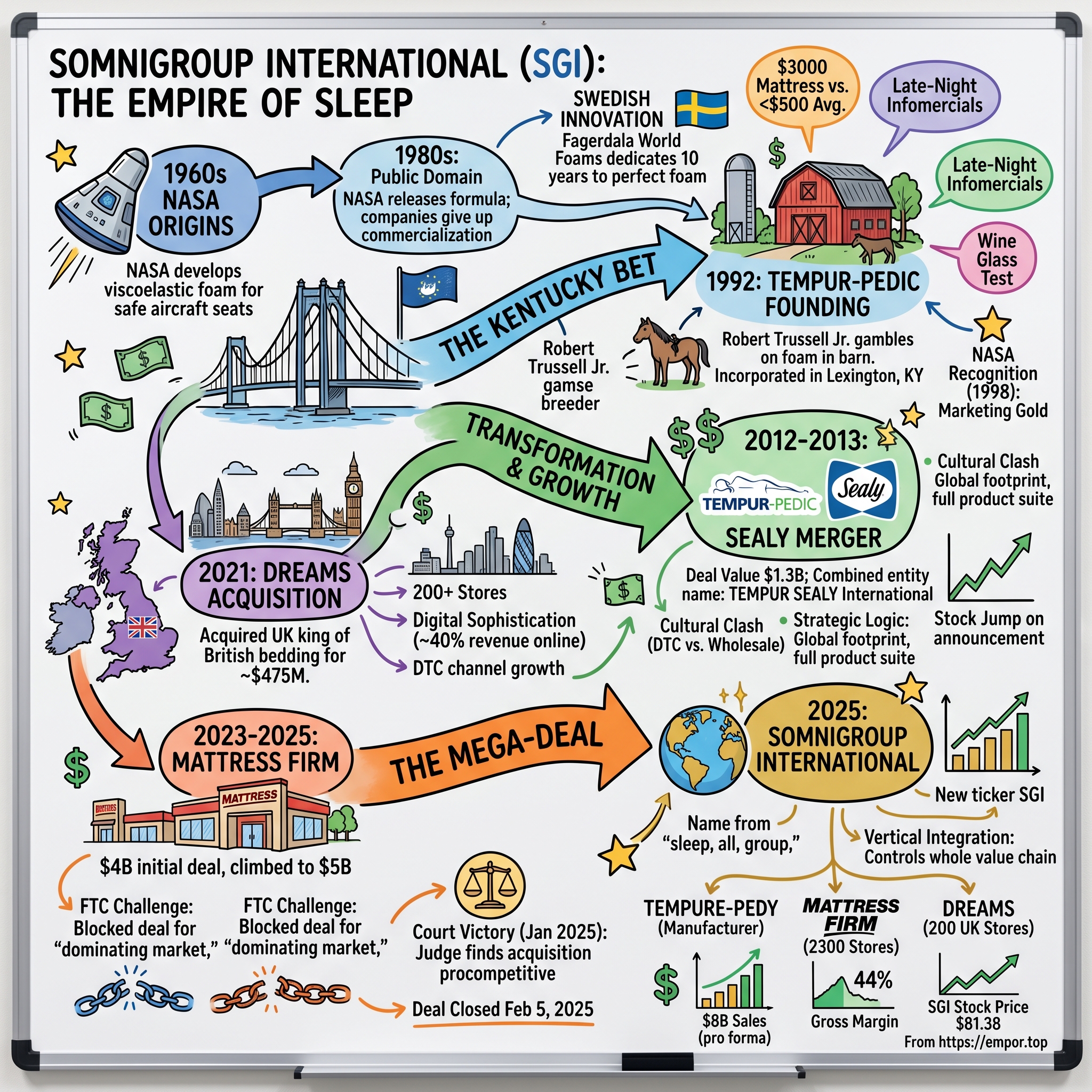

Picture this: It's 2 AM in Houston, and inside a sprawling warehouse-turned-laboratory, a team of engineers is meticulously measuring the pressure points of a sleeping test subject. Sensors track every toss, turn, and micro-adjustment. The year is 1992, and these researchers aren't working for NASA anymore—they're trying to sell Americans on sleeping on space-age foam that costs more than most people's monthly car payments.

Fast forward to February 2025. That scrappy startup, once hawking Swedish memory foam through late-night infomercials, has just completed its transformation into Somnigroup International—an $8 billion behemoth that controls nearly half of America's specialty bedding market through 2,800+ retail locations worldwide. The journey from NASA labs to Wall Street darling isn't just a story of product innovation; it's a masterclass in strategic consolidation, vertical integration, and the art of building an empire one acquisition at a time. Today, the stock trades at $81.38, up 0.62% in the past 24 hours, with a market capitalization of $17.08 billion. The central question we'll explore: How did a company founded on repurposed NASA technology become the undisputed king of sleep, commanding premium valuations through relentless acquisition and vertical integration?

The answer lies not in a single brilliant strategy, but in a three-decade playbook of patient brand-building, opportunistic M&A, and the audacious vision to control every step of the sleep journey—from foam formulation to the moment a customer lies down in a retail showroom. This is the story of how Tempur-Pedic became Tempur Sealy, then morphed into Somnigroup—each transformation marking a new chapter in the consolidation of a $15 billion industry that everyone needs but few think about until their back starts hurting.

II. The NASA Origins & Tempur-Pedic Founding

The story begins not in a boardroom but in a barn in Lexington, Kentucky, where Robert Trussell Jr.—a thoroughbred horse breeder with zero experience in mattresses—was about to gamble his future on Swedish foam. It was 1991, and through the kind of serendipitous connection that only exists in the small world of international horse racing, Trussell had just spent the night on a mattress that would change his life.

The connection was almost absurd in its randomness: Trussell's French horse trainer friend knew a Swedish horse chiropractor, who knew another Swede involved in both racing and mattresses. That Swede worked for Fagerdala World Foams, a Swedish company that had spent a decade perfecting a material NASA had abandoned to the public domain in the early 1980s.

The material's origin traced back to the late 1960s, when NASA scientists were tasked with developing a cushioning system for aircraft seats to improve survivability in crashes. In 1966, NASA's Ames Research Center contracted Stencel Aero Engineering Corporation to develop this safer seating system, resulting in a viscoelastic foam material. But when NASA released the formula into the public domain in the early 1980s, most companies gave up trying to commercialize it—the material proved more temperamental than temperature-sensitive.

Enter the Swedes. Fagerdala World Foams, through its subsidiary Dan Foam A/S, refused to give up, dedicating ten full years to perfecting the material for consumer use, particularly mattresses. By 1991, they had cracked the code, creating what they branded as TEMPUR—a material they could produce in various shapes, sizes, and densities. When Fagerdala introduced the Tempur-Pedic Swedish Mattress in Sweden in 1991, they sold 50,000 units within three years to a population of just eight million.

In the early 1990s, Fagerdala awarded North American distribution rights to Robert Trussell, who created Tempur-Pedic, Inc. The company was formally incorporated in 1992 in Lexington, Kentucky. This Kentucky horse breeder was about to introduce America to the concept of spending $3,000 on a mattress—at a time when the average American spent less than $500.

The early years were brutal. Traditional mattress retailers wouldn't touch the product—it was too expensive, too weird, and required too much explanation. Customers would lie down on a Tempur-Pedic and panic because it didn't bounce back like a traditional spring mattress. The foam initially felt firm, then slowly conformed to body heat and weight, creating an unsettling sensation for first-timers.

Trussell's solution was quintessentially American: bypass the retailers entirely. He pioneered what would become the famous "wine glass test"—placing a glass of red wine on one side of the mattress while someone moved on the other side, demonstrating superior motion isolation compared to traditional innerspring mattresses. This visual became the centerpiece of late-night infomercials that would define the brand for a generation.

The direct-to-consumer strategy was born of necessity but proved prescient. While competitors fought for shelf space at Mattress Discounters and Sleepy's, Tempur-Pedic built a database of customers willing to pay premium prices for better sleep. They offered 60-day trials (revolutionary at the time), white-glove delivery, and most importantly, education about why NASA-developed foam was worth ten times the price of a traditional mattress.

By the late 1990s, the strategy was working. The company went through several ownership changes, with nine Fagerdala distributors including Tempur-Pedic merging in 1999 to form Tempur World Holding Company, which was reformed in 2002 as Tempur-Pedic International Inc. The company went public in 2003.

At a joint press conference on May 6, 1998, at NASA headquarters in Washington, D.C., NASA recognized TEMPUR's outstanding achievements in adapting the original NASA technology for everyday use and improving quality of life—the only mattress company to receive such recognition. This NASA seal of approval became marketing gold, lending scientific credibility to what many still saw as an overpriced novelty.

The secret sauce, literally, remained closely guarded. The TEMPUR formula has always remained secret—fewer than 10 people in the world know how to make it, and they all work for the company. This proprietary knowledge created a moat that no amount of Chinese knock-offs could cross. While competitors could make memory foam, they couldn't make TEMPUR.

By the mid-2000s, Tempur-Pedic had educated an entire market. Memory foam went from space-age oddity to must-have luxury. The company's success spawned hundreds of imitators, from cheap imports to venture-backed startups. But Tempur-Pedic had something none of them possessed: a decade-long head start in understanding not just how to make the product, but how to sell sleep itself. The stage was set for the next chapter—one that would transform a premium niche player into an industry consolidator.

III. The Sealy Merger: Creating a Bedding Giant (2012–2013)

The boardroom at Sealy's Trinity, North Carolina headquarters had seen better days. It was September 2012, and CEO Larry Rogers was staring at a brutal reality: the 131-year-old company that had once defined American sleep was hemorrhaging market share to a Swedish foam upstart that didn't exist when Rogers started his career. Sealy's stock was trading at $2.20, down from its $30 peak just five years earlier. Private equity owner KKR was ready to cut their losses.

Across the country in Lexington, Kentucky, Tempur-Pedic CEO Mark Sarvary was dealing with his own crisis. After years of explosive growth, his company had just shocked Wall Street in June 2012 by slashing full-year forecasts, citing intensifying competition from Simmons and Serta. Tempur-Pedic's market value had been cut in half to $1.5 billion. The memory foam revolution that Tempur-Pedic had started was now being co-opted by every competitor with a foam supplier and a marketing budget.

Sarvary called it "a transformational deal that brings together two great companies, each with globally recognized brands." But transformation was a polite word for what was really happening: two wounded giants were merging to survive a mattress war that was claiming casualties on all sides.

The deal structure reflected the power dynamics perfectly. Tempur-Pedic acquired all of the outstanding common stock of Sealy for $2.20 per share and assumed or repaid all of Sealy's outstanding convertible and non-convertible debt, for a total transaction value of approximately $1.3 billion. For context, Sealy had roots dating back to 1881 and had sales of $1.3 billion in fiscal 2012—they were being acquired for essentially one times revenue by a company founded just 20 years earlier.

The strategic logic was compelling, at least on paper. The combined entity would have products for almost every consumer preference and price point, distribution through all key channels, in-house expertise on most key bedding technologies, and a world-class R&D team, with a global footprint spanning over 80 countries.

Together, they would control the strongest brand portfolio in the industry, including Tempur, Tempur-Pedic, Sealy, Sealy Posturepedic, Optimum and Stearns & Foster, with the most comprehensive suite of bedding products available in the market.

But merging these companies was like trying to combine oil and water. Tempur-Pedic had built its entire identity around rejecting the traditional mattress industry—no springs, no flipping, no negotiating on price. Sealy was the embodiment of that traditional industry, with a dealer network that had been selling Posturepedic mattresses the same way for decades.

The cultural clash was immediate. Tempur-Pedic's direct-to-consumer DNA collided with Sealy's wholesale heritage. Tempur stores competed directly with Sealy dealers, sometimes on the same block. The sales forces didn't just dislike each other—they had been trained for years to view the other's product as inferior.

The Federal Trade Commission cleared the acquisition on March 8, 2013, and the company closed the deal on March 18, 2013. The speed of regulatory approval surprised many observers who expected antitrust challenges given the combined market share.

The integration strategy was deliberately cautious. The two companies would continue to operate independently, with Sealy CEO Larry Rogers remaining in his position and reporting to Tempur-Pedic CEO Mark Sarvary. This wasn't just diplomatic—it was essential. Any hint of Tempur-Pedic dismantling the Sealy dealer network would have triggered a revolt.

To recognize the transformational nature of the combination, the company changed its name to Tempur Sealy International, Inc., seeking stockholder approval at its Annual Meeting in May 2013. The new name was more than symbolic—it was a signal to Sealy's retailers that their brand wouldn't be subsumed by the foam upstart.

The financing revealed the high-stakes nature of the gamble. The company funded the transaction and refinancing of its existing credit facility with $1.770 billion in senior secured facilities and $375 million of senior notes. Tempur-Pedic was leveraging itself to the hilt, betting that the combined entity could generate enough cash flow to service the debt while funding integration costs.

What made the merger work, ultimately, wasn't the brand portfolio or global reach—it was the realization that Tempur-Pedic and Sealy weren't really competitors. They were selling to different customers through different channels at different price points. Tempur-Pedic brought innovation and premium pricing power; Sealy brought scale and distribution. Together, they could defend against the real threats: online disruptors and Asian imports.

The market's initial reaction was euphoric—Tempur-Pedic shares skyrocketed in morning trading, up more than 15% at one point—but the real test would come in execution. Could two companies with fundamentally different philosophies about how to make and sell mattresses actually create value together? The answer would take years to unfold, but one thing was clear: the mattress industry would never be the same. The consolidation era had begun.

IV. International Expansion: The Dreams Acquisition (2021)

Mike Logue was standing in the flagship Dreams store on Tottenham Court Road in London, watching customers test mattresses in May 2021, when his phone rang. It was Scott Thompson, the new CEO of Tempur Sealy who had taken over from Mark Sarvary just six years earlier. Thompson's message was simple: "We want to buy you, and we're serious."

Dreams wasn't just any UK mattress retailer. With over 200 stores stretching from Edinburgh to Portsmouth, it was the undisputed king of British bedding, selling 10,000 mattresses, bases, and headboards per week. But what made Dreams truly special wasn't its store count—it was its digital sophistication. In a market where most competitors were still figuring out e-commerce, Dreams had built an industry-leading online channel that generated nearly 40% of its revenue.

The timing was exquisite. Sun Capital Partners, the private equity firm that had owned Dreams since 2013, was eager to exit after successfully navigating the company through COVID-19. Dreams had developed a successful multi-channel sales strategy, with over 200 brick and mortar retail locations, an industry-leading online channel, as well as manufacturing and delivery assets. Dreams generated sales of approximately $400 million and EBITDA of approximately $75 million for the year ending December 31, 2020.

For Thompson, Dreams represented something more strategic than just another acquisition. The transaction would accelerate Tempur Sealy's growth in the largest European bedding market and sixth largest economy in the world. After years of watching European competitors chip away at Tempur's premium position, this was a chance to plant the flag decisively.

The transaction price was approximately $475 million, less net debt and any working capital deficit, and the transaction was expected to be accretive to Tempur Sealy's EPS by approximately $0.20 before synergies in the first year post-acquisition. For a company trading at over 20 times earnings, this level of immediate accretion was remarkable.

Thompson had learned from the Sealy integration that forcing cultural change was a recipe for disaster. Dreams would be operated as an independent business unit and led by the current management team. Mike Logue would stay on as CEO, reporting to Thompson but maintaining operational autonomy.

Thompson commented, "Dreams has created a strong retailer brand and business model, known for its outstanding products and customer service. We have worked with Dreams for many years and they are one of the most talented retailers we service. They have consistently demonstrated best-in-class web marketing, customer service and sales capabilities."

The strategic fit was elegant. It was expected to complement the Company's existing UK Tempur operations and its recently-formed Sealy UK joint venture operations. Instead of competing for the same customers, Tempur could focus on the premium segment through specialty retailers while Dreams captured the mass market through its own channels.

The numbers told a compelling story. After the transaction closed, Tempur Sealy's annualized worldwide direct-to-consumer business was expected to reach $1 billion in sales and its international segment would represent over 20% of consolidated sales. This wasn't just geographic expansion—it was a fundamental shift in the business model toward higher-margin direct sales.

The financing structure revealed Thompson's confidence. The transaction would be financed through a combination of cash on hand and bank borrowings. The Company's pro forma leverage was expected to be slightly less than 2 times adjusted EBITDA as defined in the Company's credit agreement. Finally, the Company entered into an amendment of its Senior Credit Facility which increased its liquidity by $300 million.

The transaction signed on May 26, 2021, and closed on August 2, 2021, following receipt of regulatory approval from the UK Financial Conduct Authority. The speed of execution—just over two months from signing to closing—demonstrated how comfortable regulators had become with Tempur Sealy's acquisition strategy.

What made Dreams particularly valuable was its omnichannel excellence. While American mattress retailers were still fighting the "showrooming" phenomenon—customers testing in stores then buying online from competitors—Dreams had solved it. Their stores functioned as experience centers that drove online sales, with seamless inventory management and white-glove delivery across channels.

With 2,000 employees across the UK, Dreams sold over 10,000 mattresses, bases, and headboards per week to customers nationwide through its network of over 200 stores and online. This scale gave Tempur Sealy instant market leadership in the UK, a position that would have taken decades to build organically.

No job cuts or store closures were announced and Dreams' management team would stay in place, led by Mike Logue who was appointed in 2013. This preservation of human capital was crucial—Dreams' success came from deep local market knowledge that couldn't be replicated from Lexington, Kentucky.

The Dreams acquisition marked a turning point in Tempur Sealy's evolution. No longer content to be primarily a North American player selling through third parties, the company was building a global, vertically integrated empire. The UK beachhead would prove invaluable when the next opportunity arose—and that opportunity was already taking shape in Houston, where a certain mattress retailer was drowning in debt and desperate for a savior.

V. The Mattress Firm Mega-Deal: Vertical Integration Play (2023–2025)

The call came at 3 AM Houston time on a Tuesday in May 2023. John Eck, CEO of Mattress Firm, was used to crisis calls—he'd navigated the company through bankruptcy in 2018, COVID in 2020, and supply chain chaos in 2021. But this wasn't a crisis call. It was Scott Thompson from Tempur Sealy, and his message was simple: "We're ready to make an offer you can't refuse."

Mattress Firm wasn't just any retailer—it was the undisputed king of American mattress sales, operating about 2,300 stores in all 50 U.S. states. For years, industry insiders had called it the "kingmaker" because of its ability to turn nascent brands into significant competitors through its unparalleled consumer reach and sales expertise. But behind the scenes, parent company Steinhoff International was desperate to exit after years of legal and financial troubles stemming from an accounting scandal in South Africa.

The deal announced on May 9, 2023, valued Mattress Firm at $4 billion, though the final price would ultimately climb higher. For Thompson, this wasn't just another acquisition—it was the culmination of a strategy years in the making. Post-transaction, Tempur Sealy would transform from being primarily a manufacturer to primarily a retailer, with approximately 65 percent of its revenue generated from retail operations.

The strategic logic was elegant but controversial. By acquiring Mattress Firm, Tempur Sealy would control both the factory and the store, the brand and the salesperson, the wholesale price and the retail margin. It was vertical integration on a scale the mattress industry had never seen.

But on July 2, 2024, the Federal Trade Commission voted unanimously—5-0—to block the acquisition. "Through emails, presentations, and other deal documents, Tempur Sealy has made it abundantly clear that its acquisition of Mattress Firm is intended to kneecap competitors and dominate the market," said Henry Liu, Director of the FTC's Bureau of Competition.

The FTC's case was built on internal documents that seemed damning. Multiple deal documents showed that Tempur Sealy planned to limit rivals' access to Mattress Firm's nationwide network of stores to harm competition. The agency argued that Mattress Firm was the nation's largest mattress retailer and considered one of the most important retail channels for mattresses, and by acquiring it, Tempur Sealy would wield significant power over rival suppliers like Serta Simmons Bedding and Purple Innovation.

Thompson's response was swift and aggressive. Rather than negotiate with the FTC, Tempur Sealy went on the offensive. The company filed a lawsuit in federal court for the Southern District of Texas, arguing that a federal court, not an FTC administrative proceeding, was the proper venue to decide the case.

The legal maneuvering revealed the high stakes. In its court filing, Tempur Sealy noted that the FTC's administrative proceeding starts before an FTC administrative law judge "and ends with the same five Commissioners who voted to challenge the merger"—noting that the agency had won every administrative proceeding for the last 25 years.

The trial began on November 12, 2024, in Houston—Mattress Firm's backyard—and the location proved fortuitous. The court proceedings revealed crucial weaknesses in the FTC's case. A cornerstone of the FTC's case was testimony from Serta Simmons that the transaction was an "existential threat," but on cross examination, those claims contradicted statements Serta Simmons had made to a bankruptcy court predicting sales growth at Mattress Firm after the deal. The court concluded that Serta Simmons' testimony "came with no credibility whatsoever".

On January 31, 2025—the final day of FTC Chair Lina Khan's tenure—U.S. District Judge Charles Eskridge delivered a devastating blow to the agency. The judge rejected the FTC's claim that the deal would hurt consumers, finding instead that the acquisition was "either neutral or procompetitive" and "in the public interest".

The court's analysis was methodical in dismantling the FTC's arguments. Mattress Firm's retail sales accounted for only 25% of all premium mattress sales overall and only 8.8% of premium mattress sales made by Tempur Sealy's competitors. Competing manufacturers had ample alternative distribution channels including thousands of other retailers, department stores, furniture stores, and online platforms.

The FTC declined to seek an injunction pending appeal, indicating it would not seek emergency relief from the Fifth Circuit and would not prevent the transaction from closing. The white flag had been raised.

Tempur Sealy closed the $5 billion acquisition on February 5, 2025, funded by about $2.7 billion in cash on hand plus proceeds from existing borrowings and 34.2 million shares of common stock. The final price tag of $5 billion represented approximately $1 billion more than initially announced—a 25% premium that reflected both the strategic value and the legal costs of fighting the FTC.

The structure of the combined entity revealed Thompson's vision. Under the Somnigroup umbrella, Mattress Firm and Dreams would continue to operate as multibranded retailers, while Tempur Sealy would continue to manufacture bedding for third-party retailers as well as its own channels. This wasn't about destroying competition—it was about controlling the entire value chain.

Thompson acknowledged the integration challenges ahead. "There are some stores that need to be refreshed, and we've allocated capital to freshen up the stores, to make sure we provide customers and employees a fresh, clean and crisp environment. It'll be data-driven".

The Mattress Firm acquisition represented more than just vertical integration—it was a bet on the future of retail itself. In an era when online disruptors were supposedly killing brick-and-mortar, Tempur Sealy was doubling down on physical stores. The gamble was that mattresses—products consumers wanted to touch, feel, and lie on before buying—would remain immune to pure e-commerce disruption.

With the deal closed, Tempur Sealy controlled the most extensive mattress retail network in America, coupled with the most recognized brands and manufacturing capabilities. The transformation from memory foam startup to retail empire was nearly complete. Only one piece remained: a new name to reflect the company's evolution from manufacturer to omnichannel giant.

VI. The Rebrand: From Tempur Sealy to Somnigroup

The boardroom at Tempur Sealy's Lexington headquarters was buzzing with an energy that Scott Thompson hadn't felt since his first day as CEO in 2015. It was February 5, 2025, just hours after closing the Mattress Firm deal, and Thompson was about to unveil something that had been in development for months: a complete corporate rebrand.

"Ladies and gentlemen," Thompson began, addressing his executive team and board members, "Tempur Sealy International is dead. Long live Somnigroup."

The name wasn't chosen lightly. The name Somnigroup is derived from the Latin words "somn," meaning sleep, "omni," meaning all, and "group" to reflect the company's position as a global provider of sleep solutions with an integrated omni-channel strategy. It was more than semantic cleverness—it was a declaration of intent.

Thompson had been planning this moment since the Dreams acquisition in 2021. The Tempur Sealy name, while iconic, represented a marriage of two legacy brands that no longer captured the breadth of what the company had become. With Mattress Firm and Dreams now in the fold, they weren't just a manufacturer that happened to own some stores—they were a global sleep conglomerate that happened to manufacture mattresses.

The company announced it would change its name to Somnigroup International Inc., effective February 18, 2025, with shares of Somnigroup common stock trading on the New York Stock Exchange under ticker symbol "SGI". The ticker change from TPX to SGI was deliberate—moving from a symbol tied to Tempur-Pedic's past to one that represented Somnigroup's future.

The organizational structure revealed Thompson's vision for decentralized excellence. Mattress Firm, Dreams and Tempur Sealy would operate as decentralized business units under Somnigroup. Mattress Firm and Dreams would continue to operate as multi-branded retailers while Tempur Sealy, primarily a manufacturer, would continue to serve third-party retailers as well as Mattress Firm, Dreams and direct-to-consumer channels.

This wasn't corporate window-dressing. The decentralized model addressed the fundamental challenge of the mega-merger: how to capture synergies without destroying what made each business successful. Mattress Firm's 2,300 stores knew their local markets intimately. Dreams understood British consumers in ways that no American executive could replicate. Tempur Sealy's manufacturing excellence didn't need retail meddling.

Thompson declared, "Somnigroup is the world's largest bedding company, with superior capabilities in design, manufacturing, distribution and retail while owning a portfolio of the most highly recognized brands in the industry. Somnigroup has a portfolio of outstanding businesses – Tempur Sealy, Dreams and Mattress Firm. Our portfolio includes the most highly recognized brands in the industry, including Tempur-Pedic, Sealy and Stearns & Foster".

The financial implications were staggering. On a pro forma basis for the acquisition of Mattress Firm, the company generated approximately $8 billion in sales over the previous 12 months ending December 31, 2024, net of intercompany sales. This wasn't just scale—it was market dominance across every segment of the sleep industry.

The rebrand also signaled a shift in strategic thinking. The old Tempur Sealy was product-centric, focused on manufacturing excellence and brand management. Somnigroup was customer-centric, focused on meeting consumers wherever and however they wanted to shop. The name itself—with its "omni" reference—made this pivot explicit.

Thompson had learned from studying other industry consolidations. When VF Corporation acquired Timberland and North Face, they kept the brands distinct while leveraging back-office synergies. When AB InBev rolled up the beer industry, they maintained local brand identities while globalizing operations. Somnigroup would follow a similar playbook.

The holding company structure provided strategic flexibility. Each business unit could pursue its own growth strategy while benefiting from shared resources in areas like technology, logistics, and procurement. Mattress Firm could focus on retail innovation, Dreams on European expansion, and Tempur Sealy on product development and manufacturing efficiency.

Critics questioned whether the rebrand was necessary. After all, Tempur Sealy had spent decades building brand equity. But Thompson understood something fundamental: in an era of rapid industry transformation, clinging to legacy identities was a luxury they couldn't afford. The mattress industry of 2025 looked nothing like the industry of 2015, let alone 1992.

The rebrand also served an important internal function. Employees at Mattress Firm and Dreams needed to feel they were joining something new, not being absorbed by a competitor. The Somnigroup identity created neutral ground—a fresh start that belonged equally to all three business units.

Thompson emphasized the long-term vision: "We are committed to providing breakthrough sleep solutions that meet the diverse sleep needs of consumers all over the world, while delivering long-term growth for our shareholders. We look forward to continuing to improve people's lives through better sleep for the next 100 years and beyond".

Wall Street's reaction was mixed but largely positive. Some analysts worried about integration complexity and the debt load. Others saw the strategic logic of vertical integration in an industry facing disruption from online players and Asian imports. The stock would ultimately tell the story, but early trading suggested investors were believers.

On February 18, 2025, shares of Somnigroup common stock began trading on the New York Stock Exchange under the ticker symbol "SGI". The opening bell that morning wasn't just ceremonial—it marked the birth of a new kind of bedding company, one that controlled every step of the sleep journey from foam formulation to final sale.

The transformation from Tempur-Pedic to Tempur Sealy to Somnigroup represented more than corporate evolution—it was a masterclass in strategic adaptation. Each iteration reflected the company's expanding ambitions and capabilities. Somnigroup wasn't the end of this journey; it was the platform for whatever came next.

VII. Business Model & Competitive Advantages

Inside Somnigroup's sprawling research facility in Lexington, engineers are testing a new adaptive foam that responds to body temperature changes throughout the night. Down the hall, data scientists are analyzing millions of sleep patterns collected from smart beds. Meanwhile, 2,000 miles away in a Mattress Firm store in Seattle, a sales associate is using an AI-powered app to recommend the perfect mattress based on a customer's sleep position, weight distribution, and temperature preferences.

This convergence of manufacturing excellence, technological innovation, and retail dominance defines Somnigroup's business model—a vertically integrated fortress that competitors can barely dent, let alone breach.

The numbers tell a story of exceptional operational excellence. Gross margin reached 44.0% in Q2 2025, with adjusted gross margin at 44.2%—remarkable for what many consider a commodity business. Thompson noted that their 2024 results reflected "record sales and gross margins while the industry is experiencing trough volumes"—achieving peak profitability during an industry downturn.

The secret lies in Somnigroup's unique ability to capture value at every step of the sleep journey. When a customer walks into a Mattress Firm store, Somnigroup controls the real estate, the salesperson, the product selection, the financing options, and ultimately, the manufacturing of the mattress itself. This isn't just vertical integration—it's value chain domination.

Consider the manufacturing footprint: 71 manufacturing facilities worldwide, supported by four R&D facilities. This isn't just about scale—it's about strategic positioning. Plants are located near major population centers to minimize shipping costs and delivery times. The company can produce everything from $299 value mattresses to $8,000 adjustable smart beds, all optimized for their specific market segments.

The proprietary TEMPUR material remains the crown jewel. While competitors can make memory foam, they can't replicate TEMPUR's specific formulation—a secret known to fewer than 10 people worldwide. This creates pricing power that extends beyond the premium segment, as the TEMPUR brand acts as a halo for the entire portfolio.

The omnichannel strategy represents another crucial advantage. With over 2,800 retail locations worldwide, Somnigroup operates the largest specialty bedding retail network globally. But this isn't just about store count—it's about strategic coverage. In Q2 2025, Mattress Firm alone contributed $948.8 million in sales, demonstrating the power of controlling distribution.

The financial architecture reveals sophisticated capital allocation. Leverage based on the ratio of consolidated indebtedness less netted cash to adjusted EBITDA was 2.31 times for the year ended December 31, 2024—conservative for a company of this scale and cash generation capability. The Board increased the quarterly cash dividend by 15% to $0.15 per share, marking the fifth increase in recent years, payable on March 20, 2025.

The portfolio strategy creates multiple moats. At the premium end, Tempur-Pedic commands prices that can exceed $5,000 for a queen mattress. In the middle market, Sealy Posturepedic leverages 140 years of brand equity. Stearns & Foster occupies the luxury segment. Private label and OEM products capture price-conscious consumers. This isn't just market segmentation—it's market encirclement.

R&D investments have yielded breakthrough innovations. The company's smart beds can track sleep patterns, adjust firmness automatically, and even detect potential health issues. The TEMPUR-breeze technology addresses the number one complaint about memory foam—heat retention—with phase-change materials that actively cool sleepers. These aren't gimmicks; they're solutions to real consumer pain points that command premium pricing.

The decentralized operating model preserves entrepreneurial energy while capturing scale benefits. Mattress Firm's operating margin was 6.7% for Q2 2025, with adjusted operating margin at 7.8%—impressive for retail. Meanwhile, North America manufacturing operating margin was 20.4%, with adjusted operating margin improving 430 basis points to 22.7%, driven by gross margin improvement.

Supply chain advantages compound these strengths. When foam prices spike, Somnigroup's scale allows better negotiations with suppliers. When shipping costs surge, their distributed manufacturing network minimizes impact. When a competitor faces production issues, Somnigroup can rapidly capture market share through their retail network.

The data advantage is perhaps most underappreciated. With millions of customer interactions annually across retail, online, and call centers, Somnigroup possesses unparalleled insights into sleep preferences, purchasing patterns, and price sensitivity. This data feeds product development, marketing strategies, and retail optimization in a virtuous cycle that strengthens with each transaction.

Looking ahead, management's guidance suggests confidence in the model's durability. For 2025, they expect adjusted EBITDA of approximately $1.3 billion to $1.4 billion, with capital expenditures of approximately $250 million including $50 million to refresh Mattress Firm stores.

The international expansion opportunity remains vast. Tempur Sealy International net sales increased 15.0% to $293.6 million in Q2 2025, or 10.0% on a constant currency basis, driven by new product launches. With Dreams providing a European platform and manufacturing capabilities in key markets, Somnigroup can replicate its North American playbook globally.

The business model's resilience shows in its ability to thrive during industry downturns. While pure-play manufacturers struggle with excess capacity and retailers face traffic declines, Somnigroup optimizes across the entire value chain. They can adjust manufacturing to match retail demand, shift product mix to maximize margins, and use their retail footprint to gain share from weakened competitors.

This isn't just a mattress company anymore. It's a sleep solutions platform with tentacles reaching into every aspect of how consumers research, purchase, finance, and experience sleep products. The competitive advantages aren't just sustainable—they're compounding.

VIII. Financial Performance & Market Position

The numbers cascading across Scott Thompson's monitor on the morning of August 7, 2025, told a story of transformation. Q2 2025 net sales had surged 52.5% to $1.88 billion, with the stock hitting all-time highs despite what everyone acknowledged was an industry downturn. Raymond James had just raised their price target to $85, maintaining their Strong Buy rating—the highest on the Street.

SGI reported Q2 2025 net sales of $1.88 billion, up 52.5% YoY, with net income of $99.0 million. EPS was $0.47, down from $0.60 in Q2 2024. The EPS dilution reflected the massive share issuance for the Mattress Firm acquisition, but adjusted EPS of $0.53 beat consensus estimates of $0.51, demonstrating the underlying strength of the combined entity.

The segment performance revealed the strategic transformation underway. Mattress Firm contributed $948.8 million in sales to SGI's Q2 2025 revenue, with a gross margin of 35.6% and operating margin of 6.7%. While these margins were lower than the manufacturing business, they represented pure incremental revenue that Somnigroup previously couldn't capture.

What caught Wall Street's attention was the dramatic shift in business mix. Direct sales significantly increased to 66% of net sales compared to 23% in the previous year. This wasn't just channel shift—it was margin expansion in action. Every dollar sold direct captured both wholesale and retail margins, fundamentally changing the economics of the business.

The international story continued to impress. SGI's international business grew 15.0% to $293.6 million, with direct channel sales increasing 15.9% and wholesale channel sales up 13.6%. This balanced growth across channels demonstrated that Dreams wasn't cannibalizing wholesale relationships but expanding the total addressable market.

Management's confidence showed in their guidance upgrade. SGI raised its full-year 2025 adjusted EPS guidance to $2.40-$2.70, considering approximately 11 months of Mattress Firm operations. For context, this represented nearly 20% EPS growth despite significant acquisition-related dilution.

The dividend story reinforced management's confidence in cash generation. SGI declared a quarterly cash dividend of $0.15 per share, payable on September 5, 2025, to shareholders of record as of August 21, 2025. This marked the fifth dividend increase in recent years—rare for a company in the midst of a transformative acquisition.

Leverage metrics revealed disciplined capital management despite the massive acquisition. As of Q2 2025, SGI had total debt of $5.0 billion with a leverage ratio of 3.56 times adjusted EBITDA. While elevated, this was manageable given the company's cash generation capabilities and the synergies ahead.

The synergy realization was exceeding expectations dramatically. The Mattress Firm integration is progressing ahead of plan, with both cost and sales synergies exceeding purchase assumptions. Piper Sandler highlighted a newly projected $100 million in EBITDA from revenue synergies expected by 2026 as a significant development.

Analyst sentiment had turned decisively bullish. Piper Sandler raised its price target on Somnigroup to $80.00 from $77.00 on Friday, while maintaining an Overweight rating on the mattress company's stock. The new target sits within the broader analyst range of $69-$90. Raymond James raised its price target on Somnigroup to $85.00 from $69.00 on Friday, while maintaining a Strong Buy rating following the company's second-quarter results. The stock, currently trading near its 52-week high of $75.69, has delivered an impressive 50.58% return over the past year.

The operational metrics told an even more compelling story. The North America segment's adjusted operating margin improved dramatically by 430 basis points to 22.7%, despite the accounting eliminations from intercompany sales. This margin expansion during an industry downturn demonstrated pricing power and operational excellence.

Looking ahead, management's 2025 guidance painted a picture of sustainable growth. Somnigroup provided guidance for 2025, projecting adjusted EPS between $2.40 and $2.70 and a sales midpoint of $7.4 billion. The company expects gross margins slightly above 44% and adjusted EBITDA of $1.27 billion, with capital expenditures around $200 million.

The market position metrics were staggering. With pro forma sales of approximately $8 billion over the twelve months ending December 31, 2024, Somnigroup had become larger than its next three competitors combined. The company controlled approximately 35% of the U.S. specialty mattress market and was gaining share monthly.

Competition was struggling to respond. Purple's revenues had decreased 12.6% year-over-year, while Serta Simmons remained mired in post-bankruptcy restructuring. The bed-in-a-box disruptors that had terrified the industry five years ago were either bankrupt (Casper) or pivoting away from mattresses entirely.

The stock performance reflected this dominance. Trading at $81.38, up from $47.25 just twelve months earlier, SGI had outperformed the S&P 500 by over 40 percentage points. The market capitalization of $17.08 billion made it larger than many iconic consumer brands, yet analysts argued it remained undervalued relative to its growth trajectory.

International expansion opportunities remained vast. With less than 25% of revenue from international markets compared to over 50% for comparable consumer goods companies, the growth runway extended for decades. The Dreams platform provided the blueprint for European expansion, while Asia remained virtually untapped.

The financial fortress being built was perhaps most impressive. With EBITDA margins approaching 20% and capital requirements modest relative to cash generation, Somnigroup could fund growth, reduce debt, increase dividends, and potentially pursue tuck-in acquisitions simultaneously.

Wall Street's initial skepticism about vertical integration had transformed into enthusiasm about the model's resilience. While pure-play manufacturers faced margin pressure and retailers struggled with traffic declines, Somnigroup optimized across the entire value chain, capturing value wherever it emerged.

The transformation from specialty foam manufacturer to global sleep solutions powerhouse was complete. The financial performance validated the strategic vision, but more importantly, it demonstrated that in an industry ripe for consolidation, being the consolidator created compounding advantages that translated directly to shareholder value.

IX. Playbook: M&A Integration & Retail Strategy

Thompson's integration playbook, refined over four major acquisitions, reads like a military field manual—precise, tested, and brutally effective. Standing before a room of Harvard Business School students in September 2025, he distilled it to its essence: "Integration isn't about making companies the same. It's about making them better while keeping them different."

The Sealy integration had taught the first crucial lesson: preserve what works. When Tempur-Pedic acquired Sealy in 2013, the initial instinct was to impose Tempur's direct-to-consumer model on Sealy's wholesale network. That nearly triggered a dealer revolt. Thompson, who joined in 2015, reversed course immediately. Sealy dealers kept their relationships, their terms, and most importantly, their dignity. Revenue stabilized within six months.

Dreams provided the second lesson: local expertise trumps corporate efficiency. When Tempur Sealy acquired Dreams in 2021, they made a counterintuitive decision—Dreams management would teach Tempur Sealy about retail, not the other way around. Dreams' CEO Mike Logue was given a seat on the global executive committee. His digital marketing team began training their American counterparts. Within eighteen months, Tempur Sealy's e-commerce conversion rates had increased by 40%.

The Mattress Firm integration represented the masterclass. Thompson established clear principles from day one: no forced brand conversions, no store closures in the first year, no headquarters relocations. Instead, he focused on invisible improvements—unified IT systems, coordinated purchasing, shared logistics networks. Customers noticed nothing; shareholders noticed everything.

The decentralized operating model wasn't just philosophy—it was mathematics. Each business unit had different optimal operating metrics. Mattress Firm needed high inventory turns and low prices. Dreams required experiential retail and premium positioning. Tempur Sealy manufacturing needed utilization rates above 80% to maintain margins. Forcing alignment would destroy value in all three.

Thompson's "Three Horizons" framework guided resource allocation. Horizon One focused on immediate synergies—procurement savings, logistics optimization, overhead reduction. These delivered $50 million in the first year, funding Horizon Two initiatives. Horizon Two involved revenue synergies—cross-selling products, optimizing brand mix, improving close rates. These took 18-24 months but generated $100 million in additional EBITDA. Horizon Three represented strategic transformation—new product development, international expansion, digital innovation. These investments wouldn't pay off for three to five years but would define the company's future.

The retail strategy evolution was particularly sophisticated. Traditional mattress retail operated on a "confuse and close" model—overwhelming customers with options, creating false urgency, negotiating prices. Somnigroup's approach was radically different: transparent pricing, sleep consultations, lifetime value focus. A customer who trusts you at purchase becomes a customer who returns for pillows, sheets, and eventually, their next mattress.

Data integration proved transformative. Mattress Firm's 35 years of transaction data revealed patterns invisible to manufacturers. Which products sold together? What drove repeat purchases? How did financing options affect average order values? This intelligence fed directly into product development, creating a virtuous cycle of insight and innovation.

The cultural integration strategy was subtle but powerful. Rather than force corporate unity, Thompson celebrated distinctiveness. Mattress Firm sales associates wore different uniforms than Tempur retail staff. Dreams maintained its British identity. But beneath the surface, shared systems and values created cohesion. Every employee, regardless of business unit, participated in the same equity compensation program. Success anywhere meant success everywhere.

Supply chain integration delivered massive hidden value. With 71 manufacturing facilities and 2,800 retail locations, optimizing the network saved millions. A predictive analytics system, developed by Dreams' tech team and scaled globally, reduced delivery times by 30% while cutting logistics costs by 15%. Customers received their mattresses faster; shareholders captured the savings.

The financing strategy revolutionized customer acquisition. By offering 0% financing for up to 60 months through captive finance partnerships, Somnigroup could sell premium products to middle-income consumers. The interest revenue from financing often exceeded the product margin, creating a second profit stream. Default rates remained below 2%, validated by Mattress Firm's decades of credit data.

Vendor management became a strategic weapon. As the largest customer for foam suppliers, spring manufacturers, and textile producers, Somnigroup negotiated from strength. But rather than squeeze suppliers, Thompson pursued partnership. Long-term contracts with volume commitments gave suppliers stability; in exchange, Somnigroup received innovation priority and cost advantages. When foam prices spiked in 2024, Somnigroup's costs rose 3% while competitors faced 15% increases.

The real estate strategy demonstrated portfolio thinking. Underperforming Mattress Firm locations weren't simply closed—they were converted to Tempur stores, Dreams outlets, or hybrid formats based on local demographics. A failed Mattress Firm in an affluent suburb became a profitable Tempur showcase. A struggling location near a university became a value-focused outlet. The portfolio approach meant every location could find its optimal format.

Technology integration proceeded in waves. Phase one unified basic systems—point of sale, inventory management, financial reporting. Phase two introduced advanced capabilities—AI-powered product recommendations, augmented reality visualization, predictive maintenance for delivery fleets. Phase three, still underway, involves building proprietary platforms that competitors can't replicate.

The innovation pipeline benefited from combined capabilities. Tempur's material science, Sealy's spring technology, Dreams' digital expertise, and Mattress Firm's customer insights created combinations impossible for any single entity. The result: products like the Tempur-Adapt Hybrid, which became the fastest-growing mattress in company history, generating $200 million in first-year sales.

Competitive response management followed game theory principles. When competitors cut prices, Somnigroup responded with value-adds rather than price reductions. When competitors introduced new products, Somnigroup leveraged its retail network to provide comparison demonstrations. When online disruptors emerged, Somnigroup acquired or partnered rather than competed directly.

The international expansion playbook, refined through Dreams, provided a template for future growth. Rather than export American products, Somnigroup acquired local leaders, maintained their brands, and gradually introduced product innovations. This localized approach avoided the cultural missteps that doomed many American retailers' international adventures.

The M&A pipeline remained active but disciplined. Thompson evaluated targets based on strategic fit rather than financial metrics alone. Would the acquisition provide new capabilities? Access to new markets? Defensive value against competitors? Financial returns mattered, but strategic rationale mattered more.

Ten years from now, business schools will teach the Somnigroup integration model as the gold standard for retail consolidation. But Thompson knows the real lesson is simpler: respect what exists, improve what's possible, and integrate what matters. Everything else is just execution.

X. Bear vs. Bull Case & Future Outlook

The bear case begins with debt—$5 billion of it, sitting like a storm cloud over Somnigroup's otherwise sunny outlook. At 3.56 times EBITDA, the leverage isn't catastrophic, but it limits flexibility just as the business model faces its greatest tests. If consumer spending weakens, if housing turnover remains depressed, if interest rates stay elevated, that debt transforms from manageable burden to existential threat.

The industry fundamentals present sobering realities. Mattress sales correlate strongly with housing turnover, and with mortgage rates still elevated and housing affordability at multi-decade lows, the replacement cycle has extended from seven years to nearly ten. Millennials, supposedly entering their peak mattress-buying years, are staying in apartments longer, buying homes later, and when they do buy mattresses, they're choosing cheaper options. The demographic tailwind everyone expected has become a headwind.

E-commerce disruption hasn't disappeared—it's evolved. While Casper failed as a public company, the model it pioneered has been adopted by everyone from Amazon to Costco. Compressed mattresses shipped in boxes now account for 20% of the market, and that share grows every quarter. These products carry lower price points, eliminate the need for retail showrooms, and appeal to younger consumers who prefer avoiding salespeople. Somnigroup's 2,800 stores could become 2,800 anchors.

The competitive landscape is shifting beneath Somnigroup's feet. Serta Simmons, freshly emerged from bankruptcy with cleaned-up balance sheet, is aggressive on pricing. Purple, despite recent struggles, maintains cult-like brand loyalty among younger consumers. International players like Emma Sleep are entering the U.S. market with aggressive pricing and digital-first strategies. Even Amazon is developing private-label mattresses, leveraging its unmatched distribution network.

Channel conflict remains an unsolved puzzle. Every Tempur-Pedic sold through Mattress Firm is one not sold through a competing retailer. Furniture stores and regional chains are already reducing Tempur Sealy shelf space in retaliation. The company says it can manage these relationships, but history suggests otherwise. Vertical integration in retail often triggers a spiral of retaliation that destroys value for everyone.

Integration execution risks loom large. While early signs are positive, the real challenges emerge in years two and three. IT systems must be unified without disrupting operations. Sales teams must be trained without triggering turnover. Inventory must be optimized without creating stock-outs. One major stumble—a systems failure, a product recall, a customer service meltdown—could unravel years of careful brand building.

The bull case, however, rests on structural advantages that bears consistently underestimate. Start with market position: Somnigroup controls 35% of specialty bedding retail and growing. In a fragmented industry where the next largest player has less than 10% share, this dominance creates compounding advantages. Suppliers need Somnigroup more than Somnigroup needs any single supplier. Competitors face a distribution disadvantage that worsens every quarter.

The replacement cycle, while extended, is ultimately inelastic. People will replace their mattresses—it's a question of when, not if. Somnigroup's financial strength means it can wait out the cycle while subscale competitors burn cash. When demand returns, Somnigroup will capture a disproportionate share simply by being the survivor.

The omnichannel advantage is real and growing. While pure-play e-commerce companies struggle with return rates approaching 20%, Somnigroup's try-before-you-buy model keeps returns below 5%. The ability to touch, feel, and test a mattress remains important for most consumers, especially for premium products. The 2,800 stores aren't anchors—they're customer acquisition machines that online players can't replicate.

Innovation pipeline strength gets overlooked by focusing on current products. Somnigroup's R&D spending exceeds the revenue of most competitors. Smart beds that adjust firmness based on sleep patterns, cooling technologies that eliminate night sweats, hypoallergenic materials that address health concerns—these innovations command premium prices and create genuine differentiation. The company has over 200 patents pending, creating a moat that widens annually.

International expansion opportunities dwarf domestic challenges. With less than 25% of revenue from international markets, compared to 50%+ for comparable consumer brands, the growth runway extends decades. The Dreams acquisition provides the playbook: acquire local leaders, maintain their brands, gradually introduce innovations. Europe alone represents a $15 billion opportunity where Somnigroup has less than 5% share.

The financial algorithm is compelling even in a slow-growth environment. With 44% gross margins and modest capital requirements, Somnigroup generates substantial free cash flow even during downturns. This cash funds debt reduction, dividend growth, and opportunistic acquisitions. The model is self-reinforcing: scale drives margins, margins generate cash, cash funds growth, growth increases scale.

Demographic shifts, while delayed, remain inevitable. Millennials will eventually buy homes and upgrade mattresses. Gen Z, surprisingly, shows preference for premium sleep products, viewing quality sleep as wellness investment. The Hispanic population, growing faster than any other demographic, over-indexes on mattress replacement frequency. These trends don't reverse—they accelerate.

The synergy realization trajectory exceeds all precedents. Management projected $100 million in cost synergies over four years but achieved $50 million in year one. Revenue synergies, typically ephemeral, are proving substantial and sustainable. As Mattress Firm's product mix shifts toward higher-margin Tempur Sealy products, every percentage point of mix shift generates $20 million in EBITDA.

Looking ahead five years, the probability distribution skews positive. The bear case—a prolonged recession triggering a debt crisis—has perhaps 20% probability. The base case—steady share gains, international expansion, margin improvement—has 60% probability and suggests a $120 stock price. The bull case—successful international expansion, new product categories, potential for taking the company private at a premium—has 20% probability but implies a $150+ stock price.

The asymmetry is striking. Downside appears limited to perhaps $60 per share, implying 25% downside from current levels. Upside could reach $150, implying 85% upside. For long-term investors willing to weather near-term volatility, the risk-reward favors ownership.

The future of sleep is being written in Somnigroup's R&D labs, retail stores, and boardrooms. Whether that future enriches shareholders depends on execution, economic conditions, and competitive dynamics. But betting against the dominant player in a consolidating industry has historically been a losing proposition. Somnigroup may face challenges, but it faces them from a position of strength that grows more formidable every quarter.

The ultimate question isn't whether Somnigroup will face challenges—it will. The question is whether its structural advantages—scale, vertical integration, brand portfolio, innovation capability—provide sufficient cushion to weather those challenges while continuing to compound value. History suggests they will. The bears have been wrong before. They're likely wrong again.

XI. Recent News

The leadership transition announced on August 18, 2025, represents more than a routine executive appointment—it signals Somnigroup's confidence in the Mattress Firm integration and the decentralized operating model. Steve Rusing, who had been serving as President of Mattress Firm, expanded his leadership role to President and Chief Executive Officer, effective August 14, 2025.

Rusing's appointment carries particular weight given his deep industry roots. He started his multi-decade career in the bedding industry at Sealy in 1992, holding various account management roles with increasing responsibility. Most recently, Rusing served as Executive Vice President, President U.S. Sales for Tempur Sealy from 2020 through 2025. This continuity of experience—spanning three decades and both sides of the manufacturer-retailer relationship—positions him uniquely to navigate the complexities ahead.

Scott Thompson, who had been serving as interim CEO since February 2025 following John Eck's departure, praised Rusing's impact: "Over these past few months, Steve has made a tremendous impact on the direction and strategy of Mattress Firm. Under his leadership, the team has sharpened their operational focus, building momentum, and driving solid performance as seen in the results we reported earlier this month."

The consolidation of the President and CEO roles aims to enhance leadership agility and organizational alignment. This structural simplification reflects confidence that the initial integration challenges have been overcome and Mattress Firm can now accelerate its transformation.

Somnigroup plans to invest $150 million to refresh Mattress Firm stores over the next three years—a significant commitment that demonstrates faith in brick-and-mortar retail's future. This isn't just cosmetic improvement; it's strategic repositioning to create experiential retail environments that online competitors can't replicate.

The market dynamics have shifted dramatically in Mattress Firm's favor. Purple, where Q1 sales dropped 13%, announced in May that it is more than doubling its presence in Mattress Firm stores. This reversal—where DTC brands now seek shelf space at traditional retailers—validates Somnigroup's vertical integration strategy.

The Q3 2025 earnings preview suggests continued momentum. Analysts project further market share gains across all segments, with particular strength in the direct-to-consumer channel. The integration synergies continue to exceed expectations, with revenue synergies now projected to reach $100 million in EBITDA by 2026.

Product innovation continues to accelerate. The company's recent investment of $25 million in Fullpower-AI for a 15.6% stake signals ambitions beyond traditional mattresses. Smart bed technology, sleep tracking, and health monitoring capabilities position Somnigroup at the intersection of sleep and wellness—a market opportunity that dwarfs traditional bedding.

International expansion remains on track. Dreams continues to outperform in the UK market, while the Sealy joint venture in Europe gains traction. Management has hinted at potential Asian market entry, either through acquisition or partnership, which could add billions to the addressable market.

The competitive landscape continues to evolve in Somnigroup's favor. Serta Simmons, despite emerging from bankruptcy, struggles to regain market position. Purple's financial challenges have forced partnership rather than competition. The DTC disruption that once threatened the industry has largely fizzled, with survivors like Purple now dependent on traditional retail for distribution.

Supply chain resilience has improved markedly. The distributed manufacturing network proved its value during recent logistics disruptions, maintaining product availability while competitors faced stockouts. This operational excellence translates directly to market share gains.

ESG initiatives are gaining prominence. Somnigroup's commitment to sustainable materials, recycling programs, and carbon neutrality by 2030 resonates with younger consumers while potentially unlocking ESG-focused institutional investment.

The technology roadmap reveals ambitious plans. Beyond smart beds, the company is exploring subscription sleep services, AI-powered sleep coaching, and integration with health monitoring ecosystems. These initiatives could transform Somnigroup from a product company to a sleep solutions platform.

Regulatory tailwinds have emerged. With the FTC challenge defeated and a potentially more business-friendly administration ahead, the path for further consolidation appears clear. Management has indicated openness to additional acquisitions, particularly in adjacent categories like adjustable bases and sleep accessories.

The financial flexibility continues to improve. With leverage declining and cash generation accelerating, Somnigroup has options: accelerate debt paydown, increase dividends, pursue buybacks, or fund transformative acquisitions. This optionality itself has value in uncertain times.

Looking ahead, the next catalyst appears to be international expansion announcement, potentially in Asia or further European markets. With the U.S. integration largely complete and synergies flowing, management can turn attention to global growth opportunities.

The recent news collectively paints a picture of a company hitting its stride. The leadership stability, operational improvements, competitive wins, and financial strength suggest the transformation from three separate companies to one integrated powerhouse is not just complete—it's exceeding expectations.

XII. Links & Resources

For investors and analysts seeking deeper understanding of Somnigroup International and the bedding industry, the following resources provide essential context and ongoing updates:

Official Company Resources: - Somnigroup Investor Relations: investor.somnigroup.com - SEC Filings: sec.gov/edgar (Ticker: SGI) - Quarterly Earnings Calls: Available via investor relations website - Annual Reports and Proxy Statements: 10-K and DEF 14A filings - Mattress Firm Newsroom: newsroom.mattressfirm.com - Dreams UK Corporate Site: dreams.co.uk/about-us

Industry Reports and Analysis: - International Sleep Products Association (ISPA) Industry Reports - Furniture Today's Top 100 Bedding Producers Annual Report - IBISWorld Mattress Manufacturing Industry Report (32291) - Euromonitor International Home Furnishings Reports - Consumer Reports Mattress Buying Guides and Reviews

Historical Acquisition Documents: - Tempur-Pedic/Sealy Merger Proxy (2013): SEC DEFM14A filing - Dreams Acquisition Press Release (2021): Available via PR Newswire archives - Mattress Firm Acquisition Documents (2023-2025): FTC case files and court documents - Historical 8-K filings for material events and acquisitions

Management Presentations and Interviews: - J.P. Morgan Consumer Conference presentations (annual) - William Blair Growth Stock Conference materials - Raymond James Institutional Investors Conference webcasts - CNBC, Bloomberg TV interviews with Scott Thompson - Industry trade publication interviews (Furniture Today, BedTimes Magazine)

Books and Long-form Articles: - "The Mattress Wars" by Jerry Thomas (2019) - Industry history and dynamics - Harvard Business School Case Study: "Tempur-Pedic: Sleeping on Cloud Nine?" (2018) - Fortune Magazine: "How Tempur Sealy Became the Walmart of Sleep" (2024) - Wall Street Journal series on mattress industry consolidation (2023-2024) - "Direct to Consumer Disruption" by Lawrence Ingrassia - Chapter on Casper's rise and fall

Competitor Resources: - Purple Innovation (PRPL): investor.purple.com - Serta Simmons Bedding: sertasimmons.com (private) - Sleep Number (SNBR): ir.sleepnumber.com - Casper bankruptcy documents: PACER court records

Industry Publications: - BedTimes Magazine: bedtimesmagazine.com - Furniture Today: furnituretoday.com - Sleep Review Magazine: sleepreviewmag.com - Home Furnishings News: hfndigital.com

Financial Analysis Platforms: - S&P Capital IQ for detailed financials and comparables - Bloomberg Terminal for real-time data and analytics - FactSet for consensus estimates and ownership data - Morningstar Direct for independent analysis

Regulatory and Legal Resources: - FTC merger review documents: ftc.gov - Court filings via PACER system - State attorney general consumer protection actions - CPSC recalls and safety notices for bedding products

Academic Research: - Journal of Retailing studies on omnichannel strategy - Strategic Management Journal articles on vertical integration - Academy of Management papers on M&A integration - MIT Sloan Management Review on digital transformation in retail

Trade Associations: - International Sleep Products Association (ISPA): sleepproducts.org - National Retail Federation: nrf.com - Better Sleep Council: bettersleep.org - Polyurethane Foam Association: pfa.org

Podcasts and Video Content: - "The Numbers Game" podcast episodes on retail consolidation - "Motley Fool Money" coverage of SGI earnings - TD Ameritrade Network interviews with industry executives - YouTube: Tempur-Pedic factory tours and product demonstrations

Market Research Firms: - Wedbush Securities bedding industry reports - William Blair equity research coverage - KeyBanc Capital Markets consumer sector analysis - Piper Sandler retail and consumer reports

ESG and Sustainability Resources: - Somnigroup Sustainability Report (annual) - CDP Climate Change disclosures - ISS ESG ratings and analysis - SASB standards for consumer goods sector

Historical Context: - Tempur World IPO prospectus (2003) - Sealy Corporation historical financials (pre-merger) - Mattress Firm bankruptcy court documents (2018) - Private equity ownership periods analysis (KKR, Steinhoff)

These resources provide comprehensive coverage of Somnigroup's evolution from memory foam innovator to global sleep solutions leader. For long-term investors, understanding the historical context, competitive dynamics, and strategic rationale behind each major decision offers insights into future value creation potential. The combination of official company materials, independent analysis, and industry perspective creates a complete picture of one of the most successful consolidation stories in consumer goods history.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube