Stitch Fix: The Data Science Fashion Experiment

I. Introduction and Episode Roadmap

Picture this: a box arrives at your door. Inside are five clothing items you never searched for, never browsed, never clicked on. An algorithm and a human being, working in tandem, decided these were right for you. You try them on in your living room, keep what you like, send back what you don't. Every return, every note, every hesitation feeds back into a machine that promises to know you better next time.

That was the pitch behind Stitch Fix, the San Francisco company that dared to answer one of retail's most audacious questions: Can software pick your clothes better than you can?

For a fleeting moment, Wall Street believed the answer was yes. Stitch Fix went public in 2017 as a profitable, fast-growing company led by the youngest woman ever to take a venture-backed startup through an IPO. The stock eventually surged past $113. Analysts called it the "Netflix of fashion." The data science team published research papers and hired PhDs at a clip that would make a university department jealous.

The company seemed to represent everything the 2010s tech economy promised: that algorithms could optimize any human experience, including something as subjective and emotional as getting dressed in the morning.

Then it all came apart.

The stock collapsed more than 98% from its peak. Active clients bled away by the millions. Three different CEOs cycled through in four years. The company's signature innovation, the algorithmically curated box of clothing, turned out to be a product that a passionate minority loved and the mass market shrugged at.

Every strategic pivot seemed to undermine the original premise. And the competition didn't come from copycat startups; it came from TikTok, Shein, and the simple fact that most people actually enjoy browsing for their own clothes.

The Stitch Fix story is a case study in the gap between what data science can do in theory and what it can do in practice, particularly when the thing you're trying to predict is human taste. It tests the limits of subscription commerce, the durability of narrative-driven valuations, and the question every founder eventually confronts: Is this a product for everyone, or just for early adopters?

This is the story of how a Harvard Business School project became a two-billion-dollar company, then nearly vanished. What went right, what went wrong, and what it teaches us about the collision between technology and fashion.

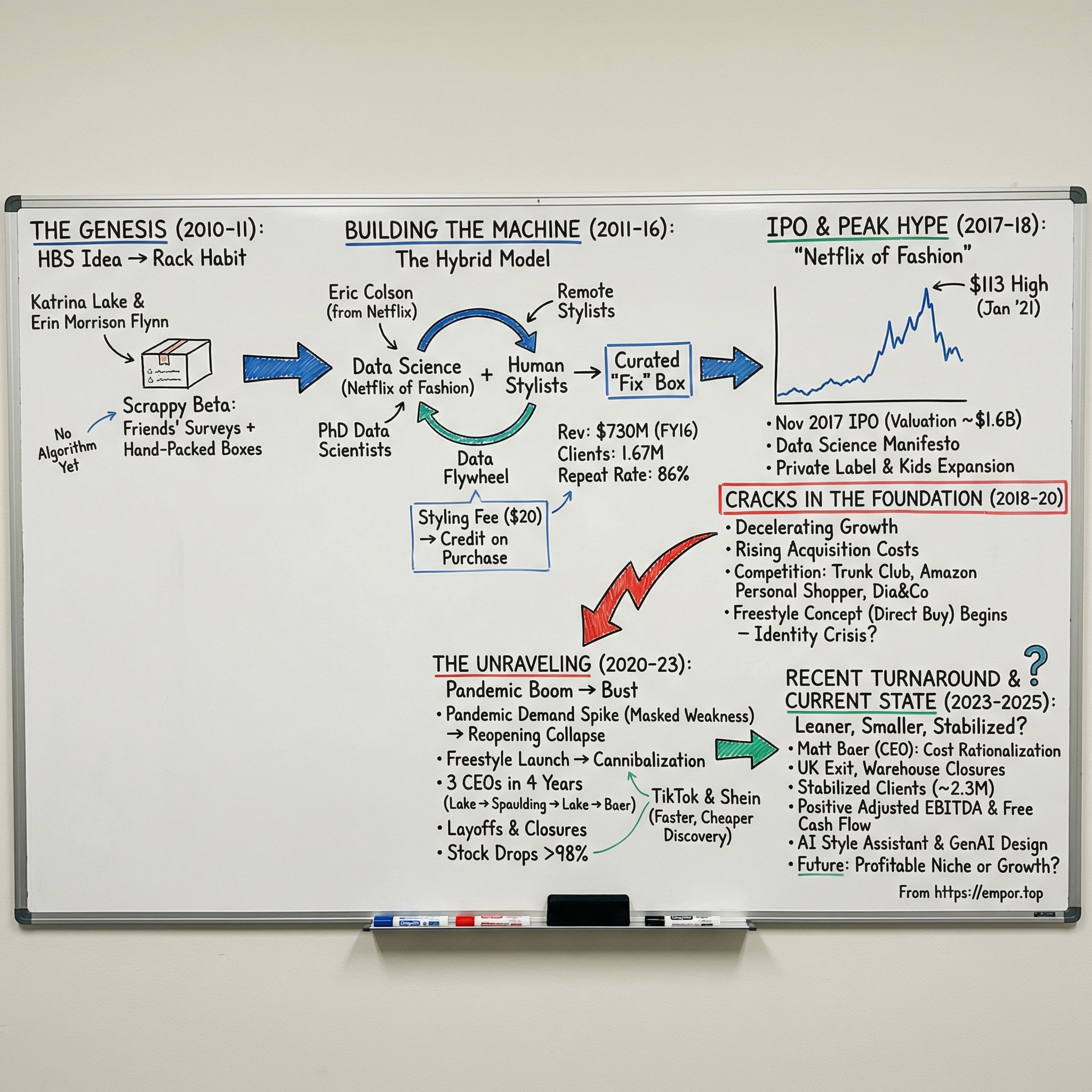

II. The Genesis: Katrina Lake and the Founding Story (2010-2011)

In the winter of 2009, Katrina Lake sat in a Harvard Business School classroom in Boston and thought about a problem that had nagged her for years: shopping for clothes online was broken. You could scroll through thousands of items on a website, but the experience was overwhelming, impersonal, and oddly joyless. Meanwhile, hiring a personal stylist cost hundreds of dollars an hour and was reserved for the wealthy. There had to be something in between.

Lake was not a typical HBS student. Born in 1982 in San Francisco to a physician father and a Japanese immigrant mother who was a schoolteacher, she had studied economics at Stanford as an undergraduate, where she briefly considered following her father into medicine before the pull of business won out.

After graduation, she spent two years at The Parthenon Group (now EY-Parthenon), a management consulting firm, where she worked with e-commerce and traditional retailers. That experience gave her a bird's-eye view of how the fashion industry actually operated: the guesswork of buying, the inefficiency of inventory, the staggering return rates. She then moved to Leader Ventures, a small venture capital firm, where she invested in early-stage startups and saw firsthand how founders turned observations into companies.

By the time she arrived at Harvard Business School in 2009, Lake had a thesis forming in her mind. The subscription commerce model was gaining traction across industries: Birchbox for beauty samples, Dollar Shave Club for razors, Blue Apron for meal kits. Data science was becoming the hottest discipline in Silicon Valley, with companies like Netflix demonstrating that algorithms could predict human preferences with uncanny accuracy.

And fashion e-commerce was maturing rapidly, with Zappos, ASOS, and others proving that people would buy clothes they hadn't tried on. The pieces were there. Nobody had assembled them.

During the summer before her second year, Lake interned at Polyvore, a social commerce platform in San Francisco where users created digital fashion collages. The experience confirmed her intuition: people craved curation. They wanted someone, or something, to cut through the noise and say, "This is for you."

Back in Cambridge for her final semester, Lake began beta-testing an idea that was comically low-tech given the data science ambitions that would later define the company. She asked friends and friends-of-friends in the Boston area to fill out style surveys, detailed questionnaires about their preferences, sizes, lifestyles, and budgets. Then she went out with her own credit card, bought clothes she thought they would like, and dropped off boxes at their homes. Payments came back through PayPal or, in some cases, handwritten credit card numbers on slips of paper stuffed into the return envelope.

The initial investment was ten thousand dollars of her own savings and a twenty-thousand-dollar loan from her parents. The company's first name was Rack Habit. Her co-founder was Erin Morrison Flynn, a former J.Crew buyer who brought merchandising expertise to complement Lake's analytical bent. The two women ran the operation out of Lake's Cambridge apartment, the living room doubling as a warehouse.

What Lake discovered in those early months was revelatory. Customers didn't just tolerate the service; they loved it. The combination of convenience, personalization, and surprise created an emotional response that traditional e-commerce couldn't match.

Opening the box felt like receiving a gift. The feedback was immediate, specific, and actionable: "I loved the color but the fit was too tight." "This is exactly my style but too expensive." Every data point made the next box better.

Lake graduated from HBS in 2011, renamed the company Stitch Fix, and moved operations to San Francisco. The early days in the Bay Area were scrappy. Lake and Flynn sorted through racks of clothes, packed boxes by hand, and juggled everything from customer service emails to supplier negotiations. There was no algorithm yet, just two women with good taste and a spreadsheet.

The co-founder dynamic, however, would become a painful footnote. After the company secured its first venture funding in 2012, Lake asked Flynn to give up some of her equity stake to create a pool for new hires. Flynn's role gradually diminished, and by the time of the IPO filing, she received only a brief mention in the S-1.

Fast Company later published an investigation titled "The Mysterious Case of Stitch Fix's Missing Co-founder," which highlighted the tension between Flynn's early contributions and her eventual absence from the company's origin narrative. It was an uncomfortable blemish on an otherwise compelling founding story.

Steve Anderson of Baseline Ventures led a $750,000 seed round, becoming the first outside investor. Anderson saw something most VCs missed at the time: the combination of subscription economics and data-driven personalization in a massive, fragmented market. The pitch Lake made to him and subsequent investors was deliberate and precise: "We're not a fashion company. We're a data science company that happens to sell clothes." That framing would prove to be both the company's greatest asset and, eventually, the source of its most painful reckoning.

III. Building the Machine: The Hybrid Model (2011-2016)

The first critical hire Stitch Fix made was not a designer or a merchandiser. It was Eric Colson, who in August 2012 left his position as Vice President of Data Science and Engineering at Netflix to become Stitch Fix's Chief Algorithms Officer. At Netflix, Colson had built the recommendation systems that powered the "Because you watched" suggestions seen by millions of subscribers. His arrival sent a clear signal: Stitch Fix was serious about being a technology company first and a retailer second.

Colson's challenge was to build an entirely new kind of recommendation engine, and to understand why, it helps to grasp what makes fashion recommendation so much harder than other domains. Netflix recommended movies from a fixed catalog; a user either watched something or didn't. The feedback signal was binary and clean. Fashion was exponentially more complex. A dress isn't just "liked" or "disliked." It might be the wrong size, the right style but wrong color, perfect for work but not for weekends, appealing in theory but unflattering on a particular body type. And unlike a movie, which looks the same to everyone, a garment looks different on every body. The dimensionality of the problem was staggering.

Think of it this way: a movie recommendation engine operates in a world where the product is identical for every consumer and the feedback is simple (watched it, liked it, didn't finish it). A fashion recommendation engine operates in a world where the same product (a medium blue blouse) has a completely different value proposition depending on the customer's body shape, skin tone, existing wardrobe, upcoming calendar, local climate, and current emotional state.

The data requirements are orders of magnitude greater, and the feedback is far more nuanced.

Here is how a "Fix" actually worked, once Colson and his growing team had built the system. A new customer would fill out an online style profile providing upward of ninety data points: measurements, preferred price ranges, lifestyle details (office job? stay-at-home parent? weekend warrior?), style preferences (classic? trendy? bohemian?), colors they gravitated toward, patterns they avoided, even a Pinterest board they admired. The algorithms would ingest this profile and compare it against every item in Stitch Fix's inventory, ranking thousands of pieces in predicted order of relevance for that specific customer.

Then came the human element. A stylist, working remotely from anywhere in the country, would receive the algorithmic output: a rank-ordered list of recommendations along with the customer's profile, any personal notes they had left ("I have a wedding in two weeks" or "I'm trying to dress more professionally"), and their complete feedback history from prior Fixes. The stylist would make the final call, selecting five items from the algorithm's suggestions, adding their own judgment about what combinations would work together and what would surprise the customer in the right way. They would write a personal note explaining their choices.

The box shipped. The customer tried everything on at home. They kept what they wanted and returned the rest in a prepaid envelope, along with detailed feedback on every item: why they kept it, why they returned it. That feedback flowed directly back into the algorithms, sharpening the model for next time.

The elegance of this system was that it turned every transaction into training data. Most retailers get almost no signal about why a customer didn't buy something. Stitch Fix got rich, structured feedback on every single item it sent out.

Over time, the data compounded. By the time of the IPO, the company's repeat purchase rate had climbed to 86%, meaning nearly nine out of ten customers who received a Fix came back for another one.

The pricing model was equally clever. Customers paid a twenty-dollar styling fee per Fix, which was credited toward any items they purchased. If you bought something, the styling was effectively free. If you didn't buy anything, the fee covered the cost of curation and shipping. This created a psychological nudge: once you'd paid the twenty dollars, you were motivated to find at least one item worth keeping. And the revenue model was straightforward: the styling fee plus the markup on whatever customers purchased.

Building the stylist workforce was an innovation in its own right. By the time of the IPO, Stitch Fix employed roughly 3,400 part-time and full-time stylists, most working remotely from their homes across the country.

This was years before remote work became mainstream, and it gave Stitch Fix access to a talent pool that traditional retailers couldn't tap: stay-at-home parents with fashion expertise, aspiring designers in small towns, fashion school graduates who didn't want to relocate to New York.

The company recruited people with fashion sensibility, empathy, and communication skills, then armed them with algorithmic tools that handled the data-heavy lifting. It was a genuinely novel division of labor: machines did what machines do best (processing millions of data points, identifying statistical patterns), and humans did what humans do best (understanding context, exercising taste, building relationships). The personal note that accompanied each Fix became a beloved feature. Customers felt known. They felt cared for. That emotional connection, which no algorithm alone could create, was arguably the company's most underrated asset.

Colson's team grew to more than a hundred data scientists, over half of whom held PhDs in fields like astrophysics, computational neuroscience, and statistics. They published research through a technical blog called Multithreaded and released an interactive Algorithms Tour in March 2017 that showcased the breadth of the company's data science applications: recommendation systems, demand forecasting, inventory management, warehouse logistics optimization, and even algorithmic fashion design, where the system could identify gaps in the product assortment and help create entirely new garments to fill them.

Colson himself would transition to an emeritus role in June 2019 and depart entirely by May 2021, his exit preceding the worst of the company's struggles. It was a quietly significant departure: the man who had built the algorithmic engine walked away before it became clear the engine alone couldn't sustain the business.

The business grew at a pace that venture investors rarely see in physical retail. Revenue jumped from $342 million in fiscal 2015 to $730 million in fiscal 2016, a 113% increase. Active clients nearly doubled in the same period, from 867,000 to 1.67 million.

By fiscal 2017, revenue reached $977 million and active clients stood at 2.19 million.

The profitability story was equally compelling. The company became profitable in 2014 and posted $33 million in net income in fiscal 2016 on a remarkably capital-efficient foundation. Total equity capital raised before the IPO was approximately $42.5 million, a fraction of what most consumer startups burn. To put that in perspective, Stitch Fix generated roughly twenty-three dollars in annual revenue for every dollar of venture capital it raised, one of the best ratios of any consumer startup of the 2010s era.

The strategic sequencing was methodical. Stitch Fix launched with women's clothing only in 2011, added maternity in 2015, expanded to men's apparel in September 2016, introduced plus sizes in 2017, and launched a kids' line with a proprietary brand called Rumi and Ryder in 2018.

Each category expansion followed the same playbook: collect data, build the recommendation model, recruit specialized stylists, and launch.

The venture funding rounds told the story of rising confidence. Baseline Ventures led the seed in 2011. Lightspeed Venture Partners co-led the Series A in February 2013 at $4.75 million. Then came the pivotal Series B in October 2013: Bill Gurley of Benchmark, one of Silicon Valley's most respected and contrarian investors, led the $12 million round and joined the board. Gurley's involvement was a signal to the market. He had made his reputation at Benchmark by backing companies like Uber and Zillow, and his willingness to invest in a fashion startup suggested he saw something beyond the clothing racks. Two other experienced board members joined at the same time: Marka Hansen, a former Gap executive, and John Fleming, the former CEO of Walmart.com, lending retail operational credibility to the data science narrative. A $30 million Series C followed in June 2014, valuing the company at roughly $330 million.

The total pre-IPO equity capital raised came to approximately $42.5 million. For context, Blue Apron raised over $200 million before going public, and Dollar Shave Club raised roughly $160 million before its Unilever acquisition. Stitch Fix's capital efficiency was remarkable and spoke to the fundamental soundness of the early model: the styling fee provided upfront cash flow, the inventory turned quickly, and the company didn't need to build physical stores.

Why did VCs love this? Subscription revenue was predictable and recurring. The styling fee created negative working capital dynamics: customers paid before Stitch Fix had to pay for the merchandise. The AI narrative was catnip for Silicon Valley storytelling. And the unit economics, at least in the early days, appeared to work. But the question that would haunt the company for years was already lurking beneath the surface: How big was the addressable market for people who wanted an algorithm and a stranger to pick their clothes?

IV. The IPO and Peak Hype (2017-2018)

On the morning of November 17, 2017, Katrina Lake stood on the floor of the Nasdaq exchange and watched Stitch Fix begin trading as a public company. She was thirty-four years old, the youngest woman ever to take a venture-backed company through an IPO, and the only woman to lead a tech offering that year. The S-1 filing she had shepherded to the SEC contained seventy-four mentions of the word "algorithms" and sixty-four mentions of "data science." This was not an accident. The document was a manifesto: Stitch Fix was a technology company that happened to sell clothes.

The IPO itself was a complicated debut. The company had initially planned to sell 10 million shares at $18 to $20 each, which would have raised roughly $180 million. Investor appetite was softer than expected. The offering was downsized to 8 million shares, and the price was cut to $15, raising $120 million and valuing the company at approximately $1.6 billion. Shares opened at $16.90, briefly popped 20%, then drifted back to close at $15.15, just a penny above the offering price. The financial press called it lukewarm.

But the narrative that Wall Street bought into was powerful, even if the first-day trading was muted. Here was a profitable company (it had posted $33 million in net income the prior fiscal year, though it was roughly breakeven in the IPO year) growing revenue at 34% annually, with 2.2 million active clients and an 86% repeat rate. The bull case was intoxicating: the U.S. apparel market was a $334 billion opportunity, and Stitch Fix had penetrated less than one percent of it. The data flywheel was spinning. Every Fix sent out made the algorithms smarter, which made the next Fix better, which drove higher retention, which generated more data. In theory, this was an unassailable competitive moat.

Analysts reached for the highest compliment the 2010s tech economy could bestow: they called Stitch Fix the "Netflix of fashion." The comparison was irresistible. Netflix used algorithms to recommend entertainment; Stitch Fix used algorithms to recommend clothing. Netflix had a subscription model; so did Stitch Fix. Netflix had disrupted an entrenched industry; Stitch Fix was doing the same.

The analogy fell apart on closer inspection (Netflix's marginal cost of serving another customer was near zero; Stitch Fix had to physically buy, warehouse, ship, and process returns of physical garments), but it was good enough for a compelling pitch deck.

Over the following months and into 2018, the stock found its footing and began to climb. Revenue for fiscal 2018 came in at $1.2 billion, crossing the billion-dollar threshold. Active clients grew to 2.7 million. The company launched kids' clothing, expanding its addressable demographic. Lake appeared on magazine covers and at industry conferences, articulating a vision of personalized retail that resonated with the zeitgeist. She was compelling: cerebral, data-oriented, and quietly confident in a way that contrasted with the bluster common in Silicon Valley. In an era of charismatic, attention-seeking tech CEOs, Lake was a refreshing contrast: measured, analytical, and focused on the product rather than the spotlight.

The company also began experimenting with something that would prove fateful: private-label brands. Stitch Fix's data science team had identified gaps in the merchandise assortment, styles and price points where customer demand existed but no suitable third-party product did. Rather than wait for brands to fill those gaps, Stitch Fix designed and manufactured its own garments, a practice that would eventually grow to represent nearly half of all sales. The initiative, which included algorithmic fashion design where the system could literally help create new clothing styles, was both a genuine innovation and a sign of the company's growing ambition to control its own destiny.

What the Street was not pricing in, however, was the emerging competitive threat. Nordstrom had acquired Trunk Club in 2014 for $350 million and was investing heavily in personal styling. Amazon was building its own personal shopper service. Wantable, Dia&Co, and a growing roster of startups were chasing the same thesis.

More importantly, customer acquisition costs were climbing as the easily converted early adopters were already on board, and the next wave of customers required significantly more persuasion. The 86% repeat rate was impressive in isolation, but the question was whether new cohorts would retain at the same rate as the enthusiasts who had signed up first. There was growing evidence inside the company that later cohorts were less engaged, less likely to stick around, and more expensive to acquire, a pattern common in subscription businesses but one that can be masked for years by the enthusiasm of the early base.

These were the cracks that nobody wanted to look at while the stock was rising and the narrative was intact. They wouldn't stay hidden for long.

V. Cracks in the Foundation (2018-2020)

The first warning signs appeared in the metrics before they appeared in the headlines. Starting in late 2018, the rate of active client growth began to decelerate. Not decline, not yet, but the pace of new additions was slowing in a way that raised uncomfortable questions about the company's total addressable market. Revenue growth for fiscal 2019 came in at roughly $1.58 billion, still growing at about 29%, but the growth rate had dropped from 113% just three years earlier. Active clients grew to around 3.2 million, solid growth in absolute terms but decelerating rapidly. In a subscription business, growth deceleration is a leading indicator. It means either your addressable market is smaller than you thought, your acquisition funnel is getting less efficient, or both.

The competitive picture was evolving rapidly, and the threat came from multiple directions simultaneously. Trunk Club, backed by Nordstrom's buying power and retail expertise, was going after the same affluent, time-pressed customer with a similar box-of-clothes model but with the credibility of a department store brand behind it.

Amazon launched its Personal Shopper service in July 2019 at $4.99 per month, dramatically undercutting Stitch Fix's $20 styling fee and leveraging the logistics infrastructure of the world's most efficient fulfillment machine. Wantable targeted the activewear and lifestyle niche. Dia&Co, which had raised over $100 million in venture capital, focused on the plus-size market that Stitch Fix was also pursuing. The subscription styling concept that had seemed like a proprietary innovation was starting to look more like a strategy anyone could copy, albeit not profitably.

The fundamental challenge was one that Lake and her team understood better than anyone but struggled to solve: customer acquisition costs were high and rising, while customer lifetime values were uncertain at scale. The early adopters who loved the service were relatively cheap to find; they were already reading fashion blogs, following influencers, and searching for styling solutions. The next tier of potential customers required expensive marketing campaigns that promised an experience many of them ultimately didn't stick with. The math of subscription commerce is unforgiving. If it costs you $200 to acquire a customer and they churn after four Fixes with a $50 profit per Fix, you've barely broken even. If retention drops even a few percentage points, the model collapses.

Then, in early 2020, the world changed. COVID-19 shut down physical retail overnight, and the initial impact on Stitch Fix was severe. On March 20, 2020, the company temporarily closed two distribution centers in South San Francisco and Bethlehem, Pennsylvania, due to local health orders. By the end of March, roughly 70% of warehouse capacity was offline. Order backlogs doubled week over week. Revenue for the quarter ended May 2020 fell 9% year over year.

But the pandemic quickly became a double-edged sword. As lockdowns extended and physical stores remained shuttered, consumers who had never tried online shopping services gave Stitch Fix a look. People stuck at home, flush with stimulus checks and craving novelty, discovered the dopamine hit of opening a curated box of clothing.

By the fall of 2020, the company reported a surprise quarterly profit, active clients grew 10% year over year to 3.8 million, and the stock surged 45% after earnings. Management guided for 20 to 25% revenue growth in fiscal 2021.

Beneath the surface euphoria, however, a strategic tension was building that would define the next three years. In 2019, Stitch Fix had begun developing a feature internally called Direct Buy, which would become publicly known as Freestyle. The concept was simple: let customers browse and purchase individual items on the website, like any other e-commerce store, without ordering a curated Fix box. It was an acknowledgment, implicit but unmistakable, that the core styling model had a ceiling. Not everyone wanted to hand over control of their wardrobe to an algorithm and a stranger. Some people just wanted to shop.

Freestyle represented a profound identity crisis. Stitch Fix's entire brand was built on the promise that curation was better than browsing, that the company's data science could know you better than you knew yourself. Launching a browse-and-buy feature was the equivalent of Netflix suddenly letting you pick your own shows instead of relying on recommendations. It might expand the addressable market, but it undermined the founding thesis.

Meanwhile, leadership changes were stirring. In January 2020, Stitch Fix hired Elizabeth Spaulding as President, reporting to Lake. Spaulding came from Bain & Company, where she had founded the firm's global digital practice and built a reputation as an expert on digital transformation. Her appointment signaled that the company was preparing for a strategic shift, one that would accelerate far faster than anyone anticipated once the pandemic reshuffled the deck.

VI. The Unraveling (2020-2023)

January 27, 2021 was the peak. On that day, Stitch Fix shares hit an intraday high of $113.76, propelled by the same forces lifting every pandemic-era growth stock: stimulus-fueled consumer spending, a mass migration to e-commerce, and an investor mania for anything that could plausibly be called a technology company. The market cap briefly touched $10 billion. For a company that had gone public at a $1.6 billion valuation just three years earlier, it was a staggering run.

Within weeks, the story began to reverse. On March 8, 2021, the company disclosed delays in the rollout of Direct Buy, and the stock dropped 28% in a single session. Then, on April 13, Katrina Lake announced she would step down as CEO, effective August 1, transitioning to the role of Executive Chairperson. The market took the news as a vote of no confidence in the company's trajectory; shares fell another 5%.

Lake's departure mattered more than the typical CEO transition because she was the company. Her personal brand, the thoughtful founder who merged data science with fashion, was inseparable from Stitch Fix's identity. Every profile written about Stitch Fix mentioned Lake's Stanford and Harvard pedigree, her data-science-first philosophy, her quiet intensity. She was the embodiment of the thesis.

Handing the reins to Elizabeth Spaulding, a management consultant by training who had spent her career at Bain & Company advising companies rather than running them, signaled a pivot from visionary founder mode to operational execution mode. The implicit message was that the company's challenges now required a different skillset than the one that had built it.

Spaulding's background was impressive in its own right. At Bain, she had founded the firm's global digital practice and created ADAPT, Bain's software engineering group. She understood digital transformation in theory, but understanding transformation as a consultant and executing it as a CEO are different disciplines. The fashion industry is unforgiving to outsiders, and Spaulding would find that the Bain playbook didn't translate cleanly to the messy reality of managing thousands of stylists, millions of garments, and a customer base that was beginning to question the value proposition.

Spaulding took over on August 1, 2021, and immediately pushed Freestyle to center stage. The feature launched publicly in August and September of that year, with a splashy rollout that positioned it as a new era for the company. Anyone visiting stitchfix.com would now see a direct-buy shopping experience before they saw the curated Fix option. Management told investors that Freestyle was "additive" and "incremental," that it would expand the total addressable market without cannibalizing the core styling business.

The data told a different story. Active clients peaked at approximately 4.18 million in the quarter ended October 2021, then began to decline and never recovered. On December 7, 2021, during the fiscal first-quarter earnings call, Spaulding made a critical admission: Freestyle was causing "short-term impacts of cannibalization." The stock dropped 24%. What she described as "inadvertent friction," the website redesign that funneled customers toward Freestyle and made it harder to order a Fix, was eroding the core business.

The damage accelerated through 2022. In June, the company announced it was laying off 15% of its salaried workforce, roughly 330 employees, and disclosed that Freestyle conversion rates were failing to meet targets. The stock fell another 27%. By September, management reversed course and restricted Freestyle to existing Fix subscribers only, an acknowledgment that the open-access strategy had backfired. A class-action securities fraud lawsuit was later filed alleging that management had known from internal testing that Freestyle was cannibalizing Fix orders while publicly insisting otherwise.

The unraveling reached its nadir on January 5, 2023. Spaulding stepped down as CEO effective immediately, also resigning from the board. Simultaneously, the company announced it would cut 20% of its remaining salaried workforce. Katrina Lake returned as interim CEO, a rescue mission that underscored how dire the situation had become. The stock was trading around $4, down 97% from its peak.

The numbers told a brutal tale. Revenue, which had peaked at $2.1 billion in fiscal 2021, fell to $2.0 billion in fiscal 2022 and then collapsed to $1.59 billion in fiscal 2023. Active clients dropped from 4.18 million to 3.3 million.

The company posted a net loss of $195 million in fiscal 2022 and $92 million in fiscal 2023. The data science promise that had justified a $10 billion valuation was failing its most fundamental test: people were leaving, and the algorithms couldn't convince them to stay.

The competitive landscape had also shifted beneath Stitch Fix's feet in ways that no amount of data science could counter. Shein, the Chinese ultra-fast-fashion company, had exploded onto the American market, capturing nearly a third of fast-fashion sales in the first quarter of 2022 by offering thousands of new styles daily at prices that made Stitch Fix's curated boxes seem expensive and slow.

TikTok had become the dominant platform for fashion discovery, with its algorithmic feed showing users clothes, trends, and shopping links in a format that was entertaining, social, and instant. TikTok Shop came to dominate social shopping, capturing over 68% of social shopping gross merchandise value; 85% of Gen Z consumers reported that social media influenced their buying decisions. Instagram Shopping made visual discovery seamless.

The "too much choice" problem that Stitch Fix had been founded to solve was being addressed by social media algorithms that were faster, more fun, and free.

This was perhaps the cruelest irony of all. Stitch Fix had been built on the insight that algorithmic curation could help people discover clothes they would love. A decade later, algorithmic curation was indeed helping people discover clothes, but it was happening on TikTok and Instagram, not in a subscription box. The curation had moved to social platforms where discovery was entertainment, not a transaction. Stitch Fix's delivery mechanism, the curated box, was being obsoleted not by better boxes but by an entirely different paradigm of fashion discovery.

In June 2023, Stitch Fix named Matt Baer as its third CEO in two years. Baer came from Macy's, where he had served as Chief Customer and Digital Officer, and before that from Walmart's e-commerce division. His background was firmly in traditional retail digital transformation rather than in the startup or data science worlds.

He held a J.D. from the Benjamin N. Cardozo School of Law and had even practiced complex commercial litigation before pivoting to e-commerce. He was an operator, not a visionary, and his mandate was clear: stop the bleeding, cut costs, and figure out if there was a viable business left.

Baer moved quickly. He exited the UK market entirely, closing international operations by October 31, 2023. He shuttered the Dallas and Bethlehem fulfillment centers, reducing the U.S. footprint from five distribution centers to three and laying off roughly 950 warehouse workers. He cut more than $100 million in annualized general and administrative expenses. The company that had once aspired to be the future of retail was now in triage mode.

The stock hit an all-time low of $2.06 on April 22, 2024. From peak to trough, that represented a decline of more than 98%. A hundred-dollar investment at the January 2021 high was now worth less than two dollars.

VII. Recent Developments and Current State (2023-2025)

Walk into Stitch Fix's remaining headquarters operations today and you'll find a very different company than the one that rang the Nasdaq bell in 2017. The workforce is a fraction of its former size. Two of its five warehouses stand empty. The UK expansion is a memory. The word "Freestyle" is no longer uttered with the breathless optimism of a strategy that would unlock a $300 billion market. What remains is smaller, leaner, and cautiously optimistic in a way that would have seemed unimaginable during the pandemic euphoria.

Matt Baer's turnaround strategy has been executed in distinct phases, each building on the last. Phase one, completed through fiscal 2025, was pure cost rationalization: exit unprofitable markets, close excess capacity, and right-size the organization to match its reduced revenue base. The combined annualized savings from the UK exit and warehouse consolidation alone approached $50 million.

Phase two, currently underway, focuses on reinvesting in the core Fix experience. The company increased the number of items per Fix from five to eight, driving a roughly 10% year-over-year increase in average order value. Private-label brands, which carry higher margins than third-party merchandise, now account for 40 to 50% of total sales. A men's proprietary brand called The Commons has become one of the top ten brands in the overall portfolio.

The company has also embraced generative AI, using it for product design and development and launching an AI "Style Assistant" chatbot that provides personalized outfit recommendations. This represents an evolution of the original data science vision: less "we'll pick your clothes for you" and more "we'll help you navigate your choices."

The financial trajectory under Baer shows genuine stabilization. Full-year fiscal 2025 revenue was $1.27 billion, down 5.3% from the prior year but with the rate of decline slowing markedly. More importantly, the company achieved positive adjusted EBITDA of $49 million and generated $9.3 million in free cash flow for the first time in years.

The most recent quarter, Q1 of fiscal 2026 ended November 2025, delivered $342 million in revenue, up 7.3% year over year, the first meaningful revenue growth in over three years. Adjusted EBITDA was $13.4 million.

Active clients continue to decline but at a dramatically slower rate: 2.307 million as of November 2025, down 5.2% year over year but essentially flat on a sequential basis, declining just 0.1% from the prior quarter. Revenue per active client, meanwhile, continues to climb: $559, up 5.3% from a year earlier, reflecting the expanded Fix size and higher engagement from the remaining customer base. Client lifetime values are at three-year highs.

The balance sheet provides a meaningful cushion. As of the most recent reporting, Stitch Fix held $244 million in cash and investments against roughly $87 million in total debt, yielding a net cash position of approximately $157 million.

The company extended its credit facility maturity to December 2028, removing near-term debt concerns. At a market capitalization of roughly $500 million, the company trades at an enterprise value of approximately $250 to $330 million, meaning the market assigns modest value to the operating business above the cash on the balance sheet.

Management's guidance for full-year fiscal 2026 calls for revenue between $1.32 and $1.35 billion, implying 4 to 7% growth, with adjusted EBITDA of $38 to $48 million and positive free cash flow. The next earnings report, for the quarter ending January 2026, is scheduled for March 9, 2026.

One piece of competitive news has been quietly favorable: Amazon shut down its competing "Prime Try Before You Buy" service in January 2025, removing one of the most formidable competitors from the space. Trunk Club, Nordstrom's entry, had already been shuttered in May 2022. Dia&Co filed for bankruptcy in 2023.

The graveyard of subscription styling competitors is now longer than the list of active participants, which either validates the difficulty of the model or suggests the market itself was never as large as hoped.

The loyal customer base that remains, roughly 2.3 million active clients, skews 70% female, with the largest cohort aged 25 to 34. These are time-constrained professionals who genuinely value the curation and convenience the service provides. Sixty-seven percent of retained customers attribute their loyalty to the relationship they've built with their assigned human stylist, a data point that both validates the hybrid model and raises questions about scalability.

The ultimate question for Stitch Fix today is whether it can grow from here or whether this is the steady state: a niche service for a loyal but limited audience, generating modest profits on a billion-dollar-plus revenue base. The answer will determine whether the stock, currently hovering in the $3.50 to $4.50 range, represents a deeply discounted turnaround opportunity or a value trap.

VIII. What Went Wrong: The Deep Dive

The autopsy of Stitch Fix's decline reveals not a single fatal flaw but an accumulation of structural challenges that the company's early success masked. Understanding them requires examining several interlocking failures, each of which compounded the others.

Start with the AI and data science mirage, the most fundamental miscalculation. The company's founding thesis, that algorithms could predict human fashion taste at scale, turned out to be far harder than predicting what movies you'd enjoy or what songs you'd listen to. Fashion is not merely dimensional (size, color, pattern); it is social, contextual, emotional, and constantly shifting.

A woman doesn't just want clothes that fit her body and match her stated preferences. She wants clothes that make her feel a certain way, that signal something to the people around her, that work for a specific occasion she might not have mentioned. The cold-start problem, the challenge of making good recommendations for new customers with limited data, was never truly solved.

And as one former data scientist put it, the human stylists were doing far more of the heavy lifting than the company's public narrative suggested. The algorithms were powerful at filtering and ranking, but the magic of a great Fix often came down to a stylist's intuition about what would delight a customer. The "Netflix of fashion" analogy broke down because taste in clothing is fundamentally more personal, more physical, and more volatile than taste in entertainment.

Then there was subscription fatigue, a force that hit Stitch Fix and dozens of other companies simultaneously. The 2010s had produced a subscription box for seemingly every product category: food, cosmetics, pet supplies, razors, vitamins, socks, even underwear. By the early 2020s, consumers were drowning in recurring charges. The average American household had multiple active subscriptions, and the first ones to get cut during belt-tightening were the ones that felt discretionary.

Here is the hierarchy that consumers revealed through their behavior: streaming entertainment (Netflix, Spotify) was the last thing people canceled because it provided daily value at low cost. Grocery and convenience subscriptions (Amazon Prime) were retained because they saved time on necessities.

Fashion subscriptions were among the first to go because clothing is discretionary, the purchase frequency is lower, and the value proposition, someone else picking your clothes, requires a level of trust and satisfaction that is hard to maintain over time. A clothing subscription, no matter how good the algorithms, was inherently more discretionary than a streaming service or a grocery delivery.

The customer acquisition economics never penciled out at scale. In the early years, when the early-adopter audience found Stitch Fix through word of mouth and organic press coverage, acquisition costs were manageable. As the company pushed to grow beyond that initial base, it had to spend heavily on digital advertising, influencer partnerships, and brand campaigns to reach consumers who had never considered algorithmic styling. Those later cohorts retained at lower rates than the enthusiasts who had signed up first, creating a toxic dynamic: spending more to acquire customers who were worth less.

The inventory trap deserves its own examination. Traditional retailers buy inventory for stores based on local demand patterns and merchant intuition. Stitch Fix bought inventory for algorithms, a fundamentally different and far more complex undertaking. The system needed to have the right item, in the right size, in the right warehouse, at the right time for a customer whose Fix might be ordered two weeks or two months from now. When the algorithms misjudged demand, the company was left with mountains of unsold merchandise that had to be marked down, destroying gross margins. The complexity of buying for an algorithmic recommendation system, rather than for a store with a known customer base and foot traffic, proved to be an underappreciated operational burden.

Perhaps the deepest flaw was a category error. Wall Street valued Stitch Fix as a technology company, assigning it multiples that reflected high-margin, asset-light software businesses. But the economics were stubbornly those of a retailer: physical inventory, warehouse leases, shipping costs, return processing, and gross margins in the mid-40s. When the growth story faded, the stock repriced not just for slower growth but for its true identity as a retail business, which trades at a fraction of the multiples the market had once assigned.

The pandemic provided one final act of distortion. The surge in demand during 2020 and early 2021, driven by locked-down consumers and stimulus spending, masked the underlying deterioration in the business. Management interpreted the boom as validation of the model and invested accordingly, launching Freestyle, hiring aggressively, and expanding warehouse capacity. When the world reopened and consumers returned to physical stores, the organic demand evaporated, leaving Stitch Fix overextended and overbuilt. The pandemic boom was the worst thing that could have happened to Stitch Fix's strategic clarity. It provided precisely the wrong signal at precisely the wrong moment, encouraging the company to double down on expansion when it should have been fortifying its core.

IX. Business Model and Strategy Analysis

To understand Stitch Fix's strategic position with the rigor it deserves, it helps to apply two of the most enduring frameworks in competitive analysis: Michael Porter's Five Forces and Hamilton Helmer's Seven Powers.

Porter's Five Forces paint a picture of a company operating in one of the most structurally challenging competitive environments in all of retail.

The threat of new entrants was and remains high. The subscription styling model, while operationally complex, has no meaningful patent protection, no regulatory barrier, and no network effects that create winner-take-all dynamics. Trunk Club, Wantable, Dia&Co, Amazon, and numerous smaller players all entered the space within years of Stitch Fix's founding. The barriers to entry are high enough to require real capital (warehouses, inventory, stylists, technology), but not so high as to deter well-funded competitors. That every major competitor ultimately failed or exited is less a vindication of Stitch Fix's moat than an indictment of the entire category's economics.

The bargaining power of suppliers sits at moderate. Stitch Fix sources from a mix of third-party brands and its own private-label lines. Third-party brands have alternatives (department stores, their own direct channels, other e-commerce platforms), which limits Stitch Fix's leverage. The shift toward private label, now representing 40 to 50% of sales, has been a deliberate move to improve margins and reduce supplier dependency, but it also means the company must bear the full risk of designing and producing its own merchandise.

The bargaining power of buyers is high. Customers face near-zero switching costs. Canceling a Stitch Fix subscription takes seconds. There are countless alternative ways to buy clothes, from walking into a store to opening an Instagram ad. The twenty-dollar styling fee, once a clever mechanism to drive conversion, became a barrier as competitors offered free or cheaper alternatives.

The threat of substitutes is arguably the most devastating force. Stitch Fix doesn't just compete with other subscription styling services. It competes with every way a person can acquire clothing: fast fashion (Shein, Zara, H&M), traditional retail (Nordstrom, Macy's, Target), mass e-commerce (Amazon), direct-to-consumer brands, resale platforms (ThredUp, Poshmark), and social commerce (TikTok Shop, Instagram Shopping). The styling-box model is a substitute for traditional shopping, but traditional shopping is also a substitute for the styling box, and most consumers have revealed a preference for the latter.

Competitive rivalry is intense and gets worse every year. The online apparel market is a battlefield with Amazon, Walmart, and every major retailer investing billions in digital personalization. Stitch Fix's share of the overall online apparel market is tiny, and the competitors bringing AI-powered recommendations to their own platforms are closing the personalization gap.

Helmer's Seven Powers framework reveals the absence of durable competitive advantage.

Scale economies proved limited. Stitch Fix never achieved the scale required to make its infrastructure costs trivially small relative to revenue. The company's fixed costs, warehouses, technology, and stylist management, remained significant even at $2 billion in revenue, and when revenue declined, those costs became crushing.

Network effects were essentially absent. Your Fix does not get better because someone else uses the service. There is no user-generated content, no social graph, no marketplace dynamic where more participants create more value. Each customer relationship is essentially bilateral between the customer and the platform.

Counter-positioning was initially strong, and this was perhaps the most compelling element of the original bull case. When Stitch Fix launched, no traditional retailer wanted to cannibalize its own stores by offering a subscription styling service that might divert customers from the higher-margin in-store experience. This is the classic innovator's dilemma: the incumbents understood the threat but couldn't respond without undermining their existing business.

Nordstrom's Trunk Club acquisition was the closest attempt, and even that was operated as a separate entity rather than integrated into the core Nordstrom experience. But counter-positioning eroded over time as the broader retail industry adopted AI-powered personalization within their existing channels, achieving the recommendation benefits without requiring customers to adopt a new subscription model.

The incumbents didn't need to copy Stitch Fix's business model; they just needed to copy its best feature, algorithmic personalization, and embed it in their own.

Switching costs are among the lowest in any consumer business. A customer's style profile and preference data live within the Stitch Fix platform, but this creates inconvenience, not lock-in. Rebuilding a preference profile on a competing service takes minutes.

Branding was moderate at its peak. Stitch Fix successfully positioned itself as an innovative, data-driven alternative to conventional shopping. But the brand became associated with decline as headlines shifted from AI innovation to layoffs and stock collapse. Brand equity in consumer retail is fragile and hard to rebuild once tarnished.

The cornered resource was supposed to be data: billions of customer feedback data points on style, fit, and preference that no competitor could replicate. In practice, the data moat proved far weaker than the one enjoyed by search engines or social networks.

Fashion preferences shift constantly, making historical data less valuable over time. And the data was only useful in the context of Stitch Fix's specific inventory and styling model; it couldn't be easily monetized or leveraged elsewhere.

Process power, the advantage derived from the company's unique hybrid human-AI styling system, was real but not defensible. The combination of algorithms and human stylists was genuinely innovative and difficult to replicate exactly. But "difficult to replicate exactly" is not the same as "impossible to compete with," and the broader retail industry found other ways to provide personalization that customers found adequate.

The KPIs That Matter Most

For investors tracking Stitch Fix's ongoing performance, two metrics matter above all others. The first is active client count and its quarter-over-quarter trajectory. Everything in the business, revenue, data quality, algorithm improvement, stylist utilization, flows from whether the customer base is growing, stable, or shrinking. The recent near-stabilization at 2.3 million is the most important data point in the entire story. The second is revenue per active client, which captures engagement intensity, average order value, and purchase frequency in a single number. This metric has been rising even as the client base contracts, reflecting the loyalty of the remaining cohort. Together, these two numbers will tell you whether Stitch Fix is consolidating into a profitable niche or still sliding toward irrelevance.

X. Lessons and Takeaways: The Playbook

The Stitch Fix story contains lessons that extend far beyond a single company. They speak to how Silicon Valley narratives get built, how subscription businesses live and die, and how the gap between technological ambition and market reality can swallow billions of dollars.

For founders, the most searing lesson is the danger of over-indexing on a single technology narrative. Katrina Lake's genius in framing Stitch Fix as a data science company rather than a fashion retailer attracted world-class talent, won over skeptical VCs, and earned a technology-tier valuation.

But the framing created expectations the business could never meet. When the algorithms couldn't solve taste at scale, when retention rates for newer cohorts lagged the early adopters, the narrative that had built the company became the standard against which it was judged and found wanting. Technology should serve the business model, not define it.

Unit economics matter more than growth at all costs. Stitch Fix was profitable before the IPO, which was a genuine achievement and a source of credibility. But the relentless push for growth, expanding to new categories, new geographies, and new channels like Freestyle, diluted the focus on what actually made the business work: the core Fix experience for a specific type of customer. The decision to pursue Freestyle was driven by the reasonable observation that the Fix model had a ceiling, but the execution destroyed the company's most valuable asset, its brand identity as a curated styling service, without successfully replacing it with something better.

Customer retention is the single most important metric in any subscription business. A subscription that retains 85% of customers annually sounds healthy until you run the math: after five years, only 44% of the original cohort remains. To sustain growth, you need a continuous torrent of new signups, each of whom must be acquired at a cost that their lifetime value can justify. When acquisition costs rise and retention rates drop even slightly, the model moves from virtuous cycle to death spiral with alarming speed.

For investors, Stitch Fix offers a masterclass in narrative risk. The "Netflix of fashion" analogy was a category error that went unexamined for years. Netflix's marginal cost of serving an additional subscriber is near zero. Stitch Fix's marginal cost involves buying physical merchandise, shipping it, processing returns, and paying stylists.

The economics are fundamentally different, but the valuation at the peak was assigned as though they were the same. Beware any pitch that relies on an "X of Y" analogy. The X and the Y almost always differ in the ways that matter most.

High Net Promoter Scores among a small, passionate customer base do not guarantee mass-market appeal. Stitch Fix's early customers loved the service. The mistake was assuming that enthusiasm could be maintained as the company scaled to customers who were less fashion-curious, less patient with imperfect Fixes, and less willing to pay a premium for curation. A startup's early traction can be the worst kind of mirage if it creates conviction about a total addressable market that doesn't exist.

Data moats in consumer taste are much weaker than in search or social. Google's data moat grows with every query, creating a reinforcing loop that makes the product better and the barrier to competition higher. Stitch Fix's data moat erodes as fashion trends shift, as customers' bodies and lifestyles change, and as the insights from last year's Fixes become less relevant to this year's preferences. Taste data depreciates; search data compounds.

For operators, the Stitch Fix experience demonstrates that managing hybrid human-AI systems at scale is incredibly difficult. The magic of the Fix depended on algorithms and humans working in concert, each handling what they did best. But this required a level of organizational sophistication, continuous training, tooling investment, and cultural alignment that is hard to sustain through rapid growth, leadership turnover, and strategic pivots. When the company cut stylist headcount to reduce costs, the quality of the human element declined, which reduced the quality of the Fixes, which accelerated customer churn. The system was only as strong as its weakest component.

Inventory-intensive businesses need fundamentally different risk management than pure technology companies. Stitch Fix carried tens of millions of dollars in physical merchandise across multiple warehouses, with the constant risk that fashion trends would shift, seasons would change, and unsold inventory would require markdowns. This is the daily reality of every retailer, but it sat uncomfortably alongside the "we're a tech company" narrative that drove the valuation. Operators building at the intersection of technology and physical goods must price in the complexity of atoms, not just bits.

The pivot from Fix-only to Freestyle and back again illustrates another operational lesson: in subscription businesses, pivot fast when core metrics weaken, but don't pivot toward a model that contradicts your brand identity. Stitch Fix waited too long to acknowledge that active client growth was slowing, then overcorrected with Freestyle, which cannibalized the core product. A narrower, more disciplined response, perhaps improving Fix quality, reducing churn, and focusing on the most profitable customer segments, might have preserved the business model's integrity.

The big question that remains unanswered is whether the Stitch Fix model was fundamentally flawed or merely poorly executed in its later years. The fact that every competitor who tried the same model also failed (Trunk Club, Amazon Personal Shopper, Dia&Co) suggests the problem was structural, not operational. Nordstrom poured hundreds of millions into Trunk Club and couldn't make it work. Amazon, with the most advanced logistics infrastructure on earth, tried and walked away. These were not underfunded startups; they were well-resourced companies that concluded the economics didn't work. The mass market for algorithmic personal styling may simply not exist in the way that the 2010s tech optimism imagined.

XI. Bull vs. Bear Case and Future Outlook

The Bull Case

The optimistic view begins with an observation that is easy to overlook amid the wreckage: Stitch Fix still has 2.3 million active clients who choose to pay for the service. That base has nearly stabilized, declining just 0.1% sequentially in the most recent quarter, suggesting the floor may be near. Revenue has returned to growth at 7.3% year over year. Adjusted EBITDA is positive. Free cash flow is positive. The balance sheet holds $244 million in cash against $87 million in debt. The company has, by any reasonable measure, survived the crisis and emerged leaner.

The valuation reflects extreme pessimism. At a market cap of roughly $500 million, with $157 million in net cash, the enterprise value is roughly $300 million for a business generating $1.3 billion in revenue and nearly $50 million in adjusted EBITDA. Put differently, the market is valuing Stitch Fix's operating business at roughly 0.25x revenue and about 6x adjusted EBITDA, multiples that would be cheap even for a declining brick-and-mortar retailer, let alone a business with a significant technology component and positive free cash flow. If the turnaround under Matt Baer gains further traction, there is meaningful room for multiple expansion.

The competitive landscape has paradoxically improved. Amazon shut down its "Prime Try Before You Buy" service in January 2025. Trunk Club was shuttered by Nordstrom in May 2022, after Nordstrom had already written down $197 million of its original $350 million acquisition price. Dia&Co, which had raised over $100 million in venture funding targeting the plus-size market, filed for bankruptcy in 2023.

Stitch Fix is the last major player standing in subscription personal styling. This creates a nuanced dynamic: it may mean the market was never as large as hoped, but it also means the company faces less direct competition for the customers who do want this service. Sometimes being the last one standing in a niche is more valuable than being one of many competitors in a huge market.

The company's investment in generative AI could reignite the technology narrative. The AI Style Assistant and algorithmic design tools represent a new iteration of the original data science vision, one that may be more compelling to customers and investors alike. Revenue per active client continues to rise, indicating that the remaining customers are deepening their engagement.

The Bear Case

The pessimistic view starts with the trajectory. Active clients have fallen 45% from their peak and continue to decline year over year. The recent near-stabilization on a sequential basis is encouraging but could be a temporary pause before further attrition. Revenue remains 40% below its 2021 peak. The company has never demonstrated sustained client growth in the post-pandemic era.

There is no clear differentiation left. The "AI styling" promise that once justified a premium valuation has been commoditized as every major retailer now offers personalized recommendations. Shein's algorithm surfaces trend-driven fashion at a fraction of the cost. TikTok's algorithm discovers styles in a format that is entertaining rather than transactional. Stitch Fix's technology, while sophisticated, is no longer unique enough to justify a standalone business model.

The subscription apparel model may be in secular decline. The broader subscription economy has matured, and consumers are actively pruning recurring charges. The clothing subscription category has a higher bar to clear because fashion is inherently unpredictable and personal, making the "trust the algorithm" pitch harder with each year.

Cash burn risk, while reduced, has not been eliminated. The company remains GAAP unprofitable, posting a $6.4 million net loss in the most recent quarter and $28.8 million for fiscal 2025. The gap between adjusted EBITDA (positive) and GAAP net income (negative) is largely explained by stock-based compensation and restructuring charges, which are real economic costs even if they don't consume cash.

If revenue growth stalls or the economy enters a consumer spending downturn, the path to GAAP profitability could stretch further than the market's patience allows. The stock trades below $5, which creates its own set of problems: many institutional investors have policies against holding penny stocks or near-penny stocks, which limits the potential buyer base and can create a self-reinforcing cycle of low liquidity and high volatility.

Management turnover remains a concern. Three CEOs in four years creates execution risk and cultural instability that reverberates through the entire organization. Every leadership transition brings a new strategic direction, new priorities, and new uncertainty for employees, suppliers, and customers. Baer appears to be stabilizing the ship, but the company has not yet demonstrated the sustained strategic clarity needed to convince the market that the turnaround is durable rather than temporary.

There is also a lingering legal overhang. The securities fraud class action, covering stock purchases between June 2020 and June 2022, alleges that management knew Freestyle was cannibalizing the Fix business while publicly insisting it was additive. The outcome of this litigation remains uncertain and could result in a material settlement or judgment that would pressure the balance sheet.

The Likely Outcome

The most probable path forward is neither a triumphant return to growth-company status nor a bankruptcy filing. Stitch Fix appears to be settling into something more modest: a niche service for a loyal customer base, generating revenues of $1.3 to $1.5 billion and modest profits. It could be a comfortable, profitable niche business, not the unicorn it once promised to be, but a viable enterprise serving a dedicated customer base. Think of it less as the "Netflix of fashion" and more as the "Costco of personal styling," a business with limited appeal but fierce loyalty among those who use it.

It could also become an acquisition target. The proprietary data, warehouse infrastructure, technology platform, and 2.3 million engaged customers represent assets that would be valuable to a larger retailer looking to bolt on a personalization capability. At current enterprise values of roughly $300 million, the price tag would be modest for a Nordstrom, a Target, or even a private equity firm looking to take the company private, strip costs further, and operate it as a cash-flow business.

What to Watch

The two KPIs that will determine which scenario unfolds are the ones identified earlier: active client count (specifically, whether the sequential decline can turn to growth) and revenue per active client (whether deepening engagement can compensate for a smaller base). The fiscal second-quarter results, due March 9, 2026, will be the next major data point. If revenue growth accelerates and client count stabilizes or inflects upward, the turnaround thesis strengthens considerably. If clients continue to bleed, no amount of cost optimization can build a growth story.

XII. Epilogue and Reflections

Stitch Fix captured a moment in the American economy with precision. It was founded during the subscription commerce boom, grew during the data science hype cycle, peaked during the pandemic e-commerce frenzy, and crashed during the great repricing of speculative growth stocks. Each era left its mark on the company, and each transition exposed the gap between narrative and reality.

The subscription economy story is instructive. In the early 2010s, the idea that consumers would pay monthly for curated experiences seemed revolutionary. Dollar Shave Club sold to Unilever for a billion dollars. Blue Apron went public at a $1.9 billion valuation. Birchbox was the darling of beauty media.

A decade later, Dollar Shave Club was wound down by Unilever in late 2023 after years of declining sales. Blue Apron was acquired by Wonder Group for a fraction of its IPO value. Birchbox was sold for parts.

The subscription model proved to be a powerful customer acquisition tool but a poor retention mechanism for physical goods. The pattern was remarkably consistent: early adopters loved the novelty, growth looked exponential, valuations soared, and then the churn caught up. The survivors, Netflix, Spotify, Amazon Prime, succeeded because their content or services had near-zero marginal costs and improved with scale. The ones that shipped physical products consistently struggled with the economics.

Stitch Fix was perhaps the most impressive of the physical-goods subscription companies, having actually achieved profitability and a billion dollars in revenue, which makes its subsequent decline all the more sobering.

The AI and machine learning hype cycle followed a similar arc. The promise that algorithms could optimize any human experience, from choosing movies to picking clothes to diagnosing diseases, drove enormous investment and inflated expectations.

In domains with clean data, clear feedback signals, and objective success metrics, the promise was realized: recommendation engines for entertainment, search engines for information, routing algorithms for logistics. In domains where success is subjective, contextual, and constantly changing, the reality proved far more modest.

Fashion turned out to be one of the hardest problems in applied machine learning, not because the math was wrong, but because the question itself, "What do you want to wear tomorrow?", doesn't have an answer that data alone can provide.

Katrina Lake's legacy deserves to be assessed with nuance. She identified a genuine pain point, built an innovative solution, attracted world-class talent, and took a company public at a time when female founders leading tech IPOs was vanishingly rare. The company she built generated billions in revenue and served millions of customers. The fact that the market she envisioned was smaller than hoped and the competitive dynamics more brutal than anticipated does not diminish the ambition or the achievement. It does, however, place her story in the broader context of a generation of founders who were told that data science could solve anything and discovered, sometimes painfully, the limits of that belief.

Where does personalization in retail go from here? The answer is probably not toward subscription boxes curated by stylists and algorithms, but rather toward AI-powered tools embedded in the shopping experiences consumers already use. The future looks less like "a box arrives at your door" and more like "an AI assistant helps you navigate a store, online or physical, in real time."

Every major retailer is now investing in AI-powered personalization, from virtual try-on technology to conversational shopping assistants to algorithmically curated product feeds.

The insight that Stitch Fix pioneered, that data science could improve the shopping experience, turned out to be correct. The delivery mechanism, a subscription box of five items curated by a remote stylist, turned out to be the wrong wrapper for that insight.

Ironically, Stitch Fix itself seems to be recognizing this evolution. The company's latest AI Style Assistant chatbot and its shift from "we pick for you" to "we help you choose" represents a tacit acknowledgment that the future of personalized fashion is collaborative rather than prescriptive. Whether Stitch Fix can execute that pivot fast enough, and at sufficient scale, to matter in a world where every retailer is racing toward the same destination remains the open question.

In the end, Stitch Fix was a company that captured lightning in a bottle: the right founder, the right technology narrative, the right market moment. For a few brilliant years, it made the impossible seem inevitable. Then the bottle broke, and the lightning went looking for somewhere else to land.

XIII. Further Reading and Resources

Books and Long-Form

- "The New Rules of Retail" by Robin Lewis and Michael Dart, for context on how retail transformation works and fails

- Stitch Fix S-1 filing and subsequent 10-K filings (SEC EDGAR), the most revealing documents on the company's actual economics

- Harvard Business School case study on Stitch Fix, for the classroom analysis of the hybrid model

- "Subscribed" by Tien Tzuo, for the broader subscription economy thesis that shaped Stitch Fix's strategy

- Katrina Lake's pre-IPO blog posts and interviews, for insight into the founding vision before Wall Street reframed the narrative

- Benedict Evans' essays on retail and e-commerce disruption, for the structural context of why fashion retail is so hard to disrupt

- "Competing in the Age of AI" by Marco Iansiti and Karim Lakhani, for the framework on AI-powered operating models

- Stitch Fix earnings call transcripts from 2017 through 2025, which track the evolution of management's narrative in real time

- "The Everything Store" by Brad Stone, for understanding the Amazon competitive backdrop

- Academic papers on algorithmic personalization in fashion, particularly the work published on Stitch Fix's own Multithreaded blog

Key Articles

Business of Fashion's coverage of Stitch Fix's rise and fall provides the fashion industry perspective. The Information published deep dives on unit economics and internal strategy debates. Recode and Vox featured extensive Katrina Lake interviews during the company's ascent. The Wall Street Journal and Bloomberg offered the financial and market analysis that tracked the stock's collapse. Fast Company's investigation into the "mysterious case of Stitch Fix's missing co-founder" remains one of the most illuminating pieces of reporting on the company's early dynamics.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube