SolarEdge Technologies: The Rise and Fall of Solar's Optimization Pioneer

I. Introduction: From $20 Billion Empire to 95% Collapse

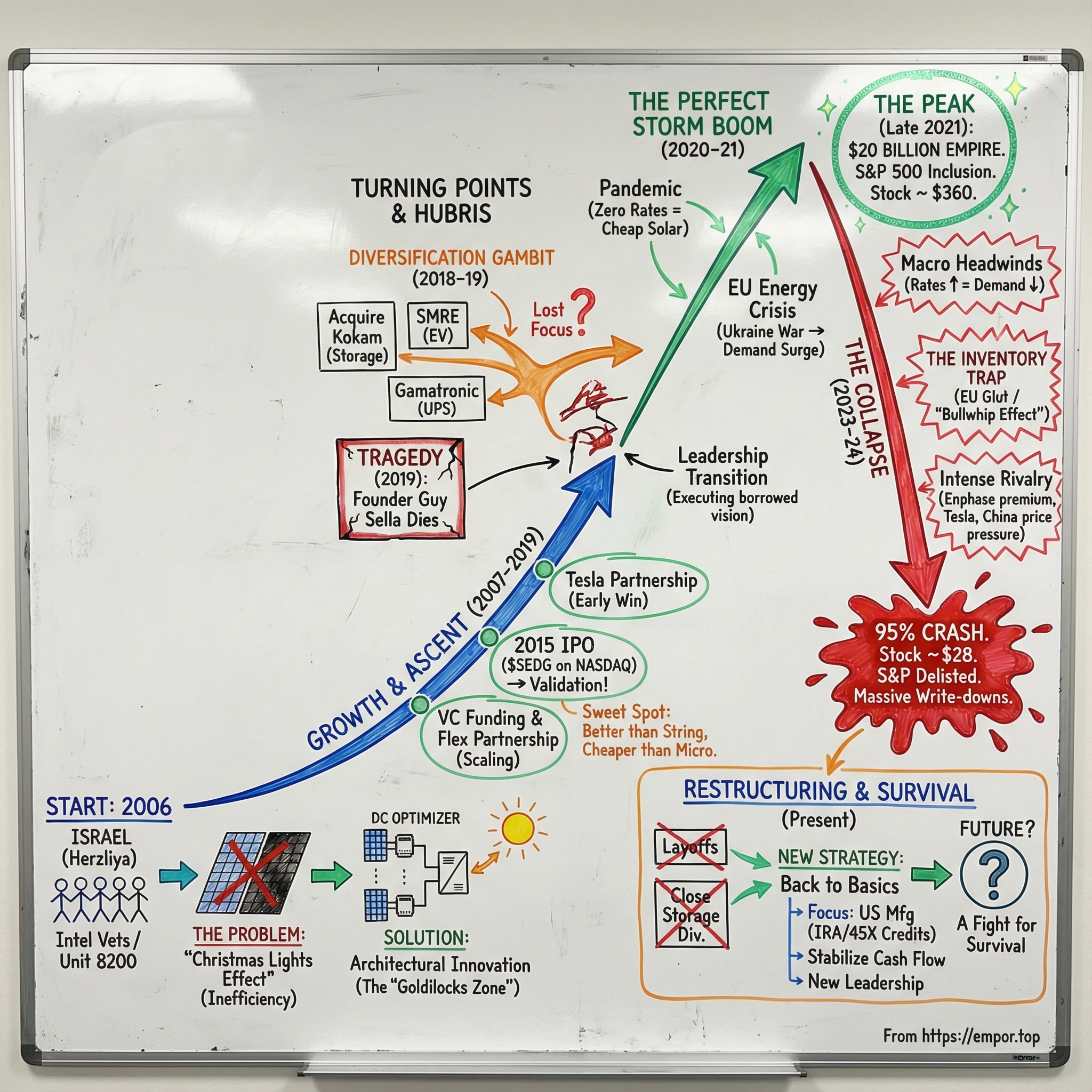

Picture the scene in a nondescript office in Herzliya, Israel, circa 2006. Five veterans of Israel's elite Electronics Research Department—men who had spent careers developing complex intelligence systems for the nation's defense establishment—sit around a whiteboard sketching diagrams of solar panels and DC-to-DC converters. They weren't solar veterans. They had never worked in renewable energy. But they saw something the industry's incumbents had missed: a fundamental inefficiency in how solar systems harvested power.

On June 25th, 2024, SolarEdge plunged nearly 15% in early morning trading to around $28 per share, down from an all-time high above $360—a devastating collapse of more than 90% from peak to trough. In 2023, SolarEdge became the most losing stock in the S&P 500 for the year, which resulted in its delisting from the index.

How did an Israeli startup founded by intelligence veterans build a $20 billion solar empire—and then lose virtually all of it? The SolarEdge story is a masterclass in architectural innovation, the perils of diversification without focus, and what happens when a visionary founder dies and a company must execute someone else's strategy. It's also a cautionary tale about the intersection of macro headwinds—interest rates, inventory cycles, and geopolitical shocks—with company-specific challenges that can turn a market leader into a cautionary tale.

This is a story of brilliant innovation, tragic loss, fatal strategic miscalculations, and an ongoing fight for survival. The company that once solved solar's "Christmas lights problem" now finds itself struggling to find its own light.

II. The Founders: Israel's Intelligence Elite Goes Solar

In the world of startup mythology, origin stories often feature scrappy founders working out of garages. SolarEdge's founding story is different—more Tom Clancy than Silicon Valley legend. SolarEdge Technologies was founded in 2006 by a team of former employees of Israel's Electronics Research Department: Guy Sella, Lior Handelsman, Yoav Galin, Meir Adest and Amir Fishelov.

Guy Sella had served as the director of technology for the Israeli National Security Council and as the secretary for the National Committee for Cyber Protection. He also served as the head of the Electronics Research Department, one of Israel's national labs, which is tasked with developing innovative and complex systems. Before founding SolarEdge, Sella was a partner at Star Venture, a venture capital firm with investments in a number of tech startups including AeroScout and Vidyo.

The other founders brought equally formidable credentials. Yoav Galin previously worked at Israel's Electronics Research Department, where he developed innovative and complex electronic systems, primarily in research, development, and management roles. Galin holds a bachelor's degree in Electrical Engineering from Tel Aviv University.

Lior Handelsman was employed by the Electronics Research Department, where he held several positions including research and development power electronics engineer, Head of the Power Electronics Group and manager of several large-scale development projects. Handelsman holds a bachelor's degree in Electrical Engineering and a master's degree in Business Administration from the Technion, Israel's Institute of Technology in Haifa.

The company was originally located in Herzliya, Israel—a coastal city north of Tel Aviv that had become a hub for Israel's high-tech industry, home to R&D centers for Intel, Microsoft, and countless cybersecurity firms.

Why would intelligence veterans pivot to solar? The answer lies in their training. These were engineers who had spent careers optimizing complex systems, finding inefficiencies, and solving problems through elegant technical solutions. When they looked at the solar industry in 2006, they saw a fundamental problem hiding in plain sight—one that the industry's traditional players had failed to address. The founders recognized the need for a more efficient and reliable way to harness solar energy, and their background in developing sophisticated electronic systems gave them unique tools to solve it.

Sella is often remembered for being determined and aggressive—a creative figure, colorful and tumultuous. One of his signature features was his affection for flip-flops, which he would often wear even at formal occasions. This combination of technical brilliance and unconventional style would define SolarEdge's culture in its formative years.

III. The Problem They Solved: Why Traditional Inverters Failed

To understand why SolarEdge mattered at all, you first need to understand what installers used to call the “Christmas lights problem.” It’s one of those metaphors that instantly makes a complex technical issue obvious.

In a solar system, panels generate direct current (DC) electricity from sunlight. Homes and businesses, however, run on alternating current (AC). The inverter—the box most homeowners never think about—is the critical piece of equipment that converts DC into usable AC power. Without it, solar panels are just expensive roof ornaments.

For decades, the industry standard was the string inverter. Multiple panels were wired together in series, forming a “string,” and their combined output was sent to a single inverter mounted on a wall. This design was simple, cheap, and easy to install—but it had a fatal flaw.

In a string system, all panels are forced to operate at the same voltage. If one panel underperforms—because it’s partially shaded by a chimney, covered in dust, degraded by heat, or aging faster than the rest—it drags down the entire string. Just like old Christmas lights, where one bad bulb can dim or kill the whole chain.

In the real world, no rooftop is perfect. Shadows move. Panels get dirty. Weather changes. Over time, mismatch losses quietly eat away at production. Industry estimates suggested traditional string inverter systems routinely lost anywhere from 5% to 25% of potential energy—a massive inefficiency in a business where every watt matters.

This was the gap SolarEdge saw.

Instead of abandoning string inverters entirely, SolarEdge attacked the weakest link. The company introduced power optimizers—small DC/DC converters installed underneath each panel. These devices allowed every panel to operate at its own maximum power point, independent of its neighbors.

The effect was transformative. A shaded or underperforming panel no longer poisoned the entire system. Each module could produce as much energy as conditions allowed, while the centralized inverter handled only the final DC-to-AC conversion.

Technically, it was an elegant solution. Each optimizer continuously monitored voltage and current at the panel level, dynamically adjusting output to maximize efficiency. From the outside, the system still looked like a traditional string inverter setup. Under the hood, it behaved more like a distributed, intelligent network.

This architecture put SolarEdge squarely in the “Goldilocks zone.” Microinverters—championed by rival Enphase—solved the Christmas lights problem by placing a full inverter behind every panel. That approach worked beautifully, but it came with higher costs, more electronics on the roof, and more potential points of failure. Traditional string inverters were cheap and simple, but increasingly outdated.

SolarEdge offered a third way: far smarter than legacy string systems, but meaningfully cheaper than full microinverter designs.

For installers, it meant better performance without blowing up system costs. For homeowners, it meant higher energy yields, panel-level monitoring, and improved safety features. And for SolarEdge, it created a powerful differentiation at exactly the right moment in solar’s evolution.

This architectural insight—small, almost obvious in hindsight—became the foundation of SolarEdge’s rise. Everything that followed, from explosive growth to market dominance, rested on this single realization: the inverter wasn’t just a box. It was the brain of the entire solar system.

IV. Early Years & The Race to Market (2006-2014)

With a technically elegant solution in hand, SolarEdge needed capital to bring it to market. In 2007, SolarEdge secured its initial seed funding of $12 million from Walden Israel and Genesis Partners. This was just the beginning.

The company was backed by a deep bench of venture investors, including GE Energy Financial Services, Norwest Venture Partners, Lightspeed Venture Partners, ORR Partners, Genesis Partners, Walden International, Vertex Ventures Israel, JP Asia Capital, and Opus Capital Ventures. The roster reflected both the caliber of the founding team and the size of the opportunity they were pursuing.

The path from prototype to production was methodical. The company started mass production of its products by contract manufacturer Flex at the end of 2009. The partnership with Flex—one of the world's largest contract manufacturers—was strategically important. It allowed SolarEdge to scale production without the capital intensity of building its own factories, a classic "asset-light" approach that would contribute to the company's attractive margins.

The early market traction was striking. By 2010, the company had shipped hundreds of thousands of power optimizers and inverters, capturing the majority of the nascent power optimizer market.

By Q4 2012, the company's momentum was accelerating. SolarEdge had essentially created and dominated an entirely new product category—the DC power optimizer segment. The company wasn't just competing in an existing market; it had defined a new one and claimed the lion's share from the start.

This period established several patterns that would persist through SolarEdge's growth phase. First, the company demonstrated an ability to execute at scale—going from lab prototype to mass production in just three years. Second, the Flex partnership showed a willingness to leverage external capabilities rather than build everything internally. Third, the dominant market share in power optimizers validated the founders' core insight about where value could be created in the solar value chain.

The competitive landscape during these years was relatively benign. Traditional string inverter manufacturers like SMA and Fronius hadn't yet developed competitive optimizer solutions. Enphase, the microinverter leader, was targeting a different segment of the market—higher-end installations where customers were willing to pay premium prices for maximum per-panel optimization. SolarEdge occupied the sweet spot: better than traditional string inverters, more affordable than microinverters.

V. The IPO & The Breakout (2015-2019)

By 2015, SolarEdge had proven its technology, demonstrated market fit, and built a profitable business. It was time for the public markets.

In March 2015, SolarEdge went public at $18 a share, raising $126 million. The shares began trading on the NASDAQ Global Select Market under the ticker symbol "SEDG." Goldman Sachs and Deutsche Bank acted as joint book-running managers for the offering.

The IPO timing proved fortuitous. While Europe had historically been SolarEdge's largest market, growth across the US solar energy market saw the US become the Company's principal source of sales. In 2015, sales in the US accounted for 73.3% of total annual revenue, a geographic diversification that would prove important in subsequent years.

Just two months after the IPO came a partnership that seemed to validate SolarEdge's strategic position. In May 2015, SolarEdge partnered with Tesla Energy to develop an inverter that could charge the Tesla Powerwall home energy storage battery that was unveiled in April 2015. The SolarEdge inverter manages both the conversion of energy from solar panels along with charging and discharging of the Powerwall.

The Tesla partnership was a double-edged sword. On one hand, it provided tremendous validation—Elon Musk's company had chosen SolarEdge over Enphase and traditional string inverter manufacturers. On the other hand, it signaled that Tesla viewed inverters as a strategic component of its energy ecosystem, not just a commodity to be purchased from suppliers.

The partnership's end came gradually, then suddenly. Over time, Tesla phased out its partnership with SolarEdge, with Tesla adding an inverter to its Powerwall 2 that was introduced in October 2016, and introducing its own solar inverter in January 2021. SolarEdge survived the loss of Tesla as a customer—a testament to the strength of its broader installer relationships—but it was an early warning sign about the risks of depending on large customers in an industry where vertical integration was increasingly attractive.

The post-IPO years (2015-2019) saw SolarEdge's business compound impressively. SolarEdge shipped record inverter capacity in late 2018, with revenues surging more than fifty percent year-over-year alongside healthy gross margins and strong profitability.

The stock reflected this operational success. From the $18 IPO price, shares climbed steadily as the company delivered quarter after quarter of growth. Margins remained healthy, market share expanded, and the total addressable market for solar continued to grow with each passing year of declining panel costs and increasing climate awareness.

VI. The Great Diversification Gambit (2018-2019)

With the core solar business humming, SolarEdge's leadership made a fateful strategic decision: diversification. The logic was straightforward—the company had built deep expertise in power electronics, and adjacent markets like energy storage and electric mobility were experiencing similar growth trajectories. Why not leverage SolarEdge's engineering DNA to capture value across the entire clean energy ecosystem?

The acquisition spree began in late 2018. In October 2018, SolarEdge acquired approximately 75% of Kokam Co., Ltd., a South Korean provider of lithium-ion battery cells, batteries, and energy storage solutions, for a reported $88 million.

Just months later, the company made an even more ambitious move. In January 2019 SolarEdge announced the acquisition of a majority stake in SMRE – an Italian EV powertrain manufacturer. Founded in 1999 and traded on the Italian AIM, SMRE has three business units: e-mobility, automated production machines and telematics software. The company has more than fifteen years of experience developing end-to-end e-mobility solutions for electric and hybrid vehicles used in motorcycles, commercial vehicles and trucks. These solutions include innovative high-performing powertrains with e-motor, motor drive, gearbox, battery, BMS, chargers, Vehicle Control Unit (VCU) and software for electric vehicles.

SolarEdge closed its acquisition of approximately 57% of S.M.R.E. Spa, an Italian supplier of electric vehicle integrated powertrain technology and electronics, for about $85 million.

The acquisitions didn't stop there. In 2019 SolarEdge announced the acquisition of Gamatronic, a UPS manufacturer, and established its Critical Power division.

Guy Sella explained the rationale at the time: "In addition to the growth and strong profitability of our solar business, this quarter we continued to lay the foundations for our non-solar future growth with the acquisition of Kokam, a leading provider of lithium-ion batteries and the post quarter acquisition of a majority holding of S.M.R.E, a provider of innovative integrated powertrain technology and electronics for the e-mobility market."

The strategic logic made sense on paper. Energy storage was essential for solar's future—batteries allow solar systems to shift energy from sunny afternoons to evening peak demand. Electric vehicles were clearly the future of transportation, and their power electronics had significant overlap with solar inverter technology. UPS systems provided a stable, high-margin adjacent market.

But there was a fatal flaw that would only become apparent later: these acquisitions were being made by a visionary founder who might not be around to execute the integration strategy. And the businesses themselves—particularly Kokam's grid-scale battery cells—had limited synergy with SolarEdge's core residential solar business.

"SolarEdge's acquisition spree in 2H is beginning to translate into margin contraction," said James Evans, Global Clean Energy Analyst with Bloomberg Intelligence. "We anticipate this will persist in 2019 as the company integrates the new lower-margin businesses and tries to realize cost synergies."

VII. The Death of a Founder & Leadership Transition (2019)

The year 2019 brought a tragedy that would reshape SolarEdge's trajectory. Guy Sella revealed to "Colleagues and Shareholders" in November 2017 that he had been diagnosed with colon cancer. At the time, Sella believed that "the condition is treatable" and that he expected "that the medical therapy I will be undergoing will allow me to travel and remain working."

Sella's untimely death came within days of his announced leave of absence and replacement by Zvi Lando, VP of Global Sales, as acting CEO. The CEO handover followed a reshuffle within SolarEdge's executive ranks.

Guy Sella was one of the founders of SolarEdge and served as the Chairman of the board of directors and Chief Executive Officer from the company's inception in 2006 until his death in August 2019.

The hire followed SolarEdge's naming of new co-chair and board director member Nadav Zafrir. As SolarEdge said at the time, Zafrir's incorporation was meant to bolster the firm's leadership structures amid Guy Sella's "continued illness." Nadav Zafrir, cybersecurity think-tank and fund Team8 founder and former Commander of the IDF's Technology & Intelligence Unit 8200, was appointed co-chairman.

He stayed on as CEO and chairman of the company until three days before his death. The two years during which he was sick was a complicated time, in many ways. Ten days before the last board meeting he chaired, Zvi Lando traveled to the U.S. When he landed in New York he had a message from Guy asking that he get back to him. Sella told him 'according to a test I did yesterday — it's over, a matter of weeks. We have to start preparing.'

The transition left SolarEdge in a precarious position. The company had just completed a string of ambitious acquisitions—Kokam, SMRE, Gamatronic—that reflected Sella's vision of building a diversified clean energy conglomerate. Now it would be up to his successors to integrate these businesses and deliver on the strategic promise, without the visionary founder who had conceived the strategy.

The new battery plant that SolarEdge was building in South Korea would be named "Sella 2" and "there will be many more Sellas in the future," a senior executive at the company said. The company's new manufacturing facility was named in Sella's honor—"Sella 1"—featuring a commemoration wall at its entrance.

For investors, the founder transition introduced a new risk factor. SolarEdge had lost its visionary leader at a moment when it was most vulnerable—in the midst of integrating multiple acquisitions in markets adjacent to its core expertise. Zvi Lando, while an experienced sales executive, had not been the architect of the diversification strategy he was now charged with executing.

VIII. The Pandemic Boom & All-Time High (2020-2021)

Just as SolarEdge was navigating its leadership transition, a perfect storm of favorable conditions was building that would propel the stock to unimaginable heights.

The COVID-19 pandemic, paradoxically, proved to be a catalyst for residential solar adoption. Homeowners stuck at home had both the time to consider solar installations and the motivation—as electricity bills rose from increased home usage. Interest rates collapsed to near zero, making solar financing more attractive than ever. And the climate narrative reached new heights of public attention, driving demand from environmentally conscious consumers.

SolarEdge went public on Nasdaq in 2015 with a market value of $620 million. Before joining the S&P 500 in late 2021, it reached $19 billion, peaking near $20 billion shortly thereafter.

The market value of SolarEdge approached $20 billion—making it the Israeli company with the highest market cap at the time. S&P Dow Jones Indices announced changes effective prior to the open of trading on Monday, December 20, 2021: S&P MidCap 400 constituents Signature Bank, SolarEdge Technologies Inc., and FactSet Research Systems Inc. moved to the S&P 500.

The removal comes only two years after SolarEdge made its way onto the world's most-watched index of the 500 largest companies, joining the likes of multinationals such as Apple, Microsoft, Meta (Facebook), Amazon and Tesla. When SolarEdge joined S&P 500 in 2021, it had a market cap of $16 billion and was considered among the most valuable Israeli companies, alongside NICE Systems and cybersecurity giant Check Point Software Technologies.

The company became the first and only Israeli company in the S&P 500 index—a milestone that brought both prestige and new investor attention. The stock rocketed from its $18 IPO price to an all-time high of $368.33 on November 15, 2021—a 20x return that vindicated early believers in the SolarEdge story.

Europe's energy crisis following Russia's invasion of Ukraine in early 2022 added fuel to the fire. European consumers, facing soaring electricity prices due to natural gas supply disruptions, rushed to install solar systems. SolarEdge, with its strong European distribution network, saw orders surge.

But the Ukraine-driven demand contained the seeds of SolarEdge's future troubles. Distributors, fearful of future shortages, stockpiled inventory far in excess of actual installation demand. This created a "bullwhip effect"—the distortion of demand signals as they travel up a supply chain—that would haunt the company for years.

IX. The Competitive Landscape: SolarEdge vs. Enphase

Throughout SolarEdge's rise and fall, one competitor has remained the constant benchmark: Enphase Energy. Understanding the SolarEdge-Enphase rivalry illuminates both companies' strategic positioning and explains some of SolarEdge's current challenges.

SolarEdge and Enphase are the two biggest companies in the solar inverter space. Between them, they dominate the category, especially in the U.S.—a duopoly dynamic that shapes installer loyalty, pricing, and product expectations across the industry.

The difference between Enphase and SolarEdge is the point in the system where the conversion happens. Enphase uses microinverters, which sit behind each solar panel and have a few functions: maximum power point tracking, DC/AC conversion, communication, and rapid shutdown. First, the microinverters detect the output of the solar panel and determine the exact mix of voltage and current that will produce the most power.

SolarEdge uses a string inverter with power optimizers. Like microinverters, power optimizers are located behind each panel and perform a few functions. Power optimizers do the MPPT tracking and communicating with the main inverter and also act as rapid shutdown devices. Unlike Enphase's microinverters, SolarEdge's power optimizers do not perform the DC-to-AC conversion. Instead, DC power is sent to the main inverter box, where it is converted to AC.

The analogy often used by industry observers: Enphase is like a Mercedes—a high-end machine with all the bells and whistles—while SolarEdge is more like a Toyota—more affordable, but with enough bells and whistles to set it apart.

In general, industry experts recommend Enphase products over SolarEdge, because more installers trust them, they are more user-friendly for owners, and they come with better warranty protection. But there are a few reasons to choose SolarEdge, especially for installations that include a battery.

More solar installers like working with Enphase than SolarEdge. Installers say that Enphase products tend to experience fewer failures than SolarEdge. Surveys of solar installers show that more companies use Enphase, and more of them complain about problems with SolarEdge. On top of that, if one fails, you'll only be down a couple of kilowatt-hours a day, whereas if a SolarEdge inverter fails, your whole system goes down.

This installer sentiment represents a significant competitive challenge. In the fragmented residential solar market, installers are the gatekeepers—their recommendations drive consumer choices. However, recently, SolarEdge has had a noticeable increase in reliability concerns. Their latest products, while robust and comparable in theory, do not always function as intended. This creates big issues for consumers in the long run whose solar array should last them up to 20-25 years.

Tesla's gains have come at the expense of established players. Enphase's market share fell from 55% in 2023 to 47% in 2024. In Q4 2024, Enphase's market share dipped below 40% for the first time since Q2 2020. The SunPower bankruptcy and competition from Powerwall 3 proved to be strong headwinds for the company.

SolarEdge does retain certain advantages. California's NEM 3.0 regime potentially benefits SolarEdge because batteries store DC energy, and every time DC is converted to AC or vice versa, a little bit of power gets lost. Since Enphase's microinverters transform DC to AC at the panel level, that electricity has to be converted back to DC to be stored in a battery, then reconverted to AC to be used—three conversions versus one conversion with SolarEdge's system.

SolarEdge does not enjoy the same competitive position in Europe as in the US. This geographic weakness in Europe—historically SolarEdge's largest market—would prove particularly damaging as the European inventory crisis unfolded.

X. The Unraveling: 2023-2024 Crisis

The collapse of SolarEdge's stock price and business performance in 2023-2024 stemmed from a toxic combination of macroeconomic headwinds and company-specific challenges that fed on each other in a vicious cycle.

Companies such as SolarEdge with heavy exposure to the residential solar market have faced a collapse in demand as high interest rates have made installations more expensive for households, leaving the industry buried with too much inventory.

The company's crisis stemmed from two main factors. The first was the increase in interest rates in the U.S., which hurt the economic viability of installing solar systems. For residential solar customers, the economics are highly sensitive to financing costs—a typical solar installation is financed over 15-25 years, so even modest interest rate increases substantially impact monthly payments.

The second factor was the accumulation of product stock in European warehouses following the wave of orders at the onset of the war in Ukraine. In Europe, SolarEdge faced a crisis of excess inventory. This oversupply stemmed from the initial response to the war in Ukraine, during which restrictions on importing natural gas from Russia prompted countries to stockpile alternative energy products. While energy and gas prices subsequently stabilized, the surplus inventory continued to weigh on the company's performance.

SolarEdge's third-quarter 2024 numbers showed the severity of the downturn: revenue fell sharply from the prior year, and even aggressive cost controls couldn't keep pace with the sudden drop in demand and the weight of excess channel inventory.

The third quarter of 2024 results were devastating. A massive loss was driven largely by inventory write-downs—an accounting recognition that products sitting in warehouses were worth less than the company had carried them for. At the same time, sales collapsed while costs moved in the wrong direction, leaving SolarEdge absorbing the worst of both worlds: weaker demand and an expense base that could not be cut fast enough.

In the weeks leading up to the third-quarter report, SolarEdge issued a profit warning that triggered a sharp one-day selloff. Momentum had already turned negative, and the company then compounded the damage by guiding the market to expect a much weaker fourth quarter than analysts had been modeling.

The inventory crisis created a perverse dynamic. Distributors who had over-ordered in 2022-2023 found themselves sitting on warehouses full of SolarEdge products. Rather than placing new orders, they worked through existing inventory—starving SolarEdge of revenue even as underlying installation demand remained relatively stable. CEO Zvi Lando told analysts during SolarEdge's earnings call that the company won't clear its inventory backlog until the end of 2024, though he expects underlying demand to normalize at $600 million to $650 million in the second half of the year.

Since the beginning of 2023, the company's stock has fallen sharply. Two years after making history by becoming the first Israeli company in the S&P 500 index, SolarEdge lost its spot in the prestigious index, underscoring how quickly the market’s view of the business had deteriorated.

XI. The Restructuring: Layoffs, Closures & Leadership Changes

Facing an existential crisis, SolarEdge embarked on a brutal restructuring that touched every aspect of the business—from workforce to leadership to strategic focus.

In January 2024, SolarEdge laid off 900 employees, about 16% of its workforce at the time. A second wave in July cut 400 more jobs, half of them in Israel.

The restructuring extended to the diversification strategy that Guy Sella had championed. SolarEdge announced that, as part of its focus on its core solar activities, it would cease all activities of its Energy Storage division. This decision will result in a workforce reduction of approximately 500 employees, most of whom are in South Korea. Management said the closure was expected to reduce ongoing operating expenses, with the full savings expected to show up over time as the shutdown and wind-down were completed. The Company intends to sell the assets related to the storage division activities including its manufacturing facilities for battery cells and packs.

In 2023, SolarEdge generated $160 million from energy storage, a small fraction of its $2.8 billion solar revenue. The company has implemented three rounds of layoffs this year, reducing its workforce from 5,000 to approximately 3,700 employees.

The energy storage division, built around the 2018 acquisition of South Korean company Kokam for $88 million, primarily focused on large-scale battery cells designed for grid stability. However, Kokam's NMC batteries were not used in SolarEdge's residential energy storage systems, which depend on LFP batteries sourced from other suppliers. As a result, the closure is unlikely to impact SolarEdge's residential operations, its primary revenue driver.

The leadership changes were equally dramatic. The company's leadership is also undergoing significant changes. CEO Zvi Lando stepped down in August but remains a director and consultant. Ronen Faier, previously CFO, was named interim CEO. Chairman Nadav Zafrir also left his role to become CEO of Check Point, although he remains on SolarEdge's board.

Shuki Nir was appointed as the Company's new Chief Executive Officer, effective immediately. Mr. Nir, who has served as SolarEdge's CMO since June 2024, will succeed Mr. Ronen Faier, who has served as the Company's Interim CEO since August 2024.

Mr. Nir is a proven leader within the technology sector, with nearly three decades of experience in leadership roles at multinational technology companies. He was the General Manager of the consumer business at SanDisk (NASDAQ: SNDK), where he led the strategic transformation and turnaround of a loss-making division into a profitable global market leader.

Mr. Nir's extensive tenure includes strategic consulting for multinational corporations and serving on several boards, including IronSource, Kornit Digital, and Oddity.

Nadav Zafrir served as chairman until November 2024, stepping down upon his appointment at Check Point but remaining on the SolarEdge board. He is now leaving that position as well. Nadav Zafrir resigned from SolarEdge's Board on October 2, 2025. The Board reduced its size to seven directors following Zafrir's departure.

The Board elected Avery More as Chairman of the Board of Directors, replacing Nadav Zafrir, who remained on the Board.

XII. The Turnaround Attempt (2024-Present)

Under new leadership, SolarEdge has pivoted to a strategy focused on financial stability, core solar business strength, and leveraging U.S. manufacturing incentives from the Inflation Reduction Act.

The Company signed safe harbor agreements with Sunrun, as well as with one of the largest financers of residential solar installations in the United States. Under the agreements, SolarEdge will provide inverters, Power Optimizers and batteries manufactured at its facilities in the United States, which, when paired with other U.S. made equipment, are expected to enable its partners to qualify for domestic content bonus tax credits.

Section 45X supports the Company's rapid expansion of U.S. manufacturing capabilities, with two facilities now operational and producing inverters and power optimizers. The rule positively impacts SolarEdge's U.S. operations, with the Company now manufacturing from two U.S.-based facilities. The facility in Austin, Texas reached a quarterly manufacturing run rate of 50,000 residential Home Hub Inverters in Q2 2024 and has continued to ramp up production throughout the year. The Tampa, Florida facility began shipping Domestic Content Power Optimizers in Q2 2024 and is expected to reach a production capacity of approximately 2 million per quarter in Q1 2025.

Inverter manufacturer SolarEdge is another company that sold its 2024 45X credits for $40 million. J.B. Lowe, head of SolarEdge investor relations, said 45X credit transfers are another way to cut corporate taxes.

SolarEdge's domestic manufacturing operations have created approximately 2,000 American jobs while ensuring a resilient local supply chain for partners.

CEO Shuki Nir said: "The safe harbor agreements and 45X credit sale announced today are important milestones on our recovery path. They improve visibility into our business outlook, and we believe that they will enhance our cash position, strengthen our balance sheet and further advance our priority of financial stability."

Early results from the turnaround are cautiously encouraging. CEO Shuki Nir stated: "There are exciting opportunities ahead for SolarEdge. We are just getting started on our turnaround story. The return to positive free cash flow generation in Q4 is a solid first step, and we expect to be free cash flow positive in Q1 2025 and for the full year 2025."

In Q3 2025 SolarEdge delivered 44% year over year revenue growth and continued expanding margins for the fourth straight quarter. "We're making steady progress in our turnaround, with three consecutive quarters of revenue growth and improving margins, and we're not done yet," said Shuki Nir, CEO of SolarEdge.

SolarEdge Technologies reported its Q2 2025 financial results, showing signs of recovery with revenues of $289.41 million, up 32% from the previous quarter. The company shipped 1,194 MW of inverters and 247 MWh of batteries for PV applications. GAAP gross margin improved to 11.1% from 8.0% in Q1, while non-GAAP gross margin reached 13.1%. The company reported a GAAP net loss of $124.7 million. For Q3 2025, SolarEdge expects revenues between $315-355 million with non-GAAP gross margins of 15-19%.

The company is also exploring new market opportunities. SolarEdge announced a collaboration with Infineon to advance its Solid State Transformer platform for the data centers of the future. This has the potential to strategically expand our core technology into the data center market, positioning us to help build smarter, more efficient energy systems for the AI era.

Can SolarEdge ride the IRA tailwinds to recovery? The Inflation Reduction Act provides meaningful support—the 45X manufacturing credits help offset the cost disadvantage of U.S. production, while domestic content bonuses make U.S.-manufactured equipment more attractive to customers. But the macro environment remains challenging, with interest rates still elevated and political uncertainty surrounding the future of clean energy incentives.

XIII. Playbook: Business & Investing Lessons

The SolarEdge story offers several enduring lessons for investors and business strategists.

The Power of Architectural Innovation SolarEdge didn't invent solar, inverters, or power electronics. Instead, the founders found the "Goldilocks zone" between cheap traditional string inverters and expensive microinverters. This architectural innovation—power optimizers that provide panel-level optimization at lower cost than microinverters—created a new product category and established SolarEdge's market position. The lesson: breakthrough value creation often comes not from inventing new technologies but from finding novel architectures that combine existing technologies in superior ways.

The Founder Premium Guy Sella's death in 2019 exposed a critical vulnerability. The diversification strategy—Kokam, SMRE, Gamatronic—reflected his vision of building a clean energy conglomerate. But integrating acquisitions in adjacent markets requires a particular kind of visionary leadership. When Sella died, the company was left executing someone else's strategy, without the architect who understood how all the pieces fit together. The eventual unwinding of most of these acquisitions suggests they never fully achieved their strategic promise.

The Inventory Trap The Ukraine war created what appeared to be a demand surge in European solar. Distributors stockpiled inventory, creating a classic "bullwhip effect" that distorted demand signals up the supply chain. When the inventory needed to be absorbed, SolarEdge faced years of depressed sales even as underlying installation demand remained relatively stable. For investors, this illustrates the danger of confusing channel fill with end-market demand—a distinction that's often visible only in retrospect.

Cyclicality in Clean Energy Despite the secular growth story, residential solar is intensely cyclical and highly sensitive to interest rates. When rates rose sharply in 2022-2023, the economic proposition for solar installations deteriorated dramatically. SolarEdge's dependence on residential solar—and particularly the financed installation market—left it acutely exposed to rate sensitivity. The clean energy narrative doesn't insulate companies from macro headwinds.

Diversification vs. Focus The acquisitions of Kokam, SMRE, and Gamatronic raised SolarEdge's growth optionality on paper but distracted management attention and capital from the core business. When the crisis hit, the company was forced to shed these businesses anyway—but only after years of integration effort and significant write-offs. Sometimes focus is more valuable than optionality.

The S&P 500 Curse SolarEdge's addition to the S&P 500 in December 2021 coincided almost exactly with its peak market capitalization. Two years later, it was removed from the index at a fraction of that valuation. For investors, index inclusion often signals that a growth stock's "discovery phase" is over—the easy money has been made, and future returns will depend on continued operational excellence rather than multiple expansion.

XIV. Competitive Analysis: Porter's Five Forces

Threat of New Entrants: MODERATE-HIGH The solar inverter market has relatively low barriers to entry for basic technology. Top competitors now include Enphase Energy, APsystems, and Chinese manufacturers like Deye Inverter. Chinese competitors are increasingly competitive on price. However, the software and monitoring ecosystem creates switching costs that provide some protection for incumbents. The regulatory complexity around safety standards (like rapid shutdown requirements) also creates modest barriers.

Bargaining Power of Suppliers: MODERATE Semiconductor supply chain constraints during COVID highlighted SolarEdge's vulnerability to component shortages. The manufacturing partnership with Flex reduces fixed cost risk and provides supply chain flexibility. With the Kokam closure, battery cell sourcing is now simplified—the company sources LFP batteries from third parties rather than relying on internal NMC production.

Bargaining Power of Buyers: HIGH SolarEdge's customers are highly concentrated. Among its largest customers are SolarCity, SunRun, and Vivint Solar, which provide solar power systems to residential and commercial end users. This concentrated installer base has significant negotiating leverage. The price-sensitive residential market forces continuous cost reductions, limiting pricing power.

Threat of Substitutes: MODERATE Traditional string inverters remain a cheaper alternative for simple installations. Microinverters (Enphase) appeal to the premium segment willing to pay for maximum optimization. Integrated solutions from Tesla—particularly the Powerwall 3 with built-in inverter—bypass the standalone inverter market entirely, representing a structural threat.

Competitive Rivalry: HIGH SolarEdge does not enjoy the same competitive position in Europe as it does in the US. Enphase commands premium positioning with better installer satisfaction. Chinese manufacturers are gaining share on price. Technology differentiation is narrowing over time as competitors develop their own optimization solutions.

XV. Strategic Power Analysis: Hamilton's 7 Powers Framework

Scale Economies: MODERATE Manufacturing scale provides cost advantages, and SolarEdge did establish the DC power optimizer segment with dominant market share. However, scale hasn't prevented margin compression during the downturn, suggesting these economies are insufficient to maintain pricing power in cyclical downturns.

Network Effects: LOW-MODERATE The monitoring platform creates a data moat—SolarEdge has visibility into the performance of millions of installed systems. The installer ecosystem creates some switching costs through training and certification programs. But this isn't a true network effect business where each additional user makes the product more valuable for existing users.

Counter-Positioning: ERODED The original power optimizer architecture was brilliant counter-positioning versus traditional string inverters—incumbents couldn't respond without cannibalizing their existing product lines. But Enphase's microinverter approach has proven equally valid, perhaps superior in installer preference terms. Neither side can claim definitive technological superiority, and Chinese competitors are rapidly closing the gap.

Switching Costs: MODERATE The cloud monitoring platform creates some lock-in—installers and homeowners become accustomed to the SolarEdge app and interface. Installer training and certification programs create modest switching friction. But hardware is relatively commoditized at the component level—installers can switch brands for new installations without massive retraining costs.

Branding: MODERATE SolarEdge has strong brand recognition among solar installers. However, brand perception has suffered during the crisis years, with reliability concerns emerging in installer surveys. The Enphase brand appears to command a premium positioning that SolarEdge lacks.

Cornered Resource: WEAK The talented founding team has departed—through death, resignation, or transition to other roles. Israeli engineering talent remains an asset, but no unique patents or resources provide lasting competitive advantages that cannot be replicated. The Unit 8200 alumni network provides access to talent, but this isn't exclusive to SolarEdge.

Process Power: MODERATE This innovative approach has captured a significant portion of the global solar inverter market, with over 52.6 GW of SolarEdge inverters shipped globally and more than 3.7 million installations worldwide as of 2025. SolarEdge developed unique Power Optimizers, all-in-one inverters, and specialized solutions addressing specific residential and commercial market needs. The vertical integration of hardware, software, and monitoring creates some process complexity that's hard to replicate. But execution has faltered during the crisis period, and process power erodes when operational excellence declines.

XVI. Key Performance Indicators for Ongoing Monitoring

For investors tracking SolarEdge's ongoing performance, three KPIs merit particular attention:

1. Megawatts (MW) Shipped Per Quarter This measures actual unit volume flowing to customers and provides the clearest signal of underlying demand. During the crisis, MW shipped collapsed from peak levels as channel inventory was absorbed. Recovery will manifest first in stabilizing, then growing MW shipments. Investors should compare MW shipped against installation data from industry sources (Wood Mackenzie, SEIA) to assess whether SolarEdge is gaining or losing market share.

2. Gross Margin Trajectory Gross margin reflects both pricing power and cost structure. During the crisis, margins compressed dramatically due to pricing pressure, underutilized manufacturing capacity, and inventory write-downs. Recovery requires margin expansion, which will come from some combination of improved pricing, manufacturing efficiency, and 45X tax credit benefits. Management has guided for improving margins in 2025; tracking quarterly progress against this guidance will indicate turnaround success.

3. Free Cash Flow The results were mixed: despite deep losses, the company reported positive cash flow—an important psychological and financial milestone after a long cash-burn stretch. After burning cash through the crisis period, return to positive free cash flow represents a critical milestone. SolarEdge has indicated expectations for positive free cash flow in 2025. This metric matters because it determines whether the company can self-fund operations, reduce debt, and invest in growth without additional dilutive capital raises.

XVII. Legal and Regulatory Considerations

Investors should note several material legal and regulatory factors affecting SolarEdge:

Securities Litigation The steep stock price decline triggered securities class action lawsuits from shareholder plaintiffs. Law firms have been investigating potential claims on behalf of SolarEdge shareholders. While the outcome of such litigation is uncertain, it represents a contingent liability and management distraction.

Policy Uncertainty The Inflation Reduction Act's 45X manufacturing credits provide meaningful support for SolarEdge's U.S. manufacturing operations. However, the future of the 45X credit remains uncertain under the new Trump administration, which is expected to prioritize oil and gas interests. Some members of Congress have proposed restrictions on 45X eligibility for companies with ties to China, which could impact certain manufacturers.

Net Metering Changes California's transition from NEM 2.0 to NEM 3.0 significantly changed the economics of residential solar in the state. While SolarEdge's DC-coupled battery solution may be advantaged under NEM 3.0 (which encourages self-consumption rather than grid export), the overall impact of policy changes on residential solar demand remains a material uncertainty.

European Political Shifts Europe's shifting political landscape also poses risks. In the Netherlands, a new government less supportive of renewable energy has led to stagnation in the solar market. Germany could face similar challenges with upcoming elections and the declining influence of the Greens in parliament. If the Greens are excluded from the coalition, it could harm Germany's solar market, mirroring the Netherlands' experience.

XVIII. Conclusion: A Fight for Survival

SolarEdge's story arc—from intelligence veterans sketching inverter diagrams in Herzliya to a $20 billion market cap to a 95% collapse—contains multitudes. It's a story of brilliant architectural innovation that created an entirely new product category. It's a tragedy of a visionary founder taken too soon, leaving an ambitious diversification strategy for successors to execute. It's a cautionary tale about inventory cycles, interest rate sensitivity, and the dangers of mistaking channel fill for end-market demand.

The stock remained down roughly 90% over the past several years.

The company that solved solar's "Christmas lights problem" now faces its own crisis of illumination. Under new CEO Shuki Nir, SolarEdge has returned to basics—focusing on the core solar business, leveraging U.S. manufacturing incentives, and rebuilding financial stability. "I'm proud of the steady progress we made in turning SolarEdge around this quarter," said Shuki Nir. "This was our second consecutive quarter of year-over-year and sequential revenue growth, along with margin expansion."

The early turnaround signs are encouraging—three consecutive quarters of revenue growth, improving margins, return to positive free cash flow. But significant challenges remain. The competitive landscape has intensified, with Enphase maintaining premium positioning and Tesla's Powerwall 3 disrupting the market structure. Interest rates, while lower than 2023 peaks, remain elevated relative to the zero-rate environment that fueled the 2020-2021 boom. Political uncertainty around clean energy incentives adds another layer of risk.

For investors, SolarEdge represents a high-risk, high-uncertainty situation. Wall Street analysts, on balance, have remained skeptical, and the wide range of price targets underscored how uncertain the turnaround path still looked.

Morningstar does not assign SolarEdge a moat, as they don't have enough confidence that its excess profits will last beyond 10 years, the threshold to justify a narrow moat rating.

The SolarEdge saga isn't over. Whether the company can recapture its former glory—or even stabilize at a fraction of its peak—depends on execution under new leadership, macro conditions largely beyond management's control, and the broader trajectory of residential solar adoption. What's certain is that the story offers enduring lessons about innovation, founder dependence, diversification risk, and the unforgiving nature of cyclical industries—lessons that will resonate long after the current crisis resolves, one way or another.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube