ScanSource Inc.: The Story of Tech Distribution's Quiet Giant

Introduction and Episode Roadmap

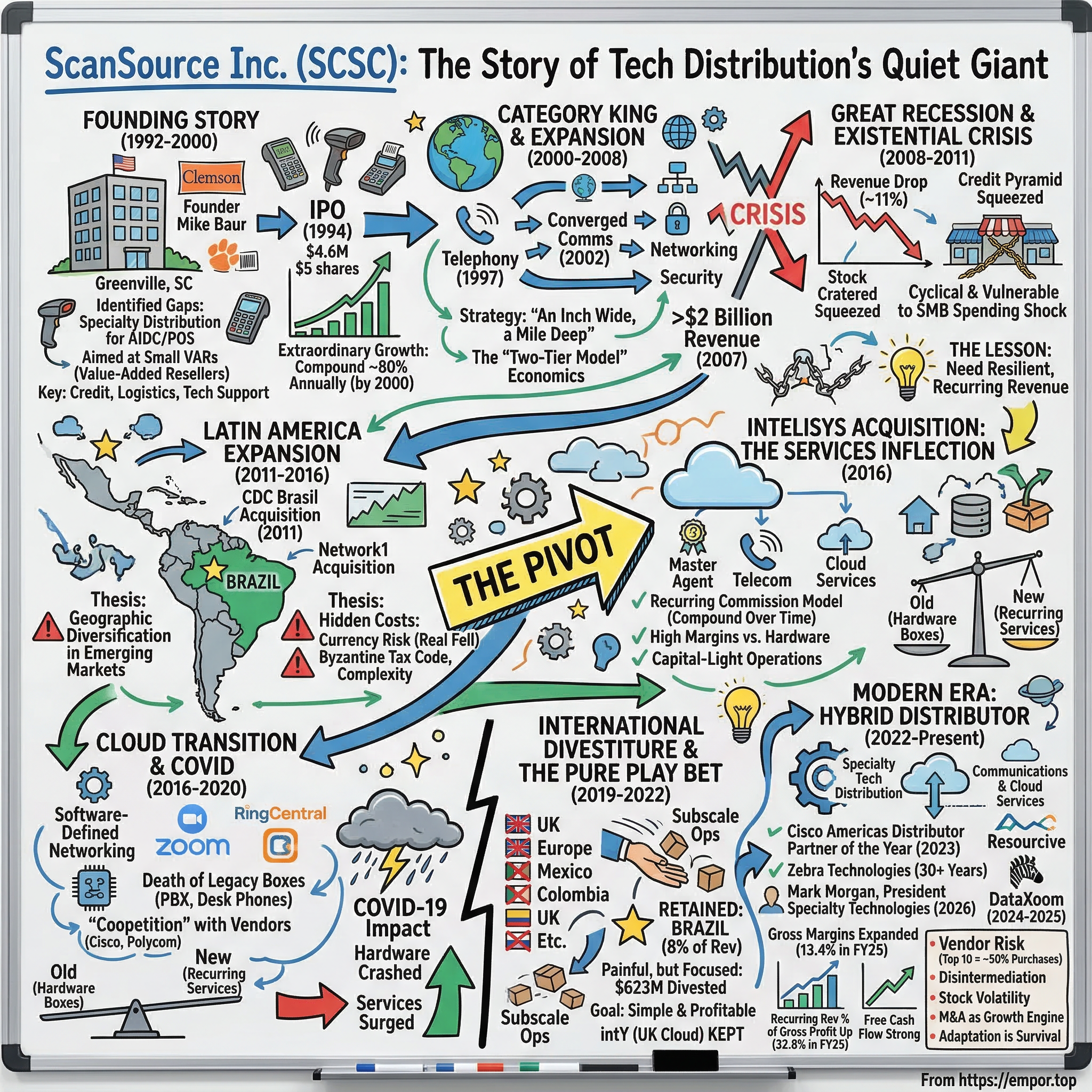

There is a company headquartered in Greenville, South Carolina, that most people have never heard of, yet it quietly touches the daily lives of millions. Every time a cashier scans a barcode at a grocery store, every time a warehouse worker picks up a handheld scanner to track inventory, every time a small business plugs in a video conferencing system for a Monday morning meeting, there is a reasonable chance that the hardware traveled through a distribution center run by ScanSource Inc. With over three billion dollars in annual revenue, ScanSource sits at the unglamorous but essential intersection of technology manufacturers and the thousands of small resellers who actually deploy that technology in the real world.

The central puzzle of ScanSource is deceptively simple: in an era when Amazon delivers anything to your door in twenty-four hours, when manufacturers increasingly want to sell directly to customers, and when cloud computing is replacing physical hardware at an accelerating pace, why does a company whose original business was distributing barcode scanners not only still exist but remain a publicly traded, cash-generating enterprise more than three decades after its founding?

The answer involves one of the most underappreciated dynamics in technology: the middleman's dilemma. ScanSource has spent its entire existence navigating the tension between adding enough value to justify its position in the supply chain and the relentless forces of disintermediation that threaten to eliminate that position entirely. It is a story of a founder who saw a gap in the market that bigger players ignored, built a specialty distribution powerhouse, survived multiple near-death experiences, and then attempted one of the most ambitious strategic pivots in the industry, transforming from a transactional hardware mover to a hybrid platform that combines physical distribution with recurring cloud services revenue.

The three inflection points that define ScanSource's trajectory are the 2016 acquisition of Intelisys, a master agent for telecom and cloud services that fundamentally altered the company's revenue model; the wrenching decision to divest its international hardware distribution operations in 2019 and 2020, shrinking the company to refocus it; and the ongoing cloud transition that threatens to make some of ScanSource's legacy categories obsolete while opening new ones. Each of these moments forced the company's leadership to answer the same existential question: what is a distributor actually for?

The themes running through this story are universal. The middleman's dilemma applies to any business that sits between producers and consumers. The specialty-versus-broadline debate is relevant to any company choosing between being a generalist or a specialist. And the challenge of navigating technological obsolescence while your core business still generates the cash flow you need to fund your transformation is perhaps the defining strategic challenge of our era.

Founding Story and The Barcode Revolution, 1992 to 2000

Picture Greenville, South Carolina, in the early 1990s. The textile mills that once defined the Upstate economy were closing, but a new identity was forming. BMW had just announced its first American manufacturing plant twenty miles away in Spartanburg. The region was cheap, centrally located on the Eastern Seaboard, and hungry for new business. It was exactly the kind of place where a scrappy startup could stretch a dollar.

Mike Baur did not set out to become a technology distributor. Born in 1957 in nearby Anderson, South Carolina, he studied chemical engineering at Clemson University, interviewing with companies like Dow Chemical before concluding that the field was, in his words, "painfully boring." Through a personal connection, his sister's boyfriend who knew the CEO, Baur landed at Gates/FA Distributing Inc., a Greenville-based distributor, in 1989. There, working as a product manager for AST, a PC maker later acquired by Samsung, he got a front-row education in the distribution business. He learned how the economics worked, where the margins lived, and crucially, where the gaps were.

The gap Baur identified was specific and overlooked. In the early 1990s, the barcode revolution was just beginning to transform retail, manufacturing, and logistics. Companies like Symbol Technologies were producing increasingly sophisticated scanners and mobile computing devices, but the distribution infrastructure to get those products into the hands of the small Value-Added Resellers who actually installed and serviced them was woefully underdeveloped. The big broadline distributors like Ingram Micro and Tech Data focused on PCs and peripherals, where the volumes were massive. They had little interest in the relatively niche world of Automatic Identification and Data Capture, known in the industry as AIDC. The VARs serving this market, small companies with maybe five to twenty employees who sold and supported barcode systems for local businesses, could not get the attention, the credit terms, or the technical support they needed from the big players.

In December 1992, Baur and Steve Owings, the CEO of Gates/FA, incorporated ScanSource as a joint venture. The company launched with roughly six employees and a simple value proposition: be the specialty distributor that VARs for barcode and POS equipment actually wanted to work with. This meant offering three things the big distributors would not bother with for such a niche market: generous credit terms so small resellers could finance their inventory, fast and reliable logistics so equipment arrived when promised, and deep technical support so VARs could actually troubleshoot and install increasingly complex systems.

The early years were a grind. In its first seven months, ScanSource lost $243,000 on just $2.4 million in sales. But the model worked. In the following six months, the company eked out a $65,000 profit on $6.5 million in sales. By fiscal year 1994, revenues had reached $16.1 million with $352,000 in profit. The company initially represented about twenty vendors, including Symbol Technologies, Fargo Electronics, and Star Micronics, names that meant nothing to consumers but everything to the small businesses deploying barcode systems in warehouses and retail stores across America.

The IPO came remarkably early. On March 18, 1994, ScanSource went public, raising $4.6 million with shares priced at approximately five dollars. The stock nearly tripled to fourteen dollars within months. In July 1994, ScanSource severed its partnership with Gates/FA, receiving $1.4 million in compensation and gaining full independence. What followed was extraordinary growth. Revenue hit $74.6 million by fiscal 1996, then $131 million in 1997, and an astonishing $572 million by the turn of the millennium. The company was compounding at nearly eighty percent annually, riding the barcode revolution as retailers, manufacturers, and logistics companies across America automated their operations.

The playbook Baur established in those early years would define ScanSource for decades. The company was not trying to compete with the broadline distributors on volume or price. It was building what amounted to a service business wrapped around a distribution business. Credit, logistics, and technical support were the competitive advantages, not scale. The VARs who bought from ScanSource were not just buying boxes of scanners. They were buying a relationship with a distributor that understood their business, extended them credit when they needed it, and could help them troubleshoot a complex installation at a customer site. In an era when Circuit City and CompUSA were thriving by selling consumer electronics directly, ScanSource's bet on the unglamorous B2B channel seemed almost quaint. But it was building something those consumer retailers never had: sticky, relationship-driven revenue with high switching costs for its customers.

The Broadline Expansion and Category King Strategy, 2000 to 2008

The dot-com crash of 2000 and 2001 was the first real test of whether ScanSource's model could survive a downturn. Technology spending cratered. The NASDAQ lost nearly eighty percent of its value. Companies that had been racing to digitize their operations suddenly froze their budgets. But ScanSource's customer base, the small VARs serving local businesses with barcode and POS equipment, proved more resilient than the venture-backed startups and enterprise software companies that dominated the headlines. Businesses still needed to scan inventory and process transactions at the point of sale. The spending slowdown was real, but it was not an extinction event.

What it did do was clarify the strategic question facing Mike Baur: could ScanSource grow by staying exclusively in AIDC and POS, or did it need to expand into adjacent categories? The answer, which would shape the next decade, was expansion, but with a crucial twist. Rather than becoming a broadline distributor trying to compete with Ingram Micro and Tech Data across every product category, ScanSource would pursue what might be called a "category king" strategy. The company would enter new technology verticals one at a time, applying the same specialty distribution playbook, deep expertise, credit, logistics, technical support, to each new category. The philosophy, as Baur described it, was "an inch wide, a mile deep."

The expansion began with telephony. In 1997, ScanSource acquired ProCom Supply, a telephony distributor, and created the Catalyst Telecom division. This was not a random diversification. Enterprise telephony, the desk phones, PBX systems, and voice infrastructure that businesses relied on, was distributed through a channel that looked remarkably similar to the barcode world. Small VARs installed and maintained phone systems for local businesses, and they needed a distributor that understood the technology and could extend credit. Catalyst Telecom applied the ScanSource playbook to telephony and grew rapidly.

The acquisition engine accelerated. POS ProVisions in Canada came in 1997 for $4.3 million in stock, giving ScanSource its first international footprint. The CTI Authority followed in 1998, adding $8 million in annual sales and expanding the telephony business. By 2001, ScanSource had acquired a fifty-two percent stake in Netpoint International, a Miami-based distributor serving Latin America, opening the door to geographic expansion beyond North America. A year later, the company acquired ABC in the United Kingdom, establishing European operations with a warehouse and sales office in Belgium.

New product categories kept coming. POS terminals, video security, networking equipment, and converged communications all got the ScanSource treatment. In 2002, the company created the Paracon sales unit internally to address the converged communications market. Each new category was entered the same way: hire people who understood the technology, build relationships with the key vendors, and offer VARs the same credit-logistics-support trifecta that had worked in barcode.

The two-tier distribution model was central to everything ScanSource did, and it is worth pausing to explain why. In technology distribution, the "two-tier" model means manufacturers sell to distributors, who sell to VARs, who sell to end customers. The obvious question is: why not cut out the middleman? Why does not Cisco or Zebra just sell directly to the small reseller in Des Moines? The answer is economics. A manufacturer like Zebra might have thousands of small resellers buying its products. Managing credit, shipping, returns, technical support, and marketing for each of those small accounts is expensive and distracting. It is far more efficient to sell in bulk to a distributor like ScanSource, which then handles all of those downstream relationships. For the VAR, the value proposition is equally clear: rather than maintaining separate accounts with dozens of manufacturers, each with different ordering systems, credit terms, and support structures, the VAR can buy everything from one or two distributors who aggregate the whole portfolio.

By fiscal 2007, ScanSource had crossed the two billion dollar revenue mark. Revenue reached $2.12 billion that year, and the stock was trading in the mid-thirties. The company had successfully executed its category expansion strategy, transforming from a barcode distributor into a multi-category specialty technology distributor while maintaining the focused, expertise-driven approach that differentiated it from the broadline giants. The pre-recession ScanSource was a company firing on all cylinders, with a diversified product portfolio, growing international operations, and a proven acquisition playbook. What the company could not know was that the world was about to change in ways that would test every assumption underpinning its business model.

The Great Recession and Existential Crisis, 2008 to 2011

The 2008 financial crisis hit ScanSource where it lived: the small and mid-sized business economy. The company's customers were not Fortune 500 enterprises with deep balance sheets and committed IT budgets. They were the local VARs who sold barcode scanners to regional retailers, installed phone systems for law offices, and set up security cameras for strip malls. When the credit markets froze and consumer spending collapsed, those end customers stopped buying. And when end customers stopped buying, VARs stopped ordering from ScanSource.

Revenue dropped from $2.08 billion in fiscal 2008 to $1.86 billion in fiscal 2009, a decline of roughly eleven percent. The stock cratered, falling from the mid-thirties to the low teens, a drop of more than fifty percent. But the revenue decline, while painful, was not the real crisis. The real crisis was the credit squeeze. ScanSource's business model depended on extending credit to small VARs, essentially financing their inventory so they could fulfill orders and pay ScanSource back after collecting from their own customers. When end customers stopped paying VARs, and VARs could not pay ScanSource, the entire credit pyramid threatened to collapse. Simultaneously, vendors were tightening their own payment terms, creating a cash flow vise that squeezed distributors from both sides.

Mike Baur's response was measured. He cut costs, reducing headcount and trimming operating expenses, but he deliberately avoided cutting what he called "muscle," the technical support staff, vendor relationship managers, and logistics capabilities that differentiated ScanSource from cheaper alternatives. This was a bet that the recession would end, and when it did, customers would remember which distributors had maintained service quality through the downturn. It was also an acknowledgment of a deeper truth: in a commodity business, the moment you cut the things that make you special, you have nothing left to sell but price.

The recovery was agonizingly slow. SMB spending remained depressed well into 2010 and 2011, and ScanSource's revenue did not regain its pre-recession peak until fiscal 2010, when sales bounced back to $2.39 billion, partly driven by pent-up demand. But the recession planted a seed that would grow into the company's most important strategic decision. The core lesson was that ScanSource was deeply cyclical, utterly dependent on SMB hardware spending, and vulnerable to any shock that disrupted the credit chain connecting manufacturers, distributors, VARs, and end customers. If the company wanted to survive the next crisis, it needed revenue streams that were more resilient, more recurring, and less tied to the transactional sale of physical hardware.

The recession also surfaced the existential question that haunts every distribution company: is distribution itself becoming obsolete? As e-commerce grew, as manufacturers built their own online ordering platforms, as logistics companies like Amazon demonstrated that you could ship anything anywhere for next to nothing, the traditional value proposition of the distributor, aggregation, credit, logistics, was being commoditized. ScanSource survived the recession because of its balance sheet strength, its vendor relationships, and its expertise in specialty categories. But survival was not the same as thriving, and the strategic imperative for the next decade was clear: find new sources of value or face a slow fade into irrelevance.

International Expansion and The Brazil Bet, 2011 to 2016

If the recession taught ScanSource that it needed diversification, the question was what kind. The first answer, which seemed logical at the time, was geographic diversification. The thesis was straightforward: emerging markets, particularly Latin America, had a growing middle class, underdeveloped distribution infrastructure, and increasing demand for the same barcode, POS, and communications technology that ScanSource distributed in North America. If the company could replicate its model in Brazil, Mexico, Colombia, and other markets, it would reduce its dependence on the North American economic cycle.

The marquee move was the 2011 acquisition of CDC Brasil, the leading AIDC and POS distributor in Brazil, for an initial price of roughly $35 million with earn-outs that could bring the total to approximately $64 million. CDC had about $140 million in annual revenue and an established network of Brazilian VARs. The deal made ScanSource a meaningful player in Latin America's largest economy, a country with over two hundred million people and a rapidly modernizing retail and logistics infrastructure.

Three years later, ScanSource doubled down with the acquisition of Network1, Brazil's leading communications value-added distributor. The initial price was approximately $60 million in US dollars, with additional earn-outs tied to performance. Network1 was a substantial business, with roughly $374 million in revenue and four hundred employees across Brazil, Mexico, Colombia, Chile, and Peru. The acquisition gave ScanSource a major presence in Latin American communications distribution and pushed the company's non-US revenue to approximately ten percent of the total.

On paper, the Latin American expansion made strategic sense. In practice, it was a masterclass in the hidden costs of geographic diversification. The complexity multiplier was enormous. Each country had different tax regimes, regulatory requirements, and vendor relationships. The Brazilian tax code alone is legendarily Byzantine, with cascading federal, state, and municipal levies that can consume enormous management attention. Currency risk turned out to be the most painful variable. The Brazilian real, which had been relatively stable against the dollar during the early 2010s, went into freefall starting in 2014 as commodity prices collapsed and Brazil's economy entered its worst recession in a century. Revenue denominated in reais could grow handsomely in local currency terms while shrinking when translated back to US dollars for ScanSource's consolidated financial statements.

The Brazil experience exposed a fundamental challenge of international distribution: the margins were different, the risks were different, and the management bandwidth required was far greater than simply replicating a domestic playbook overseas. ScanSource was simultaneously trying to manage currency hedging, navigate local labor laws, maintain vendor relationships that operated differently in each country, and integrate acquired companies with their own cultures and systems. For a company headquartered in Greenville, South Carolina, with a total employee count of a few thousand people, the cognitive and operational load of managing a multi-country Latin American business was significant.

The Brazil bet was not a failure in the traditional sense, as the operations generated revenue and served real customers, but it consumed management attention and capital that might have been more productively deployed elsewhere. It was also a precursor to the more dramatic strategic decision that would come a few years later, when ScanSource would conclude that geographic diversification through hardware distribution was not the path to long-term value creation. The real opportunity, it turned out, was not in distributing the same kinds of products in more places, but in distributing fundamentally different kinds of products and services.

The Intelisys Acquisition: The Services Inflection, 2016

If there is a single moment that divides ScanSource's history into "before" and "after," it is the announcement in September 2016 that the company would acquire Intelisys Communications for an initial price of $83.6 million in cash, with additional earn-out payments tied to EBITDA performance over four years that would ultimately bring the total consideration to something in the range of $180 to $230 million. It was, by a significant margin, the most transformative deal in ScanSource's history, and it represented a fundamental bet on the future of distribution itself.

To understand why the Intelisys deal mattered so much, you first need to understand what a master agent is, because it is one of those concepts that sounds simple but contains multitudes. In the telecommunications and cloud services industry, a master agent acts as an intermediary between service providers, think carriers like AT&T, Comcast, and cloud providers like Microsoft and RingCentral, and a network of independent sales agents who sell those services to businesses. The master agent does not sell directly to end customers. Instead, it recruits, trains, and supports a nationwide network of independent agents, providing them with tools, quoting engines, and back-office support to sell telecom and cloud services. When an agent closes a deal, the service provider pays the master agent a commission, and the master agent shares a portion of that commission with the agent. Critically, these commissions are recurring. As long as the end customer keeps paying their monthly bill, the commissions keep flowing.

At the time of the acquisition, Intelisys had roughly 2,400 sales partners, more than 130 supplier partners, and was generating approximately $120 million in gross commissions with about $34 million in net revenue and EBITDA margins in the forty-five to fifty percent range. The business was growing at double digits and employed only about 120 people. Compare that to ScanSource's core distribution business, which required massive warehouses, thousands of employees, and hundreds of millions of dollars in inventory to generate single-digit operating margins on billions in revenue. Intelisys was, in every financial dimension, a fundamentally superior business model.

The strategic logic was compelling but risky. On the compelling side, Intelisys offered exactly what ScanSource's core business lacked: recurring revenue, high margins, and capital-light operations. Hardware distribution is transactional: you buy a scanner from Zebra, sell it to a VAR, book the revenue, and the relationship resets. Master agent commissions, by contrast, compound. Every new customer an agent signs generates a stream of monthly commissions that can persist for years. Over time, the base of recurring commissions grows like a snowball rolling downhill. The "death of the box" thesis that was gaining traction in the industry, the idea that physical hardware was commoditizing while services and cloud solutions were where the value was migrating, made Intelisys look like the future.

On the risky side, Intelisys was a completely different business from anything ScanSource had ever operated. Different customers, different vendor relationships, different skills, different culture. Hardware distribution is about logistics, credit, and inventory management. Master agent operations are about sales enablement, partner recruitment, and platform technology. The people who excelled at running warehouses and managing credit lines were not the same people who excelled at recruiting independent sales agents and building cloud quoting tools. Wall Street was initially skeptical, viewing the acquisition as a distraction from ScanSource's core competency.

The proof came in the numbers. Intelisys grew consistently after the acquisition, expanding its partner network, adding new supplier relationships, and increasing its contribution to ScanSource's gross profit. By fiscal year 2025, recurring revenue accounted for 32.8 percent of ScanSource's gross profit, up from 27.5 percent, with Intelisys as the primary driver. The final earn-out payment was delivered in October 2020, and by any reasonable measure, the deal delivered on its strategic promise. The Intelisys acquisition did not just add a new revenue stream; it changed ScanSource's narrative from "cyclical hardware distributor" to "hybrid distribution platform with growing recurring revenue." That narrative shift, while still a work in progress, is arguably worth more than any single revenue contribution.

The deeper lesson of the Intelisys acquisition is about the courage required to cannibalize your own identity. Mike Baur built ScanSource as a hardware distribution company. His entire career, his expertise, his relationships, his reputation, were all rooted in moving physical products through a supply chain. Buying Intelisys was an admission that the future of distribution lay elsewhere, that the boxes and scanners and phones that had built the company were becoming commodities, and that the real value was in the services flowing through those devices. It takes a particular kind of founder to make that bet, especially when the core business is still generating cash. Many founders cannot bring themselves to do it. Baur did, and it may prove to be the decision that ensures ScanSource's survival for another thirty years.

The Cloud Transition and Death of Legacy Categories, 2016 to 2020

The Intelisys acquisition was ScanSource's answer to a question that the entire technology distribution industry was grappling with: what happens when the products you distribute become obsolete? Starting in the mid-2010s, the cloud transition began systematically dismantling several of ScanSource's most important product categories. Desk phones, the bread and butter of the Catalyst Telecom division, were being replaced by software-based unified communications platforms. On-premise PBX systems were giving way to cloud-hosted voice solutions from companies like RingCentral and Zoom. Traditional networking equipment was being supplemented and sometimes replaced by software-defined networking and cloud-managed solutions. Even POS terminals, one of ScanSource's founding categories, were evolving toward software-based solutions running on tablets and smartphones.

The strategic response was multi-pronged. ScanSource leaned into the categories that were growing, unified communications, security both physical and cyber, and IoT, while slowly pruning the categories that were in structural decline. The company continued its acquisition strategy, adding Network1 in Brazil in the 2014-2015 timeframe to expand its communications distribution capabilities in Latin America, and building out its European presence. The vendor landscape was also shifting in challenging ways. Major manufacturers like Cisco and Polycom were changing their channel strategies, sometimes seeking to sell more directly to larger customers and sometimes restructuring their partner programs in ways that reduced distributor margins. The constant dance between cooperation and competition with vendors, what the industry calls "coopetition," required relentless relationship management and a willingness to adapt when a key vendor changed the rules of the game.

The defense ScanSource mounted against disintermediation was the same one it had deployed since its founding: expertise and service. As products became more complex, as customers needed to integrate hardware, software, and cloud services into unified solutions, the technical support and integration capabilities that ScanSource offered became more valuable, not less. A VAR trying to deploy a hybrid communications system that combined on-premise phones, cloud-based video conferencing, and mobile integration needed a distributor that could help them architect the solution, not just ship the boxes. This was ScanSource's argument for continued relevance: as technology became more complex, the need for a knowledgeable intermediary actually increased.

Then COVID-19 hit, and everything accelerated. The initial impact in March and April 2020 was devastating. Hardware orders froze as businesses closed and uncertainty paralyzed purchasing decisions. But the pandemic almost immediately created explosive demand for exactly the technologies ScanSource was positioned to distribute: video conferencing systems, remote access solutions, cybersecurity tools, and cloud communications platforms. The fiscal year ending June 2020 was a tale of two businesses. Hardware categories crashed as offices emptied and construction projects halted. But the services business, led by Intelisys, surged as businesses scrambled to equip remote workers with the communications and collaboration tools they needed.

The pandemic compressed what might have been a five-year transition into eighteen months. Companies that had been slowly evaluating cloud communications suddenly needed to deploy them immediately. VARs that had been cautiously exploring cloud services suddenly needed to sell them to survive. And ScanSource, which had spent four years integrating Intelisys and building its cloud services capabilities, was positioned to help. The pandemic did not create ScanSource's services strategy, but it validated it in the most dramatic way possible, demonstrating that the recurring revenue streams the company had been building were not just more profitable than hardware sales but also more resilient in a crisis.

The International Divestiture and the Pure Play Bet, 2019 to 2022

In August 2019, a few months before anyone had heard of COVID-19, ScanSource made what was arguably the most painful strategic decision in its history: the announcement that it would divest its hardware distribution businesses outside of the United States, Canada, and Brazil. This meant selling or shutting down operations in the United Kingdom, continental Europe, Mexico, Colombia, Chile, Peru, and its Miami-based export operations. These were businesses that had collectively generated $623 million in net sales in fiscal 2019, representing a significant chunk of ScanSource's total revenue.

The decision was driven by a clear-eyed assessment of where the company could and could not win. The international hardware distribution operations were subscale in most markets, facing fierce competition from larger local and regional distributors, and consuming management bandwidth disproportionate to their contribution to profits. The complexity of managing multiple currencies, tax regimes, regulatory environments, and vendor relationships across a dozen countries was draining resources that could be better deployed in North America and in growing the higher-margin services business. In essence, ScanSource was acknowledging that the geographic diversification strategy of the early 2010s had not produced the returns it needed to justify the complexity and risk.

The execution unfolded over more than a year. In October 2020, the Latin American operations outside Brazil were sold. In November 2020, the European and UK hardware business was sold to Ten Oaks Group, a US-based private equity firm, for approximately thirty million dollars, covering roughly three hundred employees specializing in POS and communications solutions. The financial impact was significant: ScanSource recorded an $88.9 million non-cash loss on the held-for-sale classification and $13.7 million in impairment charges. The fiscal 2020 net loss from discontinued operations was $113.4 million, with an additional $34.6 million loss in fiscal 2021.

Crucially, ScanSource retained two things. First, it kept its Brazilian operations, which remained a meaningful and profitable part of the business. Second, it retained intY, a UK-based cloud business it had acquired in 2019, which aligned with the company's services strategy rather than its hardware distribution legacy. The message was clear: ScanSource was not retreating from international markets entirely, but it was retreating from the business of distributing commodity hardware in markets where it lacked scale and competitive advantages.

Wall Street's reaction was mixed. Some analysts appreciated the strategic clarity, the idea that ScanSource was pruning low-return operations to focus on higher-margin opportunities. Others worried about the revenue hole, the loss of more than half a billion dollars in annual sales that would not be replaced overnight. The stock, already under pressure from the pandemic, reflected this uncertainty.

The portfolio shift accelerated in the years that followed. ScanSource doubled down on its services strategy, with Intelisys contributing an increasingly significant share of gross profit. Share buybacks became a meaningful capital allocation tool, with the diluted share count declining from roughly 25.5 million in fiscal 2021 to approximately 23.8 million by fiscal 2025, a reduction of nearly seven percent that demonstrated management's confidence in the stock's undervaluation. Debt management was equally disciplined: total debt dropped from $343.6 million in fiscal 2023 to $147.1 million by fiscal 2025, with net debt approaching zero.

The new ScanSource that emerged from this period was a smaller but arguably better company. Revenue had come down from the fiscal 2019 peak of $3.87 billion to approximately $3.04 billion in fiscal 2025, but the quality of those earnings had improved markedly. Gross margins expanded from 11.1 percent in fiscal 2021 to 13.4 percent in fiscal 2025, reflecting the shift toward higher-margin services and cloud revenue. The company generated $104 million in free cash flow in fiscal 2025, a free cash flow yield of over ten percent on the current market capitalization. The question that hung over the stock was whether this was a successful transformation or merely the early innings of a slow decline. The answer depended entirely on whether the services business could grow fast enough to offset the structural headwinds facing hardware distribution.

Modern Era: The Hybrid Distributor Play, 2022 to Present

ScanSource in early 2026 is a fundamentally different company from the barcode scanner distributor that Mike Baur founded in 1992, even if the Greenville, South Carolina headquarters and the founder's name on the door remain the same. The company generates approximately three billion dollars in annual revenue across two broad business areas: specialty technology distribution, encompassing enterprise mobile computing, data capture, barcode printing, POS, payments, networking, and physical and cyber security; and communications and cloud services, including unified communications, video conferencing, and the Intelisys master agent platform.

The geographic footprint has been deliberately simplified. After the international divestitures, ScanSource now operates in just three countries: the United States, which accounts for over ninety-two percent of revenue; Canada; and Brazil. The remaining Brazilian operations contribute about eight percent of revenue, down from roughly ten percent in prior years, partly reflecting continued currency headwinds and a smaller Brazilian economy relative to the US.

In fiscal year 2025, ScanSource restructured its reporting to create greater visibility into the services transformation. The new structure separates the Intelisys and Advisory unit, which includes Intelisys, the recently acquired Resourcive technology advisory firm and Advantix managed connectivity provider (acquired together for approximately $57 million in 2024), and the Channel Exchange platform, from the traditional hardware distribution operations. This organizational clarity was a signal to investors that ScanSource viewed its services business as a distinct growth engine deserving of its own strategic identity. In early 2026, Mark Morgan was appointed President of Specialty Technologies, adding another dedicated leader to the hardware side while the services business continued its independent trajectory.

The vendor landscape has evolved considerably. Cisco remains the company's most important vendor partner. ScanSource won the Americas Distributor Partner of the Year award at the Cisco Partner Summit in 2023, underscoring the depth of that relationship. Zebra Technologies, with which ScanSource has maintained a distribution relationship for more than thirty years, remains a key partner in the mobile computing and data capture categories. The supplier portfolio for Intelisys has expanded beyond traditional telecom carriers to include cloud platforms, cybersecurity vendors, and managed services providers, reflecting the broadening definition of what "technology services" means to business customers.

Recent financial performance tells the story of a company in transition. Revenue declined from $3.79 billion in fiscal 2023 to $3.04 billion in fiscal 2025, driven primarily by normalization of pandemic-era hardware demand and ongoing softness in certain legacy categories. But gross margins expanded from 11.9 percent to 13.4 percent over the same period, and the company generated strong free cash flow. The most recent quarterly report, for the second quarter of fiscal 2026 ending December 31, 2025, showed net sales of $766.5 million, up 2.5 percent year-over-year, with gross profit of $102.9 million, up 1.2 percent. These are modest numbers, but they suggest stabilization after two years of declining revenue.

The stock has been volatile. After reaching an all-time high of $53.90 in December 2024, shares declined to approximately $35.84 as of mid-March 2026, a drop of roughly one-third. The decline reflects broader market uncertainty, concerns about the pace of the services transition, and a February 2026 earnings release that showed continued revenue pressure. The stock trades at about 13.7 times trailing earnings, 7.5 times EV/EBITDA, and 1.08 times book value, multiples that suggest the market remains skeptical about the growth trajectory while acknowledging the company's cash generation and asset value.

One notable milestone: in January 2026, ScanSource was named to the Fortune World's Most Admired Companies list for the tenth consecutive year, a recognition that speaks to the company's reputation within the industry even if it remains largely unknown to the broader public. Mike Baur, now sixty-eight years old and still serving as Founder, Chairman, CEO, and President, shows no signs of stepping back. His total compensation in fiscal 2025 was approximately $3.1 million, modest by public company CEO standards and reflective of a founder who is still deeply embedded in the day-to-day operations of the business he built.

Business Model Deep Dive: Why Distributors Still Exist

The most important question any potential investor in ScanSource must answer is deceptively simple: why do technology distributors still exist? In a world where Amazon delivers anything to your doorstep in hours, where manufacturers can reach customers directly through their own websites, and where digital marketplaces eliminate the need for physical intermediaries in an increasing number of industries, the persistence of the two-tier distribution model in technology requires explanation.

The answer starts with working capital. A typical ScanSource customer is a VAR with maybe ten employees and a few million dollars in revenue. That VAR needs to buy equipment from multiple manufacturers, often in advance of receiving payment from its own customers. It does not have the balance sheet to finance large inventory purchases, and individual manufacturers do not want to extend credit to thousands of small resellers they have never met. ScanSource solves this problem by acting as a financial intermediary: it buys inventory from manufacturers using its own capital, extends credit terms to VARs, and manages the credit risk across a diversified portfolio of thousands of customers. In essence, ScanSource is providing working capital as a service, and it is a service that neither manufacturers nor VARs can easily replicate on their own.

The logistics function is equally important but more vulnerable to disruption. ScanSource operates distribution centers that can ship products quickly to VARs across its geographic footprint. But logistics is increasingly commoditized, and the argument that a specialty distributor adds unique value in moving boxes from point A to point B is weaker than it was twenty years ago. Where ScanSource's logistics truly add value is in "kitting," the process of assembling complex multi-vendor solutions, configuring devices, and pre-staging equipment so that a VAR can deploy a complete system at a customer site rather than receiving individual components from multiple manufacturers and assembling them on location.

The technical support function is perhaps the most underappreciated aspect of the distributor value proposition. As technology solutions become more complex, involving the integration of hardware, software, cloud services, and security, the VARs who deploy these solutions need a knowledgeable partner who can help them architect, troubleshoot, and support increasingly sophisticated systems. ScanSource employs technical specialists in each of its product categories who can assist VARs with pre-sales design, post-sales support, and training. This is not something that can be easily replicated by an online marketplace or a manufacturer's call center.

The economics of the business are razor-thin but not unattractive when managed well. ScanSource's gross margins run in the eleven to thirteen percent range, meaning for every hundred dollars of product sold, the company keeps eleven to thirteen dollars after paying the manufacturer. Operating margins are two to three percent, reflecting the cost of the credit, logistics, and technical support infrastructure. These margins look painfully thin compared to a software company, but they are applied to billions of dollars in throughput, and the business is relatively asset-light when measured by return on invested capital. The company's ROIC of approximately six percent, while modest, understates the returns on the more capital-efficient services business.

The specialists-versus-broadliners question is central to ScanSource's positioning. The broadline distributors, now dominated by TD SYNNEX following the 2021 merger of Tech Data and Synnex, operate at vastly larger scale, with TD SYNNEX generating roughly $60 billion in annual revenue. ScanSource is a fraction of that size, but it competes effectively in its specialty niches because it offers deeper expertise, more focused vendor relationships, and more attentive service to small and mid-sized VARs. The trade-off is that ScanSource can never achieve the purchasing leverage or logistics efficiency of a broadliner, which puts a structural ceiling on its margins in commodity product categories.

The services overlay, led by Intelisys, represents ScanSource's attempt to escape the gravitational pull of commodity distribution economics. Master agent commissions have gross margins that are multiples of hardware distribution margins, and the recurring nature of the revenue provides visibility and stability that transactional hardware sales cannot match. The strategic question is whether the services business can grow large enough to fundamentally change ScanSource's economic profile, or whether it will remain a valuable but relatively small complement to a hardware distribution core that faces structural headwinds.

Competitive Landscape and Industry Dynamics

The technology distribution industry has undergone a dramatic consolidation over the past decade, and ScanSource's decision to remain independent while others merged is one of the defining strategic choices of its modern era. The landmark event was the 2021 merger of Tech Data and Synnex to form TD SYNNEX, creating a roughly $60 billion revenue behemoth that dominates broadline technology distribution globally. The merger reflected a widely held industry view that scale is destiny in distribution: larger companies can negotiate better terms with vendors, operate more efficient logistics networks, and spread their fixed costs over a bigger revenue base.

ScanSource chose a different path. Rather than seeking a merger partner to achieve broadline scale, the company bet that specialty distribution, combined with a growing services business, could generate sustainable returns without the disruption and integration risk of a mega-merger. This is a defensible strategy but not without risks. ScanSource is too small to be a broadliner but potentially too large to be as nimble as the smallest specialty distributors. It occupies a middle ground that requires constant demonstration of value to both vendors and customers.

The direct competitive set includes companies like D&H Distributing, a family-owned broadline distributor; Westcon-Comstor, which focuses on security and networking; and Jenne, a smaller specialty distributor. But the more significant competitive threats come from outside the traditional distribution model. Amazon Business has emerged as a formidable competitor, offering an ever-expanding selection of technology products with the logistics efficiency and customer experience that Amazon is known for. CDW, which operates as a direct marketer and solutions provider rather than a traditional two-tier distributor, has grown into a $20 billion-plus business by selling directly to end customers with a consultative approach. And vendors themselves are increasingly building their own marketplaces and direct sales channels, cutting distributors out of the equation for certain products and customer segments.

The vendor relationship dynamic is the most nuanced competitive factor. ScanSource's vendors are simultaneously its most important partners and its most significant competitive threat. A vendor like Cisco depends on ScanSource to reach thousands of small resellers that Cisco cannot efficiently serve directly. But Cisco also has the power to change its channel strategy, adjust distributor margins, or even bypass distributors entirely for certain products or customer segments. The decision by various vendors over the years to restructure their distribution arrangements has been a recurring source of disruption for ScanSource and the entire industry.

The industry is shrinking in aggregate, as disintermediation, margin pressure, and the shift from hardware to cloud services reduce the total addressable market for traditional distribution. The winners' playbook, which ScanSource is attempting to execute, involves specialization in high-value categories, growth in services and recurring revenue, selective international operations, and disciplined M&A to acquire capabilities and market share. The losers either get acquired, go private, or slowly fade as their product categories decline and their vendor relationships erode. ScanSource's challenge is to stay on the right side of that divide.

Playbook: Business and Investing Lessons

The ScanSource story offers a rich set of lessons for founders, operators, and investors, each earned through decades of navigating an industry that has been perpetually disrupted.

The first and most important lesson is the middleman's dilemma: add value or die. Every intermediary in every industry faces this challenge, but it is particularly acute in technology distribution, where the products are increasingly commoditized and the information asymmetries that once justified the middleman's existence have been largely eliminated by the internet. ScanSource has survived by continuously finding new ways to add value, from credit and logistics in the early days to technical support and integration services as products became more complex, to recurring cloud services through Intelisys. The moment a distributor becomes nothing more than a pass-through for boxes, it is doomed.

The second lesson is about category management: knowing when to hold and when to fold. ScanSource's history is a study in entering categories at the right time, riding them during their growth phase, and then having the discipline to exit or de-emphasize them when they enter structural decline. The company's addition of telephony in the late 1990s, security in the 2000s, and cloud services in the 2010s were well-timed entries. The divestiture of international hardware operations and the de-emphasis of legacy categories like traditional desk phones were equally important exits.

The services transformation, the third lesson, is about escaping the commodity trap. ScanSource's acquisition of Intelisys was an acknowledgment that the long-term future of the company lay not in distributing physical products at thin margins but in enabling the sale of recurring services at much higher margins. This is a playbook that applies far beyond distribution: any business facing commoditization of its core product should be looking for ways to wrap services, recurring revenue, and higher-value offerings around that product.

Geographic diversification, the fourth lesson, offers benefits but carries hidden costs that are easy to underestimate. ScanSource's Latin American expansion consumed years of management attention and significant capital, and the eventual decision to divest most international operations was an implicit acknowledgment that the costs of complexity outweighed the benefits of diversification. For investors, this is a reminder that revenue diversification across geographies is only valuable if the incremental revenue generates adequate returns on the capital and management bandwidth it consumes.

Balance sheet conservatism, perhaps the most boring but most important lesson, is what allows a cyclical business to survive downturns and emerge strong enough to pursue opportunities on the other side. ScanSource's ability to weather the 2008 recession, the pandemic, and the ongoing industry transformation has depended on maintaining a strong balance sheet with manageable debt levels and adequate liquidity. The company's aggressive deleveraging from $344 million in total debt in fiscal 2023 to $147 million in fiscal 2025, combined with near-zero net debt, provides a cushion against future shocks and optionality for future acquisitions.

Finally, capital allocation in a slow-growth business presents a unique challenge. ScanSource does not pay a dividend, instead choosing to allocate free cash flow to share buybacks, debt reduction, and selective acquisitions. The share buyback program has been meaningful, reducing the share count by roughly seven percent over four years. For a stock trading at modest multiples of earnings and cash flow, buybacks at these prices are likely to be value-accretive over time. The absence of a dividend is a deliberate choice to maintain financial flexibility for acquisitions and to avoid the signaling risk of cutting a dividend during a downturn.

Porter's Five Forces and Hamilton's Seven Powers Analysis

The technology distribution industry presents a challenging structural environment through the lens of competitive strategy frameworks. Competitive rivalry in the industry is intense. The market is fragmented but consolidating, with the TD SYNNEX mega-merger creating a dominant broadline player while dozens of smaller specialty distributors compete for niches. Switching costs for both customers and vendors are relatively low: a VAR can typically shift its purchasing from one distributor to another without enormous friction, and vendors routinely work with multiple distributors simultaneously. Margin pressure is relentless, driven by both competitor pricing and vendor efforts to capture more margin for themselves. This creates an environment where operational excellence and relationship management are the primary differentiators, not proprietary technology or brand loyalty.

The threat of new entrants is moderate. On one hand, the capital requirements for maintaining inventory, extending credit, and operating logistics networks create a meaningful barrier. Vendor relationships, built over decades, are difficult for newcomers to replicate quickly. On the other hand, technology platforms are lowering barriers in certain segments, and a well-capitalized entrant with a differentiated business model, as Amazon Business has demonstrated, can gain share quickly.

Supplier power is high and represents one of the most significant risks in the industry. ScanSource's top ten vendors account for approximately fifty percent of its purchases, creating significant concentration risk. Vendors have the power to change terms, go direct, or restructure their channel strategies in ways that can dramatically impact a distributor's business. The international divestiture was driven in part by vendor decisions that made certain markets less attractive for distribution. This is a structural reality that no amount of operational excellence can fully mitigate.

Buyer power is moderate to high. While ScanSource's individual VAR customers are small and have limited negotiating leverage individually, they are collectively critical to the business, and the transparency created by online pricing makes it easier for them to comparison-shop across distributors. Larger resellers have even more leverage, with the ability to negotiate directly with vendors or shift their purchasing volumes to competing distributors.

The threat of substitutes is the most concerning force. Direct purchasing from vendors, Amazon Business, vendor-built marketplaces, and the shift from hardware to cloud services all represent substitutes for the traditional distribution model. This is not a theoretical threat but an ongoing reality that is slowly but persistently eroding the addressable market for hardware distribution.

Through Hamilton Helmer's Seven Powers framework, ScanSource's competitive position appears modest. Scale economies provide some benefit in logistics and credit operations, but they are not dominant; regional specialists can compete effectively in their niches. Network effects are weak in traditional distribution but show some promise in the Intelisys platform, where a larger network of sales partners attracts more supplier participation and vice versa. Switching costs are moderate: VARs have established credit lines, systems integrations, and personal relationships with their distributor contacts, but these are not insurmountable barriers. The Intelisys business has somewhat higher switching costs because agents have established recurring commission streams that they would not want to disrupt.

Process power is perhaps ScanSource's strongest power. Three decades of expertise in credit management, logistics, technical support, and vendor relationship management have created institutional capabilities that are difficult to replicate quickly. The Intelisys master agent operations, with their complex commission tracking, partner management, and supplier integration systems, have genuine process power built through years of operational refinement.

Branding, counter-positioning, and cornered resources are all weak or not applicable. In B2B distribution, the vendor's brand matters far more than the distributor's brand. There is no counter-positioning advantage because incumbents can replicate ScanSource's model. And the company does not possess unique assets, intellectual property, or exclusive access to resources that competitors cannot obtain.

The overall assessment is that ScanSource operates in an industry with limited durable competitive advantages. Success depends on execution, relationships, and strategic positioning rather than structural moats. The Intelisys and services business represents the company's best opportunity to build stronger competitive power over time, as the recurring revenue model, platform characteristics, and higher switching costs of the master agent business create a meaningfully stronger competitive position than traditional hardware distribution.

Bull versus Bear Case

The bull case for ScanSource rests on the thesis that the company's transformation from cyclical hardware distributor to hybrid distribution platform is working and is underappreciated by the market. Services revenue, led by Intelisys, now accounts for nearly a third of gross profit, up from negligible levels a decade ago, and is growing while hardware revenue stabilizes or declines. Gross margins have expanded from eleven percent to over thirteen percent as the revenue mix shifts toward higher-margin services and cloud solutions. The company generates strong free cash flow, with a yield of over ten percent on the current market capitalization, and management has been disciplined about deploying that cash through debt reduction and share buybacks at what appear to be attractive valuations.

The digital transformation tailwind is real. Small and mid-sized businesses, ScanSource's core end market, are still in the relatively early stages of adopting cloud communications, cybersecurity, and IoT solutions. These businesses need help navigating an increasingly complex technology landscape, and the VAR channel that ScanSource supports is well-positioned to provide that help. As the mix of spending shifts from one-time hardware purchases to ongoing services subscriptions, ScanSource's Intelisys platform stands to capture a growing share of that spending through recurring commission streams.

The valuation is objectively modest. At thirteen to fourteen times trailing earnings, seven to eight times EV/EBITDA, and roughly book value, ScanSource trades at a significant discount to both the broader market and to pure-play services businesses. If the services transformation continues to gain traction and the market begins to value ScanSource's recurring revenue streams at a higher multiple, there is meaningful upside to the stock. The company has also demonstrated a willingness to pursue value-creating acquisitions, as evidenced by the Resourcive and Advantix deals in 2024 and the DataXoom acquisition in 2025, which expanded the Intelisys platform's capabilities in managed connectivity and technology advisory services.

The bear case is equally compelling. Technology distribution is a structurally challenged industry. Disintermediation, whether from vendor direct sales, Amazon Business, or the shift from hardware to cloud, is slowly but persistently shrinking the addressable market for traditional distribution. ScanSource's revenue has declined from its fiscal 2019 peak of $3.87 billion to roughly $3 billion, and there is no guarantee that this decline has bottomed. Legacy product categories like traditional POS terminals and desk phones are in secular decline, and the new categories the company is entering may not grow fast enough to offset those losses.

Vendor risk remains a constant concern. ScanSource's dependence on its top ten vendors for approximately half of its purchases means that a single vendor decision to restructure its distribution arrangements could have an outsized impact on revenue and profitability. The international divestiture was partly driven by vendor dynamics that made certain markets uneconomical for ScanSource. There is no structural protection against similar dynamics unfolding in the company's remaining markets.

The services business, while growing nicely, is still a relatively small part of the overall revenue picture. Intelisys contributes roughly a third of gross profit, but ScanSource remains primarily a hardware distribution company by revenue. If the hardware business declines faster than the services business grows, the company could find itself in a structurally declining revenue trajectory that no amount of margin improvement can offset. The "value trap" concern, that the stock looks cheap because the underlying business is a melting ice cube, is legitimate and will only be resolved over time as the relative trajectory of services growth versus hardware decline becomes clearer.

The realistic assessment is that ScanSource is a slow-growth, cash-generative business navigating genuine secular challenges. It is not a growth compounder that will multiply an investor's capital many times over. But it is also not a business in terminal decline. The key variable is the pace of the services transformation: if Intelisys and the advisory businesses can continue growing at double digits while hardware stabilizes, ScanSource can sustain its current profitability and potentially earn a higher valuation multiple. If the hardware decline accelerates or the services growth stalls, the stock could remain stuck at current levels or drift lower.

Key Metrics and What to Watch

For investors tracking ScanSource's ongoing performance, two metrics matter more than anything else on the income statement or balance sheet.

The first and most important is recurring revenue as a percentage of gross profit. This single metric captures the progress of ScanSource's transformation from transactional hardware distributor to hybrid distribution platform. In fiscal 2025, this figure stood at 32.8 percent, up from 27.5 percent. The trajectory of this number tells you whether the Intelisys-driven services strategy is gaining enough momentum to fundamentally change the company's economic profile. If this metric continues climbing toward forty percent and beyond, ScanSource is succeeding in its transformation. If it plateaus or reverses, the transformation thesis is in trouble.

The second critical metric is gross margin percentage. Because ScanSource's revenue can fluctuate based on the mix of high-volume, low-margin hardware sales and lower-volume, higher-margin services revenue, the gross margin percentage tells you whether the revenue the company is keeping is getting better or worse over time. The expansion from 11.1 percent in fiscal 2021 to 13.4 percent in fiscal 2025 reflects the positive mix shift toward services. Continued expansion would validate the strategy; compression would suggest that competitive pressures in hardware are overwhelming the benefits of the services mix shift.

Beyond these two primary indicators, investors should monitor vendor concentration risk, particularly the revenue contribution from the top ten vendors and any changes in key vendor relationships. Days sales outstanding, currently at approximately eighty-eight days, serves as a credit quality indicator for ScanSource's VAR customer base. And free cash flow generation, which has been robust at over $100 million annually, is the ultimate arbiter of whether the business model is sustainable regardless of the revenue trajectory.

Red flags to watch for include major vendor defections or restructurings, a collapse in gross margins back toward the eleven percent level, failed acquisitions that destroy capital, and any deterioration in credit quality among the VAR customer base that would signal stress in the small business economy.

Epilogue and The Path Forward

ScanSource enters the second half of fiscal 2026 at a strategic crossroads that will likely define the company's next decade. The most recent quarterly results showed modest revenue growth and stable margins, suggesting that the worst of the post-pandemic normalization may be behind the company. But the longer-term questions remain unanswered.

The strategic options are clear, if not easy. The first scenario is successful transformation: Intelisys and the advisory businesses continue to scale, recurring revenue grows to forty percent or more of gross profit, margins expand further, and the market re-rates the stock to reflect the growing services component. Under this scenario, ScanSource remains independent and earns a valuation more reflective of its recurring revenue characteristics than its hardware distribution legacy.

The second scenario is a slow fade: hardware revenue continues to decline as disintermediation and category obsolescence take their toll, services growth is insufficient to offset the decline, and the company manages for cash while gradually shrinking. Under this scenario, ScanSource might eventually attract a private equity buyer seeking to extract the remaining cash flow from the business, much as the international operations were sold to Ten Oaks Group.

The third scenario is consolidation: ScanSource becomes an acquisition target for a larger distributor or a private equity firm looking to roll up specialty distribution assets. The company's strong cash flow, clean balance sheet, and established vendor relationships make it an attractive platform for a consolidation play.

The bigger question that ScanSource's story raises is about the future of B2B distribution in the platform era. As artificial intelligence and automation transform purchasing, logistics, and technical support, the functions that distributors perform may be augmented or replaced by technology. AI-powered recommendation engines could help VARs design complex solutions without human technical support. Automated logistics platforms could make the distributor's warehouse and shipping infrastructure less valuable. Or, conversely, the increasing complexity of technology solutions could make human expertise more valuable, not less, creating new opportunities for distributors that invest in their people and capabilities.

What ScanSource's thirty-four-year journey demonstrates, more than anything, is that adaptation is survival. Mike Baur started with barcode scanners, expanded into telephony and security, bet big on international markets and then retreated, acquired a fundamentally different business in Intelisys and rode it toward a new identity. Every one of those moves was a response to changing market conditions, and every one required the willingness to challenge assumptions about what the company was and what it could become. Whether the current transformation succeeds or not, the willingness to transform is itself the most valuable asset ScanSource possesses.

For founders, the lesson is that the businesses that survive are not necessarily the ones with the strongest competitive moats or the most innovative products. Sometimes they are the ones whose leaders are willing to look honestly at the landscape, acknowledge when the old playbook is no longer working, and make the difficult, sometimes painful decisions required to build a new one. ScanSource may never be a glamorous company. It will never be the subject of breathless profiles in Wired or the darling of growth-stock investors. But it is the kind of business that makes the world work: connecting manufacturers with the small companies that actually deploy technology in the real world, financing their purchases, supporting their technical needs, and quietly ensuring that the barcode scanner at your local grocery store, the video conferencing system in your office, and the security camera at your neighborhood business are there when you need them.

Further Reading and Resources

For those wanting to go deeper on ScanSource and the technology distribution industry, the following resources provide valuable primary and secondary source material.

ScanSource's annual reports and investor presentations from 2016 to the present offer the best primary source for understanding the transformation narrative, particularly the evolution of the services strategy and the rationale behind the international divestitures. The company's proxy statements provide insight into management compensation structures, board composition, and governance practices that reveal how leadership thinks about long-term value creation.

For industry context, TD SYNNEX investor materials illuminate the broader distribution landscape and the scale advantages that broadline distributors enjoy. Channel Partners Magazine and Channel Futures provide ongoing coverage of competitive dynamics, vendor relationship changes, and emerging trends in the channel. CRN, published by The Channel Company, offers comprehensive coverage of the VAR and distribution ecosystem.

Key SEC filings to review include the Form 10-K annual reports, which contain detailed business segment information and risk factor disclosures; the 8-K filings for major acquisitions, particularly the Intelisys deal and the more recent Resourcive and Advantix transactions; and the definitive proxy statements for governance and executive compensation details. The earnings call transcripts from 2016 to the present provide a real-time window into management's strategic thinking and the questions that analysts and investors consider most important.

For broader frameworks applicable to ScanSource's strategic position, "The Outsiders" by William Thorndike offers capital allocation lessons that are directly relevant to a slow-growth, cash-generative business. "Supply Chain Management" by Sunil Chopra provides the theoretical foundation for understanding distribution economics and the role of intermediaries in complex supply chains. And the Harvard Business Review's literature on specialty versus broadline distribution strategies offers frameworks for evaluating ScanSource's positioning relative to larger competitors.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube